the university of bristol pension and assurance scheme ... · pdf filepension and assurance...

TRANSCRIPT

The University of Bristol Pension and Assurance Scheme Trustees Annual Report and Financial Statements for the Year Ended 31 July 2014

Contents Administration of the scheme Trustees annual report Membership statistics Schedule of contributions Recovery plan Actuarial valuation Actuarial certifications Statement of investment principles Investment report Independent auditors’ report Summary of contributions Fund account Net assets statement Principal accounting policies Notes to the accounts

1 4 6 7 8 10 12 14 19 22 24 25 26 27 28

University of Bristol Pension and Assurance Scheme Year ended 31 July 2014

1

Administration of the scheme Trustees Jonathan Lord (Chairman) Pat French Professor Len Hall Tony Macdonald Andy Nield John O’Hara Jayne Oram Scheme Secretary Emma Butler Scheme Actuary Tim Panter Towers Watson Limited 3 Temple Quay, Temple Back East, Bristol BS1 6DZ Investment Advisor Kate Charsley Aon Hewitt Limited 40 Queen Square, Bristol BS1 4QP Investment Managers Insight Investment Management (Global) Ltd 160 Queen Victoria Street, London EC4V 4LA Legal & General Assurance (Pensions Management) Limited One Coleman Street, London EC2R 5AA Solicitors Osborne Clarke 2 Temple Back East, Bristol BS1 6EG Bankers RBS National Westminster Bank PLC 40 Queen’s Road, Bristol BS99 5AD Auditors Mazars LLP Clifton Down House, Bristol BS8 4AN Scheme number 0032 9823RF

University of Bristol Pension and Assurance Scheme Year ended 31 July 2014

2

Administration of the scheme (continued) Scheme administration The scheme administration is carried out by the Payroll and Pensions Team in the Finance Services Division of the University of Bristol. Any queries should be referred to: The Payroll and Pensions Manager, University of Bristol, Senate House, Tyndall Avenue, Bristol BS8 1TH, telephone 0117 928 7907. The Scheme The University of Bristol Pension and Assurance Scheme (UBPAS) was set up in 1969 to provide retirement and death benefits for eligible employees of the University. The operation of the scheme, which is a final salary scheme, is governed by a definitive trust deed dated 20th April 2012 (as amended). The Scheme is a registered scheme within the meaning of section 153 of the Finance Act 2004. All transfer values have been calculated and verified in the manner prescribed by the legislation and regulations under the Pension Act 1995. No allowance is made in transfer values for the possibility of discretionary benefits. Members of the Scheme are contracted out of the State Second Pension. Trustees The Trustees comprise four Trustees appointed by the principal employer, the University of Bristol, and three Trustees nominated by the members for a 6-year term. One of the University appointments is an independent Chairman, which is subject to approval by the Trustees. The Trustees usually meet quarterly but can meet at any other time to discuss urgent business. Statement of Trustees’ responsibilities Under the Pension Scheme trust deed and rules, the Trustees are required to prepare accounts for each scheme year. These accounts should show a true and fair view of the financial transactions of the scheme during the scheme year and of the disposition, at the end of the scheme year, of the assets and liabilities. Assets do not include insurance policies which are specifically allocated to the provision of benefits for, and which provide all the benefits payable under the scheme to, particular members; liabilities do not include liabilities to pay pensions and benefits after the end of the year. In preparing those accounts, the Trustees are required to:

Select suitable accounting policies and then apply them consistently;

Make judgements and estimates that are reasonable and prudent;

State whether the accounts have been prepared in accordance with guidelines set out in the Statement of Recommended Practice, Financial Reports of Pension Schemes, subject to any material departures disclosed in the accounts;

Prepare the accounts on a going concern basis unless it is inappropriate to presume that the scheme will continue in operation.

The Trustees are required to act in accordance with the trust deed and rules of the scheme, within the framework of pension and trust law. They are responsible for safeguarding the scheme’s assets and for taking reasonable steps for the prevention and detection of fraud and other irregularities.

University of Bristol Pension and Assurance Scheme Year ended 31 July 2014

3

Administration of the scheme (continued) Statement of Trustees’ responsibilities continued The financial statements have been prepared and audited in accordance with guidelines set out in the Statement of Recommended Practice (revised 2007) and regulations made under section 41 (1) and (6) of the Pensions Act 1995. Pension disputes procedures An agreed disputes procedure is in operation to resolve complaints by members, potential members and beneficiaries. Additional copies of the forms are available from the Payroll and Pensions team (Telephone 0117 928 7907), Senate House, Tyndall Avenue, Bristol BS8 1TH. Pensions ombudsman and occupational pensions advisory service The Government has appointed a Pensions Ombudsman to deal with complaints and disputes of fact or law in respect of pension schemes. The Ombudsman is completely independent and acts as an impartial adjudicator. Before writing to the Ombudsman however, it is better to seek help from The Pensions Advisory Service (TPAS), if there are difficulties which cannot be resolved with the Trustees. This independent voluntary organisation has expert local pension advisers who are able to help pension scheme members and beneficiaries. Both TPAS and Pensions Ombudsman can be contacted at: 11 Belgrave Road, London SW1V 1RB In addition, the Pensions Regulator is responsible for the Pension Scheme Registry which maintains a record of the addresses and other basic details of all pension plans in operation. The Pensions Regulator can be contacted at: Napier House, Trafalgar Place, Brighton BN1 4DW Pension payments Under the rules of the scheme, pensions in payment are increased in accordance with the Pensions (Increase) Act 1971. Increases awarded by the Pension Increase Orders are based on the consumer price index figure for the previous September. For September 2013, this published rate was 2.7%. Therefore, pensions in payment from April 2014 were increased by 2.7%. Deferred pensions are increased by the lesser of 5.0% per annum and the increase in the retail price index. There were no discretionary pension increases during the year. Transfers All transfer values paid were cash equivalents calculated and paid in the manner prescribed by the actuary. The calculation of transfer values includes an allowance for discretionary pension increases which may be awarded from time to time in addition to the guaranteed level of pension increases set out in the rules.

University of Bristol Pension and Assurance Scheme Year ended 31 July 2014

4

Trustees annual report to members Once again it has been a busy year for the Trustees. Apart from the management of the Scheme’s assets and liabilities, the key features of the year included:

Implementation of major changes to the employee benefit/contribution structure effective from 1 November 2013. Members are now offered a choice of 3 benefit/contribution level options.

Establishment of the Investment Sub Committee, with the objectives to: o Devise and recommend to the Trustee Board a suitable asset allocation policy and

investment strategy that maximises the ability of the Scheme to pay members’ benefits as they fall due;

o Implement and monitor the approved policy and strategy; and o Ensure that the Trustees are complying with their fiduciary duties in respect of

investment issues

Development of a new investment strategy including: o A progressive increase in the level of liabilities ‘matched’ by investments including

the use of liability driven investments (LDI) instruments o A ‘flightpath’ for the progressive reduction in the proportion of the scheme’s assets

held in growth assets o The appointment of a new manager (Insight) for the LDI and Absolute Return Bond

Fund investments. Trustees The Trustee board includes 3 member nominated members together with 4 employer nominated Trustees one of which is an independent Chair to the Trustees. The Investment Sub Committee includes the Independent Chair as well as the Scheme’s investment advisors. The Investment Sub Committee is tasked with making recommendations to the Trustee board on the Scheme’s investment strategy and the first formal meeting took place on 24 October 2013. Payments to Trustees No Trustees received any payment in respect of his/ her services as a Trustees except for Jonathan Lord, the Independent Trustee and Chairman. Full details are provided in note 11 to the accounts. Conflicts of interest The Trustees have developed a conflict of interest policy, whereby all trustees and advisers are required to declare any potential continuous conflicts of interest in addition to other conflicts arising from time to time. When Trustees do have a potential conflict of interest they withdraw from the Trustees decision making process on the relevant issue. The Trustees agreed that with the governance structure of the scheme and the changing financial landscape over the coming years, it is considered an advantage to have the Finance Director of the University on the Trustee Board. Any potential conflicts of interest of the Finance Director as one of the University nominated Trustees will be managed on a case by case basis. For example, Andy Nield will play no part as a Trustee during funding negotiations.

University of Bristol Pension and Assurance Scheme Year ended 31 July 2014

5

Trustees annual report to members (continued) Actuarial valuation of the Scheme as at 31 July 2012 The latest available actuarial valuation of the Scheme is as at 31 July 2012. The valuation report shows a shortfall of the technical provisions to £82.6m at that date. From the financial covenant review, in which the Trustees deemed the University’s covenant as tending to strong, the Trustees re-confirmed that a 20 year deficit recovery period to 2030 as agreed for 2008 valuation would still be appropriate. The Trustee agreed a programme of deficit recovery payments by the University of £1.9m in 2014/15 followed by £6.9m pa until 2030. Contributions paid in the year For the year ending 31 July 2014, the Scheme received £13.6m (2012/13: £13.6m) of contributions. This included an advance payment of additional deficit related contributions by the University of £6.9 million (2012/13: £6.9 million). A summary of these contributions is shown in Note 1 of the

accounts.

Changes to the scheme From 1 November 2013, active members have a choice of 3 levels of future benefit accrual/ contribution. The contribution rates are specified in the Scheme Rules and summarised below:

Option Pension Lump sum Member’s contribution

1 1/80th accrual 3/80th 17% 2 1/100th accrual 3/100th 11% 3 1/110th accrual 3/110th 9%

These rates do not include members' Additional Voluntary Contributions.

University of Bristol Pension and Assurance Scheme Year ended 31 July 2014

6

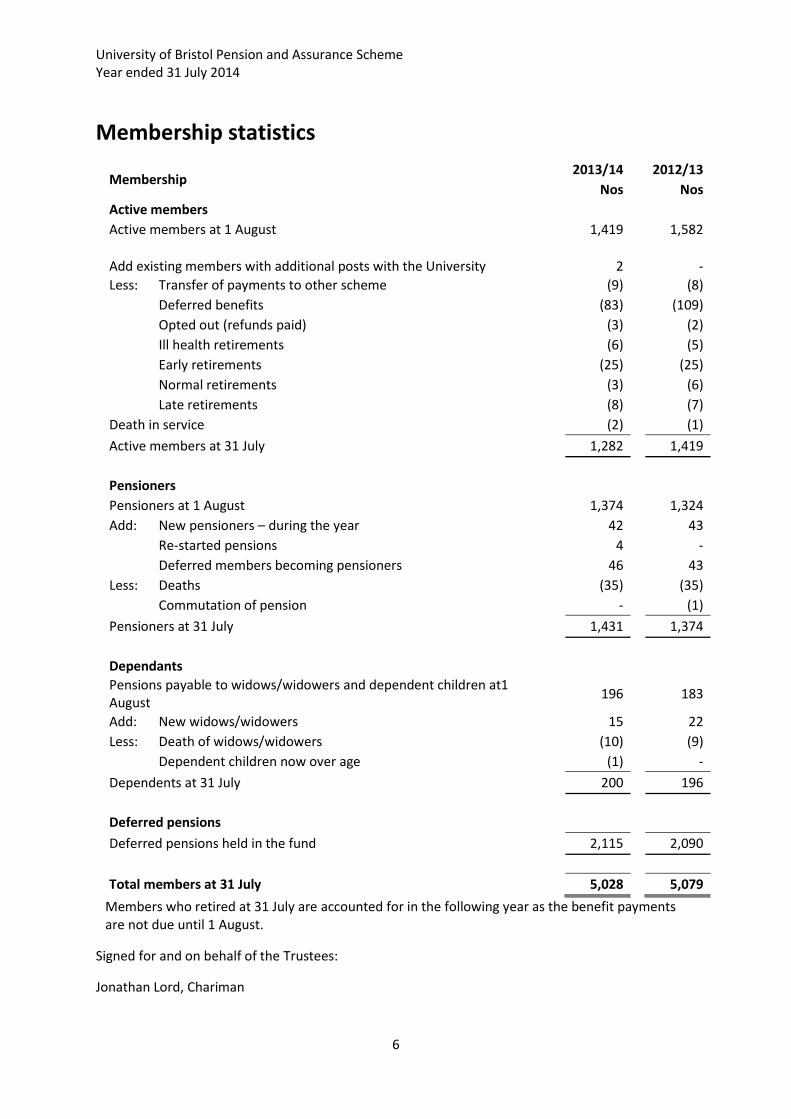

Membership statistics

Membership 2013/14 2012/13

Nos Nos

Active members

Active members at 1 August 1,419 1,582

Add existing members with additional posts with the University

2

-

Less: Transfer of payments to other scheme (9) (8)

Deferred benefits (83) (109)

Opted out (refunds paid) (3) (2)

Ill health retirements (6) (5)

Early retirements (25) (25)

Normal retirements (3) (6)

Late retirements (8) (7)

Death in service (2) (1)

Active members at 31 July 1,282 1,419

Pensioners

Pensioners at 1 August 1,374 1,324

Add: New pensioners – during the year 42 43

Re-started pensions 4 -

Deferred members becoming pensioners 46 43

Less: Deaths (35) (35)

Commutation of pension - (1)

Pensioners at 31 July 1,431 1,374

Dependants

Pensions payable to widows/widowers and dependent children at1 August

196

183

Add: New widows/widowers 15 22

Less: Death of widows/widowers (10) (9)

Dependent children now over age (1) -

Dependents at 31 July 200 196

Deferred pensions

Deferred pensions held in the fund 2,115 2,090

Total members at 31 July 5,028 5,079

Members who retired at 31 July are accounted for in the following year as the benefit payments are not due until 1 August.

Signed for and on behalf of the Trustees:

Jonathan Lord, Chariman

University of Bristol Pension and Assurance Scheme Year ended 31 July 2014

7

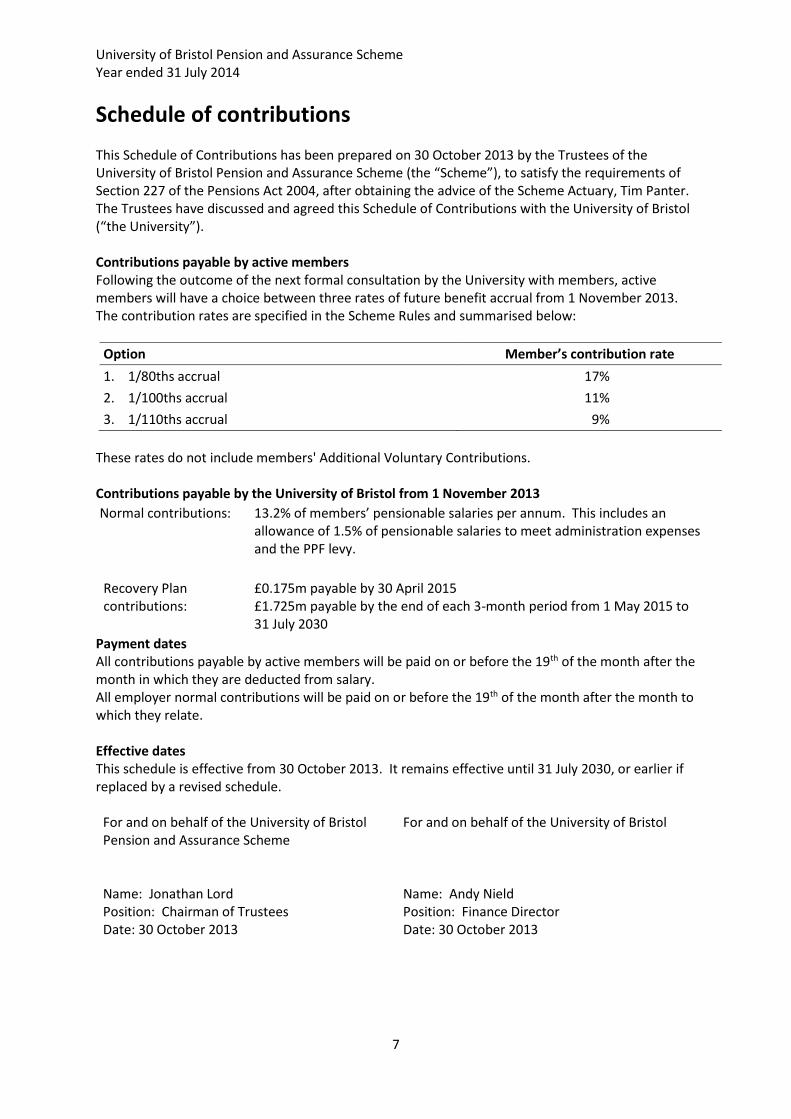

Schedule of contributions

This Schedule of Contributions has been prepared on 30 October 2013 by the Trustees of the University of Bristol Pension and Assurance Scheme (the “Scheme”), to satisfy the requirements of Section 227 of the Pensions Act 2004, after obtaining the advice of the Scheme Actuary, Tim Panter. The Trustees have discussed and agreed this Schedule of Contributions with the University of Bristol (“the University”). Contributions payable by active members Following the outcome of the next formal consultation by the University with members, active members will have a choice between three rates of future benefit accrual from 1 November 2013. The contribution rates are specified in the Scheme Rules and summarised below:

Option Member’s contribution rate

1. 1/80ths accrual 17%

2. 1/100ths accrual 11%

3. 1/110ths accrual 9%

These rates do not include members' Additional Voluntary Contributions. Contributions payable by the University of Bristol from 1 November 2013

Normal contributions: 13.2% of members’ pensionable salaries per annum. This includes an allowance of 1.5% of pensionable salaries to meet administration expenses and the PPF levy.

Recovery Plan contributions:

£0.175m payable by 30 April 2015 £1.725m payable by the end of each 3-month period from 1 May 2015 to 31 July 2030

Payment dates All contributions payable by active members will be paid on or before the 19th of the month after the month in which they are deducted from salary. All employer normal contributions will be paid on or before the 19th of the month after the month to which they relate. Effective dates This schedule is effective from 30 October 2013. It remains effective until 31 July 2030, or earlier if replaced by a revised schedule.

For and on behalf of the University of Bristol Pension and Assurance Scheme

For and on behalf of the University of Bristol

Name: Jonathan Lord Position: Chairman of Trustees

Name: Andy Nield Position: Finance Director

Date: 30 October 2013 Date: 30 October 2013

University of Bristol Pension and Assurance Scheme Year ended 31 July 2014

8

Recovery plan

The Recovery Plan has been prepared on 30 October 2013 by the Trustees of the University of Bristol Pension and Assurance Scheme (the “Scheme”), to satisfy the requirements of Section 226 of the Pensions Act 2004, after obtaining the advice of the Scheme Actuary, Tim Panter. The Trustees have discussed and agreed this Recovery Plan with the University of Bristol (“the University”). Results of the actuarial valuation at 31 July 2012 The actuarial valuation of the Scheme at 31 July 2012 revealed a funding shortfall (the Scheme’s Technical Provisions less the value of its assets) of £82.6 million. Steps to be taken to ensure that the statutory funding objective is met As at 31 July 2012, the University had made contributions that were £10m above those required under the previous Recovery Plan dated 19 May 2010. In July 2013 the University made a further contribution of £6.9m, and £5m had become due under the 2010 Recovery Plan, so total prepayments of University contributions amounted to £11.9m. Taking this into account, the Trustees and University have agreed (through this document) that the following additional contributions will be paid into the Scheme by the University to eliminate the remainder of the funding shortfall disclosed at 31 July 2012:

£0.175m payable by 30 April 2015

£1.725m payable by end of each 3-month period from 1 May 2015 to 31 July 2030. Period in which the statutory funding objective should be met The funding shortfall is expected to be eliminated by 31 July 2030, which is eighteen years from the valuation date of 31 July 2012. Half the total contributions in this Recovery Plan will be paid by 31 July 2022. Matters taken into account before preparing this Recovery Plan In preparing this Recovery Plan the Trustees have taken into account the following matters.

the Statement of Funding Principles dated 30 October 2013;

the actuarial valuation at 31 July 2012 and the information it provides on the asset and liability structure, the risk profile of the Scheme, the profile of the membership and the effect of the assumptions not being borne out by experience; and

its assessment of the financial strength of the University and its ability to pay future contributions.

University of Bristol Pension and Assurance Scheme Year ended 31 July 2014

9

Recovery plan (continued)

Assumptions underlying the elimination of the shortfall The major financial assumptions used in the calculation of the Scheme’s Technical Provisions of 31 July 2012 are shown in the table below. The full details of the assumptions are included in the Statement of Funding Principles dated 30 October 2013.

Assumption % per annum

Pre-retirement discount rate 5.4 Post-retirement discount rate 3.4 Rate of salary increases 3.6 Rate of increase of RPI 2.9 Rate of increase of CPI 2.3

The Recovery Plan allows for asset outperformance of 0.35% above the discount rates used to calculate the Technical Provisions as at 31 July 2012. For and on behalf of the Trustees For and on behalf of the University of Bristol Name: Jonathan Lord Name: Andy Nield Position: Chairman of Trustees Position: Finance Director Date: 30 October 2013 Date: 30 October 2013

University of Bristol Pension and Assurance Scheme Year ended 31 July 2014

10

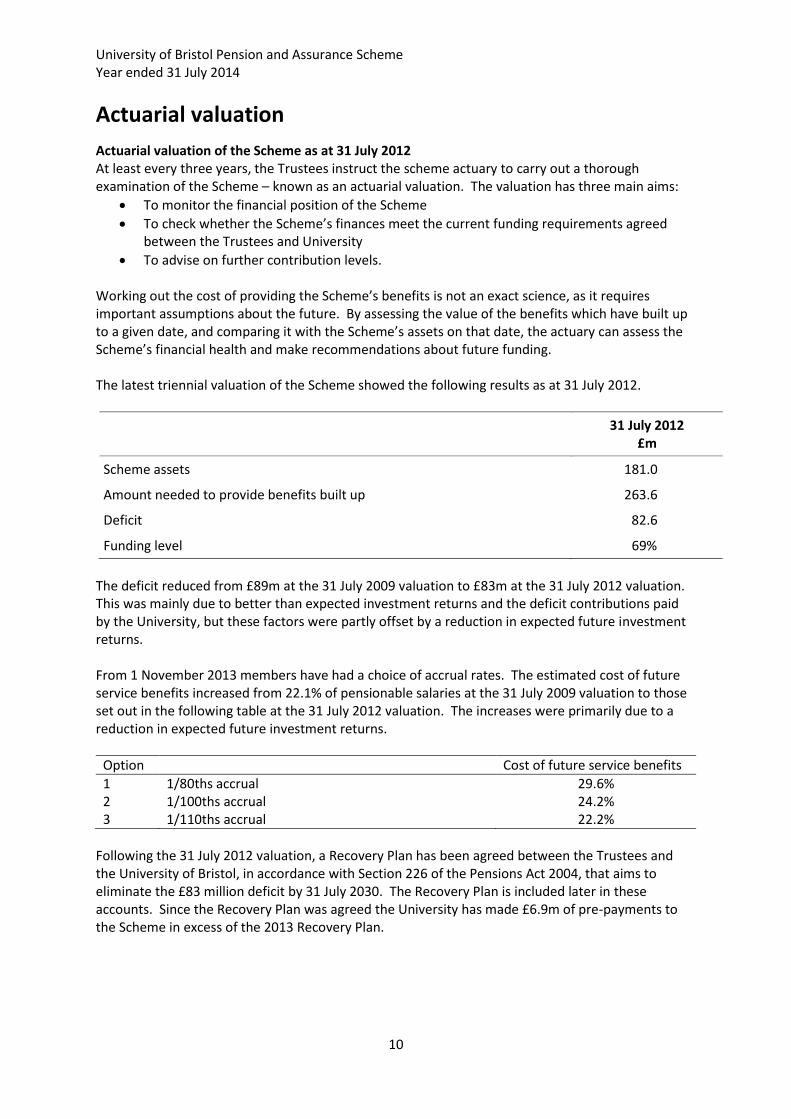

Actuarial valuation

Actuarial valuation of the Scheme as at 31 July 2012 At least every three years, the Trustees instruct the scheme actuary to carry out a thorough examination of the Scheme – known as an actuarial valuation. The valuation has three main aims:

To monitor the financial position of the Scheme

To check whether the Scheme’s finances meet the current funding requirements agreed between the Trustees and University

To advise on further contribution levels. Working out the cost of providing the Scheme’s benefits is not an exact science, as it requires important assumptions about the future. By assessing the value of the benefits which have built up to a given date, and comparing it with the Scheme’s assets on that date, the actuary can assess the Scheme’s financial health and make recommendations about future funding. The latest triennial valuation of the Scheme showed the following results as at 31 July 2012.

31 July 2012 £m

Scheme assets 181.0

Amount needed to provide benefits built up 263.6

Deficit 82.6

Funding level 69%

The deficit reduced from £89m at the 31 July 2009 valuation to £83m at the 31 July 2012 valuation. This was mainly due to better than expected investment returns and the deficit contributions paid by the University, but these factors were partly offset by a reduction in expected future investment returns. From 1 November 2013 members have had a choice of accrual rates. The estimated cost of future service benefits increased from 22.1% of pensionable salaries at the 31 July 2009 valuation to those set out in the following table at the 31 July 2012 valuation. The increases were primarily due to a reduction in expected future investment returns.

Option Cost of future service benefits

1 1/80ths accrual 29.6% 2 1/100ths accrual 24.2% 3 1/110ths accrual 22.2%

Following the 31 July 2012 valuation, a Recovery Plan has been agreed between the Trustees and the University of Bristol, in accordance with Section 226 of the Pensions Act 2004, that aims to eliminate the £83 million deficit by 31 July 2030. The Recovery Plan is included later in these accounts. Since the Recovery Plan was agreed the University has made £6.9m of pre-payments to the Scheme in excess of the 2013 Recovery Plan.

University of Bristol Pension and Assurance Scheme Year ended 31 July 2014

11

Actuarial valuation (continued)

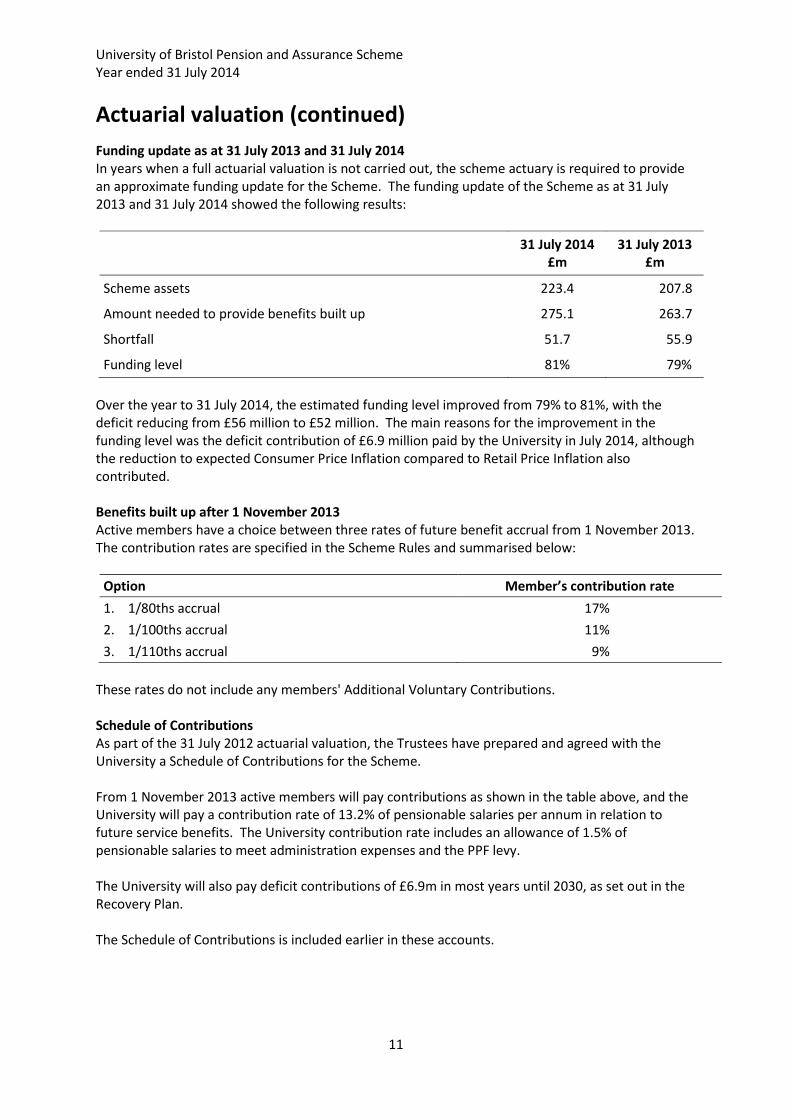

Funding update as at 31 July 2013 and 31 July 2014 In years when a full actuarial valuation is not carried out, the scheme actuary is required to provide an approximate funding update for the Scheme. The funding update of the Scheme as at 31 July 2013 and 31 July 2014 showed the following results:

31 July 2014 £m

31 July 2013 £m

Scheme assets 223.4 207.8

Amount needed to provide benefits built up 275.1 263.7

Shortfall 51.7 55.9

Funding level 81% 79%

Over the year to 31 July 2014, the estimated funding level improved from 79% to 81%, with the deficit reducing from £56 million to £52 million. The main reasons for the improvement in the funding level was the deficit contribution of £6.9 million paid by the University in July 2014, although the reduction to expected Consumer Price Inflation compared to Retail Price Inflation also contributed. Benefits built up after 1 November 2013 Active members have a choice between three rates of future benefit accrual from 1 November 2013. The contribution rates are specified in the Scheme Rules and summarised below:

Option Member’s contribution rate

1. 1/80ths accrual 17%

2. 1/100ths accrual 11%

3. 1/110ths accrual 9%

These rates do not include any members' Additional Voluntary Contributions. Schedule of Contributions As part of the 31 July 2012 actuarial valuation, the Trustees have prepared and agreed with the University a Schedule of Contributions for the Scheme. From 1 November 2013 active members will pay contributions as shown in the table above, and the University will pay a contribution rate of 13.2% of pensionable salaries per annum in relation to future service benefits. The University contribution rate includes an allowance of 1.5% of pensionable salaries to meet administration expenses and the PPF levy. The University will also pay deficit contributions of £6.9m in most years until 2030, as set out in the Recovery Plan. The Schedule of Contributions is included earlier in these accounts.

University of Bristol Pension and Assurance Scheme Year ended 31 July 2014

12

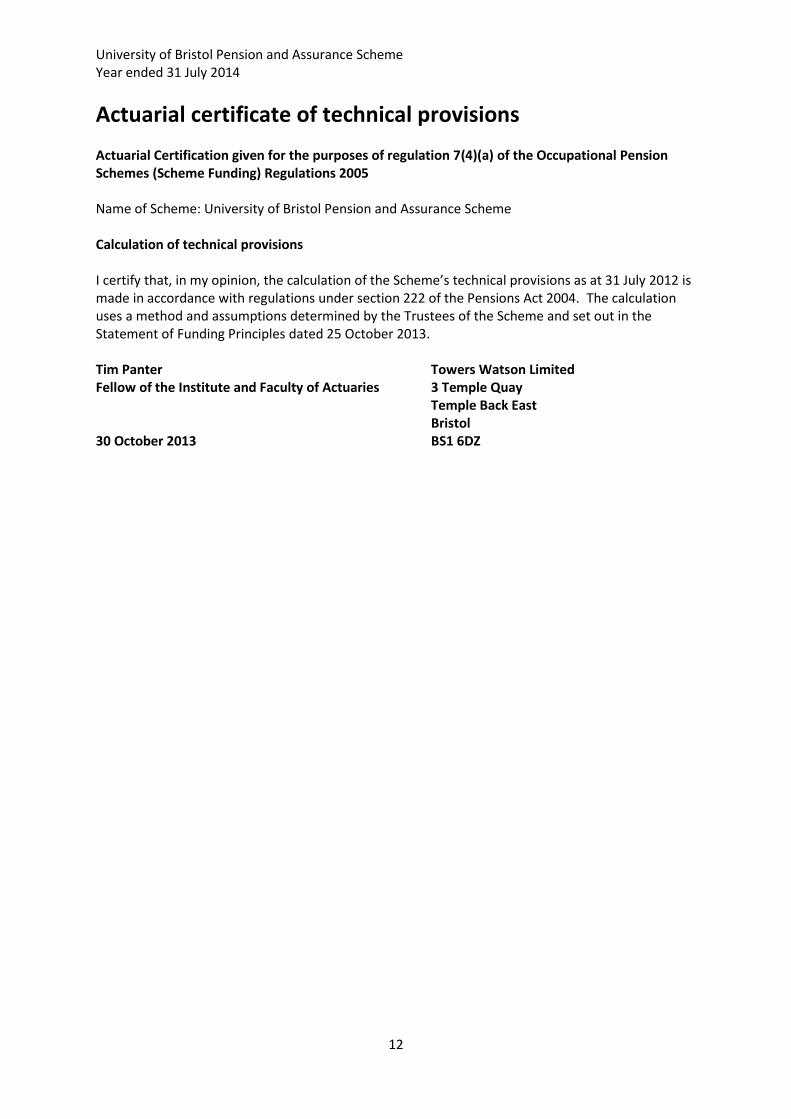

Actuarial certificate of technical provisions Actuarial Certification given for the purposes of regulation 7(4)(a) of the Occupational Pension Schemes (Scheme Funding) Regulations 2005 Name of Scheme: University of Bristol Pension and Assurance Scheme Calculation of technical provisions I certify that, in my opinion, the calculation of the Scheme’s technical provisions as at 31 July 2012 is made in accordance with regulations under section 222 of the Pensions Act 2004. The calculation uses a method and assumptions determined by the Trustees of the Scheme and set out in the Statement of Funding Principles dated 25 October 2013. Tim Panter Towers Watson Limited Fellow of the Institute and Faculty of Actuaries 3 Temple Quay Temple Back East Bristol 30 October 2013 BS1 6DZ

University of Bristol Pension and Assurance Scheme Year ended 31 July 2014

13

Actuarial certificate of the schedule of contributions

Adequacy of rates of contributions

1 I certify that, in my opinion, the rates of contributions shown in this schedule of contributions are such that the statutory funding objective can be expected to be met by the end of the period specified in the recovery plan dated 30 October 2013.

Adherence to Statement of Funding Principles

2 I certify that, in my opinion, this schedule of contributions is consistent with the Statement of Funding Principles dated 30 October 2013.

The certification of the adequacy of the rates of contributions for the purpose of securing that the statutory funding objective can be expected to be met is not a certification of their adequacy for the purpose of securing the Scheme’s liabilities by the purchase of annuities, if the Scheme were to be wound up.

Tim Panter Towers Watson Limited Fellow of the Institute and Faculty of Actuaries 3 Temple Quay Temple Back East Bristol 30 October 2013 BS1 6DZ

University of Bristol Pension and Assurance Scheme Year ended 31 July 2014

14

Statement of investment principles

Investment Objective

The Trustees aim to invest the assets of the Scheme prudently to ensure that the benefits promised to

members are provided. In setting investment strategy, the Trustees first considered the lowest risk asset

allocation that they could adopt in relation to the Scheme's liabilities. The asset allocation strategy they

have selected is designed to achieve a higher return than the lowest risk strategy while maintaining a

prudent approach to meeting the Scheme’s liabilities.

Strategy

The current planned asset allocation strategy chosen to meet the objective above is set out in the

table below. The Trustees will monitor the actual asset allocation versus the target weight and the

ranges set out in the table below at regular meetings.

Asset class Target weighting %

Ranges %

Liability Driven Investment

30.0

+/-5.0%

Matching assets 30.0 25.00 – 35.00

Equities

27.75

22.75 – 32.75

UK Equities 7.9 +/-5.0% Overseas Equities 19.85 +/-5.0% Alternatives 26.0 21.0 – 31.0 Property 7.5 +/-2.5% Diversified Growth Fund 18.5 +/-5.0% Absolute Return Bonds 16.25 +/-5.0%

Growth Assets 70.0 65.0 – 75.0

* Liability Driven Investment (LDI) aims to reduce the fund's exposure to changes in interest rates and inflation. This is done through investing in assets that move in line with the liability values such as swaps, gilts and index-linked gilts. As part of the regular monitoring, the Trustees will rebalance back to the target weighting if the asset allocation moves outside the ranges specified above. This rebalancing policy can be temporarily suspended if the Investment Committee is close to or in the process of moving to a new investment strategy, for example, in order to reduce the growth assets when a funding level trigger is hit, as discussed over the page. This Statement of Investment Principles is produced to meet the requirements of the Pensions Acts 1995 & 2004, the Occupational Pension Schemes (Investment) Regulations 2005 and to reflect the Government's Voluntary

Code of Conduct for Institutional Investment in the UK. The Trustees also comply with the requirements to

maintain and take advice on the Statement and with the disclosure requirements.

University of Bristol Pension and Assurance Scheme Year ended 31 July 2014

15

Statement of investment principles (continued) Strategy continued The Trustees have allocated 30% of the Scheme's assets to LDI with the medium term aim of hedging 50% of the Scheme's liabilities calculated on a Gilts + 0.5% basis (equivalent to 60% on the 2012 technical provisions basis). The initial hedge level (starting when the LDI mandate is implemented) will be 25% of the Scheme's liabilities calculated on a Gilts + 0.5% basis, with time based accumulation in place to move this up to 50% over the next three years. The time based hedge accumulation may be accelerated for two reasons. Firstly, yield based triggers are in place such that if gilt yields increase above market expectations during the three years, the hedge accumulation to 50% will be accelerated. Secondly funding level triggers are in place such that if the funding level improves significantly the hedge accumulation will be accelerated. The final hedge level when fully funded on the Gilts + 0.5% basis will be 90%. The Trustees have established funding level trigger points with the intention of considering increasing the allocation to matching assets as the funding level improves. Once a funding level trigger is hit, the asset allocation (shown on page 1) will change, as growth assets are reduced in favour of matching assets. The appropriate trigger levels will be regularly reviewed. The longer term target is to invest 25% in growth assets and 75% in matching assets once the funding level reaches 100% on a gilts +0.5% basis. The planned asset allocation strategy was determined with regard to the actuarial characteristics of the Scheme, in particular the strength of the funding position and the liability profile, and the covenant of the Employer. When choosing the Scheme’s planned asset allocation strategy the Trustees considered written advice from their investment advisers and, in doing so, addressed the following:

The need to consider a full range of asset classes.

The risks and rewards of a range of alternative asset allocation strategies.

The suitability of each asset class.

The need for appropriate diversification. In addition, the Trustees have also consulted with the sponsoring employer when setting this strategy. Risk The Trustees recognise that the key risk to the Scheme is that it has insufficient assets to make provisions for 100% of its liabilities (“funding risk”). The Trustees have identified a number of risks which have the potential to cause a deterioration in the Scheme’s funding level and therefore contribute to funding risk. These are as follows:

The risk of a significant difference in the sensitivity of asset and liability values to changes in financial and demographic factors (“mismatching risk”). The Trustees and their advisers considered this mismatching risk when setting the investment strategy.

The risk of a shortfall of liquid assets relative to the Scheme’s immediate liabilities (“cash flow risk”). The Trustees and their advisers will manage the Scheme’s cash flows taking into account the timing of future payments in order to minimise the probability that this occurs.

The failure by the fund managers to achieve the rate of investment return assumed by the Trustees (“manager risk”). This risk is considered by the Trustees and their advisers both upon the initial appointment of the fund managers and on an ongoing basis thereafter.

The failure to spread investment risk (“risk of lack of diversification”). The Trustees and their advisers considered this risk when setting the Scheme’s investment strategy.

The possibility of failure of the Scheme’s sponsoring employer[s] (“covenant risk”). The Trustees and their advisers considered this risk when setting investment strategy and consulted with the sponsoring employer as to the suitability of the proposed strategy. The risk of fraud, poor advice or acts of negligence (“operational risk”). The Trustees have sought to minimise such risk by ensuring that all advisers and third party service providers are suitably qualified and experienced and that suitable liability and compensation clauses are included in all contracts for professional services received.

University of Bristol Pension and Assurance Scheme Year ended 31 July 2014

16

Statement of investment principles (continued)

Risk continued Due to the complex and interrelated nature of these risks, the Trustees consider the majority of these risks in a qualitative rather than quantitative manner as part of each formal investment strategy review. Some of these risks may also be modelled explicitly during the course of such reviews. The Trustees’ policy is to monitor, where possible, these risks periodically. The Trustees receive periodic reports showing:

Actual funding level versus the Scheme specific funding objective.

Performance versus the Scheme benchmark.

Performance of individual fund managers versus their respective targets.

Any significant issues with the fund managers that may impact their ability to meet the performance targets set by the Trustees.

Implementation Aon Hewitt Ltd has been selected as investment adviser to the Trustees. They operate under an agreement to provide a service which ensures the Trustees are fully briefed to take decisions themselves and to monitor those they delegate. Aon Hewitt is paid an agreed annual fee which includes all services needed on a regular basis. Some one-off projects fall outside the annual fee and the fees for these are negotiated separately. This structure has been chosen to ensure that cost-effective, independent advice is received. The fund manager structure and investment objectives for each fund manager (“mandates”) are as follows: Legal & General UK Equities – to track the FTSE All-Share Index to within an acceptable range World (ex-UK) Equities – to track the FTSE All World (ex-UK) Index to within an acceptable range UK Property – Managed Property Fund – To outperform the CAPS Property Median over a rolling three year period BlackRock Global Investors Diversified Growth Fund – to achieve 3 month LIBOR plus 3% p.a. over a three year period (net of fees) Insight LDI – to track the liability benchmark provided by Aon Hewitt using the most efficient hedging instrument Absolute Return Bond Fund – to achieve 3 month sterling LIBOR plus 4% p.a. over a market cycle (gross of fees) The Trustees have delegated all day-to-day decisions about the investments that fall within each mandate, including the realisation of investments, to the relevant fund manager through a written contract. When choosing investments, the Trustees and the fund managers (to the extent delegated) are required to have regard to the criteria for investment set out in the Occupational Pension Schemes (Investment) Regulations 2005 (regulation 4). The managers’ duties also include:

Taking into account social, environmental or ethical considerations in the selection, retention and realisation of investments.

Voting and corporate governance in relation to the Scheme's assets.

University of Bristol Pension and Assurance Scheme Year ended 31 July 2014

17

Statement of investment principles (continued) Governance The Trustees are responsible for the investment of the Scheme’s assets. The Trustees take some decisions themselves and delegates others. When deciding which decisions to take themselves and which to delegate, the Trustees have taken into account whether they have the appropriate training and expert advice in order to take an informed decision. The Trustees have appointed an Investment Committee to make some more specialist investment related decisions. The Trustees have established the following decision making structure: Trustees

Agree the Scheme investment objective.

Agree the long term strategy.

Appoint the investment adviser.

Set structures and processes for carrying out the Trustee's role.

Consult with the Employer on major investment decisions via the Investment Committee. Investment Committee

Devise, and recommend to the Trustee Board a suitable asset allocation policy and investment strategy.

Implement and monitor the approved asset allocation policy and investment strategy.

Ensure that the Trustees are complying with their fiduciary duties in respect of investment issues.

Select, appoint and terminate mandates with fund managers

Monitor investment advisers and fund managers.

Monitor direct investments (see below).

Make ongoing decisions relevant to the operational principles of the Scheme’s investment strategy.

Carry out additional duties delegated by the Trustee Board from time to time. Investment Adviser

Advise on all aspects of the investment of the Scheme assets, including implementation.

Advise on this statement.

Provide required training. Fund Managers

Operate within the terms of this statement and their written contracts.

Advise Trustees on suitability of the indices in its benchmark

Select individual investments with regard to their suitability and diversification. The Pensions Act 1995 distinguishes between investments where the management is delegated to a fund manager with a written contract and those where a product is purchased directly, e.g. the purchase of an insurance policy or units in a pooled vehicle. The latter are known as direct investments. The Trustees’ policy is to review their direct investments and to obtain written advice about them at regular intervals. These include vehicles available for members' AVCs. When deciding whether or not to make any new direct investments the Trustees will obtain written advice and consider whether future decisions about those investments should be delegated to the fund manager(s).

University of Bristol Pension and Assurance Scheme Year ended 31 July 2014

18

Statement of investment principles (continued) Governance continued The written advice will consider the issues set out in the Occupational Pension Schemes (Investment) Regulations 2005 and the principles contained in this statement. The regulations require all investments to be considered by the Trustees (or, to the extent delegated, by the fund managers) against the following criteria:

The best interests of the members and beneficiaries

Security

Quality

Liquidity

Profitability

Nature and duration of liabilities

Tradability on regulated markets

Diversification

Use of derivatives The Trustees’ investment adviser has the knowledge and experience required under the Pensions Act 1995. The Trustees expect the fund managers to manage the assets delegated to them under the terms of their respective contracts and to give effect to the principles in this statement so far as is reasonably practicable. Fund managers are remunerated on an ad valorem basis. In addition, fund managers pay commissions to third parties on many trades they undertake in the management of the assets and also incur other ad hoc costs. The Trustees will review this SIP at least every three years and immediately following any significant change in investment policy. The Trustees will take investment advice and consult with the Sponsoring Employer over any changes to the SIP.

………………………………………….. Trustee Effective Date: October 2014

University of Bristol Pension and Assurance Scheme Year ended 31 July 2014

19

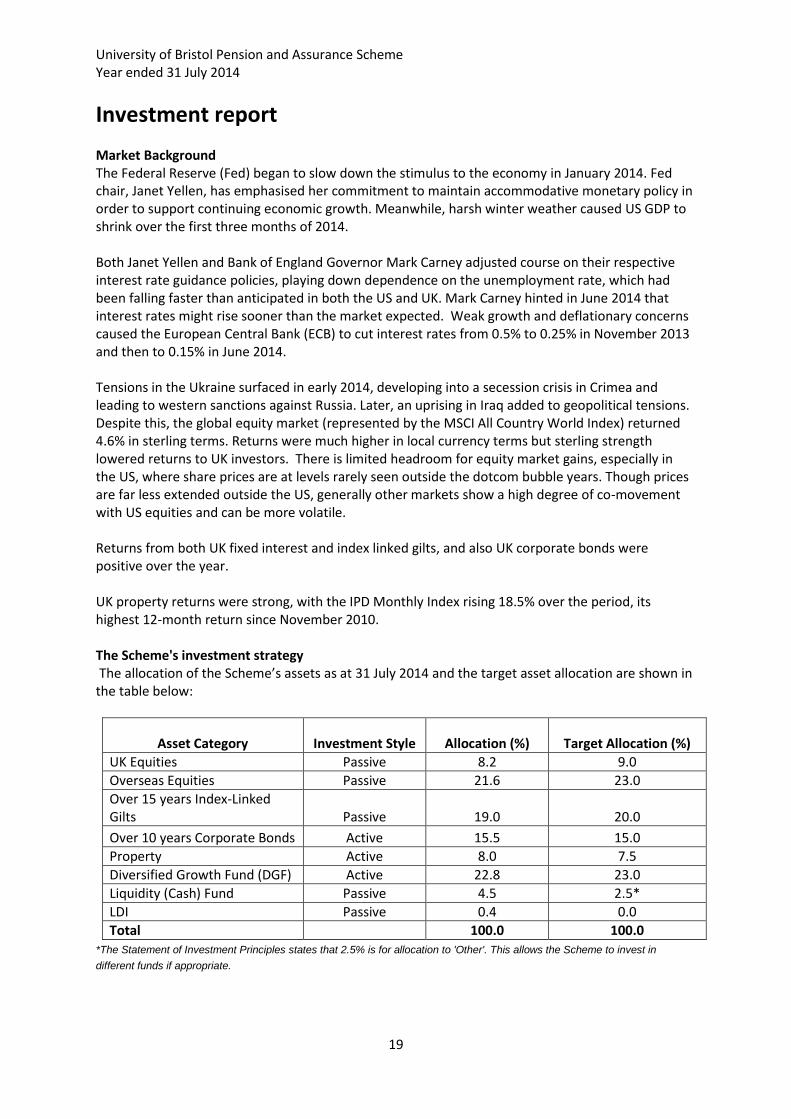

Investment report Market Background The Federal Reserve (Fed) began to slow down the stimulus to the economy in January 2014. Fed chair, Janet Yellen, has emphasised her commitment to maintain accommodative monetary policy in order to support continuing economic growth. Meanwhile, harsh winter weather caused US GDP to shrink over the first three months of 2014. Both Janet Yellen and Bank of England Governor Mark Carney adjusted course on their respective interest rate guidance policies, playing down dependence on the unemployment rate, which had been falling faster than anticipated in both the US and UK. Mark Carney hinted in June 2014 that interest rates might rise sooner than the market expected. Weak growth and deflationary concerns caused the European Central Bank (ECB) to cut interest rates from 0.5% to 0.25% in November 2013 and then to 0.15% in June 2014. Tensions in the Ukraine surfaced in early 2014, developing into a secession crisis in Crimea and leading to western sanctions against Russia. Later, an uprising in Iraq added to geopolitical tensions. Despite this, the global equity market (represented by the MSCI All Country World Index) returned 4.6% in sterling terms. Returns were much higher in local currency terms but sterling strength lowered returns to UK investors. There is limited headroom for equity market gains, especially in the US, where share prices are at levels rarely seen outside the dotcom bubble years. Though prices are far less extended outside the US, generally other markets show a high degree of co-movement with US equities and can be more volatile. Returns from both UK fixed interest and index linked gilts, and also UK corporate bonds were positive over the year. UK property returns were strong, with the IPD Monthly Index rising 18.5% over the period, its highest 12-month return since November 2010. The Scheme's investment strategy The allocation of the Scheme’s assets as at 31 July 2014 and the target asset allocation are shown in the table below:

Asset Category Investment Style Allocation (%) Target Allocation (%)

UK Equities Passive 8.2 9.0

Overseas Equities Passive 21.6 23.0

Over 15 years Index-Linked Gilts Passive 19.0 20.0

Over 10 years Corporate Bonds Active 15.5 15.0

Property Active 8.0 7.5

Diversified Growth Fund (DGF) Active 22.8 23.0

Liquidity (Cash) Fund Passive 4.5 2.5*

LDI Passive 0.4 0.0

Total 100.0 100.0 *The Statement of Investment Principles states that 2.5% is for allocation to 'Other'. This allows the Scheme to invest in

different funds if appropriate.

University of Bristol Pension and Assurance Scheme Year ended 31 July 2014

20

Investment report (continued)

Investment Performance Over the year to 31 July 2014, the investments had the following performance:

Asset Category Fund Performance

(%) Benchmark

Performance (%) Relative

Performance (%)

UK Equities 5.7 5.6 0.1

Overseas Equities 4.6 4.5 0.1

Over 15 years Index-Linked Gilts 7.1 7.1 0.0

Over 10 years Corporate Bonds 7.8 7.6 0.2

Property 16.5 n/a n/a

Diversified Growth Fund** 2.1 4.5 (2.4)

Liquidity (Cash) Fund 0.5 0.3 0.2

Total* 5.9 6.5 (0.6)

* The total has been calculated approximately by weighting performance of each asset class at the beginning of the year. **Diversified Growth Fund performance is net of fess Subsequent to the 31 July Scheme year end, the two key decision makers at Barings (the Scheme's diversified growth fund manager) left. In response, Aon Hewitt revised their rating of the fund and downgraded it from a 'Buy' to a 'Sell'. The assets were disinvested from Barings and will be transferred into the new diversified growth fund (with BlackRock Global Investors) in due course. Over the year to 31 July 2014, the combined assets underperformed the benchmark. This underperformance came from the Scheme's investment in the Diversified Growth Fund which performed poorly overall, in the 12 month period to 31 July 2014. The Scheme's asset allocation benchmark was adjusted over the year in line with the Scheme's de-risking policy.

University of Bristol Pension and Assurance Scheme Year ended 31 July 2014

21

Investment report (continued)

Scheme Outlook

Following the Scheme trialling a small Liability Driven Investment (LDI) portfolio strategy with Legal & General (L&G,) it was decided to invest 30% of the Scheme's assets with Insight investment management in a full LDI solution. An LDI Portfolio, when fully utilised, is designed to protect the pension scheme's funding position from changes in interest rate markets and changes in the outlook for inflation. To further diversify the Scheme's assets it was also decided to invest 16.25% of the Scheme's assets in an Absolute Return Bond Portfolio. The new investment strategy is set out below:

Asset Category Investment Style Target Allocation (%)

UK Equities Passive 7.90

Overseas Equities Passive 19.85

Property Active 7.50

Diversified Growth Fund Active 18.50

Absolute Return Bonds Active 16.25

LDI Passive 30.0

Total 100.0

Together with the Scheme's Trustees we are continuing to monitor the investment strategy; in particular the Scheme employs a dynamic strategy, which will trigger moving from growth assets to protection assets (e.g. gilts and/or LDI assets once they have been implemented) which move in line with the Scheme's liabilities. This allows the Scheme to increase the allocation to assets that better match the benefit payments when it is affordable to do so. In addition the Scheme agreed with Insight to increase the amount of assets that move in line with the Scheme's liabilities if market conditions look suitable. They have also agreed a time-based underpin with Insight to ensure the Scheme better matches the liabilities as time progresses. In summary, we are working closely with our advisors and the University in the management of the investment strategy.

University of Bristol Pension and Assurance Scheme Year ended 31 July 2014

22

Independent auditors’ report To the Trustees of the University of Bristol Pension and Assurance Scheme

We have audited the financial statements of University of Bristol Pension and Assurance Scheme

pension scheme for the year ended 31 July 2014 which comprises the fund account, the net assets

statement and the related notes. The financial reporting framework that has been applied in their

preparation is applicable law and United Kingdom Accounting Standards (United Kingdom Generally

Accepted Accounting Practice).

Respective responsibilities of Trustees and auditor

As explained more fully in the Trustees’ Responsibilities Statement set out on page [x], the schemes

trustees are responsible for the preparation of the financial statements which give a true and fair view.

Our responsibility is to audit and express an opinion on the financial statements in accordance with

applicable law and International Standards on Auditing (UK and Ireland). Those standards require us

to comply with the Auditing Practices Board’s Ethical Standards for Auditors. This report is made solely

to the scheme’s trustees as a body in accordance with The Occupational Pension Schemes

(Requirement to obtain Audited Accounts and a Statement from the Auditor) Regulations 1996 made

under the Pensions Act 1995. Our audit work has been undertaken so that we might state to the

scheme trustees those matters we are required to state to them in an auditors’ report and for no

other purpose. To the fullest extent permitted by law, we do not accept or assume responsibility to

anyone other than the scheme and the scheme’s trustees as a body, for our audit work, for this report,

or for the opinions we have formed.

Scope of the audit of the financial statements

A description of the scope of an audit of financial statements is provided on the Financial Reporting

Council’s website at www.frc.org.uk/auditscopeukprivate. Opinion on the financial statements

In our opinion the financial statements:

show a true and fair view of the financial transactions of the scheme during the year ended 31 July

2014, and of the amount and disposition at that date of its assets and liabilities, other than the

liabilities to pay pensions and benefits after the end of the year;

have been properly prepared in accordance with United Kingdom Generally Accepted Accounting

Practice; and

contain the information specified in Regulation 3 of, and the Schedule to, the Occupational Pension

Schemes (Requirement to obtain Audited Accounts and a Statement from the Auditor) Regulations

1996, made under the Pensions Act 1995. Mazars LLP Chartered Accountants and Statutory Auditor Clifton Down House Beaufort Buildings Clifton, Bristol. BS8 4AN

University of Bristol Pension and Assurance Scheme Year ended 31 July 2014

23

Independent auditors’ statement about contributions to the trustees of University of Bristol Pension and Assurance Scheme

We have examined the summary of contributions of University of Bristol Pension and Assurance

Scheme payable in respect of the scheme year ended 31 July 2014 to which this statement is attached

Respective responsibilities of Trustees and auditors

As described in the statement of trustees’ responsibilities, the scheme’s trustees are responsible for

ensuring that there is prepared, maintained and from time to time revised a schedule of contributions

which sets out the rates and due dates of certain contributions payable towards the scheme by or on

behalf of the employer and the active members of the scheme The trustees are also responsible for

keeping records in respect of contributions received in respect of active members of the scheme and

for monitoring whether contributions are made to the scheme by the employer in accordance with

the schedule of contributions.

It is our responsibility to provide a statement about contributions paid under the schedule of

contributions and report our opinion to you. This statement is made solely to the scheme’s trustees,

as a body, in accordance with The Occupational Pension Schemes (Requirement to obtain Audited

Accounts and a Statement from the Auditor) Regulations 1996 made under the Pensions Act 1995.

Our work has been undertaken so that we might state to the scheme trustees those matters we are

required to state to the in an auditors’ statement about contributions and for no other purpose. To

the fullest extent permitted by law, we do not accept or assume responsibility to anyone other than

the scheme and the scheme’s trustees as a body, for our work, for this statement, or for the opinions

we have formed.

Scope of work on statement about contributions Our examination involves obtaining evidence sufficient to give reasonable assurance that contributions reported in the attached summary of contributions have in all material respects been paid at least in accordance with the schedule of contributions. This includes an examination, on a test basis, of evidence relevant to the amounts of contributions payable to the scheme and the timing of those payments under the schedule of contributions. Statement about contributions

In our opinion the contributions for the scheme year ended 31 July 2014 as reported in the summary

of contributions attached on page 23 and payable under the schedule of contributions have in all

material respects been paid at least in accordance with the schedule of contributions certified by the

scheme actuary on 19 May 2010. Mazars LLP Chartered Accountants and Statutory Auditor Clifton Down House Beaufort Buildings Clifton Bristol. BS8 4AN

University of Bristol Pension and Assurance Scheme Year ended 31 July 2014

24

Summary of contributions paid in the year

During the year, the contributions paid to the scheme by the employer under the Schedule of Contributions were as follows:

£,000

Employer normal contributions 3,607 Employer additional contributions under salaries exchange scheme 2,818 Employer additional deficit related contributions 6,900 Employee normal contributions 173 Employee additional voluntary contributions 92

Total contributions 13,590

Signed on behalf of the Trustees:

Jonathan Lord

Chairman

University of Bristol Pension and Assurance Scheme Year ended 31 July 2014

25

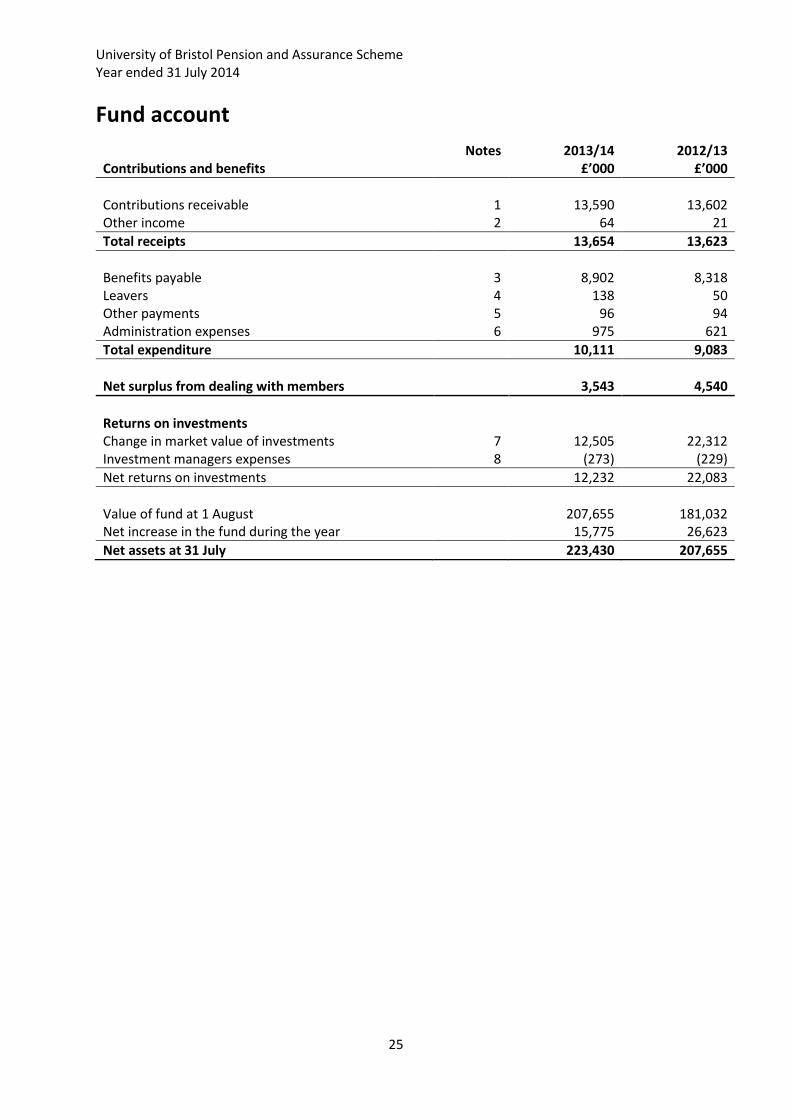

Fund account

Contributions and benefits

Notes 2013/14 £’000

2012/13 £’000

Contributions receivable

1

13,590

13,602

Other income 2 64 21

Total receipts 13,654 13,623

Benefits payable

3

8,902

8,318

Leavers 4 138 50 Other payments 5 96 94 Administration expenses 6 975 621

Total expenditure 10,111 9,083

Net surplus from dealing with members

3,543

4,540

Returns on investments

Change in market value of investments 7 12,505 22,312 Investment managers expenses 8 (273) (229)

Net returns on investments 12,232 22,083

Value of fund at 1 August

207,655

181,032

Net increase in the fund during the year 15,775 26,623

Net assets at 31 July 223,430 207,655

University of Bristol Pension and Assurance Scheme Year ended 31 July 2014

26

Net assets statement

Notes 2013/14 £’000

2012/13 £’000

Investments 7 223,987 209,818 Current assets 9 510 268 Current liabilities 10 (1,067) (2,431)

Net assets of the Scheme at 31 July 223,430 207,655

The financial statements summarise the transactions of the scheme and deal with the net assets at the disposal of the Trustees. They do not account for obligations to pay pensions and benefits which fall due after the year end of the scheme. The actuarial position of the scheme, which does not account for such obligations is dealt with in the Trustees annual report and the actuarial report, and these financial statements should be read in conjunction with them. These accounts were approved by the Trustees of the University of Bristol Pension and Assurance Scheme on 21st November 2014 and signed on its behalf by; Jonathan Lord Chairman

University of Bristol Pension and Assurance Scheme Year ended 31 July 2014

27

Principal accounting policies Basis of preparation The financial statements have been prepared in accordance with the Occupational Pension Schemes (Requirement to obtain Audited Accounts and a Statement from the Auditor) Regulations 1996 and with the guidelines set out in the Statement of Recommended Practice (revised 2007), Financial Reports of Pension Schemes. The financial statements summarise the transactions of the scheme and deal with the net assets at the disposal of the Trustees. They do not take account of obligations to pay pensions and benefits which fall due after the end of the scheme year. The actuarial position of the scheme, which does take account of such obligations, is dealt with in the statements pages 8 to 11 of the annual report and these financial statements should be read in conjunction with it. Accounting policies a) Contribution income from ordinary contributions relating to salaries earned in the financial year are included on the accrual basis at rates agreed between the Trustees and the University and as recommended by the actuary. For 2012-2013 these rates were:-

Employer 13.2%

Employees 9.0%, 11% or 17% depending upon the future accrual rate chosen by the employee

Special contributions including deficit recovery related contributions from the employer and additional voluntary contributions from employees are accounted for when received. b) Transfer values received and paid are accounted for when received or when paid. All values are based on methods determined by the consultant actuary and in accordance with the regulations issued under the Pensions Act 1995. There was no discretionary benefit included in the transfer values. c) Refunds of contributions and payments to Department of Social Security are accounted for when paid. d) Investment income dividends are credited to income as received. Dividends and interest are grossed up for the amount of any tax recoverable. e) Investments are marked to market and valued at the lower of bid or mid-market price. f) The money purchase AVCs to obtain additional benefits for some members requiring additional benefits are invested in policies with the Prudential Insurance Company.

University of Bristol Pension and Assurance Scheme Year ended 31 July 2014

28

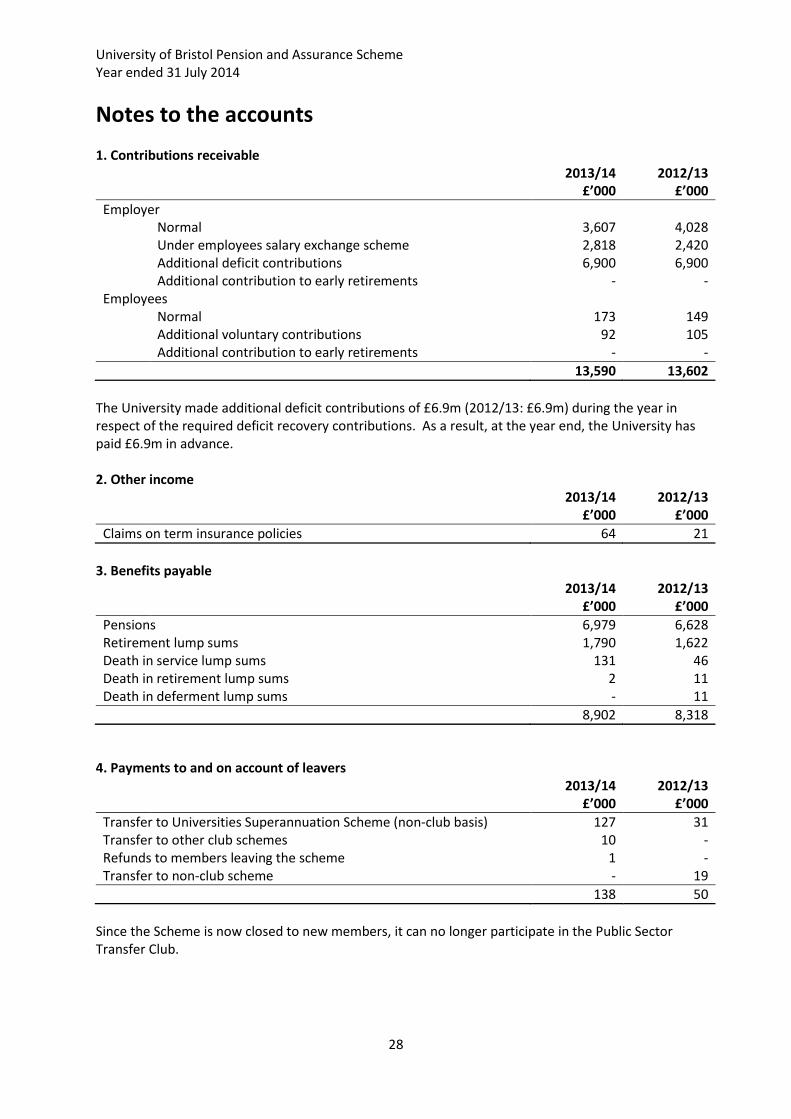

Notes to the accounts 1. Contributions receivable

2013/14 £’000

2012/13 £’000

Employer Normal 3,607 4,028 Under employees salary exchange scheme 2,818 2,420 Additional deficit contributions 6,900 6,900 Additional contribution to early retirements - - Employees Normal 173 149 Additional voluntary contributions 92 105 Additional contribution to early retirements - -

13,590 13,602

The University made additional deficit contributions of £6.9m (2012/13: £6.9m) during the year in respect of the required deficit recovery contributions. As a result, at the year end, the University has paid £6.9m in advance. 2. Other income

2013/14 £’000

2012/13 £’000

Claims on term insurance policies 64 21

3. Benefits payable

2013/14 £’000

2012/13 £’000

Pensions 6,979 6,628 Retirement lump sums 1,790 1,622 Death in service lump sums 131 46 Death in retirement lump sums 2 11 Death in deferment lump sums - 11

8,902 8,318

4. Payments to and on account of leavers 2013/14

£’000 2012/13

£’000

Transfer to Universities Superannuation Scheme (non-club basis) 127 31 Transfer to other club schemes 10 - Refunds to members leaving the scheme 1 - Transfer to non-club scheme - 19

138 50

Since the Scheme is now closed to new members, it can no longer participate in the Public Sector Transfer Club.

University of Bristol Pension and Assurance Scheme Year ended 31 July 2014

29

Notes to the accounts (continued) 5. Other payments

2013/14 £’000

2012/13 £’000

Premiums on term insurance policies 96 94

6. Administrative expenses

2013/14 £’000

2012/13 £’000

Administrative and processing 271 172 Pension Protection Fund 147 152 Actuarial fees 233 146 Audit fees 13 11 Legal and other professional fees 311 140

975 621

All expenses include unrecoverable VAT

University of Bristol Pension and Assurance Scheme Year ended 31 July 2014

30

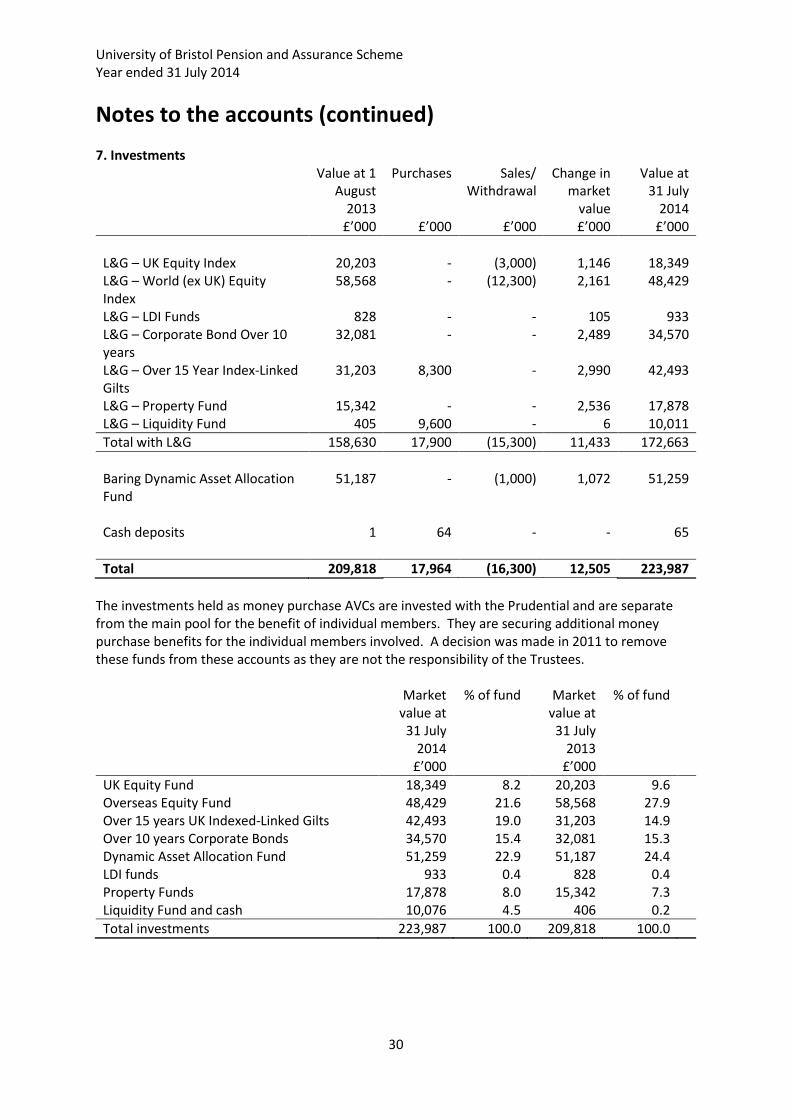

Notes to the accounts (continued) 7. Investments

Value at 1 August

2013

Purchases Sales/ Withdrawal

Change in market

value

Value at 31 July

2014 £’000 £’000 £’000 £’000 £’000

L&G – UK Equity Index 20,203 - (3,000) 1,146 18,349 L&G – World (ex UK) Equity Index

58,568 - (12,300) 2,161 48,429

L&G – LDI Funds 828 - - 105 933 L&G – Corporate Bond Over 10 years

32,081 - - 2,489 34,570

L&G – Over 15 Year Index-Linked Gilts

31,203 8,300 - 2,990 42,493

L&G – Property Fund 15,342 - - 2,536 17,878 L&G – Liquidity Fund 405 9,600 - 6 10,011

Total with L&G 158,630 17,900 (15,300) 11,433 172,663

Baring Dynamic Asset Allocation Fund

51,187 - (1,000) 1,072 51,259

Cash deposits 1 64 - - 65

Total 209,818 17,964 (16,300) 12,505 223,987

The investments held as money purchase AVCs are invested with the Prudential and are separate from the main pool for the benefit of individual members. They are securing additional money purchase benefits for the individual members involved. A decision was made in 2011 to remove these funds from these accounts as they are not the responsibility of the Trustees.

Market value at

31 July 2014

£’000

% of fund Market value at

31 July 2013

£’000

% of fund

UK Equity Fund 18,349 8.2 20,203 9.6 Overseas Equity Fund 48,429 21.6 58,568 27.9 Over 15 years UK Indexed-Linked Gilts 42,493 19.0 31,203 14.9 Over 10 years Corporate Bonds 34,570 15.4 32,081 15.3 Dynamic Asset Allocation Fund 51,259 22.9 51,187 24.4 LDI funds 933 0.4 828 0.4 Property Funds 17,878 8.0 15,342 7.3 Liquidity Fund and cash 10,076 4.5 406 0.2

Total investments 223,987 100.0 209,818 100.0

University of Bristol Pension and Assurance Scheme Year ended 31 July 2014

31

Notes to the accounts (continued) 8. Investment management expenses

2013/14 £’000

2012/13 £’000

Administration, management and custody services SEI - (6) L&G 273 235

273 229

Baring Asset Management Limited expenses are levied directly to their fund 9. Current assets

2013/14 £’000

2012/13 £’000

Prepayments and accrued income 24 - Lump sums on retirement prepaid on 31 July for retirements effective on 1 August

486 268

510 268

10. Current liabilities

2013/14 £’000

2012/13 £’000

Working capital balances with employer 907 2,274 Accrued expenses 160 157

1,067 2,431

All balances are due within one year. The working capital balances with employer mainly represent the payment by the University to retiring members. 11. Related party transactions The Scheme is administered by the University of Bristol. As at 31 July 2014, the Scheme owed £907,000 (2013: £2,274,000) to the University in respect of the Scheme’s operational costs. There were no employer related investments during the year. During the year, the Scheme paid Jonathan Lord £30,500 (2012/13: £19,000) including VAT for his services as a professional independent Trustee and independent chairman of the Scheme. No other Trustees receive any payments.