the value at risk concept in financial risk ... · pdf filethe value at risk concept in...

TRANSCRIPT

THE VALUE AT RISK CONCEPT IN THE VALUE AT RISK CONCEPT IN THE VALUE AT RISK CONCEPT IN THE VALUE AT RISK CONCEPT IN FINANCIAL RISK MANAGEMENTFINANCIAL RISK MANAGEMENTFINANCIAL RISK MANAGEMENTFINANCIAL RISK MANAGEMENT

THESISTHESISTHESISTHESIS

SUBMITTED TO THE

SWISS BANKING INSTITUTE

OF THE

UNIVERSITY OF ZÜRICH

PROF. DR. RÜDIGER FREYPROF. DR. RÜDIGER FREYPROF. DR. RÜDIGER FREYPROF. DR. RÜDIGER FREY

Subject: Monetary Economics Course: Finance Author: Theresa Ursula A. Supremo Scheuchzerstr. 27 8006 Zürich Tel. 01 362 43 51 Email: [email protected] Business Economics, 11th semester Zürich, Revised Edition as of February 2001

Executive SummaryExecutive SummaryExecutive SummaryExecutive Summary

1.1.1.1. Statement of the Problem Statement of the Problem Statement of the Problem Statement of the Problem

Arriving at a single number to depict the risk shouldered by an institution in the framework of an integrated risk management system is a great challenge. First and foremost, the risks faced by the firm should be quantifiable. Second, there should be a proper risk measurement system or analytics that is able to efficiently capture risk across different risk categories. Third, the risk measures derived should share a common unit, such that they could be aggregated. Fourth, the risk measure should behave properly in the aggregation process in the sense that there will be no incoherent consequences. For instance, if there is to be a diversification effect in the portfolio, then the risk of this portfolio should be lower than the sum of isolated risk measures derived separately for single instruments comprising it.

Currently, the quantification of market risk proceeds mainly through Value at Risk (VaR). This methodology takes the potential loss facing an instrument, portfolio or firm to be equal to the loss at a particular point of a profit and loss distribution. This is established by a predetermined confidence level and conditioned by the chosen holding period. In practice, the VaR is relatively easy to compute and communicate. However, not all VaR figures calculated using the different approaches for particular portfolios are coherent. That is, there are cases where the sum of the VaRs of individual instruments is smaller than the VaR of a portfolio consisting of these two instruments. If such holds, there will be an advantage to keep instruments, accounts, subsidiaries, and firms apart so as to keep the risk figure at a minimum. Capital adequacy or margin requirements of a portfolio can be kept low via separation of the held instruments.

But VaR is not totally incoherent. For this reason, it still retains its worth as a risk measure. Nevertheless, other methodologies have been raised as alternatives. This study will look into VaR, alternative risk measures and the concept of coherency.

2.2.2.2. Procedure of the InvestigationProcedure of the InvestigationProcedure of the InvestigationProcedure of the Investigation

Axioms that have to be satisfied by risk measures in order for them to be coherent have been raised by Artzner, Delbaen, Eber and Heath (1997, 1998). These are translation invariance, subadditivity, positive homogeneity, and monotonicity. Whether the different VaR methodologies are coherent will be investigated upon. These include the parametric VaR, historical simulation and Monte Carlo simulation methods.

Executive Summary 2

The following are the axioms of coherency against which VaR will be examined:

(1) ρ(X+ N • R) = ρ(X) N. Translation invariance specifies that the addition of a risk-free investment into a portfolio will simply reduce the risk measure by as much as the value of the investment.

(2) ρ(X + Y) < ρ(X) + ρ(Y). Subadditivity states that the risk of a portfolio consisting of two instruments should be lower than or equal to the sum of the individual risks of the instruments.

(3) ρ(λ • X) = λ • ρ(X). Positive homogeneity upholds the risk of one and the same instrument to be void of any incremental risk, once the position is scaled. Increasing the size of the instrument by λ increases its risk by λ. Liquidity is hereby assumed.

(4) ρ(X) ≥ ρ(Y), if X < Y. Monotonicity proposes a ranking specification of risk measures of differing instruments. The smaller the portfolio returns, the greater is its risk.

3.3.3.3. ResultsResultsResultsResults

Parametric VaR or the variance-covariance approach builds on the mean and variance of a profit and loss distribution to come up with the potential loss of an instrument or portfolio, given a holding period and confidence level. The assumption made is that risk factor movements follow a normal distribution. This determines the consequently normally distributed profit and loss distribution. Knowing the portfolio mean and variance, one could easily calculate the VaR of a particular confidence level. The VaR is the difference between the mean and the value at the specified quantile of the distribution. One actually arrives at this on the basis of the variances of the risk factors. The weighted variances are added together, while allowing for correlations. The total volatility is then multiplied with the corresponding quantile factor. Analyzed as against the axioms of coherency, parametric VaR qualifies as a coherent risk measure. This holds for a distribution with a confidence level above 50% and a joint multivariate normal distribution of risk factors. The accuracy of the risk measure can however only be certified under the delta-normal approach. This approach assumes a linear relationship of the risk factors to the value of the portfolio. The existence of non-linear relationships in the portfolio, e.g. options, cannot be efficiently captured. Furthermore, satisfactory results cannot be reached with the use of the specialized delta-gamma approach.

In contrast, the VaR derived from historical simulation does not always satisfy the most crucial subadditivity axiom. The sum of the VaR of a given portfolio X and portfolio Y is, in some cases, smaller than the VaR of a portfolio with X and Y together. Historical simulation arrives at the VaR by taking historical data on the risk factors and inputting them into the valuation formula of the given instrument or portfolio. These are then subtracted from the current value. The VaR is the value at

Executive Summary 3

the specified quantile of the number of days or data chosen. Why this methodology sometimes comes up with superadditive values lies in the fact that the percentile VaR calculated for a portfolio combination of individual instruments is largely dependent on the valuation function of the portfolio and the factors inputted, whose correlations are not taken into consideration. The values that are entered to construct the profit and loss distribution of the chosen period fall into play arbitrarily.

The same holds for the VaR results of Monte Carlo simulation. Subadditivity is not at all times respected. Under this methodology, the values of risk factors follow a process specified by a random generator. Similar to historical simulation, the VaR is the value at the specified quantile of the resulting randomly generated profit and loss figures. The VaR is thus made dependent on the inputted risk factors, whose correlations need not be considered by such a random generation of the risk factor values. The portfolio VaR need not be the same as the sum of the individual VaRs of the instruments. It may even exceed it, depending on the portfolio components.

As an alternative to VaR, the maximum loss methodology has been upheld by Studer (1997) as a coherent risk measure that moreover captures the non-linear behavior of portfolios efficiently. Under maximum loss, probability information is made use of to arrive at the likely loss that the portfolio will face, given a particular threshold of risk factor values or a trust region. A whole distribution need not be set up. The minimum of the values of the profit and loss function derived on the basis of the selected risk factor values is the maximum loss. Correlations between the risk factors are carried over by the risk factor processes assumed.

Another coherent risk measure can be derived from the expected shortfall methodology. The expected shortfall is the average of the losses of an instrument that is beyond a given benchmark or limit. It has a quite simple methodology and provides information on the extent of loss beyond VaR or any given benchmark value.

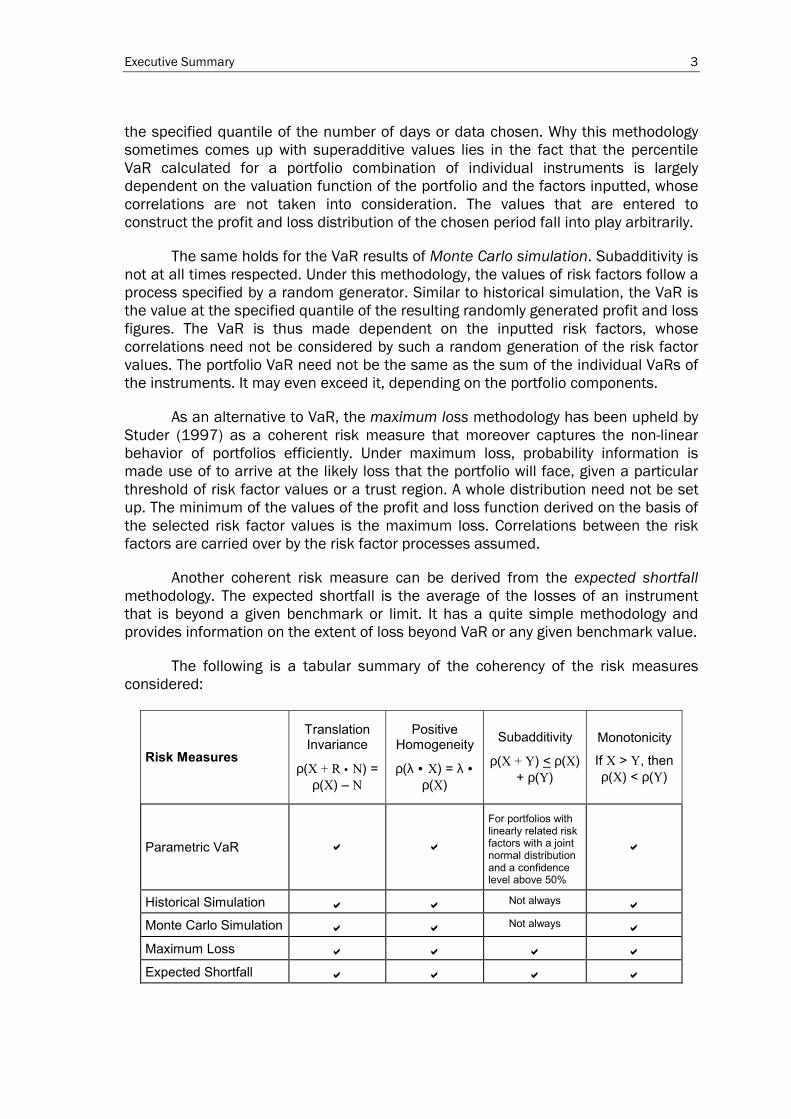

The following is a tabular summary of the coherency of the risk measures considered:

Risk Measures

Translation Invariance

ρ(X + R • N) = ρ(X) N

Positive Homogeneity

ρ(λ • X) = λ • ρ(X)

Subadditivity

ρ(X + Y) < ρ(X) + ρ(Y)

Monotonicity

If X > Y, then ρ(X) < ρ(Y)

Parametric VaR

For portfolios with linearly related risk factors with a joint normal distribution and a confidence level above 50%

Historical Simulation

Not always

Monte Carlo Simulation

Not always

Maximum Loss

Expected Shortfall

Executive Summary 4

VaR is disadvantaged by its occasional non-adherence to the axiom of subadditivity. Moreover, a look into the computational framework of the different methodologies indicate how some methodologies do not efficiently capture the true VaR. Parametric VaR, as said, buckles down when the portfolio involves non-linear components. Fat tails, which occur in reality, are also not efficiently captured. Monte Carlo simulation is in this regard better. Variations in time and extreme scenarios are also captured. The modeling used in Monte Carlo should however take pains to capture reality as most probably done by a historical simulation. In line with accuracy, other dependence measures other than correlation should perhaps be looked into in order to capture well the intricacies of non-linear relationships, which are not considered by the distributional assumptions of correlation measurement.

4.4.4.4. General EvaluationGeneral EvaluationGeneral EvaluationGeneral Evaluation

In spite of its drawbacks, VaR however continues to dominate in the risk measurement practice. Current research on credit risk measurement is also heading towards the direction of VaR-based measurement. That is, credit-at-risk akin to value-at-risk is sought to be measured. Making credit risk measurement compatible with VaR will facilitate in the near future the integration of market and credit risk factors into a single risk measure derived from the same VaR-based methodology.

What are the prospects for the extensive use of expected shortfall and maximum loss? Considering the wide acceptance of VaR, a sharp turn towards these alternative methods is not to be expected. These may however not be the case in the long run. Adhering to coherency without hitches, expected shortfall and maximum loss measurement could be the upcoming tools of integrated risk management.

Subadditivity is indeed a relevant consideration. Its violation leads to dumb consequences. It cannot be that a trader would have an advantage of separating two instruments from each other, because he or she will be required lesser capital for the maintenance of these instruments in isolation as compared with holding them in a portfolio. Knowing that VaR measurement has occasional troubles with subadditivity should not simply be laid aside. The information that VaR provides is however of worth, such that VaR measurement remains feasible. For as long as subadditivity is respected in capital requirement measurement, VaR could still come up with reliable information.

But adherence to the axioms of coherency need not be the criterion in choosing the best risk measurement methodology. Much as the axioms are helpful in the determination whether particular risk measures are sound for whatever purpose that they may serve, e.g., for capital or margin requirements, the axioms of coherency should not be the ultimate basis for choosing an appropriate risk measurement methodology. If we use risk measures for investment choice, then the axioms are not sufficient, because what they emphasize is the behavior of the risk measures. No focus is given on the returns.

Executive Summary 5

Possible grounds for choosing a risk measurement methodology are its usefulness in the analyses required by the firms financial activities. Others could revolve around economic considerations and the type of additional information that the methodology yields. The simplicity of its application is also a plus factor, although not the most essential. The following table summarizes the properties of the different risk measurement methodologies against the four enumerated criteria:

VaR Maximum Loss Expected Shortfall

Coherency Subadditivity violated at times

Coherent Coherent

Information provided

The potential loss specified at a chosen quantile of a distribution

The minimum of the profit and loss function of a dense trust region of risk factor values; it captures non-linear behavior efficiently

The mean of the expected losses beyond a benchmark value

Economic considerations

Simulation infrastructure requires much resources

The calculation requires much resources

Relatively fewer data requirements

Simplicity Simple Complex Simple

In this regard, expected shortfall gains ground against the other risk measurement methodologies, as its methodology is coherent, simple and economical. There is also additional information on the extent of loss beyond a certain established tolerance level.

But whatever risk measurement methodology be in prominent use in the future, what is important is that the risk measure indeed captures what is desired to be captured by a particular analysis, may it be for total enterprise-wide risk management or investment choice analysis decisions. Coherency is necessary. But so is axiomatic investigation validity.

Table of ContentsTable of ContentsTable of ContentsTable of Contents

List of FiguresList of FiguresList of FiguresList of Figures................................................................................................................................................................................................................................................................................................................................................ iiiiiiii List of TablesList of TablesList of TablesList of Tables .................................................................................................................................................................................................................................................................................................................................................... iiiiiiii List of Abbreviations and SymbolsList of Abbreviations and SymbolsList of Abbreviations and SymbolsList of Abbreviations and Symbols ........................................................................................................................................................................................................ iiiiiiiiiiii Chapter 1Chapter 1Chapter 1Chapter 1 INTRODUCTIONINTRODUCTIONINTRODUCTIONINTRODUCTION....................................................................................................................................................................................................................................................1111

1.1 Historical Background............................................................................................. 1

1.2 Regulatory Requirements....................................................................................... 2

1.3 Risk and its Different Types.................................................................................... 3

Chapter 2Chapter 2Chapter 2Chapter 2 THE VALUE AT RISK CONCEPTTHE VALUE AT RISK CONCEPTTHE VALUE AT RISK CONCEPTTHE VALUE AT RISK CONCEPT ....................................................................................................................................................5555

2.1 What is Value at Risk? ............................................................................................ 5

2.2 Calculating Value at Risk........................................................................................ 7

2.2.1 Parametric VaR ............................................................................................... 7

2.2.2 Historical Simulation.....................................................................................12

2.2.3 Monte Carlo Simulation................................................................................15

2.3 Criticisms on VaR ..................................................................................................16

2.3.1 General Evaluation .......................................................................................16

2.3.2 Summative Evaluation from a Computational Perspective .......................18

Chapter 3Chapter 3Chapter 3Chapter 3 Value at Risk and CoherencyValue at Risk and CoherencyValue at Risk and CoherencyValue at Risk and Coherency ................................................................................................................................................ 20202020

3.1 Coherency..............................................................................................................20

3.1.1 Translation Invariance [ρ(X+ N • R) = ρ(X) N] .........................................21

3.1.2 Subadditivity [ρ(X + Y) < ρ(X) + ρ(Y)] ........................................................21

3.1.3 Positive Homogeneity [ρ(λ • X) = λ • ρ(X)] ...................................................21

3.1.4 Monotonicity [ρ(X) ≥ ρ(Y), if X < Y] ...............................................................22

3.2 The Coherency of VaR...........................................................................................22

3.2.1 The Coherency of Parametric VaR (Delta-Normal) .....................................23

3.2.2 The Coherency of Historical Simulation ......................................................24

3.2.3 The Coherency of Monte Carlo Simulation..................................................27

3.3 Alternatives to VaR................................................................................................28

ii

3.3.1 Maximum Loss ..............................................................................................28

3.3.2 Expected Shortfall.........................................................................................30

Chapter 4Chapter 4Chapter 4Chapter 4 CONCLUSIONCONCLUSIONCONCLUSIONCONCLUSION .................................................................................................................................................................................................................................................... 35353535

ReferencesReferencesReferencesReferences ............................................................................................................................................................................................................................................................................................................................................ 39393939

LiLiLiList of Figuresst of Figuresst of Figuresst of Figures

Figure 1: An overview of the value-at-risk concept...................................................... 5

Figure 2: Value at risk methodologies.......................................................................... 6

Figure 3: Parametric VaR methods .............................................................................. 7

Figure 4: Expected Shortfall.......................................................................................... 31

List of TablesList of TablesList of TablesList of Tables

Table 1: Hypothetical data used for the historical simulation VaR............................ 15

Table 2: Summary of the features of VaR.................................................................... 17

Table 3: Problematic factors related to mathematical considerations ..................... 18

Table 4:Subadditivity of the parametric VaR of elliptical distributions...................... 23

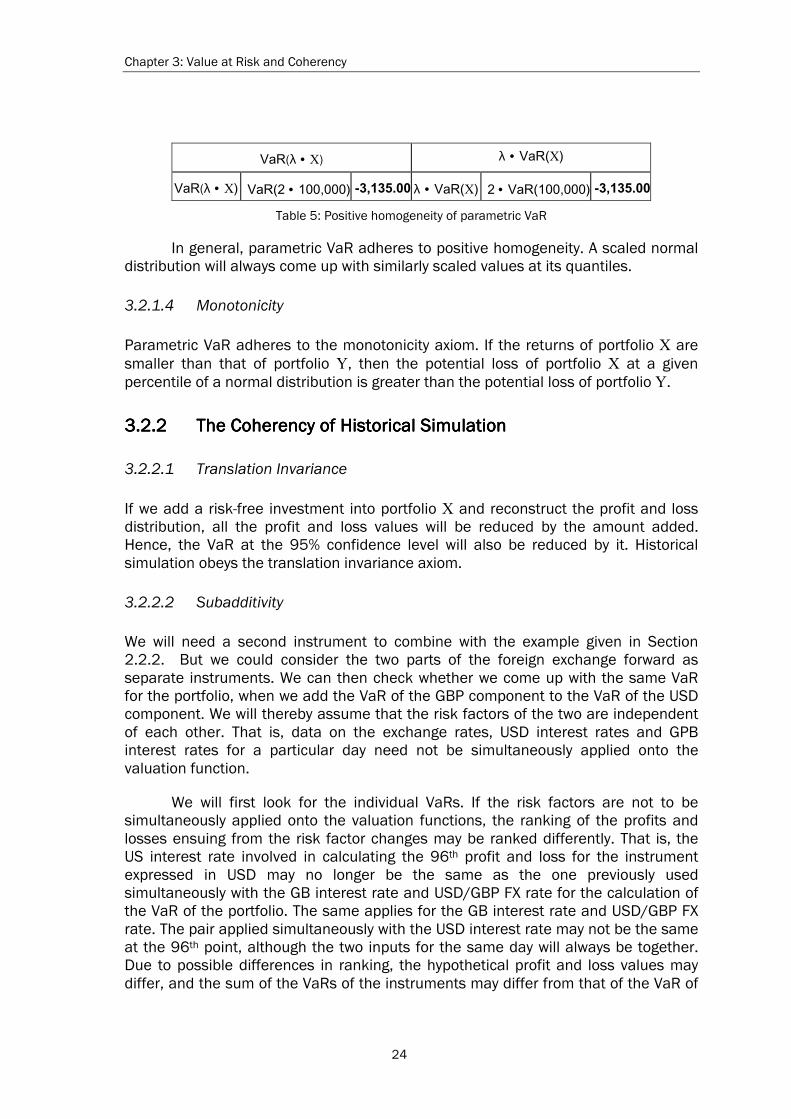

Table 5: Positive homogeneity of parametric VaR ...................................................... 24

Table 6: Subadditivity of the VaR per historical simulation........................................ 25

Table 7: Violation of subadditivity of percentile VaR................................................... 25

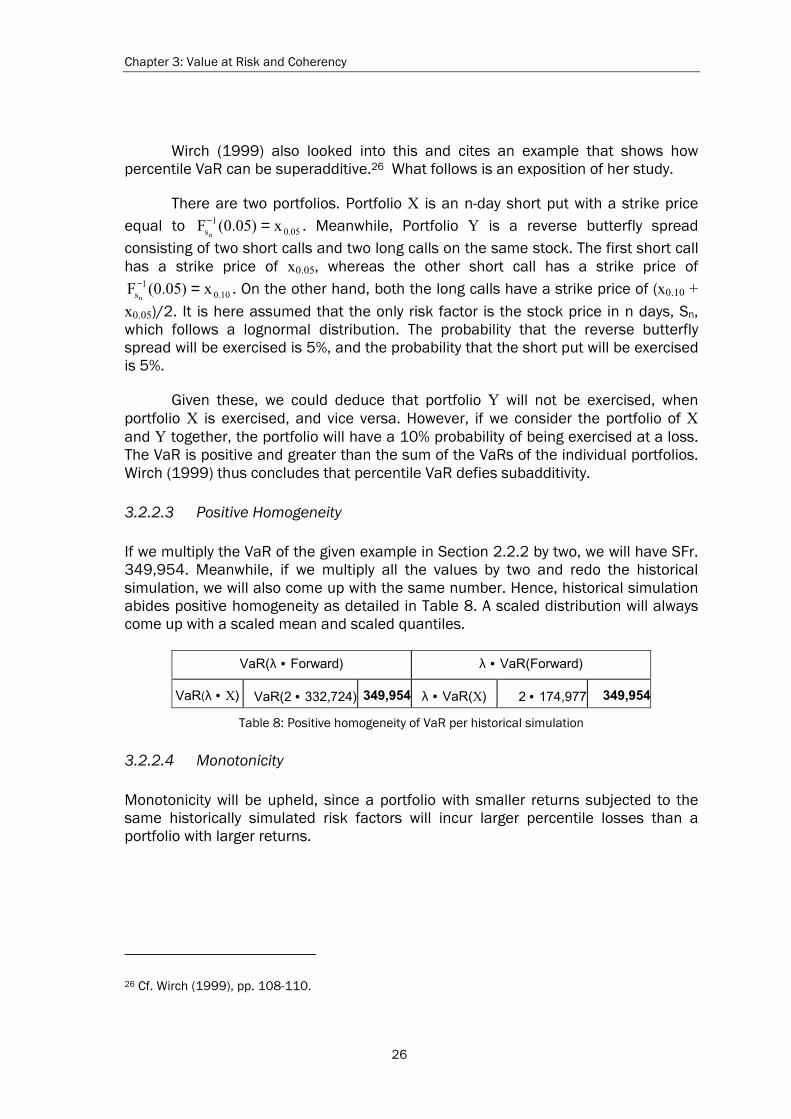

Table 8: Positive homogeneity of VaR per historical simulation ................................ 26

Table 9: Data on portfolios X and Y .............................................................................. 33

Table 10: Expected shortfall of the portfolio of X and Y together .............................. 33

Table 11: Subadditivity of expected shortfall .............................................................. 33

Table 12: Comparison of VaR, maximum loss and expected shortfall...................... 37

iii

List of Abbreviations and SymbolsList of Abbreviations and SymbolsList of Abbreviations and SymbolsList of Abbreviations and Symbols

α confidence level

B benchmark value

cα quantile value

cov covariance

T trust region, a subset of Ω (maximum loss methodology)

FX foreign exchange

GBP British pound (Great Britain = GB)

λ a scaling factor or a positive number

LPM lower partial moment

µ mean

n number of variables

N additional risk-free investment

Ω the total set

P probability

PF portfolio

q risk factor

r interest rate

R total returns

IR real number

ρ risk measure

σ standard deviation

σ2 variance

correlation matrix

SFr Swiss francs

t years

USD United States dollar

υ random variable

iv

υ(ω) a profit and loss function or a random value function

V(X) value of a security X

VaR Value at Risk

w weight factor

[w] sensitivity vector (VaR)

[w]t transposed sensitivity vector (VaR)

ω scenario, random value

X a security or returns of a security X

Y a security or returns of a security Y

Chapter 1Chapter 1Chapter 1Chapter 1 INTRODUCTIONINTRODUCTIONINTRODUCTIONINTRODUCTION

1.11.11.11.1 Historical BackgroundHistorical BackgroundHistorical BackgroundHistorical Background

Risk management has gained much importance over the years. Incidence of catastrophic investments that were not subjected to careful surveillance caught the attention of several financial institutions. Primary importance has then been given to the development of strategies to prevent financial mishaps, as well as to the measurement of the potential loss faced by the firm.

A look at historical developments shows us how markets have fluctuated increasingly. In other words, market variables have grown to be quite volatile. With the flexibility lent to the exchange rates of various currencies against the dollar back in the 1970s, exchange rate fluctuations and its repercussions onto other market factors became mighty powers behind international market developments. Moreover, increased international capital mobility and reduced trade barriers have paved the way for a high level of market interdependence. Effects of stock market crashes, oil price shocks and financial crises have thus crossed national and regional borders. We have witnessed this in the case of the Asian financial crisis, which has turned several stock markets haywire not only in Asia but also in Russia and in the Americas. The threat of contagion faced subsequently by industrial countries is indicative of the fact that sound fundamentals do not provide a surefire assurance against financial market turmoil.

Meanwhile, several types of financial instruments have surfaced not only as a way of insuring firms from catastrophic outcomes but also as a result of innovations fostered by developments in financial theory and technology. But the variety of products, the numerous possibilities they allowed and the strategies and ensuing rampant speculation taken on by various institutions have also contributed to market uncertainties. The renowned case of the failure of the high-risk Long Term Capital Management fund and the brouhaha it caused attest to this fact.

Risk management has thus become a must in view of the volatile and increasingly complex market. The delivery of a single number that would spell out the potential loss faced by a firm was first conceptualized and launched by J. P. Morgan in 1994. If not for previous developments in financial theory such as the Markowitz portfolio theory and Sharpes model of security risk set against a market index, the emergence of such a conceptualization would not have materialized. Quite revolutionary, J. P. Morgans so-called 4:15 reports demanded a clear-cut figure indicating succinctly the risk exposure of the firm an improvement from other

Chapter 1: Introduction

2

analyses such as duration and gap. To accomplish this, a system had to be set up in order to come up regularly with a quick estimate. Correlations taken into consideration, a single estimate would already indicate how much of a given value is at risk. This was called the Value at Risk (VaR). With its public disclosure and incorporation in regulatory risk measurement systems, the VaR technique grew in popularity.

1.21.21.21.2 Regulatory RequirementsRegulatory RequirementsRegulatory RequirementsRegulatory Requirements

The use of VaR to come up with capital adequacy level requirements was put forward by regulatory authorities. In 1996, the recommended techniques for risk measurement entailed VaR measurement.

If we take a look at the historical flow of events, we would note that the need for risk management and measurement was first officially put into paper by the Bank of International Settlement (BIS) in 1988. Sufficient capital as coverage against credit risk was required. This was equal to 8% of the total risk-weighted assets, 50% of which must be stock issues and disclosed reserves. Moreover, large risks pertaining to exposures that entail more than 10% of a banks capital was restricted.

In 1996, market risk was added into the consideration. This came about because of the aforementioned market developments primarily characterized by market volatility and increased incidence of financial debacles. Sufficient capital must be held to cover market risks as well. Two possibilities towards the encapsulation of the potential risks were laid down: a standard BIS-formulated approach and an internally adopted approach subject to quantitative and qualitative criteria. The standard methodology utilizes a building block approach for the calculation of the potential risk for every risk category. It is based on the VaR concept.

In the light of recent developments including the financial crisis of the late 1990s, a new capital adequacy framework is currently being worked upon. Intensive analyses are undertaken to find the appropriate capital charges for interest rate risks in the banking book for banks with highly risky investments.1 The proper treatment of operational risks is also under study. In general, three pillars have already been put forward: minimum capital requirements, a supervisory review process and the effective use of market discipline.

Capital requirements have always been central from the very beginning. Hence, this pillar entails the same fundamental concepts as before. VaR continues to be the primary method recommended in the estimation of risk, although the standard approach is on review. Mainly, a new risk-weighting scheme and the

1 In the 1996 amendment, only the trading book was relevant in the calculation of the interest and equity risks.

Chapter 1: Introduction

3

allowance of alternative internal ratings-based approaches are being sought. Moreover, the standardization of approaches in portfolio credit risk modeling, as well as the approaches used in measuring risks from credit derivatives and other instruments, is being looked into. The main thrust is to improve the way regulatory capital requirements reflect underlying risks. It is also sought to better address the financial innovations of the recent years. The advent of innovations has made the current regulation less effective in matching capital requirements with a banks true risk profile.

The need for the second pillar a supervisory review process has come up to ensure that a banks capital position is consistent with its overall risk profile and strategy. This has been fashioned to encourage early supervisory intervention. Supervisors will have the ability to require banks to hold capital in excess of the minimum required capital. This has not been covered by earlier frameworks as the consideration was centered on the conditions of the G-10 countries, which contributed to the drafting of the existing regulation. As for the third pillar on market discipline, the main aim is to encourage disclosure or transparency.2

1.31.31.31.3 Risk and its Different TypesRisk and its Different TypesRisk and its Different TypesRisk and its Different Types

Risk management is a policy-based measurement, regulation and control system of the risks affecting the financial activities of an institution. Insofar as a total risk figure is sought for a whole firm encompassing several types of risk we speak of integrated risk management or enterprise-wide risk management. Risk, on its part, is the uncertainty involving future developments that affect the value of an instrument. This definition does not leave out the occurrence of excessive, rarely occurring positive returns at a certain point, which could actually turn out bad at a later time. Thus, a large dispersion from the normal case whether towards negative or positive extremes means a high degree of riskiness. Risk can take on many forms or can be grouped into different categories:

Business risk is the uncertainty faced in view of the particular business activity that has been taken on. For example, European airlines face the business risk that more and more people utilize speedy trains for short routes instead of boarding a plane. The jet business might prove to be unprofitable in the long run. Financial risk, meanwhile, encompasses the uncertainty involving future developments that affect the value of asset holdings and possibly impair liquidity or solvency.

Financial risk can ensue from various sources:

2 Cf. BIS (2000a), pp. 1-2.

Chapter 1: Introduction

4

Market risk is the uncertainty or potential adversity faced by financial assets or values due to fluctuations in market factors, such as stock prices, indices, commodity prices, interest rates and exchange rates.

Credit risk is the uncertainty or potential adversity faced by capital lenders due to developments that affect their lending activities. Movements in interest rates could for example be detrimental to the value of debt. Moreover, losses can ensue from a downgrading, since debt market value recedes. Credit risk is also oftentimes referred to as default risk. As a matter of fact, several literature take credit risk to be default risk. The thin line that demarcates them is the fact that the latter refers concretely to the potential adversity resulting from the prospect that a given agreement will not be honored by a counterparty, may it be a credit or a swap agreement, whereas credit risk need not end up with an actual failure of payment. Nevertheless, default risk is the primary component of credit risk, and both types of risk are affected by the same set of factors. That is the reason behind their assumed synonymy. Moreover, insofar as the solvency of the borrower is affected by market risk, credit risk and default risk are intertwined with market risk.

Liquidity risk is the potential adversity ensuing from difficulties in dissolving, e.g., encashing, a given asset at a particular point in time. This type of risk is however difficult to quantify. A standard or universal liquidity risk measurement approach has not yet been laid down.

Similarly, the appropriate measurement of operational risk is still in question. Operational risk is the potential adversity faced as a result of system failures or manipulations. Measuring this requires both estimating the probability of an operational loss event and the potential size of the loss.3

Legal risk is the potential adversity arising from various lawfully imposed conditions: non-enforceability of a particular transaction or business activity, penalties from non-compliance of regulations including lawsuits, etc.

To perform its function well, risk management relies on the accuracy of the adopted risk measurement technique for the above-mentioned risk types. Risk measurement could however not proceed if the risk is not quantifiable. If it were quantifiable, then the risk measurement methodology or analytics used should come up with risk measures having a common unit in order to add them all up.

VaR measurement is focused on the measurement of market risk. The inclusion of credit risk into the VaR figure will have to consider closely the correlations existing between these two types of risk, albeit the VaR already has the problem of ensuring the consideration of the correlations between the different market risk factors. Insofar as the VaR comes up with an aggregate risk figure, it is a useful tool in integrated risk management.

3 Cf. BIS (2000b), p. 4.

Chapter 2Chapter 2Chapter 2Chapter 2 THE VALUE AT RISK CONCEPTTHE VALUE AT RISK CONCEPTTHE VALUE AT RISK CONCEPTTHE VALUE AT RISK CONCEPT

2.12.12.12.1 What is Value at Risk?What is Value at Risk?What is Value at Risk?What is Value at Risk?

The Value at Risk is a numerical figure signifying the potential loss of an asset or portfolio, given a certain holding period and confidence level. The holding period is the length of time that a security or portfolio is held or the specific time horizon chosen for the analysis, whereas the confidence level is a statistical property denoting in percentage form the boundary level of the values or the probability of occurrence of a particular value. For instance, a 95% confidence level denotes the quantile or percentile corresponding to 95% of the whole set of calculated values. Selecting a confidence level is thus akin to specifying a tolerance level for the change in values. Choosing the holding period and confidence level proceeds arbitrarily, although it has implications on the derived VaR.

Concretely, if we have an asset X, the value that we are at risk of losing, say, in a days time at a 95% confidence level is the difference between the mean of the assets value and the value at the 95th quantile of the probability distribution of the assets values after one day. The VaR is equal to the distance X95% and µ. We are 95% sure that the loss over one day will not exceed this amount. This is illustrated in Figure 1.

Figure 1: An overview of the value-at-risk concept

σσσσ

X95% µ

VaR

Value-at-Risk (VaR)

Value

Chapter 2: The Value at Risk Concept

6

We see here that the VaR is dependent on the left-side boundary value corresponding to the selected tolerance level. The µ and σ stand for the mean and standard deviation of the distribution, respectively.

In simple mathematics, the VaR is generally:

α−µ= X)relative(VaR , (1 )

where µ is the expected value of the asset X, and Xα is the value of X at the chosen confidence level.

The above equation results to a VaR relative to the mean. VaR may also be taken relative to 0. The VaR in this case will then be an absolute potential loss. It is equal to the negative of the value of the asset or portfolio at the selected confidence level:

α−= XX)absolute(VaR 0 , (2 )

where X0 is equal to zero.

Note that in a standard normal distribution, the mean is always equal to zero.

As already seen, a distribution is required for the VaR computation. Methods used in arriving at a distribution may vary, depending on the type of approach preferred to arrive at the VaR. These several approaches with which the VaR may be calculated may be classified in various literature differently, but some order could be established. In general, VaR methodologies can be classified into two: analytical and numerical. Figure 2 provides an overview of the VaR methodologies broken down to their approaches.

Value at Risk Methods

Analytical Numerical

Parametric VaR

Historical Simulation

Monte Carlo

Simulation

Figure 2: Value at risk methodologies

Source: Brouwer/Densing (2000)

Chapter 2: The Value at Risk Concept

7

Briefly, analytical VaR denotes an assessment of the parameters that underlie a profit and loss distribution. The approach that belongs to this type is the parametric VaR. Numerical VaR, on the other hand, is a calculation of VaR based on serial data4, as its name implies. This includes the historical simulation and Monte Carlo simulation approaches.

Parametric VaR, historical simulation and Monte Carlo simulation are normally the three approaches discussed by various literature. The following sections undertake an explanation on the risk measurement followed by these approaches.

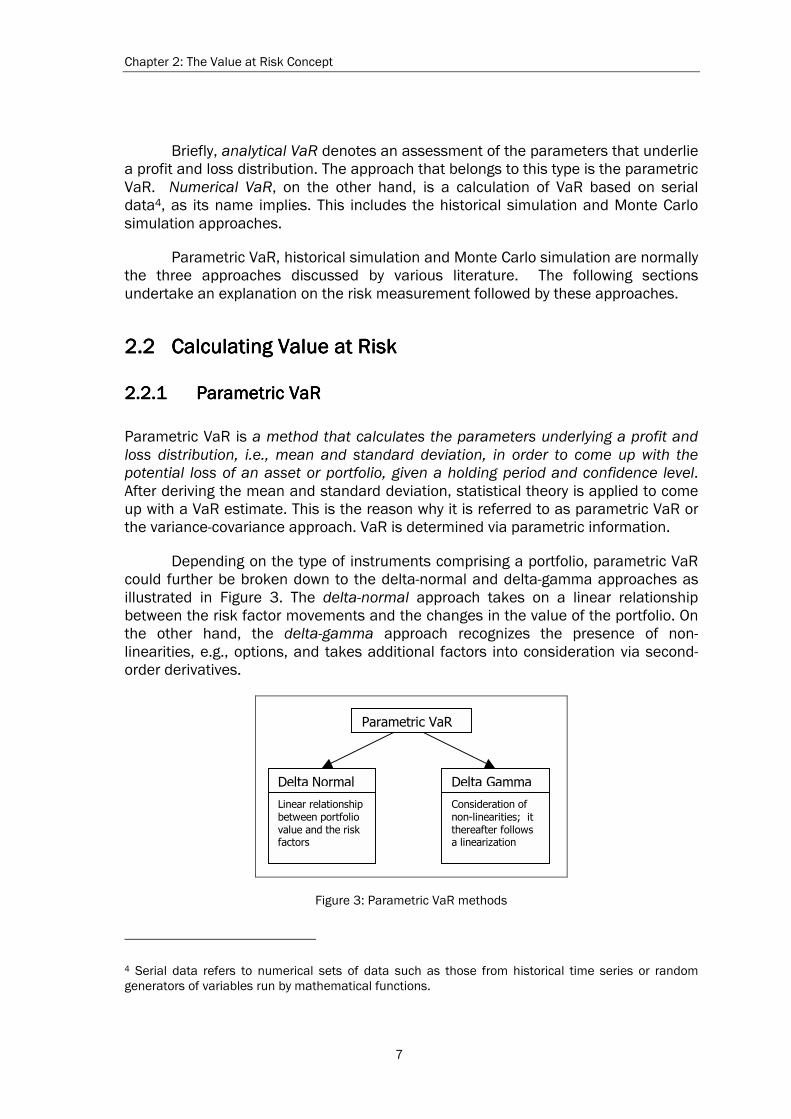

2.22.22.22.2 Calculating Value at RiskCalculating Value at RiskCalculating Value at RiskCalculating Value at Risk

2.2.12.2.12.2.12.2.1 PaPaPaParametric VaRrametric VaRrametric VaRrametric VaR

Parametric VaR is a method that calculates the parameters underlying a profit and loss distribution, i.e., mean and standard deviation, in order to come up with the potential loss of an asset or portfolio, given a holding period and confidence level. After deriving the mean and standard deviation, statistical theory is applied to come up with a VaR estimate. This is the reason why it is referred to as parametric VaR or the variance-covariance approach. VaR is determined via parametric information.

Depending on the type of instruments comprising a portfolio, parametric VaR could further be broken down to the delta-normal and delta-gamma approaches as illustrated in Figure 3. The delta-normal approach takes on a linear relationship between the risk factor movements and the changes in the value of the portfolio. On the other hand, the delta-gamma approach recognizes the presence of non-linearities, e.g., options, and takes additional factors into consideration via second-order derivatives.

Parametric VaR

Delta Normal Delta Gamma

Linear relationship between portfolio value and the risk factors

Consideration of non-linearities; it thereafter follows a linearization

Figure 3: Parametric VaR methods

4 Serial data refers to numerical sets of data such as those from historical time series or random generators of variables run by mathematical functions.

Chapter 2: The Value at Risk Concept

8

Risk factor movements determine the profit and loss distribution, and ergo, the mean and standard deviation. A set of risk factors that are known to affect the value of the asset is then required for the analysis. From the assumed movements in the risk factors, the distribution of profits and losses of the asset or portfolio can be constructed. It is further assumed that a given risk factor distribution applies for the whole length of the period covered. Moreover, as the individual risk factors accounted for in the distribution are not independent of each other, correlations are taken into account. This will be elucidated in the coming section.

2.2.1.1 Delta-Normal Method

The delta-normal method is a parametric VaR method that arrives at the VaR after building a distribution of profit and loss values based on an assumption of a linear relationship between the value of a position and the movements of underlying risk factors. A further assumption is that such risk factor movements follow a normal distribution. Consequently, the resulting distribution of values is also normal.

To illustrate the assumption of linearity, let us for example assume that two risk factors affect the value of a portfolio X. The sensitivity or delta of the portfolio value with respect to two risk factor changes is expressed as follows:

22

11

dqq

)X(Vdq

q

)X(V

dq

)X(dV

∂∂+

∂∂≈ , (3 )

where V(X) is the value of a portfolio X, whereas q1 and q2 represent the two risk factors.

This denotes the effect of a change in one unit of the risk factors. Arriving at the total value changes and their mean will require further operations. The task involved in VaR calculation is the determination of the mean and variance of these values, so that we will obtain the parameters of a distribution the quantile of which is our value at risk. The mean of the distribution should be the sum of all the expected portfolio value changes. But we will take the mean of the value changes to be equal to zero (we are dealing with a standard normal distribution). Ergo, the key figure is the standard deviation.5 We will primarily look into the volatility of the returns.

The formula of the standard deviation of a distribution of portfolio value changes allows for the covariances of the risk factors. The variance of an instrument with two risk factors is expressed as:

)q,qcov(ww2ww 21qq2

q2

q2

q2

q2

212211+σ+σ=σ , (4 )

5 Cf. Linsmeier/Pearson (2000), p. 53.

Chapter 2: The Value at Risk Concept

9

where w1q and w

2q signify the weighting6 of the risk factor change as we are purporting here a linear relationship, and cov(q1, q2) is the covariance of the two risk factors.

The challenge is then to find out the variances of the individual risk factor changes and their correlation or covariance. The variance of the portfolio is expressed as the sum of the variances and covariances.

What if there are more than two risk factors? The variance formula will be:

+ σ=σ= ≠==

n

1i

n

ij,1jjijqiq

n

1i

2

iq2

iq2 )q,qcov(www (5 )

In matrix form, this will be:

[ ] [ ]ww t2 Σ=σ , (6 )

where Σ represents the covariance matrix, and [w] is the variance vector.

What is then the value at risk? Fundamental to the determination of the VaR is the choice of the holding period and confidence level. Given that the holding period and confidence level has been determined, the VaR may then be calculated as:

( )[ ]σα−µ=VaR , (7 )

where α is the statistically derived value corresponding to the desired quantile to be multiplied with the standard deviation (e.g., 1.65 for a 95% confidence level).

If the mean is equal to zero, the VaR could be reduced as:

)(VaR σα−= (8 )

or in matrix form:

]w[]w[VaR t Σα−= . (9 )

Given the VaRs of individual instruments, the portfolio VaR is:

[ ] [ ] [ ]VaRVaRVaR t ⋅Σ⋅−= ,7 (10 )

6 This will be the sensitivities in the portfolio, i.e., ∂V(X)/∂qi* qi. 7 Cf. Biermann (1999), p. 112. The transformation of Equation 9 to this expression is indicated therein.

Chapter 2: The Value at Risk Concept

10

which is similar to our standard deviation equation in matrix form.

This is the general idea behind parametric VaR and more specifically, the delta-normal approach. But the method through which the parameters are taken may vary. Risk mapping, for instance, is a RiskMetrics methodology that reduces the instruments within the portfolio into simple, approximating instruments, whose sensitivities are estimated. This avoids the task of computing numerous variances.

Given the assumptions, parametric VaR is relatively fast and easy to compute and not too prone to model risk. The data requirements are also considerably attainable. The number of criticisms, as summarized below, might be disconcerting, but it should be noted that this methodology has in practice provided good approximations of the VaR. The standard deviation provides far more information than mere quantiles based on values taken from history or a random generation function.8 Moreover, in terms of utility theory-based analyses, this is the only VaR approach does not violate the rational ranking of choices based on expected utility value.9 Among the criticisms are10:

- The stipulated linear relationship of the risk factors to the value of the position is only an approximation. Portfolios containing a significant number of options may not be optimally assessed.

- The size of the covariance matrix increases geometrically as the number of assets increases.

- It assumes a normal distribution of returns. This is negated by empirical evidence that suggest fat tails.

- Volatility is taken to be a function of the assumed normal distribution of risk factor returns weighted by sensitivities. Whether volatility is indeed determined by this function is uncertain. It is observable that prices are also conditioned by the conditions of the times. If prices yesterday were volatile, it will also likely be volatile tomorrow. Just as the stochastic process followed by price movements is under question in financial theory, the volatility function espoused here is an inference.

- It is greatly disadvantaged under extreme situations. It accounts for such situations as stock market crashes or exchange rate collapses poorly. This is thus related to the previous criticism.

- It conducts purely a static analysis. Changes that ensue in time and through changes in portfolio composition are not considered.

8 The other VaR calculation methods are discussed subsequently. 9 Cf. Guthoff/Pfingsten/Wolf (1998), pp. 133 and 136. 10 Cf. Jorion (2000), pp. 220-221, and Brouwer/Densing (2000), pp. 5 and 10.

Chapter 2: The Value at Risk Concept

11

To remedy the non-consideration of non-linear relationships in the portfolio, the delta-gamma method provides an alternative approach at VaR calculation.

2.2.1.2 Delta-Gamma Method

The delta-gamma method is a parametric VaR approach that recognizes non-linear relationships in an instrument or portfolio by adding additional factors into the profit/loss equation that capture non-linear behavior. This means that we do not plainly assume constant, linear relationships between the value of the portfolio and its risk factors just as in the delta-normal method. Under the delta-gamma method, the non-linear relationships are first estimated and then inputted into the linear equation as an approximation of the non-linearities.

Non-linear relationships are for example present in portfolios containing options. The value of the portfolio is thereby dependent on the underlying value of the variable upon which the contained option is dependent. These non-linearities are captured by means of a Taylor expansion. Not just the delta or the sensitivity of the portfolio of the risk factor is required; the options gamma or its second order term is calculated.

Under the delta-normal method, we already have the sensitivity of the portfolio value with respect to the option as a linearly related term. This is for instance the first term of right side of Equation 11 . The delta-gamma method then applies the Taylor expansion as shown by the succeeding terms:

...dtt

)X(Vdq

q

)X(V

2

1dq

q

)X(V

dq

)X(dV 2

2

2

+∂

∂+∂

∂+∂

∂≈ , (11 )

which, in using ∆ for the sensitivity, Γ for the second order term and Θ for the time drift, is equal to:

...dtdq2

1dq

dq

)X(dV 2 +Θ+Γ+∆≈ . (12 )

To arrive at the VaR, the standard deviation is required, just as in the delta-normal method. This is:

)dq,dqcov(2

12dq

2

1dq 222

2222

Γ∆+σ

Γ+σ∆=σ . 11 (13 )

Thus, the VaR is:

11 Cf. Jorion (2000), pp. 211-213.

Chapter 2: The Value at Risk Concept

12

)dq,dqcov(2

12dq

2

1dq)(VaR 222

222

Γ∆+σ

Γ+σ∆α−=σα−= . (14 )

Whether this is an efficient way of accounting for non-linearities stands however in question. Moreover, criticisms made against the delta-normal method could be extended to the delta-gamma method.

2.2.22.2.22.2.22.2.2 Historical SimulationHistorical SimulationHistorical SimulationHistorical Simulation

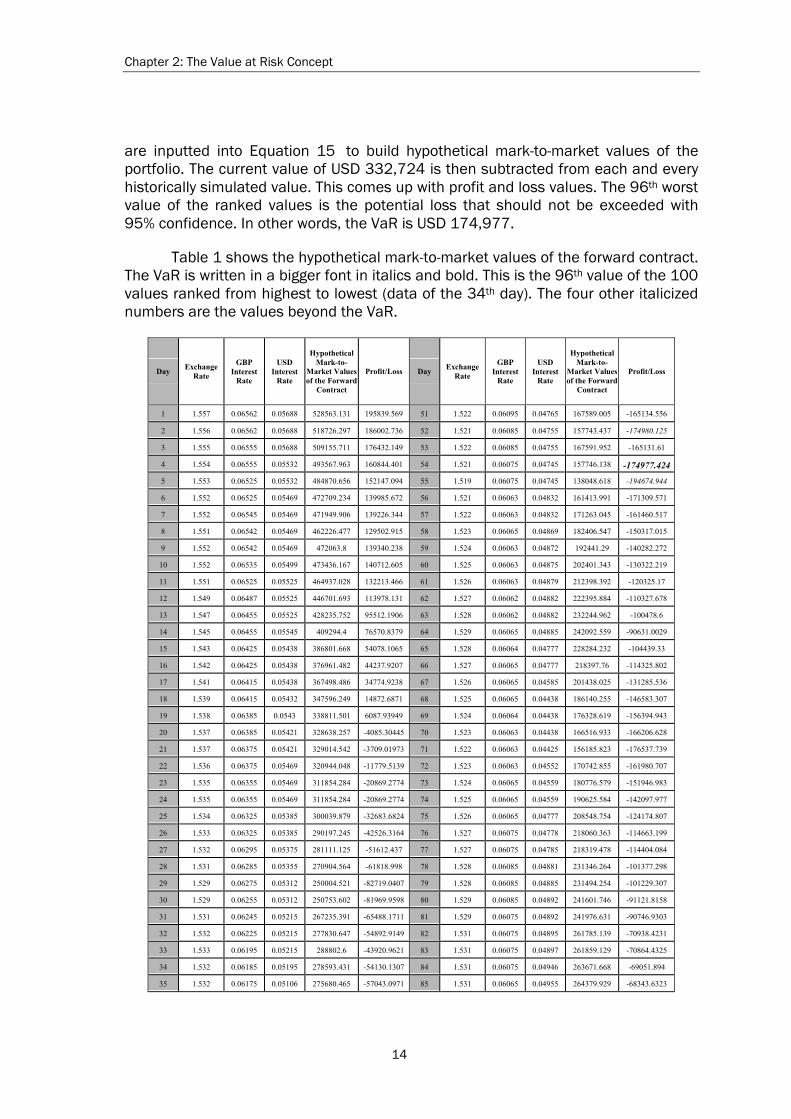

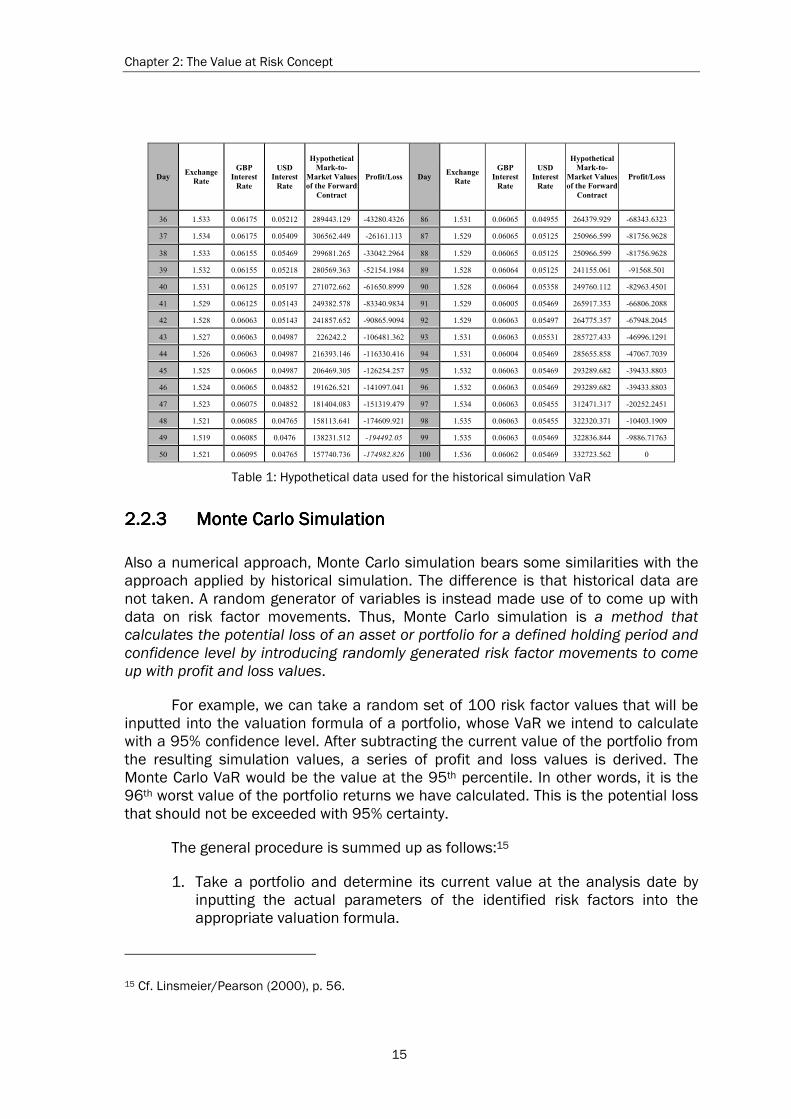

Historical simulation is a numerical approach at calculating the VaR of an asset or portfolio for a specified holding period and confidence level that takes past data on the movements of underlying risk factors to determine the probable returns. The whole calculation process arrives at a series of profit and loss figures. The value at the specified quantile is the absolute VaR.

If, for example, we want to calculate the VaR of a portfolio given a 95% confidence interval using a historical simulation of risk factor movements covering 100 days, then the historical simulation VaR would be the value of the 95th percentile of all the derived values. In other words, it is the 96th worst value of the portfolio returns we have calculated. To arrive at this, the risk factors are first of all inputted into the valuation formula of the portfolio to yield hypothetical mark-to-market values of the portfolio.12 This could include an exchange rate, an interest rate, etc. Meanwhile, the current value of the portfolio at the analysis date is also derived. This current value is then subtracted from each of the 100 historically simulated values. These are ranked from highest to lowest. The 96th worst value of the ranked values is the potential loss that should not be exceeded with 95% certainty.

The generalized procedure is as follows:13

1. Take a portfolio and determine its current value at the analysis date by inputting the actual parameters of the identified risk factors into the appropriate valuation formula.

2. Choose a confidence level and holding period for which the potential loss will be determined.

3. Take a set of historical risk factor values appropriate or significant for the holding period chosen. Input these historical values into the valuation formula

12 As these risk factor movements are actual data of the period in question, the process of incorporating them into the valuation function is called marking to market. 13 Cf. Linsmeier/Pearson (2000), p. 50.

Chapter 2: The Value at Risk Concept

13

of the portfolio. As a result, hypothetical mark-to-market values will be calculated.

4. Subtract the current value of the portfolio from the hypothetical mark-to-market values. This yields the profit and loss values of the portfolio.

5. Rank the profit and loss values. The value at the chosen confidence level is the VaR per historical simulation.

Historical simulation is relatively easy to implement and takes on a full valuation of all positions in its VaR computation, while using only one sample path. There is no modeling or approximation of some sort. But the calculation could quickly become complicated for large portfolios with complex structures. On the other hand, if the sample size is too small, then an estimation error could ensue. Another point against its credibility is the use of historical data to forecast future risk factor movements. It is assumed that historical risk factor movements would capture future risk factor movements, and thus, taking historical data is justifiable. There is an element of realism there, because historical trends could actually repeat. But taking a sample of values arbitrarily will also have its effects. The results depend heavily on the set of variables chosen. Moreover, an analyst is lucky if all values corresponding to the number of days chosen are all available.

Example. The following concrete example is an adjusted version of the case given by Linsmeier/Pearson (2000), who illustrate the VaR calculation of a single, three-month foreign exchange (FX) forward contract.14 The analysis date is May 20, 2000. The forward contract requires a payment of 15 million US dollars on August 19, 2000, which is 91 days hence. In exchange, the company will receive 10 million pounds. The valuation formula is:

( ) ( ))360/91(r1

M15USD

)360/91(r1

M10GBPFX)X(V

USDGBP

USDGBP +

−

+⋅= , (15 )

where USDGBPFX is the USD/GBP FX rate, rGBP the British pound interest rate and

rUSD the US dollar interest rate.

Given the interest and exchange rates prevailing on May 20, Equation 15 yields USD 182,663. To calculate the VaR using historical simulation, we will take a holding period of one day, e.g., the potential loss from May 20 to May 21, and a confidence level of 95%.

Historical data on the risk factor values will be taken from the most recent 100 business days. The risk factors include the three-month British pound interest rate, the three-month US dollar interest rate, and the spot USD/GBP FX rate. These

14 Cf. Linsmeier/Pearson (2000), p. 50-52.

Chapter 2: The Value at Risk Concept

14

are inputted into Equation 15 to build hypothetical mark-to-market values of the portfolio. The current value of USD 332,724 is then subtracted from each and every historically simulated value. This comes up with profit and loss values. The 96th worst value of the ranked values is the potential loss that should not be exceeded with 95% confidence. In other words, the VaR is USD 174,977.

Table 1 shows the hypothetical mark-to-market values of the forward contract. The VaR is written in a bigger font in italics and bold. This is the 96th value of the 100 values ranked from highest to lowest (data of the 34th day). The four other italicized numbers are the values beyond the VaR.

Day Exchange

Rate

GBP Interest

Rate

USD Interest

Rate

Hypothetical Mark-to-

Market Values of the Forward

Contract

Profit/Loss Day Exchange

Rate

GBP Interest

Rate

USD Interest

Rate

Hypothetical Mark-to-

Market Values of the Forward

Contract

Profit/Loss

1 1.557 0.06562 0.05688 528563.131 195839.569 51 1.522 0.06095 0.04765 167589.005 -165134.556

2 1.556 0.06562 0.05688 518726.297 186002.736 52 1.521 0.06085 0.04755 157743.437 -174980.125

3 1.555 0.06555 0.05688 509155.711 176432.149 53 1.522 0.06085 0.04755 167591.952 -165131.61

4 1.554 0.06555 0.05532 493567.963 160844.401 54 1.521 0.06075 0.04745 157746.138 -174977.424

5 1.553 0.06525 0.05532 484870.656 152147.094 55 1.519 0.06075 0.04745 138048.618 -194674.944

6 1.552 0.06525 0.05469 472709.234 139985.672 56 1.521 0.06063 0.04832 161413.991 -171309.571

7 1.552 0.06545 0.05469 471949.906 139226.344 57 1.522 0.06063 0.04832 171263.045 -161460.517

8 1.551 0.06542 0.05469 462226.477 129502.915 58 1.523 0.06065 0.04869 182406.547 -150317.015

9 1.552 0.06542 0.05469 472063.8 139340.238 59 1.524 0.06063 0.04872 192441.29 -140282.272

10 1.552 0.06535 0.05499 473436.167 140712.605 60 1.525 0.06063 0.04875 202401.343 -130322.219

11 1.551 0.06525 0.05525 464937.028 132213.466 61 1.526 0.06063 0.04879 212398.392 -120325.17

12 1.549 0.06487 0.05525 446701.693 113978.131 62 1.527 0.06062 0.04882 222395.884 -110327.678

13 1.547 0.06455 0.05525 428235.752 95512.1906 63 1.528 0.06062 0.04882 232244.962 -100478.6

14 1.545 0.06455 0.05545 409294.4 76570.8379 64 1.529 0.06065 0.04885 242092.559 -90631.0029

15 1.543 0.06425 0.05438 386801.668 54078.1065 65 1.528 0.06064 0.04777 228284.232 -104439.33

16 1.542 0.06425 0.05438 376961.482 44237.9207 66 1.527 0.06065 0.04777 218397.76 -114325.802

17 1.541 0.06415 0.05438 367498.486 34774.9238 67 1.526 0.06065 0.04585 201438.025 -131285.536

18 1.539 0.06415 0.05432 347596.249 14872.6871 68 1.525 0.06065 0.04438 186140.255 -146583.307

19 1.538 0.06385 0.0543 338811.501 6087.93949 69 1.524 0.06064 0.04438 176328.619 -156394.943

20 1.537 0.06385 0.05421 328638.257 -4085.30445 70 1.523 0.06063 0.04438 166516.933 -166206.628

21 1.537 0.06375 0.05421 329014.542 -3709.01973 71 1.522 0.06063 0.04425 156185.823 -176537.739

22 1.536 0.06375 0.05469 320944.048 -11779.5139 72 1.523 0.06063 0.04552 170742.855 -161980.707

23 1.535 0.06355 0.05469 311854.284 -20869.2774 73 1.524 0.06065 0.04559 180776.579 -151946.983

24 1.535 0.06355 0.05469 311854.284 -20869.2774 74 1.525 0.06065 0.04559 190625.584 -142097.977

25 1.534 0.06325 0.05385 300039.879 -32683.6824 75 1.526 0.06065 0.04777 208548.754 -124174.807

26 1.533 0.06325 0.05385 290197.245 -42526.3164 76 1.527 0.06075 0.04778 218060.363 -114663.199

27 1.532 0.06295 0.05375 281111.125 -51612.437 77 1.527 0.06075 0.04785 218319.478 -114404.084

28 1.531 0.06285 0.05355 270904.564 -61818.998 78 1.528 0.06085 0.04881 231346.264 -101377.298

29 1.529 0.06275 0.05312 250004.521 -82719.0407 79 1.528 0.06085 0.04885 231494.254 -101229.307

30 1.529 0.06255 0.05312 250753.602 -81969.9598 80 1.529 0.06085 0.04892 241601.746 -91121.8158

31 1.531 0.06245 0.05215 267235.391 -65488.1711 81 1.529 0.06075 0.04892 241976.631 -90746.9303

32 1.532 0.06225 0.05215 277830.647 -54892.9149 82 1.531 0.06075 0.04895 261785.139 -70938.4231

33 1.533 0.06195 0.05215 288802.6 -43920.9621 83 1.531 0.06075 0.04897 261859.129 -70864.4325

34 1.532 0.06185 0.05195 278593.431 -54130.1307 84 1.531 0.06075 0.04946 263671.668 -69051.894

35 1.532 0.06175 0.05106 275680.465 -57043.0971 85 1.531 0.06065 0.04955 264379.929 -68343.6323

Chapter 2: The Value at Risk Concept

15

Day Exchange

Rate

GBP Interest

Rate

USD Interest

Rate

Hypothetical Mark-to-

Market Values of the Forward

Contract

Profit/Loss Day Exchange

Rate

GBP Interest

Rate

USD Interest

Rate

Hypothetical Mark-to-

Market Values of the Forward

Contract

Profit/Loss

36 1.533 0.06175 0.05212 289443.129 -43280.4326 86 1.531 0.06065 0.04955 264379.929 -68343.6323

37 1.534 0.06175 0.05409 306562.449 -26161.113 87 1.529 0.06065 0.05125 250966.599 -81756.9628

38 1.533 0.06155 0.05469 299681.265 -33042.2964 88 1.529 0.06065 0.05125 250966.599 -81756.9628

39 1.532 0.06155 0.05218 280569.363 -52154.1984 89 1.528 0.06064 0.05125 241155.061 -91568.501

40 1.531 0.06125 0.05197 271072.662 -61650.8999 90 1.528 0.06064 0.05358 249760.112 -82963.4501

41 1.529 0.06125 0.05143 249382.578 -83340.9834 91 1.529 0.06005 0.05469 265917.353 -66806.2088

42 1.528 0.06063 0.05143 241857.652 -90865.9094 92 1.529 0.06063 0.05497 264775.357 -67948.2045

43 1.527 0.06063 0.04987 226242.2 -106481.362 93 1.531 0.06063 0.05531 285727.433 -46996.1291

44 1.526 0.06063 0.04987 216393.146 -116330.416 94 1.531 0.06004 0.05469 285655.858 -47067.7039

45 1.525 0.06065 0.04987 206469.305 -126254.257 95 1.532 0.06063 0.05469 293289.682 -39433.8803

46 1.524 0.06065 0.04852 191626.521 -141097.041 96 1.532 0.06063 0.05469 293289.682 -39433.8803

47 1.523 0.06075 0.04852 181404.083 -151319.479 97 1.534 0.06063 0.05455 312471.317 -20252.2451

48 1.521 0.06085 0.04765 158113.641 -174609.921 98 1.535 0.06063 0.05455 322320.371 -10403.1909

49 1.519 0.06085 0.0476 138231.512 -194492.05 99 1.535 0.06063 0.05469 322836.844 -9886.71763

50 1.521 0.06095 0.04765 157740.736 -174982.826 100 1.536 0.06062 0.05469 332723.562 0

Table 1: Hypothetical data used for the historical simulation VaR

2.2.32.2.32.2.32.2.3 Monte Carlo SimulationMonte Carlo SimulationMonte Carlo SimulationMonte Carlo Simulation

Also a numerical approach, Monte Carlo simulation bears some similarities with the approach applied by historical simulation. The difference is that historical data are not taken. A random generator of variables is instead made use of to come up with data on risk factor movements. Thus, Monte Carlo simulation is a method that calculates the potential loss of an asset or portfolio for a defined holding period and confidence level by introducing randomly generated risk factor movements to come up with profit and loss values.

For example, we can take a random set of 100 risk factor values that will be inputted into the valuation formula of a portfolio, whose VaR we intend to calculate with a 95% confidence level. After subtracting the current value of the portfolio from the resulting simulation values, a series of profit and loss values is derived. The Monte Carlo VaR would be the value at the 95th percentile. In other words, it is the 96th worst value of the portfolio returns we have calculated. This is the potential loss that should not be exceeded with 95% certainty.

The general procedure is summed up as follows:15

1. Take a portfolio and determine its current value at the analysis date by inputting the actual parameters of the identified risk factors into the appropriate valuation formula.

15 Cf. Linsmeier/Pearson (2000), p. 56.

Chapter 2: The Value at Risk Concept

16

2. Choose a confidence level and holding period for which the potential loss will be determined.

3. Run the random generator and value the portfolio using a number of parameters that is appropriate for the holding period chosen. As a result, hypothetical values of the portfolio will be yielded.

4. Subtract the current value of the portfolio from the simulated values. This yields the profit and loss values of the portfolio.

5. Rank the profit and loss values. The value at the chosen confidence level is the VaR per Monte Carlo simulation.

This is said to be the most powerful method to compute the VaR. If non-linear relationships are involved in the portfolio, the use of Monte Carlo simulation will better accomplish the VaR estimation. If the number of variables were large enough, the resulting values would capture the profit and loss distribution well. Unlike other VaR analyses that provide only a static consideration of value changes, Monte Carlo simulation allows for dynamic developments in the variables as well as the portfolio composition. Moreover, we do not have a general assumption on the process followed by risk factor movements. Ergo, it is a very open and comprehensive approach in measuring market risk, if the modeling were correct. The calculation is however tedious (but less tedious than non-VaR-based methodologies). Since it involves several variables, it requires resources, e.g., computer power, that could tackle this effortlessly.16

The tabulated results of a Monte Carlo simulation could appear similar to the example given in Section 2.2.2. The factors used are however derived from a model.

2.32.32.32.3 Criticisms on VaRCriticisms on VaRCriticisms on VaRCriticisms on VaR

2.3.12.3.12.3.12.3.1 General EvaluationGeneral EvaluationGeneral EvaluationGeneral Evaluation

We have seen the different methodologies that may be used to arrive at the VaR. The strengths and weaknesses of such methodologies were touched upon briefly in the respective subsections. Before we conduct a general evaluation of the VaR, let us take a look at Table 2, which is a summary of the features of the discussed VaR approaches.

16 Cf. Jorion (2000), pp. 225-226 and Brouwer/Densing (2000), pp. 4-5.

Chapter 2: The Value at Risk Concept

17

Parametric VaR Historical Simulation

Monte Carlo Simulation

Holding period and confidence level

Determined as required by the analysis; results are thereby affected by the choice

Determined as required by the analysis; results are thereby affected by the choice

Determined as required by the analysis; results are thereby affected by the choice

Risk factor movements

Normally distributed Based on historical values

Based on a random generation function

VaR calculation The value at the specified quantile of the profit and loss distribution; the difference between the mean and the chosen quantile value of the assumed normal distribution.

The value at the specified quantile of the profit and loss distribution; the difference between the current value and the chosen quantile value of the historical distribution of values

The value at the specified quantile of the profit and loss distribution; the difference between the current value and the chosen quantile value of the simulated distribution of values

Communicability Easy Easy Easy

Level of difficulty of calculation

Easy; complication arises when the number of assets increase

Easy; complication arises for complex structures

Easy; complication arises for complex structures

Infrastructure/data requirements

Surmountable Surmountable Requires powerful calculation systems

Table 2: Summary of the features of VaR

This summary points out that VaR is generally an easily communicable risk figure. However, depending on the methodology followed to derive the figure and the chosen holding period and confidence level, the number always changes. Several studies have shown this. Assumptions on how the risk factors move are for instance critical. Historical values appear realistic. On the other hand, Monte Carlo simulation could capture better non-linear behavior, which cannot be efficiently captured by parametric VaR.

Ideally, the results of the different methodologies that take up a huge sample data for the same confidence level and holding period should converge. Huge discrepancies between parametric VaR and Monte Carlo simulation could be attributed to the non-consideration of non-linearities. On the other hand, discrepancies between historical simulation and a Monte Carlo simulation that adopts normally distributed risk factor movements could indicate a disparity of the assumed movements in Monte Carlo from the historical path of the values, which may be deemed more realistic.17

17 Cf. Bonvin (2000), p. 8.

Chapter 2: The Value at Risk Concept

18

History however need not give the right answer. VaR is often criticized as driving by looking mainly at the rearview mirror. Even adopted future scenarios are based on already reviewed past events.18

What VaR method to use is a decision of the analyzer. When it does not cost much time and effort, the use of all methodologies, whose results could then be compared against each other as a form of check and balance, is ideal.

2.3.22.3.22.3.22.3.2 Summative Evaluation from a Computational PerspectiveSummative Evaluation from a Computational PerspectiveSummative Evaluation from a Computational PerspectiveSummative Evaluation from a Computational Perspective

How non-linear components of a portfolio are not efficiently captured by parametric VaR has been pointed out in the previous section. This also holds true for historical simulation. Inability to capture non-linear behavior is actually one of the most relevant critiques that could be raised against VaR. Monte Carlo simulation however attempts to accomplish this. This is stated in Table 3, which summarizes the features of VaR as against some factors or criteria that imply mathematical considerations.

Parametric VaR Historical Simulation Monte Carlo SimulationMonte Carlo SimulationMonte Carlo SimulationMonte Carlo Simulation

Non-linear components

May be attempted to be captured by the delta-gamma approach, albeit insufficiently

Not captured Can be captured

Fat tails Not incorporated Can be accounted for Can be accounted for

Extreme scenarios Not considered Not considered Can be considered

Variations in time A static analysis; no portfolio composition or other changes over time

A static analysis; no portfolio composition or other changes over time

Could perform a dynamic analysis; changes over time may be covered

Table 3: Problematic factors related to mathematical considerations

Inability to capture non-linear behavior results logically to estimation errors. Along with this, if the assumed risk factor movements are wrong, then estimation errors can also naturally ensue. In the case of historical simulation, it is crucial that the sample size be representative of the period in study. As for Monte Carlo simulation, the data should considerably be close to reality.

As regards actual facts, several studies have claimed that reality points to the existence of fat tails in the distribution. Simulation techniques have the possibility of taking this into consideration. This is however problematic for parametric VaR. The correctness of assuming a normal distribution becomes questionable. The VaR derived from a normal distribution underestimates then the true VaR. The higher

18 Cf. Frey (2000).

Chapter 2: The Value at Risk Concept

19

number of observations on the left tail of a fat-tailed distribution points to a higher VaR.

Since the normal distribution assumption is doubtful, what follows is the question on the advisability of using correlation as a dependence measure. Correlation measurement is normally undertaken in a world of joint multivariate normal distributions and not for other distributions, which depict other phenomena such as fat tails.

Moreover, only Monte Carlo simulation can possibly efficiently capture extreme scenarios. Again, this statement is rooted in the fact that parametric VaR assumes normality. On the other hand, historical simulation only considers past scenarios, which need not include circumstances that go to the extremes. For this reason, the development and use of extreme value theory has ensued.

Variations in time are also important. At particular points, volatility may for example heavily increase. Static parametric analysis and historical simulation are not hereby ideal. McNeil and Frey (1999) have conducted research in this area.19 They have pointed out that historical simulation cannot distinguish between periods of high and low volatility. On the other hand, the assumption of normality made by parametric VaR, although yielding estimates that reflect current volatility, does not seem to hold for normal data.20 In line with portfolio component changes in time, only Monte Carlo simulation could reflect such changes in the analyses.

All in all, it appears that in consideration of the computational perspective, the Monte Carlo VaR gains ground against the other VaR methodologies. It does not however always observe the axioms of coherency. This will be discussed by the succeeding chapter.

19 They focus on conditional return distributions (conditioned on current volatility) and the marginal distribution of the stochastic volatility process. 20 Cf. McNeil/Frey (1999), p. 3.

Chapter 3Chapter 3Chapter 3Chapter 3 Value at Risk and CoherencyValue at Risk and CoherencyValue at Risk and CoherencyValue at Risk and Coherency

3.13.13.13.1 CoherencyCoherencyCoherencyCoherency

In spite of its drawbacks, VaR is the most popular market risk measurement technique. But aside from market risk, attempts have been made to capture credit risk via VaR-based methodologies. CreditMetrics of J.P. Morgan attempts for example to generate a profit and loss distribution for loans, such that a quantile may be selected to determine the credit-at-risk. The challenge is to come up with a single VaR figure for portfolios subject to market, credit and other risks. Modern risk management now demands for the integration of various risk factors into one VaR figure. The aim of the so-called integrated risk management is however not simple to achieve. Assumptions have to be made as to the distribution that the factors follow, correlations have to be adjusted into the figures, and aggregation obstacles related to the fact that the estimates are expressed in different units or are taken for different periods in time have to be overcome.

Due to the inherent complexity of the considerations to be made, chances are high that at critical points in the analysis, one could take a wrong turn. Artzner, Delbaen, Eber and Heath (1997, 1998) have proposed axioms that should be fulfilled by risk measures in order for them to be coherent in the aggregation process. Their main argument is: the risk measures ρ(X) and ρ(Y) derived for a pair of investments X and Y, dependent or not, given a total return R, and positive numbers λ and N, should fulfill the following properties:

Translation invariance ρ(X+ N • R) = ρ(X) - N (16 )

Subadditivity ρ(X + Y) < ρ(X)+ ρ(Y) (17 )

Positive homogeneity ρ(λ • X) = λ • ρ(X) (18 )

Monotonicity ρ(X) ≥ ρ(Y), if X < Y (19 )

As outlined by the above-mentioned academicians, these axioms of coherency convey the following:

Chapter 3: Value at Risk and Coherency

21

3.1.13.1.13.1.13.1.1 Translation InvariancTranslation InvariancTranslation InvariancTranslation Invariance e e e [ρ [ρ [ρ [ρ((((X+ + + + N • • • • R) = ) = ) = ) = ρ(ρ(ρ(ρ(X) ) ) ) N]

By adding a risk-free amount to the initial position X and investing it in the instrument in use, the risk measure will simply decrease by N. This is also referred to as the risk-free condition.

What does it mean when translation invariance does not hold? An additional risk-free investment will appear to add risk to the already existing position. The new investment will have a factor in it that makes the existing X behave differently when combined with it. Problems may for example occur in some insurance premium calculations, e.g., proportional risk loading.21

3.1.23.1.23.1.23.1.2 Subadditivity [Subadditivity [Subadditivity [Subadditivity [ρρρρ((((X + Y) ) ) ) <<<< ρ(ρ(ρ(ρ(X) ) ) ) + ρρρρ((((Y)])])])]

When we put two instruments together to form a portfolio, the total risk of the two together should not be above the sum of the individual risks of the instruments. In other words, the risk of X and Y together should be equal or less than the sum of the risk of X alone and the risk of Y alone.

If this did not hold, there are possible ways of taking advantage of it. For instance, an investor in an exchange would rather set up two separate accounts for two instruments instead of putting them together. In this way, he avoids a higher margin requirement. On the other hand, a firm would break up its business into two in order to reduce its capital adequacy requirement. Regulatory authorities namely impose capital requirements on the basis of the firms market risk exposures.

But over and beyond regulatory concerns, subadditivity also has its relevance in risk management. If the risks of two desks have been calculated independently and if subadditivity holds, then one could just add the two individually derived risks together. This would then indicate the total risk. Subadditivity then allows for a decentralized calculation of the risks of various positions taken within the firm, which may then be simply aggregated.

3.1.33.1.33.1.33.1.3 Positive Homogeneity Positive Homogeneity Positive Homogeneity Positive Homogeneity [[[[ρρρρ((((λλλλ • • • • X) = ) = ) = ) = λλλλ • • • • ρρρρ((((X)])])])]

Whereas subadditivity implies lower risk figures for composite positions, this axiom states that the size of a position does not directly affect its risk. For all λ ≥ 0, risk is scalar multiplicative. The risk measure peculiar to X remains the same and will just have to be multiplied by λ as the size of the position increases.

21 This has been identified by Delbaen in correspondence.

Chapter 3: Value at Risk and Coherency

22

This confirms that there is no imposed restriction on any firm or investor to take the same position in whatever instrument. Each takes a position choice according to his capacity. Increased position in an instrument does not induce incremental risk. Liquidity is assumed.

What is the relevance of positive homogeneity? Similar to translation invariance, the derived risk measure should already capture the fundamental risk elements faced by an instrument. To arrive at its multiple, the figures will just have to be scaled. If size were a factor, then this will have its consequence on the speed of liquidation, among others. Such will then have to be factored in. It will be definitely unreasonable to impose this condition, if position size directly affects risk.22

3.1.43.1.43.1.43.1.4 Monotonicity [Monotonicity [Monotonicity [Monotonicity [ρρρρ((((X) ) ) ) ≥≥≥≥ ρρρρ((((Y), if ), if ), if ), if X <<<< Y]]]]

In analyzing positive homogeneity, we have been dealing with positions of the same reference instrument. Monotonicity compares two different instruments. If X < Y, it follows that ρ(X) ≥ ρ(Y). The risk faced by an instrument with lower returns is greater than that of another instrument with higher returns. If X = 10 and Y = 20, then the risk measure ρ(X) is greater than the risk measure ρ(Y).

What is the relevance of monotonicity? Monotonicity upholds the returns of an instrument as an ordering determinant of risk ranking between instruments. If this did not hold, we will not be able to rank instruments in terms of their risks. Comparability of risk measures meanwhile denotes the possibility of risk aggregation.

Note that this axiom rules out standard deviations and its multiples as risk measures.

Given all these axioms, we can then proceed to investigate the coherency of the different VaR approaches. Once they are adhered to, then the approach may be declared coherent.

3.23.23.23.2 The Coherency of VaRThe Coherency of VaRThe Coherency of VaRThe Coherency of VaR

VaR is not coherent at all times. Although some analyses involving selected instruments satisfy the axioms of coherency, others do not. The following section will conduct an analysis of the coherency of different VaR methodologies.

22 Cf. Gaese (1999), p. 56.

Chapter 3: Value at Risk and Coherency

23

3.2.13.2.13.2.13.2.1 The Coherency of Parametric VaR (DeltaThe Coherency of Parametric VaR (DeltaThe Coherency of Parametric VaR (DeltaThe Coherency of Parametric VaR (Delta----Normal)Normal)Normal)Normal)

3.2.1.1 Translation Invariance

Translation invariance holds for delta-normal VaR calculations. The underlying idea is that the standard deviation changes in accordance with any added risk-free amount. A smaller VaR results.

3.2.1.2 Subadditivity