three bis research themes in the 2015 annual report

TRANSCRIPT

Three BIS research themes in the Annual Report

Hyun Song ShinEconomic Adviser and Head of Research

85th Annual General Meetinghttp://www.bis.org/speeches/sp150628b_presentation.pdf

http://www.bis.org/speeches/sp150628b.htm

http://www.bis.org/events/agm2015.htm

The Annual Report reflects three BIS research themes

2

1. Characteristics of financial intermediation Banks and non-banks “Know your players”

2. Global liquidity and spillovers First and second phases

3. Monetary and financial stability policy frameworks “Risk-taking channel” of monetary policy

http://www.bis.org/speeches/sp150628b.htm

1994

Sources: Bloomberg; national data.

3http://www.bis.org/speeches/sp150628b.htm

2014–15

1 Decomposition of the 10-year nominal yield according to an estimated joint macroeconomic and term structuremodel. Yields are expressed in zero coupon terms; for the euro area, French government bond data are used. Sources: Bloomberg; national data.

4http://www.bis.org/speeches/sp150628b.htm

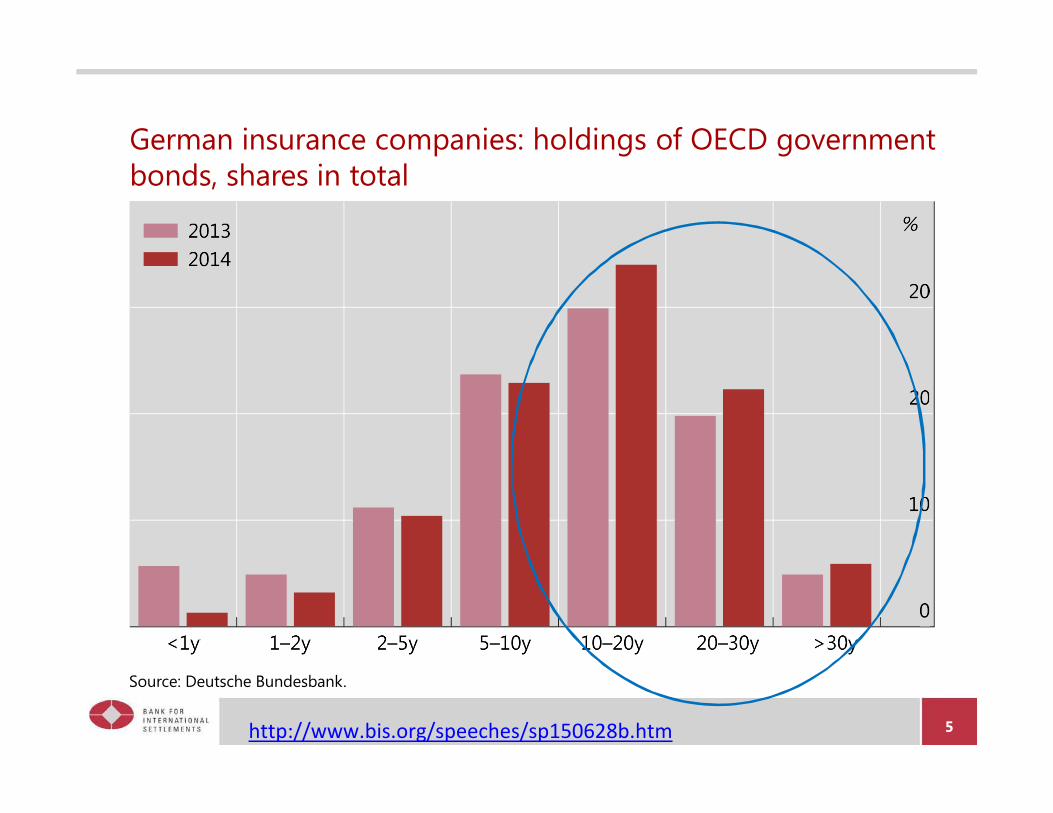

German insurance companies: holdings of OECD government bonds, shares in total

Source: Deutsche Bundesbank.

5http://www.bis.org/speeches/sp150628b.htm

Duration of assets and liabilities of European insurancecompanies

Source: Europ n Ins ance a d Occupational Pensions Authority (EIOPA).ea ur n

6http://www.bis.org/speeches/sp150628b.htm

“Knowing your players” – example of the insurance sector

7

Increasing weight of German insurance sector bond portfolio Insurance sector, 12.5% of total resident bond holdings In 2014, accounted for 40% of net purchase of bonds

Duration-matching as potential amplification channel In bond market rally, accumulate long-dated bonds;

chase disappearing yields

In reversals, reduce positions in long-dated bonds

Long-maturity bonds in foreign currency Amplification channel influences long rates elsewhere

http://www.bis.org/speeches/sp150628b.htm

Currencies are globaleven when monetary policy is territorial

US dollar-denominated cross-border bank claimsIn USD billions

2002

-

Source: BIS locational banking statistics by residence.

9

US dollar-denominated cross-border bank claimsIn USD billions

2003

Source: BIS locational banking statistics by residence.

10

US dollar-denominated cross-border bank claimsIn USD billions

2004

Source: BIS locational banking statistics by residence.

11

US dollar-denominated cross-border bank claimsIn USD billions

2005

Source: BIS locational banking statistics by residence.

12

US dollar-denominated cross-border bank claimsIn USD billions

2006

Source: BIS locational banking statistics by residence.

13

US dollar-denominated cross-border bank claimsIn USD billions

2007

Source: BIS locational banking statistics by residence.

14

US dollar- and euro-denominated cross-border bank claimsIn USD billions

2007

Source: BIS locational banking statistics by residence.

15

US dollar cross-border bank lending: 2002–07

16

Increase of $3.6 trillion between 2002 and 2007

Two thirds of increase ($2.3 trillion) due to US-Europe nexus

US-based banks account for only 35% of total increase in USdollar cross-border bank lending

European banks intermediating US dollar funding

At end-2007, European banks had twice the dollar claims onAsian borrowers as US-based banks ($393 bn vs $190 bn)

2008

US dollar-denominated cross-border bank claimsIn USD billions

Source: BIS locational banking statistics by residence.

17

2009

US dollar-denominated cross-border bank claimsIn USD billions

Source: BIS locational banking statistics by residence.

18

2010

US dollar-denominated cross-border bank claimsIn USD billions

Source: BIS locational banking statistics by residence.

19

2011

US dollar-denominated cross-border bank claimsIn USD billions

Source: BIS locational banking statistics by residence.

20

2012

US dollar-denominated cross-border bank claimsIn USD billions

Source: BIS locational banking statistics by residence.

21

2013

US dollar-denominated cross-border bank claimsIn USD billions

Source: BIS locational banking statistics by residence.

22

2014

US dollar-denominated cross-border bank claimsIn USD billions

Source: BIS locational banking statistics by residence.

23

US dollar-denominated cross-border bank claimsUSD billions Source: BIS locational banking statistics by residence.

2002 20042003 20052004 2005

2006 2007 2008 2009 2010

2011 2012 20142013

The Bank for International Settlements, often described as the central bankers’ bank, has warned for years of the dangers posed by ultra-low interest rates to the global economy.

http://www.ft.com/intl/cms/s/0/320475de-1c27-11e5-a130-2e7db721f996.html

85th Annual General Meeting June 2015http://www.bis.org/events/agm2015.htm

Currency denomination does not followthe national income boundary:

the case of non-banks

US dollar credit to non-banks outside the United States

Bank loans include cross-border and locally extended loans to non-banks outside the United States. For China and Hong Kong SAR, locally extendedloans are derived from national data on total local lending in foreign currencies on the assumption that 80% are denominated in US dollars. Forother non-BIS reporting countries, local US dollar loans to non-banks are proxied by all BIS reporting banks’ gross cross-border US dollar loans tobanks in the country. Bonds issued by US national non-bank financial sector entities resident in the Cayman Islands have been excluded.Sources: IMF, International Financial Statistics; Datastream; BIS international debt statistics and locational banking statistics by residence; BIS calculations.

28http://www.bis.org/speeches/sp150628b.htm

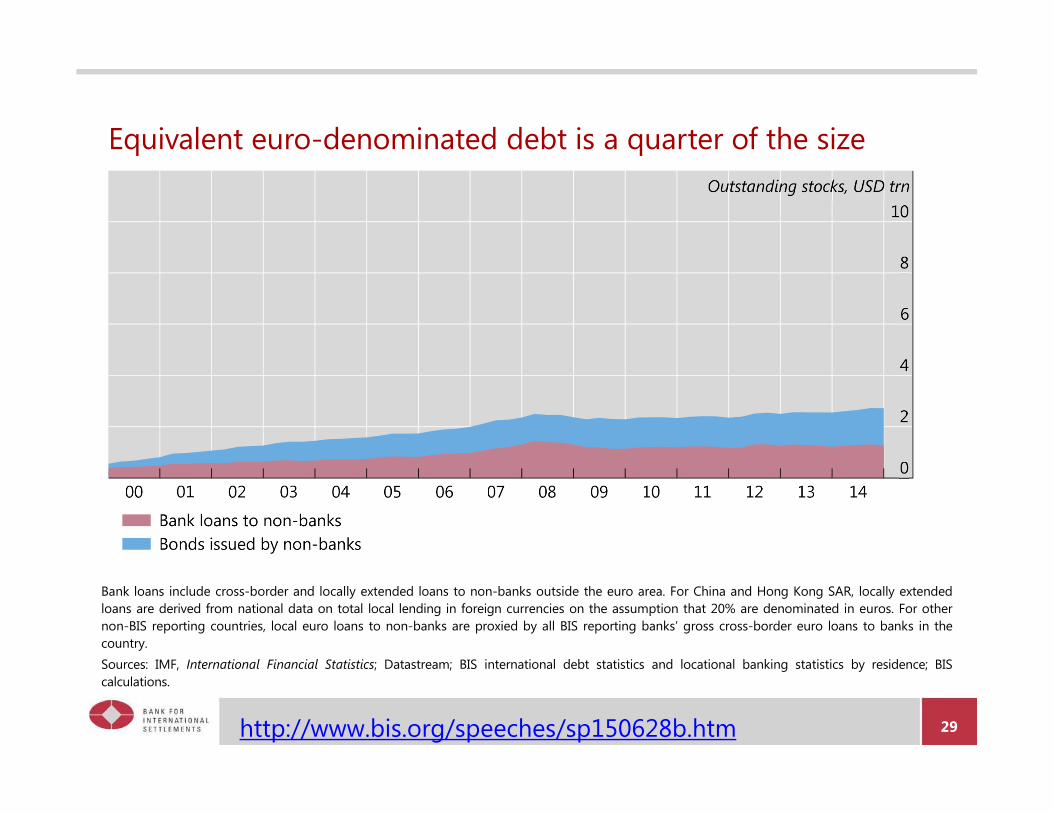

Equivalent euro-denominated debt is a quarter of the size

Bank loans include cross-border and locally extended loans to non-banks outside the euro area. For China and Hong Kong SAR, locally extendedloans are derived from national data on total local lending in foreign currencies on the assumption that 20% are denominated in euros. For othernon-BIS reporting countries, local euro loans to non-banks are proxied by all BIS reporting banks’ gross cross-border euro loans to banks in thecountry.Sources: IMF, International Financial Statistics; Datastream; BIS international debt statistics and locational banking statistics by residence; BIScalculations.

29http://www.bis.org/speeches/sp150628b.htm

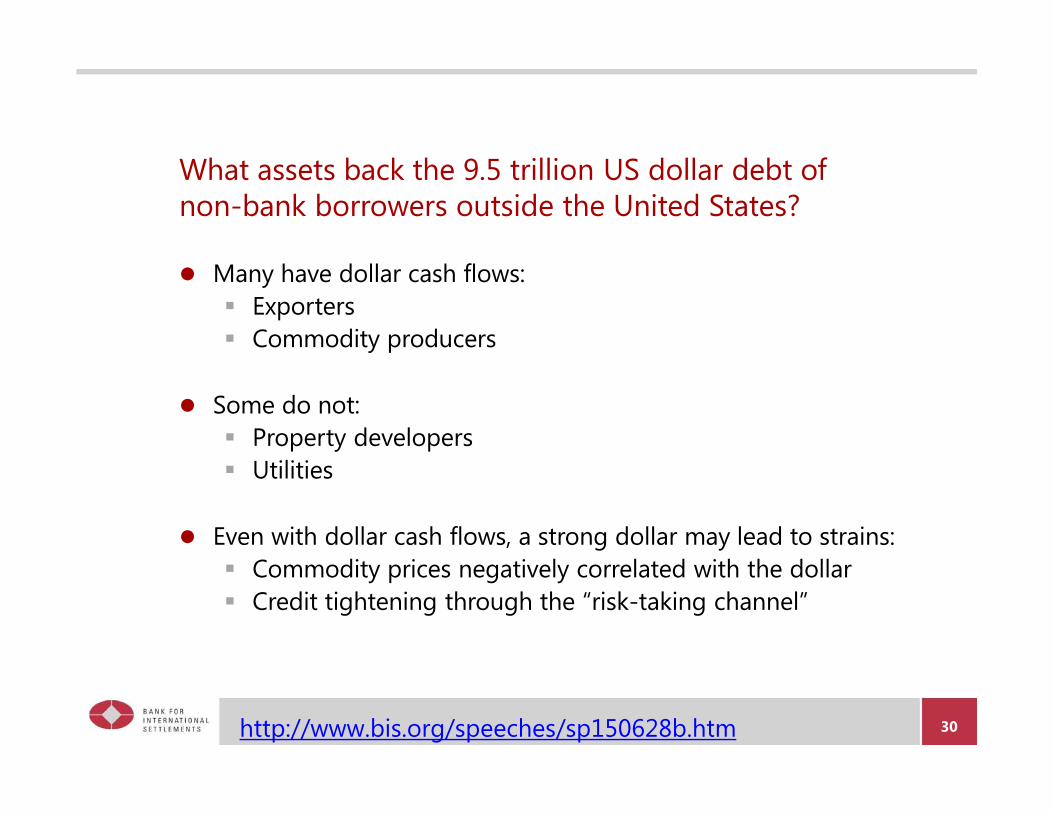

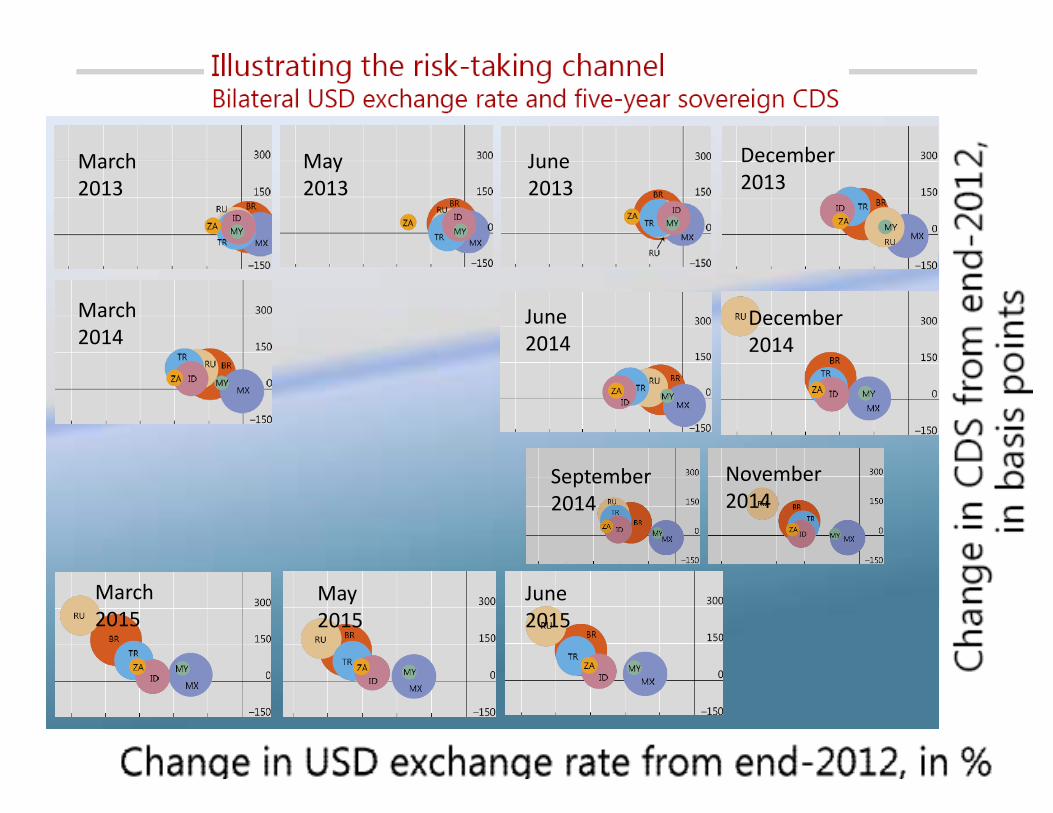

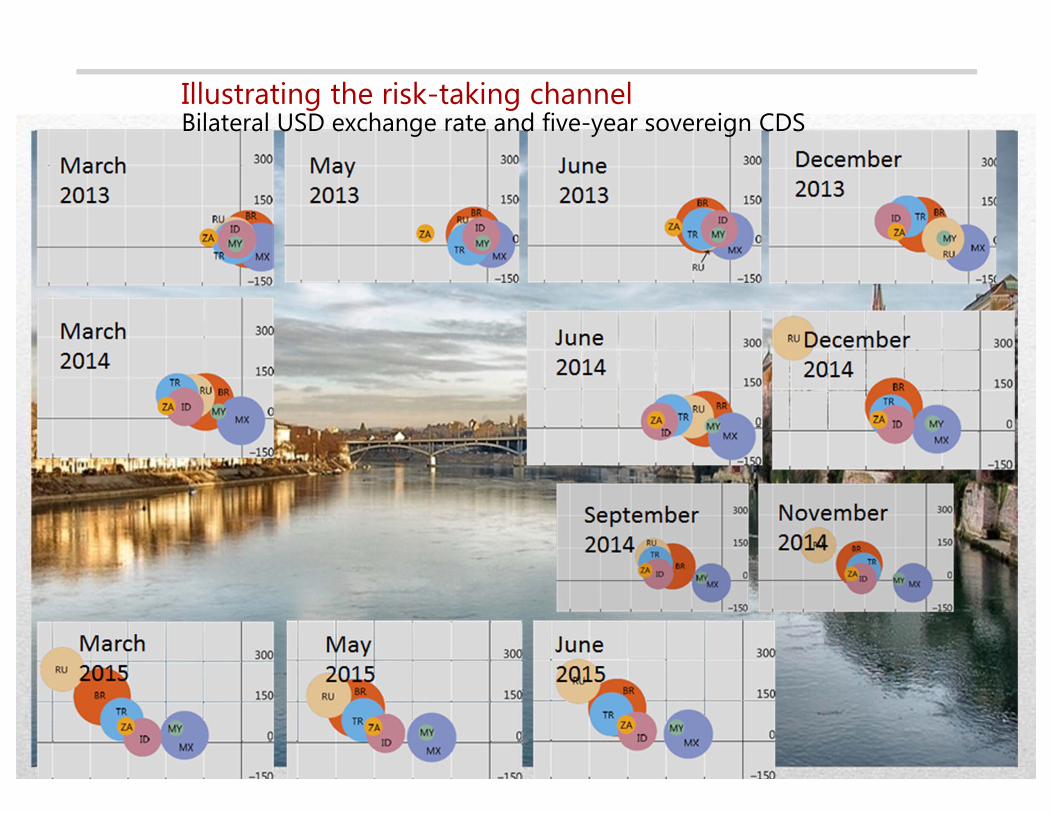

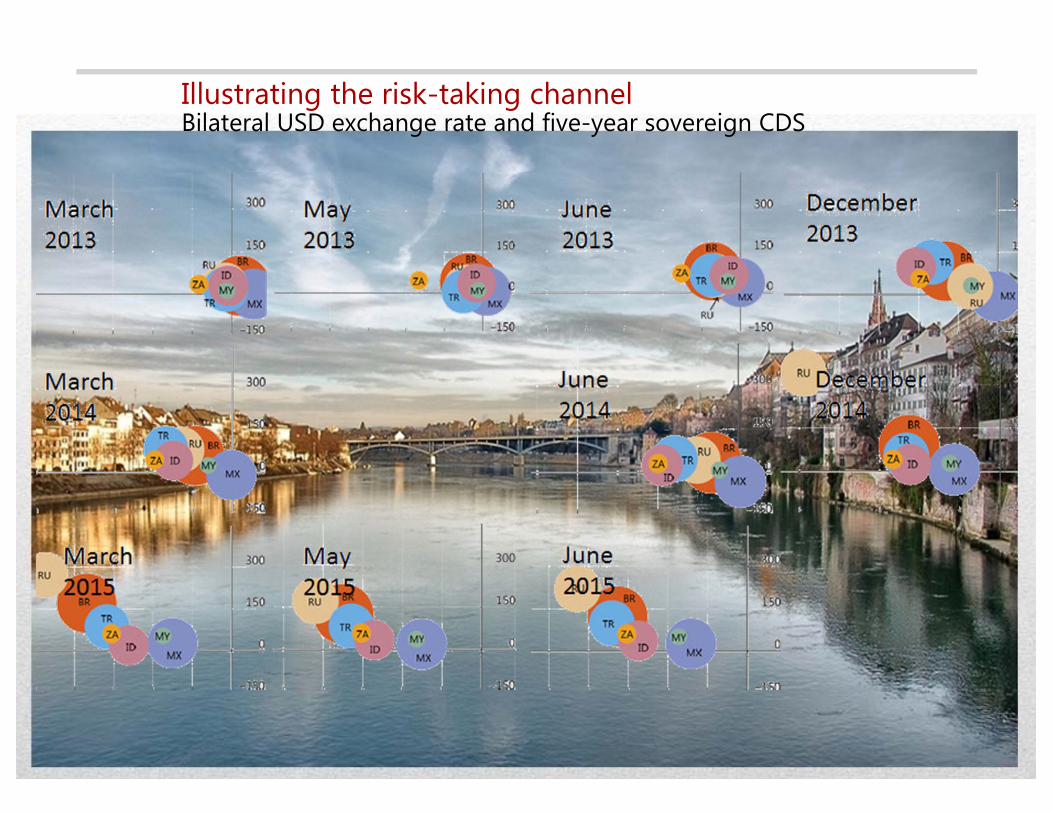

What assets back the 9.5 trillion US dollar debt of non-bank borrowers outside the United States?

30

Many have dollar cash flows: Exporters Commodity producers

Some do not: Property developers Utilities

Even with dollar cash flows, a strong dollar may lead to strains: Commodity prices negatively correlated with the dollar Credit tightening through the “risk-taking channel”

http://www.bis.org/speeches/sp150628b.htm

Illustrating the risk-taking channelBilateral USD exchange rate and five-year sovereign CDS

End-March 2013

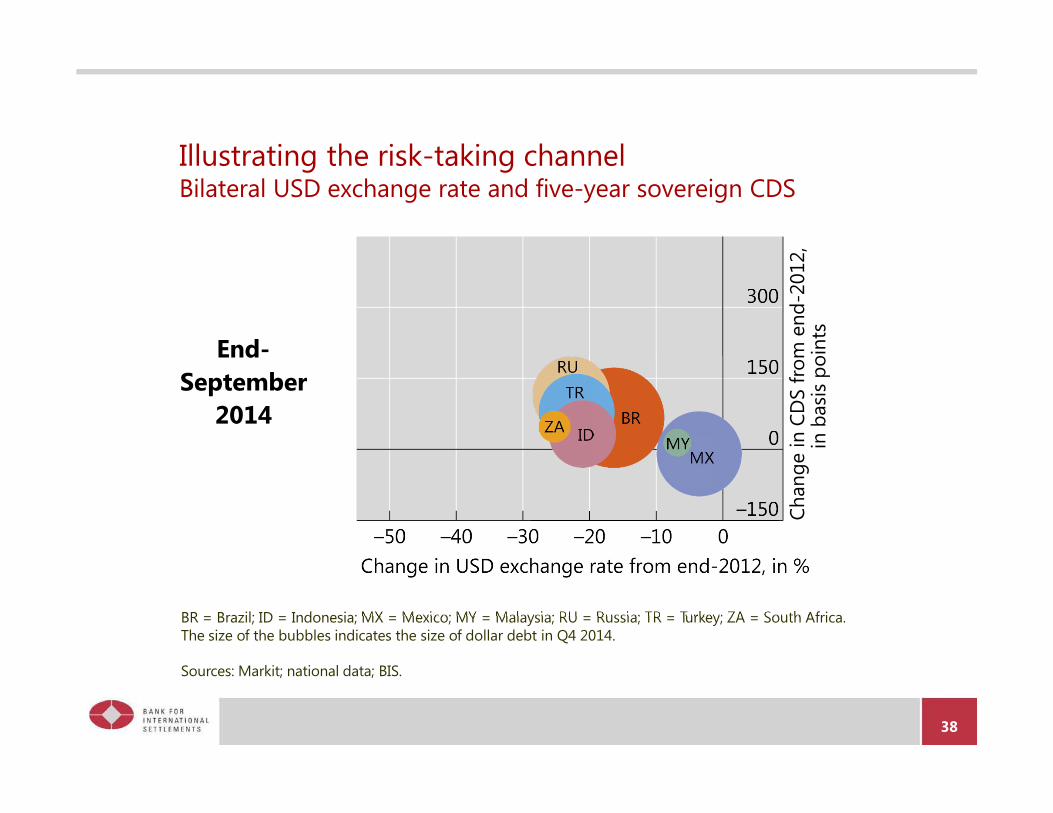

BR = Brazil; ID = Indonesia; MX = Mexico; MY = Malaysia; RU = Russia; TR = Turkey; ZA = South Africa. The size of the bubbles indicates the size of dollar debt in Q4 2014.

Sources: Markit; national data; BIS.

Chan

ge in

CD

S fro

m e

nd-2

012,

in

bas

ispo

ints

31

Illustrating the risk-taking channelBilateral USD exchange rate and five-year sovereign CDS

End-May 2013

BR = Brazil; ID = Indonesia; MX = Mexico; MY = Malaysia; RU = Russia; TR = Turkey; ZA = South Africa. The size of the bubbles indicates the size of dollar debt in Q4 2014.

Sources: Markit; national data; BIS.

Chan

ge in

CD

S fro

m e

nd-2

012,

in

bas

ispo

ints

32

Illustrating the risk-taking channelBilateral USD exchange rate and five-year sovereign CDS

End-June 2013

BR = Brazil; ID = Indonesia; MX = Mexico; MY = Malaysia; RU = Russia; TR = Turkey; ZA = South Africa. The size of the bubbles indicates the size of dollar debt in Q4 2014.

Sources: Markit; national data; BIS.

Chan

ge in

CD

S fro

m e

nd-2

012,

in

bas

ispo

ints

30

Illustrating the risk-taking channelBilateral USD exchange rate and five-year sovereign CDS

End-September

2013

BR = Brazil; ID = Indonesia; MX = Mexico; MY = Malaysia; RU = Russia; TR = Turkey; ZA = South Africa. The size of the bubbles indicates the size of dollar debt in Q4 2014.

Sources: Markit; national data; BIS.

Chan

ge in

CD

S fro

m e

nd-2

012,

in

bas

ispo

ints

34

Illustrating the risk-taking channelBilateral USD exchange rate and five-year sovereign CDS

End-December

2013

BR = Brazil; ID = Indonesia; MX = Mexico; MY = Malaysia; RU = Russia; TR = Turkey; ZA = South Africa. The size of the bubbles indicates the size of dollar debt in Q4 2014.

Sources: Markit; national data; BIS.

Chan

ge in

CD

S fro

m e

nd-2

012,

in

bas

ispo

ints

35

Illustrating the risk-taking channelBilateral USD exchange rate and five-year sovereign CDS

End-March 2014

BR = Brazil; ID = Indonesia; MX = Mexico; MY = Malaysia; RU = Russia; TR = Turkey; ZA = South Africa. The size of the bubbles indicates the size of dollar debt in Q4 2014.

Sources: Markit; national data; BIS.

Chan

ge in

CD

S fro

m e

nd-2

012,

in

bas

ispo

ints

36

Illustrating the risk-taking channelBilateral USD exchange rate and five-year sovereign CDS

End-June 2014

BR = Brazil; ID = Indonesia; MX = Mexico; MY = Malaysia; RU = Russia; TR = Turkey; ZA = South Africa. The size of the bubbles indicates the size of dollar debt in Q4 2014.

Sources: Markit; national data; BIS.

Chan

ge in

CD

S fro

m e

nd-2

012,

in

bas

ispo

ints

37

Illustrating the risk-taking channelBilateral USD exchange rate and five-year sovereign CDS

End-September

2014

BR = Brazil; ID = Indonesia; MX = Mexico; MY = Malaysia; RU = Russia; TR = Turkey; ZA = South Africa. The size of the bubbles indicates the size of dollar debt in Q4 2014.

Sources: Markit; national data; BIS.

Chan

ge in

CD

S fro

m e

nd-2

012,

in

bas

ispo

ints

38

Illustrating the risk-taking channelBilateral USD exchange rate and five-year sovereign CDS

Mid-November

2014

BR = Brazil; ID = Indonesia; MX = Mexico; MY = Malaysia; RU = Russia; TR = Turkey; ZA = South Africa. The size of the bubbles indicates the size of dollar debt in Q4 2014.

Sources: Markit; national data; BIS.

Chan

ge in

CD

S fro

m e

nd-2

012,

in

bas

ispo

ints

39

Illustrating the risk-taking channelBilateral USD exchange rate and five-year sovereign CDS

End-December

2014

BR = Brazil; ID = Indonesia; MX = Mexico; MY = Malaysia; RU = Russia; TR = Turkey; ZA = South Africa. The size of the bubbles indicates the size of dollar debt in Q4 2014.

Sources: Markit; national data; BIS.

Chan

ge in

CD

S fro

m e

nd-2

012,

in

bas

ispo

ints

40

Illustrating the risk-taking channelBilateral USD exchange rate and five-year sovereign CDS

End-March 2015

BR = Brazil; ID = Indonesia; MX = Mexico; MY = Malaysia; RU = Russia; TR = Turkey; ZA = South Africa. The size of the bubbles indicates the size of dollar debt in Q4 2014.

Sources: Markit; national data; BIS.

Chan

ge in

CD

S fro

m e

nd-2

012,

in

bas

ispo

ints

41

Illustrating the risk-taking channelBilateral USD exchange rate and five-year sovereign CDS

End-May 2015

BR = Brazil; ID = Indonesia; MX = Mexico; MY = Malaysia; RU = Russia; TR = Turkey; ZA = South Africa. The size of the bubbles indicates the size of dollar debt in Q4 2014.

Sources: Markit; national data; BIS.

Chan

ge in

CD

S fro

m e

nd-2

012,

in

bas

ispo

ints

42

Illustrating the risk-taking channelBilateral USD exchange rate and five-year sovereign CDS

Mid-June2015

BR = Brazil; ID = Indonesia; MX = Mexico; MY = Malaysia; RU = Russia; TR = Turkey; ZA = South Africa. The size of the bubbles indicates the size of dollar debt in Q4 2014.

Sources: Markit; national data; BIS.

Chan

ge in

CD

S fro

m e

nd-2

012,

in

bas

ispo

ints

40

March2013

May2013

June2013

March2014

June2014

September2014

November2014

December2014

March2015

May2015

June2015

December2013

Illustrating the risk-taking channelBilateral USD exchange rate and five-year sovereign CDS

Illustrating the risk-taking channelBilateral USD exchange rate and five-year sovereign CDS

Illustrating the risk-taking channelBilateral USD exchange rate and five-year sovereign CDS

Lessons for the international monetary and financial system

41

Channels of monetary policy spillovers Portfolio choice of investors with global reach Currencies are global, even if monetary policy is territorial

“Spillbacks” arise if accumulated vulnerabilities materialise Bidding-up of the international currency by borrowers Overhang of “net short” position in the international currency

How far can enlightened self-interest internalise the spillover effects?

What additional steps to go from keeping one’s own house in order to keeping the neighbourhood in order?

@HyunSongShinhttps://twitter.com/HyunSongShin/status/615263873868922880

http://www.bis.org/speeches/sp150628b.htm

Three BIS research themes in the Annual Reporthttp://www.bis.org/speeches/sp150628b.htm

Video: https://youtu.be/qXNf31yCUkw

the occasion of the Bank's Annual General Meeting, Basel, 28 June 2015http://www.bis.org/speeches/sp150628b.htm

Video: https://youtu.be/qXNf31yCUkw

스피카 - 하늘에서남자들이비처럼내려와https://youtu.be/Ku-8ifqmCVQ