thesis - jeremy - 9-7-16 final

TRANSCRIPT

Power to the People: The Future of Electric Utilities and Distributed

Energy Resources in the 21st Century

By Jeremy Conway

Reviewed by Chris Gadomski

1

Copyright © 2016 by Jeremy Conway

All rights reserved. No part of this publication may be reproduced, distributed or transmitted without the express consent of the author.

2

Acknowledgements

First and foremost, I would like to express my gratitude to the professors who have kindled my interests in energy, finance, economics and environmental policy. In particular, I would like to thank Carolyn Kissane for providing one of the most engaging and enjoyable classroom experiences in my academic career and for taking such an interest in nurturing future energy leaders. I would like to especially thank Chris Gadomski for arousing my curiosity in the economics and finance of energy and Jay Taparia for urging me to take on this challenging topic. I am indebted to all of my professors, friends and family who have encouraged me along the way. I dedicate this work to my grandparents who have always believed in me. Without their kindness and generosity, this thesis never would have seen the light of day.

3

Recommended Research Sources

America’s Power Plan. http://americaspowerplan.com Center on Global Energy Policy. http://energypolicy.columbia.edu/ Cost of Renewable Energy Spreadsheet Tool. https://financere.nrel.gov/finance/content/crest-cost-energy-models Database of State Incentives for Renewables & Efficiency. http://www.dsireusa.org/ Edison Electric Institute. http://www.eei.org/ Energy Information Administration. http://www.eia.gov/ Federal Energy Regulatory Commission. http://www.ferc.gov/ Freeing the Energy Grid. http://freeingthegrid.org/ Institute for Local Self-Reliance. https://ilsr.org/ International Energy Agency. http://www.iea.org/ Interstate Renewable Energy Council. http://www.irecusa.org/ Lawrence Berkeley National Laboratory. http://www.lbl.gov MIT Energy Initiative. http://mitei.mit.edu/ National Renewable Energy Laboratory. http://www.nrel.gov/ NC Clean Energy Technology Center. https://nccleantech.ncsu.edu/ PV Watts Calculator. http://pvwatts.nrel.gov/ Rocky Mountain Institute. http://www.rmi.org/ Shared Renewables HQ. http://sharedrenewables.org/ Solar Energy Industries Association. http://www.seia.org/ SEIA Major Solar Projects List. http://www.seia.org/map/majorprojectsmap.php Smart Electric Power Association. http://www.solarelectricpower.org/ The Open PV Project. https://openpv.nrel.gov/rankings

4

List of Acronyms IOU – Investor Owned Utility EE—Energy Efficiency EEI – Edison Electric Institute EIA – Energy Information Administration DER – Distributed Energy Resource DG – Distributed Generation DR – Demand Response DOE – Department of Energy DSIRE – Database of State Incentives for Renewables & Efficiency DSP – Distribution Service Platform FERC – Federal Energy Regulatory Commission IPP – Independent Power Producer IREC – Interstate Renewable Energy Council ISO – Independent System Operator ITC – Investment Tax Credit LCOE – Levelized Cost of Electricity NCCETC – NC Clean Energy Technology Center NEG – Net Excess Generation NEM – Net Energy Metering NREL – National Renewable Energy Laboratory PUC – Public Utility Commission PURPA – Public Utility Regulatory Policies Act (1978) PV – Photovoltaic QF – Qualifying Facility REV – New York State’s Reforming the Energy Vision RTO – Regional Transmission Organization SEIA – Solar Energy Industries Association SEPA – Smart Electric Power Alliance T&D – Transmission & Distribution TPO – Third Party Ownership

5

Table of Contents Page 1 Executive Summary---------------------------------------------------------------------------7 2 An Overview of Investor Owned Utilities------------------------------------------------------9 3 Current Industry Structure and Competitive Forces-----------------------------------------25 4 IOUs Current Strategic Reactions (Case Studies)--------------------------------------------56 5 Policy Recommendations for Power Industry Stakeholders---------------------------------70 6 Conclusions----------------------------------------------------------------------------------75

List of Figures Figure 2.1: Growing Economies of Scale Reduces a Company’s Average Total Costs-------------10 Figure 2.2: Declining Economies of Scale for IOU Industry --------------------------------------- 15 Figure 2.3: Regional Transmission Organizations in the U.S.-------------------------------------- 16 Figure 2.4: Declining Electricity Use Now a Long Term Trend------------------------------------- 17 Figure 2.5: Evolving Energy Efficiency Standards--------------------------------------------------19 Figure 2.6: IOU’s Historical Credit Ratings--------------------------------------------------------- 20 Figure 2.7: The So Called Utility Death Spiral------------------------------------------------------ 21 Figure 2.8: IOU Industry Capital Spending & Retail Rates------------------------------------------ 23 Figure 3.1: Solar Prices & Installation Rates------------------------------------------------------- 27 Figure 3.2: Nationwide Electricity Rates by County------------------------------------------------ 30 Figure 3.3: Soft Costs for a Typical Solar Installation---------------------------------------------- 31 Figure 3.4: Residential PV System Costs Reaching Grid Parity------------------------------------ 32 Figure 3.5: Financial Performance of Pure Play Residential Solar Companies-------------------- 35 Figure 3.6: Financial Performance of IOUs--------------------------------------------------------- 36 Figure 3.7: EBITDA Comparison of Solar Providers & IOUs-----------------------------------------37 Figure 3.8: PV Solar Insolation Across the US------------------------------------------------------39 Figure 3.9: Solar Insolation & Retail Rates Shape the Economics of Solar Systems-------------- 40 Figure 3.10: State Changes to NEM Policies------------------------------------------------------- 47 Figure 3.11: Interconnection Standards by State-------------------------------------------------- 48 Figure 3.12: ITC Stimulates Annual Solar Installations-------------------------------------------- 50 Figure 3.13: Map of Third Party Ownership (TPO) Regulations------------------------------------ 52 Figure 3.14: Community Solar Policies & Programs----------------------------------------------- 54 Figure 3.15: Residential Solar Market Potential by State------------------------------------------ 55 Figure 4.1: Top 10 Utility Solar Installations, 2015------------------------------------------------- 58 Figure 4.2: Utility Scale Solar in South Atlantic Region Dominated by North Carolina, Georgia--- 59 Figure 4.3: APS Solar Innovation Study------------------------------------------------------------ 62 Figure 4.4: Integration of Customer, DER Service Providers and the Utility through the DSP----- 65 Figure 5.1: Performance-based Ratemaking------------------------------------------------------ 71 Figure 5.2: Generic Smart Utility Business Models------------------------------------------------ 72 Figure 5.3: The Power Industry’s “Inseparable Triad---------------------------------------------- 73

6

List of Tables Table 3.1: Ranking of States with Third Party Solar Operators by Retail Rate---------------------29 Table 3.2: Average Capacity Factors for Generation Technologies-------------------------------- 38 Table 3.3: Southern Nevada Net Metering Rate Change Forecast--------------------------------- 43 Table 3.4: NEM Rates in Top 10 DG Markets by Per Capita Installations, 2016-------------------- 45 Table 3.5: Solar Investment Tax Credit Time Horizon---------------------------------------------- 49 Table 3.6: Renewable Portfolio Standards Policies------------------------------------------------ 51 Table 5.1: Business Model Elements--------------------------------------------------------------- 72

7

Chapter 1

Executive Summary During the 20th century, the US power industry and its regulatory overseers sought to make electricity reliable, cheap and accessible to all of the nation’s citizens. The regulatory compact formulated by these stakeholders succeeded in accomplishing these goals by promoting the development of vast electrical transmission and distribution networks interconnected to large central power stations. However, in the 21st century, this regulatory structure is now being challenged. While policymakers seek to maintain the goals of sustaining affordable and reliable electricity as a public good, public policy also seeks to preserve a modern power grid that mitigates the negative “public health and environmental costs” caused by carbon emissions.1 Moreover, now that economies of scale peaked in the 1970s, infrastructure spending leads to rate increases—meaning that the investor owned utilities’ financial incentive encouraging infrastructure spending (an incentive embedded in the regulated ratemaking framework) no longer provides cost reducing benefits to consumers. Since 2008, the growth of residential solar energy markets has created interest in developing distributed energy resource (DER) markets that help consumers reduce their power consumption and lower their electricity bills while providing potential benefits to the whole grid through deferred investments and aggregation of demand side resources (i.e. demand side management and load shifting) to optimize the grid’s operation. As a whole, investor owned utilities (IOUs) dislike DERs because the rise of these resources exacerbate the declining consumption of centralized power. This secular trend completely undermines the traditional financial motive of utilities: namely, to promote consumer demand for utility delivered kilowatt hours as a means to boost revenue and justify future investments in grid infrastructure. So far, the rise of DERs is most pronounced in regions that complement non-policy supporting factors (i.e. higher than average retail prices and/or high solar capacity factors) with a strong collection of market enabling policies such as the availability of net metering and investment tax credits. However, while the rise of DERs is most pronounced in the following regions (the Mid-Atlantic, Northeast, Southwest and California), even IOUs operating in markets with low DER deployment levels have taken strategic precautions to confront the disruptive threat. Financial incentives of IOUs create conflict with policymakers that aim to facilitate DER growth and integrate the DER market into the power sector’s value chain. The growth of DERs hurt IOUs because they render future infrastructure spending unnecessary and cause some customers to reduce their consumption. Under the 1 Harvey, Hal and Sonia Aggarwal. “Rethinking Policy to Deliver a Clean Energy Future,” Energy Innovation Policy & Technology LLC. September 2013. http://energyinnovation.org/wp-content/uploads/2014/06/APP-OVERVIEW-PAPER.pdf

8

IOUs traditional business model and ratemaking framework, the growth of DERs poses a threat to their business strategy and financial well-being through the ongoing loss of revenue and loss of potential investment opportunities with a regulated rate of return. In general, vertically integrated IOUs have wielded defensive strategies aimed at hindering DER growth. Others have instituted offensive strategies seeking to enter and potentially control the DER market. Meanwhile IOUs operating in progressive DER markets like California have made unprecedented progress in stimulating DER market growth, but much of this has occurred under a compliance mindset. It has not principally been driven by natural business initiatives. Consequently, even IOUs in California rely more on regulatory mandates rather than financial drivers to integrate DERs into their business operations. In order to overcome this conflict between the goals of policymakers and regulators on the one hand and the goals of IOU shareholders on the other, the major stakeholders involved in the power industry’s future must cooperate to realign IOUs’ financial incentives to see DER growth as an opportunity rather than an existential threat. Working in tandem to create new business models supported by performance based regulation, policymakers, IOUs and other major energy stakeholders can potentially create a regulatory compact for the future—a regulatory compact that provides new valuable energy services for consumers while unleashing new revenue generating opportunities for utilities. Transforming the regulatory compact and utility business model of the 20th century without creating unintended consequences will be a challenging feat. Therefore, regulators and utilities will need to work in concert to develop a cogent transition plan.

9

Chapter 2

An Overview of Investor Owned Utilities I. A Brief History of Investor Owned Utilities

A. The Power Industry: Origins The origins of the electric utility industry emerged as a result of two key inventions by Thomas Edison: the introduction of the incandescent light bulb in 1879 and the emergence of the “world’s first central generating power station in New York City’s financial district” in 1882.2 Shortly after the arrival of centralized power, Thomas Edison and other innovative entrepreneurs took advantage of this new power source and created a variety of new electrical machines for commercial, industrial and residential applications. Within a few years, electricity now began to power manufacturing processes, public transportation, heating, etc. In short order, Edison’s innovations created the initial push toward electrification. But it would take another innovator to shape the “economic, structural and regulatory framework“ that would give rise to the modern vertically integrated electric utility companies that came to dominate the 20th century and still play an essential role in today’s electric power industry.3 His name was Samuel Insull.

B. Industry Growth Through Economies of Scale Samuel Insull, formerly Thomas Edison’s principal assistant in charge of Edison’s finances and business strategy, understood that growth in the power industry necessitated massive investment in new generation technology and infrastructure, mass consumption and industry consolidation. In other words, he realized that industry growth required his business to attain cost leadership position vis-à-vis his competitors through economies of scales. Economies of scale refer to the overall cost benefits a business attains from increasing the scale of its operations.4 As a business increases its economies of scales, it will reduce the cost of each unit produced as the total volume of output rises.5 Figure 2.1 below demonstrates how increased output reduces the average total cost for the industry. Growing asset heavy industries can significantly reduce these fixed costs by spreading them out over a larger quantity of output. During the early to mid 20th century, the power industry lived through a “decreasing cost era” that hinged on increasing economies of scale, and as

2 “Emergence of Electrical Utilities in America,” The National Museum of American History. http://americanhistory.si.edu/powering/past/h1main.htm 3 Lambert, Jeremiah D. The Power Brokers: The Struggle to Shape and Control the Electric Power Industry. MIT Press, 2015, 1. 4 Porter, Michael E. Competitive strategy: Techniques for analyzing industries and competitors. Simon and Schuster, 1980, 7. 5 Ibid.

10

utilities reduced the average total cost of its business operations, they were able to pass these savings on to their consumers.6

Figure 2.1: Growing Economies of Scale Reduces a Company’s Average Total Costs

Source: Investopedia

C. Transmission and Distribution Network Creates Mass Market Potential

A low cost business strategy through economies of scale also “requires a relatively high market share.”7 Insull’s creation of a vast unprecedented alternating current (AC) transmission system permitted generated electricity to reach ever greater distances and therefore immensely expanded the range of his company’s captive market. Before Insull, a central station’s generated electricity delivery radius exceeded no further than one-mile from the generation source.8 Even with additional steam turbine generators creating electricity more efficiently, electric power flowing over distribution lines would degrade quickly under Edison’s direct current system. With the introduction of AC technology, power stations could now break through this barrier and electricity could travel great distances “without experiencing much degradation.”9 This new transmission and distribution (T&D) system allowed utilities to reach every end user in its service area. By allowing power companies to reach every single end user in its extended service area, the T&D system may have been the most important element in permitting the scaling up of production. Consequently, the creation of this system greatly increased Insull’s marketing and distribution advantages relative to his

6 Olson, Wayne. The A to Z of Public Utility Regulation. Public Utilities Reports, Inc, 2015, 182. 7 Porter, Competitive Strategy, 36. 8 Lambert, The Power Brokers, 6. 9 Emergence of Electrical Utilities.

11

competitors and was one of the factors that led to Commonwealth Edison obtaining a virtual monopoly in the greater Chicago area.

D. A Capital Intensive Industry Requiring High Market Share and Large Revenue There is, however, a significant challenge in building and maintaining a large T&D network: its cost. While Insull’s scalable steam turbines and T&D system allowed his company to scale up power production and reach an ever larger audience compared to his competitors, it required enormous capital investments. As Michael Porter notes in his seminal work Competitive Strategy, a low cost position through economies of scale “requires heavy upfront capital investment, aggressive pricing and startup losses to build market share.”10 Insull employed all of these tactics, but the large capital investments required to secure economies of scale are still a key trait of the industry even to this day. In order to reduce overall costs and pass on price savings to the customer, Commonwealth Edison had to attract large amounts of capital to acquire the enormous cost reducing assets. To accomplish that, the company needed a large, steady revenue stream and profit margin to cover these investment expenses. Insull constantly found ways to increase his revenue intake through an aggressive customer acquisition strategy, and, as we’ll see later, through political regulation. Although Insull had the capacity to produce power in bulk and the potential to reach a large market, he needed to attract more customers to his company. Insull understood that his generation capacity needed to be large enough to provide peak demand, which tends to occur in the early evening.11 While obtaining enough power to provide peak power is necessary to meet the needs of a service area’s energy demand, it also means that the most expensive portion of a utility company’s generating assets—those providing peak power—will remain inactive and unproductive for much of the day. To compensate for this dilemma, Insull sought to maximize the load factor of all of his power plants i.e. the average time each plant generated electricity. The power plants’ assets—the turbines, pipes, wires, and boilers—still need to be paid off even when the plant is sitting idle.12 Insull astutely understood that profit margins hinged upon increasing each power plant’s average time of use—i.e. the load factor. According to Insull, “the nearer you can bring your average to the maximum load, the closer you approximate the most economical condition of production, and the lower you can afford to sell your current.”13 In general, this required diversifying his customer base in order to include a variety of consumers based on time of use and volatility of use. To raise the load factor, Insull needed more customers during off peak hours,

10 Porter, Competitive Strategy, 36. 11 Lambert, The Power Brokers, 11. 12 Ibid. 13 Lambert, The Power Brokers,12.

12

less customers with volatile usage patterns and a more diverse group of customers whose time of use varied.14 Insull also made use of a new innovative demand meter created by Arthur Wright that allowed him to determine the actual use and the degree to which each consumer utilized his installed capacity. In other words, each consumer’s monthly bill revealed his disaggregated portion of the fixed costs of the utility company that arose from the generating capacity the utility provided to meet peak load.15 In measuring the quantity of electricity each user consumed, it also reflected each user’s contribution toward a central plant’s operating costs. In short, with the arrival of the Wright meter, monthly charges suddenly seemed more transparent, fair and reasonable. Additionally, Wright’s demand meter revealed that two customers with the same installed capacity (let’s say, 15 lamps as example) could have vastly different cost profiles.16 As an example, customer A only uses her electricity three times a year, while customer B uses her electricity every single day.17 Since the company must “invest so heavily in equipment” to provide peak load capacity for each customer, it actually costs more to serve the customer who uses her lamps only three times a year than the customer who leaves her lamp running each and every evening.18 Hence, the Wright meter concretely validated Insull’s growth paradigm: as customers increased their consumption, costs declined. Thus, the Wright meter reinforced Insull’s general growth strategy: to attract more end users and increase revenue through mass consumption.19 Ultimately, the Wright meter further encouraged Insull to capture a larger audience, abandon unprofitable power plants and confirmed a monopolistic system as the best path to push down both company expenses and service pricing.20

E. Natural Monopoly Leads to Regulatory Compact Despite Insull’s success vis-à-vis his competitors, remaining competition still undermined industry growth and subverted the benefits of economies of scale. Intense rivalry split market share, meaning that no single company could produce sufficient revenue to justify investment in larger turbines and an expanding T&D system.21 In order to overcome this limitation, Insull began to buyout competitors and consolidate the electricity market. This allowed him to absorb more customers and escalate his company’s load factor—that is, to increase the average use of his plants

14 Hughes, Thomas Parke. Networks of power: electrification in Western society, 1880-1930. JHU Press, 1993., 220 15 Ibid. 16 McDonald, Forrest. Insull: the rise and fall of a billionaire utility tycoon. Beard Books, 2004, 67. 17 Ibid. 18 Ibid. 19 Lambert, The Power Brokers, 12. 20 Lambert, The Power Brokers, 13. 21 Lambert, The Power Brokers, 13.

13

through customer acquisition.22 Despite Insull’s initial successes through free market competition, the destabilizing threat of competition persisted. Through parallel experiences in the railroad industry, some economists, politicians and industry insiders understood that certain asset heavy industries “exhibiting economies of scales” represented what some would deem as “natural monopolies.”23,24 While most consumers and politicians abhorred the potential for market abuse inherent in a monopolistic system, the exorbitant investment requirement in building a large T&D network tied to enormous turbine generators meant that “duplication” would be wasteful, raise both business costs and consumer prices and create an unstable bankrupt conducive business climate.25 At the same time, while some of the most powerful political, consumer and financial stakeholders accepted the electric utility industry as a natural monopoly, both investors and Progressive era politicians agreed upon the need to create a robust regulatory framework for the industry. The guiding principles that underpinned this regulation came to be known as the regulatory compact. Under the auspices of the regulatory compact, utility companies and consumers reached a bargain with state political committees providing regulatory oversight over utility companies. To this day, the basic features of the regulatory compact remains intact. The terms are as follows: each utility company in a given service area is “granted a monopoly,” and it is permitted to price its electricity at an approved rate that provides a fair return on its investments.26 In return for this favorable arrangement, the company must provide “low-cost, reliable” electricity to all of the consumers residing in its service area as a public good.27 In order to hold the utility accountable to this arrangement, a state appointed public utility commission (PUC) possesses ultimate authority over approving the utilities’ annual investment decisions and consumer pricing.28 For investors, regulation provided enormous financial benefits. In many markets, fierce competition pushed electricity prices under marginal costs—driving many power companies into insolvency.29 Protection from competition assured a steady and

22 Emergence of Electrical Utilities. 23 Emergence of Electrical Utilities. 24 Roberts, David. “Utilities for dummies: How they work and why that needs to change,” Grist. 21 May 2013. 25 Emergence of Electrical Utilities. 26 Ibid. 27 Ibid.28 A monopoly may have a perverse incentive to abuse its market power in a way that serves its own profit maximizing agenda in lieu of maximizing consumer utility. A monopoly seeking to increase profits can merely raise its price or reduce its output. Regulators can ensure that utility monopolies keep price and quantity in line with the lowest point of the firm’s average total cost curve in order to maximize public benefits to consumers and society at large. See Olson, Wayne. The A to Z of Public Utility Regulation, 31-34. 29 Brooks, Cameron. "The Periodic Table of the Electric Utility Landscape: A Series of Visual Tools for Enhanced Policy Analysis." The Electricity Journal 28.6 (2015): 82-95, 84

14

dependable revenue stream which guaranteed return on investment. As a result, capital costs declined and credit quality soared allowing cheaper financing, which was critical for such a “capital intensive and highly leveraged industry.”30,31

F. The Hope Case Creates Modern Ratemaking Paradigm Then, in 1944, the Supreme Court passed a ruling that left a momentous legacy on the utility industry’s ratemaking patterns. The ruling in the Federal Power Commission v. Hope Natural Gas Co. case proffered even greater financial protection to IOUs’ investment decisions by approving a new ratemaking standard that bundled utility capital expenditures along with a guaranteed rate of return into the customers’ rates.32 This ratemaking system allowed utilities to minimize risks to shareholders, and, hence, more effectively attract capital. However, as will be explained later, this ratemaking system embedded an incentive structure within the business model that favors the deployment of expensive capital projects (i.e. grid infrastructure) as a means to boost profit margins. While favorable to shareholders’ interests and the societal need for cheap, reliable and ubiquitous electrification in the 20th century, this incentive structure may not always adequately serve the interests of a society demanding a nimbler, more efficient and cleaner grid.

G. The Mid 20th Century: The Industry’s Boom Phase As utility CEOs like Insull relinquished regulatory authority to state commissions, conditions for industry growth boomed. Under this new system of regulatory protection, the industry quickly consolidated into vertically integrated monopolies all over the country, and throughout the 20th century, most of the country’s generation capacity and T&D system arose under this arrangement. The industry realized greater economies of scale, reduced costs in conjunction with rising demand while curtailing undesirable factors—like competing infrastructure—averse to industry growth.33 In sum, regulation accelerated the industry’s growth rate during the middle of the 20th century.

H. The Late 20th Century: Industry Maturation, Oil Shocks, and PURPA

During the 1970s, the industry began to undergo some economic changes. Firstly, as the industry entered the 1970s, the industry no longer achieved the same cost reducing benefits from boosting economies of scale. Figure 2.2 demonstrates how the electric industry’s increasing output beyond 20 billion kWh provided no further cost reductions for the industry at large; the cost curve remained completely flat beyond 20 billion kWh of generated power. Secondly, the two major oil shocks of the 1970s motivated utilities to lobby for the inclusion of fuel costs into customers’ electricity rates in order to attain greater financial security from volatile fuel 30 Brooks, The Periodic Table of the Electric Utility Landscape, 85. 31 Lambert, The Power Brokers, 17. 32 Brooks, The Periodic Table of the Electric Utility Landscape, 87.33 Ibid.

15

expenses.34 Within two decades, fuel costs were included into most utility customers’ rate cases.35 Moreover, during the 1970s, a greater focus on environmentalism and energy security in public policy began to place higher priority in clean and efficient energy generation.36 Then, with the passage of the Public Utility Regulatory Policies Act of 1978 (PURPA), the federal government pushed to end the total monopolization of the power generation part of the electric industry. It sought to promote the development of a “non-utility power sector” comprised of independent power producers competing side by side with utilities.37 PURPA encouraged energy efficiency through the growth of cogeneration facilities as well as other alternative energy sources such as solar power production. Over the past forty years, PURPA has played an essential role in promoting the deployment of small renewable energy production facilities under 80 MW.38

Figure 2.2: Declining Economies of Scale for IOU Industry39

Source: Christensen, L.R. Green.

34 Brooks, "The Periodic Table of the Electric Utility Landscape,” 87. 35 Ibid. 36 Ibid.37 Campbell, Richard J. “Customer Choice and the Power Industry of the Future” Congressional Research Service. September 2014, 1.38 “What is a Qualifying Facility?” Federal Energy Regulatory Commission. 30 June 2016. 39 Christensen, L.R. Green, W.R., 1976. Economies of Scale in US Electric Power Generation. J. Polit Econ 74 (4), 671.

16

I. The 90s: An Era of Industry Restructuring With the introduction of the Energy Policy Act of 1992 and the creation of the Federal Energy Regulatory Commission (FERC) in 1996, the federal government urged states to promote open wholesale market access between states and overall greater levels of competition in the energy utility sector. Throughout the 1990s, 16 states voluntarily embraced this shift toward restructuring and as of 2011, non-utility power producers generated as much as 40% of the electricity consumed in the United States.40 In order to manage and ensure more competition in electricity generation, participating states developed Regional Transmission Organizations (RTOs). RTOs seek to create transparent, non-discriminating and open wholesale electricity markets within its regional interstate service territory. In general, the RTOs have created a system that allows non-utility generators to compete more fairly with IOU owned generation facilities.

Figure 2.3: Regional Transmission Organizations in the U.S.

Source: FERC As a result of these changes, the traditional vertically integrated IOU industry fragmented into two more distinct entities in these 16 states: restructured utilities (an assortment of distribution companies) and retail utilities (which function as 40 Campbell, “Customer Choice and the Power Industry of the Future,” 2.

17

“commodity energy brokers”).41 With the exceptions of California and Texas, the regions most devoted to restructuring have been the Midwest, Mid-Atlantic and New England states. The rest of the country’s IOUs operating in the Southern or Western United States continue to adhere to the age old vertically integrated model pioneered by Insull.

J. Present Challenges for IOUs and with Current Utility Business & Regulatory Model

a. Declining Electricity Use Throughout the 20th century, economic growth heavily relied on substantial amounts of electricity. However, over time, GDP growth has come to be less reliant on electricity use. Between 1975 and 1995, as electricity use declined, the two variables moved in synchrony. Since the beginning of the 1990s, GDP growth steadily surpassed electricity use, which now appears to be flattening to about a 0.9% growth rate. The EIA projects that this will continue to be a long run trend. While this slowdown is partially a result of macroeconomic factors—such as a slowing population growth and outsourcing of heavy industry—it is also a result of improvements in energy efficiency.42 If this trend moves forward in line with the EIA’s estimates, there will likely be less overall demand for electricity in the coming future. This outcome could challenge the IOUs’ current investment and profit making strategies, which heavily rely on state regulators to sign off on the need for such capital spending.

Figure 2.4: Declining Electricity Use Now a Long Term Trend

Source: Energy Information Administration

41 Brooks, "The Periodic Table of the Electric Utility Landscape,” 87-88. 42 “U.S. Economy and Electricity Demand Growth Are Linked but Relationship Is Changing,” U.S. Energy Information Administration. 22 March 2013.

18

b. Societal and Consumer Aims for Energy in 21st Century Over the past forty years, consumer attitudes and public policy have demonstrated greater concern for environmental issues, especially concerning energy production. Changing environmental attitudes continue to create stricter legal and regulatory standards from state and federal governments. Meanwhile, innovative companies are seeking to capitalize from stricter clean energy requirements and growing consumer demand for clean energy. An ongoing survey conducted between 2002 and 2010 by the Natural Marketing Institute’s (NMI) Lifestyles of Health and Sustainability (LOHAS) Consumer Trends Database®, demonstrates that 80% to 90% of consumers contacted in the survey “care about renewable energy.”43 The survey reveals that about 80% of consumers increasingly care about using renewable energy in order to protect the environment. With that said, if given the choice for renewable sources of electricity at a higher price, many consumers in the survey demonstrate a degree of price sensitivity. In 2010, 69% of consumers stated that they “cared about the environment,” but that purchasing decisions were ultimately based on price.44 Twenty-six percent of the consumers said they would willingly pay “$5-$20 extra each month to have some of their power” derived from renewable sources.45 Finally, only 16% of consumers in the survey demonstrated a willingness to “pay more than 20% for products that are produced sustainably or in an environmentally friendly” manner.46 According to these trends, IOUs and state regulators will increasingly face more pressures from consumers and legal standards to simultaneously maintain affordable electricity, while also offering more environmentally friendly forms of electricity. Unfortunately, the IOUs’ outdated business model and regulatory framework may limit its potential to effectively innovate and meet the growing demand of its consumer base. As a result, in localities where utilities and lawmakers fail to cater to this demand, third party companies will attempt—where possible—to meet this demand. In the future, distributed energy resources, when priced appropriately, may play a significant role in the household of consumers. If that is the case, it could pose a significant threat to IOUs’ business model. 43 Bird, Lori and Jenny Sumner. “Consumer Attitudes About Renewable Energy: Trends and Regional Differences,” National Renewable Energy Laboratory, 6. 44 Bird and Sumner. “Consumer Attitudes About Renewable Energy,” 12. 45 Ibid. 46 Ibid.

19

c. Growing Threats: Demand Side Management and Distributed Energy Resources

At the same time the growth of electricity use has leveled out at less than one percent per annum, utility customers have demonstrated greater interest in demand side management through the adoption of energy efficiency appliances, demand response programs and the use of distributed energy resources—such as residential solar panels. Figure 2.5 shows how government standards have forced appliance manufacturers to improve their energy efficiency by more than two-thirds in the past forty years. All of these distributed energy resources and energy efficiency initiatives represent a threat to utilities by reducing its revenue stream.

Figure 2.5: Evolving Energy Efficiency Standards

Source: Energy Information Administration On a societal and consumer basis, many argue that distributed energy resources and demand reduction initiatives—such as energy efficiency improvements, demand side management, distributed rooftop solar systems and residential energy storage systems—have an important role to play in mitigating climate change, reducing pollution and offering cost savings to certain consumers. Many public policies, incentives, subsidies and utility commissions have forced utilities to adopt these measures—even though they run counter to the principle that undergirds their traditional cost of service business model: mass consumption. The industry’s current trend—slowing growth and a declining revenues—serves as a signal that IOUs are facing a growing competitive threat. Some analysts even believe that these distributed energy resources may pose an existential threat to the IOU industry.47 In fact, if we look at the historical credit rating trends of the utility industry 47 Kind, Peter. “Disruptive Challenges: Financial Implications and Strategic Responses to a Changing Retail Electric Business,” Edison Electric Institute, 2013, 11-12.

20

listed in figure 2.6, it becomes apparent that a combination of economic trends, business model and regulatory changes and increased competition over the past few decades have had a depressing impact on the industry’s credit ratings. The arrival of additional competitive forces could further pull down the industry’s credit ratings, raise the cost of capital and reduce “credit availability and investor receptivity to the sector.”48 Since the electric utility industry is such a highly leveraged industry, poor investment grades from ratings agencies could significantly “reduce the industry’s access to low cost capital” that it has relied upon historically to make needed improvements to the grid.49 It could also serve, according to some analysts, as a foreboding signal for worse things to come.

Figure 2.6: IOU’s Historical Credit Ratings

Source: EEI, Standard & Poor’s, Macquarie Capital

In fact, according to a report commissioned by the Edison Electric Institute (EEI)—the IOU industry’s leading think tank and lobby group—the continued growth of distributed energy resources could eventually undermine the strategic and financial viability of the utility business model.50 Under this potential scenario, revenues and profits would decline and credit quality would plummet leading to a higher cost of capital. Higher capital costs would require IOUs to raise retail rates. As more customers reduce their usage or defect from the grid, the utility would have less

48 Kind, “Disruptive Challenges,”, 9-10. 49 Kind, “Disruptive Challenges,” 9. 50 Ibid.

21

customers to cover the costs of its fixed investments. It would have to raise rates to cover these fixed costs and the remaining customers would be required to shoulder a greater burden of the utilities’ investments. Many of these remaining customers would likely react to these growing rate hikes by retrofitting their homes and adopting solar panels as a cost competitive alternative. Some have referred to this phenomenon as the utility industry’s potential “death spiral.”51

Figure 2.7: The So Called Utility Death Spiral

Source: EEI The figure above represents a worst case scenario. While the aforementioned disruption may not unfold with such severity, the IOU industry cannot ignore the threat posed by these competitive forces. To overcome this dilemma, many analysts believe the IOU industry will eventually need to adapt their business models. New business models could permit IOUs to take advantage of new opportunities and to capture new markets and revenue streams that could be a source of profit rather than a disruptive threat. Specifically, some argue that IOUs should compete or offer services that work in line with trends occurring along the consumer side of the distribution meter to prevent such an outcome. This approach would require managers, shareholders and regulators to develop new business models and regulatory frameworks to operate beyond its duty as a commodity provider of centralized power. It would also require the creation of new profit making incentives and scenarios for utilities to enter into the distributed energy market.

51 Kind, “Disruptive challenges,” 11-12.

22

d. Investor Owned Utilities’ Financial Incentives

i. Profit Maximization through Capital Spending and Asset Growth

Ever since the famous Hope Case ruling “invested capital” became the main criterion encouraging IOUs’ investment habits.52 Indeed, utility executives and shareholders have a vested interested to boost capital expenditures as a means to enhance profits since all of these fixed costs are automatically included into the rate base. Here is the ratemaking formula that most utilities still use today:

• 𝑅𝑒𝑣𝑒𝑛𝑢𝑒 = 𝐴𝑠𝑠𝑒𝑡𝑠 ratebase 𝑥𝑅𝑎𝑡𝑒𝑜𝑓𝑅𝑒𝑡𝑢𝑟𝑛 + 𝑂𝑝𝑒𝑟𝑎𝑡𝑖𝑛𝑔𝐸𝑥𝑝𝑒𝑛𝑠𝑒 • 𝐶𝑢𝑠𝑡𝑜𝑚𝑒𝑟𝑅𝑎𝑡𝑒𝑠 = 𝑅𝑒𝑣𝑒𝑛𝑢𝑒 + 𝐹𝑢𝑒𝑙𝐶𝑜𝑠𝑡𝑠53

As you can see, the utilities projected customer rates not only include all of its costs—fixed, operational and variable costs—but also include a predetermined rate of return attached to its capital investments. Because utilities’ capital spending offer a compounded growth in relation to its rate of return, these companies have a perverse incentive to spend on expensive supply side “generation and transmission” projects in lieu of “demand reduction, consumer side initiatives” and other such alternative demand side solutions.54 On the contrary, as our historical overview demonstrates, utilities prefer to invest in projects that boost economies of scale and mass consumption. Between 2003 and 2014, utilities’ capital spending more than doubled and residential rates surged by 40% (see figure 2.8). This is problematic—and some would argue a wasteful allocation of resources—since the benefits associated with increasing economies of scale already reached its limits in the 1970s. While a focus on increasing scale may have been ideal in the early to mid 20th century, this growth strategy is no longer as effective nor ideal in an era that places greater priority on social, environmental and consumer value added factors. In contrast to more competitive sectors, the electric industry’s static business model offers no intrinsic incentive for efficiency or for innovative practices that could produce large benefits to society at large. As will be argued later, the adoption of more distributed energy resources may prevent the need to invest as heavily in such expensive centralized generation facilities and T&D expansion projects.

52 Brooks, "The Periodic Table of the Electric Utility Landscape,” 87. 53 Brooks, "The Periodic Table of the Electric Utility Landscape,” 89. 54 Brooks, "The Periodic Table of the Electric Utility Landscape,” 89-90.

23

Figure 2.8: IOU Industry Capital Spending & Retail Rates

Source: EEI (spending), Department of Energy (prices), The Wall Street Journal

ii. Profit Maximization Through Sales and Revenue Growth Like all businesses, IOUs have an intrinsic incentive to boost its sales. After all, extra sales boost revenue and more revenue—once expenses are deducted—will create a heftier bottom line. However, in the case of utilities, regulators set the rates to meet the utility’s revenue requirement. For instance, using the regulatory principles of a cost of service rate of return, the PUC will attempt to set rates so that gross revenues “equal prudently incurred actual costs for the service proved plus a fair return on invested capital.”55 In setting the rate, regulators typically “work backward”—that is, they start with the “required revenue” amount they seek to achieve and then divide it by the projected quantity of power sales they predict in their forecasts.56 For example, if required revenue is $200 and estimated sales are 1,000 kWh, regulators will set the average rate at 20 cents/kWh.57 After regulators establish the average rate, it tends to stay in place for about “two to five years” before regulators will repeat the procedure.58 However, creating a static regulated rate that endures unchanged for long periods of time “encourages larger sales by utilities and discourages their energy efficiency efforts.”59 Because rates are

55 Fox-Penner, Peter. Smart power: Climate change, the Smart Grid and the Future of Electric Utilities.

Washington (2010), 181. 56 Ibid. 57 Ibid. 58 Ibid. 59 Ibid.

24

set in kilowatts per hour, the more kilowatt hours a utility sells will equate to larger revenues for the company. Therefore, utilities will often attempt to sell beyond the projected quantity estimated by the regulator. After all, more sales will eventually translate into larger profits. Moreover, larger sales, which signals business growth, will also please a company’s investors and shareholders—especially since such growth justifies the need to construct more infrastructure to meet rising demand.60 As a result of this sales incentive, many IOUs tend to dislike distributed energy resources, energy efficiency and other demand reducing entities or initiatives. Consequently, until a utility’s regulation, business model and financial incentives are adapted, utility shareholders and board members may continue to view demand side management, energy efficiency and distributed energy resources as source of competition rather than a business opportunity. 60 Fox-Penner, Peter. Smart power, 183.

25

Chapter 3

Current Industry Structure & Competitive Forces

A. Definition of Investor Owned Utility Electric Industry Today To this day, many IOUs still operate in all segments of the electricity value chain—from generation, transmission, distribution to retail. From the perspective of our analysis, I will refer to this entire value chain—in aggregate or in its separate components—as centralized power. Regardless of the market they operate in, the IOUs—integrated or restructured—in some way shape or form, generate, procure and distribute centralized power to a variety of industrial, commercial and residential end users. The structural analysis of the industry that follows will investigate and highlight the competitive forces emerging outside of the traditional segments of this value chain. It will especially demonstrate how distributed energy resources—represented by photovoltaic solar panels in this analysis—will be playing a significant disruptive role in the IOUs’ market power, industry structure and traditional business model.

B. Structural Analysis of the Investor Owned Utilities

In this current section, I will highlight the competitive forces and disruptive threats emerging against IOUs. Since the 1970s, IOUs faced competition from IPPs seeking to provide non-regulated power mostly to industrial and commercial end users. Now a new wave of competition has emerged in the form of distributed roof top solar companies. Unlike the earlier wave of competition, which focused more widely on industrial and commercial users exploiting cogeneration technology, providers of distributed roof top solar systems include residential end users as one of their primary markets. In the following section, we will look at how distributed solar providers represent competitive entrants into the electricity market by circumventing the utilities relationship with consumers and providing distributed power directly to end users. To analyze this market trend, I will utilize Michael Porter’s paradigm for structural analysis of industries. This analysis will particularly focus on the economic and regulatory factors that raise and lower barriers of entry into state electric markets.

26

i. Threat of Entry into IOUs’ Market According to Porter, the threat of entry in any given industry hinges upon the barriers of entry in place, as well as the organized response from incumbent competitors an entrant may face upon entering into the industry.61 In the analysis that follows, I have added additional variables unique to the electric utility industry to create a more detailed framework specific to the industry under consideration. The main barriers to entry include the following:

a. Economies of Scale As stated earlier in the chapter, IOUs centralized production of power utilizes economies of scale to reduce its average total costs of generating and distributing electricity. However, in general, economies of scale may create both barriers and opportunities for third party solar entrants facing off against incumbent IOUs. Since IOUs operate with scale efficiencies in the production of electricity, the distributed roof top solar industry will face cost challenges against the incumbent IOUs in certain markets across the United States where power prices remain lower than average (see table 3.1). And, generally speaking, the industry will need to incur heavy capital spending requirements to attain the cost benefits of scale. Many vertically integrated IOUs operating in traditionally regulated markets may have retained more cost benefits from scale vis-à-vis restructured IOUs that were forced to divest their generation assets. In general, markets with vertically integrated utilities offer lower rates than utilities operating in competitive markets.62 Therefore, markets with vertically integrated IOUs—whether through price competition or regulatory impediments—will likely retain stronger barriers to entry. These cost barriers will generally be stronger in most—though not all—states in the south, northwest, lower plains and upper plains. While residentially scaled solar does not experience scale efficiencies in the production of electrons, the PV panels used in such markets incur the benefits of scale economies during its manufacturing phase. As the prices of PV modules have declined from increased economies of scales, so too have PV sales and the level of PV installations (see figure 3.1). As solar PV prices continue to decline from technological improvements and scalability, third party solar operators should attract more clients and further build its customer base. This will create competitive pressures in certain markets where consumers have greater financial incentives to

61 Porter, Michael E. Competitive strategy: Techniques for analyzing industries and competitors. Simon and Schuster, 1980, p. 7. 62Johnston, David Cay. “Competitively Priced Electricity Cost More, Studies Show,” The New York Times. 06 November 2007.

27

switch over to a more cost competitive source of electricity—especially in regions that charge end users higher retail rates.

Figure 3.1: Solar Prices & Installation Rates

Source: GTM Research, SEIA Moreover, economies of scale no longer produces cost reduction benefits for IOUs. Since the end of the IOUs “decreasing cost era” by the 1970s, the industry entered into an increasing cost era. Now when a utility builds a new power plant or expands its distribution network, the utility must raise its rates to cover these investments. These rate increases (see figure 2.4 in the previous chapter) may impel some customers to view a distributed solar system as a more cost competitive source of electricity—especially in regions that charge end users higher retail rates.

b. Electricity Retail Rates

Regional electricity retail rates may create significant entry barriers—or opportunities—for third party solar operators seeking to establish beach heads or increase market share in certain markets. Retail rates for electricity vary significantly in the United States. Where utility retail rates are lower than average, solar companies may be much more reliant on government polices to create the financial incentives for residential users to adopt solar panels. Meanwhile, high retail rates create an enormous incentive for third party solar companies to enter into a state’s market. As Christensen Associates highlights, “the ten jurisdictions that offer the highest rate of return when tax incentives are removed

28

are present in states with retail rates that are 42% higher than those of the next ten states.”63 Table 3.1 lists a selected sample of US states ordered by retail price. In a number of states, electricity rates (measured in cents per kilowatt hour) have climbed high enough that adopting solar for residential use has reached a point of grid parity, i.e. the point in which the levelized cost of electricity (LCOE) for distributed solar is less than or equal to the price of centralized grid power. According to a report by Greentech Media, as of 2016, retail pricing in 20 states allow many rooftop PV users to attain grid parity.64 Where local utility rates exceed 15 cents per kilowatt hour, residential solar often becomes price competitive with grid power—granting certain customers the opportunity to save money by producing their own electricity.65 Moreover, if we assume that higher retail rates are correlated with higher wholesale costs, then states with higher retail rates could be appealing for those seeking higher net metering rates—even if the net metering credit offered in some states is pushed below the retail rate. 66 This means that utility companies will most likely face greater competitive threats in these jurisdictions where fundamental pricing trends will impel residential users—even before artificial subsidies are accounted for—to adopt solar panels as a means to save money on their monthly utility bills. 63 Olson, Wayne. “Customer Choice, Solar 3rd-Party Operators, Utility Ratemaking, and the Future of the Electric Distribution Business,” Seeking Alpha. 29 February 2016.64 However, most of these grid parity figures depend on government tax benefits and subsidies (such as net metering). Munsell, Mike. “GTM Research: 20 States at Grid Parity for Residential Solar,” Greentech Media. 10 February 2016.65 Biello, David. "Solar Wars." Scientific American 311.5 (2014): 66-71.66 Olson, Wayne. “Customer Choice.”

29

Table 3.1: Ranking of States with Third Party Solar Operators by Retail Rate67 State 2015

Residential Rate (Cents/kWh)*

DG Solar Capacity (Watts) per capita (2016)

RTO Retail Competition

SolarCity SunRun Vivint Solar

Hawaii 29.61* 237.54 No No Yes Yes Yes

Connecticut 20.91* 46.51 ISO-NE Yes Yes Yes Yes

New York 18.57* 24.13 NYISO Yes Yes Yes Yes

New Hampshire 18.52* 19.77 ISO-NE Yes Yes Yes Yes

Massachusetts 19.81* 84.88 ISO-NE Yes Yes Yes Yes

Vermont 17.07* 88.01 ISO-NE No Yes No No

California 17.02* 93.47 CAISO No Yes Yes Yes

Rhode Island 19.29* 10.51 ISO-NE Yes Yes No No

New Jersey 15.97* 98.63 PJM Yes Yes Yes Yes

Delaware 13.46 57.40 PJM Yes Yes Yes No

Nevada 12.77 53.10 No No No No No

Maryland 13.91 54.59 PJM Yes Yes Yes Yes

Pennsylvania 13.84 12.4 PJM Yes Yes Yes Yes

South Carolina 12.42 1.88 No No No Yes Yes

Texas 11.64 5.42 ERCOT Yes Yes No No

Colorado 11.98 48.38 No No Yes Yes No

New Mexico 12.55 37.94 No No Yes No Yes

Arizona 12.18 98.11 No No Yes Yes Yes

Utah 10.98 20.33 No No No No Yes

Oregon 10.66 18.62 No No Yes Yes No

Washington 9.00 8.14 No No Yes No No Source: Wayne Olson, EIA, US Census As figure 3.2 below demonstrates, states in the Northeast, Southwest and California have electricity rates that significantly exceed this price threshold. Thus far, service areas that have surpassed this electricity rate threshold and/or offer strong solar radiation have seen the largest adoption of solar panels. 67 Olson, Wayne. “Customer Choice”. * These jurisdictions have retail rates at or above 15 cents/kWh, a price point that raises consumers’ incentive to use solar energy instead of utility power.

30

Figure 3.2: Nationwide Electricity Rates by County

Source: US News, Joshua Rhodes, University of Texas at Austin

c. Soft Costs Perhaps one of the biggest cost hurdles third party solar companies must overcome are soft costs. Soft costs are all of the non-hardware costs involved in the development of a solar project. These include financing costs, installation labor, permitting, inspection and interconnection fees, and customer acquisition costs. While China’s massive output of PV panels have significantly pushed down hardware costs, soft costs—accounting for as much as 64% of the total system costs—are now seen as the biggest hurdle in solar deployment.68

68 OfficeofEnergyEfficiency&RenewableEnergy.“SoftCosts,”http://energy.gov/eere/sunshot/soft-costs

31

Although the U.S. Department of Energy Sunshot Initiative’s soft cost program seeks to lower these costs through data analysis, training programs, business innovation and networking and technical assistance to state and local lawmakers, this will be a difficult challenge because of the United States’ “fragmented energy marketplace.”69 In the U.S. “there are over 18,000 jurisdictions and 3,000 utilities” that impose unique “rules and regulations” for solar projects.70 However, greater market growth, competition and more streamlined and standardized rulemaking and regulation could significantly lower these costs. For instance, in 2013, German solar soft costs were $0.33 per watt; at the same time, they were $1.22 per watt in the U.S.—about 3.7 times higher.71 As of the fourth quarter of 2015, total system costs for residential solar systems fell to $3.50 per watt—though soft costs actually rose by 7 percent due to customer acquisition costs.72 Therefore, soft costs are stymying efforts to reduce residential solar system costs and LCOE.73 The DOE’s Sunshot Initiative aims to reduce 69 US Department of Energy. “Soft Costs Fact Sheet,” May 2016. http://energy.gov/sites/prod/files/2016/05/f32/SC%20Fact%20Sheet-508.pdf 70 US Department of Energy. “Soft Costs Fact Sheet,” May 2016. 71 Calhoun, Koben and Jesse Morris. “Can the Cost of Solar in the US Compete with Germany?” Rocky Mountain Institute. 05 December 2013. http://blog.rmi.org/blog_2013_12_05_can_usa_solar_cost_compete_with_germany 72 Gallagher, Ben. “Pricing for Solar Systems in the U.S. Dropped 17% in 2015,” Greentech Media. 15 March 2016. http://www.greentechmedia.com/articles/read/Pricing-For-Solar-Systems-in-the-US-Dropped-17-in-2015 73 The DOE defines the LCOE as “the ratio of an electricity-generation system’s costs to the electricity generated by the system over its operational lifetime, given units of cents/kilowatt-hour (kWh).” A system’s LCOE is “sensitive to installed costs, O&M costs, local solar resource and climate, PV panel orientation, financing terms, system lifetime, taxation and policy.” For more information, see Sunshot Vision Study, 76: http://energy.gov/sites/prod/files/2014/01/f7/47927_chapter4.pdf.

Figure 3.3: Soft Costs for A Typical Solar Installation

Source: Department of Energy

32

residential solar system costs to $1.50 per watt by 2020—mainly by reducing soft costs. If the DOE is successful in this endeavor, the LCOE of solar PV systems in certain jurisdictions could become less than or equal to the LCOE of utility retail rates. This would mean solar systems in such localities would attain grid parity—that is, the cost of generating residential solar would be equal to or cheaper than consuming electricity from the grid. Greater collaboration and cooperation between the private and public sector and federal and local governments could reduce these costs. If so, as system costs decline, more jurisdictions may attain grid parity and residential solar development will accelerate even further. To see how this may play out, figure 3.4 shows how reducing residential system costs from $3.50 per watt to $1.50 per watt could enable jurisdictions in almost all of the lower 48 US states to attain grid parity.74 Therefore, if residential solar soft costs continue to decline, IOUs’ protective barriers may erode at an even faster rate.

Figure 3.4: Residential PV System Costs Reaching Grid Parity

Source: US News, Joshua Rhodes, University of Texas at Austin

d. Product Differentiation Companies attain product differentiation when they possess “brand identification and customer loyalties” from “advertising, customer service, product differences or simply being the first in the industry.”75 Most IOUs—at least at the distribution level—possess a captive market due to their monopolized status. As a result, these distribution utility companies have not had much incentive to offer differentiated energy products or services. Rather, they have merely sold their product to consumers as a commodity. Hence, brand identification stems mostly from its market power and monopoly status, not due to the nature of the product or service rendered.

74 Grid parity estimates often rely on assumptions such as net metering compensation at retail rates and other market enabling incentives like state and federal tax credits. 75 Porter, 9.

33

By contrast, solar companies have a wide range of means to differentiate their product from the commoditized electricity sold by utility companies. Firstly, solar energy produces its electricity from a renewable resource: the sun. The product’s “green” credentials have already won over many environmentalists seeking to consume cleaner forms of energy. Other conservative or libertarian minded consumers celebrate how the product would promote more energy independence and boost self-reliance.76 The introduction of affordable rooftop solar panels, therefore, would please a large group of consumers. While energy storage technologies needed to go “off-grid” are still fairly expensive, there are still consumers seeking to develop micro-grids and community solar projects as a means to limit full reliance upon centralized power. Increasingly, some third party non-utility companies are offering “value added services” to further differentiate their company offerings from incumbent utilities. In the future, we may see both distributed rooftop solar companies and utilities including more “value added” services into their business models as competition along the distribution edge of the grid becomes more intense. However, at the moment, lack of product differentiation is a highlighted weakness of the IOUs that lowers the barriers of entry into the power industry. Third party companies will likely exploit product differentiation in order to attract a customer base seeking clean energy and greater energy independence.

e. Capital Requirements Capital requirements to enter in the power industry have always been high, creating a significant barrier to entry. Utility companies often allocate billions of dollars annually toward capital expenditures, though, as previously mentioned, these costs are recovered when regulators set the electricity rates in each service area. By contrast, non-regulated electricity companies face greater challenges in meeting capital requirements, raising capital and recovering the costs of these investments. As a basis of comparison, SolarCity, a vertically integrated roof top solar company, spent $1.8 billion in capex in 2015.77 Since its IPO in 2011, SolarCity reported growing negative free cash flows. By contrast, in 2015, Con Edison spent $3.2 billion and Southern Co allocated $7.4 billion in capex. In the past five years, Con Edison sustained positive cash flows; Southern Co reported negative free cash flows in the past two years, but, with such large operating cash flows and regulatory protection, the company can afford to take on moderate losses. The graphs below demonstrate how high capital requirements can challenge an industry entrant’s financial health. 76 Biello, 70 77 Financial data in this section obtained from Morningstar.com.

34

Mature companies operating in a stable industry environment, on the other hand, can more predictably and easily translate these capital expenditures into a healthy return on investment. This large capital requirement could give some utility companies a distinct advantage in entering the distributed solar rooftop space. An entrant like SolarCity or SunRun, by contrast, must be willing and able to accept large—and potentially unrecoverable—start-up losses to enter into a new market and compete with an established industry. New entrants assuming loads of debt, reporting negative cash outflows and attempting to take on stable cash flow positive industries like the IOUs would likely require ongoing access to capital markets and favorable government subsidies to stay afloat. These high capital costs combined with fierce competition in the PV solar sector could put additional pressure on margins leading to bankruptcies, mergers and acquisitions and/or greater vertical integration.78,79 As an example, in 2011, Total SA, one of Europe’s largest oil companies, bought a 60% stake of Sunpower Inc.80 As part of the deal, Total offered Sunpower a $1 billion line of credit and with cheaper borrowing costs, it may be able to help Sunpower procure cheaper capital as needed.81 While these capital costs for solar companies seem like an insurmountable burden in the short run, if the residential PV industry potentially consolidates in such a way, the economics of residential solar continues to improve and residential solar assumes larger market share in the generation mix of a utility’s service territory, cash flows and margins could surge into healthier levels. Should this happen, capital outlays could one day become much more manageable for the residential solar industry.

78 Ali-Oettinger, Shamsiah. “More mergers and acquisitions to come,” PV Magazine. 22 July 2015. http://www.pv-magazine.com/news/details/beitrag/more-mergers-and-acquisitions-to-come_100020302/ 79 Groom, Nichola. “Solar company Sungevity to go public in reverse merger,” Reuters. 29 June 2016. http://www.reuters.com/article/us-sungevity-easterlyacquisition-idUSKCN0ZF1HS 80 Herndon Andrew, et al. “Total to Buy 60% of SunPower for $1.38 Billion in Solar Bet,” Bloomberg. 29 April 2011. http://www.bloomberg.com/news/articles/2011-04-28/total-to-begin-friendly-tender-for-up-to-60-of-sunpower-shares 81 Herndon Andrew, et al. “Total to Buy 60% of SunPower for $1.38 Billion in Solar Bet,” Bloomberg. 29 April 2011.

35

Figure 3.5: Capital Expenditures & Financial Performance of Pure Play Residential Solar Companies, USD in Thousands82

82 The emerging rooftop solar industry requires immense capital spending to fuel its growth. However, SolarCity and SunRun have reported negative free cash flows and negative profit margins since their respective IPOs. These companies will continue to rely on further injections of debt and/or equity from capital markets as well as government subsidies while they attempt to expand their market share vis-à-vis utility companies and develop positive cash flows. (Financial data from Morningstar).

36

Figure 3.6: Capital Expenditures & Financial Performance of IOUs, USD in Thousands83

83 These graphs demonstrate how the IOU industry also utilizes heavy capital spending to boost profits. Although utilities worry how widespread distributed solar adoption could undermine the industry’s profitability in the long run, so far their cash flows and margins remain at healthy levels. This financial strength gives IOUs a competitive advantage over its solar competitors. (Financial data from Morningstar).

37

Figure 3.7: EBITDA Comparison of Solar Providers & IOUs, USD in Thousands84

84 Rooftop solar companies’ growing negative EBITDA demonstrates that it suffers problems producing both profit and cash flow. As more customers adopt solar panels, these companies may be able to overcome these financial difficulties. In the meantime, this metric is a further demonstration of the solar industry’s over reliance on capital markets to stay afloat. (Financial Data from Morningstar).

38

f. Switching Costs

Switching costs are defined as one-time costs consumers endure when switching from one product to another. For some, this could include the cost of learning how to use the new system. Since most distributed solar users remain connected to the grid and use centralized power as a secondary source of power, switching costs should be scant. For customers seeking to go off the grid completely—which would require some sort of storage device synced to the solar panels—switching costs would likely be more significant for customers unwilling to deal with this cost. Switching costs could create a barrier in customer acquisition.

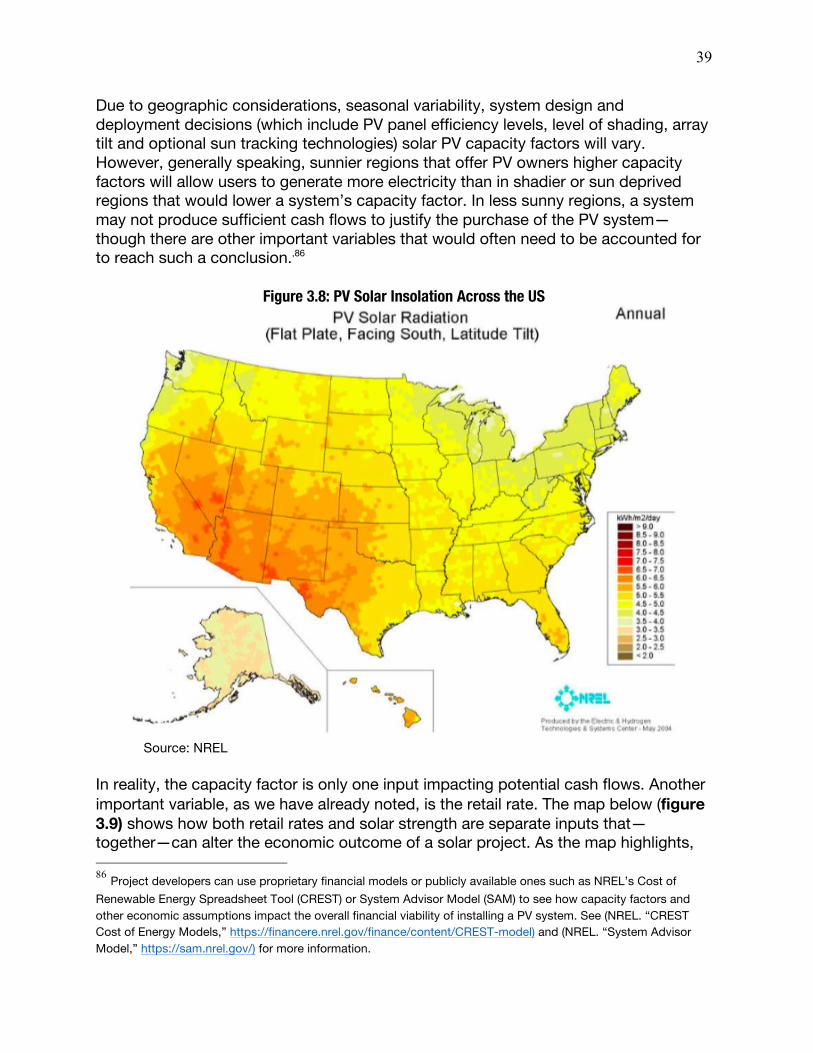

g. Solar Insolation and Capacity Factors Solar electricity produced by a photovoltaic system is an intermittent source of energy—that is, it only generates electricity while the sun shines. Moreover, as a result of geographic sunlight variations, PV systems produce different quantities of electricity in different regions. A map from NREL (figure 3.8) shows the PV solar radiation differentiation in the United States—and even variation between regions within each state. This variation in annual solar irradiance—or solar insolation—can significantly alter how much electricity a solar panel generates over the course of its productive lifespan. Since many PV owners receive financial compensation for the electricity they generate, this variation in solar irradiance can alter the financial performance of a PV system. Using a financial model, analysts can estimate the cash flows a PV system will produce over the course of its economic lifespan. One of the project performance assumptions an analyst can manipulate in the model is the system’s capacity factor. The capacity factor is a ratio that measures the amount of electricity a plant produces divided by the total amount of electricity it could have produced if it were hypothetically running 100% of the time over the course of a year. Basically, generating technologies with higher capacity factors have the capacity to generate more electricity during the course of a year.

• 𝐶𝑎𝑝𝑎𝑐𝑖𝑡𝑦𝐹𝑎𝑐𝑡𝑜𝑟 = DEFGHIJKLMNOPGEQPMQNRQHNJKLMQNRQHNHFNHFQPOGFMGF×TUVWLOGNXMQNRQHN

Table 3.2: Average Capacity Factors for Generation Technologies85 Plant Type Capacity Factor (%) Dispatchable Technologies Combined Cycle Gas Turbine 87 Advanced Nuclear 90 Geothermal 91 Non Dispatchable Technologies Wind 42 Solar PV 26

Source: EIA

85 Table 3.2 shows that solar PVs have a lower capacity factor in relation to other generation technologies. However, a solar panel that can store its surplus energy for later use would have a higher capacity factor. If manufacturers can reduce the cost of batteries, the economics of solar would become even more attractive.

39

Due to geographic considerations, seasonal variability, system design and deployment decisions (which include PV panel efficiency levels, level of shading, array tilt and optional sun tracking technologies) solar PV capacity factors will vary. However, generally speaking, sunnier regions that offer PV owners higher capacity factors will allow users to generate more electricity than in shadier or sun deprived regions that would lower a system’s capacity factor. In less sunny regions, a system may not produce sufficient cash flows to justify the purchase of the PV system—though there are other important variables that would often need to be accounted for to reach such a conclusion.,86

Figure 3.8: PV Solar Insolation Across the US

Source: NREL

In reality, the capacity factor is only one input impacting potential cash flows. Another important variable, as we have already noted, is the retail rate. The map below (figure 3.9) shows how both retail rates and solar strength are separate inputs that—together—can alter the economic outcome of a solar project. As the map highlights, 86 Project developers can use proprietary financial models or publicly available ones such as NREL’s Cost of Renewable Energy Spreadsheet Tool (CREST) or System Advisor Model (SAM) to see how capacity factors and other economic assumptions impact the overall financial viability of installing a PV system. See (NREL. “CREST Cost of Energy Models,” https://financere.nrel.gov/finance/content/CREST-model) and (NREL. “System Advisor Model,” https://sam.nrel.gov/) for more information.

40

California and Hawaii have both high retail rates and high solar insolation. Many areas in the southwest have lower retail rates. However, this is offset by the region’s strong annual solar irradiance and higher capacity factors. The northeast region is reversed; the retail rates are high and insolation levels are low. In these jurisdictions, PV systems can often produce sufficient cash flows in spite of the lower capacity factors. Finally, while Alaska has expensive retail rates, the state’s extremely low solar insolation levels pushes down the capacity factor for PV system. This would likely reduce the economic viability of solar in Alaska and help explain why Alaska has virtually no installed distributed solar capacity in the state. Hence, jurisdictions with extremely low solar irradiance can be a potential barrier for solar development.

Figure 3.9: Solar Insolation & Retail Rates Shape the Economics and Finance of Solar Systems

h. Key Government Policy Drivers Stimulating Residential Solar PV Markets Government policies have the power to reinforce or reduce barriers to entry to any given industry—especially highly regulated industries such as the electricity sector. For most of the 20th century, government regulation has greatly benefited the IOU industry. However, in the past 30 years, federal and state governments have designed standards and encouraged the development of renewable electricity. Some of these regulatory changes have also forced the utilities to slightly modify their business practices and have opened up the electricity sector to greater levels of competition.

41

In the following sections, I will enumerate and explain the most important government policies that have encouraged the development of the distributed PV solar market. h.1 Net Metering & Interconnection Standards Another potential market barrier to entry for any business is the need to access distribution channels to deliver its product.87 As it turns out, residential solar markets depend on access to a utility’s distribution network because most homeowners with solar panels can receive compensation for their surplus electricity through an arrangement made with their local utility companies. Through a policy known as net energy metering (NEM), owners of rooftop solar panels who receive authorization from their utility can connect their solar panels to the utility’s local distribution system. Through the NEM arrangement, a bidirectional meter is installed at the end user’s residence that measures both the inflows of grid power and outflows of surplus solar electricity sent back to the grid. During the course of each billing period, customers only pay for the net amount of electricity consumed at that time. For customers that produce ample solar power, this means they can, at times, “zero-out their utility bill.”88 During especially productive billing periods, they can even produce surplus power, which can then be credited toward future billing periods.89 While owners of rooftop solar panels—so long as they have ample storage capabilities—could in theory produce their own electricity off the grid all of the time—most potential consumers would need access to the grid and NEM in order to even make the investment a viable option.90 For this reason, quick and affordable interconnection to the grid—without debilitating red tape—and the capacity to sell net excess generation (NEG) through NEM to local distribution utilities is arguably the key market-enabling policy driver for residential solar markets.91,92 While 41 states offer NEM, the terms, limits and stability of NEM policy vary in each state and these variations impact the effectiveness of the NEM program as an market enabling tool. Interconnection best practices and standards also vary significantly. Historically, states that have had fewer NEM restrictions and laxer interconnection standards have developed more robust residential solar markets. 87 Porter, 10. 88 California Energy Commission & CPUC. “Net Energy Metering in California,” http://www.gosolarcalifornia.ca.gov/solar_basics/net_metering.php 89 Biello, 68 90 Due to high costs, battery storage technologies are too expensive for most residential solar users. 91 Interconnection is defined as the “technical rules and procedures allowing customers to plug into the grid.” Some states and municipalities have more onerous procedures to connect to the grid. These interconnection delays significantly raise the solar system’s soft costs. See www.freeingthegrid.org for more details. 92 Steward, D and E. Doris. “The Effect of State Policy Suites on the Development of Solar Markets,” National Renewable Energy Laboratory. November 2014.

42