time's up: accounting for leases - tidewater chapter of ...• examine general ledger detail...

TRANSCRIPT

1

Time's Up: Accounting for LeasesImplementation

2

Presenter

Jennifer GeorgePartner, DHG Professional Standards GroupDixon Hughes Goodman [email protected]

3

Learning Objectives

Establish population, transition methods, and relevant lease provisions

Identify lease term

Identify lease payments and calculation of straight-line expense

Determining remaining lease payments

Calculate the initial lease liability

Calculate the initial right-of-use (ROU) asset

Record transition entry

Prepare new amortization schedule for remaining lease term

Determine disclosure requirements

4

Recap of ASC Topic 842, Leases

Requires all leases to be capitalized

• Exception for short-term leases

Right-of-use (ROU) asset

• Represents the lessee’s right to use the leased asset over the lease term

Implementing the new leasing standard may:

• Change key ratios used for debt covenant compliance

• Alter return on assets, regulatory capital requirements, credit ratings, working capital

Lease liability

• Represents the lessee’s contractual obligation to make lease payments over the lease term

5

Recap of ASC Topic 842, Leases

FINANCE LEASE

• Right-of-use asset• Lease Liability• Amortization expense• Interest expense• Cash paid for principal and

interest payments

OPERATING LEASE

• Right-of-use asset• Lease Liability• Single lease expense on a

straight-line basis• Cash paid for lease payments

6

What Can Go Wrong with Implementation?

All arrangements containing leases are not identified.

All modifications have not been identified.

Data utilized for calculating the transition adjustment does not

agree to the terms of the related contract documents.

Lease agreements are not properly classified.

Use of an inappropriate discount rate or a rate that is not supported.

Incorrect identification of initial direct costs.

Incorrect measurement of the ROU asset.

Changes in facts and circumstances not fully considered

when using hindsight practical expedient to determine lease term.

Not considering the effect of implementation on income tax

calculations.

Implementation of new or modifying existing information systems and data is not accurately transferred, access controls are not implemented, or system/spreadsheets do not function in compliance with ASC 842.

7

Basic Lease Terms and Assumptions

• ABC enters into lease commencing 1/1/2016 for 50,000 sq. ft. of office space• Initial term is 10 years (120 mo.) with 5-year renewal option • 6 mo. free rent as incentive to sign lease• $250,000 tenant improvement allowance for build-out of space• 3% escalation per year

8

Basic Lease Terms and Assumptions

• ABC is responsible for paying its share of real estate taxes and insurance based on amounts billed to lessor. ABC received $45,000 bill for 2019.

• At the commencement date, ABC determined it was an operating lease. • ABC has elected to early adopt ASC 842 effective January 1, 2019.• Legal fees and document processing costs were $125,000 and determined to qualify

as initial direct costs under ASC 840. Initial direct costs include only those costs incurred by the lessor that have both of the following characteristics: a. They are costs to originate a lease incurred in transactions with independent third parties that meet both of the following

conditions: 1. The costs result directly from and are essential to acquire the lease. 2. The costs would not have been incurred had that leasing transaction not occurred.

b. They are costs directly related to only the following activities performed by the lessor for that lease1. Evaluating the prospective lessee’s financial condition2. Evaluating and recording guarantees, collateral, and other security arrangements3. Negotiating lease terms4. Preparing and processing lease documents5. Closing the transaction

9

Establish the Population, Transition Method, and Relevant Provisions

• ABC has two transition options available under ASC 842-10-65-1c:1. Initially adopt ASC 842 as of beginning of the earliest comparative period

presented with cumulative effect adjustment to opening balance of retained earnings.

2. Initially apply ASC 842 as of beginning of the period of adoption with cumulative effect adjustment to opening balance of retained earnings.

• ABC has elected the following package of three transition practical expedients and therefore will not:

1. Reassess whether expired or existing contracts are or contain leases2. Reassess the lease classification for any expired or existing leases3. Reassess initial direct costs for any existing leases

10

Establishing the Population

Identify the current lease population• These are the leases you’ve

known about all along.• Conduct interviews or

surveys of employees regarding additional leases of which they are aware.

IDENTIFYEvaluate completeness of population• Group expense accounts by

natural classification (e.g., Payroll, Maintenance, IT support, etc.)

• Rating (High, Medium, Low) for each expense classification

• Examine general ledger detail for all High and Medium risk ratings.

EVALUATESummarize population of contracts and evaluate whether they include leases• Use lease identification

criteria in either ASC 840 or ASC 842 depending on whether package of practical expedients is elected.

SUMMARIZE

11

Identify the Lease Term

• At commencement, 5-year renewal option not reasonably certain of exercise.

• ABC has option to use same lease term as was used under ASC 840 or elect the hindsight practical expedient.

+ Hindsight practical expedient considers all changes in facts and circumstances through the effective date.

• ABC elects the hindsight practical expedient and therefore will re-evaluate the term of all of its leases.

• ABC determined there was no change to facts and circumstances so lease term is 10 years (120 mos.).

12

Hindsight Implementation Note

• Hindsight allows an entity to:+ Consider all changes in facts and circumstances through the effective date

when determining lease term. + Does not need to be a discrete change.

• Do not need to determine what you knew back at lease commencement

• If term changes as a result of electing hindsight practical expedient+ Use remaining lease payments from ASC 840 as if that term had been

used from the commencement date.

13

Hindsight Implementation Note

• May be beneficial when: + There is a large number of embedded leases not historically accounted for

as leases. + Significant change in facts and circumstances since lease commencement.

• Election of hindsight without package of three transition practical expedients

+ Could change lease classification:• Economic life criterion • Present Value of minimum rental payments relative to Fair Value of

asset

14

Identify Lease Payments and Calculate Straight-Line Expense

• ABC has uneven rents (6 months free with 3% escalation), initial direct cost ($125,000 legal and doc. prep), and received incentives ($250,000 TIA).

• ABC recognizes these expenses under ASC 840 on straight-line basis.

15

Identify Lease Payments and Calculate Straight-Line Expense

16

Determine Remaining Lease Payments

• ABC is first applying the standard as of January 1, 2019 (rather than retrospectively applying to prior comparative period).

• From January 1, 2019 to December 31, 2025, 84 lease payments remain totaling $10,466,224.20.

17

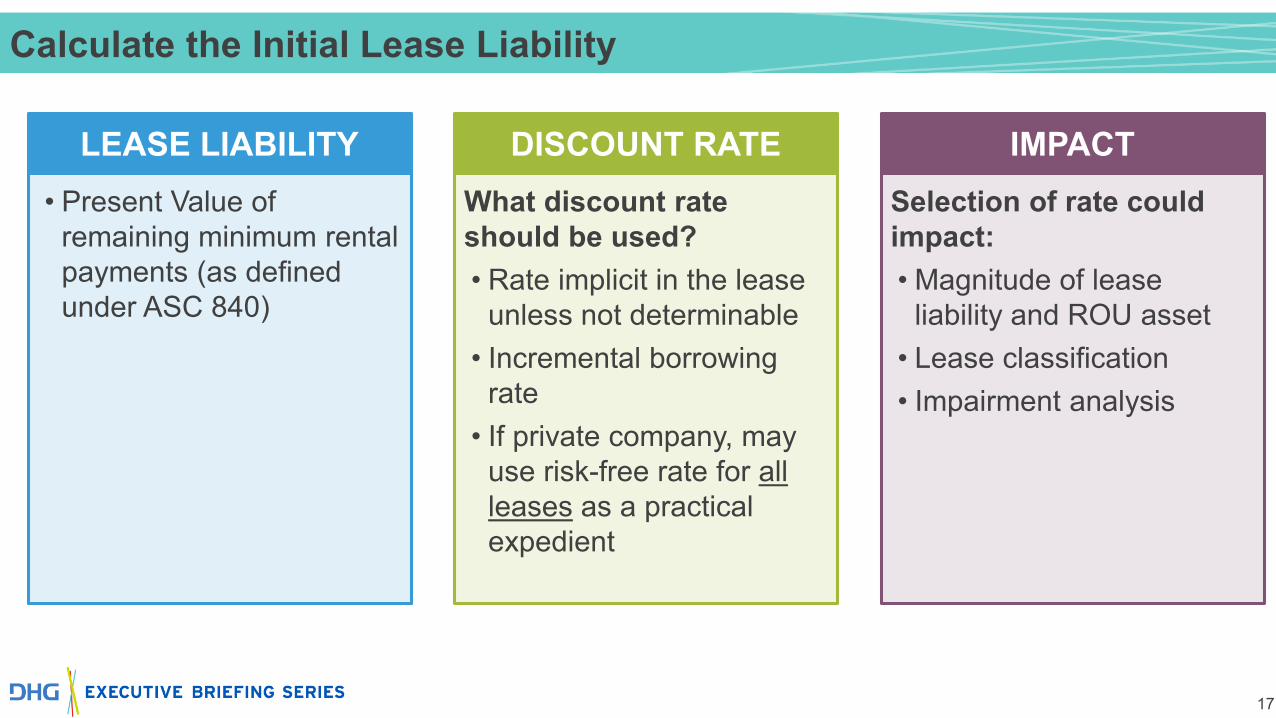

Calculate the Initial Lease Liability

• Present Value of remaining minimum rental payments (as defined under ASC 840)

LEASE LIABILITYWhat discount rate should be used?• Rate implicit in the lease

unless not determinable • Incremental borrowing

rate• If private company, may

use risk-free rate for all leases as a practical expedient

DISCOUNT RATESelection of rate could impact:• Magnitude of lease

liability and ROU asset• Lease classification• Impairment analysis

IMPACT

18

Calculate the Initial Lease Liability

• ABC chose not to utilize the risk-free rate practical expedient noting it was lower than its incremental borrowing rate and therefore would result in a larger liability.

• ABC recently entered into a 10 year collateralized loan with a similar term to the lease at a rate of 5%. ABC will utilize its incremental borrowing rate as the rate implicit in the lease is not available.

19

Present Value of Lease Payments

$8,763,726.12 Present value of remaining minimum rental payments

20

Calculate the Initial Right-of-Use (ROU) Asset

Initial ROU Asset =

Initial Lease Liability+/-

Prepaid / Accrued Expenses+

Unamortized Initial Direct Costs-

Unamortized Lease Incentives Received

21

Calculate the Initial Right-of-Use (ROU) Asset

22

Calculate the Initial Right-of-Use (ROU) Asset

23

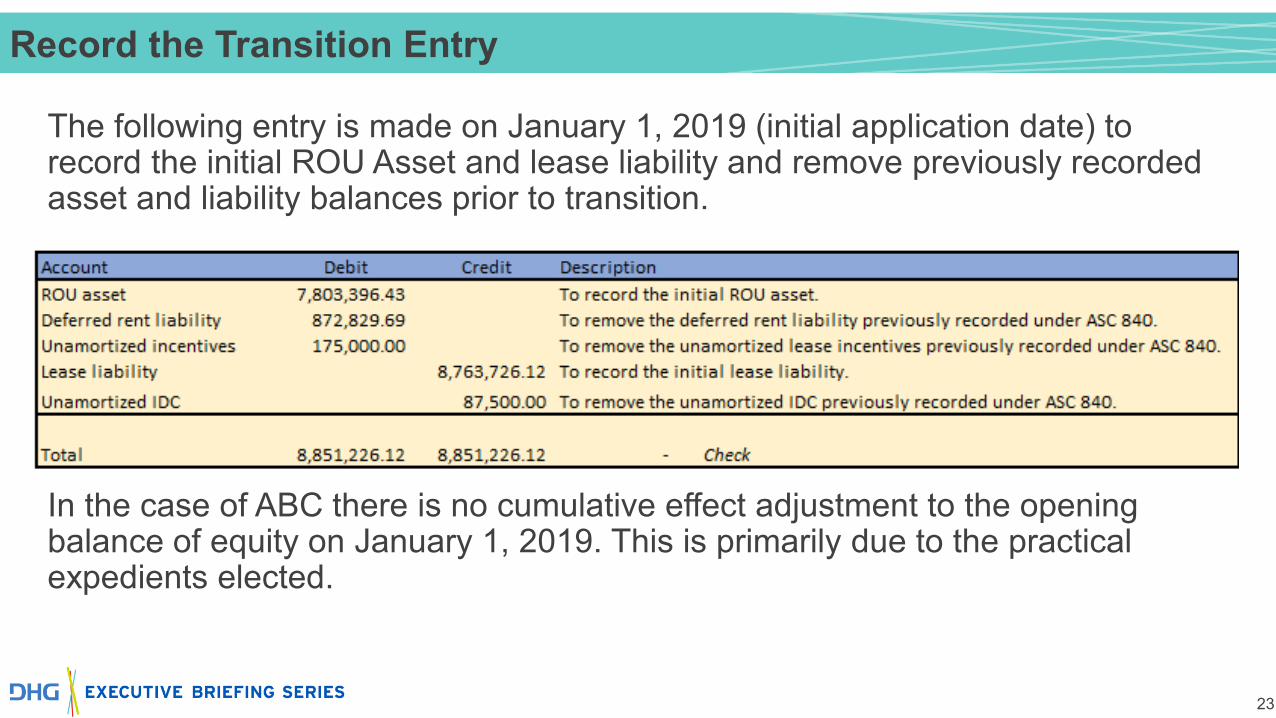

Record the Transition Entry

The following entry is made on January 1, 2019 (initial application date) to record the initial ROU Asset and lease liability and remove previously recorded asset and liability balances prior to transition.

In the case of ABC there is no cumulative effect adjustment to the opening balance of equity on January 1, 2019. This is primarily due to the practical expedients elected.

24

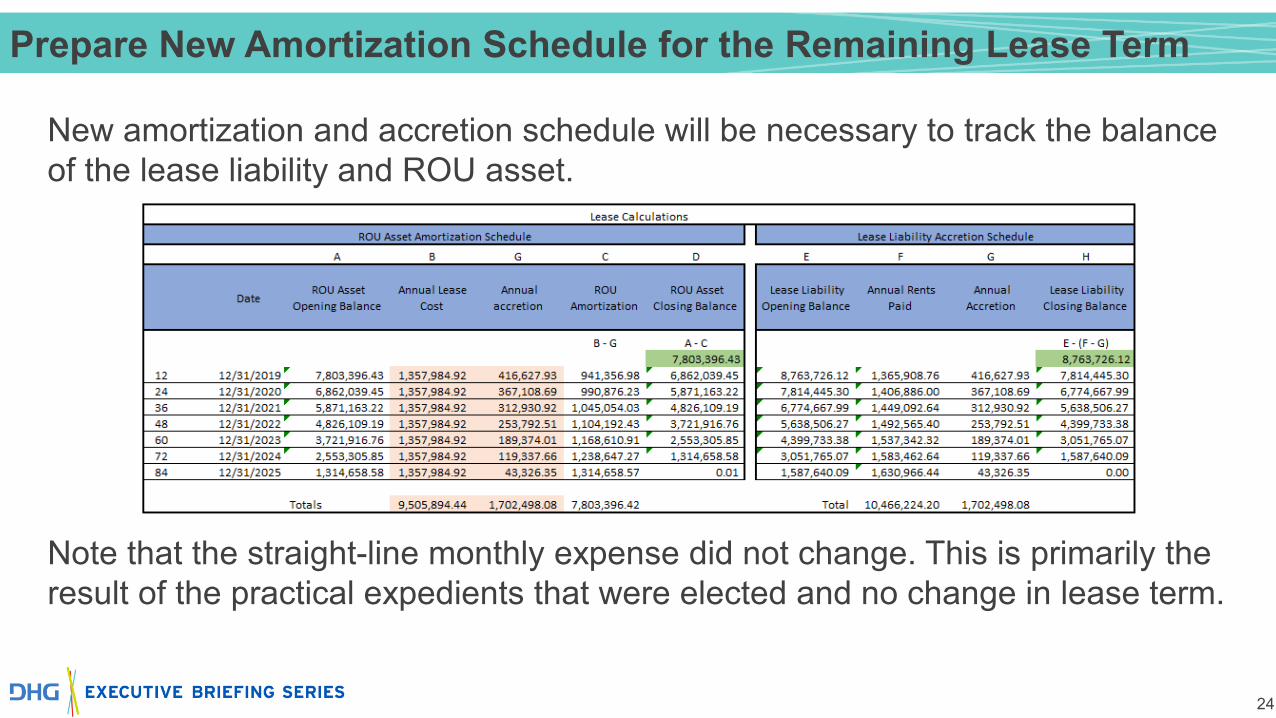

Prepare New Amortization Schedule for the Remaining Lease Term

New amortization and accretion schedule will be necessary to track the balance of the lease liability and ROU asset.

Note that the straight-line monthly expense did not change. This is primarily the result of the practical expedients that were elected and no change in lease term.

25

Disclosure Requirements

General description of leases

Leases that haven’t commenced yet but create significant rights and obligations

Significant assumptions and judgments in application of GAAP for leases

Basis, terms, and conditions for determining variable lease payments

Restrictions or covenants imposed by leases

Existence, terms, and conditions of residual value guarantees

Existence, terms, and conditions of any options to extend or terminate

26

Disclosures Relating to Lease Cost

Operating lease cost

Finance lease cost, with separate disclosure of amortization of ROU asset and interest on

lease liability

Variable lease cost Gross sublease income

Net gain or loss from sale leaseback

transactions

Cash paid for amounts included in lease

liabilities (separately for operating and financing

cash flows)

Supplemental noncash information on lease

liabilities resulting from obtaining ROU assets

Weighted-average remaining lease term

Weighted-average discount rate

Maturity analysis of finance and operating

lease liabilities (separately),

undiscounted for 5 years and thereafter

Reconciliation of undiscounted cash flows

to finance lease and operating lease liabilities

recognized on the balance sheet

Practical expedients elected

27

Disclosure

28

Disclosure

29

Disclosure

30

Disclosure

31

Disclosure

32

Disclosure

33

Disclosure

34

Disclosure

35

Recap Summary

Select transition method • Beginning of earliest period presented• Beginning of year of adoption

Select practical expedients

• Package of three (must be elected together)• Hindsight

Lease population • May take significant time to identify• Allocate sufficient resources

Transition calculation • Discount rate: implicit rate, incremental borrowing rate, risk-free rate

Disclosure • Expansion over ASC 840• Include both qualitative and quantitative disclosures

36

Q&A