the use of technology to automate the registration process ... · the use of technology to automate...

TRANSCRIPT

The use of technology to automate the registration

process within the Torrens system and its impact on

fraud: An analysis Rouhshi Low LLB, LLM, MIT

School of Law, Queensland University of Technology

Academic qualification for which this thesis is submitted: Doctor of Philosophy

Year submitted: 2008

I

Keywords Torrens system – fraud – internet – information technology – computer security –

Internet security – identity fraud - conveyancing – registration process – land

registration system - National Electronic Conveyancing System – NECS – digital

signatures – security of title – electronic registration system – public key

cryptography – public key infrastructure – digital certificates – indefeasibility of title

Abstract

Improvements in technology and the Internet have seen a rapid rise in the use of

technology in various sectors such as medicine, the courts and banking. The

conveyancing sector is also experiencing a similar revolution, with technology touted

as able to improve the effectiveness of the land registration process. In some

jurisdictions, such as New Zealand and Canada, the paper-based land registration

system has been replaced with one in which creation, preparation, and lodgement of

land title instruments are managed in a wholly electronic environment. In Australia,

proposals for an electronic registration system are under way. The research

question addressed by this thesis is what would be the impact on fraud of

automating the registration process. This is pertinent because of the adverse impact

of fraud on the underlying principles of the Torrens system, particularly security of

title. This thesis first charts the importance of security of title, examining how

security of title is achieved within the Torrens system and the effects that fraud has

on this. Case examples are used to analyse perpetration of fraud under the paper

registration system. Analysis of functional electronic registration systems in

comparison with the paper-based registration system is then undertaken to reveal

what changes might be made to conveyancing practices were an electronic

registration system implemented. Whether, and if so, how, these changes might

impact upon paper based frauds and whether they might open up new opportunities

for fraud in an electronic registration system forms the next step in the analysis. The

final step is to use these findings to propose measures that might be used to

minimise fraud opportunities in an electronic registration system, so that as far as

possible the Torrens system might be kept free from fraud, and the philosophical

objectives of the system, as initially envisaged by Sir Robert Torrens, might be met.

II

Table of Contents

CHAPTER 1: INTRODUCTION

1.1 Introduction

1.1.1 The research question

1.1.2 Research hypothesis

1.1.3 Impetus for this research

1.1.4 The Torrens system in the digital age

1.1.5 The effect of fraud on security of title

1.1.6 Need for research

1.1.7 The aim of this research and its significance

1.2 Methodology

1.3 Scope of this research and its limitations

1.4 Chapter outlines

1.5 Conclusion

CHAPTER 2: THE IMPORTANCE OF MINIMISING FRAUD IN THE TORRENS

SYSTEM OF LAND REGISTRATION

2.1 Introduction

2.2 The principles and objectives of the Torrens system

2.2.1 The importance of achieving security of title and facility of transfer in

a land registration system

2.2.1.1 Conceptualising security of title and facility of transfer in terms of

static and dynamic security

2.2.2 In what way was Torrens able to achieve these two concepts of

security of title and facility of transfers?

2.2.2.1 Achieving security of title

2.2.2.2 Achieving facility of transfer

2.3 Fraud within the Torrens system

2.4 The effect of fraud on security of title and facility of transfer

2.4.1 How does the Torrens system deal with the conflict between static

and dynamic security?

2.5 Why is it important that fraud be minimised so that security of title can

be maintained?

III

2.5.1 Current lack of analysis of the impact on fraud of automating the

registration process and of possible measures to minimise fraud

within an electronic environment

2.6 Conclusion

CHAPTER 3: OPPORTUNITIES FOR FRAUD IN THE TORRENS SYSTEM USING

A PAPER BASED REGISTRATION PROCESS

3.1 Introduction

3.2 Incidence of fraud within the paper registration system

3.3 Implications from the incidence of paper-based frauds

3.3.1 Trends in fraud perpetration

3.3.2 Issues arising out of fraud trends which require further analysis

3.3.2.1 How is it that fraud may be perpetrated despite the existence of

certain conveyancing practices that are said to act as safeguards

against fraud?

3.3.2.1.1 Witnessing requirements

3.3.2.1.2 Use of the paper certificate of title

3.3.2.1.3 Examination process of instruments lodged for registration

3.3.2.2 Why are the majority of perpetrators known to the victim of the fraud?

3.3.2.3 Why is fraud perpetrated in this manner?

3.3.2.4 Why are mortgages and transfers the most common transactions

targeted?

3.3.3 Summary of issues for further analysis

3.4 Analysis of case examples

3.4.1 Forgery

3.4.1.1 Individual as victim of the fraud

3.4.1.1.1 Conclusions drawn

3.4.1.2 Corporation as victim of the fraud

3.4.1.2.1 Conclusions drawn

3.4.1.3 Forged power of attorney

3.4.1.3.1 Conclusions drawn

3.4.2 Alteration of document after execution

3.4.2.1 Conclusions drawn

3.4.3 Fraud by misleading or fraudulently inducing the victim into signing

relevant documentation

3.4.3.1 Conclusions drawn

IV

3.4.4 Fraud by impersonation of the victim or identity fraud

3.4.4.1 Conclusions drawn

3.5 Synthesis of findings

3.5.1 How is fraud perpetrated in the paper registration system?

3.5.2 Is the manner of perpetration of the fraud linked to certain

conveyancing practices and processes?

3.5.3 How are fraudulent persons able to circumvent certain conveyancing

practices that are said to act as a safeguard against fraud?

3.5.4 What factors may facilitate the perpetration of the fraud?

3.5.5 Do perpetrators act alone or do they act in collusion with others?

3.5.6 Why are the majority of frauds perpetrated by persons known to the

victim?

3.5.7 Are some types of fraud more susceptible to being perpetrated by

persons known to the victim while some types of fraud more

susceptible to those unknown to the victim?

3.5.8 Are some perpetrators better placed to perpetrate fraud than others?

3.5.9 Why does fraud normally involve mortgages or a combination of

transfers and mortgages?

3.6 How will automating the registration process within the Torrens

system impact on these findings?

3.7 Conclusion

CHAPTER 4: WHAT CHANGES MAY BE MADE TO CONVEYANCING

PRACTICES IF TECHNOLOGY WAS USED TO AUTOMATE THE REGISTRATION

PROCESS WITHIN THE TORRENS SYSTEM?

4.1 Introduction

4.2 Jurisdictional overview of the move towards an electronic registration

system

4.2.1 Proposed systems

4.2.2 Fully operational systems

4.2.2.1 Partial systems

4.2.2.2 Fully automated systems

4.3 Comparative analysis

4.3.1 Access

4.3.1.1 Who has access

4.3.1.2 How is access controlled

V

4.3.1.3 What is the process for obtaining access

4.3.1.4 Generation & transmission of the authentication mechanism used to

control access

4.3.1.5 System features: common and differing features

4.3.1.6 What will these changes mean for fraud opportunities?

4.3.2 Preparation, lodgement, examination and registration of land title

instruments

4.3.2.1 Preparation and lodgement

4.3.2.2 Examination

4.3.2.3 Registration – updating the register

4.3.2.4 System features: common and differing features

4.3.2.5 What will these changes mean for fraud opportunities?

4.3.3 Execution and witnessing of land title instruments

4.3.3.1 Technology used to replace handwritten signatures

4.3.3.1.1 System features: common and differing features

4.3.3.1.2 What will these changes mean for fraud opportunities?

4.3.3.2 Classes of authorised users entitled to digitally sign land title

instruments

4.3.3.2.1 System features: Common and differing features

4.3.3.2.2 What will this mean for fraud opportunities?

4.3.3.3 Client signing the authorisation form

4.3.3.3.1 System features: Common and differing features

4.3.3.3.2 What will these changes mean for fraud opportunities

4.3.3 The paper certificate of title

4.3.3.1 Use of the paper certificate of title

4.3.3.2 Use of a client identification process and certifications as to identity

4.3.3.3 System features: Common and differing features

4.3.3.4 What will these changes mean for fraud opportunities?

4.4 Conclusion

CHAPTER 5: CAN THE TYPES OF FRAUD PERPETRATED IN THE PAPER

REGISTRATION SYSTEM CONTINUE TO BE PERPETRATED IN AN

ELECTRONIC REGISTRATION SYSTEM?

5.1 Introduction

5.2 Forgery

VI

5.2.1 Method of perpetrating fraud by forgery in the paper registration

system

5.2.2 Likely changes due to automating the Torrens registration process

5.2.3 Impact of these changes on fraud by forgery

5.2.3.1 Individual as the client

5.2.3.1.1 Can this fraud be perpetrated in an electronic registration system?

5.2.3.1.2 Under what circumstances might this fraud be perpetrated?

5.2.3.1.3 Who might be the likely perpetrators of this fraud?

5.2.3.1.4 How might witnessing requirements be circumvented?

5.2.3.1.5 What factors may facilitate the perpetration of this type of fraud?

5.2.3.1.6 What are the transactions likely to be targeted by fraudulent persons?

5.2.3.1.7 Conclusions

5.2.3.2 Company as the client

5.2.3.2.1 Can this fraud be perpetrated in an electronic registration system?

5.2.3.2.2 Under what circumstances might this fraud be perpetrated?

5.2.3.2.3 Who might be the likely perpetrators of this fraud?

5.2.3.2.4 How might witnessing requirements be circumvented?

5.2.3.2.5 What factors may facilitate the perpetration of this type of fraud?

5.2.3.2.6 What are the transactions likely to be targeted by fraudulent persons?

5.2.3.2.7 Conclusions

5.2.3.3 Attorney as the client using falsified power of attorney

5.2.3.3.1 Can this fraud be perpetrated in an electronic registration system?

5.2.3.3.2 Under what circumstances might this fraud be perpetrated?

5.2.3.3.3 Who might be the likely perpetrators of this fraud?

5.2.3.3.4 How might witnessing requirements be circumvented?

5.2.3.3.5 What factors may facilitate the perpetration of this type of fraud?

5.2.3.3.6 What are the transactions likely to be targeted by fraudulent persons?

5.2.3.3.7 Conclusions

5.3 Fraudulent misrepresentations

5.3.1 Method of perpetrating fraudulent misrepresentation in the paper

registration system

5.3.2 Likely changes due to automating the Torrens registration process

5.3.3 Impact of these changes on fraud by fraudulent misrepresentations

5.3.3.1 Can this fraud be perpetrated in an electronic registration system?

5.3.3.2 Under what circumstances might this fraud be perpetrated?

5.3.3.3 Who might be the likely perpetrators of this fraud?

5.3.3.4 How might witnessing requirements be circumvented?

VII

5.3.3.5 What factors may facilitate the perpetration of this type of fraud?

5.3.3.6 What are the transactions likely to be targeted by fraudulent persons?

5.3.3.7 Conclusions

5.4 Fraudulent alterations

5.4.1 Method of perpetrating fraudulent alterations in the paper registration

system

5.4.2 Likely changes due to automating the Torrens registration process

5.4.3 Impact of these changes on fraud by fraudulent alteration

5.4.3.1 Can this fraud be perpetrated in an electronic registration system?

5.4.3.2 Under what circumstances might this fraud be perpetrated?

5.4.3.3 Who might be the likely perpetrators of this fraud?

5.4.3.4 What factors may facilitate the perpetration of this type of fraud?

5.4.3.5 What are the transactions likely to be targeted by fraudulent persons?

5.4.3.6 Conclusions

5.5 Identity fraud

5.5.1 Method of perpetrating identity fraud in the paper registration system

5.5.2 Likely changes due to automating the Torrens registration process

5.5.3 Impact of these changes on identity fraud

5.5.3.1 Can this fraud be perpetrated in an electronic registration system?

5.5.3.1.1 Systems where certificates of title are not used

5.5.3.1.2 Systems using electronic certificates of title

5.5.3.2 Under what circumstances might this fraud be perpetrated?

5.5.3.3 Who might be the likely perpetrators of this fraud?

5.5.3.4 What factors may facilitate the perpetration of this type of fraud?

5.5.3.5 What are the transactions likely to be targeted by fraudulent persons?

5.5.3.6 Conclusions

5.6 Fraud by solicitors

5.6.1 Opportunities for solicitors to perpetrate fraud in the paper

registration system

5.6.2 Likely changes affecting fraud by solicitors after automating the

Torrens registration process

5.6.3 Impact of these changes on the opportunities for solicitors to

perpetrate fraud in an electronic registration system

5.7 Synthesis of findings: what is the impact of automating the Torrens

registration process on the paper based frauds identified in Chapter

3?

VIII

5.7.1 Can the frauds currently being perpetrated in the paper registration

system continue in an electronic registration system?

5.7.2 Would the manner of perpetration be altered due to changes in

conveyancing practices?

5.7.3 Where conveyancing practices might act as safeguards against

fraud, how could these be circumvented?

5.7.4 Who might be the likely perpetrators of these types of fraud in an

electronic registration system?

5.7.5 Are these perpetrators likely to act alone or in collusion with others?

5.7.6 In an electronic registration system, which frauds could be

perpetrated by those known to the victim and which by those

unknown?

5.7.7 For frauds persisting in an electronic registration system, will

opportunistic fraud by those known to the victim continue to be the

more prevalent?

5.7.8 Which factors might facilitate the perpetration of these frauds in an

electronic registration system?

5.7.9 Will solicitors continue to have an opportunity to perpetrate fraud in

an electronic registration system?

5.7.10 In an electronic registration system, is it likely that mortgages or a

combination of mortgages and transfers will continue to be targeted?

5.8 Conclusion

CHAPTER 6: WILL AN ELECTRONIC REGISTRATION SYSTEM INTRODUCE

NEW OPPORTUNITIES FOR PERPETRATING FRAUD?

6.1 Introduction

6.2 A new opportunity for fraud?

6.3 How may this type of fraud be perpetrated?

6.3.1 Those with no access and unable to digitally sign instruments

6.3.1.1 Obtaining access

6.3.1.1.1 Circumventing the identification or registration process

6.3.1.1.2 Circumventing the authentication process

6.3.1.2 Being able to digitally sign instruments

6.3.1.2.1 Systems using PKI to control access and to digitally sign documents

6.3.1.2.2 Systems not using PKI to control access but to digitally sign

documents

IX

6.3.2 Access but no ability to digitally sign instruments

6.3.3 Conclusions

6.4 Could there be safety mechanisms to act as a check against this type

of fraud?

6.5 Who might be the likely perpetrators of this type of fraud

6.6 What are the likely factors that may facilitate this type of fraud

6.7 Conclusion

CHAPTER 7: THE TYPES OF MEASURES THAT MAY BE USED IN AN

ELECTRONIC REGISTRATION SYSTEM TO MINIMISE FRAUD

7.1 Introduction

7.2 Drivers of fraud

7.3 Forgery

7.3.1 Individual as client

7.3.1.1 Processes for executing the authorisation form

7.3.1.2 Compliance with witnessing requirements

7.3.1.3 Ensuring that the witness’ signature was not forged

7.3.1.4 Effectiveness in preventing fraud

7.3.2 Company as client

7.3.2.1 Effectiveness in preventing fraud

7.3.3 Attorney as client under false power of attorney

7.3.3.1 Effectiveness in preventing fraud

7.4 Fraudulent alterations

7.4.1 Notification of alterations

7.4.2 Tracking changes

7.4.3 ‘Locking’ and examination of instruments lodged for registration

7.4.4 Restricting access privileges

7.4.5 Effectiveness of technological measures in minimising fraud

7.5 Misleading the signatory

7.6 Identity fraud

7.6.1 Documents used to verify identity

7.6.2 Whose identity is to be verified?

7.6.3 Who verifies identity and when should identity be verified

7.6.4 Steps taken to verify identity

7.6.5 Effectiveness in preventing identity fraud

7.6.5.1 Improving the issuing process of identity documents

X

7.6.5.2 Improving the accuracy of identity information held on databases

7.6.5.3 Improving the security of identity documents

7.7 Fraudulently accessing, preparing, digitally signing & lodging

instruments for registration

7.7.1 Measures to secure the digital certificate/PSP for digital signatures

7.7.1.1 Strengthening the registration process for obtaining digital

certificates/PSPs

7.7.1.2 Secure methods for generating digital certificates/PSPs

7.7.1.3 Secure storage and usage of digital certificates/PSPs

7.7.1.4 Secure selection and usage of passwords

7.7.2 Measures to strengthen the de-registration process

7.7.3 Safety mechanisms

7.7.3.1 Permanent client identification numbers

7.7.3.2 One-off client identification numbers

7.7.3.3 Notification mechanism

7.8 Preventing internal fraud

7.8.1 Entry controls

7.8.2 Regular monitoring of personnel

7.8.3 Audit trails

7.8.4 Education and training

7.8.5 Creating an anti-fraud culture

7.8.6 Fraud reporting and response

7.8.7 A fraud control policy

7.9 Summary

7.10 Conclusion

CHAPTER 8: CONCLUSION

8.1 The importance of this research

8.2 Research findings

8.3 Areas for further research

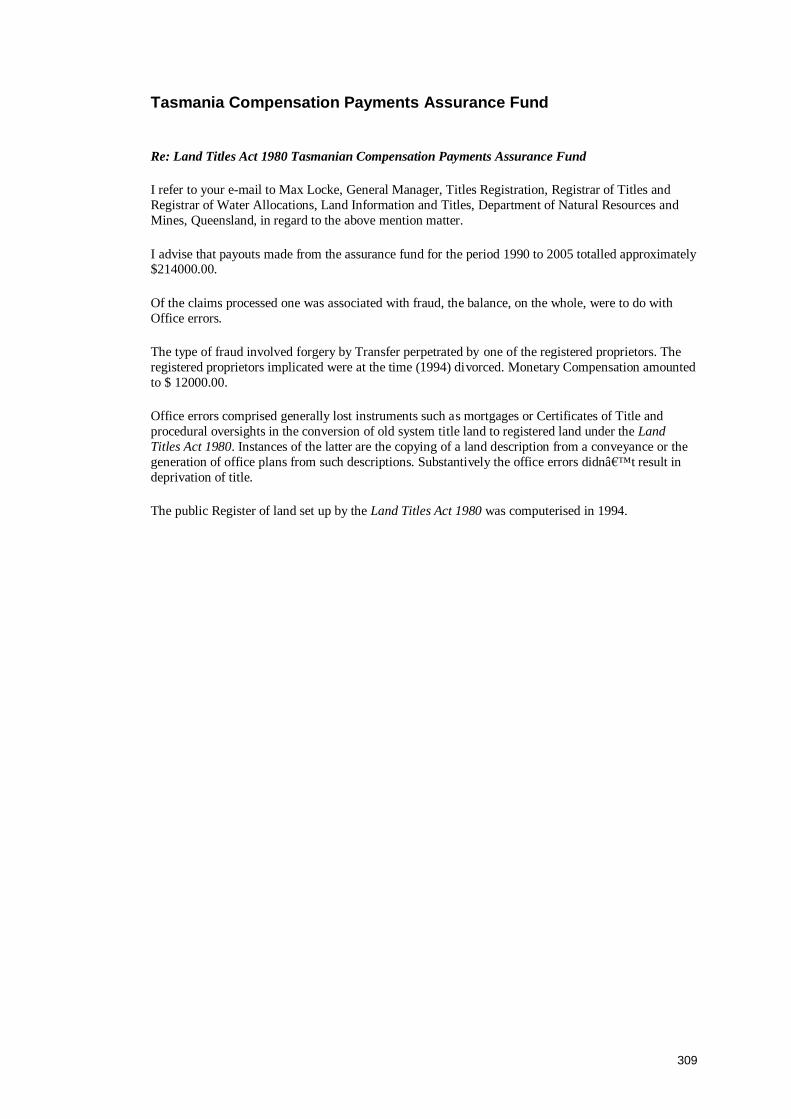

Appendix A: Compensation claims made against the States of Queensland, South

Australia and Tasmania for the period 1989 to 2005

Bibliography

XI

Statement of original authorship:

The work contained in this thesis has not been previously submitted for a degree or

diploma at any other higher education institution. To the best of my knowledge and

belief, the thesis contains no material previously published or written by another

person except where due reference is made.

Signed:

Date:

Acknowledgments

I would like to thank my supervisors, Sharon Christensen, Bill Duncan and Ernest

Foo, for their support and encouragement throughout my candidature. I am

extremely grateful to Max Locke, Registrar of Titles (Queensland), for his help in

providing me with the requested data as well as involving me in the National

Electronic Conveyancing State Project Team. I also owe gratitude to the following

people: the Registrar of Titles in Victoria, Tasmania and South Australia for

supplying me with data on fraud compensation claims; Steve Smith, Thomas Cutler

and Rod Thomas for patiently answering all my queries; Darcy Hammett for not only

answering my numerous questions but also reading through a first draft of this

thesis; Bill Dixon, for ongoing help and encouragement; Michael Weir, for his helpful

comments; Geoff Foster, for proof-reading and editing this thesis at short notice

(thank you Geoff!); Frances Hannah, life-coach extraordinaire; Mark Burdon, for help

in formatting this thesis and lending a supportive ear whenever it was needed and

Tzyy Shang Low, for providing sage brotherly advice when it was required.

Katherine Samuelowicz, who provided me with love and support throughout my

university life and beyond – I am extremely grateful for this - thank you. Christian

Bernat, I couldn’t have done this without you, thank you for being there, for your

support and for your understanding. And finally, I would like to thank my parents for

their unwavering love and support; without them I would not be where I am today.

1

CHAPTER 1

INTRODUCTION

Table of contents

1.1. Introduction.........................................................................................................2 1.1.1 The research question ..................................................................................2 1.1.2 Research hypothesis.....................................................................................2 1.1.3 Impetus for this research...............................................................................2 1.1.4 The Torrens system in the digital age............................................................3 1.1.5 The effect of fraud on security of title.............................................................5 1.1.6 Need for research .........................................................................................7 1.1.7 The aim of this research and its significance.................................................8

1.2. Methodology .......................................................................................................9 1.3. Scope of this research and its limitations ..........................................................11 1.4. Chapter outlines................................................................................................12 1.5. Conclusion........................................................................................................16

2

Chapter 1: Introduction

1.1. Introduction

1.1.1 The research question

The research question addressed by this thesis is twofold:

• will automating the registration process within the Torrens system of land

registration have an impact on opportunities for perpetrating fraud?

• can fraud minimisation strategies be used to counter this fraudulent conduct?

1.1.2 Research hypothesis

The hypothesis to be tested by this research is as follows:

Automating the registration process will not alter the opportunities for

perpetrating frauds that are possible in the paper registration system, with

the possible exception of reduced opportunities for fraudulent alterations.

Moreover, automating the registration system will introduce new

opportunities for perpetrating fraud.

1.1.3 Impetus for this research

The lack of detailed and comprehensive analysis of the impact on fraud of using

technology to automate the registration process within the Torrens system in

Australia, or of the types of measures that might be used to minimise these frauds,

is the impetus for this research. This study is vital, given the importance of the twin

objectives of the Torrens system: providing for security of title and facilitating title

transfers. As will be shown in Chapter 2, fraud has a negative impact on both of

these, particularly on security of title. So it is imperative that critical analysis be

undertaken to examine the impact on fraud of automating the registration process of

the Torrens system, as well as investigating the ways by which these opportunities

for fraudulent conduct may be reduced.

3

1.1.4 The Torrens system in the digital age

The Torrens system of land registration has been in operation in Australia since it

was first introduced into South Australia in 1858 by Sir Robert Torrens.1 As will be

seen in the next chapter, Torrens wanted to create a system that “would be simple,

inexpensive, and fast” and capable of “giving a secure and accurate title”.2 To

achieve this, a central register containing records of the parcels of land coming

within the system was established. This register became the focal point of the

system since it was the register that provided the source of title and it was the act of

registration that created the legal interest in the land. It was established that the

‘register of title is a mirror which reflects accurately and completely and beyond all

argument the current facts that are material to a man’s title,’3 so that the information

that is shown on the mirror is deemed to be complete and accurate.4 A title that is

so registered is deemed ‘free from all adverse burdens, rights and qualifications

unless they are mentioned on the register’.5 Further, as the register was intended to

be the sole source of information for purchasers, they would have no need to look

beyond what was stated on the register.6 Torrens also recognised that ‘through

human frailty’7 a flaw might appear on the mirror of title. In these circumstances,

compensation would be provided to the person suffering loss as a consequence of

this flaw. These underlying principles have formed the basis of the Torrens system

since its inception in 1858.

Recent years have seen rapid improvements in information technology and an

increased reliance on its use in various sectors, such as banking, medicine,

construction, and the courts system. Within the conveyancing sector, it was as early

as 1967 that Whalan recognised the importance of technology in the land

registration system, calling for the use of technology to improve the effectiveness of

the registration process8 and in 1981, Kirby J wrote that:

1 The current Torrens legislation in each State in Australia is: Transfer of Land Act 1958 (Vic), Real

Property Act 1900 (NSW), Land Title Act 1994 (Qld), Real Property Act 1886 (SA), Land Title Act 2000 (NT), Land Titles Act 1925 (ACT), Land Titles Act 1980 (Tas) and Transfer of Land Act 1893 (WA).

2 Robert White, 'The Elements of a Torrens Title' (1973) 11 Alberta Law Review 392, 396. See also James Edward Hogg, The Australian Torrens System (1905), 2: “The Australian system has been said to aim at combining security of title to land with facility in its transfer” and Warrington Taylor, 'Scotching Frazer v Walker' (1970) 44 Australian Law Journal 248, 250.

3 Theodore Ruoff, An Englishman Looks at the Torrens System (1957), 8. 4 Ibid, 16. 5 Ibid, 8. 6 Ibid, 11. 7 Ibid,17. 8 Douglas Whalan, 'Electronic Computer Technology and the Torrens System' (1967) 40 Australian

Law Journal 413.

4

the system of Torrens title…and the specially rapid computerisation of the records of

local and other land use authorities, makes the penetration of land title conveyancing

by computers inevitable. The controversy is one about timing.9

Since then, technology has been making increasing inroads into land registration

systems. The extent to which technology has been incorporated into these systems

differs from jurisdiction to jurisdiction. In some jurisdictions, such as New Zealand, a

fully automated land registration process has replaced the traditional paper

registration process. In contrast, other jurisdictions have only partially automated

their registration processes. In Australia, whilst an electronic register to record title10

is used in all States and Territories, none of them have introduced a fully automated

registration to replace the paper registration process. Currently, two electronic

systems have been proposed. One is the National Electronic Conveyancing System

(NECS)11 which is being developed by the National Steering Committee, a

committee made up of government and industry representatives12 of all the States

and Territories in Australia. Another is a system being developed by the Department

9 Michael Kirby, 'The computer, the Individual and the Law' (1981) 55 Australian Law Journal 443,

455. 10 Transfer of Land Act 1958 (Vic) s 27: ‘(2) Subject to the regulations, the Registrar a) may keep the

Register-(i) in any form or combination of forms; and(ii) on any medium or combination of mediums; and (iii) in any manner that he or she thinks fit; and (b) may at any time vary the medium, form or manner in which the Register or a part of the Register is kept’; Real Property Act 1900 (NSW) s 31B: ‘(3) The Register may be maintained in or upon any medium or combination of mediums capable of having information recorded in or upon it or them. (4) The Registrar-General may, from time to time, vary the manner or form in which the whole or any part of the Register is maintained’; Land Title Act 1994 (Qld) s 8: ‘(1) A register kept by the registrar may be kept in the form (whether or not in a documentary form) the registrar considers appropriate. (2) Without limiting subsection (1), the registrar may change the form in which a register or a part of a register is kept’; Real Property Act 1886 (SA) s51B: ‘Where the Registrar-General is required by this or any other Act or any other law to register title to land or record any other information relating to land, the Registrar-General may register the title or record the information by an electronic, electromagnetic, optical or photographic process and, in that case, the provisions of this Act …and any other relevant Act will be construed so as to apply to, and in relation to, the registration of title or recording of information by that process and in particular-- (a) the term "Register Book" will be taken to include the records maintained by the Registrar-General pursuant to this section relating to the land’; Land Title Act 2000 (NT) s 6: ‘(3) The land register may be kept in the form (whether or not in a documentary form) the Registrar-General considers appropriate. (4) The Registrar-General may change the form in which the land register or a part of the land register is kept’; Land Titles Act 1925 (ACT) s 43: ‘(2) The registrar-general may – (a) keep the register – (i) in such form or combination of forms; and (ii) on such medium or combination of media; and (iii) in such manner; as the registrar-general thinks fit…(3) A reference to a medium in subsection (2) includes but is not limited to – (a) a computer’; Land Titles Act 1980 (Tas) s 33: ‘(3) Subject to any regulation under this section the Register may be kept wholly or partly – (a) on paper, on microfilm, or in or on such other medium as may be approved by the Recorder; or (b) in such device for storing or processing information as may be approved by the Recorder’; and Transfer of Land Act 1893 (WA) s 48: ‘(2) The Register may be maintained in any medium for the storage and retrieval of information or combination of such media — (a) whether or not the kind of medium is the same as that in which the information was originally presented for registration or lodgment’.

11 The website for the national electronic conveyancing system is: http://www.necs.gov.au/, and see National Electronic Conveyancing System, How the National Electronic Conveyancing System (NECS) Will Work (2005) <http://www.necs.gov.au/How-NECS-will-work/default.aspx> at 18 April 2006.

12 All States and Territories are represented in the National Steering Committee.

5

of Sustainability and Environment in Victoria. Both are in the proposal stage,

although the Victorian system is more advanced in its progress than the NECS.

1.1.5 The effect of fraud on security of title

The concept of a secure title and its importance generally for a growing economy, as

well as its importance within the Torrens system, has been well documented.13

Within the Torrens system, the concept of security of title, usually referred to as

‘indefeasible title’, has been referred to as the ‘foundation of the Torrens system of

title’,14 the ‘keystone’15 of the Torrens system and ‘is central in the system of

registration’.16 Generally, the literature on the need for certainty and security in

property rights concludes that there is a strong correlation between clearly defined

and secure property rights and efficient market investments. It has been reasoned

that the greater an individual’s security in his/her title, the less will be that

individual’s uncertainty in using and trading in those rights, hence an overall

increase in confidence in trading in them.17 However, in order for individuals to be

able to trade in these rights, the purchasers must also be secure in their

acquisitions, hence the importance of providing an environment that facilitates

transfers of title. As noted by O’Connor,18 existing owners of property must be

13 For example Armen Alchian and Harold Demsetz, 'The Property Right Paradigm' (1973) 33(1)

Journal of Economic History 16, Harold Demsetz, 'Towards a Theory of Property Rights' (1967) 57 American Economic Review 347, David Palmer, 'Security, Risk and Registration' (1998) 15 Land Use Policy 83, Joyce Palomar, 'Land Tenure Security as a Market Stimulator in China' (2002) 12(1) Duke Journal of Comparative and International Law 7, Joyce Palomar, 'Contributions Legal Scholars Can Make to Development Economics: Examples from China' (2004) 45(3) William and Mary Law Review 1011, Hernando deSoto, The Mystery of Capital (2000), Johan Torstensson, 'Property Rights and Economic Growth - An Empirical Study' (1994) 47 Kyklos 231, Arthur Goldsmith, 'Democracy, Property Rights and Economic Growth' (1995) 32(2) Journal of Development Studies 157, Gershon Feder and Akihiko Nishio, 'The Benefits of Land Registration and Titling: Economic and Social Perspectives' (1999) 15 Land Use Policy 25, Joel M Ngugi, 'Re-Examining the Role of Private Property in Market Democracies: Problematic Ideological Issues Raised by Land Registration' (2004) 25 Michigan Journal of International Law 467, Pamela O'Connor, Security of Property Rights and Land Title Registration Systems (PhD Thesis, Monash University, 2003), Frank Byamugisha, The Effects of Land Registration on Financial Development and Economic Growth: A Theoretical and Conceptual Framework (1999) <http://www-wds.worldbank.org/servlet/WDS_IBank_Servlet?pcont=details&eid=000094946_99122006330167> at 16 January 2006.

14 Bahr v Nicolay (No 2) (1988) 164 CLR 604, 613. 15 Douglas Whalan, The Torrens System in Australia (1982), 19. 16 Frazer v Walker [1967] 1 AC 569, 580–581. 17 See Timothy Besley, 'Property Rights and Investment Incentives: Theory and Evidence From

Ghana' (1995) 103(5) Journal of Political Economy 903 and Robert Ellickson, 'Property in Land' (1993) 102 Yale Law Journal 1315, Thomas Miceli, CF Sirmans and Geoffrey Turnbull, 'Title Assurance and Incentives for Efficient Land Use' (1998) 6(3) European Journal of Law and Economics 305, 306. See also Joyce Palomar, 'Land Tenure Security as a Market Stimulator in China' (2002) 12(1) Duke Journal of Comparative and International Law 7, Joyce Palomar, 'Contributions Legal Scholars Can Make to Development Economics: Examples from China' (2004) 45(3) William and Mary Law Review 1011, David Palmer, 'Security, Risk and Registration' (1998) 15 Land Use Policy 83, Otomunde Johnson, 'Economic Analysis, the Legal framework and Land Tenure Systems' (1972) 15 Journal of Law and Economics 259, 259.

18 Pamela O'Connor, Security of Property Rights and Land Title Registration Systems (PhD Thesis, Monash University, 2003).

6

secure in their title (that they will not be deprived of their property), but

correspondingly purchasers must also be secure in their acquisition of property (that

they are acquiring a title free of prior claims). These two types of security

correspond with Torrens’ objectives of devising a system that would facilitate

transfers of land as well as providing owners with security of title. Demogue19 terms

the first type ‘static security’ and the second ‘dynamic security’.

An occurrence where there has been a fraudulent dealing with a registered

proprietor’s title to land, and where a bona fide purchaser for value obtains title to

the subject land without notice of the fraud, causes a conflict between the owner

who has been deprived of title and the bona fide purchaser. Where this conflict

occurs, it has been said that a land registration system can be designed to enforce

one of the two competing interests – the owner deprived of title or the bona fide

purchaser20 but that it cannot protect both.21 The Torrens system, through the

principle of immediate indefeasibility, provides a stronger protection for innocent

purchasers of title but at the expense of the original owner deprived of title. Hence,

the impact of fraud is that it derogates from an owner’s static security and erodes

from the owner the confidence that he/she is able to hold title securely.

Correspondingly, the owner’s confidence in the system as a whole would also be

reduced.

Thus it is argued that it is critical, whether using paper or an electronic registration

process, that the Torrens system operates in such a framework that the occurrence

of fraud can be minimised. However, this can only be achieved after a detailed and

comprehensive analysis of the fraud risks within the Torrens system, including the

ways that fraud occurs and what factors may facilitate it. By understanding the fraud

risks faced by stakeholders in the Torrens system, strategies to minimise each of

them may be devised, to ensure that the twin objectives of the system can be

achieved.

19 Rene Demogue, 'Security' in A Fouillee (ed), Modern French Legal Philosophy (1986). 20 Baird defines this as ‘the person who last acquired the land via a sequence of consensual

transfers’: Douglas Baird and Thomas Jackson, 'Information, Uncertainty and the Transfer of Property' (1984) 13 Journal of Legal Studies 299, 301.

21 Baird ibid at 300: ‘In a world where information is not perfect, we can protect a later owner’s interest fully, or we can protect the earlier owner’s interest fully. But we cannot do both’. See also Mary-Anne Hughson, Marcia Neave and Pamela O'Connor, 'Reflections on the Mirror of Title: Resolving the Conflict Between Purchasers and Prior Interest Holders' (1997) 21 Melbourne University Law Review 460, 461: ‘[t]here are two main ways of resolving such conflicts. One approach is to protect the holder of an interest by preventing the transferor from passing a title which he or she lacks…The alternative approach, typified by systems of registration of title, is to protect innocent purchasers of interests, regardless of whether or not the transferor has a good title’.

7

1.1.6 Need for research

I submit that, at present, there is a lack of detailed and comprehensive analysis in

Australia of the impact on fraud of automating the registration process within the

Torrens system, as well as a lack of analysis of the types of measures that may be

used to minimise fraud. Given the importance of fraud minimisation, undertaking

such an examination is imperative.

It is within this context that this research is being undertaken. Thus far in Australia,

only two studies have analysed the impact of automating the registration process

within the Torrens system on fraud and have examined possible measures that may

be used to minimise these fraud risks. One was undertaken by Clayton Utz on

behalf of the National Electronic Conveyancing System Steering Committee22 in

response to proposals to implement a National Electronic Conveyancing System

(NECS) in Australia. The purpose of the assessment was to identify and assess all

of the risks associated with implementation of the National Electronic Conveyancing

System and to develop a cost-effective and equitable means of liability management

for all parties exposed to significant adverse outcomes. The second is an article by

me23 which compared the opportunities for fraud under the present paper-based

Torrens system with the proposed NECS, and also examined possible measures

that might be adopted to minimise fraud within NECS.

Both the Clayton Utz risk assessment and my article are relevant to this research, to

the extent that they both examine the various fraud risks associated with the

proposed NECS. In particular, both of them compare the occurrence of fraud under

the paper-based Torrens system with NECS and look at measures to minimise fraud

within NECS.

However, the analysis in both the risk assessment and the article were based on the

NECS, which at that stage was still in proposal form. Furthermore, the strategies

examined by the risk assessment to minimise fraud were restricted to examining the

various control strategies as provided for in the NECS Operations Description and

the NECS Business Model rather than investigating general strategies that might be

used for fraud prevention. 22 See National Electronic Conveyancing Office, Risk Assessment of the National Electronic

Conveyancing System (2007) <http://www.necs.gov.au/default.aspx?FolderID=116> at 12 June 2007.

23 Rouhshi Low, 'Opportunities for Fraud in the Proposed Australian National Electronic Conveyancing System: Fact or Fiction?' (2006) 13(2) Murdoch University Electronic Journal of Law 225.

8

1.1.7 The aim of this research and its significance

This study is intended to fill this gap in the literature by providing critical analysis of

how the perpetration of fraud may be altered by automating the registration process.

This is achieved by comparing fraud opportunities available in the Torrens system

where the registration process is conducted in a paper-based environment with a

corresponding automated registration process. However, rather than basing analysis

solely on the proposed NECS, this research will refer to electronic land registration

systems that are in operation in other Torrens jurisdictions. In this way a

comparative analysis may be undertaken to determine whether and, if so, in what

ways, various features of an electronic registration system24 might affect the

perpetration of fraud. Starting from this analysis, the study will then examine

possible measures to minimise fraud within the electronic registration system. It will

also analyse the fraud minimisation strategies used in the paper registration system

and their effectiveness, and discuss whether these strategies will still be relevant in

an electronic registration system.

Hence, the aim of this research is twofold:

• to identify the impact of automating the registration process on fraud within

the Torrens system, in particular to find:

� whether the types of fraud being perpetrated in the Torrens system

where the registration process is conducted in a paper-based

environment can continue to be perpetrated when registration has

been automated; and

� whether an electronic registration system might introduce new

opportunities for fraudulent conduct;

• to identify measures that might be used to minimise fraud in the electronic

registration system.

The significance of this research is that its findings may be used to inform

stakeholders within the conveyancing sector of the various fraud risks that can arise

in an automated registration process, as well as alerting them to measures that may

minimise these risks, thus assisting to ensure that the twin objectives of the Torrens

system are met in an electronic environment.

24 The term electronic registration system denotes the Torrens system where the registration process

has been automated. The term paper registration system will be used to denote the Torrens system where the registration process has not been automated.

9

1.2. Methodology

The primary research method used in this study is a comparison of the Torrens

system in Australia using a paper registration process with the Torrens system using

an automated registration process, to determine the following:

• the types of fraud that are currently being perpetrated in the paper

registration system;

• whether these types of fraud might continue to be perpetrated in an

electronic registration system;

• whether an electronic registration system will introduce a medium for new

opportunities for fraudulent conduct; and

• what measures could be implemented in the electronic registration system to

minimise fraud in that system.

The following steps were undertaken to enable this comparison to occur:

First, in order to establish a baseline for the types of frauds that might occur in the

paper registration system, data was obtained from various Land Title Offices in

Australia relating to claims made against the State for loss as a consequence of

fraud. This data was obtained by making a personal request to the Registrars of the

Land Titles Offices in all the States and Territories in Australia. The Registrars of

Titles for Victoria, Queensland, South Australia and Tasmania responded by

providing me with data covering compensation claims made during the period 1989

to 2005. For the States of Western Australia and New South Wales, this study will

use the data obtained by Hammond25 in her study in 2000 that examined the impact

on fraud of abolishing the paper certificate of title.

This data was used to find common trends in the perpetration of fraud in the Torrens

system using a paper based registration process, including a profile of the most

common perpetrators of these types of fraud and the types of transactions usually

targeted by them.

Case examples were then used to augment these findings by facilitating an in-depth

and comprehensive analysis of:

• the methods by which these frauds are perpetrated; 25 See Celia Hammond, 'The Abolition of the Duplicate Certificate of Title and its Potential Effect on

Fraudulent Claims Over Torrens Land' (2000) 8 Australian Property Law Journal 115.

10

• the factors that facilitate the perpetration of the fraud;

• how certain practices that are meant to act as safeguards against fraud may

be circumvented by fraudulent persons;

• the reasons why certain perpetrators are more likely – or have a better

opportunity – to perpetrate fraud than others; and

• the reasons why certain transactions are targeted by these fraudulent

persons.

These case examples comprise reported Australian and International cases

involving loss of title due to fraud as well as compensation claims made against the

State of Queensland for loss caused by fraud. The reported cases were obtained

using library database search engines. Information about the compensation claims

made against the State of Queensland were provided to me by the Queensland

Registrar of Titles, Mr Max Locke, and reproduced in Appendix A of this research.

Due to the voluminous nature of these cases, it was not possible for this research to

examine in detail every case involving fraud. Instead, analysis is restricted to those

cases that best illustrate the characteristics of the types of fraud that may occur in

the paper registration system.

Second, salient features of those electronic land registration systems that are fully

operational, and those systems proposed in Australia, were examined to identify

changes that will be made to conveyancing practices and requirements of the paper

registration system if the paper registration system is replaced with an electronic

registration system. An internet-based search was conducted to determine which

Torrens jurisdictions are using an electronic registration system. From there, in-

depth information about the features of the system, including its operational

requirements, was obtained by various means. These include downloading

operational guides from the system’s websites and personally requesting additional

information from the system’s help desk.

Once these changes had been determined, their impact upon fraud opportunities

and the various strategies that might be used to minimise these opportunities could

then be analysed.

The findings from this analysis could then be used to answer the research question

posed by this thesis; they would also enable the hypothesis to be tested and

appropriate conclusions to be drawn.

11

1.3. Scope of this research and its limitations

This research is undertaken within the context of the Torrens system of land

registration as introduced by Sir Robert Torrens to South Australia in 1858. Although

there are jurisdictional differences in Torrens legislation across the various

Australian States and Territories, the underlying framework is essentially the same.

Accordingly, for the purposes of this research, any reference to the Torrens System

should be treated as a reference to the underlying framework introduced by Torrens,

having Australia-wide application.26

This study will analyse two different types of registration process: the registration

process conducted within a paper-based Torrens system, in which land title forms

are prepared on paper and physically lodged with the Land Titles Office; and the

registration process within an automated Torrens system, where land title

instruments are prepared and lodged in a wholly electronic environment.27

Within these distinct processes, the underlying principles of the Torrens system

remain the same, whether registration operates within a paper-based or electronic

environment.

The fraud that is the focus of this research is restricted to those cases where there

has been a fraudulent dealing with a registered proprietor’s title during the

conveyancing and registration process that has led to a claim for compensation as a

result of loss caused by the fraud. This research will not be examining every type of

fraud that may be involved in a land transaction, such as value fraud, where the

value of a property has been artificially inflated.

In proposing fraud minimisation measures for an electronic registration system, I am

not suggesting that implementing these measures will lead to the complete

prevention of fraud; I recognise that it may be impossible to eradicate it. My goal is

to identify measures that can operate to minimise its occurrence. Further, whilst the

measures suggested by this research will include technological measures, it is

recognised that, since technology is evolving at a rapid rate there may be various

types of technology that could be used to minimise fraud. Thus, identifying the

26 For the current Torrens legislation in each State in Australia, see footnote 1. 27 As noted above in footnote 24, for the purposes of this research, the term ‘electronic registration

system’ is used to describe the Torrens system using a fully automated registration process and the term ‘paper registration system’ to describe the Torrens system using a paper based registration process.

12

precise type of technology that may be used to prevent fraud in an electronic

registration system is beyond the scope of this study.

Finally, the scope of this research is restricted to analysing the effects on fraud of

automating the registration process within the Torrens system. This is not a

quantitative analysis to find whether there might be more or less fraud in an

electronic registration system. Rather, it is a comparative analysis between the

paper and electronic registration systems to determine whether there might be

differences between them in:

1. opportunities for fraud between these two systems;

2. the manner in which fraud may be perpetrated;

3. the types of factors that might facilitate fraud;

4. the types of transactions targeted by fraudulent persons; and

5. the types of perpetrator of fraud.

As noted earlier, data on compensation claims was available only from Victoria,

Queensland, South Australia and Tasmania for the period 1990 to 2005 and was

unavailable from Western Australia and New South Wales. For Western Australia

and New South Wales, the data analysed will rely on that obtained by Hammond in

her study conducted in 2000.28

1.4. Chapter outlines

Chapter 1 : This chapter has introduced the concepts and issues are examined in

this thesis; it has also set out the aims of this research, its scope, and the

methodology used to answer the research question.

Chapter 2 : This chapter will set the context within which this research is being

undertaken, demonstrating why fraud minimisation is such a vital concept for the

successful functioning of the Torrens system, in whatever environment. Chapter 2

will analyse sources that describe the underlying principles and objectives of the

Torrens system, as well as examining the importance of achieving these objectives,

in particular that of providing security of title. This chapter will also demonstrate the

importance of security of title, not only for the successful functioning of a land

registration system, including the Torrens system, but also for the economic

wellbeing of a modern economy. This chapter will then examine the concept of

28 See Celia Hammond, 'The Abolition of the Duplicate Certificate of Title and its Potential Effect on

Fraudulent Claims Over Torrens Land' (2000) 8 Australian Property Law Journal 115.

13

fraud, to determine the scope of fraud that will be the focus of this research. The

impact of fraud on the goals and principles of the Torrens System will then be

examined; it will be shown that fraud has the effect of eroding the confidence of

registered proprietors in their ability to hold title securely and that this can lead to a

reduction in their confidence in the Torrens system. It will argue that the success of

the Torrens system depends on its ability to instil confidence in its users in the

security of their title, and that this confidence is well placed, whether in a paper or

electronic environment. Hence it is postulated that the registration process of the

Torrens system in Australia should not be fully automated until the risks of fraud

emerging from such a transition have been carefully analysed and examined. This is

the chief aim of this research. Finally, in setting the context within which this

research is being undertaken, this chapter will also provide an overview of the

literature that has an impact on this research to demonstrate the gaps in it that this

study intends to fill.

Chapter 3 : This chapter will analyse the ways in which fraud is currently being

perpetrated in the paper registration system. To do this, it will use data obtained

from the various Land Titles Offices in Australia relating to compensation claims

made against the State for loss caused by fraud, elucidating common trends in the

perpetration of fraud in the Torrens system in Australia, including profiles of the most

common perpetrators of these types of fraud and the kinds of transaction usually

targeted by them. Given these findings, case examples will then be analysed in this

chapter for the purposes of examining:

• the methods by which these frauds are perpetrated, including whether the

perpetrator works alone or in collusion with others;

• the factors that facilitate the perpetration of the fraud;

• how certain practices that are said to act as safeguards against fraud might

be circumvented;

• the reasons why certain perpetrators, such as those who are known to the

victim of the fraud, are more likely than others to perpetrate fraud, or have a

better opportunity to do so;

• which types of fraud are more susceptible to being perpetrated by persons

known to the victim of the fraud and which types of fraud are more

susceptible to being perpetrated by persons unknown to the victim of the

fraud; and

14

• the reasons why certain transactions are targeted by these fraudulent

persons.

The conclusions drawn from this analysis will be used in Chapter 5 when comparing

whether the types of fraud occurring in the paper registration system may continue

to occur in an electronic registration system.

Chapter 4 : Chapter 4 will review what changes would be made to current

conveyancing practices and requirements where the registration process within the

Torrens system is automated. This will be achieved by examining the salient

features of electronic registration systems in which the registration process has

been fully automated and operational and of the electronic registration systems

proposed in Australia, so as to find what changes, if any, will be made to current

conveyancing practices and requirements that act as a safeguard against fraud. The

conclusions drawn from this analysis will be used in Chapters 5 and 6 to determine

how these changes in conveyancing practices and requirements might impact upon

the manner in which fraud may be perpetrated in an electronic registration system.

Chapter 5 : This chapter will use the analysis of Chapters 3 and 4 to find whether the

types of frauds that may be perpetrated in the paper registration system may

continue to be perpetrated in an electronic registration system. For those frauds that

are found likely to continue being perpetrated in an electronic registration system,

the following analysis will be undertaken:

• will the manner of perpetration of the fraud in the electronic registration

system be similar to that in the paper registration system?

• what factors might facilitate the perpetration of these frauds?

• who might be the likely perpetrators of these frauds?

• are these perpetrators likely to act alone or in collusion with others?

• which types of fraud may be more susceptible to being perpetrated by

persons known to the victim of the fraud and which to persons unknown to

the victim of the fraud?

• will the types of transactions targeted by fraudulent persons in the paper

system continue to be targeted in an electronic registration system?

• will solicitors continue to have the same opportunities for perpetrating fraud

as in the paper registration system or will these opportunities be reduced or

increased?

15

The findings from this analysis will then be compared to the findings obtained in

Chapter 3 and conclusions drawn.

Chapter 6: Chapter 6 will examine whether automating the registration process

within the Torrens system might introduce methods for fraudulent conduct that are

different from those in the paper system. For these new types of fraud, the following

analysis will be undertaken in this chapter and conclusions drawn:

• how will these frauds be perpetrated in the electronic registration system?

• what factors might facilitate the fraud?

• who are the likely perpetrators?

• are the perpetrators likely to act alone or in collusion with others; and

• whether these types of fraud would be more susceptible to being perpetrated

by persons known to the victim or by those unknown to the victim.

Chapter 7 : This chapter will examine the types of measures that could be adopted

to minimise the types of fraud identified in Chapters 5 and 6 that might occur in an

electronic registration system. Chapter 5 would have shown that some types of

fraud currently occurring in the paper system may continue to occur in the electronic

registration system.

For these frauds, an examination will be conducted in this chapter as to whether the

conveyancing practices used in the paper registration system as a safeguard

against fraud may continue to be relevant in an electronic registration system. This

examination will utilise the analysis, undertaken in Chapter 3, of the manner in which

these conveyancing practices could be circumvented by fraudulent persons. If these

conveyancing practices might continue to be relevant in an electronic registration

system, then this chapter will also consider whether these practices may be made to

function more effectively as safeguards against fraud, and if so, how.

In addition, where appropriate, other practices and measures that may be used to

minimise opportunities for fraudulent conduct will also be suggested, having regard

to the factors identified in Chapter 5 that act to facilitate the perpetration of these

frauds.

Chapter 6 would have shown that new opportunities for fraudulent conduct might

arise from implementation of an electronic registration system due to changes made

to conveyancing practices. For these new types of fraud, this chapter will utilise the

16

analysis from Chapter 6 of how these frauds might be perpetrated and the factors

that might act to facilitate them to establish the types of measures that may be

adopted to minimise these opportunities for fraudulent conduct. Finally, conclusions

will be drawn in this chapter as to the likely effectiveness of these measures against

fraud.

Chapter 8 is the concluding chapter. It will provide a synthesis of the conclusions

drawn in Chapters 3, 4, 5, 6 and 7, highlighting areas where automation of the

registration process will cause the most impact on opportunities for fraud. This

chapter will also suggest new areas of research arising from the findings of this

thesis.

1.5. Conclusion

Successful implementation of a fully automated registration process within the

Torrens system requires that the occurrence of fraud be minimised so that security

of title, a key pillar of the Torrens system, is maintained. Whilst there has been an

increasing level of encroachment of technology into the registration process in the

Torrens system, to date there has been no comprehensive academic research or

analysis undertaken on the impact of using technology to automate the registration

process on fraud, nor has there been any comprehensive research or analysis on

the type of measures that may be incorporated into a registration system using a

fully automated registration process to minimise fraud.

This research proposes to fill this gap in the literature and thus provide an original

contribution to knowledge by providing a comprehensive analysis on:

• the types of fraud that may occur in the paper registration system, the

manner in which these frauds are perpetrated, the factors that allow the

fraud to occur, the likely perpetrators of these types of fraud including

whether certain perpetrators have a better opportunity to perpetrate the fraud

than others and the transactions that are likely to be targeted by fraudulent

persons;

• whether these types of fraud occurring in the paper registration system may

continue to be perpetrated in an electronic registration system, and if so, by

whom, the type of factors that might facilitate these frauds and whether those

perpetrators who have a better opportunity to perpetrate fraud in the paper

registration system may continue to have similar opportunities in an

electronic registration system;

17

• whether an electronic registration system may introduce different

opportunities for fraud to occur and if so, the manner in which these frauds

may be perpetrated, the likely perpetrators of these frauds, the likely factors

that may facilitate the perpetration of these frauds; and

• what measures may be adopted to prevent these fraud from occurring in an

electronic registration system.

The end result is to identify the various fraud risks that may arise in an electronic

registration system and corresponding measures that may be used to minimise

these risks so that the Torrens system can operate in an environment that is

capable of minimising fraud.

18

CHAPTER 2

THE IMPORTANCE OF MINIMISING FRAUD IN THE TORRENS SYSTEM OF

LAND REGISTRATION Table of contents 2.1 Introduction........................................................................................................19 2.2 The principles and objectives of the Torrens System .........................................19

2.2.1 The importance of achieving security of title and facility of transfer in a land registration system...............................................................................................21

2.2.1.1 Conceptualising security of title and facility of transfer in terms of static and dynamic security .......................................................................................25

2.2.2 In what way was Torrens able to achieve these two concepts of security of title and facility of transfers?.................................................................................26

2.2.2.1 Achieving security of title ......................................................................29 2.2.2.2 Achieving facility of transfer..................................................................30

2.3 Fraud within the Torrens system........................................................................30 2.4 The effect of fraud on security of title and facility of transfer...............................34

2.4.1 How does the Torrens system deal with the conflict between static and dynamic security? ................................................................................................35

2.5 Why is it important that fraud be minimised so that security of title can be maintained?.............................................................................................................38

2.5.1 Current lack of analysis of the impact on fraud of automating the registration process and of possible measures to minimise fraud within an electronic environment .........................................................................................................39

2.6 Conclusion.........................................................................................................47

19

Chapter 2: The importance of minimising fraud in th e Torrens system of land registration

2.1 Introduction

Chapter 2 will show that minimisation of fraud is vital for the successful functioning

of the Torrens system, in either a paper or electronic environment, using established

literature on the Torrens system to examine its underlying principles and objectives.

This analysis will show that the two objectives of the Torrens system are to facilitate

transfers of title and to provide owners with a secure title. This concept of a secure

title, more commonly known as an indefeasible title, is the hallmark of the Torrens

system; security of title is vital to the proper functioning of a modern economy.

The scope of fraud that will be the focus of this research is fraud that causes a

deprivation of title. This type of fraud has the effect of causing a conflict between

the two objectives of the Torrens system, which through the principle of immediate

indefeasibility, favours facility of transfer over security of title. The effect of this, as

will be shown, is a derogation of an owner’s security of title, eroding the owner’s

confidence in the ability to hold title securely. Consequently it is postulated that the

owner’s confidence in the system as a whole will also be reduced. Given this

negative effect of fraud on security of title, it is therefore vital that the Torrens

system operate in a framework where fraud is minimised. However, to see how to

achieve this, the fraud risks within the Torrens system must first be analysed.

This chapter will demonstrate that at present, whilst there is a push towards

automating the registration process of the Torrens system in Australia, there is a

lack of detailed and comprehensive analysis of the effects of this on fraud. Neither

has there been any study on the types of measures that might be used to minimise

the occurrences of fraud within an electronic registration system. The aim of this

research, as noted in Chapter 1, is to fill this gap in the literature and to provide the

necessary analysis.

2.2 The principles and objectives of the Torrens Sy stem

The Torrens system, named after Sir Robert Torrens who conceived and introduced

the system into South Australia in 1858, has been adopted in all the States and

Territories in Australia, and in many other parts of the world such as New Zealand

and Canada. There is an abundance of literature on the Torrens system, its

20

underlying principles and its objectives.29 Torrens conceived the Torrens system to

rectify the problems he encountered as Registrar in administering the deeds system

in operation in South Australia. These included30:

• its complexity,

• its heavy costs, losses and perplexity for purchasers and mortgagees

because of the uncertainty relating to the validity of titles,

• the slowness of the conveyancing process, and

• diminution of the value of land as a secure and convenient basis of credit.

Torrens thought that all these defects of the deeds registration system stemmed

from the underlying principle of the deeds system, that no man could confer on a

purchaser or mortgagee a better title than he had.31 This characteristic of the deeds

system meant that every time a piece of land was dealt with, each step in the

devolution of title had to be examined to make sure (as far as it was possible to do

so) that it was valid and there were no outstanding equitable interests. Transfers of

title could not be completed until the historical search of title was concluded, with

each dealing requiring a fresh examination. The more complex the chain of title, the

longer it took to examine the chain and thus the more expensive it became. This

slowed down the transfer process.

Furthermore, as proof of title depended on evidence in the documents of title

themselves, difficulties arose where there was accidental loss, destruction, forgery

or alteration of these documents. An interest holder might lose everything despite

searching, if the title turned out to be defective in some way. For example, if one of

the deeds in the chain of title was forged the particular purchaser and subsequent

29 These include: P Moerlin Fox, 'The Story Behind the Torrens System' (1950) 23 Australian Law

Journal 489, Carmel MacDonald, Les McCrimmon and Anne Wallace, Real Property Law in Queensland (1998), Douglas Whalan, The Torrens System in Australia (1982), Theodore Ruoff, An Englishman Looks at the Torrens System (1957), Barry Goldner, 'The Torrens System of Title Registration: A New Proposal for Effective Implementation' (1982) 29 UCLA Law Review 661, John McCormack, 'Torrens and Recording: Land Title Assurance in the Computer Age' (1992) 18 William Mitchell Law Review 61, AG Lang, 'Computerised Land Title and Land Information' (1984) 10 Monash University Law Review 196, Lynden Griggs, 'Torrens Title in a Digital World' (2001) 8(3) Murdoch University Electronic Journal of Law , Robert Stein, 'The "Principles, Aims and Hopes" of Title by Registration' (1983) 9(2) Adelaide Law Review 267 & Robert Stein and Margaret Stone, Torrens Title (1991).

30 AG Lang, 'Computerised Land Title and Land Information' (1984) 10 Monash University Law Review 196, 197.

31 See for example Robert Stein, 'Sir Robert Richard Torrens, 1814-1884: Select Documents. Transcribed and With an Introduction by Robert Stein' (1984) 23(1) South Australiana 2, 20-28 which is an extract of a lecture given by Sir Robert Torrens at Kapunda on the South Australian Real Property Act. In that lecture, Sir Robert Torrens provides examples of the defects of the English deeds system.

21

proprietors acquired no interest in the property. This meant that the purchaser could

never be certain about the security of his/her title.

Torrens sought to rectify these problems encountered by the deeds system by

creating a land registration system that would be capable of giving both a secure

and accurate title as well as a system that would facilitate transfers of land.32

Before examining the manner in which Torrens sought to achieve the twin aims of

secure title and efficiency of transfers, an analysis as to the importance of achieving

these aims will first be undertaken, to demonstrate that the operation of these two

concepts is vital for fostering economic growth. This will be used to lay down the

foundation that forms the basis of this research – that it is vital that the Torrens

system should operate in an environment where both these concepts are capable of

being achieved, rather than one to the detriment of the other.

2.2.1 The importance of achieving security of title and facility of transfer in a

land registration system

Generally speaking, it has been said that the need for security33:

is one of the most important of the desiderata of social and legal life. The idea of

providing for the security of individuals is at the base of very important principles with

respect to the sources of law, whether public or private law.

Specifically, in terms of land, the strongest arguments for achieving certainty and

security in property rights are economic ones. It is well accepted that the more

certain and clearly defined are property rights, the more efficient are market

investments.34

32 See Robert White, 'The Elements of a Torrens Title' (1973) 11 Alberta Law Review 392, 396:

Torrens’ objective was to create a system that ‘would be simple, inexpensive, and fast, while at the same time giving a secure and accurate title’. See also James Edward Hogg, The Australian Torrens System (1905), 2: ‘The Australian system has been said to aim at combining security of title to land with facility in its transfer’; Warrington Taylor, 'Scotching Frazer v Walker' (1970) 44 Australian Law Journal 248, 250, and Robert Stein, 'The "Principles, Aims and Hopes" of Title by Registration' (1983) 9(2) Adelaide Law Review 267, 273. It should be noted that these two objectives are not mutually compatible. This will be discussed below.

33 Rene Demogue, 'Security' in A Fouillee (ed), Modern French Legal Philosophy (1986), 419. 34 See Timothy Besley, 'Property Rights and Investment Incentives: Theory and Evidence From

Ghana' (1995) 103(5) Journal of Political Economy 903 and Robert Ellickson, 'Property in Land' (1993) 102 Yale Law Journal 1315.

22

As explained by Miceli, Sirmans and Turnbull35:

Well-defined property rights in land decrease the risk of land expropriation, thereby

increasing the expected returns from investments in capital improvements and

stimulating such investments. In addition, well-defined property rights decrease the

risk to mortgage holders of losing their collateral to expropriation or competing

claims. This decreased collateral risk, the argument goes, lowers the mortgage risk

premium, thereby lowering marginal financing costs of capital improvements and

stimulating investment. Well–defined property rights also reduce the costs of

foreclosure, should such action become necessary. Lower foreclosure costs reduce

overall financing costs, thereby increasing the liquidity of land transactions. Finally,

well-defined property rights simply reduce transaction costs, thereby increasing the

likelihood that efficient transactions will be consummated.

These rights must also be capable of being held securely because without security,

‘people tend to devote their energies to protecting their claims to land. They tend not

to make the necessary investments of capital and labor for improving productivity

and meeting the needs of society’.36

It is also well accepted that there is a range of sources from which security in

property rights may be acquired, such as through the community or polity,37 and that

each source may provide different levels of security.38 Most experts39 agree that a

high degree of certainty and security in property rights is achievable through

formalising property ownership, land registration systems being the highest level of

35 Thomas Miceli, CF Sirmans and Geoffrey Turnbull, 'Title Assurance and Incentives for Efficient

Land Use' (1998) 6(3) European Journal of Law and Economics 305, 306. See also Joyce Palomar, 'Land Tenure Security as a Market Stimulator in China' (2002) 12(1) Duke Journal of Comparative and International Law 7 and David Palmer, 'Security, Risk and Registration' (1998) 15 Land Use Policy 83.