the use of linear programming for the allocation of scarce resources

DESCRIPTION

LEARNING NOTE 11.1. The use of linear programming for the allocation of scarce resources. LN11.1 (1a). Linear programming. LN11.1 (1b). Example (cont.). LN11.1 (2). Materials constraint (8Y + 4Z 3,440 (When Y= 0, Z = 860; when Z= 0, Y = 430. LN11.1 (3). - PowerPoint PPT PresentationTRANSCRIPT

Cost and Management Accounting: An Introduction, 7 th editionColin Drury

ISBN 978-1-40803-213-9 © 2011 Cengage Learning EMEA

The use of linear programming for the allocation of scarce resources

LEARNING NOTE 11.1

Cost and Management Accounting: An Introduction, 7 th editionColin Drury

ISBN 978-1-40803-213-9 © 2011 Cengage Learning EMEA

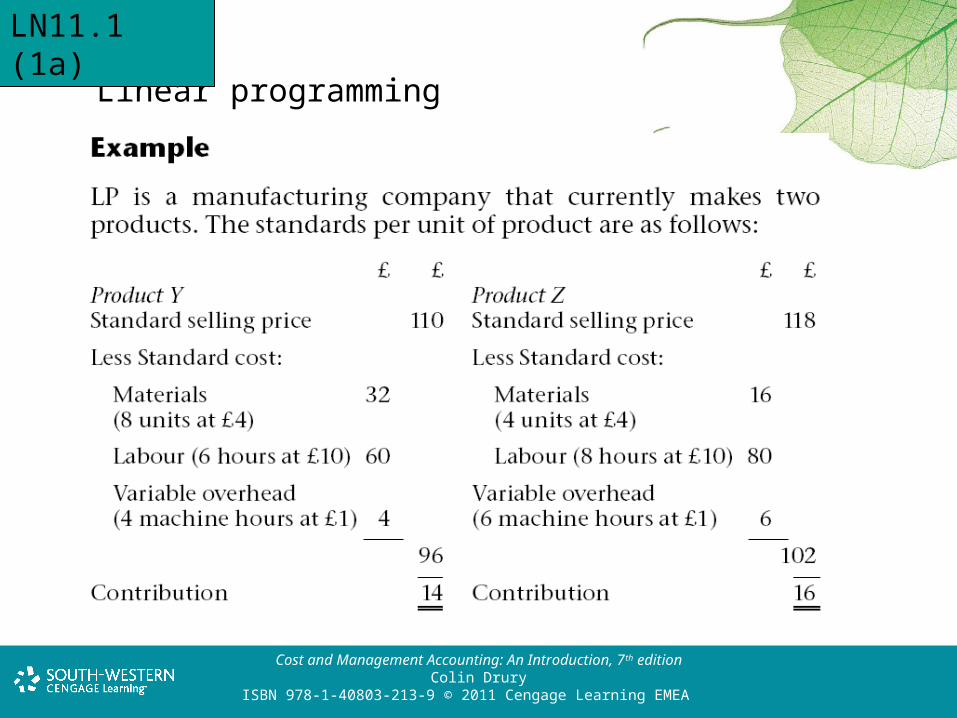

Linear programming

LN11.1 (1a)

Cost and Management Accounting: An Introduction, 7 th editionColin Drury

ISBN 978-1-40803-213-9 © 2011 Cengage Learning EMEA

Example (cont.)

LN11.1 (1b)

Cost and Management Accounting: An Introduction, 7 th editionColin Drury

ISBN 978-1-40803-213-9 © 2011 Cengage Learning EMEA

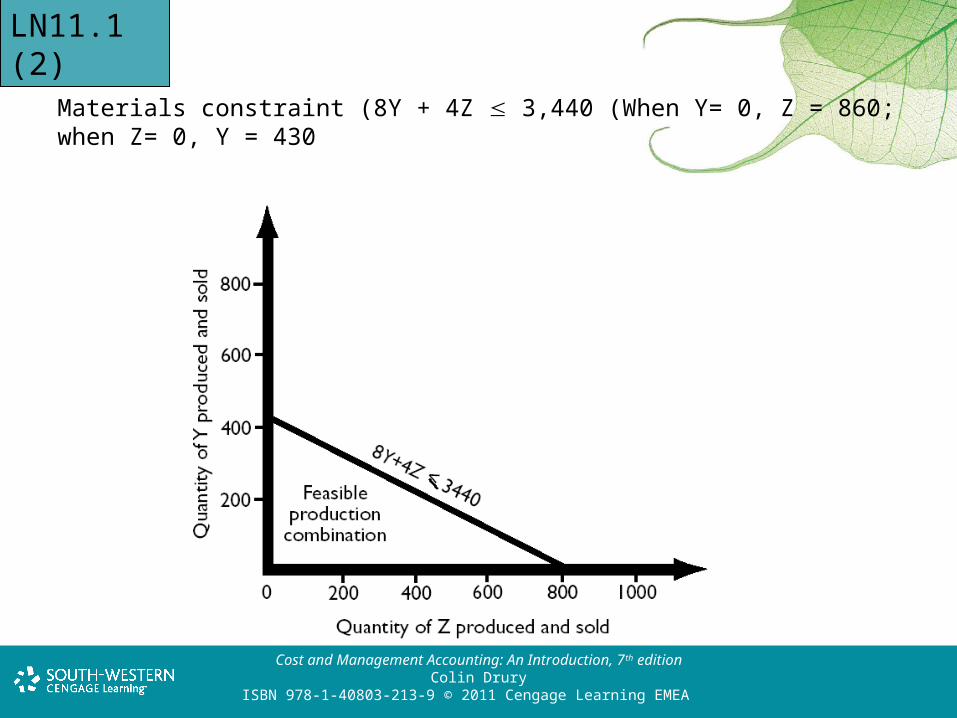

Materials constraint (8Y + 4Z 3,440 (When Y= 0, Z = 860;when Z= 0, Y = 430

LN11.1 (2)

Cost and Management Accounting: An Introduction, 7 th editionColin Drury

ISBN 978-1-40803-213-9 © 2011 Cengage Learning EMEA

Labour constraint 6Y + 8Z 2,880 (when Z = 0, Y = 480;when Y = 0, Z = 360)

LN11.1 (3)

Cost and Management Accounting: An Introduction, 7 th editionColin Drury

ISBN 978-1-40803-213-9 © 2011 Cengage Learning EMEA

Machine capacity constraint 4Y + 6Z 2,760 (when Z = 0, Y = 690; when y = 0, Z = 460)

LN11.1 (4)

Cost and Management Accounting: An Introduction, 7 th editionColin Drury

ISBN 978-1-40803-213-9 © 2011 Cengage Learning EMEA

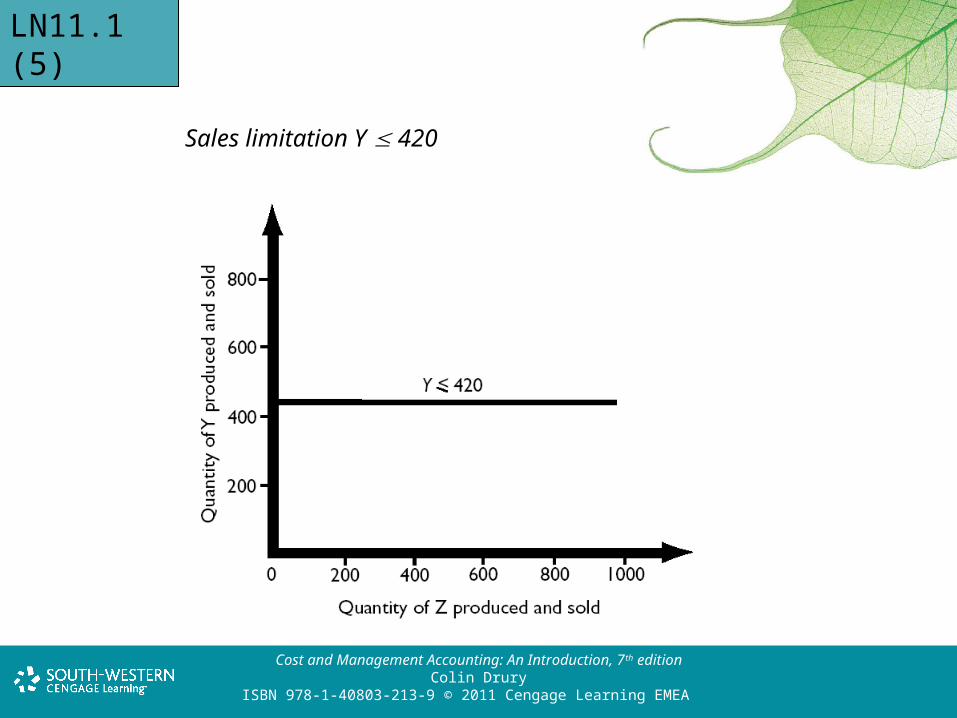

Sales limitation Y 420

LN11.1 (5)

Cost and Management Accounting: An Introduction, 7 th editionColin Drury

ISBN 978-1-40803-213-9 © 2011 Cengage Learning EMEA

Optimum solution

Feasible production combination = Area ABCDE

LN11.1 (6)

Cost and Management Accounting: An Introduction, 7 th editionColin Drury

ISBN 978-1-40803-213-9 © 2011 Cengage Learning EMEA

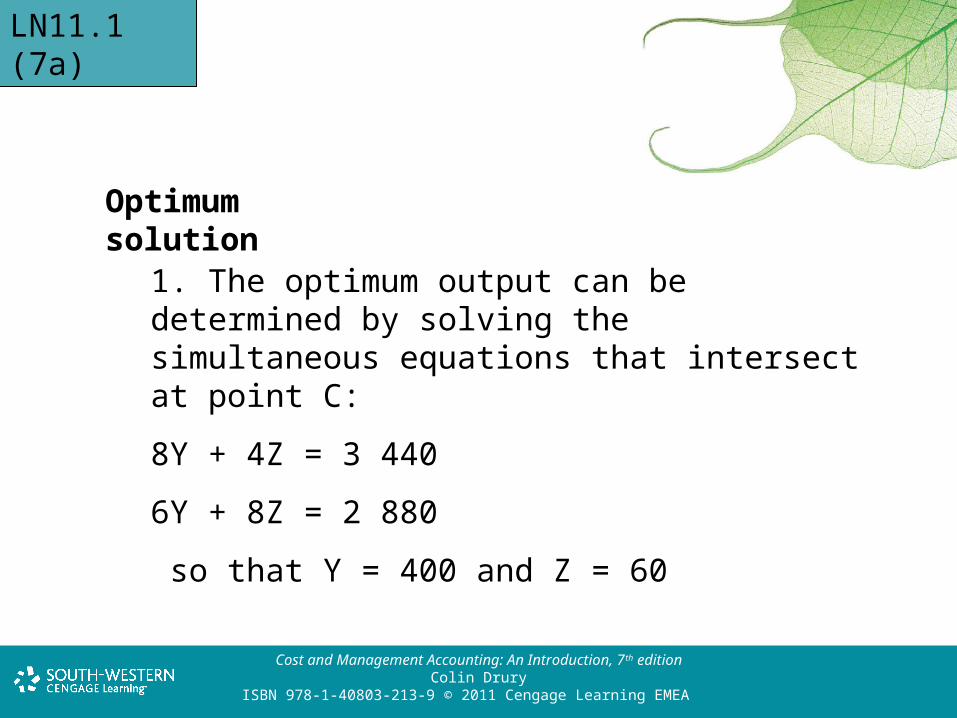

Optimum solution

1. The optimum output can be determined by solving the simultaneous equations that intersect at point C:

8Y + 4Z = 3 440

6Y + 8Z = 2 880

so that Y = 400 and Z = 60

LN11.1 (7a)

Cost and Management Accounting: An Introduction, 7 th editionColin Drury

ISBN 978-1-40803-213-9 © 2011 Cengage Learning EMEA

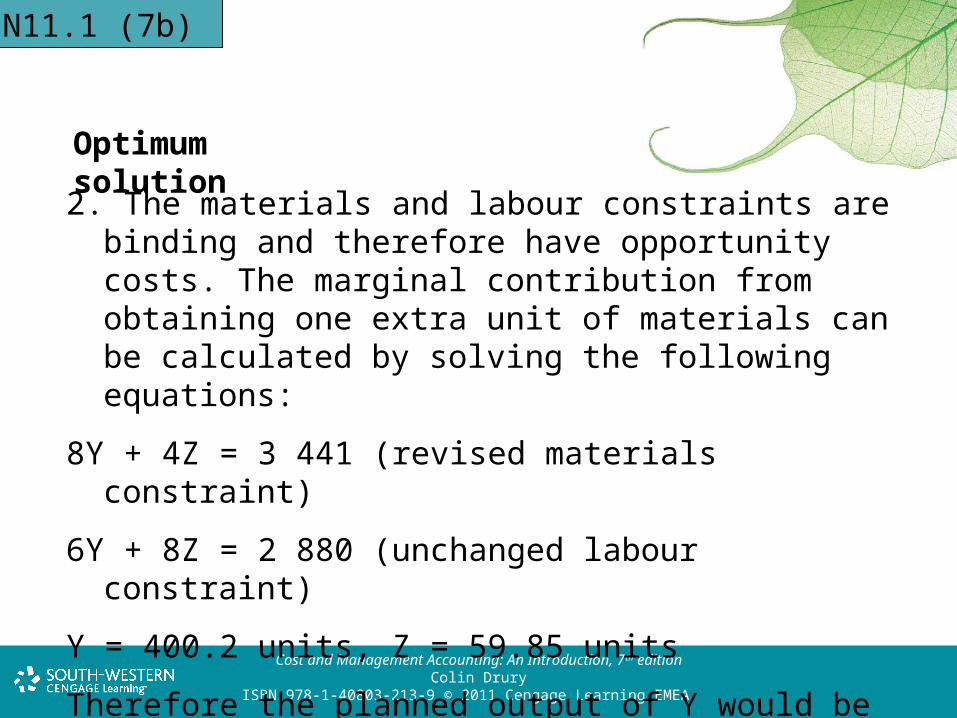

Optimum solution

2. The materials and labour constraints are binding and therefore have opportunity costs. The marginal contribution from obtaining one extra unit of materials can be calculated by solving the following equations:

8Y + 4Z = 3 441 (revised materials constraint)

6Y + 8Z = 2 880 (unchanged labour constraint)

Y = 400.2 units, Z = 59.85 units

Therefore the planned output of Y would be increased by 0.2 units and Z reduced by 0.15 units and contribution will increase by £0.40 (the opportunity cost).

LN11.1 (7b)

Cost and Management Accounting: An Introduction, 7 th editionColin Drury

ISBN 978-1-40803-213-9 © 2011 Cengage Learning EMEA

Optimum solution

3. The marginal contribution from obtaining one extra labour hour can be found in a similar way:

8Y + 4Z = 3 400 (unchanged materials constraint)

6Y + 8Z = 2 881 (revised labour constraint)

Y = 399.9 and Z = 60.2

Marginal contribution = £1.80

LN11.1 (7c)