third international pharmaceutical regulatory and ... · pdf filethird international...

TRANSCRIPT

Third International Pharmaceutical Regulatory

and Compliance Congress and Best Practices Forum

May 28 2009 Rome

Pre-conference I - International Compliance Program Basics

Dominique Laymand Sue EganSenior Director Compliance & Ethics EMEA Vice-President Compliance, ISMO

Bristol-Myers Squibb AstraZeneca

2

International Compliance Program Basics

• How can we maintain a robust Compliance Programme in the current difficult economic environment?

• How can we maintain a robust Compliance Programme in the changing internal environment of the pharmaceutical industry?

Let’s begin by taking a look at the external environment…

3

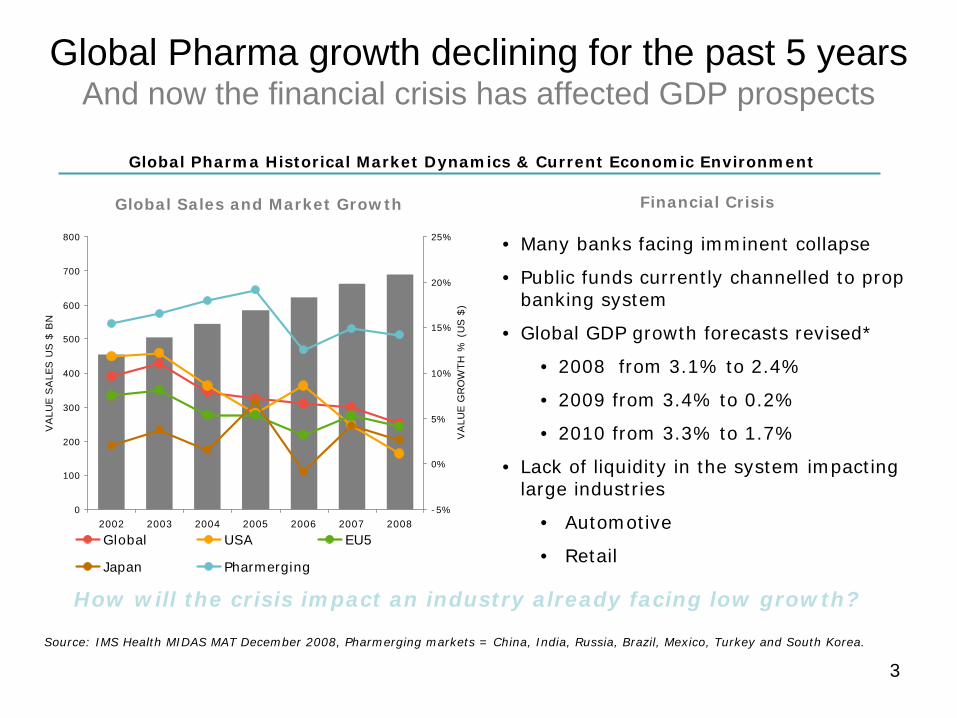

Global Pharma growth declining for the past 5 years And now the financial crisis has affected GDP prospects

0

100

200

300

400

500

600

700

800

2002 2003 2004 2005 2006 2007 2008

VA

LUE

SA

LES

US

$ B

N

-5%

0%

5%

10%

15%

20%

25%

VA

LUE

GR

OW

TH %

(U

S $

)

Global USA EU5

Japan Pharmerging

Source: IMS Health MIDAS MAT December 2008, Pharmerging markets = China, India, Russia, Brazil, Mexico, Turkey and South Korea.

Global Sales and Market Growth Financial Crisis

Global Pharma Historical Market Dynamics & Current Economic Environment

• Many banks facing imminent collapse

• Public funds currently channelled to prop banking system

• Global GDP growth forecasts revised*

• 2008 from 3.1% to 2.4%

• 2009 from 3.4% to 0.2%

• 2010 from 3.3% to 1.7%

• Lack of liquidity in the system impacting large industries

• Automotive

• Retail

How will the crisis impact an industry already facing low growth?

4

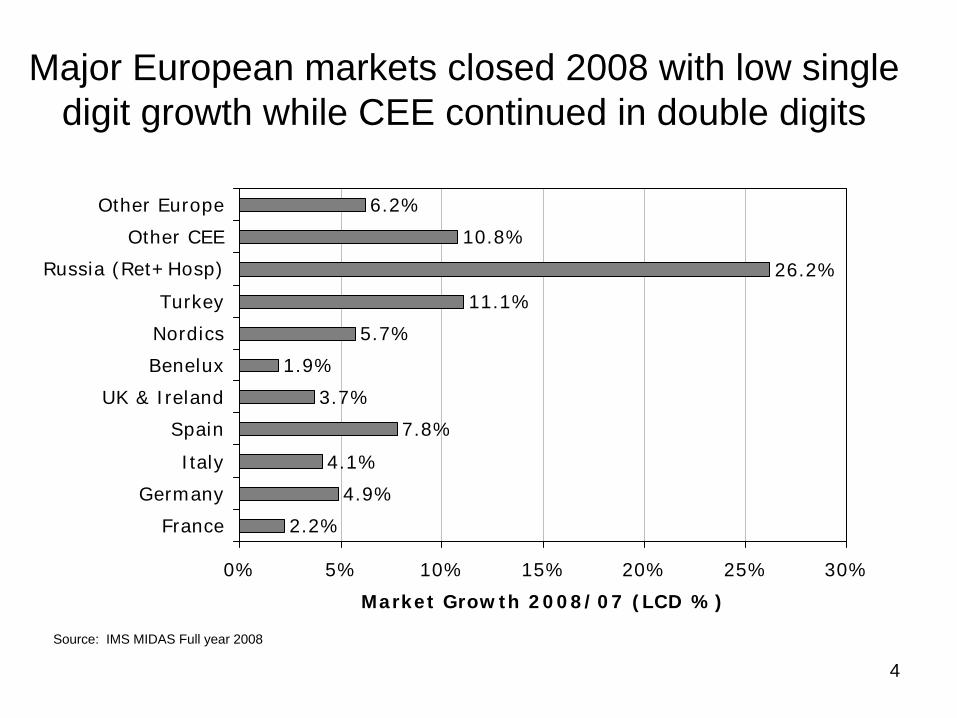

Major European markets closed 2008 with low single digit growth while CEE continued in double digits

2.2%

4.9%

4.1%

7.8%

3.7%

1.9%

5.7%

11.1%

26.2%

10.8%

6.2%

0% 5% 10% 15% 20% 25% 30%

France

Germany

Italy

Spain

UK & Ireland

Benelux

Nordics

Turkey

Russia (Ret+Hosp)

Other CEE

Other Europe

Market Growth 2008/07 (LCD %)

Source: IMS MIDAS Full year 2008

5

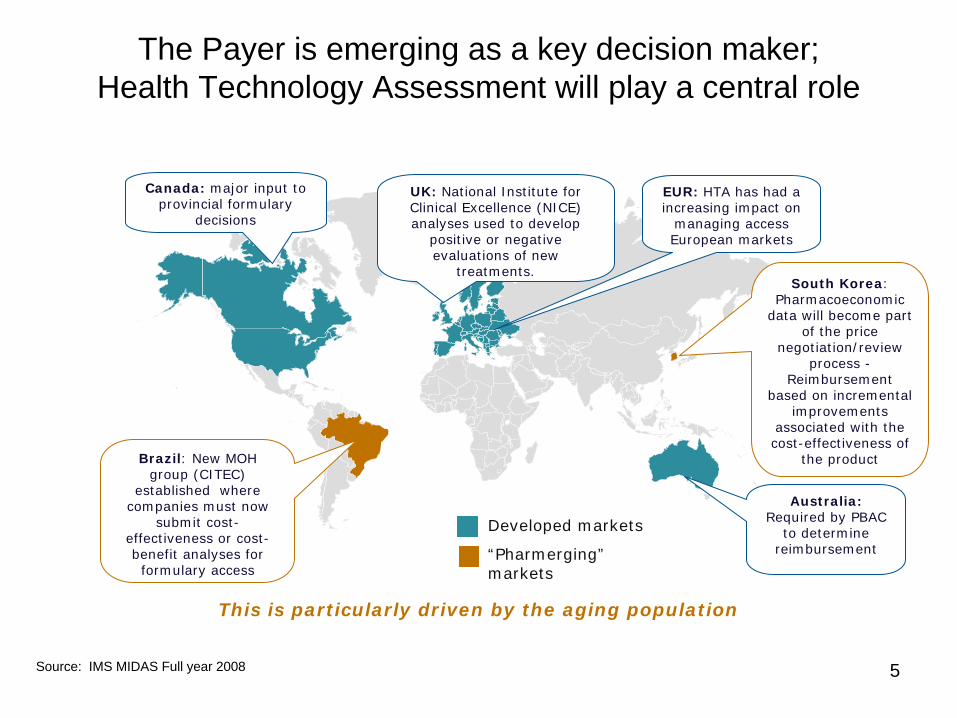

The Payer is emerging as a key decision maker; Health Technology Assessment will play a central role

This is particularly driven by the aging population

Canada: major input to provincial formulary

decisions

UK: National Institute for Clinical Excellence (NICE) analyses used to develop

positive or negative evaluations of new

treatments.

EUR: HTA has had a increasing impact on

managing access European markets

Australia: Required by PBAC

to determine reimbursement

Brazil: New MOH group (CITEC)

established where companies must now

submit cost- effectiveness or cost- benefit analyses for formulary access

South Korea: Pharmacoeconomic

data will become part of the price

negotiation/review process -

Reimbursement based on incremental

improvements associated with the cost-effectiveness of

the product

Developed markets

“Pharmerging” markets

Source: IMS MIDAS Full year 2008

6

Payers are increasingly fragmented within key markets, as decision making becomes increasingly ‘localised’

UK: PCTs power & influence varies resulting in divergent prescribing behaviour & implementation of national guidelines

France: Recent health reforms decentralisation process will create Agences Regionales de Sante (ARS) and consolidate control over both primary & hospital care. Potential impact is more control over GP prescribing & increased efficiency

Italy: Regional governments taken on increasing healthcare financing responsibility. North-South affluence divide reflected in Lombardy seeking increased responsibilities, whilst Lazio & Sicily struggle with huge deficits and central government disciplinary pacts.

Spain: Decentralised healthcare in 2002 to 17 autonomous regions. Over half of spending in 4 key regions Andalusia (16.4%), Catalonia (15.5%), Valencia (2.9%) and Madrid (10.6%). The 17 regions all pursue variable policies but reference pricing is now nationwide.

Source: IMS Health Consulting

France

Spain

UK

Italy

German y

Germany: Contracting with the different sick funds has increased regional variability. Regional sick funds are partnering with corps to issue treatment guidance with preferred therapy, becoming key decision makers.

Local managed care (style) influence develops in Europe

7

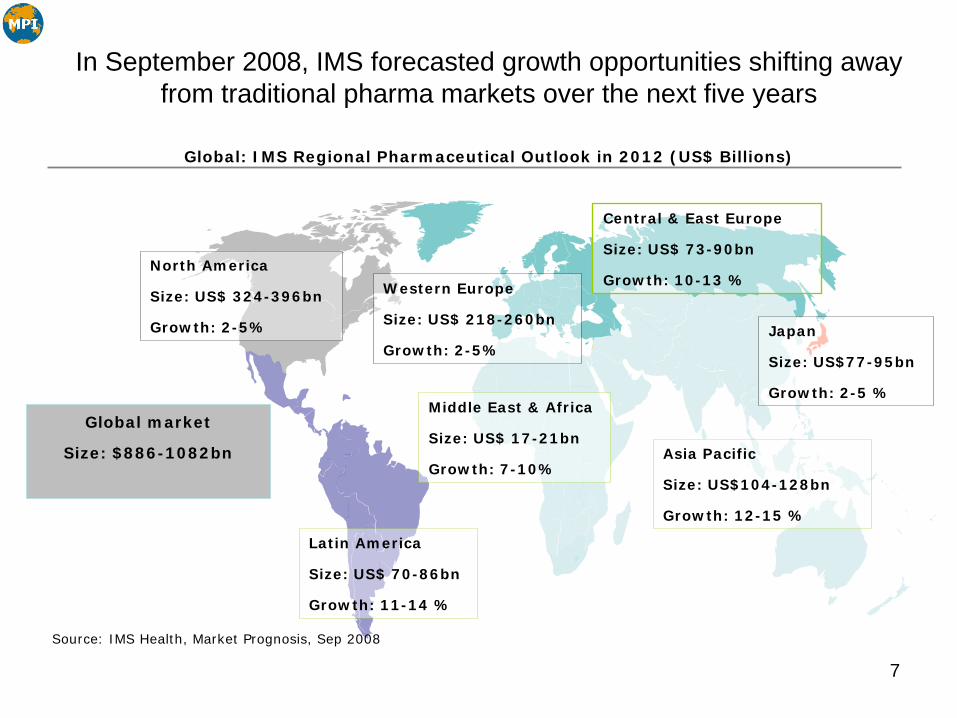

In September 2008, IMS forecasted growth opportunities shifting away from traditional pharma markets over the next five years

Japan

Size: US$77-95bn

Growth: 2-5 %

North America

Size: US$ 324-396bn

Growth: 2-5%

Global market

Size: $886-1082bn

Source: IMS Health, Market Prognosis, Sep 2008

Western Europe

Size: US$ 218-260bn

Growth: 2-5%

Latin America

Size: US$ 70-86bn

Growth: 11-14 %

Central & East Europe

Size: US$ 73-90bn

Growth: 10-13 %

Middle East & Africa

Size: US$ 17-21bn

Growth: 7-10%Asia Pacific

Size: US$104-128bn

Growth: 12-15 %

Global: IMS Regional Pharmaceutical Outlook in 2012 (US$ Billions)

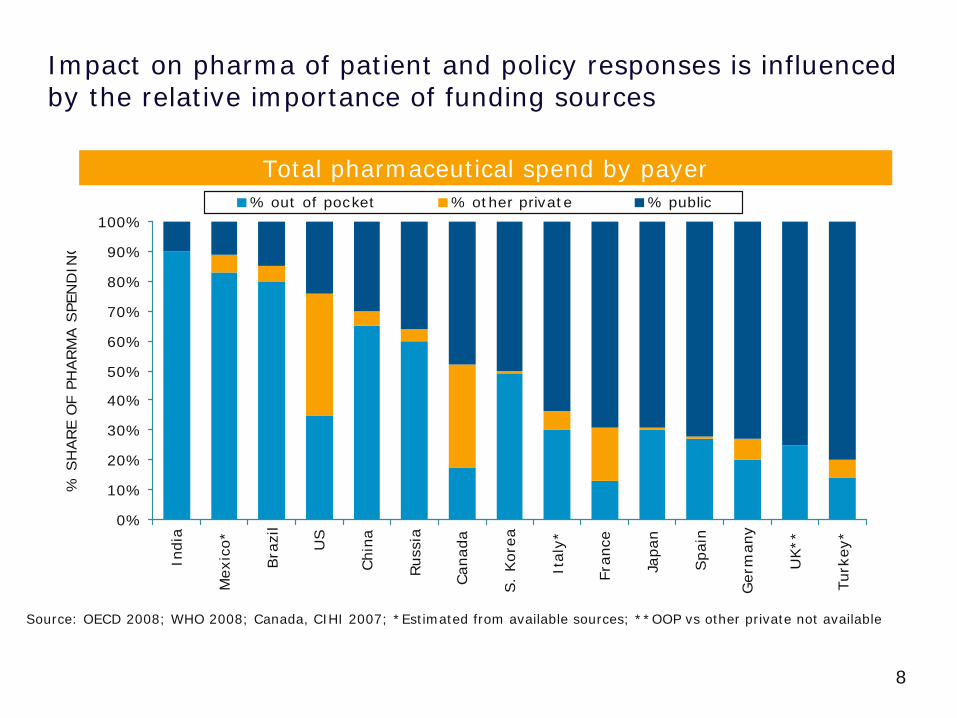

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Indi

a

Mex

ico*

Bra

zil

US

Chi

na

Rus

sia

Can

ada

S.

Kor

ea

Ital

y*

Fran

ce

Japa

n

Spa

in

Ger

man

y

UK**

Turk

ey*

% S

HARE

OF

PHARM

A S

PEN

DIN

G

% out of pocket % other private % public

Impact on pharma of patient and policy responses is influenced by the relative importance of funding sources

Source: OECD 2008; WHO 2008; Canada, CIHI 2007; *Estimated from available sources; **OOP vs other private not available

Total pharmaceutical spend by payer

8

9

Pharmaceutical Companies – Internal environment

• Evolution of organisations in response to the external environment by reducing costs, streamlining internal structures, etc…

• Key components for maintaining a robust Compliance Programme as a business enabler through the approaches of 2 companies:

– BMS approach Slides 10 and 11– AstraZeneca approach Slides 12 and 13

10

Office of Compliance & Ethics

MISSION STATEMENTTo establish an effective Compliance & Ethics program that ensures a culture of integrity enabling BMS to conduct its global business with the highest ethical standards, in full compliance with all applicable laws and regulations and our own Pledge and the Standards of Business Conducts & Ethics.

BMS Approach

10

11

EMEA Business Compliance & Ethics Governance Model Overview

Business strategy and Risk-based ApproachFocused on Accountability

Collaborative working process with Finance Control and Legal Functions

EMEA BusinessControl Program

EMEA BusinessCompliance & Ethics

Program

EMEA Compliance & Ethics Governance Model

Contribution to Productivity Transformationand Continuous Improvement by:

4A standardized approach on core activities4A focus on innovative and new projects

4Continuous assessment of processes in terms of controls and compliance efficiency with the objective of working in a safe environment while removing bureaucracy

BMS Approach

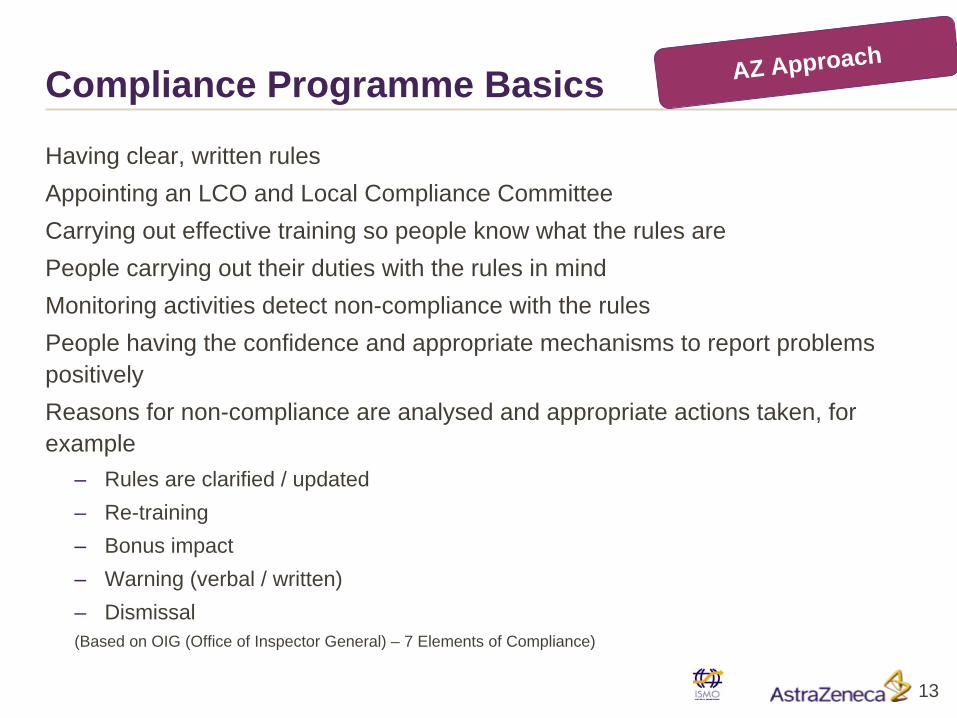

Compliance Programme Basics

Having clear, written rulesAppointing an LCO and Local Compliance CommitteeCarrying out effective training so people know what the rules arePeople carrying out their duties with the rules in mindMonitoring activities detect non-compliance with the rulesPeople having the confidence and appropriate mechanisms to report problems positivelyReasons for non-compliance are analysed and appropriate actions taken, for example

– Rules are clarified / updated– Re-training– Bonus impact– Warning (verbal / written)– Dismissal(Based on OIG (Office of Inspector General) – 7 Elements of Compliance)

13

AZ Approach

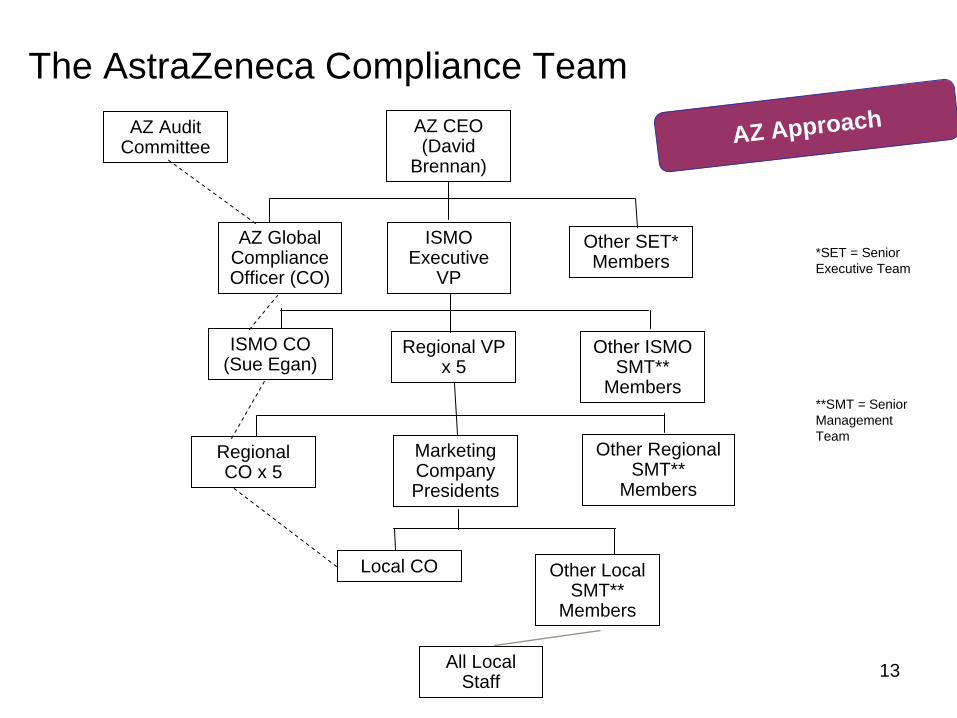

13

The AstraZeneca Compliance TeamAZ CEO (David

Brennan)

ISMO Executive

VP

AZ Global Compliance Officer (CO)

Other SET* Members

Regional VP x 5

Other ISMO SMT**

Members

ISMO CO (Sue Egan)

Regional CO x 5

Other Regional SMT**

Members

Marketing Company Presidents

Other Local SMT**

Members

Local CO

All Local Staff

AZ Approach

*SET = Senior Executive Team

**SMT = Senior Management Team

AZ Audit Committee

14

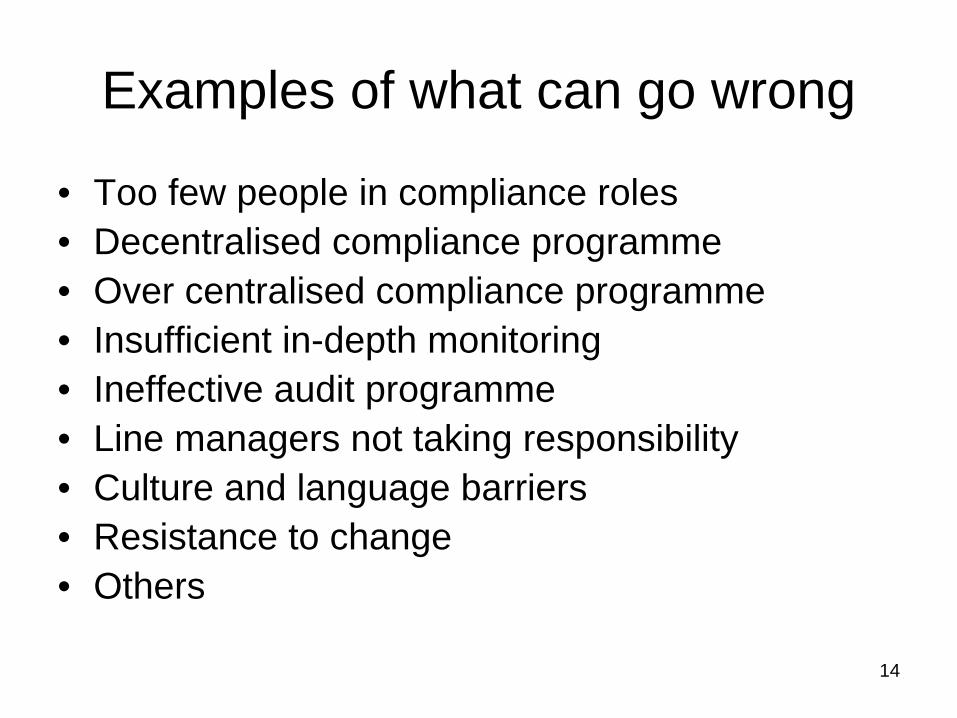

Examples of what can go wrong

• Too few people in compliance roles• Decentralised compliance programme• Over centralised compliance programme• Insufficient in-depth monitoring• Ineffective audit programme• Line managers not taking responsibility• Culture and language barriers• Resistance to change• Others

15

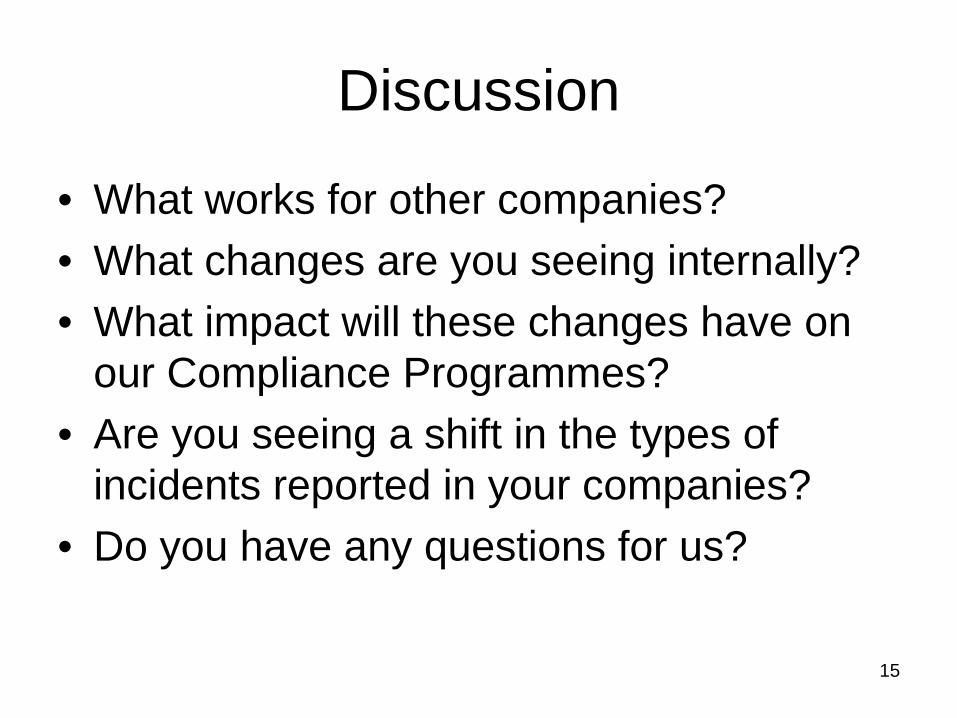

Discussion

• What works for other companies?• What changes are you seeing internally?• What impact will these changes have on

our Compliance Programmes?• Are you seeing a shift in the types of

incidents reported in your companies?• Do you have any questions for us?