the vietnam provincial competitiveness index 2009 · founded in 1963, the vietnam chamber of...

TRANSCRIPT

VNCI Policy Paper # 14

THE VIETNAM PROVINCIALCOMPETITIVENESS INDEX 2009

MEASURING ECONOMIC GOVERNANCE

FOR PRIVATE SECTOR DEVELOPMENT

Founded in 1963, the Vietnam Chamber of Commerce and Industry (VCCI) is a national organization that

assembles and represents the business community, employers, and business associations of all economic sectors

in Vietnam. The mission of VCCI is to protect and assist business enterprises, to contribute to the socio-economic

development of the country, and to promote economic, commercial, and technological cooperation between

Vietnam and other countries in the world.

VCCI’s two main functions are: (i) representing the Vietnamese business community through the promotion and

protection of the lawful, legitimate interests of Vietnamese enterprises and employers in domestic and international

relations; and (ii) promoting the development of business enterprises, facilitating cooperation among business

entities, and offering assistance in trade and investment, economic and technical cooperation as well as other

business activities of enterprises in Vietnam and abroad.

VNCI is a USAID-funded project that provides technical assistance to improve the business enabling environment

in top priority areas for government and business leaders. VNCI’s programs include: (i) policy advocacy using the

PCI data and other policy activities that assist the government and business sector to improve decision-making

and policy-making to achieve optimal economic performance and promote participation and transparency; (ii)

regulatory reform responding to the Prime Minister-led Decision 30 Master Plan to Simplify Administrative

Procedures, supporting the Office of the Government to design and implement reform strategies to clean up the

existing stock of regulations, apply regulatory quality control, and develop an effective regulatory framework and

policy coordination; (iii) infrastructure financing through revenue-backed bonds that leverage financial markets to

support the financing of a wide range of infrastructure projects through an effective and transparent financing

tool which takes the burden off the Government budget; and (iv) provincial reform activities that respond to

specific requests from reform-minded provinces that aspire to improve economic governance.

Visit www.pcivietnam.org or www.pci.com.vn to download this report and the PCI data

THE VIETNAM PROVINCIALCOMPETITIVENESS INDEX 2009MEASURING ECONOMIC GOVERNANCE

FOR PRIVATE SECTOR DEVELOPMENT

Primary Author and Lead Researcher:

Dr. Edmund Malesky

Research Team:

Tran Huu Huynh

Dau Anh Tuan

Le Thanh Ha

Le Thu Hien

Nguyen Ngoc Lan

FOREWORDThe Provincial Competitiveness Index (PCI) 2009 report represents the views of 9,890 Vietnameseenterprises and provides a rigorous analysis of economic governance and the regulatory environment inVietnam. Our objective since the first PCI report in 2005 has been to overcome the enormous problemsfacing enterprises in fully understanding the government’s regulations and requirements and, moreimportantly, to identify areas for improvement that will increase investment, jobs, enterprise performance,and economic growth. By the latest count, the People’s Committees of more than 40 provinces have usedthe PCI to conduct diagnostics, formulate action plans and decisions to improve performance, adopt bestpractices of high-performing provinces, and monitor progress in key areas. The consistency achieved byprovinces such as Binh Duong and Da Nang in maintaining excellent overall governance, and by Lao Cai andBen Tre in excelling in specific areas such as transparency and reducing informal charges during the last fiveyears of PCI surveys highlights the importance of leadership in making a dedicated commitment toimproving economic governance and business environment. This year’s report also emphasizes the increasingimportance that economic governance plays in investors’ decision making.

The PCI 2009 survey provides valuable information about the impact of policy reform initiatives at the centraland local levels, of which the Prime Minister’s Master Plan to Simplify Administration Procedures in StateManagement (known as Project 30) is the breakthrough regulatory reform effort in Vietnam. Its purpose is tosimplify a minimum of 30 percent of all administrative procedures at central, provincial, district, and communelevels to meet international business standards. Forty-two percent of our nationally weighted sample ofbusinesses are familiar with Project 30, which bodes well for widespread use of the first-ever Project 30 NationalDatabase of Administrative Procedures, a searchable, online database of more than 5,700 procedures and 9,500legal documents. The PCI metrics will identify problematic areas to complement Project 30’s regulatorystreamlining of the irrelevant and harmful procedures and serve as a tool to monitor progress.

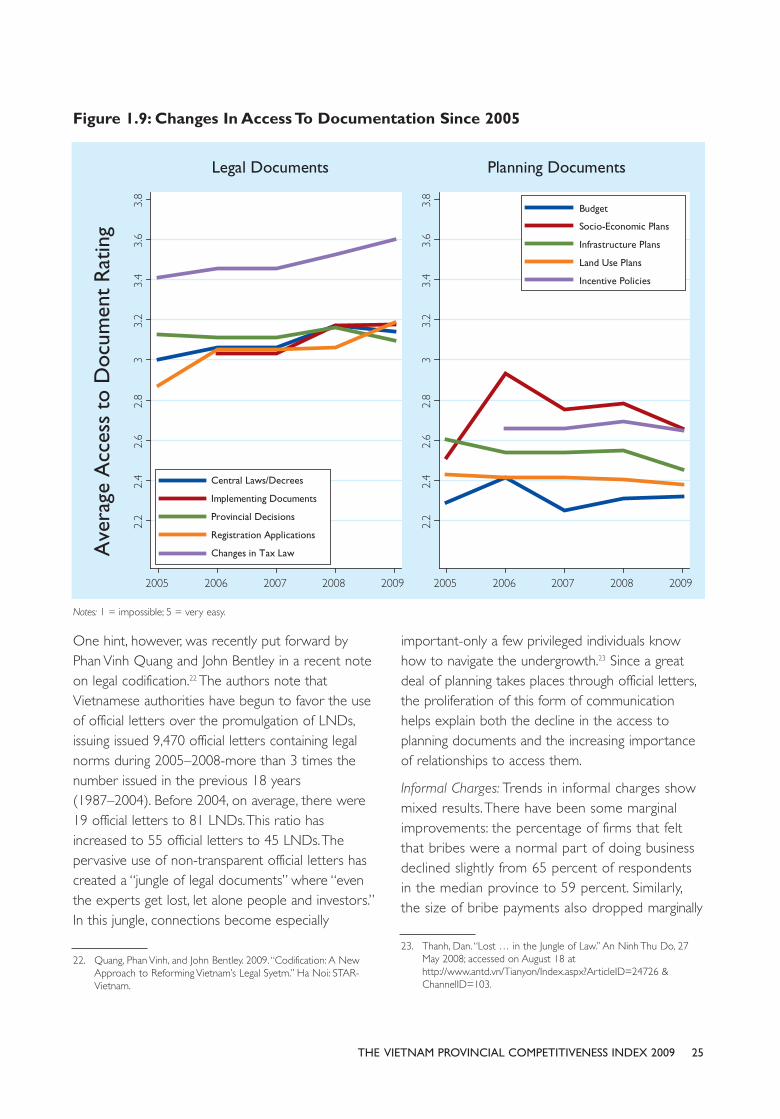

PCI also supports the decentralization process by informing policy makers about gaps in policyimplementation between the national and local level and provincial leaders about how they can enhancetheir capacity and performance, and deliver better services. Many provinces, for example, have improvedtransparency in access to legal documents and information in compliance with the country’s World TradeOrganization and Bilateral Trade Agreement with the United States commitments. However, this year, firmsreport that access to planning documents, such as provincial budgets, socioeconomic plans, infrastructureplans, and land-use and zoning maps, has declined to 2006 levels. This dangerous finding deserves theimmediate attention of policy makers.

The tremendous progress, in terms of economic growth and poverty alleviation, that Vietnam has made overthe past two decades has been remarkable. But Vietnam faces an important crossroads in its economicdevelopment. To make the best possible decisions so that the country can maintain the positive momentumof its past performance requires that policy makers and investors have the best available information. Ourgoal is to provide that information through our PCI research project, a new series of policy papers on criticalissues, datasets, and policy advice for the challenges ahead.

James Packard Winkler, Ph.D

DirectorVietnam Competitiveness Initiative

Vu Tien Loc, Ph.D

ChairmanVietnam Chamber of Commerce & Industry

iTHE VIETNAM PROVINCIAL COMPETITIVENESS INDEX 2009

ii THE VIETNAM PROVINCIAL COMPETITIVENESS INDEX 2009

ACKNOWLEDGEMENTS

This report is dedicated to the memory of Susan Adams, a dear friend and mentor to all of us.

The Provincial Competitiveness Index (PCI) 2009 is the result of a major, ongoing collaborative effortbetween the Vietnam Chamber of Commerce and Industry (VCCI) and the U.S. Agency for InternationalDevelopment’s Vietnam Competitiveness Initiative (USAID/VNCI), managed by DAI.

Edmund Malesky of the University of California–San Diego led the development of the PCI’s researchmethodology and authored the presentation of its analytical findings.

Professor Malesky was supported by a PCI research team that included Tran Huu Huynh, Deputy SecretaryGeneral and Director of the Legal Department at VCCI; Dau Anh Tuan and Le Thanh Ha of VCCI; Le ThuHien and Nguyen Ngoc Lan of USAID/VNCI; and Natasha Hanshaw of the University of California–SanDiego. The translation and administration team included Nguyen Le Ha of VCCI; Tran Minh Thu, Nguyen ThiThu Hang, Do Hai Ha, Trinh Thi Hong Hanh, Trinh Thi Hang and Le Thanh Giang of USAID/VNCI. The PCIwas developed under the overall leadership of Vu Tien Loc, Chairman of VCCI, James Packard Winkler,USAID/VNCI Project Director, and benefited from valuable support and inputs provided by Do Hoang Anh,USAID/VNCI Deputy Project Director; Geoffrey Parrish and David Brunell, Directors of Economic Growthfor USAID.

Jim Anderson, Ulrich Ernst, Le Dang Doang, and Do Hong Hanh reviewed the manuscript and providedexpert commentary.

Suggested citation when referencing report or data: Malesky, Edmund. 2009. “The Vietnam ProvincialCompetitiveness Index: Measuring Economic Governance for Private Sector Development. 2009 Final Report.”Vietnam Competitiveness Initiative Policy Paper #14. Vietnam Chamber of Commerce and Industry (VCCI)and United States Agency for International Development’s Vietnam Competitiveness Inititative (VNCI):Ha Noi, Vietnam.

THE VIETNAM PROVINCIAL COMPETITIVENESS INDEX 2009 iii

Development Alternatives, Inc. (DAI) is a global consulting firm providing socialand economic development solutions to governments, communities andcompanies with projects in developing and transitioning countries. Founded in1970 and headquartered in the Washington, DC area, DAI now includescompanies in Brazil, South Africa, Palestine, the United Kingdom, Jordan, Mexicoand Pakistan. DAI’s global team of 2,000 development professionals works in 75countries. Clients include global development agencies, international lendinginstitutions, global corporations and host country governments.

The PCI research team extends special thanks to the members of our expert advisory panel, who providedvaluable insights on methodology and indicator selection.

Mme. Pham Chi Lan Senior Economist

Mr. Vu Quoc Tuan President, Association of Vietnamese Trade Villages

Mr. Nguyen Dinh Cung Vice President, Central Institute for Economic Management

Mme. Vu Xuan Nguyet Hang Vice President, Central Institute for Economic Management

Mr. Nguyen Minh Man Director of State Administration and Civil Service Department, Office of theGovernment

Mr. Lê Dang Doanh Senior Economist

Mr. Cao Sy Kiêm President, Association of Vietnamese Small and Medium-Sized Enterprises

Mr. Nguyen Van Thoi National Assembly Member and Director of the Thai Ngueyen Joint-StockExport Company

Mr. Vu Thành Tu Anh Director of Research, Harvard Fulbright Economics Teaching Program, Ho ChiMinh City

Mr. Võ Hung Dung Director, VCCI Can Tho

Mr. Nguyen Ngoc Phi Chairman, People’s Committee of Vinh Phuc

Mr. Nguyen Van Tu Vice Director of Planning and Investment Department, Hanoi

Mr. Pham Phuong Bac Vice Director of Planning and Investment Department, Bac Ninh

Mr. Trinh Van Anh Planning and Investment Departement, Dong Nai

Mr. Nguyen Thai Son Senior Expert of the Government and Member of the Committee forImplementation of the Enterprise Law and Investment Law

Mr. Cao Ba Khoat Economist, Director of K & Associates Consulting

Mr. Lê Minh Thong K & Associates Consulting

Mr. Phan Duc Hieu Vice Director, Competitiveness and Business Environment Department,Central Institute for Economic Management

Mr. Vu Quoc Huy Economist, National Economic University

Mme. Pham Thi Thu Hang Director, Center for Supporting Small and Medium Size Enterprises, VCCI

Mr. Pham Duy Nghia Legal Department, National University of Hanoi

Mr. Le Duy Binh Director, Economica

Mr. Nguyen Van Lan Economist, Mekong Private Sector Development Facility

Mr. Vu Xuan Tien Director, VFAM Consulting

Mr. Tran Phuong Senior Vice President, Head of Corporate Planning, Bank for Investment andDevelopment of Vietnam

Mr. Tran Tho Dat Vice Rector, National Economic University

Mr. Nguyen Van Thang National Economic University

Mr. Doan Hong Quang Senior Economist, World Bank

THE VIETNAM PROVINCIAL COMPETITIVENESS INDEX 2009iv

TABLE OF CONTENTS

ACKNOWLEDGMENTS .........................................................................III

ABBREVIATIONS AND ACRONYMS ...................................................IX

EXECUTIVE SUMMARY ......................................................................XIIIExecutive summary ...............................................................................................xiiiOverall rankings and scores................................................................................xiiiAssociation of governance and economic outcomes....................................xiiiAssociation of governance and prospective investment ..............................xiiiMost critical PCI sub-indices for economic development ...........................xivTrends in provincial governance over time .....................................................xivInfrastructure index ...............................................................................................xvAnalyzing the Ha Noi expansion........................................................................xviChanges in PCI methodology .............................................................................xvi

CHAPTER ONEBACKGROUND AND KEY FINDINGS...................................................3

A picture of the PCI respondents ........................................................................7The final 2009 Provincial competitiveness ranking.........................................11

Weights............................................................................................................11Importance of Transparency for Private Sector Development ..........16Importance of Labor Quality for Private Sector Development ........16Lower-Weighted Indicators ........................................................................18Robustness of the rankings.........................................................................19Robustness of Performance Tiers .............................................................19Robustness Over Time ................................................................................19

Largest improvements in provincial PCI scores..............................................20Summary of nationwide trends in provincial governance.............................20

Improvements ................................................................................................20Challenges.......................................................................................................23

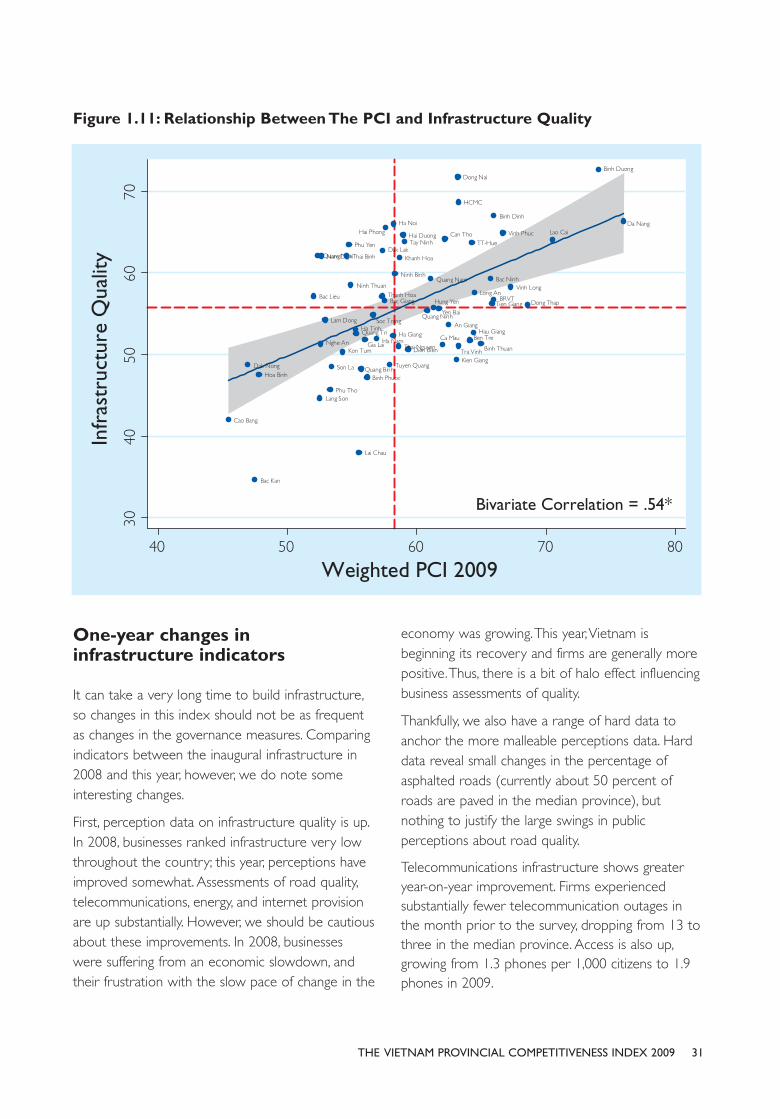

Assessment of infrastructure...............................................................................26Relationship between Governance and Infrastructure ........................30One-Year Changes in Infrastructure Indicators.....................................31Caution About Attribution About Infrastructure Quality ...................32

Future questions for research using PCI data .................................................32The Impact of the Economic Stimulus on Domestic, Private ................Investment ......................................................................................................33Improvements in Vocational Training ........................................................33Transparency of Processes and Documentation ...................................34

In conclusion............................................................................................................34

THE VIETNAM PROVINCIAL COMPETITIVENESS INDEX 2009 v

CHAPTER TWO GOVERNANCE IMPACT OF HANOI’S GEOGRAPHIC EXPANSION.39

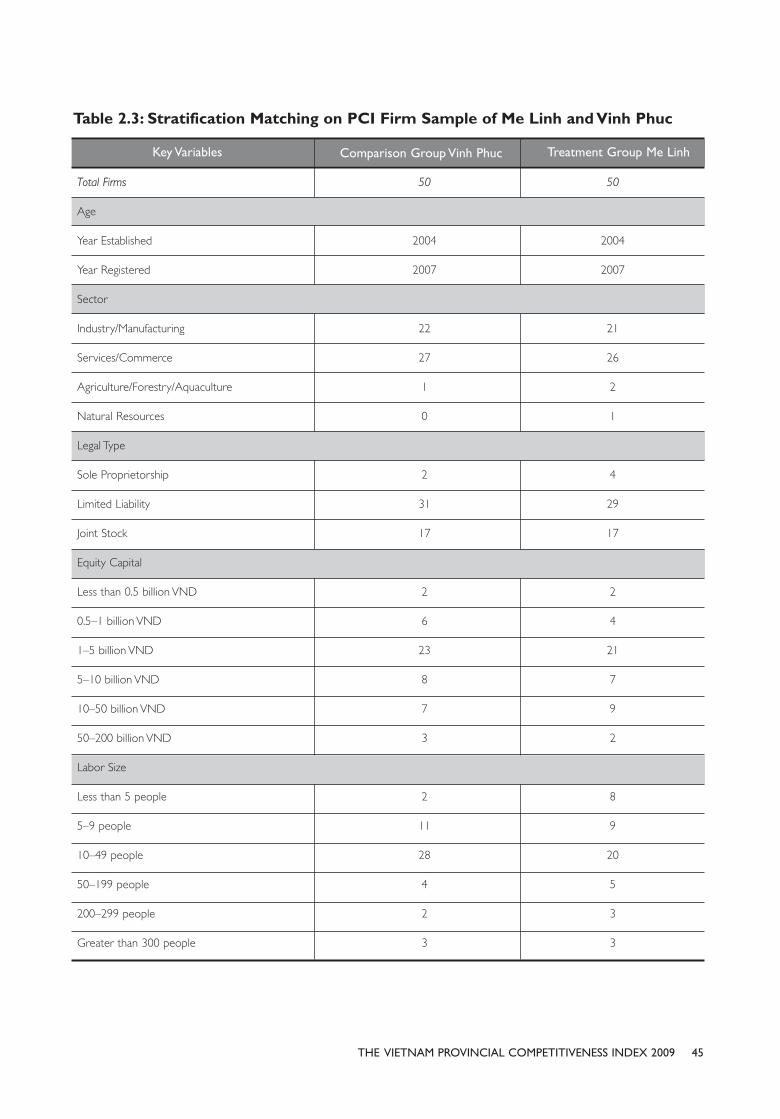

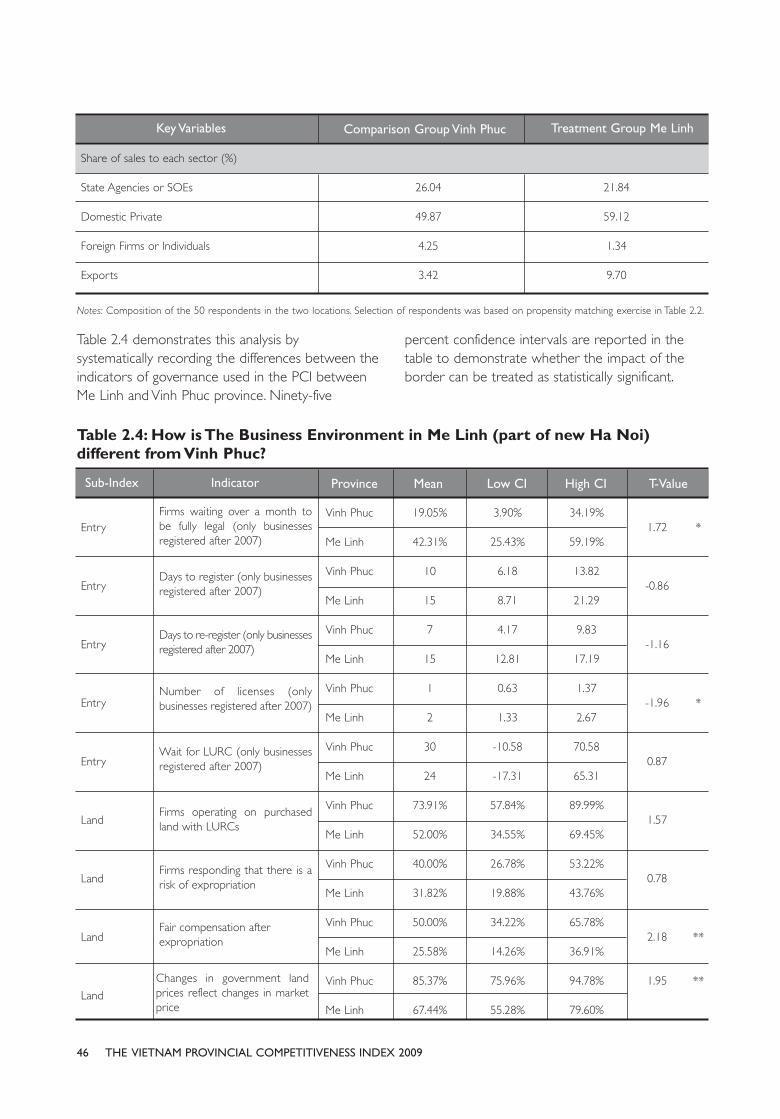

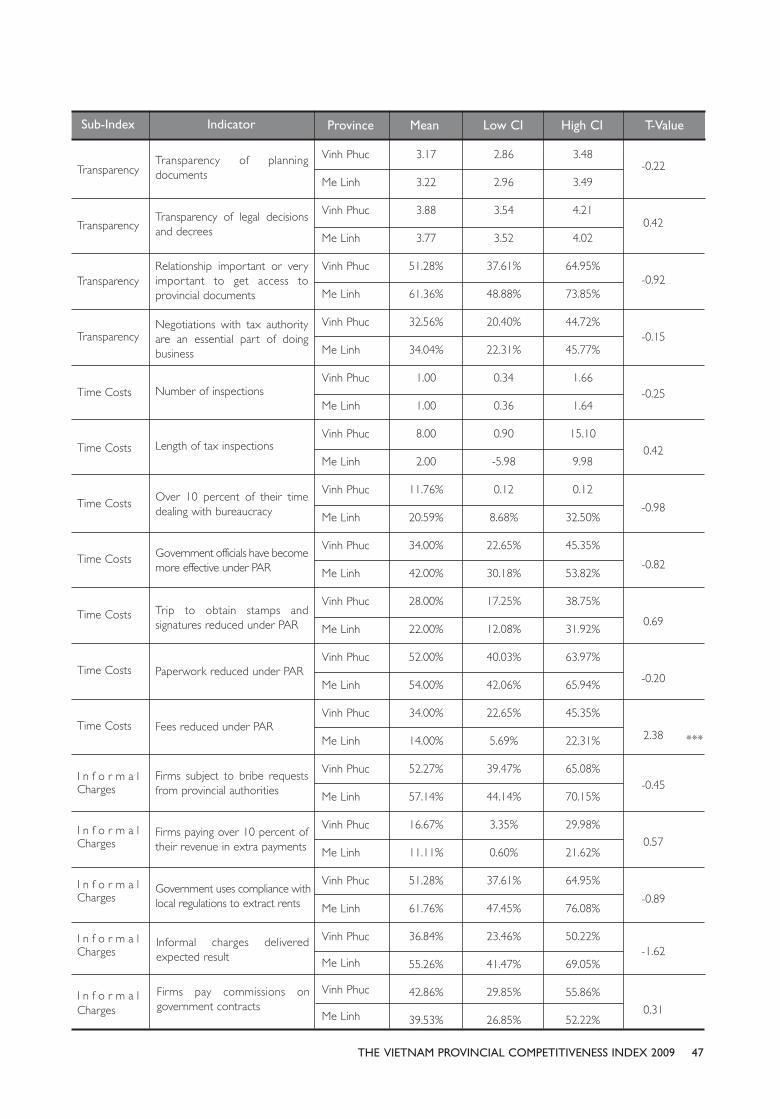

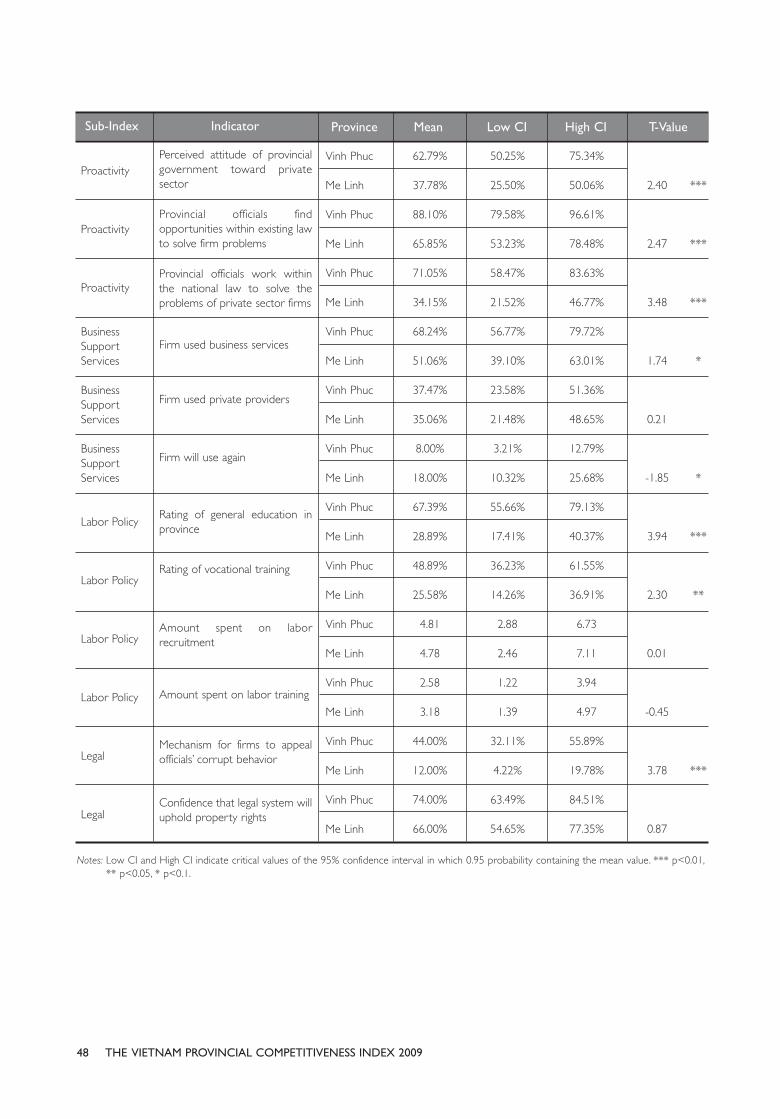

Background ..............................................................................................................39Analysis ...............................................................................................................41Matching analysis for Me Linh and Vinh Phuc ..................................................42The economic impact of exogenous governance change.............................49Conclusion ...............................................................................................................50

CHAPTER THREECHANGES IN THE PCI METHODOLOGY ...............................................................53

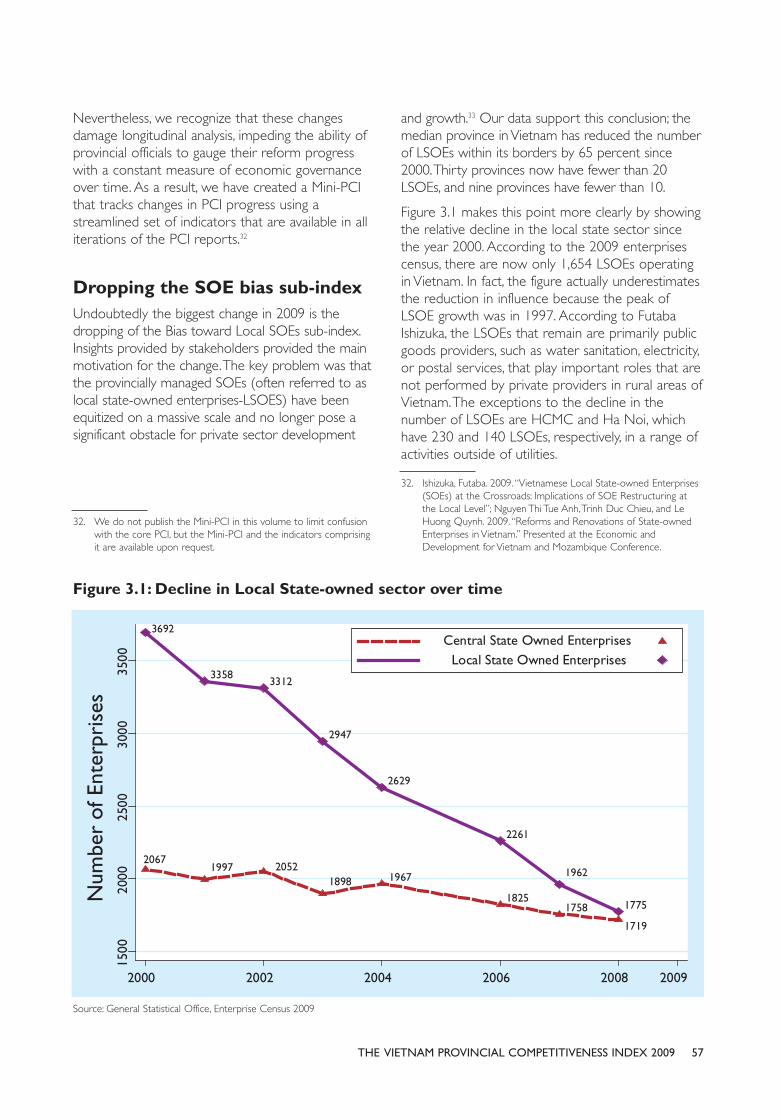

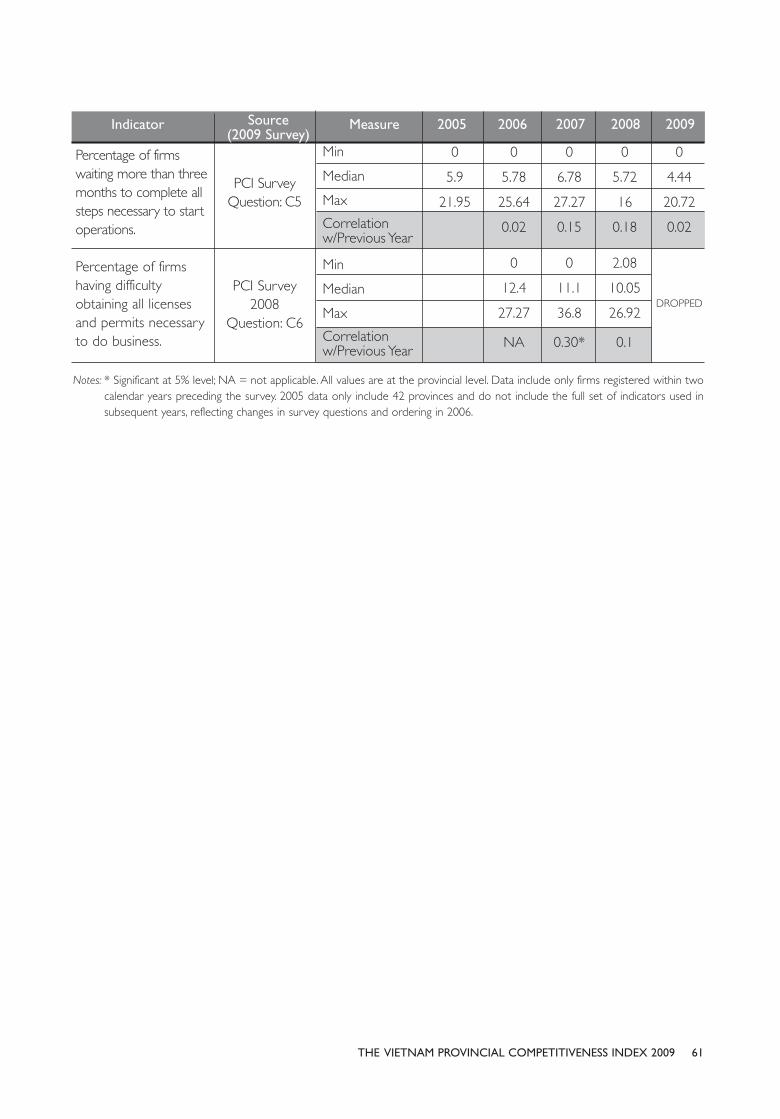

Dropping the SOE bias sub-index ......................................................................57Changing indicators within sub-indices .............................................................60

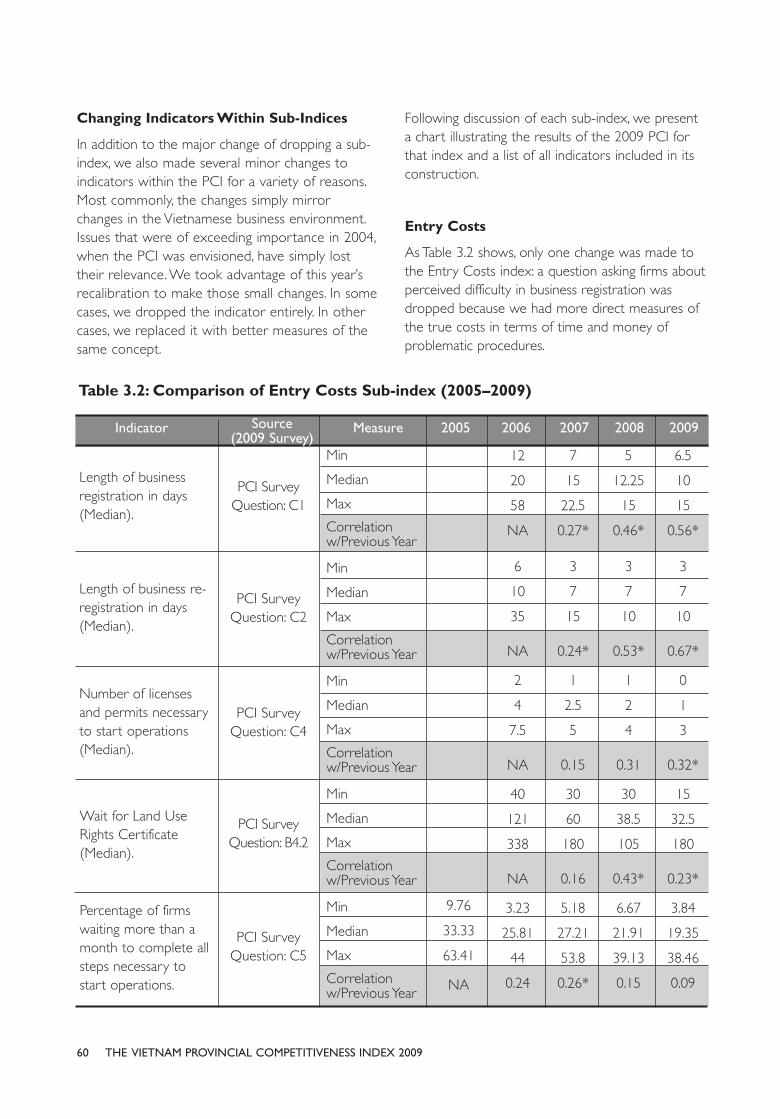

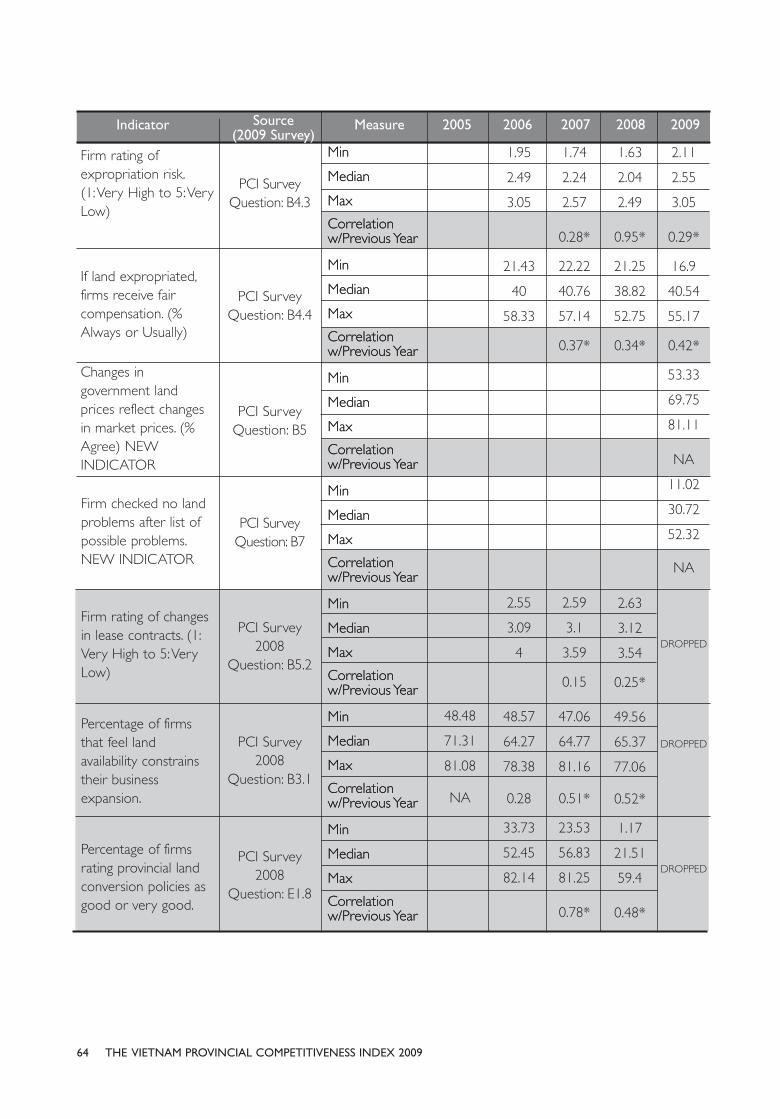

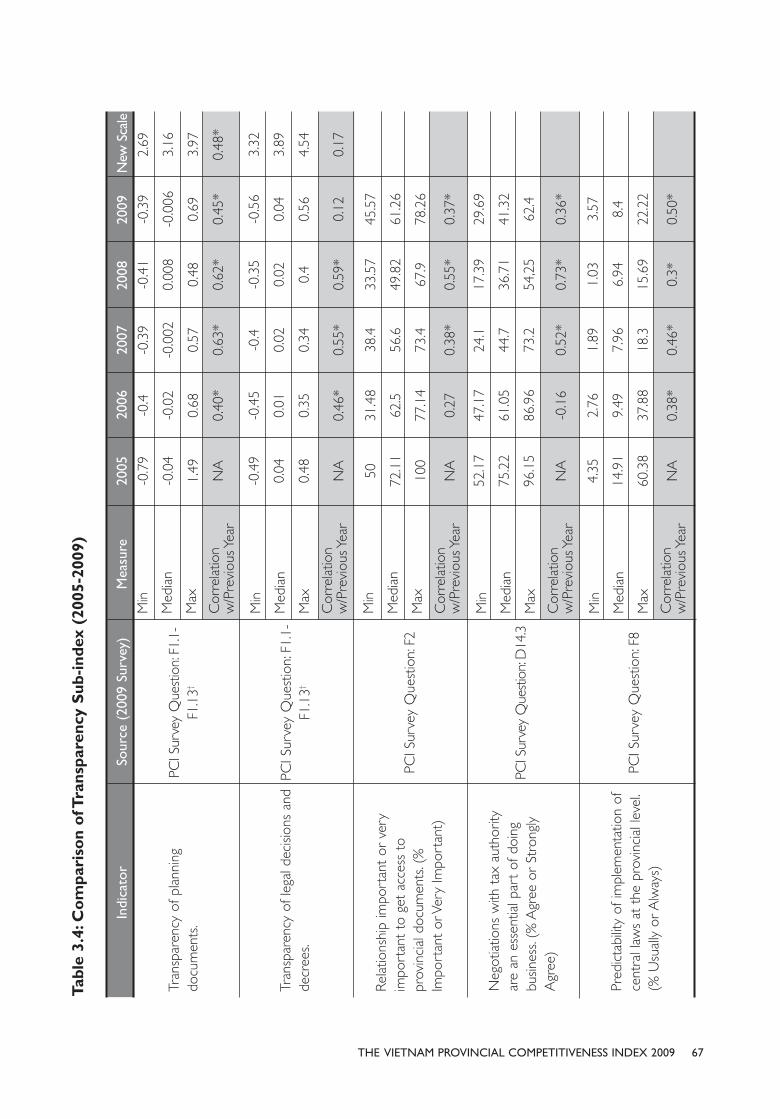

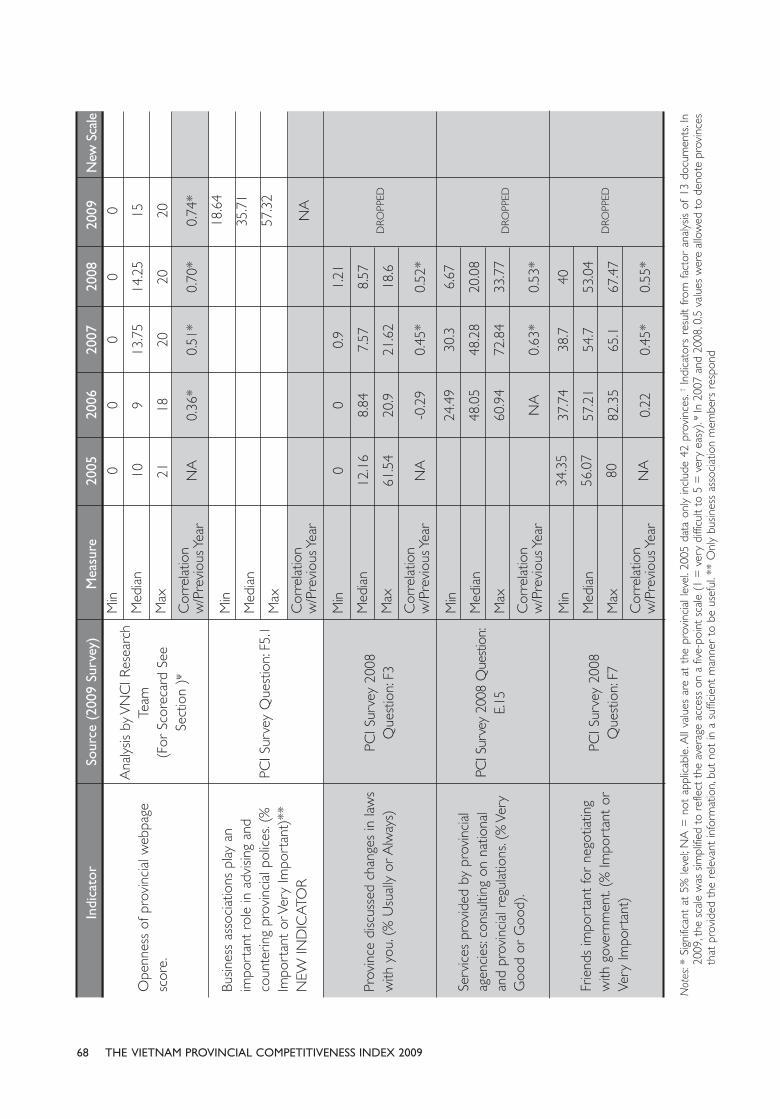

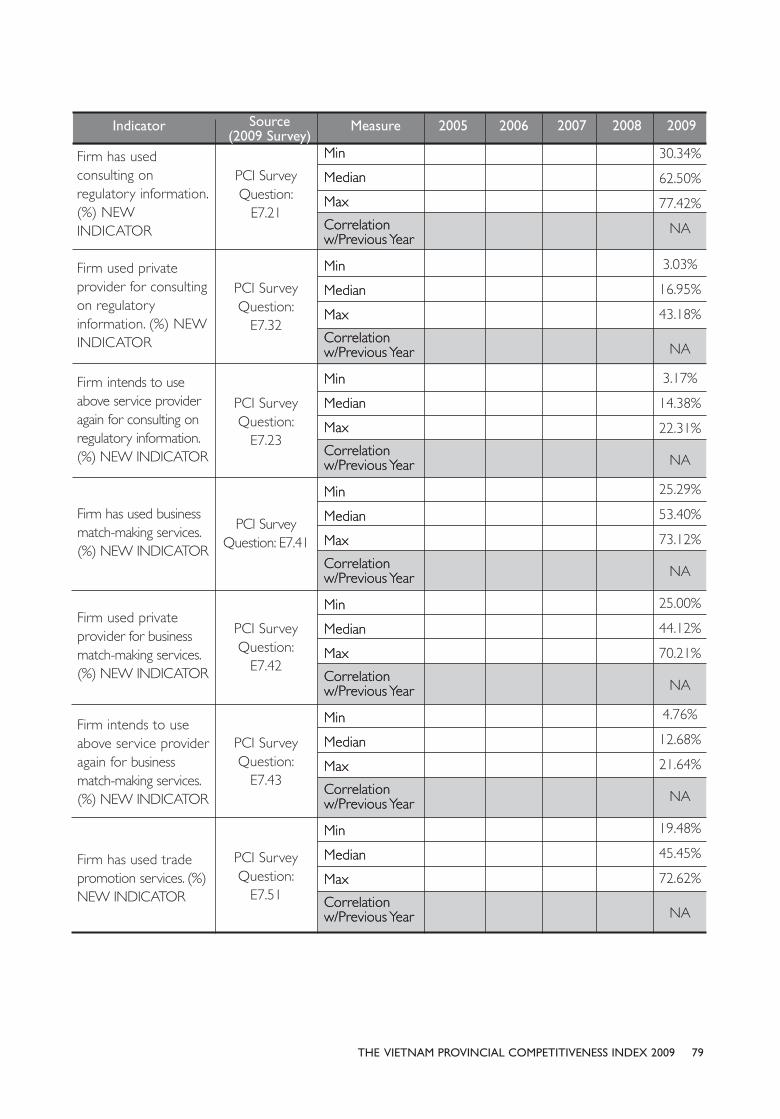

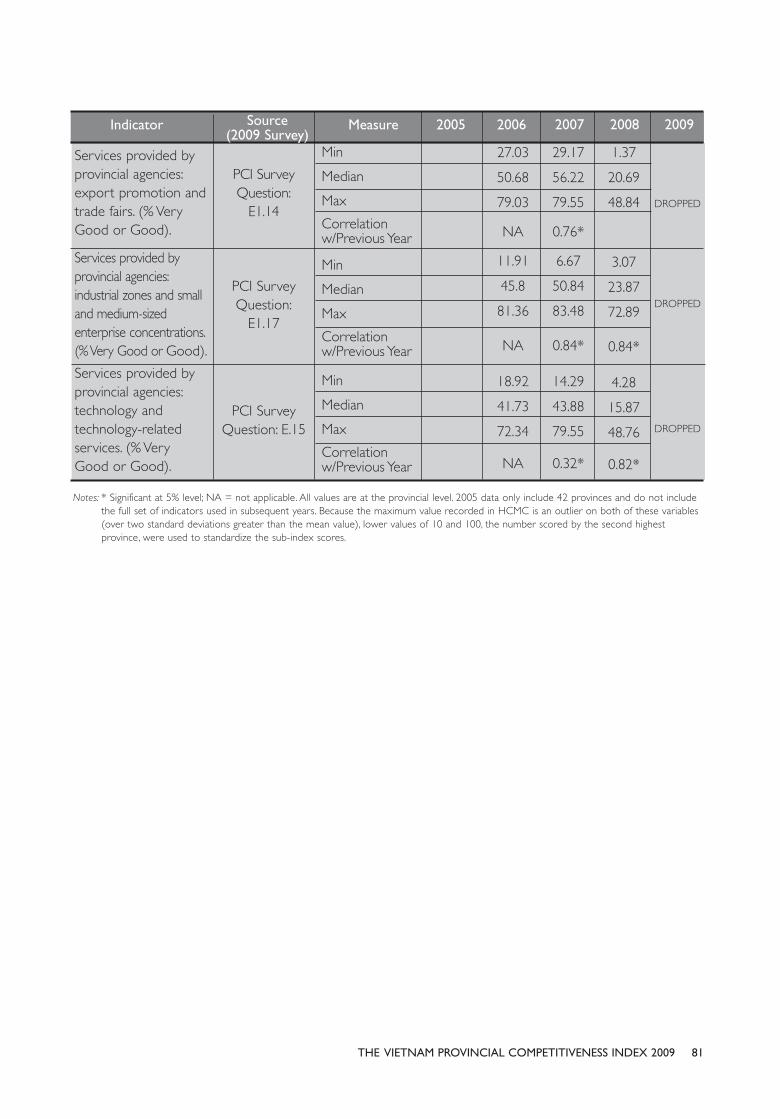

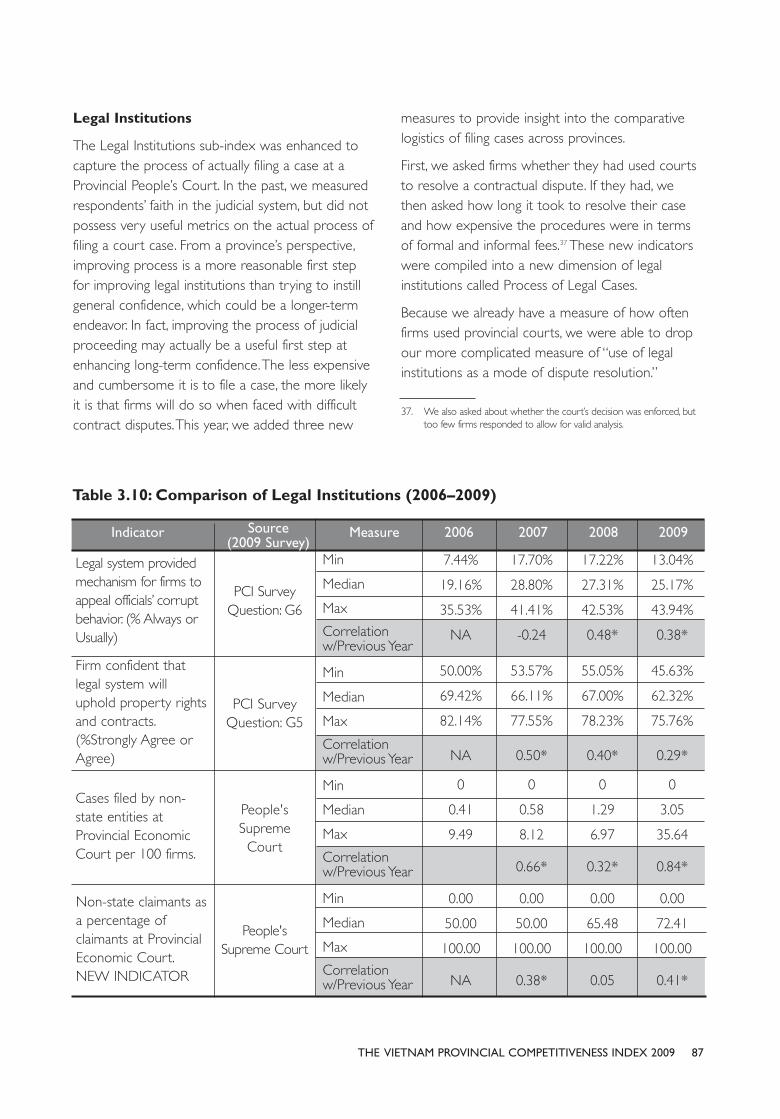

Entry Costs ....................................................................................................60Land Access and Security of Tenure .........................................................63Transparency ..................................................................................................66Time Costs of Regulatory Compliance ...................................................70Informal Charges...........................................................................................72Proactivity .......................................................................................................74Business Support Services ..........................................................................77Labor Policy....................................................................................................83Legal Institutions ...........................................................................................87

Changing the weighting strategy.........................................................................90

CHAPTER FOURAPPENDICES ...............................................................................................................93

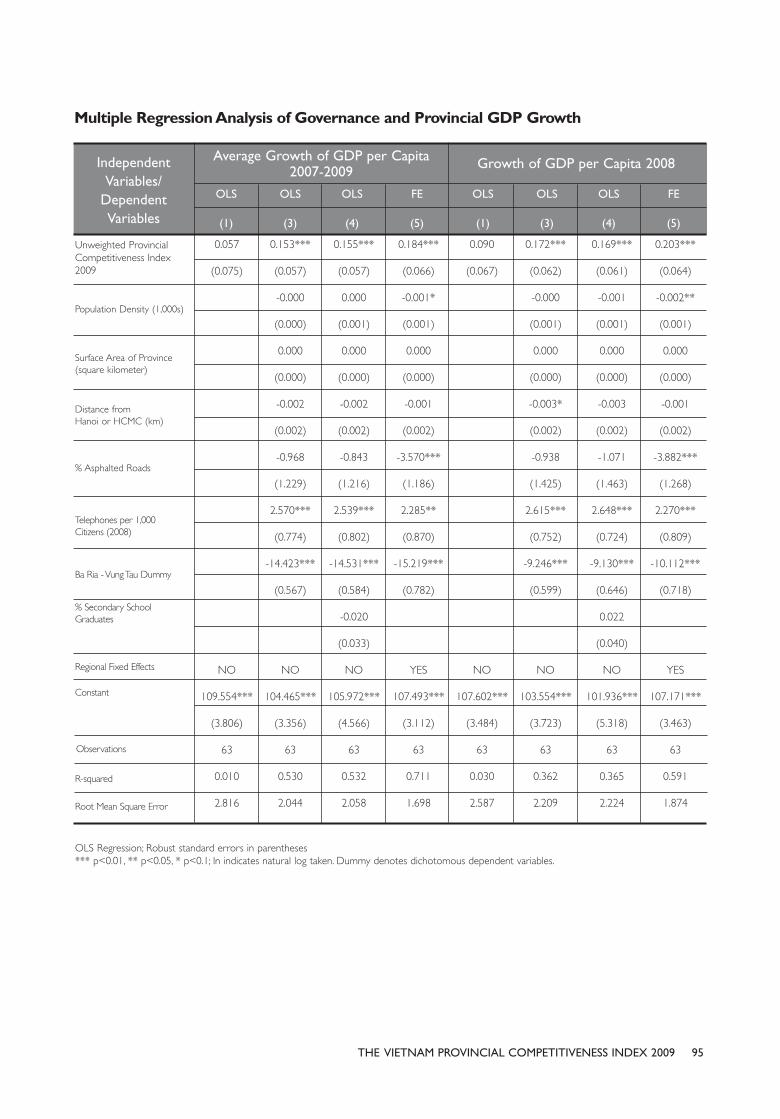

Multiple Regression Analysis of Governance and Key Private SectorOutcome Variables .................................................................................................94 Multiple Regression Analysis of Governance and Provincial GDP Growth .....95DATASETS USED IN ANALYSIS.........................................................................96

THE VIETNAM PROVINCIAL COMPETITIVENESS INDEX 2009vi

TABLES

Table 1.1: Who Answers the PCI Survey? .................................................................................7

Table 1.2: PCI Sample versus Nationally Representative Sample ...............................10

Table 1.3: Sub-Index Weighting .......................................................................................................14

Table 1.4: Indicators Used in Infrastructure Index...............................................................28

Table 2.1: Re-calculated PCI for the Areas Comprising the new Hanoi ................41

Table 2.2: Propensity Score Matching Exercise for Location in Me Linh Province.....43

Table 2.3: Stratification Matching on PCI Firm Sample of Me Linh and Vinh Phuc ....45

Table 2.4: How Is the Business Environment in Me Linh (Part of New Hanoi)

Different from Vinh Phuc?............................................................................................46

Table 3.1: Scores and Correlation of PCI Sub-Indices Over Time (2006–2009) ........54

Table 3.2: Comparison of Entry Costs Sub-Index (2005–2009) ................................60

Table 3.3: Comparison of Land Access and Tenure Security Sub-Index

(2005–2009)........................................................................................................................63

Table 3.4: Comparison of Transparency Sub-Index (2005–2009) ..............................67

Table 3.5: Comparison of Time Costs of Regulatory Compliance (2005–2009) .......70

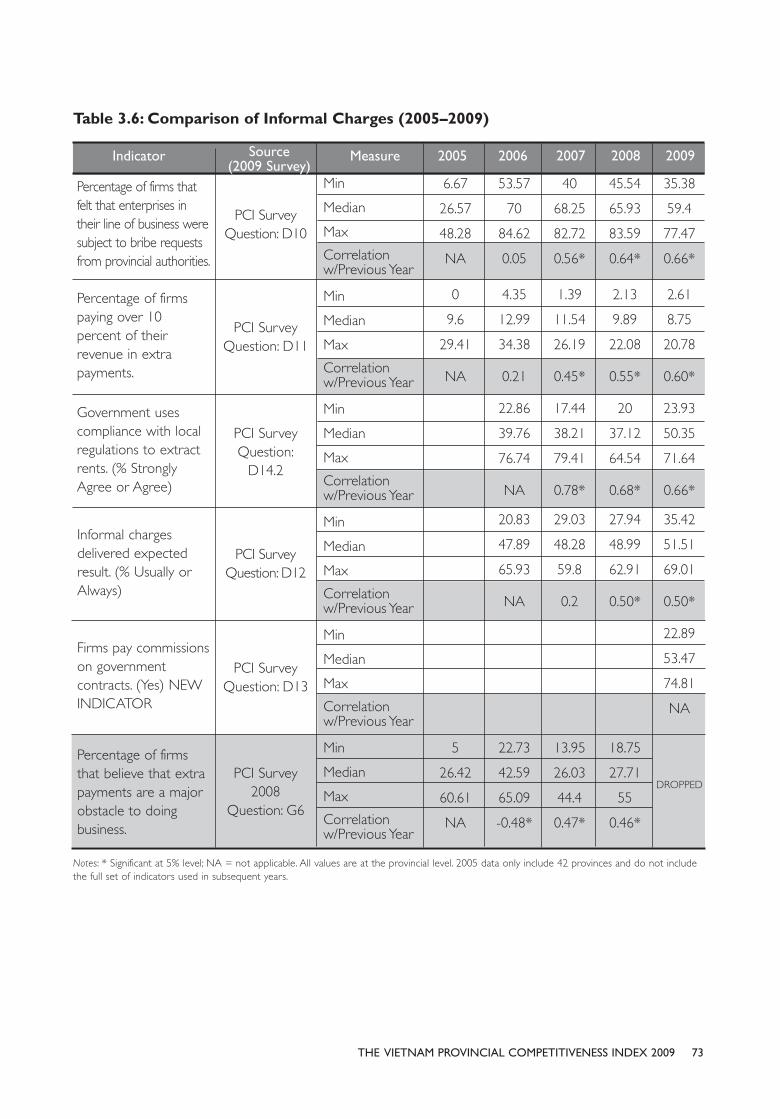

Table 3.6: Comparison of Informal Charges (2005–2009).............................................73

Table 3.7: Comparison of Proactivity (2005–2009)............................................................75

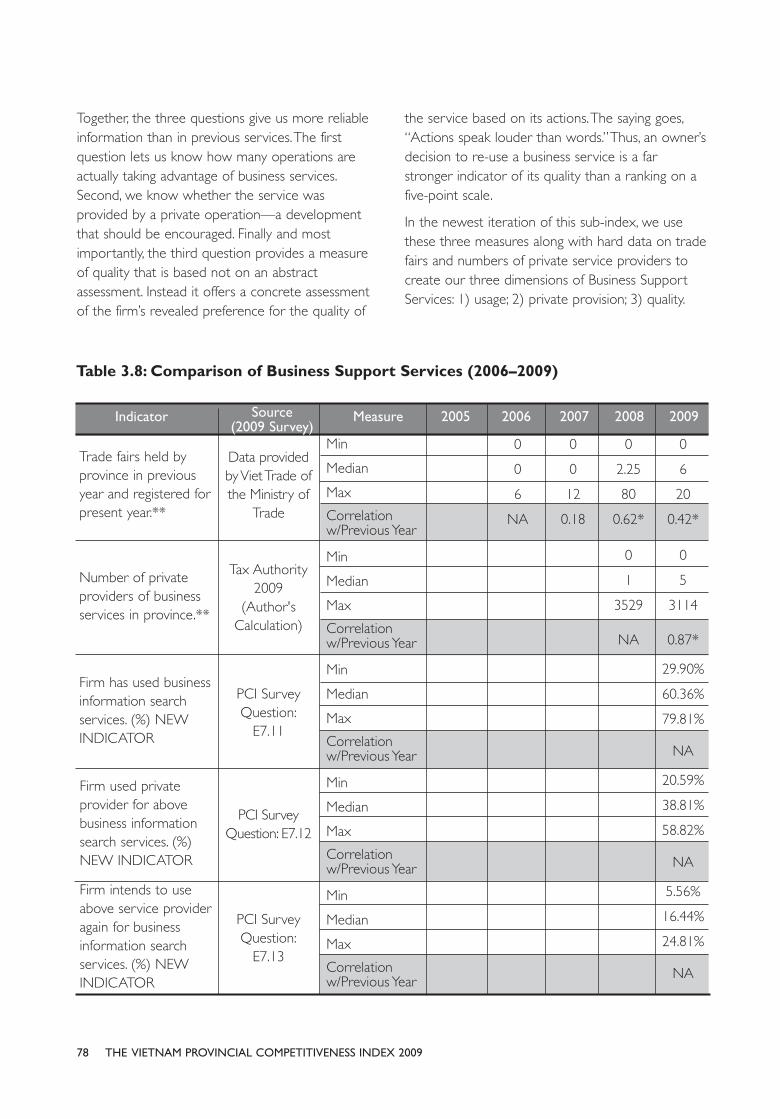

Table 3.8: Comparison of Business Support Services (2006–2009) ........................78

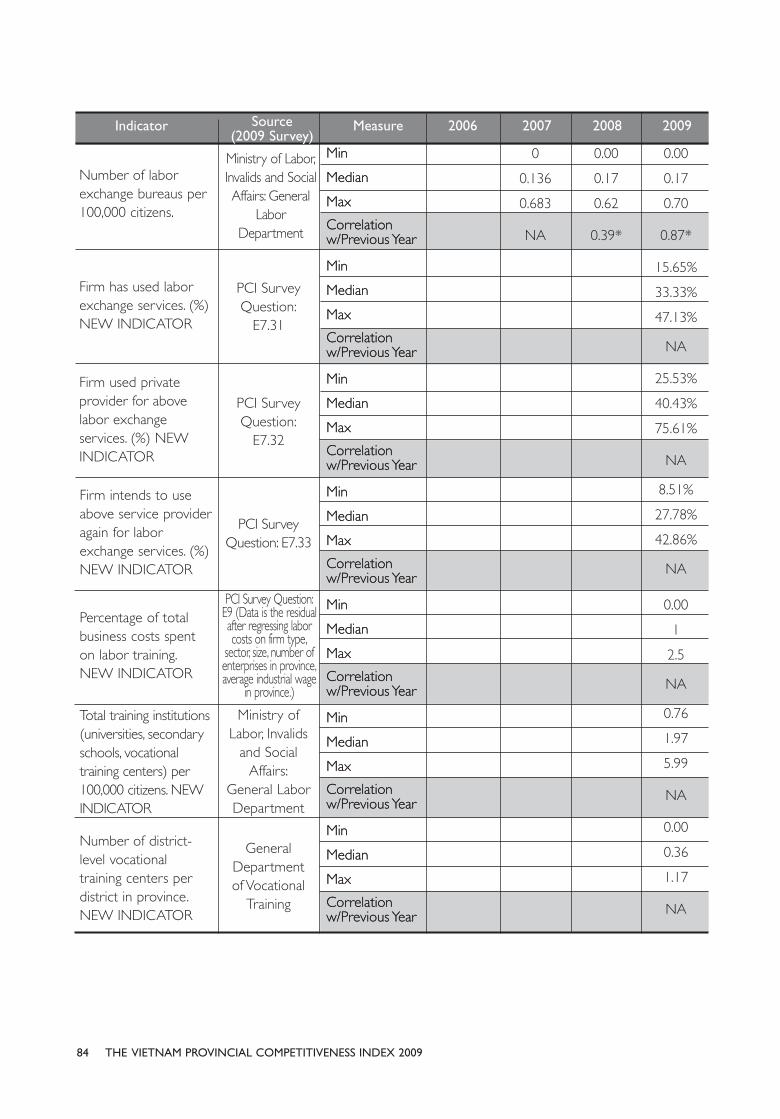

Table 3.9: Comparison of Labor Policy (2006–2009) .......................................................83

Table 3.10: Comparison of Legal Institutions (2006–2009)..............................................87

Table 3.11: Explanation of Approach to Sub-Index Weighting........................................91

TABLES AND FIGURES

THE VIETNAM PROVINCIAL COMPETITIVENESS INDEX 2009 vii

FIGURES

Figure 1.1: Business Thermometer (Percentage of Respondents Planning to

Expand Business over Next Two Years)....................................................................4

Figure 1.2: Relationship between Governance and Selection as Location for

Expansion ...................................................................................................................................5

Figure 1.3: Drivers of Locational Choice .........................................................................................6

Figure 1.4: Weighted Provincial Competitiveness Index 2009 .........................................12

Figure 1.5: College Entrance Exams and Assessment of Labor Quality .....................17

Figure 1.6: Province Performance by Sub-Index .......................................................................18

Figure 1.7: Stability of PCI Ranking Over Time..........................................................................19

Figure 1.8: Improvement in PCI Ranking Between 2008 and 2009..............................21

Figure 1.9: Changes in Access to Documentation Since 2005 ........................................25

Figure 1.10: Infrastructure Quality Index..........................................................................................27

Figure 1.11: Relationship Between the PCI and Infrastructure Quality .........................31

Figure 2.1: Re-calculated PCI Sub-indices for the Areas Comprising the new Hanoi..42

Figure 2.2: Relative Business Performance of Matched Enterprises ..............................50

Figure 3.1: Decline in Local State-Owned Sector Over Time..........................................57

Figure 3.2: Comparative Importance of Local and Central State-Owned Sectors.......59

Figure 3.3: Entry Costs Sub-Index 2009........................................................................................62

Figure 3.4: Land Access Sub-Index 2009.......................................................................................65

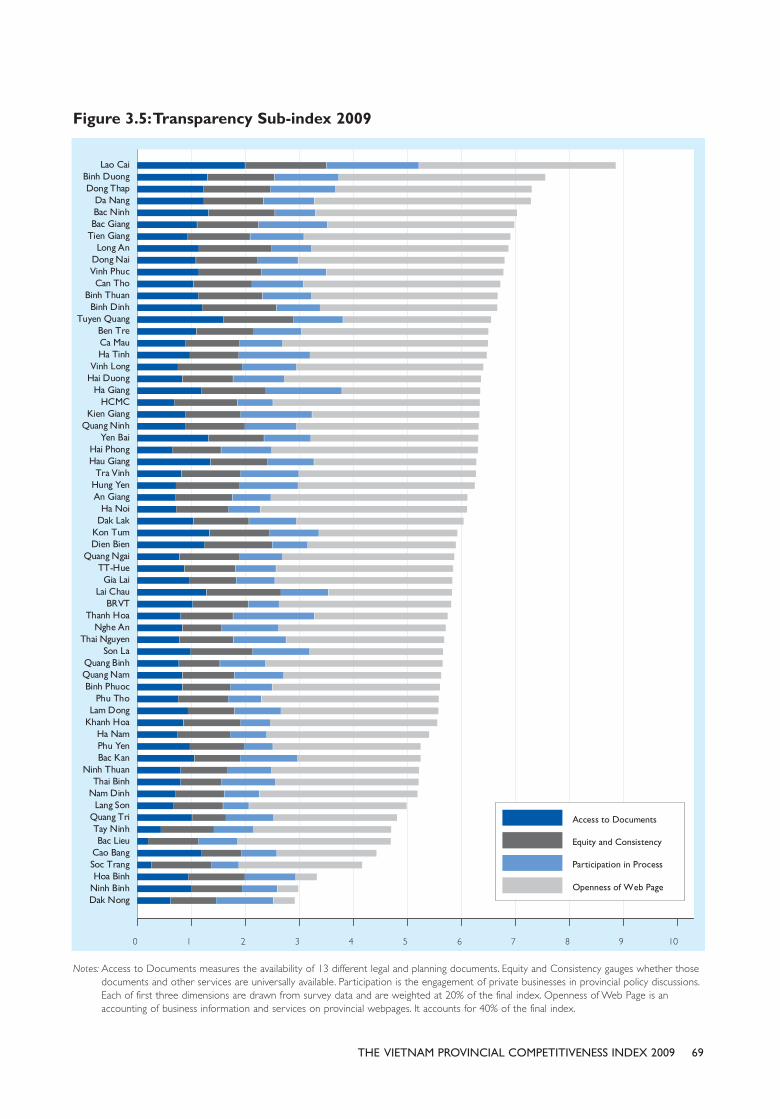

Figure 3.5: Transparency Sub-Index 2009.....................................................................................67

Figure 3.6: Time Costs of Regulatory Compliance Sub-Index 2009 ............................72

Figure 3.7: Informal Charges Sub-Index 2009............................................................................74

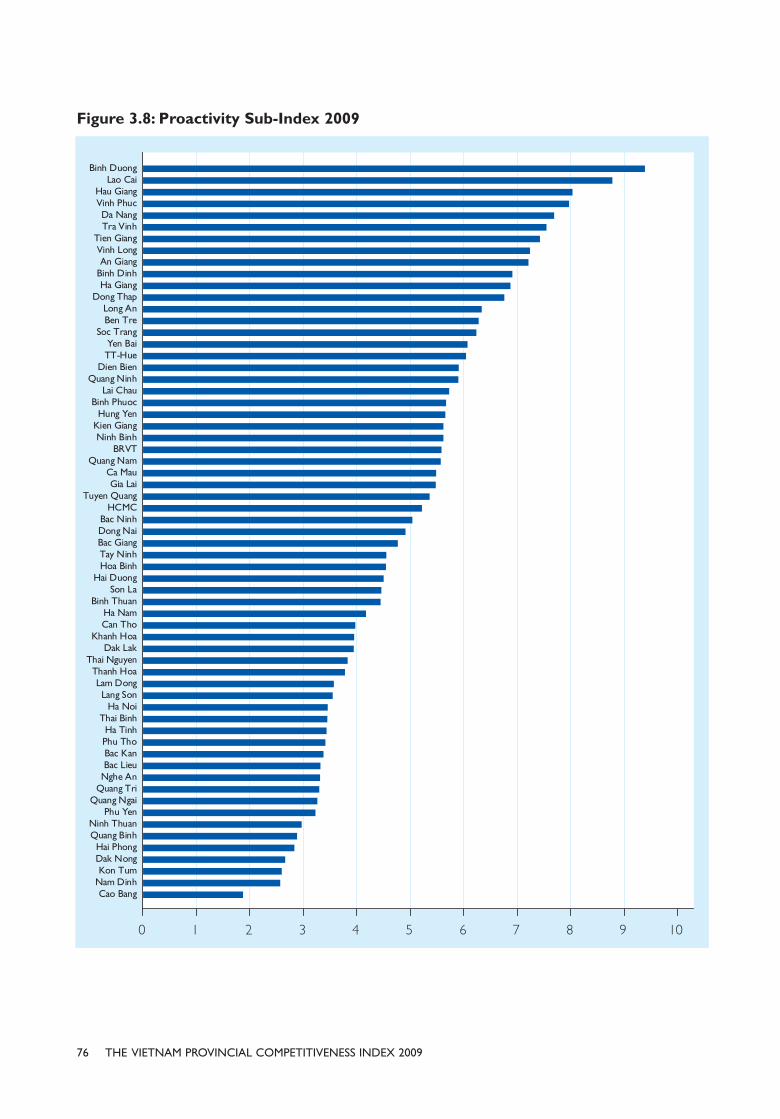

Figure 3.8: Proactivity Sub-Index 2009...........................................................................................76

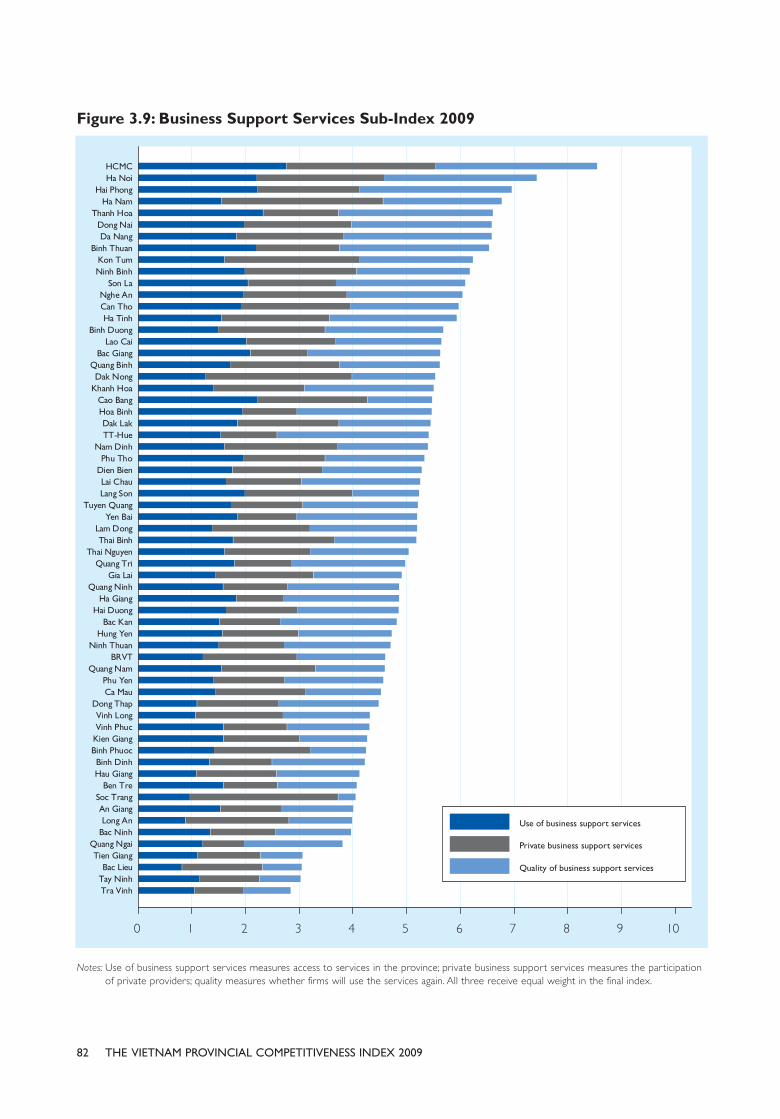

Figure 3.9: Business Support Services Sub-Index 2009........................................................82

Figure 3.10: Labor Policy Sub-Index 2009.......................................................................................86

Figure 3.11: Legal Institutions Sub-Index 2009 .............................................................................89

THE VIETNAM PROVINCIAL COMPETITIVENESS INDEX 2009viii

ABBREVIATIONS AND ACRONYMS

AP Administrative Procedure

BRVT Ba Ria-Vung Tau province

CSOE Central state-owned enterprise

GDP Gross domestic product

GSO General Statistics Office

HCMC Ho Chi Minh City

IZ Industrial zone

LND Legal normative document

LSOE Local state-owned enterprise

LURC Land use rights certificate

PAR Public administration reform

PCI Provincial Competitiveness Index

PSM Propensity score matching

SOE State-owned enterprise

VCCI Vietnam Chamber of Commerce and Industry

VNCI Vietnam Competitiveness Initiative

THE VIETNAM PROVINCIAL COMPETITIVENESS INDEX 2009 ix

EXECUTIVE SUMMARY

The Provincial Competitiveness Index (PCI) wasdeveloped in 2005 by the Vietnamese Chamber ofCommerce and Industry and the U.S. Agency forInternational Development-funded VietnamCompetitiveness Initiative. Since that time, the PCIhas come to be seen as a critical tool for measuringand assessing the standards of economicgovernance in Vietnam’s 63 provinces from theperspective of private sector businesses.

The year 2009, which marks the fifth iteration ofthe PCI analysis, is especially important because ittakes place during a period of declining privatesector optimism. Only 65 percent of privateoperations in Vietnam intend to expand theirbusinesses over the next two years, compared with78 percent in 2008 and 77 percent in 2007. Smallfirms have been more severely traumatized by thecurrent global economic crisis than others; only 47percent claim they plan to expand.

It is in these periods of declining businessconfidence that economic governance becomesmost important to entrepreneurial decision making.Business owners are concerned about theirprospects for the future because they are uncertainboth about economic events outside of the controlof Vietnamese policy makers and about the policydecisions of Vietnamese officials themselves. In suchan environment, clear, transparent, and fair regulatoryrules and policies become paramount for assuagingfirms’ fears and helping them make accuratepredictions about future business prospects.

Thus, the 2009 PCI can be a helpful signpost tohelp provincial policy makers address weaknesses,and thereby help private entrepreneurs overcomethe current economic hardships.

Overall rankings and scoresJust as in 2008, Da Nang is the number one rankedprovince in the country, followed closely by Binh

Duong. Once again, the two provinces arestatistically indistinguishable. Lao Cai, Dong Thap,Vinh Long and Vinh Phuc round out the tier ofexcellent performers. Cao Bang, Dak Nong, and BacKan—at the bottom of the rankings—still requirethe most improvement in provincial governance.

Association of governance andeconomic outcomesOnce again, governance scores are highly correlatedwith the size of the private sector, individualenterprise performance, and overall provincialeconomic growth1. To determine this, we regressedthese outcome variables on the unweighted PCI,controlling for measures of infrastructure (roadquality and telecommunications), structuralendowments (population size, density, and distancefrom major markets), and regional fixed effect(dichotomous variables for each region, which allowus to hold constant regionally specific history andsociocultural factors).

In each regression, the unweighted PCI score provesstatistically significant and substantively large. Inshort, better governed provinces have larger andmore successful private sectors, as well as higherlevels of economic welfare.

Association of governance andprospective investmentThis year, our analysis of the importance of economicgovernance added an additional feature. We askedbusinesses to record to which provinces, outside oftheir home province, they would likely expand ifgiven the opportunity. The variable gave us a measureof prospective investment potential for the next twoyears. Once again, governance was highly important

xiiiTHE VIETNAM PROVINCIAL COMPETITIVENESS INDEX 2009

EXECUTIVE SUMMARY

1. See Chapter Four for tables of regression results.

THE VIETNAM PROVINCIAL COMPETITIVENESS INDEX 2009xiv

maintain equipment or manage complex businessand financial processes. Firms are finding it very hardto upgrade technology and expand operationswhen they are handicapped by an insufficient talentpool. General education, vocational education, andlabor exchange bureaus in many provinces havelagged behind the business needs of many firms.Other provinces have made significant investmentsin improving their labor pool. Correspondingly, aone point improvement in the Labor sub-index isassociated with an estimated 30 percentimprovement in enterprises per capita, a 47 percentenhancement in investment per capita, and astatistically insignificant but sizable 58 million VNDincrease in profitability.

Two indicators receive quite low weights of 5percent (Land Access and Legal Institutions), but notbecause they are unimportant; rather, they aregenerally problematic across the entire country. Veryfew provinces excel on these dimensions, leading tolow variance across the country and, consequently, alow correlation with private sector outcomes. Theweights on the issues hint that moving forward onboth these dimensions requires national-level policyreform in addition to provincial initiatives, whichhave been insufficient.

Trends in provincial governanceover timeThis year’s report tracks changes in provincialgovernance over time by using changes in themedian provincial score for each indicator. Sustainedincrease in the median province’s score is evidenceof improvement in the indicator throughout thecountry as a whole. Measures of Entry Costs, Accessand Security of Land, Time Costs, Labor Quality, andConfidence in Legal Institutions show signs ofdefinitive improvement over the past year. Policymakers should be proud of these accomplishments.Worrisome declines, however, are evident in termsof Transparency, Informal Charges, and the Proactivityof local leaders.

For the median province, Time Costs of RegulatoryCompliance improved the most, after several years

in the selections, even after controlling forinfrastructure and structural endowments.

For each one point improvement in the unweightedPCI score of a province, three more investors werelikely to choose it as an investment location. This is asizable effect. By way of comparison, a 10percentage point improvement in the amount ofasphalted road would yield about the same numberof selections by potential investors.

Most critical PCI sub-indices foreconomic developmentRegression analysis on private sector developmentoutcomes (number of enterprises, size ofinvestment, and profitability) revealed that two mostimportant sub-indices for generating private sectorgrowth are Transparency and Labor Quality.Consequently, these two sub-indices receive thehighest weight—20 percent—in the PCI index.

There are important reasons why transparency ofbusiness information has critical implications for thesuccess of entrepreneurs. When entrepreneurs haveadequate information about a province’s initiativesregarding regulatory changes, infrastructure roll-outs,or land use planning, they can forecast theirinvestment prospects deep into the future. Themore comfortable they feel about long-termbusiness prospects, the more willing they will be torisk their hard-earned capital today. Whenentrepreneurs are worried about sudden changes inregulation, infrastructure, or land, they will hold backfrom large-scale projects, investing incrementally asthey test the water. Regression analysis confirmsthese hypotheses: a one point improvement intransparency is associated with a 13 percentimprovement in enterprises per capita, a 17 percentimprovement in investment per capita, and a 62million VND increase in firm profitability.2

Labor quality is also very important. A key businesscomplaint in multiple surveys is that there is notenough skilled and semi-skilled labor to handle and

2. See Chapter Four for full regression results.

THE VIETNAM PROVINCIAL COMPETITIVENESS INDEX 2009 xv

and Decree 136/2005/ND-CP, which mandated thatprovinces publish all legal normative documentspassed at the provincial level in a provincial gazette(Công Báo).

Because these achievements have impaired theflexibility of individual policy makers, some officialshave found a loophole in the issuance of officialletters, which do not require public distribution.During 2005–2008, Vietnam issued 9,470 officialletters containing legal norms, which is more thanthree times higher than the number issued in theprevious 18 years (1987–2004). As Phan VinhQuang and John Bentley have argued, the use ofnon-transparent official letters has created a legaljungle of complex and contradictory rules that onlyofficials and connected entrepreneurs have theability to safely navigate. Further research isnecessary, but the more planning decisions that arearticulated through officials letters, the moreimportant political relationships become and themore insiders benefit at the expense of economicproductivity.

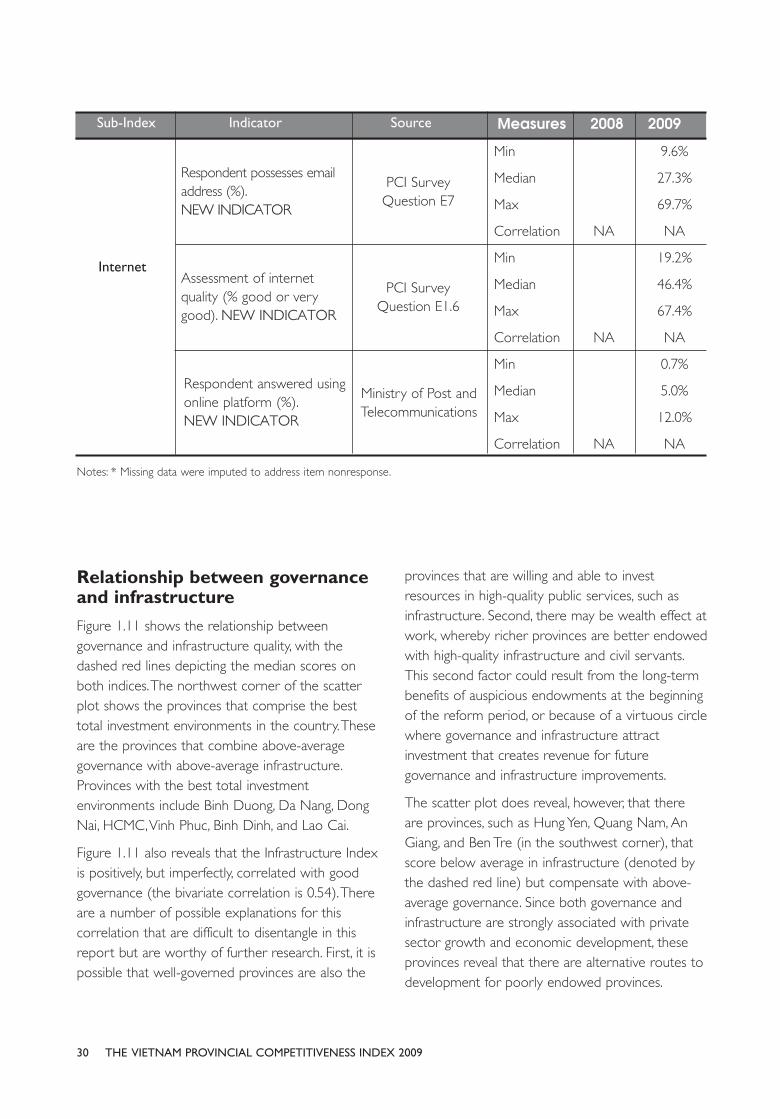

Infrastructure indexThis year continues our supplemental InfrastructureIndex begun in 2008. Problems with Vietnam’sinfrastructure are harming its competitive advantageinternationally. Although infrastructure quality cannotbe attributed directly to provincial officials, increasedfiscal decentralization has, in theory, increased theopportunities for provinces to raise their ownresources for infrastructure improvements.

The Infrastructure Index ranks provinces along fourdimensions: 1) industrial zone quality and capacity;2) road quality and transportation costs; 3)telecommunications and energy costs and stability;and 4) information and communications technology.Binh Duong, Dong Nai, Ho Chi Minh City, BinhDinh, Da Nang and Hanoi emerge as having thebest overall infrastructure in the country; the ruralNorthwestern Uplands score the worst.

Firm perceptions of infrastructure quality haveimproved substantially since the 2008 financial crisis.

of stagnation. The total amount of time thatmanagers spend on bureaucratic procedures hasdeclined from 22 percent to 15 percent, while thenumber of hours for the tax inspection declinedfrom 8 to 5 hours. In addition, 47 percent ofrespondents report that the government-requiredpaperwork has declined in the past two years, and44 percent of firms acknowledge that civil servantshave become more effective at dealing withbureaucratic procedures. These numbers indicate thatsome headway is finally being made on the goals ofpublic administration reform. But there is still roomfor improvement. Only 30 percent of respondentsnoted a decline in the time necessary to receiverequired stamps and signatures from provincialbureaucrats and only 24 percent observed areduction in official fees for these services.

Transparency, an area of tremendous achievement inthe country in the past years, shows remarkabledecline in 2009. Access to provincial planningdocuments and the percentage of firms that believerelationships are necessary to receive businessdocumentation (61.3 percent) are back to 2006levels after consistent improvement over time.Similarly, the percentage of firms claiming thatimplementation of central laws is predictable (8.4percent) and the share of businesses negotiatingwith the local tax authority (41 percent) are backto 2007 levels.3

Interestingly, transparency of legal documents hasimproved over the same period, leading to afascinating puzzle. Why have planning documentsbecome more difficult to obtain while legalnormal documents (laws, decrees, implementingordinances, and provincial decisions) have becomeeasier to access?

We theorize that the dichotomy results from thefact that commitments made under the WorldTrade Organization and the Bilateral TradeAgreement with the United States have compelledpolicy makers to improve access to legislationthrough such advances as the Law on Laws (2008)

3. These worrisome results are supported by our analysis of a separatepanel dataset of 2,500 firms answering in multiple years.

Hard data measures of infrastructure demonstrateslightly slower improvement, indicating that firms areresponding positively to these initial forays intoinfrastructure improvements.

Analyzing the Ha Noi expansionThe annexation of Ha Tay province, Me Linh districtof Vinh Phuc, and the Luong Son of Hoa Binh bythe Hanoi city government created an interestingopportunity to observe how an exogenous changein borders affects the quality of governance, as wellas business performance and prospects.

Treating the new parts of Hanoi as separateprovinces finds that Hanoi would actually rankslightly behind Me Linh and Ha Tay. In other words,the addition of these provinces actually raised Hanoi’sfinal PCI scores slightly, although the changes areminor. For firms in Ha Tay and Luong Son, the mergerinto Hanoi did not lead to worse governance.Businesses in these provinces may have been affectedby the shock of transition and the difficulties oflearning the locations of new agencies. Nevertheless,we can expect that their business prospects will notbe greatly altered in the long term.

For businesses located in Me Linh district, however,there is more reason for concern. Comparingsimilar groups of firms in Me Linh and Vinh Phucsuggests that firms in Me Linh are significantly morenegative about a range of governance indicatorsthan their counterparts in Vinh Phuc. If governancematters for economic performance, and wecertainly believe it does, there is reason to worrythat the merge may have negative long-termimplications for Me Linh businesses and the welfareof citizens in that district.

Changes in PCI methodologyOne challenge that the PCI faces is the difficulty ofkeeping pace with the dynamism of the Vietnameseeconomy and changes in the country’s regulatoryenvironment. To ensure that the PCI is relevant tocurrent needs of Vietnamese policy makers, the

2009 PCI has been altered slightly. Indicators andsub-indices whose utility had become obviated bychanges in the Vietnamese economy were dropped,appropriate new indicators were added, andweighting of sub-indices was re-calibrated to reflectthe changing importance of different aspects ofgovernance.

These changes are documented in Chapter Threeof this report. By far this most important changewas the decision to drop the index measuring biastoward local state-owned enterprises (LSOEs).Massive equitization of LSOEs means that, in mostprovinces, biased incentives toward LSOEs nolonger pose an obstacle to private sectorperformance. While we recognize that there are stillsignificant issues with centrally managed enterprises(CSOEs), particularly in terms of access to bankcapital and land, these are central-level policydiscussions that cannot be appropriately measuredby surveys of businesses located in Vietnameseprovinces. Analysis of biases toward CSOEs requiresan empirical approach beyond the scope of the PCI.

The methodological changes had very little impacton the overall ranking of provinces. There is a strongstatistical correlation (0.84) between the 2009 and2008 rankings. This is roughly the same as previousyears, indicating that the ranking of governance isquite stable, but provinces do have opportunities tomake improvements that can raise their scores.

As an additional test, we also re-created the 2009index without dropping the state-owned enterprisebias index. The correlation between the final PCIand the index containing the state-ownedenterprise bias is 0.93, indicating that the changesdid not have a strong impact on firm rankings.

18 THE VIETNAM PROVINCIAL COMPETITIVENESS INDEX 2009

CHAPTER ONE

BACKGROUND ANDKEY FINDINGS

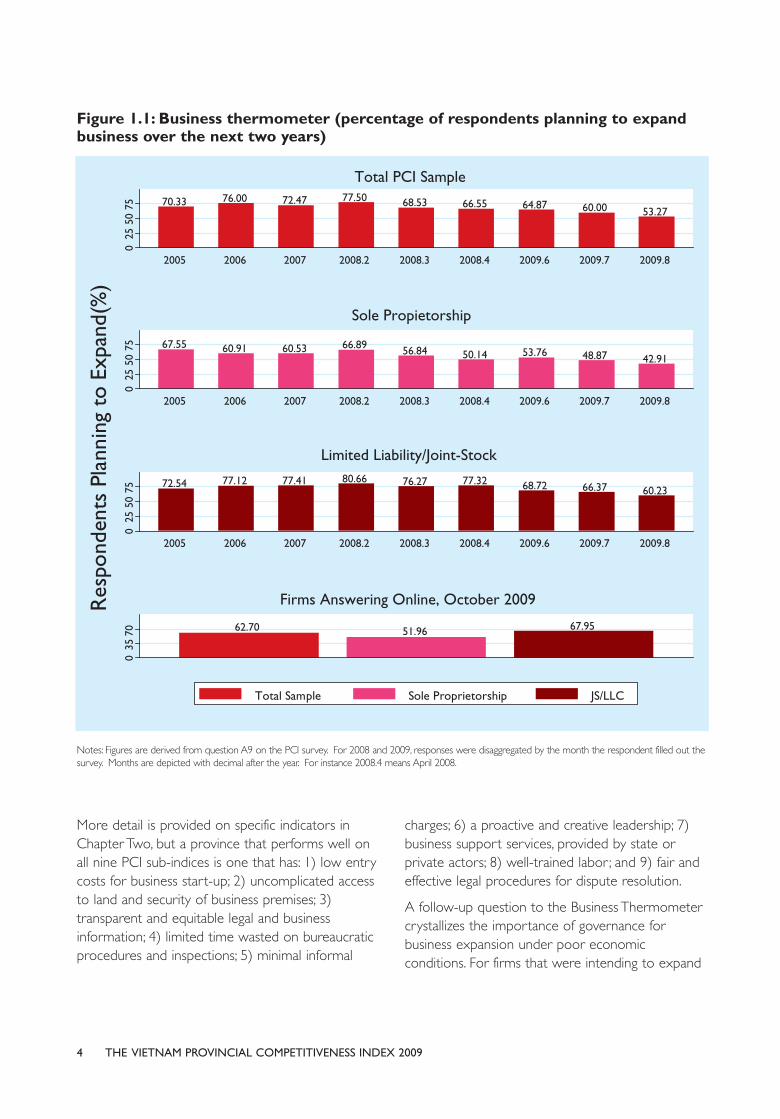

Each year, the Provincial Competitiveness Index(PCI) research team asks respondents about theirbusiness plans for the next two years. The questionis such an excellent gauge of future growth andeconomic development in Vietnam that we havedubbed it the “Business Thermometer.” This year,Business Thermometer answers carry an ominousmessage. Despite macroeconomic figures indicatingthat Vietnam has escaped the worst of the 2009global financial crisis, the optimism thatcharacterized entrepreneurs a few years ago hasdeclined over time. Far fewer businesses plan toexpand their operations over the next two years.

Figure 1.1 depicts the trends in the businessthermometer. Responses for 2008 and 2009 aresub-divided by the date that the entrepreneur filledout the survey, so that we can track the nuancedchanges in business responses as Vietnam’seconomic stimulus was implemented. Results for2009 indicate that business confidence actuallydeclined over the summer.4 In addition, results aresub-divided by the legal form of enterprises.Declines for sole proprietorships are greater for thelarger and more sophisticated legal forms, but adeclining trend is clear for all types of companies.Should this current prediction prove accurate, itcould have long-term negative implications forVietnam’s economy because less business expansionimplies less job creation and less taxable revenue.

It is in these periods of declining business optimismthat economic governance becomes mostimportant for the decisions of entrepreneurs.Business owners are concerned about theirprospects for the future because they are uncertainboth about economic events outside of the controlof Vietnamese policy makers and about the policydecisions of Vietnamese officials themselves. In suchan environment, clear, transparent, and fairregulatory rules and policies become paramount.The 2009 PCI is a useful tool for assessing how thequality of governance is affecting firm decisions.

At its root, the PCI is the voice of 9,890 domesticprivate firms, collected in a survey of the opinionsof private entrepreneurs regarding economicgovernance in their provinces. After someadjustments on the basis of published data toaddress perception biases, the survey responses areaggregated into provincial-level scores. The finaloutcome is a composite index ranking Vietnam’s 63provinces according to their performance on nineaspects of governance that are critical for privatesector development.5 As a result, the PCI providesthe most objective metric available for gauging theimpact of economic and administrative reforms atprovincial and national levels.

3THE VIETNAM PROVINCIAL COMPETITIVENESS INDEX 2009

BACKGROUND ANDKEY FINDINGS

4. There is a small uptick in October 2009, but we should be cautiousabout interpreting too much from this information. The Octoberrespondents are composed of a small group of firms who respondedto the survey using our online platform. They tend to be bigger andmore sophisticated and are predominantly in Hanoi and Ho ChiMinh City. Thus, it is not clear whether opinions are improving or thisgroup is systematically different from earlier respondents.

5. Previous iterations of the PCI had 10 sub-indices, but the sub-indexmeasuring bias toward local state-owned enterprises was droppedthis year. See Chapter Three for more details.

4 THE VIETNAM PROVINCIAL COMPETITIVENESS INDEX 2009

Figure 1.1: Business thermometer (percentage of respondents planning to expandbusiness over the next two years)

Notes: Figures are derived from question A9 on the PCI survey. For 2008 and 2009, responses were disaggregated by the month the respondent filled out thesurvey. Months are depicted with decimal after the year. For instance 2008.4 means April 2008.

More detail is provided on specific indicators inChapter Two, but a province that performs well onall nine PCI sub-indices is one that has: 1) low entrycosts for business start-up; 2) uncomplicated accessto land and security of business premises; 3)transparent and equitable legal and businessinformation; 4) limited time wasted on bureaucraticprocedures and inspections; 5) minimal informal

charges; 6) a proactive and creative leadership; 7)business support services, provided by state orprivate actors; 8) well-trained labor; and 9) fair andeffective legal procedures for dispute resolution.

A follow-up question to the Business Thermometercrystallizes the importance of governance forbusiness expansion under poor economicconditions. For firms that were intending to expand

5THE VIETNAM PROVINCIAL COMPETITIVENESS INDEX 2009

Figure 1.2: Relationship between governance and selection as location

Notes: Vertical axis displays the natural log of the number of times entrepreneurs from other provinces selected province as possible location for expansion. lnindicates natural log of variable taken. The natural log of number of selections is taken to address outliers and allow for easier graphical depiction.

their businesses, we further queried whichprovinces, outside of their own, they envisioned asthe most attractive places for business expansion.Figure 1.2 depicts the results of this query. Thenumber of times a province was selected as aninvestment location is shown on the vertical axis,while the 2009 PCI score is shown on thehorizontal axis.6 A large number of firms selectedthe urban centers of Hanoi (352), Ho Chi Minh

City (HCMC) (493), and Da Nang (221), which,because of their large, middle-class populations,offer attractive markets for domestic sales. Settingaside these choices, however, we can see that thenumber of times a particular province was selectedis strongly associated with provincial economicgovernance, as measured by the PCI. For instance,Binh Duong received 335 selections, Vinh Phucreceived 98, and the correlation between these twovariables is statistically significant 0.40. In theseuncertain times, it appears that ambitious investorsare using governance as a focal point for theirbusiness decisions.

6. The natural log of number of selections is taken to address outliersand allow for easier graphical depiction.

One might imagine that governance is just a proxyfor other attractive factors for investors, such asinfrastructure or population size. Figure 1.3 tacklesthis issue by presenting the results of regressionanalysis of number of selections as investmentlocation on provincial PCI scores, controlling for arange of other factors. The marginal effect of eachvariable is depicted with a diamond between rangebars illustrating 90 percent confidence intervalsaround the estimate. Variables where range barscross over zero are considered not statisticallysignificant because we cannot be certain that inrepeated iterations of the survey the variable willcontinue to have a positive relationship withlocational choices.

The analysis reveals that four variables aresignificantly associated with the selection of aprovince for new investment: 1) governance, as

measured by the PCI; 2) wealth, measured by GDP;3) surface area, indicating that geographicallydispersed provinces tend to attract investors,perhaps because of easier access to land orresources; and 4) road quality measured by thepercentage of asphalted roads. Distance from themajor cities of Hanoi and HCMC is negative, butjust shy of statistical significance -the farther aprovince is from these locations, the less likely it isto be chosen as an investment location.

We can interpret the substantive implication of the reddiamonds directly off the figure. For each one pointimprovement in the unweighted PCI score of aprovince, three more investors were likely to choose itas an investment location. This is a sizable effect. By wayof comparison, a 10 percentage point improvement inthe amount of asphalted road would yield about thesame number of selections by potential investors.

THE VIETNAM PROVINCIAL COMPETITIVENESS INDEX 20096

Figure 1.3: Drivers of locational choice

Notes: Results of multiple regression analyzing number of companies wishing to expand to new province. Results are from a negative binomialregression with robust standard errors. Dependent variable is the number of times a province was selected as the site of future investment.Non-displayed controls include dummy variable for city and geographic region. The Pseudo R-Squared for the regression is 0.799 and the LogLikelihood is -276.76 and significant at the .001 level.

THE VIETNAM PROVINCIAL COMPETITIVENESS INDEX 2009 7

In years past, the PCI report has demonstrated aretrospective correlation between governance andinvestment-PCI scores were strongly correlatedwith previous investment in the province.7 Thisyear’s result is more important for policy makersbecause it is prospective-PCI scores are correlatedwith future investment.

The bottom line is that in difficult economic times,good economic governance is critical for raising theconfidence of investors. Entrepreneurs will votewith their feet, choosing the locations where publictransparency allows for better forecasting ofbusiness prospects and where equitable and fairprocedures lower undue risk. The PCI provides animportant measure of these factors.

A picture of the PCI respondentsThe claim that the PCI represents the collective voiceof the private sector is an ambitious one. Who arethese entrepreneurs who are selected to speak for theentire business community? After all, any bias in theselection of operations affects the value of theinformation that can be gleaned from the survey.

By delineating the PCI sample according to keyfactors, Table 1.1 shows that firms answering the PCIsurvey look much like the business community as awhole, representing all sizes and flavors ofentrepreneurial activity in Vietnam. This, of course, isby design. Respondents are randomly selected from alist of registered private firms that is supplied by theNational Tax Authority, stratified by business age,sector, and legal form. The process ensures a highlyrepresentative sample.8

7. This finding remains true. Multiple regressions of enterprises percapita, investment per capita, average profitability and GDP on thePCI scores, controlling for infrastructure and endowments, revealsthat governance is still strongly correlated with business performanceand welfare in 2009. See Chapter Four for regression results.

8. Results are based on a stratified random sample and mail-out surveyin each province, yielding a national response rate of 25 percent,about the same as in 2008. Response rates are similar throughout thecountry, so non-response bias is likely systematic across jurisdictions.Last year, we followed up with non-responders in our survey, findingthat 21 percent of our mail-out went to firms that were no longer inexistence or had moved their operations, or where the Tax Authorityhad incorrect contact information. Taking these into account, our trueresponse rate is 31.7 percent.

Table 1.1: Who answers the PCI survey? Composition of the 9,890 total respondents

Provincial SampleCharacteristic National Sample

Legal Form

Sole Proprietorship

Limited Liability

Joint Stock

Joint Stock with Shared Listed on Stock Exchange

Partnership and Other

Sector with Majority Output

Manufacturing/Construction

Service/Commerce

PCI

35.5%

45.3%

18.6%

0.2%

0.4%

PCI

32.7%

56.9%

Median Tax Authority

27.2%

46.0%

10.6%

NA

0

Median Tax Authority

42.0%

52.6%

Weighted PCI

19.5%

57.1%

22.9%

0.2%

0.3%

Weighted PCI

29.6%

64.9%

Total Tax Authority

22.1%

57.5%

20.4%

NA

0

Total Tax Authority

34.5%

62.2%

8 THE VIETNAM PROVINCIAL COMPETITIVENESS INDEX 2009

Provincial SampleCharacteristic National Sample

Agriculture/Aquaculture

Natural Resources

Age of Firm

Registered Before Enterprise Law

Registered After Enterprise Law

Size of Operations (Employees)

Under 5

5–9

10–49

50–200

Over 200

Size of Operations (Total Assets, Billions of VND)

Under 0.5

From 0.5 to under 1

From 1 to under 5

From 5 to under 10

From 10 to under 50

Over 50

History of Company

Greenfield Private Company

Began Operation as Household Enterprise

Former Local State-Owned Enterprise (SOE)

Former Central SOE

7.6%

2.8%

PCI

14.2%

85.8%

PCI

15.0%

21.6%

41.8%

15.9%

5.7%

PCI

12.2%

17.1%

43.1%

14.2%

10.3%

3.3%

2.4%

2.3%

Median Tax Authority

4.2%

95.8%

Median GSO

13.60%

35.72%

36.65%

10.21%

3.8%

Median GSO

15.5%

18.2%

42.7%

7.8%

7.6%

8.2%

4.6%

0.9%

Weighted PCI

13.3%

86.7%

Weighted PCI

14.2%

22.5%

41.6%

16.0%

5.7%

Weighted PCI

12.3%

16.4%

42.3%

14.2%

10.2%

4.5%

1.9%

1.4%

Total Tax Authority

5.96%

94.04%

GSO Census

13.5%

46.8%

30.4%

7.3%

2.1%

GSO Census

12.1%

16.6%

48.8%

9.5%

8.8%

4.2%

PCI

29.4%

63.5%

5.8%

1.3%

Weighted PCI

33.5%

60.3%

4.5%

1.6%

9THE VIETNAM PROVINCIAL COMPETITIVENESS INDEX 2009

Provincial SampleCharacteristic National Sample

Owner Background

University Degree

MBA

Leader of State Agency

Military Officer

Former Manager of SOE

Former SOE Employee (Never Manager)

Primary Customers

Vietnamese Individuals and Companies

State-Owned Companies

State Agencies

Export Directly or Indirectly

Foreign Individuals or Companies in Vietnam

PCI

42.1%

1.5%

5.1%

7.0%

14.9%

19.6%

PCI

58.3%

14.9%

16.8%

7.0%

3.1%

Weighted PCI

58.4%

4.0%

4.6%

6.5%

14.2%

15.8%

Weighted PCI

58.1%

15.0%

11.4%

8.6%

6.9%

Notes: PCI is the PCI survey sample, stratified at the provincial level. Median Tax Authority provides the values in the median province. Total TaxAuthority shows the national-level aggregate scores. GSO Census is the 2008 Enterprise Census of the General Statistical Office(http://www.gso.gov.vn/default_en.aspx?tabid=479&idmid=4&ItemID=7184).

Thirty-five percent of respondent firms are soleproprietorships, 45 percent are limited liabilitycompanies, and 18 percent are registered as joint-stock companies. By design, these proportionsreflect the average provincial patterns. Thus, oursample is perfectly adjusted to each province.

Because the PCI sampling strategy is intended tomirror provinces, it requires that we sample a largerportion of businesses in small provinces than wouldbe necessary if we were taking a nationallyrepresentative sample. As a result, larger cities suchas Hanoi and HCMC represent a smaller share ofthe PCI sample than they do national-level privatesector activity. This can be misleading for the

diagnosis of national-level trends, because larger andeconomically important provinces are under-represented among PCI respondents. For example,according to the GSO Enterprise Census, the fivenational-level cities plus Binh Duong, Dong Nai, andBa Ria-Vung Tau (BRVT) account for 59 percent oftotal private operations in the country, but only 22percent of the business operation in the PCI sample.Table 1.2. shows the mismatch between the goals ofprovincially representative samples in the PCI andnational representation for these eight importantprovinces. As a result, trying to infer national-levelpolicy decisions from unweighted PCI descriptivestatistics would be biased toward smaller provinces.

To capture national-level trends, it is necessary toadjust answers slightly, so provinces with largepopulations of private sector operations are notunder-represented. To do this, we re-weightanswers by the proportion of total businessescontained in a single province. After thisadjustment, firms located in more populous areasreceive a slightly higher weight, so their locationsreceive the equivalent weight to the one theywould have in a nationally representative sample.These nationally weighted responses are shown incolumn 3 of Table 1.2.

Nineteen of the joint-stock companies in thesample are traded on either the Hanoi or Saigonstock exchanges. These enterprises included in thesurvey account for about 7 percent of all listedfirms and include some of the most importantoperations in the country.

Over half of the respondents are engaged in theservice or commerce sectors, and about 32percent are involved in manufacturing or

construction. By way of comparison, according tothe Tax Authority data, 62 percent of registeredfirms are involved in service and commerce and35 percent in manufacturing and constructionnationally. Eighty-six percent of PCI respondentsregistered after the 2000 Enterprise Law; 14percent precede that law and, therefore, registeredunder older, less efficient procedures.

Forty-three percent of firms have between 1 billionVND ($56,000) and 5 billion VND ($282,500) intotal assets. Twenty-nine percent of firms have lessthan 1 billion VND in assets and 27 percent haveover 5 billion VND. Three percent of firms haveover 50 billion VND ($2.8 million) in assets. This isnot a dramatic share of large firms, but it doesmirror national-level data. Over 41 percent of firmshave between 10 and 50 employees. Six percent ofrespondents have more than 200 employees and50 companies have more than 1,000.

Sixty-three percent of PCI respondents beganoperations as household firms before they decided

10 THE VIETNAM PROVINCIAL COMPETITIVENESS INDEX 2009

ProvincePCI Sample National Representation

HCMC

Ha Noi

Hai Phong

Da Nang

Dong Nai

Binh Duong

Can Tho

BRVT

8 Provinces

National

Number

435

508

207

263

253

204

144

165

2,179

9,890

Proportion

4.4%

5.1%

2.1%

2.7%

2.6%

2.1%

1.5%

1.7%

22.0%

100.0%

Number

43,116

25,628

4,193

3,899

3,418

3,311

2,016

1,457

78,852

147,314

Proportion

29.3%

17.4%

2.8%

2.6%

2.3%

2.2%

1.4%

0.9%

59.0%

100.0%

Table 1.2: PCI Sample versus National Representative Sample

Notes: Data taken from 2008 GSO Enterprise Census.

to formalize their activities by registering atprovincial Departments of Planning andInvestment. This is a critical statistic because itdemonstrates that some provincial businessenvironments are conducive to formalization.9 Atotal of 693 (7 percent) enterprises resulted fromequitizations (the Vietnamese form of privatization)of local or central SOEs. An additional 14.9percent of companies have owners who formerlymanaged SOEs, and 19.6 percent have ownerswho worked in some capacity for an SOE. Finally,about 30 percent of firms are greenfield entities,meaning that their owners established andregistered the firms at roughly the same time.

With respect to nationally representative data,most companies concentrate their business activityon the domestic market, selling either toVietnamese individuals and private companies (58percent) or to SOEs or state agencies (26percent). About 9 percent are actively engaged inexporting, either directly or indirectly throughtrading companies. This is a relatively small numbergiven the importance of exports for theVietnamese economy. Nevertheless, it reflects thefact that exports tend to be dominated by largebusinesses (especially foreign and statecompanies), and that enormous export potentialamong smaller private entities remains untapped.

An additional 7 percent of companies sell primarilyto foreign companies or individuals based inVietnam. It is remarkable that sales to SOEs andstate agencies are roughly four times those to theforeign sector : the tremendous growth of foreigndirect investment in Vietnam has not createdsubstantial opportunities for private producers.10

Finally, and quite importantly for the purposes ofthe PCI, all of Vietnam’s 63 provinces arerepresented in the Index. The average number ofresponses per province was 157, with only oneprovince (Lai Chau) having fewer than 75respondents. Nevertheless, the 63 firms that didanswer in Lai Chau account for about one-third ofall operations in the rural, Northwestern locality.

The final 2009 Provincialcompetitiveness rankingWeights

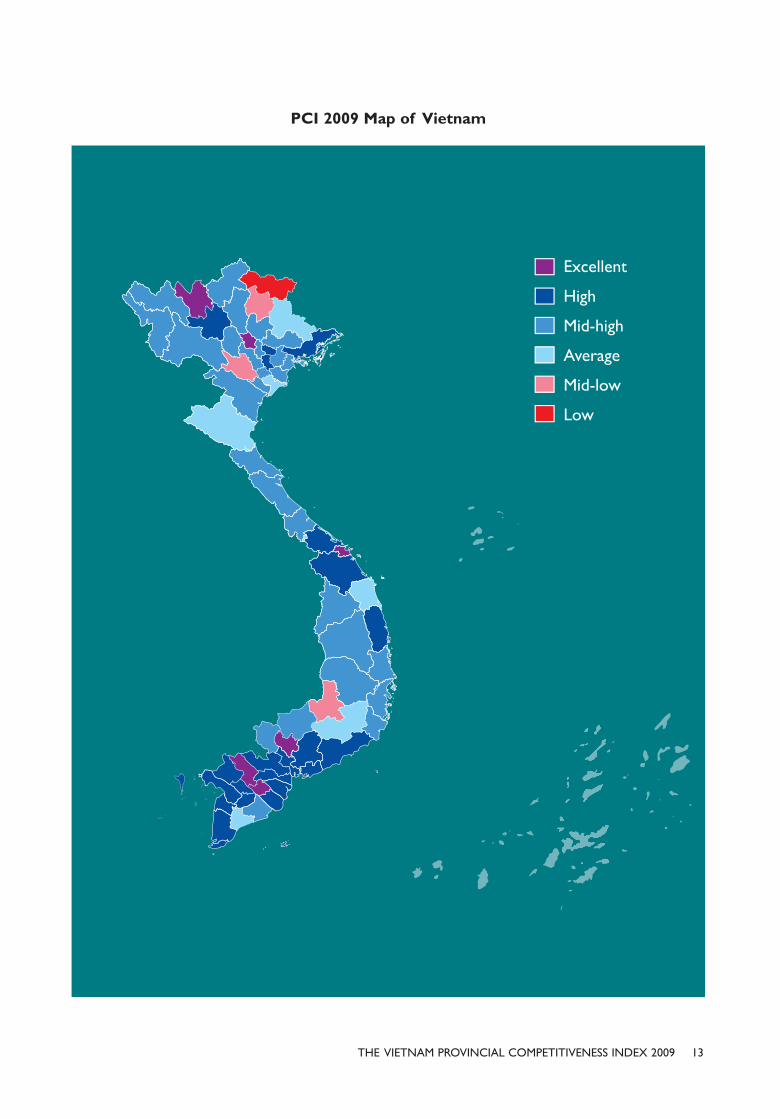

The weighted 2009 PCI ranking is shown in Figure1.4. Each province is ranked on a 100-point scale.As in 2008, Da Nang (75.96) remains slightlyahead of the perennially excellent Binh Duong(74.01). Also reaching the excellent tier this yearare Lao Cai (70.47), Dong Thap (68.54), Vinh Long(67.24), and Vinh Phuc (66.65).

11THE VIETNAM PROVINCIAL COMPETITIVENESS INDEX 2009

9. For a more detailed discussion of the formalization in Vietnam, seeMalesky, Edmund, and Markus Taussig. 2009. “Out of the Gray: TheImpact of Institutions on Business Formalization.” Journal of EastAsian Studies. 9.2: 249–79.

10. For a deeper analysis of the domestic opportunities and spillovercreated by the foreign sector, see Nguyen, N.A., T. Nguyen, D.T. Le,Q.N. Pham, D.C. Nguyen, and D.N. Nguyen. 2008. “Foreign DirectInvestment in Vietnam: Is There Any Evidence of Spillover Effects.”DEPOCEN Working Paper, Hanoi, Vietnam.

12 THE VIETNAM PROVINCIAL COMPETITIVENESS INDEX 2009

Figure 1.4: Weighted Provincial Competitiveness Index 2009

13THE VIETNAM PROVINCIAL COMPETITIVENESS INDEX 2009

PCI 2009 Map of Vietnam

14 THE VIETNAM PROVINCIAL COMPETITIVENESS INDEX 2009

The ranking represents the weighted sum of thescores of the nine sub-indices, based on the weightsshown in Table 1.3. These weights were re-calibratedin 2009 to ensure that the PCI reflects the changesin the Vietnamese economy and regulatoryenvironment. Weights were calculated using a three-step statistical procedure that is discussed in thefinal section of Chapter Three. The ultimate goal ofweighting is to ensure that PCI scores are calibratedto private sector performance and, therefore, thatthe PCI relates the most relevant information toprovincial officials regarding the impact of their

policies on private sector activity. Sub-indices thatwere shown to have the largest association withprivate sector growth, investment, and profitabilityreceived the highest weight class of 20 percent.Correspondingly, those that are not stronglycorrelated with private sector developmentoutcomes received the lowest weight class of 5percent. Medium weight classes of 10 and 15 percentwere reserved for average correlations across thethree outcome variables or a large substantive effecton one outcome (e.g., profitability), but a minimalrelationship with the other two.

Sub-Index Enterprises perCapita (ln)

Investment perCapita (ln)

Profit perEnterprise

Weights

Entry Costs

Land Access and Security

of Tenure

Transparency and Access

to Information

Time Costs of Regulatory

Compliance

Informal Charges

Proactivity of Provincial

Leadership

Business Support Services

Labor and Training

Legal Institutions

(1)

0.186*

(0.104)

-0.001

(0.091)

0.134***

(0.045)

0.089

(0.068)

0.044

(0.089)

0.014

(0.045)

0.215**

(0.092)

0.297***

(0.086)

-0.041

(0.072)

(2)

0.282**

(0.132)

0.058

(0.147)

0.167*

(0.086)

0.199***

(0.068)

0.212*

(0.126)

0.137**

(0.059)

0.251**

(0.112)

0.468***

(0.115)

0.122

(0.098)

(3)

12.585

(36.023)

31.242

(48.948)

62.440***

(20.663)

55.032**

(27.379)

90.308*

(51.523)

54.368***

(19.770)

-58.121

(42.919)

58.876

(47.141)

87.193**

(43.391)

(4)

9.61%

2.37%

19.77%

14.12%

9.00%

12.36%

6.71%

20.03%

6.04%

100%

(5)

10%

5%

20%

15%

10%

10%

5%

20%

5%

100%

1

2

3

4

5

6

7

8

9

Table 1.3: Sub-Index Weighting

True Weight Rounded

Total

Notes: Columns 1, 2, and 3 report the coefficients and standard errors (in parentheses) of the regressions of the three outcome variables (Enterprises perCapita, Investment per Capita, and Profit per Enterprise) on each sub-index, controlling for structural factors (population density, surface area, distancefrom Hanoi or HCMC in kilometers), infrastructure (measured by the percentage of paved road in the province), and dummy variables for the sevenregions of Vietnam (known as regional fixed effects). Column 4 reflects the true weight that would be assigned to this variable given the cumulativevariance it explains in the three outcome variables. Column 5 reports rounded weights that will be used for the next five years.

Because weights are calibrated to reflect theimportance of sub-indices for private sectordevelopment, they reveal important information. Most

importantly, we learn that the single biggest factors inimproving PCI scores and thereby economicdevelopment are Transparency and Labor Quality.

15THE VIETNAM PROVINCIAL COMPETITIVENESS INDEX 2009

The Sub-Indices of the PCI

As in early reports, the PCI 2009 uses a range of indicators that are grouped into nine compositesub-indices:

1. Entry Costs: A measure of 1) the time it takes a firm to register and acquire land; 2) the timeto receive all the necessary licenses needed to start a business; 3) the number of licensesrequired to operate a business; and 4) the perceived degree of difficulty to obtain alllicenses/permits.

2. Land Access and Security of Tenure: A measure combining two dimensions of the landproblems confronting entrepreneurs: how easy it is to access land and the security of tenureonce land is acquired.

3. Transparency and Access to Information: A measure of whether firms have access to theproper planning and legal documents necessary to run their businesses, whether thosedocuments are equitably available, whether new policies and laws are communicated to firmsand predictably implemented, and the business utility of the provincial webpage.

4. Time Costs of Regulatory Compliance: A measure of how much time firms waste onbureaucratic compliance, as well as how often and for how long firms must shut theiroperations down for inspections by local regulatory agencies. This year, the index alsoincludes a battery of indicators measuring progress on public administration reform (PAR).

5. Informal Charges: A measure of how much firms pay in informal charges, how much of anobstacle those extra fees pose for business operations, whether payment of those extra feesresults in expected results or “services,” and whether provincial officials use compliance withlocal regulations to extract rents.

6. Proactivity of Provincial Leadership: A measure of the overall attitude of provincial officials aswell as their creativity and cleverness in implementing central policy, designing their owninitiatives for private sector development, and working within sometimes unclear nationalregulatory frameworks to assist and interpret in favor of local private firms.

7. Business Support Services: A measure of the availability of business services, such as privatesector trade promotion, provision of regulatory information to firms, business partnermatchmaking, and technological services for firms; the number of private providers of theseservices; and the quality of these services.

8. Labor and Training: A measure of the efforts by provincial authorities to promotevocational training and skills development for local industries and to assist in theplacement of local labor.

9. Legal Institutions: A measure of the private sector’s confidence in provincial legal institutions;whether firms regard provincial legal institutions as an effective vehicle for dispute resolutionor as an avenue for lodging appeals against corrupt official behavior.

16 THE VIETNAM PROVINCIAL COMPETITIVENESS INDEX 2009

Importance of transparency forprivate sector developmentThis is the fifth year that transparency has receivedthe highest weight in the PCI, despite alterations inmethodology and economic crises in 2008 and2009. There are important reasons whytransparency of business information has criticalimplications for the success of entrepreneurs. Whenentrepreneurs have adequate information about aprovince’s initiatives regarding regulatory changes,infrastructure roll-outs, or land-use planning, theycan forecast their investment prospects deep intothe future. The more comfortable they feel aboutlong-term business prospects, the more willing theywill be to risk their hard-earned capital today. Whenentrepreneurs are worried about sudden changes inregulation, infrastructure, or land, they will hold backfrom large-scale projects, investing incrementally asthey test the waters.

Transparency also allows entrepreneurs to shieldthemselves against potential abuses by unscrupulousofficials, if they exist. The more information thatbusinesses have about the law, the less likely theywill fall prey to officials using compliance regulationsas means of attracting rents. Businesses can learnabout these regulations ahead of time and makenecessary adjustments. Far too often in Vietnam,businesses are blind-sided when they learn that theyare in violation of government regulations that theyhad never heard about. When they are presentedwith this information by government inspectors,they find that they must pay expensive fines, engagein time-consuming adjustments, or resolve theproblem through more surreptitious meansinvolving informal payments. If the business manageris able to access the regulations ahead of time,these episodes could be avoided.

Similarly, more information about infrastructure willensure that capable firms can turn premier businessland into productive business operations. Currently,the most valuable land, such as premises adjacent tonew roads or near industrial zones, often ends up inthe hands of those with better access toinformation about new land conversions or roadimprovements. Individuals with insider informationare not necessarily those who could make the bestuse of those assets. As a result, key business

locations in many Vietnamese provinces areinefficiently deployed. Transparency and a fairauction of these valuable assets would lead to farmore productive investments, benefitting businessoperators and the welfare of province. Readingdirectly off the regression coefficients, we can seethat a one point improvement in transparencyyields a 13 percent improvement in enterprisesper capita, a 17 percent improvement ininvestment per capita, and a 62 million VNDincrease in firm profitability. 11

Importance of labor quality forprivate sector developmentLabor quality is also very important. A key businesscomplaint in multiple surveys is that there is notenough semi-skilled and skilled labor to handle andmaintain equipment or manage complex businessand financial processes. Firms are finding it difficultto upgrade technology and expand operationswhen they are handicapped by an insufficient talentpool. General education, vocational education, andlabor exchange bureaus in provinces have laggedbehind the business needs of many firms.

As we discuss in Chapter Three, this year’s PCIoffers a more thorough metric of labor quality thattakes into account the participation of privatetraining providers. Figure 1.5 shows that ourmeasure of labor quality is strongly associated withother measures of general education. Provinces thatreceived the highest average scores on collegeadmission exams in 2009 are the same ones whererespondents are most satisfied with the labor talentpool. This finding may indicate that generaleducation is a critical way to improve labor quality.Although a small portion of secondary educationrecipients may migrate to urban centers for college,investment in high-quality teachers and training willhave long-term implications for the skill-sets ofindividuals remain in the province as well.12 Of thefour different types of college entrance exams, TypeB shows the strongest correlation (0.59) with Labor

11. See Chapter Four for full regression results.12. Thanh, Nguyen Duc. 2005. Heterogeneous Talent and Optimal

Emigration: A Contribution to the New Economics of Brain Drain.Presented at the Vietnam Economic Research Conference, Hanoi:April 29.

17THE VIETNAM PROVINCIAL COMPETITIVENESS INDEX 2009

Quality.13 Not surprisingly, this is the test geared forstudents who want to study business and evaluatestraining in math, chemistry, and biology.Correlations are statistically significant but lower forthe Type A test for science education (0.49), Type Cfor social science education (0.28), and Type D forthe humanities (0.34).

These skill-sets will pay dividends in terms of private

sector performance. We find that this new measure

is strongly associated with private sector

development outcomes. Other provinces have

made significant investments in improving their labor

pool. Correspondingly, a one point improvement in

the Labor sub-index is correlated with a 30 percent

improvement in enterprises per capita, a 47 percent

enhancement in investment per capita, and a

statistically insignificant but sizable 58 million VND

increase in profitability.

13. Entrance exams are divided into four categories according to thefields of study the student plans to pursue and the universityoffering that subject. The categories of exams and the subjectstested follow: Type A: tests knowledge of math, physics andchemistry (for students of engineering, computer science, physics,etc.); Type B: tests knowledge of math, chemistry and biology (forstudents of natural sciences and business); Type C: testsknowledge of literature, history and biology (for students of socialsciences and humanities) ; Type D: tests knowledge of literature,math and foreign language (for students of foreign languages,either in education or translation/interpretation tracks). See Kelly,Kristy. 2009. “The Higher Education System in Vietnam.” WorldEducation News and Reviews <http://www.wes.org/ewenr/00May/feature.htm> for more detail.

Figure 1.5: College entrance exams and assessment of labor quality

18 THE VIETNAM PROVINCIAL COMPETITIVENESS INDEX 2009

Lower-weighted indicatorsTwo indicators receive quite low weights (LandAccess and Legal Institutions), but not because theyare unimportant; rather, they are generallyproblematic across the entire country. Very fewprovinces excel on these dimensions, leading to lowvariance across the country and, consequently, a low

correlation with private sector outcomes. Theweights on the issues hint that moving forward onboth of these dimensions will require national-levelpolicy reform in addition to provincial initiatives,which have been insufficient. Figure 1.6 shows theperformance of each Vietnamese province vis-a-visthe nine sub-indices.

Figure 1.6: Province Performance By Sub-Index

Robustness of the rankingsRobustness of performance tiers

Once again, to facilitate comparisons with previousyears, we pegged the six performance tiers(Excellent, High, Mid-High, Average, Mid-Low, andLow) to the break-points in the rankings. These tiersare robust to different weighting and indexconstruction approaches and, therefore, are morevaluable for benchmarking relative performance.Individual rankings within tiers can change quite a bit,depending on small changes in index construction.

Robustness over timeThe change in the ranking methodology cited abovehad a systematic impact across the country. No

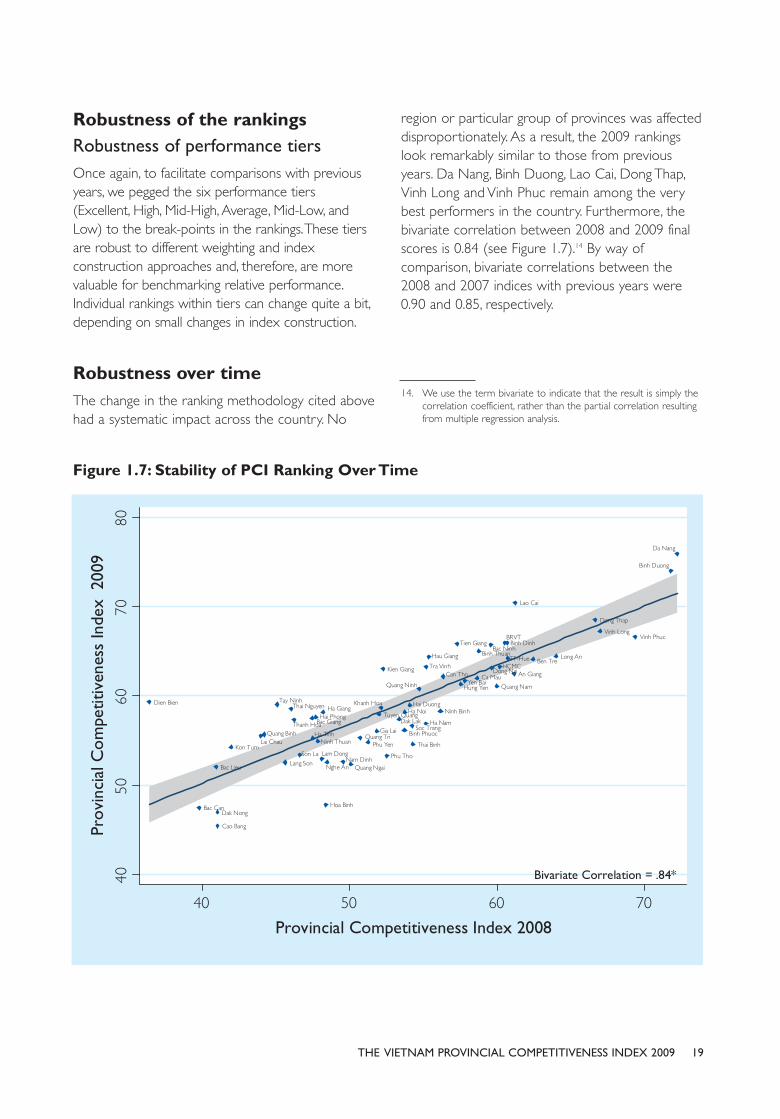

region or particular group of provinces was affecteddisproportionately. As a result, the 2009 rankingslook remarkably similar to those from previousyears. Da Nang, Binh Duong, Lao Cai, Dong Thap,Vinh Long and Vinh Phuc remain among the verybest performers in the country. Furthermore, thebivariate correlation between 2008 and 2009 finalscores is 0.84 (see Figure 1.7).14 By way ofcomparison, bivariate correlations between the2008 and 2007 indices with previous years were0.90 and 0.85, respectively.

19THE VIETNAM PROVINCIAL COMPETITIVENESS INDEX 2009

14. We use the term bivariate to indicate that the result is simply thecorrelation coefficient, rather than the partial correlation resultingfrom multiple regression analysis.

Figure 1.7: Stability of PCI Ranking Over Time

The figure shows that governance dependssignificantly on historical governance. Governancepractices cannot change overnight. It takes time toplan and implement new initiatives, and there is evena longer lag between implementation and firmsexperiencing their effects.

This consistency in the provincial rankings implies thatthe PCI can consistently identify top performers,while allowing room for other provinces to improveand receive higher scores in subsequent years. Suchstability is confirmation that the PCI approach offers aconsistent and accurate measure of provincialeconomic governance over time.

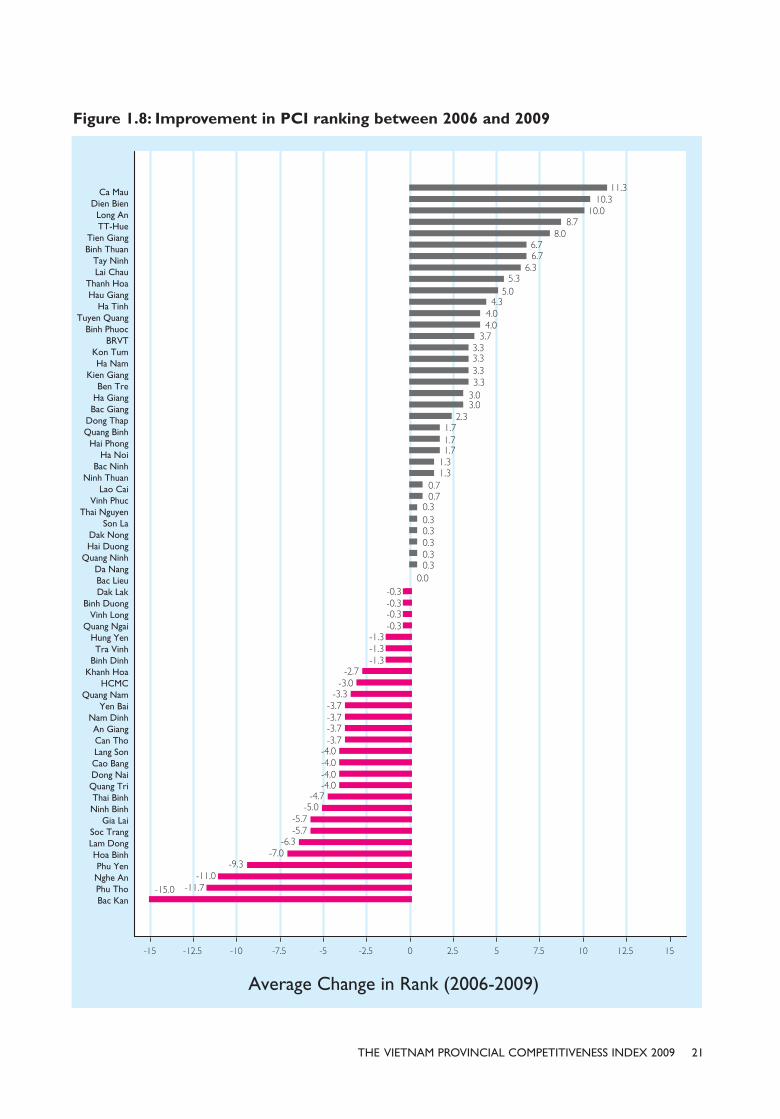

Largest improvements inprovincial PCI scores“Stability,” however, should not be confused with“static”. Over the past two years, a number ofprovinces have gradually climbed up the PCI ladder.Figure 1.8 shows the average annual change in PCIscores since 2006.

Ca Mau, Dien Bien and Long An deserve specialrecognition for having made the greatest averageannual leaps in the PCI rankings. Interestingly, theseprovinces raised their scores in very different arenas.Dien Bien made substantial improvements in reducinginformal costs, increasing the proactivity of leadership,and enhancing the quality of the labor force. Ca Maufound ways to reduce entry costs and informalcharges. Long An’s leaps were propelled by increasesin transparency, exemplified by a computer monitoroutside Long An’s Department of Natural Resourcesand the Environment where individuals can accessland-use plans, legal documents, and applicationmaterials.

Summary of nationwide trends inprovincial governanceAlthough the re-calibration of the PCI makes itdifficult to compare the weighted PCI ranking overtime, we can get a sense of trends in governancefrom observing the changes in individual indicatorsover time. Changes in scores for the median provinceprovide a useful measure of trends in national-levelperformance. Increases in the median provincetherefore indicate improvements in the indicatorthroughout the country as a whole. In general,measures of Entry Costs, Access and Security ofLand, Time Costs, Labor Quality, and Confidence inLegal Institutions show signs of definitiveimprovement over the past year. Policy makersshould be proud of these accomplishments. On theother hand, worrisome declines are evident in termsof Transparency, Informal Charges, and the Proactivityof local leaders.

Tables tracking changes in the median provinceover time for each indicator are reported inChapter Three.