three warrants plays set to triple or more

TRANSCRIPT

BY DAVE FOREST, EDITOR, STRATEGIC TRADER

Three Warrants Plays Set to Triple or More

2

Strategic Trader THREE WARRANTS PLAYS SET TO TRIPLE OR MORE

Dear Reader,

Thank you for joining me, and welcome to Strategic Trader.

Right now, we’re on the cusp of the biggest revolution in money-making.

It involves investments called “warrants.”

For far too long, the explosive profit power of these investments has been reserved for billionaires. But that ends today. Because you don’t need to be an insider, accredited investor, or high-net-worth individual to take part.

All you need is a small stake – and this report – to get you started.

There’s simply no better opportunity for the smart speculator to make big, fast gains. That’s because…

• You can multiply your gains up to 217x more than stocks.

• You can build a substantial position for just a few hundred bucks. That means far less risk… for explosive upside potential.

• The trades can take off in no time – days or weeks in some cases.

And right now, we’re entering a new golden age of warrants. Last year, we saw more than a fourfold increase in these unique deals.

That’s why they’re one of the most exciting windfalls on my radar. And as you’ll see in this report, you can use them to play any trend… often for quadruple-digit gains.

Because at Strategic Trader, we have a unique proprietary system to pinpoint the world’s best warrants.

In short, we look at three important metrics: Time (T), Underlying Stock (U), and Volume (V). It’s how we find warrants with the most upside potential and the least amount of risk. You can read our full write-up on this proprietary formula here.

And if this is your first time trading warrants, check out our Warrants Master Course video to get started.

With that in mind, let’s take a look at three warrants set to triple or more… thanks to massive trends set to push them higher in the years ahead…

NO. 1: TRAVEL IS COMING BACK. IT’S TIME FOR A SHOPPING VACATION.2020 was a great time to shop overseas. That is, if you could travel overseas. For those who don’t know, the great thing about buying luxury goods overseas is the tax refund. Depending on where you travel, you can get a tax refund on certain goods over a specific dollar amount.

3

Strategic Trader THREE WARRANTS PLAYS SET TO TRIPLE OR MORE

With COVID lingering, travel today is still half in the grave. But it’s starting to wake up. That’s good news for travel-dependent businesses and luxury retailers around the world.

That’s also good news for companies that process those tax refunds…

Global Blue Group Holding AG (GB) is a powerhouse. Anyone shopping internationally probably recognizes the name Global Blue.

The company pioneered the concept of tax-free shopping in Sweden in 1980. That’s when travelers sailing from Trelleborg, Sweden, to Germany could get a tax refund in cash by presenting their purchases at customs. By 1999, the company was refunding 8 million shoppers per year.

Today, it’s the heavyweight of the tax-free shopping industry.

Despite a brutal 2020, the company’s quick cost-cutting measures and over $250 million in cash are helping it survive.

So is the commitment from major shareholders. This includes private equity firms Silver Lake Partners, Partners Group, and Chinese payments giant Ant Group. As a whole, those three own 87% of the company’s shares. With that much at stake, they’re not about to let Global Blue fail.

Globally, the company operates across more than 50 countries, processing refunds for over 29 million international shoppers. Overall, that adds up to about 66 million transactions per year, worth about $28 billion.

The way Global Blue’s refund process works is simple: You buy goods from a merchant. Before you head back home, you validate the form with customs at the airport. Finally, you get your refund, less some fees paid to Global Blue. It’s a win-win for everyone involved.

Today, the company operates two main segments. The first is the Tax-Free Shopping (TFS) segment. That makes up about 85% of revenue. The company serves over 300,000 merchants, including luxury brands like Prada, Burberry, Hermes, and Louis Vuitton. Overall, the TFS segment processes 35 million transactions per year.

It’s Global Blue’s bread and butter. That’s why it has about a 70% market share and is more than three times bigger than its next competitor.

The other segment is Added-Value Payment Solutions (AVPS). This is where Global Blue partners with a merchant to help with the actual transaction, not just the tax refund. That includes currency conversion at the point of sale.

So far, the company has about 150,000 points of interaction in the AVPS segment. That includes shops, ATMs, and e-commerce.

But what puts Global Blue head-and-shoulders above the rest is its transformation with technology.

4

Strategic Trader THREE WARRANTS PLAYS SET TO TRIPLE OR MORE

First, it introduced things like electronic kiosks to help validate transactions faster.

Global Blue Validation KiosksSource: Luxe.co

No more waiting in long lines to validate your purchase. All you need to do is scan the barcode on your form and that’s it. You can be on your way.

It’s all part of the company’s move toward a digital experience. In fact, about 54% of Global Blue validations today are digital.

Now, the company is taking things a step further with its Shop Tax Free app.

Global Blue’s Shop Tax Free appSource: Global Blue

5

Strategic Trader THREE WARRANTS PLAYS SET TO TRIPLE OR MORE

The app helps you track your tax refunds instantly to see how much you’re saving. It also has an autofill option for your tax forms, and helps you find locations to validate your purchase.

This is just the next step toward full automation. When that happens, you won’t even need to stop by the customs office or visit a kiosk. You can request your refund all through the company’s mobile app. Global Blue is working on that now.

As the dominant player in the space, the company is in a great position to recover from the COVID hangover.

That’s what makes Global Blue a great speculation on the travel industry. For the most part, investors are overlooking travel-related business. That includes Global Blue.

All that means is, we have the perfect opportunity to get in while everyone’s looking the other way… before the market catches on and shares take off.

However, we don’t want to play it with the company’s stock. With such high insider ownership, the warrants look like a better bet.

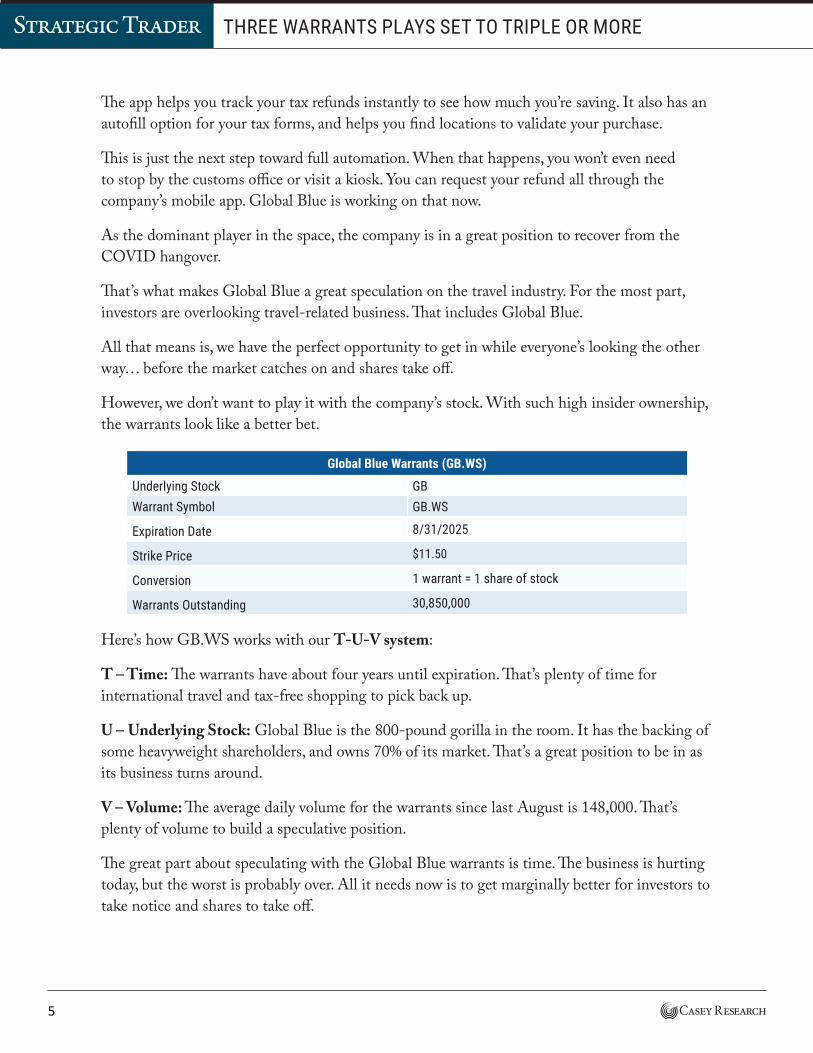

Global Blue Warrants (GB.WS)

Underlying Stock GBWarrant Symbol GB.WS

Expiration Date 8/31/2025

Strike Price $11.50

Conversion 1 warrant = 1 share of stock

Warrants Outstanding 30,850,000

Here’s how GB.WS works with our T-U-V system:

T – Time: The warrants have about four years until expiration. That’s plenty of time for international travel and tax-free shopping to pick back up.

U – Underlying Stock: Global Blue is the 800-pound gorilla in the room. It has the backing of some heavyweight shareholders, and owns 70% of its market. That’s a great position to be in as its business turns around.

V – Volume: The average daily volume for the warrants since last August is 148,000. That’s plenty of volume to build a speculative position.

The great part about speculating with the Global Blue warrants is time. The business is hurting today, but the worst is probably over. All it needs now is to get marginally better for investors to take notice and shares to take off.

6

Strategic Trader THREE WARRANTS PLAYS SET TO TRIPLE OR MORE

In the meantime, we can sit back and wait. Four years is a long time for travel to recover. We’re betting it happens faster than anyone thinks.

Action to Take: BUY the Global Blue August 31, 2025 $11.50 warrants (GB.WS) up to $2.50. Use a limit order.

Now, onto our second pick…

NO. 2: PROFITING FROM RISING CLOUD TECHNOLOGIESAlmost every company today runs their business in the “cloud.” It’s cost-effective and efficient.

That’s why we hear so much about the cloud and data centers. They’re popping up everywhere. In 2016, there were 870 exabytes of storage capacity in data centers globally, according to Statista. In 2021, that number is set to rise to 2,300. That’s nearly 4x growth in five short years.

It’s easy to see why. According to research firm IDC, data traffic is exploding. By 2025, the firm predicts we will create 463 exabytes of data per day. That’s four times greater than the total amount of data humans collectively created through 2020.

However, there are still some issues even with the advantages that cloud computing brings.

For many of us, cloud computing involves using a service like Dropbox instead of a bulky hard drive. No more lugging around your hard drive to access your files. You can take them anywhere using just your smartphone.

But for large enterprises, it’s something different.

For instance, the average enterprise uses 464 different software applications to manage their business, according to McAfee. With that many applications, it can get tricky to streamline all those technology systems… and make sure things work properly. Especially with exploding data traffic due to the growing work-from-home trend.

It would be a major problem if 500 employees were asking the IT department to fix 100 different software issues at the same time.

When your employees need to switch back and forth between that many applications, you better have the right system to handle it.

That’s why we’re recommending one small company working to do just that.

American Virtual Cloud Technologies (AVCT) is a growing player in cloud computing, specifically the Unified Communications-as-a-Service (UCaaS) business.

That may sound confusing, but it’s actually quite simple. AVCT helps companies streamline their technology systems. That includes the way they communicate, access data, and secure their networks.

7

Strategic Trader THREE WARRANTS PLAYS SET TO TRIPLE OR MORE

As I mentioned above, the average enterprise uses 464 different software applications to manage its business. With AVCT, clients can use one single point of contact for different parts of its business. And it’s all based in the cloud.

A company signs up with a service provider like AVCT. That gives the company access to its own virtualized data center in the cloud. It also gives it more flexibility to scale up or down depending on its needs.

The reason is, building out the tech is expensive. It also takes a lot of guesswork. Companies would need to accurately estimate how much capacity they need and try to figure out potential demand ahead of time.

With cloud computing companies like AVCT, there’s no more guesswork. Instead, you get on-demand computing power.

And there’s only one point of contact, not dozens. That helps reduce money on equipment and facilities. It’s less capital intensive, meaning potentially greater profit.

And UCaaS is a fast-growing market. More and more companies are turning to the cloud to manage their businesses – like AVCT customers Hertz and the City of Los Angeles. By 2025, 85% of enterprises will have a cloud-first principle, according to Gartner.

And according to Global Industry Analysts, the global unified communications market is set to grow from $31 billion in 2020 to $114 billion by 2027. Some of the major players include Zoom (ZM) and RingCentral (RNG).

It’s also still a highly fragmented market. No one player has more than 10% market share.

8

Strategic Trader THREE WARRANTS PLAYS SET TO TRIPLE OR MORE

AVCT is looking to change that through organic growth, and strategic partnerships and acquisitions.

Last April, it acquired Computex Technology Solutions. Computex provides its clients with four key services:

1. Managed cybersecurity

2. Managed infrastructure

3. Cloud services

4. Digital workplace (such as desktop/server management and help desk services for customers)

Computex has over 30 years of operating history. Today, the company counts over 350 clients with a 95% customer satisfaction rating.

But Computex was just the start. Just nine months later, AVCT acquired cloud communications platform Kandy from Ribbon Communications (RBBN). In exchange, Ribbon received $45 million of convertible debt and warrants to purchase 4.5 million shares of AVCT.

That means Ribbon didn’t just sell Kandy to AVCT. It now has a vested interest in the company, too. Add in a strategic partnership with AT&T – through its Partner Exchange program where AT&T customers can sign on with AVCT for specific services – and we can see where AVCT’s business is heading.

That’s why AVCT company insiders are all-in on making the company a leading player in the space. In fact, together, they own 86% of the company.

Plus, with work-from-home gaining more traction in the wake of COVID-19, UCaaS and other cloud services are more important than ever as demand for cloud-based solutions and streamlining ramps up.

But, with insiders owning 86% of the company, shares are in too few hands. That’s where the warrants come into play.

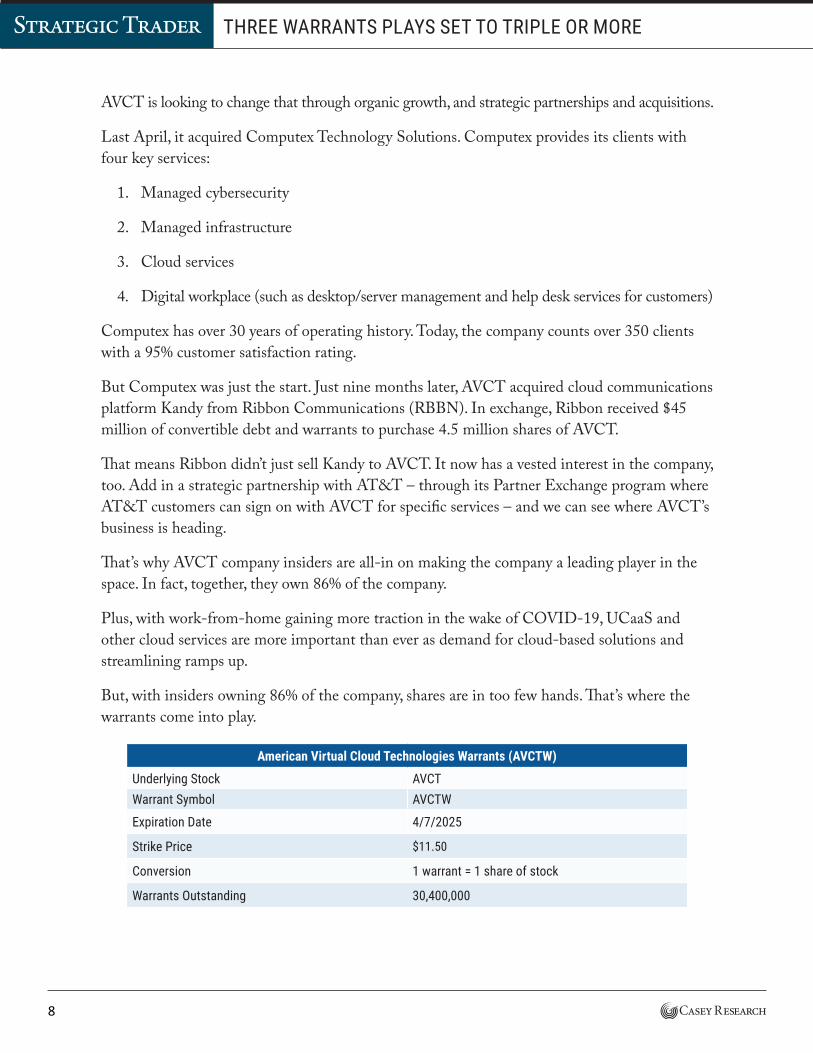

American Virtual Cloud Technologies Warrants (AVCTW)

Underlying Stock AVCTWarrant Symbol AVCTW

Expiration Date 4/7/2025

Strike Price $11.50

Conversion 1 warrant = 1 share of stock

Warrants Outstanding 30,400,000

9

Strategic Trader THREE WARRANTS PLAYS SET TO TRIPLE OR MORE

Here’s how AVCTW stacks up in our T-U-V system:

T – Time: The warrants have four years until expiration. That’s an eternity in the tech world.

U – Underlying Stock: AVCT is a growing player in a high-growth industry. The company’s management has past success in building businesses in the communications industry. Combining a fast-growing industry with an experienced management team is usually a recipe for success.

V – Volume: The average daily volume for the warrants since last April is 159,000. That’s plenty of volume to build a small speculative position.

With AVCT’s annual revenue run-rate at close to $100 million today, we’re getting in on the ground floor of potentially explosive growth. More and more companies are turning to the cloud to manage their business. That’s good news for AVCT and its warrants.

Action to Take: BUY the American Virtual Cloud Technologies April 7, 2025 $11.50 warrants (AVCTW) up to $1.50. Use a limit order.

And finally, onto our third opportunity…

NO. 3: PROFIT FROM A MONEY PROCESSING POWERHOUSEPaysafe Limited (PSFE) is a growing powerhouse that’s helping the budding esports and online gaming industry find its footing.

It makes money processing payments, and it’s a leader in digital commerce with over $92 billion processed in 2020.

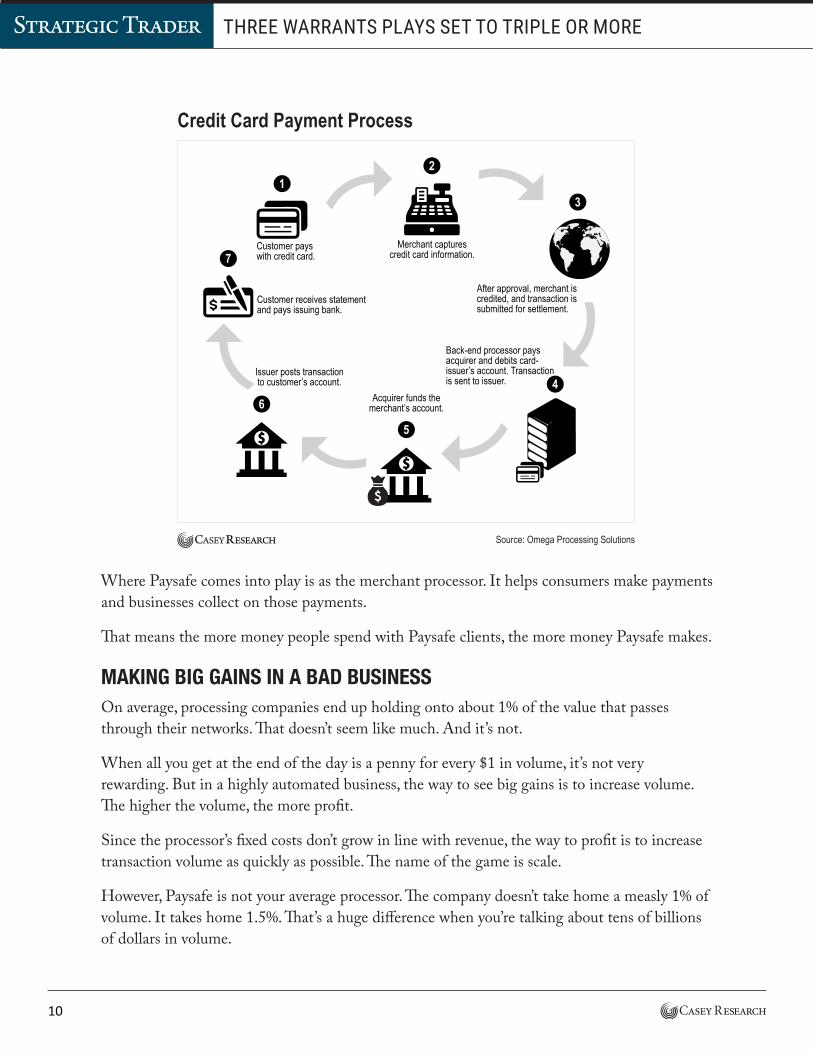

Here’s how the business works…

When a customer uses a credit card or other form of digital payment, it first goes through a processing company. A centralized approval company verifies the method of payment. That company pre-authorizes the charge.

So if you use a MasterCard or Visa, it verifies that your card is legitimate. It sends that verification back to the store to accept the charge.

The process looks a little something like this.

10

Strategic Trader THREE WARRANTS PLAYS SET TO TRIPLE OR MORE

Credit Card Payment Process

Customer pays with credit card.

Merchant captures credit card information.

After approval, merchant is credited, and transaction is submitted for settlement.

Back-end processor pays acquirer and debits card-issuer’s account. Transaction is sent to issuer.

Acquirer funds the merchant’s account.

Source: Omega Processing Solutions

2

31

46

5

7

Issuer posts transaction to customer’s account.

Customer receives statement and pays issuing bank.

Where Paysafe comes into play is as the merchant processor. It helps consumers make payments and businesses collect on those payments.

That means the more money people spend with Paysafe clients, the more money Paysafe makes.

MAKING BIG GAINS IN A BAD BUSINESSOn average, processing companies end up holding onto about 1% of the value that passes through their networks. That doesn’t seem like much. And it’s not.

When all you get at the end of the day is a penny for every $1 in volume, it’s not very rewarding. But in a highly automated business, the way to see big gains is to increase volume. The higher the volume, the more profit.

Since the processor’s fixed costs don’t grow in line with revenue, the way to profit is to increase transaction volume as quickly as possible. The name of the game is scale.

However, Paysafe is not your average processor. The company doesn’t take home a measly 1% of volume. It takes home 1.5%. That’s a huge difference when you’re talking about tens of billions of dollars in volume.

11

Strategic Trader THREE WARRANTS PLAYS SET TO TRIPLE OR MORE

HIGHER RISK, HIGHER REWARDYour traditional processing giant doesn’t like to take on much risk. When you process around $1.5 trillion in payments, like processing giant Fiserv, it’s hard to justify adding too much risk to your core business.

That’s where Paysafe has an advantage.

The company focuses on the digital economy and in specialized, higher-risk industries like sports betting and cryptocurrency trading. That’s why it can charge higher rates to its customers. It’s only fair for processing payments in industries that recently emerged as legal.

Right now, about 75% of Paysafe revenue comes from online payments. Research firm eMarketer expects global eCommerce spending to grow to $6.4 trillion by 2024, up from $4.3 trillion in 2020. It’s growing around 17% annually.

But eCommerce still has a long way to go. At $6.4 trillion, that’s still only about 22% of global retail sales.

There’s no doubt some of that is due to the shift in consumer spending from the pandemic economy. Paysafe is making the most of it.

A GIANT IN THE MAKINGToday, Paysafe counts over 250,000 businesses as clients across the U.S., Canada and Europe. It also has over 15 million active users in more than 120 countries.

12

Strategic Trader THREE WARRANTS PLAYS SET TO TRIPLE OR MORE

The company operates in three segments.

Integrated processing is the largest segment with over $67 billion processed in 2020. That’s large enough to make Paysafe the number four merchant acquirer in the U.S.

The reason is, businesses with physical locations and an online presence want a complete solution. So Paysafe provides them with a platform to do just that.

However, since it’s a more traditional method of payment processing, the company only earns about 1.1% of volume.

The company’s digital wallet segment is its next largest, at over $20 billion processed. It earns about 1.9% from this segment.

A digital wallet is exactly what it sounds like. It’s a virtual wallet where users can upload funds and send them anywhere.

Today, Paysafe is number two in the global stored-value digital wallet market. Customers include sports betting giants DraftKings, bet365 and William Hill.

However, the company’s third and smallest segment by revenue may be the one to catapult it to new heights. The eCash segment only makes up 23% of revenue, but it’s the fastest growing with the highest fees collected. The company brings in just over 7% of processing volume through eCash.

Paysafe is currently the world’s top iGaming eCash network… and that gives the company massive opportunity to scale.

This is all great news for the company and its shareholders.

It’s also great news for the warrants.

Paysafe Limited Warrants (PSFE.WS or PSFE+)

Underlying Stock PSFEWarrant Symbol PSFE.WS or PSFE+

Expiration Date 3/3/26

Strike Price $11.50

Conversion 1 warrant = 1 share of stock

Warrants Outstanding 53,901,025

For those of you just joining us, before we recommend a warrant, we run it through our proprietary T-U-V system. Here’s how Paysafe stacks up:

T – Time value. The warrants have just under five years until expiration. That’s plenty of time for the company to accelerate its growth plans in the digital payments space.

13

Strategic Trader THREE WARRANTS PLAYS SET TO TRIPLE OR MORE

U – Underlying stock potential. Paysafe is a billion-dollar company with a focus on eCommerce. Having the top spot in the growing iGaming industry gives the company an advantage. Plus, having a veteran financial services titan like Bill Foley as Chairman of the Board should help steer the company into a long-term winner.

V – Volume. The average daily volume for the warrants is over 800,000. That means over $2 million of warrants trade daily. That should be plenty of volume to build a speculative position.

Action to Take: BUY the Paysafe March 3, 2026 $11.50 warrants (PSFE.WS or PSFE+) up to $5. Use a limit order.

With all of our warrant recommendations, remember to be patient and don’t chase the stock.

As always, please only invest money you can afford to lose, and do not borrow money to invest.

Losing is a possibility with all investments.

Keep walking the path,

Dave Forest Editor, Strategic Trader

If any of the investment recommendations in this Special Report are trading above our buy-up-to prices by the time you read this, please be patient, put in a limit order, and don’t chase higher. Our recommendations usually come back into buying range.

To contact us, call toll free Domestic/International: 1-888-512-2739, Mon-Fri: 9am-7pm ET, or email us here.

© 2021 Casey Research, LLC. 55 NE 5th Ave, Delray Beach, FL 33483. All rights reserved. Any reproduction, copying, or redistribution, in whole or in part, is prohibited without written permission from the publisher.

Information contained herein is obtained from sources believed to be reliable, but its accuracy cannot be guaranteed. It is not designed to meet your personal situation—we are not financial advisors nor do we give personalized advice. The opinions expressed herein are those of the publisher and are subject to change without notice. It may become outdated and there is no obligation to update any such information.

Recommendations in Casey Research publications should be made only after consulting with your advisor and only after reviewing the prospectus or financial statements of the company in question. You shouldn’t make any decision based solely on what you read here.

Casey Research writers and publications do not take compensation in any form for covering those securities or commodities.

Casey Research expressly forbids its writers from owning or having an interest in any security that they recommend to their readers. Furthermore, all other employees and agents of Casey Research and its affiliate companies must wait 24 hours before following an initial recommendation published on the Internet, or 72 hours after a printed publication is mailed.