time to strike - cexr.clcexr.cl/wp-content/uploads/2015/07/cer28-eng-fin.pdf · time to strike...

TRANSCRIPT

9 8 5 4 Project Showcase

Crowd-funding exploration

Exploration News

No.28 / July 2015 www.cexr.cl

As market valuations bottom out, is private equity about to strike?

Time to strike

Q&A: White Mountain Titanium

A s the slump in the mining indus-try enters its third year, deals are growing rarer. Consultants EY calculated that the number

of transactions in the first three months of the year was down by half from a year ago and by a third from the previous quarter. By value, M&A was down 18% at US$5.9B. The dearth of deals mirrors the focus among mining companies on slimming bloated portfolios and boosting produc-tivity as lower metals prices squeeze profits. However, major mining companies are once again at least entertaining the pos-sibility of acquisitions. The state of readi-ness varies from company to company, depending how far cost-cutting has pro-gressed. Some, like Anglo American (LSE: AAL) and Barrick Gold (TSX: ABX), are still trying to cut the flab, selling unwanted assets to pay off debt. But even BHP Billiton (LON: BLT), which prepared for the downturn ahead of the crowd, remains extremely cautious. “Should an opportunity arise, we are pre-pared to move, but… it has to be one hell of a deal,” CEO Andrew MacKenzie warned recently. After all, it only recently spun off US$9.1B of second tier assets as South32 (ASX: S32). However, in a recent assessment, based on discussions with clients, EY identified a switch to growth as the main risk facing

the global mining industry, ahead of productivity and access to capital. After years of falling valuations, opportu-nities abound. According to the Prospec-tors and Developers Association of Cana-da (PDAC), at an average of C$0.11, share prices on the TSX Venture Ex-change last year were just a fifth of the peak achieved in 2010. Now a corner may have been turned. Confidence in the mining industry is be-ginning to improve. Market analysts in Chile surveyed by the Chilean Copper Commission (Cochilco) expect copper

© 2015 Chile Explore Report All Rights Reserved

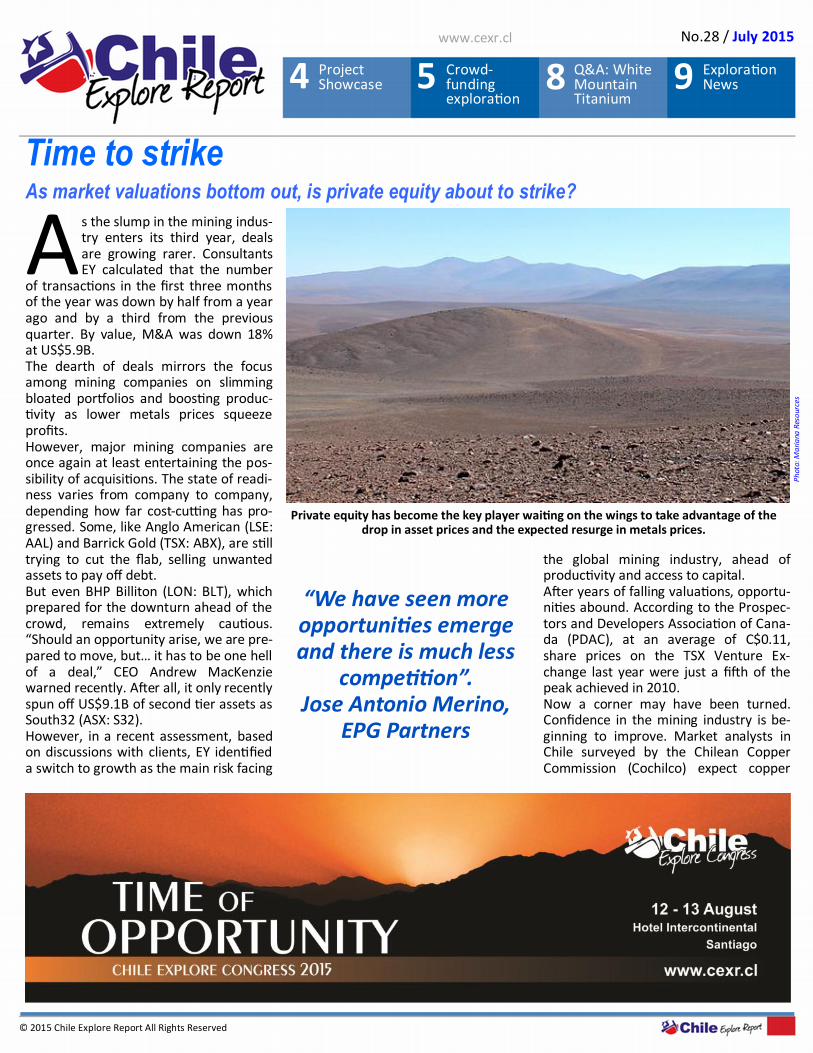

Private equity has become the key player waiting on the wings to take advantage of the drop in asset prices and the expected resurge in metals prices.

“We have seen more opportunities emerge and there is much less

competition”. Jose Antonio Merino,

EPG Partners

Ph

oto:

Ma

ria

na R

eso

urce

s

2

prices to average US$2.89/lb in 2016, up from US$2.77/lb this year. However, as mining companies scour the horizon again, they are facing a new am-bitious and wealthy competitor. Private equity has become a key player waiting on the wings to take advantage of the drop in asset prices and the expected resurge in metals prices by the end of the decade. The private equity’s incursion into min-ing has attracted some of the industry’s biggest beasts, including former Xstrata CEO Mick Davies (X2 Resources) and for-mer Barrick Gold CEO Aaron Regent (Magris Resources). But despite the bil-lions reported to have been raised for investment in undervalued assets, the number of deals done has been few. Last October, Magris partnered Singa-pore’s sovereign wealth fund Temasek Holdings to acquire a niobium mine and rare earth deposit from Iamgold (TSX:IMG) for US$500M. In Chile, private equity has been quietly taking up positions. New York-based AMCI Group has held a 33% stake in Grupo Minero Las Cenizas since 2010. B&A Mineraçao, a joint venture between Brazilian investment bank BTG Pactual and AGN Participações, led by former Vale (NYSE: VALE) CEO Roger Agnelli, has developed Cuprum Resources which is preparing to restart the Puquios Cu mine in Region IV in 2017.

Other deals have followed, but the num-ber has not matched the fanfare that heralded private equity’s entry into the sector. X2, which has funds totaling US$5.6B, has yet to close a deal despite plenty of rumors. That caution to do deals probably reflects the impulse to catch asset prices at their lowest point. In the last two years, prices have contin-ued to fall. Where firms have struck, indications are that they may have moved too fast. BlackRock World Mining had to write off its US$110M investment in London Mining, which was hit by the collapse in iron ore prices and the Ebola outbreak in West Africa. Resource Capital Fund

faces a similar situation at US rare earths

producer Molycorp which went bust in June. But now with signs that sentiment im-proving and valuations may be bottom-ing out, the time to strike may be at hand. “We are seeing more and more invest-ment opportunities throughout the re-gion,” says Victor Muñoz, Managing Di-rector of Denham Capital Management’s Latin America office in São Paulo, Brazil. Formed in 2007, Denham backs experi-enced mining management teams and entrepreneurs focused on creating valua-ble enterprises throughout these chang-ing environments. The firm’s standards are high, says Múñoz, and it works with

management teams that are targeting projects that can be quickly moved into production to generate cash-flow. In or-der to mitigate the risk posed by volatile commodity prices, they must be low-cost operations, preferably in the first quar-tile of the cost curve. At the height of the commodity boom, such projects were inaccessible. But now with many companies running out of funds and unable to raise capital, such assets are coming to market. “Four years ago, it was difficult for teams to find the right deal. Now there are pro-jects that can be taken control of and moved into operation”, he says. Other funds are seeking similar opportu-nities here. In June, Greenstone Resources signed a deal with Coro Mining (TSXV: COP) to bring COPs Berta Cu project in Region III into production. Led by JP Morgan’s for-mer head of mining and metals Michael Haworth, London-based Greenstone will provide a total of US$9M to develop the first stage of Berta, including the acquisi-tion and remediation of a SX-EW plant. In exchange, it will receive 33% of COP and the right to name two directors to the board. The opportunities are not limited to con-struction-ready projects. The number of exploration prospects available has also risen.

Ph

oto:

Den

ha

m C

ap

ita

l Ma

nag

emen

t

Ph

oto:

Ch

ile E

xplo

re R

epor

t

Feature

www.cexr.cl

© 2015 Chile Explore Report All Rights Reserved

No.28 / July 2015

Jose Antonio Merino, EPG FIP Exploración Minera.

“Four years ago, it was difficult for teams to

find the right deal. Now there are projects that can be taken control of and moved into opera-

tion”. Victor Muñoz,

Denham Capital Management

Victor Muñoz, Denham Capital Management

3

Feature

www.cexr.cl

© 2015 Chile Explore Report All Rights Reserved

No.28 / July 2015

Although the market capitalization of exploration companies have been falling since 2012, it has taken some time for this to be transferred to asset prices, says Jose Antonio Merino, general man-ager of EPG FIP Exploración Minera, one of Chile’s six Fénix funds. When they were launched three years with government funding, there were fears that the funds might have missed the commodities super-cycle. But with asset prices down sharply from two years ago and exploration costs at rock bottom, Merino says conditions for the Fénix funds and other private equity players are now much better. Given that most mining companies are not actively seeking acquisitions and cap-ital markets remain weak, private equity is sometimes the only option for compa-nies which are struggling. “We have seen more opportunities emerge and there is much less competi-tion,” he says. Companies which once refused to talk are now opening their doors. In recent weeks, EPG has been able to line up deals on attractive terms with two listed junior companies. After an initial drilling campaign at South-ern Hemisphere Mining’s (ASX: SUH) Juan Soldado IOCG project in Region IV, EPG has now signed a farm-out option agreement for SUHs Mantos Grandes property. Drilling of the El Verde target is

likely to begin there in August while it assesses the results from Juan Soldado. Meanwhile it has struck a farm-in agree-ment with fellow Australians Helix Re-sources (ASX: HLX) for the latter’s Joshua Cu project, also in Region IV, earning a 50.1% stake in exchange for 10,000m of drilling. It is also partnering a private UK exploration group on a gold project in Region III. “Our focus is on the asset, not the com-pany,” explains Merino.

Fellow Fenix fund Asset Chile is also ben-efitting from juniors’ new willingness to do deals. It has recently signed a deal to earn 50% of the Doña Ines and Explora-dora East projects in Region III from Mar-iana Resources (AIM: MARL) in exchange for funding US$1.65M of exploration. It could also earn up to 40% of Orosur Mining’s (ASX: OMI) interest in the Anillo project, held under option from state-owned Codelco, by financing US$3.5M of exploration over the next 2.5 years. While funds are not beholden to short-term market movements like public com-panies, their investment periods are lim-ited. The Fenix funds must commit to invest their resources by January 2017. To date EPG has committed around US$20M of its US$36M mix of private capital and loans from economic devel-opment agency CORFO. Although aware of the deadline, Merino says they feel no particular pressure. “The pressure has always been there, but we evaluate every investment opportuni-ty in its merits, using high evaluation standards. Despite the great number of exploration projects that are presented to us, we have consistently invested in only 2 – 3 projects a year,” he says. All the private equity funds circling the mining industry face the similar pressure to spend. And with the sense that a re-covery is building, the time may be now. CER

EPG has struck a farm-in agreement with Helix Resources for the Joshua Cu project.

Asset Chile has recently signed a deal to earn 50% of the Doña Ines and Exploradora East projects, in Region III, from Mariana Resources.

Ph

oto:

Ma

ria

na R

eso

urce

s

Ph

oto:

Hel

ix R

eso

urce

s

4

Project Showcase

Available Exploration Alliance Area: Capricornio At surface gold mineralization with sufficient drilling for an initial resource estimate. Veins extensions that trend northward under cover remain untested.

www.cexr.cl

© 2015 Chile Explore Report All Rights Reserved

No.28 / July 2015

Contact: [email protected]

Daniel Jimenez Senior VP of Exploration [email protected] +56998223038

Darryl D. Lindsay, PhD, PGeo Manager Metal Business Development [email protected] +56966488511

Tomas Esguep Metal Business Development Engineer [email protected] +56966373482

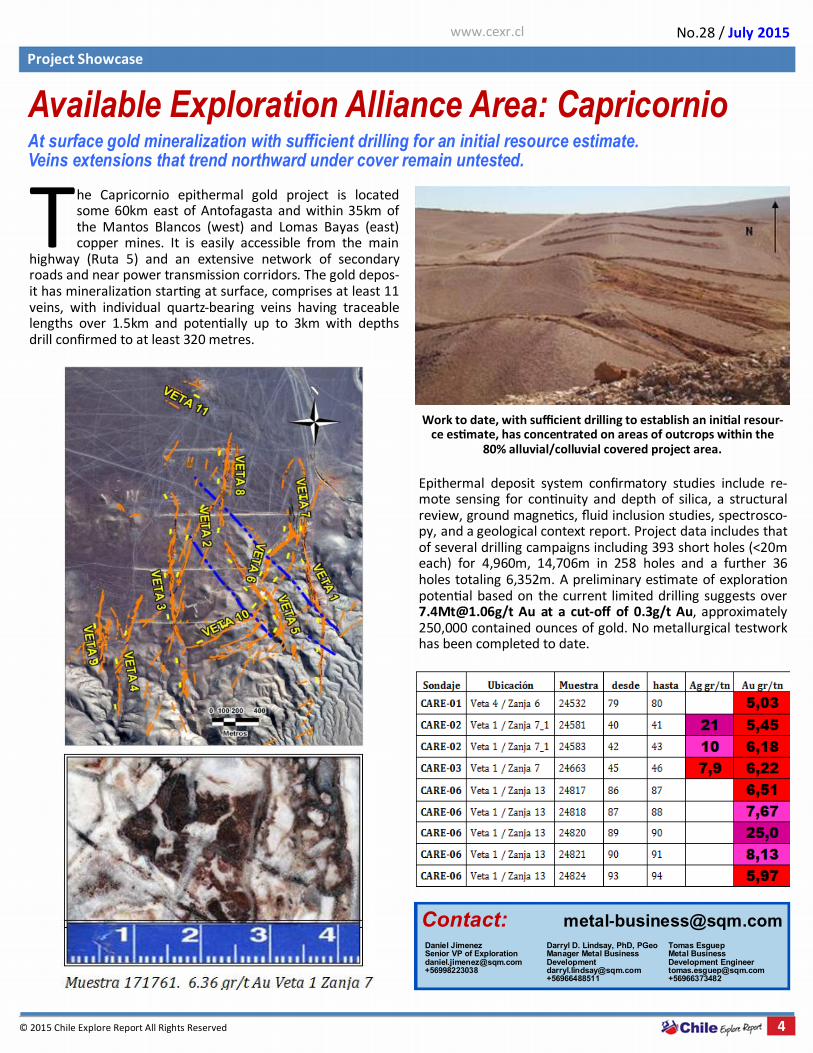

T he Capricornio epithermal gold project is located some 60km east of Antofagasta and within 35km of the Mantos Blancos (west) and Lomas Bayas (east) copper mines. It is easily accessible from the main

highway (Ruta 5) and an extensive network of secondary roads and near power transmission corridors. The gold depos-it has mineralization starting at surface, comprises at least 11 veins, with individual quartz-bearing veins having traceable lengths over 1.5km and potentially up to 3km with depths drill confirmed to at least 320 metres.

Work to date, with sufficient drilling to establish an initial resour-ce estimate, has concentrated on areas of outcrops within the

80% alluvial/colluvial covered project area.

Epithermal deposit system confirmatory studies include re-mote sensing for continuity and depth of silica, a structural review, ground magnetics, fluid inclusion studies, spectrosco-py, and a geological context report. Project data includes that of several drilling campaigns including 393 short holes (<20m each) for 4,960m, 14,706m in 258 holes and a further 36 holes totaling 6,352m. A preliminary estimate of exploration potential based on the current limited drilling suggests over [email protected]/t Au at a cut-off of 0.3g/t Au, approximately 250,000 contained ounces of gold. No metallurgical testwork has been completed to date.

5

Feature

www.cexr.cl

© 2015 Chile Explore Report All Rights Reserved

C rowdfunding is a way for entre-preneurs to raise small amounts of capital over the internet from thousands of individuals to fi-

nance their projects. Investing online in unknown companies may seem risky, but millions have done so. The earliest and simplest form of crowdfunding was for good causes – whether to help someone pay for costly medical treatment or raise money for international relief - from which donors sought nothing more than good karma in return. Entrepreneurs then saw the system as a way of financing new ventures, typically offering donors early access to an exclusi-ve product. New portals, such as Kickstarter, have appeared especially designed to raise money this way from investors. The op-portunities financed through this method span almost every possibility which could occur to you, including new films, elec-tronic devices and the inevitable apps for your smartphone. While many such raisings succeed, thou-sands more have failed. And just occasio-nally, entrepreneurs get much more than they bargained for. Last August, Oregon-based inventor Ryan Grepper sought US$200,000 to develop a new drinks cooler fit for the 21st century (it can play music from your I-Phone and blend a smoothie while keeping your beer ice-cold). But Grepper massively underestimated the thirst for such a pro-duct and so far has raised almost US$13.3M from 62,000 parched inves-tors. Meanwhile crowdfunding has moved onto the next stage of evolution: offering online investors equity in the new com-pany. “This is the Holy Grail of crowdfunding,” says Oscar Jofre, CEO of KoreConX, which provides eco-system infrastructure platforms for the crowdfunding and capi-tal markets. According to crowdfunding advocates, the secret of its success is that it is demo-cratizing investment. Only the wealthiest

and best-connected heard about Face-book and Google before they really took off. Through an open system like crowdfunding, anybody could be an early investor in what might become a major corporation. “It lets everybody get in on the opportu-nity and that’s the reason why it’s gro-wing,” says Jofre. The main barrier so far has been outda-ted securities regulations, but govern-ments have been catching up gradually. Australia enacted changes a decade ago while the US only did so in 2013.

Since then growth has been explosive. In the first twelve months since the legisla-tion was approved in the US, more than US$61 billion were raised through under the relevant chapter of JOBS Act. The largest deal alone was for US$130M and the second for US$64M. With numbers like these, Jofre dismisses the idea that the market has lost its ap-petite for high-risk opportunities. Instead changes to the structure of Cana-da’s financial industry mean that the ju-nior mining companies have lost they access they once had to retail investors. Many financial houses have pulled out of the traditional broking business through which juniors could raise C$1 or C$2M for the next drill campaign. Many have moved into wealth management for high net-worth individuals and will not look at any opportunity below C$10M. That business has now been taken by exempt market dealers who lack the reach of their predecessors. And eviden-ce shows that the mass of Canadian in-vestors do not have the level of access to deals that they might imagine.

No.28 / July 2015

With stock markets in the doldrums, crowdfunding offers a new way to reach investors.

Crowdfunding mineral exploration

“Crowdfunding lets everybody get in on the opportunity and that’s

the reason why it’s growing”.

Oscar Jofre, KoreConX

Ph

oto:

Pla

net

ary

Res

ourc

es

Planetary Resources raised US$1.5M to finance a prototype telescope.

6

According to one study, over the last ten years, just 200,000 of Canada’s 1.4M ac-credited investors were given access to every mining deal. Often brokers stick to their home markets, typically around Toronto and Vancouver, and will not cha-se potential investors elsewhere in the country, Jofre says. And the problem is not a lack of capital. There are almost US$5 trillion squirreled away in saving accounts in Canadian bank, earning negligible interest. In the US, the figure is estimated at US$36 tri-llion. “It’s false to say that there are no high level risk investors out there,” he says. “The broken part was the middle piece.” Crowdfunding, which links entrepreneurs with the market directly, could bridge that gap, he says. But to date, mineral exploration has not made many inroads with crowdfunding. The industry has raised just US$61M through this method of investment. Some of the deals that have been done are rather leftfield. In 2013, Planetary Resources raised US$1.5M on Kickstarter to finance a prototype telescope that will help look for mineral-bearing asteroids to mine. But the experiences of other industries suggest significant potential interest in a high-risk sector such as mineral explora-tion. An estimated 48% of the US$61B raised through crowdfunding in the US went to

life sciences, an area with notable para-llels with exploration, notes Jofre. Like junior mining companies, biotech firms are typically small and looking to raise a couple of million dollars to finan-ce the next stage of research. And like an undrilled porphyry target, if the techno-logy is successful, the potential returns are huge. If retail investors are prepared to put their money in this kind of venture, it is not too much of a leap to see them in-vesting in drill rigs and geology. “The opportunities for mining companies are enormous,” says Jofre.

Last year, a new crowdfunding portal specializing in mining opportunities was launched: Klondike Strike. InvestX, led by Marcus New, chairman of Stockhou-se.com, is another equity crowdfunding portal marketing itself in the mining spa-ce. But to make that leap, mining companies need to learn how to sell themselves to new investors who probably know nothing or little of the sector. Wandering around his eighth PDAC con-vention last March, Jofre says he still has problems as a non-specialist telling one mining opportunity from another. Too often geologists rely on undecipherable rainbow-colored charts to explain their pitch to the retail investors they seek to attract. Biotech companies, on the other hand, avoid talking about how the technology works and concentrate instead on the problem it will solve, whether it is a ge-netic fix for an inherited disease or a new cancer-busting drug. Importantly, com-panies hired marketing professionals to sell their story to the public. Rather than the traditional roadshows and seminars, social media is the key. Once investors are hooked, then the op-portunity could go viral. CER Oscar Jofre will be speaking at Chile Explore Congress 2015: Time of Oppor-tunity.

www.cexr.cl

© 2015 Chile Explore Report All Rights Reserved

No.28 / July 2015

Ph

oto:

Ko

reCo

nx

Ph

oto:

Co

ole

st

Oscar Jofre, CEO of KoreConX,

Feature

Inventor Ryan Grepper has raised almost US$13.3M to develop his new drink cooler.

7

Feature

W ritten by Michael Dentith, Professor of Geophysics at The University of Western Australia, and Stephen

Mudge of Vector Research, Geophysics for Mineral Exploration Geoscientist is designed not only as a teaching tool but as a practical guide for working geoscien-tists. “We wanted to write a book that would be useful to the industry,” Dentith told CER. As the mining industry is forced increa-singly to look deeper and under cover, geophysics is becoming an ever more important exploration tool. As well as going deep, it can also allow exploratio-nists to cover large areas of potentially inaccessible ground relatively quickly and cheaply. The technology of geophysics has not changed significantly in recent years. Over the ten years that it took to write the book, Dentith says that the main ad-vance has been the improvement in air-borne electromagnetic surveys. Use of seismic data, a mainstay of the oil and gas industry, has also become more widespread. Another important trend is the increased use of inverse modelling, using computer algorithms to build models of the Earth’s crust based on observations from geop-hysical surveys. But analyzing the almost infinite number of models that these te-chniques can produce requires a good understanding of geophysical data and its limitations, says Dentith. Even though geophysics has become mo-re prominent as an exploration tool, the number of geophysicists in mining and exploration companies has fallen drama-tically over the past two decades with many companies that once employed a significant number of geophysicists in-creasingly, or entirely, reliant on outside expertise. “It’s really become a profession of con-sultants,” he notes. Companies, especially small ones, often lack the in-house expertise needed to understand and interpret geophysical

data. As a result, geologists are fre-quently required to take on tasks once asked of geophysicists, sometimes with questionable results. “I think it’s fair to say that perhaps the understanding of the results of inverse modelling is not as good as it should be,” warns Dentith. Despite the proximity of geologists and geophysicists, they are often speaking different languages. While geologists should try to understand more about the capabilities and limitations of geophysics, geophysicists should strive to present the information they produce in a more rea-dily understandable form, he says. More effort could be made at university-level to encourage mutual understan-ding. Dentith’s own University of Wes-tern Australia decided to stop offering undergraduate degrees in geophysics several years ago, but it strives to ensure its geology graduates have a good groun-ding in the science that will serve them when they enter the industry.

Mining companies should also seek to integrate geophysics with other sort of geoscientific data rather than treating it as a separate realm. Dentith points to First Quantum Minerals (LON: FQM) as one of the leaders in this effort, by ma-king geophysics an integral part of its mineral exploration activity, closely com-bining the discipline with geology and geochemistry to better understand the geology of the exploration area and iden-tify likely targets. Another important development for the discipline is the growth of publicly availa-

ble geophysics data. As governments around the world compete for mine in-vestment, leading mining jurisdictions are spending heavily on public geoscien-tific research to attract mineral explorati-on firms with high quality exploration information. Geophysical datasets cove-ring vast areas are available over the in-ternet, as are maps produced by ASTER (the Advanced Spaceborne Thermal Emission and Reflection Radiometer). More information will bring new challen-ges. With large mining companies increasingly leaving the greenfield exploration space to junior mining companies with much more constrained budgets, learning how to best use this free geophysical data will become a key competitive advantage. As in other fields, companies will need to employ big data technologies to work through the reams of information availa-ble in order to identify prospective ground and likely targets, a move that could important ramifications for the way mineral exploration is carried out in the future. CER Geophysics for the Mineral Exploration Geoscientist by Michael Dentith and Stephen Mudge is published by Cam-bridge University Press.

Bridging a gap

www.cexr.cl

© 2015 Chile Explore Report All Rights Reserved

No.28 / July 2015

Despite the proximity of geologists and geop-

hysicists, they are often speaking different lan-

guages.

Geologists need to learn more about the limitations of geophysics in order to use it better, says one of the authors of a new book on the subject.

8 © 2015 Chile Explore Report All Rights Reserved

Interview

Having obtained environmental approv-al, WMTM is seeking a partner to devel-op its Cerro Blanco Ti project in Region III. CER: How was Cerro Blanco discovered? MK: The Cerro Blanco project was initial-ly discovered and owned by the local subsidiary of what used to be Phelps Dodge, Minera Ojos del Salado. They spent about US$8M between 1992 and 1998, putting in roads and completing around 18,000m of diamond and RC drilling. Then Phelps decided to become a pure copper play and to dispose of Cerro Blanco. CER: When did WMTM become in-volved? MK: One of our directors through a con-tact in Chile asked us to step in. Ulti-mately Cerro Blanco was bought from Phelps Dodge for US$750,000 through a combination of cash and shares and WMTM was inaugurated in 2004. CER: What work have you done since then? MK: We have put in another US$30M to hugely increase the resource. Phelps be-gan with Las Carolinas. Since then we have advanced three or four other pro-spects, including La Cantera and Eli. We have, in total, 9 prospects and we have also announced the discovery of another prospect south of Cerro Blanco: La Marti-na. We are always on the lookout for new prospects. CER: Can you describe the geology? MK: It’s an intrusive and there’s been secondary hydrothermal alteration. It’s obviously associated with the iron ore belt between Copiapo and La Serena, but there’s been albitic alteration and the iron ore and copper have been remobi-lized. But titanium operates in a higher temperature and therefore it gets left behind, as disseminated mineralization. CER: How big is the project? MK: We have drilled around 36,000m so far at the Cerro Blanco project, which include Las Carolinas and La Cantera. There’s 174.5mt @ 1.62% TiO2 which gives production of around 80-100,000tpy of rutile concentrate over a

20 year mine life. The other prospects represent the future upside of the pro-ject. This year we are carrying out lots of geochemistry in the rest of the district to incorporate the potential gradually into the current development plan. There is a good high-grade area near La Cantera which could let us double the plant ca-pacity in the future. CER: How much will cost to build? MK: When we submitted the EIS, we said it was going to be US$380M but that fig-ure is 2-3 years old. We now are looking at below US$300M. At US$1,250/t for the product, we could pay off the debt in 3 to 4 years. CER: What’s driving titanium demand? MK: Around 85% of titanium feedstock is used in paints and pigments - a US$18B industry -, where it is used as the color carrier. We already have two offtake contracts from the paints industry. Paint demand grows with GDP. Meanwhile, more and more titanium metal is being used in new aircraft because it is half the weight and structurally stronger than steel. Forty years ago, the Jumbo Jet contained just 25t of metal: the Airbus 380 contains 70t. That’s really one of the commercial drivers for this project. CER: Has titanium been affected by the end of the supercycle? MK: Until 2008-2009, the price of rutile had been about US$500/t for the previ-

ous 20 years. In 2009 and 2010, the cycle picked up and, in 2011, prices hit US$2,800/t. Now it’s back at about US$1,000/t and it’s bottoming out. CER: What’s the importance of rutile? MK: Around 85% of the world’s titanium comes from ilmenite but it contains an iron molecule which you have to get rid of, invariably through a pyro-metallurgical operation. It’s really the cost of removing that iron molecule that sets the price for rutile. If oil prices had fallen back to US$25/barrel, rutile might be back at US$500/t but oil is picking up. Forecasts by RBC and Credit Suisse put the long-term price at about US$1,250/t. CER: What’s next for Cerro Blanco? MK: We are completing a major part of the FS which will be ready next year and in parallel we are starting to apply for permits to start construction in 2H16. That’s depends on efforts to find a part-ner to speed up the construction. CER: What kind of partner are you look-ing for? MK: It could be a titanium producer or a Chilean mining company. This is a Chile-an mining project using the same tech-nology you use in a copper mine. The only difference is the specific chemical collectors which you use in the floatation of rutile. This would not be a challenge for a Chilean mining company. CER

www.cexr.cl

Mike Kurtanjek, COO & President WHITE MOUNTAIN TITANIUM CORPORATION (OTCMKTS: WMTM)

No.28 / July 2015

9

Exploration News

Coro Mining (TSX: COP) Has secured a US$9M financing package from private equity firm Greenstone Resources LP and announced the results of an updated PEA for its Berta CU project in Region III. The new PEA envisages a phased start-up, beginning with the acquisition of the Nora SX-EW plant and followed by the installation of the Berta crusher, pads and site facility and expansion of Nora to 5kpty in a second stage. Using a base case Cu price of US$2.80/lb, the document estimates an after-tax NPV (8%) of US$35.2M and an IRR of 75%. The mine will produce 4,700tpy of Cu cath-ode over eight years, beginning as soon as next October. The combined convertible debenture (US$6.5M) and equity financ-ing (US$2.5M) from Greenstone will provide US$7.15M for Phase 1 capital expenditure requirements and US$1.85M in working capital for COP. Under the deal, Greenstone will ac-quire up to 79.8M shares via a private placement for total gross proceeds of C$3.192M, after which Greenstone would own 33% of COPs issued and outstanding common shares and have the right to name two directors to the board. New and existing shareholders will have the opportunity to provide ad-ditional equity at the same price. Phase 2 at Berta requires ap-proximately US$12.6M of additional capital, of which US$5.9M could come from cash flow. Advanced discussions with vendors and construction companies have identified approximately US$8M in vendor and construction finance that may be availa-ble for this stage. “Greenstone's investment in COP is a major vote of confidence in our projects and management team and we are confident that we are now on our way to achieving our objective of becoming a Cu producer from a number of opera-tions in Chile,” said COP CEO Alan Stephens.

Kinross Gold (TSX: K) Is continuing geological mapping of key targets, together with trenching, geochemical sampling and geophysical profiling, at the Las Pampas property in Region II, held under option with Revelo Resources (TSXV: RVL). K has also begun to reinterpret existing geophysical data. A decision on further drilling will be taken later this year.

Hot Chili (ASX: HCH) Has begun a 9,000m drill campaign on the Alice Cu porphyry deposit at its Productora project in Region III. The results from the program, including 8,000m of RC and 1,000m of diamond drilling, will allow a first Mineral Resource and Ore Reserve at Alice to be included in the PFS for Productora scheduled for 2H15. Drilling will also test for mineralized extensions to the N and S of Alice and define the larger potential of the recently identified +6km copper porphyry footprint (Alunite-silica lithocap). The resource at Productora currently stands at 1Mt Cu and 675,000oz Au in the main zone deposit. Alice is located 400m W of the planned pit.

Asset Chile Has signed a definitive option agreement with Orosur Mining (TSX: OMI) for OMIs Anillo project in Region II. Under the deal, Asset Chile Exploración Minera Fondo de Inversión Privado can earn up to 40% in OMIs stake in Anillo by funding US$3.475M of exploration work, including 9,100m of drilling, over the next 18 months. Asset must spend $850,000, including 3,600m of RC drilling plus a geophysics campaign, over ten months, to earn a 16% stake. This can be lifted to 32.5% by spending US$1.25M, including further geophysics and 5,500m of RC drill-ing, over the following 18 months. It can lift its share to 40% by spending a further $1.375M over the following 18 months on drilling and geophysics. OMI will contribute a total of US$300,000 in the first two stages. OMI holds an option agree-ment with Codelco-Chile to earn a 65% stake in Anillo by spending over US$3M (now spent) and completing a FS by Jan-uary 2020. This may be extended by two years to January 2022 if OMI has a discovery and defines a mineral resource by 2020. “This transaction is non-dilutive to OMI shareholders and ena-bles us to progress a solid exploration program at Anillo for the next three years with limited capital requirements by OMI,” said CEO Ignacio Salzar. As Asset is supported under the gov-ernment’s Fenix fund program, it requires approval from eco-nomic development agency CORFO.

www.cexr.cl

© 2015 Chile Explore Report All Rights Reserved

No.28 / July 2015

Hot Chili’s Productora project, in Region III.

Ph

oto:

Co

ro M

inin

g

Ph

oto:

Ho

t C

hili

The Berta Cu project in Region III.

10

Exploration News

Exeter Resource (TSXV: XRC) Has completed the expanded water exploration drilling pro-gram for its Caspiche Au-Cu project in Region III, drilling an ad-ditional large diameter hole before the onset of winter condi-tions. Bore hole (LV07) at its Peñas Blancas 1 water concession returned water flow rates of over 100l/s, with rapid recharges rates, “again demonstrating the significance of the Peñas Blan-cas aquifer.” The aggregate flow rate from the six large diame-ter exploration wells completed is now over 400l/s, considera-bly above XRCs original target of 200l/s. XRC expanded the pro-gram to define the extent of the aquifer and potential flow rates but due to the extreme weather event that hit the region in March, only one of two holes were completed. XRC said it believes the aquifer could support any of three low capex de-velopment options identified for Caspiche in a 2014 PEA. XRC is now compiling technical reports on the aquifer that will form the basis of an application for water rights which it will submit to water authorities within three months.

Metminco (ASX: MNC) Has completed an updated mineral resource estimate for its Los Calatos Cu porphyry complex in southern Peru. The docu-ment estimates a total resource of 352Mt @ 0.76% Cu & 318ppm Mo at a 0.5% Cu cut-off but highlights potential for a higher grade, lower tonnage mine targeting 126Mt @ 1.03% Cu & 351ppm Mo, located entirely within the modeled brecci-as units. The proposed mine would produce 50,000tpa Cu. A new study by Runge Pincock Minarco is due for completion by mid-July 2015. “This is a very exciting development…as MNC can now focus on optimizing the new economics for develop-ing their major Cu asset in South America, “ said MD William Howe. “Subject to the outcome of this new mining study, MNC will advance the development of Los Calatos by commencing permitting and FS and EIS as an important next step,” he add-ed.

Asset Chile Has signed a subscription and option agreement with Mariana Resources (AIM: MARL) to explore the Doña Inés (Au-Ag) and Exploradora East (Cu-Mo) projects in Region III. Asset Chile Ex-ploración Minera Fundo de Inversión Privado can earn up to a 50% interest in the properties by funding US$1.65M of explora-tion which will be carried out by MARL. Previous geochemical sampling identified potential for an oxidized, high sulfidation epithermal Au-Ag system at Doña Ines and a porphyry Cu-Mo-Au system under thin post-mineralization cover at Exploradora East. MARL acquired both projects through its acquisition of Aegean Metals last year. “The financing from Asset…allows MARL to advance the exciting Doña Ines project, located within an underexplored epithermal gold- silver belt that extends north from the Maricunga Gold Belt to the Peruvian border, where Gold Fields Limited (JSE: GFI) recently announced the discovery of the 3Moz Au Salares Norte deposit,” said CEO Glen Parsons. Asset acquired 20% on signing with a commit-ment to spend US$250,000. The interest rises to 40% with the provision of a further US$200,000. Under phase II, Asset must invest a further US$1.2M. The first stage of work will include further target generation and first-pass RC drill testing of prior-ity targets at both sites. Phase II will include resource definition drilling on any potential discovery. “The key to the option agreement is that funding received from Asset will not dilute shareholders directly but rather at the asset level, with MARL retaining the role of operator, as the potential of these two properties is investigated,” said Parsons.

Newmont Mining (NYSE: NEM) Is completing detailed geological mapping of its Montezuma Cu project in Region II, having recently completed a major pro-gram of geophysical surveying using in-house technologies over the principal targets. NEM owns 50.1% of Montezuma, with the balance held by Revelo Reousrces (TSXV: RVL). It can lift its stake to 65% by spending another US$5.5M over the next 2.5 years. NEM is also working on 3D modelling of historic drilling, geology and geophysics from key anomalies. A series of targets have been identified which are being evaluated to com-mence drill testing of priority targets in 4Q15.

www.cexr.cl

© 2015 Chile Explore Report All Rights Reserved

Ph

oto:

Exe

ter

Res

ou

rce

No.28 / July 2015

Ph

oto:

Ma

ria

na R

eso

urce

s

The Caspiche Au-Cu project in Region III

The Doña Inés and Exploradora East projects in Region III.

11

Exploration News

www.cexr.cl

EPG Exploration Minera Has signed an earn-in agreement with Helix Resources (ASX: HLX) for the Joshua Cu project in Region IV by which it can ac-quire a 50.1% by spending US$3M over next 2.5 years. Under the first phase, EPG can earn a 33.4% interest by undertaking a minimum of 3,500m of diamond drilling within a year for a minimum commitment of US$1.2M. In the second stage, EPG must carry out up to 6,500m of RC and diamond drilling within 1.5 years for a minimum commitment of US$1.8M. Thereafter, EPG and HLX will form a JV to progress the project. HLX ac-quired Joshua in 2009, confirming the presence of a large Cu-Au porphyry target by mid-2013. The main system is defined by an IP anomaly covering 10km2, coincident with anomalous soil geochemistry. Only 10% of the target has been tested with 2,000m of RC and diamond drilling. Results included 400m @ 0.3% Cu & 0.1g/t Au from surface in hole DDH2. The deal will allow HLX “to test the large porphyry target over a short timeframe.” “Subject to positive drill results… HLX will retain a significant equity stake in a greenfield Cu-Au porphyry discov-ery, located in a world class mining district,” HLX said.

Estrella Resources (ASX: ESR) Has renegotiated its agreement with SQM (NYSE: SQM) over its Cu projects in Region II, deferring options fees and mini-mum exploration expenditure due in 2015 until Feb 28 2016, while increasing ESRs stake in all metals discoveries to 90%. The new deal covers four projects: Ivannia (1,000h), Dania (1,476h), Colupo (1,700h) and Antucoya West (5,270h), which will be consolidated into a single exploration tenement pack-age. “The new agreement between ESR and SQM is a clear in-dication of the quality of the exploration ground and the re-spect both parties have for the current difficult market condi-tions,” said MD Jason Berton. The deal is subject to the signing of a formal, binding agreement.

Lara Exploration (TSXV: LRA) Has terminated a LoI with GoldPlata to consolidate their re-spective property interests in the Condorama project in Peru and the Murindo project in Colombia into a new Cu explora-tion project. After six months of discussions, LRA and GoldPlata were unable to consolidate the properties and have agreed to terminate the deal. Meanwhile, LRA has entered a LoI to grant Kiwanda Group a six month option to acquire its Picha Cu pro-ject in Peru in exchange for mineral rights and community obli-gations due during 3015. If the option is exercised, Kiwanda will grant LRA a 2% NSR on any precious metals and 1% NSR on any base metals or other minerals produced at the project. Kiawanda will also pay or transfer to LRA 30% of the proceeds upon a sale or transfer of the project. The 3,000h project is located in southern Peru’s Tertiary Volcanic Arc adjacent to the mineral rights blocks where Compañia de Minas Buenaventura (NYSE: BVN) is developing its San Gabriel gold deposit (I&I 12.3Mt @ 6.5g/t).

Lowell Copper (TSXV: JDL) Has signed an option agreement with Avrupa Minerals (TSXV: AVU) for the Alvito Fe-Cu-Au project in southern Portugal. JDL can earn up an 80% stake in the project by spending US$4.4M on the project and completing a PFS over an 8 year period. JDL can earn a 51% stake by spending US$300,000 and US$1.1M in years 1 and 2 and can earn an additional 14% by spending US$3M in years 3 to 5 as well as issuing 50,000 shares to AVU each years. The stake can be lifted to 80% by completing a PFS in years 6 to 8. Alvito covers 853km2 in the Ossa Morena zone. Recent work by AVU concentrated on the Alcaçovas IOCG tar-get, successfully identifying potential for significant copper-gold mineralization in known and new occurrences, including a previously un-documented, large epithermal Ag-Pb-Zn veining system. Altius Minerals (TSX: ALS) holds a 1.5% NSR. “The Alvi-to IOCG project has large potential, and we are looking for-ward to working with the Avrupa team in this prolific mining region of Portugal,” said JDL CEO David Lowell.

© 2015 Chile Explore Report All Rights Reserved

No.28 / July 2015

Lara’s Condorama project in Peru.

The Joshua Cu project in Region IV.

Ph

oto:

Hel

ix R

eso

urce

s

Ph

oto:

Lar

a E

´xp

lora

tio

n

12

Calendar

Conferences and Events Calendar

www.cexr.cl

© 2015 Chile Explore Report All Rights Reserved

July 8th - 10th GEOMIN 2015 Hotel Enjoy Antofagasta, CHILE www.gecamin.com/geomin

August 3th - 5th Diggers and Dealers Goldfields Arts Centre Kalgoorlie, AUSTRALIA www.diggersndealers.com.au

August 12th - 13th Hotel Intercontinental Santiago, CHILE

August 13th Medmin 2015 Hotel Sheraton Santiago, CHILE www.medmin.cl

September 8th Mineramerica Hotel Miramar Viña del Mar, CHILE www.mineramerica.cl

September 9th Asset Valuation and Capital Markets Hotel Radisson Santiago, CHILE www.comisionminera.cl

September 17th - 19th Colombia Minera 2015 Plaza Mayor Medellin, COLOMBIA www.andi.com.co

September 21st - 25th PERUMIN Mining Convention 2015 Campo Ferial Cerro Juli Arequipa, PERU www.convencionminera.com

September 24th - 25th Canadian Investor Conference 2015 Vancouver Convention Centre West Vancouver, CANADA www.cambridgehouse.com

October 4th - 8th Chilean Geological Congress Hotel-Casino Enjoy La Bahia de Peñuelas La Serena, CHILE www.congresogeologicochileno.cl

October 7th - 10th ExpominMexico Resort Mundo Imperial Acapulco, MEXICO www.camese.org

October 8th - 11th Expo Bolivia Minera Campo Ferial Chuquiago Marka La Paz, BOLIVIA www.tecnoeventos.org

October 28th - 31th ExpoMinera del Pacifico Ex Estadio Cavancha Iquique, CHILE www.industriales.cl

November 3th - 5th First International Metallic Mining Trade Show Centro de Congresos y Convenciones FIBES Seville, SPAIN www.mmhseville.com

November 10th Atacamamin 2015 Hotel Antay Copiapo, CHILE www.atacamamin.cl

January 25th - 28th Mineral Exploration Roundup 2016 Vancouver Convention Cen-tre East Vancouver, CANADA www.amebc.ca

No.28 / July 2015

13

Corporate News

www.cexr.cl

© 2015 Chile Explore Report All Rights Reserved

Hot Chili raises A$8.1M Hot Chili (ASX: HCH) has raised A$8.1M through a A$0.12 per share placement to major shareholders, including Taurus Funds Management, Exploration Capital Partners 2008 LP (affiliate of Sprott Inc.), Megeve Investments and CAP, the parent company of Compañía Minera del Pacífico S.A., HCHs JV partner at its Productora Cu project in Region III. Blue Spec Sondajes Chile SpA, a drilling company associated with HCH Chairman Murray Black, has agreed to subscribe for A$2.6M, gaining a 5% stake in HCH. The raising will allow HCH to complete a PFS on Productora and drilling at Alice without increasing debt or drawing down the remaining US$.85M of its credit facility with Sprott Resource Lending Partnership, repayment of which has been extended by 12 months to June 30th 2016. "This financial strength and the options it gives us are highly significant, given we are now underway with first drill testing of large-scale porphyry potential in the centre of our planned development,” said MD Christian Easterday. Completion of the PFS will trigger a US$26M payment by CMP to HCH under its option to in-crease its stake from 17.5% to 50.1%.

Estrella raises A$537,000 Estrella Resources (ASX: ESR) has raised A$537,000 through raisings since April, which it will use “maximize the value” of its advanced stage exploration projects in Chile. However, its lat-est rights offering closed June 10th with eligible shareholders accepting just 7.4M of the 82.4M shares offered.

Admiralty plans A$6.4M rights offer Admiralty Resources (ASX: ADY) is planning a one-for-three non-renounceable rights offer to raise up to A$6.397M. Sharehold-ers will be able to buy shares at A$0.02, a 10% discount to the share price on June 11th. The fund raised will be used to accel-erate exploration at Harper South and Pampa Tololo and ad-vance the Soberana project towards early production, “with a view to encourage the LoI between ADY and State owned China Nuclear Industry 22nd Construction Co.”

Atacama Pacific raises C$1.778M Atacama Pacific Gold (TSXV: ATM) has closed the second and final tranche of a non-brokered private placement. In aggre-gate ATM issued 8.89M units for gross proceeds of C$1.778M. In the final tranche, ATM issued 125,000 units at an issue price of C$0.20 for gross proceeds of C$25,000. Each unit comprises one common share and one-half common share purchase war-rant which entitles the holder to subscribe for one additional share at an exercise price of C$0.25 at any time during the next 36 months. The proceeds will be used to advance ATMs Cerro Maricunga Oxide Au project in Region III, as well as for working capital requirements and other general corporate purposes.

West Face reduces stake in Mandalay West Face Long Term Opportunities Global Master LP, a fund by managed by West Face Capital Inc., has closed a secondary offering of 20M shares in Mandalay Resources (TSX:MND) for gross proceeds of C$18.4M. The offering was completed on a bought deal basis and was underwritten by BMO Capital Mar-kets. West Face now holds 70.988M shares in MND, repre-senting approximately 17.3% of outstanding shares. "West Face has been a significant shareholder of MND since 2010, and we have been very pleased with our investment. We are happy to confirm the successful completion of our secondary offering which has allowed us to monetize a portion of our investment in MND," said West Face President & CEO Greg Boland.

Ph

oto:

Ho

t C

hili

No.28 / July 2015

Ph

oto:

Ata

cam

a P

aci

fic

Go

ld

Productora Cu project in Region III.

The Cerro Maricunga Oxide Au project in Region III.

14

Ph

oto:

Inca

On

e G

old

Ph

oto:

Sa

nta

cru

z Si

lver

Min

ing

Santiago Venture News

www.cexr.cl

Inca One achieves production milestone… Inca One Gold (SSEV: IOCL) has achieved an operating rate of 100tpd at its Chala One Au processing plant in Peru. The plant operated at or in excess of this level of production for ten days over the last two weeks, plus two days at lower levels of pro-duction for scheduled maintenance. IOCL is now focusing on purchasing ore and increasing the size of its stockpiles in order to sustain the 100tpd rate while boosting production levels and recoveries. The plant has produced 5,518oz Au and 5,011oz Ag since December 3rd 2014. “We are very happy with the con-sistent progress in scaling up our mineral purchasing activities, and recently achieving new highs both in weekly tonnes of min-eral acquisition, along with plant throughput,” said CEO Ed-ward Kelly.

… raises US$500,000… IOCL is expecting to raise up to US$500,000 through a non-brokered debenture financing. IOCL will issue up to 20 units, each consisting of one non-convertible debenture in the princi-ple amount of US$250,000 and 25,000 non-transferable war-rants, exercisable into one IOCL at a price of C$0.25 until 12 months from the closure date. Holders of the debentures will be entitled to receive interest of 14% per annum and paid quarterly in arrears. The term of the debentures is 12 months renewable by a further 12 months. Proceeds from the financ-ing will be used to fund the purchase of capital goods, including a desorption plant, to retire higher interest debt, and for gen-eral working capital purposes.

… names finance director IOCL also named Rafael Rossi as director of finance and admin-istration, Peru, where he will work alongside Jaime Polar, VP Operations and Development, Peru and plant manager Emilio Ortiz. Like Polar and Ortiz, Rossi previously worked at Barrick Gold (TSX: ABX) as a senior manager for 16 years at the Pierina and Lagunas Norte operations. “The hiring of Rafael Rossi…further enhances the Peruvian senior management team and their ability to deliver on goals as we strive to be a leader in the Peruvian mineral processing space,” said IO CFO Oliver Foeste.

Santacruz renegotiates San Felipe agreement Santacruz Silver Mining (SSEV: SZCL) has renegotiated the terms of an agreement between subsidiary Impulsora Minera Santacruz SA de CV and Minera Hochshchild Mexico SA de CV, part of Hochschild Mining (LSE: HOC), to acquire a 100% stake in the San Felipe project and the adjacent El Gachi property near Hermosilla, in the Mexican state of Sonora. Under the amended agreement, Impulsora may acquire 100% of the two by paying US$19M by December 1st 2016. HOC had previously required an initial payment of US$5M by December 1st 2015. “The flexibility created through the extension will allow us to further de-risk the San Felipe project through additional tech-nical studies ultimately leading to a PFS and the permits neces-sary for construction at San Felipe,” said SZCL president Arturo Prestamo.

U3O8 discovers U anomaly U3O8 Corp (SSE: UWECL) has identified an extensive anomaly near its Laguna Salada U deposit in Chubut Province, Argentina. The anomaly extends over a 90km2 area in the same gravel plain as Laguna Salada and was detected through a radon cup survey. The intensity and extent of the alpha radioactivity is interpreted to be indicative of widespread U. “This large radon anomaly, along with other discoveries at La Rosada and La Su-sana, underscores the district-scale U potential of the region,” said President and CEO Dr. Richard Spencer. UWECL now plans to extend radon cup exploration over the whole of the 1,500km2 gravel plain, prioritizing the area between the cur-rent survey and the La Rosada target located 5km to the N where the highest U grades have been discovered in the La-guna Salada district. Vertical channel samples through the grav-el at La Rosada have a weighted average grade of 1,500ppm U3O8 & 780ppm V2O5 from a 0.7m thick gravel layer located at an average depth of 0.3m below surface. The survey will also cover three concessions owned by the oil and mining com-pany of Chubut Province with which UWECL recently signed an exploration agreement to form a joint venture.

The San Felipe project in Sonora, Mexico.

© 2015 Chile Explore Report All Rights Reserved

No.28 / July 2015

Inca One’s Au processing plant in Peru.

15

Turgeon Cu-Zn VMS project in eastern Canada.

Santiago Venture News

www.cexr.cl

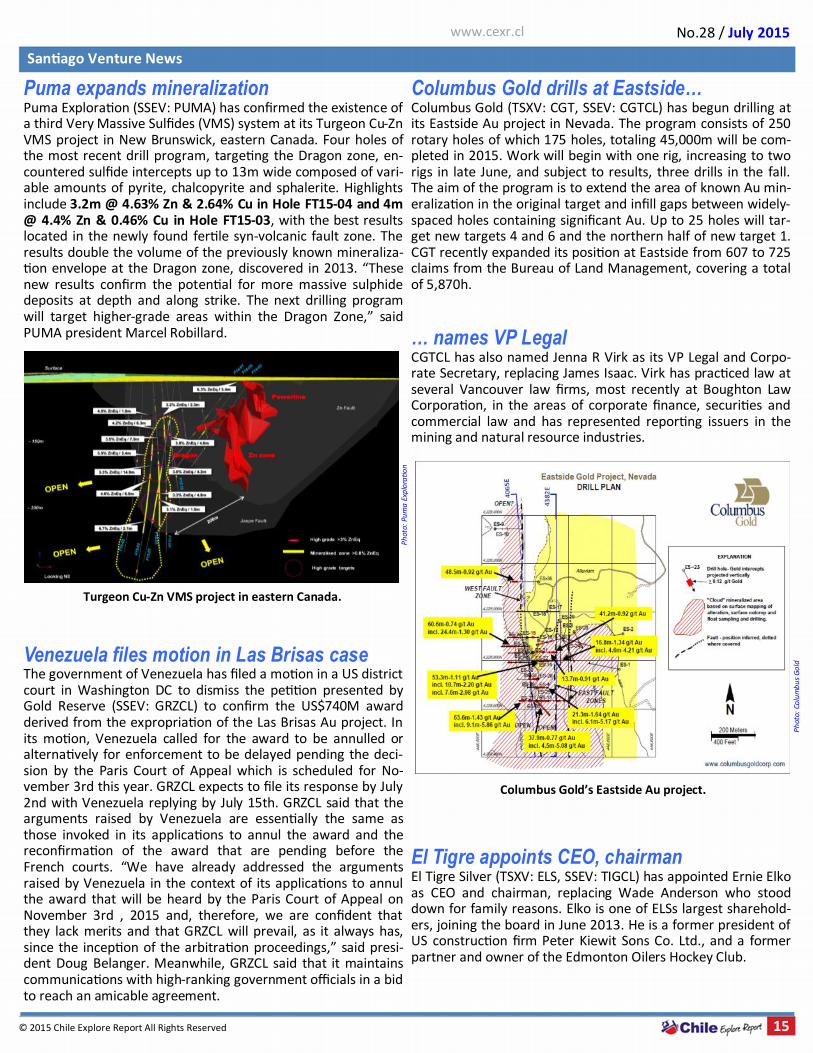

Puma expands mineralization Puma Exploration (SSEV: PUMA) has confirmed the existence of a third Very Massive Sulfides (VMS) system at its Turgeon Cu-Zn VMS project in New Brunswick, eastern Canada. Four holes of the most recent drill program, targeting the Dragon zone, en-countered sulfide intercepts up to 13m wide composed of vari-able amounts of pyrite, chalcopyrite and sphalerite. Highlights include 3.2m @ 4.63% Zn & 2.64% Cu in Hole FT15-04 and 4m @ 4.4% Zn & 0.46% Cu in Hole FT15-03, with the best results located in the newly found fertile syn-volcanic fault zone. The results double the volume of the previously known mineraliza-tion envelope at the Dragon zone, discovered in 2013. “These new results confirm the potential for more massive sulphide deposits at depth and along strike. The next drilling program will target higher-grade areas within the Dragon Zone,” said PUMA president Marcel Robillard.

Venezuela files motion in Las Brisas case The government of Venezuela has filed a motion in a US district court in Washington DC to dismiss the petition presented by Gold Reserve (SSEV: GRZCL) to confirm the US$740M award derived from the expropriation of the Las Brisas Au project. In its motion, Venezuela called for the award to be annulled or alternatively for enforcement to be delayed pending the deci-sion by the Paris Court of Appeal which is scheduled for No-vember 3rd this year. GRZCL expects to file its response by July 2nd with Venezuela replying by July 15th. GRZCL said that the arguments raised by Venezuela are essentially the same as those invoked in its applications to annul the award and the reconfirmation of the award that are pending before the French courts. “We have already addressed the arguments raised by Venezuela in the context of its applications to annul the award that will be heard by the Paris Court of Appeal on November 3rd , 2015 and, therefore, we are confident that they lack merits and that GRZCL will prevail, as it always has, since the inception of the arbitration proceedings,” said presi-dent Doug Belanger. Meanwhile, GRZCL said that it maintains communications with high-ranking government officials in a bid to reach an amicable agreement.

Columbus Gold drills at Eastside… Columbus Gold (TSXV: CGT, SSEV: CGTCL) has begun drilling at its Eastside Au project in Nevada. The program consists of 250 rotary holes of which 175 holes, totaling 45,000m will be com-pleted in 2015. Work will begin with one rig, increasing to two rigs in late June, and subject to results, three drills in the fall. The aim of the program is to extend the area of known Au min-eralization in the original target and infill gaps between widely-spaced holes containing significant Au. Up to 25 holes will tar-get new targets 4 and 6 and the northern half of new target 1. CGT recently expanded its position at Eastside from 607 to 725 claims from the Bureau of Land Management, covering a total of 5,870h.

… names VP Legal CGTCL has also named Jenna R Virk as its VP Legal and Corpo-rate Secretary, replacing James Isaac. Virk has practiced law at several Vancouver law firms, most recently at Boughton Law Corporation, in the areas of corporate finance, securities and commercial law and has represented reporting issuers in the mining and natural resource industries.

El Tigre appoints CEO, chairman El Tigre Silver (TSXV: ELS, SSEV: TIGCL) has appointed Ernie Elko as CEO and chairman, replacing Wade Anderson who stood down for family reasons. Elko is one of ELSs largest sharehold-ers, joining the board in June 2013. He is a former president of US construction firm Peter Kiewit Sons Co. Ltd., and a former partner and owner of the Edmonton Oilers Hockey Club.

© 2015 Chile Explore Report All Rights Reserved

No.28 / July 2015

Ph

oto:

Pu

ma

Exp

lora

tio

n

Columbus Gold’s Eastside Au project. P

hot

o: C

olu

mb

us

Go

ld

16

ABOUT CHILE EXPLORE REPORT: Chile Explore Report is published twelve times a year during the first week of each month by Tiger Information Services SpA, Badajoz 130, of 1406, Las Condes, Santiago; legal representative Iain Cassidy, [email protected]. The information contained herein is derived from sources believed to be reliable but no warranty expressed or implied exists between the recipient and the Publisher that this information is accurate. The contents of Chile Explore Report are intended for information purposes only based on news and information obtained and/or res earched by the Publisher and is not intended to be construed as advice to buy or sell shares in any security or asset. The Chile Explore Report is intended to be authoritative, critical and independent. The Publisher is not a stock tipper or promoter and is not paid, sponsored, provided with stock options or otherwise enticed to write positive pieces about the companies covered. The Publisher does invest in some of the companies’ active in the Chile exploration sector and ends up with dogs as well as winners. The Publisher has been involved in mining information research, analysis and publication for over ten years including roles such as investor relations, media relations, senior reporter and research consultant for companies involved in mining and exploration, and reputable industry informa-tion providers. The Publisher is not a registered securities professional and as such is not qualified to give personal or in dividual investment advice. Resource investing is risky and you could lose part or all of your investment. Consult a registered investment professional before making any investment in any security. For more information contact please write to [email protected]. COPYRIGHT: © 2013 Chile Explore Report. All Rights Reserved. Unauthorized duplication or distribution of all content herein prohibited. This document is copyright protected and may not be copied, dis seminated or distributed without the prior express consent of the publisher.

www.cexr.cl

© 2015 Chile Explore Report All Rights Reserved

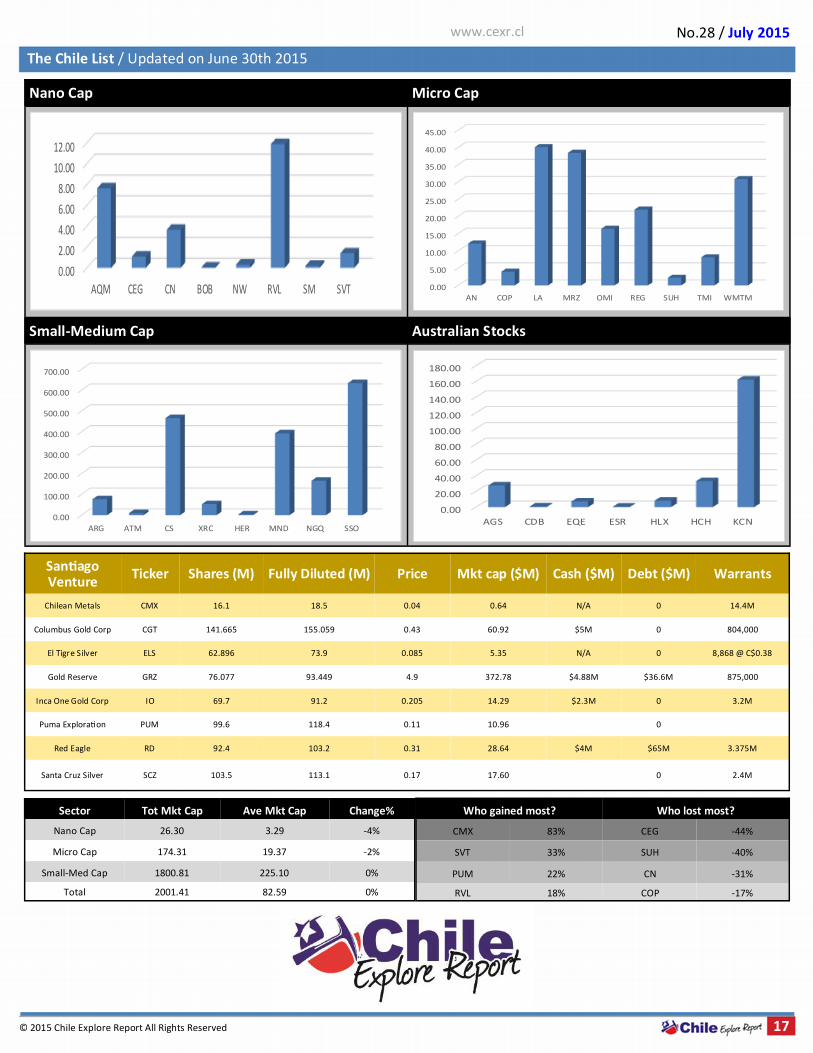

The Chile List / Updated on June 30th 2015

No.28 / July 2015

Nano Cap Ticker Shares (M) Fully Diluted (M) Price Mkt cap ($M) Cash ($M) Debt ($M) Warrants

AQM Copper AQM 139 139.246 0.055 7.65 N/A 0 25.4M

Cerro Grande Mining CEG 110 120 0.01 1.10 N/A 0 14.3M

Condor Resources CN 81.2 100.8 0.045 3.65 0.8 0 13.65M

Global Hunter BOB 14 14 0.02 0.05 0.0185 2.5 0

New World Resource NW 13.3 17.7 0.025 0.33 0.7 0 4M @ 0.2 Mar 2015

Revelo Resources RVL 91.4 129.6 0.13 11.88 N/A 0

1.23M @ $0.7 Jun 2015,

1.44M @ $0.88 Jan 2016,

28.5M @ $0.31 Apr 2019

Sendero Mining SM 21.9 28.5 0.01 0.22 0.5 0 5.4M

Savant Explorations SVT 70.65 88.06 0.02 1.41 0.7 0 11.8M

Micro Cap Ticker Shares (M) Fully Dilluted (M) Price Mkt cap ($M) Cash ($M) Debt ($M) Warrants

Arena Minerals AN 60.8 67.2 0.2 12.16 1.6 0 672k @$0.61 Apr 2014 / 7.1M @ $0.80 Oct 2014

Coro Mining COP 159.4 177.9 0.025 3.99 0.4 0 10.5

Los Andes Copper LA 200.4 200.9 0.2 40.08 0.6 0 None

Mirasol Resources MRZ 44.2 47.9 0.87 38.45 19.3 0 2.2M

Orosur Mining OMI 96.6 100.8 0.17 16.42 10.8 4.9 4.2

Regulus Resources REG 56.4 66.5 0.39 22.00 3.2 0 12.5m @ $1.60

Southern Hemisphere SUH 248.5 286.32 0.009 2.24 3 0 N/A

TriMetals Mining Inc TMI 135.7 144.2 0.06 8.14 29.5 0 1.7M

White Mountain Titan WMTM 88.1 114.2 0.35 30.84 2 0 12.7M

Small-Med Cap

Ticker Shares (M) Fully Dilluted (M) Price Mkt cap ($M) Cash ($M) Debt ($M) Warrants

Amerigo Resources ARG 173.7 187.4 0.44 76.43 9.2 0 None

Atacama Pacific Gold ATM 55.3 64.8 0.18 9.95 20.0 0 0.2M @ $1.00 4M @

$1.40

Capstone Mining CS 382 403.3 1.22 466.04 500.0 0 None

Exeter Resource XRC 88.4 96.8 0.6 53.04 30 0 None

Herencia Resources HER 24.43 21.40 0.173 4.23 N/A 0 N/A

Mandalay Resources MND 408.8 425.9 0.96 392.45 69 60 None

NGex Resources NGQ 187.7 192.5 0.88 165.18 34 0 None

Silver Standard Re-

sources SSO 80.7 80.7 7.85 633.50 234 N/A None

Australian Stocks

Ticker Shares (M) Fully Diluted (M) Price Mkt cap (A$M) Cash (A$M) Debt

(A$M) Warrants

Alliance Resources AGS 341.2 342.2 0.081 27.64 1.4 1.3 1M

Condor Blanco Mines CDB 938 1,116 0.001 0.94 N/A N/A N/A

Equus Mining EQE 379.3 379.3 0.019 7.21 7.3 N/A N/A

Estrella Resources ESR 114 116.08 0.006 0.68 1.1 0 None

Helix Resources HLX 235 270 0.035 8.23 1.8 N/A N/A

Hot Chili HCH 347.7 358.7 0.095 33.03 20 25 N/A

Kingsgate Consolida-

ted KCN 224 N/A 0.725 162.40 N/A N/A N/A

17

The Chile List / Updated on June 30th 2015

www.cexr.cl

© 2015 Chile Explore Report All Rights Reserved

No.28 / July 2015

Santiago Venture

Ticker Shares (M) Fully Diluted (M) Price Mkt cap ($M) Cash ($M) Debt ($M) Warrants

Chilean Metals CMX 16.1 18.5 0.04 0.64 N/A 0 14.4M

Columbus Gold Corp CGT 141.665 155.059 0.43 60.92 $5M 0 804,000

El Tigre Silver ELS 62.896 73.9 0.085 5.35 N/A 0 8,868 @ C$0.38

Gold Reserve GRZ 76.077 93.449 4.9 372.78 $4.88M $36.6M 875,000

Inca One Gold Corp IO 69.7 91.2 0.205 14.29 $2.3M 0 3.2M

Puma Exploration PUM 99.6 118.4 0.11 10.96 0

Red Eagle RD 92.4 103.2 0.31 28.64 $4M $65M 3.375M

Santa Cruz Silver SCZ 103.5 113.1 0.17 17.60 0 2.4M

Sector Tot Mkt Cap Ave Mkt Cap Change%

Nano Cap 26.30 3.29 -4%

Micro Cap 174.31 19.37 -2%

Small-Med Cap 1800.81 225.10 0%

Total 2001.41 82.59 0%

Who gained most? Who lost most?

CMX 83% CEG -44%

SVT 33% SUH -40%

PUM 22% CN -31%

RVL 18% COP -17%

Nano Cap Micro Cap

Small-Medium Cap Australian Stocks

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

40.00

45.00

AN COP LA MRZ OMI REG SUH TMI WMTM

0.00

100.00

200.00

300.00

400.00

500.00

600.00

700.00

ARG ATM CS XRC HER MND NGQ SSO

0.00

2.00

4.00

6.00

8.00

10.00

12.00

AQM CEG CN BOB NW RVL SM SVT

0.00

20.00

40.00

60.00

80.00

100.00

120.00

140.00

160.00

180.00

AGS CDB EQE ESR HLX HCH KCN