tomatoes market overview in romania - gti › wp-content › uploads › 2018 › 08 › ... ·...

TRANSCRIPT

June 2018

Tomatoes market

overview in Romania

2

TABLE OF CONTENTS

Summery ______________________________________________________ 4

PEST Analysis __________________________________________________ 7

Political Environment ______________________________________________________ 7

The Political System in Romania ___________________________________________ 7

Government Stability ____________________________________________________ 7

Employment laws _______________________________________________________ 7

Tax Regulations ________________________________________________________ 8

Corruption Levels _______________________________________________________ 8

Trade Regulations& Customs _____________________________________________ 8

Economic Environment ____________________________________________________ 9

GDP and Inflation ______________________________________________________ 9

Currency & Interest rates:_________________________________________________ 9

Credit accessibility: _____________________________________________________ 10

Disposable income of buyers: ____________________________________________ 10

Tax& Duties __________________________________________________________ 11

Social Environment ______________________________________________________ 12

Demographics ________________________________________________________ 12

Cross-cultural communication ____________________________________________ 13

Consumer behavior ____________________________________________________ 15

Distribution of Income ___________________________________________________ 16

Happiness Index: ______________________________________________________ 16

Human Development: ___________________________________________________ 17

Age dependency ratio: __________________________________________________ 17

Technology Environment __________________________________________________ 18

Port traffic & infrastructure _______________________________________________ 18

Railway transport of goods: ______________________________________________ 18

Road transportation ____________________________________________________ 18

Enabling Trade ________________________________________________ 19

Overview _____________________________________________________________ 19

Most problematic factors for exporting to Romania ____________________________ 21

3

Most problematic factors for exporting from Romania __________________________ 21

Product Brief __________________________________________________ 22

Product Definition ________________________________________________________ 22

Local Production ________________________________________________________ 23

Romania Imports of Tomatoes ______________________________________________ 25

Romania Exports of tomatoes ______________________________________________ 28

Consumption ___________________________________________________________ 29

Product Quality __________________________________________________________ 30

Product Trends and outlook ________________________________________________ 36

Compliance for export ___________________________________________ 38

A. Legal & Non-Legal requirement the product must comply with ______________ 39

Distribution Channel ____________________________________________ 43

SUpplying Markets and competition ________________________________ 47

Pricing _______________________________________________________ 48

MArket Requirments & Certificates _________________________________ 51

Potential Leads ________________________________________________ 53

References ___________________________________________________ 55

Appendix: OVERVIEW GLOBAL tomatoes MARKET ___________________ 57

4

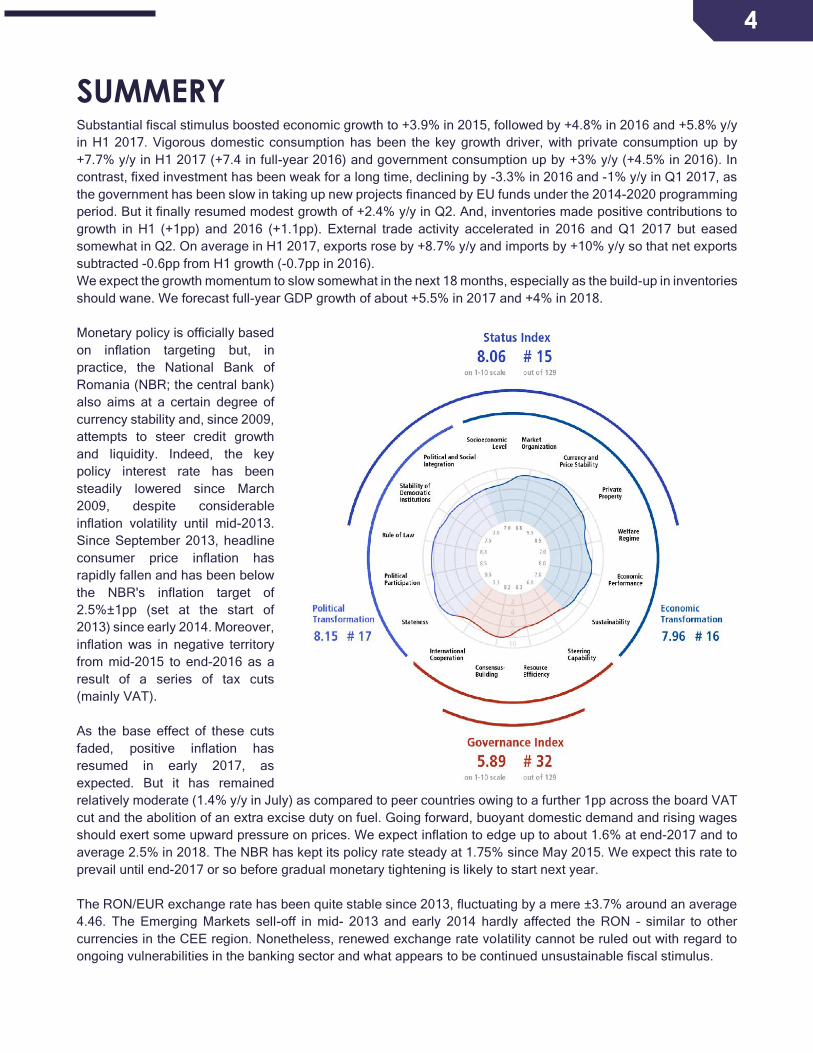

SUMMERY Substantial fiscal stimulus boosted economic growth to +3.9% in 2015, followed by +4.8% in 2016 and +5.8% y/y

in H1 2017. Vigorous domestic consumption has been the key growth driver, with private consumption up by

+7.7% y/y in H1 2017 (+7.4 in full-year 2016) and government consumption up by +3% y/y (+4.5% in 2016). In

contrast, fixed investment has been weak for a long time, declining by -3.3% in 2016 and -1% y/y in Q1 2017, as

the government has been slow in taking up new projects financed by EU funds under the 2014-2020 programming

period. But it finally resumed modest growth of +2.4% y/y in Q2. And, inventories made positive contributions to

growth in H1 (+1pp) and 2016 (+1.1pp). External trade activity accelerated in 2016 and Q1 2017 but eased

somewhat in Q2. On average in H1 2017, exports rose by +8.7% y/y and imports by +10% y/y so that net exports

subtracted -0.6pp from H1 growth (-0.7pp in 2016).

We expect the growth momentum to slow somewhat in the next 18 months, especially as the build-up in inventories

should wane. We forecast full-year GDP growth of about +5.5% in 2017 and +4% in 2018.

Monetary policy is officially based

on inflation targeting but, in

practice, the National Bank of

Romania (NBR; the central bank)

also aims at a certain degree of

currency stability and, since 2009,

attempts to steer credit growth

and liquidity. Indeed, the key

policy interest rate has been

steadily lowered since March

2009, despite considerable

inflation volatility until mid-2013.

Since September 2013, headline

consumer price inflation has

rapidly fallen and has been below

the NBR's inflation target of

2.5%±1pp (set at the start of

2013) since early 2014. Moreover,

inflation was in negative territory

from mid-2015 to end-2016 as a

result of a series of tax cuts

(mainly VAT).

As the base effect of these cuts

faded, positive inflation has

resumed in early 2017, as

expected. But it has remained

relatively moderate (1.4% y/y in July) as compared to peer countries owing to a further 1pp across the board VAT

cut and the abolition of an extra excise duty on fuel. Going forward, buoyant domestic demand and rising wages

should exert some upward pressure on prices. We expect inflation to edge up to about 1.6% at end-2017 and to

average 2.5% in 2018. The NBR has kept its policy rate steady at 1.75% since May 2015. We expect this rate to

prevail until end-2017 or so before gradual monetary tightening is likely to start next year.

The RON/EUR exchange rate has been quite stable since 2013, fluctuating by a mere ±3.7% around an average

4.46. The Emerging Markets sell-off in mid- 2013 and early 2014 hardly affected the RON – similar to other

currencies in the CEE region. Nonetheless, renewed exchange rate volatility cannot be ruled out with regard to

ongoing vulnerabilities in the banking sector and what appears to be continued unsustainable fiscal stimulus.

5

Foreign exchange (FX) reserves have moved side-wards over the past seven years, in the range of EUR29-36bn.

The current level of reserves is comfortable with regard to import cover (about five months). However, reserves

cover only 90% of the estimated external debt payments due in the next 12 months. While this is an improvement

compared to 78% two years ago, the figure is still below an adequate level of at least 100%.

Romania has a geo-strategically important position, with an exit on the Black Sea which enables seagoing traffic

flows. Constantza Port has tremendously expanded over the past few years in terms of capacity expansion and

storage/handling facilities

The business climate is improving and the Romanian Government is making efforts to ensuring a fair environment

for businesses. The VAT rate for food was cut from 24 percent to 9 percent in June 2015. Starting January 2016,

the standard / general VAT was reduced from 24 percent to 20 percent. These VAT reductions increased

consumer purchasing power. Consumer demand was also boosted by rising real household disposable income

as a result of increases in wages, pensions and remittances from abroad and rapid growth of new consumer loans.

Retail sales grew by an average of 12.4 percent per month in volume terms in the second half of 2015, compared

with an average of 4.8 percent in the first half. In 2015 retail turnover grew by 8.9 percent, with sales of food,

alcohol and tobacco rising by 19.1 percent. Sales of non-food goods grew by 2.8 percent. Sales of marketed

services grew by 9.5 percent. Increases in public-sector wages in December 2015 and the VAT reduction from 24

percent to 20 percent in January 2016 has boosted consumer demand in 2016, and some of this will spill over to

imports.

Total agricultural imports in Romania reached a total level of U.S. $ 6.7 billion in 2015. The major food product

import categories are meats, grains, protein meals, dairy, edible fruits, and sugar. Total consumer oriented

agricultural products imports in Romania were U.S.$ 3 billion in 2015.

Exporters should take into consideration the fact that in most of the food sectors there are well- established brands,

and to successfully enter the market might require significant marketing funds directed to consumer

communication. It is essential to visit the market to conduct market research, especially for product testing, price

comparisons, gauging competitors, preferences, etc. The products should be localized: products adjusted to local

tastes, in line with consumers’ preferences, and with a competitive price.

Romania is viewed as a market where consumers are prone to try different products. Romanian food shopping

has changed dramatically over the past years. They are more informed, more prone to follow foreign trends, have

become more selective, searching for the best cost benefit products.

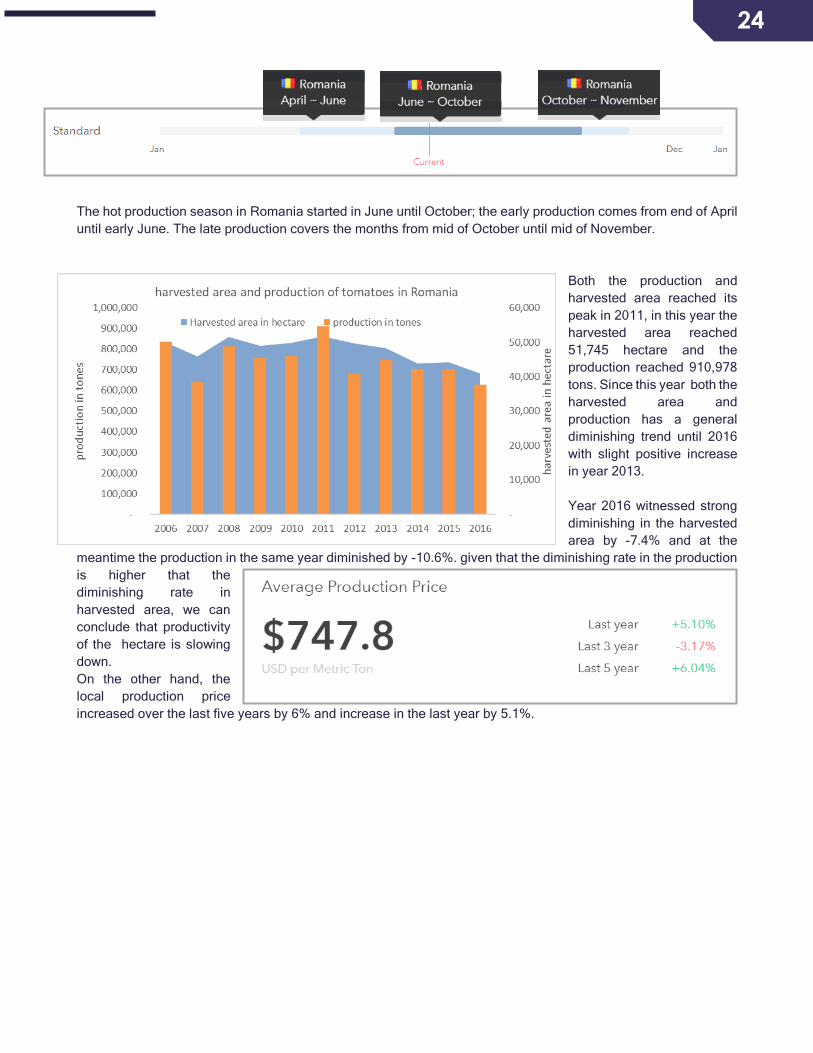

The area harvested for tomatoes in Romania reached 40,967 hectare in 2016 hectare with annual diminishing in

the area since 2011 with annual average diminishing by -4.6%. the production of tomatoes also is diminishing

yearly since 2011 by average annual diminishing by -7.2%. Year 2016 witnessed strong diminishing in the

harvested area by -7.4% and at the meantime the production in the same year diminished by -10.6%.

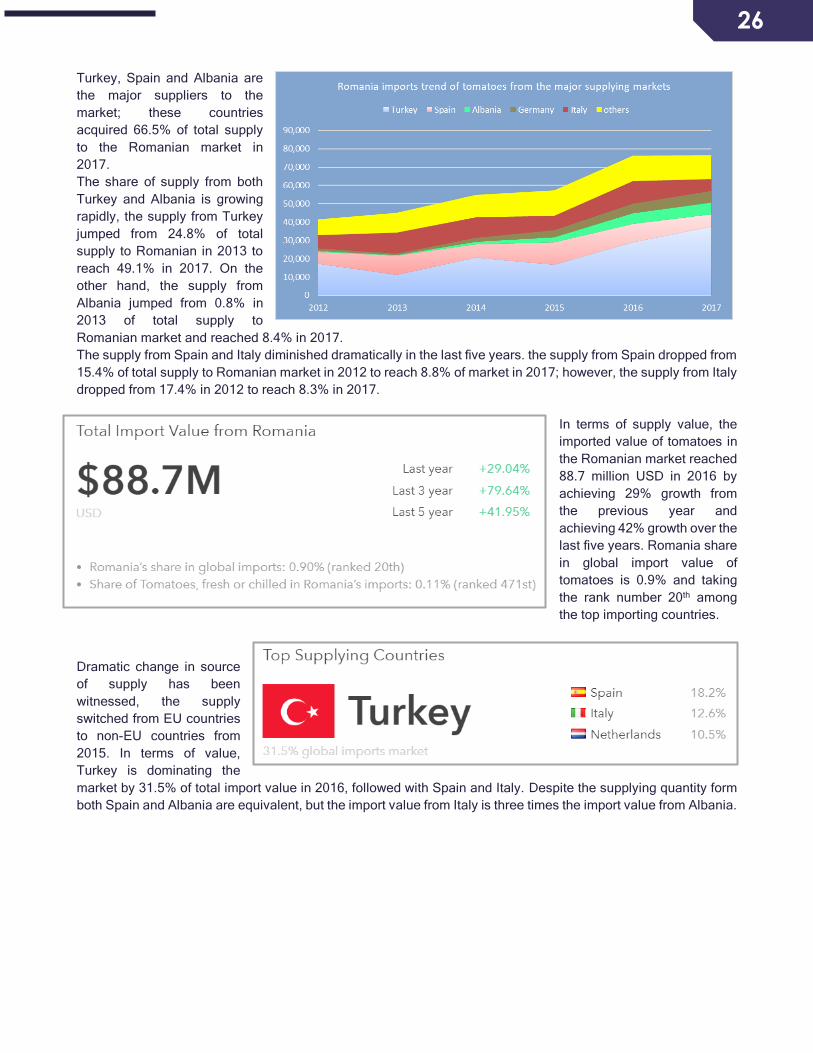

Romania imports of tomatoes witnessing annual increase since the year 2012 until 2017, the imported quantity

almost doubled in the last five years and jumped from 41,395 tons in 2012 to reach 76,507 tons in 2017 to achieve

compound average growth rate in the last five years by 13.1%. The majority of supply since 2013 until 2016 was

coming from EU countries. The share of EU in supply of tomatoes to Romanian market reached 72.6% in year

2013. The market witnessed annual diminishing in EU share in supply to reach 53.6% in 2016. Turkey, Spain and

Albania are the major suppliers to the market; these countries acquired 66.5% of total supply to the Romanian

market in 2017.

In terms of supply value, the imported value of tomatoes in the Romanian market reached 88.7 million USD in

2016 by achieving 29% growth from the previous year and achieving 42% growth over the last five years. Romania

share in global import value of tomatoes is 0.9% and taking the rank number 20th among the top importing

countries.

6

Egypt is not a known direct supplier of tomatoes to Romania. The market need to be discovered by the Egyptian

exporter of tomatoes who are able to be flexible in terms of supplying quantities and prices.

The average supplying price reached 991.0 USD/tons in 2018, the prices have decreased by -1.49% compared

to the price ranges in 2017. But the current price range still lower than the prices of 2015 and 2013 by -3.05% and

-1.38% respectively.

The revealed comparative advantage for export of tomatoes from Romania is too low. Romania does not have

any comparative advantage for exporting tomatoes.

Annual average consumption per capita in Romania has fluctuated from one year to the next (see the chart below).

The highest annual average of tomatoes consumption per capita was recorded in 2013 (40.0 kilograms per capita)

and the lowest was 35.26 kg/inhabitant. Regarding the monthly average of tomato consumption per person, at

national level and by residence area, it was found that it varied from one year to another.

The highest consumption is registered in the urban environment as opposed to rural areas. The amount of

tomatoes purchased by a household by residence area varied from one year to the next in the analyzed period. In

2016 there is a decrease (-5.4%) of the tomatoes quantity purchased at national level. The biggest quantity of

tomatoes purchased was recorded in 2013 (0.859 kg), and the lowest was 0.699 kg (2017).

In Romania there are more than 1,700 modern retail stores which are structured in hypermarkets, supermarkets, cash&carry, discounters. One third of the total modern retail stores are in Bucharest; the following major cities by considering the number of modern retail stores are Ilfov, Brasov, Cluj, Timisoara. Modern retail continues to gain market share year by year, while traditional retailer numbers gradually decline. In 2012 modern trade and traditional trade has equal shares and starting 2012 modern trade share continued to grow.

In 2015 Romania registered the highest consumption growth rate since 2008 (9 percent), thus Romania being one of the most dynamic countries and one of the most attractive food and beverages markets in Europe. The latest salary increases plus VAT food reduction to 9 percent put money into consumers’ pockets, so modern retailers have many growth opportunities. The retail market continues to expand rapidly both in Bucharest and throughout the country.

7

PEST ANALYSIS

Political Environment

The Political System in Romania

The President is the Head of State and is elected by universal suffrage for a term of five years. The President is

also the Commander in Chief of the army and is responsible for protecting the Constitution. Under the Romanian

Constitution, the President acts as a mediator between the various centres of power in the country. The Prime

Minister is appointed by the President (and is usually the leader of the majority party) for a term of four years. The

Prime Minister is the Head of Government and holds executive power, including law enforcement and

management of the affairs of the country. The Council of Ministers is appointed by the Prime Minister.

The legislature in Romania is bicameral. The Parliament consists of: Senate (the upper house) having 137 seats

and the Chamber of Deputies (the lower house) having 332 seats. The members of both houses are elected by

direct, popular vote on a proportional representation basis to serve four-year terms. The executive branch of the

Government is directly or indirectly dependent on the support of the parliament, often expressed through a vote

of confidence. The Prime Minister does not have the power to dissolve the Parliament directly, but the President

can do so after consultation with the political parties represented in the Parliamnet. The people of Romania have

considerable political rights.

Government Stability

The world bank score for the political stability boundaries are 2.50 & -2.50, the score for Romania reached 0.27

in 2016, Romania ranked number 80 out of 194 countries.

Romania’s Political Turbulence Threatens Economic Growth; in 2018, By the end of this year, Romania is set to

become the largest economy in the Balkans - but experts warn that if political instability continues, it will struggle

to maintain the current momentum. Growth in Romania is now threatened by political instability and the conflicting

economic policies of the government.

Employment laws

Romania rank 11th largest labor force in Europe among 41 countries with 8.83 million people in 2017 according

to the World Bank estimations. Romania ranked the 27th highest unemployment rate in Europe among 41

countries by 5.9% in 2017 according to World Bank estimations.

Romania ranked 14th among the highest unemployment rates of youth out of 41 countries by 23.6% in 2017.

There are 2 types of employment agreements in Romania, no matter if the individuals are residents or non-

residents:

1- Employment agreement for indefinite period

2- Employment agreement for definite period

As a rule, the employment contract has to be concluded for an unlimited duration. The unlimited duration is a

measure of protection for the Employee. By way of exception for project-based work, the individual employment

contract may also be concluded for a limited duration, under the terms expressly provided by the law, maximum

number of defined employment agreement is 3 successive ones, and the maximum period is 36 months.

Regardless if the employers in Romania contract Romanian or foreign individuals, they must fulfill certain

obligations.

8

Tax Regulations

The standard profit tax rate is 16% for Romanian companies and foreign companies operating through a

permanent establishment (PE) in Romania. Resident companies are taxed on their worldwide income, unless a

double tax treaty (DTT) stipulates otherwise. Non-resident companies are taxed on all income derived from

Romanian taxpayers, regardless of whether the services are rendered in Romania or abroad. The profit tax due

for nightclubs and gambling operations is either 5% of the revenue obtained from such activities or 16% of the

taxable profit, whichever is higher.

Among the tax law changes affecting individual taxpayers is an income tax rate reduction to 10% but increased

social security contributions for employees (effectively because the social security contributions are transferred

from employers to employees).

Romania's tax legislation is particularly volatile, with tax increases and amendments to legislation often being

introduced at very short notice. In the current economic climate, the authorities are also especially vigilant about

protecting budget revenue.

Corruption Levels

Romania rank 13th among the highest corruption levels in Europe out of 41 countries according to the World

bank estimations in 2016, Romania score is 0.0, this indicators score boundaries are 2.50 & -2.50

Corruption is a serious problem in Romania and raises the risks of doing business in the country. Foreign investors

complain of complicated procedures, arbitrary application of rules and requests for bribes when resolving

administrative tasks related to business operations. The Romanian Criminal Code and other supporting laws

criminalize active and passive bribery, including bribery of foreign officials. A company can be held criminally

liable for corruption offenses committed by individuals acting on its behalf. The government, however, does not

enforce anti-corruption laws effectively and impunity is widespread. Early 2017 saw large numbers of protesters

take to the streets of Bucharest to protest a decree that would have shielded many officials from corruption

charges. The decree was ultimately rescinded. Petty corruption is a problem in Romania as irregular payments

and bribes are common practice. The law does not distinguish between bribes and facilitation payments, and gifts

and hospitality may be considered illegal depending on their intent and the benefit obtained.

Trade Regulations& Customs

Romania rank 28th among the highest trade openness markets out of 41 countries in EUrope according to the

World bank estimations in 2016, Romania score is 82.9, this indicator score boundaries are 405 & 49.

The Union Customs Code (UCC) was adopted in 2013 and its substantive provisions apply from May 1, 2016. It

replaces the Community Customs Code (CCC). In addition to the UCC, the EC has published delegated and

implementing regulations on the actual procedural changes.

Consecutively, starting in April 2016, Romanian Customs implemented a working schedule to develop and install

the electronic systems envisioned by the EU Customs Code. Presently, Romanian Customs has drafted 25

legislative orders to be signed by the President of National Agency for Fiscal Administration and published in the

local Official Journal in the near future. The new orders will impact procedures referring to: companies’ registration,

customs representation, origin of goods, taxation, special regimes and free-zones, temporary warehouses, re-

export notification and electronic signatures.

Most customs duties and value added tax (VAT) are expressed as a percentage of the value of goods being

declared for importation. Thus, it is necessary to dispose of a standard set of rules for establishing the goods'

value, which will then serve for calculating the customs duty.

9

Economic Environment

GDP and Inflation

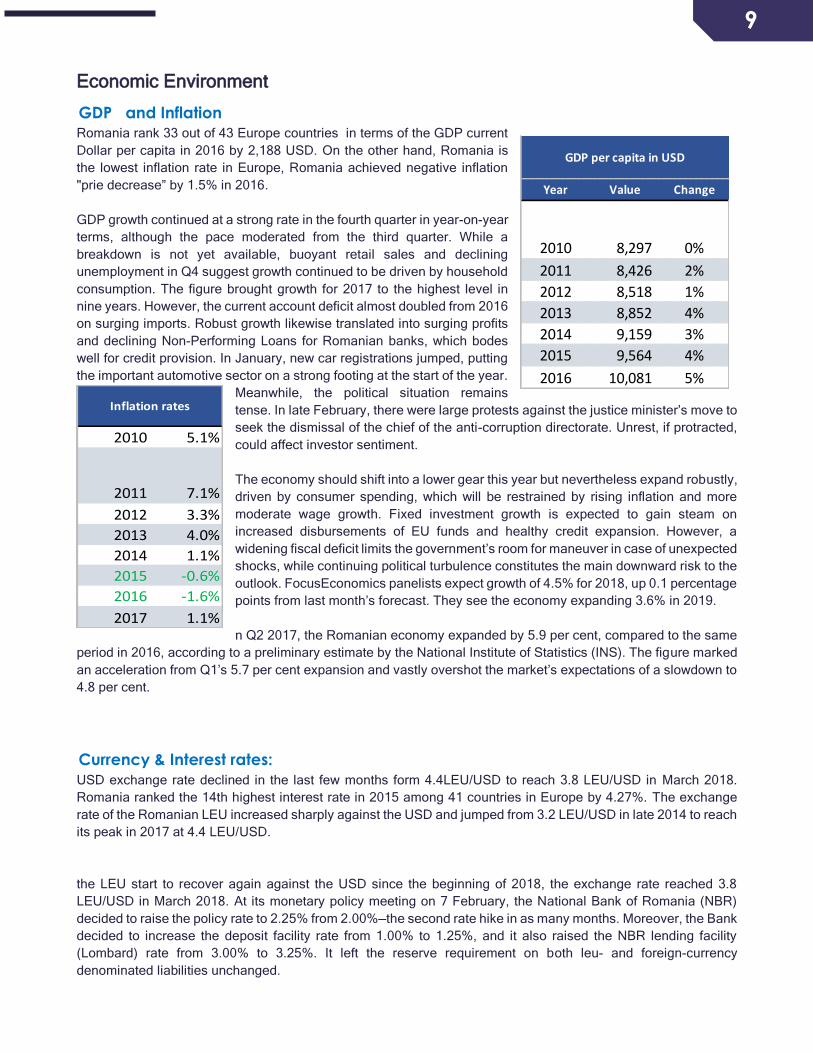

Romania rank 33 out of 43 Europe countries in terms of the GDP current

Dollar per capita in 2016 by 2,188 USD. On the other hand, Romania is

the lowest inflation rate in Europe, Romania achieved negative inflation

"prie decrease” by 1.5% in 2016.

GDP growth continued at a strong rate in the fourth quarter in year-on-year

terms, although the pace moderated from the third quarter. While a

breakdown is not yet available, buoyant retail sales and declining

unemployment in Q4 suggest growth continued to be driven by household

consumption. The figure brought growth for 2017 to the highest level in

nine years. However, the current account deficit almost doubled from 2016

on surging imports. Robust growth likewise translated into surging profits

and declining Non-Performing Loans for Romanian banks, which bodes

well for credit provision. In January, new car registrations jumped, putting

the important automotive sector on a strong footing at the start of the year.

Meanwhile, the political situation remains

tense. In late February, there were large protests against the justice minister’s move to

seek the dismissal of the chief of the anti-corruption directorate. Unrest, if protracted,

could affect investor sentiment.

The economy should shift into a lower gear this year but nevertheless expand robustly,

driven by consumer spending, which will be restrained by rising inflation and more

moderate wage growth. Fixed investment growth is expected to gain steam on

increased disbursements of EU funds and healthy credit expansion. However, a

widening fiscal deficit limits the government’s room for maneuver in case of unexpected

shocks, while continuing political turbulence constitutes the main downward risk to the

outlook. FocusEconomics panelists expect growth of 4.5% for 2018, up 0.1 percentage

points from last month’s forecast. They see the economy expanding 3.6% in 2019.

n Q2 2017, the Romanian economy expanded by 5.9 per cent, compared to the same

period in 2016, according to a preliminary estimate by the National Institute of Statistics (INS). The figure marked

an acceleration from Q1’s 5.7 per cent expansion and vastly overshot the market’s expectations of a slowdown to

4.8 per cent.

Currency & Interest rates:

USD exchange rate declined in the last few months form 4.4LEU/USD to reach 3.8 LEU/USD in March 2018.

Romania ranked the 14th highest interest rate in 2015 among 41 countries in Europe by 4.27%. The exchange

rate of the Romanian LEU increased sharply against the USD and jumped from 3.2 LEU/USD in late 2014 to reach

its peak in 2017 at 4.4 LEU/USD.

the LEU start to recover again against the USD since the beginning of 2018, the exchange rate reached 3.8

LEU/USD in March 2018. At its monetary policy meeting on 7 February, the National Bank of Romania (NBR)

decided to raise the policy rate to 2.25% from 2.00%—the second rate hike in as many months. Moreover, the Bank

decided to increase the deposit facility rate from 1.00% to 1.25%, and it also raised the NBR lending facility

(Lombard) rate from 3.00% to 3.25%. It left the reserve requirement on both leu- and foreign-currency

denominated liabilities unchanged.

Year Value Change

2010 8,297 0%

2011 8,426 2%

2012 8,518 1%

2013 8,852 4%

2014 9,159 3%

2015 9,564 4%

2016 10,081 5%

GDP per capita in USD

2010 5.1%

2011 7.1%

2012 3.3%

2013 4.0%

2014 1.1%

2015 -0.6%

2016 -1.6%

2017 1.1%

Inflation rates

10

Building inflationary pressures, together with booming economic activity, underpinned the Bank’s decision.

Inflation in December stepped up to a multi-year high of 3.3% from 3.2% in November, moving closer to the upper

limit of the Bank’s target range of 1.5%–3.5%. Faster core inflation was behind the acceleration in headline inflation,

which was also fueled by an increase in food and tobacco prices. Core inflation was again influenced by strong

economic momentum, rising wages and supply-side factors.

Credit accessibility:

Romania score of credit accessibility by private sector is 28.1 in 2016 that rank the country the lowest third country

in Europe in terms of credit accessibility . The best score was 227.2 for Cyprus and the lowest was 21.8 for

Belarus.

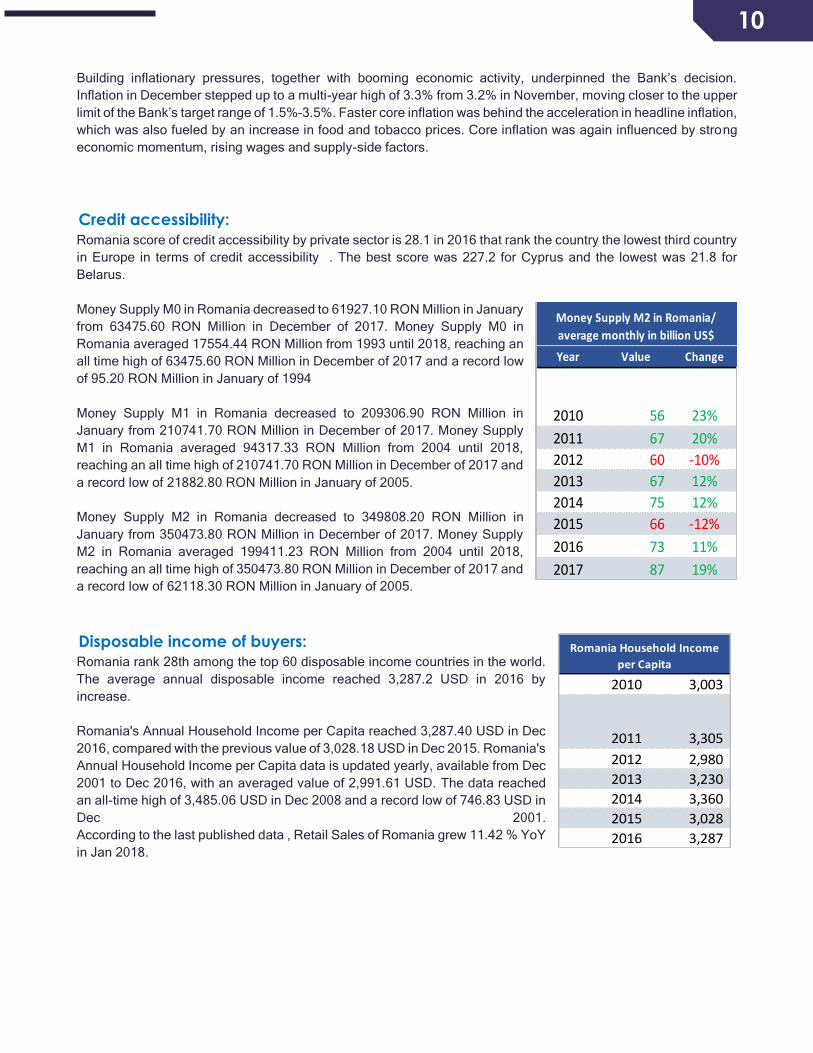

Money Supply M0 in Romania decreased to 61927.10 RON Million in January

from 63475.60 RON Million in December of 2017. Money Supply M0 in

Romania averaged 17554.44 RON Million from 1993 until 2018, reaching an

all time high of 63475.60 RON Million in December of 2017 and a record low

of 95.20 RON Million in January of 1994

Money Supply M1 in Romania decreased to 209306.90 RON Million in

January from 210741.70 RON Million in December of 2017. Money Supply

M1 in Romania averaged 94317.33 RON Million from 2004 until 2018,

reaching an all time high of 210741.70 RON Million in December of 2017 and

a record low of 21882.80 RON Million in January of 2005.

Money Supply M2 in Romania decreased to 349808.20 RON Million in

January from 350473.80 RON Million in December of 2017. Money Supply

M2 in Romania averaged 199411.23 RON Million from 2004 until 2018,

reaching an all time high of 350473.80 RON Million in December of 2017 and

a record low of 62118.30 RON Million in January of 2005.

Disposable income of buyers:

Romania rank 28th among the top 60 disposable income countries in the world.

The average annual disposable income reached 3,287.2 USD in 2016 by

increase.

Romania's Annual Household Income per Capita reached 3,287.40 USD in Dec

2016, compared with the previous value of 3,028.18 USD in Dec 2015. Romania's

Annual Household Income per Capita data is updated yearly, available from Dec

2001 to Dec 2016, with an averaged value of 2,991.61 USD. The data reached

an all-time high of 3,485.06 USD in Dec 2008 and a record low of 746.83 USD in

Dec 2001.

According to the last published data , Retail Sales of Romania grew 11.42 % YoY

in Jan 2018.

Year Value Change

2010 56 23%

2011 67 20%

2012 60 -10%

2013 67 12%

2014 75 12%

2015 66 -12%

2016 73 11%

2017 87 19%

Money Supply M2 in Romania/

average monthly in billion US$

2010 3,003

2011 3,305

2012 2,980

2013 3,230

2014 3,360

2015 3,028

2016 3,287

Romania Household Income

per Capita

11

Tax& Duties

Companies are directly responsible for determining and charging the correct Romanian VAT rates. These are set

by the government, although the EU set the broad rules for use of the standard, higher rate and reduced rates. The

EU does insist that the standard rate is at least 15%.

Applied VAT in Romania

Rate Type Which goods or services

19% Standard All other taxable goods and services. Standard VAT rate decreased from 20% to 19% on 1 Jan 2017

9% Reduced

Foodstuffs; pharmaceutical products; medical equipment for disabled persons; hotel accommodation; water supplies; restaurants and catering services (includes supply of food in bars, cafes and nightclubs); some beer; soft drinks; cut flowers and plants for food production; some agricultural supplies.

5% Reduced Social housing; books (excluding e-books); newspapers and periodicals; admission to cultural events; admission to sporting events.

0% Zero Intra-community and international passenger transport.

12

Social Environment

Demographics

Romania is the 10th largest population inEurope by 19.7 million

resident in 2016 according to the estimations of worls bank.

In 2030, the population of Romania will reach 18.3 million, a decrease

of 7.8% from 2015. This ongoing depopulation, which has been taking

place since the fall of communism, is due to continued negative net

migration, increasing death rates and falling birth rates. The

population will continue to age rapidly in 2015-2030 due to large

declines in all population groups under 49 years and by 2030

Romania will be the 21st oldest country in the world by median age.

Romania is a small country that is constituted of 84.1% Ethnic

Romanians from its total population while a small Hungarian minority

makes up 5.4% of the population demographics.

As of early 2014, the population of Romania was around 21,595,302,

a slight decrease from the estimated 21,668,721 in 2013 and from the

2011 population estimates when the figure stood at 21,801,942.

Romania's population is

actually decreasing at a rate of

0.32% per year. According to historical figures, Romania actually hit its

population peak in the early 90s, when there were 23,372,101 people in

Romania. In 2018 the population is estimated at 19.58 million.

The age structure of Romania is skewed heavily towards its inhabitants in

the 25-54 year age group. They make up around 45.1% of the population.

The younger generation in the 0-25 year age bracket also has a significant

majority in the country with 27.1%. These are encouraging numbers, which

show that Romania has a thriving work force and an upcoming generation

available for its development, provided it can create suitable opportunities

for its inhabitants to help develop it further in the long run. Moreover, the

population of senior citizens in Romania (people 55 years and over) also

make up a significant portion of the country's population at 27.8%. This

population spread also shows that Romania has a very uniform distribution of its population in all age brackets

except the 25-54 year olds.

Year Population Growth

2010 20,440,000 -0.86%

2011 20,293,000 -0.72%

2012 20,171,000 -0.60%

2013 20,068,000 -0.51%

2014 19,973,000 -0.48%

2015 19,876,000 -0.48%

2016 19,778,000 -0.50%

2017 19,679,000 -0.50%

Romania Population

13

Cross-cultural communication

Cross –Cultural communication

Note

Greetings

- Man greeting Man – If it is a new acquaintance, men will most likely shake hands. If it is a friend, many will grasp hands and then hug. Some good friends and family may also kiss on both cheeks.

- Woman greeting Woman- If it is a new acquaintance, they can shake hands, if one of them initiates by extending her hand. If it is a friend, they will kiss on both cheeks, and if a good friend, they may also hug.

- Greetings between Men & Women- If it is a new acquaintance, and the woman is older, very often men will kiss her hand as a sign of respect. They can shake hands, but the woman must initiate by extending her hand first. If it is a friend, they will kiss on both cheeks, and if a good friend, they will also hug.

Note: Usually, young people say "buna ziua" to older men which means "good day" and to women "sarut mana" that means “I kiss your hand" but people say it in a hurry, so it sounds like "sarumana" . People do not say “sarut mana" to men, only to priests. The youth greet with "salut", “servus" or even “hello" or "hallo".

Communication Style

- Romanians tend to be very polite and hospitable, so they will always take time to ask about one’s family and make other small talk before getting to the business at hand.

- They are generally direct about what they feel, but can be very indirect when talking about ideas and plans. There are many cultural reasons for this. To really understand, it is a good idea to ask questions and tactfully ask for more information, at least up to a point.

- Some people are direct and say exactly what they mean, and others take a more indirect path.

- If you are asking for directions most people will be happy to help you. But this depends from city to city, for example in Bucharest , people may not be as open to helping out.

Eye Contact

- Direct eye contact is preferred. Some people could say that you are not listening if you are not making an eye contact, and get upset.

- In a professional setting amongst colleagues, direct eye contact is acceptable and in most cases, expected.

Personal Space & Touching

- An arms length of personal space is the norm during conversations. This space may decrease when speaking with friends and family.

- Touching of the arms and shoulders is common during conversations. Touching and hugging is more common with friends as well as family.

Views Of Time

- raditional Romanian hospitality requires that much time is devoted to friendly conversation and taking time to visit, rather than adhering to set schedules or agendas.

- In more modern business settings, people are beginning to be prompt and pay attention to the time.

- There is no point in getting upset if people are a little late, or very late, and “immediate” can sometimes mean a long wait.

- Trains frequently run late. The rails are gradually being upgraded, but often they do not allow for speedy transit.

14

- Depending on the city, buses may have schedules, but in most towns the bus runs are more sporadic and people learn to be patient.

- Most people are not in too much of a hurry except when they are driving. - You might hear the word "immediate" that means "I'm coming right away" but you

may want to ask where the person is, to be sure they are really on their way. Usually they say "immediate" when they are still at home.

- There are also some institutions where punctuality is expected, for example schools, not all of them but most.

- Romanians, although late almost all the time, tend not to be patient and usually don`t like to wait.

Gestures

- One is expected to give up one's seat in public transport for the elderly or very young.

- In some homes shoes are removed indoors and people put on slippers, or “papoosh”, and visitors will be strongly encouraged to wear them as well.

- If you point to something, you point with one finger but if you want to be more subtle, you can just stretch your head, or move your eyes in the direction you want to point.

- When you beckon someone you move you whole hand toward yourself. in a downward motion.

- When you wave goodbye, you move your hand from left to right, or, you close your hand and open it, so that the outside part of the hand is toward you.

- Holding the door for the person following you, or even helping a person with overweight baggage is a sign of politeness, but it is not expected.

- In traffic, when you give someone right of way, it is polite to say thank you by nodding the head, or showing one hand.

- At school, when you want to answer, you raise your hand, and hold two fingers, just like the “ peace “ sign.

- For approving something, or saying "ok", you just raise your thumb. - If you`re going to a store, always say hello and bye to the vendor, and thanks after

you buy something.

Business Dress

- For Men: Dark suit, white shirt, and a tie with polished shoes.

- For Women: Elegant style is common. Business suits, usually with a skirt and

preferably with high heels.

TITLES & BUSINESS CARDS

- Mr. and Mrs.are common title. Mr. means “domn" and Mrs. means “doamna". Some people combine title them like Mr. Doctor (domnul doctor ) or Mrs. Lawyer.

- Business cards are usually presented with one hand and holding it between two fingers, like a cigarette.

Meetings

- Meetings are generally taken seriously and it’s best to be on time. - It is common to greet the highest ranking person first. - Some small talk is usually expected. It's best to allow the host to dictate the

business discussion. - The main purposes of initial meetings are to get to know one another and discuss,

not to always make decisions. It's best to go with the flow and not impose your agenda too forcefully.

Negotiations

- Romanians tend to take time when negotiating and expect some give and take in the bargaining sessions. It's best not not rush them or appear impatient. Expect a great deal of time to be spent reviewing details before a final decision is made.

- Decisions are generally made from the top down and once a decision is made and terms are agreed upon, making any further changes can prove difficult.

Gift Giving - Gifts are not generally exchanged at initial business meetings.

15

Consumer behavior

According to the PMR study on the food retail market of

Central Europe (Bulgaria, Czech Republic, Hungary,

Poland, Romania and Slovakia)-EC, food sales in 2011

have achieved a level of 107 billion euro, in a 2.8%

increase from previous year. The increase was due

mainly to the increase of sales in supermarkets and

discount stores, and to food price rise. The most

important economic operator in grocery retail is the

Schwarz Group, owner of Lidl and Kaufland stores.

Retail food market in the EC has lost 5.5 billion euro

during 2007-2010, due to the economic crisis and to the

decline of national currencies. The forecast for 2014 is

optimistic; the food retail market is estimated at 17 billion

euro. . According to the estimates, all forms of traditional

trade will be affected by the growth of online commerce,

evaluated in 2014 to 0.6% at European level. In the year 2013 Romania has exceeded the European average in

electronic commerce, registering an increase of 4.3%. In June 2014, the European retail has made an increase of

2.5%.

According to Dabija and Alt (2012), the emergence and

development of the modern commercial sector in

Romania is marked by the establishment of the network of

supermarket stores La Fourmi (1991), followed by the

opening of Mega Image stores in 1994. In 1996 the

network of Metro Cash & Carry stores began to operate

through the unit in Otopeni. A forecast of the year 2014 for

the retail market in Romania provides a value of 26 billion

euro; the national sector performance is being the best in

Europe. The study conducted by Gfk, the largest market

research company at the local level, states that in 2014 a

slight decrease in the pace of economic growth in the area

of trade will take place.

- If invited over for dinner or a drink to a Romanian home, you should always bring a gift. Either a bottle of high quality imported wine, liquor, flowers or a dessert/candy is acceptable.

- Always give flowers in odd numbers as even ones are usually given at funerals. - Gifts tend to be opened when received.

19.40% 20.80% 21.10%

16.30% 18.20% 20.10%9%

12.60%16.50%

55.40% 48.30% 41.90%

2 0 0 8 2 0 1 1 2 0 1 5

C H A N G E I N T H E S H O P P I N G P A T T E R N O F R O M A N I A N C O N S U M E R S

Hypermarkets Supermarkets

discount stores open markets & others

Fruits 2013 KG 2014 KG Growth

Fruit and fruit products in fresh

fruit

equivalent 73.2 80.2 9.6%

Apples 23.5 25.1 6.8%

Plums 4.5 4.7 4.4%

Apricots 1.6 2.2 37.5%

Cherries - sour cherries 4 4 0.0%

Peaches – nectarines 3.1 4.1 32.3%

Grapes 6.7 6.2 -7.5%

Southern and exotic fruits 23.1 25.7 11.3%

Other fruits 7.2 8.1 12.5%

Melons 25.4 21.8 -14.2%

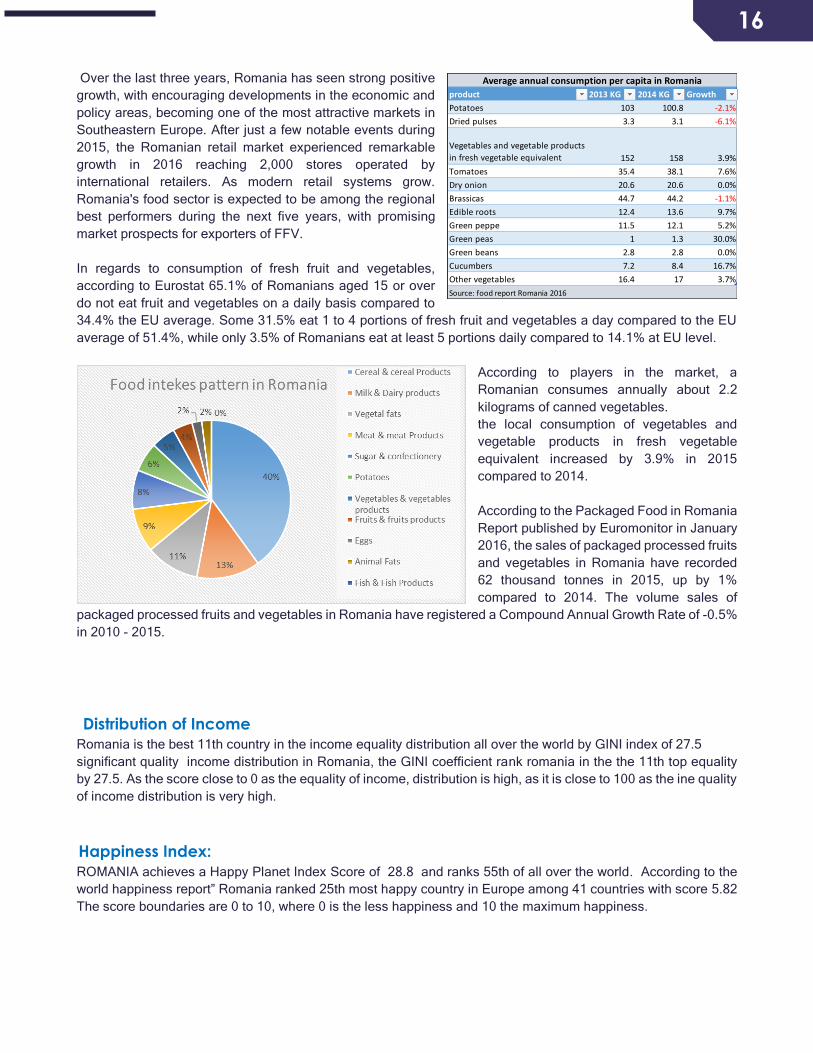

Average annual consumption per capita in Romania

Source: food report Romania 2016

16

Over the last three years, Romania has seen strong positive

growth, with encouraging developments in the economic and

policy areas, becoming one of the most attractive markets in

Southeastern Europe. After just a few notable events during

2015, the Romanian retail market experienced remarkable

growth in 2016 reaching 2,000 stores operated by

international retailers. As modern retail systems grow.

Romania's food sector is expected to be among the regional

best performers during the next five years, with promising

market prospects for exporters of FFV.

In regards to consumption of fresh fruit and vegetables,

according to Eurostat 65.1% of Romanians aged 15 or over

do not eat fruit and vegetables on a daily basis compared to

34.4% the EU average. Some 31.5% eat 1 to 4 portions of fresh fruit and vegetables a day compared to the EU

average of 51.4%, while only 3.5% of Romanians eat at least 5 portions daily compared to 14.1% at EU level.

According to players in the market, a

Romanian consumes annually about 2.2

kilograms of canned vegetables.

the local consumption of vegetables and

vegetable products in fresh vegetable

equivalent increased by 3.9% in 2015

compared to 2014.

According to the Packaged Food in Romania

Report published by Euromonitor in January

2016, the sales of packaged processed fruits

and vegetables in Romania have recorded

62 thousand tonnes in 2015, up by 1%

compared to 2014. The volume sales of

packaged processed fruits and vegetables in Romania have registered a Compound Annual Growth Rate of -0.5%

in 2010 - 2015.

Distribution of Income

Romania is the best 11th country in the income equality distribution all over the world by GINI index of 27.5

significant quality income distribution in Romania, the GINI coefficient rank romania in the the 11th top equality

by 27.5. As the score close to 0 as the equality of income, distribution is high, as it is close to 100 as the ine quality

of income distribution is very high.

Happiness Index:

ROMANIA achieves a Happy Planet Index Score of 28.8 and ranks 55th of all over the world. According to the

world happiness report” Romania ranked 25th most happy country in Europe among 41 countries with score 5.82

The score boundaries are 0 to 10, where 0 is the less happiness and 10 the maximum happiness.

product 2013 KG 2014 KG Growth

Potatoes 103 100.8 -2.1%

Dried pulses 3.3 3.1 -6.1%

Vegetables and vegetable products

in fresh vegetable equivalent 152 158 3.9%

Tomatoes 35.4 38.1 7.6%

Dry onion 20.6 20.6 0.0%

Brassicas 44.7 44.2 -1.1%

Edible roots 12.4 13.6 9.7%

Green peppe 11.5 12.1 5.2%

Green peas 1 1.3 30.0%

Green beans 2.8 2.8 0.0%

Cucumbers 7.2 8.4 16.7%

Other vegetables 16.4 17 3.7%

Average annual consumption per capita in Romania

Source: food report Romania 2016

17

Human Development:

Human development indicator calculated by the United nations, it is described by value between 0 and 1 where 0

is the less human development countries. Romania ranked the 1oth worst country in Europe for human

development with score 0.802 that lower than the europe average (0.853).

The Human Development Index measures three basic dimensions of human development: long and healthy life,

knowledge, and a decent standard of living. Four indicators are used to calculate the index: life expectancy at

birth, mean years of schooling, expected years of schooling, and gross national income per capita. The world

average for 2015 was 0.701 points. The highest value was in Norway: 0.949 points and the lowest value was in

the C.A. Republic: 0.352 points.

Age dependency ratio:

Romania is the 25th highest age dependency in Europe by 49.54% of the work force in the country. Age

dependency ratio is the ratio of dependents--people younger than 15 or older than 64--to the working-age

population--those ages 15-64. The average in EUrope for 2016 was 50.31%t. The highest value was in France:

61% percent and the lowest value was in Moldova by: 35%.

The dependency ration of Romania less partially then the average in Europe ; it is a good advantage for the country

and give good space for more expendature of quality products.

18

Technology Environment

Port traffic & infrastructure

Romania rank 19th highest port traffic in Europe in 2014 according to “Containerization International”. Romania

is the 7th worst port infrastructure in Europe with score 3.42 out of 7 in 2015.

Romania has average port traffic in Europe in comparison with the other European countries. Romania rank is

19th by 775,742 container in 2014, it comes after Ukraine and Ireland. And comes before Slovenia and Austria.

Romania is keeping the same rank since 2010.

The infrastructure of the ports in Romania ranked the country among the worst 2 ports infrastructure in Europe.

This definitely affecting the cost of the service, the safety and the time required to process the consignment.

Railway transport of goods:

Romania is the 11th top railway transport of goods in Europe by 10,598 metric tons times the kilometers traveled.

Railway network for moving goods in Romania is quite good for moving goods across the country and to the other

boarder countries.

Road transportation

Romania has the 7th biggest railroad lines in Europe by 10,799km. Romania ranked the 5th worst road

transportation in Europe with score 2.56 out of 7. Despite Romania has large railroad network as the country

considered the the 7th largest road network in Europe, but it is one of the worst roads in Europe.

19

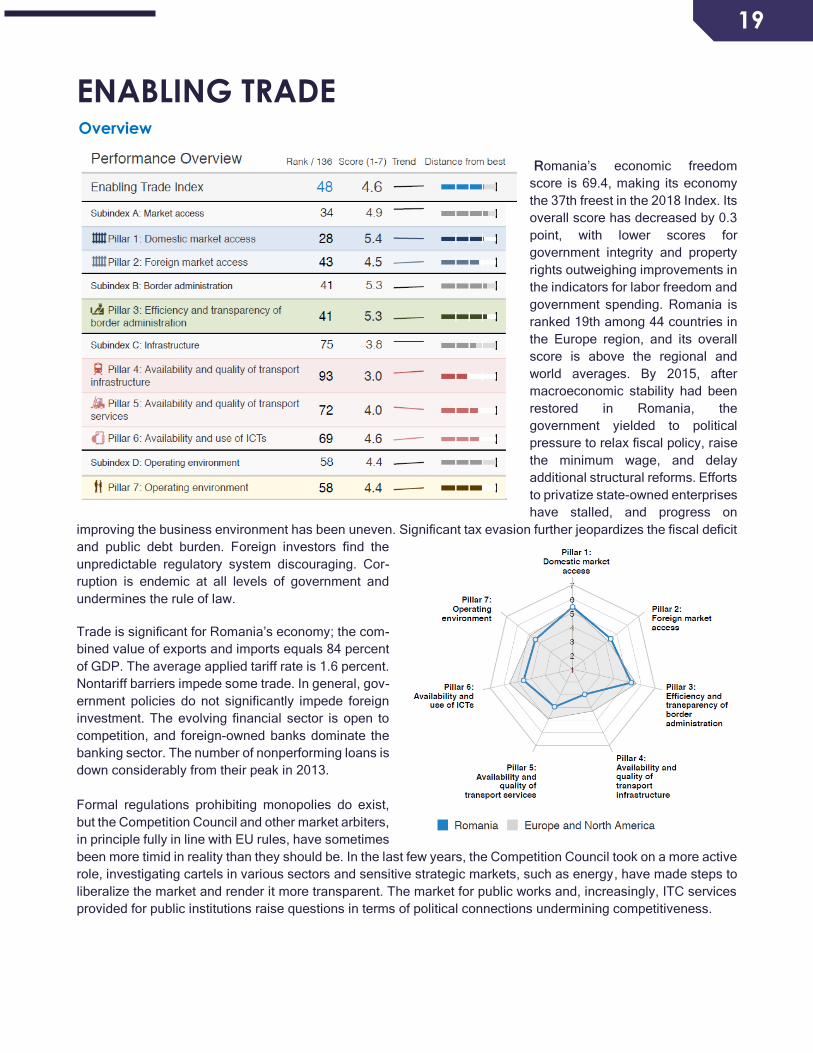

ENABLING TRADE Overview

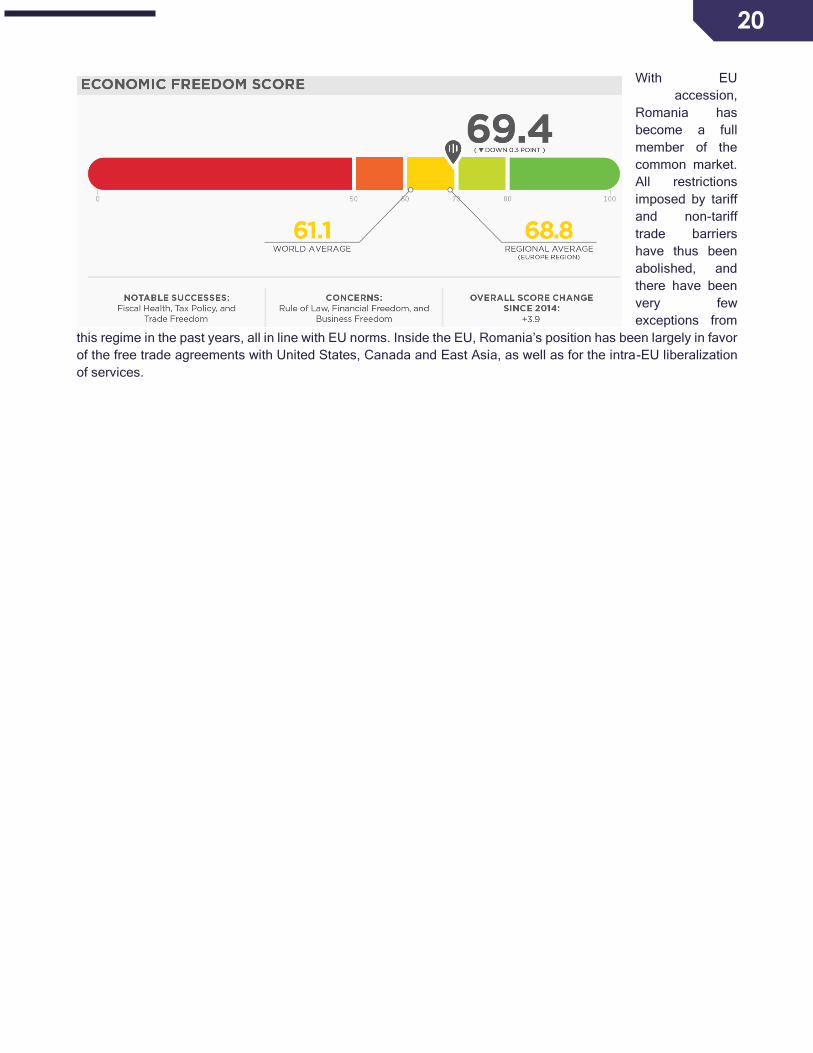

Romania’s economic freedom

score is 69.4, making its economy

the 37th freest in the 2018 Index. Its

overall score has decreased by 0.3

point, with lower scores for

government integrity and property

rights outweighing improvements in

the indicators for labor freedom and

government spending. Romania is

ranked 19th among 44 countries in

the Europe region, and its overall

score is above the regional and

world averages. By 2015, after

macroeconomic stability had been

restored in Romania, the

government yielded to political

pressure to relax fiscal policy, raise

the minimum wage, and delay

additional structural reforms. Efforts

to privatize state-owned enterprises

have stalled, and progress on

improving the business environment has been uneven. Significant tax evasion further jeopardizes the fiscal deficit

and public debt burden. Foreign investors find the

unpredictable regulatory system discouraging. Cor-

ruption is endemic at all levels of government and

undermines the rule of law.

Trade is significant for Romania’s economy; the com-

bined value of exports and imports equals 84 percent

of GDP. The average applied tariff rate is 1.6 percent.

Nontariff barriers impede some trade. In general, gov-

ernment policies do not significantly impede foreign

investment. The evolving financial sector is open to

competition, and foreign-owned banks dominate the

banking sector. The number of nonperforming loans is

down considerably from their peak in 2013.

Formal regulations prohibiting monopolies do exist,

but the Competition Council and other market arbiters,

in principle fully in line with EU rules, have sometimes

been more timid in reality than they should be. In the last few years, the Competition Council took on a more active

role, investigating cartels in various sectors and sensitive strategic markets, such as energy, have made steps to

liberalize the market and render it more transparent. The market for public works and, increasingly, ITC services

provided for public institutions raise questions in terms of political connections undermining competitiveness.

20

With EU

accession,

Romania has

become a full

member of the

common market.

All restrictions

imposed by tariff

and non-tariff

trade barriers

have thus been

abolished, and

there have been

very few

exceptions from

this regime in the past years, all in line with EU norms. Inside the EU, Romania’s position has been largely in favor

of the free trade agreements with United States, Canada and East Asia, as well as for the intra-EU liberalization

of services.

21

Most problematic factors for exporting to Romania

High cost or delays caused by domestic transportation, Burdensome import procedures and Tariffs and non-tariff

barriers are the most problematic factors for exporting to Romania according to “Executive Opinion Survey” of the

world economic forum.

Most problematic factors for exporting from Romania

Exporting from Romania is facing many challenges, the major challenges the exporters facing are Identifying

potential markets and buyers, Access to trade finance and High cost or delays caused by domestic transportation.

High cost or delays caused by domestic transportation

Burdensome import procedures

Tariffs and non-tariff barriers

High cost or delays caused by international transportation

Domestic technical requirements and standards

Inappropriate telecommunications infrastructure

Crime and theft

Corruption at the border0 5 10 15 20 25

21.1

19.5

17.9

13.1

13

6.7

4.9

3.8

Identifying potential markets and buyers

Access to trade finance

High cost or delays caused by domestic transportation

Access to imported inputs at competitive prices

Inappropriate production technology and skills

Technical requirements and standards abroad

Difficulties in meeting quality/quantity requirements of buyers

Burdensome procedures at foreign borders

High cost or delays caused by international transportation

Rules of origin requirements abroad

Tariff barriers abroad

Corruption at foreign borders0 4 8 12 16 20

11.7

18.5

13.4

12.6

1.1

0.9

11.5

8.6

8

5.2

4.9

3.7

22

PRODUCT BRIEF

Product Definition

Scientific name: Solanum lycopersicum

HS codes: 070200

tomatoes, fresh or chilled

Varieties

- Big Beef Tomato (Solanum lycopersicum 'Big Beef')

- Waltham Tomato (Solanum lycopersicum 'Waltham')

- Red seedless Tomato (Solanum lycopersicum 'Red seedless')

- Red Globe Tomato (Solanum lycopersicum 'Red globe')

- Larochelle Tomato (Solanum lycopersicum 'Larochelle')

- ErliHanne Tomato (Solanum lycopersicum 'ErliHanne')

- Dalphine Tomato (Solanum lycopersicum 'Dalphine')

- Dan Ben Hanna (Solanum lycopersicum 'Dan Ben Hanna')

- Blen-Ben-Hann (Solanum lycopersicum 'Blen-Ben-Hann')

- Bonheur Tomato (Solanum lycopersicum 'Bonheur')

- Barlinka Tomato (Solanum lycopersicum 'Barlinka')

- Alphonso La Valee (Solanum lycopersicum 'Alphonso La Valee')

- Salad Tomato (Lycopersicon lycopersicum 'Salad')

- Slicing Tomato (Lycopersicon lycopersicum 'Slicing')

- Cherry Tomato (Lycopersicon lycopersicum 'Cherry')

- Romania Tomato (Lycopersicon lycopersicum 'Romania')

- Rosa Tomato (Lycopersicon lycopersicum 'Rosa')

- Premio Tomato (Solanum lycopersicum 'Premio')

- Cherokee purple Tomato (Solanum lycopersicum 'Cherokee purple')

- Brandywine Tomato (Solanum lycopersicum 'Brandywine')

23

Romania is a key player in the fresh tomatoes market either on the production side or on imports side, Romania

ranked top 32 producers of tomatoes with share of 0.35% of global production and ranked top 20th importer in the

world with value imported share 0.90 of global trade in Tomatoes.

Local Production

The area harvested for tomatoes in Romania reached 40,967 hectare in 2016 hectare with annual diminishing in

the area since 2011 with annual average diminishing by -4.6%. the production of tomatoes also is diminishing

yearly since 2011 by average annual diminishing by -7.2%.

Sharp diminishing in the harvested area by tomatoes in

Romania by -21% in the previous five years. the harvested area

diminished from 49,620 Hectare in 2012 to 40,967 hectare in

2016.

The production of tomatoes in Romania facing sharp

diminishing over the last five years by -7.2% on average

annually. In year 2016 the production diminished from 701,800

tons to 627,177 tons only. The production diminished by

-10.6%

Production Volume 627,177 Metric Ton in 2016

Last year -10.60%

Last 3 years -16.30%

Last 5 years -31.15%

24

The hot production season in Romania started in June until October; the early production comes from end of April

until early June. The late production covers the months from mid of October until mid of November.

Both the production and

harvested area reached its

peak in 2011, in this year the

harvested area reached

51,745 hectare and the

production reached 910,978

tons. Since this year both the

harvested area and

production has a general

diminishing trend until 2016

with slight positive increase

in year 2013.

Year 2016 witnessed strong

diminishing in the harvested

area by -7.4% and at the

meantime the production in the same year diminished by -10.6%. given that the diminishing rate in the production

is higher that the

diminishing rate in

harvested area, we can

conclude that productivity

of the hectare is slowing

down.

On the other hand, the

local production price

increased over the last five years by 6% and increase in the last year by 5.1%.

25

Romania Imports of Tomatoes

Romania imports of

tomatoes witnessing

annual increase since

the year 2012 until

2017, the imported

quantity almost

doubled in the last five

years and jumped from

41,395 tons in 2012 to

reach 76,507 tons in

2017 to achieve

compound average

growth rate in the last

five years by 13.1%.

On the other hand, a dramatic

change in the direction and source of

supply to the Romanian market over

the last five years. the majority of

supply since 2013 until 2016 was

coming from EU countries. The

share of EU in supply of tomatoes to

Romanian market reached 72.6% in

year 2013. The market witnessed

annual diminishing in EU share in

supply to reach 53.6% in 2016. In

2017 the supply from countries

outside EU overcame the supply

from EU and acquired 58.3% rom market compared to only 41.2% to the supply form EU countries.

11th top ranked EU importing country of fresh tomatoes, 2.57%

share in the EU imports of fresh tomatoes in year 2017

Despite the imports achieved slight low growth in year 2017 by

0.21%, but over the last five years the average annual growth

rates hiked 10.8%

Imports volume

performance 76,506 Metric Ton in 2017

5 years CAGR 10.78%

Last year 0.21%

Last 3 years 39.74%

Last 5 years 84.82%

26

Turkey, Spain and Albania are

the major suppliers to the

market; these countries

acquired 66.5% of total supply

to the Romanian market in

2017.

The share of supply from both

Turkey and Albania is growing

rapidly, the supply from Turkey

jumped from 24.8% of total

supply to Romanian in 2013 to

reach 49.1% in 2017. On the

other hand, the supply from

Albania jumped from 0.8% in

2013 of total supply to

Romanian market and reached 8.4% in 2017.

The supply from Spain and Italy diminished dramatically in the last five years. the supply from Spain dropped from

15.4% of total supply to Romanian market in 2012 to reach 8.8% of market in 2017; however, the supply from Italy

dropped from 17.4% in 2012 to reach 8.3% in 2017.

In terms of supply value, the

imported value of tomatoes in

the Romanian market reached

88.7 million USD in 2016 by

achieving 29% growth from

the previous year and

achieving 42% growth over the

last five years. Romania share

in global import value of

tomatoes is 0.9% and taking

the rank number 20th among

the top importing countries.

Dramatic change in source

of supply has been

witnessed, the supply

switched from EU countries

to non-EU countries from

2015. In terms of value,

Turkey is dominating the

market by 31.5% of total import value in 2016, followed with Spain and Italy. Despite the supplying quantity form

both Spain and Albania are equivalent, but the import value from Italy is three times the import value from Albania.

27

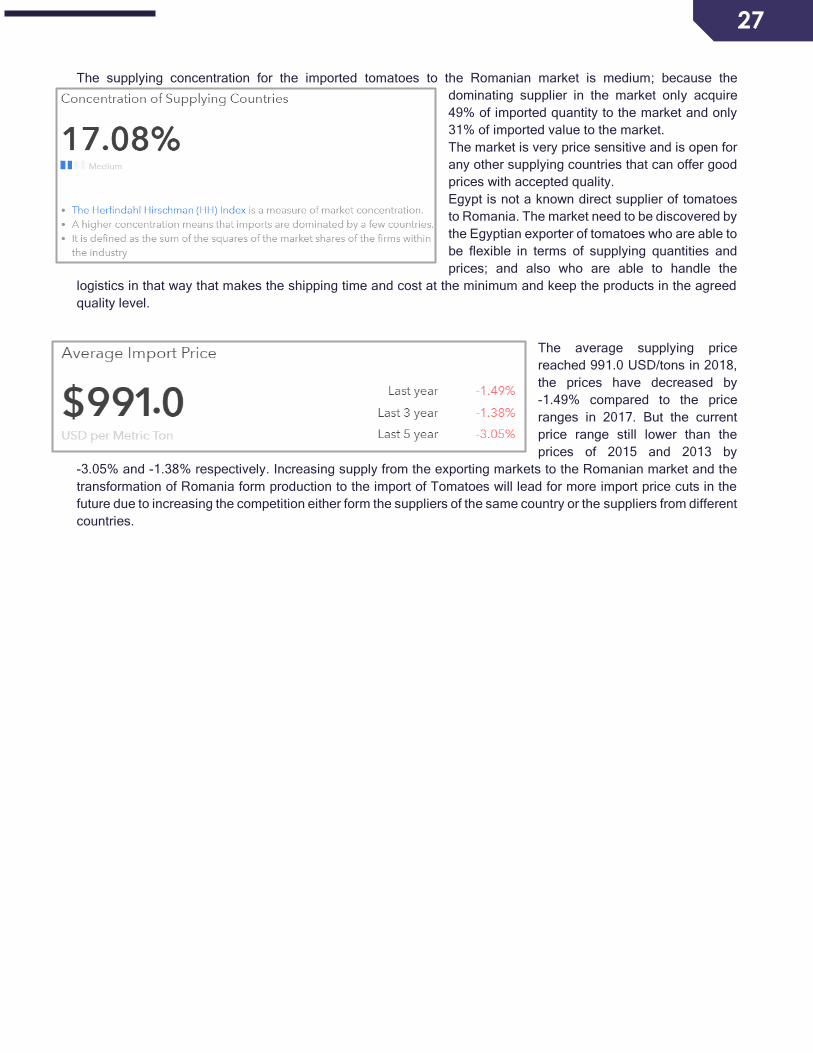

The supplying concentration for the imported tomatoes to the Romanian market is medium; because the

dominating supplier in the market only acquire

49% of imported quantity to the market and only

31% of imported value to the market.

The market is very price sensitive and is open for

any other supplying countries that can offer good

prices with accepted quality.

Egypt is not a known direct supplier of tomatoes

to Romania. The market need to be discovered by

the Egyptian exporter of tomatoes who are able to

be flexible in terms of supplying quantities and

prices; and also who are able to handle the

logistics in that way that makes the shipping time and cost at the minimum and keep the products in the agreed

quality level.

The average supplying price

reached 991.0 USD/tons in 2018,

the prices have decreased by

-1.49% compared to the price

ranges in 2017. But the current

price range still lower than the

prices of 2015 and 2013 by

-3.05% and -1.38% respectively. Increasing supply from the exporting markets to the Romanian market and the

transformation of Romania form production to the import of Tomatoes will lead for more import price cuts in the

future due to increasing the competition either form the suppliers of the same country or the suppliers from different

countries.

28

Romania Exports of tomatoes

Romania is not recognized as an exporter of tomatoes, the export quantity is not reaching 500 tons in either 2016

or 2017. Around 70% of exports go for Moldova, Netherlands and Hungary. Two of them are boarder countries.

The majority of exports take place during the production season of Romania; this means Romania is not a transit

hub for any boarder countries.

Romania Export value

diminished in 2016 by -49% to

reach 629,000 USD, over the

last five years the export value

diminished by more than -65%.

Globally, Romania share in the

global exports of tomatoes is

less than 0.01% and ranked

number 89 among the global

exporting markets.

The revealed comparative

advantage for export of tomatoes

from Romania is too low.

Romania does not have any

comparative advantage for

exporting tomatoes.

As a conclusion, Romania is

switching from producing

country into a net importing

country of tomatoes, over the

last years Romania has increasing trend of importing tomatoes from non-EU countries. This means there is a good

opportunity for the world suppliers especially if the months before June and after October.

29

Consumption

Annual average consumption per capita in Romania has fluctuated from one year to the next (see the chart below). The highest annual average of tomatoes consumption per capita was recorded in 2013 (40.0 kilograms per capita) and the lowest was 35.26 kg/inhabitant. In 2017, the annual average consumption of tomatoes decreased by 11.8% compared to 2013.

Regarding the monthly average of tomato consumption per person, at national level and by residence area, it was found that it varied from one year to another.The highest consumption is registered in the urban environment as opposed to rural areas. The highest monthly average consumption of tomato per person in the urban area was registered (0.9625 kg / inhabitant), and in the rural area was 0.9311kg/inhabitant.

The amount of tomatoes purchased by a household by residence area varied from one year to the next in the analyzed period. In 2016 there is a decrease (-5.4%) of the tomatoes quantity purchased at national level. The biggest quantity of tomatoes purchased was recorded in 2013 (0.859 kg), and the lowest was 0.699 kg (2017). From the data presented, it can easily be noticed that the situation in the residence area is different. In the urban area, the amount of tomatoes purchased by a household is definitely superior to that purchased in rural areas. This is explained by the fact that part of the rural population produces in their households the tomatoes required for consumption. In winter, when imported tomatoes are generally eaten, rural households buy a small amount of tomatoes because of high prices for the category of tomatoes and, on the other hand, the small incomes of these households. In 2015, in the urban area, there is a 3.1% decrease in the quantity of purchased tomatoes. This decline can also be explained by the fact that consumers in the urban area acquire other categories of imported vegetables. In rural areas, in 2015, the amount of tomatoes purchased by a household accounted for only 44.6% of the amount purchased by the urban population.

Romanian tomatoes market has multiple weaknesses. In the analyzed period (2011-2017), the area cultivated with tomatoes and production decrease. Regards from area decreased in 2015 with 15.1%. Also, total tomatoes production decreased with 14.7% and average production registered the same trend. The most significant average production per hectare of tomatoes was obtained in 2011 (17,602 kg / ha). This made to increase quantitative imports of tomatoes and to decrease exports. As a result, the highest average annual consumption per capita of tomatoes was achieved in 2013 (40 kilograms per capita). The highest average annual per capita consumption was recorded in urban areas as opposed to rural areas. The quantity of tomatoes purchased by residential household has recorded oscillations by year to year. Also, the highest average price was registered in 2012 (3.06 lei / kg). The average monthly expenditure per person for the purchase of tomatoes increased by 9.4% in 2017 compared to 2012.

30

Product Quality

This section presents UNECE Standard FFV-36 that is applied in the EU countries concerning the marketing and commercial quality control of tomatoes. This standard applies to tomatoes of varieties (cultivars) grown from Solanum lycopersicum L. to be supplied fresh to the consumer, tomatoes for industrial processing being excluded.

Tomatoes may be classified into the following commercial types:

• “round”;

• “ribbed”;

• “oblong” or “elongated”;

• Cherry/cocktail tomatoes (miniature varieties) of all shapes.

Quality of tomatoes

The purpose of the standard is to define the quality requirements for tomatoes at the export-control stage after preparation and packaging. However, if applied at stages following export, products may show in relation to the requirements of the standard:

• A slight lack of freshness and turgidity

• For products graded in classes other than the “Extra” Class, a slight deterioration due to their development and their tendency to perish.

The holder/seller of products may not display such products or offer them for sale, or deliver or market them in any manner other than in conformity with this standard. The holder/seller shall be responsible for observing such conformity.

1. Minimum requirements

In all classes, subject to the special provisions for each class and the tolerances allowed, the tomatoes must be:

Intact

Sound; produce affected by rotting or deterioration such as to make it unfit for consumption is excluded

Clean, practically free from any visible foreign matter

Fresh in appearance

Practically free from pests

Free from damage caused by pests affecting the flesh

Free of abnormal external moisture.

Free of any foreign smell and/or taste.

In the case of trusses of tomatoes, the stalks must be fresh, healthy, clean and free from all leaves and any visible foreign matter.

The development and condition of the tomatoes must be such as to enable them:

To withstand transportation and handling

To arrive in satisfactory condition at the place of destination.

31

2. Maturity requirements

The development and state of maturity of the tomatoes must be such as to enable them to continue their ripening process and to reach a satisfactory degree of ripeness.

3. Classification

Tomatoes are classified in three classes, as defined below:

i. Class I: Extra class

Tomatoes in this class must be of superior quality. They must be firm and characteristic of the variety. They must be free from greenbacks and other defects, with the exception of very slight superficial defects, provided these do not affect the general appearance of the produce, the quality, the keeping quality and presentation in the package.

ii. Class I

Tomatoes in this class must be of good quality. They must be reasonably firm and characteristic of the variety.

They must be free of cracks and visible greenbacks.

The following slight defects, however, may be allowed provided these do not affect the general appearance of the produce, the quality, the keeping quality and presentation in the package:

• A slight defect in shape and development;

• Slight defects in colouring;

• Slight skin defects;

• Very slight bruises.

Furthermore, “ribbed” tomatoes may show:

• Healed cracks not more than 1 cm long;

• No excessive protuberances;

• Small umbilicus, but no suberization;

• Suberization of the stigma up to 1 cm2;

• Fine blossom scar in elongated form (like a seam), but not longer than two-thirds of the greatest diameter of the fruit.

iii. Class II

This class includes tomatoes that do not qualify for inclusion in the higher classes but satisfy the minimum requirements specified above.

They must be reasonably firm (but may be slightly less firm than in Class I) and must not show unhealed cracks.

The following defects may be allowed, provided the tomatoes retain their essential characteristics as regards the quality, the keeping quality and presentation:

• Defects in shape and development;

32

• Defects in colouring;

• Skin defects or bruises, provided the fruit is not seriously affected;

• Healed cracks not more than 3 cm in length for round, ribbed or oblong tomatoes.

Furthermore, “ribbed” tomatoes may show:

• More pronounced protuberances than allowed under Class I, but without being misshapen;

• An umbilicus;

• Suberization of the stigma up to 2 cm2;

• Fine blossom scar in elongated form (like a seam).

Sizing of tomatoes

Size is determined by the maximum diameter of the equatorial section, by weight or by count.

The following provisions shall not apply to

• trusses of tomatoes;

And are optional for:

• Cherry and cocktail tomatoes below 40 mm in diameter;

• Ribbed tomatoes of irregular shape; and

• Class II.

To ensure uniformity in size, the range in size between produce in the same package shall not exceed:

a) For tomatoes sized by diameter:

• 10 mm, if the diameter of the smallest fruit (as indicated on the package) is under 50 mm;

• 15 mm, if the diameter of the smallest fruit (as indicated on the package) is 50 mm and over but under 70 mm;

• 20 mm, if the diameter of the smallest fruit (as indicated on the package) is 70 mm and over but under 100 mm

• There is no limitation of difference in diameter for fruit equal or over 100 mm.

In case size codes are applied, the codes and ranges in the following table have to be respected:

Size Code Diameter (mm)

0 ≤ 20

1 > 20 ≤ 25

2 > 25 ≤ 30

3 > 30 ≤ 35

4 > 35 ≤ 40

33

5 > 40 ≤ 47

6 > 47 ≤ 57

7 > 57 ≤ 67

8 > 67 ≤ 82

9 > 82 ≤ 102

10 > 102

b) For tomatoes sized by weight or by count, the difference in size should be consistent with point (a).

Tolerances of tomatoes

At all marketing stages, tolerances in respect of quality and size shall be allowed in each lot for produce not satisfying the requirements of the class indicated.

1. Quality tolerance

Extra Class

A total tolerance of 5 per cent, by number or weight, of tomatoes not satisfying the requirements of the class but meeting those of Class I is allowed. Within this tolerance not more than 0.5 per cent in total may consist of produce satisfying the requirements of Class II quality.

Class I

A total tolerance of 10 per cent, by number or weight, of tomatoes not satisfying the requirements of the class but meeting those of Class II is allowed. Within this tolerance not more than 1 per cent in total may consist of produce satisfying neither the requirements of Class II quality nor the minimum requirements, or of produce affected by decay.

In the case of trusses of tomatoes, 5 percent, by number or weight, of tomatoes detached from the stalk is allowed.

Class II

A total tolerance of 10 per cent, by number or weight, of tomatoes satisfying neither the requirements of the class nor the minimum requirements is allowed. Within this tolerance not more than 2 per cent in total may consist of produce affected by decay.

In the case of trusses of tomatoes, 10 per cent, by number or weight, of tomatoes detached from the stalk is allowed.

2. Size tolerances

For all classes: a total tolerance of 10 per cent, by number or weight, of tomatoes not satisfying the requirements as regards sizing is allowed.

34

Presentation of tomatoes

1. Uniformity

The contents of each package must be uniform and contain only tomatoes of the same origin, variety or commercial type, quality and size (if sized).

The ripeness and colouring of tomatoes in “Extra” Class and Class I must be practically uniform. In addition, the length of “oblong” tomatoes must be sufficiently uniform. However, a mixture of tomatoes of distinctly different varieties, commercial types and/or colours may be packed together in a package, provided they are uniform in quality and, for each variety, commercial type and/or colour concerned, in origin.

The visible part of the contents of the package must be representative of the entire contents.

2. Packaging

Tomatoes must be packed in such a way as to protect the produce properly. The materials used inside the package must be clean and of a quality such as to avoid causing any external or internal damage to the produce. The use of materials, particularly paper or stamps bearing trade specifications, is allowed, provided the printing or labelling has been done with non-toxic ink or glue.

Stickers individually affixed to the produce shall be such that, when removed, they neither leave visible traces of glue nor lead to skin defects.

Packages must be free of all foreign matter.

Marking of tomatoes

Each package must bear the following particulars, in letters grouped on the same side, legibly and indelibly marked, and visible from the outside.

1. Identification

Packer and/or dispatcher/shipper:

Name and physical address (e.g. street/city/region/postal code and, if different from the country of origin, the country) or a code mark officially recognized by the national authority.

2. Nature of produce

“Tomatoes” or “trusses of tomatoes” and the commercial type, or “cherry/cocktail tomatoes” or “trusses of cherry/cocktail tomatoes” or equivalent denomination for other miniature varieties if the contents are not visible from the outside.

“Mixture of tomatoes”, or equivalent denomination, in the case of a mixture of distinctly different varieties, commercial types and/or colours of tomatoes. If the produce is not visible from the outside, the varieties, commercial types and/or colours and the quantity of each in the package must be indicated.

Name of the variety (optional).

3. Origin of produce

Country of origin and, optionally, district where grown, or national, regional or local place name.

35

In the case of a mixture of distinctly different commercial types and/or colours of tomatoes of different origins, the indication of each country of origin shall appear next to the name of the commercial type and/or colour concerned.

4. Commercial specifications

Class

Size (if sized) expressed as

o Minimum and maximum diameters; or

o Minimum and maximum weights; or

o Size code as specified in Section III; or

o Count followed by the minimum and maximum sizes.

36

Product Trends and outlook

1- Despite the sharp drop in local production of tomatoes in Romania over the last five years, The Romanian

Ministry of Agriculture wants to increase the country's own supply of tomatoes and is putting 40 million

euro a year towards a program to enable this. So far, around 35 million euros have been spent in

Romania, according to authorities, to import 50,000 metric tonnes of tomatoes. In return, only around

3,000 metric tonnes worth two million euros will be exported. This is despite the fact that Romania farming,

climate-wise, is predestined for vegetable production and especially tomato production, according to

experts. That is why the foreign trade balance in the vegetable sector should change as a result of the

"tomato program" launched this year, which has initially been planned for eight years.

2- EU average tomato prices in March 2018 were 19% below the reference period average (5 preceding

years). That indicator is very different among EU Member States. 27% above average in IT, 23% below

average in ES, 6% under average in the NL and 5% below average in FR.

3- There is, therefore, a dual situation at MS level: price levels are very low in ES and IT and moderately

under average in FR and NL. Southern MS face increasing competition from early productions in Central

Europe thanks to technological advance. Imports from Morocco in the 1st quater of 2018 were at relatively

high levels when compared to the reference period.

4- When looking backwards, EU average tomato prices were at about the maximum level of the reference

period in November 2017; between December 2017 and January/February 2018 prices registered gradual

reductions until stabilizing in February and March at around the minimum level price of the reference

period. Provisional April prices show additional price reductions in ES and IT.

5- As an exception to the generally good market situation in 2017, the month of May was a difficult month

(the period between May to Aug in the case of NL) due to the importance of exports during that month

before the loss of the Russian market. A specific feature of the tomato market is that the level of prices

can change very quickly in a matter of 2 or 3 months from very high to very low or vice-versa.

6- Romanians become more and more aware about the importance of food quality and this creates a new

segment of customers that will be targeted with special menu offerings. This trend towards an improved

lifestyle and healthier products was not considered as a core development strategy for foodservice’s

strong brands. This changed when Salad Box was launched as a healthy fresh food alternative in fast

food, one of the categories with high rates of processed products. It is expected that other companies will

consider the growth potential represented by healthy fresh food, to improve their positioning and to

increase sales. New healthy concepts such as natural juice and smoothie bars, fresh soups, vegetarian

food and fruit mixes developed through street stalls or other formats are still possible. Organic menu

offerings represent the highest objective in healthy foodservice but for this to be present, important

transformations still need to take place.

7- Since is it expected that price will remain an important element when Romanians make a consumption

decision, best price or best value for money is the strategy used by many foodservice businesses. Special