thoughts on the global economy · thoughts on the global economy april 2017 deloitte economics...

TRANSCRIPT

©2017 Global Equity Organization Page 1

Thoughts on the global economyApril 2017

Deloitte Economics & Markets Team Ian Stewart, Chief Economist, Deloitte LLP, London

©2017 Global Equity Organization Page 2

2

Leading indicators signal stronger growth ahead

Deloitte Economics & Markets Team

©2017 Global Equity Organization Page 3

3

Global growth nudges up in 2017, but not back to pre-crisis rates

Real GDP growth (% YoY)*

Pre-Crisis

Post-Crisis 2016 2017 2018

World 4.2 3.3 3.1 3.5 3.6

Advanced 2.8 1.0 1.7 2.0 2.0

Emerging 5.9 5.2 4.1 4.5 4.8

*Pre-crisis = 1998-2007, Post-crisis = 2008-15, Forecasts for 2017, 2018

Source: IMF World Economic Outlook, April 2017

Deloitte Economics & Markets Team

©2017 Global Equity Organization Page 4

4

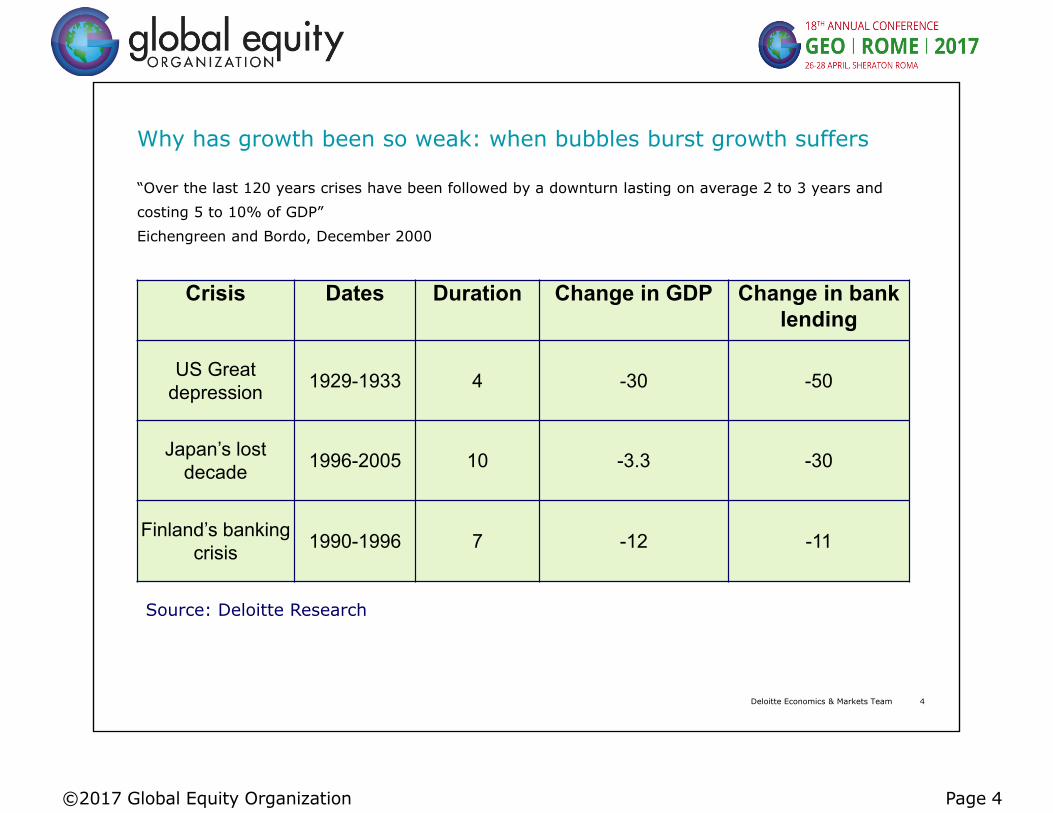

Why has growth been so weak: when bubbles burst growth suffers

“Over the last 120 years crises have been followed by a downturn lasting on average 2 to 3 years and costing 5 to 10% of GDP” Eichengreen and Bordo, December 2000

Crisis Dates Duration Change in GDP Change in bank lending

US Great depression 1929-1933 4 -30 -50

Japan’s lost decade 1996-2005 10 -3.3 -30

Finland’s banking crisis 1990-1996 7 -12 -11

Source: Deloitte Research

Deloitte Economics & Markets Team

©2017 Global Equity Organization Page 5

5Deloitte Economics & Markets Team

Growth forecasts: 6-10 years ahead

Growth potential of Western economies falling

©2017 Global Equity Organization Page 6

6

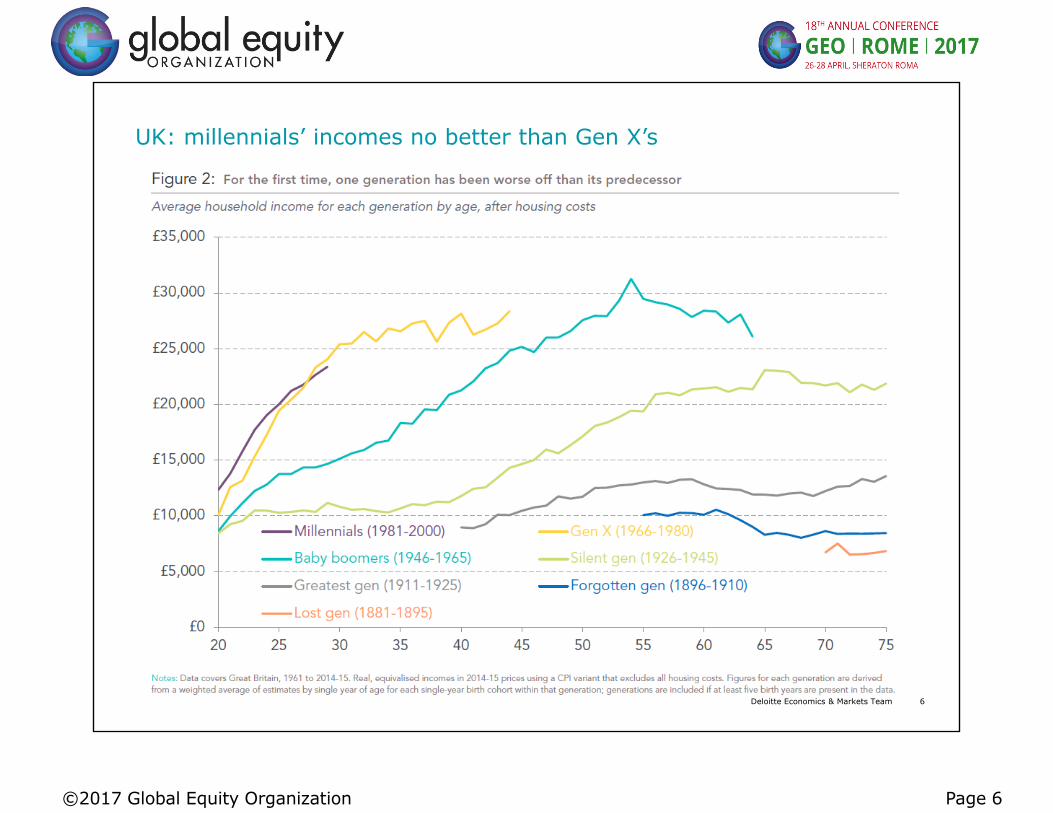

UK: millennials’ incomes no better than Gen X’s

Deloitte Economics & Markets Team

©2017 Global Equity Organization Page 7

7

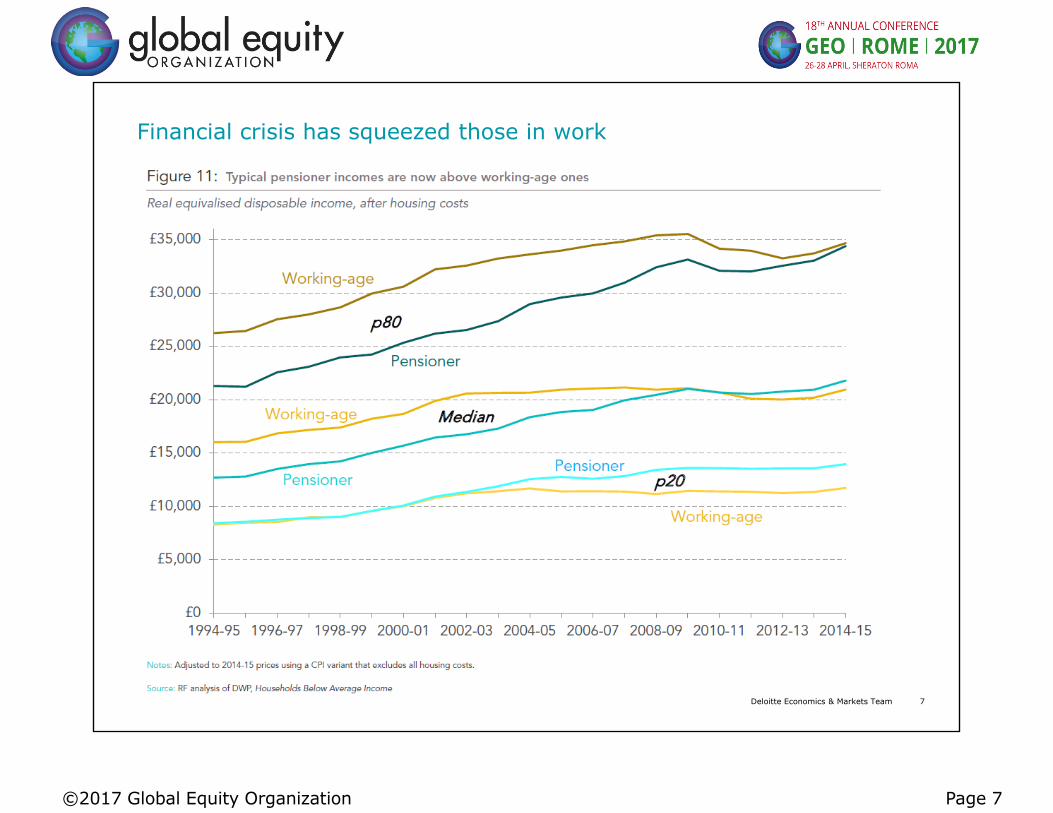

Financial crisis has squeezed those in work

Deloitte Economics & Markets Team

©2017 Global Equity Organization Page 8

8

Shocking increase in mortality among middle age Americans

Deloitte Economics & Markets Team

©2017 Global Equity Organization Page 9

9

Free trade needs re-booting

Deloitte Economics & Markets Team

©2017 Global Equity Organization Page 10

10

Ageing populations

Deloitte Economics & Markets Team

©2017 Global Equity Organization Page 11

11

Declining workforce participation = slower growth

Deloitte Economics & Markets Team

©2017 Global Equity Organization Page 12

12

Job insecurity

Deloitte Economics & Markets Team

©2017 Global Equity Organization Page 13

13

vs

Is innovation is no longer moving the dial on growth?

Deloitte Economics & Markets Team

©2017 Global Equity Organization Page 14

14

Creative destruction drives prosperity

Deloitte Economics & Markets Team

©2017 Global Equity Organization Page 15

15

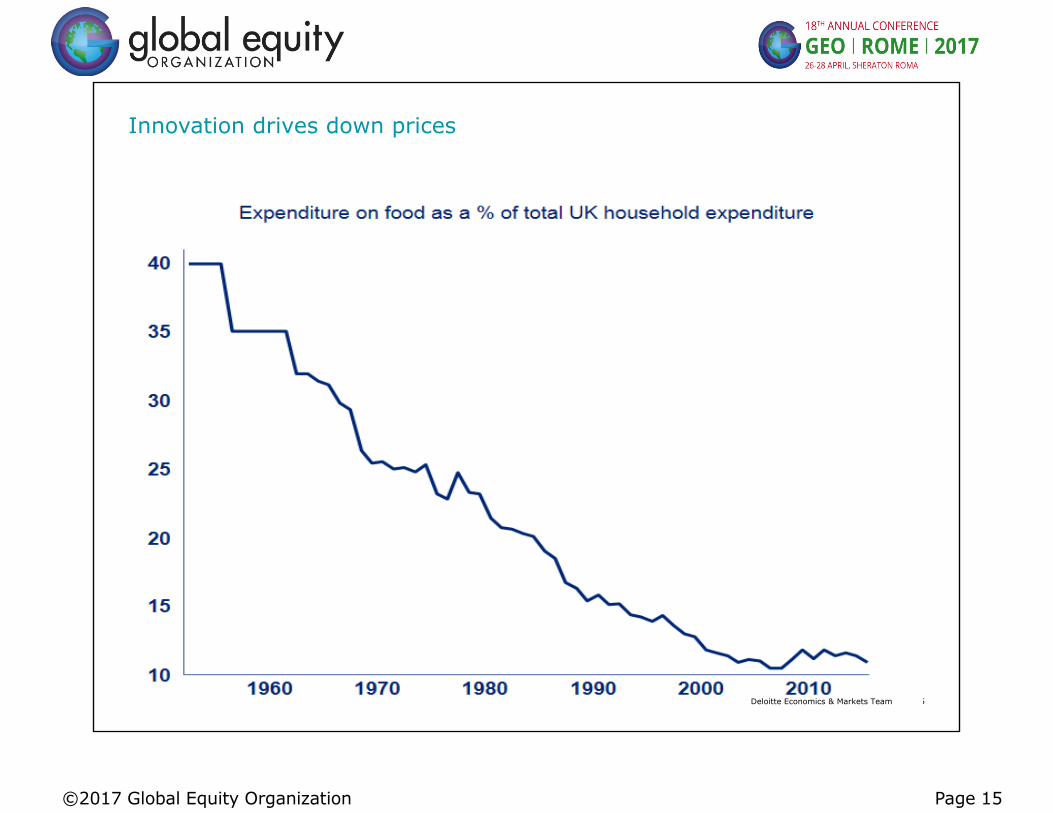

Innovation drives down prices

Deloitte Economics & Markets Team

©2017 Global Equity Organization Page 16

16

More computer power for your money

Deloitte Economics & Markets Team

©2017 Global Equity Organization Page 17

17

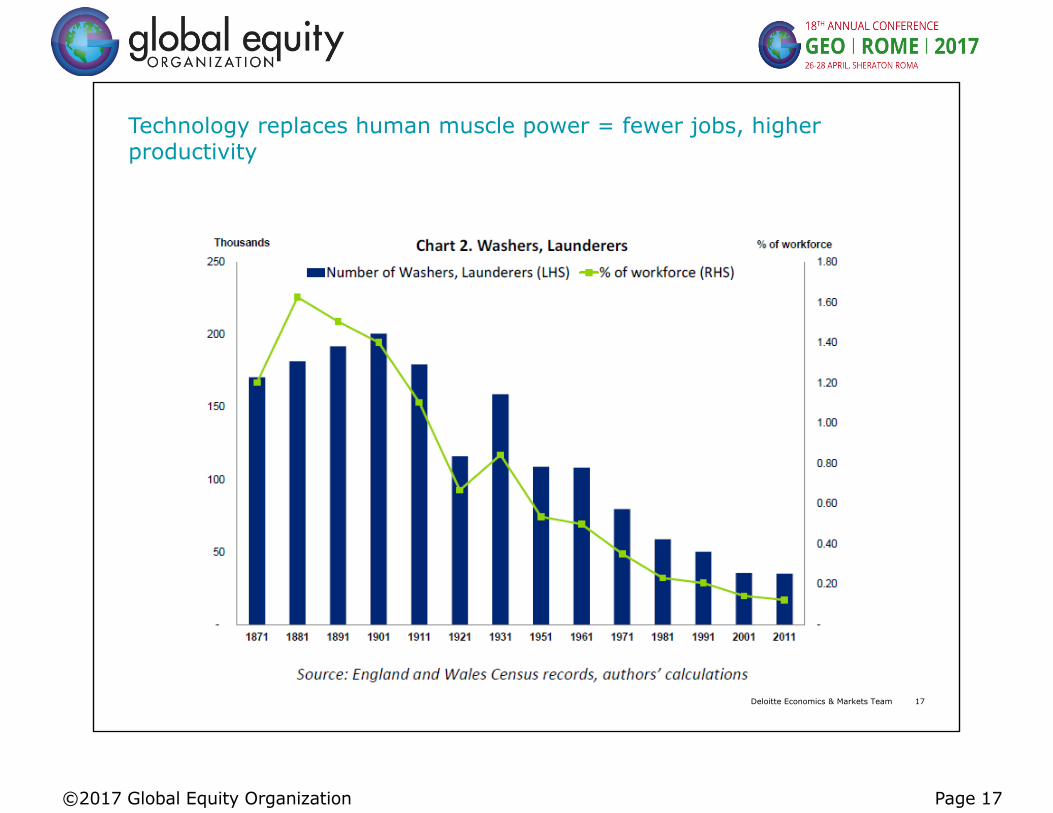

Technology replaces human muscle power = fewer jobs, higher productivity

Deloitte Economics & Markets Team

©2017 Global Equity Organization Page 18

18

Less spent on essentials, more spending elsewhere

Deloitte Economics & Markets Team

©2017 Global Equity Organization Page 19

19

Productivity raises living standards = more spending on “luxuries”

Deloitte Economics & Markets Team

©2017 Global Equity Organization Page 20

20

Jobs in knowledge-intensive sectors rise

Deloitte Economics & Markets Team

©2017 Global Equity Organization Page 21

21

Human desires unpredictable

Deloitte Economics & Markets Team

©2017 Global Equity Organization Page 22

22

Conventional measures of GDP struggle to capture these benefits

Deloitte Economics & Markets Team

©2017 Global Equity Organization Page 23

23

Is the world really getting worse?

Deloitte Economics & Markets TeamDeloitte Economics & Markets Team

©2017 Global Equity Organization Page 24

24

World population living in extreme povertyDefined as consumption/income < $1.90 per day adjusted for inflation

Deloitte Economics & Markets Team

©2017 Global Equity Organization Page 25

25

Long squeeze on labour’s share of GDP coming to an end?

Deloitte Economics & Markets Team

©2017 Global Equity Organization Page 26

26

GDP per head

Hours worked per year

Working long hours doesn’t make you productive or rich

Deloitte Economics & Markets Team

©2017 Global Equity Organization Page 27

27

• Global growth accelerating

• Upturn in emerging and developed markets

• Trend growth rates can be raised

• Increase workforce participation

• Re-boot global trade

• Invest and innovate

• Improve regulation, open markets, sharpen incentives

• Measure better

Conclusions

Deloitte Economics & Markets Team