third quarter accounting & tax update - kpmg€¦ · october 5, 2017. welcome murray suey....

TRANSCRIPT

Third Quarter Accounting & Tax UpdateCalgary, AB

—

October 5, 2017

Welcome

Murray SueyRegional Managing Partner

3© 2017 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

Agenda— IFRS standards update

— Climate risk disclosure

— Impairment

— US update

— Private company tax reform

— US tax reform

— Cyber security

New Partner announcement

Jassie KangPartner, Audit

Stephanie PankratzPartner, Audit

Kevin MoodyPartner, Advisory (MC)

Laura RiveroPartner, Enterprise Audit

IFRS standards update

Reinier DeurwaarderPartner, Audit

6© 2017 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

IFRS standards update— IFRS 9 Financial Instruments – January 1, 2018

— IFRS 15 Revenue from contracts with Customers – January 1, 2018

— IFRS 16 Leases – January 1, 2019

— IFRS 17 Insurance – January 1, 2021

— IFRIC 22 Foreign Currency Translation – Advance Consideration – January 1, 2018

— IFRIC 23 Uncertainty over Income Tax treatments – January 1, 2019

— Income Tax: Interest and Penalties (IFRIC)

— Definition of Material – Exposure Draft feedback by January 15, 2018

— Accounting Policies and Estimates – Exposure Draft feedback by January 15, 2018

7© 2017 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

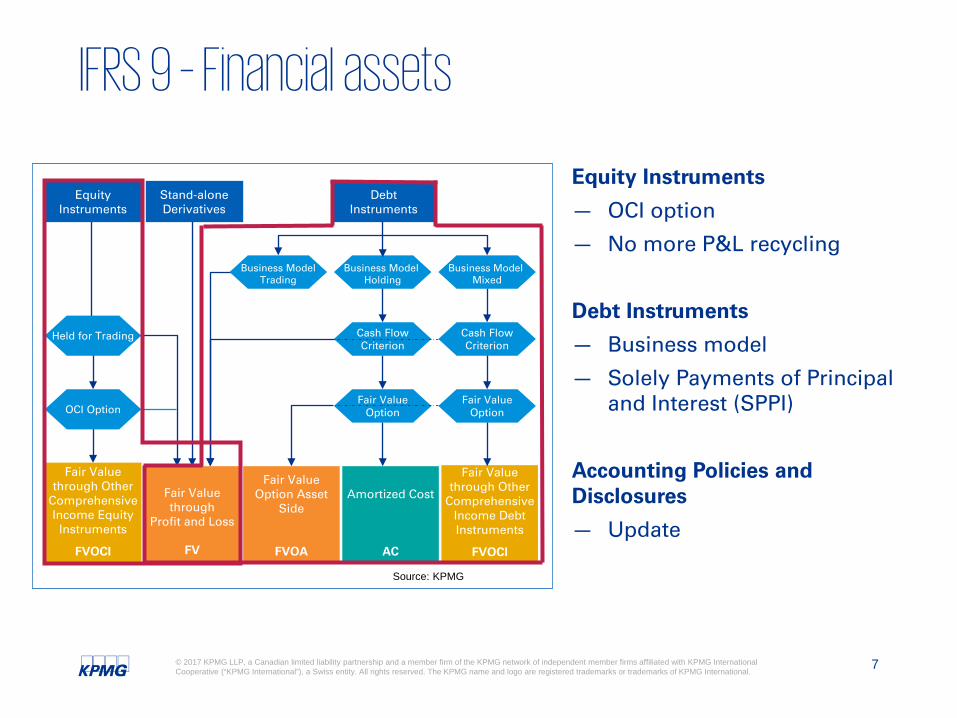

IFRS 9 – Financial assets

Equity Instruments

— OCI option

— No more P&L recycling

Debt Instruments

— Business model

— Solely Payments of Principal and Interest (SPPI)

Accounting Policies and Disclosures

— Update

Fair Value Option Asset

Side

FVOA

Fair Value through Other

Comprehensive Income Debt Instruments

FVOCI

DebtInstruments

Business Model Holding

Business Model Mixed

Cash FlowCriterion

Fair ValueOption

Amortized Cost

AC

Cash FlowCriterion

Stand-aloneDerivatives

Equity Instruments

Held for Trading

OCI OptionFair Value

Option

Business ModelTrading

Fair Value through Other

Comprehensive Income Equity

Instruments

FVOCI

Fair Value through

Profit and Loss

FV

Source: KPMG

8© 2017 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

IFRS 9 – Debt modification

— Current accounting

— Adjust directly attributable costs against the carrying amount of the loan:

— Dr. Loan 5,000

— Cr. Cash 5,000

— The costs are then amortized over the remainder of the life of the loan.

— No immediate P&L impact.

— IFRS 9 accounting

— Record the change in NPV – based on original effective interest rate – against income:

— Dr. Loan 6,000

— Cr. Cash 5,000

— Cr. Finance gain 1,000

In 2012, Company A entered into a $100,000 loan with a bank. At the end of 2016, as a result of decreasing results, Company A successfully renegotiated the covenants for the loan, for which $5,000 of costs were incurred, and extended the maturity date of the loan from 2025 to 2026. The changes to the terms of the loan were concluded to be non-substantial, but reduced the NPV of the loan from $91,500 to $90,500 (based on original effective interest rate).

Different from current

practice under IAS 39

9© 2017 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

IFRS 15 performance obligations

Contract: Provide drilling services to Customer A to drill a well.

Performance obligations identified:

— Drilled well

— Drilling

— People, equipment.

Revenue recognition:

Distinct performance obligation

Not distinct – combine with other goods and services

Capable of being distinct

Can the customer benefit from the good or service either on its own

or together with other resources that are

readily available to the customer?

Distinct within context of the

Contract

Is the promise to transfer the good or service separately

identifiable from other promises in the

contract?

+

Yes No

A performance obligation (PO) is a promise to deliver a good or service that meets both the following criteria

PO Recognize revenue

Drilled well When well has been drilled

Drilling Per day/ft drilling

Source: KPMG

10© 2017 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

IFRS 15 – Over time assessment

Company A builds service equipment. Construction only starts after customers place their order, which specifies several characteristics of the equipment to be build. The billing schedule allows Company A to bill in advance, and will ensure that the amounts billed exceed costs incurred by at least 10%.

Situation 1 – the customer specific details will make that the equipment cannot be used by other companies without making extensive modifications to the equipment.

Situation 2 – the contract details clarify the choices customers have made from several available options.

Customer simultaneously receives and consumes the benefits as the entityperforms

The customer controls the asset as the entity creates or enhances it

Entity’s performance does not create an asset for which the entity has an alternate use and there is a right to payment for performance completed to date

A performance obligation is satisfied over time if one of the following criteria are met:

Service Contract

Asset built on customer’s

site

Asset built to order

11© 2017 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

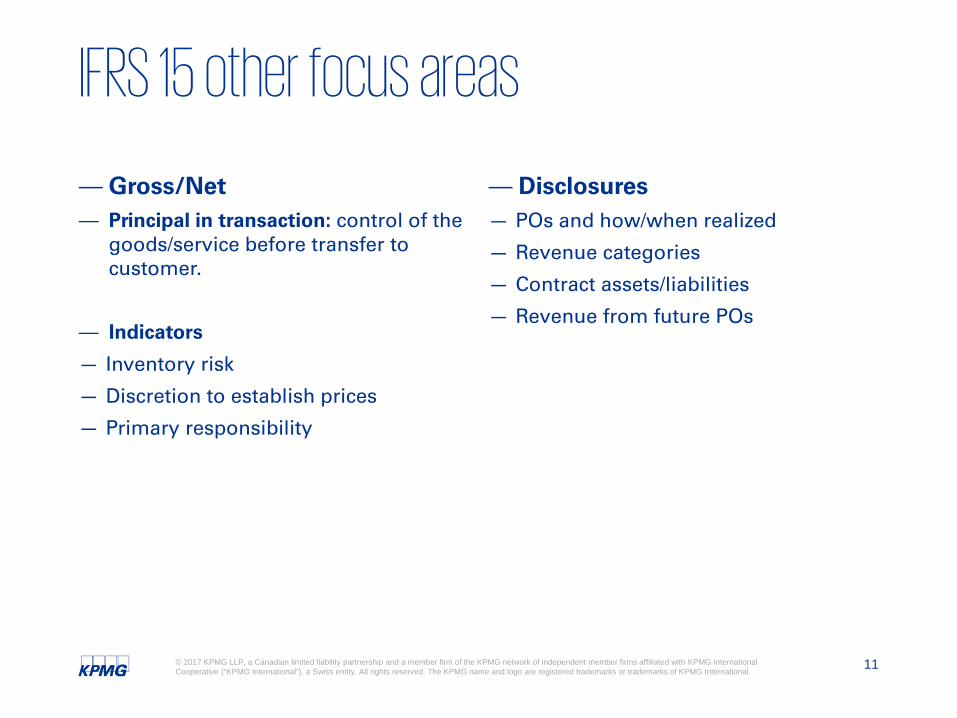

IFRS 15 other focus areas

— Gross/Net— Principal in transaction: control of the

goods/service before transfer to customer.

— Indicators

— Inventory risk

— Discretion to establish prices

— Primary responsibility

— Disclosures— POs and how/when realized

— Revenue categories

— Contract assets/liabilities

— Revenue from future POs

Climate riskdisclosure

Sander JansenManager, Audit

13© 2017 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

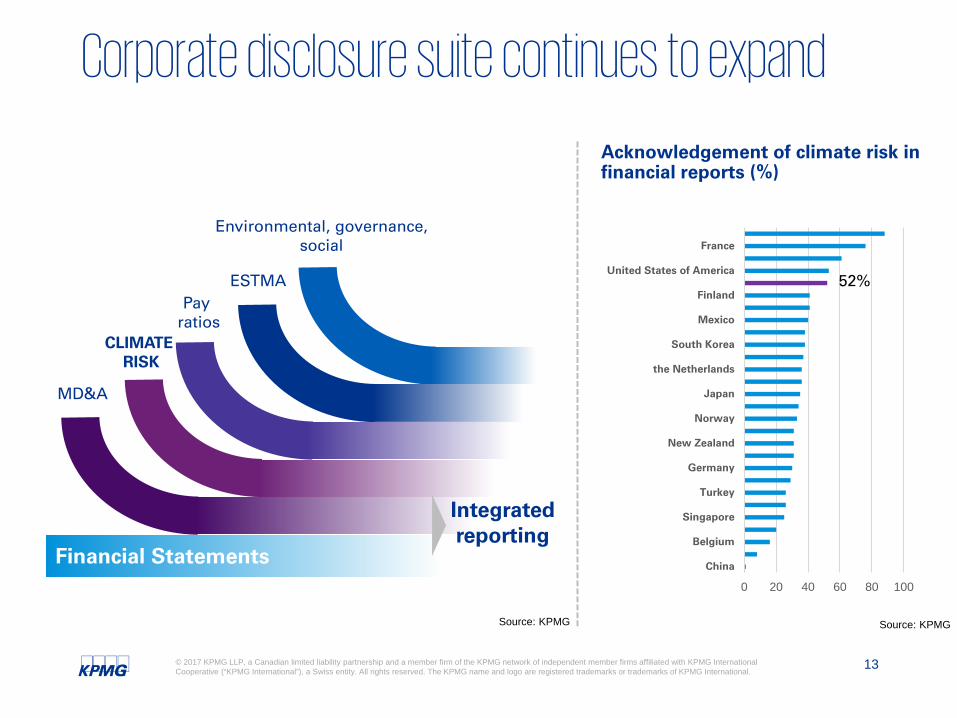

MD&A

Environmental, governance,social

CLIMATE RISK

ESTMAPay

ratios

Financial Statements

Integrated reporting

0 20 40 60 80 100

China

Belgium

Singapore

Turkey

Germany

New Zealand

Norway

Japan

the Netherlands

South Korea

Mexico

Finland

United States of America

France

Acknowledgement of climate risk in financial reports (%)

52%

Corporate disclosure suite continues to expand

Source: KPMG Source: KPMG

14© 2017 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

Drivers for climate risk disclosure

REGULATIONS INVESTORS

Climate change regulations in Alberta and around the world are gathering pace –becoming more stringent and covering more sectors.

Growing investor demand for climate disclosures to de-risk investment portfolio.

1. Carbon Pricing 3. Phasing out coal

2. Capping oil sands emissions

4. Reducing methane emissions

Source: CBC News

Headline: Suncor investors approve more climate disclosure

15© 2017 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

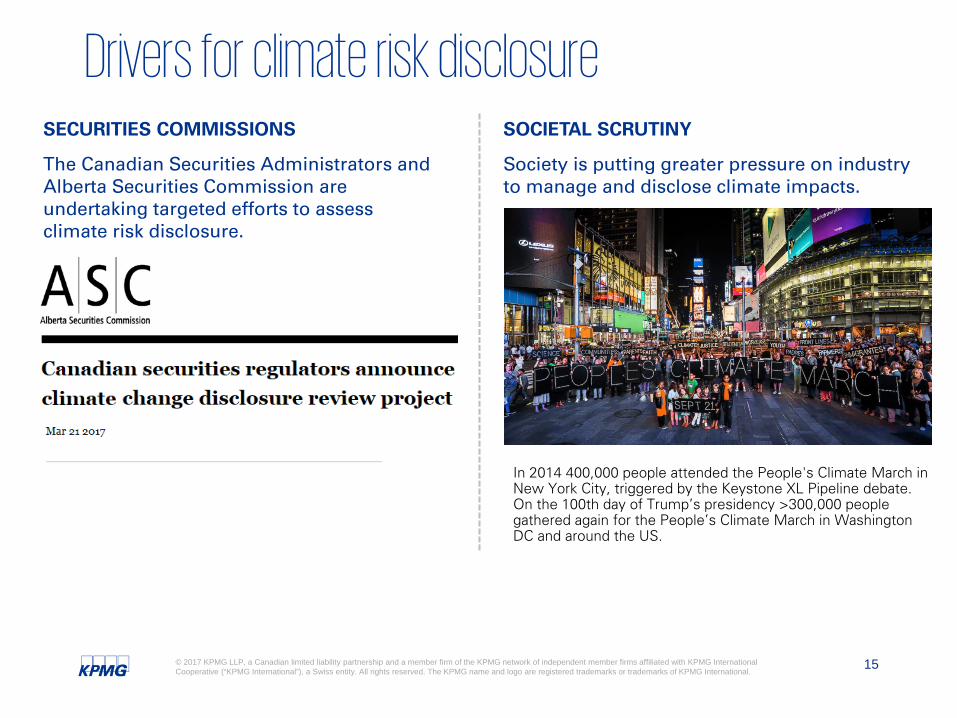

Drivers for climate risk disclosureSECURITIES COMMISSIONS SOCIETAL SCRUTINY

The Canadian Securities Administrators and Alberta Securities Commission are undertaking targeted efforts to assess climate risk disclosure.

Society is putting greater pressure on industry to manage and disclose climate impacts.

In 2014 400,000 people attended the People's Climate March in New York City, triggered by the Keystone XL Pipeline debate. On the 100th day of Trump’s presidency >300,000 people gathered again for the People’s Climate March in Washington DC and around the US.

16© 2017 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

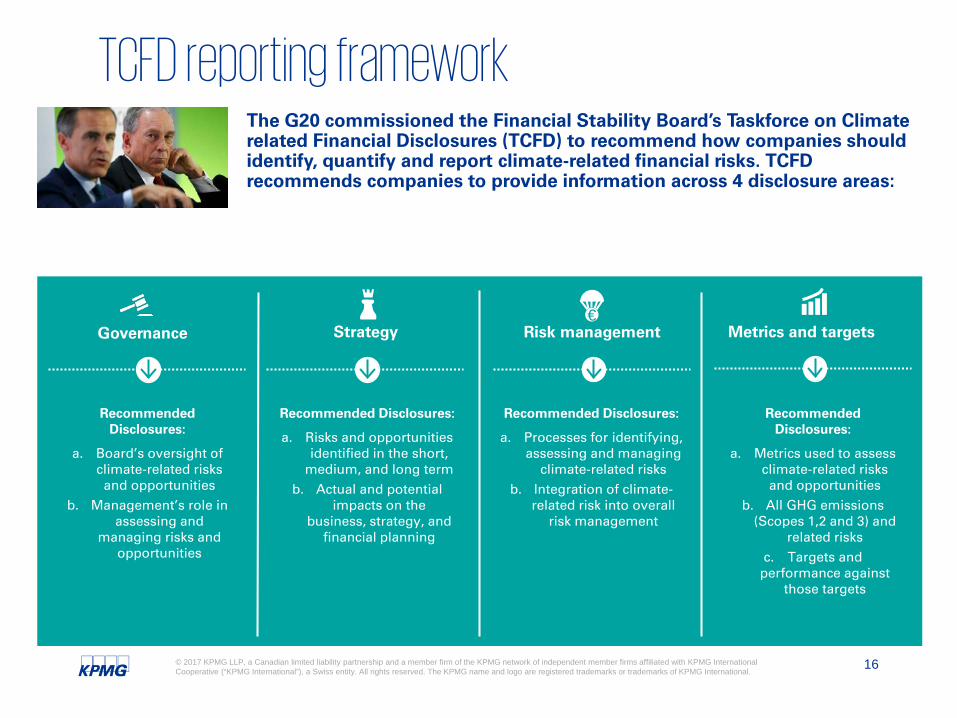

Recommended Disclosures:

a. Board’s oversight of climate-related risks and opportunities

b. Management’s role in assessing and

managing risks and opportunities

Recommended Disclosures:

a. Risks and opportunities identified in the short,

medium, and long termb. Actual and potential

impacts on the business, strategy, and

financial planning

Recommended Disclosures:

a. Processes for identifying, assessing and managing

climate-related risksb. Integration of climate-

related risk into overall risk management

Recommended Disclosures:

a. Metrics used to assess climate-related risks and opportunities

b. All GHG emissions (Scopes 1,2 and 3) and

related risksc. Targets and

performance against those targets

Governance Strategy Risk management Metrics and targets€

TCFD reporting frameworkThe G20 commissioned the Financial Stability Board’s Taskforce on Climate related Financial Disclosures (TCFD) to recommend how companies should identify, quantify and report climate-related financial risks. TCFD recommends companies to provide information across 4 disclosure areas:

17© 2017 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

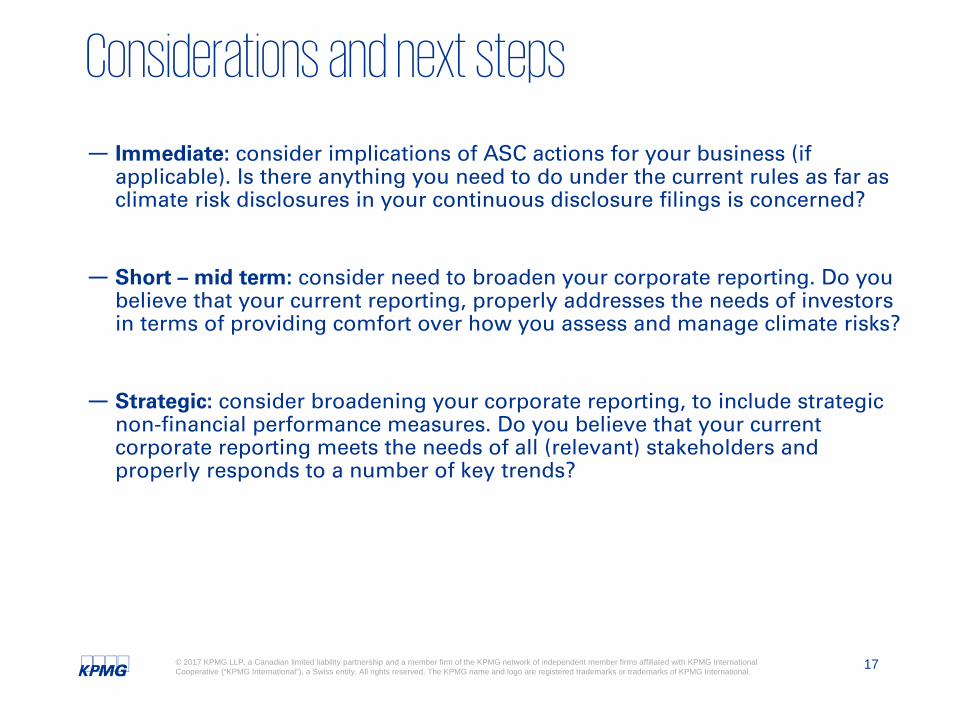

Considerations and next steps

— Immediate: consider implications of ASC actions for your business (if applicable). Is there anything you need to do under the current rules as far as climate risk disclosures in your continuous disclosure filings is concerned?

— Short – mid term: consider need to broaden your corporate reporting. Do you believe that your current reporting, properly addresses the needs of investors in terms of providing comfort over how you assess and manage climate risks?

— Strategic: consider broadening your corporate reporting, to include strategic non-financial performance measures. Do you believe that your current corporate reporting meets the needs of all (relevant) stakeholders and properly responds to a number of key trends?

Impairment

Shane DoigPartner, Audit

19© 2017 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

Impairment or no impairment – that is the question— Are we seeing impairments at Q3 in the O&G producers?

— Winter drilling programs

— “System” wide impairments – not expected at this time

— Very similar facts and circumstances to prior three quarters

— Continue to keep an eye out for underperforming assets or CGU’s

US update

Imam HasanPartner, Audit

21© 2017 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

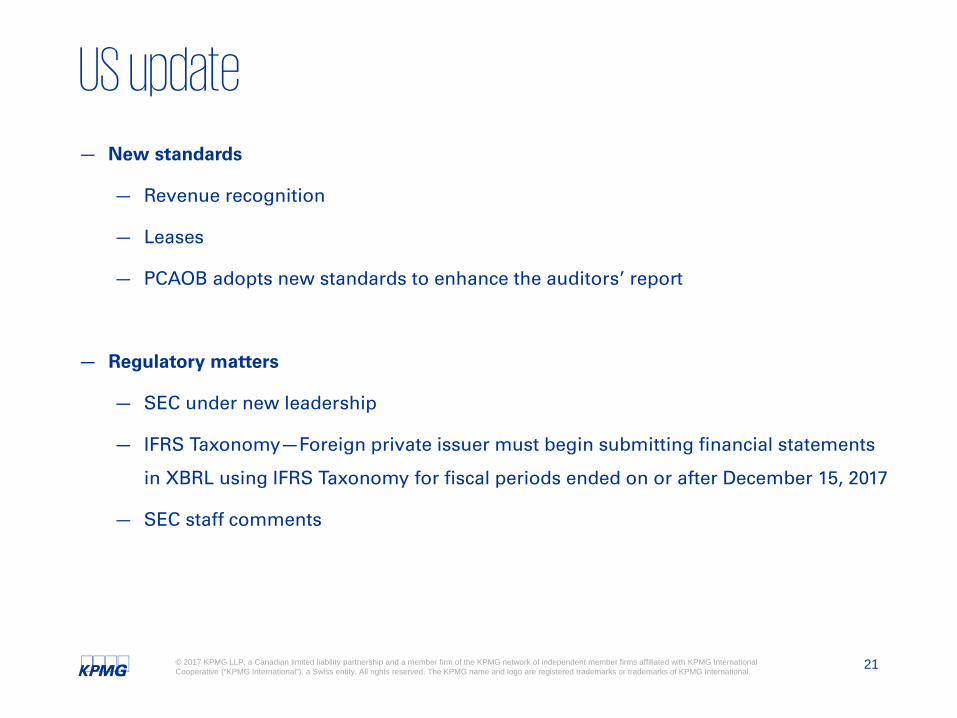

US update— New standards

— Revenue recognition

— Leases

— PCAOB adopts new standards to enhance the auditors’ report

— Regulatory matters

— SEC under new leadership

— IFRS Taxonomy—Foreign private issuer must begin submitting financial statements

in XBRL using IFRS Taxonomy for fiscal periods ended on or after December 15, 2017

— SEC staff comments

Private companytax reform

Marcello D’EgidioPartner, Enterprise tax

23© 2017 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

Private company tax reform - Tax on split income (“TOSI”)— More types of income of family members will be subject to highest tax rate (formerly

“kiddie tax”)

— Any Canadian resident including a trust, regardless of age, can be caught

— Related individuals definition is greatly expanded

— Affected individuals are those “related” to shareholder who has influence

— Elimination of most income splitting opportunities if not actively involved in business

— Greater “reasonableness” test threshold for individuals aged 18 – 24

24© 2017 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

Private company tax reform - Capital gains exemption— Minors (under 18) and gains accrued while a minor – no longer eligible

— If property subject to new Tax on Split Income – no longer eligible

— Gains accrued before distribution from a family trust – no longer eligible

— Transitional rules – potential to file election to realize a gain in 2018

— Potentially costly – need for valuations and payment of AMT

— No “grandfathering” for existing family trust arrangements

25© 2017 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

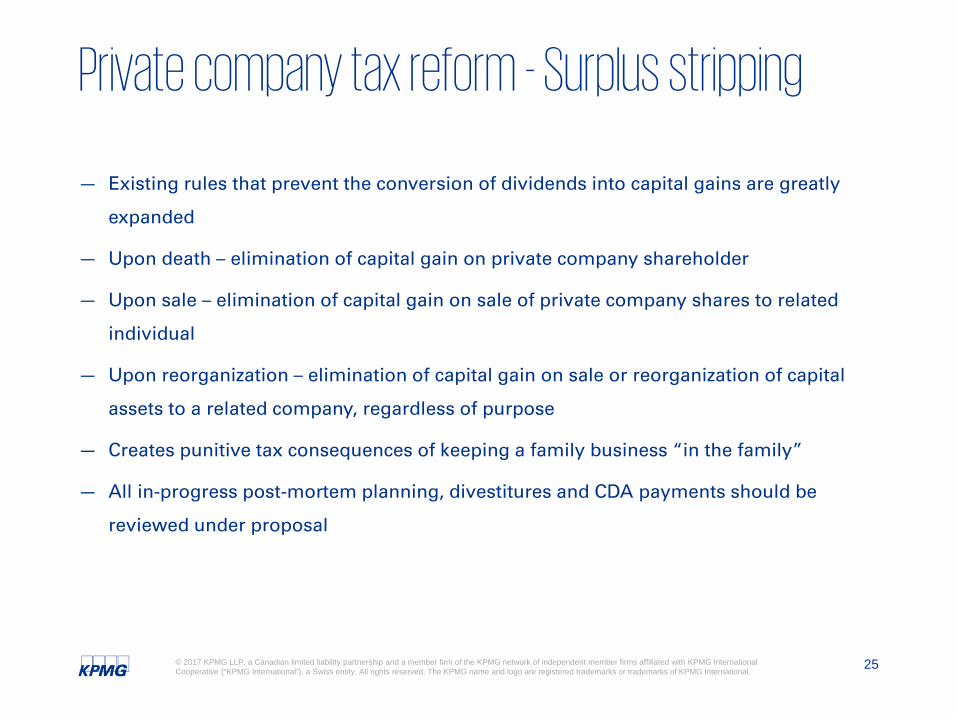

Private company tax reform - Surplus stripping

— Existing rules that prevent the conversion of dividends into capital gains are greatly

expanded

— Upon death – elimination of capital gain on private company shareholder

— Upon sale – elimination of capital gain on sale of private company shares to related

individual

— Upon reorganization – elimination of capital gain on sale or reorganization of capital

assets to a related company, regardless of purpose

— Creates punitive tax consequences of keeping a family business “in the family”

— All in-progress post-mortem planning, divestitures and CDA payments should be

reviewed under proposal

26© 2017 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

Private company tax reform - Passive income

— Affects corporations that do not distribute or reinvest after-tax earnings but rather invest

in passive assets

— Due to the low tax rates, corporations start with larger after-tax pool for investment when

compared to income earned at the individual level

— Finance is considering three alternatives:

(1) Apportionment Method – tracking after-tax income in three separate pools

(2) Elective Method – avoids tracking requirements; income subject to “default

treatment”

(3) Corporations focused on passive investments – all income may be taxed as passive

income.

US tax reform

Kathy WangSenior Manager, US tax

28© 2017 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

US tax reform – “Now”— “Unified Framework for Fixing Our Broken Tax Code” was issued on September 27, 2017

— The Framework is generally consistent with President Trump’s “four principles” of tax reform discussed in his speeches given in late August and early September:

— the tax code should be simple, fair and easy to understand

— the tax code should be competitive and create more jobs and higher wages for Americans

— there must be tax relief for middle class families

— offshore wealth should be repatriated to the United States.

“It is now time for all members of Congress — Democrat, Republicanand Independent — to support pro-American tax reform. It’s time

for Congress to provide a level playing field for our workers, to bringAmerican companies back home, to attract new companies and businesses

to our country, and to put more money into the pockets of everydayhardworking people.” – President Donald J. Trump

29© 2017 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

US tax reform – “Then”

Moving from an income tax to a consumption tax

— Intended to be revenue neutral— Lower rate – 20%— Immediate expensing— No deduction for net interest expense— Disallowance of management fee deduction

— Territorial taxation

— Border adjustability feature

— General Features— Wages Remain Deductible — Cash Method Accounting— NOLs

— Not carried back— Carried forward indefinitely— Indexed for inflation— Can offset only 90% of taxable

income in a given year— Taxes on “Financial Receipts,” including

income from dividends, interest, derivatives, and qualifying hedges?

The House Blueprint

Barebones outline and fluid concepts

— Lower rate – 15%

— Election to expense or can retain interest deduction

— International business taxation

— Early support for a worldwide tax system

— 15% rate

— FTCs allowed

— Then focused on taxes/tariffs on “round tripped” imports

— Ambiguous reaction to the Blueprint’s border adjustability feature

— Consistent support for a transition tax – 10% Rate

— Potential Revenue Shortfall?

The Trump Plan

Source: KPMG from US Department of the Treasury

30© 2017 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

The framework in general

— To reduce the corporate tax rate to 20%

— Aims to eliminate the corporate AMT

— “Immediate write-off” of the cost of depreciable assets “other than structures”

— A “partial limit” to the deduction of net interest expense by C corporations

— Repealing or restricting “special exclusions and deductions” – “section 199” deduction would be eliminated

— Specific “tax incentives” may be preserved

31© 2017 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

The framework in general (continued)

— On the international side, the Framework proposes to adopt a “territorial system”

— The Framework also provides that it would tax the foreign profits of U.S. multinational corporations, albeit at a reduced rate.

32© 2017 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

The framework in general (continued)

— On the international side, the Framework proposes to adopt a “territorial system”

— The Framework also provides that it would tax the foreign profits of U.S. multinational corporations, albeit at a reduced rate

Cyber security

Ivan AlcoforadoSenior Manager, Cyber security

34© 2017 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

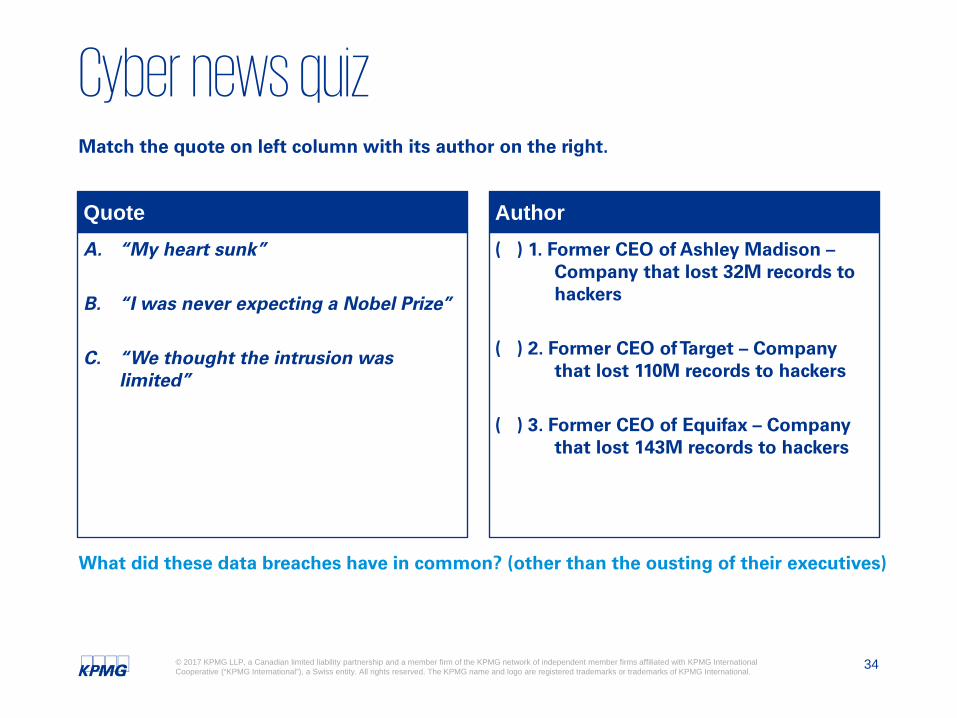

Cyber news quizMatch the quote on left column with its author on the right.

What did these data breaches have in common? (other than the ousting of their executives)

A. “My heart sunk”

B. “I was never expecting a Nobel Prize”

C. “We thought the intrusion was limited”

Quote( ) 1. Former CEO of Ashley Madison –

Company that lost 32M records to hackers

( ) 2. Former CEO of Target – Company that lost 110M records to hackers

( ) 3. Former CEO of Equifax – Company that lost 143M records to hackers

Author

35© 2017 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

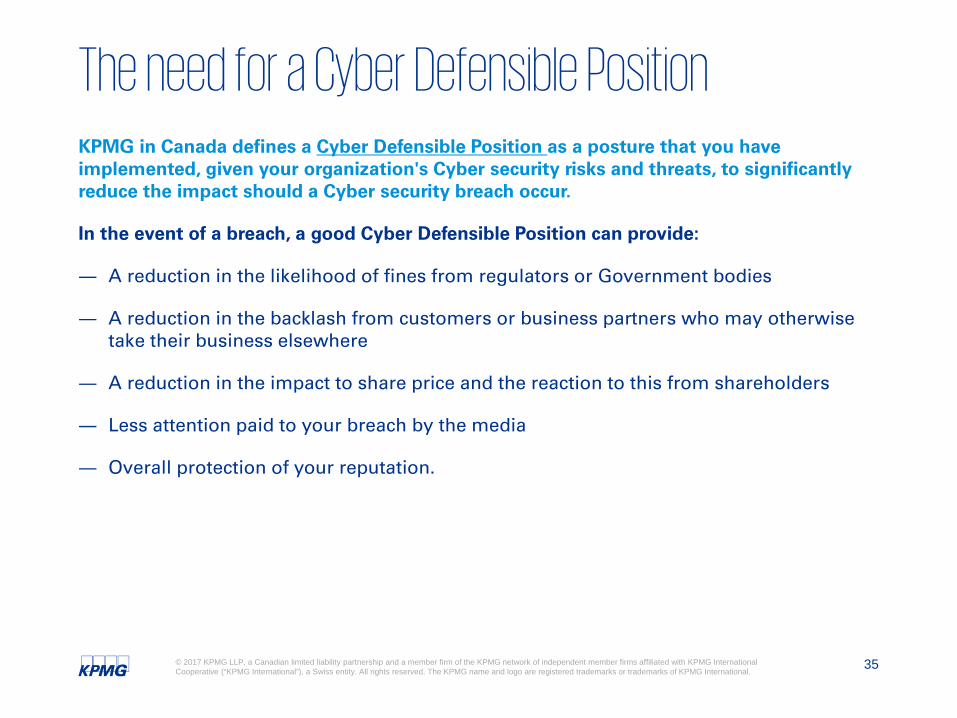

The need for a Cyber Defensible PositionKPMG in Canada defines a Cyber Defensible Position as a posture that you have implemented, given your organization's Cyber security risks and threats, to significantly reduce the impact should a Cyber security breach occur.

In the event of a breach, a good Cyber Defensible Position can provide:

― A reduction in the likelihood of fines from regulators or Government bodies

― A reduction in the backlash from customers or business partners who may otherwise take their business elsewhere

― A reduction in the impact to share price and the reaction to this from shareholders

― Less attention paid to your breach by the media

― Overall protection of your reputation.

36© 2017 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

The need for a cyber defensible positionThere are a number of steps to take for achieving a good Cyber Defensible Position.

The following figure takes each of these in turn and summarizes the typical inputs, phase, status output and usual actions to take:

Board Question Step Defensible Position Status

KPMG Cyber Services Framework

1. What are the new cybersecurity threats and risks and how do they affect our organization?

Risk Assessment None

2. Is our organization’s cybersecurity program ready to meet the challenges of today’s (and tomorrow’s) cyber threat landscape?

Capability Assessment and Security Testing

Defined

3. What key risk indicators should I be reviewing at the executive management and board levels to perform effective risk management in cyber security?

Cyber Security Strategy and Program

Plan Created

Execute and verify progress (ongoing) AchievedDETECT & RESPONDHelps clients respond to and investigate cyber attacks.

PROTECTHelps clients design and implement their cyber defence infrastructure.

PREPAREHelps clients understand their vulnerabilities and improve their preparedness against cyber attack.

Source: KPMG

37© 2017 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

What would make us a headline?Impact versus Assets

Industrial Systems

Unauthorized use or disruption

Safety, Business Interruption and Environment

Business StrategyUnauthorized access or copy

Financial Impact of loss of Business or Opportunities

Financial Data

Fraudulent wire transfers

Direct Financial impact

Personal Data

Unauthorized access or copy

Impact on Reputation and Employee Relations

Intellectual Property

Unauthorized access or copy

Financial impact of loss of competitive advantage

Restricted Data

Unauthorized access or copy

Reputation impact if data on sensitive areas is breached

Source: KPMG

38© 2017 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

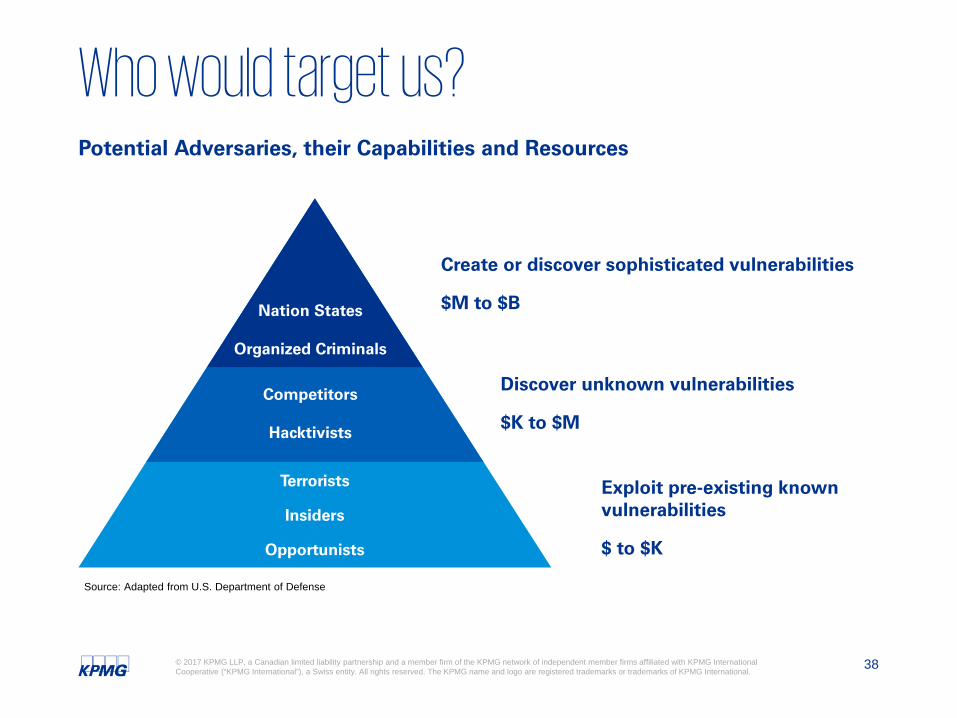

Who would target us?Potential Adversaries, their Capabilities and Resources

Nation States

Organized Criminals

Competitors

Hacktivists

Terrorists

Insiders

Opportunists

Source: Adapted from U.S. Department of Defense

Create or discover sophisticated vulnerabilities

$M to $B

Discover unknown vulnerabilities

$K to $M

Exploit pre-existing known vulnerabilities

$ to $K

39© 2017 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

Before we underestimate our adversariesA story on capability migration

1. Equation Group, a supposedly NSA-funded hacking group was allegedly hacked.

2. Shadow Brokers, another hacker group attempts to auction and later release captured Equation Group tools for free.

3. WannaCry ransomware affects millions worldwide, including the NHS in the UK, leveraging an Equation Group vulnerability.

Source: The Guardian

Source: The Guardian

Source: NSA and Kaspersky

40© 2017 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

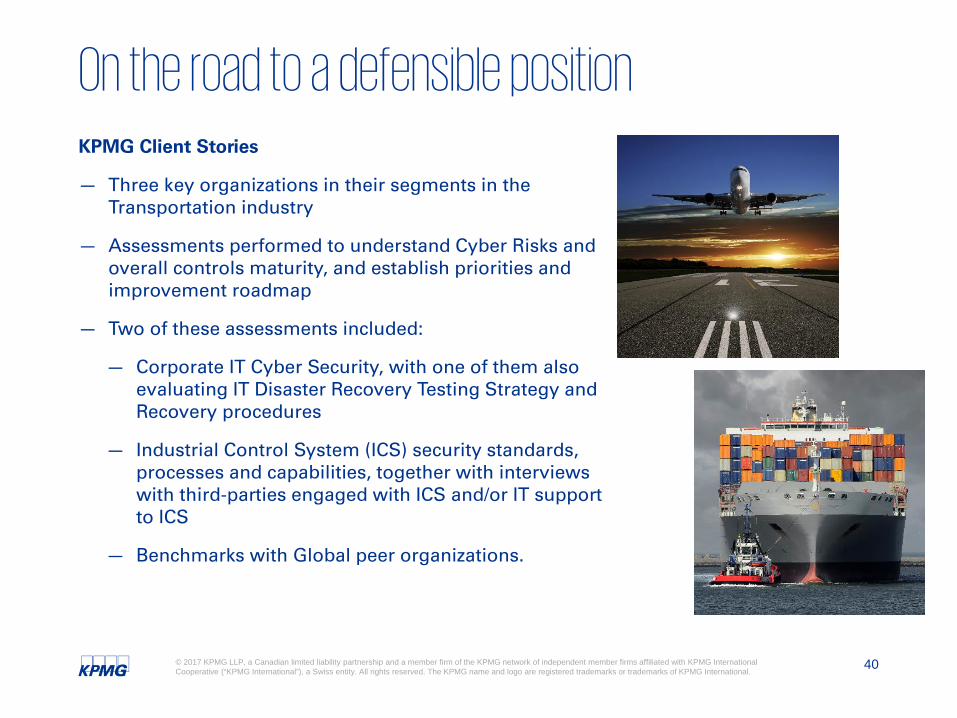

On the road to a defensible positionKPMG Client Stories

— Three key organizations in their segments in the Transportation industry

— Assessments performed to understand Cyber Risks and overall controls maturity, and establish priorities and improvement roadmap

— Two of these assessments included:

— Corporate IT Cyber Security, with one of them also evaluating IT Disaster Recovery Testing Strategy and Recovery procedures

— Industrial Control System (ICS) security standards, processes and capabilities, together with interviews with third-parties engaged with ICS and/or IT support to ICS

— Benchmarks with Global peer organizations.

41© 2017 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

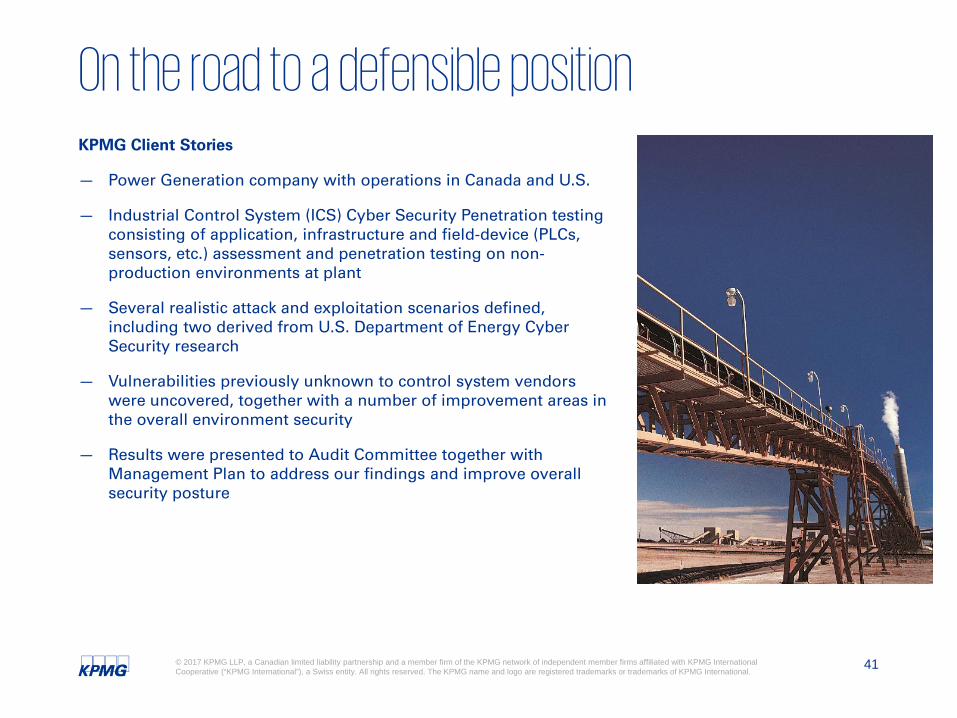

On the road to a defensible positionKPMG Client Stories

— Power Generation company with operations in Canada and U.S.

— Industrial Control System (ICS) Cyber Security Penetration testing consisting of application, infrastructure and field-device (PLCs, sensors, etc.) assessment and penetration testing on non-production environments at plant

— Several realistic attack and exploitation scenarios defined, including two derived from U.S. Department of Energy Cyber Security research

— Vulnerabilities previously unknown to control system vendors were uncovered, together with a number of improvement areas in the overall environment security

— Results were presented to Audit Committee together with Management Plan to address our findings and improve overall security posture

Questions?

Today’s presentation will be posted to

kpmg.ca/quarterlyupdate

Trevor HammondPartner, Audit

Thank you

kpmg.ca

© 2017 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity. Although we endeavour to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation.