threadneedle investments

DESCRIPTION

TRANSCRIPT

Nicolas Robin

Threadneedle Enhanced Commodities Strategy

May 2012

Agenda

01 Commodity market overview – risk back on the agenda

02 Commodities at Threadneedle – a strong fund management team

03 Threadneedle Enhanced Commodities Strategy

AP Appendix

2 PT/12/01215

3

01

Commodity market overview – risk back on the agenda

Market outlook: mixed macro, energy fundamentals strong

Asia

Prospects for Chinese growth weakening, with target now looking to be closer to 7.5%

Europe

Continued uncertainty amid key election year (France, Greece) and renewed concerns around

Spain

US

Macro environment starting to improve but monetary policy to continue to be accomodative and

benefit of an election year

4 PT/12/01215

Market outlook: mixed macro, energy fundamentals strong

Geopolitical risk still high: Iran, Syria, Irak, Nigeria, Libya

Wild card: Chavez’s health and the risk associated with political transition in Venezuela

On the supply side, Saudi Arabia probably running much closer to full capacity than anticipated

Mild weather in Northern hemisphere has put a lid on demand this winter

Despite the mild weather, the Brent market still remains extremely well supported

Japan’s continued problems with nuclear plants support demand for LNG and oil products

5 PT/12/01215

Market outlook: mixed macro, energy fundamentals strong

Environment continues to favour the energy sector and, within it, refined products

Downside risk in base metals and agricultural products

Improving US economy could lead to a stronger dollar and therefore put more pressure on base and

precious metals generally

6 PT/12/01215

US Natural Gas: it’s all about shale gas, still...

Shale gas expansion continues to be the

driving force behind US natural gas

weakness

The domestic nature of the US market and

the difference in pricing mechanism with

international LNG markets is the key to

understand the current price dislocation

The situation is likely to endure until US

producer curtail production and/or export

capacity comes online

7

Since 2000, U.S shale gas production has

increased 17-fold and now comprises about 30%

of total U.S. dry production

Source: Lippman Consulting, Inc. gross withdrawal estimates as of November 2011

and converted to dry production estimates with EIA-calculated average gross-to-dry

shrinkage factors by state and/or shale play. Note: 2011 is annual for first 10 months.

Annual shale gas production (dry) trillion cubic feet

PT/12/01215

…and the mild weather this winter has exacerbated the glut

Mild temperatures in the US this winter are

to blame for the sharp decline recorded so

far this year

Inventories are now trending more than

50% above averages and may lead to

containment issues later this year

Average injections during the injection

season would take inventories to unknown

territory near 4.5Tcf

8

Total Lower 42 Natural Gas Inventories

Source: IEA, Threadneedle

1 Estimated inventory trajectory assuming average injections

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

1 4 7 10 13 16 19 22 25 28 31 34 37 40 43 46 49 52

Week

Avg High Low 2010

2011 2012 2012E1

PT/12/01215

Libyan production has been recovering faster than anticipated but spare capacity is shrinking fast…

Oil and the return of geopolitical risk

OPEC crude production (million barrels per day)

Source: International Energy Agency as at 12 April 2012

1 Capacity levels can be reached within 30 days and sustained for 90 days

2 Includes half of Neutral Zone production

3 Nigeria’s current capacity estimate excludes some 200kb/d of shut-in capacity

4 Includes upgraded Orinoco extra-heavy oil assumed at 470kb/d in September

Supply Sustainable

production capacitiy1

Spare capacity vs.

March 2012 supply

3Q12 Average

Sustainable

Production Capacity

3Q12 Average

Sustainable 2Q12

Capacity Jan 2012 Feb 2012 Mach 2012

Algeria 1.20 1.14 1.14 1.18 0.04 1.23 0.05

Angola 1.70 1.76 1.68 1.90 0.22 2.00 0.10

Ecuador 0.48 0.48 0.48 0.52 0.04 0.54 0.02

Iran 3.30 3.35 3.30 3.51 0.21 3.45 -0.07

Kuwait2 2.75 2.70 2.72 2.84 0.12 2.89 0.05

Libya 1.15 1.29 1.32 1.39 0.07 1.40 0.01

Nigeria3 2.04 2.10 2.05 2.55 0.50 2.59 0.04

Qatar 0.82 0.81 0.81 0.86 0.05 0.86 0.00

Saudi Arabia2 9.85 10.00 10.00 11.88 1.88 11.88 0.00

UAE 2.58 2.59 2.65 2.75 0.10 2.79 0.04

Venezuela4 2.47 2.46 2.44 2.53 0.09 2.53 0.00

OPEC-11 28.34 28.67 28.59 31.90 3.31 32.14 0.24

Iraq 2.65 2.62 2.84 3.01 0.17 3.13 0.12

Total OPEC 30.99 31.29 31.43 34.91 3.48 35.27 0.36

Excluding Iraq, Nigeria and Venezuela 2.54

9 PT/12/01215

Oil and the return of geopolitical risk

10

… demand continues to strengthen, driven by Asia / Pacific

Global oil demand – 2010–2012 (million barrels per day)

Source: International Energy Agency as at 12 April 2012

2010 2011 2012

Q1 Q2 Q3 Q4 Total Q1 Q2 Q3 Q4 Total Q1 Q2 Q3 Q4 Total

Africa 3.3 3.5 3.4 3.5 3.4 3.4 3.4 3.3 3.4 3.4 3.5 3.6 3.5 3.6 3.5

Americas 29.5 30.0 30.6 30.2 30.1 30.1 29.8 30.2 29.9 30.0 29.6 29.7 30.3 30.2 30.0

Asia / Pacific 27.2 27.0 26.7 28.3 27.3 28.6 27.3 27.4 28.9 28.0 29.4 28.1 28.0 29.4 28.7

Europe 15.0 14.9 15.6 15.5 15.3 14.9 14.8 15.4 14.8 15.0 14.4 14.3 15.1 14.7 14.6

FSU 4.4 4.3 4.5 4.6 4.4 4.4 4.6 4.8 4.8 4.7 4.6 4.7 4.9 4.9 4.8

Middle East 7.4 7.8 8.3 7.7 7.8 7.6 8.0 8.5 8.0 8.0 7.9 8.2 8.7 8.2 8.2

World 86.8 87.5 89.1 89.8 88.3 89.1 87.9 89.6 89.8 89.1 89.4 88.6 90.6 91.0 89.9

Annual change (%) 2.6 3.3 3.5 3.5 3.2 2.6 0.5 0.5 0.0 0.9 0.4 0.7 1.1 1.3 0.9

Annual change (mb/d) 2.2 2.8 3.0 3.1 2.8 2.3 0.4 0.5 0.0 0.8 0.3 0.6 1.0 1.2 0.8

Changes from last OMR (mb/d) 0.00 0.01 0.02 0.01 0.01 0.04 0.04 0.05 0.02 0.03 0.10 -0.14 0.10 -0.14 -0.02

PT/12/01215

Non-OECD: Demand by product

11

Demand Annual Change (kb/d) Annual Change %

Dec 2011 Jan 2012 Feb 2012 Jan 2012 Feb 2012 Jan 2012 Feb 2012

LPG & Ethane 5,111 4,990 5,071 83 66 1.7 1.3

Naphtha 2,589 2,725 2,729 -96 -129 -3.4 -4.5

Motor Gasoline 8,789 8,526 8,674 547 467 6.9 5.7

Jet Fuel & Kerosene 2,777 2,784 2,718 48 -37 1.8 -1.4

Gas/Diesel Oil 13,804 13,488 13,796 505 399 3.9 3.0

Residual Fuel Oil 5,657 5,409 5,730 -308 90 -5.4 1.6

Other Products 5,576 5,528 5,808 282 202 5.4 3.6

Total Products 44,302 43,450 44,527 1,061 1,057 2.5 2.4

Source: International Energy Agency as at 12 April 2012

Non-OECD: Demand by product (thousand barrels per day)

PT/12/01215

Non-OECD product demand continues to be strong, driven by transportation fuels (Motor Gasoline

and Diesel)

Chinese Strategic Petroleum Reserve: more capacity coming on stream

12

Operator Location Capacity Status Completion

Sinopec Zhenhai, Zhejiang 32.7 Filled 3Q06

Sinochem Zhoushan, Zhejiang 31.4 Filled 4Q07

Sinopec Huangdao, Shandong 20.1 Filled 4Q07

CNPC Dalian, Liaoning 18.9 Filled 4Q08

Phase 1 103.2 2008

CNPC Dushanzi, Xinjiang 18.9 Completed and ready to

be filled 3Q11

CNPC Lanzhou, Gansu 18.9 Completed and ready to

be filled 4Q11

CNPC Jinzhou, Liaoning 18.9 Under construction 1Q12

Sinopec Tianjin 22.0 Unser construction 1Q12

Other 90.3 2013

Phase 2 169.0 2013

Phase 3 227.8 2016

Total SPR 500.0

Chinese Strategic Petroleum Reserve Sites (million barrels)

According to the IEA, up to 79mb of new SPR capacity would be ready to receive Crude Oil in 2012

Source: IEA

PT/12/01215

US Shale Oil: towards of remake of shale gas in oil?

Production growth in the unconventional US

Oil plays is projected to increase strongly

from 2013 onwards

Shale Oil expansion is set to mimic the

production growth in Natural Gas at the end

of the last decade

This production growth will put increasing

strain on oil logistics

13

US shale oil plays could add well over 2-m b/d of

output over this decade

Source: Citi Investment Research and Analysis

End Game

27 February 2012

Citigroup Global Markets 8

Figure 11. US shale oil plays could add well over 2-m b/d of output over this decade

Bakken

Eagle Ford

Granite Wash

Permian Delaware

Permian Midland

Niobrara

Anadarko

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022

Bakken Eagle Ford Granite Wash Permian Delaware

Permian Midland Niobrara Uinta Barnett

Utica Woodford/Anadarko Monterey Upside potential?

Source: Citi Investment Research and Analysis

The surplus of crude production and imports over refinery needs is growing more

acute too. Although Cushing crude stocks were able to draw down in 2H'11, this

was only due to PADD II refiners running at blistering utilization rates as they made

the most of favorable margins. These high rates, hitting 98% at times, have only just

managed to keep stocks roughly flat, but will soon be unable to keep rising crude

production in check. Outages should place huge pressures on the logistical system.

In particular, PADD II planned maintenance in 2012 is likely to hit in the fall, with a

high of 400-k b/d of planned maintenance set for this October; and given that

unplanned outages in PADD II have averaged around 50-k b/d over planned

maintenance capacity in the last few years, actual outages could be somewhat

higher, and in our view should drive a major blow-out in late-2012.

…and this is already happening while

refineries are running at full steam

PT/12/01215

US Shale Oil: rising Canadian and US production choking logistics

The rapid growth in US unconventional

Crude Oil production, couple with that of

Western Canada, has created a crude

corridor in the US Midwest

While crude oil logistics are being upgraded

(rail terminal, new pipelines, reversal of

existing), such upgrades are not keeping

pace with production growth

Constraints surrounding US crude oil

exports are likely to keep US physical

market crude prices depressed

14

Simplified schematic of the crude glut corridor with major

production centres feeding Cushing and the broad direction of

crude oil flows amongst the PADD regions

Source: EIA, Citi Investment Research and Analysis

PT/12/01215

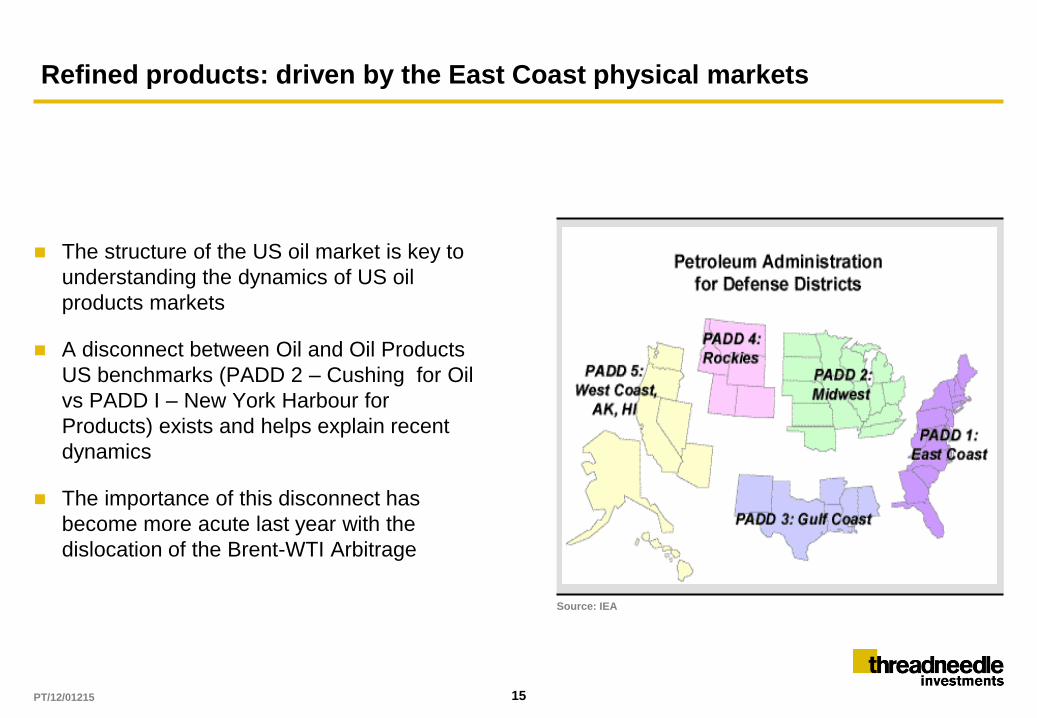

Refined products: driven by the East Coast physical markets

The structure of the US oil market is key to

understanding the dynamics of US oil

products markets

A disconnect between Oil and Oil Products

US benchmarks (PADD 2 – Cushing for Oil

vs PADD I – New York Harbour for

Products) exists and helps explain recent

dynamics

The importance of this disconnect has

become more acute last year with the

dislocation of the Brent-WTI Arbitrage

15

Source: IEA

PT/12/01215

Refining capacity in the US North East (PADD I): dangerously shrinking…

16

Owner City State Operating Crude Unit

capacity(bbl / calender day) Percent of Region (%) Status

Operating and Idled

Refineries

Conoco Phillips Linden NJ 238,000 17 Operating

PBF Energy Co. LLC Delaware City DE 182,200 13 Operating

PBF Energy Co. LLC Paulsboro NJ 160,000 12 Operating

United Refining Co. Warren PA 65,000 5 Operating

American Refining Bradford PA 10,000 1 Operating

Ergon-West Virgina Newell / Congo WV 20,000 1 Operating

Hess Corp. Port Reading NJ 01 0 Operating

Sunoco Inc. Philadelphia PA 335,000 24 Operating, For Sale

Sunoco Inc. Marcus Hook PA 178,000 13 Idled 12/2011, For Sale

Conoco Phillips Trainer PA 185,000 13 Idled 9/2011, For Sale

Total operating and idled 1,373,200 100

Recently shut refineries

Western refining Yorktown VA 66,300 Shut 9/2010

Sunoco Inc. Eagle Pt / Westville NJ 145,000 Shut 2/2010

Source: U.S. Energy Information Administration

1 Hess Port Reading has a production capacity of 70,000 bbl / calendar day but no crude unit capacity.

Notes: indicates operating refineries for sale and at risk of shutdown. indicates idled refineries for sale and at risk of shut down. indicates shut refineries. Total refinery capacity

excludes two refineries that primarily asphalt, as well as the Yorktown VA and Eagle Point refineries that were shut down in 2010.

US North East refiners have traditionally used Brent and Brent related grade as feedstock

The dislocation of the Brent WTI arbitrage has had devastating effects on PADD I margins and led to a string of closures

Up to 50% of PADD I distillation capacity is set to close by July 2012

PT/12/01215

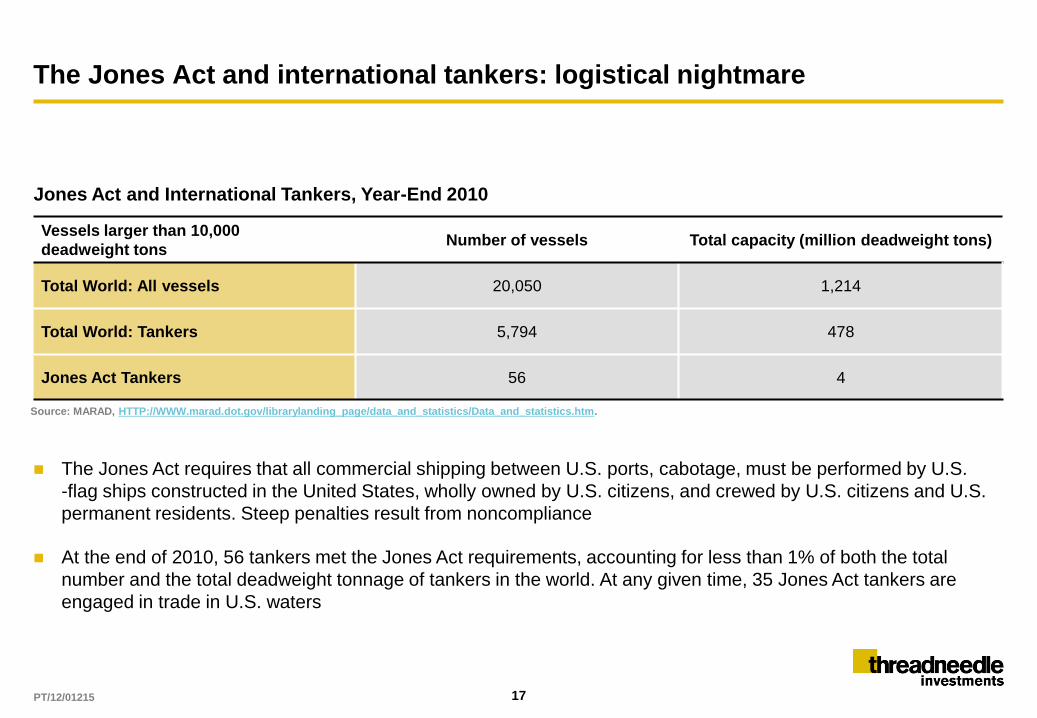

The Jones Act and international tankers: logistical nightmare

17

Vessels larger than 10,000

deadweight tons Number of vessels Total capacity (million deadweight tons)

Total World: All vessels 20,050 1,214

Total World: Tankers 5,794 478

Jones Act Tankers 56 4

Source: MARAD, HTTP://WWW.marad.dot.gov/librarylanding_page/data_and_statistics/Data_and_statistics.htm.

Jones Act and International Tankers, Year-End 2010

The Jones Act requires that all commercial shipping between U.S. ports, cabotage, must be performed by U.S.

-flag ships constructed in the United States, wholly owned by U.S. citizens, and crewed by U.S. citizens and U.S.

permanent residents. Steep penalties result from noncompliance

At the end of 2010, 56 tankers met the Jones Act requirements, accounting for less than 1% of both the total

number and the total deadweight tonnage of tankers in the world. At any given time, 35 Jones Act tankers are

engaged in trade in U.S. waters

PT/12/01215

PADD I Petroleum Product Assets: further logistical bottlenecks

Lack of ports and terminal capable of handling

waterbone products in PADD I is the largest

logistical hurdle

Existing infrastructure handles crude oil

deliveries and docks and tanks are not

equipped to receive oil products

The Colonial Pipeline delivers more than

500kbd into NY Harbour

Additional capacity on the line could be up to

100kbd according to the DOE, far less than the

lost output should Sunoco’s Philadelphia

refinery be shut permanently

18

U.S. Energy Information Administration | Potential Impacts of Reductions in Refinery Activity on Northeast Petroleum Product Markets 6

3. Logistical Constraints on Moving Product to the Northeast

As discussed below, ULSD replacement supplies may have limited foreign sources and may need to

come from the U.S. Gulf Coast. When suppliers move product from the U.S. Gulf Coast to the Northeast,

they will need to overcome both pipeline and tanker constraints. Currently, most Gulf Coast products

move to the Northeast through the Colonial Pipeline, which is running near capacity. The Lower Atlantic,

excluding Florida, is supplied largely from the Gulf Coast by the Colonial and Kinder Morgan Plantation

pipelines. The Colonial pipeline extends into the Northeast, but the majority of its volumes supply the

Southeast. Still, more than 500,000 bbl/d of gasoline and distillate are delivered into the Northeast via

the Colonial pipeline, which terminates in Linden, NJ (part of New York Harbor). This pipeline may be

able to move slightly more product into the Northeast in the coming summer. In the short term,

however, additional movements into the Northeast are unlikely to exceed 100,000 bbl/d – well less than

the expected production shortfall if the Sunoco Philadelphia refinery is closed.

The larger logistical hurdle is the lack of terminal and pipeline connections to move products from

waterborne vessels (either from foreign supply sources or from the Gulf Coast) into the product

distribution system that currently supplies areas through Pennsylvania and into western New York

(Figure 1). Ports serving Philadelphia-area refineries primarily handle crude oil and their docks and tanks

are not equipped to offload waterborne products.

Figure 1. Petroleum Product Assets in the Northeast

Source: U.S. Energy Information Administration.

Petroleum Product Assets in the Northeast

PT/12/01215

PADD I Gasoline balances: tighter, considerably

19

2007 2008 2009 2010 20111 2012 outlook 2013 outlook

Consumption 1,660 1,630 1,620 1,610 1,540 1,540 1,540

Supply 1,660 1,630 1,610 1,610 1,540 1,380 1,300

In-Region

Production (+) 750 710 640 560 580 420 350

Ethanol Inputs (+) 100 120 140 150 150 150 150

Net Receipts from

other Regions (+) 120 120 200 270 270 250 250

Imports (+) 720 700 630 -610 560 560 550

Exports (-) 20 20 - - - - -

Stock Decrease (+) /

Increase (-) - -10 - 10 - - -

Surplus (+) / Gap (-) - - - - - -160 -240

1 Data through November 2011

Notes: Projected consumption is based on data from EIA’s Short-Term Energy Outlook. Projected production is based on assumed yields and the capacity of remaining refineries. Sunoco

Philadelphia is assumed to close in July 2012. Projected imports are 3-year historical averages adjusted down by U.S. Virgin Islands contributions. Historical net receipts are estimated.

Projected net receipts are 3-year historical averages. The Surplus / Gap indicates the under-or-over supply needed to meet consumption.

Northeast Gasoline Supply-Demand Balance and Projections: Annual average 2007-2013

The impact of refinery closures is even more severe in the PADD I Gasoline market

The market is set to turn into a marked deficit this summer in the middle of the summer driving season making

the supply response even more difficult

PT/12/01215

Conclusion: energy remains our preferred sector

Energy fundamentals are strong and underpinned by geopolitical risk

Mixed macroeconomic environment negative for metals and to a lesser extent agricultural

commodities

Overweight Oil based energy: strong conviction overweight in Refined Products and Brent but

underweight WTI and Natural Gas

Underweight base metals sector: overweight Nickel, underweight Aluminium and Copper

Underweight soft commodities: full underweight in Cotton and Coffee

20 PT/12/01215

Commodities at Threadneedle – a strong fund management team

02

Commodities at Threadneedle

An integral component of the Threadneedle Investment Platform

Building commodities as the fourth asset class

A team drawn from the Commodities Markets

Leveraging the resources of the Fixed Income Group …

Making the most of the group’s trade-flow information

Participating if formulation of the Macro and Fundamental views

… and Threadneedle’s extensive strength in equities

Sharing investment ideas and broadening our perspective on commodity markets

Meeting with resources companies’ management teams provides unique insights into supply and

demand and technological developments across commodity markets

22 PT/12/01215

An experienced team with genuine commodities expertise

Source: Threadneedle as at 31 March 2012

David Donora

over 25 years’ experience

4 years at Threadneedle

Nicolas Robin

11 years’ experience

2 years at Threadneedle

Daniel Belchers

10 years’ experience

4 years at Threadneedle

23

Ullaas Misra

7 years’ experience

6 months at Threadneedle

Head of Commodities

Co-Lead Manager of Threadneedle Enhanced Commodities Fund and Columbia

Commodity Strategy Fund

Fund Manager

Co-Lead Manager of Threadneedle Enhanced Commodities Fund and Columbia

Commodity Strategy Fund

Fund Manager

Responsible for Materials

Analytics, bulk commodities, base and precious metals

Quantitative Specialist

Develop commodity analytics and models

PT/12/01215

Commodities at Threadneedle – the investment team

A wealth of expertise covering all aspects of commodity trading

More than 40 years of combined investment and trading experience

From physical and futures commodity trading to commodity related equities investment

Strong expertise in macro, volatility, forward curve and relative value trading

Products to capitalise on generating outperformance

A strong track record in both absolute returns and long only

Threadneedle Enhanced Commodity Fund launched June 2010

Columbia Commodity Strategy launched July 2011

24 PT/12/01215

Threadneedle Enhanced Commodities Strategy

03

Threadneedle Enhanced Commodities Fund Product highlights and features

Current target outperformance of 3–6%1 (benchmark: DJ-UBS TR Commodity Index)

tracking error up to 6%

Actively managed long-only fund investing in commodities

No leverage

No shorting

Fully invested

Daily liquidity

UCITS qualifying fund

Exposure created through Commodity Index swaps margined daily, (futures and physical not

permitted by regulator)

Diversified exposure across the commodity futures spectrum

Collateral invested in US T-Bills with maturities to 1 year

Hedged Share Classes: Euro, Sterling, Swiss Franc and Singapore Dollar

26

1 Gross of fees, per annum

PT/12/01215

Threadneedle Enhanced Commodities Fund Active management of Commodities

Fundamentally driven investment process which aims to generate outperformance

Active Weights

Driven by investment process

Active rebalancing of weights

Proactive curve positioning

Positioning of individual commodity weight along the term-structure

Timing of moving allocations along the curve

Seeking to capture curve volatility and uncorrelated alpha

27 PT/12/01215

Bottom up – the engine room of idea generation

28

Source: Threadneedle

Proprietary Database

Underlying markets

Sectors

Indices

Supply/Demand

Inventories

Logistics

Weather

Technological development

Investment flows

Speculative positioning

Hedger Activity

Algorithmic traders impact

Futures Exchange Rules

Options activity and

Volatility

Trade

Ideas

Market Structure

and Technicals Fundamentals

Seasonality

PT/12/01215

Portfolio construction: emphasis on relative value

Focus on relative value opportunities within the commodity universe

Intra sector

Across sectors

Position size to reflect both conviction and underlying market liquidity

Portfolio positions constructed with emphasis on:

Correlation

Volatility

Maximise performance outcome within the tracking error budget constraint

Deliver high risk adjusted relative returns with a portfolio volatility close benchmark

29 PT/12/01215

NY Harbour Gasoline v. Henry Hub Natural Gas

30

Relative

Value

Market

Structure and

Technicals Fundamentals

Seasonality

NG seasonality negative through

summer

RBOB seasonal most positive ahead of

US summer and winter changeover

Natural Gas storage constraint

Robust supply +16,800 wells in ‘11

Little infrastructure to export

NGL’s & wet gas increase margins

Gasoline tight with Middle East

supply disruption

Logistics impaired / affects refining

US refiners reducing capacity

NG producers actively hedge

affecting front of curve

US NG is a domestic market

RBOB inclined to backwardation

50

70

90

110

130

150

170

Oct 10 Dec 10 Feb 11 Apr 11 Jun 11 Aug 11 Oct 11 Dec 11

Re

ba

se

d =

10

0

Dow Jones – UBS Natural Gas Sub-Index

S&P GSCI Unleaded Gasoline Official Close Index

Strong seasonal

Lower 48 Inventory surplus (deficit) to other years

Source: EIA, Citi Investment Research and Analysis

PT/12/01215

Wheat – In an active strategy, it is possible to capture the volatility in the

protein spread and the difference in carry

31

Relative

Value

Market

Structure and

Technicals Fundamentals

Seasonality

We allocated to MW wheat Feb

2011 - fundamentals and structure

MW wheat has high protein content

Grown in different regions of NA

La Nina effect severely impacted

MW production in 2011

Logistics impaired shipment of

2010 crop

Minneapolis, Kansas and Chicago

wheat all have different physical

delivery conditions

Chicago wheat most affected by

VSR

MW more inclined to

backwardation/positive roll yield

Less speculative and index activity

MW in backwardation,

W in contango

50

60

70

80

90

100

Feb 11 Apr 11 Jun 11 Aug 11 Oct 11 Dec 11

Reb

ased

= 1

00

DJ-UBS Wheat Sub-Index

S&P GSCI Kansas Wheat Index

Citi Minneapolis F3 Custom Index

MW has stronger Spring and Summer

seasonal performance

Source: EIA, Citi Investment Research and Analysis

PT/12/01215

Source: Threadneedle / FactSet as at 31 March 2012. Gross performance based on official global close prices adjusted by the TER. Performance figures for periods greater than 1 year are

cumulative.

1 Since inception at 30 June 2010 (cumulative)

2 Index – Dow Jones-UBS Commodity Index

Past performance is not a guide to future performance

Threadneedle Enhanced Commodities Fund Performance to Date (in USD)

2010 Jul Aug Sep Oct Nov Dec 2010

Fund (gross) 7.3% -1.2% 6.4% 5.5% -0.1% 10.8% 31.5%

Index2 6.8% -2.5% 7.3% 5.0% -0.4% 10.7% 29.2%

Relative +0.5% +1.3% -0.9% +0.5% +0.3% +0.1% +1.8%

32

2011 Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec 2011 Since

inception1

Fund

(gross) 1.9% 3.6% 2.4% 4.8% -5.5% -3.3% 3.8% 1.7% -14.0% 6.5% -1.4% -1.6% -2.8% 27.9%

Index2 1.0% 1.3% 2.1% 3.5% -5.1% -5.0% 3.0% 1.0% -14.7% 6.6% -2.2% -3.7% -13.3% 12.0%

Relative +0.9% +2.2% +0.3% +1.3% -0.4% +1.8% +0.8% +0.7% +0.9% -0.1% +0.9% +2.3% +12.2% +14.2%

2012 Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Since

inception1

Fund

(gross) 4.6% 3.4% -1.8% 35.9%

Index2 2.5% 2.7% -4.1% 13.0%

Relative +2.1% +0.7% +2.4% +20.2%

PT/12/01215

Threadneedle Enhanced Commodities Fund Performance to Date (in USD)

Performance vs. index

33

2012 YTD Since inception1

(annualised)

Since inception1

(cumulative) Historical Volatility

Fund (gross) 6.2% 19.1% 35.9% 18.5%

Index2 0.9% 7.2% 13.0% 19.3%

Relative +5.3% +11.1% +20.2%

Source: Threadneedle / FactSet as at 31 March 2012. Gross performance based on official global close prices, Fund data is quoted on a bid to bid basis with gross income re-invested at bid.

Fund returns calculated Gross of TER (and Tax) for comparison with index

1 Since inception at 30 June 2010

2 Index – Dow Jones-UBS Commodity Index

3 Threadneedle / FactSet as at 31 March 2012. Based on monthly observations since inception

4 Backtesting using TECF’s daily realised relative performance vs DJUBSTR

Past performance is not a guide to future performance

100

105

110

115

120

125

130

135

140

145

150

Jun

10

Jul

10

Aug

10

Sep

10

Oct

10

Nov

10

Dec

10

Jan

11

Feb

11

Mar

11

Apr

11

May

11

Jun

11

Jul

11

Aug

11

Sep

11

Oct

11

Nov

11

Dec

11

Jan

12

Feb

12

Mar

12

Reb

ased

= 1

00

T-Lux Enhanced Commodities Fund DJ-UBS Commodity (TR) Index

Historical Tracking Error3: 3.1%

Correlation of alpha with index4: -0.06

PT/12/01215

Threadneedle Enhanced Commodities Strategy Product update

Strong inflows since inception – more than $600 million in AUM, highly diversified client base

US clone fund (futures based) launched at the end of July 2011 by Columbia AM

Long / short, market neutral product to launch in Q2

34 PT/12/01215

Risk control and monitoring

Multiple controls inside and outside the process ensure that risks are intended and appropriate

Within the process

Adherence to risk budgeting discipline

Daily review of exposures

Weekly review of all trades vs. targets and market developments

Robust external controls

Blend of proprietary and third-party analytics provide comprehensive view of portfolio risk (Threadneedle uses

Advanced Portfolio Technologies, Inc. (APT) as a risk model provider)

Ongoing portfolio monitoring and challenge of fund managers by dedicated (and independent) investment risk

team

Formal reviews by Head of Fixed Income and Head of Risk Management

35 PT/12/01215

Managing risk for investment return

Investment risk: daily reports provide insight

into portfolio exposures and risks

Positions, number of holdings, net and gross

exposures

Tracking error, value-at-risk, breakdowns by

commodity, sector and size

Scenario analysis/stress tests

Sensitivity analysis

Operational risk: Safeguards and analysis

Dedicated unit within risk management team

conducts on-going analysis of counterparty risk

IRIS, Threadneedle’s risk reporting system

For illustrative purposes only

36 PT/12/01215

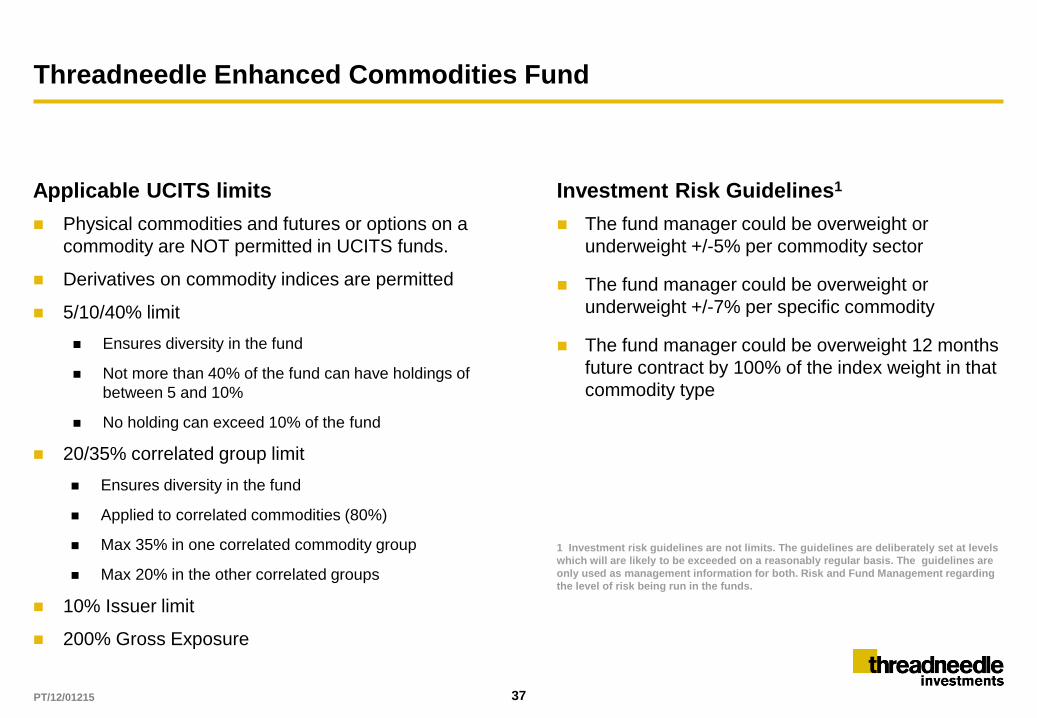

Threadneedle Enhanced Commodities Fund

37

Physical commodities and futures or options on a

commodity are NOT permitted in UCITS funds.

Derivatives on commodity indices are permitted

5/10/40% limit

Ensures diversity in the fund

Not more than 40% of the fund can have holdings of

between 5 and 10%

No holding can exceed 10% of the fund

20/35% correlated group limit

Ensures diversity in the fund

Applied to correlated commodities (80%)

Max 35% in one correlated commodity group

Max 20% in the other correlated groups

10% Issuer limit

200% Gross Exposure

Applicable UCITS limits

The fund manager could be overweight or

underweight +/-5% per commodity sector

The fund manager could be overweight or

underweight +/-7% per specific commodity

The fund manager could be overweight 12 months

future contract by 100% of the index weight in that

commodity type

Investment Risk Guidelines1

1 Investment risk guidelines are not limits. The guidelines are deliberately set at levels

which will are likely to be exceeded on a reasonably regular basis. The guidelines are

only used as management information for both. Risk and Fund Management regarding

the level of risk being run in the funds.

PT/12/01215

Appendix

AP

Source: Threadneedle as at 30 March 2012

Bridging the gap towards theoretical spot returns?

39

90

100

110

120

130

140

150

160

Jun

10

Jul

10

Aug

10

Sep

10

Oct

10

Nov

10

Dec

10

Jan

11

Feb

11

Mar

11

Apr

11

May

11

Jun

11

Jul

11

Aug

11

Sep

11

Oct

11

Nov

11

Dec

11

Jan

12

Feb

12

Mar

12

Reb

ased

= 1

00

DJUBSSP Index DJUBSTR Index DJUBSF3T Index T-Lux Enchanced Commodities Fund

Since inception, the strategy has tracked spot returns closer than a passive forward exposure

Trading the curve actively allows to seek forward exposure to minimise contango while taking advantage of the

curve volatility to generate outperformance

PT/12/01215

Source: Threadneedle as at 30 March 2012

Gold vs. gasoline – is gold really your inflation hedge?

40

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

SPGCHUTR Index SPGCGCTR Index

In spite of recent precious bull market, gold continues to underperform gasoline over the long-term

PT/12/01215

Backwardation, contango and roll yield

The slope of the futures / forward curve indicates the

state of available, deliverable inventory relative to

market demand

Commodities with abundant supply are typically in

contango – short-dated futures prices are lower than

longer-dated ones. Precious metals are usually in

contango because of the significant stocks available and

therefore the low metal lease rates

Commodities with tight supply are typically

backwardated – short-dated futures prices are higher than

longer-dated ones

Maintaining long positions in commodity futures

necessitates replacing maturing futures contracts with

longer dated futures. For a commodity market in contango

the investor will suffer an erosion of return by replacing

cheap futures with more expensive futures further along

the curve. Conversely, for a market in backwardation the

investor will benefit from improvement in the return

Contango – negative roll return

Commodity indices – roll return impacting performance

Backwardation – positive roll return

Roll return has historically eroded 50% of the returns of the spot returns for S&P GSCI and 55% of

the spot returns for DJ-UBSCI

Pri

ce

Maturity

Maturity

Pri

ce

Source: JP Morgan

41 PT/12/01215

Hypothetical cumulative roll return

Commodity indices – from ‘roll return’ to ‘roll drag’

-70%

-60%

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

1991 1993 1995 1997 1999 2001 2003 2005 2007 2009

S&P GSCI S&P GSCI Light Energy DJ-UBSCI

Excess return = price return + roll return

Price return – change in contracts’ prices

The roll return is the incidental cost or

benefit of tracking the price index and is

inherent to commodity investing

42 PT/12/01215

NICOLAS ROBIN

Fund Manager

Nicolas Robin joined Threadneedle in 2010 and is the Co- Lead Manager of the Threadneedle (Lux) Enhanced

Commodities Fund and Columbia Commodity Strategy Fund.

Nicolas has more than 10 years experience at managing both long only and relative value strategies focusing on

commodity markets and brings both hedge fund and commodity index trading experience to the team. He started his

career at Barep Asset Management (SG Group) in 2002, helping to set up a Commodity Arbitrage hedge fund desk.

He became Co-Manager in 2004 and Lead Manager in 2005, seeing assets rise to $200 million. The strategy was

focused on relative value strategies in commodities and aimed to take advantage of short-term dislocations in

commodity forward curves. In 2006 Nicolas joined JPMorgan Chase to run the bank’s commodity index trading

book. During his tenure, index assets under management trebled making JPMorgan Chase a leading index dealer.

In his time at JPMorgan Chase, Nicolas was responsible overhauling the bank’s commodity index trading platform

and driving the bank’s effort into fully customisable commodity index solutions. He participated in the creation of the

JPMorgan Commodity Curve Index (JPMCCI), the bank’s foray into second generation commodity indices launched

in 2007. He also contributed to the development of the bank’s commodity customised indices and algorithmic

strategies, looking at both momentum and curve based strategies. Alongside his commodity index trading

responsibilities, Nicolas also ran a proprietary trading book across commodities, using both relative value and

directional strategies with an emphasis on the energy complex.

Nicolas holds a BSc in Government and Economics and a MSc in Political Theory from the London School of

Economics.

Threadneedle start date: 2010

Industry start date: 2001

Biography

43 PT/12/01215

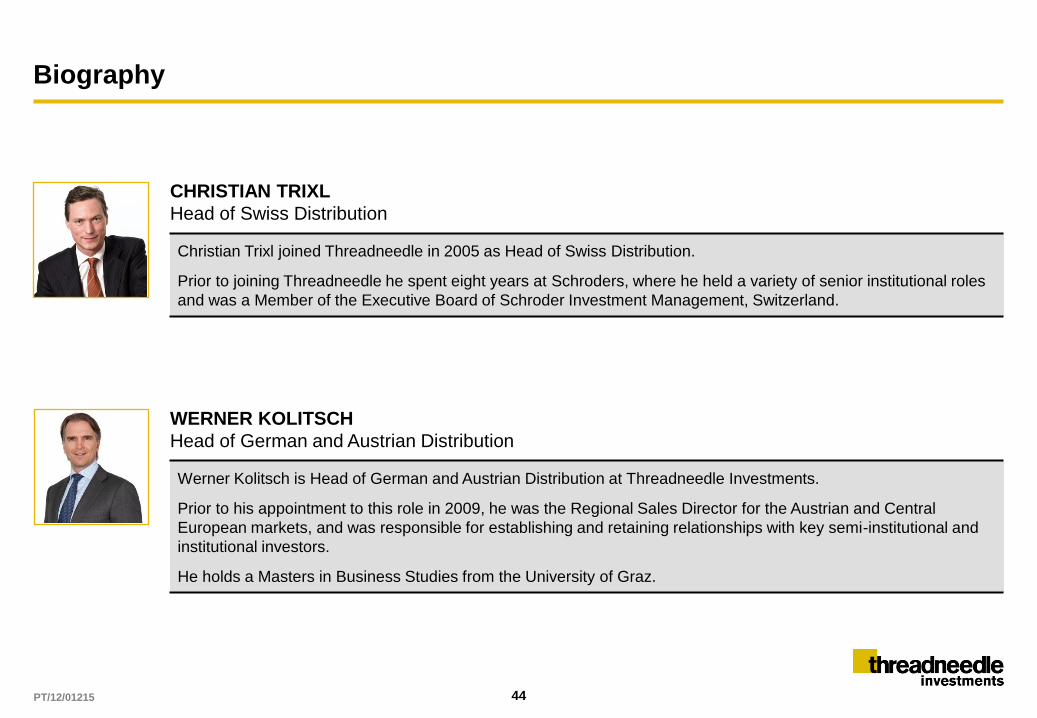

Biography

44

CHRISTIAN TRIXL

Head of Swiss Distribution

Christian Trixl joined Threadneedle in 2005 as Head of Swiss Distribution.

Prior to joining Threadneedle he spent eight years at Schroders, where he held a variety of senior institutional roles

and was a Member of the Executive Board of Schroder Investment Management, Switzerland.

WERNER KOLITSCH

Head of German and Austrian Distribution

Werner Kolitsch is Head of German and Austrian Distribution at Threadneedle Investments.

Prior to his appointment to this role in 2009, he was the Regional Sales Director for the Austrian and Central

European markets, and was responsible for establishing and retaining relationships with key semi-institutional and

institutional investors.

He holds a Masters in Business Studies from the University of Graz.

PT/12/01215

Important information

For Investment Professionals use only, not to be relied upon by private investors.

Past performance is not a guide to future returns. The value of investments and any income is not guaranteed and can go down as well as up and may be affected by exchange rate fluctuations.

This means that an investor may not get back the amount invested.

Where investments are made in assets that are denominated in foreign currency, changes in exchange rates may affect the value of the investments.

The fund invests in markets where economic and political risk can be significant and where governance and regulation may not be well developed. These factors can affect liquidity, settlement

and asset values. The fund invests in assets that are not always readily saleable without suffering a discount to fair value. The portfolio may have to lower the selling price, sell other investments

or forego another, more appealing investment opportunity. The fund may exhibit significant price volatility. The fund invests in commodity derivatives rather than physical commodities.

Therefore, changes in the prices of the underlying commodities will not be mirrored exactly in the fund price.

Threadneedle (Lux) is an investment company with variable capital (Société d’investissement à capital variable, or "SICAV") formed under the laws of the Grand Duchy of Luxembourg. The

SICAV issues, redeems and exchanges shares of different classes, which are listed on the Luxembourg Stock Exchange. The management company of the SICAV is Threadneedle

Management Luxembourg S.A, who is advised by Threadneedle Asset Management Ltd. and/or selected sub-advisors..

The SICAV is registered in Austria, France, Germany, Hong Kong, Italy, Luxembourg, The Netherlands, Portugal, Spain, Sweden, Switzerland, Taiwan and the UK; however, this is subject to

applicable jurisdictions and some sub-funds and/or share classes may not be available in all jurisdictions. Shares in the Funds may not be offered to the public in any other country and this

document must not be issued, circulated or distributed other than in circumstances which do not constitute an offer to the public and are in accordance with applicable local legislation.

Shares in the Funds may not be offered, sold or delivered directly or indirectly in the United States or to or for the account or benefit of any “U.S. Person”, as defined in Regulation S under the

1933 Act.

Subscriptions to a Fund may only be made on the basis of the current Prospectus and the Key Investor Information Document, as well as the latest annual or interim reports, which can be

obtained free of charge on request, and the applicable terms & conditions. Please refer to the ‘Risk Factors’ section of the Prospectus for all risks applicable to investing in any fund and

specifically this Fund. The above documents are available in English, French, German, Portuguese, Italian, Spanish and Dutch (no Dutch Prospectus) and free of charge on request by writing to

the SICAV’s registered office at 69, route D’Esch. L-1470 Luxembourg, Grand Duchy of Luxembourg.

The research and analysis included in this document has been produced by Threadneedle Investments for its own investment management activities, may have been acted upon prior to

publication and is made available here incidentally. Any opinions expressed are made as at the date of publication but are subject to change without notice. Information obtained from external

sources is believed to be reliable but its accuracy or completeness cannot be guaranteed.

This presentation and its contents are confidential and proprietary. The information provided in this presentation is for the sole use of those attending the presentation. It may not be reproduced

in any form or passed on to any third party without the express written permission of Threadneedle Investments. This presentation is the property of Threadneedle Investments and must be

returned upon request.

Threadneedle Management Luxembourg S.A. Registered with the Registre de Commerce et des Societes (Luxembourg), Registered No. B 110242, rue Mühlenweg, L-2155 Luxembourg, Grand

Duchy of Luxembourg.

In the UK issued by Threadneedle Asset Management Limited. Registered in England and Wales, Registered No. 573204, 60 St Mary Axe, London EC3A 8JQ, United Kingdom. Authorised and

regulated in the UK by the Financial Services Authority.

Threadneedle Investments is a brand name and both the Threadneedle Investments name and logo are trademarks or registered trademarks of the Threadneedle group of companies.

45 PT/12/01215