third quarter report march 31, 2008 - home | centamin/media/files/c/centamin/documents/... ·...

TRANSCRIPT

THIRD QUARTER REPORT

March 31, 2008

CONTENTS

REPORT TO SHAREHOLDERS 1

MANAGEMENT DISCUSSION AND ANALYSIS 16

UNAUDITED INTERIM CONSOLIDATED INCOME STATEMENTS 25

UNAUDITED INTERIM CONSOLIDATED BALANCE SHEETS 26

UNAUDITED INTERIM CONSOLIDATED STATEMENTS OF CHANGES IN EQUITY 27

UNAUDITED INTERIM CONSOLIDATED CASH FLOW STATEMENT 28

NOTES TO THE UNAUDITED INTERIM CONSOLIDATED FINANCIAL STATEMENTS 29

CERTIFICATE OF INTERIM FILINGS 39

CENTAMIN EGYPT LIMITED ____________________________________________________________________________________

Page 1

RREEPPOORRTT TTOO SSHHAARREEHHOOLLDDEERRSS

QUARTERLY HIGHLIGHTS

Sukari mineral resource upgraded to 8.12 million ounces of gold Measured and Indicated, plus 3.5 million ounces of gold Inferred at 0.5 g/t cut off grade

Measured and Indicated resources account for 70% of the total resource

An increase of 660,000oz Measured and Indicated ounces above the mineral resource announced in December 2007

Amun Deeps discovery continues to add significant high grade ounces

22,430m of drilling completed during the quarter

Follow up regional exploration drilling at Kurdeman returned significant assay results

Appointment of Underground Mine Manager

Process plant site civil works complete using owner mining fleet

Process plant refurbishment commences on site

Initial concrete poured in process plant site area

Sea water pipeline commenced

Tailings storage facility (TSF) earth works commence

Drilling continues with 8 rigs on site

Employees and contractors exceed 600

Significant intersections received for the quarter include:

Amun Deeps (9900N – 10700N) D1280 – 35m @ 164.09g/t Au (including 1m @ 5,420g/t Au) D1328 – 19m @ 8.03g/t Au and 72m @ 2.36g/t Au D1308 – 11m @ 12.90g/t Au D1307 – 19m @ 5.31g/t Au D1298 – 19m @ 3.73g/t Au D1295 – 16m @ 3.44g/t Au D1301 – 51m @ 2.04g/t Au D1306 – 86m @ 1.91g/t Au

Kurdeman Prospect KRC007 – 17m @ 3.81g/t Au KRC011 – 8m @ 7.76g/t Au KRC014 – 2m @ 26.59g/t Au KRC015 – 2m @ 34.69g/t Au

CENTAMIN EGYPT LIMITED ____________________________________________________________________________________

Page 2

RESOURCE ESTIMATION AND DRILLING PROGRAMME In the March quarter, the Sukari Mineral Resource was upgraded to 8.12 Moz Measured and Indicated, plus 3.5 Moz Inferred at a 0.5g/t cut off grade. The Measured and Indicated Mineral Resource has increased by 660,000 oz, approximately 9% to 8.12 Moz from 7.46 Moz (19 December 2007) showing the effectiveness of the infill drilling programme (Table 1). Measured and Indicated resources account for 70% of total resource. Resource growth at Sukari occurred within the Amun Deeps from 9900N to 10700N, testing the Hapi Zone and deeper, sub-parallel mineralized structures.

Table 1 – March 2008 Resource Calculation

Measured Indicated Total

(Measured + Indicated) Inferred

Cut-off g/t Au

Tonnes (Mt)

Grade (g/t Au)

Tonnes (Mt)

Grade (g/t Au)

Tonnes (Mt)

Grade (g/t Au)

Gold (Moz)

Tonnes (Mt)

Grade (g/t Au)

Gold (Moz)

0.50 63.85 1.43 107.84 1.50 171.69 1.47 8.12 63.2 1.7 3.5 0.70 46.12 1.75 78.99 1.82 125.11 1.80 7.23 46.7 2.1 3.2 1.00 29.94 2.24 52.19 2.33 82.13 2.30 6.07 31.8 2.7 2.8

Note to Table: Figures in table may not add correctly due to rounding

3.7 3.7 3.7 3.7 3.7 3.7

0.7 0.8 0.9 1.0 1.2 1.5 1.7

3.13.6

4.3 4.6

1.72.4 2.8 3.1

3.84.4

0.6 0.7 0.8 0.8 0.81.2

1.3

1.4

2.2

2.5

3.1

2.8

2.9

3.33.6

3.7

3.5

0.0

2.0

4.0

6.0

8.0

10.0

12.0

Apr 97

Sep 00

Jan 0

1Ju

l 01

Jan 0

2Ju

l 02

Feb 03

Mar 03

Dec 05

Apr 06

Jul 0

6

Nov 06

Feb-07

May 07

Aug 07

Sep 07

Dec-07

Mar-08

Au

Oun

ces

(Moz

)

InferredMeasured & IndicatedProven & Probable

Figure 1 – Resource growth at Sukari from April 1997 to March 2008

The resources are estimates of recoverable tonnes and grades using Multiple Indicator Kriging (“MIK”) with block support correction. Typically, measured resources lie in areas where drilling is available at a nominal 25 x 25 metre spacing, indicated resources occur in areas drilled at approximately 25 x 50 metre spacing and inferred resources exist in areas of broader spaced drilling. The resource model extends from 9700mN to 12200mN and to an approximate depth of 350mRL (approximately a maximum depth of 950 metres below the crest of the Sukari hill) and is based on all assay data available at 30 March 2008. The sampling from an additional 21,000 metres of drilling (primarily diamond drill core) has been added to the resource sampling data set used in the new mineral resource estimate. DRILLING PROGRAMME The drilling programme during the quarter was concentrated in the Amun Deeps area, testing down dip extensions of the Hapi and deeper, sub-parallel mineralisation zones at depth. This resulted in added resource ounces down dip of the current

CENTAMIN EGYPT LIMITED ____________________________________________________________________________________

Page 3

geological data, infilling resource block and geological data gaps at and beneath the pit margins and increased the understanding of the mineralization trends. Planned drilling will continue to infill and step-out to test the extension of the Hapi Zone and related structures in the Amun Deeps Zone to 11200N. Drilling will re-commence in the Ra/Gazelle and Pharaoh Zones north of 11200N where mineralization is open and requires infill to fully define the Hapi Zone and related high grade structures. Amun Deeps (9900 – 10700N) The Amun Deeps system has been intersected over 700m along strike from 9950N, drilling continues to define the extent of the mineralization. Several holes returned strong assays over significant widths (Table 2); most have visible gold in the high grade Hapi Zone quartz veins, strongly disrupted geological contacts and areas of higher intensity arsenopyrite and pyrite mineralisation.

Figure 2 – Long section of Sukari showing the high grade mineralized structures (Main and Hapi Zone) and highlighting the drill intercepts through the Amun Deeps.

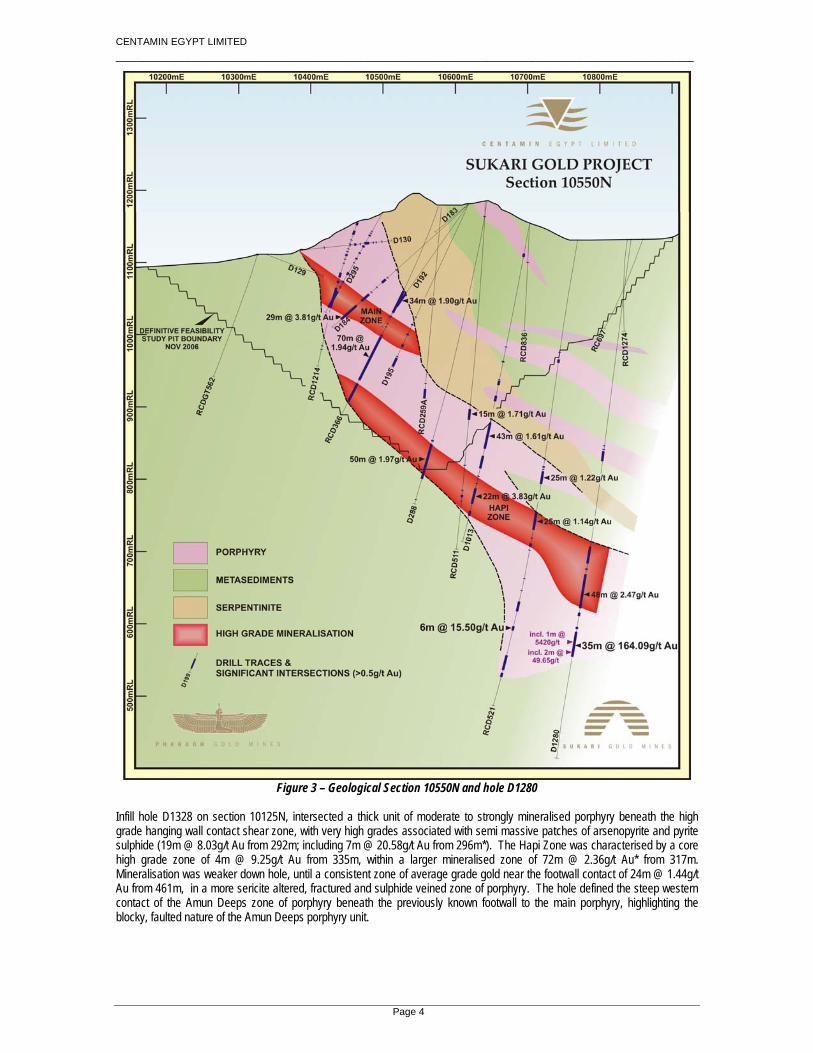

High grade gold intersections returned included hole D1280 at 10550N which intersected spectacular visible gold and galena in a massive quartz vein (558-559m) within highly mineralised porphyry returning 35m @ 164.09g/t Au from 550m (including 1m @ 5,420g/t Au from 558m) (figure 3). This deeper structure sits below the existing Hapi zone and correlates to 6m @ 15.21g/t Au in hole RCD521 from 542m and 22m @ 21.83g/t Au from 549m in hole RCD1221 25m to the south (announced 6 February 2008 and 21 November 2007 respectively).

CENTAMIN EGYPT LIMITED ____________________________________________________________________________________

Page 4

Figure 3 – Geological Section 10550N and hole D1280

Infill hole D1328 on section 10125N, intersected a thick unit of moderate to strongly mineralised porphyry beneath the high grade hanging wall contact shear zone, with very high grades associated with semi massive patches of arsenopyrite and pyrite sulphide (19m @ 8.03g/t Au from 292m; including 7m @ 20.58g/t Au from 296m*). The Hapi Zone was characterised by a core high grade zone of 4m @ 9.25g/t Au from 335m, within a larger mineralised zone of 72m @ 2.36g/t Au* from 317m. Mineralisation was weaker down hole, until a consistent zone of average grade gold near the footwall contact of 24m @ 1.44g/t Au from 461m, in a more sericite altered, fractured and sulphide veined zone of porphyry. The hole defined the steep western contact of the Amun Deeps zone of porphyry beneath the previously known footwall to the main porphyry, highlighting the blocky, faulted nature of the Amun Deeps porphyry unit.

CENTAMIN EGYPT LIMITED ____________________________________________________________________________________

Page 5

Hole D1301 on section 10375N intersected, including 31m @ 2.84g/t Au* from 306m in the Hapi Zone near the hanging wall contact, also strong mineralisation at the footwall zone intersected 51m @ 2.04g/t Au* from 404m. D1307 on 10400N, 25 metres to the north returned 19m @ 5.31g/t Au* from 422m through the down dip extension of the Hapi Zone. At the southern end of the Amun Deeps Zone, on section 9950N hole D1308 intersected a thick continuous zone of porphyry with strong mineralisation at the footwall zone returning 11m @ 12.90g/t Au* from 419m. On section 10025N hole D1306 returned 86m @ 1.91g/t Au * from 390m (incl. 2m @ 18.55g/t Au from 401m). Notes: * Denotes assay intersections previously announced on 08 April 2008. Ra – Gazelle Zone – 10700N – 11200N Drilling recommenced in early April, no drilling activity was undertaken in the Ra – Gazelle Zone during the quarter. REGIONAL EXPLORATION Regional and near mine exploration continued, drilling at Kurdeman and Sukari North intersected high grade and anomalous gold mineralization results respectively. Follow up drilling, detailed mapping and sampling continued at Sukari North and Kurdeman (Figure 4) and it is planned to continue the regional scale mapping and sampling geochem program in the belt from Sukari North to Kurdeman in the coming quarter.

Figure 4 – Regional map of prospects and the current 160km2 licence area.

CENTAMIN EGYPT LIMITED ____________________________________________________________________________________

Page 6

Kurdeman Follow up RC drilling (2,420 metres) from the successful initial 5 hole drill program, detailed mapping and rock chip sampling (750 samples) was completed at the Kurdeman prospect. Drilling targeted the quartz vein - shear zone, which was worked by ancient and colonial miners. Sixteen drill holes (not all results received) were drilled to follow up previous strong assays, trace the southern extensions of the quartz vein – shear zone in fine grained felsic volcanic rocks some 300m to the south and targeted the high grade mineralised structures in the old underground mine workings. Several significant assay results were returned, including hole KRC007 – 17m @ 3.81g/t Au from 111m, hole KRC011 – 8m @ 7.76g/t Au from 77m, KRC014 – 2m @ 26.59g/t Au from 89m and KRC015 – 2m @ 34.69g/t Au from 116m. See Table 2 for other significant assays received to date. Gold mineralisation in the drilling was predominantly within the fine grained, cherty felsic volcanic unit, associated with the smoky grey, recrystallised quartz vein, fine grained pyrite dusting, carbonate-silica weak sericite alteration halo and moderate shearing. Hole KRC007 confirmed the near vertical extent of the high grade zone intersected in KRC002, indicating at least 100m of vertical extent, for a 5 – 10m wide quartz vein-shear zone. Sukari North Assay results have been returned for the RC drilling campaign (1,530 metres) at Sukari North, aimed at testing the main felsic intrusive unit in the area of the workings and gold anomalous rock chip samples, the main mineralised structural trends (East to SE dipping), the rock itself, and the geological contacts with surrounding rocks. Several zones of weak to moderate gold anomalism were detected, associated mainly with zones of strong ankeritic alteration and quartz veining in the felsic intrusive unit, and at contacts to the surrounding sediments and mafic volcanic rocks. The drilling suggests the felsic unit is narrow and surrounded by black shaley sediment, felsic flows, mafic and ultramafic rock units and cut by several felsic and mafic dykes. Further regional mapping and sampling through the area is planned. Sami South No significant activity. GRADE CONTROL The new Atlas Copco L8 RC grade control drill rig was delivered and commissioned, and training commenced. Grade control drilling continued on available tracks on Sukari Hill within the mine footprint, 3,196m were drilled. Gold mineralisation estimated from grade control modelling corresponds well to expected mineralisation in the resource model; assay results highlight shallow easterly and westerly dipping structures. UNDERGROUND MINE PLANNING During the quarter the company successfully filled the position of Underground Mine Manager. Work has now begun on several fronts including the following reviews:

- Geology of the high grade Amun Deeps - Geotechnical - Mining method - Contract mining v Owner Operator - Capital expenditure estimates - Infrastructure preparation.

It is the intention to target an initial underground mining rate of 500,000t per annum and the Company will be able to provide further guidance on the progress of the underground mining operation by mid 2008.

CENTAMIN EGYPT LIMITED ____________________________________________________________________________________

Page 7

SUKARI GOLD PROJECT (CONSTRUCTION UPDATE) The project schedule has been updated to 31 March 2008, covering all phases of the project. Key completion dates are listed below:

Project Go-Ahead Decision Feb 2007 (Completed) Kori Kollo Plant Arrives Egypt Q4 2007 (Completed) 28MW Power Station Arrives Q4 2007 (Completed) Project Finance Q4 2007 (Completed) Project Engineering & Design Q2 2008 (Commenced) Site Civil Works Q2 2008 (Commenced) Seawater Pipeline Q3 2008 (Commenced) Tailings Storage Facility Q4 2008 (Commenced) Mining Pre-strip Q3 2008 Commissioning and Production Q1 2009

Progress pictures can be viewed on the Company’s website – www.centamin.com. Kori Kollo Process Plant /28MW Isparta Power Station On 24 October 2007, the Company announced that both the Kori Kollo processing plant and the Isparta power plant had arrived safely at the Egyptian seaport of Alexandria and their cargoes had been discharged. The dismantling of the Kori Kollo processing facility in Bolivia and the Isparta 28MW power plant in Turkey were completed in September and both sites were closed and signed off. All staff from Bolivia and Turkey have now relocated to Egypt to continue with the reassembly of the plants at Sukari. The Isparta power plant consisted of 24 pieces of break bulk and 56 containers holding more than 900 individual packages. The Kori Kollo processing plant comprised 270 pieces of break bulk and 55 containers. Trucking of freight to the Sukari site was completed during quarter four of 2007. The refurbishment program for the Kori Kollo processing plant is underway with sand blasting and undercoating of equipment progressing under the supervision of the Plant Maintenance Manager. Temporary workshops have been erected to accommodate the refurbishment program. Project Engineering and Design MetPlant Engineering Services Pty Ltd, an Australian-based company have continued with the engineering and design work for the Process Plant. Site Works Activities completed and commenced to the end of the quarter are as follows:

• Upgrading of the 10km access road to the Sukari site (completed) • Establishment of container and mine lay down and security hut complex facilities (completed) • Temporary maintenance, warehousing and fuelling facilities (completed) • Bulk earthworks for the plant site (completed) • Crushed ore stockpile reclaim tunnel (commenced) • Excavation of crusher and power plant foundations (commenced)

A significant amount of rocky outcrops overlaying the plant site area have been removed through the utilisation of the new mining equipment which has facilitated in the training of owner personnel. The concrete batch plant is schedule for arrival on site during April 2008 (arrived at date of writing) permitting concrete foundation for crusher, CIL tanks, power plant, stockpile reclaim tunnel etc. to progress at an accelerated pace. Due to the late arrival of the batch plant insufficient concrete was poured during Q1 2008 which has led to the process plant commissioning date slipping to Q1 2009.

CENTAMIN EGYPT LIMITED ____________________________________________________________________________________

Page 8

Tailings Storage Facility Knight Piesold Pty Ltd has been appointed to carry out the design and construction supervision of the Tailings Storage Facility. Design work is complete and construction of the dam commenced in quarter one 2008 with the bulk earthworks part of the program involving excavation of the embankment and deliveries of gypsum sand to the site which will be the bedding material for the liner. Completion of the tailings dam is scheduled for quarter four 2008. Seawater Supply System Construction of the seawater pipeline commenced during the quarter with rock breaking and road works of the pipeline schedule for completion in quarter two. Installation and welding of the HDPE pipe has commenced and is progressing well with just over half the pipe already installed. Pressure testing will commence in April 2008 with the overall program scheduled for completion in Q3 2008. Work on the seawater wells is due to commence in Q2 2008. The Seawater Supply System will draw in and transport raw seawater, via a staged pumped pipeline, to the Sukari site where it will be processed through a desalination plant for end use as process plant water, mine site dust suppression water and, after secondary processing and treatment for construction camp drinking water. Mining Fleet Caterpillar, through their Egyptian authorised dealer Mantrac, was selected through a competitive tender as the supplier of haulage trucks, articulated dump trucks, excavators, graders and dozers for the project. The initial mining fleet sufficient to commence mining pre-strip work will largely comprise:

CAT 785C Rear Dump Trucks (5) CAT 785C Water Truck (1) O&K RH120E Excavator (1) CAT D10T Dozers (2) CAT 14H Grader (1) CAT 16M Grader (1) CAT 365 BLME Excavator (1) CAT 988G Wheel Dozers (2) H180D Rock Breaker (1)

Atlas Copco has been selected to supply grade control and blast hole drilling equipment. Initial fleet selection comprises:

ROC F9 Pioneer Drill (1) L8 MKII Production Drill (1) L8 MKII RC Rig (1)

The majority of the initial fleet is on site and already in use for plant site and TSF civil work. Mining pre-strip activity is scheduled to commence in quarter three of 2008. Project Finance On 23 November 2007, the Company announced that it had sold on a private basis an aggregate of 112,000,000 special warrants at a price of C$1.20 per special warrant for aggregate gross proceeds of C$134,400,000, which includes the exercise in full by the Underwriters of the Underwriters’ option. The net proceeds of this equity financing are to be applied to fund the continued development of the Sukari Gold Project, underground development, other exploration and general corporate purposes. The Sukari Gold Project is 100% fully funded through to gold production currently forecast to be the first quarter of 2009. As a result the Company no longer needs to pursue debt financing, has no debt, no hedging and at 31 March 2008, had a cash balance of US$200M.

CENTAMIN EGYPT LIMITED ____________________________________________________________________________________

Page 9

SUKARI GOLD PROJECT (BACKGROUND) Centamin is a mineral exploration and development company that has been actively exploring in Egypt since 1995. The principal asset of Centamin is its interest in the Sukari Gold Project, located in the Eastern Desert of Egypt. The Sukari Gold Project is at an advanced stage of development, with construction having commenced in quarter two of 2007 and first gold production expected during the first quarter of 2009. A definitive feasibility study (the “DFS”) for the development to commercial production of the Sukari Gold Project was completed in February 2007. A summary of the findings of the DFS were:

• the DFS concluded that a 4mpta plant producing on average 200,000 ounces per annum, over 15 years of mining, is economically robust; and

• total Capital Construction costs are estimated at US$216m with average cash operating costs of US$290/oz (inclusive of 3% royalty) over the 15 year mining period.

The Sukari Gold Project will be the first large-scale modern gold mine to be developed in Egypt. Centamin’s operating experience in Egypt gives it a significant first-mover advantage in acquiring and developing other gold projects in the prospective Arabian-Nubian Shield. The Sukari Gold Project is hosted by a large, sheeted vein-type and brittle-ductile shear zone hosted gold deposit developed in a granitoid intrusive complex. Gold mineralization is hosted exclusively by a granitoid body of granodiorite - tonalite composition referred to as the Sukari Porphyry. The Company has entered into a Concession Agreement with the Egyptian Government that provides for exploration and exploitation rights at the Sukari Gold Project and whereby the Operating Company, owned 50% by the Company’s wholly owned subsidiary, Pharaoh Gold Mines NL (“PGM”) and 50% by Egyptian Mineral Resource Authority (“EMRA”), has been established. Centamin is entitled to recover all of its exploration, operating and capital costs from operating surpluses of the operating company. The Sukari Mining Licence covers an area of 160 km2 and is for a period of 30 years, with an option for a further 30 years. The Sukari Gold Project has been scheduled for open pit mining over an initial 15-year period. During that time 78 Mt ore @ 1.5 g/t Au is expected to be mined, producing 3.7 Moz gold. A further 374 Mt of waste material is also expected to be mined resulting in a waste to ore strip ratio of 4.8:1. Ore and waste will be mined using conventional open pit mining methods. The operation is planned to utilize selective mining techniques to separate ore and waste. Provision has been made for drilling and blasting all primary and oxide materials. Ore will be hauled to the run of mine pad next to the Processing Plant and either direct tipped to the crusher or stockpiled for future reclaim at the 4 Mtpa Process Plant throughput rate. Mining will be progressed at an increased rate compared to processing; approximately 5 Mt of ore is expected to be mined and 4 Mt of ore will be processed annually. Operating at an increased mining rate allows the cut off grade for feed to the Plant (referred to as “cutover” grade) to be increased in the early years of the schedule. This in turn increases the metal output and project revenue in these early years, thus increasing the discounted operating surplus cashflow. According to current schedules, the low-grade stockpile produced as a result of applying a cutover grade, will be processed after mining has ceased, extending the current operating life of the project for a further six years. As a result, the average milled grade during the mining period is forecast to be 1.87 g/t Au, compared to 0.66 g/t Au for the low-grade stockpile. Centamin will own and operate its mining fleet. The production fleet will be based on 380 t class excavators and 150 t class rigid body trucks. At full production, three production fleets, each comprising a single excavator and sharing a maximum of 21 trucks, will be required. The capital cost of the initial mining fleet has been estimated by AMC at US$48.8 million. The proposed process route entails:

• crushing; • stockpiling crushed ore; • grinding; • flotation of a (bulk sulphide) concentrate containing the precious metals; • thickening of the concentrate; • fine milling of the concentrate;

CENTAMIN EGYPT LIMITED ____________________________________________________________________________________

Page 10

• leaching the precious metals from the concentrate in a dilute cyanide solution; • adsorbing the precious metals onto activated carbon; • stripping the precious metals from the carbon; • recovering the precious metals as gold doré; and • placing the concentrate tailing in the tailings storage facility.

Tailings from the treatment of weathered oxide ore early in the mining schedule contain too much gold to discard. Hence, the bulk flotation tail is further treated by:

• thickening; • leaching the precious metals into a dilute cyanide solution; • adsorbing the precious metals onto activated carbon; • stripping the precious metals from the carbon; • recovering the precious metals as gold doré; and • placing these tailings in the tailings storage facility.

Process water will be drawn from the Red Sea. The seawater will be pumped approximately 25 km to the mine site to satisfy all Process Plant and mining requirements. Most of the seawater will be pumped into a raw water pond located near the Processing Plant, whilst around 500m³/day will be pumped to a Water Treatment Plant for potable and fresh water supplies. Power will be generated on site by a 28 MW power station, operated on heavy fuel oil. A temporary construction camp facility will be required to cater for approximately 500 construction employees and 20 senior staff. This is being constructed at the Sukari Gold Project site (completed in Qtr 1, 2008). On behalf of Centamin Egypt Limited Josef El-Raghy Managing Director/CEO May 12, 2008 For more information please contact: Centamin Egypt Limited + 61 (8) 9316 2640 Josef El-Raghy

Pelham Public Relations Te l : + 44 (0) 207 743 6376

Mobile : + 44 (0) 7894 462 114 Candice Sgroi

Ambrian Partners Limited + 44 (0) 207 776 6400

Richard Brown

Information in this report which relates to exploration, geology, sampling and drilling is based on information compiled by geologist Mr R Osman who is a full time employee of the Company, and is a member of the Australasian Institute of Mining and Metallurgy with more than five years experience in the fields of activity being reported on, and is a ‘Competent Person’ for this purpose and is a “Qualified Person” as defined in “National Instrument 43-101 of the Canadian Securities Administrators”. His written consent has been received by the Company for this information to be included in this report in the form and context which it appears. The assay samples were analysed by Ultra Trace Pty Ltd, Canning Vale, Western Australia. The information in this report that relates to mineral resources is based on work completed by Mr Nicolas Johnson, who is a Member of the Australian Institute of Geoscientists. Mr Johnson is a full time employee of Hellman and Schofield Pty Ltd and has sufficient experience which is relevant to the style of mineralisation and type of deposit under consideration and to the activity which he is undertaking to qualify as a “Competent Person” as defined in the 2004 edition of the "Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves" and is a “Qualified Person” as defined in “National Instrument 43-101 of the Canadian Securities Administrators”. Mr Johnson consents to the inclusion in the report of the matters based on his information in the form and context in which it appears. Refer to the Technical Report which was filed in March 2007 for further discussion of the extent to which the estimate of mineral resources/reserves may be materially affected by any known environmental, permitting, legal, title, taxation, socio-political, marketing or other relevant issue.

CENTAMIN EGYPT LIMITED ____________________________________________________________________________________

Page 11

Table 2 – Significant Intersections March 2008 Quarter

HOLE NORTH EAST DIP AZI EOH FROM TO INTERVAL Gold (g/t)

Sukari Resource Drilling *D1280 10550 10842.63 -82 270 726.7 430 454 24 0.93

469 517 46 2.21 incl. 471 473 2 6.47 incl. 477 478 1 5.71 incl. 500 501 1 11.30 incl. 513 516 3 5.74 550 585 35 164.09 incl. 558 559 1 5,420.00 incl. 576 578 2 49.65

D1282 10075 10646.28 -88 270 560.3 368 438 70 1.47 incl. 379 380 1 35.30

D1284 10350 10753 -85 270 587.0 363 374 11 2.98 incl. 365 366 1 6.71 incl. 368 369 1 6.72 387 392 5 1.90 427 462 35 1.58 incl. 429 430 1 6.55 incl. 435 436 1 9.09 468 494 26 1.13 incl. 480 481 1 5.03 incl. 493 494 1 8.58

D1287 10375 10525 -70 270 310.6 49 58 9 1.23 63 70 7 2.12 118 149 31 1.40 incl. 137 139 2 6.26 incl. 143 144 1 7.63 171 173 2 5.21 238 265 27 1.47 incl. 262 263 1 5.75

D1289 10150N 10725 -84 270 599.5 400 404 4 1.62 410 423 13 2.17 incl. 412 413 1 8.00 430 438 8 1.31

D1294 10225 10715 -83 270 655.5 212 214 2 1.37 355 412 57 1.72*

CENTAMIN EGYPT LIMITED ____________________________________________________________________________________

Page 12

incl. 362 363 1 9.05 incl. 365 366 1 5.15 incl. 388 389 1 6.40 427 447 20 2.04* incl. 444 446 2 6.42 489 490 1 12.20

D1295 10475 10515 -83 270 342.8 82 91 9 1.87 126 135 9 2.01 incl. 132 133 1 6.01 159 175 16 3.44* incl. 162 163 1 9.34 incl. 168 169 1 6.02 incl. 170 171 1 23.90 214 287 73 1.12 incl. 252 253 1 5.94

D1297 10412 10565 -72 255 295.5 110 114 4 1.06 153 174 21 2.02 incl. 159 161 2 9.76 incl. 171 172 1 5.67 183 190 7 1.56 196 213 17 1.47 223 235 12 2.21 incl. 225 226 1 13.70 245 265 20 3.20 incl. 246 247 1 7.51 incl. 264 265 1 35.20

D1298 10325 10700 -74 270 501.7 299 305 6 1.59 315 330 15 1.65 incl. 324 325 1 6.87 343 348 5 4.09 incl. 345 346 1 16.20 359 372 13 2.45 incl. 368 369 1 6.64 incl. 371 372 1 14.50 421 440 19 3.73* incl. 426 427 1 9.27 incl. 439 440 1 44.40

D1301 10375 10700 -78 270 636.9 280 286 6 1.83 298 300 2 1.79 306 337 31 2.84* incl. 309 311 2 9.35

CENTAMIN EGYPT LIMITED ____________________________________________________________________________________

Page 13

incl. 323 326 3 7.49 incl. 333 334 1 14.00 370 385 15 1.06 404 455 51 2.04* incl. 419 420 1 30.60 incl. 453 455 2 11.76

D1303 10525 10547 -75 270 390.0 104 233 129 1.80 incl. 127 128 1 7.82 incl. 146 147 1 5.51 incl. 163 168 5 7.65 incl. 183 184 1 5.75 incl. 195 198 3 8.02 incl. 213 215 2 7.29 238 241 3 1.21 245 285 40 1.43 incl. 280 281 1 13.80 291 317 26 1.98 incl. 301 302 1 5.79 incl. 306 307 1 5.29 incl. 314 315 1 6.40

D1304 10300N 10831 -80 270 656.0 437 452 15 2.88 incl. 450 451 1 25.00 457 469 12 1.74 incl. 468 469 1 7.82

D1306 10025N 10612 -87 270 555.6 344 366 22 1.07 390 476 86 1.91* incl. 401 403 2 18.55 incl. 417 420 3 5.19 incl. 468 469 1 8.91

D1307 10400 10845 -80 270 469.2 391 393 2 3.03 403 410 7 1.43 422 441 19 5.31* incl. 422 424 2 9.27 incl. 429 430 1 63.50*

D1308 9950N 10645 -80 270 535.4 377 379 2 6.24 398 414 16 2.29 incl. 399 400 1 5.64 419 430 11 12.90* incl. 420 421 1 119.00*

CENTAMIN EGYPT LIMITED ____________________________________________________________________________________

Page 14

D1313 10050N 10665 -88 270 606.2 408 453 45 1.07 incl. 449 450 1 9.74

D1320 10500N 10875 -82 270 710.3 459 461 2 2.44 505 507 2 11.24 553 554 1 4.08

D1321 9975N 10965 -82 270 584.8 390 393 3 1.11 413 418 5 1.07

RCD1322 10600N 10875 -82 270 708.0 454 487 33 1.63 incl. 477 478 1 9.01 incl. 481 483 2 7.13 538 539 1 5.91 569 570 1 3.40

D1328 10125N 10660 -76 270 654.4 292 311 19 8.03* incl. 296 303 7 20.58* 317 389 72 2.36* incl. 335 339 4 9.25 incl. 351 352 1 5.06 incl. 381 382 1 5.29 439 455 16 1.36 incl. 453 454 1 5.12 461 485 24 1.44

Kurdeman Prospect

KRC007 2752145 671212 -60 270 150.0 111 128 17 3.81 incl. 111 112 1 9.72 incl. 118 120 2 22.39

KRC011 2751685 671180 -60 270 150.0 77 85 8 7.76 incl. 78 83 5 11.44

KRC012 2751638 671166 -60 270 150.0 58 60 2 1.43

KRC013 2752341 671102 -60 40 150.0 54 55 1 2.50

KRC014 2752307 671116 -60 40 150.0 89 91 2 26.59

KRC015 2752267 671139 -60 40 150.0 116 118 2 34.69

KRC018 2752175 671197 -60 270 150.0 52 56 4 3.25 incl. 52 53 1 8.13

CENTAMIN EGYPT LIMITED ____________________________________________________________________________________

Page 15

Sukari North Prospect SNRC007 2765261 676731 -60 290 30.0 2 5 3 1.18

SNRC007A 2765227 676740 -60 290 150.0 11 15 4 1.18

85 86 1 3.35

SNRC008 2765259 676771 -60 290 150.0 21 27 6 0.56 incl. 25 26 1 1.34 33 38 5 0.23

Notes: (1) Intervals shown in the table are down hole intercepts, drilled at high angles relative to the internal mineralized structures and the Sukari Porphyry; true widths do not apply or are not used in drilling the stockwork style mineralization at Sukari; (2) * Denotes assay intersections previously announced on 06 February 2008 and 08 April 2008.

CENTAMIN EGYPT LIMITED ____________________________________________________________________________________

Page 16

MMAANNAAGGEEMMEENNTT DDIISSCCUUSSSSIIOONN AANNDD AANNAALLYYSSIISS

The following Management’s Discussion and Analysis of the Financial Condition and Results of Operations (“MD&A”) for Centamin Egypt Limited (the “Company” or “Centamin”) should be read in conjunction with Unaudited Interim Consolidated Financial Statements for the nine months ended March 31, 2008 and related notes thereto. The effective date of this report is May 12, 2008. The accompanying unaudited interim consolidated financial statements have been prepared in accordance with generally accepted accounting principles in Australia. The financial statements are prepared using the same accounting policies and methods of application as those disclosed in note 3 to the consolidated financial statements for the year ended June 30, 2007, but they do not include all the disclosures required by Australian Accounting Standards for annual financial statements. In addition to these Australian requirements, further information has been included in the Unaudited Interim Consolidated Financial Statements for the nine months ended March 31, 2008 in order to comply with applicable Canadian securities law, as the Company is listed on the Toronto Stock Exchange. Additional information relating to the Company, including the Company’s most recent Annual Report for the year ended June 30, 2007 and other public announcements is available at www.centamin.com. All amounts in this MD&A are expressed in United States dollars unless otherwise identified. FORWARD LOOKING STATEMENTS Some of the statements contained in this MD&A, including those relating to strategies and other statements, are predictive in nature, and depend upon or refer to future events or conditions, or include words such as “expects”, “intends”, “plans”, “anticipates”, “believes”, “estimates” or similar expressions that are forward looking statements. Forward looking statements include, without limitations, the information concerning possible or assumed further results of operations as set forth herein. These statements are not historical facts but instead represent only expectations, estimates and projections regarding future events and are qualified in their entirety by the inherent risks and uncertainties surrounding future expectations generally. The forward looking statements contained in this MD&A are not guarantees of future performance and involve certain risks and uncertainties that are difficult to predict. The future results of the Company may differ materially from those expressed in the forward looking statements contained in this MD&A due to, among other factors, the risks and uncertainties inherent in the business of the Company. The Company does not undertake any obligation to update or release any revisions to these forward looking statements to reflect events or circumstances after the date of this MD&A or to reflect the occurrence of unanticipated events. GENERAL Centamin is a mineral exploration and development company that has been actively exploring in Egypt since 1995. The principal asset of Centamin is its interest in the Sukari Project, located in the eastern desert of Egypt. The Sukari Project is at an advanced stage of development, with construction having commenced in March 2007 and first gold production expected during the first quarter of 2009. The Sukari Project will be the first large-scale modern gold mine to be developed in Egypt. Centamin’s operating experience in Egypt gives it a significant first-mover advantage in acquiring and developing other gold projects in the prospective Arabian-Nubian Shield. A definitive feasibility study (the “DFS”) for the development to commercial production of the Sukari Project was compiled in February 2007 by Roche Process Engineering Pty Ltd. The DFS provides that the capital cost to develop the project is estimated at US$216.5 million (including mining fleet and contingencies but not including the leased mining fleet). According to the DFS, the Sukari Project reserve will be mined by a single open pit over a 15-year period. During that time 78 Mt ore grading 1.5 g/t is expected to be mined, containing 3.7M oz gold. Over this 15-year mining period the project is expected to produce on average 200,000 oz of gold annually at an average cash operating cost of US$290/oz.

CENTAMIN EGYPT LIMITED ____________________________________________________________________________________

Page 17

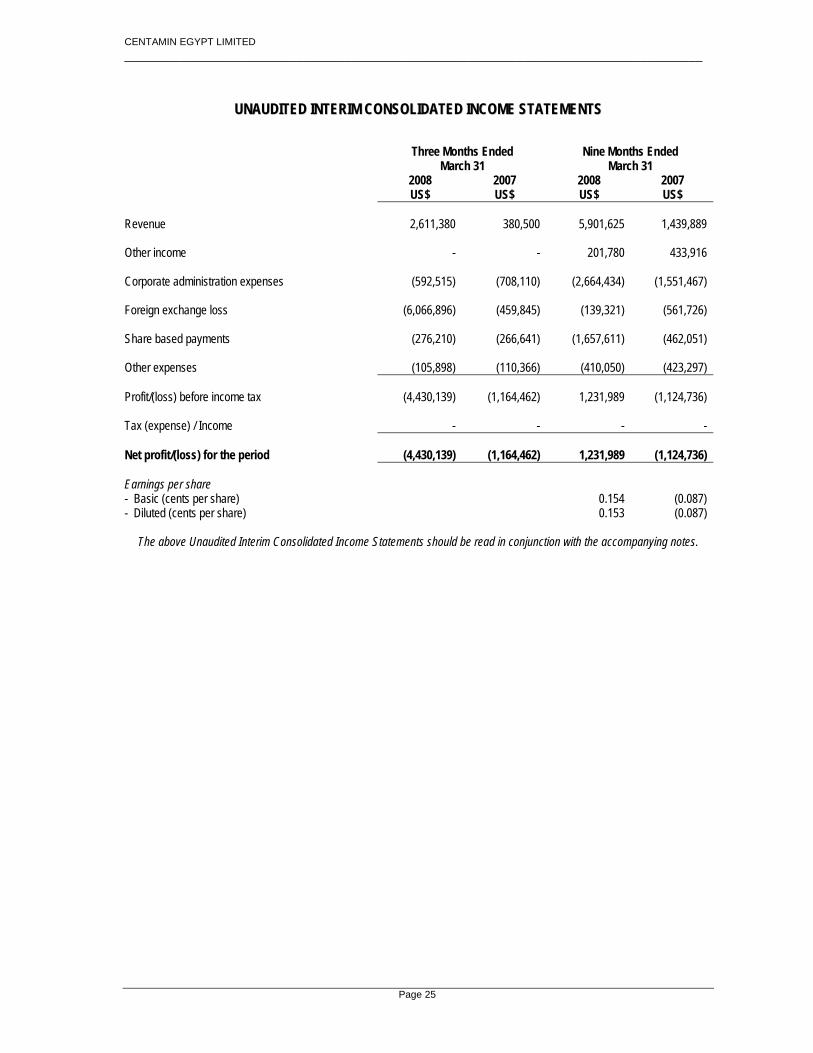

SELECTED FINANCIAL INFORMATION FROM THE UNAUDITED INTERIM CONSOLIDATED INCOME STATEMENTS

Three Months Ended Nine Months Ended March 31 March 31 2008 2007 2008 2007

US$ US$ US$ US$ Revenue 2,611,380 380,500 5,901,625 1,439,889 Other income - - 201,780 433,916 Corporate administration expenses (592,515) (708,110) (2,664,434) (1,551,467) Foreign exchange loss (6,066,896) (459,845) (139,321) (561,726) Share based payments (276,210) (266,641) (1,657,611) (454,659) Other expenses (105,898) (110,366) (410,050) (430,689) Profit/(loss) before income tax (4,430,139) (1,164,462) 1,231,989 (1,124,736) Tax (expense) / Income - - - - Net profit/(loss) for the period (4,430,139) (1,164,462) 1,231,989 (1,124,736) Earnings per share - Basic (cents per share) 0.154 (0.087) - Diluted (cents per share) 0.153 (0.087)

Revenue reported comprises interest revenue applicable on the Company’s available cash and working capital balances and term deposit amounts. On a comparative year to date basis the Revenue figure is significantly higher due to the higher average cash holdings. Other income reported represents an unbudgeted asset sale of minor equipment from the purchase of the Kori Kollo plant in Bolivia deemed not necessary for transportation to Egypt. Corporate administration expenses reported comprise expenditure incurred for communications, consultants, directors’ fees, stock exchange listing fees, share registry fees, employee salaries and general office administration expenses. The year to date amount also includes a once off charge of $926,436 for project debt financing and due diligence fees incurred during the financing process with Barclays Capital. As reported on page 18 the Company has raised the funding for the Sukari project from the equity markets and no longer needs to pursue debt financing discussions with Barclays Capital. Foreign exchange loss reported is attributable to negative exchange rate movements during the period as a result of the strengthening United States dollar against the Canadian dollar. Share based payments reported relate to the requirement to recognise the cost of granting options (or warrants) to directors, company executives, employees under the Employee Share Option Plan or for payment for services done under a contractual arrangement which are subsequently approved at a general meeting of the Company’s shareholders. Calculation of the cost is done under AIFRS over the option (or warrant) vesting period. Other expenses reported comprise non-cash expenses for depreciation and employee entitlements. The loss after tax of the consolidated entity for the three months ended March 31, 2008 was $4,430,139.

CENTAMIN EGYPT LIMITED ____________________________________________________________________________________

Page 18

SELECTED FINANCIAL INFORMATION FROM THE UNAUDITED INTERIM CONSOLIDATED BALANCE SHEETS

March 31, 2008 June 30, 2007 US$ US$

Total current assets 200,546,592 136,735,715 Total non-current assets 152,303,794 81,982,697 Total assets 352,850,386 218,718,412 Total current liabilities 3,740,334 6,367,968 Total non-current liabilities 150,000 150,000 Total liabilities 3,890,334 6,517,968 Net assets 348,960,052 212,200,444 Current assets reported have increased due to the capital raising completed during the quarter ended December 31, 2007. On November 23, 2007 the Company announced that it had sold on a private basis an aggregate of 112,000,000 special warrants at a price of C$1.20 per special warrant for aggregate gross proceeds of C$134,400,000 which includes the exercise in full by the Underwriters of the Underwriters’ option. The net proceeds of this equity financing are to be applied to fund the continued development of the Sukari gold project, underground development, other exploration and general corporate purposes. Non-current assets reported have increased during the period as a result of the expenditure incurred with regard to ongoing exploration resource drilling at Sukari and initial construction activities at Sukari. The Company’s accounting policy is to capitalise expenditure of this nature under the categories of Property, Plant and Equipment and Exploration, Evaluation & Development. Current liabilities reported have decreased during the nine month period due to the final payment in the amount of US$1.7M being made for the acquisition of a second hand power plant in Turkey. Non-current liabilities reported during the period remain unchanged and represent a payment due to a related party upon commencement of gold production from the Sukari project. SELECTED FINANCIAL INFORMATION FROM THE UNADUITED INTERIM CONSOLIDATED STATEMENTS OF CHANGES IN EQUITY

Three Months Ended March 31, 2008

Nine Months Ended March 31, 2008

US$ US$ Total equity at beginning of period 352,273,446 212,200,444 Movement in issued equity (722,634) 134,132,868 Movement in reserves 1,839,379 1,394,751 Profit/(loss) for the period (4,430,139) 1,231,989 Total equity at end of period 348,960,052 348,960,052 Issued equity reported has increased in the nine months ended March 31, 2008 due to the exercise of employee options and the announcement on November 23, 2007 that the Company had sold on a private basis an aggregate of 112,000,000 special warrants at a price of C$1.20 per special warrant for aggregate gross proceeds of C$134,400,000 which includes the exercise in full by the Underwriters of the Underwriters’ option. The decrease in issued equity in the three months ended March 31, 2008 is due to the issue of 5,600,000 share warrants with an exercise price of C$1.29 each and an expiry date of 23 November 2009. These warrants were issued as partial compensation in relation to the capital raising which closed 23 November 2007.

CENTAMIN EGYPT LIMITED ____________________________________________________________________________________

Page 19

Reserves reported comprise two separate and distinct transactions within the reported figure. Firstly there was a share based payment valued under AIFRS over the option (or warrant) vesting period and secondly upon exercise of the option (or warrant) an amount is required under AIFRS to be transferred from the reserve to the issued equity account. Loss for the three months ended March 31, 2008 is analysed under the section Consolidated Income Statement. SELECTED FINANCIAL INFORMATION FROM THE UNAUDITED INTERIM CONSOLIDATED CASH FLOW STATEMENTS

Three Months Ended Nine Months Ended March 31 March 31 2008 2007 2008 2007

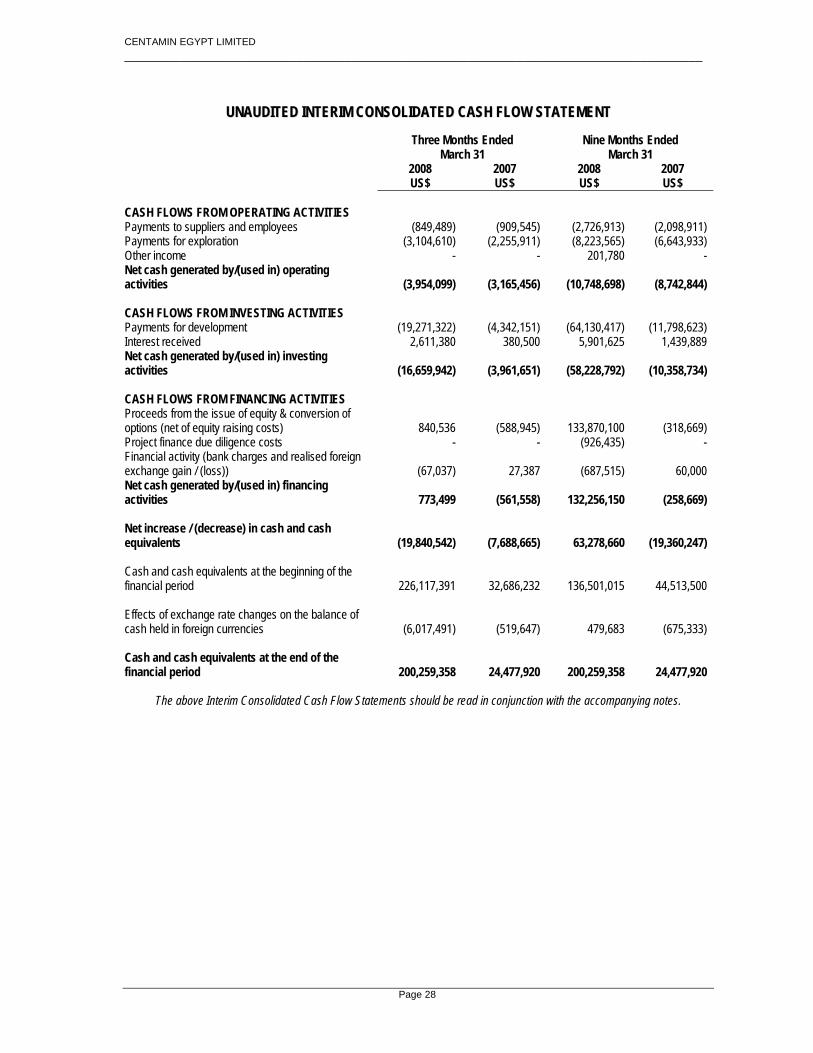

US$ US$ US$ US$ Net cash flow from operating activities (3,954,099) (3,165,456) (10,748,698) (8,742,844) Net cash flow from investing activities (16,659,942) (3,961,651) (58,228,792) (10,358,734) Net cash flow from financing activities 773,499 (561,558) 132,256,150 (258,669) Net increase / (decrease) in cash and cash equivalents (19,840,542) (7,688,665) 63,278,660 (19,360,247) Cash and cash equivalents at the beginning of the financial period 226,117,391 32,686,232 136,501,015 44,513,500 Effects of exchange rate changes (6,017,491) (519,647) 479,683 (675,333) Cash and cash equivalents at the end of the financial period 200,259,358 24,477,920 200,259,358 24,477,920 Net cash flow from operating activities reported comprises payments for corporate salary and wages, corporate administration and compliance, and exploration expenditure costs offset by interest revenue received. On a comparative three month and nine month period basis expenditure is higher due to additional compliance and exploration activity. Net cash flow from investing activities reported comprises preproduction and capital development expenditures at the Sukari project. On a comparative three month and nine month period basis expenditure is significantly higher due to commencement of preproduction and capital development activity which in the same period last year had not yet commenced. Figures reported for the comparative period last year comprised work directed towards completion of the definitive feasibility study into the Sukari project which was completed in February 2007. Net cash flow from financing activities reported comprises funding obtained through the exercise of share options (or warrants) and equity raisings undertaken.

CENTAMIN EGYPT LIMITED ____________________________________________________________________________________

Page 20

FOREIGN INVESTMENT IN EGYPT Foreign investments in the petroleum and mining sectors in Egypt are governed by individual production sharing agreements (concession agreements) between foreign companies and the Ministry for Petroleum and Mineral Resources or EMRA (as the case may be) and are individual Acts of Parliament. Title, exploitation and development rights to the Sukari Project are granted under the terms of the Concession Agreement promulgated as Law No. 222 of 1994, signed on January 29, 1995 and effective from June 13, 1995. The Concession Agreement was issued by way of Presidential Decree after the approval of the People’s Assembly in accordance with the Egyptian Constitution and Law No. 61 of 1958. The Concession Agreement was issued in accordance with the Egyptian Mines and Quarries Law No. 86 of 1956 which allows for the Ministry to grant the right to parties to explore and mine for minerals in Egypt. While the Company will be the first foreign company to develop a modern large-scale gold mine in Egypt there is significant foreign investment in the petroleum sector. Several large multinational oil and gas companies operate successfully in Egypt, some of which have long histories in the country and have dedicated significant amounts of capital. The Company believes that the successful track record of foreign investment established by these companies in the petroleum sector is an important indication of the ability of foreign companies to attract financing and receive development approvals for the construction of major projects in Egypt. OVERVIEW OF SUKARI CONCESSION AGREEMENT Pharaoh Gold Mines NL (PGM) a 100% wholly owned subsidiary of the Company, EGSMA (now EMRA) and the Arab Republic of Egypt (ARE) entered into the Concession Agreement dated January 29, 1995, granting PGM and EMRA the right to explore, develop, mine and sell gold and associated minerals in specific concession areas located in the Eastern Desert of Egypt identified in the Concession Agreement. The Concession Agreement came into effect under Egyptian law on June 13, 1995. The initial term of the Concession Agreement was for one year and was extended by the parties for three two-year periods in accordance with its terms. In accordance with the terms of the Concession Agreement, PGM undertook a feasibility study to support its application to EMRA for a “Commercial Discovery” (within the meaning of the Concession Agreement) with respect to the Sukari Project. On November 9, 2001, EMRA notified PGM that the feasibility submission had demonstrated that a Commercial Discovery had been made at the Sukari Project. As a result, the Concession Agreement was converted from exploration to exploitation status and PGM, together with EMRA, were granted an Exploitation Lease over 160 km2 surrounding the Sukari Project site. The Exploitation Lease was signed by PGM, EMRA and the Egyptian Minister of Petroleum and gives tenure for a period of 30 years, commencing May 24, 2005 and extendable by PGM for an additional 30 years upon PGM providing reasonable commercial justification. The Exploitation Lease will lapse if production of gold is not achieved within 5 years of the signing date. Following demonstration of a Commercial Discovery, PGM and EMRA were required to establish an operating company owned 50% by each party (the “Operating Company”).The Operating Company, named Sukari Gold Mining Company, was incorporated under the laws of Egypt on March 27, 2006. The Operating Company was formed to conduct exploration, development, exploitation and marketing operations in accordance with the Concession Agreement. The registered office of the Operating Company is at 361 El-Horreya Road, Sedi Gaber, Alexandria, Egypt. The ARE is entitled to a royalty of 3% of net sales revenue from the sale of gold and associated minerals from the Sukari Project, payable in cash in each calendar half year. Net sales revenue is calculated by deducting from sales revenue all shipping, insurance, smelting and refining costs, delivery costs not payable by customers, all commercial discounts and all penalties (relating to the quality of gold and associated minerals shipped). Under the Concession Agreement, PGM solely funds the Operating Company but is entitled to recover the following costs and expenses payable from sales revenue (excluding the royalty payable to ARE):

• all current operating expenses incurred and paid after the initial commercial production; • exploration costs, including those accumulated to the commencement of commercial production (at the rate of 33.3%

per annum); and • exploitation capital costs, including those accumulated prior to the commencement of commercial production (at the

rate of 33.3% per annum).

CENTAMIN EGYPT LIMITED ____________________________________________________________________________________

Page 21

Recovery of capital costs shall include interest on a maximum of 50% of investment borrowed from financial institutions not affiliated with PGM provided that PGM shall use best efforts to obtain the most favourable rate of interest, not to exceed LIBOR + 1%. If costs recoverable by PGM exceed the sales revenue (excluding any royalty payable to ARE) in any financial year, the excess is carried forward for recovery in the next financial year or years until fully recovered, but in no case after the termination of the Concession Agreement. After deduction of the royalty payments and recoverable expenses by PGM, the remainder of the sales revenue from the Sukari Project will be shared equally by PGM and EMRA except that for the first and second years in which there are net proceeds for the entire year, an additional 10% of such proceeds will be paid to PGM as an incentive (i.e. 60% to PGM and 40% to EMRA), and for each of the next two years in which there are net proceeds for the entire year, an additional 5% of such proceeds will be paid to PGM (i.e. 55% to PGM and 45% to EMRA). In addition, under the Concession Agreement, certain tax exemptions have been granted, including the following:

• commencing on the date of commercial production, PGM will be entitled to a 15 year exemption from any taxes imposed by the Egyptian government. The parties intend that the Operating Company will in due course file an application to extend the tax-free period for a further 15 years. The extension of tax-free period requires that certain activities in remote areas of the lands under the Concession Area have been programmed and agreed by all parties;

• PGM, EMRA and the Operating Company are exempt from custom taxes and duties with respect to the importation of machinery, equipment and consumable items required for the purpose of exploration and mining activities at the Sukari Project;

• PGM, EMRA, the Operating Company and their respective buyers will be exempt from any duties or taxes on the export of gold and associated minerals produced from the Sukari Project;

• PGM will at all times be free to transfer in US dollars or other freely convertible foreign currency any cash of PGM representing its share of net proceeds and recovery of costs, without any Egyptian government limitation, tax or duty; and

• PGM’s contractors and sub-contractors are entitled to import machinery, equipment and consumable items under the “Temporary Release System” which provides exemption from Egyptian customs duty.

Under the Concession Agreement, all land in the Sukari Project shall be the property of EMRA as soon as it is purchased. The title to the fixed and movable assets are to be transferred by PGM to EMRA as soon as their costs are recovered by PGM, with PGM being entitled to use all fixed and movable assets during the term of the Exploitation Lease and any extensions thereof. In case of national emergency, due to war or imminent expectation of war or internal causes, ARE may requisition all or part of the production from the areas that are the subject of the Concession Agreement, and require the Operating Company to increase production to the utmost extent. ARE may also requisition the mine itself and, if necessary, related facilities. In the event of any requisition, ARE must indemnify EMRA and PGM for the period during which the requisition is maintained. ARE has the right to terminate the Concession Agreement in the following circumstances:

• PGM has knowingly submitted any material false statements to the Egyptian government; • PGM assigns any interest to any unrelated party without the written consent of the Egyptian government; • PGM does not comply with any final decision reached as a result of provisions in the Concession Agreement with

respect to disputes and arbitration; • PGM intentionally extracts any mineral other than gold and associated minerals authorized by the Concession

Agreement without the approval of the Egyptian government; or • PGM commits any material breach of the Concession Agreement.

If the Egyptian government deems that any one of the foregoing causes exists, the government is required to give PGM 90 days’ notice to remedy the defaults. If the default remains unremedied at the expiration of the grace period, the Egyptian government may terminate the Concession Agreement. LIQUIDITY AND CAPITAL RESOURCES The Company’s principal source of liquidity as at March 31, 2008 is cash of $200,259,358 (March 31, 2007 - $24,477,921). Of this amount $193,069,336 has been invested in weekly rolling short term higher interest money market deposits. The reason for the significant change to the cash position is the equity raising completed on November 23, 2007 where it was announced that the Company had sold on a private basis an aggregate of 112,000,000 special warrants at a price of C$1.20 per special warrant for aggregate gross proceeds of C$134,400,000, which includes the exercise in full by the Underwriters of the Underwriters’ option.

CENTAMIN EGYPT LIMITED ____________________________________________________________________________________

Page 22

The net proceeds of this equity financing are to be applied to fund the continued development of the Sukari gold project, underground development, other exploration and general corporate purposes. The following is a summary of the Company’s outstanding commitments as at March 31, 2008: Payments due Total

US$ Less than 1 year

US$ 1 to 5 years

US$ Creditors 3,007,239 3,007,239 -

Total commitments 3,007,239 3,007,239 - The Company’s financial commitments are limited to controllable discretionary spending on work programs at the Sukari Project, administration expenditure at the Egyptian and Australia office locations and for general working capital purposes. The following is a summary of the Company’s estimated cash outflow for the next quarter as at March 31, 2008: Cash outflow Total

US$ Exploration & Evaluation 3,164,091 Corporate Administration 617,755 Preproduction and Sukari Development 45,179,518

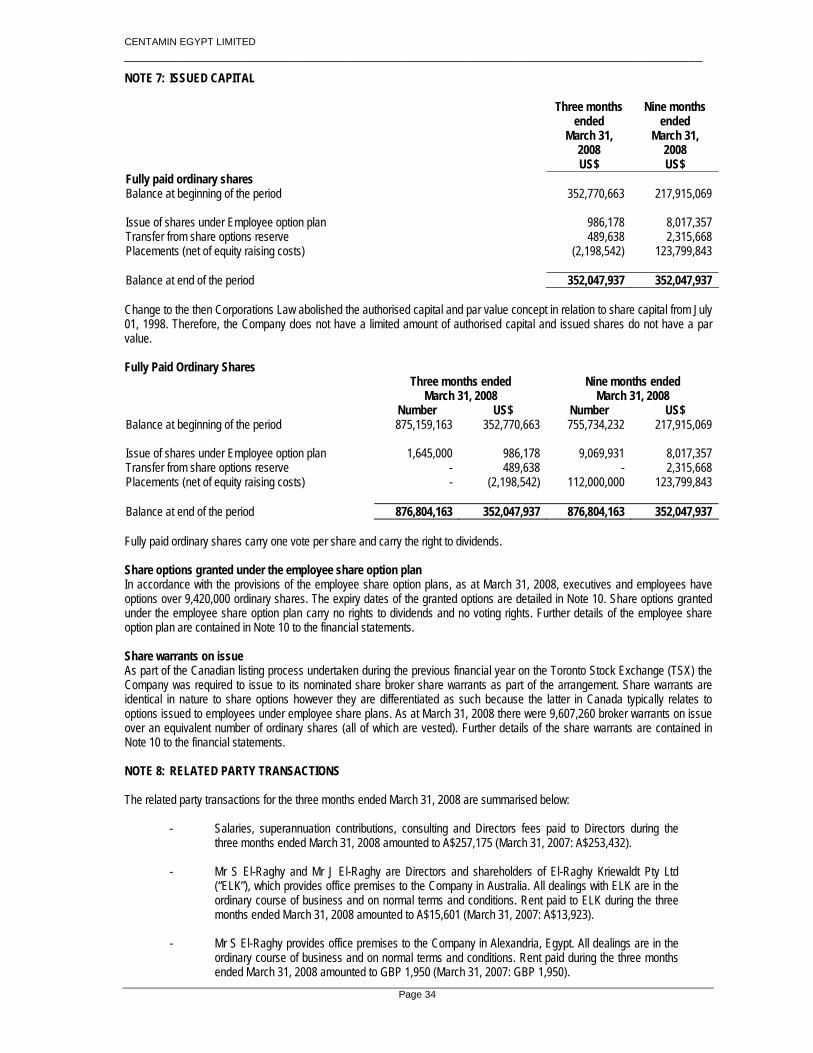

Total commitments 48,961,364 Funding for the Sukari project was completed during the previous quarter with the receipt of funds raised through the equity raising mentioned above. Previously the Company had announced that it had Barclays Capital, the investment banking division of Barclays Bank PLC, as Mandated Lead Arranger to arrange a financing facility of up to US$100M for the Sukari Gold Project. However with the receipt equity funds the need to arrange external project debt finance is no longer required. Other than described above the company has no other off balance sheet arrangements. OUTSTANDING SHARE INFORMATION As at May 12, 2008 the Company had 877,344,163 fully paid ordinary shares issued and outstanding. The following table sets out the fully paid ordinary shares on issue, and the outstanding unquoted options and broker warrants on issue:

As at May 9, 2008 Number Shares on Issue 877,344,163 Options issued but not exercised 12,360,000 Broker Warrants issued but not exercised 9,607,260

899,311,423 SEGMENT DISCLOSURE The Company is engaged in the business of exploration for precious and base metals only, which is characterised as one business segment only. SIGNIFICANT ACCOUNTING ESTIMATES Management is required to make various estimates and judgements in determining the reported amounts of assets and liabilities, revenues and expenses for each period presented and in the disclosure of commitments and contingencies. The significant areas where management uses estimates and judgements in preparing the consolidated financial statements are the determination of carrying values and impaired values of exploration assets.

CENTAMIN EGYPT LIMITED ____________________________________________________________________________________

Page 23

INTERNAL CONTROLS Disclosure controls and procedures are designed to provide reasonable assurance that all relevant information is gathered and reported to management, including the CEO and CFO, on a timely basis so that appropriate decisions can be made regarding public disclosure. Management, with the participation of the certifying officers, has evaluated the effectiveness of the design and operation, as of June 30, 2007, of the Company's disclosure controls and procedures (as defined by the Canadian Securities Administrators). Based on that evaluation, the certifying officers have concluded that such disclosure controls and procedures are effective and designed to ensure that material information relating to the Company and its subsidiaries is known to them by others within those entities. Internal controls over financial reporting are designed to provide reasonable assurance regarding the reliability of our financial reporting and compliance with Canadian generally accepted accounting principles in our financial statements. Management has evaluated the design of internal control over financial reporting and has concluded that such internal controls over financial reporting are designed to provide reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements for external purposes in accordance with generally accepted accounting principles in Canada. In addition, there have been no changes in the Company's internal control over financial reporting during the quarter ended March 31, 2008 that have materially affected, or are reasonably likely to materially affect, its internal control over financial reporting. FINANCIAL INSTRUMENTS At March 31, 2008 the Company has exposure to interest rate risk which is limited to the floating market rate for cash. The Company does not have foreign currency risk for non-monetary assets and liabilities of the Egyptian operations as these are deemed to have a functional currency of United States dollars. The Company has no significant monetary foreign currency assets and liabilities apart from Canadian dollar and United States dollar cash term deposits which are held for the purposes of funding a portion of the mine construction for the Sukari Project. The Company currently does not engage in any hedging or derivative transactions to manage interest rate or foreign currency risks. RELATED PARTY TRANSACTIONS The related party transactions for the three months ended March 31, 2008 are summarised below:

- Salaries, superannuation contributions, consulting and Directors fees paid to Directors during the three months ended March 31, 2008 amounted to A$257,175 (March 31, 2007: A$253,432).

- Mr S El-Raghy and Mr J El-Raghy are Directors and shareholders of El-Raghy Kriewaldt Pty Ltd

(“ELK”), which provides office premises to the Company in Australia. All dealings with ELK are in the ordinary course of business and on normal terms and conditions. Rent paid to ELK during the three months ended March 31, 2008 amounted to A$15,601 (March 31, 2007: A$13,923).

- Mr S El-Raghy provides office premises to the Company in Alexandria, Egypt. All dealings are in the

ordinary course of business and on normal terms and conditions. Rent paid during the three months ended March 31, 2008 amounted to GBP 1,950 (March 31, 2007: GBP 1,950).

- Mr C Cowden, a non-executive director, is also a director and shareholder of Cowden Limited, which

provides insurance broking services to the Company. All dealings with Cowden Limited are in the ordinary course of business and on normal terms and conditions. Amounts paid to Cowden Limited for insurances during the 3 months ended March 31, 2008 amounted to A$34,362 (March 31, 2007: A$14,363).

CENTAMIN EGYPT LIMITED ____________________________________________________________________________________

Page 24

SUBSEQUENT EVENTS Other than as set out above there has not arisen in the interval between the end of the financial period and the date of this report any item, transaction or event of a material and unusual nature likely in the opinion of the Directors of the Company to affect significantly the operations of the company, the results of those operations, or the state of affairs of the Company in subsequent financial periods. The accompanying Interim Consolidated Financial Statements for the quarter ended March 31, 2008 have been prepared in accordance with Australian Equivalents to International Financial Reporting Standards and has not been audited by the Company’s Auditors.

CENTAMIN EGYPT LIMITED ____________________________________________________________________________________

Page 25

UUNNAAUUDDIITTEEDD IINNTTEERRIIMM CCOONNSSOOLLIIDDAATTEEDD IINNCCOOMMEE SSTTAATTEEMMEENNTTSS

Three Months Ended Nine Months Ended March 31 March 31 2008 2007 2008 2007

US$ US$ US$ US$ Revenue 2,611,380 380,500 5,901,625 1,439,889 Other income - - 201,780 433,916 Corporate administration expenses (592,515) (708,110) (2,664,434) (1,551,467) Foreign exchange loss (6,066,896) (459,845) (139,321) (561,726) Share based payments (276,210) (266,641) (1,657,611) (462,051) Other expenses (105,898) (110,366) (410,050) (423,297) Profit/(loss) before income tax (4,430,139) (1,164,462) 1,231,989 (1,124,736) Tax (expense) / Income - - - - Net profit/(loss) for the period (4,430,139) (1,164,462) 1,231,989 (1,124,736) Earnings per share - Basic (cents per share) 0.154 (0.087) - Diluted (cents per share) 0.153 (0.087)

The above Unaudited Interim Consolidated Income Statements should be read in conjunction with the accompanying notes.

CENTAMIN EGYPT LIMITED ____________________________________________________________________________________

Page 26

UUNNAAUUDDIITTEEDD IINNTTEERRIIMM CCOONNSSOOLLIIDDAATTEEDD BBAALLAANNCCEE SSHHEEEETTSS

March 31, 2008 June 30, 2007 US$ US$

CURRENT ASSETS Cash and cash equivalents 200,259,358 136,501,015 Trade and other receivables 27,199 86,893 Inventories - 140,400 Prepayments and deposits 260,035 7,407 Total current assets 200,546,592 136,735,715 NON-CURRENT ASSETS Plant and equipment 11,888,621 12,067,243 Exploration, evaluation and development expenditure – Note 5 140,415,173 69,915,454 Total non-current assets 152,303,794 81,982,697 Total assets 352,850,386 218,718,412 CURRENT LIABILITIES Trade and other accounts payable 3,061,400 5,910,093 Provisions 678,934 457,875 Total current liabilities 3,740,334 6,367,968 NON-CURRENT LIABILITIES Trade and other accounts payable 150,000 150,000 Total non-current liabilities 150,000 150,000 Total liabilities 3,890,334 6,517,968

NET ASSETS 348,960,052 212,200,444 EQUITY Issued Capital – Note 7 352,047,937 217,915,069 Reserves 7,442,491 6,047,740 Accumulated losses (10,530,376) (11,762,365)

TOTAL EQUITY 348,960,052 212,200,444

The above Unaudited Interim Consolidated Balance Sheets should be read in conjunction with the accompanying notes.

CENTAMIN EGYPT LIMITED ____________________________________________________________________________________

Page 27

UUNNAAUUDDIITTEEDD IINNTTEERRIIMM CCOONNSSOOLLIIDDAATTEEDD SSTTAATTEEMMEENNTTSS OOFF CCHHAANNGGEESS IINN EEQQUUIITTYY

Issued

Capital US$

Reserves

US$

Options Reserve

US$

Accumulated Losses

US$

Total US$

At June 30, 2006 94,219,681 2,294,794 440,584 (18,646,792) 78,308,267

Loss for the period - - - (1,124,736) (1,124,736)

Share options exercised 318,376 - - - 318,376

Cost of share based payments - - 454,659 - 454,659

Contributions of equity (1) (637,044) - - - (637,044)

Transfer to retained earnings - - (5,759) (5,759)

At March 31, 2007 93,901,013 2,294,794 895,243 (19,777,287) 77,313,763

At June 30, 2007 217,915,069 2,294,794 3,752,946 (11,762,365) 212,200,444

Profit for the period - - - 1,231,989 1,231,989

Share options exercised 8,017,357 - - - 8,017,357

Cost of share based payments - - 3,710,419 - 3,710,419

Contributions of equity 123,799,843 - - - 123,799,843

Transfer to issued capital 2,315,668 - (2,315,668) - -

At March 31, 2008 352,047,937 2,294,794 5,147,697 (10,530,376) 348,960,052 (1) Contributions of equity is in deficit due to early accrual of equity raising fees associated with the Company’s TSX listing in April 2007. The above Unaudited Interim Consolidated Statement of Changes in Equity should be read in conjunction with the accompanying notes.

CENTAMIN EGYPT LIMITED ____________________________________________________________________________________

Page 28

UUNNAAUUDDIITTEEDD IINNTTEERRIIMM CCOONNSSOOLLIIDDAATTEEDD CCAASSHH FFLLOOWW SSTTAATTEEMMEENNTT

Three Months Ended Nine Months Ended March 31 March 31 2008 2007 2008 2007

US$ US$ US$ US$ CASH FLOWS FROM OPERATING ACTIVITIES Payments to suppliers and employees (849,489) (909,545) (2,726,913) (2,098,911) Payments for exploration (3,104,610) (2,255,911) (8,223,565) (6,643,933) Other income - - 201,780 - Net cash generated by/(used in) operating activities (3,954,099) (3,165,456) (10,748,698) (8,742,844) CASH FLOWS FROM INVESTING ACTIVITIES Payments for development (19,271,322) (4,342,151) (64,130,417) (11,798,623) Interest received 2,611,380 380,500 5,901,625 1,439,889 Net cash generated by/(used in) investing activities (16,659,942) (3,961,651) (58,228,792) (10,358,734) CASH FLOWS FROM FINANCING ACTIVITIES Proceeds from the issue of equity & conversion of options (net of equity raising costs) 840,536 (588,945) 133,870,100 (318,669) Project finance due diligence costs - - (926,435) - Financial activity (bank charges and realised foreign exchange gain / (loss)) (67,037) 27,387 (687,515) 60,000 Net cash generated by/(used in) financing activities 773,499 (561,558) 132,256,150 (258,669) Net increase / (decrease) in cash and cash equivalents (19,840,542) (7,688,665) 63,278,660 (19,360,247) Cash and cash equivalents at the beginning of the financial period 226,117,391 32,686,232 136,501,015 44,513,500 Effects of exchange rate changes on the balance of cash held in foreign currencies (6,017,491) (519,647) 479,683 (675,333) Cash and cash equivalents at the end of the financial period 200,259,358 24,477,920 200,259,358 24,477,920

The above Interim Consolidated Cash Flow Statements should be read in conjunction with the accompanying notes.

CENTAMIN EGYPT LIMITED ____________________________________________________________________________________

Page 29

NNOOTTEESS TTOO TTHHEE UUNNAAUUDDIITTEEDD IINNTTEERRIIMM CCOONNSSOOLLIIDDAATTEEDD FFIINNAANNCCIIAALL SSTTAATTEEMMEENNTTSS

NOTE 1: STATEMENT OF SIGNIFICANT ACCOUNTING POLICIES Nature of Operations, Going Concern and Accounting Policies Statement of Compliance Centamin Egypt Limited (the ‘Company’) and its subsidiaries (collectively ‘the Group’) are engaged in the exploration for precious and base metals located in the eastern desert region of Egypt. The Company was incorporated under the Corporations Law of South Australia on March 24, 1970. These consolidated financial statements have been prepared in accordance with Australian general accepted accounting principles, as applicable to a going concern. Accordingly, they do not give effect to adjustments that would be necessary should the Company be unable to continue as a going concern and therefore be required to realise its assets and liquidate its liabilities and commitments in other than the normal course of business and at amounts different from those in the accompanying consolidated financial statements. The Company has a need for financing for working capital, and the exploration and development of its mineral properties. The Company’s continuance as a going concern is dependent upon its ability to obtain adequate financing and to reach profitable levels of operations. It is not possible to predict whether financing efforts will be successful or if the Company will attain profitable levels of operations. Basis of Preparation The accompanying unaudited interim consolidated financial statements have been prepared in accordance with generally accepted accounting principles in Australia. The financial statements are prepared using the same accounting policies and methods of application as those disclosed in note 3 to the consolidated financial statements for the year ended 30 June 2007, but they do not include all the disclosures required by Australian Accounting Standards for annual financial statements. In the opinion of management, all adjustments considered necessary for fair presentation have been included in these financial statements. Operating results for the nine months ended March 31, 2008 are not necessarily indicative of the results that may be expected for the full year ending June 30, 2008. For further information see the Company’s consolidated financial statements, including notes thereto, for the year ended June 30, 2007. The significant accounting policies which have been adopted in the preparation of these unaudited interim consolidated financial statements are:

(A) ACCOUNTS PAYABLE

Trade payables and other accounts payable are recognised when the consolidated entity becomes obliged to make future payments resulting from the purchase of goods and services.

(B) DEBT AND EQUITY INSTRUMENTS ISSUED BY THE COMPANY

Debt and equity instruments are classified as either liabilities or as equity in accordance with the substance of the contractual arrangement.

(C) EXPLORATION, EVALUATION AND DEVELOPMENT EXPENDITURE Exploration and evaluation expenditures in relation to each separate area of interest are recognised as an exploration and evaluation asset in the year in which they are incurred where the following conditions are satisfied:

i) the rights to tenure of the area of interest are current; and ii) at least one of the following conditions is also met:

a) the exploration and evaluation expenditures are expected to be recouped through successful development and exploration of the area of interest, or alternatively, by its sale: or b) exploration and evaluation activities in the area of interest have not at the reporting date reached a stage which permits a reasonable assessment of the existence or otherwise of economically recoverable reserves, and active and significant operations in, or in relation to, the area of interest are continuing.

CENTAMIN EGYPT LIMITED ____________________________________________________________________________________

Page 30

Exploration and evaluation assets are initially measured at cost and include acquisition of rights to explore, studies, exploration drilling, trenching and sampling and associated activities. General and administrative costs are only included in the measurement of exploration and evaluation costs where they are related directly to operational activities in a particular area of interest. Exploration and evaluation assets are assessed for impairment when facts and circumstances (as defined in AASB 6 “Exploration for and Evaluation of Mineral Resources”) suggest that the carrying amount of exploration and evaluation assets may exceed its recoverable amount. The recoverable amount of the exploration and evaluation assets (or the cash-generating unit(s) to which it has been allocated, being no larger than the relevant area of interest) is estimated to determine the extent of the impairment loss (if any). Where an impairment loss subsequently reverses, the carrying amount of the asset is increased to the revised estimate of its recoverable amount, but only to the extent that the increased carrying amount does not exceed the carrying amount that would have been determined had no impairment loss been recognised for the asset in previous years. Where a decision is made to proceed with development in respect of a particular area of interest, the relevant exploration and evaluation asset is tested for impairment, reclassified to development properties, and then amortised over the life of the reserves associated with the area of interest once mining operations have commenced.

(D) FOREIGN CURRENCY

All foreign currency transactions during the period have been brought to account using the exchange rate in effect at the date of the transaction. Foreign currency monetary items at balance date are translated at the exchange rate existing at that date.

Non-monetary assets and liabilities carried at fair value that are denominated in foreign currencies are translated at the rates prevailing at the date when the fair value was determined. All exchange differences are brought to account in the interim consolidated income statement in the financial period in which they arise.

(E) GOODS AND SERVICES TAX Revenues, expenses and assets are recognised net of the amount of goods and services tax (GST), except:

i. Where the amount of GST incurred is not recoverable from the taxation authority, it is recognised as part of the cost of acquisition of an asset or as part of an item of expense; or ii. For receivables and payables which are recognised inclusive of GST.

The net amount of GST recoverable from, or payable to, the taxation authority is included as part of receivables or payables.

(F) IMPAIRMENT OF ASSETS (OTHER THAN EXPLORATION AND EVALUATION)

At each reporting date, the consolidated entity reviews the carrying amounts of its tangible and intangible assets to determine whether there is any indication that those assets have suffered an impairment loss. If any such indication exists, the recoverable amount of the asset is estimated in order to determine the extent of the impairment loss (if any). Where the asset does not generate cash flows that are independent from other assets, the consolidated entity estimates the recoverable amount of the cash-generating unit to which the asset belongs.

Recoverable amount is the higher of fair value less costs to sell and value in use. In assessing value in use, the estimated future cash flows are discounted to their present value using a pre-tax discount rate that reflects current market assessment of the time value of money and the risks specific to the asset for which the estimates of future flows have not been adjusted.

If the recoverable amount of an asset (or cash-generating unit) is estimated to be less than its carrying amount, the carrying amount of the asset (cash-generating unit) is reduced to its recoverable amount. Each cash generated unit is determined on an area of interest basis.

Where an impairment loss subsequently reverses, the carrying amount of the asset (cash-generating unit) is increased to the revised estimate of its recoverable amount, but only to the extent that the increased carrying amount does not exceed the carrying amount that would have been determined had no impairment loss been recognised for the asset (cash generating unit) in prior years.

(G) LOANS AND RECEIVABLES

Trade receivables, loans, and other receivables are recorded at amounts due less any allowance for doubtful debts.

CENTAMIN EGYPT LIMITED ____________________________________________________________________________________

Page 31

(H) PLANT AND EQUIPMENT

Plant and equipment, and equipment under finance lease are stated at cost less accumulated depreciation and impairment. Plant and equipment will include capitalised development expenditure. Cost includes expenditure that is directly attributable to the acquisition of the item as well as the estimated cost of abandonment. In the event that settlement of all or part of the purchase consideration is deferred, cost is determined by discounting the amounts payable in the future to their present value as at the date of acquisition.

Depreciation is provided on plant and equipment. Depreciation of capitalised development expenditure will be provided on a unit of production basis over recoverable reserves, whilst on other fixed assets are calculated on a straight line basis so as to write off the cost or other re-valued amount of each asset over its expected useful life to its estimated residual value. The estimated useful lives, residual values and depreciation method are reviewed at the end of each annual reporting period. The following estimated useful lives are used in the calculation of depreciation: Plant & Equipment & Office Furniture - 4-10 years Motor Vehicles - 2 -8 years (I) PRINCIPLES OF CONSOLIDATION

The consolidated financial statements are prepared by combining the financial statements of all the entities that comprise the consolidated entity, being the company (the parent entity) and its subsidiaries as defined in Accounting Standard AASB 127 “Consolidated and Separate Financial Statements”. Consistent accounting policies are employed in the preparation and presentation of the consolidated financial statements.