title / divider screen title - ifrsmedia.ifrs.org/2015/iasb/april/itcg_meeting_21042015_am/full set...

TRANSCRIPT

The views expressed in this presentation are those of the presenter,

not necessarily those of the IASB or IFRS Foundation.

International Financial Reporting Standards

ITCG Meeting Tuesday 21 April 2015

April 2015

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

* IFRS Taxonomy is a trade mark of the IFRS Foundation

October 2014

The views expressed in this presentation are those of the presenter,

not necessarily those of the IASB or IFRS Foundation.

International Financial Reporting Standards

Update on activities Disclosure Initiative including the IFRS

Taxonomy

April 2015

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Kristy Robinson – Technical Principal

* IFRS Taxonomy is a trade mark of the IFRS Foundation

October 2014

Agenda Paper 1

• To update members of the ITCG on the Disclosure

Initiative and IFRS Taxonomy developments

• Providing you with an opportunity to answer any

questions you may have

• Giving some background for our discussion today on the

IFRS Taxonomy roadmap and strategy

Aim of this agenda topic

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

3

• The Disclosure Initiative

• Upcoming IFRS Taxonomy releases

• IFRS Taxonomy due process

• Jurisdictional Profiles – access and filing requirements

Note: Appendix 1 lists other areas which may be of interest to you but

which are not discussed in detail today

Agenda

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

4

International Financial Reporting Standards

The views expressed in this presentation are those of the presenter,

not necessarily those of the IASB or IFRS Foundation

The Disclosure Initiative

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

April 2015

Why a project? What is the disclosure problem?

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

6

Disclosure problem

Not enough relevant

information

Too much irrelevant

information (overload)

Poor communication

Disclosure Initiative:

improve the effectiveness of disclosures

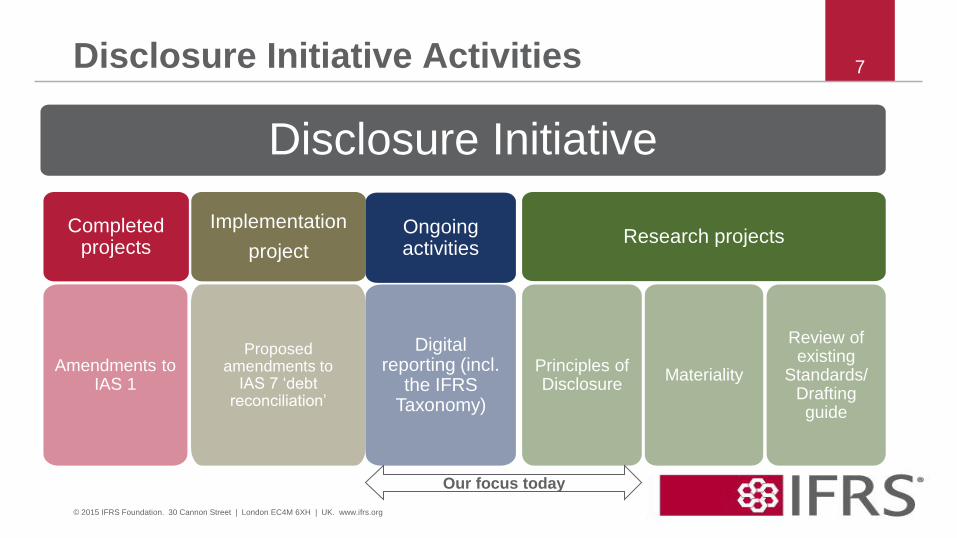

Disclosure Initiative

Completed projects

Amendments to IAS 1

Ongoing activities

Digital reporting (incl.

the IFRS Taxonomy)

Implementation

project Research projects

Principles of Disclosure

Materiality

Review of existing

Standards/ Drafting guide

Proposed amendments to

IAS 7 ‘debt reconciliation’

Disclosure Initiative Activities

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

7

Our focus today

Why

•Requests for the IASB to develop presentation and disclosure principles that apply across IFRS

•A better ‘disclosure framework’ in IFRS will result in improved disclosures because it will help:

•the IASB set better disclosure requirements in IFRS; and

•entities to make better judgements about what information to disclose and how

Output

•Discussion Paper

•Overall principles and specific issues

•Ultimate goal is to produce a disclosure Standard (IFRS) dealing with the basic structure and content of financial statements

•Redevelop parts of IAS 1 Presentation of financial statements and IAS 8 Accounting policies, changes in accounting estimates and errors

•Education guidance – communication/formatting

Principles of Disclosure (POD) project

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

8

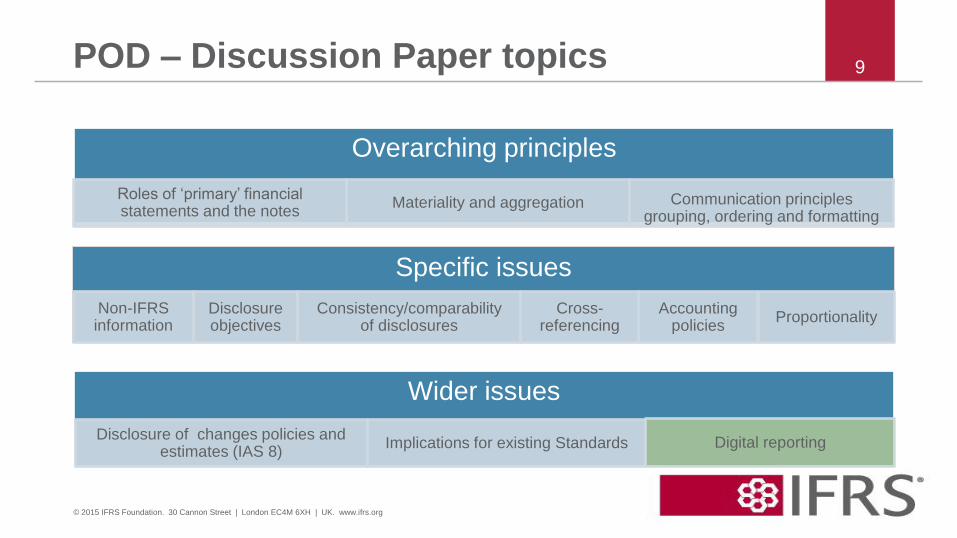

Specific issues

POD – Discussion Paper topics

Wider issues

Non-IFRS information

Disclosure of changes policies and estimates (IAS 8)

Implications for existing Standards Digital reporting

Disclosure objectives

Consistency/comparability of disclosures

Cross-referencing

Accounting policies

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

9

Proportionality

Overarching principles

Roles of ‘primary’ financial statements and the notes

Materiality and aggregation

Communication principles grouping, ordering and formatting

International Financial Reporting Standards

The views expressed in this presentation are those of the presenter,

not necessarily those of the IASB or IFRS Foundation

Upcoming IFRS Taxonomy releases

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

April 2015

IFRSs impacting the IFRS Taxonomy in 2015/2016

Topic IASB due

process stage

Expected publication

date

Impact on

the IFRS

Taxonomy

IFRS for SMEs review IFRS Q2 2015 significant

Leases IFRS H2 2015 significant

Insurance Contracts IFRS 2015/2016 significant

Amendments to IAS 7 Statement of

Cash Flows

ED Public consultation until

17 April 2015

limited

Macro Hedge Accounting Comment letter

analysis

TBC significant

Rate-regulated Activities Comment letter

analysis

TBC significant

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

11

IFRS Taxonomy common practice content

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Project scope Due process stage Expected publication

date

Impact on the

IFRS Taxonomy

utilities

information technology

media

chemicals

Review by IASB Board

Member panel

Proposed TU Q2 2015

TU Q3 2015

significant

retail

Research Proposed TU Q4 2015 analysis in

progress

2015/2016 common

practice – TBC

Project evaluation TBC TBC

TU stands for Taxonomy Update

12

International Financial Reporting Standards

The views expressed in this presentation are those of the presenter,

not necessarily those of the IASB or IFRS Foundation

IFRS Taxonomy due process

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

April 2015

• In summary, the proposed changes are: – review and approval by the IASB of updates to the Taxonomy

– a [Proposed] Taxonomy Update is the primary consultation

document that accompanies and is published at the same time

as the Exposure Draft of final Standard

• Staff Analysis of Comments on IAS 7 has just started

Content reflecting the Standards (trial 1)

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

14

• This trial incorporates two processes: – initiation of a new common practice project

– additions or amendments to common practice content

• At the December 2014 ITCG call, most of you agreed that a

clear definition of the scope of the IASB’s involvement is

needed to minimise IASB resource impact and to reduce

risks where common practice may be perceived as

authoritative

Common practice (trial 2)

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

15

• The IASB considers ‘peer review by a Board Member Panel’

as the optimal way to mitigate the above risks while at the

same time providing the required assurance that the content

of the IFRS Taxonomy is consistent with IFRSs – the common practice due process trial will proceed on that

basis and is expected to be completed at the end of May

• Appendix 2 describes the process in more depth

Common practice (trial 2) – cont’d

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

16

International Financial Reporting Standards

The views expressed in this presentation are those of the presenter,

not necessarily those of the IASB or IFRS Foundation

Jurisdictional Profiles

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

April 2015

• Developing 40 jurisdictional profiles: – Asia-Oceania:17, Europe:17, Americas: 4 and Africa: 2

– 30 jurisdictions indicate either using or having a concrete plan

to use XBRL as well as IFRS Taxonomy

• Extent of use of XBRL varies from jurisdiction to jurisdiction – Solely for one purpose (eg Stock Exchange)

– Multi-purpose information centre

– Annual reports by listed companies are usually filed using IFRS

Taxonomy; tax return and filings by SMEs are filed using locally

developed taxonomy.

Progress to date

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

18

• First profiles will be released in the first week of June

• Available on website, in PDF as well as in a more interactive

digital format (tentative)

• Further actions – Develop profiles for other jurisdictions

– Update information of developed profiles

– European Transparency Directive

– Rapid development of electronic filing worldwide

Public launch

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

19

International Financial Reporting Standards

The views expressed in this presentation are those of the presenter,

not necessarily those of the IASB or IFRS Foundation

Appendix 1 Other areas of interest

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

April 2015

IFRS Taxonomy translations

• Optional translations • the IFRS documentation labels : so far no translations have

been received

• From 2015, an additional option for users to filter on the specific

IFRS Taxonomy module they require (ifrs-full, ifrs-smes, ifrs-

mc)

• Other user requirements we know of • Versioned IFRS Taxonomy Illustrated in foreign languages

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

21

Available translations – IFRS Taxonomy

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

WIP – work in progress (requests received and files have been sent out)

Language Latest before 2012 2012 2013 2014

Arabic 2011 X X X

Chinese, simplified 2009

Chinese, traditional 2010

Dutch 2009

French 2009

German 2009

Hungarian 2006 X Q2 2015

Italian 2011 WIP

Japanese 2011 X X X

Korean 2011 X X X

Portuguese (Portugal) 2006

Slovak NA

Spanish 2011 X X X

Ukrainian NA X X WIP

Turkish NA WIP

Total: 6 5 4

22

• At the October 2014 ITCG meeting, we told you that we are

planning to: – review and update the existing terms and conditions for using

the IFRS Taxonomy Materials and ask for explicit acceptance

• A draft has been prepared by the staff, and we will ask for

your review prior to finalising them

• We are hoping to publish the new terms and conditions

towards end Q2 2015

Terms and conditions

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

23

International Financial Reporting Standards

The views expressed in this presentation are those of the presenter,

not necessarily those of the IASB or IFRS Foundation

Appendix 2 The proposed IFRS Taxonomy due

process for common practice

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

April 2015

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

25

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

26

Thank you

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

27

The views expressed in this presentation are those of the presenter,

not necessarily those of the IASB or IFRS Foundation.

International Financial Reporting Standards

Update on adoption of the IFRS Taxonomy by regulators

April 2015

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

* IFRS Taxonomy is a trade mark of the IFRS Foundation

October 2014

Agenda Paper 2

The views expressed in this presentation are those of the presenter,

not necessarily those of the IASB or IFRS Foundation.

International Financial Reporting Standards

The IFRS Taxonomy roadmap and strategy

April 2015

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Rita Ogun-Clijmans

Senior Technical Manager

October 2014

Agenda Paper 3

• To inform you of the activities we are planning for the

next twelve months and to ask for your guidance on

specific issues

• To have some initial idea sharing on the broader

strategic vision of the IASBs digital reporting activities

Aims of this agenda topic

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

30

International Financial Reporting Standards

The views expressed in this presentation are those of the presenter,

not necessarily those of the IASB or IFRS Foundation

The roadmap for the next six months

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

April 2015

Our focus for the next six months

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

IFRS Taxonomy

due process

IFRS Taxonomy

content

Management of entity-specific

disclosures

Supporting regulators

32

2015/2016

common

practice?

activities we

should

undertake?

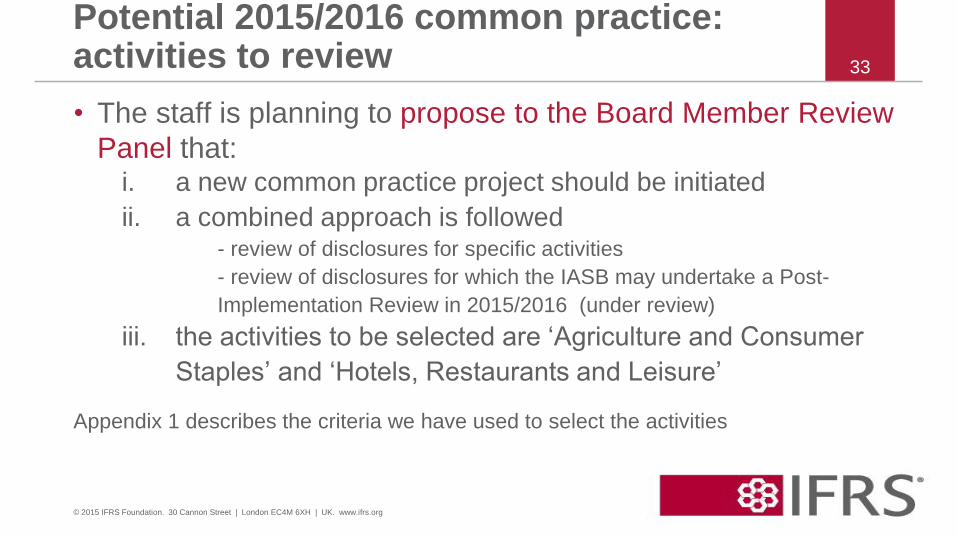

• The staff is planning to propose to the Board Member Review

Panel that: i. a new common practice project should be initiated

ii. a combined approach is followed - review of disclosures for specific activities

- review of disclosures for which the IASB may undertake a Post-

Implementation Review in 2015/2016 (under review)

iii. the activities to be selected are ‘Agriculture and Consumer

Staples’ and ‘Hotels, Restaurants and Leisure’

Appendix 1 describes the criteria we have used to select the activities

Potential 2015/2016 common practice: activities to review

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

33

• responding to the needs of regulators will remain our primary

focus in 2015: – they are currently the key users of the IFRS Taxonomy

– they play an essential role in the setting up of electronic filing

systems

– preparers will only fully engage when they will be required to

produce an electronic filing using the IFRS Taxonomy

– investors will only fully engage when there is a critical mass of

data that they ‘trust’ and can ‘try out’

Supporting regulators

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

34

Outreach

Supporting best use of the IFRS Taxonomy

Supporting regulators: activities

Thought leadership

Regional IFRS Taxonomy events and workshops

Management of entity specific disclosures POD Digital reporting

ITCG

Encouraging regular updates (today)

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

35

Guidance for regulators

Adaptable IFRS Taxonomy

Documentation & supporting materials

Common practice participation

Terms and conditions of use

Public consultation Regular meetings

• At the February ITCG call, most of you agreed with the staff

proposal to follow a combined approach for a potential

2015/2016 common practice project. Today, we would like

your views on the activities we are proposing. Do you agree

with our proposals and the criteria we have applied?

• Do you think that our current or planned activities will provide

effective support to regulators? Are there any other general

areas we should concentrate on?

Questions to the ITCG

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

36

International Financial Reporting Standards

The views expressed in this presentation are those of the presenter,

not necessarily those of the IASB or IFRS Foundation

Future focus areas for the IFRS Taxonomy team

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

April 2015

Future focus areas

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

IFRS Taxonomy data structure Organisation • Examples of activities: abstract and logical data modelling, taxonomy

simplification (duplicate dimensions, elements, …) ...

Improvements Ease of use • Examples of activities: review of the taxonomy modularisation, flexible views,

new navigation codes for elements, review of element naming scheme ….

Investors and preparers Outreach • Examples of activities: educational workshops, implementation guides,

involvement of industry groups within common practice, demonstrate how the IFRS Taxonomy can facilitate investment analysis, ….

38

• What are your experiences using the IFRS Taxonomy? Are

there other areas or activities that you think we should

consider?

Question to the ITCG

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

39

International Financial Reporting Standards

The views expressed in this presentation are those of the presenter,

not necessarily those of the IASB or IFRS Foundation

IASB digital reporting strategy

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

April 2015

• The IFRS Foundation recognises that technology is

influencing and changing the way IFRS disclosures are

disseminated by preparers and accessed by users.

• The upcoming Trustee’s review of the structure and

effectiveness of the IFRS Foundation may incorporate

specific questions on this topic.

Role of technology

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

41

As the body responsible for IFRS, our role is to develop a high quality IFRS Taxonomy

that jurisdictions such as Korea can incorporate into their own digital reporting

activities. The IFRS Taxonomy is critical to us achieving our goal of high quality

standards, applied on a globally consistent basis, and, importantly, regardless of

format.

We recently made the strategic decision to align the development of the IFRS

Taxonomy more closely with our standard-setting activities. As a consequence of this

change, digital reporting is considered by the IASB’s technical staff throughout the

project lifecycle, rather than only at the end as an alternative form of presentation. This

also means that Board members are more directly involved in the development of the

IFRS Taxonomy and we are encouraging our constituents to do the same.

http://www.ifrs.org/Alerts/Conference/Documents/2015/Speech-Hans-Mind-the-Gap-speech-Korea-

March-2015.pdf

Current activities and focus

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

42

• Can technology impact the relevance of the IFRS Taxonomy

and IFRSs? If so, how?

• Are these impacts risks or opportunities, and what can we do

to mitigate or exploit them?

Do you have any other ideas or views you would like to share

with us at this time?

And the future?

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

43

International Financial Reporting Standards

The views expressed in this presentation are those of the presenter,

not necessarily those of the IASB or IFRS Foundation

Appendix 1 Criteria and process followed to select

2015/2016 CP activities

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

April 2015

Overview

Empirical analysis of IFRS filers (listed companies)

• Number of companies

• Investor interest - market value of companies

• Size – revenue of companies

Other considerations

• Estimated impact of new IFRSs or IFRSs being

developed upon the disclosures for specific activities

• Do we anticipate significant common practice?

45

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Activity Aggrega

te

ranking

Number

ranking

MV

ranking

Revenue

ranking

Agricultural products and consumer

staples

1 1 1 2

Machinery incl Heavy Trucks 2 2 3 6

Automobiles and Components 3 11 2 1

Construction and Engineering 4 3 9 3

Hotels, Restaurants and Leisure 5 4 6 8

Industrial Conglomerates 6 20 5 4

Empirical analysis

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

46

Other considerations

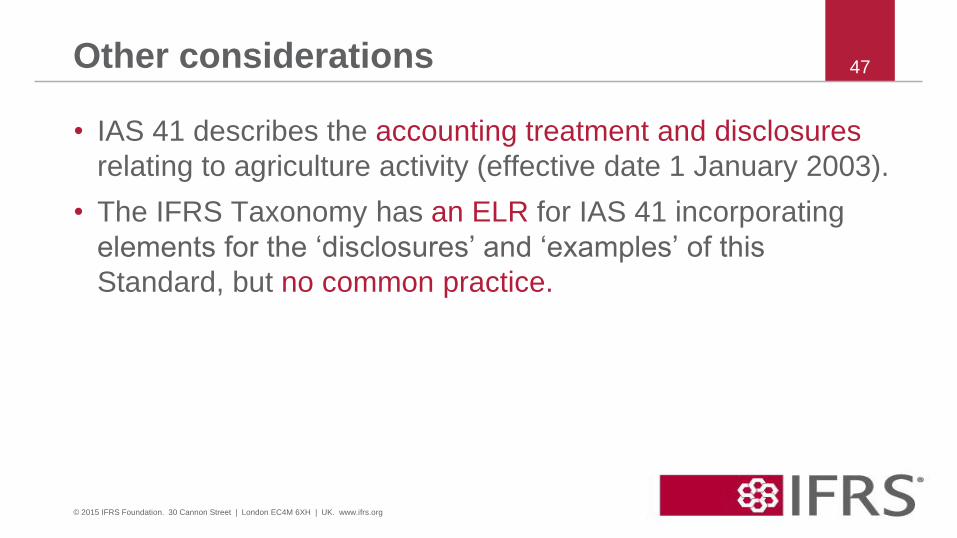

• IAS 41 describes the accounting treatment and disclosures

relating to agriculture activity (effective date 1 January 2003).

• The IFRS Taxonomy has an ELR for IAS 41 incorporating

elements for the ‘disclosures’ and ‘examples’ of this

Standard, but no common practice.

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

47

Other considerations : potential impact of new IFRS

• Construction and Engineering – IFRS 15 Revenue from Contracts with Customers (effective 1

January 2017) is likely to affect common practice disclosed

• Automobiles and Components – Entities generally have an industrial and financing arm

– As such, the new Leases standard and IFRS 15 is likely to

affect common practice disclosed

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

48

Dow we anticipate significant common practice for this activity?

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

49

• Difficult to anticipate without empirical analysis

• Review of other taxonomies and templates used by data

aggregators – the US GAAP Taxonomy has specific disclosures for

franchisors and entertainment

– some data aggregators have elements to reflect disclosures

specifically to hotels

=> review of Hotels, Restaurants and Leisure may be of interest

Thank you

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

50

The views expressed in this presentation are those of the presenter,

not necessarily those of the IASB or IFRS Foundation.

International Financial Reporting Standards

Management of entity specific disclosures – next

steps Andromeda Wood – Senior Technical Manager

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

April 2015 Agenda Paper 4

Agenda

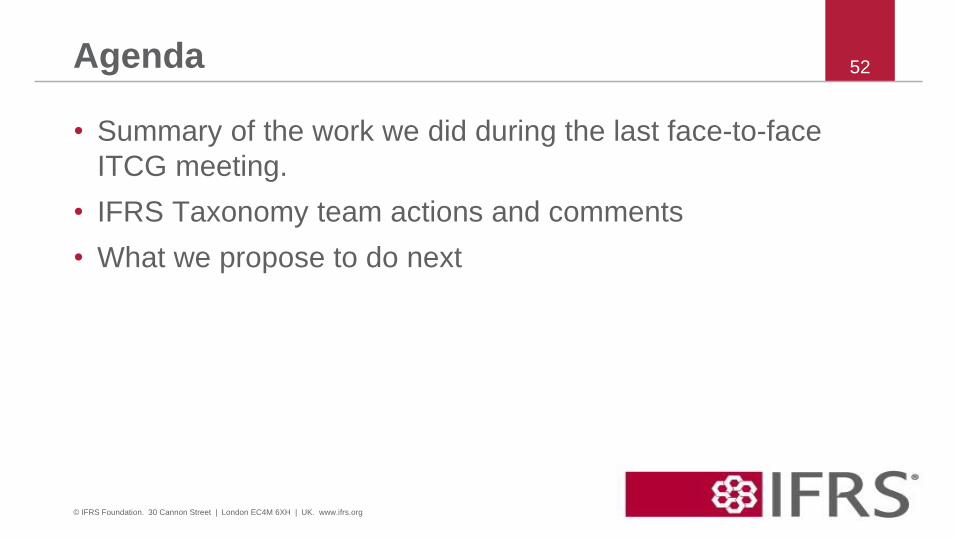

• Summary of the work we did during the last face-to-face

ITCG meeting.

• IFRS Taxonomy team actions and comments

• What we propose to do next

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

52

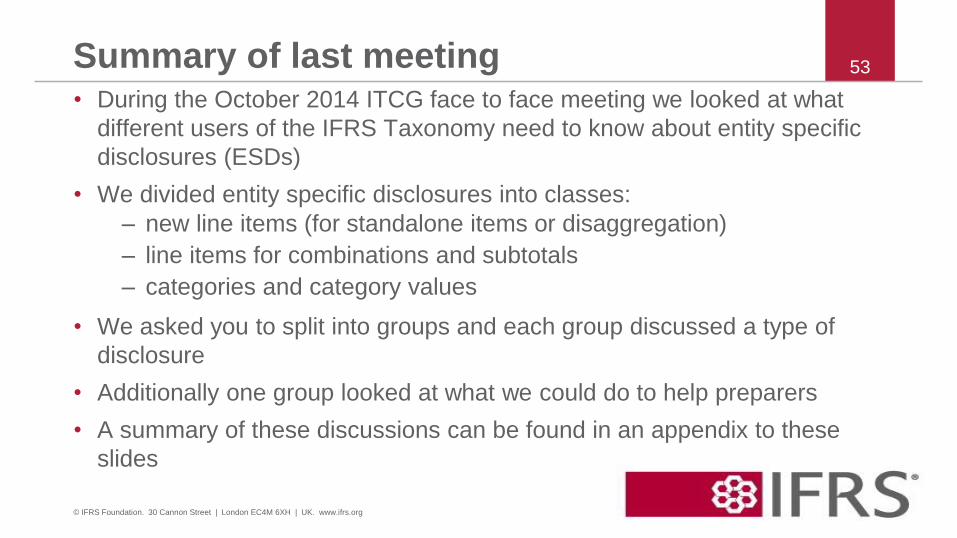

Summary of last meeting • During the October 2014 ITCG face to face meeting we looked at what

different users of the IFRS Taxonomy need to know about entity specific

disclosures (ESDs)

• We divided entity specific disclosures into classes:

– new line items (for standalone items or disaggregation)

– line items for combinations and subtotals

– categories and category values

• We asked you to split into groups and each group discussed a type of

disclosure

• Additionally one group looked at what we could do to help preparers

• A summary of these discussions can be found in an appendix to these

slides

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

53

International Financial Reporting Standards

The views expressed in this presentation are those of the presenter,

not necessarily those of the IASB or IFRS Foundation

IFRS Taxonomy team actions and comments

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

April 2015

IFRS Taxonomy

• Improve IFRS taxonomy

navigation to reduce

unnecessary creation of new

line items

• Analyse IFRS taxonomy to

ensure that entity specific items

will always have some relation

to an existing taxonomy item

(no orphaned items)

Elsewhere

• More detailed analysis of the kind

of links between new items and

existing items required for optimal

use of ESDs

• Examination of XBRL (and other

mechanisms) for providing

linking/grouping information

• Documentation for preparers on

when to use entity specific items.

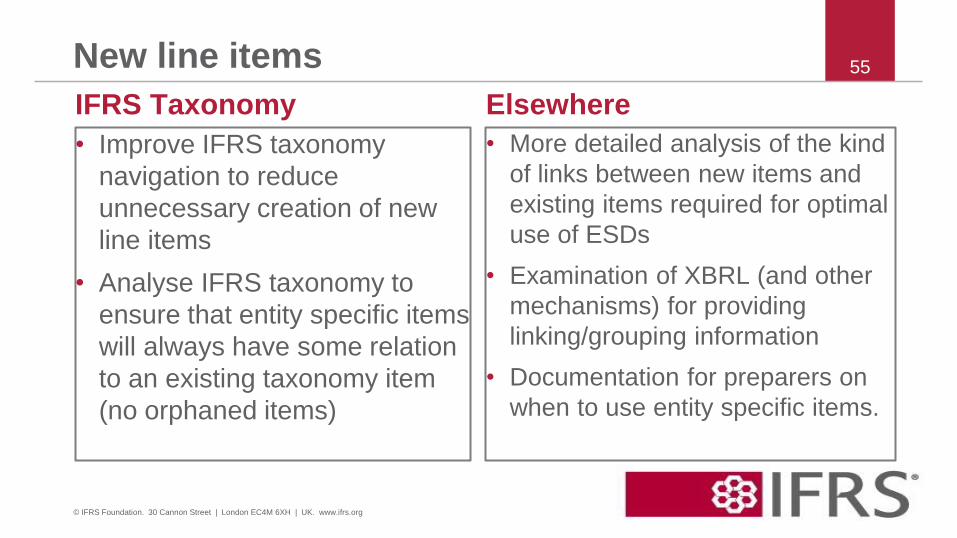

New line items

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

55

IFRS Taxonomy

• Analyse IFRS taxonomy to

ensure that common

combinations are covered

(within existing common

practice)

• Ideally a long term action

reduces the requirement to

have these directly in the

IFRS Taxonomy

Elsewhere

• Examination of XBRL (and

other) mechanisms for

providing – Linking/grouping information

– indicating a combination of

existing items

– flagging items as of a

certain type of total or

combination

Combinations and subtotals

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

56

IFRS Taxonomy

• Look at the use of generic

(product 1) category values – Where might these be of use in

the IFRS Taxonomy?

– If introduced would they be as

alternatives or replacement?

• A rationalisation of the existing

categories (and line items)

provided in the IFRS

Taxonomy (‘simplification’)

Elsewhere

• Preparer’s guides to

navigating the IFRS

Taxonomy and deciding on

appropriate items including

correct use of IFRS

dimensions and members

Categories and category values

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

57

IFRS Taxonomy

• Investigate IFRS Taxonomy

code based navigation – what kind of code system could

help?

– would codes be appropriate

given no overall IFRS

codification?

• Investigate useful alternative

‘presentation’ views

Elsewhere

• Implementation guides – how

to work with certain kinds of

disclosure when using the

IFRS Taxonomy

• Preparer’s guides to

navigating the IFRS

Taxonomy and deciding on

appropriate items

Helping preparers

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

58

Overall conclusions

• Many of the requirements, and solutions identified, for

improving the use and handling of ESDs are related to

regulatory (or other filing) rules

• Some areas could potentially be supported with changes or

additions to the current IFRS Taxonomy

• Supporting regulators as they set up and update an IFRS

filing environment is essential

• Providing some assistance to preparers may help improve

their filings but also indirectly help regulators if done carefully

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

59

International Financial Reporting Standards

The views expressed in this presentation are those of the presenter,

not necessarily those of the IASB or IFRS Foundation

Proposed actions

April 2015

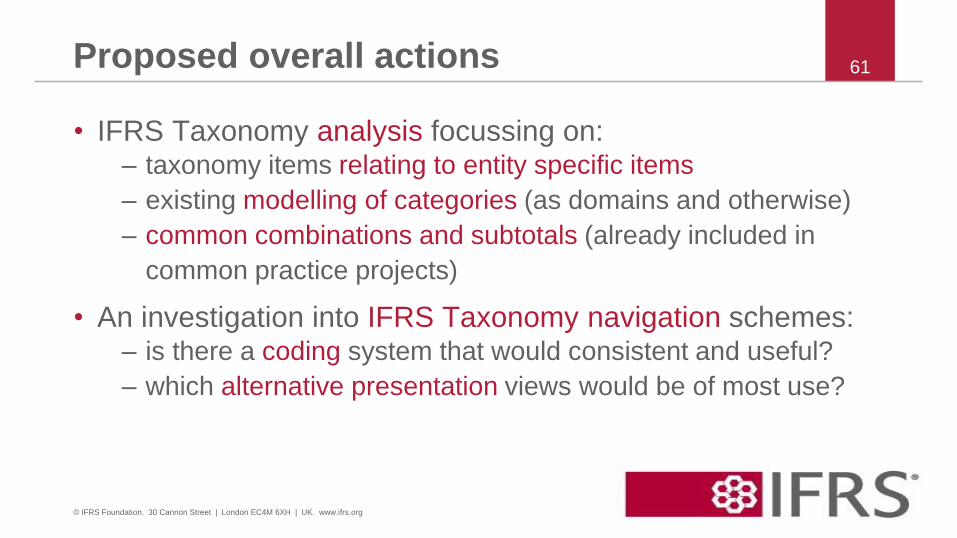

Proposed overall actions

• IFRS Taxonomy analysis focussing on: – taxonomy items relating to entity specific items

– existing modelling of categories (as domains and otherwise)

– common combinations and subtotals (already included in

common practice projects)

• An investigation into IFRS Taxonomy navigation schemes: – is there a coding system that would consistent and useful?

– which alternative presentation views would be of most use?

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

61

Proposed overall actions

• A published investigation into using entity specific disclosures

with the IFRS Taxonomy. Probably including a look at

possible XBRL (and other) technical mechanisms

• Additions to the new documentation for regulators

• New documentation for preparers including: – implementation guides

– help navigating the taxonomy and choosing appropriate items

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

62

Questions

• Do you see any other areas we could make improvements?

• After some time to reflect are there any additional comments

you would like to make on entity specific disclosures? – are there any additional organisations or individuals working in

this area we should talk to?

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

63

International Financial Reporting Standards

The views expressed in this presentation are those of the presenter,

not necessarily those of the IASB or IFRS Foundation

Appendix A: October group discussions

April 2015

New line items

• Preparers require – solutions that handle their material items properly

– provide consistency between paper filing and structured

electronic filing

• Investors are looking for – comparability

– the ability to dive deeper into the information to understand

entity-specific variability.

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

65

New line items

• For disclosures representing entity-specific disaggregation of

existing IFRS Taxonomy elements – the use of linked extensions e.g. extension elements are created for entity-

specific disclosures but associated with existing IFRS Taxonomy

elements.

– the use of ‘negative tag flagging’, i.e. an IFRS Taxonomy element tag is

used to tag an entity-specific disclosure but with a negative tag flag to

indicate that the entity-specific disclosure is akin to, but not necessarily

identical with, the IFRS Taxonomy element.

• a base taxonomy could include some specific features to

cater for the use of linked extensions.

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

66

Combinations and subtotals

• Efficient data relationship management is the optimal way to

handle entity specific combinations and subtotals that are

disaggregated in the notes.

• Tagging of combinations and subtotals may not be necessary

to meet the needs of investors

• Custom combinations and subtotals could be viewed as ‘not

extension’ as they are not wholly new reporting items

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

67

Combinations and subtotals

• ‘Double tag’ rather than creating an extension element. – double tagging means that a disclosure can be tagged with two (or more)

elements of the IFRS Taxonomy or extension and IFRS Taxonomy.

– a relationship could then be specified between the two tags applied (e.g.

this item is a combination of…)

– double tagging and better data relationship management may, however,

require changes to the XBRL technical standards.

• An alternative option to non-tagging or double tagging is to

flag these combinations and subtotals as entity-specific

aggregation points.

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

68

Categories and category values

• Handling entity-specific disclosures depends on the number of

disclosures expected to be reported within a particular IFRS

Taxonomy category.

– for categories in which the potential number of entity-specific

disclosures is expected to be large, it is not clear whether

meaningful analysis can be obtained from tagging entity-

specific disclosures through the use of entity specific extension

elements.

– the use of generic IFRS Taxonomy category elements (for

example, product line 1, product line 2) could be considered in

this case.

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

69

Categories and category values

• For generic IFRS Taxonomy category elements to be useful

for all types of investors, the following two conditions are

required: – entity specific labels are provided; and

– a specific generic category element to depict a disclosure is

consistently used over time by an entity.

• For categories in which the potential data set of entity-

specific disclosures is expected to be relatively small, tagging

of entity-specific disclosures through the use of entity-specific

extension elements could still be useful.

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

70

Helping preparers

• Searching is difficult

• First time for individual is hard

• Regulatory rules are diverse

• Taxonomy changes annually

• Diverse disclosures – disaggregation

– subtotals

– stand alone items

– immaterial items reported

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

71

Helping preparers

• Essential activities

– the development of implementation guides and the integration of

the [Proposed] IFRS Taxonomy Updates within the Standards

– the integration of the [Proposed] IFRS Taxonomy Updates within

the Standards will allow preparers to become familiar with the

taxonomy at an early stage

• Activities that were rated as important were

– improved taxonomy navigation;

– continuation of common practice projects; and

– better collaboration with industry groups.

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

72

Thank you

Expressions of individual views

by members of

the IASB and its staff

are encouraged.

The views expressed in this presentation are those

of the presenter. Official positions of the IASB on

accounting matters are determined only after extensive due

process and deliberation.

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

73

The views expressed in this presentation are those of the presenter,

not necessarily those of the IASB or IFRS Foundation.

International Financial Reporting Standards

Encouraging external taxonomy updates Andromeda Wood – Senior Technical Manager

April 2015 Agenda Paper 5

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Agenda

• What we mean when we talk about ‘taxonomy updates’

• Why we care about IFRS Taxonomy versions and

update frequency

• Some factors we think may affect updates

• Breakout sessions – What are the factors affecting update to newer taxonomy

versions? How do they vary by circumstance?

– Are there any actions we should take to encourage regular

external taxonomy updates?

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

75

IFRS Taxonomy update

• An IFRS Taxonomy update is:

• An update might include changes resulting from: – A new or amended standard

– Common practice items

– Corrections and improvements

– Architectural updates

A change to the IFRS Taxonomy resulting in a new Interim Release or

the annual IFRS Taxonomy (a compilation of all previous Interim

Releases).

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

76

External taxonomy update

• An external taxonomy update is:

• This newer version could be: – the latest annual taxonomy

– the latest final interim release

– any other more recent taxonomy than the version currently in use

– an addition to an allowed set of IFRS Taxonomies in use

The move from an older version of the IFRS Taxonomy in a system or

extension taxonomy to a newer version of the IFRS Taxonomy

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

77

International Financial Reporting Standards

The views expressed in this presentation are those of the

presenter,

not necessarily those of the IASB or IFRS Foundation

Why we care about external taxonomy

updates

April 2015

Advantages of updating

• The latest disclosures for new standards will be available

supporting early application.

• Expiring disclosures are identified

• References and documentation across the IFRS Taxonomy

(not just with new items) are updated with new and amended

standards

• Common practice additions improve coverage

• Corrections may be made to existing taxonomy items and

other improvements may be beneficial (for example

separation of SMEs)

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

79

Advantages of updating – cont’d

• To aid comparability: – Is an item from 2009 comparable with one from

2015?

– Is an extension from 2011 the same as the new

common practice item from 2015?

• To reduce the number of old versions of the IFRS

Taxonomy we continue to support

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

80

International Financial Reporting Standards

The views expressed in this presentation are those of the

presenter,

not necessarily those of the IASB or IFRS Foundation

Examples of factors affecting updates

April 2015

IFRS Taxonomy

• The IFRS Taxonomy update schedule

• The IFRS Taxonomy design

– navigation

– identification of new items and other changes

– access to elements

– identification of element/taxonomy version

• The materials provided with the IFRS Taxonomy

• For more detail on the IFRS Taxonomy see Appendix A

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

82

External factors

• Endorsement processes for IFRS

• Endorsement/approval processes for the IFRS

Taxonomy

• Changes in local law and regulation e.g. new local

company law

• Existing update schedules for filing systems

• The size and complexity of filing systems, software and

extension taxonomies

• Impact on system users © IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

83

International Financial Reporting Standards

The views expressed in this presentation are those of the

presenter,

not necessarily those of the IASB or IFRS Foundation

Breakout sessions

April 2015

What we want to look at today

• The aim of the following breakout sessions is to

identify the factors (including business

requirements) affecting external updates of the

IFRS Taxonomy in different filing environments.

• We will look at: – systems with a regulator/owner extension

– filing environments with some kind of preparer

extension/entity specific disclosures

– systems using the IFRS Taxonomy directly

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

85

Breakout group discussion topics Regulator extension

• Regulator has created an extension taxonomy based on the IFRS Taxonomy

• This extension includes any number of IFRS Taxonomy items

• It may include use of IFRS labels, references and other linkbases

• System specific items may also be added via parallel taxonomies rather than direct extension

Preparer extension

• The IFRS Taxonomy is used within a filing system expecting preparers to add entity specific items in some fashion

• The system may require preparers to create US style taxonomy extensions or may use another mechanism

• This may be to the IFRS Taxonomy directly or to a regulator extension of the IFRS Taxonomy

As published

• The IFRS Taxonomy is used as published with no extension provided or allowed.

• It may have accompanying documentation specific to the filing system however.

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

86

Features in common

• Documentation

• A taxonomy used: – solely for that system or

– shared with other organisations

• A filing that is: – used internally

– published for external users

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

87

Breakout group members Regulator extension Preparer extension As published

Board room Victoria room (downstairs – GFW)

Cannon room (downstairs – GFE)

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

88

Binh La/Doug Niven

Jinguang Zhao

Joanne Locke

John Dill

Lou Rohman

Marshall Matthews

Michal Piechocki

Ying Wei

Anna Beck

Krishnan

Balachandran

Louis Matherne

Masatomo Goto

Patricia Myles

Roxana Damianov

Thomas Egan

Carlo Alzati

Chie Mitsui

Indrit Troshani

Jim Truscott

Kimberly Earle

Koichi Kikuchi

Kyle Lamb

Maciej Piechocki

William Gee

Questions to consider • Reasons to update – are they compelling? What other

reasons might there be?

• What are the different factors affecting update for your

type of filing system? Rate these by importance.

• Do any of the features of the IFRS Taxonomy at the

moment affect update?

• Are there external factors affecting update?

• What could the IFRS Taxonomy team do to improve the

update frequency?

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

89

International Financial Reporting Standards

The views expressed in this presentation are those of the

presenter,

not necessarily those of the IASB or IFRS Foundation

Appendix A: IFRS Taxonomy updates and

structure

April 2015

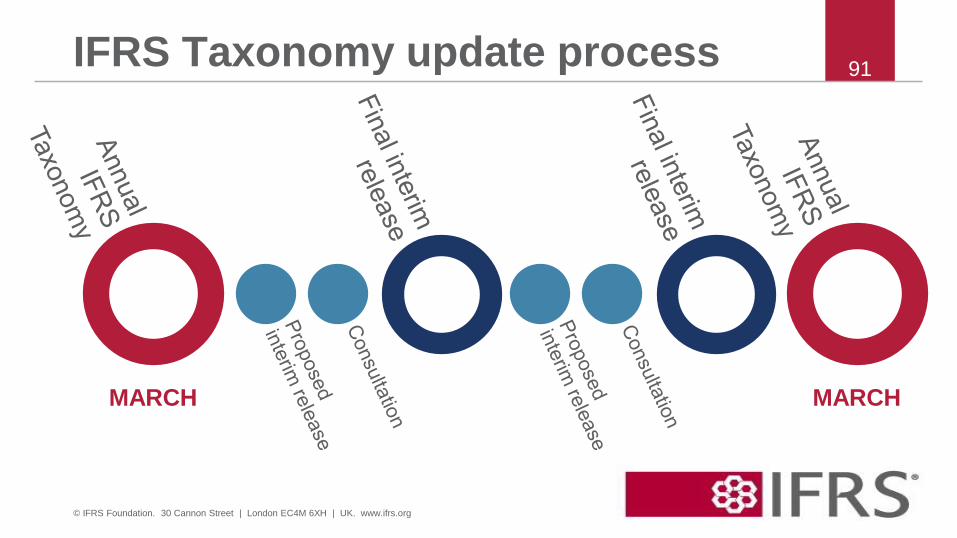

IFRS Taxonomy update process

MARCH MARCH

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

91

Which files are available when?

Typ

e o

f rele

ase

XB

RL

files

Up

da

te

do

cu

me

nt

IFR

S

Taxo

no

my

Illustra

ted

ITI +

track

ch

an

ges

XB

RL

vers

ion

ing

rep

ort

Do

cu

me

nta

tion

lab

els

xIF

RS

Illustra

tive

exam

ple

s

Proposed

interim

release O O O O O X

Final interim

release O O Annual IFRS

Taxonomy X

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

92

New element availability

• New elements are added to the IFRS Taxonomy when: – A new standard is issued

– A standard is amended

– A common practice project has been completed

– We receive feedback that an element is missing

• These elements are added during the year and are available

from the final version of the appropriate interim release.

• Each interim release is based on previous interim release (or

annual taxonomy)

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

93

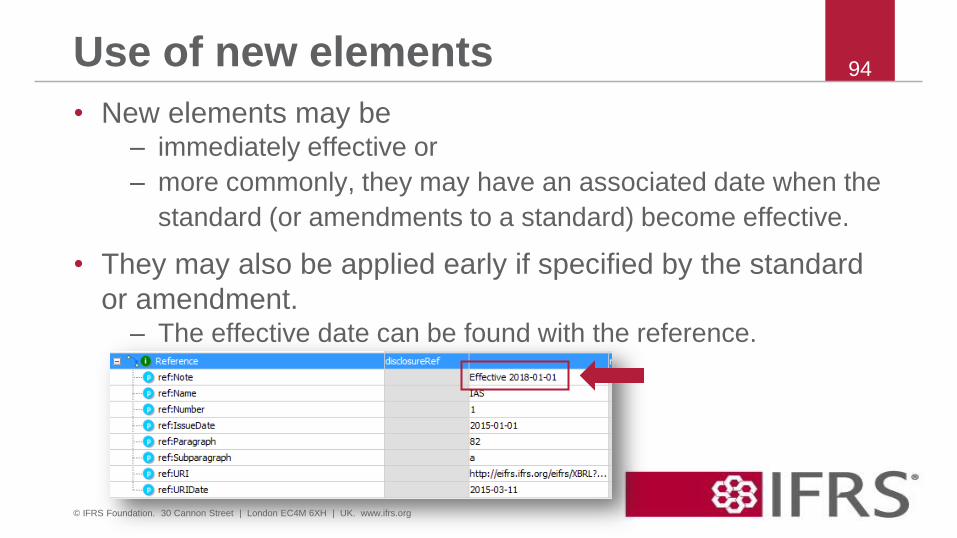

Use of new elements

• New elements may be – immediately effective or

– more commonly, they may have an associated date when the

standard (or amendments to a standard) become effective.

• They may also be applied early if specified by the standard

or amendment. – The effective date can be found with the reference.

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

94

Expiring element availability

• Elements expire (are deprecated) from the annual

taxonomy after they reach the expiry date for the

relevant standard (or pre-amendment version of a

standard)

• In the case of a correction or immediate

replacement they are expired during the

appropriate interim or annual release

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

95

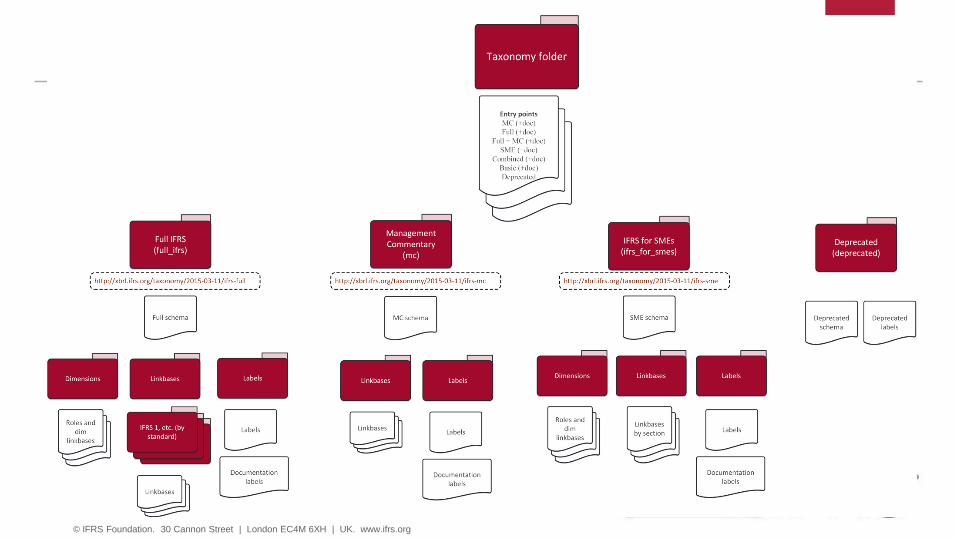

Accessing elements

• The IFRS Taxonomy has a partially modular file

structure*

• The presentation, definition and calculation linkbases

are split by standard (or section in IFRS for SMEs)

• Labels are split by element schema

• Element schemas are split into Full IFRS, Management

commentary, IFRS for SMEs and deprecated elements

*The file structure is the way the XBRL schemas and linkbases are

broken down into individual files and folders (modules)

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

96

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

97

The version of an IFRS Taxonomy release is indicated by:

Identifying IFRS Taxonomy updates

Version information Where Example

Date File names (not folder names)

full_ifrs-cor_2015-03-11.xsd

Date Namespace (IFRS identifier

associated with elements)

http://xbrl.ifrs.org/taxonomy/20

15-03-11/ifrs-full

Status of release Documentation only Interim, annual

Type of change (standard, CP, architecture)

Documentation only New standard, amended

standard, common practice,

architecture

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

98

How we identify updated elements

• An issue date is provided with each reference (set to the

release date for all elements on annual release)

• An XBRL versioning report is produced with each release

• Changes to the IFRS Taxonomy are highlighted using red &

green line formatting in the IFRS Taxonomy illustrated with

versioning information

• New and amended items are identified with each release in

the IFRS Taxonomy update document

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

99

Examples – versioning reports

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

100

Thank you

Expressions of individual views

by members of

the IASB and its staff

are encouraged.

The views expressed in this presentation are those

of the presenter. Official positions of the IASB on

accounting matters are determined only after extensive due

process and deliberation.

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

101

XII UPDATE Updating the ITCG on XBRL

International Developments

John Dill

Member of the XII Board of Directors

April 21, 2015

EXECUTIVE SUMMARY

The XII Board holds the view that there continues to be significant work to do

at a technical and implementation guidance perspective in order to further

improve regulatory reporting. It is also time for the XBRL community to turn its

attention towards discovering the value associated with standardization in the

context of enterprise reporting.

XII is working on a number of fronts to expand the capabilities of the standard,

enhance the XBRL brand, explore new areas for adoption, provide guidance

to implementers and enhance the membership and funding base of the XBRL

consortium.

The XBRL community and staff stand ready to assist the ITCG in its efforts in

this field.

Our purpose is to improve the accountability and transparency of

business performance everywhere, by being the open data exchange standard

for business reporting.

Improve accountability and

transparency – purpose of any

act of record keeping.

Business

performance itself –

not just reporting

(“Business” meaning every kind of

organization, including government,

regulators, corporations, not-for-

profits and supply chains) We are the open data exchange standard for

business reporting – that’s how we improve

business performance.

What is the XBRL consortium for?

(“Open” in the

sense that the

standard is freely

licensed. It does

not necessarily

mean that data

collected is openly

available, even

though this is a

trend. Much will

always remain

private.)

Regulatory Reporting

The “First Chapter” in XBRL

• Regulatory reporting, including regulatory reporting to

securities regulators and business registrars via XBRL is

extremely well established world wide.

• 90-100* projects across more than 45 countries.

• > ~10M companies use XBRL at least annually around the

world and this continues to grow.

• XBRL is the embedded standard, but XII is keenly aware that

the community needs to continue to improve and simplify

what has been achieved to date in order to enhance

outcomes and further expand adoption.

XII develops and maintains the specifications and promotes adoption, including via jurisdictions.

10 million + businesses use XBRL for reporting today.

15 years in XBRL is an important part of the reporting landscape, but we are still at the beginning of the process of moving to structured data exchange in this field.

* XII has not had the resources to collaborate effectively with the IFRS team on its current Jurisdictional survey. However staff are currently working to carry out a survey and interviews via an intern, which should improve the accuracy of these estimates.

The Next Chapter

Enterprise Reporting – the “Second Chapter” in XBRL

• Developments in “Big Data” technology now make it practical to leverage the benefits of data standardization at a

transactional or ledger level.

• Standardized transactional data streams allow preparation of reports in near real time.

• We are at the very earliest implementations in this field but this is likely the area that XBRL will next focus on.

• Likely to be a 10 year effort.

• IFRS and other primary taxonomies a key part of the puzzle.

Big Data capabilities mean that the entire enterprise can benefit from XBRL-based standardization of transactional and ledger level data.

Requires additional standardization and lengthy ecosystem development period.

Some Current Initiatives Open Information Model, or OIM

• Simplify representation of XBRL. • Initially, provide way of republishing data in

alternative formats to assist analytics.

Body of Knowledge • Develop formal framework providing

implementation and technical guidance. • Supports training and certification.

Other guidance • Detailed dimensions guidance via WG note. • Ongoing taxonomy architecture guidance. • Detailed extensible enumerations guidance.

OIM to make XBRL more accessible for developers, initially for analysis.

Body of Knowledge designed to expand skills

Detailed guidance to support projects

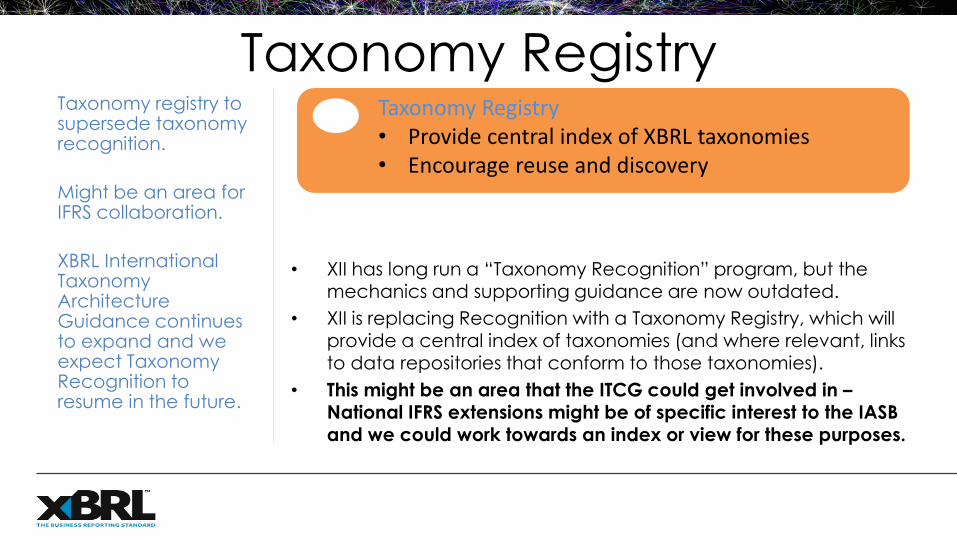

Taxonomy Registry Taxonomy Registry

• Provide central index of XBRL taxonomies • Encourage reuse and discovery

Taxonomy registry to supersede taxonomy recognition.

Might be an area for IFRS collaboration.

XBRL International Taxonomy Architecture Guidance continues to expand and we expect Taxonomy Recognition to resume in the future.

• XII has long run a “Taxonomy Recognition” program, but the

mechanics and supporting guidance are now outdated.

• XII is replacing Recognition with a Taxonomy Registry, which will provide a central index of taxonomies (and where relevant, links to data repositories that conform to those taxonomies).

• This might be an area that the ITCG could get involved in – National IFRS extensions might be of specific interest to the IASB

and we could work towards an index or view for these purposes.

Funding Initiative

• In order to expand the capabilities of the standard and

in order to make the consortium’s financial position more

resilient, the XBRL Board will shortly commence a

fundraising program.

• Funding will accelerate a number of initiatives, including

the “Body of Knowledge”.

• Further updates will be provided as we move forward.

XII will embark on

a fundraising

effort in H2 2015.

Funding initiative • Expand the capabilities of XBRL. • Increased financial resilience.

QUESTIONS

The views expressed in this presentation are those of the presenter,

not necessarily those of the IASB or IFRS Foundation.

International Financial Reporting Standards

IFRS Taxonomy (IFRST) Technology

Wladek Krawiec – IT project manager (IFRS Taxonomy)

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

April 2015 Agenda Paper 7

Agenda

• Extensible enumerations

• IFRS Taxonomy Versioning information – update

• Interactive IFRS Taxonomy Illustrated with

documentation labels

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

112

International Financial Reporting Standards

The views expressed in this presentation are those of the presenter,

not necessarily those of the IASB or IFRS Foundation

Extensible enumerations

April 2015

Enumerations

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

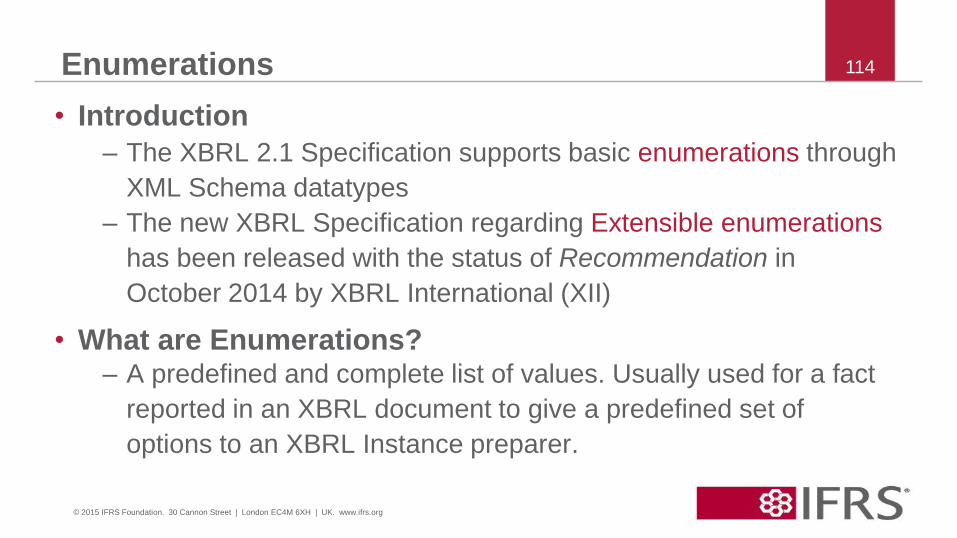

114

• Introduction

– The XBRL 2.1 Specification supports basic enumerations through

XML Schema datatypes

– The new XBRL Specification regarding Extensible enumerations

has been released with the status of Recommendation in

October 2014 by XBRL International (XII)

• What are Enumerations? – A predefined and complete list of values. Usually used for a fact

reported in an XBRL document to give a predefined set of

options to an XBRL Instance preparer.

Enumerations

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

115

• At the moment, the IFRS Taxonomy does not use

enumerations and does not contain many elements for which

enumerations would be significantly beneficial.

• Proposed use of Enumerations – Example

Description of inventory cost formulas:

Extensible enumerations - characteristics

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

116

• The key benefit of the extensible enumerations is that they

allow a preparer to customise predefined set of options in a

published Taxonomy in order to meet their requirements.

• The customisation is based on defining the additional items for

enumeration as part of the extension Taxonomy. The core

schema of the base taxonomy remains unaffected.

Extensible enumeration – Our view

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

117

• We have reviewed the new features offered by

extensible enumerations, but we do not expect to

use them in the short term. We will, however, take

new possibilities into account when further

developing the IFRS Taxonomy.

Enumerations – Questions

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

118

• Should we consider using enumerations in the IFRS

Taxonomy?

• Do you see any cases where including extensible

enumerations in the existing IFRS Taxonomy would

be useful?

International Financial Reporting Standards

The views expressed in this presentation are those of the presenter,

not necessarily those of the IASB or IFRS Foundation

The IFRST Versioning Information

April 2015

IFRST Versioning information

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

120

A set of two files describing the differences between two IFRS

Taxonomies.

• The set consists of:

– Versioning Report (xml file) - usually utilised by an XBRL

processor.

– IFRS Taxonomy Versioning Visualisation (html file).

• Based on ITCG feedback the IFRS Taxonomy Versioning

Report (xml file) has been aligned to the newest XII

Specification (excluding the Versioning Dimension

specification)

IFRST Versioning Information – update

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

121

• Previously the IFRS Taxonomy Versioning Information was

only available in the English language

• Since April 2015 Versioning Information is available in multiple

languages

– Currently available for the 2013 and 2014 IFRS Taxonomy

translations (Arabic, Japanese, Korean and Spanish).

– We will now be adding translated versioning information between

annual taxonomy releases as translations become available.

Example of the IFRS Taxonomy versioning visualisation in Japanese

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

122

International Financial Reporting Standards

The views expressed in this presentation are those of the presenter,

not necessarily those of the IASB or IFRS Foundation

Interactive IFRST Illustrated

April 2015

Interactive IFRST Illustrated

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

124

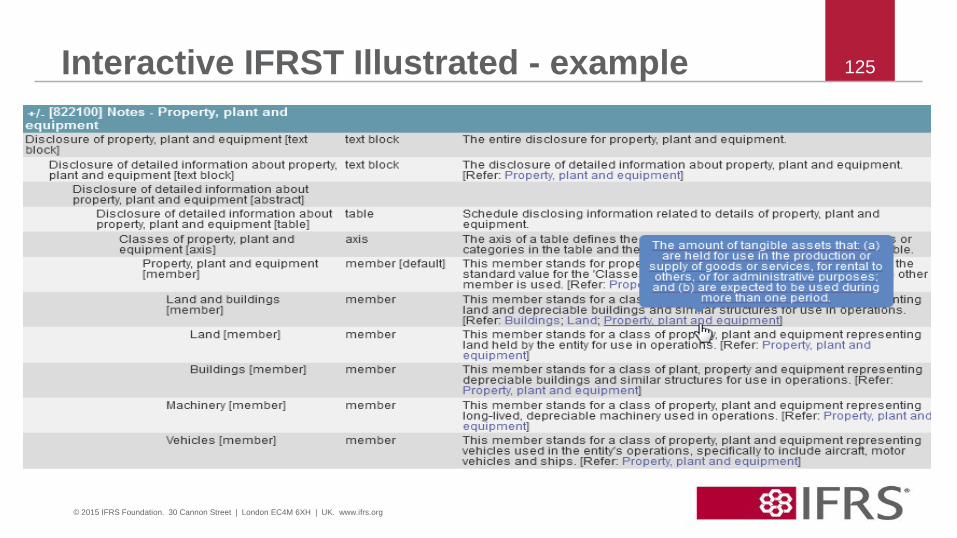

The IFRST Illustrated (ITI) is a document that present the

structure of the IFRST in a simplified, visual format that does not

require knowledge of XBRL.

The purpose of making it interactive is:

• to leverage the use of the IFRS Taxonomy documentation

labels

• to ease navigating through the IFRS Taxonomy elements and

its definitions

• additional supporting material for the IFRS Taxonomy

Interactive IFRST Illustrated - example

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

125

Thank you

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

126

The views expressed in this presentation are those of the presenter,

not necessarily those of the IASB or IFRS Foundation.

International Financial Reporting Standards

IFRS Taxonomy content ITCG meeting

Bartek Czajka – Senior Technical Manager

Richard Fraser – Assistant Technical Manager

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

April 2015 Agenda Paper 8

Agenda

• Update on common practice (CP) project

– Discussions with the Technical Staff

– Considerations for future CP projects

– Meeting with the Board Review Panel

• IFRS for SMEs amendments

• Early application – ’disclosure of fact’

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

128

International Financial Reporting Standards

The views expressed in this presentation are those of the presenter,

not necessarily those of the IASB or IFRS Foundation

Update on common practice project

April 2015

International Financial Reporting Standards

The views expressed in this presentation are those of the presenter,

not necessarily those of the IASB or IFRS Foundation

Discussions with the Technical Staff

April 2015

Discussions with the Technical Staff (TS)

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

131

We have discussed the proposed list of elements internally with

the TS. As a result of this, areas for further analysis have been

proposed. These included:

• Technology

• Programming assets (including current and non-current

breakdowns)

• Combinations of classes of property, plant and equipment

We have performed the requested analysis.

Discussions with the TS – technology

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

132

• The Technical Staff questioned whether “Technology” should be

a separate class of intangible assets or whether it is synonymous

with existing classes such as “computer software”, “recipes,

designs and prototypes”, “copyrights, patents and other rights”

• Reporting practice indicates that companies disclose technology

as a separate class of intangible assets and they do not explain

what is included in it

• Illustrative examples to IFRS 3 use and describe the term

“technology-based intangible assets”

Discussions with the TS – technology

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

133

• The following has been proposed:

– Adjust the label of the proposed element from “Technology”

to “Technology-based intangible assets” and propose this

element as a separate class of intangible assets

– Adjust the definition of the proposed element from “a class of

intangible assets representing technology” to “a class of

intangible assets representing assets based on technology.

Such assets may include patented and unpatented

technology, databases as well as trade secrets”

Discussions with the TS – programming assets

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

134

• Programming assets is a concept common to media related

activities, in particular to the broadcasting sector.

• Programming assets are often presented separately on the face

of the financial statements (including the breakdown into current

and non-current)

• The TS raised concerns regarding the classification of

programming assets. They asked whether programming assets

were not a class of intangible assets that was reported

separately due to its significance.

Discussions with the TS – programming assets

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

135

• Having analysed the classification of programming assets in

various financial statements, we have found out that

programming assets are defined and classified differently by

companies, either as intangible assets, inventories or both.

• The following has been proposed:

– Retain the proposed positioning of “Programming assets” in

the IFRS Taxonomy under the “Miscellaneous assets”

heading (therefore avoiding the classification as either

intangible assets or inventories)

– Seek feedback on this during public consultation

Discussions with the TS – classes of PPE

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

136

• Our 2014 common practice analysis identified various combinations of

PPE, specifically:

– Plant and machinery

– Plant and equipment

– Machinery and equipment

• The TS pointed out that:

– None of these combinations are defined in IFRS

– These combinations may have a conceptually equivalent meaning

– IFRS Taxonomy elements such as “Machinery”, “Fixtures and

fittings” or “Office equipment” could potentially be used

Discussions with the TS – classes of PPE

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

137

– Including these items may imply that preparers should only

apply tags with precisely matching labels and therefore

create extensions for every slight difference in labelling,

regardless of the actual accounting meaning

• The TS noted that it might be more useful to provide a top

down structured breakdown of classes of ‘property, plant and

equipment’ within the taxonomy rather than provide a flat list

which includes many potential combinations

Discussions with the TS – classes of PPE

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

138

• The following has been proposed:

– Consider analysing reported combinations of classes of

assets and liabilities in more detail as a part of the Disclosure

Initiative project

– Defer the proposals for additional combinations of classes of

PPE until a general analysis is performed

International Financial Reporting Standards

The views expressed in this presentation are those of the presenter,

not necessarily those of the IASB or IFRS Foundation

Considerations for future CP projects

April 2015

Suggestions from the TS

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

140

For future common practice projects, the TS have suggested the following:

• Further investigate (for example, by analysing accounting policies and

related notes) each potential CP element before proposing it:

– Ensures that the accounting meaning of proposed elements is

captured; and not just the label

– Helps to avoid unwarranted interpretation of the accounting meaning

of potential elements

– Allows for clearer understanding of how an element is classified and

hence better positioning in the Taxonomy.

Suggestions from the TS

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

141

• Reconsider our approach to creating documentation labels –

investigate the potential for clarifying the accounting content of

proposed elements, for instance by means of additional

examples or guidance

(If undertaken, this is likely to become a separate project, due to its

extensive scope and significance. Other functions of the Organisation may

need to be included - Board Members, Education)

International Financial Reporting Standards

The views expressed in this presentation are those of the presenter,

not necessarily those of the IASB or IFRS Foundation

Meeting with the Board Review Panel

April 2015

Meeting with the Board Review Panel

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

143

• The Staff will present a paper to the BRP on April 8, 2015*

• The aim of this paper is to:

– Present the findings of the 2014 Common Practice Project

– Highlight two specific issues for which we seek the feedback

by the BRP

1) The use of alternative performance measures such as

EBIT, EBITDA and net debt

2) The use of ‘Profit (loss)’ as a part of the equity section of

the statement of financial position in the IFRS Taxonomy

* We will update you on the outcome of this meeting during the ITCG meeting

International Financial Reporting Standards

The views expressed in this presentation are those of the presenter,

not necessarily those of the IASB or IFRS Foundation

IFRS for SMEs – amendments

April 2015

IFRS for SMEs - timeline

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

145

• The IFRS for SMEs standard was published in July 2009, with

the intention to undertake a review of its implementation after

two years of its use.

• Consequently, in June 2012 the IASB decided to seek public

views on whether there is a need to make any amendments to

the IFRS for SMEs and, if so, what amendments should be

made (Request for Information).

• Based on the feedback received, the IASB published an

Exposure Draft of the proposed amendments in October 2013

(comment period ended in March 2014)

IFRS for SMEs - timeline

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

146

• In October 2014, the SME Implementation Group report was

made available. The report contained recommendations of the

Group on proposals included in the Exposure Draft.

• The IASB finalised its technical discussions on the amendments

(including analysis of public comments on the Exposure Draft) in

December 2014.

• The final amendments to the IFRS for SMEs will be published in

Q2 2015.

IFRS for SMEs – impact on the IFRST

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

147

The projected impact of the changes on the IFRS Taxonomy for

SMEs:

• Significant – remodelling, new elements, elements deprecated,

documentation label changes

• Non-controversial – changes mostly align IFRS for SMEs to full

IFRS

The changes will be effective 1 January 2017.

IFRS for SMEs - amendments

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

148

The main amendments to the IFRS for SMEs (from the IFRS Taxonomy

perspective):

• Separation of investment property accounted for under the cost model

from property, plant and equipment

• Addition of an option to use the revaluation model for property, plant

and equipment (similarly to full IFRS)

• Separation of items within OCI that may and may not be reclassified to

profit or loss (similarly to full IFRS)

• Alignment of income tax section to IAS 12 Income taxes

IFRS for SMEs - amendments

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

149

Other amendments to the IFRS for SMEs:

• Clarification of “undue cost or effort” exemption (and a related

disclosure) in various sections of the Standard

• Addition of option to account for investees using the equity method in

separate financial statements

• Alignment to IFRS 1 to permit multiple applications of Section 35

(Transition to the IFRS for SMEs)

• Some amendments to definitions of terms (eg combined and separate

financial statements, related party) and new definitions (eg active

market, transaction costs)

IFRS for SMEs – modularisation benefits

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

150

• Until and including IFRS Taxonomy 2013, IFRS for SMEs and

full IFRS constituted one core schema.

• In 2014, after long deliberations, we split the Taxonomy into

separate core schemas.

• Having separate core schemas enables independent

management of elements (including names, labels,

documentation labels and references). There is no pressure to

re-use the full IFRS elements for IFRS for SMEs purposes.

• The following slides present benefits of the current solution.

IFRS for SMEs – modularisation benefits

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

151

• Different labels:

Element name EffectOfTransitionToIFRSsMember

Full IFRS label Effect of transition to IFRSs [member]

SMEs label Effect of transition to IFRS for SMEs [member]

Element name StatementOfIFRSCompliance

Full IFRS label Statement of IFRS compliance [text block]

SMEs label Statement of compliance with IFRS for SMEs [text block]

IFRS for SMEs – modularisation benefits

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

152

• Different documentation labels:

Element name BusinessCombinationsMember

Full IFRS label This member stands for transactions or other events in which an acquirer obtains control of one or more businesses.

SMEs label This member stands for the bringing together of separate entities or businesses into one reporting entity.

Element name InvestmentsInJointVentures

Full IFRS label A joint venture is a joint arrangement whereby the parties that have joint control of the arrangement have rights to the net assets of the arrangement.

SMEs label A joint venture is a contractual arrangement whereby two or more parties undertake an economic activity that is subject to joint control.

International Financial Reporting Standards

The views expressed in this presentation are those of the presenter,

not necessarily those of the IASB or IFRS Foundation

Early application – disclosure of fact

April 2015

Early application – disclosure of fact

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

154

• Most new IASB publications (new IFRSs and amendments to

existing IFRSs) include in the ’Effective date and transition’ the

following requirement (highlighted):

• In the IFRS Taxonomy, the above disclosure requirement has

so far remained intentionally untagged.

• We have received a comment that it might be beneficial to

have separate ’early application’ elements for each occurence

Early application – example disclosure

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

155

Early application

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

156

We believe such disclosure is initially covered by the general

requirements of:

IAS 8.28

Early application

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

157

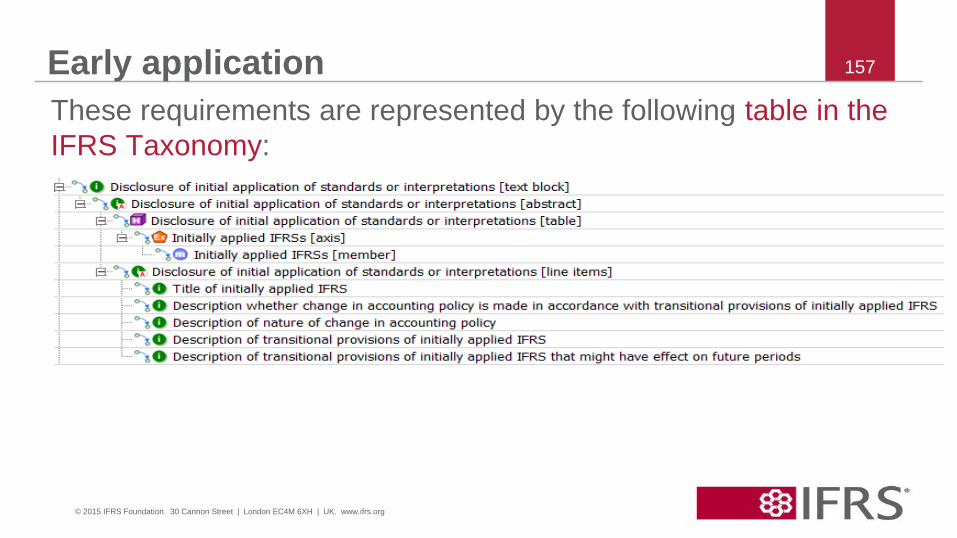

These requirements are represented by the following table in the

IFRS Taxonomy:

Early application

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

158

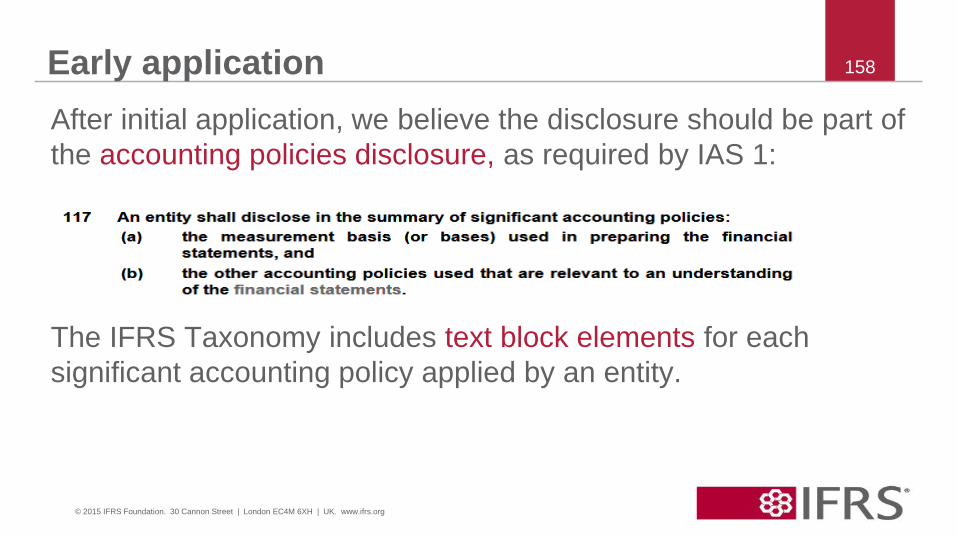

After initial application, we believe the disclosure should be part of

the accounting policies disclosure, as required by IAS 1:

The IFRS Taxonomy includes text block elements for each

significant accounting policy applied by an entity.

Early application

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

159

QUESTIONS:

Do you think the current representation is sufficient for the

disclosure of the fact of early application of an IFRS or an

amendment to an IFRS? Or should we consider separate text

elements?

If you prefer separate elements, should those elements:

• have any effective date?

• have any expiry date (eg. application date of a Standard)?

Thank you

© 2015 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

160