third party funds reforms and enhancements. manage maintenance beneficiary monies (local and...

TRANSCRIPT

Third Party Funds Reforms and

Enhancements

•Manage maintenance beneficiary monies (local and foreign),

•Collect fines on behalf of government institutions (national, provincial, local and other authorities),

•The safe-keeping of bail monies on behalf of depositors,

•The safe-keeping of payments into court, and

•The collection of debts on behalf of government institutions through the State Attorney and deeds transfers on behalf of government.

Introduction: The purpose of TPF

2

These transactions are recorded on JDAS4 or SAS which are mainly administration

systems with the main objective of delivering a service to the public.

As JDAS and SAS are case management systems it does not have sufficient

financial capabilities and internal controls to allow for proper accounting principles in

accordance with the Public Finance Management Act (PFMA) on TPF.

The administration part of the systems allow for capturing of case details of

parties, court orders, etcetera while the current financial part of the systems allows

for the recording of receipts, payments and provide for reports on these receipts

and payments, although no reliable consolidated reporting functionality is available

on JDAS or SAS.

Administrative arrangements

3

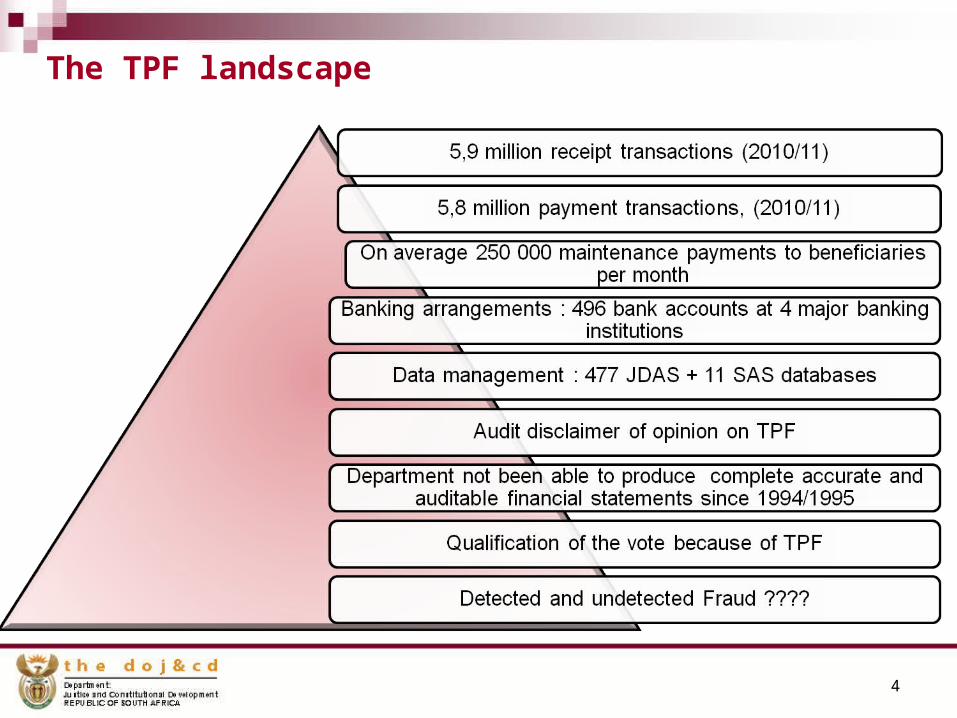

The TPF landscape

4

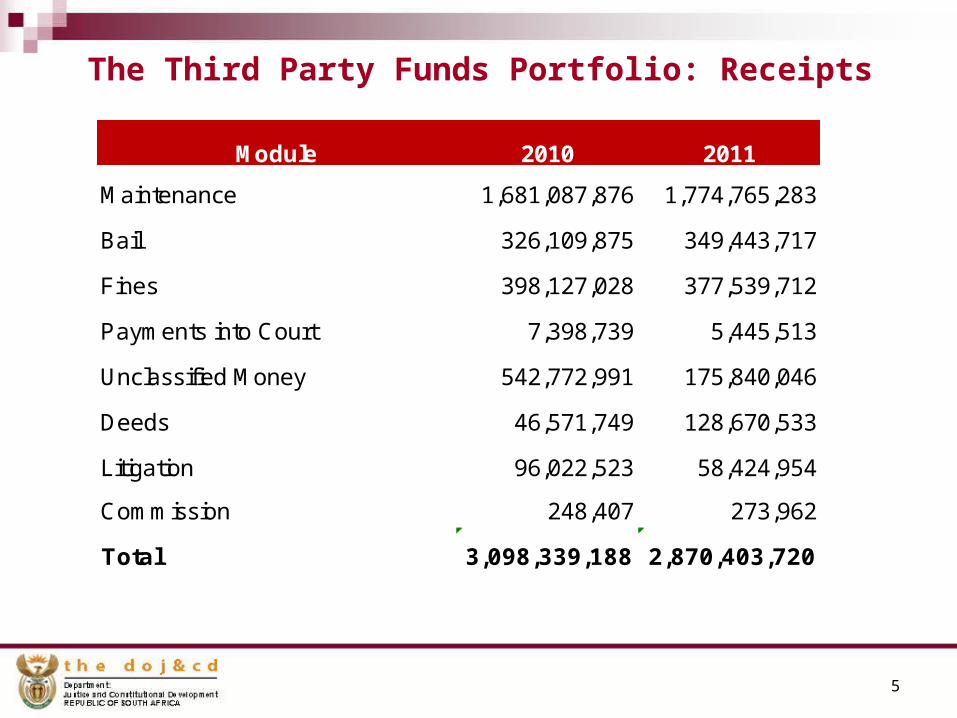

The Third Party Funds Portfolio: Receipts

Module 2010 2011

Maintenance 1,681,087,876 1,774,765,283

Bail 326,109,875 349,443,717

Fines 398,127,028 377,539,712

Payments into Court 7,398,739 5,445,513

Unclassified Money 542,772,991 175,840,046

Deeds 46,571,749 128,670,533

Litigation 96,022,523 58,424,954

Commission 248,407 273,962

Total 3,098,339,188 2,870,403,720

5

The Third Party Funds Portfolio: Receipts – Proportional Allocations per Module

Maintenance1,774,765,283

62%

Bail349,443,717

12%

Fines377,539,712

13%Payments into Court5,445,513

0%Unclassified Money

175,840,0466%

Deeds128,670,533

5%

Litigation58,424,954

2%Commission

273,9620%

The Challenge : Unclassified Receipts6

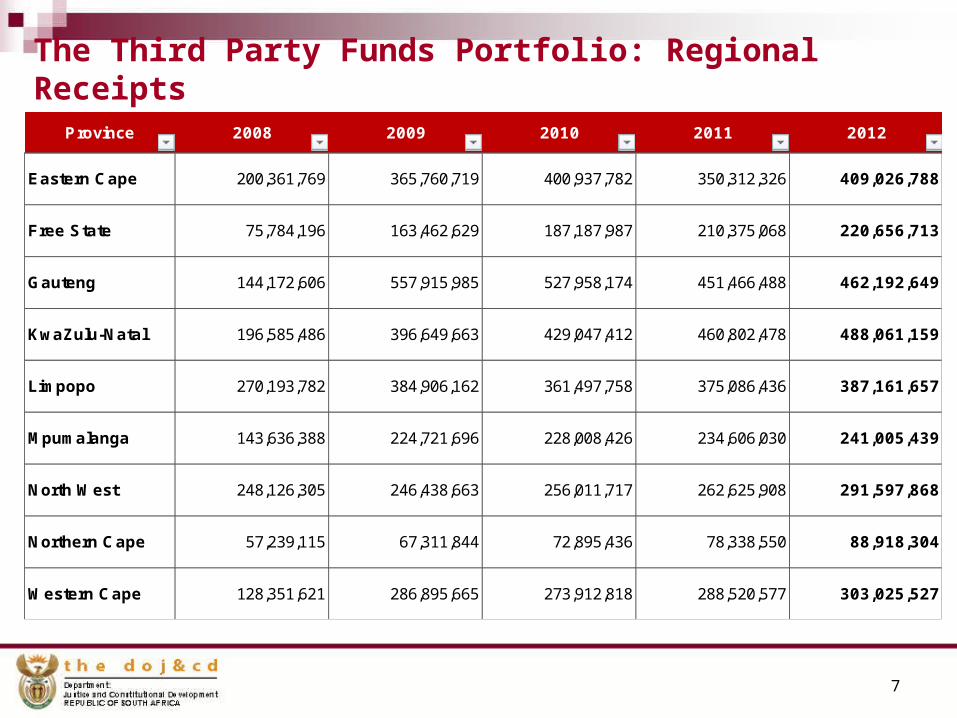

The Third Party Funds Portfolio: Regional Receipts

Province 2008 2009 2010 2011 2012

Eastern Cape 200,361,769 365,760,719 400,937,782 350,312,326 409,026,788

Free State 75,784,196 163,462,629 187,187,987 210,375,068 220,656,713

Gauteng 144,172,606 557,915,985 527,958,174 451,466,488 462,192,649

KwaZulu-Natal 196,585,486 396,649,663 429,047,412 460,802,478 488,061,159

Limpopo 270,193,782 384,906,162 361,497,758 375,086,436 387,161,657

Mpumalanga 143,636,388 224,721,696 228,008,426 234,606,030 241,005,439

North West 248,126,305 246,438,663 256,011,717 262,625,908 291,597,868

Northern Cape 57,239,115 67,311,844 72,895,436 78,338,550 88,918,304

Western Cape 128,351,621 286,895,665 273,912,818 288,520,577 303,025,527

7

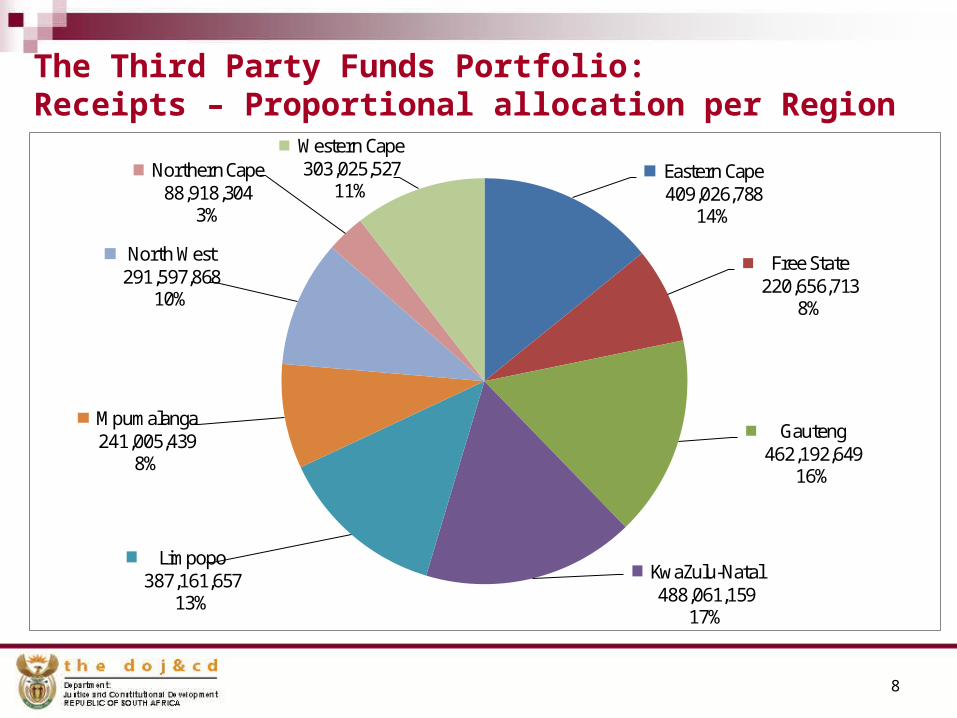

The Third Party Funds Portfolio: Receipts – Proportional allocation per Region

Eastern Cape409,026,788

14%

Free State220,656,713

8%

Gauteng462,192,649

16%

KwaZulu-Natal488,061,159

17%

Limpopo387,161,657

13%

Mpumalanga241,005,439

8%

North West291,597,868

10%

Northern Cape88,918,304

3%

Western Cape303,025,527

11%

8

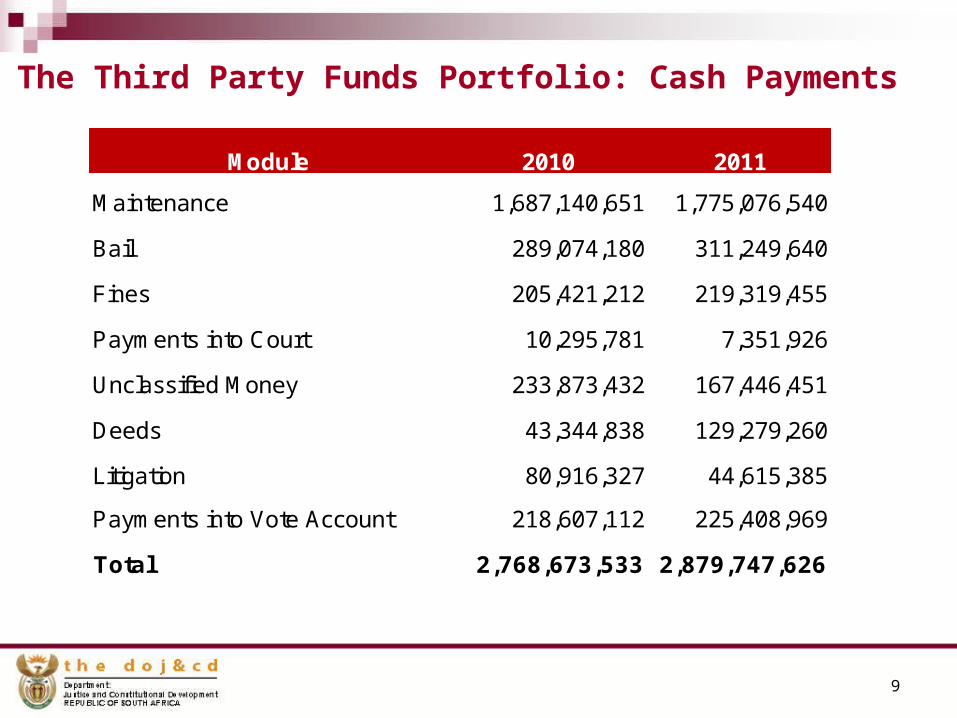

The Third Party Funds Portfolio: Cash Payments

Module 2010 2011

Maintenance 1,687,140,651 1,775,076,540

Bail 289,074,180 311,249,640

Fines 205,421,212 219,319,455

Payments into Court 10,295,781 7,351,926

Unclassified Money 233,873,432 167,446,451

Deeds 43,344,838 129,279,260

Litigation 80,916,327 44,615,385

Payments into Vote Account 218,607,112 225,408,969

Total 2,768,673,533 2,879,747,626

9

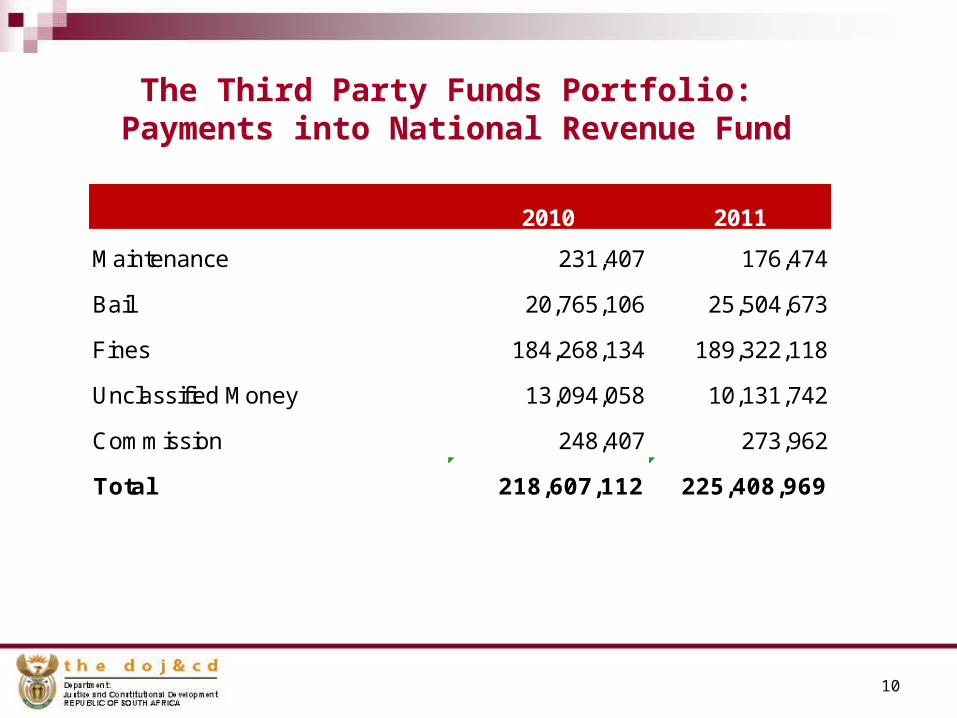

The Third Party Funds Portfolio: Payments into National Revenue Fund

2010 2011

Maintenance 231,407 176,474

Bail 20,765,106 25,504,673

Fines 184,268,134 189,322,118

Unclassified Money 13,094,058 10,131,742

Commission 248,407 273,962

Total 218,607,112 225,408,969

10

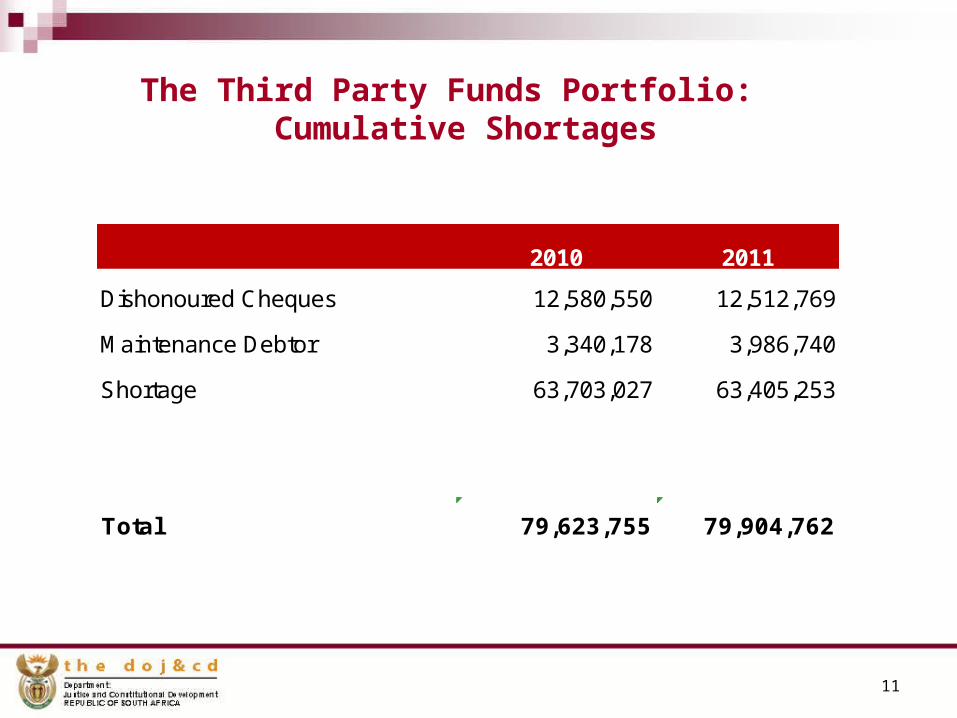

The Third Party Funds Portfolio: Cumulative Shortages

2010 2011

Dishonoured Cheques 12,580,550 12,512,769

Maintenance Debtor 3,340,178 3,986,740

Shortage 63,703,027 63,405,253

Total 79,623,755 79,904,762

11

PwC

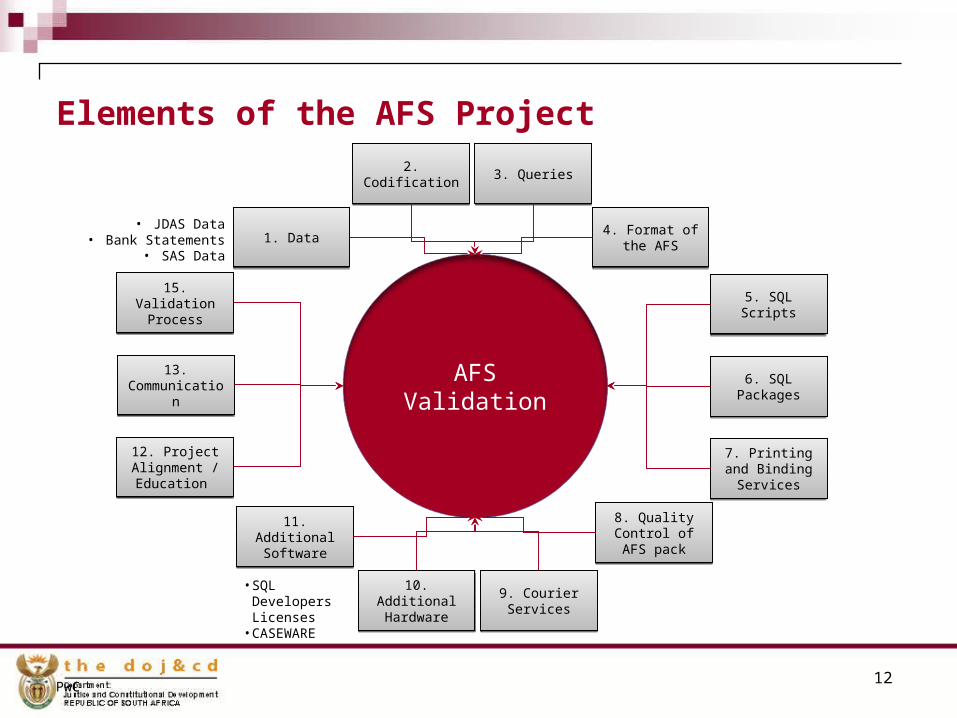

Elements of the AFS Project

12

AFS Validation

2. Codification2. Codification 3. Queries3. Queries

5. SQL Scripts5. SQL Scripts

6. SQL Packages

6. SQL Packages

4. Format of the AFS

4. Format of the AFS

9. Courier Services

9. Courier Services

7. Printing and Binding Services

7. Printing and Binding Services

8. Quality Control of AFS

pack

8. Quality Control of AFS

pack11. Additional

Software11. Additional

Software

12. Project Alignment / Education

12. Project Alignment / Education

13. Communicatio

n

13. Communicatio

n

15. Validation Process

15. Validation Process

• JDAS Data• Bank Statements

• SAS Data

• SQL Developers Licenses

• CASEWARE

10. Additional Hardware

10. Additional Hardware

1. Data1. Data

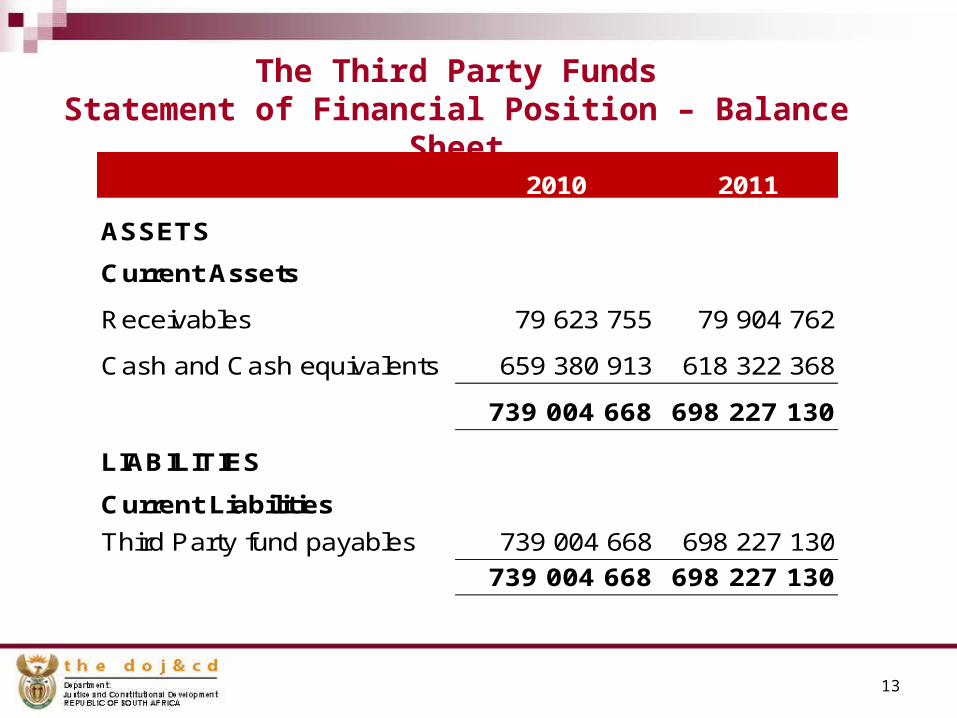

The Third Party FundsStatement of Financial Position – Balance Sheet

2010 2011

ASSETS

Current Assets

Receivables 79 623 755 79 904 762

Cash and Cash equivalents 659 380 913 618 322 368

739 004 668 698 227 130

LIABILITIES

Current Liabilities

Third Party fund payables 739 004 668 698 227 130739 004 668 698 227 130

13

14

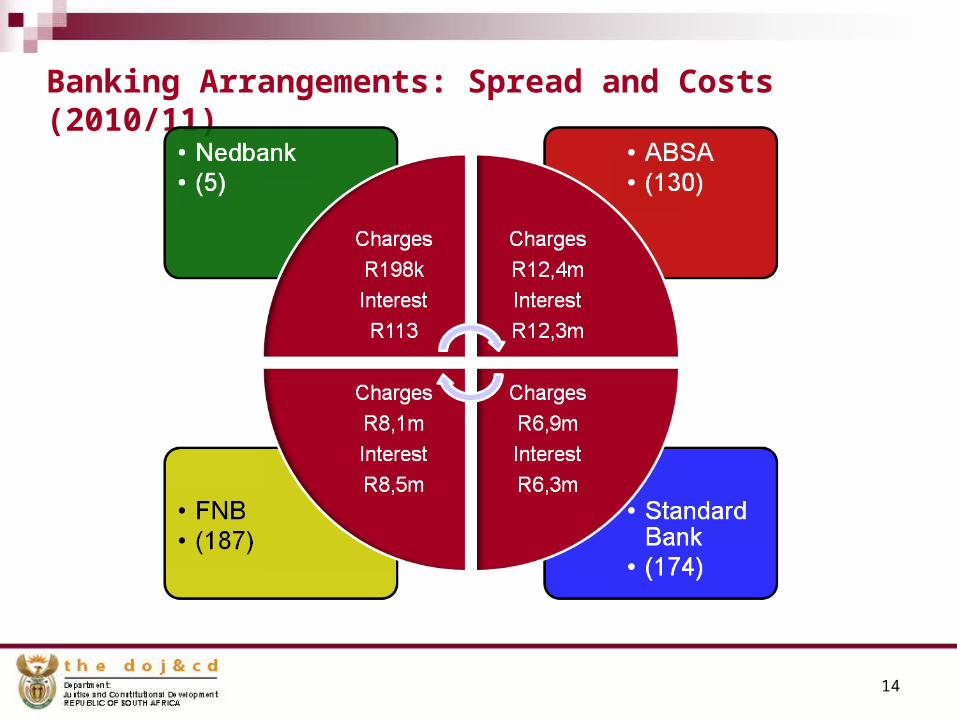

Banking Arrangements: Spread and Costs (2010/11)

We are not alone – International (HM) Experience

The courts service risks losing around £1.4 billion in uncollected fines and other financial penalties by not being able to properly account for them, according to the National Audit Office, which laid part of the blame with the beleaguered £444 million Libra system.

In a report to parliament, NAO auditor general Amyas Morse said HM Courts Service has been "unable to provide proper accounting records supporting fines, confiscation orders and penalties". This meant he "could not give an audit opinion on whether transactions and balances were complete, proper and appropriately raised".

Morse said: "Because of limitations in the underlying systems, HM Courts Service has not been able to provide me with proper accounting records relating to the collection of fines, confiscation orders and penalties. I have therefore disclaimed my audit opinion on its accounts

December 2011

”

15

Service delivery enhancement through decentralized EFT payment channel Launched in Worcester – August 2010

Reduced turn around time – payment with 24/48 hours after

identification has been concluded

Management oversight and control

Full audit trial

Segregation of duties

Actual number of courts rolled-out : 103

Number of beneficiaries paid through this system; 89 287 paid in April

2012

Planned roll-out to further sites: 100 courts in 2012/13

16

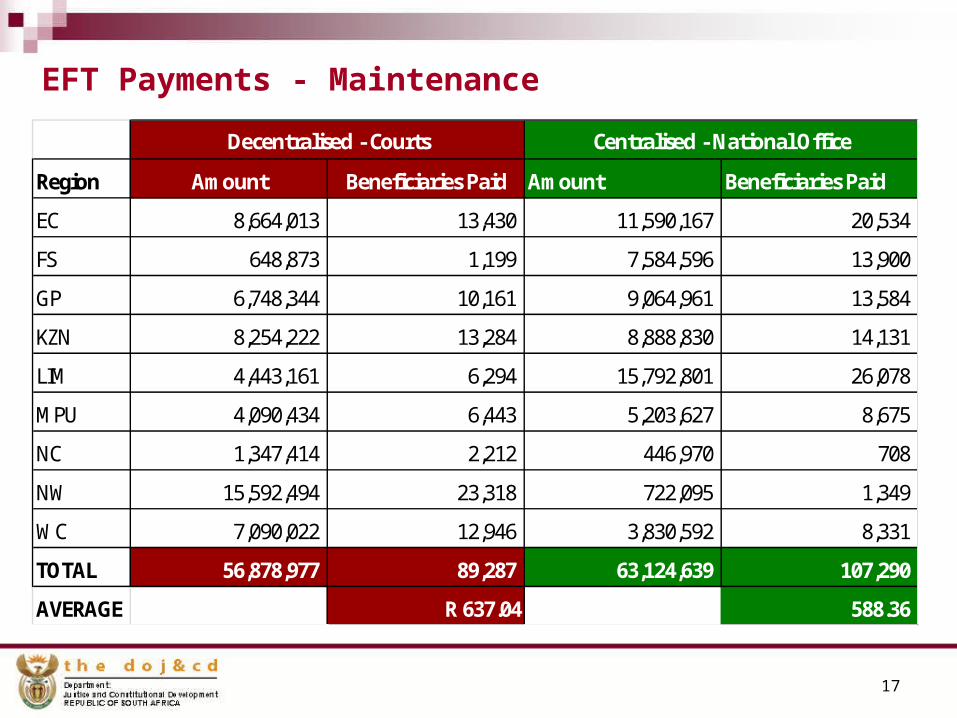

EFT Payments - Maintenance

Region Amount Beneficiaries Paid Amount Beneficiaries Paid

EC 8,664,013 13,430 11,590,167 20,534

FS 648,873 1,199 7,584,596 13,900

GP 6,748,344 10,161 9,064,961 13,584

KZN 8,254,222 13,284 8,888,830 14,131

LIM 4,443,161 6,294 15,792,801 26,078

MPU 4,090,434 6,443 5,203,627 8,675

NC 1,347,414 2,212 446,970 708

NW 15,592,494 23,318 722,095 1,349

WC 7,090,022 12,946 3,830,592 8,331

TOTAL 56,878,977 89,287 63,124,639 107,290

AVERAGE R 637.04 588.36

Decentralised - Courts Centralised - National Office

17

EFT Payments – Proportional Utilization of Decentralized EFT

8,66

4,01

3

648,

873 6,74

8,34

4

8,25

4,22

2

4,44

3,16

1

4,09

0,43

4 1,34

7,41

4

15,5

92,4

94

7,09

0,02

2

11,5

90,1

67

7,58

4,59

6

9,06

4,96

1

8,88

8,83

0

15,7

92,8

01

5,20

3,62

7

446,

970

722,

095

3,83

0,59

2

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

EC FS GP KZN LIM MPU NC NW WC

Over 90 % of payments in the North West is directly in beneficiary bank accounts

18

19

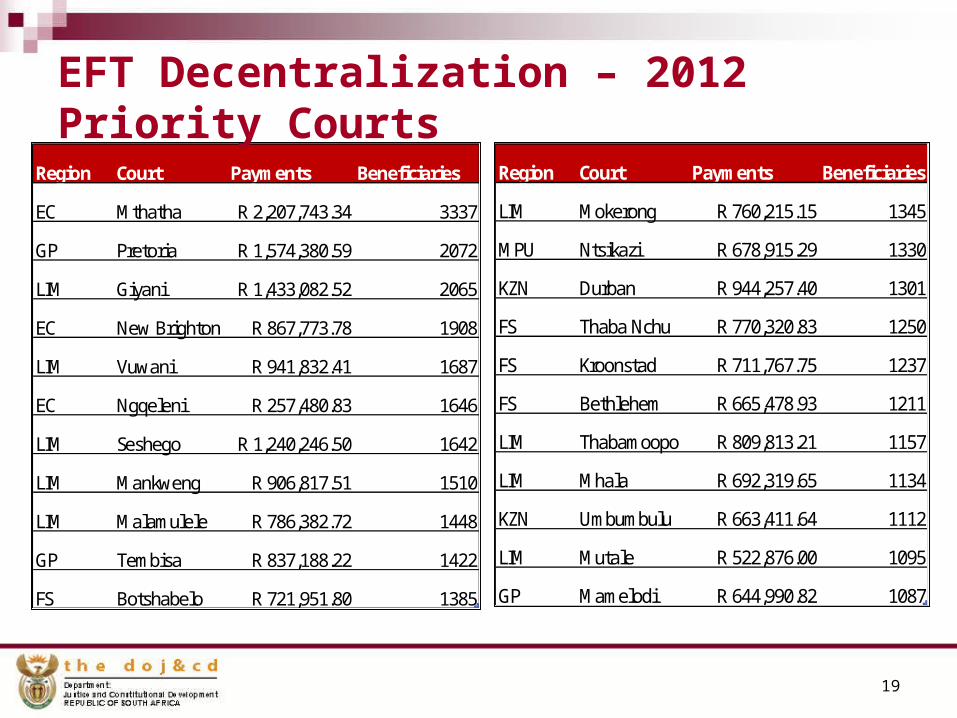

Region Court Payments Beneficiaries

EC Mthatha R 2,207,743.34 3337

GP Pretoria R 1,574,380.59 2072

LIM Giyani R 1,433,082.52 2065

EC New Brighton R 867,773.78 1908

LIM Vuwani R 941,832.41 1687

EC Ngqeleni R 257,480.83 1646

LIM Seshego R 1,240,246.50 1642

LIM Mankweng R 906,817.51 1510

LIM Malamulele R 786,382.72 1448

GP Tembisa R 837,188.22 1422

FS Botshabelo R 721,951.80 1385

EFT Decentralization – 2012 Priority Courts

Region Court Payments Beneficiaries

LIM Mokerong R 760,215.15 1345

MPU Ntsikazi R 678,915.29 1330

KZN Durban R 944,257.40 1301

FS Thaba Nchu R 770,320.83 1250

FS Kroonstad R 711,767.75 1237

FS Bethlehem R 665,478.93 1211

LIM Thabamoopo R 809,813.21 1157

LIM Mhala R 692,319.65 1134

KZN Umbumbulu R 663,411.64 1112

LIM Mutale R 522,876.00 1095

GP Mamelodi R 644,990.82 1087

20

The TPF

Challenge

TransactionVolumes

477 JDAS

Databases

Expected Shortages

Cash Collections/Payments

Unreferenced deposits

Theft And

corruption

21

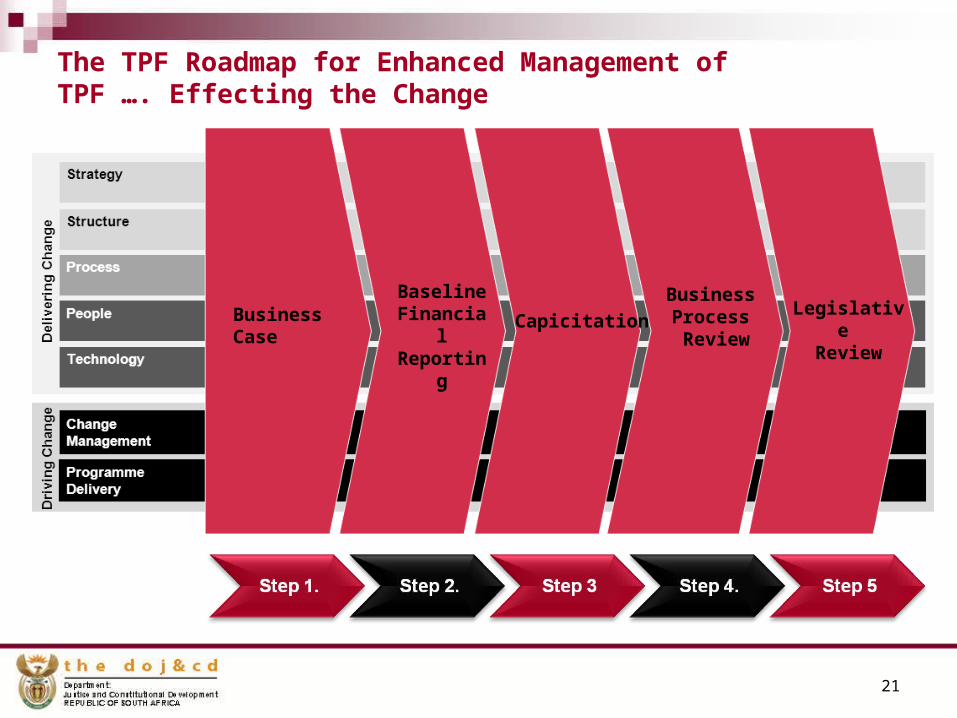

The TPF Roadmap for Enhanced Management of TPF …. Effecting the Change

Business Case

Baseline Financial Reporting

Capicitation

Business Process Review

Legislative Review

22

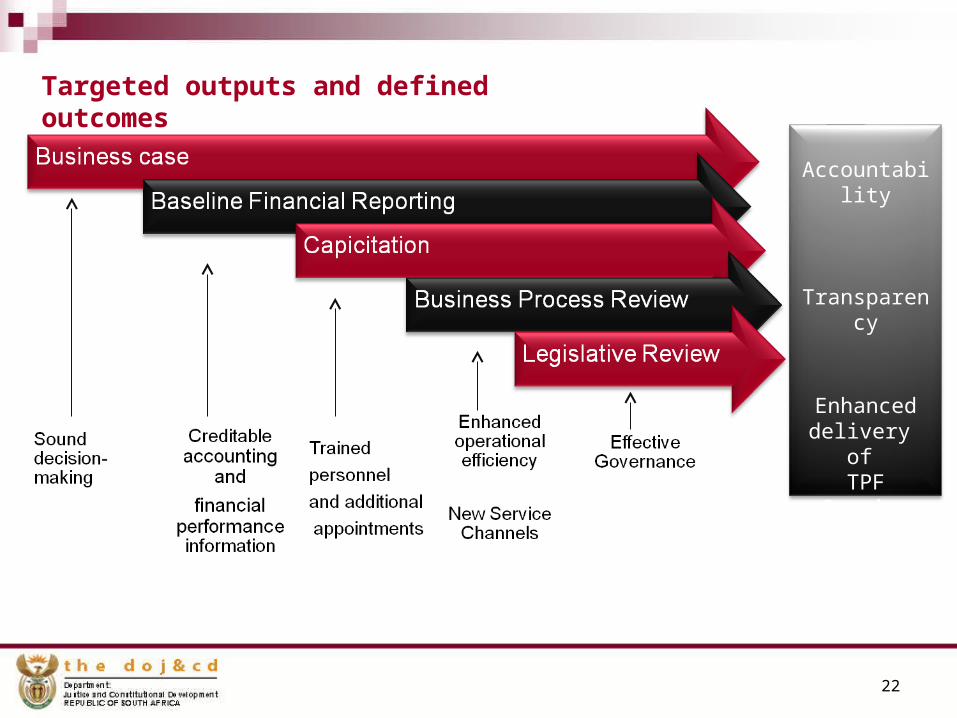

Targeted outputs and defined outcomes

Accountability

Transparency

Enhanced delivery

of TPF

Services

23

Conclusion of Compressive Business Case • Option 1:Maintenance of the status-quo• Option 2: Outsourcing through a PPP• Option 3: Enhanced Public Sector Managed TPF

Selection: Option3 – Based on affordability and Employment consideration

Communication of selection to stakeholders ( Executive Authority, Parliamentary Committees and NT)

Considerations: Value for Money, Affordability and Risk

24

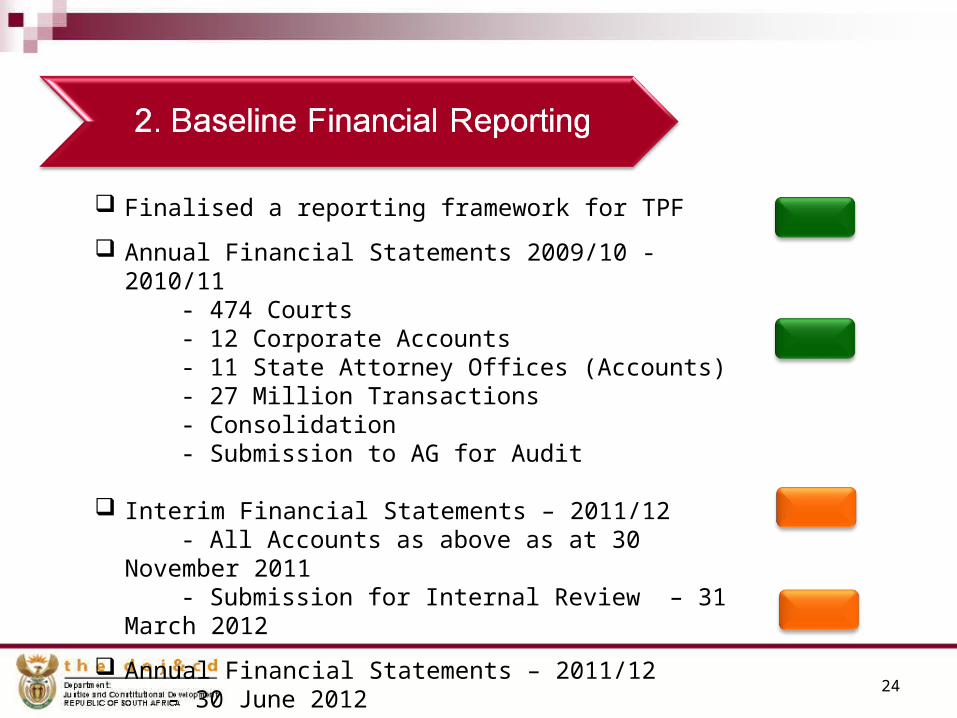

Finalised a reporting framework for TPF

Annual Financial Statements 2009/10 -2010/11 - 474 Courts - 12 Corporate Accounts - 11 State Attorney Offices (Accounts) - 27 Million Transactions - Consolidation - Submission to AG for Audit

Interim Financial Statements – 2011/12 - All Accounts as above as at 30 November 2011 - Submission for Internal Review – 31 March 2012

Annual Financial Statements – 2011/12 - 30 June 2012

25

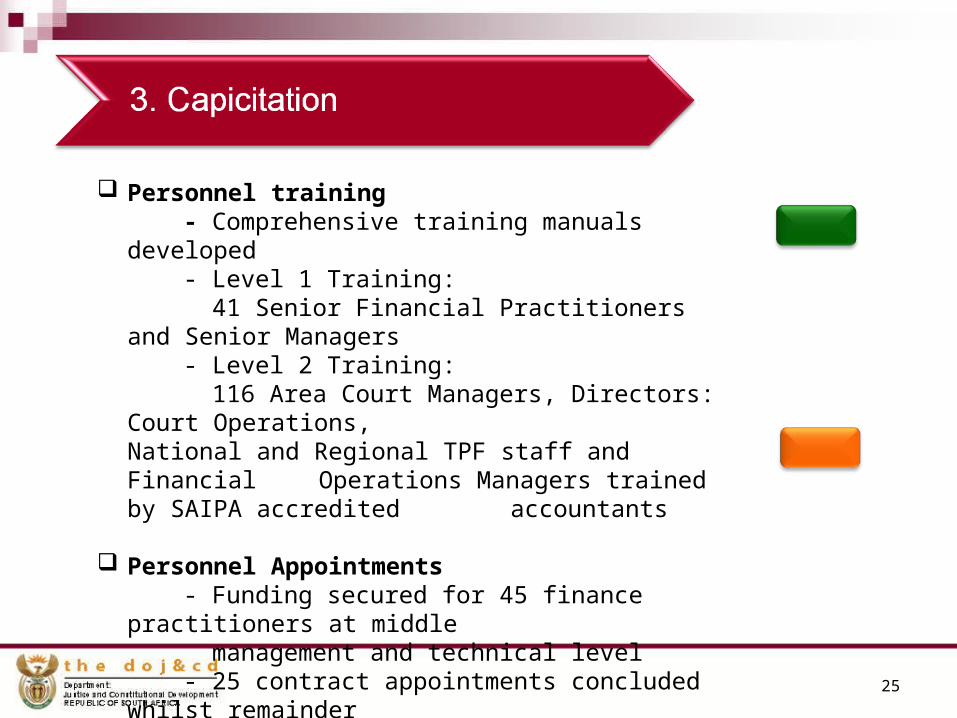

Personnel training - Comprehensive training manuals developed - Level 1 Training: 41 Senior Financial Practitioners and Senior Managers - Level 2 Training: 116 Area Court Managers, Directors: Court Operations,

National and Regional TPF staff and Financial Operations Managers trained by SAIPA accredited accountants

Personnel Appointments - Funding secured for 45 finance practitioners at middle management and technical level - 25 contract appointments concluded whilst remainder advertised - 2 database administrators and 8 quality assurance and

technical personnel appointed on six months contracts

26

Revised and Standardized Business Process - Concluded a review linking audit trails, daily reconciliations and operational performance - TPF processes standardized and process mapped - Financial operations managers and Area Court managers orientated on the standardized operating procedures Next Steps: Training all court managers and checking officers on standardized operating procedures New Payment Channel - Introduced decentralized EFT payment system at courts with reduced cycle times - Full audit trial and segregation of duty (key requirement) -Reduction of payment time from10 days to within 24 and 48 hours after beneficiary has been identified

27

Possible Legislative amendments to be considered

- Amendments to Maintenance Act in relation to direct beneficiary payments

- Amendment of Criminal Procedure Act to redirect local authority admission of guilt fines to Municipalities

- Investigate options to amend legislation for refunding of bail (Electronic refund of bail)

- Legislation Governing TPF