tonga country operations business plan 2016–2018 strategic ... · data tables 7 table 1: ... and...

TRANSCRIPT

TONGA

Country Operations Business Plan 2016–2018

STRATEGIC ANALYSIS

August 2015

CONTENTS

I. DEVELOPMENT TRENDS AND ISSUES

A. Country Background 1

B. Highlights of Previous Programming Approach 3

II. THE COUNTRY STRATEGIC PRIORITIES

A. Developing the ADB Country Strategic Priorities 3

B. Implementation Issues 5 APPENDICES TO LINKED DOCUMENT

1. Data Tables 7

Table 1: Progress towards the Millennium Development Goals 7

Table 2: Country Economic Indicators 10

Table 3: Country Poverty and Social Indicators 12

Table 4: Country Environment Indicators 13

Table 5: 2015 Country Performance Assessment Ratings 14

Table 6: Country Portfolio Indicators 15

Table 6a: Portfolio Amounts and Ratings 15

Table 6b: Disbursements and Net Transfers of Resources 16

Table 6c: Project Success Rates 17

Table 6d: Portfolio Implementation Status 18

2. Development Coordination 19

Development Coordination Matrix 19

3. Sector Assessments 21

I Infrastructure 21

II Climate Resilience 31

III Public Sector Management 41

IV Private Sector Development Assessments 49

4. Risk Assessment and Management Plan 58

5. Country Cost-Sharing Arrangements and Eligible Expenditure Financing 60

Parameters, 2016–2018

ABBREVIATIONS

ADF Asian Development Fund

CPS country partnership strategy

DPs development partners

GDP gross domestic product

IMF International Monetary Fund

MDGs millennium development goals

PFM public financial management

JPRM joint policy reform matrix

RETA regional technical assistance

SOE state-owned enterprise

TA technical assistance

I. DEVELOPMENT TRENDS AND ISSUES

A. Country Background 1. Tonga is located in the western South Pacific Ocean approximately 750 kilometers east of Fiji and 2,000 kilometers north of New Zealand. There are 170 islands in the archipelago, of which 36 are populated. The total land area of Tonga is 747 square kilometers ((km2), surrounded by an exclusive economic zone of 640,050 km2. The population of Tonga was estimated at 103,036 in 2011. Nearly 70% reside on the largest island of Tongatapu, where the capital, Nuku’alofa, is located. Emigration has been high over the past 30 years, at a rate of about 2.0% annually; this has lowered the rate of population growth to an average of 0.4% annually. Tonga has achieved a high level of human development. Gross domestic product (GDP) per capita in fiscal year (FY) 2012 was estimated at $4,572. This places the country in the ranks of middle-income countries. 2. Over the past decade, Tonga’s economy has been adversely affected by climatic shocks, in particular, tropical cyclones, soaring prices of imported fuels and food, civil disturbances in 2005 and 2006, and the global financial crisis. The resulting growth trajectory has been low, volatile, and largely public sector driven—with average growth of only 0.6% of GDP ranging between –4.6% to 4.2% of GDP from 2005–2014—highlighting the need to grow the private sector, including through enhanced economic participation of women, to create more jobs and improve future growth prospects. In recent years, the government has taken important steps to put in place the policy levers that will shape growth. Prudent management of debt and the excessive public wage bill, and further strengthening of domestic revenue mobilization, are required to put the fiscal position on a more sustainable path. More effective and efficient use of resources requires further PFM reforms. Better public service performance and continuous SOE reforms will benefit both the public and private sectors. Business environment reforms are needed to lower the cost and risk of doing business and encourage private sector activity to expand the formal economy and create employment. Measures have been taken to liberalize external trade and foreign direct investment, institute growth committees in priority sectors (e.g. tourism, agriculture and fisheries), simplify and improve the tax system, reform state-owned enterprises (SOEs), and strengthen public financial management through introducing a medium-term budget framework that links prioritized plans with annual budgets, and public procurement reforms. These measures are guided by the government-led Joint Policy Reform Matrix (JPRM), which development partners use as the basis for budget support that helps create fiscal space for critical reforms and set incentives to keep up reform momentum. 3. However, the government does not yet have control over all the policy levers. Government’s fiscal policy remains hampered by t h e large, relatively well– paid public s e c t o r that puts pressure on scarce funds, relatively high ad hoc tax exemptions, and weak implementation of budgeted policy priorities. Extensive borrowing from the Export-Import Bank of China for the reconstruction of Nuku’alofa’s central business district following civil disturbances in 2005 and 2006 led to a downgrading of Tonga’s debt distress level from moderate to high risk in 2010. Enforcement of a stricter debt policy that allows only concessional borrowing has led to an upgrade to moderate risk by the joint International Monetary Fund and World Bank debt sustainability analysis in 2013 and 2014. 4. Private sector development is essential to c r e a t e j o b opportunities for the labor-force. Its development has been constrained by multiple geographic, institutional, and policy constraints. The remnants of a state-led growth strategy, the large civil service, and SOE dominance in commercial activities, continues to hamper private sector development and new job creation. However, significant reforms have been undertaken to improve SOE governance, and selected SOEs have either been restructured or privatized between 2012 and 2014.

2

Progress with the simplification of business license registration and new companies legislation has further improved the investment climate. A critical constraint for private sector development is the lack of access to land for both local and foreign investment. This is exacerbated by typ ica l ly short term leases, the lack of provisions for regular review of rental agreements, and protection for investors. Land tenure systems are intimately linked with cultural traditions and the structure of society, making it difficult to bring land management into line with the needs of a market- based economy. 5. A key challenge for Tonga is to improve the efficiency of the public sector and develop the private sector. Tackling developmental issues will be crucial to alleviate unemployment, poverty and hardship. Reforms in many aspects of the economy are needed if Tonga is to deliver the quality of education, health and other services consistent with its status as a middle-income country. Nurturing private-sector led growth is essential to increasing levels of private sector investment, and improving productivity, competitiveness and resource efficiency. This will require effective government, appropriately functioning factor markets, and an enabling climate to be created where companies with available capital feel confident in taking forward investment.

6. The standard of living in Tonga has improved dramatically over the past 50 years and absolute poverty is not widespread. However, the incidence of hardship among the economically disadvantaged groups has been increasing. Hardship is officially defined as “having difficulties in meeting basic needs such as education and transport.” From this perspective, the rural and outer-island communities, especially those in the rural areas of Nuku’alofa and the Niuas and Ha’apai outer-island groups, are experiencing higher rates of hardship. This means that they face limited job opportunities and access to key public services, the latter which affects the quality of health and education services received They depend heavily on subsistence production including handicrafts, and on remittances from overseas members of their households to fund their social and cultural obligations for ceremonies and church donations. The results of the 2009 Household Income and Expenditure Survey, the latest data available, suggest that the incidence of hardship in Tonga has increased over the past decade. It has been estimated that in 2009, 16.4% of households (22.5% of the population) were living below the basic needs poverty line, compared with 12.2% of households (16.2% of the population) in 2001 (Table 6). Overseas employment opportunities, both related to overseas labor mobility schemes and longer term migration, not only provide major sources of income and remittances but continues to be a viable long-term option for sustaining economic growth and helping to lift people out of poverty. 7. Tonga is generally on-track in relation to the achievement of the eight Millennium

Development Goals (MDGs) agreed by the international community to strengthen performance

in social and economic development by 2015. A status report on progress towards meeting

MDG goals and targets is included in Appendix 1, Table 1. Progress is considered to be lagging

in three areas: (i) managing the incidence of non-communicable diseases where the high

incidence of diabetes, cardio-vascular disease, hypertension and diabetes is a cause for

concern; (ii) promoting gender equality and empowering women, where for example none of the

thirty seats in Parliament is held by a woman; and (iii) reducing poverty, where 22.5% of the

population is considered to remain below the national basic needs poverty line.

8. As a category A country, Tonga is eligible for Asian Development Fund (ADF) and

concessional Ordinary Capital Resources, or OCR, resources The 2015 Debt Sustainability

Analysis indicates that Tonga remains at moderate risk of debt distress. External debt in 2015 is

3

estimated at 45% of GDP and external debt and debt service indicators remain below the

thresholds. The 2014 Country Performance Assessment found that Tonga had maintained its

2012 ratings for all categories except public sector management and institutions where the

establishment of remuneration boards at the line ministry level and the 5.0% cost of living

adjustment increase in late 2013 has caused the rating to slip. In spite of this, Tonga continues

to perform well relative to the rest of the Pacific and in terms of structural policies and public

sector management and institutions, at par or better than ADB’s Group A countries.

B. Highlights of Previous Programming Approach 9. ADB’s Pacific Approach 2010-2014 has served as the country partnership strategy between ADB and Tonga since the expiry of the Country Partnership Strategy 2007-2011. The current Country Operations Business Plan (COBP) covers the period 2015-2017. ADB’s engagement during 2011–2014 has supported the government’s focus on strengthening the economy’s resilience to future shocks and improving Tonga’s long term growth prospects. The COBP supports this effort by focusing on prudent public sector management, renewable energy, and climate resilience. 10. ADB and other partners have increasingly provided budget support for Tonga to support the implementation of reform actions in the JPRM (ADB provided an initial $10m in budget support on 2009 and a further $4.5m in 2013). In total, budget support receipts from all partners have averaged about 15% of Tonga’s budget since FY2012 and have helped to restore public finances and debt at manageable levels, improve allocation of resources to priority sectors including maintenance of health and education spending at a time of fiscal consolidation, and accelerate the pace of business climate and state-owned enterprise reforms. 11. Investment in infrastructure is crucial to economic recovery in Tonga. It is vital to growth: spending on infrastructure not only provides a timely boost to economic activity and jobs but also creates a legacy of assets that could have long-lasting economic benefits. Domestic investment levels in Tonga have averaged 20% of GDP in the decade. However, the productivity of much of this investment is low, being channeled either into poorly performing state-owned enterprises or into residential construction. Government capital spending has historically been low while poor transport infrastructure and high costs of power and broadband internet services are significant constraints on doing business in Tonga; these compound the effects of remoteness on economic activity. Recognizing this challenge, the Government has signaled its intention to balance budget support with new investments in economic infrastructure once the period of the current COBP (2015–2017) ends. There are four large-scale ADB infrastructure projects ongoing in Tonga that amount to about $60 million. These are the Nuku’alofa Urban Development Project, the Climate Change Resilience Project, the Outer Island Renewable Energy Project and the Cyclone Ian Recovery Project. All are scheduled to end between 2016–2018 and occupy significant implementation capacities.

II. THE COUNTRY STRATEGIC PRIORITIES

A. Developing the ADB Country Strategic Priorities 12. The Tonga Strategic Development Framework 2015–2025 contains 5 pillars (Economic Institutions, Social institutions, Political Institutions, Infrastructure and Technology, and Natural Resources and Environment ), which are consistent with the focus of ADB’s Interim Pacific Approach 2015 and the proposed COBP 2016–2018.

4

13. The indicative ADF and concessional OCR resource allocation for 2016–2018 is $23.51 million. The final allocation will depend on the available ADF and concessional OCR resources and the outcome of the country performance assessments. The 2014 debt distress classification of Tonga was assessed as at moderate risk of debt distress. In accordance with the ADF grants framework, the country is to receive 50% of its country allocation in grants in 2015, subject to a 20% volume discount on the grant portion of the country allocation.1 ADB’s interventions during this period include $15 million for the “Building Macroeconomic Resilience Program” and $20 million for project investments in information and communication technology and urban sector development. 14. Policy-based lending. Policy-based lending will continue to feature prominently in the COBP 2016–2018. Budget support has helped the government to significantly improve its management of the economy and its finances during a period of fiscal crisis and through major Constitutional changes that have absorbed significant political and administrative attention. The fiscal situation has stabilized, delivery of crucial social services maintained, returns from state-owned enterprises increased, and the business climate improved. As a result, Tonga has steadily climbed up in the Ease of Doing Business Indicators, and is now the highest ranked Pacific country. Tonga’s country performance assessment scores have rapidly improved, which has seen its biennial ADF allocation increase by 16% since 2010. The government wishes the focus of ADB’s policy-based lending to balance sound fiscal management with structural reforms and inclusive growth to promote jobs and social protection. ADB and other development partners will work with the government to transform the JRPM into a medium term critical reform path that helps strengthen economic resilience. Planned approval of ADB’s 2015 policy-based lending operation has been pushed back to the first quarter of 2016 in order to give the government room to implement vital policy and institutional reforms in the JPRM that will serve as building blocks for more substantial change in the future. 15. New investments. New investments will be based on the 2010 Tonga National Infrastructure Investment Plan (updated in 2013) and will be carefully phased in to ensure Government has adequate capacity for implementation.2 The government and ADB have agreed that the information and communications technology (ICT) and urban and water sectors should be prioritized in ADB’s lending pipeline. Consequently, the COBP contains two new project investments in these sectors: an ICT project ($10 million) that will build on an ongoing technical assistance (TA) project to promote the use of electronic applications in the social sectors and a urban and water project ($10 million) that will enable the expansion of the Nuku’alofa water supply to growth areas (footnote 6). 16. Capacity development. TA will support program implementation and project preparation. Tonga will also continue to benefit from regional technical assistance in line with ADB’s Regional Operations Business Plan, 2015–2017. Tonga will also continue to benefit from technical support from the Pacific Region Infrastructure Facility and the International Monetary Fund’s Pacific Financial Technical Assistance Centre. 17. Knowledge solutions will be promoted by capturing, generating and disseminating relevant development management knowledge, in line with ADB’s knowledge solutions agenda of the Midterm Review of Strategy 2020, the new Knowledge Management Action Plan, ADB’s Public Communication Policy 2011, and utilizing the User Guide to Preparing Communications Strategies for Projects. Concerted efforts will be made to (a) generate knowledge from ADB operations in Tonga, and (b) apply Pacific Developing Member Country-wide knowledge in

1 The proportion of grants for the resource allocations in 2016–2018 will be determined by future annual debt

distress classifications in accordance with the ADF grants framework. 2 Government of Tonga. 2010. National Infrastructure Investment Plan. Nuku’alofa.

5

designing projects and reform programs in Tonga. This will be done in close coordination with the ADB’s Knowledge Sharing and Services Center, the Department of External Relations, and ADB’s various Communities of Practice. Lessons will be drawn from high-performance projects and programs and disseminated in policy notes, seminars, and other outreach events. B. Implementation Issues

1. Efforts to build ownership

18. Key initiatives in building Tongan ownership of ADB activities include close consultation with Tongan stakeholders at all stages of activity identification, formulation and implementation; ensuring close alignment between ADB activities and Tonga’s development strategies; working with government and other development partners in pursuing reform through the JPRM; use of local consultants wherever possible; and full-time presence through the ADB/WB Development Coordination Office.

2. Capacity

19. Tongan institutions are generally capable and staffed by educated, experienced and motivated personnel. However, these institutions are small and can lack breadth and depth in technical skills. This can put policy reform and project implementation at risk, and requires that reform and project design be supported by relatively high levels of technical support for extended periods. Capacity constraints also suggest that the reform agenda needs to be tightly focused on key policies and systems in order to be sustained.

3. Coordination

20. A joint declaration on aid effectiveness between the government and Development Partners was signed in October 2007, and high level consultations in relation to development assistance are held annually. Aid coordination is the responsibility of the Project and Aid Management Division in the Ministry of Finance and National Planning, with this institutional arrangement creating strong links between Development Partner activities, the strategic planning framework, and the annual budget process. The Division has experienced and effective staff, and acts as a key repository of information on development assistance activities. Some development partners have co-located representatives with the Division (including the ADB/WB Development Coordination Office and the UN Joint Presence Office).

4. Use of Development Coordination Office (DCO)

21. The ADB/WB Development Coordination Office in Tonga plays a pivotal role in supporting ADB’s activities in Tonga. The office is strategically located within the offices of the Ministry of Finance and National Planning, giving it ready access to key staff and smooth links with other arms of government. Experience to date has seen the office providing effective services to visiting missions and consultants, and opening very effective channels of communications with line ministries and other key stakeholders. An indicator of the success of the office is the high regard with which it is held by both ADB and the government.

6

APPENDICES TO LINKED DOCUMENT

Appendix 1 7

DATA TABLES

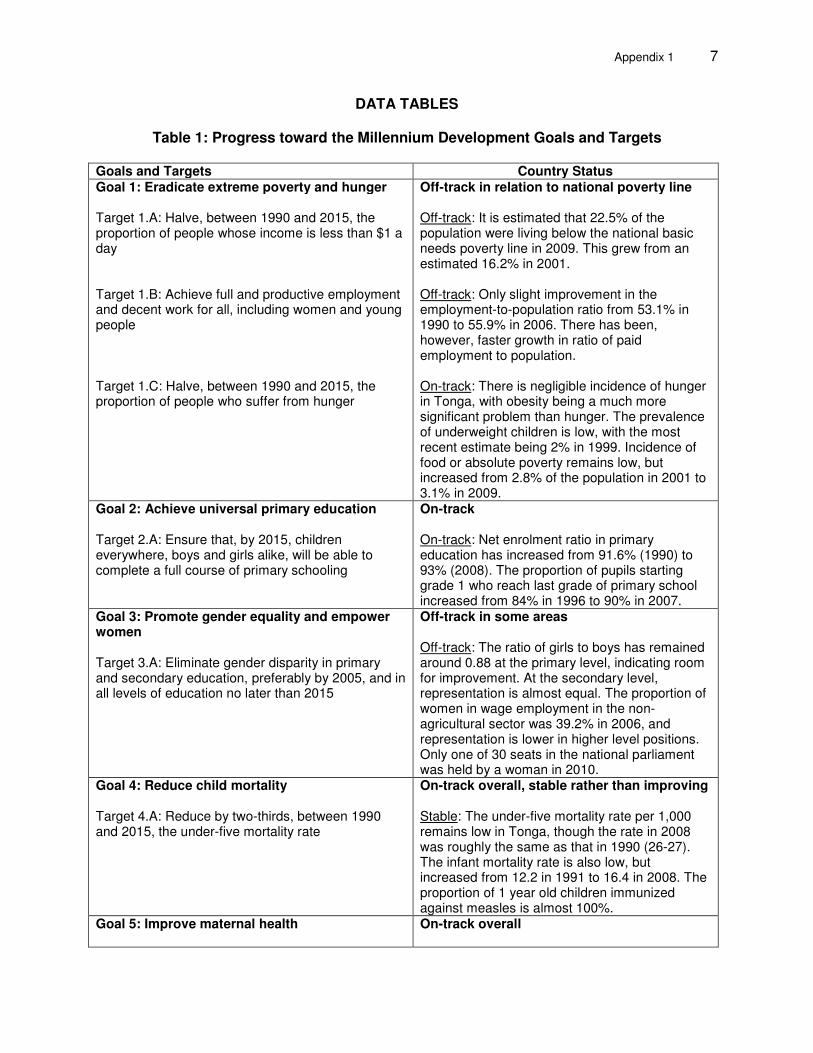

Table 1: Progress toward the Millennium Development Goals and Targets

Goals and Targets Country Status Goal 1: Eradicate extreme poverty and hunger Target 1.A: Halve, between 1990 and 2015, the proportion of people whose income is less than $1 a day Target 1.B: Achieve full and productive employment and decent work for all, including women and young people Target 1.C: Halve, between 1990 and 2015, the proportion of people who suffer from hunger

Off-track in relation to national poverty line Off-track: It is estimated that 22.5% of the population were living below the national basic needs poverty line in 2009. This grew from an estimated 16.2% in 2001. Off-track: Only slight improvement in the employment-to-population ratio from 53.1% in 1990 to 55.9% in 2006. There has been, however, faster growth in ratio of paid employment to population. On-track: There is negligible incidence of hunger in Tonga, with obesity being a much more significant problem than hunger. The prevalence of underweight children is low, with the most recent estimate being 2% in 1999. Incidence of food or absolute poverty remains low, but increased from 2.8% of the population in 2001 to 3.1% in 2009.

Goal 2: Achieve universal primary education Target 2.A: Ensure that, by 2015, children everywhere, boys and girls alike, will be able to complete a full course of primary schooling

On-track On-track: Net enrolment ratio in primary education has increased from 91.6% (1990) to 93% (2008). The proportion of pupils starting grade 1 who reach last grade of primary school increased from 84% in 1996 to 90% in 2007.

Goal 3: Promote gender equality and empower women Target 3.A: Eliminate gender disparity in primary and secondary education, preferably by 2005, and in all levels of education no later than 2015

Off-track in some areas Off-track: The ratio of girls to boys has remained around 0.88 at the primary level, indicating room for improvement. At the secondary level, representation is almost equal. The proportion of women in wage employment in the non-agricultural sector was 39.2% in 2006, and representation is lower in higher level positions. Only one of 30 seats in the national parliament was held by a woman in 2010.

Goal 4: Reduce child mortality Target 4.A: Reduce by two-thirds, between 1990 and 2015, the under-five mortality rate

On-track overall, stable rather than improving Stable: The under-five mortality rate per 1,000 remains low in Tonga, though the rate in 2008 was roughly the same as that in 1990 (26-27). The infant mortality rate is also low, but increased from 12.2 in 1991 to 16.4 in 2008. The proportion of 1 year old children immunized against measles is almost 100%.

Goal 5: Improve maternal health

On-track overall

8 Appendix 1

Goals and Targets Country Status Target 5.A: Reduce by three-quarters, between 1990 and 2015, the maternal mortality ratio Target 5.B: Achieve, by 2015, universal access to reproductive health

On-track: The maternal mortality ratio has fluctuated, but was significantly lower in 2008 (76/100,000) than in 1995 (205/100,000). The skilled birth attendance rate has been high and stable, reaching 98% in 2007. On-track overall: Ante-natal coverage is high at 98% in 2008 (one visit) and 86% (4 visits), though the contraceptive prevalence rate is low at 27% in 2008, down from 33% in 1990.

Goal 6: Combat HIV/AIDS, malaria, and other diseases Target 6.A: Have halted by 2015 and begun to reverse the spread of HIV/AIDS Target 6.B: Achieve, by 2010, universal access to treatment for HIV/AIDS for all those who need it Target 6.C: Have halted by 2015 and begun to reverse the incidence of TB. Have reduced the prevalence of non-communicable diseases (NCDs).

Off-track in relation to NCDs Little data available. Official estimates on HIV/AIDS levels are low but likely to be understated. Estimates of condom use at last high-risk are very low (21% in 2008), and awareness of HIV/AIDS is low (36% of those in the 15-24 age group). No current cases of advanced HIV infection. Off-track: Significant progress has been made in relation to the incidence, prevalence and cure rate from TB. However, mortality and morbidity arising from NCDs including diabetes, cardiovascular disease, hypertension, and obesity are major areas of concern.

Goal 7: Ensure environmental sustainability Target 7.A: Integrate the principles of sustainable development into country policies and programs and reverse the loss of environmental resources Target 7.B: Reduce biodiversity loss, achieving, by 2010, a significant reduction in the rate of loss Target 7.C: Halve, by 2015, the proportion of people without sustainable access to safe drinking water and basic sanitation Target 7.D: By 2020, to have achieved a significant improvement in the lives of at least 100 million slum dwellers

Some data gaps; generally on-track. Data not available. Data not available On-track: The proportion of the population with access to an improved drinking water source increased from 92% in 1986 to 98% in 2006. The proportion of the population using an improved sanitation facility increased from 55% in 1986 to 82% in 2006. Data not available. Settlements are growing in swampy areas around Nuku’alofa, which has implications in terms of housing quality and access to basic services.

Goal 8: Develop a global partnership for development Target 8.A: Develop further an open, rule-based, predictable, non-discriminatory trading and financial system

Data gaps; generally on-track Significant progress has been made in aid coordination and harmonization, with a significant reduction in the tying of aid Not applicable

Appendix 1 9

Goals and Targets Country Status Target 8.B: Address the special needs of the least developed countries Target 8.C: Address the special needs of landlocked developing countries and small island developing states (through the Programme of Action for the Sustainable Development of Small Island Developing States and the outcome of the twenty-second special session of the General Assembly) Target 8.D: Deal comprehensively with the debt problems of developing countries through national and international measures in order to make debt sustainable in the long term Target 8.E: In cooperation with pharmaceutical companies, provide access to affordable essential drugs in developing countries Target 8.F: In cooperation with the private sector, make available the benefits of new technologies, especially information and communications

Data gaps Off-track: Debt service as a proportion of exports of goods and services remains manageable at 9.8% (2007). However, public debt has grown with external debt now exceeding the target ceiling of 40% of GDP (2012), and debt sustainability analysis concluding that Tonga is at high risk of debt distress. On-track: In 2002 it was estimated that 95% of the population had sustainable access to the 20 most essential drugs identified by WHO. The Tongan population has access to free health care and drugs. Tonga is considered to have achieved this target. On-track: There has been rapid growth in the number of telephone lines (5 per 100 population in 1990 to 21 in 2008), mobile phone users (from 0 per 100 population in 1990 to 46.4 in 2007), and internet users (0 per hundred population in 1990 to 8.4 in 2007).

Source: Adapted from 2nd National Millennium Development Goals Report, Tonga, Status and Progress 1990-2010, MFNP, September 2010.

10

Ap

pe

ndix

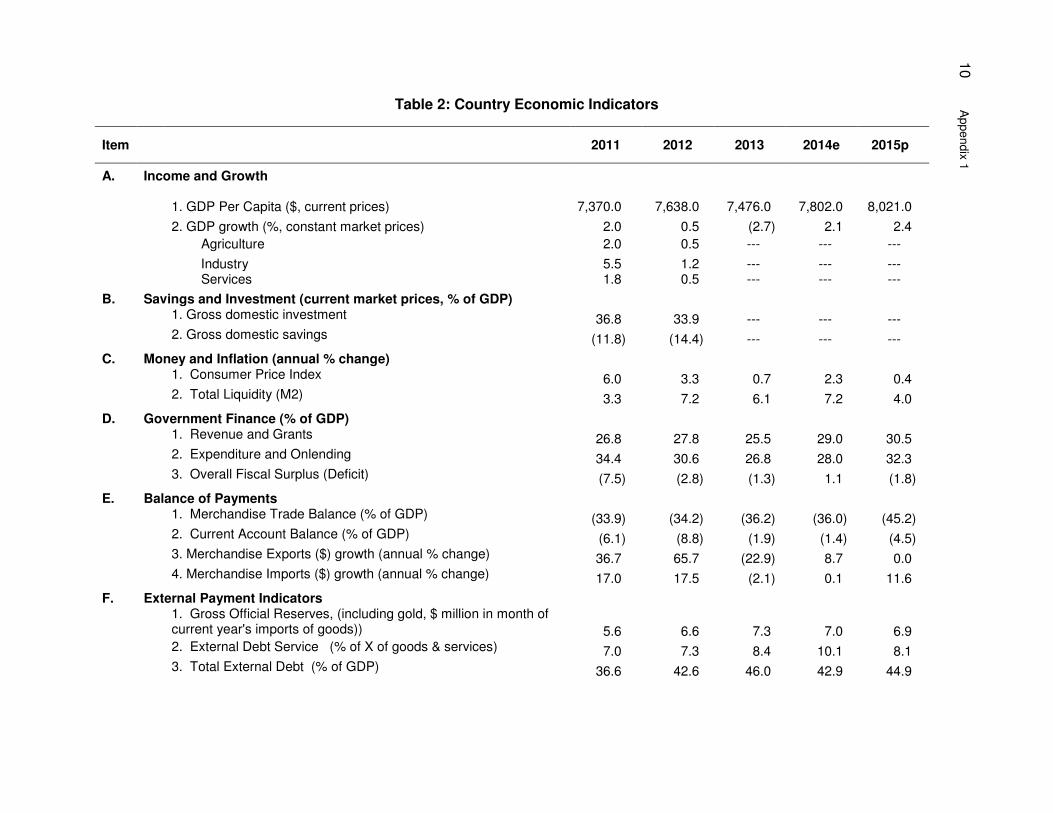

1 Table 2: Country Economic Indicators

Item

2011 2012 2013 2014e 2015p

A. Income and Growth

1. GDP Per Capita ($, current prices)

7,370.0

7,638.0

7,476.0

7,802.0

8,021.0

2. GDP growth (%, constant market prices) 2.0 0.5 (2.7) 2.1 2.4

Agriculture 2.0 0.5 --- --- ---

Industry 5.5 1.2 --- --- --- Services 1.8 0.5 --- --- ---

B. Savings and Investment (current market prices, % of GDP)

1. Gross domestic investment 36.8 33.9 --- --- ---

2. Gross domestic savings (11.8) (14.4) --- --- ---

C. Money and Inflation (annual % change)

1. Consumer Price Index 6.0 3.3 0.7 2.3 0.4

2. Total Liquidity (M2) 3.3 7.2 6.1 7.2 4.0

D. Government Finance (% of GDP)

1. Revenue and Grants 26.8 27.8 25.5 29.0 30.5

2. Expenditure and Onlending 34.4 30.6 26.8 28.0 32.3

3. Overall Fiscal Surplus (Deficit) (7.5) (2.8) (1.3) 1.1 (1.8)

E. Balance of Payments

1. Merchandise Trade Balance (% of GDP) (33.9) (34.2) (36.2) (36.0) (45.2)

2. Current Account Balance (% of GDP) (6.1) (8.8) (1.9) (1.4) (4.5)

3. Merchandise Exports ($) growth (annual % change) 36.7 65.7 (22.9) 8.7 0.0

4. Merchandise Imports ($) growth (annual % change) 17.0 17.5 (2.1) 0.1 11.6

F. External Payment Indicators

1. Gross Official Reserves, (including gold, $ million in month of current year's imports of goods)) 5.6 6.6 7.3 7.0 6.9

2. External Debt Service (% of X of goods & services) 7.0 7.3 8.4 10.1 8.1

3. Total External Debt (% of GDP) 36.6 42.6 46.0 42.9 44.9

Ap

pe

ndix

1 11

G. Memorandum Items

1. GDP (current prices, T$ million) 759.7 788.4 772.4 806.3 828.9

2. Exchange Rate ((T$/$, annual average) 1.9 1.7 1.7 1.8 2.1

3. Population (million) 0.1 0.1 0.1 0.1 0.1

--- = no available data; % = percent; $ = United States dollar; a = in fiscal year ended 30 June; e = estimate; GDP = gross domestic product;

M2 = money supply; p = projection; T$ = Tongan pa'anga.

Source: Asian Development Outlook 2015 database and ADB staff estimates.

12 Appendix 1

Table 3: Country Poverty and Social Indicators

Item 1990 2000 Latest Year A. Population Indicators 1. Population (‘000) 95.2 97.9 103.0 (2011) 2. Population growth (annual % change) 0.2 0.5 0.2 (2006-11) B. Social Indicators 1. Fertility rate (births/woman) 4.6 4.3 3.8 (2012)

2. Maternal mortality ratio (per 100,000 live births) 67 87 110 (2010) 3. Infant mortality rate (below 1 year, per 1,000 live births) 20.7 16.8 13.2 (2010)

4. Life expectancy at birth (years) 69.6 70.7 72.3 (2011) a. Female 71.1 72.8 75.2 (2011) b. Male 68.1 68.8 69.5 (2011) 5. Adult literacy (%) 98.9 (1996) … 99.0 (2006) a. Female 99.0 (1996) … 99.0 (2006) b. Male 98.8 (1996) … 99.0 (2006) 6. Primary school net enrollment (%) 92.3 91.3 (1999) 98.7 (2006) 7. Secondary school net enrollment (%) 81.9 76.1 73.0 (2004) 8. Child malnutrition (% underweight below 5 years old) … … 2.2 (1986)

9. Population below poverty line (%) … 16.2 (2001) 22.7 (2006) 10. Households with access to safe water (%) 91 (1986) 98 (1996) 98 (2006) 11. Households with access to sanitation (%) 55 (1986) 74 (1996) 82 (2006) 12. Public education expenditure (% of GDP) … 4.9 3.9 (2004) 13. Human development index rank … 55 (2004) 95/186 (2012) 14. Gender-related development index … … 0.462 (2012) C. Poverty Indicators 1. Human poverty index value (%) … … … Rank … … … 2. Provincial human poverty indices (%) not applicable 3. Poverty gap … … 6.3 (2009) 4. Poverty severity index … … … 5. Inequality (Gini Coefficient) … … 0.24 (2009) … = data not available, GDP = gross domestic product. Sources: 2nd National Millennium Development Goals Report, Tonga, Status and Progress 1990-2010, MFNP, September 2010; World Development Indicators, World Bank, 2012; UNDP Human Development Report 2013.

Appendix 1 13

Table 4: Country Environment Indicators

Indicator 1990 Latest Year A. Energy Efficiency of Emissions 1. GDP/unit of energy use (PPP$/kgoe) … … 2. Traditional fuel use (% of total energy use) … … 3. Carbon dioxide emissions (metric ton, ‘000) … … 4. Carbon dioxide emissions per capita (metric ton) … … B. Water Pollution: Water and Sanitation 1. % urban population with access to safe water … 98.3 (1996) 2. % rural population with access to safe water … 98.1 (1996) 3. % urban population with access to sanitation … 99 (1996) C. Land Use and Deforestation 1. Forest area (km

2) 90 90 (2010)

2. Average annual deforestation (km2) … …

3. Average annual deforestation (% change) … … 4. Rural population density (people/km

2 of arable land) 460 500 (2011)

5. Arable land (% of total land) 22.2 22.2 (2009) 6. Permanent cropland (% of total land) 16.7 15.3 (2009) D. Biodiversity and Protected Areas 1. Nationally protected area (km

2) 9.9 104.7 (2010)

2. Nationally protected area (% of total land) 1.4 14.5 3. Mammals (number of threatened species) 0 (1996) 2 (2012) 4. Birds (number of threatened species) 2 5 (2012) 5. Higher plants (number of threatened species) … 2 (2012) 6. Reptiles (number of threatened species) 3 (1996) … 7. Amphibians (number of threatened species) … … E. Urban Areas 1. Urban population (‘000) 21.6 24.5 (2011) 1. Urban population (% of total population) 22.7 23.5 (2011) 2. Per capita water use (liters/day) … … 3. Wastewater treated (%) ... … 4. Solid waste generated per capita (kg/day) … … … = data not available, GDP = gross domestic product, kg = kilogram, kgoe = kilograms of oil equivalent, km

2 =

square kilometer, PPP = purchasing power parity. Sources: 2nd National Millennium Development Goals Report, Tonga, Status and Progress 1990-2010, MFNP, September 2010; World Development Indicators, World Bank, 2012.

14 Appendix 1

Table 5: 2014 Country Performance Assessment Ratings

CRITERIA TUV Pacific

(Average) A. Economic Management 2.8 3.3

1. Monetary and Exchange Rate Policies 2. Fiscal Policy 3. Debt Policy and Management

3.5 3.0 2.0

3.4 3.2 3.4

B. Structural Policies 2.7 3.2 4. Trade 5. Financial Sector 6. Business Regulatory Environment

3.0 2.5 2.5

3.8 3.0 2.8

C. Policies for Social Inclusion/Equity 3.2 3.2 7. Gender Equality 8. Equity of Public Resource Use 9. Building Human Resources 10. Social Protection and Labor 11. Policies and Institutions for Environmental

Sustainability

3.0 3.0 4.0 3.0 3.0

3.0 3.2 3.4 3.1 3.0

D. Public Sector Management and Institutions 3.2 3.3 12. Property Rights and Rules-based Governance 13. Quality of Budgetary and Financial Management 14. Efficiency of Revenue Mobilization 15. Quality of Public Administration 16. Transparency, Accountability and Corruption in the

Public Sector

4.0 3.0 3.0 3.0 3.0

3.4 3.4 3.5 3.0 3.2

E. Portfolio Performance 4.0 3.8 17. Portfolio Performance 4.0 3.8 Composite Country Performance Rating (CCPR) 10.2 11.1

15

Ap

pe

ndix

1

Table 6: Country Portfolio Indicators

Table 6a: Portfolio Amounts and Ratings (sovereign loans, as of 31 December 2014)

Net Amount Total On Track Potential Problem Actual Problem

Sector ($

million) (%) (no.) (%) (no.

) (%) (no.) (%) (no.) (%)

Energy 15.29 22.47 2 33.3 2 100.

0 0 0.0 0 0.0

Information and Communication Technology 9.70 14.26 1 16.7 1 100.

0 0 0.0 0 0.0

Multisector 19.25 28.29 1 16.7 1 100.

0 0 0.0 0 0.0 Water and Other Urban Infrastructure and Services 23.80 34.98 2 33.3 1 50.0 1 50.0 0 0.0

Total

68.04

100.0 6 100.0 5 83.3 1 16.7 0 0.0

Source: eOps extract.

Note: Covers effective projects active as of 31 December 2014.

Appendix 1 16

Table 6b: Disbursements and Net Transfers of Resources (sovereign loans, as of 31 December 2014)

17

Ap

pe

ndix

1

Table 6c: Project Success Rates

Note: Based on validated PCRs and PPERs only and does not include ratings from PCRs. The period of coverage are projects approved from 1973–2009.

Ap

pe

ndix

1

18

Table 6d: Portfolio Implementation Status (sovereign loans, as of 31 December 2014)

No. Sector Grant No.

Title

Net Grant

Amount Cumulative Disbursements

($ million) Approval

Date Effectivity

Date

Closing Date ($

million) Original Revised

1 WUS 108

Integrated Urban Development Sector Project 11.300 11.256 27-May-08 18-Aug-08 30-Jun-13 31-Dec-13

2 ICT 256

Tonga-Fiji Submarine Cable Project 9.700 7.397 23-Aug-11 21-Dec-11 31-Dec-16 -

3 WUS 264

Nuku'alofa Urban Development Sector Project 6.060 1.478 17-Oct-11 10-Apr-12 31-Dec-17 31-Jan-19

4 WUS 265

Nuku'alofa Urban Development Sector Project 6.440 1.570 17-Oct-11 10-Apr-12 31-Dec-17 31-Jan-19

5 ENE 347

Outer Island Renewable Energy Project 2.000 - 27-Jun-13 9-Jun-14 30-Jun-20 -

6 ENE 348

Outer Island Renewable Energy Project 4.500 - 27-Jun-13 9-Jun-14 30-Jun-20 -

7 ANR 378

Climate Resilience Sector Project 19.250 0.046 9-Dec-13 12-Mar-14 30-Jun-19 -

8 ENE 389

Cyclone Ian Recovery Project 4.520 0.138 16-May-14 17-Sep-14 30-Jun-18 -

9 ENE 390

Cyclone Ian Recovery Project 4.266 - 16-May-14 17-Sep-14 30-Jun-18 -

Total 68.036 21.884

ANR = Agriculture, Natural Resources and Rural Development; ENE = Energy; ICT = Information and Communication Technology;

WUS = Water and Other Urban Infrastructure and Services

Source: GFIS

19

Ap

pe

ndix

2

DEVELOPMENT COORDINATION

Development Coordination Matrix

Sectors and Themes

Current ADB Strategy and/or Activities

Other Development Partners’ Strategies and/or Main Activities

Multilateral Institutions and the UN System Bilateral

Sector

Transport, ICT Submarine Fibre-Optic Cable Contribution to Pacific Infrastructure Advisory Centre (which among other activities supported the preparation and updating of the National Infrastructure Investment Plan), and co-financing from the Pacific Region Infrastructure Facility

World Bank IFC

Transport Sector Consolidation Project (TCSP), addressing all transport modes Pacific Islands Regional Connectivity (Tonga Broadband Connectivity) Pacific Islands Aviation Investment Program (including funding for Fua’amotu and Vava’u airports). Loan to Digicel Tonga

AusAID JICA China New Zealand

Co-financing for TCSP Replacement inter-island ferry Road improvement grant Concessional loan for road improvement and Vuna Wharf Vaipua Bridge, Vava’u Aircraft for domestic air service ‘Eua airport runway upgrade

Energy Renewable Energy Project Phases 1 and 2 Sustainable off-grid systems Energy efficiency

World Bank Tonga Energy Road Map (TERM)

AusAID New Zealand JICA United Arab Emirates

Co-financing for TERM Solar generation farm, Tongatapu Tonga village network upgrade Off-grid solar power systems and village power supplies, Tongatapu and Vava’u Solar micro-grid development, Tongatapu Solar power plant, Vava’u

Ap

pen

dix

2 2

0

Sectors and Themes

Current ADB Strategy and/or Activities

Other Development Partners’ Strategies and/or Main Activities

Multilateral Institutions and the UN System Bilateral

Urban development (roads, water, sanitation)

Nuku’alofa Urban Development Sector Project

AusAID China JICA

Co-financing for Nuku’alofa Urban Development Sector Project Concessional loan for Nuku’alofa Reconstruction Vava’u solid waste management

Theme

Climate resilience Strategic Program for Climate Resilience

UNDP World Bank

Pacific Risk Resilience Program covers four countries including Tonga Contributing to Pilot Program for Climate Resilience (PPCR)

AusAID JICA

Contributing to Pilot Program for Climate Resilience (PPCR) Numerous projects including training and capacity building, rural DRM activities, and earthquake observation assistance

Public sector management

Strengthening Public Finance Management (including budget support linked to joint policy matrix) Implementing the Public Finance Management Roadmap Regional TA to support economic management TA relating to social protection measures

World Bank PFTAC EU

Budget support, linked to joint policy matrix Technical assistance in PFM improvements Budget support, linked to renewable energy and energy efficiency indicators and recognizing joint policy matrix

AusAID UNDP

Budget support, linked to joint policy matrix Support for Parliament and Freedom of Information legislation

Private sector development

Regional TA to support private sector development, including funding for Private Sector Assessment

New Zealand Business Enterprise Centre Tourism Support Program

ADB = Asian Development Bank, AusAID = Australian Agency for International Development, EU = European Union, IFC = International Finance Corporation, JICA = Japan International Cooperation Agency, PFTAC = Pacific Financial Technical Assistance Centre, UNDP = United Nations Development Programme. Sources: Ministry of Finance and National Planning aid management database.

Appendix 3 21

SECTOR ASSESSMENTS

I. INFRASTRUCTURE SECTOR ASSESSMENT

A. Sector Situation and Key Issues3

1. The Tonga National Infrastructure Investment Plan (NIIP 2013 - in draft) notes that infrastructure plays a critical role in achieving the goals of the TSDF, because there is a clear and positive linkage between infrastructure, social development and economic growth. There is consensus that:

• There is a positive correlation between infrastructure and economic outcomes.

Investments in core economic infrastructure (such as electricity, telecoms, transport,

sewerage and water systems) produce the largest gains in productivity, while investments in roads and telecommunications typically deliver the greatest social

returns;

• Maintenance is not “visible” but is more likely to have a greater positive influence on

economic output than new projects.

• When access to core infrastructure has been addressed, the best economic results come from improving efficiency and then from reducing service prices.

• Infrastructure investment only adds value if it is allocated in the right way.

2. Inadequate infrastructure is a bottleneck to economic activity, and also reduces the day-to-day well-being of people; their quality of life; and the ability to withstand and respond to disasters. Sustainability is also compromised because resources are used wastefully. 3. Tonga is generally well-placed regarding access to basic infrastructure and associated services and the coverage and capacity of those services, with full national coverage of basic telecoms; a high level of access to reticulated power and water and off-grid arrangements in place elsewhere; one of the highest levels of road density in the region; and a strategically located network of ports and airports throughout the country. 4. The main priority now for development of Tonga’s infrastructure sector is to continue improving basic services, but at the same time, to use infrastructure investment as a catalyst for improved macroeconomic, social and environmental outcomes. Key drivers of need for further investment in infrastructure are:

• Continuing to provide basic infrastructure that is appropriate, well planned and

maintained.

• Achieving national goals as set out in the TSDF and developing the country as a whole.

The small dispersed population, multi-island geography, remoteness from markets, and

small market size of Tonga creates special challenges for development and operation of

infrastructure in support of these goals.

• Keeping pace with growth and shifts in demand for infrastructure services. In particular,

trends in population (especially drift to urban areas) and the opportunities arising from

new technology (such as online services) are changing the nature and pattern of

demand for infrastructure services.

• Addressing a range of specific issues and deficiencies with existing infrastructure so that the infrastructure system functions more effectively. Because of under-investment and

3 This section draws on the Tonga National Infrastructure Investment Plan 2013 (in draft).

22 Appendix 3

insufficient attention to maintenance in some areas, there is a backlog of infrastructure

deficiencies that need to be addressed.

• Improving the quality, safety, and reliability of economic infrastructure. As well as ensuring access to basic services, there are growing community expectations regarding

the quality of the services provided.

• Improving the resilience of infrastructure to the impacts of climate change and natural

disasters to protect the community and provide a safeguard so that infrastructure

services are still available when they are needed most.

• Lowering the cost of doing business (especially in areas such as energy and

telecommunications) to provide a catalyst for economic growth and enhance the

competitiveness of local business.

• Ensuring that Tonga maintains its compliance with international regulations, especially

safety and security in the international aviation and maritime sectors, so that connectivity to international markets is not constrained.

5. The role of government in relation to the infrastructure sector is changing. Government has largely moved away from taking responsibility for infrastructure investment and service delivery, to being a facilitator of infrastructure service outcomes. Under current arrangements, all economic infrastructure except roads and outer islands ports is now under the management and operation of Public Enterprises. This change is consistent with international good practice, but it requires a continuing focus by Government on the policy, legislation, institutional and regulatory environment that underpins infrastructure management. 6. The current situation and key issues in infrastructure sub-sectors, as identified in NIIP 2013, are:

i. Energy

7. Tonga has one of the highest levels of access to electricity in the region with around 85% of the population on-grid and high levels of supply reliability. But at the same time, Tonga has historically had one of the highest costs of electricity in the region. In part, this was a result of Tonga’s reliance on diesel-powered generation for on-grid services. System losses were also high at around 17% but are coming down and are expected to be reduced to around 13% by 2015. This is more consistent with international benchmarks. 8. The energy sector is in a phase of rebuilding and transformation. Tonga Power is investing heavily from its own resources to rehabilitate the electricity generation and supply system to increase efficiency and safety; and is working with development partners to upgrade village power supply systems and off-grid supply. At the same time, initiatives are underway to transform electricity production with a move towards greater stability and self-sufficiency. In 2009, Government responded to the twin challenges of reducing the Tongan contribution to global Greenhouse Gas (GHG) emissions and improving national energy security by endorsing a policy of 50% of energy from renewable resources. This is a challenging target that provides a clear indication that environmental sustainability and reducing the vulnerability of the country to future oil price shocks are key Government objectives. Government’s response to this target is set out in the Tonga Energy Road Map (TERM) 2010-2020.

Appendix 3 23

Challenges 9. Reducing the cost of doing business, improving the quality of life of people, and Government’s commitment to addressing climate change are driving the need for improved energy infrastructure. Under current conditions, growth in demand is not a major factor driving the need for investment. As noted above, Tonga has historically had some of the highest costs of electricity in the region. This has a negative impact of business costs and on household budgets. In addition, the high level of reliance on imported petroleum creates energy security and price stability issues.

ii. Telecommunications

10. In terms of access to basic telecommunications services, Tonga is well positioned. Mobile phone and internet services are already available throughout the country, including smaller and more remote communities. The completion of an undersea fibre-optic link to Fiji, scheduled for 2013, will deliver a step-change in speed, capacity and quality that will redefine telecommunications in Tonga; offset some of the geographical disadvantage experienced by Tonga; and create new economic and social opportunities. Competition and private sector involvement in the telecommunications sector has been a strong force driving these developments.

Challenges

11. Business and social connectivity and reducing the cost of doing business are key factors driving the need for improved telecommunications infrastructure. High standard telecoms can offset some of the geographical disadvantage experienced by Tonga and increase the international competitiveness of Tongan business, for instance in the tourism industry. Telecommunications also has a vital role during natural disasters and other emergency situations.

iii. Water and Sanitation

12. All Tongans have access to clean drinking water and around 85% of households have piped water supply. So in terms of meetings MDGs and providing basic access to clean water, the water sector is performing well. However problems exist in the efficiency of water supply, and a major challenge facing the reticulated water supply system is to reduce water losses. 13. Although Tonga does not currently have a central sewerage system in any urban area, important issues relating to disposal of grey water and septage (sludge pumped from septic tanks) are emerging and are likely to require a coordinated response in the short-medium term. As a partial response, a grey water collection system has been installed in central Nuku’alofa as part of the CBD redevelopment project.

Challenges

14. The need for infrastructure investment in the Water sector is driven by population trends; household consumption patterns; health and quality standards; and efficient management of valuable water supply resources. Another challenge is reducing loss and waste of valuable water. TWB is already working to reduce water losses and upgrade efficiency throughout its water supply and distribution system. There is also the opportunity for TWB and village water supply managers to be proactive in promoting responsible use of water through demand-side management (DSM) initiatives similar to the energy sector.

24 Appendix 3

iv. Solid Waste

15. In 2007, a new solid waste collection system was implemented on Tongatapu and the Waste Authority Limited (WAL) was established to take control of solid waste collection and disposal. On most other islands, formal arrangements for solid waste collection are not in place. WAL is gradually improving its performance but continues to require financial support from Government; there are also problems with the design of existing equipment and facilities, and an emerging problem with illegal dumping of waste.

Challenges

16. The need for infrastructure investment in the Solid Waste sector is driven by population trends; household consumption patterns; and health and quality standards. On Tongatapu, urban population growth at levels of up to 2.5% per year in some areas is increasing the demand for collection and disposal services. This is straining the capacity of WAL to meet the demand, especially while WAL is in a rebuilding phase. On outer islands, the challenge is to provide a long-term solution for sanitary and environmentally-acceptable disposal of solid waste.

v. Roads

17. Tonga has an extensive network of roads and one of the highest levels of road network density in the region. This network provides good access links to communities in terms of connectivity, but in some areas the condition has deteriorated significantly due to insufficient emphasis on maintenance. Government is addressing this problem through several road rehabilitation and upgrading programs in association with its development partners. Studies underway as part of the TSCP program provide a strategy for road maintenance over the next 5-10 years, including recommendations for road maintenance programming, institutional reform, sustainable funding mechanisms (such as a road fund); and the role of the private sector.

Challenges

18. Some parts of the road system are in poor condition and this is having a significant negative impact on the cost of road transport and links to market for agricultural producers. The main challenge driving the need for investment in roads is to progressively clear the backlog of maintenance and rehabilitate the road system to a standard where it can be sustainably maintained in a cost-effective way using local resources and expertise.

vi. Maritime

19. The maritime sector supports tourism; inter-island and international commerce; and inter-island travel for social, educational and medical needs. The existing ports have sufficient capacity for foreseeable needs and there are no plans to build any new ports for commercial shipping operations. In addition, the international ports comply with relevant international and IMO operating requirements. Although the port system meets basic needs for coverage, capacity and compliance, the standard of infrastructure has suffered from a lack of investment in core infrastructure and facilities; and insufficient emphasis on maintenance of outer-island ports and channels. For the medium-longer term, investment planning for the port sector is less well developed and it is important that an integrated approach is applied that enhances the overall safety, efficiency and resilience of the port system as a whole.

Challenges

20. Safety is government’s key priority for the maritime sector. Responding to this challenge will require investment in people, systems and infrastructure. There is also a need to put in

Appendix 3 25

place stronger institutional arrangements for operating and maintaining outer island ports, as the Ports Authority of Tonga currently handles only the Nuku’alofa port. The other major challenge driving the need for investment in the ports sector is building resilience to the impacts of climate change and natural disasters.

vii. Airports

21. Aviation also plays a vital role in connecting the Tongan economy and community in terms of tourism; inter-island and international commerce; and travel for social, educational and medical needs. The existing commercial airports provide sufficient coverage to all island groups and at this stage have sufficient capacity for foreseeable needs. However much of the infrastructure is nearing the end of its useful life or requires upgrade to continue to meet international and national safety and security standards. All commercial airports in Tonga are managed by Tonga Airports Ltd (TAL). 22. A significant investment program is already underway in the airport sector, with a focus on meeting safety and security compliance requirements in terms of fire and rescue capability, security screening, navigational aids, and runway condition. This includes resurfacing of runways at Fua’amotu and Vava’u.

Challenges

23. Safety, security and continuity of services are the key imperatives driving investment and reform in the aviation sector. The other major challenge in the aviation sector is to ensure that a supportive policy and institutional environment is in place for competitive and stable international and domestic air services.

viii. Multi-sector

24. Multi-sector projects generally fall into two broad categories. The first involves complex construction projects with the need for coordination across several sectors, such as electricity, telecoms, roads and water. The second category involves cross-cutting issues, especially climate change adaptation and disaster risk management (CCA/DRM).

Challenges

25. Tonga is especially vulnerable to CCA/DRM impacts. The overall challenge is firstly to ensure that potential CCA/DRM impacts are considered in all aspects of infrastructure planning, design, construction and management; and secondly that Tonga is well-prepared to respond quickly and effectively to disasters when they happen. Another key multi-sector challenge is construction coordination as projects increase in complexity. The third challenge is asset management, and especially maintenance.

26 Appendix 3

Overview of the economic infrastructure sector

Sector Notes

Energy 15.5 MW total installed capacity (Tongatapu, Vava’u, Ha’apai, ‘Eua) 1,300 km of distribution network (total of overhead, underground, submarine and low voltage cables) 16,500 domestic, 4,000 commercial customers 85% of population on-grid 15-16% line losses

Telecommunications Telephone access available throughout the country (fixed line or mobile) 15,000 landline subscribers (estimated 70% of households) 53,000 mobile customers (TCC, Digicel) 3,000 internet connections (1,200 TCC & 1597 TCC GSM Mobile Internet)

Water and sanitation 100% of population have access to safe drinking water (reticulated supply, rainwater tanks, wells, etc) 85% of households have piped water 4 x reticulated water supply schemes (Nuku’alofa, Nieafu, Pangai-Hihifo, ‘Eua) 15-39% Total losses (Nuku’alofa 39%) No central sewage collection and treatment system (septic tanks)

Solid Waste 1 x sanitary landfill (Tapuhia, Tongatapu) Household collection of solid waste on Tongatapu only No regular system for collection of recyclables

Transport Airports 1 x International/Domestic airport (Fua’amotu 2,671m asphalt

runway) 2 x Domestic airport – bitumen runway (Ha’apai, Vava’u) 1 x Domestic airport – chip seal runway (‘Eua) 2 x Domestic airport – grass runway (Niuafo’ou, Niuatoputapu) 80,000 international and 50,000 domestic departures per year 14 international flights per week (4 international destinations)

Roads 880 km (including community roads) 40% sealed 15,500 vehicles

Sea Ports 2 x International/Domestic ports (Nuku’alofa – 3 international, 2 inter-island berths; Vava’u – 1 international, 1 inter-island berth) 5 x domestic ports (‘Eua, Ha’afeva, Pangai, Niuafo’ou, Niuatoputapu) 8,500 international container movements per year (full TEU) (90% imports) 149 international ship calls at Nuku’alofa (General Cargo, Cruise, Tanker, Other)

Sources: From NIIP 2013 (in draft) – original sources: Infrastructure managers (TPL, TWB, TCC, PAT, TAL, Ministries); Tonga Census; various feasibility studies

Government’s Sector Policy and Planning Framework4 26. Outcome objective 3 of the TSDF 2011-2014 is for appropriate, well planned and maintained infrastructure that improves the everyday lives of the people and lowers the cost of

4 This section draws on the Tonga Strategic Development Framework 2011-2014.

Appendix 3 27

business, by the adequate funding and implementation of the National Infrastructure Investment Plan. Strategies directed at the achievement of this objective, as identified in TSDF, are:

• Ensuring safe and reliable transport infrastructure (roads, ports, airports), with the

necessary institutional arrangements in place to manage and fund effective development and maintenance of these facilities throughout the Kingdom.

• Increasing competition, with responsible supervision, to increase the quality of air and

sea transport services both domestically and between the Kingdom and overseas.

• Strengthening regulatory compliance and safety oversight of the transport sector to

ensure compliance with international safety standards.

• Improving the performance of the information and communications sector, with quality

service delivery, free and fair availability of information, geographical coverage, service affordability, and access to new service applications.

• Maintaining, and where possible expanding, the provision of reliable and cost efficient

power supplies, using traditional and renewable options, to all communities.

• Improving, and where possible expanding, the safe collection, disposal and recycling of

solid and liquid waste to protect people’s health and the environment.

• Maintaining and expanding access to safe water and sanitation for all communities.

• Taking a sector-wide approach to the provision and maintenance of infrastructure,

seeking alternative options for provision and cost-recovery, and implement the proposed

priority projects outlined in the NIIP (including: energy, telecoms, water, solid waste,

roads, ports and airports.

Government’s Institutional Arrangements and Capacity in the Sector5 27. NIIP 2013 notes that responsibility for infrastructure/service delivery is split between Government Ministries, Public Enterprises and the private sector (telecommunications only); and in some sectors Ministries and Public Enterprises are both involved. There is also outsourcing and sub-contracting to the private sector, which is happening in some sectors. 28. In some sectors, there are different agencies responsible for infrastructure/service delivery at different geographic/administrative levels. There are gaps in infrastructure/service delivery. It is unclear whether there is an agency responsible for infrastructure/services in the liquid waste/sanitation sector and for drainage. There are several agencies responsible for monitoring and standards (Environment & Climate Change; Health; Works), but liquid waste and run-off appear to be gaps in terms of responsibility for infrastructure. There are multiple agencies regulating different aspects of some sectors, for instance in the water sector, MLECCNR has a role in protecting water supply catchments and groundwater; Ministry of Health in testing water quality/contamination; and MAFF in some areas of resource management. This situation is not unusual, but does create potential for inefficient overlaps and delays. In the ports sector, responsibility for infrastructure/service delivery is split between a Ministry and Public Enterprise. In addition, the Ministry of Infrastructure is both operator and regulator which is contrary to general principles of good governance.

5 This section draws on the Tonga National Infrastructure Investment Plan 2013 (in draft).

28 Appendix 3

Institutional structure of the economic infrastructure sector

Sector Scope of services

Infrastructure/ Service Delivery

Regulation/ Monitoring Planning/ Policy

Power National Tonga Power Ltd

Electricity Commission TERM MLECCNR

Off-grid Outer Islands

MLECCNR/ Community

Telecoms National TCC/ Digicel PMO/MIC PMO/MIC Water National MLECCNR

MOH MAFF

MLECCNR MOH

Urban Areas Tonga Water Board (TWB)

TWB MPE

TWB MPE

Villages / Outer Islands

Village Committees Tonga Water

MOH MLECCNR

MOH MLECCNR

Sanitation National Private Sector/ Community

MLECCNR MOH

MOH

Urban Areas Villages Solid Waste National MLECCNR

MOH MLECCNR MOH

Nuku'alofa Waste Authority Ltd/ Private sector

Rural Tongatapu

Waste Authority Ltd

Other Islands Community MLECCNR MLECCNR Drainage National MOI MOI MOI Roads National MOI MOI MOI Ports Nuku'alofa Ports Authority

Tonga MOI MOI

Outer Islands MOI MOI MOI Airports National Tonga Airports Ltd MOI MOI Source: From NIIP 2013 (in draft) Legend: MLECCNR (Ministry of Lands, Environment, Climate Change and Natural Resources); MOH (Ministry of Health); MOI (Ministry of Infrastructure); TCC (Tonga Communications Corporation); MIC (Ministry of Information & Communication); MPE (Ministry of Public Enterprises); WAL (Waste Authority Ltd)

ADB Sector Experience 29. ADB has extensive experience across most infrastructure sub-sectors. In Tonga, ADB support is currently focused on:

• Urban development, with involvement in the Integrated Urban Development Sector

Project (focusing on urban roads and drainage, and capacity for urban planning) which is

coming to a close, and the Nuku’alofa Urban Development Sector Project (focusing on

improvements to water supply and sanitation, and institutional strengthening in this sector) which is underway.

• Renewable Energy, with projects underway to add solar generation capacity to power

grids in outer islands and to improve the efficiency of distribution of these grids, as well

as support through regional projects to introduce energy efficient technology and for off-grid solar installations.

Appendix 3 29

• Telecommunications, with the recent support for the Tonga-Fiji Submarine Cable Project

which will provide a major boost to the capacity of internet and other telecommunications

systems in Tonga.

Role of Other Development Partners in the Sector6 The table below provides information on the major activities supported by other Development Partners in infrastructure sub-sectors, both in recent years and planned.

Development partners involved in infrastructure

Development partner

Programming process

Recent and planned support for infrastructure

Approx. value (TOP

million) World Bank Country Assistance

Strategy (2011-14).

IFC Loan to Digicel Tonga.

Tonga Post Tsunami Reconstruction.

Pacific Islands Regional Connectivity

(Tonga Broadband Connectivity).

Transport Sector Consolidation Project

(TSCP), and transport follow-up.

Tonga Energy Road Map (TERM).

Pacific Islands Aviation Investment

Program (including funding for Fua’amotu

and Vava’u airports).

11

8

17

7

8

47

Australia Australia-Tonga

Partnership for

Development (2009-

2015).

Grant co-financing of WB led Transport

Sector Consolidation Project (TSCP),

ADB led Nuku’alofa Urban Development

Sector (NUDS) Project, WB led Tonga

Energy Road Map (TERM) Institutional

and Regulatory Framework

Strengthening Project, and assistance to

TERM Implementation Unit through

PIAC.

Upgrading of village water supplies.

27

Japan Project identification

within a development

assistance framework

(current focus on

climate change

adaptation, disaster

management, and the

environment).

Replacement inter-island ferry.

Vava’u waste management.

Small scale village water supplies.

Off-grid solar power systems and village

power supplies.

Solar micro-grid development, Tongatapu

25

3

2

12

24

6 This section draws on Annex F of the Tonga National Infrastructure Investment Plan 2013 (in draft)

30 Appendix 3

Development partner

Programming process

Recent and planned support for infrastructure

Approx. value (TOP

million) China Respond to requests

from the Government.

Roads improvement grant

Concessional loans for Nuku’alofa

Reconstruction (Vuna Wharf component)

and Roads Improvement.

Vaipua Bridge, Vava’u

Aircraft for domestic services

116

8

New Zealand Tonga-New Zealand

Joint Commitment for

Development (2011)

Solar generation farm – Tongatapu.

Tonga village network upgrade (with

World Bank and EU).

‘Eua airport runway rehabilitation.

Other involvement in infrastructure

related activities:

- Meridian operating costs (status: active)

- Major energy investment (status:

proposed)

- Ecocare Pacific Trust: solar PV and ICT

program for Tongan schools (status:

active)

- Pacific maritime safety: Manukau

Institute of Technology / NZ Maritime

School training for FISA crew in Tonga

(status: active)

- Pacific maritime safety: technical

assistance to Tonga MOT (status: active)

14

4

4

European

Union

National Indicative

Programme (2008-

13) linked to

allocations under the

European

Development Fund

(currently the 10th

EDF).

Sector budget support with renewable

energy as the focal sector.

2

United Arab Emirates

Solar power plant, Vava’u

Source: Adapted from Annex F, NIIP 2013 (in draft)

Appendix 3 31

II. CLIMATE RESILIENCE ASSESSMENT

A. Sector Situation and Key Issues7

1. The Tonga National Infrastructure Investment Plan (NIIP 2013—in draft) notes that Tonga is particularly vulnerable to natural disasters, and the effects of climate variability and long-term climate change8. Between 1991 and 2010, climate and non-climate related disasters in the form of cyclones, droughts, tsunamis and storm surge cost Tonga an average of 1.18% of GDP annually and affected thousands of households. Climate change is expected not only to exacerbate the frequency and/or intensity of extreme climate events in Tonga, but is projected to cause long-term, and in some cases irreversible, changes to climate. 2. At the national level, the Government of Tonga has prepared and endorsed the Joint National Action Plan on DRM and CCA for 2010 to 2015 (referred to as the JNAP) that highlights priority actions for Disaster Risk Management and Climate Change Adaptation over the next decade.

B. Climate and Natural Disaster Profile

3. Annex D of NIIP 2013 provides an overview of the current climate and recent observed trends in climate in terms of average terrestrial and marine parameters (rainfall, temperature, sea level, sea surface temperature and ocean acidifications), as well as extreme climate events (drought, cyclones, and storm surge). Located in the western South Pacific Ocean, Tonga experiences a typically tropical climate. There is a marked wet season between November and April, during which nearly two-thirds of annual rainfall is experienced. Remaining rainfall is experienced in the dry season between May and October. Average annual rainfall varies across the country; average annual rainfall is higher in Niua Fo’ou (2453 mm/year), Niua Toputapu (2374 mm/year) and Vava’u (2150 mm/year) than in Tongatapu (1721 mm/year) and Ha’apai (1619 mm/year). Inter-annual rainfall variability is high and during the wettest years total annual rainfall can be three times higher than during the driest years. The El Nino Southern Oscillation (ENSO) is a major influence on inter-annual rainfall variability. 4. Seasonal changes in air temperature result from the location of Tonga close to the sub-tropics, with sea surface temperature (SST) of surrounding waters an influence on seasonal variations. Average annual air temperature ranges from 27˚C at Niua Fo’ou and Niua Toputapu to 24˚C on Tongatapu. During the wet season, air temperature is generally higher than during the dry season and diurnal and seasonal variations can reach as high as 6°C throughout the country. Increases in air temperature (warming trends) have been observed for annual and seasonal mean air temperatures in Nuku’alofa for the period from 1950 to 2009, with the strongest trends of 0.16°C/decade recorded in the wet season. Data from 1970 to 2009 indicate warming trends of 0.4 to 0.9˚C in annual mean temperature over this period in Ha’apai, Vava’u and Niua Toputapu.

7 This section draws on Annex D of the Tonga National Infrastructure Investment Plan 2013(in draft), and the Joint

National Action Plan on Climate Change Adaptation and Disaster Risk Management 2010-2015 (JNAP). 8 The World Risk Report 2011, ranks Tonga as having the second highest risk globally to natural disaster risk based

on consideration of exposure, susceptibility, coping capacity and adaptive capacity (UNU IEHS, 2011); a Small States Secretariat analysis ranks Tonga third out of 111 countries in terms of vulnerability to climate change; whilst the Global Climate Risk Index ranks Tonga 19th out of 179 countries in terms of observed average annual losses as a percentage of GDP due to climate related disasters between 1991 and 2010, and 19th in terms of deaths per hundred thousand of population in this same period.

32 Appendix 3

5. Sea level trend data indicate a rising trend for sea level of approximately 6 mm/year since 1993; this equates to a cumulative sea level rise (SLR) of approximately 114mm in this 19-year period. The rate of sea level rise experienced is greater than the global average of 3.2 ± 0.4 mm / year. SLR is associated with coastal erosion and can increase the magnitude of storm surge as it provides a higher ‘starting point’ for wave action. Coastal erosion is being experienced along much of the northern coastline of Tongatapu, and along the coastline of Lifuka Island in Ha’apai. 6. SST data indicate that warming has been experienced at the rate of approximately 0.06°C per decade since 1970. However, at the regional scales at which the models operate, natural variability invariably plays a large role and it is difficult to identify long-term trends. SST is of concern because of its role in coral bleaching events; the last major coral bleaching event in the waters surrounding Tonga was in 2000. Anecdotal evidence indicates that smaller-scale coral bleaching events have become more frequent in recent years. 7. Ocean acidification, which is driven by the absorption of carbon dioxide (CO2) in seawater and measured in terms of the aragonite saturation state (Ωar), is an important influence on coral growth and the development of healthy reef ecosystems. In the Tongan region, the aragonite saturation state declined from around Ωar = 4.5 in the late 18th century to Ωar = 4.0 ± 0.1 by 2000 indicating increased acidity of seawater. 8. Tonga experiences on average 17 tropical cyclones per decade with most cyclones occurring in the wet season between November and April. Tropical cyclones exhibit high inter-annual variability ranging from zero some years to five cyclones/year in other years. Tropical cyclone incidence is highest in ENSO years. This high inter-annual variability makes it difficult to identify long term trends in cyclone frequency, however there is some evidence that decadal frequency is increasing with 7 cyclones experienced in the 1960s compared to 15 in the 1990s. Storm surge and extreme sea level events are most commonly associated with named tropical cyclones. 9. Droughts in Tonga are linked to low rainfall during ENSO periods. The last three major drought events were in 1983, 1998 and 2006. During these droughts, annual rainfall measured from 70 to 142 mm/year, more than ten times less than average annual rainfall in non-drought periods. C. Projected Future Climate Conditions

10. Information on climate projections for Tonga has been drawn from recent analyses undertaken by the Pacific Climate Change Science Program (PCCSP) and is based on the outputs of 18 global circulation models (GCM) for three emissions scenarios9. The projections discussed in this section are drawn from global level models and as such refer to average change over the broad geographic region of Tonga including the islands and surrounding ocean. 11. The “most likely climate future” for Tonga as described by the PCCSP is for warmer conditions with little change in rainfall. Intra-annual rainfall variability is expected to change with wet season rainfall expected to increase and dry season rainfall expected to decrease, but with

9 Scenarios used are drawn from IPCC (2007) and are B1 – a low emissions scenario, A1B – a medium emissions

scenario, and A2 – a high emissions scenario; the corresponding timeframes are three twenty-year periods centered on 2030, 2055 and 2090 relative to 1990.

Appendix 3 33

an overall net effect of little change in total annual rainfall. The intensity and frequency of extreme rainfall days is projected to increase. Changes in inter-annual rainfall are strongly influenced by ENSO conditions and because there is no consensus view of the likely evolution of ENSO under climate change scenarios, it is not possible to develop projections for changes in inter-annual rainfall variability. 12. Air temperature in Tonga is expected to continue to increase. An increase of < 1°C is projected by 2030, with increases of up to 2.5°C projected by 2090. The intensity and frequency of extreme hot days is projected to increase; for example, a maximum daily air temperature of at least 32.5°C current has a return period of 200 years, by 2050, it is projected that this return period will decrease to 35 years10. 13. Increases in mean sea level are expected to continue. The analyses carried out by PCCSP project SLR of 50 to 150 mm by 2030 and 200 to 600 mm by 2090. Climate change is also expected to have a significant effect on the return periods of extreme high sea levels that persist for at least an hour and which can cause coastal flooding, accelerated coastal erosion and saline intrusion into groundwater. An hourly sea level of 2.2m currently has a return period of 579 years; by 2050, it is projected that this return period will decrease to 1.5 years. 14. Estimates of the population and land area that could be affected by SLR scenarios of 0.3m and 1.0m, with and without storm surge, highlight the negative synergies projected to occur between SLR and storm surge, and indicate that with SLR of 0.3m (a scenario in the middle of the projected range), 14% of the population and nearly 4% of the land area of Tongatapu could be inundated. If the same SLR scenario occurred simultaneously with a storm surge equivalent to that recorded in 1983, over one third of the population and over 10% of the land area of Tongatapu could be affected by periodic inundation. Ha’apai, a group of 43 low elevation (≈ 1.0m ASL) coral islands, is likely to be significantly affected by SLR.

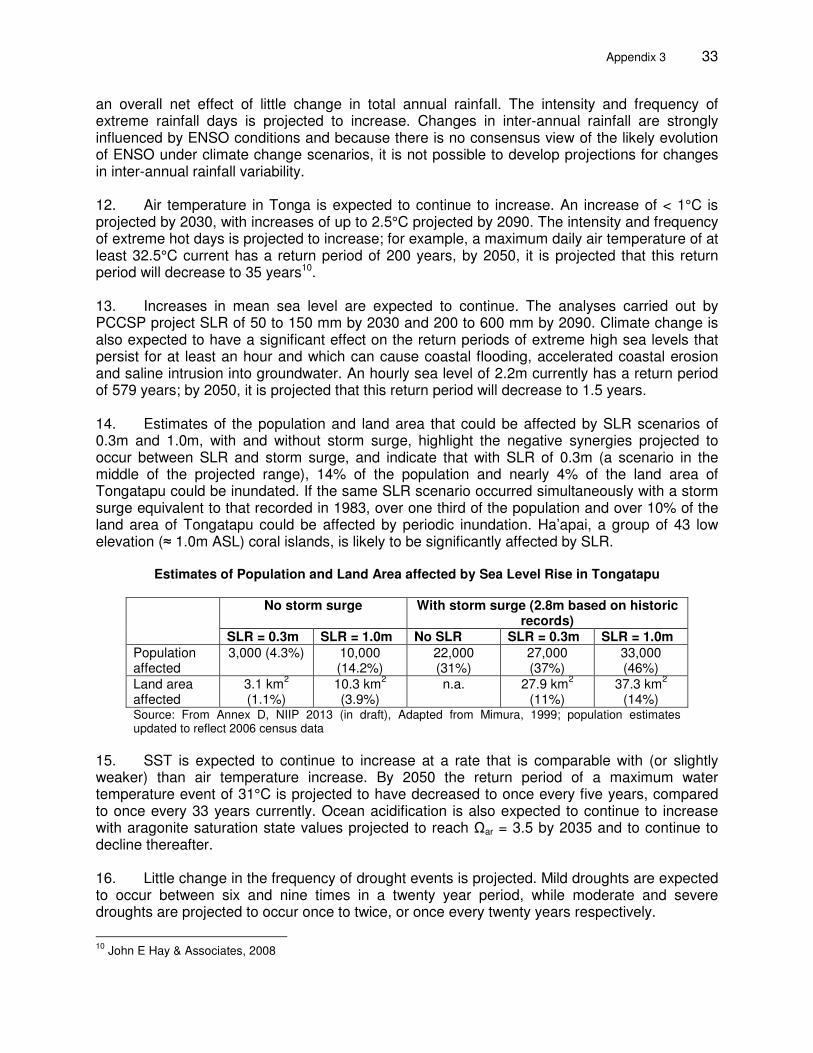

Estimates of Population and Land Area affected by Sea Level Rise in Tongatapu

No storm surge With storm surge (2.8m based on historic records)

SLR = 0.3m SLR = 1.0m No SLR SLR = 0.3m SLR = 1.0m Population affected

3,000 (4.3%) 10,000 (14.2%)