time value of money - higher ed ebooks & digital … studying appendix 1, †you should be able...

TRANSCRIPT

After studying Appendix 1,you should be able to:

•1 Explain how compoundinterest works.

•2 Use future value andpresent value tables toapply compound interest toaccounting transactions.

Time Value of Money1Appendix

Broo

ksEl

liott/

iSto

ckph

oto

Dou

gN

orm

anC

rysta

ls/A

lam

y

NEL

Time value of money is widely used in business to measure today’s value of future cashoutflows or inflows and the amount to which liabilities (or assets) will grow when com-pound interest accumulates.

In transactions involving the borrowing and lending of money, the borrower usuallypays interest. In effect, interest is the time value of money. The amount of interest paidis determined by the length of the loan and the interest rate.

However, interest is not restricted to loans made to borrowers by banks. Invest-ments (particularly, investments in debt securities and savings accounts), installmentsales, and a variety of other contractual arrangements all include interest. In all cases,the arrangement between the two parties—the note, security, or purchase agreement—creates an asset in the accounting records of one party and a corresponding liability inthe accounting records of the other. All such assets and liabilities increase as interest isearned by the asset holder and decrease as payments are made by the liability holder.

COMPOUND INTEREST CALCULATIONSCompound interest is a method of calculating the time value of money in which inter-est is earned on the previous periods’ interest. That is, interest for the period is added tothe account balance and interest is earned on this new balance in the next period. Incomputing compound interest, it’s important to understand the difference between theinterest period and the interest rate:

• The interest period is the time interval between interest calculations.• The interest rate is the percentage that is multiplied by the beginning-of-period

balance to yield the amount of interest for that period.

The interest rate must agree with the interest period. For example, if the interest periodis one month, then the interest rate used to calculate interest must be stated as a percent-age ‘‘per month.’’

When an interest rate is stated in terms of a time period that differs from the interestperiod, the rate must be adjusted before interest can be calculated. For example, supposethat a bank advertises interest at a rate of 12% per year compounded monthly. Here, theinterest period would be one month. Since there are 12 interest periods in one year, theinterest rate for one month is one-twelfth the annual rate, or 1%. In other words, if therate statement period differs from the interest period, the stated rate must be divided bythe number of interest periods included in the rate statement period. A few examples ofadjusted rates follow:

Stated Rate Adjusted Rate for Computations

12% per year compounded semiannually 6% per six-month period (12%/2)12% per year compounded quarterly 3% per quarter (12%/4)12% per year compounded monthly 1% per month (12%/12)

If an interest rate is stated without reference to a rate statement period or aninterest period, assume that the period is one year. For example, both ‘‘12%’’ and‘‘12% per year’’ should be interpreted as 12% per year compounded annually.

Compound interest means that interest is computed on the original amount plusundistributed interest earned in previous periods. The simplest compound interest calcu-lation involves putting a single amount into an account and adding interest to it at theend of each period. CORNERSTONE A1-1 (p. 700) shows how to compute future valuesusing compound interest.

O B J E C T I V E•1Explain how compound interest works.

Appendix 1 Time Value of Money 699

NEL

As you can see in Cornerstone A1-1, the balance in the account continues to groweach month by an increasing amount of interest. The amount of monthly interestincreases because interest is compounded. In other words, interest is computed on accu-mulated interest as well as on principal. For example, February interest of $100.50 con-sists of $100 interest on the $20,000 principal and 50¢ interest on the $100 Januaryinterest ($100 3 0.005 ¼ 50¢).

In Cornerstone A1-1, the compound interest only amounts to $1.50. That mightseem relatively insignificant, but if the investment period is sufficiently long, the amountof compound interest grows large even at relatively small interest rates. For example,suppose your parents invested $1,000 at ½% per month when you were born with theobjective of giving you a university graduation present at age 21. How much would thatinvestment be worth after 21 years? The answer is $3,514. In 21 years, the compoundinterest is $2,514—more than 2½ times the original principal. Without compounding,interest over the same period would have been only $1,260.

The amount to which an account will grow when interest is compounded is thefuture value of the account. Compound interest calculations can assume two fundamen-tally different forms:

• calculations of future values• calculations of present values

As shown, calculations of future values are projections of future balances based on pastand future cash flows and interest payments. In contrast, calculations of present valuesare determinations of present amounts based on expected future cash flows.

C O R N E R S T O N EA 1 - 1

Computing Future Values UsingCompound Interest

Information:

An investor deposits $20,000 in a savings account on January 1, 2015. The bank pays interest of 6% per yearcompounded monthly.

Why:

When deposits earn compound interest, interest is earned on the interest.

Required:

Assuming that the only activity in the account is the deposit of interest at the end of each month, how much moneywill be in the account after the interest payment on March 31, 2015?

Solution:

Monthly interest will be ½% (6% per year/12 months).

Account balance, 1/1/15 $20,000.00January interest ($20,000.00 3 ½%) 100.00Account balance, 1/31/15 20,100.00February interest ($20,100.00 3 ½%) 100.50Account balance, 2/28/15 20,200.50March interest ($20,200.50 3 ½%) 101.00Account balance, 3/31/15 $20,301.50

Note: Here, interest was the only factor that altered the account balance after the initial deposit. In more complexsituations, the account balance is changed by subsequent deposits and withdrawals as well as by interest.Withdrawals reduce the balance and, therefore, the amount of interest in subsequent periods. Additional depositshave the opposite effect, increasing the balance and the amount of interest earned.

700 Appendix 1 Time Value of Money

NEL

PRESENT VALUE OF FUTURE CASH FLOWSWhenever a contract establishes a relationship between an initial amount borrowed orloaned and one or more future cash flows, the initial amount borrowed or loaned is thepresent value of those future cash flows. The present value can be interpreted in twoways:

• From the borrower’s viewpoint, it is the liability that will be exactly paid by thefuture payments.

• From the lender’s viewpoint, it is the receivable balance that will be exactly satisfiedby the future receipts.

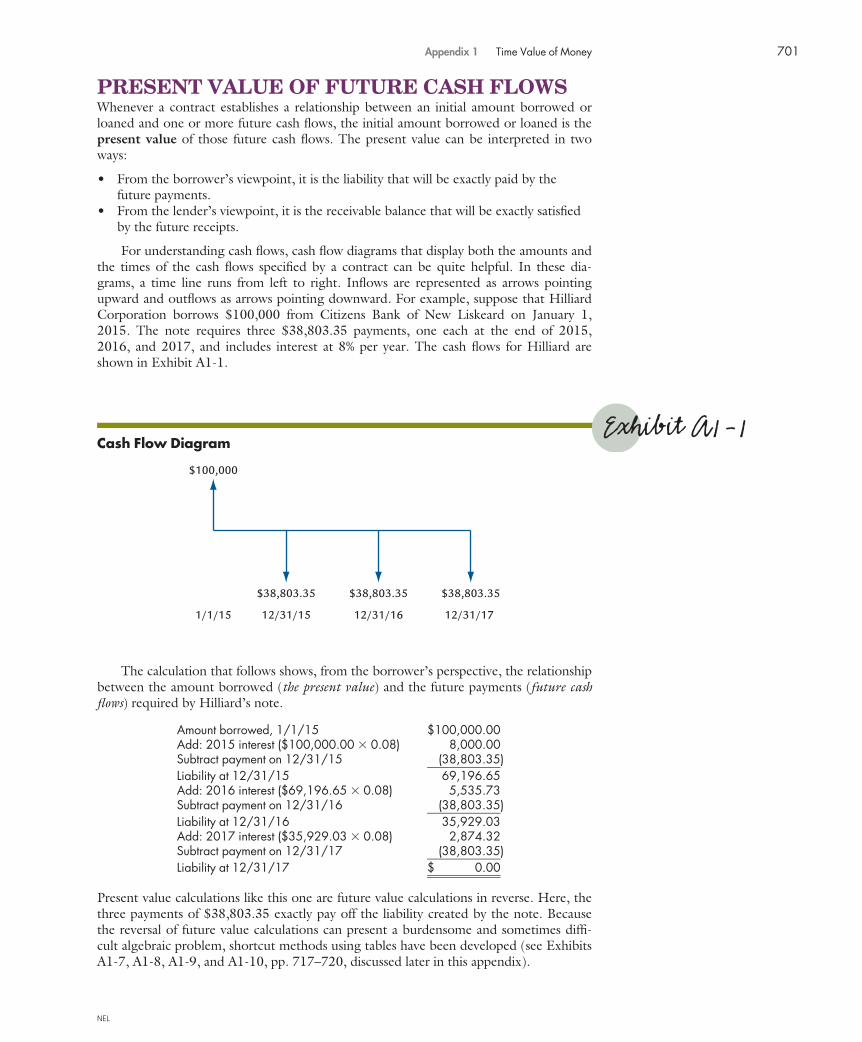

For understanding cash flows, cash flow diagrams that display both the amounts andthe times of the cash flows specified by a contract can be quite helpful. In these dia-grams, a time line runs from left to right. Inflows are represented as arrows pointingupward and outflows as arrows pointing downward. For example, suppose that HilliardCorporation borrows $100,000 from Citizens Bank of New Liskeard on January 1,2015. The note requires three $38,803.35 payments, one each at the end of 2015,2016, and 2017, and includes interest at 8% per year. The cash flows for Hilliard areshown in Exhibit A1-1.

The calculation that follows shows, from the borrower’s perspective, the relationshipbetween the amount borrowed (the present value) and the future payments (future cashflows) required by Hilliard’s note.

Amount borrowed, 1/1/15 $100,000.00Add: 2015 interest ($100,000.00 3 0.08) 8,000.00Subtract payment on 12/31/15 (38,803.35)Liability at 12/31/15 69,196.65Add: 2016 interest ($69,196.65 3 0.08) 5,535.73Subtract payment on 12/31/16 (38,803.35)Liability at 12/31/16 35,929.03Add: 2017 interest ($35,929.03 3 0.08) 2,874.32Subtract payment on 12/31/17 (38,803.35)Liability at 12/31/17 $ 0.00

Present value calculations like this one are future value calculations in reverse. Here, thethree payments of $38,803.35 exactly pay off the liability created by the note. Becausethe reversal of future value calculations can present a burdensome and sometimes diffi-cult algebraic problem, shortcut methods using tables have been developed (see ExhibitsA1-7, A1-8, A1-9, and A1-10, pp. 717–720, discussed later in this appendix).

Exhibit A1-1Cash Flow Diagram

$38,803.35 $38,803.35 $38,803.35

$100,000

1/1/15 12/31/15 12/31/16 12/31/17

Appendix 1 Time Value of Money 701

NEL

Interest and the Frequency of CompoundingThe number of interest periods into which a compound interest problem is divided canmake a significant difference in the amount of compound interest. For example, assumethat you are evaluating four 1-year investments, each of which requires an initial$10,000 deposit. All four investments earn interest at a rate of 12% per year, but theyhave different compounding periods. The data in Exhibit A1-2 show the impact of com-pounding frequency on future value. Investment D, which offers monthly compound-ing, accumulates $68 more interest by the end of the year than investment A, whichoffers only annual compounding.

FOUR BASIC COMPOUND INTERESTPROBLEMSAny present value or future value problems can be broken down into one or more of thefollowing four basic problems:

• computing the future value of a single amount• computing the present value of a single amount• computing the future value of an annuity• computing the present value of an annuity

Computing the Future Value of a Single AmountIn computing the future value of a single amount, the following elements are used:

• f: the cash flow• FV: the future value• n: the number of periods between the cash flow and the future value• i: the interest rate per period

To find the future value of a single amount, establish an account for f dollars and addcompound interest at i percent to that account for n periods:

FV ¼ (f )(1 þ i)n

The balance of the account after n periods is the future value.Because people frequently need to compute the future value of a single amount,

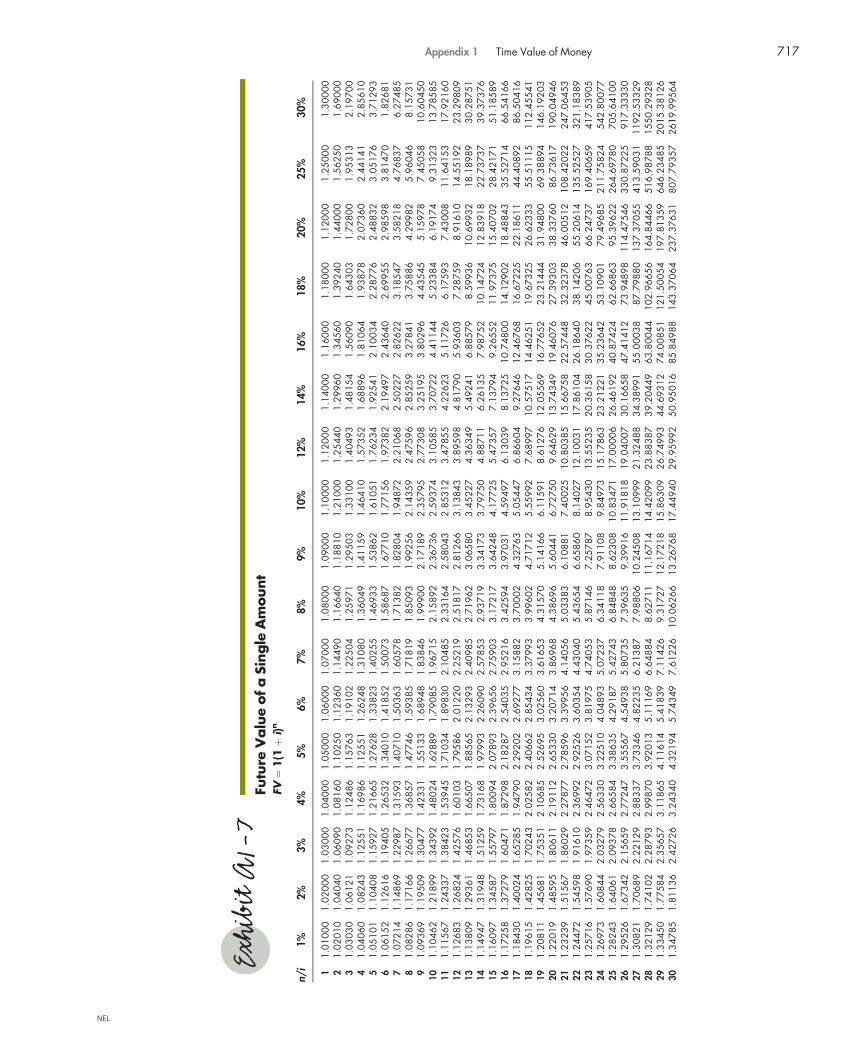

tables have been developed to make it easier. Therefore, instead of using the formulaabove, you could use the future value table in Exhibit A1-7 (p. 717), where M1 is themultiple that corresponds to the appropriate values of n and i:

FV ¼ (f )(M1)

For example, suppose Allied Financial loans $200,000 at a rate of 6% per year com-pounded annually to an auto dealership dealer for four years. Exhibit A1-3 shows how

Exhibit A1-2Effect of Interest Periods on Compound Interest

Investment Interest Period I N Calculation of Future Amount in One Year*

A 1 year 12% 1 ($10,000 3 1.12000) ¼$11,200B 6 months 6% 2 ($10,000 3 1.12360) ¼ 11,236C 1 quarter 3% 4 ($10,000 3 1.12551) ¼ 11,255D 1 month 1% 12 ($10,000 3 1.12683) ¼ 11,268

*The multipliers (1.12 for Investment A, 1.12360 for investment B, etc.) are taken from the future value table in Exhibit A1-7(p. 717).

O B J E C T I V E•2Use future value and present value tablesto apply compound interest to accountingtransactions.

702 Appendix 1 Time Value of Money

NEL

to compute the future value (FV) at the end of the four years—the amount that will berepaid. Assuming Allied’s viewpoint (the lender’s), using a compound interest calcula-tion, the unknown future value (FV) would be found as follows:

Amount loaned $200,000.00First year’s interest ($200,000.00 3 0.06) 12,000.00Loan receivable at end of first year 212,000.00Second year’s interest ($212,000.00 3 0.06) 12,720.00Loan receivable at end of second year 224,720.00Third year’s interest ($224,720.00 3 0.06) 13,483.20Loan receivable at end of third year 238,203.20Fourth year’s interest ($238,203.20 3 0.06) 14,292.19Loan receivable at end of the fourth year $252,495.39

As you can see, the amount of interest increases each year. This growth is the effect ofcomputing interest for each year based on an amount that includes the interest earned inprior years.

The shortcut calculation, using the future value table (Exhibit A1-7, p. 717), wouldbe as follows:

FV ¼ (f )(M1)¼ ($200,000)(1:26248)¼ $252,496

You can find M1 at the intersection of the 6% column (i ¼ 6%) and the fourth row (n ¼4) or by calculating 1.064. This multiple is the future value of the single amount afterhaving been borrowed (or invested) for four years at 6% interest. The future value of$200,000 is 200,000 times the multiple.

Note that there is a difference between the answer ($252,495.39) developed in thecompound interest calculation and the answer ($252,496) determined using the futurevalue table. This is because the numbers in the table have been rounded to five decimal pla-ces. If they were taken to eight digits (1.064 ¼ 1.26247696), the two answers would beequal. CORNERSTONE A1-2 shows how to compute the future value of a single amount.

Exhibit A1-3Future Value of a Single Amount: An Example

C O R N E R S T O N EA 1 - 2

Computing Future Value of a Single Amount

Information:

Kitchener Company sells an unneeded factory site for $200,000 on July 1, 2015. Kitchener expects to purchasea different site in 18 months so that it can expand into a new market. Meanwhile, Kitchener decides to invest the$200,000 in a money market fund that is guaranteed to earn 6%per year compounded semiannually (3% per six-month period).

(Continued)

Appendix 1 Time Value of Money 703

NEL

Computing the Present Value of a Single AmountIn computing the present value of a single amount, the following elements are used:

• f: the future cash flow• PV: the present value• n: the number of periods between the present time and the future cash flow• i: the interest rate per period

In present value problems, the interest rate is sometimes called the discount rate.

Why:

The future value of a single amount is the original cash flow pluscompound interest as of a specific future date.

Required:

1. Draw a cash flow diagram for this investment from Kitchener’s perspective.2. Calculate the amount of money in the money market fund on December 31, 2015, and prepare the journal

entry necessary to recognize interest income.3. Calculate the amount of money in the money market fund on December 31, 2016, and prepare the journal

entry necessary to recognize interest income.

Solution:

1.

15 15 16 16

2. Because we are calculating the value at 12/31/15, there is only one period:

FV ¼ (f )(FV of a Single Amount, 1 period, 3%)¼ ($200,000)(1:03)¼ $206,000

The excess of the amount of money over the original deposit is the interest earned from July 1 throughDecember 31, 2015.

Dec. 31, 2015 Cash 6,000Interest Income 6,000

(Record interest income)

3. FV ¼ (f )(FV of a Single Amount, 2 periods, 3%)¼ ($206,000)(1:032)¼ $218,545:40

The interest income for the year is the increase in the amount of money during 2016, which is $12,545.40($218,545.40 � $206,000). The journal entry to record interest income would be as follows:

Dec. 31, 2016 Cash 12,545.40Interest income 12,545.40

(Record interest income)

C O R N E R S T O N EA 1 - 2

(continued)

Assets 5 Liabilities 1

Shareholders’Equity

(Interest Income)þ6,000 þ6,000

Assets 5Liabilities1

Shareholders’Equity

(Interest Income)þ12,545.40 þ12,545.40

704 Appendix 1 Time Value of Money

NEL

To find the present value of a single amount, use the following equation:

PV ¼ f

(1 þ i)n

You could use the present value table in Exhibit A1-8 (p. 718), where M2 is the multiplefrom Exhibit A1-8 that corresponds to the appropriate values of n and i:

PV ¼ (f )(M2)

Suppose Marathon Oil has purchased property on which it plans to develop oilwells. The seller has agreed to accept a single $150,000,000 payment three years fromnow, when Marathon expects to be selling oil from the field. Assuming an interest rateof 7% per year, the present value of the amount to be received in three years from theborrower’s perspective can be calculated as shown in Exhibit A1-4.

The shortcut calculation, using the present value table (Exhibit A1-8, p. 718), wouldbe as follows:

PV ¼ (f )(M2)¼ ($150,000,000)(0:81630)¼ $122,445,000

You can find M2 at the intersection of the 7% column (i ¼ 7%) and the third row(n ¼ 3) in Exhibit A1-8 (p. 718) or by calculating [1/(1.07)3]. This multiple is the pres-ent value of a $1 cash inflow or outflow in three years at 7%. Thus, the present value of$150,000,000 is $150,000,000 times the multiple.

Although the future value calculation cannot be used to determine the presentvalue, it can be used to verify that the present value calculated by using the table is cor-rect. The following calculation is proof for the present value problem:

Calculated present value (PV) $122,445,000First year’s interest ($122,445,000 3 0.07) 8,571,150Loan payable at end of first year 131,016,150Second year’s interest ($131,016,150 3 0.07) 9,171,131Loan payable at end of second year 140,187,281Third year’s interest ($140,187,281 3 0.07) 9,813,110Loan payable at end of the third year (f ) $150,000,391

Again, the $391 difference between the amount here and the assumed $150,000,000cash flow is due to rounding.

When interest is compounded on the calculated present value of $122,445,000,then the present value calculation is reversed and we return to the future cash flowof $150,000,000. This reversal proves that $122,445,000 is the correct present value.CORNERSTONE A1-3 (p. 706) shows how to compute the present value of a single amount.

Exhibit A1-4Present Value of a Single Amount: An Example

Appendix 1 Time Value of Money 705

NEL

Computing the Future Value of an AnnuitySo far, we have been discussing problems that involve a single cash flow. However, thereare also instances of multiple cash flows one period apart. An annuity is a number ofequal cash flows: one to each interest period. For example, an investment in a securitythat pays $1,000 to an investor every December 31 for 10 consecutive years is an annu-ity. A loan repayment schedule that calls for a payment of $367.29 on the first day ofeach month can also be considered an annuity. (Although the number of days in amonth varies from 28 to 31, the interest period is defined as one month without regardto the number of days in each month.)

In computing the future value of an annuity, the following elements are used:

• f : the amount of each repeating cash flow• FV: the future value after the last (nth) cash flow• n: the number of cash flows• i: the interest rate per period

C O R N E R S T O N EA 1 - 3

Computing Present Value of a Single Amount

Information:

On October 1, 2015, Adelsman Manufacturing Company sold a new machine to Raul Inc. The machine repre-sented a new design that Raul was eager to place in service. Since Raul was unable to pay for the machine on thedate of purchase, Adelsman agreed to defer the $60,000 payment for 15 months. The appropriate rate of interestin such transactions is 8% per year compounded quarterly (2% per three-month period).

Why:

The present value of a single cash flow is the original cash flow that must be invested to produce a known value ata specific future date.

Required:

1. Draw the cash flow diagram for this deferred-payment purchase from Raul’s (the borrower’s) perspective.2. Calculate the present value of this deferred-payment purchase.3. Prepare the journal entry necessary to record the acquisition of the machine.

Solution:

1.

1515 16 16 16 16

2. FV ¼ (f )(FV of a Single Amount, 5 periods, 2%)¼ ($60,000)(0:90573)¼ $54,344

3.Oct. 1, 2015 Equipment 54,344

Note Payable 54,344(Record purchase of equipment)

Assets 5 Liabilities 1Shareholders’

Equityþ54,344 þ54,344

706 Appendix 1 Time Value of Money

NEL

To find the future value of an annuity, use the following equation:

FV ¼ (f )(1 þ i)n � 1

i

� �

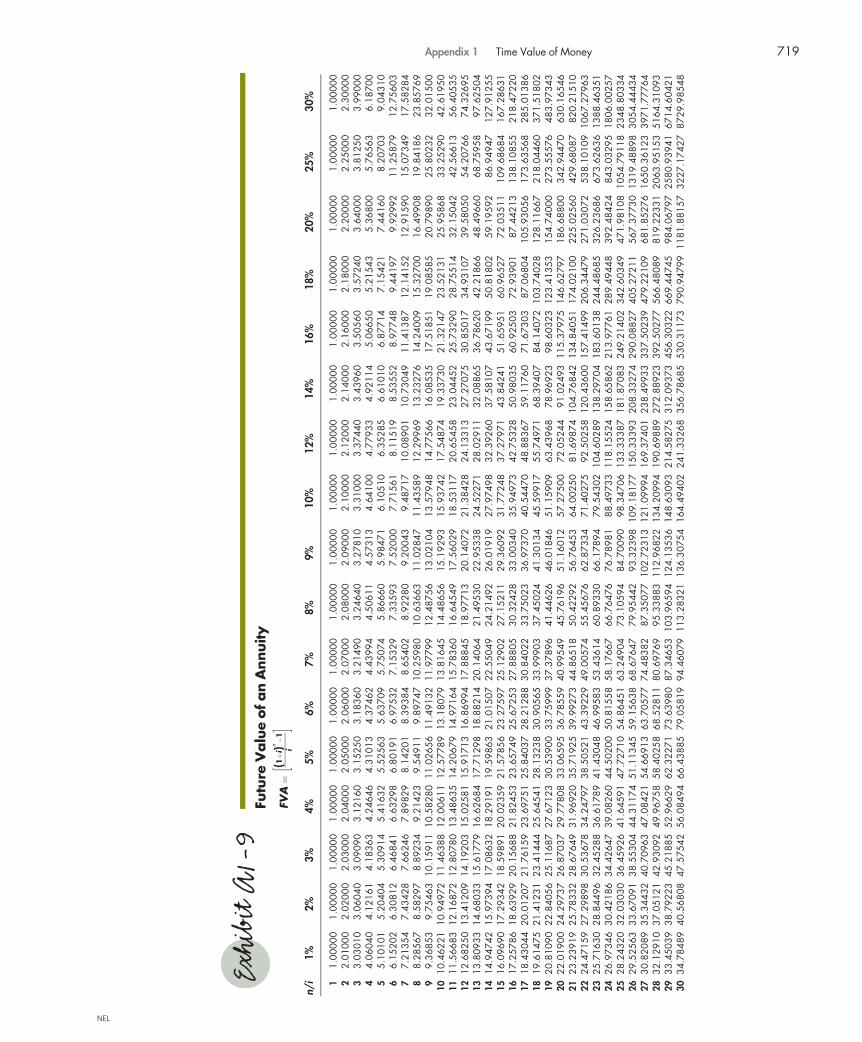

Alternatively, you could use the future value table in Exhibit A1-9 (p. 719), whereM3 is the multiple from Exhibit A1-9 that corresponds to the appropriate values of nand i:

FV ¼ (f )(M3)

Assume that CIBC wants to advertise a new savings program to its customers.The savings program requires the customers to make four annual payments of $5,000each, with the first payment due three years before the program ends. CIBC advertisesa 6% interest rate compounded annually. The future value of this annuity immediatelyafter the fourth cash payment from the investor’s perspective is shown in Exhibit A1-5.

Note that the first period in Exhibit A1-5 is drawn with a dotted line. When usingannuities, the time-value-of-money model assumes that all cash flows occur at the end ofa period. Therefore, the first cash flow in the future value of an annuity occurs at the endof the first period. However, since interest cannot be earned until the first deposit hasbeen made, the first period is identified as a no-interest period.

The future value (FV) can be computed as follows:

Interest for first period ($0 3 6%) $ 0.00First deposit 5,000.00Investment balance at end of first year 5,000.00Second year’s interest ($5,000.00 3 0.06) 300.00Second deposit 5,000.00Investment balance at end of second year 10,300.00Third year’s interest ($10,300.00 3 0.06) 618.00Third deposit 5,000.00Investment balance at end of third year 15,918.00Fourth year’s interest ($15,918.00 3 0.06) 955.08Fourth deposit 5,000.00Investment at end of fourth year $21,873.08

This calculation shows that the lender has accumulated a future value (FV) of $21,873.08by the end of the fourth period, immediately after the fourth cash investment.

The shortcut calculation, using the future value table (Exhibit A1-9, p. 719), wouldbe as follows:

FV ¼ (f )(M3)¼ ($5,000)(4:37462)¼ $21,873

Exhibit A1-5Future Value of an Annuity: An Example

Appendix 1 Time Value of Money 707

NEL

You can find M3 at the intersection of the 6% column (i ¼ 6%) and the fourth row (n ¼ 4)in Exhibit A1-9 (p. 719) or by calculating (1.064 � 1)/0.06. This multiple is the future valueof an annuity of four cash flows of $1 each at 6%. The future value of an annuity of $5,000cash flows is $5,000 times the multiple. Thus, the table allows us to calculate the future valueof an annuity by a single multiplication, no matter how many cash flows are involved. COR-NERSTONE A1-4 shows how to compute the future value of an annuity.

Present Value of an AnnuityIn computing the present value of an annuity, the following elements are used:

• f : the amount of each repeating cash flow• PV: the present value of the n future cash flows• n: the number of cash flows and periods• i: the interest (or discount) rate per period

C O R N E R S T O N EA 1 - 4

Computing Future Value of an Annuity

Information:

Greg Smith is a lawyer and CA specializing in retirement and estate planning. One of Greg’s clients, the owner ofa large farm, wants to retire in five years. To provide funds to purchase a retirement annuity from London Life atthe date of retirement, Greg asks the client to give him annual payments of $170,000, which Greg will deposit ina special fund that will earn 7% per year.

Why:

The future value of an annuity is the value of a series of equal cash flows made at regular intervals with compoundinterest at some specific future date.

Required:

1. Draw the cash flow diagram for the fund from Greg’s client’s perspective.2. Calculate the future value of the fund immediately after the fifth deposit.3. If Greg’s client needs $1,000,000 to purchase the annuity, how much must be deposited every year?

Solution:

1.

2. FV ¼ (f )(FV of an Annuity , 5 periods, 7%)¼ ($170,000)(5:75074)¼ $977,626

3. In this case, the future value is known, but the annuity amount (f ) is not:

1,000,000 ¼ (f )(FV of an Annuity , 5 periods, 7%)1,000,000 ¼ (f )(5:75074)

f ¼ 1,000,000=5:75074f ¼ $173,890:66

708 Appendix 1 Time Value of Money

NEL

To find the present value of an annuity, use the following equation:

PV ¼ (f )1 � 1

(1 þ i)n

i

You could also use the present value table in Exhibit A1-10 (p. 720), where M4 is themultiple from Exhibit A1-10 that corresponds to the appropriate values of n and i:

PV ¼ (f )(M4)

For example, assume that Xerox Corporation purchased a new machine for its man-ufacturing operations. The purchase agreement requires Xerox to make four equallyspaced payments of $24,154 each. The interest rate is 8% compounded annually and thefirst cash flow occurs one year after the purchase. Exhibit A1-6 shows how to determinethe present value of this annuity from Xerox’s (the borrower’s) perspective. Note that thesame concept applies to both the lender’s and borrower’s perspectives.

The shortcut calculation, using the present value table (Exhibit A1-10, p. 720), wouldbe as follows:

PV ¼ (f )(M4)¼ ($24,154)(3:31213)¼ $80,001:19

You can find M4 at the intersection of the 8% column (i ¼ 8%) and the fourth row (n ¼ 4)in Exhibit A1-10 or by solving for [1 � (1/1.084)]/0.08. This multiple is the presentvalue of an annuity of four cash flows of $1 each at 8%. The present value of an annuityof four $24,154 cash flows is $24,154 times the multiple.

Again, although the compound interest calculation is not used to determine thepresent value, it can be used to prove that the present value found using the table is cor-rect. The following calculation verifies the present value in the problem:

Calculated present value (PV) $ 80,001.19Interest for first year ($80,001.19 3 0.08) 6,400.10Less: First cash flow (24,154.00)Balance at end of first year 62,247.29Interest for second year ($62,247.29 3 0.08) 4,979.78Less: Second cash flow (24,154.00)Balance at end of second year 43,073.07Interest for third year ($43,073.07 3 0.08) 3,445.85Less: Third cash flow (24,154.00)Balance at end of third year 22,364.92Interest for fourth year ($22,364.92 3 0.08) 1,789.19Less: Fourth cash flow (24,154.00)Balance at end of fourth year $ 0.11

This proof uses a compound interest calculation that is the reverse of the present valueformula. If the present value (PV) calculated with the formula is correct, then the proof

Exhibit A1-6Present Value of An Annuity: An Example

Appendix 1 Time Value of Money 709

NEL

should end with a balance of zero immediately after the last cash flow. This proofends with a balance of $0.11 because of rounding in the proof itself and in the table inExhibit A1-10 (p. 720).

CORNERSTONE A1-5 shows how to compute the present value of an annuity.

SUMMARY OF LEARNING OBJECTIVES

LO1. Explain how compound interest works.• In transactions involving the borrowing and lending of money, it is custom-

ary for the borrower to pay interest.• With compound interest, interest for the period is added to the account and

interest is earned on the total balance in the next period.• Compound interest calculations require careful specification of the interest

period and the interest rate.

C O R N E R S T O N EA 1 - 5

Computing Present Value of an Annuity

Information:

Windsor Builders purchased a subdivision site from the Royal Bank on January 1, 2015. Windsor gave the bankan installment note. The note requires Windsor to make four annual payments of $600,000 each on December31 of each year, beginning in 2015. Interest is computed at 9%.

Why:

The present value of an annuity is the value of a series of equal future cash flows made at regular intervals withcompound interest discounted back to today.

Required:

1. Draw the cash flow diagram for this purchase from Windsor’s perspective.2. Calculate the cost of the land as recorded by Windsor on January 1, 2015.3. Prepare the journal entry that Windsor will make to record the purchase of the land.

Solution:

1.

4

15 15 16 17 18

2. PV ¼ (f )(PV of an Annuity , 4 periods, 9%)¼ ($600,000)(3:23972)¼ $1,943,832

3.Jan. 1, 2015 Land 1,943,832

Notes Payable 1,943,832(Record purchase of land)

Assets 5 Liabilities 1Shareholders’

Equityþ1,943,832 þ1,943,832

710 Appendix 1 Time Value of Money

NEL

LO2. Use future value and present value tables to apply compound interest to accountingtransactions.• Cash flows are described as either

• single cash flows, or• annuities.

• An annuity is a number of equal cash flows made at regular intervals.• All other cash flows are a series of one or more single cash flows.• Accounting for such cash flows may require

• calculation of the amount to which a series of cash flows will grow when interest iscompounded (i.e., the future value) or

• the amount a series of future cash flows is worth today after taking into accountcompound interest (i.e., the present value).

C O R N E R S T O N E SFOR APPENDIX 1

CORNERSTONE A1-1 Computing future values using compound interest (p. 700)

CORNERSTONE A1-2 Computing future value of a single amount (p. 703)

CORNERSTONE A1-3 Computing present value of a single amount (p. 706)

CORNERSTONE A1-4 Computing future value of an annuity (p. 708)

CORNERSTONE A1-5 Computing present value of an annuity (p. 710)

KEY TERMS

Annuity (p. 706)Compound interest (p. 699)Future value (p. 700)Interest period (p. 699)

Interest rate (p. 699)Present value (p. 701)Time value of money (p. 699)

DISCUSSION QUESTIONS

1. Why does money have a time value?2. Describe the four basic time-value-of-money problems.3. How is compound interest computed? What is a future value? What is a present value?4. Define an annuity in general terms. Describe the cash flows related to an annuity from the

viewpoint of the lender in terms of receipts and payments.5. Explain how to use time-value-of-money calculations to measure an installment note liability.

CORNERSTONE EXERCISES

Cornerstone Exercise A1-1 Explain How Compound Interest WorksJim Emig has $6,000.

Required:Calculate the future value of the $6,000 at 12% compounded quarterly for five years. (Note:Round answers to two decimal places.)

OBJECTIVE•1CORNERSTONE A1-1

Appendix 1 Time Value of Money 711

NEL

Cornerstone Exercise A1-2 Use Future Value and Present Value Tables to ApplyCompound InterestCathy Lumbattis inherited $140,000 from an aunt.

Required:If Cathy decides not to spend her inheritance but to leave the money in her savings account untilshe retires in 15 years, how much money will she have, assuming an annual interest rate of 8%,compounded semiannually? (Note: Round answers to two decimal places.)

Cornerstone Exercise A1-3 Use Future Value and Present Value Tables to ApplyCompound InterestLuAnn Bean will receive $7,000 in seven years.

Required:What is the present value at 7% compounded annually? (Note: Round answers to two decimalplaces.)

Cornerstone Exercise A1-4 Use Future Value and Present Value Tables to ApplyCompound InterestA bank is willing to lend money at 6% interest, compounded annually.

Required:How much would the bank be willing to loan you in exchange for a payment of $600 four yearsfrom now? (Note: Round answers to two decimal places.)

Cornerstone Exercise A1-5 Use Future Value and Present Value Tables to ApplyCompound InterestEd Flores wants to save some money so that he can make a down payment of $3,000 on a carwhen he graduates from university in four years.

Required:If Ed opens a savings account and earns 3% on his money, compounded annually, how much willhe have to invest now? (Note: Round answers to two decimal places.)

Cornerstone Exercise A1-6 Use Future Value and Present Value Tables to ApplyCompound InterestKristen Lee makes equal deposits of $500 semiannually for four years.

Required:What is the future value at 8%? (Note: Round answers to two decimal places.)

Cornerstone Exercise A1-7 Use Future Value and Present Value Tables to ApplyCompound InterestChuck Russo, a high school math teacher, wants to set up a RRSP account into which he will de-posit $2,000 per year. He plans to teach for 20 more years and then retire.

Required:If the interest on his account is 7% compounded annually, how much will be in his account whenhe retires? (Note: Round answers to two decimal places.)

Cornerstone Exercise A1-8 Use Future Value Tables to Apply Compound InterestLarson Lumber makes annual deposits of $500 at 6% compounded annually for three years.

Required:What is the future value of these deposits? (Note: Round answers to two decimal places.)

OBJECTIVE•2CORNERSTONE A1-2

OBJECTIVE•2CORNERSTONE A1-3

OBJECTIVE•2CORNERSTONE A1-3

OBJECTIVE•2CORNERSTONE A1-4

OBJECTIVE•2CORNERSTONE A1-4

OBJECTIVE•2CORNERSTONE A1-4

OBJECTIVE•2CORNERSTONE A1-4

712 Appendix 1 Time Value of Money

NEL

Cornerstone Exercise A1-9 Use Future Value and Present Value Tables to ApplyCompound InterestMichelle Legrand can earn 6%.

Required:How much would have to be deposited in a savings account today in order for Michelle to beable to make equal annual withdrawals of $200 at the end of each of the next 10 years? (Note:Round answers to two decimal places.) The balance at the end of the last year would be zero.

Cornerstone Exercise A1-10 Use Future Value and Present Value Tables to ApplyCompound InterestBarb Muller wins the lottery. She wins $20,000 per year to be paid for 10 years. The provinceoffers her the choice of a cash settlement now instead of the annual payments for 10 years.

Required:If the interest rate is 6%, what is the amount the province will offer for a settlement today? (Note:Round answers to two decimal places.)

EXERCISES

Exercise A1-11 Practice with TablesRefer to the appropriate tables in the text.

Required:Note: Round answers to two decimal places. Determine:

a. the future value of a single cash flow of $5,000 that earns 7% interest compounded annuallyfor 10 years.

b. the future value of an annual annuity of 10 cash flows of $500 each that earns 7% com-pounded annually.

c. the present value of $5,000 to be received 10 years from now, assuming that the interest(discount) rate is 7% per year.

d. the present value of an annuity of $500 per year for 10 years for which the interest (discount)rate is 7% per year and the first cash flow occurs one year from now.

Exercise A1-12 Practice with TablesRefer to the appropriate tables in the text.

Required:Note: Round answers to two decimal places. Determine:

a. the present value of $1,200 to be received in seven years, assuming that the interest (dis-count) rate is 8% per year.

b. the present value of an annuity of seven cash flows of $1,200 each (one at the end of each ofthe next seven years) for which the interest (discount) rate is 8% per year.

c. the future value of a single cash flow of $1,200 that earns 8% per year for seven years.d. the future value of an annuity of seven cash flows of $1,200 each (one at the end of each of

the next seven years), assuming that the interest rate is 8% per year.

Exercise A1-13 Future ValuesRefer to the appropriate tables in the text.

Required:Note: Round answers to two decimal places. Determine:

a. the future value of a single deposit of $15,000 that earns compound interest for four years atan interest rate of 10% per year.

b. the annual interest rate that will produce a future value of $13,416.80 in six years from a sin-gle deposit of $8,000.

OBJECTIVE•2CORNERSTONE A1-5

OBJECTIVE•2CORNERSTONE A1-5

OBJECTIVE•2

OBJECTIVE•2

OBJECTIVE•2

Appendix 1 Time Value of Money 713

NEL

c. the size of annual cash flows for an annuity of nine cash flows that will produce a future valueof $79,428.10 at an interest rate of 9% per year.

d. the number of periods required to produce a future value of $17,755.50 from an initial de-posit of $7,500 if the annual interest rate is 9%.

Exercise A1-14 Future Values and Long-Term InvestmentsFired Up Pottery Inc. engaged in the following transactions during 2015:

a. On January 1, 2015, Fired Up deposited $12,000 in a certificate of deposit paying 6% inter-est compounded semiannually (3% per six-month period). The certificate will mature on De-cember 31, 2018.

b. On January 1, 2015, Fired Up established an account with Rookwood Investment Manage-ment. Fired Up will make quarterly payments of $2,500 to Rookwood beginning on March31, 2015, and ending on December 31, 2016. Rookwood guarantees an interest rate of 8%compounded quarterly (2% per three-month period).

Required:1. Prepare the cash flow diagram for each of these two investments.2. Calculate the amount to which each of these investments will accumulate at maturity. (Note:

Round answers to two decimal places.)

Exercise A1-15 Future ValuesOn January 1, Beth Walid made a single deposit of $8,000 in an investment account that earns8% interest.

Required:Note: Round answers to two decimal places.

1. Calculate the balance in the account in five years assuming the interest is compounded annually.2. Determine how much interest will be earned on the account in seven years if interest is com-

pounded annually.3. Calculate the balance in the account in five years assuming the 8% interest is compounded

quarterly.

Exercise A1-16 Future ValuesKashmir Transit Company invested $70,000 in a corporate bond on June 30, 2015. The bond earns12% interest compounded monthly (1% per month) and matures on March 31, 2016.

Required:Note: Round answers to two decimal places.

1. Prepare the cash flow diagram for this investment.2. Determine the amount Kashmir will receive when the bond matures.3. Determine how much interest Kashmir will earn on this investment from June 30, 2015,

through December 31, 2015.

Exercise A1-17 Present ValuesRefer to the appropriate tables in the text.

Required:Note: Round answers to two decimal places. Determine:

a. the present value of a single $14,000 cash flow in seven years if the interest (discount) rate is8% per year.

b. the number of periods for which $5,820 must be invested at an annual interest (discount)rate of 7% to produce an investment balance of $10,000.

c. the size of the annual cash flow for a 25-year annuity with a present value of $49,113 and anannual interest rate of 9%. One payment is made at the end of each year.

d. the annual interest rate at which an investment of $2,542 will provide for a single $4,000cash flow in four years.

e. the annual interest rate earned by an annuity that costs $17,119 and provides 15 paymentsof $2,000 each, one at the end of each of the next 15 years.

OBJECTIVE•2

OBJECTIVE•2

OBJECTIVE•2

OBJECTIVE•2

714 Appendix 1 Time Value of Money

NEL

Exercise A1-18 Present ValuesWeinstein Company signed notes to make the following two purchases on January 1, 2015:

a. a new piece of equipment for $60,000, with payment deferred until December 31, 2016.The appropriate interest rate is 9% compounded annually.

b. a small building from Johnston Builders. The terms of the purchase require a $75,000 pay-ment at the end of each quarter, beginning March 31, 2015, and ending June 30, 2017.The appropriate interest rate is 2% per quarter.

Required:Note: Round answers to two decimal places.

1. Prepare the cash flow diagrams for these two purchases.2. Prepare the entries to record these purchases in Weinstein’s journal.3. Prepare the cash payment and interest expense entries for purchase b at March 31, 2015, and

June 30, 2015.4. Prepare the adjusting entry for purchase a at December 31, 2015.

Exercise A1-19 Present ValuesKrista Kellman has an opportunity to purchase a government security that will pay $200,000 infive years.

Required:Note: Round answers to two decimal places.

1. Calculate what Krista would pay for the security if the appropriate interest (discount) rate is6% compounded annually.

2. Calculate what Krista would pay for the security if the appropriate interest (discount) rate is10% compounded annually.

3. Calculate what Krista would pay for the security if the appropriate interest (discount) rate is6% compounded semiannually.

Exercise A1-20 Future Values of an AnnuityOn December 31, 2015, Natalie Livingston signs a contract to make annual deposits of $4,200 inan investment account that earns 10%. The first deposit is made on December 31, 2015.

Required:Note: Round answers to two decimal places.

1. Calculate what the balance in this investment account will be just after the seventh deposithas been made if interest is compounded annually.

2. Determine how much interest will have been earned on this investment account just afterthe seventh deposit has been made if interest is compounded annually.

Exercise A1-21 Future Values of an AnnuityEssex Savings Bank pays 8% interest compounded weekly (0.154% per week) on savings accounts.The bank has asked your help in preparing a table to show potential customers the number ofdollars that will be available at the end of 10-, 20-, 30-, and 40-week periods during which thereare weekly deposits of $1, $5, $10, or $50. The following data are available:

Length of Annuity Future Value of Annuity at an Interest Rateof 0.154% per Week

10 weeks 10.069620 weeks 20.295330 weeks 30.679640 weeks 41.2250

OBJECTIVE•2

OBJECTIVE•2

OBJECTIVE•2

OBJECTIVE•2

Appendix 1 Time Value of Money 715

NEL

Required:Complete a table similar to the one below. (Note: Round answers to two decimal places.)

Amount of Each Deposit

Number of Deposits $1 $5 $10 $50

10203040

Exercise A1-22 Future Value of a Single Cash FlowJimenez Products has just been paid $25,000 by Shirley Enterprises, which has owed Jimenezthis amount for 30 months but been unable to pay because of financial difficulties. Had it beenable to invest this cash, Jimenez assumes that it would have earned an interest rate of 12% com-pounded monthly (1% per month).

Required:Note: Round answers to two decimal places.

1. Prepare a cash flow diagram for the investment that could have been made if Shirley had paid30 months ago.

2. Determine how much Jimenez has lost by not receiving the $25,000 when it was due30 months ago.

3. Conceptual Connection: Indicate whether Jimenez would make an entry to account for thisloss. Why, or why not?

Exercise A1-23 Installment SaleWilke Properties owns land on which natural gas wells are located. Windsor Gas Company signsa note to buy this land from Wilke on January 1, 2015. The note requires Windsor to pay Wilke$775,000 per year for 25 years. The first payment is to be made on December 31, 2015. Theappropriate interest rate is 9% compounded annually.

Required:Note: Round answers to two decimal places.

1. Prepare a diagram of the appropriate cash flows from Windsor Gas’s perspective.2. Determine the present value of the payments.3. Indicate what entry Windsor Gas should make at January 1, 2015.

Exercise A1-24 Installment SaleBailey’s Billiards sold a pool table to Sheri Sipka on October 31, 2015. The terms of the sale areno money down and payments of $50 per month for 30 months, with the first payment due onNovember 30, 2015. The table they sold to Sipka cost Bailey’s $800, and Bailey uses a perpetualinventory system. Bailey’s uses an interest rate of 12% compounded monthly (1% per month).

Required:Note: Round answers to two decimal places.

1. Prepare the cash flow diagram for this sale.2. Calculate the amount of revenue Bailey’s should record on October 31, 2015.3. Prepare the journal entries to record the sale on October 31. Assume that Bailey’s records

cost of goods sold at the time of the sale (perpetual inventory accounting).4. Determine how much interest income Bailey’s will record from October 31, 2015, through

December 31, 2015.5. Determine how much Bailey’s 2015 income before taxes increased from this sale.

OBJECTIVE•2

OBJECTIVE•2

OBJECTIVE•2

716 Appendix 1 Time Value of Money

NEL

Exhi

bitA

1-7

Futu

reV

alu

eofa

Sing

leA

mount

FV

¼1

(1þ

i)n

n/i

1%2%

3%4%

5%6%

7%8%

9%10

%12

%14

%16

%18

%20

%25

%30

%

11.

0100

01.

0200

01.

0300

01.

0400

01.

0500

01.

0600

01.

0700

01.

0800

01.

0900

01.

1000

01.

1200

01.

1400

01.

1600

01.

1800

01.

1200

01.

2500

01.

3000

02

1.02

010

1.04

040

1.06

090

1.08

160

1.10

250

1.12

360

1.14

490

1.16

640

1.18

810

1.21

000

1.25

440

1.29

960

1.34

560

1.39

240

1.44

000

1.56

250

1.69

000

31.

0303

01.

0612

11.

0927

31.

1248

61.

1576

31.

1910

21.

2250

41.

2597

11.

2950

31.

3310

01.

4049

31.

4815

41.

5609

01.

6430

31.

7280

01.

9531

32.

1970

04

1.04

060

1.08

243

1.12

551

1.16

986

1.12

551

1.26

248

1.31

080

1.36

049

1.41

159

1.46

410

1.57

352

1.68

896

1.81

064

1.93

878

2.07

360

2.44

141

2.85

610

51.

0510

11.

1040

81.

1592

71.

2166

51.

2762

81.

3382

31.

4025

51.

4693

31.

5386

21.

6105

11.

7623

41.

9254

12.

1003

42.

2877

62.

4883

23.

0517

63.

7129

36

1.06

152

1.12

616

1.19

405

1.26

532

1.34

010

1.41

852

1.50

073

1.58

687

1.67

710

1.77

156

1.97

382

2.19

497

2.43

640

2.69

955

2.98

598

3.81

470

1.82

681

71.

0721

41.

1486

91.

2298

71.

3159

31.

4071

01.

5036

31.

6057

81.

7138

21.

8280

41.

9487

22.

2106

82.

5022

72.

8262

23.

1854

73.

5821

84.

7683

76.

2748

58

1.08

286

1.17

166

1.26

677

1.36

857

1.47

746

1.59

385

1.71

819

1.85

093

1.99

256

2.14

359

2.47

596

2.85

259

3.27

841

3.75

886

4.29

982

5.96

046

8.15

731

91.

0936

91.

1950

91.

3047

71.

4233

11.

5513

31.

6894

81.

8384

61.

9990

02.

1718

92.

3579

52.

7730

83.

2519

53.

8029

64.

4354

55.

1597

87.

4505

810

.604

5010

1.10

462

1.21

899

1.34

392

1.48

024

1.62

889

1.79

085

1.96

715

2.15

892

2.36

736

2.59

374

3.10

585

3.70

722

4.41

144

5.23

384

6.19

174

9.31

323

13.7

8585

111.

1156

71.

2433

71.

3842

31.

5394

51.

7103

41.

8983

02.

1048

52.

3316

42.

5804

32.

8531

23.

4785

54.

2262

35.

1172

66.

1759

37.

4300

811

.641

5317

.921

6012

1.12

683

1.26

824

1.42

576

1.60

103

1.79

586

2.01

220

2.25

219

2.51

817

2.81

266

3.13

843

3.89

598

4.81

790

5.93

603

7.28

759

8.91

610

14.5

5192

23.2

9809

131.

1380

91.

2936

11.

4685

31.

6650

71.

8856

52.

1329

32.

4098

52.

7196

23.

0658

03.

4522

74.

3634

95.

4924

16.

8857

98.

5993

610

.699

3218

.189

8930

.287

5114

1.14

947

1.31

948

1.51

259

1.73

168

1.97

993

2.26

090

2.57

853

2.93

719

3.34

173

3.79

750

4.88

711

6.26

135

7.98

752

10.1

4724

12.8

3918

22.7

3737

39.3

7376

151.

1609

71.

3458

71.

5579

71.

8009

42.

0789

32.

3965

62.

7590

33.

1721

73.

6424

84.

1772

55.

4735

77.

1379

49.

2655

211

.973

7515

.407

0228

.421

7151

.185

8916

1.17

258

1.37

279

1.60

471

1.87

298

2.18

287

2.54

035

2.95

216

3.42

594

3.97

031

4.59

497

6.13

039

8.13

725

10.7

4800

14.1

2902

18.4

8843

35.5

2714

66.5

4166

171.

1843

01.

4002

41.

6528

51.

9479

02.

2920

22.

6927

73.

1588

23.

7000

24.

3276

35.

0544

76.

8660

49.

2764

612

.467

6816

.672

2522

.186

1144

.408

9286

.504

1618

1.19

615

1.42

825

1.70

243

2.02

582

2.40

662

2.85

434

3.37

993

3.99

602

4.71

712

5.55

992

7.68

997

10.5

7517

14.4

6251

19.6

7325

26.6

2333

55.5

1115

112.

4554

119

1.20

811

1.45

681

1.75

351

2.10

685

2.52

695

3.02

560

3.61

653

4.31

570

5.14

166

6.11

591

8.61

276

12.0

5569

16.7

7652

23.2

1444

31.9

4800

69.3

8894

146.

1920

320

1.22

019

1.48

595

1.80

611

2.19

112

2.65

330

3.20

714

3.86

968

4.38

696

5.60

441

6.72

750

9.64

629

13.7

4349

19.4

6076

27.3

9303

38.3

3760

86.7

3617

190.

0494

621

1.23

239

1.51

567

1.86

029

2.27

877

2.78

596

3.39

956

4.14

056

5.03

383

6.10

881

7.40

025

10.8

0385

15.6

6758

22.5

7448

32.3

2378

46.0

0512

108.

4202

224

7.06

453

221.

2447

21.

5459

81.

9161

02.

3699

22.

9252

63.

6035

44.

4304

05.

4365

46.

6586

08.

1402

712

.100

3117

.861

0426

.186

4038

.142

0655

.206

1413

5.52

527

321.

1838

923

1.25

716

1.57

690

1.97

359

2.46

472

3.07

152

3.81

975

4.74

053

5.87

146

7.25

787

8.95

430

13.5

5235

20.3

6158

30.3

7622

45.0

0763

66.2

4737

169.

4065

941

7.53

905

241.

2697

31.

6084

42.

0327

92.

5633

03.

2251

04.

0489

35.

0723

76.

3411

87.

9110

89.

8497

315

.178

6323

.212

2135

.236

4253

.109

0179

.496

8521

1.75

824

542.

8007

725

1.28

243

1.64

061

2.09

378

2.66

584

3.38

635

4.29

187

5.42

743

6.84

848

8.62

308

10.8

3471

17.0

0006

26.4

6192

40.8

7424

62.6

6863

95.3

9622

264.

6978

070

5.64

100

261.

2952

61.

6734

22.

1565

92.

7724

73.

5556

74.

5493

85.

8073

57.

3963

59.

3991

611

.918

1819

.040

0730

.166

5847

.414

1273

.948

9811

4.47

546

330.

8722

591

7.33

330

271.

3082

11.

7068

92.

2212

92.

8833

73.

7334

64.

8223

56.

2138

77.

9880

610

.245

0813

.109

9921

.324

8834

.389

9155

.000

3887

.798

8013

7.37

055

413.

5903

111

92.5

3329

281.

3212

91.

7410

22.

2879

32.

9987

03.

9201

35.

1116

96.

6488

48.

6271

111

.167

1414

.420

9923

.883

8739

.204

4963

.800

4410

2.96

656

164.

8446

651

6.98

788

1550

.293

2829

1.33

450

1.77

584

2.35

657

3.11

865

4.11

614

5.41

839

7.11

426

9.31

727

12.1

7218

15.8

6309

26.7

4993

44.6

9312

74.0

0851

121.

5005

419

7.81

359

646.

2348

520

15.3

8126

301.

3478

51.

8113

62.

4272

63.

2434

04.

3219

45.

7434

97.

6122

610

.062

6613

.267

6817

.449

4029

.959

9250

.950

1685

.849

8814

3.37

064

237.

3763

180

7.79

357

2619

.995

64

Appendix 1 Time Value of Money 717

NEL

Exhi

bitA

1-8

Pre

sentV

alu

eofa

Sing

leA

mount

PV

¼1

(1þ

i)n

n/i

1%2%

3%4%

5%6%

7%8%

9%10

%12

%14

%16

%18

%20

%25

%30

%

10.

9901

00.

9803

90.

9708

70.

9615

40.

9523

80.

9434

00.

9345

80.

9259

30.

9174

30.

9090

90.

8928

60.

8771

90.

8620

70.

8474

60.

8333

30.

8000

00.

7692

32

0.98

030

0.96

117

0.94

260

0.92

456

0.90

703

0.89

000

0.87

344

0.85

734

0.84

168

0.82

645

0.79

719

0.76

947

0.74

316

0.71

818

0.69

444

0.64

000

0.59

172

30.

9705

90.

9423

20.

9151

40.

8890

00.

8638

40.

8396

20.

8163

00.

7938

30.

7721

80.

7513

10.

7117

80.

6749

70.

6406

60.

6086

30.

5787

00.

5120

00.

4551

74

0.96

098

0.92

385

0.88

849

0.85

480

0.82

270

0.79

209

0.76

290

0.73

503

0.70

843

0.68

301

0.63

552

0.59

208

0.55

229

0.51

579

0.48

225

0.40

960

0.35

013

50.

9514

70.

9057

30.

8626

10.

8219

30.

7835

30.

7472

60.

7129

90.

6805

80.

6499

30.

6209

20.

5674

30.

5193

70.

4761

10.

4371

10.

4018

80.

3276

80.

2693

36

0.94

205

0.88

797

0.83

748

0.79

031

0.74

622

0.70

496

0.66

634

0.63

017

0.59

627

0.56

447

0.50

663

0.45

559

0.41

044

0.37

043

0.33

490

0.26

214

0.20

718

70.

9327

20.

8705

60.

8130

90.

7599

20.

7106

80.

6650

60.

6227

50.

5834

90.

5470

30.

5131

60.

4523

50.

3996

40.

3538

30.

3139

30.

2790

80.

2097

20.

1593

78

0.92

348

0.85

349

0.78

941

0.73

069

0.67

684

0.62

741

0.58

201

0.54

027

0.50

187

0.46

651

0.40

388

0.35

056

0.30

503

0.26

604

0.23

257

0.16

777

0.12

259

90.

9143

40.

8367

60.

7664

20.

7025

90.

6446

10.

5919

00.

5439

30.

5002

50.

4604

30.

4241

00.

3606

10.

3075

10.

2629

50.

2254

60.

1938

10.

1342

20.

0943

010

0.90

529

0.82

035

0.74

409

0.67

556

0.61

391

0.55

839

0.50

835

0.46

319

0.42

241

0.38

554

0.32

197

0.26

974

0.22

668

0.19

106

0.16

151

0.10

737

0.07

254

110.

8963

20.

8042

60.

7224

20.

6495

80.

5846

80.

5267

90.

4750

90.

4288

80.

3875

30.

3504

90.

2874

80.

2366

20.

1954

20.

1619

20.

1345

90.

0859

00.

0228

012

0.88

745

0.78

849

0.70

138

0.62

460

0.55

684

0.49

697

0.44

401

0.39

711

0.35

553

0.31

863

0.25

668

0.20

756

0.16

846

0.13

722

0.11

216

0.06

872

0.04

292

130.

8786

60.

7730

30.

6809

50.

6005

70.

5303

20.

4688

40.

4149

60.

3677

00.

3261

80.

2896

60.

2291

70.

1820

70.

1452

30.

1162

90.

0934

60.

0549

80.

0330

214

0.86

996

0.75

788

0.66

112

0.57

748

0.50

507

0.44

230

0.38

782

0.34

046

0.29

925

0.26

333

0.20

462

0.15

971

0.12

520

0.09

855

0.07

789

0.04

398

0.02

540

150.

8613

50.

7430

10.

6418

60.

5552

60.

4810

20.

4172

70.

3624

50.

3152

40.

2745

40.

2393

90.

1827

00.

1401

00.

1079

30.

0835

20.

0649

10.

0351

80.

0195

416

0.85

282

0.72

845

0.62

317

0.53

391

0.45

811

0.39

365

0.33

873

0.29

189

0.25

187

0.21

763

0.16

312

0.12

289

0.09

304

0.07

078

0.05

409

0.02

815

0.01

503

170.

8443

80.

7141

60.

6050

20.

5133

70.

4363

00.

3713

60.

3165

70.

2702

70.

2310

70.

1978

40.

1456

40.

1078

00.

0802

10.

0599

80.

0450

70.

0225

20.

0115

618

0.83

602

0.70

016

0.58

739

0.49

363

0.41

552

0.35

034

0.29

586

0.25

025

0.21

199

0.17

986

0.13

004

0.09

456

0.06

914

0.05

083

0.03

756

0.01

801

0.00

889

190.

8277

40.

6864

30.

5702

90.

4746

40.

3957

30.

3305

10.

2765

10.

2317

10.

1944

90.

1635

10.

1161

10.

0829

50.

0596

10.

0430

80.

0313

00.

0144

10.

0068

420

0.81

954

0.67

297

0.55

368

0.45

639

0.37

689

0.31

180

0.25

842

0.21

455

0.17

843

0.14

864

0.10

367

0.07

276

0.05

139

0.03

651

0.02

608

0.01

153

0.00

526

210.

8114

30.

6597

80.

5375

50.

4388

30.

3589

40.

2941

60.

2415

10.

1986

60.

1637

00.

1351

30.

0925

60.

0638

30.

0443

0.0.

0309

40.

0217

40.

0092

20.

0040

522

0.80

340

0.64

684

0.52

189

0.42

196

0.34

185

0.27

751

0.27

751

0.18

394

0.15

018

0.12

285

0.08

264

0.05

599

0.03

819

0.02

622

0.01

811

0.00

738

0.00

311

230.

7954

40.

6341

60.

5066

90.

4057

30.

3255

70.

2618

00.

2109

50.

1703

20.

1377

80.

1116

80.

0737

90.

0491

10.

0329

20.

0222

20.

0150

90.

0059

00.

0023

924

0.78

757

0.62

172

0.49

193

0.39

012

0.31

007

0.24

698

0.19

715

0.15

770

0.12

640

0.10

153

0.06

588

0.04

308

0.02

838

0.01

883

0.01

258

0.00

472

0.00

184

250.

7797

70.

6095

30.

4776

10.

3751

20.

2953

00.

2330

00.

1842

50.

1460

20.

1159

70.

2953

00.

0588

20.

0377

90.

0244

70.

0159

60.

0104

80.

0037

80.

0014

226

0.77

205

0.59

758

0.46

369

0.36

069

0.28

124

0.21

981

0.17

220

0.13

520

0.10

639

0.08

391

0.05

252

0.03

315

0.02

109

0.01

352

0.00

874

0.00

302

0.00

109

270.

7644

00.

5858

60.

4501

90.

3468

20.

2678

50.

2073

70.

1609

30.

1251

90.

0976

10.

0762

80.

0468

90.

0290

80.

0181

80.

0114

60.

0762

80.

0024

20.

0008

428

0.75

684

0.57

437

0.43

708

0.33

348

0.25

509

0.19

563

0.15

040

0.11

591

0.08

955

0.06

934

0.04

187

0.02

551

0.01

567

0.00

971

0.00

607

0.00

193

0.00

065

290.

7493

40.

5631

10.

4243

50.

3206

50.

2429

50.

1845

60.

1405

60.

1073

30.

0821

50.

0630

40.

0373

80.

0223

70.

0135

10.

0082

30.

0050

60.

0015

50.

0005

030

0.74

192

0.55

207

0.41

199

0.30

832

0.23

138

0.17

411

0.13

137

0.09

938

0.07

537

0.05

731

0.03

338

0.01

963

0.01

165

0.00

697

0.00

421

0.00

124

0.00

038

718 Appendix 1 Time Value of Money

NEL

Exhi

bitA

1-9

Futu

reV

alu

eofa

nA

nnuity

FV

A¼

(1þ

i)n

�1

i

hi

n/i

1%2%

3%4%

5%6%

7%8%

9%10

%12

%14

%16

%18

%20

%25

%30

%

11.

0000

01.

0000

01.

0000

01.

0000

01.

0000

01.

0000

01.

0000

01.

0000

01.

0000

01.

0000

01.

0000

01.

0000

01.

0000

01.

0000

01.

0000

01.

0000

01.

0000

02

2.01

000

2.02

000

2.03

000

2.04

000

2.05

000

2.06

000

2.07

000

2.08

000

2.09

000

2.10

000

2.12

000

2.14

000

2.16

000

2.18

000

2.20

000

2.25

000

2.30

000

33.

0301

03.

0604

03.

0909

03.

1216

03.

1525

03.

1836

03.

2149

03.

2464

03.

2781

03.

3100

03.

3744

03.

4396

03.

5056

03.

5724

03.

6400

03.

8125

03.

9900

04

4.06

040

4.12

161

4.18

363

4.24

646

4.31

013

4.37

462

4.43

994

4.50

611

4.57

313

4.64

100

4.77

933

4.92

114

5.06

650

5.21

543

5.36

800

5.76

563

6.18

700

55.

1010

15.

2040

45.

3091

45.

4163

25.

5256

35.

6370

95.

7507

45.

8666

05.

9847

16.

1051

06.

3528

56.

6101

06.

8771

47.

1542

17.

4416

08.

2070

39.

0431

06

6.15

202

6.30

812

6.46

841

6.63

298

6.80

191

6.97

532

7.15

329

7.33

593

7.52

000

7.71

561

8.11

519

8.53

552

8.97

748

9.44

197

9.92

992

11.2

5879

12.7

5603

77.

2135

47.

4342

87.

6624

67.

8982

98.

1420

18.

3938

48.

6540

28.

9228

09.

2004

39.

4871

710

.089

0110

.730

4911

.413

8712

.141

5212

.915

9015

.073

4917

.582

848

8.28

567

8.58

297

8.89

234

9.21

423

9.54

911

9.89

747

10.2

5980

10.6

3663

11.0

2847

11.4

3589

12.2

9969

13.2

3276

14.2

4009

15.3

2700

16.4

9908

19.8

4186

23.8

5769

99.

3685

39.

7546

310

.159

1110

.582

8011

.026

5611

.491

3211

.977

9912

.487

5613

.021

0413

.579

4814

.775

6616

.085

3517

.518

5119

.085

8520

.798

9025

.802

3232

.015

0010

10.4

6221

10.9

4972

11.4

6388

12.0

0611

12.5

7789

13.1

8079

13.8

1645

14.4

8656

15.1

9293

15.9

3742

17.5

4874

19.3

3730

21.3

2147

23.5

2131

25.9

5868

33.2

5290

42.6

1950

1111

.566

8312

.168

7212

.807

8013

.486

3514

.206

7914

.971

6415

.783

6016

.645

4917

.560

2918

.531

1720

.654

5823

.044

5225

.732

9028

.755

1432

.150

4242

.566

1356

.405

3512

12.6

8250

13.4

1209

14.1

9203

15.0

2581

15.9

1713

16.8

6994

17.8

8845

18.9

7713

20.1

4072

21.3

8428

24.1

3313

27.2

7075

30.8

5017

34.9

3107

39.5

8050

54.2

0766

74.3

2695

1313

.809

3314

.680

3315

.617

7916

.626

8417

.712

9818

.882

1420

.140

6421

.495

3022

.953

3824

.522

7128

.029

1132

.088

6536

.786

2042

.218

6648

.496

6068

.759

5897

.625

0414

14.9

4742

15.9

7394

17.0

8632

18.2

9191

19.5

9863

21.0

1507

22.5

5049

24.2

1492

26.0

1919

27.9

7498

32.3

9260

37.5

8107

43.6

7199

50.8

1802

59.1

9592

86.9

4947

127.

9125

515

16.0

9690

17.2

9342

18.5

9891

20.0

2359

21.5

7856

23.2

7597

25.1

2902

27.1

5211

29.3

6092

31.7

7248

37.2

7971

43.8

4241

51.6

5951

60.9

6527

72.0

3511

109.

6868

416

7.28

631

1617

.257

8618

.639

2920

.156

8821

.824

5323

.657

4925

.672

5327

.888

0530

.324

2833

.003

4035

.949

7342

.753

2850

.980

3560

.925

0372

.939

0187

.442

1313

8.10

855

218.

4722

017

18.4

3044

20.0

1207

21.7

6159

23.6

9751

25.8

4037

28.2

1288

30.8

4022

33.7

5023

36.9

7370

40.5

4470

48.8

8367

59.1

1760

71.6

7303

87.0

6804

105.

9305

617

3.63

568

285.

0138

618

19.6

1475

21.4

1231

23.4

1444

25.6

4541

28.1

3238

30.9

0565

33.9

9903

37.4

5024

41.3

0134

45.5

9917

55.7

4971

68.3

9407

84.1

4072

103.

7402

812

8.11

667

218.

0446

037

1.51

802

1920

.810

9022

.840

5625

.116

8727

.671

2330

.539

0033

.759

9937

.378

9641

.446

2646

.018

4651

.159

0963

.439

6878

.969

2398

.603

2312

3.41

353

154.

7400

027

3.55

576

483.

9734

320

22.0

1900

24.2

9737

26.8

7037

29.7

7808

33.0

6595

36.7

8559

40.9

9549

45.7

6196

51.1

6012

57.2

7500

72.0

5244

91.0

2493

115.

3797

514

6.62

797

186.

6880

034

2.94

470

630.

1654

621

23.2

3919

25.7

8332

28.6

7649

31.9

6920

35.7

1925

39.9

9273

44.8

6518

50.4

2292

56.7

6453

64.0

0250

81.6

9874

104.

7684

213

4.84

051

174.

0210

022

5.02

560

429.

6808

782

0.21

510

2224

.471

5927

.298

9830

.536

7834

.247

9738

.505

2143

.392

2949

.005

7455

.456

7662

.873

3471

.402

7592

.502

5812

0.43

600

157.

4149

920

6.34

479

271.

0307

253

8.10

109

1067

.279

6323

25.7

1630

28.8

4496

32.4

5288

36.6

1789

41.4

3048

46.9

9583

53.4

3614

60.8

9330

66.1

7894

79.5

4302

104.

6028

913

8.29

704

183.

6013

824

4.48

685

326.

2368

667

3.62

636

1388

.463

5124

26.9

7346

30.4

2186

34.4

2647

39.0

8260

44.5

0200

50.8

1558

58.1