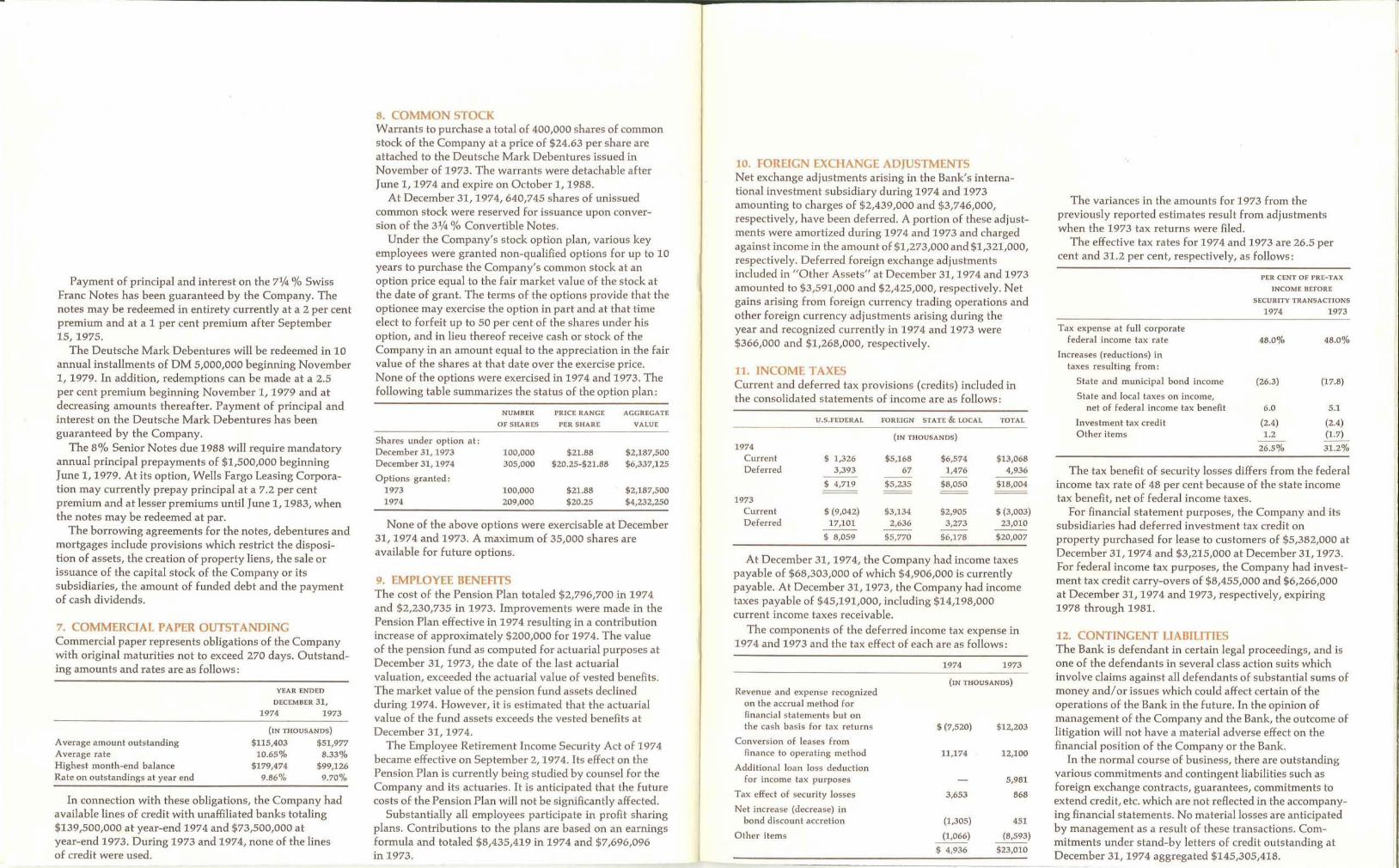

tm~ rfonl'~€¦ · highlights change per for theyear (inthousands) 1974 1973 amount cent...

TRANSCRIPT

tM~rfonl'~

1974ANNUALREPORT

-, -.",,,~. ~

•41 -t

J'l,., I • "'~I" . ,~.",~ . '..-., f·. ~:,~ ~., A ',to . "11 • . } ~ ).,.~ I .'.,

' ~ ,.. ,,",,\', .~;), 1, I . ~}I f I l., ,,' t t'l , ,J ..

• . ~.... .J '~' " ... II '" '~., ~ ,.... ',- ~... ~, Ito. \ . ,- ,-, , t' • " ~. , •

' " .\, ..... ~....._..

highlights

CHANGE PERFOR THE YEAR (IN THOUSANDS) 1974 1973 AMOUNT CENT

Income before Security Losses $50,074 $44,119 $5,955 13.5

Security Losses Net of Tax (2,705) (660) (2,045)

Net Income $47,369 $43A59 $3,910 9.0

Dividends Declared $19,059 $17,870 $1,189 6.7

PER SHARE (1)

Income before Security Losses $2.53 $2.25 $0.28 12.4

Net Income $2.39 $2.21 $0.18 8.1

Dividends Paid $0.96 $0.885 $0.075 8.5

AT THE YEAREND (IN THOUSANDS)

Assets $12,675,123 $11,767,725 $907,398 7.7

Deposits 9,740,290 9,016,894 723,396 8.0

Loans and Leases 8,065,712 7,139,368 926,344 13.0

Investments 1,737,095 1,669,793 67,302 4.0

Book Value Per Share (Excluding Capital Notes) $21.28 $19.99 $1.29 6.5

(1) Based on average number of shares outstanding of 19,804,343 for 1974 and 19,633,968 for 1973.

letter to shareholders

Wells Fargo & Company improved both

its earnings and its capital position in1974, a year of severe economic stressand of varied pressures on banks andbank holding companies.

Total earnings (net income beforesecurity transactions) were $50,074,000

or $2.53 per share, a 12.4 per centincrease over the total of $44,119,000 or$2.25 per share registered in 1974. Netincome in 1974 after security transactions was $47,369,000 or $2.39 per sharecompared with $43,459,000 or $2.21 pershare in 1973.

These earnings were achieved in a yearin which our operating strategy calledfor, first, a reduction of loan volumegrowth while emphasizing loan qualityand profitability and, second, consolida

tion rather than expansion of our international activities.

This strategy was adopted in ourCompany planning sessions in the summer of 1973 and became the basic element

of the profit plan approved for 1974.

Our objectives in pursuing this coursewere several. Loans in the previous threeyears had grown at a rate faster thanboth deposits and retained earnings. Acontinuation of this trend would haveresulted in higher leverage with a lowercapital-to-assets ratio and a lower returnon earning assets-a pattern typical ofmany of the larger banks and bank holding companies during the last few years.

At the time we approved this plan, wedid not anticipate that 1974 would endwith a severe economic recession. Nordid we foresee that the year would bringto the banking industry warnings andpressures from the regulatory agencies torestrict loan volume and to limit expansion of holding company diversification,in order to improve capital and liquidityratios.

However, the strategies we followed in 1974 served us well andwill be continued in 1975. Our loangrowth was limited to 13 per cent in

1974. Our liquidity and leverage ratioshave reversed direction, and our returnon-assets ratio was increased. In 1975,

we expect to see further strengtheningof our capital ratios as our modifiedgrowth plan is continued.

This past year has been one in whichpublic confidence in private banking

has been questioned for the first timein 40 years. This resulted from severalfactors: the failme of two major banksin the United States and one in Europe;the appearance of a number of magazinearticles claiming banks are "overextended;" the growth of bank assetsat a faster rate than bank capital, givingrise to allegations of capital inadequacv;

the increase in loan losses generatedby the recession; and the extent to whichliability management has caused overreliance on short-term funds to meetlonger-term obligations.

There is evidence in the bankingsystem of all these things. But the issueof importance to the shareholder andthe depositor and the public generally ishow serious these matters are and howtheir interests are being protected. A fewcomments about each seem warrantedat this time and hopefully will providesome perspective for your furtherevaluation.

..

With respect to bank failures, since1968 there have been 31 (there are14,000 domestic banks). Of these, 11

could be primarily attributed to insidertransactions. The same factor wassignificantly present in 16 other failures.Thus, a total of 27 of the 31 bank failures were management failures. Thisillustrates what we feel is an importantpoint-the best protection for depositorsand shareholders alike is the matureexperience and integrity of the management of their bank.

Capital adequacy is a complex issue tocover in a few sentences, but a fewthings can be said which may be useful.Absolute levels of equity capital inrelation to total assets and deposits havebeen eroding but, as we have seen,absolute levels of capital have had littleto do with why banks fail.

Since a major function of equity capi

tal is to afford protection againstabnormal losses, one must look at thecomponents of various kinds of protective funds, which include a bank'sreserves against loan losses and itsretained earnings-both of which havegrown much more rapidly than loan

Members of Wells Fargo'sExecutive Office are: Presidentand Chief Executive OfficerRichard P. Cooley, near left;Chairman Ernest C. Arbuckle,left of Mr. Cooley i Vice ChairmanJames K. Dobey, far left; and ViceChairman Ralph J. Crawford, Jr.

losses in the last 25 years. In additionthe Federal Deposit Insurance Corporation has and continues to providecomplete depositor protection now up to$40,000 per account.

The amount of straight equity desirable for any given bank depends upona number of factors. Relatively lowequity capital ratios do not necessarilyindicate weakness in a bank's capitalstructure. For instance, one must alsolook at capital provided by long-termdebt and sustained earnings growth. Thequality and source of those earnings isalso important. Consideration must begiven to the stability provided by a highratio of passbook savings to totaldeposits, and by a steady and high inflowof funds provided by the amortizationof a large percentage of consumer andmortgage loans. These stabilizing factorsare all present in Wells Fargo and aresignificant in assessing comparativestandards of adequacy and liquidity.With a slowing of loan growth and theretention of strong earnings, we feel ourtotal capital funds can sustain our current activity and modest growth in assetvolumes for the years immediately ahead.

With respect to loan losses, you havenoted in the earnings reports of manybanks the substantial increases that havebeen made to loan loss reserves in thelatter part of 1974 to protect againstthe higher loan losses which can normally be expected in a period of recession. This has and will affect bankearnings, but this increase in reserves isevidence of sound banking practice at atime of economic stringency. It is anessential step to ensure soundness andsafety.

In our own case, we added an extra$6,300,000 to our loan loss reserves overand above our normal five-year moving

average formula provision. This completely covered our 1974 loan write-offsand provided an increase in the valuationportion of our reserve for bad debts,which now exceeds $50,000,000.

Liability management refers to the useof short-term purchased funds to meetloan commitments. This practice hasbeen growing since the introduction ofthe certificate of deposit in 1961 andhas been effective in enabling banks tomeet increasing loan demands throughout the last decade. It has also providedthe flexibility to adapt to changingconditions in the economy. The use ofpurchased funds permits loans to growfaster than regular demand and consumer time deposits and does providea method for banks to meet the needs oftheir corporate customers. The result hasbeen an increased dependency on purchased funds.

The most important lesson of 1974 hasbeen that all banks cannot rely onmoney markets as dependable sourcesof funds at all times. Although theconsequences have not been serious forthe solvency and viability of the bankingsystem, they have provided an experience for banks which has resulted in arevaluation of the appropriate amountof purchased funds and the length oftheir maturities. Wells Fargo, forinstance, adopted a program which willspecifically lessen reliance on the useof overnight funds and increase the useof longer-term certificates of deposit.

We feel that the experience of the pastyear and the expectations for economictrends in 1975 will see a strengthening ofthe banking structure of our country inthe future. There has been are-emphasis

of the need for constant vigilance withrespect to loan quality. There is a greatersensitivity to the importance of accuratecost information, which will providea basis for a price structure that willensure a reasonable profit. Greater carewill be used in examining the externalforces of our environment and ourdecisions will be based on a recognitionof the critical variables in that environment. We will be refocusing on thedepositor as the key to the ability ofbanks in the years ahead to meet theunexpected demands for credit. AtWells Fargo we have maintained thatposition by paying a higher rate of interest for passbook savings than our majorcompetitors. Most important, we aregiving renewed and special attention tothe consumer-our customer-whoseneeds, both individual and corporate,we exist to serve.

To help us achieve these objectives,the Executive Office was expandedfurther in 1974 and the responsibilitiesof its new members were increased.James K. Dobey, who in 1973 was namedto the Executive Office, was made ViceChairman of the Board of the Bank andthe Company in 1974. Ralph J. Crawford,Jr., was named fourth member of theExecutive Office and Vice Chairman of theBank and the Company during the year.He joins Mr. Dobey in overseeing theday-to-day activities of our organization.

During the turbulent year just past,we received strong support and outstanding counsel from our Board ofDirectors. In the spring, we welcomed tothe Board Helen K. Copley, chairmanof The Copley Press Inc. and publisherof The San Diego Union and San DiegoEvening Tribune. She filled the vacancyleft by the resignation of Leonard K.Firestone who was appointed U.s.Ambassador to Belgium.

Our thanks for their cooperation andfine performance go to our staff whohelped us achieve our increases in earnings in a very difficult economic year.

Ernest C. ArbuckleChairman of the Board

W~~Richard P. CooleyPresidentand Chief Executive Officer

January 29, 1975

summary of bankoperations

With a network of 313 branchesin California, Wells Fargo

provides a full range of consumer banking services, including

savings programs, checkingaccounts, Master Charge credit

card, installment lendingservices, real estate loans and

safe deposit facilities. Manyof the services are groupedin the Bank's popular Gold

Account package.

CONSUMER13ANKINGWells Fargo made striking gains inconsumer banking in 1974.

The Bank's 5 per cent passbooksavings rate brought us some $199

million of additional deposits during1974 (exclusive of deposits addedthrough acquisitions and mergers), morethan were gained by all other Californiabanks combined during the year. At theend of the year, total passbook savingsdeposits amounted to $2,005,727,000,

making Wells Fargo the second bank inthe United States to pass $2 billion inthis category.

Wells Fargo's Gold Account, thepioneering package service, was augmented during the year by the additionof a $2,500 personal accident insurancefeature. Gold Account customers alsomay now obtain supplemental personalaccident insurance. Some 175,000

Californians are members of our GoldAccount program.

Increases in numbers of MasterCharge cardholders and in total outstandings in 1974 attest to the continued popularity of this service. Netgain in cardholder accounts during theyear was 107,284, and outstandingsrose to $188 million, an increase of34 per cent.

Despite the credit crunch and itsimpact on all types of loans, Wells Fargomade some 5,700 loans on singlefamily homes during 1974, totaling$206,390,488. At year end the Bank's

total portfolio of Single-family homeloans amounted to $1.49 billion.Wells Fargo also had $983,231,000 inconsumer and installment loans outstanding at year end.

With the help of two importantacquisitions during 1974, Wells Fargoexpanded its coverage of the SouthernCalifornia market. Early in the year, wepurchased certain assets and assumedcertain liabilities of the Beverly HillsNational Bank. This acquisition of threenew offices provided us with additionalvalued commercial and consumerbanking ties in this important SouthernCalifornia community.

In August, a merger with CommercialNational Bank of Buena Park wasconsummated, giving Wells Fargo sevenadditional offices with a strong consumerorientation in the growing OrangeCounty market.

Four new offices were opened in 1974,

all in Southern California: Santa Barbara, San Diego and two in Pasadena,one of the latter an innovative "StageStop" office that is primarily a checkcashing and deposit-taking convenience.One branch-the Sonoma MortgageDivision office-was closed in 1974 afterthe division became a subsidiary. WellsFargo now has 313 branches statewide,62 of them in the southern part of the

state. During the year, the number ofWells Fargo customers in the Southpassed the 250,000 mark.

In keeping with the Bank's announcedobjective of slower but higher qualitygrowth in the future, the Retail BankingDivision devoted considerable time in

1974 to examining its operations andservices. Plans were laid for a restructuring of the branch divisions to providefor greater autonomy and responsibilityat the district level. It is believed thatthis policy will permit the geographicdivisions to respond more quickly andeffectively to local conditions andcustomer needs.

In another move to use our comprehensive financial skills, and inspired by ahighly succ~ssiul ~ctivity of Beverly

Hills National Bank, Wells Fargo willaccelerate the activities of its Entertainment Division. This group is geared toprovide financial services to high incomeearners in the entertainment industry,sports and the professions-a group ofpeople with unusual financial andbanking needs.

To enhance basic banking servicestatewide, Wells Fargo in 1974 largelycompleted installation of 1,700 finger-tipcomputer terminals at teller stations inits branches. With the new system,tellers can now obtain instantaneousaccount information for customerswithout leaving their stations, regardlessof whether the customer is in the officewhere his or her account is carried. Thenew system will enable us to providesubstantially faster customer service.

CORPORATE. 'BANKINGActivities of the Corporate BankingGroup comprise a key element in implementation of the Bank's overall policyof restraining asset growth. In 1974, thegroup devoted considerable attentionto loan profitability rather than towardincreasing loan volume. As a result,the size of the Bank's corporate loanportfolio rose very little over year-end1973 totals.

This emphasis was not only inresponse to the Bank's strategy of slowing asset growth, but was also attributable to the restrictive monetary policyadopted early in the year by the FederalReserve in its effort to combat inflation.

Inflation and the prospect of higherinterest rates in the spring of 1974

caused business firms to flock to banksand the money markets to borrow fundsbefore prices and rates rose further.After mid-March, loan demand soaredand the prime rate, in company withother short-term interest rates, beganmoving upward. The prime rate hit12 per cent in early July and remained atthat level until late October; rates onother money market instruments peakedin August and September and thenbe\!'an moving downward.

High loan demand and high moneymarket rates-coupled with tightmoney-required that the CorporateBanking staff give exceptionally carefulattention during the year to the qualityand profit potential of all components ofthe corporate loan portfolio.

A valuable tool in this effort was theCorporate Account Profitability System(CAPS), which was developed and putin place in 1973 as a step toward newcorporate loan pricing techniques. During 1974, the capabilities of thiscomputer-based system enabled our corporate loan officers to examine existingand prospective corporate relationshipsfor true profitability over a period oftime and in varying economic conditions.Wells Fargo will increasinglv use CAPS

Wells Fargo's Corporate BankingGroup makes commercial

loans for all purposes to largenational companies headquartered throughout the

United States and to majorlocal and regional companiesheadquartered in California.

Projects being financed rangefrom electronics to trans

portation to thermal energy.

analysis to establish loan programs andprices for corporate customers thatmeet mutually suitable objectives ofresponsiveness to the customer anda fair return for the Bank.

Corporate Banking in 1974 alsostressed development of officers who areindustry specialists. This ongoing effortis designed to enable Wells Fargo tobetter anticipate and serve the needs ofparticular types of companie"...s~.__

Money market supply and demandpressures during the year caused theCorporate Banking staff to focus attention on fee-based services, such as thoseprovided by the Securities IndustryDepartment.

The Securities Industry Departmentgenerated fee income amounting to$2.5 million in 1974. This group makesloans to brokers, handles securitiesdrafts and processes all securities transactions for Wells Fargo and its customers. The Special Industries Group,which deals exclusively with hight~c~nology companies that appear to

have outstanding potential for growthand success, also had an active andprofitable year.

During 1975, the Corporate BankingGroup will continue to gear its effortstoward quality loans, more precise pricing policies and increased fee income.Growth in the corporate loan portfoliowill continue to be restrained as theBank works toward the goal of limitedasset growth in 1975.

INTERNATIONALBANKINGThe year 1974 presented a complexenvironment for international bankers.Affecting global financial patterns wereworldwide inflation, floating exchangerates, the strong increases in world oilprices, concomitant inflows of sizableamounts of funds to oil-producingnations and high interest rates. Theseconditions combined to create a difficultatmosphere. Some banks in severalnations suffered foreign exchange losses,and a few banks failed during this period.

Three German banks collapsed during1974, with repercussions at bankinginstitutions in many countries. The mostsignificant impact was felt followingthe collapse of Bankhaus J.D. Herstattin Cologne, Germany. Wells Fargo had adeposit of $3 million with this bank,$1.5 million of which was charged toearnings in the third quarter, resultingin an after-tax loss of about 3.5 centsper share in the quarter's earnings.Wells Fargo expects to recover theremaining $1.5 million.

Wells Fargo's International Divisionhad a profitable year, despite thesedisruptive conditions. The division con-y .... __ ......... L ....... '-': _ ......... ,... _ ..... • ~._ .... ••

tributed nearly $6 million to the Bank'safter-tax profi ts in 1974. The Bank'spolicy of increasing fee income wasimplemented by placing emphasis onsuch services as letters of credit, collection and export financing. Consequently,documentary business increased sharplyand helped to generate growth in demanddeposits from $80 million in December1973 to $140 million at the end of 1974,an increase of 75 per cent.

Other new services also contributed tothe demand deposit gain. One of thesewas the Wells Fargo Bank InternationalMoney Order, introduced in mid-1973.It is now being sold by all our branchesand by 23 of our correspondentsaround the world.

In keeping with the Bank's emphasison increased fee income, InternationalBanking again stressed syndicated loanprojects during the year, and was able toorganize four syndications amountingto $193 million.

Our major international acquisition in1974 was a 15 per cent interest in CreditChimique, a privately held $700-millioncommercial bank headquartered in Paris.

The International Division hasfor many years provided foreigntrade financing and other servicesfrom its San Francisco headquarters office, and in the pastdecade has expanded its activitiesabroad to include three branchesand 12 representative offices.

Our partners in Credit Chimique areCompagnie Francaise des Petroles andPechiney Ugine Kuhlman, which are twolarge French industrial concerns, andCommerzbank in Germany. Despiterigid credit controls in France, CreditChimique was able to attain its profittargets for the year.

One of the key investments made byWells Fargo in 1973-AllgemeineDeutsche Credit-Anstalt (ADCA)-isa $1.2-billion institution with branches inmost of the principal cities of Germany.In 1974, ADCA expanded its nationwidesystem by opening a branch in theimportant city of Hamburg. Although1974 was an unusually difficult periodfor German banking, ADCA had asatisfactory year.

Western American Bank, based inLondon, is a consortium bank in whichWells Fargo holds a 22.5 per centinterest. Several steps were taken duringthe year which were designed to enableWestern American Bank to more effectively cope with the deterioration ininternational financial markets. Thesesteps included a suspension of unprofit-

able bond trading, the closing of theLuxembourg and Zurich offices and a 30per cent reduction in staff. The shareholder banks, including Wells Fargo, alsopurchased a substantial portion ofWestern American Bank's loan portfolioto assist it with its liquidity needs.Close coordination was maintainedthroughout the year between WesternAmerican's shareholders and its management, and Western American Bank wasable to report profits for the 1974operating year higher than those for thesame period in 1973.

To increase our global recognition andprovide a convenience to Europeaninvestors, Wells Fargo & Companyduring 1974 listed its shares on TheStock Exchange in London and on theFrankfurter Boerse.

In November 1974, Wells Fargoopened a new Iberian Peninsula Representative Office in Madrid to serveinternational customers in both Spainand Portugal. This brings our total number of overseas representatives to 12.

TRUST&INVE5TMENT SERVICESTrust Division fee income increased 7.2

per cent in 1974 to $16,066,000. Incommon with other areas of the Bank,the division is accelerating its efforts todevelop and market fee-producingservices.

Two important forums were heldduring the year to inform corporateexecutives and professional financialadvisors about Wells Fargo's capabilitiesin trust business. A one-day pensionseminar was held in Chicago in Marchfor corporate executives involved insupervision of pension funds of morethan $7 billion in assets. It was designedto provide them with the latest thinkingon the investment process, the expandingrole of the financial consultant and therecent pension legislation.

The second gathering was a continuation in Southern California of along-standing and successful traditioninitiated by the Trust Department ofBeverly Hills National Bank and, sinceour acquisition of its assets, nowsponsored by Wells Fargo. It is an annualestate planning forum for attorneys,accountants and insurance underwriters, which was held December 4 inBeverly Hills. Some 1,200 personsattended the 1974 forum.

During the year, Wells Fargo beganusing the services of The DepositoryTrust Company, a leading nationwidesecurities clearing house wholly-owned.............. .a,."L ...... "'-': ........ ..-. _ ......... __ •• ._

by the New York Stock Exchange.Wells Fargo was the first California bankto use the firm's services. It is a partof the ongoing effort to provide ourcustomers with the most efficienthandling of their securities.

Another step toward increasedcustomer service was the launching in1974 of a quarterly bulletin entitled"Investment Funds Perspective." Thispublication is sent to all customerswhose accounts utilize our CommonFunds. Late in the year, the TrustDivision made some administrativechanges to bring together and bettercoordinate as many as possible of thedivision's family-related accountrelationships. The customer-orientedreview of the division's functions andservices that prompted these moveswill continue in 1975.

The Bank's Trust Divisionadministers estates and personal

trusts; provides custody andinvestment advisory services

for individuals, corporations andnon-profit organizations;

and administers pension andprofit-sharing funds. Two

unusual projects are supervisionof a ranching operation andinvestment advisory service

for the Northwest Alaska NativeAssociation.

Our Wellsplan service-which provides advice to individual and corporatecustomers on tax planning, insuranceand special investments-continued tomake progress during 1974. On theadvice of Wellsplan, investors have nowacquired nearly $9 million of investmentassets, including $2 million in oil andgas interests.

The Real Estate Equity commingledfund and the Wells Fargo Index Fund foremployee benefit trusts both madefurther progress during the year.

WELLS FARGOINVESTMENT ADVISORSIn a major reorganization oriented to themarkets and clients that it serves, theformer Financial Analysis Departmentbecame a profit center and an operatingdivision of the Bank in 1974 and wasrenamed Wells Fargo InvestmentAdvisors. The new division continues to

work closely with the Trust Division,whose customers it serves. Its investmentservices include the management ofportfolios for personal and institutionalclients, investment advisory services forother asset managers and financialadvisory services in the field of corporatefinance.

In the area of portfolio management,the division advanced its work on thecontrol of risk, the allocation of assetsand the valuation of securities in theportfolios under its direction. Its disciplined approach to investment management, with emphasis on diversificationand explicit orientation to clientobjectives, continued to show favorableresults.

During the year, Investment Advisorsextended the marketing of its CorporateAdvisory Service to business firmsneeding assistance in corporate finance.The group advises companies on thevalue of their businesses, on proposedacquisitions and mergers, on capitalstructure and financing requirements,and on dividend policy and the cost ofequity capital. The service encompassesa full spectrum of advisory activities,from analysis and planning to detailedrecommendations and guidance inprogram implementation.

Investment Advisors also expandedthe product line and marketing staff of itsInstitutional Counsel Service during1974. This group sells Wells Fargo'sinvestment research, economic andmarket information, and portfolio management advice to other asset managers.Its activities include an annual seminarat the Bank's Head Office for current andpotential customers.

COMMITMENTSTO THE COMMUNITYBanks are deeply involved in the economic livelihood of the nation, and havea special responsibility and specialopportunities to fulfill their role ascorporate citizens.

Exemplifying its belief in thisphilosophy, Wells fargo in 1974 continued to study, improve and expand itsmany programs that affect our society,our fellow citizens and the communitiesserved by the Bank.

In the important area of equalopportunity in employment, for instance,the Bank has a moving five-yearAffirmative Action Program, which isupdated each year. The current programruns through December 1979. Its goalscall for minorities to represent over 38per cent of all staff members by 1979,compared with 28 per cent currently;more than 40 per cent of all officersto be women, compared with 36 per centtoday; 18 per cent of its officers to beminorities, compared with just under 12per cent now; and for the Bank to have45 women vice presidents and 36minority vice presidents at the end of1979, compared with eight of eachcurrently.

The total staff at Wells fargo Bankat the end of 1974-on a full-timeequivalent basis-was 11,730.

..., , .l .Ll "' _ ~_••

In order to meet these goals and tohelp staff members qualify for expandedresponsibility and promotion, the Bankin 1973 started a Career DevelopmentProgram to accelerate the advancementof minority and women officers, andto aid non-officers whose upwardmobility has been restricted becauseof lack of educational skills and Englishlanguage handicaps. A total of 76 staffmembers have gone through the CareerDevelopment Program. The Bank'sUrban Affairs Training Center, established in 1968, conducts special trainingprograms known as Job EducationTraining for disadvantaged minorities.

Wells fargo has one of the mostsuccessful and long-standing minoritysmall business loan programs of anybank. The bulk of these-669 loanstotaling over $26 million-are with theparticipation of the Small BusinessAdministration. However, 164 loanstotaling $4.2 million have been granteddirectly by Wells fargo to smallminority-owned business firms. These

are not all our loans to businessesowned by women or minorities, ofcourse, but represent those that do notmeet our regular credit standards. formany years, the Bank has also supportedthe banking industry's job and economicdevelopment corporations in majorcities in California.

At the end ofl.974, Wells fargo had aportfolio of student loans that amountedto more than $56 million, representingloans to some 30,000 students.

The Bank's Low Income FinanceTerms, or LIFT, program is designed toprovide installment loans to low incomeborrowers. At year end, LIFT had 767loans outstanding totaling nearly$960,000.

In the environmental area, Wellsfargo has a number of continuingprograms and some relatively newefforts. About 90 per cent of the Bank's

data processing waste paper is sold forrecycling and many internal and externalforms are printed on recycled paper.Wells fargo was the first bank to adoptbagasse, a sugar cane by-product, forall check printing.

for energy conservation, well over ayear ago the Bank eliminated all lightedoutdoor billboards from its advertisingprogram and has scaled down the useof illuminated signs and interior lighting.The energy conservation efforts reducedthe Bank's energy consumption by about20 per cent in 1974.

During the year, the Bank with thehelp of an outside consultant undertooka consumer affairs program in whichall public contact functions and inquiryhandling practices are being examinedto pinpoint areas where improvementscan be made. In addition, Wells fargohas a Corporate Responsibility Committee that consists of 12 officers, as wellas a full-time staff assistant. TheCommittee's mission is to examine anyarea of Bank operations and policies thataffect the individuals and communitieswe serve. Areas the Committee iscurrently studying include real estateloan policies, employment of thehandicapped and of individuals with

Wells Fargo has long been oneof the leading banks in thearea of corporate social responsibility. Among programs beingimplemented are those in jobtraining and career developmentfor the disadvantaged andfinancing of small business firmsfor minorities.

arrest or conviction records, consumereducation, corporate contributions andemployee charitable solicitation policies, and collection and defaultprocedures.

Among Committee recommendationsthat have been adopted is a MinorityPurchasing Program, in which variouspurchasing units have pledged that aportion of their budgets will be used forbuying goods or services from minorityfirms. Resulting from another recommendation, the Bank adopted aneducational gift-matching program in1974 in which it matches employeegifts-up to a $500-per-year limit. Sinceinauguration of this program in June,employees have contributed a total of$10,502 to 74 educational institutionsin 24 states, an amount that has beenmatched by the Bank.

Acting on another Committee recommendation, 16 members of the Boardof Directors and senior managementparticipated in a full-day pilot seminar inNovember conducted by the GraduateTheological Union in Berkeley, toexamine ethics in business.

In briet Wells Fargo has a wide rangeof programs under way aimed at activelypromoting economic and social wellbeing for Californians. The Bank is continually seeking ways to fulfill itscommitment to the community and tobring benefits tn rlll riti7pnc

WELLS FARGO LEASINGCORPORATIONWells Fargo Leasing Corporation becameinvolved in equipment leasing for anumber of energy development projectsin 1974, in locations as widely separatedas Montana, Louisiana and the NorthSea. For the year, the corporation contributed more than $1.2 million toearnings.

Currently, the leasing company has$132 million in lease receivables outstanding, and the volume has beensteadily increasing. The company concentrated its efforts during the past 12

months toward developing businessrelationships with medium-size California corporations. In this undertaking,leasing company executives workedclosely with the Bank's branch officers.

Wells Fargo Leasing has offices inLos Angeles, San Francisco, New York

Wells Fargo & Company, a onebank holding company formedin 1969, has subsidiaries ina variety of fields. Most activein 1974 were those involving realestate projects and equipmentleasing. WeIls Fargo Leasing has,for instance, leased the firstthree-dimensional brain scannerin Northern California.

outstanding loans declined to $243

million at year end, compared with $256

million at the end of 1973.

The management fees received by theadvisors from the trust declined to$1,374,000 in 1974, compared with$2,347,000 in the previous year. Theadvisory fee income is determined by aformula which relates to the net incomeof the trust.

Wells Fargo Realty Advisors hasoffices in Los Angeles, San Francisco,Phoenix ;mrl Hnl1c:tr".,

oriented activities. Wells Fargo MortgageInvestors is listed on the New YorkStock Exchange and had loan commitments totaHng $268 million on December 31, 1974. Because of the uncertaintiesfacing the real estate industry, thetrustees decided early in 1974 to restrictthe growth of the trust. As a result.

WELLS FARGO REALTY ADVISORSWells Fargo Realty Advisors was alsoaffected by the complex economicenvironment and the particular problemsfaced by the construction and realestate industries. This subsidiary, whichprovides advisory services on a fee basisand maintains a loan portfolio for itsown account, contributed nearly $1.03

million to parent company earningsin 1974.

This subsidiary was formed in 1970 toadvise Wells Fargo Mortgage Investors,as well as to conduct other real estate

In this troubled environment, WellsFargo Mortgage Company (formerly theSonoma Mortgage Company Divisionof the Bank) completed its first full yearas a subsidiary, and generated $1.1

million in earnings. As a subsidiary, thecompany now has greater flexibility inits investments and is permitted toexpand into other states.

Despite the difficulties faced by thereal estate industry in 1974, Wells FargoMortgage Company originated $140

million in loans, down from the 1973

figure of $155 million in new mortgageloans. At the end of 1974, the companywas servicing 47,000 mortgage loans,amounting to more than $970 million, forabout 225 investors.

The mortgage company established aninsurance agency during the year, whichoffers health, accident and mortgageredemption insurance to borrowerswhose property does not exceed fourunits. This agency is already contributing to profi ts and has excellent potential

f?~_~!_O~_t?..:_ ..._. . _._

Wells Fargo & Company is the parentnot only of Wells Fargo Bank, but also ofa group of subsidiaries active in fieldsrelated to banking. These non-banksubsidiaries manage a real estate investment trust; originate, arrange financingfor and handle servicing of real estateloans for investors; and provide equipment lease financing, data processingand securities clearance services.

During the year, the subsidiaries contribu ted $3,846,000 in net profi ts tothe parent company, or 7.69 per cent ofincome before security losses.

At the end of 1974, Wells Fargo'snon-bank subsidiaries were capitalized at$60,157,000, of which $32,657,000 wasequity and $27,500,000 was subordinated debt. Assets were $303,402,000.

Overall, these subsidiaries were inexcellent capital position as compared tosimilar organizations in the financiallyrelated industries in which they compete.

WELLS FARGO MORTGAGECOMPANYThe year 1974 was an extremely difficultone for the mortgage banking industry.High interest rates on alternate types ofinvestment drew funds away frominstitutions that normally provide mostof the nation's construction and realestate loans. By year end, an easing ininterest rates had begun and funds wereflowing back into mortgage lendingfirms, but at the same time the economicslump had caused business firms andcommercial developers to scale back their

summary ofnon·banKoperations

.... ....,.. __.~.t.",.".J ..._ ; ~l":l1nc

I.I\...G.U ...;-.. J. l'-l.y.l. _ ..... _.} ..... , ........... _.

management's analysis offinancial operations

WELLS FARGO & COMPANYCOMPARATIVE COMBINED BALANCE SHEETtNON-BANK SUBSIDIARIES ONLY (IN THOUSANDS)

DECEMBER 311974 1973

tUnuudited.

WELLS FARGO & COMPANYCOMPARISON OF NON-BANK SUBSIDIARIES' PROFITt1974 & 1973

[.

~_ t _

INTEREST EXPENSEInterest expense went up at a faster pacethan interest income in 1974 and 1973.

However, the increase was much largerin 1973 as compared to the previousperiod because the average rates paid onfunds were rising more rapidly in 1973

than in 1972, and because in 1973 it wasnecessary to fund a portion of earningassets with high-cost deposits, borrowedfunds and commercial paper. In 1974,

average passbook savings-paying the5 per cent rate-and average demanddeposits increased moderately, and thishelped to mitigate somewhat the rise in

INTEREST INCOMEFrom 1972 to 1973, the growth in interestincome came from both an increase inearning assets and higher yields asshown in Table II. Except for depositsplaced by overseas offices, the same pattern continued in 1974 although theearnings gain came more from improvedyields than from asset gain. In the caseof overseas deposits, the average volumedeclined from 1973 to 1974, but the yieldon these deposits increased sufficientlyto offset the volume decline, resulting inan incrp.3sp. in ;nrnrnp n"pr 1 0'7')

securities, to make these figures comparable to taxable items. Table I showsthat the growth in income before securitygains or losses between 1972 and 1973

benefited from the same percentageincrease in both interest margin andnon-interest income. The pattern wasdifferent between 1973 and 1974 whenthe growth in interest margin was threetimes as large as in the previous y~ar

while non-interest income showed amodest decline. The favorable impact ofthe increases was lessened in bothperiods by increases in other types ofoperating expenses.

INCOME STATEMENTThe Income Statement (Table I) showsitems of income before security gains orlosses as well as expense items for theyears 1972 through 1974. All items areadjusted to a taxable-equivalent basis,which means sums have been addedto non-taxed items, primarily municipal

Wells Fargo & Company's 1974 performance demonstrated the success of thepolicies, adopted late in 1973, of slowingasset growth and improving operatingratios and earnings. Guided by thisstrategy, the Company grew solidly butunder controlled conditions in 1974

and displayed sufficient flexibility to meetthe year's unusual economic demands.

Highlights for 1974 include:Per share earnings before security

gains or losses increased 12.4 per centfrom the previous year.

Average passbook savings registereda 9.1 per cent gain over 1973, increasingthe Bank's statewide market share ofpassbook savings and reducing the overall cost of funds.

Assets-controlled in accordance withthe announced policy-increased 7.7

per cent from 1973. This compared toa 'gain of 30.7 per cent in 1973 over 1972.

The provision for loan losses wasincreased 95 per cent above the 1973

provision, a result of the uncertaineconomic and financial climate.

The general banking environment hasaltered dramatically in recent yearswith drastic changes in the prime rate, inasset yields and the cost of fundingthose assets. To meet the changing conditions, Wells Fargo and the financialcommunity at large have made successiveplanning and strategy adjustmentswhich themselves have served as agentsof change. For these reasons, and in theinterests of supplying information toassist individual assessments of theCompany's performance, a detailedreview of key financial data is being provided. The text which follows has beendesigned to assist with analyses of theSix-Year Summary of Operating State

ments on pages 26 and 27.

19731974

EARNINGS EARNINGSNET PER NET PER

INCOME SHARE INCOME SHARE(IN THOUSANDS) (IN THOUSANDS)

reorganization during the year, whenits primary operations were brought backinto the Bank.

In 1974, Wells Fargo & Companywithdrew applications with regulatoryauthorities for approval of the acquisition of an auto leasing companyand the formation of an agriculturalfinance subsidiary. The decision towithdraw the applications was consistentwith Federal Reserve policies discouraging further expansion of bank holdingcompany activities at this time.

Wells Fargo Mortgage Company $1,116 $0.056

Wells Fargo Realty Advisors 1,029 0.052 $1,148 $0.058

Wells Fargo Leasing Corporation 1,212 0.061 592 0.030

Wells Fargo Realty Services, Inc. 28 0.002 66 0.003

Wells Fargo Securities Clearance 461 0.023 571 0.029

Wellsco Data * * 487 0.025

Subsidiary Total $3,846 $0.194 $2,864 $0.145

Per Cent Contributionto Wells Fargo & CompanyIncome before Security Losses 7.69% 6.49%

*Mujor operations retllmed to Bank orgunizution in 1974. tUnul/dited.

OTHER SUBSIDIARIESWellsco Data Corporation, a dataprocessing subsidiary that primarily";,~'!<':i ~'Y.p)!~ l:."r_'>() R:mk. l~nderwenta

WELLS FARGO SECURITIESCLEARANCE CORPORATIONWells Fargo Securities ClearanceCorporation, located in New York City,handles the security clearance operationsof Wells Fargo Bank as well as some ofthe Bank's major customers.

In a year of uncertainties in the stockmarket and declining volume, the company was less active than in the past.Its contribution to profits in 1974 was$461,000, compared with more than$500,000 in 1973.

$ 19,160 $ 27,206

158,542 47,130

111,646 69,204

9,157 5,961

821 502

4,076 2,248

$303,402 $152,251

$176,775 $ 47,680

50,720 31,770

15,750 16,000

27,500 27,500

$270,745 $122,950

$ 960 $ 960

23,007 23,007

8,690 5,334

32,657 29,301

$303,402 $152,251

Stockholders' EquityCapital StockCapital SurplusRetained Earnings

LiabilitiesAdvances from Wells Fargo & CompanyAccrued Expenses and Other LiabilitiesLong-Term DebtLong-Term Subordinated Debt

Payable to Wells Fargo & Company

Total

AssetsCash and Short-Term InvestmentsLoans (Net of Reserves)Direct Lease FinancingAccounts ReceivablePremises and EquipmentOther Assets

Total Assets

Total Stockholders' Equity

Total

WELLS FARGO REALTYSERVICES, INC.In 1974, Grayco Land Escrow, Ltd.,changed its name to Wells Fargo RealtyServices, Inc., in order to heighten itsidentification with the parent company.The firm is a leading corporate trustee inthe recreational real estate industry.Currently, it provides service to 80 recreationalland developers accounting formore than $200 million in receivables. Inaddition, it performs specialized dataprocessing services for the real estateindustry.

The firm was acquired in 1972 toprovide Wells Fargo with a vehicle toservice and monitor loans or notessecured on recreational land and secondhomes. However, in view of the currentenergy shortage and environmentalconcerns, this type of lending has not_ ....1'"otr~...•....... • .._ t-·,....~ ~I· .. 'I ...

- ~~ ::~_ ...,,~ ,... _ ..... 'J -~ •• -- _••

high cost borrowings to fund incrementalasset growth. The Company expects tocontinue these policies throughout 1975and the years ahead.

Also up from 1972 and 1973 levelswere net occupancy and equipmentexpenses. The increase was expected inview of Wells Fargo's continuing commitment to retail banking. At the end of1974, statewide offices totaled 313,compared to 1973's 300 and to 1972's296. Seven of the new 1974 offices wereadded as a result of the merger ofCommercial National Bank of Buena Parkwith Wells Fargo Bank, and three moreoffices were obtained when Wells FargoBank purchased certain assets and certainliabilities of Beverly Hills NationalBank. Expenses were also boosted by therelocation in late 1973 of the Data Processing Division into new quarters atFirst and Market Streets, San Francisco;and the openings in late 1973 of newregional staff headquarters in Oaklandand corporate headquarters in downtownLos Angeles. The year-to-year increasesin equipment expenses result from ageneral upgrading of equipment andfrom purchase of additional equipmentto meet the expanding volume of work.Only moderate increases in net occupancy and equipment expenses areexpected over the next few years.

Items of expense which are included inthe "Other Expense" in the Six-Year

Summary of Operating Statements for1974 have increased notably over 1973levels. The increase can be attributed tothe higher costs of utilities, supplies and

Net Taxable Equivalent Interest Incomeas a Percentage of Earning Assets

Earning Assets inBillions of Dollars

OTHER OPERATING EXPENSESThe inflationary price trend influencedexpenses markedly in 1973 and 1974, eventhough general cost control procedureswere in effect throughout these periods.In addition to the normal merit salaryincreases and staff additions, personnelexpenses increased because of specialsalary adjustment programs, more comprehensive medical benefits and additional fringe benefits designed to helpemployees keep pace with the rising costof living.

The other items included in "OtherOperating Income" varied significantlybetween 1973-1974. Fees for bankingservices increased from the previousyear whereas foreign exchange income,income from foreign equity investments,service fees from data processingconsulting and real estate managementfees declined.

EARNING ASSETS ANDNET INTEREST INCOME

$7

$6

$3

$9

$S

$4

$11

$8

$10

$0

$1

$2

3.71% 3.81%

1969 1970 1971 1972 1973 1974

Trust fees for the most part are basedon the market value of the assetsheld in trust. The 14.3 per cent increasein trust fees from 1972 to 1973 resultedprimarily from an increase in trustbusiness. While the fees generated in1974 were depressed due to the lowermarket value of assets, fees from newtrust accounts and from clients addedthrough the acquisition of Beverly HillsNational Bank in January helped toimprove the trust revenue for 1974.

1974. The increase in service chargeincome from 1972 to 1973 stemmedprimarily from the success of the WellsFargo Gold Account, the first package ofconsumer banking services which wasintroduced early in 1973 by Wells Fargo.Other major banks quickly followedWells Fargo's lead with the result thatcompetition for the individual customer'sdeposits has been unusually keenthroughout 1974. The Gold Accountmet the competition squarely and hadsubstantial increases in volume andincome for 1974.

1ST 2ND 3RD 4TH 1ST 2ND 3RD 4TH1973 1974

5%

6%

7%

8%

9%

11%

10%

12%

EJDB

Investments

Average PrimeRate for Quarter

Loans

SELECTED ASSET YIELDS(Taxable Equivalent Basis)

OTHER OPERATING INCOMEThe "Other Operating Income" figuresshown in Table I are a total of the noninterest income items-on a taxableequivalent basis-detailed in the Six-Year

Summary of Opemting Statements.

Service charges on deposit accountsprimarily those of individual depositorswere the largest single non-interestitem of income in 1972, 1973 and

MARGIN ANALYSISAs interest expense rose because earningassets had to be funded with increasingly costly funds, the net taxableequivalent interest income declined as aper cent of earning assets from 1970through 1973. Between the end of 1972and 1973, for instance, net interestincome dropped from 3.28 per cent ofearning assets to 2.76 per cent. Althoughthe decline had a negative impact onearnings, the rise in earning assets in thesame period was more than enough tooffset the impact.

The pattern changed in 1974, and netinterest income as a per cent of earningassets increased to 3.11 per cent. Thiswas primarily because of the increase inyields coupled with slower growth inearning assets. Earning assets increasedonly 13 per cent in 1974, comparedto a 31 per cent increase in 1973 and a 19per cent increase in 1972.

The Company's strategy to constrainthe growth of earning assets whileimproving the net yield on those assetshas proved successful, even though theunfavorable financial climate and heavyloan demand made 1974 a difficult timeto institute new policies. Implementationof the strategy has resulted in the funding of higher yielding assets, a reductionof activities in lower yielding areas ofbanking operations, and less reliance on

TABLE I • INCOME STATEMENT: TAXABLE-EQUIVALENT BASIS TABLE II· USES OF FUNDS: AVERAGE BALANCES & TAXABLE-EQUIVALENT YIELDS

1974 PERCENTAGE 1973 PERCENTAGE 1972 1974 1973 1972

(IN THOUSANDS) CHANGE (IN THOUSANDS) CHANGE (IN THOUSANDS) AMOUNT YIELD AMOUNT YIELD AMOUNT YIELD

INCOME FROM:(IN MILLIONS) (IN MILLIONS) (IN MILLIONS)

Loans and Leases $793,513 41.0% $562,725 60.8% $349,903 CASH AND DUE FROM BANKS $ 1,134 $ 984 $ 893

Investments 136,054 32.5 102,657 18.1 86,894 DEPOSITS PLACED BY OVERSEAS OFFICES 772 8.69% 963 6.39% 640 4.83%

Other Interest 78,479 11.6 70,302 111.2 33,291 INVESTMENT SECURITIES:

Total Income from Earning Assets 1.008,046 37.0 735,684 56.5 470,088U.S. Treasury Securities 239 6.58 346 5.96 341 5.64

LESS INTEREST EXPENSE:Securities of Other u.s. Government

Interest on DepositsAgencies and Corporations 610 6.85 444 6.35 232 5.48

520,442 41.6 367,592 69.6 216,689 Obligations of States and Political Subdivisions 760 9.09 594 7.46 715 7.20Interest on Borrowed Funds 155,728 43.9 108,228 350.3 24,032 Other Securities (Excluding Equity Investments) 116 8.15 130 7.36Interest on Long-Term Debt

62 5.6817,784 41.1 12,602 114.0 5,890 TRADING ACCOUNT SECURITIES 109 10.47 112 7.85 43 5.58

Total Interest Expense 693,954 42.1 488,422 98.1 246,611 FUNDS SOLD 148 9.34 32 7.94 59 4.92

NET INTEREST MARGIN 314,092 27.0 247,262 10.6 223,477 LOANS AND LEASES:

PLUS OTHER OPERATING INCOME 64,096 (3.1) 66,128 10.5 59,843 *Commercial Loans (Net of Overdrafts) 3,150 11.42 2,892 8.82 2,283 6.55

LESS OTHER OPERATING EXPENSE 267,638 21.6 220,091 10.8 198,667 *Real Estate Loans 2,100 8.31 1,738 7.79 1,393 7.44

INCOME BEFORE INCOME TAXES 110,550 18.5 93,299 10.2 84,653*Consumer Loans (Net of Unearned Discount) 988 11.51 787 10.23 579 10.07

INCOME TAXES ON A FULL-RATE BASIS 60,476 23.0 49,180 7.9 45,559Loans of Overseas Offices 941 11.91 807 9.65 421 7.13

INCOME BEFORE SECURITY GAINS OR LOSSES 50,074 13.5Direct Lease Financing 168 11.63 109 10.31 58 9.26

44,119 12.9 39,094 ALL OTHER ASSETS 556 431 334TOTAL $11,791 $10,369 $8,053

-"-'r--~.~."....... ,.... ...... -....... "-> 1 I ~ *Yields computed on an all-inclusive basis (including loan fees)._-:5.'-.-...... ~-.. ":-.. ~ ..........!~...... ~ .... - .... • j-~ •• _-_•• . . - .. .- .. - -

TABLE III • SOURCES OF FUNDS : AVERAGE BALANCES & RATES PAID1974 1973

Net loans written off to the reservefor loan losses during 1974 totaled $21.1

million compared to $10.9 million in1973 and $9.1 million in 1972. Thefollowing paragraphs discuss the lossesin the various loan categories.

For commercial loans, write-offs ineach of these years were: $10.6 million in1974, $6.5 million in 1973 and $6.2 million in 1972. The losses in 1974 were notconcentrated in any particular industry.Recently, there has been widespreadnews coverage of problems experiencedby real estate developers and companiesinvolved in real estate related activities.Wells Fargo & Company has unsecuredloans outstanding to real estate relatedcompanies and real estate investmenttrusts. These loans are included in commercialloans and loans of overseasoffices. Losses to date on these loanshave been minimal.

Net losses on monthly payment loanstotaled $4.5 million in 1974, $2 millionin 1973 and $1 million in 1972. Much ofthe increase in losses from 1973 to 1974

was attributable to a combination of50ft used car prices, a very slow mobilehome market and a practically nonexistent market for recreational vehiclesresulting in losses from resales ofrepossessed vehicles.

Income Before Securities Gains orLosses in Millions of Dollars

Dividends Declared During the Yearin Millions of Dollars

reserve during 1974. If economic conditions continue to deteriorate, it is likelythat the loan 1055 provision as well asthe net loan 1055 write-offs will increase.

As of any given date, Wells Fargo &Company, along with other financialinstitutions, has loans outstanding tocorporations which are experiencingvarying degrees of financial difficulty.Such loans, in the aggregate, usuallyexceed the valuation portion of thereserve for loan losses. The managementof the Company believes, however, thatthe valuation portion of the reserve forloan losses is adequate to cover anypotential losses.

INCOME AND DIVIDENDS

IIII

$SO

$ss

1969 1970 1971 1972 1973 1974

In 1974, the moving average formulaindicated a provision for loan losses of$15.2 million compared to $11 million in1973 and $7.9 million in 1972, but themanagement of the Company determinedthat the provision needed to be increasedby approximately $6.3 million because ofeconomic conditions and to fully providefor the net loan losses charged to the

TABLE IV· QUARTERLY HISTORY1972

INCOMEAMOUNT RATES

DIVIDENDS DIVIDENDSPER SHARE BEFOREPRICE OF THE STOCK*(IN MILLIONS) PAID

PAIDSECURITY GAINS NET INCOME DECLARED$ 2,136 OR LOSSES PER SHARE PER SHARE PER SHARE HIGH LOW END OF PERIOD

1,736 4.01%First Quarter -1973 $ .52 $ .52 $ .215 $ .215 $291/2 $22% $22%

902 5.34Second Quarter-1973 .57 .57 .215 .215 241/2 19% 23%

315 5.20Third Quarter -1973 .55 .55 .24 .215 243/1 20 23%

555 4.73Fourth Quarter-1973 .61 .57 .24 .24 26 20% 22%

1,062 5.31Fiscal-1973 $2.25 $2.21 $ .91 $ .885 $291/2 $19% $22%

3244 4.33

First Quarter $ $ .51 $ .24 $ .24 $27 $22% $25%-1974 .51545 4.38Second Quarter-1974 .66 .66 .24 .24 25% 15% 15%

126 4.68Third Quarter -1974 .62 .62 .24 .24 17% 101/4 101/4

348Fourth Quarter-1974 .74 .60 .24 .24 141/2 9% 13

$ 8,053 Fiscal-1974 $2.53 $2.39 $ .96 $ .96 $27 $ 9% $13

~Per closing quote on New York Stock Excl1nn!{e, the IJrincivn/mnrket itl 7Illtirl1 /1,0 <'M/' ;- "'-~-~

experience to the evaluations of outstanding loans made periodically byregulatory agencies, by an internalreview department of the Bank and byindependent certified accountants.Further, management's evaluation of theexisting loan portfolio takes into accountparticular credit exposure and economicconditions. Through this procedure,management independently assesses theadequacy of the loan 1055 reserve and ofthe related loan 1055 provision charged toexpense.

1969 1970 1971 1972 1973 1974

$22

$21

$20

$19

$18

$17

$16

$IS

$14

$13

$12

$11

$10

$9

$8

$7

Provision for Loan Losses IIin Millions of Dollars

Net Charge-offs IIin Millions of Dollars

To maintain the valuation portion ofthe reserve, the Company has since 1968

consistently followed an approvedregulatory formula which computes theminimum provision (or reserve addition)by multiplying average loans outstanding during the year by a five-year movingaverage ratio. The moving averageratio is derived by determining theaverage of actual net charge-offs duringthe most recent five years and dividingthis amount by the average of daily loanbalances for such period.

In addition to the formula computation, the management of the Companyreviews the actual loans charged offduring the previous six-year period andrelates the previous loan charge-off

. -- -- -=

PROVISION FOR LOSSES ON LOANS

AMOUNT RATES AMOUNT RATES

(IN MILLIONS) PAID (IN MILLIONS) PAID

DEMAND DEPOSITS $ 2,503 $ 2,342SAVINGS DEPOSITS 1,897 4.97% 1,739 4.63%SAVINGS CERTIFICATES 1,198 7.01 977 5.76CERTIFICATES OF DEPOSIT 1,272 10.49 733 8.41OTHER TIME DEPOSITS 525 9.11 593 6.77DEPOSITS IN OVERSEAS OFFICES 1,670 9.64 1,781 7.24OTHER LIABILITIES 494 356COMMERCIAL PAPER OUTSTANDING 115 10.65 52 8.33FUNDS BORROWED 1,433 10.01 1,197 8.68LONG-TERM DEBT 274 6.49 203 6.21STOCKHOLDERS' EQUITY 410 396

TOTAL $11,791 $10,369

professional services, and to a determinable 1055 of $1.5 million-half of a$3 million placement with BankhausI.D. Herstatt, Cologne, Germany, whichclosed in June. Wells Fargo expects torecover the remaining $1.5 million.

The differences in income tax expenseshown in Table I compared to the incometax expense shown in the Six-YearSummary of Operating Statements areprimarily related to the tax-exemptinterest income earned during the year.Tax-exempt interest income declined in1973 from the 1972 level, thereforethe effective tax rate, which is a ratio ofincome tax expense to income beforetaxes, of 31.2 per cent for 1973 washigher than the 1972 rate of 29.7 percent. Conversely, tax-exempt interestincome in 1974 increased over 1973,

which lowered the effective tax rate to26.5 per cent.

PROVISION FOR LOSSES ON LOANSThe reserve for loan losses, as shown onthe Consolidated Balance Sl1eet, has threecomponents: the valuation portion,deferred taxes and a contingency reserve.Only the valuation portion is availableat any given time to absorb potentialloan losses of the Company. At December 31, 1974, the valuation portion ofthe reserve totaled $51,687,000. It was$48,613,118 at the end of the previousyear and $48,527,095 at year-end 1972.

--'r ...._-."'=··~..·.... ""'"'· ...... ,·... 11 ...

_~ ~~5~ .,,"~ - ';_ _-_.

financial statements3.87%

4TH2ND 3RD

1974

3.41%

1ST4TH

improvement from the second quarter,but non-interest expenses rose notablydue to the Herstatt loss, more thanoffsetting the net interest increase anddecreasing the earnings per share forthe quarter below that of the secondquarter.

Early in the fourth quarter, depositand borrowed fund rates droppedquickly. The prime rate descended slowlyduring the quarter to 101/4 per cent atyear end. Because the prime laggedbehind borrowing rates, the spread in thefourth quarter was favorably affectedand increased 10 per cent over theprevious quarter. Earning assetsincreased by 4 per cent over the thirdquarter. Non-interest income rosemodestly from the previous quarter whilenon-interest expenses, principally theprovision for losses on loans, rosesignificantly in the final quarter. The endresult was a most satisfactory earningsperformance in the fourth quarter.

2ND 3RD

1973

3.53"/0 3.52%

11%

10%

9%

8%

7%

6%

5%

4%

3%

2%

1%

0%1ST

BIIIII

per cent and maintaining that level untilmid-March when it began to rise. Incomparing fourth quarter 1973 with firstquarter 1974, Wells Fargo's net taxableequivalent interest income wideneddue principally to lower funding costs.Non-interest income lagged, and noninterest expenses climbed sharply fromthe earlier period combining to more thannegate the effect on net income ofthe improved interest spread.

The second quarter was marked by aprecipitous rise in the prime rate. Atthe same time, earning assets and thespread between taxable-equivalent yieldsand rates paid increased moderatelyover the first quarter. In addition, noninterest income recovered from the lowlevels of the first quarter, and tightexpense controls limited increases in noninterest expenses. As a result, thesecond quarter produced better earningsthan the first quarter.

The prime rate stabilized at its all-timehigh of 12 per cent during the thirdquarter. Spreads, under considerablepressure, were improved, and togetherwith a modest increase in earning assetswidened the net taxable-equivalentinterest income over the second quarter.

._'7"~ ~"3-2'"": :--::j.:~~c~ :i~r"rnp ~h()"Yed no

YIELD AND RATES PAID BY QUARTER

Net Domestic Taxable Equivalent InterestIncome as a Percentage of Earning Assets

Taxable Equivalent Yield onDomestic Earning Assets

Pooled Cost of FundsSupporting these Earning Assets

SECURITY TRANSACTIONSSecurity transactions, net of the relatedincome tax effect, resulted in a loss of$2,705,000 in 1974, a loss of $660,000 in1973 and a gain of $338,000 in 1972.

The large increase in security losses in1974 resulted from a program adoptedby the Company to gradually sell offmunicipal bonds with maturities of morethan 10 years and relatively unattractive yields.

QUARTERLY REVIEW-1974In view of the extremes of change thatcharacterized the 1974 banking environment, it is especially relevant to retraceand examine the Company's performanceduring this period as shown in Table IV.In a climate of general uncertainty, theprime rate climbed to 12 per cent, anhistoric high. Serious problems at twolarge U. S. banking organizations causedconcern in the industry.

In the opening weeks of the year, theprime rate steadily moved downward,

Net losses on credit card loans were$4.9 million in 1974, $2.4 million in 1973

and $1.6 million in 1972. In 1973 and1974, the Company broadened its cardholder base. In the early stages of suchan expansion, loan losses predictablyincrease. Despite these increased losses,the overall program improved the profitability of the credit card operations.

Real estate loan losses were less than$50,000 in 1974 and 1973, and totaledabout $300,000 in 1972. These modestlosses came from a portfolio that nowtotals more than $2 billion in real estateloans outstanding, largely representing loans on single-family homes.

Losses on internationa110ans amountedto $1.1 million in 1974 and less than$100,000 in 1973 and 1972.

--T---.""'"· ~· ·~tt ....~ _..&#-. -.J _ ... • ~ ••

CONSOLIDATED SIX-YEAR SUMMARYOF OPERATING STATEMENTSWELLS FARGO & COMPANY AND SUBSIDIARIES (IN THOUSANDS)

ANALYSIS

CHANGE FIVE-YEARCOMPOUND

1974 1973 1972 1971 1970 1969 1974/1973 GROWTH RATE

INCOMEInterest and Fees on Loans and Leases $ 790,964 $ 560,618 $ 348,792 $ 298,997 $ 302,974 $ 265,501 41.1% 24.4%

Interest and Dividends on Investment Securities 101,016 80,224 60,874 56,693 47,328 49,116 25.9 15.5

Interest on Deposits Placed by Overseas Offices 67,072 61,516 30,893 25,873 13,653 5,922 9.0 62.5

Trading Account Income 7,979 7,680 2,499 5,376 5,364 663 3.9 64.5

Service Charges on Deposit Accounts 24,245 21,718 20,664 20,078 19,600 17,814 11.6 6.4

Trust Income 16,066 14,984 13,112 11,409 10,745 10,101 7.2 9.7

Other Income 22,820 26,876 24,747 20,368 11,987 11,153 (15.1) 15.4

Total Income 1,030,162 773,616 501,581 438,794 411,651 360,270 33.2 23.4

EXPENSESalaries $ 119,777 $ 106,324 $ 96,331 $ 86,967 $ 79,923 $ 68,599 12.7 11.8

Pension and Other Employee Benefits 26,764 22,642 21,196 17,153 15,224 13,306 18.2 15.0

Interest on Deposits, Borrowings, Capital Notes and Debentures 693,954 488,422 246,611 214,843 202,470 173,435 42.1 32.0

Net Occupancy Expense 28,393 23,721 19,663 17,851 15,104 12,966 19.7 17.0

Equipment Expense 17,063 15,329 13,030 11,010 9,925 8,114 11.3 16.0

Provision for Loan Losses 21,500 11,034 7,864 6,479 5,937 5,945 94.9 29.3

Other Expense 54,633 42,018 41,302 34,821 32,400 29,670 30.0 13.0

Total Expense 962,084 709,490 445,997 389,124 360,983 312,035 35.6 25.3

INCOME BEFORE INCOME TAXES AND SECURITY GAINS OR LOSSES 68,078 64,126 55,584 49,670 50,668 48,235 6.2 7.1

Applicable Income Taxes 18,004 20,007 16,490 15,318 18,084 16,188 (10.0) 2.2

INCOME BEFORE SECURITY GAINS OR LOSSES $ 50,074 $ 44,119 $ 39,094 $ 34,352 $ 32,584 $ 32,047 13.5 9.3Security Gains (Losses) (5,981) (1,439) 735 (10,383) 325 (44)

Related (Increase) Reduction of Income Taxes 3,276 779 (397) 5,416 (178) 25

Net Income $ 47,369 $ 43,459 $ 39,432 $ 29,385 $ 32,731 $ 32,028 9.0 8.1

INCOME PER SHAREIncome before Security Gains or Losses $2.53 $2.25 $2.10 $1.85 $1.77 $1.75 12.4 7.7

Net Income $2.39 $2.21 $2.12 $1.58 $1.78 $1.75 8.1 6.4

INCOME PER SHARE ASSUMING FULL DILUTIONIncome before Security Gains or Losses $2.46 $2.18 $2.03 $1.79 $1.71 $1.69 12.8 7.8

Net Income $2.33 $2.15 $2.05 $1.54 $1.72 $1.69 8.4 6.6

AVERAGE SHARES OUTSTANDING 19,804,343 19,633,968 18,643,285 18,543,162 18,421,480 18,283,778

203,486 274,814 (71,328)551,460 622,711 (71,251)

805,823 594,149 211,674

176,326 178,119 (1,793)

1,737,095 1,669,793 67,302

86,597 222,655 (136,058)479,592 102,900 376,692

3,359,327 3,179,062 180,2652,237,841 1,966,527 271,314

~

1,171,231 960,309 210,9221,059,613 908,352 151,261

237,700 125,118 112,582

8,065,712 7,139,368 926,344

128,054 118,647 9,407153,048 53,876 99,172149,629 124,744 24,885138,287 103,825 34,462

$12,675,123 $11,767,725 $907,398

CONSOLIDATED'BALANCE SHEETSASSETS (IN THOUSANDS)

Cash and Due from BanksDeposits Placed by Overseas Offices

Investment Securities:U.S. Treasury Securities

Securities of Other u.s. Government Agencies and CorporationsObligations of States and Political SubdivisionsOther Securities

Total Investment Securities

Trading Account SecuritiesFunds Sold

Loans and Direct Lease Financing:Commercial LoansReal Estate LoansConsumer LoansLoans of Overseas OfficesDirect Lease Financing

Total Loans and Direct Lease Financing

Premises and EquipmentCustomers' Acceptance LiabilityAccrued Interest ReceivableOther Assets

Total Assets

The accompanying notes are an integral part of these statements.

DECEMBER 31,1974

$ 1,238,589498,520

DECEMBER 31,1973

$ 1,164,5341,067,383

CHANGE

$ 74,055(568,863)

LIABILITIES AND STOCKHOLDERS' EQUITY (IN THOUSANDS)

Demand DepositsSavings DepositsSavings CertificatesCertificates of Deposit

Other Time DepositsDeposits in Overseas Offices

Total Deposits

Funds Borrowed

Commercial Paper OutstandingAcceptances OutstandingAccrued Taxes and Other ExpensesUnearned DiscountOther Liabilities

Reserve for Loan LossesLong-Term Debt:41/2 % Capital Notes of Wells Fargo Bank, N.A., due 1989

31/4 % Convertible Capital Notes, due 1989Debentures, Notes and Mortgages

Total Long-Term Debt

Stockholders' Equity:

Common Stock-$5 par value, authorized 30,000,000 shares,outstanding 20,010,109 shares on December 31,1974 and19,651,229 on December 31, 1973

Capital SurplusRetained Earnings

Total Stockholders' Equity

Total Liabilities and Stockholders' Equity

The accompanying notes are an integral part of these statements.

DECEMBER 31, DECEMBER 31,1974 1973 CHANGE

$ 2,724,560 $ 2,910,240 $(185,680)

2,005,727 1,782,181 223,546

1,311,889 1,020,201 291,688

1,894,209 775,159 1,119,050

431,885 554,889 (123,004)

1,372,020 1,974,224 (602,204)

9,740,290 9,016,894 723,396

1,395,613 1,540,802 (145,189)

179,474 60,545 118,929

153,787 53,876 99,911

147,365 106,488 40,877

106,628 90,928 15,700

130,882 120,504 10,378

116,322 113,248 3,074

50,000 50,000

18,902 20,930 (2,028)

210,138 200,736 9,402

279,040 271,666 7,374

100,050 98,256 1,794

186,504 184,483 2,021

139,168 110,035 29,133

425,722 392,774 32,948

$12,675,123 $11,767,725 $ 907,398

FOR THE TWO YEARS ENDED DECEMBER 31, 1974 (IN THOUSANDS)

CONSOLIDATED STATEMENTS OF STOCKHOLDERS' EQUITY

CONSOLIDATED STATEMENTS OF INCOME(IN THOUSANDS)

YEAR ENDED YEAR ENDEDDECEMBER 31, DECEMBER 31,

1974 1973 CHANGE

INCOMEInterest and Fees on Loans and Leases $ 790,964 $560,618 $230,346Interest and Dividends on Investment Securities:

U.s. Treasury Securities 15,726 20,594 (4,868)Securities of Other u.s. Government

Agencies and Corporations 41,783 28,216 13,567Obligations of States and Political Subdivisions 34,051 21,851 12,200Other Securities 9,456 9,563 (107)

Interest on Deposits Placed by Overseas Offices 67,072 61,516 5,556Trading Account Income:

Interest 7,258 6,617 641Profits 721 1,063 (342)

Trust Income 16,066 14,984 1,082Service Charges on Deposit Accounts 24,245 21,718 2,527Other Income 22,820 26,876 (4,056)

Total Income 1,030,162 773,616 256,546

EXPENSESalaries 119,777 106,324 13,453Pension and Other Employee Benefits 26,764 22,642 4,122Interest on Deposits 520,442 367,592 152,850Interest on Borrowed Money 155,728 108,228 47,500Interest on Long-Term Debt 17,784 12,602 5,182Net Occupancy Expense 28,393 23,721 4,672Equipment Expense 17,063 15,329 1,734Provision for Losses on Loans 21,500 11,034 10,466Other Expense 54,633 42,018 12,615

Total Expense 962,084 709,490 252,594

INCOME BEFORE INCOME TAXES ANDSECURITY LOSSES 68,078 64,126 3,952Less Applicable Income Taxes 18,004 20,007 (2,003)

-INCOME BEFORE SECURITY LOSSES $ 50,074 $ 44,119 $ 5,955Security Losses Less Related Reduction of Income

Taxes of $3,276 and $779 (2,705) (660) (2,045)

Net Income $ 47,369 $ 43,459 $ 3,910

INCOME PER SHAREIncome before Security Losses $2.53 $2.25 $ .28Security Losses, Net of Tax (.14) (.04) (.10)

Net Income $2.39 $2.21 $ .18

INCOME PER SHARE ASSUMING FULL DILUTIONIncome before Security Losses $2.46 $2.18 $ .28Security Losses, Net of Tax (.13) (.03) (.10)

Net Income $2.33 $2.15 $ .18

The accompanying notes are an integral part of these statements.

COMMON CAPITALSTOCK SURPLUS

BALANCE DECEMBER 31, 1972 $ 97,790 $181,452

Net Income-1973Conversion of Convertible Notes 274 1,344

Stock Issued in Exchange forStock of Grayco Land Escrow Ltd. 192

Cash Dividends DeclaredProvision for Losses on Loans, Exclusive of Portion

Charged Against Income, LessRelated Income Tax Effect $(9,720)

Proceeds from Issuance of WarrantsAttached to Deutsche Mark Debentures 1,746

Other-Net of Tax (59)

Net Increase (Decrease) 466 3,031

BALANCE DECEMBER 31, 1973 $ 98,256 $184,483

Net Income-1974Conversion of Convertible Notes 343 1,684

Stock Issued in Exchange for Stockof Commercial National Bank 1,451 389

Cash Dividends DeclaredOther-Net of Tax (52)

Net Increase (Decrease) 1,794 2,021

BALANCE DECEMBER 31, 1974 $100,050 $186,504

The accompanying notes are an integral part of these statements.

RETAINEDEARNINGS

$100,464

43,459

62(17,870)

(15,880)

(200)

9,571

$110,035

47,369

536(19,059)

287

29,133

$139,168

TOTALSTOCK-

HOLDERS'EQUITY

$379,706

43,4591,618

254(17,870)

(15,880)

1,746(259)

13,068

$392,774

47,3692,027

2,376

(19,059)235

32,948

$425,722

I,

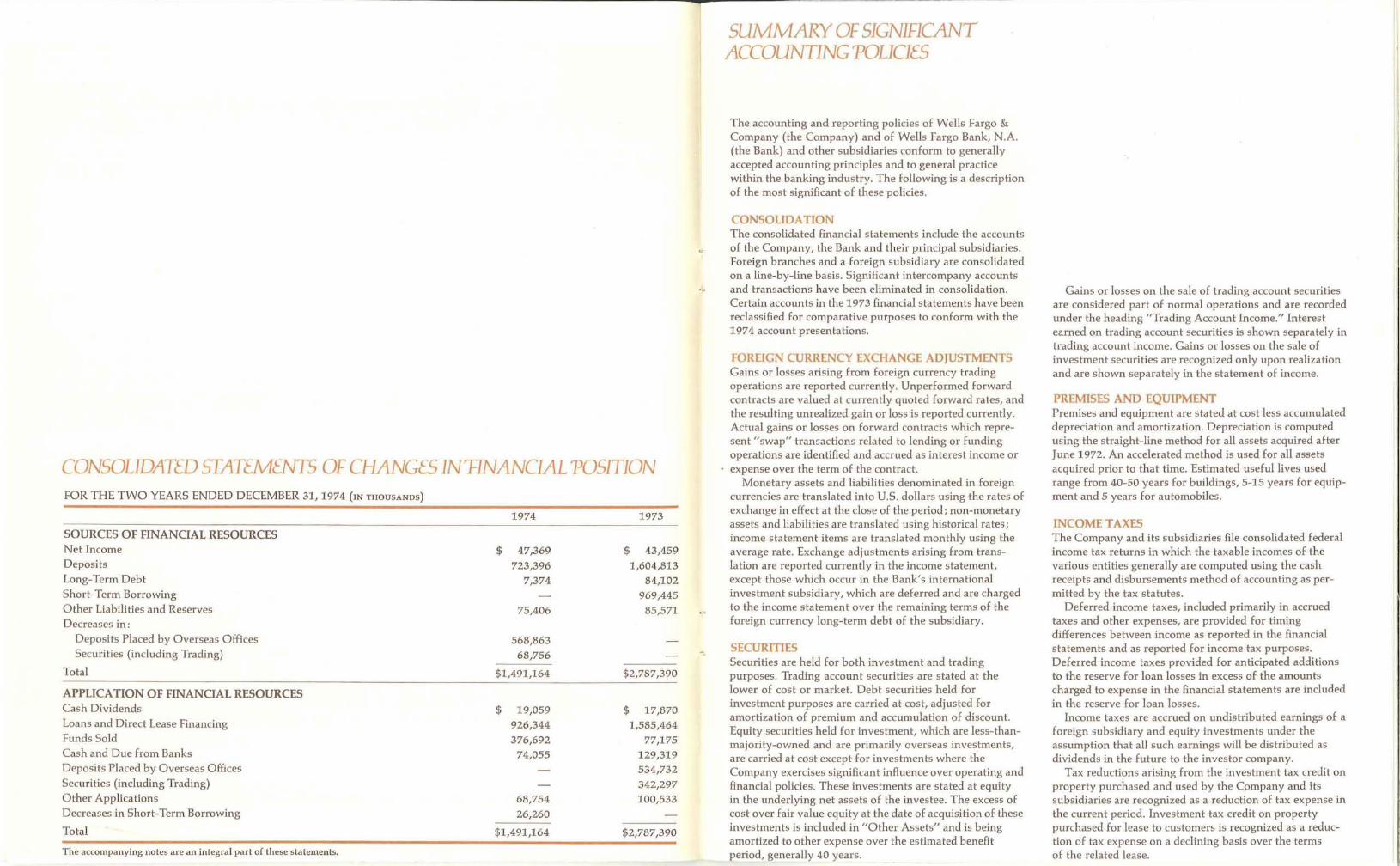

CONSOLIDATED STATEMENTS OF CHANGES IN'FINANCIAL POSITIONFOR THE TWO YEARS ENDED DECEMBER 31, 1974 (IN THOUSANDS)

SOURCES OF FINANCIAL RESOURCESNet IncomeDepositsLong-Term DebtShort-Term BorrowingOther Liabilities and ReservesDecreases in:

Deposits Placed by Overseas OfficesSecuri ties (including Trading)

Total

APPLICATION OF FINANCIAL RESOURCESCash DividendsLoans and Direct Lease FinancingFunds SoldCash and Due from BanksDeposits Placed by Overseas OfficesSecurities (including Trading)Other ApplicationsDecreases in Short-Term Borrowing

Total

The accompanying notes are an integral part of these statements.

1974

$ 47,369

723,396

7,374

75,406

568,863

68,756

$1,491,164

$ 19,059

926,344

376,692

74,055

68,754

26,260

$1,491,164

1973

$ 43,459

1,604,813

84,102

969,445

85,571

$2,787,390

$ 17,870

1,585,464

77,175

129,319

534,732

342,297

100,533

$2,787,390

SUMMARY OFSIGNIFICANTACCOUNTING POLICIES

The accounting and reporting policies of Wells Fargo &Company (the Company) and of Wells Fargo Bank, N.A.(the Bank) and other subsidiaries conform to generallyaccepted accounting principles and to general practicewithin the banking industry. The following is a descriptionof the most significant of these policies.

CONSOLIDATIONThe consolidated financial statements include the accountsof the Company, the Bank and their principal subsidiaries.Foreign branches and a foreign subsidiary are consolidatedon a line-by-line basis. Significant intercompany accountsand transactions have been eliminated in consolidation.Certain accounts in the 1973 financial statements have beenreclassified for comparative purposes to conform with the1974 account presentations.

FOREIGN CURRENCY EXCHANGE ADJUSTMENTSGains or losses arising from foreign currency tradingoperations are reported currently. Unperformed forwardcontracts are valued at currently quoted forward rates, andthe resulting unrealized gain or loss is reported currently.Actual gains or losses on forward contracts which represent "swap" transactions related to lending or fundingoperations are identified and accrued as interest income orexpense over the term of the contract.

Monetary assets and liabilities denominated in foreigncurrencies are translated into U.s. dollars using the rates ofexchange in effect at the close of the period; non-monetaryassets and liabilities are translated using historical rates;income statement items are translated monthly using theaverage rate. Exchange adjustments arising from translation are reported currently in the income statement,except those which occur in the Bank's internationalinvestment subsidiary, which are deferred and are chargedto the income statement over the remaining terms of theforeign currency long-term debt of the subsidiary.

SECURITIESSecurities are held for both investment and tradingpurposes. Trading account securities are stated at thelower of cost or market. Debt securities held forinvestment purposes are carried at cost, adjusted foramortization of premium and accumulation of discount.Equity securities held for investment, which are less-thanmajority-owned and are primarily overseas investments,are carried at cost except for investments where theCompany exercises significant influence over operating andfinancial policies. These investments are stated at equityin the underlying net assets of the investee. The excess ofcost over fair value equity at the date of acquisition of theseinvestments is included in "Other Assets" and is beingamortized to other expense over the estimated benefitperiod, generally 40 years.

Gains or losses on the sale of trading account securitiesare considered part of normal operations and are recordedunder the heading "Trading Account Income." Interestearned on trading account securities is shown separately intrading account income. Gains or losses on the sale ofinvestment securities are recognized only upon realizationand are shown separately in the statement of income.

PREMISES AND EQUIPMENTPremises and equipment are stated at cost less accumulateddepreciation and amortization. Depreciation is computedusing the straight-line method for all assets acquired afterJune 1972. An accelerated method is used for all assetsacquired prior to that time. Estimated useful lives usedrange from 40-50 years for buildings, 5-15 years for equipment and 5 years for automobiles.

INCOME TAXESThe Company and its subsidiaries file consolidated federalincome tax returns in which the taxable incomes of thevarious entities generally are computed using the cashreceipts and disbursements method of accounting as permitted by the tax statutes.

Deferred income taxes, included primarily in accruedtaxes and other expenses, are provided for timingdifferences between income as reported in the financialstatements and as reported for income tax purposes.Deferred income taxes provided for anticipated additionsto the reserve for loan losses in excess of the amountscharged to expense in the financial statements are includedin the reserve for loan losses.

Income taxes are accrued on undistributed earnings of aforeign subsidiary and equity investments under theassumption that all such earnings will be distributed asdividends in the future to the investor company.

Tax reductions arising from the investment tax credit onproperty purchased and used by the Company and itssubsidiaries are recognized as a reduction of tax expense inthe current period. Investment tax credit on propertypurchased for lease to customers is recognized as a reduction of tax expense on a declining basis over the termsof the related lease.

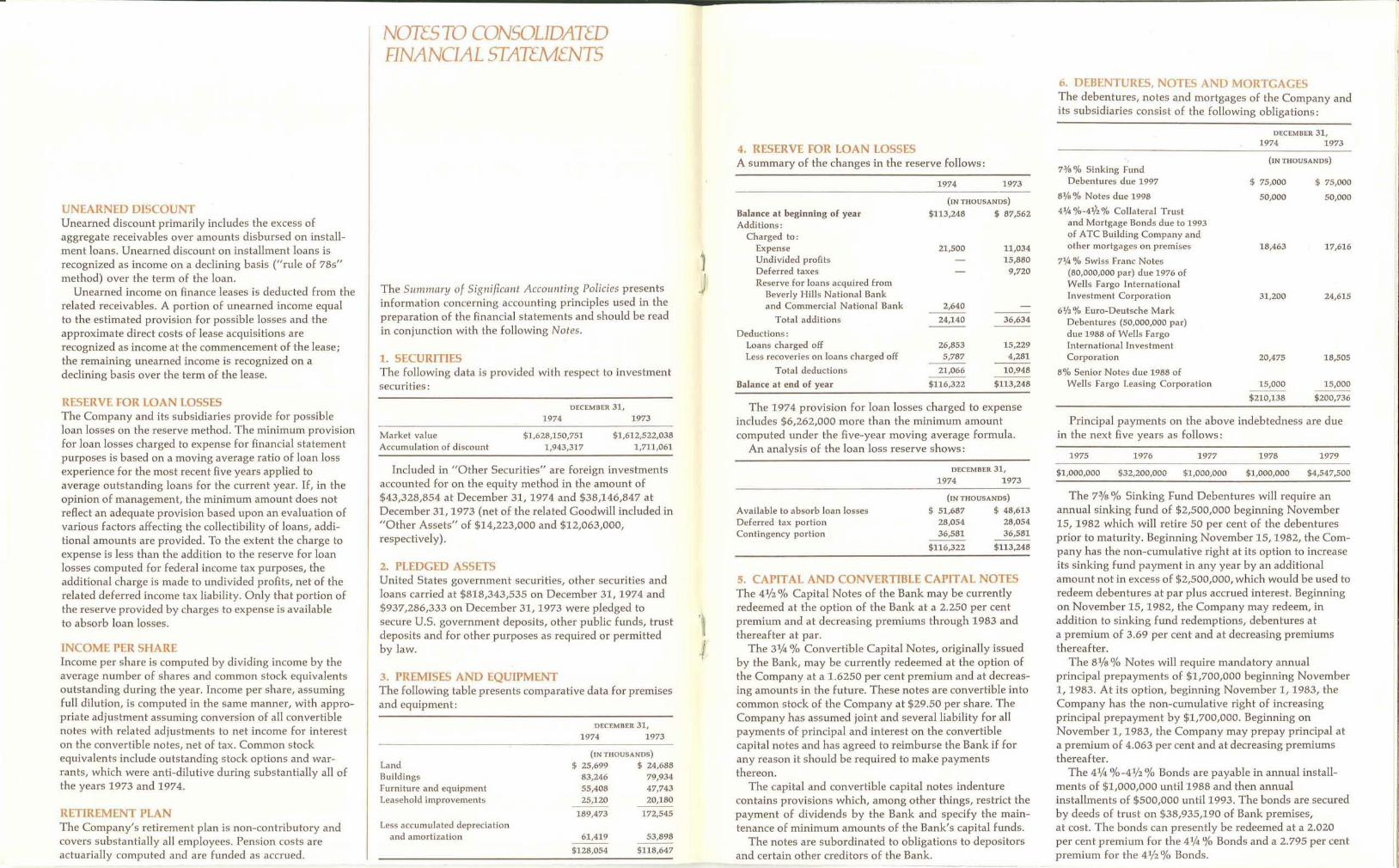

NOTES TO CONSOLIDATEDFINANCIAL STATEMENTS

6. DEBENTURES, NOTES AND MORTGAGESThe debentures, notes and mortgages of the Company andits subsidiaries consist of the following obligations:

1. SECURITIESThe following data is provided with respect to investmentsecurities:

3. PREMISES AND EQUIPMENTThe following table presents comparative data for premisesand equipment:

The Summary of Significant Accounting Policies presentsinformation concerning accounting principles used in thepreparation of the financial statements and should be readin conjunction with the following Notes.

24,615

17,616

18,505

1979

$ 75,000

50,000

15,000

$200,736