this document is important and requires … made for the enlarged ordinary share capital to be...

TRANSCRIPT

THIS DOCUMENT IS IMPORTANT AND REQUIRES YOUR IMMEDIATE ATTENTION. If you are in any doubt about the

contents of this Document, you should consult your stockbroker, bank manager, solicitor, accountant or other

independent professional adviser who specialises in advising on the acquisition of shares and other securities and is

duly authorised under the Financial Services and Markets Act 2000 (as amended) (“FSMA”).

Application has been made for the entire issued and to be issued ordinary share capital of the Company to be admitted to trading

on AIM, a market operated by London Stock Exchange plc. It is expected that Admission will become effective, and dealings in

the Ordinary Shares will commence, on 21 December 2017. The Existing Ordinary Shares are not dealt on any other recognised

investment exchange and no application has been or is being made for the Ordinary Shares to be admitted to any such exchange.

AIM is a market designed primarily for emerging or smaller companies to which a higher investment risk tends to be

attached than to larger or more established companies. AIM securities are not admitted to the Official List of the UK

Listing Authority. A prospective investor should be aware of the risks of investing in such companies and should make

the decision to invest only after careful consideration and, if appropriate, consultation with an independent financial

adviser. Each AIM company is required, pursuant to the AIM Rules published by London Stock Exchange plc, to have a

nominated adviser. The nominated adviser is required to make a declaration to London Stock Exchange plc on

admission in the form set out in Schedule Two to the AIM Rules for Nominated Advisers. Neither the UK Listing Authority

nor London Stock Exchange plc has itself examined or approved the contents of this Document.

Prospective investors should read the whole text of this Document and should be aware that an investment in the Company is

speculative and involves a high degree of risk and prospective investors should carefully consider the section entitled “Risk

Factors” set out in Part II of this Document. All statements regarding the Company’s business, financial position and prospects

should be viewed in light of these risk factors.

This Document, which is drawn up as an AIM admission document in accordance with the AIM Rules, has been issued in

connection with the application for admission to trading on AIM of the entire issued and to be issued ordinary share capital of the

Company. This Document does not constitute an offer to the public requiring an approved prospectus under section 85 of FSMA

and, accordingly, this Document does not constitute, or contain, a prospectus, or any part of an offer, for the purposes of FSMA

and the Prospectus Rules and has not been pre-approved by the FCA pursuant to section 85 of FSMA. Copies of this Document

will be available free of charge to the public during normal business hours on any day (Saturdays, Sundays and public holidays

excepted) at the offices of Zeus Capital, 82 King Street, Manchester M2 4WQ and the registered office of the Company from the

date of this Document until one month from the date of Admission in accordance with the AIM Rules. A copy of this Document

will also be available from the Company’s website at www.sumogroupplc.com.

The Directors and the Proposed Director, whose names appear on page 8 of this Document, and the Company accept

responsibility, both individually and collectively, for the information contained in this Document. To the best of the knowledge and

belief of the Company, the Directors and the Proposed Director (having taken all reasonable care to ensure that such is the case),

the information contained in this Document is in accordance with the facts and does not omit anything likely to affect the import

of such information.

Sumo Group plc(a company incorporated in England and Wales under the Companies Act 2006 with company number 811071913)

Placing of 38,445,869 Ordinary Shares at 100 pence per Ordinary Share

Vendor Placing of 39,704,131 Ordinary Shares at 100 pence per Ordinary Share

and

Admission to trading on AIM

Nominated Adviser and Broker

Enlarged Ordinary Share Capital immediately following Admission

Number Issued and fully paid Amount £145,000,000 ordinary shares of £0.01 each 1,450,000

The Placing and the Vendor Placing are conditional, inter alia, on Admission taking place by 8.00 a.m. on 21 December 2017 (or

such later date as the Company and Zeus Capital may agree, being not later than 19 January 2018). The Placing Shares and

the Existing Ordinary Shares will, upon Admission, rank pari passu in all respects and will rank in full for all dividends and other

distributions declared paid or made in respect of the Ordinary Shares after Admission. It is emphasised that no application is

being made for the Enlarged Ordinary Share Capital to be admitted to the Official List or to any other recognised investment

exchange.

Zeus Capital, which is authorised and regulated in the United Kingdom by the FCA, is acting as nominated adviser and broker to

the Company in connection with the proposed Placing, Vendor Placing and Admission. Its responsibilities as the Company’s

nominated adviser under the AIM Rules for Nominated Advisers are owed solely to London Stock Exchange plc and are not owed

to the Company or to any Director or Proposed Director or to any other person in respect of his decision to acquire shares in the

Company in reliance on any part of this Document. Zeus Capital will not be offering advice and will not otherwise be responsible

to anyone other than the Company for providing the protections afforded to clients of Zeus Capital or for providing advice in

relation to the contents of this Document or any other matter.

Without limiting the statutory rights of any person to whom this Document is issued, no representation or warranty, express or

implied, is made by Zeus Capital as to the contents of this Document. Apart from the responsibilities and liabilities, if any, which

may be imposed on Zeus Capital by FSMA or the regulatory regime established thereunder, no liability whatsoever is accepted

by Zeus Capital for the accuracy of any information or opinions contained in this Document, for which the Directors and the

Proposed Director are solely responsible, or for the omission of any information from this Document for which it is not responsible.

In accordance with the AIM Rules for Nominated Advisers, Zeus Capital has confirmed to London Stock Exchange plc that it has

satisfied itself that the Directors and the Proposed Director have received advice and guidance as to the nature of their

responsibilities and obligations to ensure compliance by the Company with the AIM Rules and that, in its opinion and to the best

of its knowledge and belief, all relevant requirements of the AIM Rules have been complied with.

This Document does not constitute an offer to sell or an invitation to subscribe for, or solicitation of an offer to subscribe for or

buy, shares to any person in any jurisdiction to whom it is unlawful to make such offer, invitation or solicitation. In particular, this

Document must not be taken, transmitted, distributed or sent, directly or indirectly, in, or into, the United States of America,

Canada, Australia, Japan, the Republic of Ireland or the Republic of South Africa or transmitted, distributed or sent to, or by, any

national, resident or citizen of such countries. Accordingly, neither the Placing Shares nor the Vendor Placing Shares may, subject

to certain exceptions, be offered or sold, directly or indirectly, in, or into, or from, the United States of America, Canada, Australia,

Japan, the Republic of Ireland or the Republic of South Africa or in any other country, territory or possession where to do so may

contravene local securities laws or regulations. The Placing Shares and the Vendor Placing Shares have not been, and will not

be, registered under the United States Securities Act of 1933 (as amended) or under the securities legislation of any state of the

United States of America, any province or territory of Canada, Australia, Japan, the Republic of Ireland or the Republic of South

Africa and may not be offered or sold, directly or indirectly, within the United States of America, or Canada, Australia, Japan, the

Republic of Ireland or the Republic of South Africa or to or for the account or benefit of any national, resident or citizen of the

United States of America, Canada, Australia, Japan, the Republic of Ireland or the Republic of South Africa or to any US person

(within the definition of Regulation S made under the United States Securities Act 1933 (as amended)).

The distribution of this Document outside the UK may be restricted by law. No action has been taken by the Company or Zeus

Capital that would permit a public offer of shares in any jurisdiction outside the UK where action for that purpose is required.

Persons outside the UK who come into possession of this Document should inform themselves about the distribution of this

Document in their particular jurisdiction. Failure to comply with those restrictions may constitute a violation of the securities laws

of such jurisdiction.

2

IMPORTANT INFORMATION

In deciding whether to invest in Ordinary Shares in connection with the Placing and/or the VendorPlacing, prospective investors should rely only on the information contained in this Document. Noperson has in connection with the Placing and/or the Vendor Placing been authorised to give anyinformation or make any representations in connection with the Placing and/or the Vendor Placing otherthan as contained in this Document and, if given or made, such information or representations must notbe relied on as having been authorised by the Company, the Directors, the Proposed Director or ZeusCapital. Neither the delivery of this Document nor any subscription or purchase made in connection withthe Placing and/or the Vendor Placing, under any circumstances, create any implication that there hasbeen no change in the affairs of the Company since the date of this Document or that the informationin this Document herein is correct as at any time after its date.

Investment in the Company carries risk. There can be no assurance that the Company’s strategy willbe achieved and investment results may vary substantially over time. Investment in the Company is notintended to be a complete investment programme for any investor. The price of Ordinary Shares andany income from Ordinary Shares can go down as well as up and investors may not realise the valueof their initial investment. Prospective investors should carefully consider whether an investment inOrdinary Shares is suitable for them in light of their circumstances and financial resources and shouldbe able and willing to withstand the loss of their entire investment (see “Part II: Risk Factors” of thisDocument).

Potential investors contemplating an investment in Ordinary Shares should recognise that their marketvalue can fluctuate and may not always reflect their underlying value. Returns achieved are reliant uponthe performance of the Company. No assurance is given, express or implied, that investors will receiveback the amount of their investment in Ordinary Shares.

If you are in any doubt about the contents of this Document, you should consult your stockbroker oryour financial or other professional adviser.

Investment in the Company is suitable only for financially sophisticated individuals and institutionalinvestors who have taken appropriate professional advice, who understand and are capable ofassuming the risks of an investment in the Company and who have sufficient resources to bear anylosses which may result from such an investment.

Potential investors should not treat the contents of this Document or any subsequent communicationsfrom the Company as advice relating to legal, taxation, investment or any other matters. Potentialinvestors should inform themselves as to: (a) the legal requirements within their own countries for thesubscription, purchase, holding, transfer or other disposal of Ordinary Shares; (b) any foreign exchangerestrictions applicable to the subscription, purchase, holding, transfer or other disposal of OrdinaryShares that they might encounter; and (c) the income and other tax consequences that may apply intheir own countries as a result of the subscription, purchase, holding, transfer or other disposal ofOrdinary Shares. Potential investors must rely upon their own representatives, including their own legaladvisers and accountants, as to legal, tax, investment or any other related matters concerning theCompany and an investment in it.

This Document should be read in its entirety before making any investment in the Company orshares in it.

Forward looking statements

Certain statements contained in this Document are forward looking statements and are based oncurrent expectations, estimates and projections about the potential returns of the Company and theindustry and markets in which the Company operates, the Directors’ and the Proposed Director’s beliefsand assumptions made by the Directors and the Proposed Director. Words such as “expects”,“anticipates”, “may”, “should”, “could”, “will”, “intends”, “plans”, “believes”, “targets”, “seeks”,“estimates”, “aims”, “projects”, “pipeline”, “predicts”, “assumes”, “envisages” (or, in each case, theirnegative) and variations of such words and similar expressions are intended to identify such forwardlooking statements and expectations. These statements are not guarantees of future performance orthe ability to identify and consummate investments and involve certain risks, uncertainties, outcomes ofnegotiations and due diligence and assumptions that are difficult to predict, qualify or quantify.

3

Therefore, actual outcomes and results may differ materially from what is expressed in such forwardlooking statements or expectations. Among the factors that could cause actual results to differ materiallyare: the general economic climate, competition, interest rate levels, loss of key personnel, the result oflegal and commercial due diligence, the availability of financing on acceptable terms and changes inthe legal, taxation or regulatory environment.

Such forward looking statements are based on numerous assumptions regarding the Company’spresent and future business strategies and the environment in which the Company will operate in thefuture. These forward looking statements speak only as of the date of this Document. The Companyexpressly disclaims any obligation or undertaking to disseminate any updates or revisions to anyforward looking statements contained in this Document to reflect any change in the Company’sexpectations with regard to them, any new information or any change in events, conditions orcircumstances on which any such statements are based, unless required to do so by law or anyappropriate regulatory authority.

Presentation of financial information

The financial information contained in this Document, including that financial information presented ina number of tables in this Document, has been rounded to the nearest whole number or the nearestdecimal place. Therefore, the actual arithmetic total of the numbers in a column or row in a certain tablemay not conform exactly to the total figure given for that column or row. In addition, certain percentagespresented in the tables in this Document reflect calculations based upon the underlying information priorto rounding and, accordingly, may not conform exactly to the percentages that would be derived if therelevant calculations were based upon the rounded numbers.

No incorporation of website

The contents of the Company’s website (or any other website) do not form part of this Document andinvestors should not rely on them.

General notice

This Document has been drawn up in accordance with the AIM Rules and it does not comprise aprospectus for the purposes of the Prospectus Rules. It has been drawn up in accordance with therequirements of the Prospectus Directive only in so far as required by the AIM Rules and has not beendelivered to the Registrar of Companies in England and Wales for registration.

This Document has been prepared for the benefit only of a limited number of persons all of whomqualify as “qualified investors” for the purposes of the Prospectus Directive, to whom it has beenaddressed and delivered, and may not in any circumstances be used for any other purpose or beviewed as a document for the benefit of the public. The reproduction, distribution or transmission of thisDocument (either in whole or in part) without the prior written consent of the Company and Zeus Capitalis prohibited.

Governing law

Unless otherwise stated, statements made in this Document are based on the law and practice currentlyin force in England and Wales and are subject to changes in such law and practice.

4

CONTENTS

PageKEY STATISTICS 6

EXPECTED TIMETABLE OF PRINCIPAL EVENTS 7

DIRECTORS, SECRETARY AND ADVISERS 8

DEFINITIONS 9

GLOSSARY 13

EXECUTIVE SUMMARY 15

PART I INFORMATION ON THE GROUP 19

PART II RISK FACTORS 38

PART III HISTORICAL FINANCIAL INFORMATION 46

PART IV UNAUDITED PRO FORMA STATEMENT OF NET ASSETS 89

PART V ADDITIONAL INFORMATION 91

5

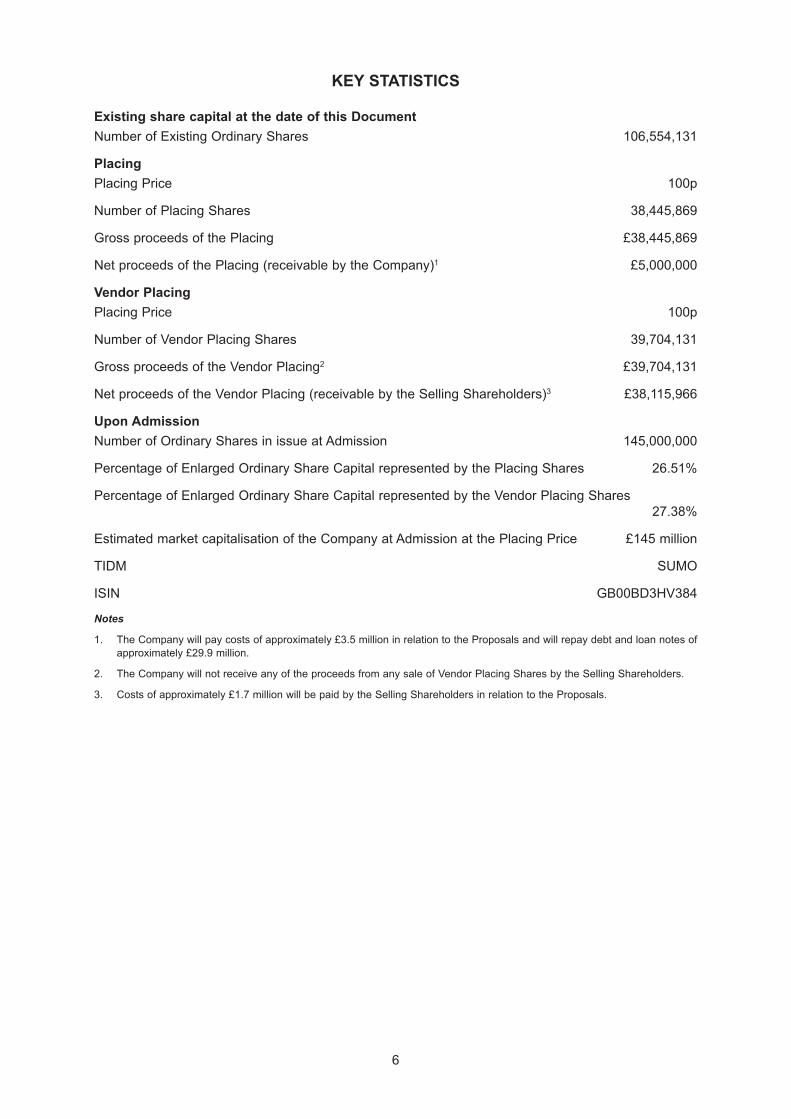

KEY STATISTICS

Existing share capital at the date of this Document

Number of Existing Ordinary Shares 106,554,131

Placing

Placing Price 100p

Number of Placing Shares 38,445,869

Gross proceeds of the Placing £38,445,869

Net proceeds of the Placing (receivable by the Company)1 £5,000,000

Vendor Placing

Placing Price 100p

Number of Vendor Placing Shares 39,704,131

Gross proceeds of the Vendor Placing2 £39,704,131

Net proceeds of the Vendor Placing (receivable by the Selling Shareholders)3 £38,115,966

Upon Admission

Number of Ordinary Shares in issue at Admission 145,000,000

Percentage of Enlarged Ordinary Share Capital represented by the Placing Shares 26.51%

Percentage of Enlarged Ordinary Share Capital represented by the Vendor Placing Shares27.38%

Estimated market capitalisation of the Company at Admission at the Placing Price £145 million

TIDM SUMO

ISIN GB00BD3HV384

Notes

1. The Company will pay costs of approximately £3.5 million in relation to the Proposals and will repay debt and loan notes of

approximately £29.9 million.

2. The Company will not receive any of the proceeds from any sale of Vendor Placing Shares by the Selling Shareholders.

3. Costs of approximately £1.7 million will be paid by the Selling Shareholders in relation to the Proposals.

6

EXPECTED TIMETABLE OF PRINCIPAL EVENTS

2017

Publication of this Document 15 December

Admission and commencement of dealings in the Enlarged Ordinary Share Capital on AIM 21 December

CREST accounts credited (where applicable) 21 December

Dispatch of definitive share certificates (where applicable) by 5 January 2018

Notes

1. References to time in this Document are to London (GMT) time unless otherwise stated.

2. If any of the above times or dates should change, the revised times and/or dates will be notified by an announcement on a

RIS.

7

DIRECTORS, SECRETARY AND ADVISERS

Directors: Kenneth Robert Beaty (Non-Executive Chairman)Carl Cavers (Chief Executive Officer)David Charles Wilton (Chief Financial Officer)Ian Livingstone CBE (Independent Non-Executive Director)

Proposed Director: Michael Sherwin (Independent Non-Executive Director)All of whose business addresses are at:

32 Jessops RiversideBrightside LaneSheffieldS9 2RX

Registered office: 32 Jessops RiversideBrightside LaneSheffieldS9 2RX

Company secretary: Steven Webb

Company website: www.sumogroupplc.com

Nominated adviser and broker: Zeus Capital Limited

82 King Street and 10 Old Burlington StreetManchester LondonM2 4WQ W1S 3AG

Reporting accountants: Grant Thornton UK LLP

No. 1 Whitehall RiversideWhitehall RoadLeedsLS1 4BN

Auditors: Grant Thornton UK LLP

2 Broadfield CourtSheffieldSouth YorkshireS8 0XF

Solicitors to the Company: Addleshaw Goddard LLP

One St. Peter’s SquareManchesterM2 3DE

Solicitors to Zeus Capital: Eversheds Sutherland (International) LLP

70 Great Bridgewater StreetManchesterM1 5ES

Financial public relations: Belvedere Communications Limited

Enterprise House1 – 2 HatfieldsLondonSE1 9PG

Company registrars: Link Market Services Limited

The Registry34 Beckenham RoadBeckenhamKentBR3 4TU

Principal bankers: Clydesdale Bank plc

94 – 96 BriggateLeedsLS1 6NP

8

DEFINITIONS

The following definitions apply throughout this Document, unless the context requires otherwise orunless defined in Part III of this Document, for the purposes of that part only:

“Act” the Companies Act 2006 (as amended)

“Admission” admission of the issued and to be issued Ordinary Shares totrading on AIM becoming effective in accordance with Rule 6 ofthe AIM Rules

this document dated 15 December 2017

“AIM” the market of that name operated by the London StockExchange

“AIM Rules” the AIM Rules for Companies (including, without limitation, anyguidance notes or statements of practice) published by theLondon Stock Exchange from time to time, which govern therules and responsibilities of companies whose shares areadmitted to trading on AIM

the rules setting out the eligibility, ongoing obligations andcertain disciplinary matters in relation to nominated advisers, aspublished by the London Stock Exchange from time to time

“Articles” the articles of association of the Company, as at the date ofAdmission, a summary of which is set out in paragraph 5 ofPart V of this Document

“Atomhawk” Atomhawk Design Limited, a company incorporated in Englandand Wales with registered number 6968171 and registered officeat Northern Design Centre Abbott’s Hill, Baltic Business Quarter,Gateshead, Tyne and Wear, NE8 3DF

“Audit Committee” the audit committee of the Board, as constituted from time totime

“Board” the board of directors of the Company from time to time, or aduly constituted committee thereof

“certificated” or “certificated form” recorded on the relevant register of the share or securityconcerned as being held in certificated form in physical paper(that is not in CREST)

“Company” or “Sumo Group plc” Sumo Group plc, a public limited company incorporated inEngland and Wales with registered number 11071913 andregistered office at 32 Jessops Riverside, Brightside Lane,Sheffield, England, S9 2RX

“CREST” the computer based system and procedures which enable title tosecurities to be evidenced and transferred without a writteninstrument, administered by Euroclear UK & Ireland inaccordance with the CREST Regulations

“CREST Regulations” the Uncertificated Securities Regulations 2001 (SI 2001/3755),including (i) any enactment or subordinate legislation whichamends those regulations and (ii) any applicable rules madeunder those regulations or such enactment or subordinatelegislation for the time being in force

“Dealing Day” a day on which the London Stock Exchange is open for thetransaction of business

“Admission Document” or“Document”

“AIM Rules for NominatedAdvisers”

9

“Directors” the directors of the Company as at the date of this Document,whose details are set out on page 8 of this Document and“Director” means any one of them

“EBITDA” Operating Profit before finance costs, taxation, depreciation andamortisation

“Enlarged Ordinary Share Capital” the Ordinary Shares in issue immediately following the Placingand Admission, comprising the Existing Ordinary Shares and thePlacing Shares

“EU” the European Union

“Euroclear UK & Ireland” Euroclear UK & Ireland Limited, a company incorporated underthe laws of England and Wales with registered number 2878738and the operator of CREST

“Existing Ordinary Shares” the 106,554,131 Ordinary Shares in issue as at the date of thisDocument (which include the Vendor Placing Shares)

“FCA” the Financial Conduct Authority

“FSMA” the Financial Services and Markets Act 2000 (as amended)

“Gross Profit” a Company’s total revenue minus costs of goods sold

“Group” or “Sumo Digital” the Company and its subsidiary undertakings and “GroupCompany” means any one of them

“HMRC” HM Revenue and Customs

“ITEPA” Income Tax (Earnings and Pensions) Act 2003

“London Stock Exchange” London Stock Exchange plc

“LTIP” The Sumo Group plc Long Term Incentive Plan

“Nomination Committee” the nomination committee of the Board, as constituted from timeto time

“NorthEdge Capital LLP” NorthEdge Capital LLP, a limited liability partnership withregistered number OC345118 and with registered office at6th Floor Vantage Point, Hardman Street Spinningfields,Manchester, M3 3HF

“Official List” the official list maintained by the UK Listing Authority

“Operating Profit” total revenue minus costs of goods sold, operating expenses,depreciation and amortisation

“Ordinary Shares” ordinary shares of £0.01 each in the capital of the Company

“Panel” the Panel on Takeovers and Mergers

“Perwyn LLP” Perwyn LLP, a limited liability partnership with registered numberOC383773 and with registered office at 8 Hanover Square,London, England, W1S 1HQ

“Placees” the subscribers for Placing Shares and purchasers of VendorPlacing Shares pursuant to the Placing and Vendor Placing,respectively

“Placing” the conditional placing of the Placing Shares by Zeus Capital asagent for the Company, pursuant to the Placing Agreement

“Placing Agreement” the placing agreement dated 15 December 2017 between theCompany, the Directors, the Proposed Director, Zeus Capitaland the Selling Shareholders relating to the Placing and theVendor Placing

10

“Placing Price” 100 pence per Placing Share and Vendor Placing Share

“Placing Shares” the 38,445,869 new Ordinary Shares to be issued and allottedpursuant to the Placing, such allotment being conditional uponAdmission

“Pre-Admission Reorganisation” the corporate reorganisation of the Group being undertaken inconnection with Admission and the Placing, the material detailsof which are summarised at paragraph 3 of Part V of thisDocument

“Proposals” the Placing, the Vendor Placing and Admission

“Proposed Director” Michael Sherwin, whose details are set out on page 8 of thisDocument

“Prospectus Directive” the EU Prospectus Directive 2003/71/EC, as amended

“Prospectus Rules” the Prospectus Rules made by the FCA pursuant tosections 73(A)(1) and (4) of FSMA

“QCA Corporate Governance Code” the Corporate Governance Code for Small and Mid-Size QuotedCompanies 2013 published by the Quoted Companies Alliance

“Registrars” the Company’s registrars, being Link Asset Services

“Relationship Agreement” the relationship agreement, dated 15 December 2017, between(1) Perwyn LLP, (2) Sumo Group plc and (3) Zeus CapitalLimited, details of which are set out in paragraph 12.3 of Part Vof this Document

“Remuneration Committee” the remuneration committee of the Board, as constituted fromtime to time

“Republic of Ireland” the island of Ireland excluding Northern Ireland

“RIS” a Regulatory Information Service (as defined in the AIM Rules)

“Selling Shareholders” those persons set out in paragraph 12.1 of Part V of thisDocument

“Share Plans” the LTIP and the SIP

“Shareholder(s)” holder(s) of Ordinary Shares

“SIP” The Sumo Group plc Share Incentive Plan

“Sumo Digital” Sumo Digital Ltd., a company incorporated in England andWales with registered number 4703224 and registered office at32 Jessops Riverside, Brightside Lane, Sheffield, S9 2RX

“Takeover Code” the City Code on Takeovers and Mergers

“UK” or “United Kingdom” the United Kingdom of Great Britain and Northern Ireland

“UK Listing Authority” the FCA, acting in its capacity as the competent authority for thepurposes of FSMA

recorded on the relevant register of the share or security asbeing held in uncertificated form in CREST and title to which, byvirtue of the CREST Regulations, may be transferred by meansof CREST

“US” the United States of America and all of its territories andpossessions

“VAT” value added tax

“Vendor Placing” the conditional placing of the Vendor Placing Shares by ZeusCapital as agents for the Selling Shareholders, pursuant to thePlacing Agreement

“uncertificated” or “uncertificatedform”

11

“Vendor Placing Shares” the 39,704,131 Existing Ordinary Shares to be sold pursuant tothe Vendor Placing, such sale being conditional upon Admission

“VGTR” video games tax relief, which allows UK game developers toclaim back approximately 20% of their qualifying productioncosts. To be eligible for VGTR, the game must pass the BritishFilm Institute (BFI) cultural test and the developer must beresponsible for the majority of the planning, designing,developing and testing of the game

“Zeus Capital” Zeus Capital Limited, a company incorporated in England andWales with registered number 4417845 and registered office at82 King Street, Manchester, M2 4WQ

“£” or “Sterling” British pounds sterling

“$” or “US Dollars” US dollars

12

GLOSSARY

AAA-rated AAA-rated game is an informal classification given to videogames with typical investment of greater than $10 million indevelopment and production. It is the video game equivalent ofa ‘blockbuster’ movie

CAGR Compound annual growth rate, the mean annual growth rate ofan investment or metric over a specified period of time longerthan one year

Co-development Game development work undertaken by a third party contractorwhere the creative responsibility is shared between publisherand developer

eShops Charts Nintendo’s digital distribution platform

Expansion packs An expansion pack, expansion set, supplement, or simplyexpansion is an addition to an existing role-playing game,tabletop game or video game

Franchise A collection of related games in which several derivative workshave been produced following an original

FY Financial year, the period that a company uses for preparingfinancial statements

Game and/or video game A game played by electronically manipulating images producedby a computer program on a monitor or other display

Game Jam An internal Group event where ideas for own-IP games arediscussed, developed and presented

Game patches Patches to fix game compatibility problems after their initialrelease or applied to change game rules or algorithms

Gamer and/or video gamer An end-user or consumer of video games

Games as a service A business model whereby games receive significant developerpost-release support, including multiplayer hosting, communitymanagement, post-release patching, game fixes, downloadablecontent and expansions

Indie game A video game that is created without the financial support of apublisher

IP Intellectual property

Micro-transactions Micro-transaction is a business model where users canpurchase virtual goods via micro-payments. Micro-transactionsare often used in free-to-play games to provide a revenue sourcefor the developers

PC personal computer

Tent pole title A publisher or developer’s highest profile release, typicallydeveloped in-house with a very high budget

TIGA The Independent Game Developers’ Association, a network forgames developers and digital publishers and a trade associationrepresenting the video games industry

13

Turnkey End to end game development work undertaken by a third-partycontractor where the creative responsibility lies with thecontractor

Vertical Slice A pre-defined part of a game, produced to a high level of qualitythat can be played and demonstrates elements of gameplay andvisuals as targeted in the finished game

Work for hire Game development work undertaken by a third party contractorwhere the contractor is given limited or no creative discretion

14

EXECUTIVE SUMMARY

The following information is derived from, and should be read in conjunction with, the whole of

this Document including, in particular, the section headed “Risk Factors” in Part II of this

Document. Potential investors should read the whole of this Document and not rely on this

Executive Summary section.

INTRODUCTION

Sumo Digital is one of the UK’s largest independent developers of AAA-rated video games providingboth turnkey and co-development solutions to an international blue-chip client base. Its full-servicedevelopment solution, includes initial concept and pre-production, production and development, andpost-release support.

Sumo Digital was established in 2003 and now has studios in Sheffield, Nottingham, Newcastle, Pune(India) and Vancouver (Canada). The Company has developed deep relationships with some of theworld’s largest computer games publishers and platform manufacturers. It has relationships withinternational developers and publishers, including Microsoft, Sony, Sega, CCP Games andIO Interactive. Since 2003, Sumo Digital has provided co-development and turnkey developmentservices on more than 40 released titles, including contributions to franchises such as Outrun 2, Forza,Hitman, LittleBigPlanet, and Sega & Sonic All-Stars.

The video games industry is the largest entertainment market in the world valued in excess ofUS$113bn and growing at 8.4% per annum. The growth of digital distribution and backwardscompatibility of new hardware releases has resulted in a smoothing of console cycles seen historicallyand an increase in the demand for high quality creative output from publishers to satisfy consumerrequirements. The Directors and the Proposed Director believe that the Company is well positioned tobenefit from this growth in demand.

The Directors and the Proposed Director believe that Admission will provide a permanent source ofcapital to deleverage the balance sheet, raise the profile of the Company, provide the ability toincentivise key employees and allow the Company to execute its strategy. Admission will also providea partial exit for funds advised by Perwyn LLP, the Company’s private equity investor. On Admission,funds advised by Perwyn LLP will hold approximately 28.39 per cent of the Company’s EnlargedOrdinary Share Capital.

INFORMATION ON SUMO DIGITAL

Sumo Digital is a co-development partner to some of the world’s leading publishers, offering turnkeygame development solutions. Sumo Digital can develop games across all console platforms, PC,handheld and mobile devices.

The Directors and the Proposed Director believe the Group’s competitive advantage lies in its scale,management systems, technology and creative solutions, which enable it to offer flexible co-development and full end-to-end solutions for publishers and other developers.

Sumo Digital operates a lower risk contracting model than the majority of other developers andpublishers who are more exposed to the commercial success or failure of the game. The Directors andthe Proposed Director believe these long-term contracts de-risk the Group’s model by securing thatpayment is made in accordance with the achievement of a number of key milestones, during andfollowing release of the game, which are agreed prior to the start of the project, rather than oncompletion and/or sales performance.

The Group principally works across the following phases of the development of a computer game:

Phase 1 – Initial Concept

Prototyping key ideas and concepts with the Company’s publishing clients. At this stage, early conceptart is created to explore the visual direction of the game as well as gameplay ideas being roughlyblocked out in a basic form. The process seeks to align publishing, marketing and development with thepublisher’s vision for the game at this stage.

15

Phase 2 – Pre-production

Once through the concept phase, the team will move into pre-production. The team will grow at thisstage to accommodate a wider remit. The key deliverable at this stage is often identified as a “verticalslice” of the game. This is a pre-defined part of the game, produced to a high level of quality that canbe played and demonstrates elements of gameplay and visuals as targeted in the finished game.

Phase 3 – Production

The peak of the game development process and testing with key milestones agreed with customers.Typically, production of a full game can take between 12 and 24 months and can involve large teamsof over 100 people, involved in many different disciplines, such as programming, art, design,production, depending on the size and complexity of the game.

The production phase builds on the work done in pre-production and expands the feature set createdfor the “vertical slice” into a full game experience. Mechanics, game play, level design, art andanimation, visual effects and audio are all undertaken in the production phase.

Phase 4 – Closedown

In the closedown phase, quality assurance work, user research feedback and major bug elimination arethe goals.

Phase 5 – Games as a service

Once a game has been launched, Sumo Digital can provide further support including development ofdownloadable content, development of new game features, community management, real time datamining and feedback and server operations.

Sumo Digital’s core technology

The Sumo Digital research and development team serves a number of key roles:

• Development of future game engine and tools technology. The key responsibility of the researchand development team is to enhance and maintain the Company’s existing in-house coretechnology to keep it up to date with the current state of the art along with adding support for newplatforms as they come to market.

• Development of tools to enhance the efficiency of project build processes. Systems have beendeveloped and are supported by the research and development team to improve build times andstreamline integration of external game engines.

• Provide expertise and technical support to existing game teams. The members of the R&D teamcan be deployed to give technical help to existing projects to aid optimisation, development ofnew features or simply advise on best practice with code with which they are more familiar.

As a result, Sumo Digital has an ever-growing library of tools and technology that assists to driveefficiency and helps underpin margins in the business.

Own intellectual property

In 2017, Sumo Digital successfully released its first own intellectual property title, Snake Pass. The ideafor the game was originated and developed internally using a gated process which regularly assessesthe potential of a game developed by a dedicated team at relatively low cost, making this a lower riskroute to own intellectual property and exploit these games for improved commercial terms. Snake Passhas proved successful with over 170,000 units sold since March 2017, generating a return oninvestment in excess of 83%. Snake Pass was released for PC, Xbox One, PlayStation 4 and NintendoSwitch and it reached the number one position in the eShops charts in the UK.

Metacritic scoring

Metacritic is an independent aggregator of video game reviews, which provides the ability to compareand rank the critical performance of games relative to other releases. Video games developed and co-

16

developed by Sumo Digital have achieved consistently high Metacritic scores with an average of 72.The Directors and the Proposed Director believe that this ranks Sumo Digital highly amongst its peers.

STRATEGY

Sumo Digital’s core strategy is to continue to grow organically as one of the leading co-developers ofAA/AAA-rated gaming titles in the world, primarily using its contracted development fee model tominimise risk, and taking advantage of the forecast growth in the global video games market.

Key areas of strategic focus are as follows:

Deliver and expand

• Well placed to deliver significant growth through developing new franchise titles as the demandfor creative content continues to grow;

• Develop downloadable content for existing titles that can be used to extend further the revenuegenerating capability of games for publishers; and

• Continue to recruit, retain, incentivise and develop the Group’s talent pool in order to increasethe Group’s core development capacity and capability.

New strategic partners

• Continue to win new customers and extend its publisher portfolio;

• Collaboration with other developers and publishers, extending existing co-developmentrelationships; and

• Potential to open or acquire new studios to enable recruitment from further pools of talent andgain exposure to new publishers and game genres.

Own intellectual property

• Following the successful launch of Snake Pass, which has generated a return on investment inexcess of 83% since launch, the Directors and the Proposed Director intend to continue tooperate Group-wide Game Jams and selectively develop “Indie Games”.

Acquisition of complementary revenue streams

• Consider earnings enhancing acquisitions of premium video game service providers andcomplementary video game developers.

PLACING AND VENDOR PLACING

The Placing

The Company is proposing to raise a total of approximately £38.45 million by way of a conditionalplacing by the Company of the Placing Shares, at the Placing Price, with new investors. The PlacingShares will represent approximately 26.51 per cent. of the Enlarged Ordinary Share Capital atAdmission.

The Vendor Placing

The Selling Shareholders have indicated a desire to realise a proportion of their investment in theCompany. The Vendor Placing will allow the Selling Shareholders to achieve this. Under the VendorPlacing, the Selling Shareholders have agreed to sell 39,704,131 Vendor Placing Shares at the PlacingPrice and these shall be conditionally placed with investors by Zeus Capital at the Placing Price. TheVendor Placing Shares will represent approximately 27.38 per cent. of the Enlarged Ordinary ShareCapital at Admission.

17

DIRECTORS

Kenneth Beaty (Non-Executive Chairman, aged 48)

Ken works as a Chairman and Non-Executive Director, following a 20-year private equity career. He hasextensive experience working with high growth private equity backed and entrepreneurial businesses.Ken has been a non-executive director of the Group since December 2014 and acts as a consultant toPerwyn on matters outside the Company.

Carl Cavers (Chief Executive Officer, aged 50)

Carl joined Gremlin Interactive in 1995. Following its acquisition by Infograms in 1999, he wasappointed to European Development Director with responsibility for all internal development studios inthe UK, France and Australia. Carl co-founded Sumo Digital in 2003, and led the management buy-outwith NorthEdge Capital in 2014. In 2015, he received the TIGA Most Outstanding Individual Award(TIGA is a trade association representing the video games industry). Carl holds an honorary doctoratefrom Sheffield Hallam University.

David Wilton (Chief Financial Officer, aged 55)

David was appointed Chief Financial Officer in September 2017. He is a “Big Four” qualified charteredaccountant with approximately 30 years’ post-qualification experience as Finance Director, Non-Executive Director and consultant, having previously worked in mergers and acquisitions withRothschild. David has experience of plc and private equity roles, including as Group Finance Directorof WYG plc, and as Non- Executive Director and Chair of the Audit Committee of Sweett Group plc.

Ian Livingstone CBE (Independent Non-Executive Director, aged 67)

Ian is one of the founding fathers of the UK gaming industry, with over 40 years’ of games industryexperience. He is former Executive Chairman of Eidos plc, where he was behind major franchises suchas Tomb Raider. Ian also co-founded the games company Games Workshop in 1975, responsible forthe successful Warhammer franchise, and co-created the Fighting Fantasy gamebook series in 1982.In 2002, Ian won the BAFTA Interactive Special Award for outstanding contribution to the video gamesindustry, and was appointed CBE in 2013. Ian has been a non-executive director of the Group sinceSeptember 2015.

Michael Sherwin (Independent Non-Executive Director, aged 58)

Michael is currently Chief Financial Officer of Vertu Motors plc and has extensive retail, transactionaland public market experience. From 1999 to 2008, Michael was Group Finance Director of GamesWorkshop PLC, a FTSE listed consumer goods company. Michael is a qualified Chartered Accountanthaving trained with Price Waterhouse, where he held positions in the UK, Paris and Sydney. He wasalso Non-Executive Director of Plusnet plc, an AIM listed internet business, from 2004-2007. Michaelwill be appointed to the Board conditional on Admission.

RISK FACTORS

Your attention is drawn to the risk factors set out in Part II of this Document. Your attention is also drawnto the section entitled “Important Information” of this Document and to the section entitled “Forwardlooking statements” in that section. In addition to all other information set out in this Document, potentialinvestors should carefully consider the risks described in those sections before deciding whether toinvest in the Company.

18

PART I

INFORMATION ON THE GROUP

SUMO GROUP PLC

1. INTRODUCTION

Sumo Digital is one of the UK’s largest independent developers of AAA-rated video games, providingboth turnkey and co-development solutions to an international blue chip client base. Its full-servicedevelopment solution includes initial concept and pre-production, production and development, andpost-release support.

Sumo Digital was established in 2003 and now has studios in Sheffield, Nottingham, Newcastle, Pune(India) and Vancouver (Canada). Sumo Digital has developed deep relationships with some of theworld’s largest computer games publishers and platform manufacturers. It has relationships withinternational developers and publishers, including Microsoft, Sony, Sega, CCP Games andIO Interactive. Since 2003, Sumo Digital has provided co-development and turnkey developmentservices on more than 40 released titles, including contributions to franchises such as Outrun 2, Forza,Hitman, LittleBigPlanet, and Sega and Sonic All-Stars.

The video games industry is one of the largest entertainment market in the world valued in excess ofUS$113 billion and growing at 8.4% per annum. The growth of digital distribution and backwardscompatibility of new hardware releases has resulted in a smoothing of console cycles seen historicallyand an increase in the demand for high quality creative output from publishers to satisfy consumerrequirements. The Directors and the Proposed Director believe that the Company is well positioned tobenefit from this growth in demand.

The Directors and the Proposed Director believe that Admission will provide a permanent source ofcapital to deleverage the balance sheet, raise the profile of the Company, provide the ability toincentivise key employees and allow the Company to execute its strategy. Admission will also providea partial exit for funds advised by Perwyn LLP, the Company’s private equity investor. On Admission,funds advised by Perwyn LLP will hold approximately 28.39 per cent of the Company’s EnlargedOrdinary Share Capital.

The Placing will result in the issue of 38,445,869 Placing Shares, raising approximately £38.45 millionall of which will be used to settle existing debt within the Group, pay the Group’s costs in connectionwith the Placing and provide additional working capital. In addition, Selling Shareholders propose to sell39,704,131 Ordinary Shares under the Vendor Placing. Further details of the Placing and the VendorPlacing are set out in paragraph 11 of this Part I.

2. HISTORY AND BACKGROUND

Carl Cavers, Paul Porter and Darren Mills founded Sumo Digital in 2003, having previously workedtogether at Gremlin plc and Infogrames Studios Ltd. A studio in Pune (India) was established in 2007,providing a flexible and lower cost base with a highly skilled workforce. In 2007, Sumo Digital becamepart of a larger group of studios, when it was acquired by Foundation 9, an American entertainmentmedia company.

Sumo Digital was originally set up as a ‘work for hire’ games developer, working alongside developersand publishers on less creative sections of a game’s production. Successful delivery of co-developmentprojects enhanced the company’s experience of franchise IP, enabling it to take responsibility for fullturnkey projects.

In 2014, Carl, Paul, Darren and Chris Stockwell led a management buyout backed by NorthEdgeCapital, which enabled Sumo Digital to expand its services significantly, through investment in Sheffield,where it increased headcount by 41% to 336, and opening a new office in Nottingham.

In September 2016, Carl, Paul, Darren and Chris led a secondary buyout backed by funds advised byPerwyn LLP. Since completion of the secondary buyout, the Group has completed the acquisition of

19

Atomhawk in June 2017, David Wilton has joined as Chief Financial Officer, and total headcount hasincreased to 483 as at 30 November 2017.

The recent acquisition of Atomhawk, a premium digital art and design agency, has added studios inNewcastle and Vancouver (Canada) and further expanded Sumo Digital’s integrated videogame serviceoffering, as well as adding exposure to new sectors such as film and television concept art.

3. VIDEO GAMES MARKET

The video games market eco-system

The video games industry is made up of software providers, game developers, game publishers,platform providers, also acting as games publishers (such as Sony, Microsoft and Nintendo),distributors, retailers and service providers.

As an independent third-party developer of AAA-rated games, Sumo Digital’s customers are thepublishers and developers, from whom the Company generates development fees and incrementalroyalties. The platform manufacturers, in their role as exclusive publishers for their respective consoles,are also a key relationship for Sumo Digital.

Publishers typically outsource three types of work: turnkey (whole projects); co-development projects;and game development services. Sumo Digital typically partners with publishers on turnkey andco-development projects which require high levels of creative and technical expertise. Gamedevelopment services range from highly technical, high value-add services, such as motion capture,concept art and visual effects, to more commoditised services, such as testing, quality assurance andasset creation.

Video Games Market Ecosystem

Source: management information

AAA-rated games

AAA-rated game is an informal classification given to video games with typical investment of greaterthan $10 million in development and promotion. It is the video game equivalent of a ‘blockbuster’ movie.

AAA-rated games are important to both publishers and the major hardware providers as they help togenerate console sales and game franchise longevity. Certain ‘tent pole’ titles may be producedin-house, as publishers seek to maintain control over the intellectual property, whereas some AAA-ratedgames are outsourced to trusted developers. Sumo Digital, therefore, provides the ability for publishersto satisfy the increasing demand for creative content without the requirement to invest in growing andmaintaining internal teams.

Typically, the top 75 games released each year will generate approximately 55% of total video games’sales revenue. It is usual for the top ten releases to receive significantly more than $10 million

Specialist software providers:

Epic GamesAdobeThe FoundryAutodesk

Middleware/Tool Providers Game Developers Game Publishers Hardware

manufacturingRetail and

Distribution Consumer

Licence Fees Hardware Revenue

Software Revenue

Game sales

Prepaid Development Fees & Incremental Royalty

Vertically integrated publishers / console

manufacturers, with in-house developer

studios. Some have online distribution

platforms and their own ‘game engine’

Independent third-party developers (many have their own ‘game engine’ / tools):Sumo Digital

bEhaviour

Splash Damage

Saber Interactive

Climax Studios

Avalanche Studios

Ninja Theory

Platinum Games

Playground Games

High street and online specialists:

SteamGame

SUMO’S PRIMARY ROLE

CAPTIVE

INDEPENDENT

SUM

O’S

TAR

GET

C

UST

OM

ER B

ASE

Naughty DogRareRetro Studios

Polyphony DigitalBioWare Corp

Sony Interactive Entertainment

Microsoft Studios

Koch Media

EA

Nintendo

SEGA

PlayStation

Xbox

Nintendo

PlayStationNetwork

Xbox Live

My Nintendo

20

investment from publishers in the expectation of generating higher sales volumes. These games arereferred to as AAA+-rated and are typically developed in-house by publishers. Sumo Digital targetsgames that are positioned in the AA/AAA-rated category and these are turnkey or co-developed withpublishers. An illustrative representation of anticipated sales volumes for each category of game isshown below:

Source: management information

4. BUSINESS OVERVIEW

Sumo Digital is a co-development partner to some of the world’s leading publishers, offering turnkeygame development solutions. Sumo Digital develops games across all console platforms, PC, handheldand mobile devices.

The Directors and the Proposed Director believe the Group’s competitive advantage lies in its scale,management systems, technology and creative solutions, which enable it to offer flexible co-development and full end-to-end solutions for publishers and other developers.

The Group principally works across the following phases of the development of a computer game:

Phase 1 – Initial concept

The initial concept phase can vary in length but is essentially an amount of time and resource agreedbetween Sumo Digital and the customer at the start of a project to prototype key ideas and concepts.At this stage, early concept art is created to explore the visual direction of the game as well as gameplayideas being roughly blocked out in a basic form. Sumo Digital seeks to align development with thepublisher’s vision for the game at this stage.

Screenshots of early stage concept artwork for Snake Pass

Source: management information

SUMO POSITIONING

UNITS SOLD(ILLUSTRATIVE

GAME TYPE

IN-HOUSEvs

THIRD PARTY

NEXT TOP 30 TITLES (approximately 21% of market)AA / AAA TITLES

TYPICAL BUDGET $1-20m

TOP 10 TITLES(approximately 24% of market)

AAA+ TENT POLE TITLESTYPICAL BUDGET $10-100m

ACQUIRED (AAA) TYPICAL BUDGET $1-20m

LONG TAIL / INDIETYPICAL BUDGET <$1m

In-house teams, withsupport of third party

for some asset creation

AAA ‘whole game’ outsourced to a large,high quality third party studios

Self-published by developer

Mix of in-house and smallerthird party developers

21

The acquisition of Atomhawk in June 2017 further enhanced the Group’s ability to provide bespokeconcept art solutions for a wider range of customers.

Phase 2 – Pre-production

Once through the concept phase, the team moves into pre-production. The team will grow at this stageto accommodate a wider remit. The goals of pre-production are to refine the ideas and elementsinvestigated in the initial concept phase and de-risk these elements in preparation for full production.The key deliverable at this stage is often identified as a “vertical slice” of the game. This is a pre-definedpart of the game, produced to a high level of quality, that can be played and demonstrates elements ofgameplay and visuals as targeted in the finished game.

Screenshot of a ‘vertical slice’ of Snake Pass

Source: management information

Phase 3 – Production

In the production phase, Sumo Digital undertakes the peak of the game development process andtesting with key milestones agreed with customers. Typically, production of a full game takes between12 and 24 months and can involve large teams of over 100 people, in many different disciplines, suchas programming, art, design and production, depending on the size and complexity of the game.

The production phase builds on the work done in pre-production and expands the feature set createdfor the “vertical slice” into a full game experience. Mechanics, game play, level design, art andanimation, visual effects and audio are all undertaken in the production phase.

22

Screenshots of Snake Pass game in development

Source: management information

Phase 4 – Closedown

In the closedown phase, quality assurance work, user research feedback and major bug elimination arethe goals.

Sumo Digital has integrated, cross site project management tools for all stages of production.The approach is a flexible one to accommodate customers’ internal production systems. Sumo Digitalcan integrate with a number of production management software solutions, either off-the-shelf solutionsor bespoke management tools if customers prefer to use their own systems. Transparency at all stagesensures an agile approach is taken to development and both Sumo Digital and its customers are ableto access information for all actions on the project, from the early concept and planning phases throughto the final closedown, bug fixing and launch phase.

Phase 5 – Games as a service

Once a game has been launched, Sumo Digital is able to provide further support, includingdevelopment of downloadable content, development of new game features, community management,real time data mining and feedback and server operations.

The prevalence of connected hardware has extended game lifespans post release and providesongoing revenue streams for publishers and developers. Sumo Digital becomes more embedded infranchise knowledge by providing games as a service under separate contracts, and potentially furtherbenefits from additional royalties. Services include:

• Game patches and updates

• Developing add-on downloadable content for micro transactions and expansion packs

• Managing multiplayer servers

• Community management

Following the release of a game, Sumo Digital is well positioned to provide further franchise supportand undertake work on new titles as the publisher continues to expand its range.

23

Lower risk co-development operating model

Sumo Digital operates a lower risk contracting model than the majority of other developers andpublishers who are more exposed to the commercial success or failure of the game. The Directors andthe Proposed Director believe these long-term contracts de-risk the Group’s model by securing thatpayment is made in accordance with the achievement of a number of key milestones, during andfollowing release of the game which are agreed prior to the start of the project, rather than oncompletion and/or sales performance.

Visibility of revenue

Contract duration can last up to four years, providing visibility of future earnings based on man-monthcharge out rates specified in the contract. Staff utilisation is a key performance indicator for the Group.The Directors target approximately 95% utilisation in UK development studios, whilst maintaining lowerlevels of utilisation in Pune, providing flexibility at lower costs when required.

Royalties

Sumo Digital’s contracts increasingly include potential royalties alongside development fees. TheDirectors and the Proposed Director believe this enables Sumo Digital to align itself more closely withits customers and become further embedded into future iterations of the relevant game. Royalties arehigh margin revenue received for several years after a game has been released.

Video games tax relief

The VGTR is a tax relief to support the development of video games in the UK. It was first proposed bythe Labour government in 2010 and made policy by the Coalition Government in 2014.

The VGTR is part of a wider UK creative sector tax relief which seeks to incentivise investment into UKinventions or productions that may otherwise take place outside of the country, and promote thelong-term sustainability of technology skills and infrastructure. It is claimed by many companies in thewider UK creative sector marketplace. Similar government incentive schemes are prevalent in the videogames industry globally, most notably in the US, Canada, France and Scandinavia.

The majority of current games developed by Sumo Digital qualify for VGTR. The tax relief is at a rateof 25% on up to 80% of the core development costs of a game, subject to certain qualifying criteria. TheVGTR is a cash benefit and it may be claimed in the place of, not in addition to, the tax relief againstresearch and development costs for small to medium sized enterprises allowed under the 2007 FinanceAct.

TIGA estimates that since the introduction of VGTR, net employment in the UK video games industryhas increased by 7.1% per year on average. As of July 2017, 295 games productions have claimedVGTR, supporting in excess of £690 million of UK expenditure.

The Directors and the Proposed Director believe that the major UK political parties continue to supportthe VGTR and that there are no indications of any significant changes being contemplated for the VGTRregime.

In November 2017, the European Commission announced that the VGTR scheme in the UK willcontinue until at least 2023.

Own intellectual property

In 2017, Sumo Digital successfully released its first own intellectual property title, Snake Pass. The ideafor the game was originated and developed internally, using a gated process which regularly assessesthe potential of a game by a dedicated team at relatively low cost, making this a lower risk route to ownintellectual property and exploit these games for improved commercial terms. Snake Pass has provedsuccessful, with over 170,000 units sold since March 2017, generating a return on investment in excessof 83%. Snake Pass was released for PC, Xbox One, PlayStation 4 and Nintendo Switch, and itreached the number one position in the eShops charts in the UK.

The selection and release of own intellectual property is a controlled process involving approvalgateways with ideas submitted by staff at regular internal events known as “Game Jams”. Ownintellectual property development benefits Sumo Digital by providing motivation to staff to work on their

24

own ideas whilst taking their own AAA-rated development practices and applying them to smaller scaleand less risky “indie” titles. The illustration shows some of the creative process involved in developingSnake Pass:

Source: management information

Until it is decided that a game will be taken forward as a potential release, all costs relating to the titleare expensed in the income statement. Following the decision to take the project forward, direct costsof development are capitalised with regular assessment of the commercial viability of the game.Typically, all development costs are expensed in the first year following a game’s release or earlier, ifconsidered appropriate.

Customers

Sumo Digital creates content for some of the largest global video games publishers and developers.Publishers typically appoint Sumo Digital to undertake whole game projects, taking existing intellectualproperty or initial concept, and using Sumo Digital’s creative and technical talent to develop that into afull game. The publisher then releases the game through physical and digital distribution channels withSumo Digital typically credited as developer.

Examples of Sumo Digital’s current and historical customers are set out below:

Customer First engagement Games include:

Microsoft 2003

Sega 2004

Sony 2005 LittleBigPlanet 2 DLC, LittleBigPlanet 3

Koch Media 2015 Dead Island 2

IO Interactive 2016 Hitman episodic content

CCP 2017 Project Nova

Management typically looks to work on premium titles and expects to continue to work on higher budgetgames with a view to expanding Sumo Digital’s involvement in any given franchise over time. As theGroup continues to grow in scale, it will be possible for new strategic relationships to develop. Forexample, in October 2017, Sumo Digital announced a new relationship with CCP, the publisher anddeveloper of the successful EVE franchise.

Metacritic scoring

Metacritic is an independent aggregator of video game reviews, which provides the ability to compareand rank the critical performance of games relative to other releases. Video games developed andco-developed by Sumo Digital have consistently achieved high Metacritic scores with an average of 72.The Directors and the Proposed Director believe that this ranks Sumo Digital highly amongst its peers.

Atomhawk

Atomhawk, which was acquired in June 2017, is a multi-award winning visual design company thatservices the games, film and visual effects industries. Founded in 2009 by Cumron Ashtiani, Atomhawkhas studios in Newcastle and Vancouver (Canada), and employs 34 people.

Crackdown 3, Xbox Fitness, Nike+ Kinect Training,Forza Horizon 2 (Xbox 360)

Sonic & Sega All-stars Racing, Sonic All Stars RacingTransformed, Sega Superstars Tennis, Virtua TennisWorld Tour, Outrun 2

25

Key services include visual development (concept art), marketing art as well as motion graphics anduser interface design. The business is centered around helping its customers to define a visual look fortheir product from inception through development and, also, at the final point of sale through marketingimagery, videos and box packaging design. Atomhawk primarily serves the creative industries, workingwith video games studios, as well as for film and television.

Atomhawk has been involved in the creation of many high profile projects, including movies likeGuardians of the Galaxy, Thor II, Avengers II and games such as Mortal Kombat, Injustice, RYSE andKillzone. Atomhawk provides creative design and content of J.K. Rowling’s Pottermore and is a regularcreative vendor for global brands such as Lego, Microsoft, Sony, Amazon, Marvel and Warner Bros.

Atomhawk’s customers include a number of high profile video game developers, movie studios andproduct designers, including NetherRealm Studios, CCP, Rebellion, Deep Silver, Rock Steady Studios,Square Enix, Ninja Theory, BBC, Rare and Ubisoft.

The acquisition was funded through a mixture of cash and equity. Cumron continues to lead Atomhawkand will have a shareholding in the Company.

Sumo Digital’s core technology

The Sumo Digital research and development team serves a number of key roles:

• Development of future game engine and tools technology. The key responsibility of the researchand development team is to enhance and maintain the Group’s existing in house core technologyto keep it up to date with the current state of the art, along with adding support for new platformsas they come to market.

• Development of tools to enhance the efficiency of project build processes. Systems have beendeveloped and are supported by the research and development team to improve build times andstreamline integrations of external game engines.

• Provide expertise and technical support to existing game teams. The members of the researchand development team may be deployed to give technical help to existing projects to aidoptimisation, development of new features or simply advise on best practice with code with whichthey are more familiar.

As a result, Sumo Digital has an ever-growing library of tools and technology that assists to driveefficiency and helps improve margins in the business.

Locations and employees

Sumo Digital’s head office is in Sheffield, where the Group occupies several separate buildings on thesame site, facilitating the confidential development of multiple projects simultaneously.

The Indian studio in Pune provides a lower cost base and flexible capacity to the Group. The Punestudio is an extension of the UK talent pool. Its teams are integrated with the UK teams, providingsignificant timing efficiencies due to the complementary time difference to the UK. Providing theopportunity for variety of work and ownership of projects aids employee retention, versus traditionaloutsourcing often provided in this region that focuses on repetitive, lower skilled, lower margin work.

In 2016, the business opened a second UK studio in Nottingham, allowing Sumo Digital to recruit fromtwo centres and tap into a talent pool outside Sheffield.

26

The recent acquisition of Atomhawk added studios in Newcastle-upon-Tyne and Vancouver, Canada.

No. of employees at

Studio 30 November 2017

Sheffield 302Nottingham 66Pune 80Newcastle 29Vancouver 6 ––––––––Total 483 ––––––––Business development

The business development pipeline is actively managed and fully controlled utilising Pipedrive, a salesmanagement productivity tool. Sumo Digital opportunities are filtered through the following developmentstages: lead-in, contact raised, proposal made, live discussions, near contracted and contracted.

Atomhawk utilises the same tool in a different manner, in which headcount data is fed into the businessdevelopment process to ensure appropriate resources are available for escalation of an opportunity.

5. MARKET AND COMPETITION

Market and competitors

The video games industry is one of the largest entertainment sectors in the world, valued in excess of$113bn. The biggest subset is the video games software market, which was valued at $90bn in 2016and is forecast to grow at a compound annual growth rate of 9.2% to $140bn by 2021.

Source: McKinsey Global Media Report 2017, PwC Entertainment and Media Outlook, Euromonitor

Sales of consoles that offer gamers a premium experience enjoyed steady growth of 4% p.a. between2012 and 2016, with the current 8th generation Xbox and PlayStation consoles outselling the previousgeneration by over 70% in the first three years post-launch.

Source: VGChartz

Sumo Digital develops its game technology for any appropriate medium, including console, PC andmobile, although to date the focus has been primarily console and PC.

The chart below shows the expected growth of the video games software market globally by hardwareplatform category.

Global video games software market by hardware platform

Source: PwC Entertainment and Media Outlook

There are a number of important factors powering market growth in the video games industry; anexpanding demographic reach; emerging markets growth; continuous demand for better technology,graphics and functionality; and the prevalence of connected hardware extending video game lifespan.These growth factors bode well for Sumo Digital’s role in the market as a trusted development partnerto major publishers and developers.

23 26

25 3231542

75

0

20

40

60

80

100

120

140

160

FY16 FY21E

$ bi

llion

s

Console PC VR Mobile/Other

CAGR %

FY12-16 FY17-21

37% 10%

- 36%

9% 5%

4% 3%

27

Sumo Digital has the capability to develop mobile games and continually assesses opportunities in thisarea.

Shift to digital

The proliferation of online distribution platforms such as Steam, PlayStation Network, Xbox Live andNintendo E-Shop has resulted in a significant growth in the sale of digitally distributed games andadditional content through micro-transactions. Historically, games have been sold through physical retailchannels, as discrete units. By enabling digital downloads, the retailer is sometimes cut out of thisprocess, although the Directors and the Proposed Director believe physical sales will have a presence inthe foreseeable future due to the sheer data size required in complex games. This has resulted in areduced cost of distribution, greater ease of self-publishing and promotion, the potential for dynamicpricing and the potential for games to move from a product to a service. This has also enabled SumoDigital to publish its first own IP game in Snake Pass by removing any need for physical inventory andassociated stock risk. The chart below shows the historic and anticipated shift from physical to digitaldistribution of video games.

Video games sales by distribution channel

Source: PwC Entertainment and Media Outlook

Publishers have taken advantage of the opportunity granted by digital distribution to extend the lifespanand revenue generation of a game title post-release by providing an array of additional services anddigital content.

This creates new opportunities for trusted third party developers such as Sumo Digital in a “games-as-a-service” role by taking on additional development work and managing direct end user engagement onbehalf of the publisher. This extension of developer support further embeds Sumo Digital’s role in thelife of a game and it has taken this service approach with a number of games. The chart belowillustrates the greater level of developer support required under a games as a service model.

Post launch developer support enabled by digital distribution

Source: PwC Entertainment and Media Outlook

05

101520253035404550

2012 2013 2014 2015 2016 2017E 2018E 2019E 2020E 2021E

Rev

enue

($bn

)

Physical Digital

DEVELOPER SUPPORT

INITIAL TITLE DEVELOPMENT GAMES AS A SERVICE

Emerging model(Physical and digital distribution)

Release date

Multiplayer hosting and community management

Downloadable content andexpansions

Post-release patching and game fixes

Historic model(Physical distribution)

DEVELOPER SUPPORT

28

Embedded user base

Historically, there was a clearly defined console hardware cycle, which in turn defined the softwarecycle. Low installed base numbers during the early stages meant that third party publishers were moreinclined to wait for the market to be in a position for them to maximise the return on investment beforeinvesting in software. Gamers would also be less inclined to purchase new games at the end of oneconsole’s life cycle, instead waiting for the next generation of console to be on sale.

The current installed console base is now beginning to benefit from backward compatibility, which is theability to play games from previous generation consoles on the new generation consoles. This is viewedas potentially transformative for the industry and has substantial benefits for the game developers,establishing an embedded user base which provides the opportunity for constant mass marketpenetration. The new Xbox One S and PS4 Pro upgrades reflect a more iterative approach to consoledesign and backwards compatibility for future console generations is the stated aim of Microsoft. Thechart below shows the cumulative sales of PlayStation 4 and Xbox One consoles achieved in the period2014-2016 and expected in the period 2017-2020.

Cumulative console sales (8th generation)

Source: VG Chartz, VG Sales Wikia and management information

Geographic expansion

The video games market is also benefiting from global emerging markets. In China, the sale of gamesconsoles was banned in 2000 by the government. However, the ban was lifted in January 2014 andMicrosoft entered the market in September 2014 and Sony in March 2015. There is also huge potentialdemand from South America (+15% CAGR for retail sales, FY16-21, the fastest of all geographies). Thechart below shows the value of the video games market by region, with year on year growth rates.

Source: Newzoo

Global video games market per region with year on year growth rates

Source: Newzoo

1937

54 5671 83 90

11

20

2841

5160

67

0

20

40

60

80

100

120

140

160

180

2014 2015 2016 2017E 2018E 2019E 2020E

Uni

ts M

illio

ns

PS4 Xbox One

4%

25%

47%

24%

2017 Total

$108.9bn+7.8% YoY

EMEA$26.2bn

+8.0% YOY

APAC$51.2bn

+9.2% YOY

North America$27.0bn+4.0% YOY

Latin America$4.4bn+13.9% YOY

China Total$27.5bn

29

Broadening demographics

The age demographics of video gamers continues to broaden, as consumers remain engaged pastadolescence due to continued innovation. Video games attract a wide mix of consumers, who aretypically ‘sticky’ over time. The current average video game player is 35 years old. The video gamesmarket has also become non-gender specific with over 40% being female gamers.

Source: Entertainment Software Association Survey

Competitors

There are only a handful of independent developers with Sumo Digital’s scale that can provide fullservice to the largest game publishers. The Directors and the Proposed Director believe that thefollowing are the closest comparable developers to Sumo Digital:

Average

Number of Metacritic

Developers Staff score

Sumo Digital 483 72

Avalanche Studios, bEhaviour, Saber Interactive 200 – 400 52 – 70

Climax Studios, Ninja Theory, Platinum Studios, Playground Games 100 – 200 69 – 81

Source: Metacritic, publicly available information on staff numbers

Sumo Digital is one of the UK’s largest independent third-party video games developers, with a totalheadcount of 483.

6. STRATEGY

Growth opportunities for Sumo Digital