the united kingdom, a major development area for energy ... · the united kingdom, a major...

TRANSCRIPT

The United Kingdom,

a major development area for energy services

LONDON PRESS TRIP March 2015

GDF SUEZ, a major energy player in the UK

Steve RILEY,

CEO and President GDF SUEZ Energy UK-Turkey

London Press Trip - March 2015

GDF SUEZ: partner for the UK

• A major investor in the UK’s energy

infrastructure

• 2014 revenues of €5 billion

• 19 businesses employing around

c.20,000 people

• 8th largest foreign employer

• Serving key sectors through

power gas & services activities

• Strong focus on Health & Safety

across all our businesses

3

London Press Trip - March 2015

GDF SUEZ: Long-standing presence in the UK

• Active in the UK market for over 25 years

• Expanded the footprint through organic growth and acquisitions

2011 Combination

of GDF SUEZ &

International Power

2014

Acquisition

of Lend Lease

FM

2014 Opening

of Storengy

gas storage

site at Stublach 1997 E&P

business

established

in the UK

2001 E&P: First

production,

from Elgin-

Franklin

2005 E&P:

Entry into

West of

Shetland

2012 E&P:

Cygnus & Juliet

sanctioned

2014

Acquisition

of West Coast

Energy

1999 UK retail

business

established

1990 Privatisation

of UK energy

market, National

Power formed

2000 Demerger

of National Power,

creation of

International Power

2010 Acquisition

of Utilcom

(Cofely District

Energy Limited)

2013 Acquisition

of Balfour Beatty

Workplace

2007 Work started

on Storengy's

Stublach site

4

1990-1995 1996-2000 2001-2005 2006-2010 2011-2015

1999 Acquisition

of Heatsave

2013

Acquisition

of 25% of Dart

Energy (IGas)

– onshore

licences

2002

Acquisition

of BP Energy

Services

POWER

GAS

SERVICES

London Press Trip - March 2015

UK and EU Energy developments

UK developments

• Political environment

Energy will not determine the General Election but the outcome

will determine energy policy

Competition and Markets Authority Investigation of the Energy market

important for the industry

• Electricity Market Reform

Carbon price floor to encourage low carbon investment across

the economy

Contracts for Difference Scheme to incentivise low carbon deployment

Capacity Market to ensure security of supply

Levy Control Framework to control cost to the consumer

• Oil & gas industry

North sea offshore oil and gas production under pressure from costs

and taxes

UK Government supportive of shale gas development but slowed

down by permitting process

Onshore gas storage in the UK - an important development

EU Developments 2030 targets provide greater clarity for low carbon investment

Energy Union Package emphasises greater "connectivity"

to ensure energy security, decarbonisation, and competiveness

5

London Press Trip - March 2015

GDF SUEZ, a key player in the UK energy market

• One of the largest independent

generators by capacity in the UK

Diverse technology mix amounting

to 5GW gross capacity

Most significant provider of Grid

balancing services in UK

Flexible, reliable plant

• Major retail supplier to Industrial

and Commercial sector

• West Coast Energy, leading UK

wind developer

• Strong technical and trading

capabilities

• Developed a key onshore

gas storage facility

• Leading North Sea investor

and operator

• A major nuclear power project

KEY ATTRIBUTES

Saltend Natural gas 1,197 MW

First Hydro Pumped storage

2,088 MW

Rugeley Coal 1,026 MW

Indian Queens Oil 129 MW

Deeside Natural gas

515 MW

Retail Centre (Leeds)

West Coast Energy Office

(Mold)

Head Office (London)

6

Offices Pumped storage Gas Wind farm Oil Coal

Nuclear E&P Gas Storage

Onshore Wind Portfolio 70 MW (7 wind farms)

E&P Office (Aberdeen)

E&P: Juliet & Cygnus fields

NuGen site

Stublach gas storage facility

London Press Trip - March 2015

Power Generation: Case study

First Hydro, the fastest generation asset in the UK

• First Hydro comprises the pumped storage facilities

at Ffestiniog and Dinorwig in North Wales

• Largest pumped storage facility in the UK,

amounting to 2,088 MW

(Dinorwig 1,728 MW & Ffestiniog 360 MW)

• Dinorwig unique design minimised environmental

impact - 16 km of underground tunnels and turbine

hall within the mountain

• Strategic asset for the company, and the UK

• Able to deliver 2 GW in 16 seconds providing

system security; 30,000 mode changes per annum

• Over 250,000 visitors to Electric Mountain

facility each year

• Continuous improvement to the 30 year Dinorwig

plant, e.g. expansion of upper reservoir by 10%

7

KEY CHARACTERISTICS

London Press Trip - March 2015

Retail: Strengthening retail position in the UK

• GDF SUEZ Energy UK is well established

as a specialist energy supplier to industry

and commerce across the UK:

Operating in the UK supply market

since 1999

Top 7 UK supplier of power

and gas to businesses

650 million therms gas

and 10 TWh power portfolio

11,000 customer sites

Offering an innovative range

of energy supply products

Purchaser of green certificates and power

production from a range of technologies

A leader in load management services

8

Major brands in customer base

London Press Trip - March 2015

E&P: A leading North Sea operator

Key Growth areas

• Southern North Sea : Cygnus and Cepheus (discovered in 2014)

to be connected to the existing grid

• Central North Sea :

Austen, Faraday and Marconi discoveries as operator

Significant exploration portfolio

• West Shetland : first exploration wells in 2012-2013

• Participation in 2013 in 13 licenses onshore with unconventional

potential

9

Interest in almost

offshore licences

as operator

200+ staff in offices in London

and Aberdeen

2P reserves

onshore

licences

(non-operated)

Partner in pipeline

systems

(ETS and CMS) 2

47.6Mboe

Award of

new licences

offshore in the 27th bid round 9

Onshore UK

13

50

18

London Press Trip - March 2015

Cygnus : 2nd gas producer in the UK in 2016

• GDF SUEZ is operator with a 38.7%

share

• Gross 2P reserves of 18 billion cu.m

• Largest gas discovery in the Southern

North Sea in the last 25 years

• Peak annual production equivalent

to gas consumption of 1.5 million UK

homes

• 4,000 direct and indirect jobs during

the construction phase

10

Main Hub (Cygnus

Alpha Hub)

Platform

Cygnus Bravo

Cygnus Platforms Licenses operated

by GDF SUEZ Development area

Prospects

Development

potential

Cygnus field

Well in the Leman

Well in the carboniferous

Exploration potential

London Press Trip - March 2015

Stublach Gas Storage:

A key asset to meet UK gas market needs

• Stublach will be the biggest onshore underground gas storage in the UK by 2020

• Total Investment: c.£500m

• Located in a high demand area, Stublach will improve UK energy security of supply

• When fully developed it will have 20 salt caverns with total capacity of 400 mcm - close to 10% of the current UK underground gas storage capacity

• Operations now underway with 5 caverns (25% of the site total capacity)

• Very fast-cycle storage: injection and withdrawal rates shall be up to 30mcm/d

• Community Development Fund created by Storengy to support a wide range of local projects

11

London Press Trip - March 2015

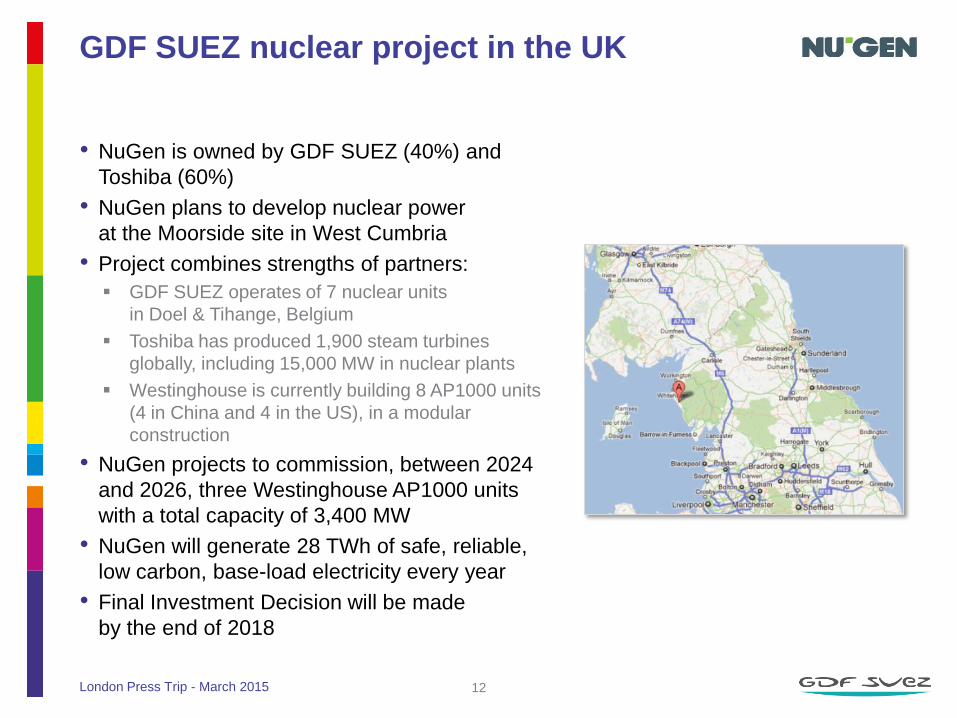

GDF SUEZ nuclear project in the UK

• NuGen is owned by GDF SUEZ (40%) and

Toshiba (60%)

• NuGen plans to develop nuclear power

at the Moorside site in West Cumbria

• Project combines strengths of partners:

GDF SUEZ operates of 7 nuclear units

in Doel & Tihange, Belgium

Toshiba has produced 1,900 steam turbines

globally, including 15,000 MW in nuclear plants

Westinghouse is currently building 8 AP1000 units

(4 in China and 4 in the US), in a modular

construction

• NuGen projects to commission, between 2024

and 2026, three Westinghouse AP1000 units

with a total capacity of 3,400 MW

• NuGen will generate 28 TWh of safe, reliable,

low carbon, base-load electricity every year

• Final Investment Decision will be made

by the end of 2018

12

London Press Trip - March 2015

Key Messages

GDF SUEZ is a major investor in the UK across the energy supply chain

Significant presence in the wholesale power generation market since 1990

A leading supplier of electricity and gas to Industrial and Commercial sector

An important investor in the offshore gas sector

Recently opened a state-of-the-art onshore, underground gas storage facility

Nuclear project to secure 7% of U.K.’s projected electricity requirements

13

Major provider of energy and integrated services throughout the UK

Energy services, a major lever for development for GDF SUEZ

to be leader in energy transition in Europe

JÉRÔME TOLOT,

GDF SUEZ Executive Vice-President

in charge of the Energy Services business line

London Press Trip - March 2015

ENERGY INTERNATIONAL

INFRASTRUCTURES ENERGY EUROPE GLOBAL GAS & GNL

GDF SUEZ Energy Services One of the 5 Business Lines of GDF SUEZ

95%

5% Europe

Rest of the world

ENERGY SERVICES

€15.7bn

~100,000 employees

Public tertiary 28%

Private tertiary 25%

Industry 35%

Infrastructures 12%

SALES BREAKDOWN 2014 Figures

15

FRANCE

ENERGY

SERVICES

€2.5bn sales

12,500

employees

DISTRICT

ENERGY

€0.9bn

1,500

employees

FRANCE

SYSTEMS,

INSTALLATIONS

&

MAINTENANCE

€4.4bn sales

29,500

employees

BENELUX

€3bn sales

18,500

employees

INTERNATIONAL

€4.3bn sales

29,500

employees

ENGINEERING

€0.6bn sales

4,500

employees

Cofely Fabricom

Cofely Services

Cofely Axima

Cofely Services

Cofely Axima

Cofely Endel

Cofely Ineo

Tractebel

Engineering Cofely

Cofely Réseaux

Climespace

CPCU

2014 figures

London Press Trip - March 2015

Key figures 2014

ENGINEERING INSTALLATION /

MAINTENANCE

SERVICES

INTEGRATION

DISTRICT

ENERGY

INDUSTRIAL

UTILITIES

ENERGY

PERFORMANCE

16

100,000

employees

> 1,300

locations

90

public-private

partnerships

230

district heating &

cooling schemes

700,000

light points under

management

500,000m²

of data centers

operated

€15.7bn

of sales

5%

EBIT margin

London Press Trip - March 2015

GDF SUEZ Energy Services A leader in key markets for energy transition

Install and operate local urban

infrastructures

(district heating/cooling, mobility,

public lighting)

Develop physical and virtual

exchange networks (smart city)

Develop ecodistrict, notably

with “ smart grid ” systems

Offer a range of Facility Management services

in addition to technical solutions in energy efficiency

Provide energy performance

solutions for buildings

(public & private tertiary,

head offices, housing…)

Provide energy performance

solutions to our industrial

clients

INFRASTRUCTURES Take part in the development of major infrastructures

designed to optimize the energy mix

Build, develop and maintain

renewable energies

Ensure the evolution

of mature energies

(nuclear decomissioning,

oil&gas…)

Adapt the major transport

and distribution

infrastructures

CITIES Develop sustainable urban networks

20%

BUILDINGS AND INDUSTRY Offer the optimal energy performance tailored

to the specific needs of every client

15% 65%

17

% Revenues

London Press Trip - March 2015

Consulting Engineering

5%

Installations

40%

Services

55%

Fully integrated services to meet its clients’ needs

GDF SUEZ ENERGY SERVICES

GDF SUEZ ENERGY SERVICES 12/2013

Consulting services

Energy audits

Engineering studies

Project implementation

Electrical

Heating Ventilation &

Air-Conditioning (HVAC)

Mechanical

Information &

Communication

Technologies (ICT)

& Automation

Multi technical

maintenance

Industrial utilities

District energy networks

Facility Management

18

London Press Trip - March 2015

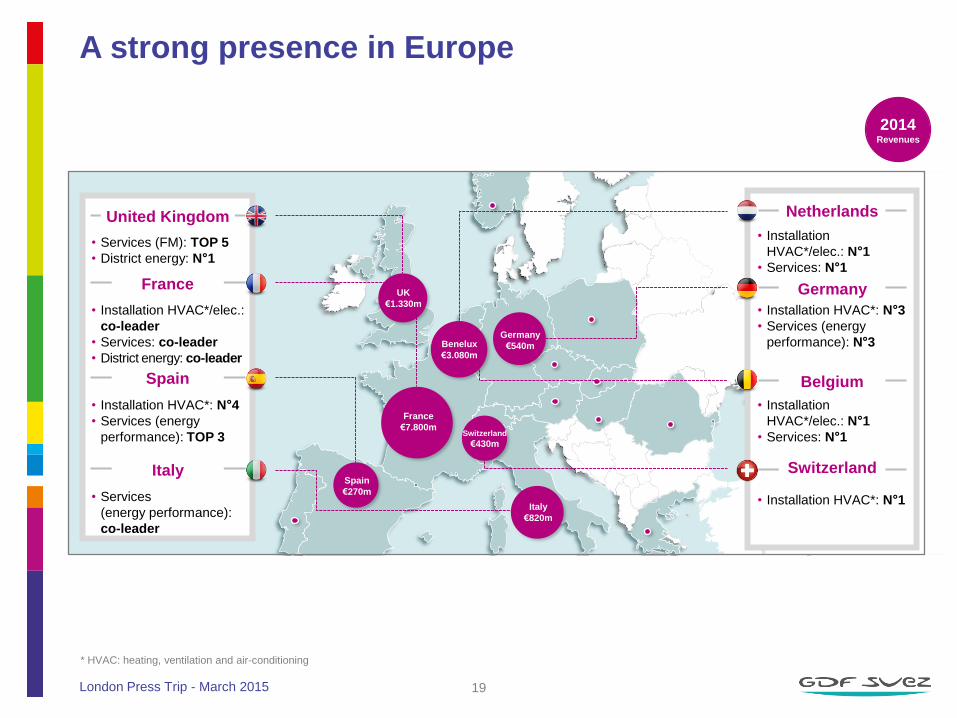

Netherlands

Germany

Belgium

Switzerland

United Kingdom

France

Spain

Italy

UK

€1.330m

France

€7.800m

Benelux

€3.080m

Spain

€270m

Germany

€540m

Italy

€820m

• Installation

HVAC*/elec.: N°1

• Services: N°1

• Installation HVAC*: N°3

• Services (energy

performance): N°3

• Installation

HVAC*/elec.: N°1

• Services: N°1

• Installation HVAC*: N°1

• Services (FM): TOP 5

• District energy: N°1

• Installation HVAC*/elec.:

co-leader

• Services: co-leader

• District energy: co-leader

• Installation HVAC*: N°4

• Services (energy

performance): TOP 3

• Services

(energy performance):

co-leader

A strong presence in Europe

* HVAC: heating, ventilation and air-conditioning

Switzerland

€430m

19

2014 Revenues

London Press Trip - March 2015

MIDDLE

EAST

130 180 / 400

200 350 / 800 460 560

NORTH

AMERICA

SOUTH

AMERICA

AUSTRALIA

PACIFIC

VARIOUS

(AFRICA,

INDIAN OCEAN)

60 / 200

40 100 / 600

125* 200 / 300 20

SOUTH EAST ASIA

Strengthen our local presence or develop new leaderships

Seize new opportunities

Maintain (eventually strengthen) our positions

GDF SUEZ Group’ management (China business unit)

An ever-growing international presence

Revenues 2014 in €million

Our ambition: Double our international revenues by 2020

800 1 500 /

3 000 TOTAL

(outside EUROPE)

* Unconsolidated. GSES current share

Ambition 2020 in €million

25* 100/200

20

London Press Trip - March 2015

Acquisitions completed these previous years

EUROPE

2011

OUTSIDE EUROPE

Canada (Adelt)

Mechanical installation

€44m, €2m

Chili (Térmika)

Installation / maintenance

€15m, €1m

Brazil (Telca 2000)

Electrical installation

€8m, €1m

Country (Target) Main activity TO*, EBITDA*

Legend

France (Resplandy)

Electrical installation

€10m, €1m

France (Sinovia (remaining 55%))

Supervision sofware

Malaysia (Cyberjaya DC)

District cooling scheme

€12m, €5m

United Kingdom (Energy

Centre Excel Conference Centre)

District heating/cooling scheme

€6m, €1m

France (CTTG)

CCTV monitoring

€1m, €0.2m

Australia (TSC (19% share))

Technical maintenance

€125m**

Brazil (EMAC)

HVAC

€30m, €2m

United Kingdom (Balfour Beatty Workplace) Facility Management €573m, €28m

Poland (E.On Sverige DH assets) District heating scheme €19m, €3.5m

France (acquisition of SESAS / disposal of ERIVA) District cooling scheme €3.8m, €2.5m

Netherlands (ATES Systems of buildings) Heating storage €2m, €1m

Singapore (Keppel FMO) Facility Management 55 m€, 3.4 m€

Qatar (Mannai (49% share)) Facility Management €20m**, €1.2m

USA (Ecova) Energy supply and data management €132m, €22m

Singapore (SMP Pte) Technical maintenance of data centres €5m, €0.6m

Germany (Lahmeyer)

Ingineering

€135m, 18.2m€

Switzerland (Commande SA)

Building automation

€4.1m, €0.33m

Germany (HGS)

Technical maintenance

€30m, €3.2m

*100% acquisition year data (yearly average contribution)

**For the whole firm.

2012 2013 2014

21

London Press Trip - March 2015

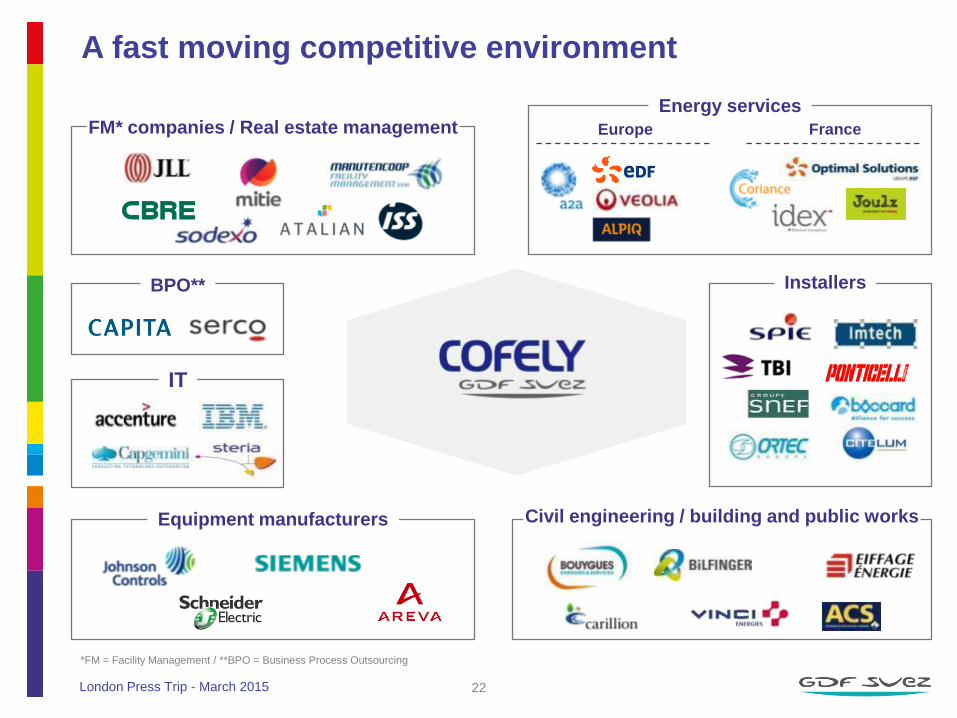

Europe France

A fast moving competitive environment

*FM = Facility Management / **BPO = Business Process Outsourcing

FM* companies / Real estate management

BPO**

IT

Equipment manufacturers Civil engineering / building and public works

Installers

Energy services

22

London Press Trip - March 2015

Technological boom affecting all businesses

TECHNOLOGY

Cloud, communication

IT environment Decentralized energy

PV, storage

Mobility

Electrical cars, hydrogen,

IT Services

Data management

Data analytics,

dashboards

New possibilities

Robotics, drones,

3D printing, …

23

London Press Trip - March 2015

Acceleration of innovative digital solutions in our business

Tools to improve energy monitoring and performance

management

• Cofely Vision,

• 3EBox…

1

2

Smart dashboards to give summary information

to customers in real time

• Vertuoz,

• Cit’ease…

3

« Big data » in our businesses: concrete applications

under development:

• Deepki (for tertiary buildings),

• Blu-e (for industrial buildings)

24

London Press Trip - March 2015

Seize new markets’ opportunities

Large projects Data management Cybersecurity

Urban mobility Nuclear decommissioning Large outsourcings

25

London Press Trip - March 2015

Finance trajectory

1,040 1,100 1,180

1,280 1,400

1,500 1,610

1,710

800

1,100

800 790 750 750 750 750

2013 2014 2015 2016 2017 2018 2019 2020

EBITDA

CAPEX

In €m

14,700 15,700 16,000 16,900 17,800

18,900 19,900 20,900

7.1% 7.1% 7.4% 7.6% 7.9% 7.9% 8.1% 8.2%

4.8% 5.0% 5.1% 5.2% 5.5% 5.6% 5.7% 5.8%

2013 2014 2015 2016 2017 2018 2019 2020

TO

EBITDA margin

EBIT margin

26

London Press Trip - March 2015

Strategic orientations

• Maintain our leadership in Europe

• Continue our targeted international development

• Adapt our business model to the new energy context

and our new clients’ expectations

• Increase the technology content of our businesses

• Develop new talents

27

Cities & Local Authorities: Evolution of Service Solutions

Becoming a Strategic Partner in the ‘Desirability of Place’

WILFRID PETRIE,

Chief Executive Officer of Cofely UK

London Press Trip - March 2015

Key Developments of Cofely in the UK

• 2010: Acquisition of Utilicom

Consolidation of market leading position

in District Energy

• 2013: Acquisition of Balfour Beatty WorkPlace

Additional capabilities for the delivery of TFM

& outsourcing of business processes

• 2014: Acquisition of Lend Lease’s FM business

Long-term portfolio of contracts in key healthcare

& education markets

New life-cycle management capability

29

End 2014 vs.

2013

x3 revenues

x7 employees in UK

London Press Trip - March 2015

• No.1 in District Energy

• No.1 in Industrial Energy Services

• Saving 150,000t CO2 p.a

• 2 GW of thermal generation managed

• 25 million m2 of managed premises

• Over 1,400 Government Buildings

20 hospitals

8 nuclear power stations

• 14,000 sites managed

• Unique transformational partnerships

• Digital Channel Shift

Energy

Services

Technical

Services

Facility

Management

Business

Process

Cofely in the UK:

£1 billion revenues & 19,000 employees

30

2015 - 2020: Vision for further strategic growth • Reach £2 billion revenues

• Consolidate No.1 position in Energy Services

• Top 3 provider of outsourced integrated services

London Press Trip - March 2015

UK: Outsourcing Evolution –

move to strategic integration of services

31

1980

In-house

1990

Single

service

2000

Bundled

services

2010

Integrated

FM

2015

Strategic

outsourcing

Security

M&E engineering

Catering

Cleaning

Technical Maintenance

Pest control

Broad

Single point contact

Standardised provision

Best practice

Integrated delivery

Management

information systems

Property Management

International delivery

Consultancy

Supply chain

Project management

Buildings management

& services

Business process

outsourcing

Technology

Data management

Asset investment

& lifecycle

Energy/carbon

Add-on specialist services

Service

Evolution

London Press Trip - March 2015

UK: A landscape of opportunity for Cities

& Local Authorities

UK is open, liberal market for energy and services with many opportunities

• Planned devolution of powers to regions within the UK

• Reduced funding from Central Government – ‘pressure to more with less’ Austerity due to financial crisis

In 2016, Government funding for local authorities will have dropped in real terms by 37%

since 2010

• Citizen requirements & ‘Channel Shift’ UK Government Digital First Initiative

• Legislative Drivers Social Value Act

Carbon reduction targets

Local Energy Production Targets

32

London Press Trip - March 2015

Strategic Partnerships with UK Local Authorities

• Customer or citizen centric, transformational contracts for local government

• Partners to deliver Local and regional master plans

Sustainable future

Meaningful analytics of usage data

• Delivering services is not just about maintaining assets or infrastructure efficiently

anymore Not a traditional (client/contractor) relationship

• Measurement on tangible outcomes for the local area including: Inward investment & growth

Social responsibility

Sustainable and efficient energy solutions

• Making a city or locality a desirable place to live, or invest

33

London Press Trip - March 2015

Our involvement at the Queen Elizabeth Olympic Park

Timeline

2008 – Design & build of energy centres & network begins

2010 – Kings Yard Energy Centre operational

2011 – Stratford City Energy Centre operational – Westfield Shopping Centre

2012

• Heating, Cooling & FM provision for London 2012 Olympics

• 40 year heating & cooling concession begins

2014

• 10 year FM services agreement begins

• Launch of ‘Our Parklife’ Community Interest Company

• East London Energy: First provision of heating to East Village

(former Athletes Village)

• South Park opens to public (including mgnt of the ArcelorMittal Orbit)

34

London Press Trip - March 2015

Legacy, Growth & Development:

Queen Elizabeth Olympic Park

• Masterplan for Games-time infrastructure and transition to legacy growth

and development

Long-term investment in low CO2 energy infrastructure

Constant ‘quality management’ of the Park

Together makes a pleasant environment to live and work – nicely landscaped,

secure and investible

• Post-Games the Olympic Park area is being redeveloped with only ‘core’ Olympic

venues retained

Nearly 3.7 million sq m of new development

29,000 homes and 1.36 million sq m of commercial space

• Cofely is supporting London Legacy Development Corporation (LLDC)

to deliver legacy regeneration as the delivery partner for:

Legacy Transformation from ‘Games’ to ‘post-Games’

Sustainability best-practice and energy transition

Re-opening of the Park to the Public

Presenting the Park in a way that will attract further investment

35

London Press Trip - March 2015

Cofely Activities Overview:

Queen Elizabeth Olympic Park

• Design, build & operate district

energy scheme £100m investment

40 year concession (2012 – 2052)

• 18km of networks, 2 energy centres 195 MW Heating

64 MW Cooling

30 MW Electrical

• Facilities management of iconic venues 10 year contract (2013 – 2023)

24 separate services to LLDC across the Park

• Parkland, highways and waterways, Park security

• ArcelorMittal Orbit and South Park Hub Marketing, sales, visitor experience

Catering, hospitality and event management

36

London Press Trip - March 2015

Engaging with the Local Community

37

Park-wide security

& landscaping Park Control Centre

Facilities Management

Park Venues

Our Parklife Community Interest

Company /

Social Enterprise

71% ADDING

SOCIAL VALUE:

employed

are local residents 25% operational workforce

previously unemployed Training programs long-term

unemployed women in workplace

London Press Trip - March 2015

North East Lincolnshire Council

• NEL holds ambition to create a desirable place to live through regeneration,

transport / infrastructure and energy efficiency solutions

• Output specification in-line with Council strategic plan

• Improve the lives of residents, generate jobs and deliver sustainable economic

growth: Secure £500m of investment & growth

Secure 4,000 new jobs for the area

Create 60,000 sq m of employment space

Achieve 33% reduction in road traffic accidents & deaths

• Provide £multi-million savings to Council including efficient management

of NELC portfolio Property rationalisation

Refurbishment

Energy Efficiency & Sustainability

38

London Press Trip - March 2015

North East Lincolnshire Council

- strategic, transformational partnership

• 10 year Regeneration Partnership

(2010 – 2020)

• 300 staff

• Property Services

Architectural Design

Strategic Asset Management & FM

• Highways & Transportation

Including parking enforcements

• Regeneration & Development

Incl. Economic Development,

Planning & Buildiing Control,

& Home Improvement Services

• Additionally, Energy Management

now in scope

39

London Press Trip - March 2015

North Tyneside Council

• Ambition to create channel shift in the way

citizens access services and efficiency

of back-office functions.

• 800 employees, 10 year partnership Option to extend by further 5 years

• Management and delivery through local

based employees Information and Communication

Technology Services

Payroll & HR services

Financial Services (including revenue

& benefits)

40

London Press Trip - March 2015

Cheshire West & Chester Council

• Desirability and channel shift to provide

easy access to public services

• Help the local authority to ‘modernise,

improve and save as efficiently as possible’

• Joint Venture (51% Cofely, 49% CW&C) £200m over 10 years

Transfer of 300 council employees in JV

• Scope of Services: Technical Services & FM

Customer Services

Business Operations

Potential to expend scope into planning

and regeneration aspects

41

London Press Trip - March 2015

CW&C: Extending Expertise to other Local

Authorities

• £3 million investment into Councils IT system

Big data analysis of service usage

Development of software tools to develop greater insight into citizen needs

and help plan for the future

Deployment of GDF SUEZ Smart City Dashboard to give visibility and simplicity

to captured data sets

• Social Value & Commitments

65 apprenticeships, 20 graduate placements & 1,000 hours of work experience

for local people

Community Interest Company with % of profits re-invested into local community

• JV plans to ‘trade’ with other public and private sector entities

Services to be offered to neighbouring / regional areas to create revenue stream

for CW&C

Pioneering: UK first for a public / private partnership JV to focus on external growth

42

London Press Trip - March 2015

Future Service Provision for Cities

& Local Authorities

• A convergence of big data, energy transition and the shifting role of the state

• ‘Desirability’ is a key driver for place Place to live

Place to work

Place to invest

Sustainable economic growth and social well-being

• Service providers acting as strategic partners to help them achieve their goals

• Creation of major opportunities for GDF SUEZ & Cofely to combine people,

technology, assets, and data Energy transition

Smart buildings & lifecycle management of assets

Integrator of services to provide holistic, customer centric solutions

43

Cofely UK’s Activities at the British Library

London Press Trip - March 2015

British Library

• 150 million items (3 million added each year)

• 13 million books

• 7 million manuscripts

• 4.5 million maps

• 6 million stamps

• Legal deposit library, receives copies

of all books produced in the United Kingdom

and Ireland

• Over 625 km of shelves, 12 km added every year

London Press Trip - March 2015

British Library (St. Pancras)

• Largest public sector building built in

modern times

• 110,000 m2 over 14 levels & 76 plantrooms

9 MW chilling and 3.4 MW heating

Book handling system with 1.6 km of

conveyors

• Technical Services & Energy Efficiency

45 Cofely employees

Awarded 5 year contract in 2008 (now extended until 2016)

• 23% reduction in energy consumption

Winner of Green 500 Award

46

London Press Trip - March 2015

British Library (Boston Spa)

• 61,000 m2 state-of-the-art archive

facility across a 42 acre site

• Specifically designed for document

delivery service processes

• Over 100km of shelving housing

a collection devoted to storage

interlibrary loan

• Low oxygen storage environment

Similar to that found 3,000 metres

up a mountain, to prevent fire breaking out

47

London Press Trip - March 2015

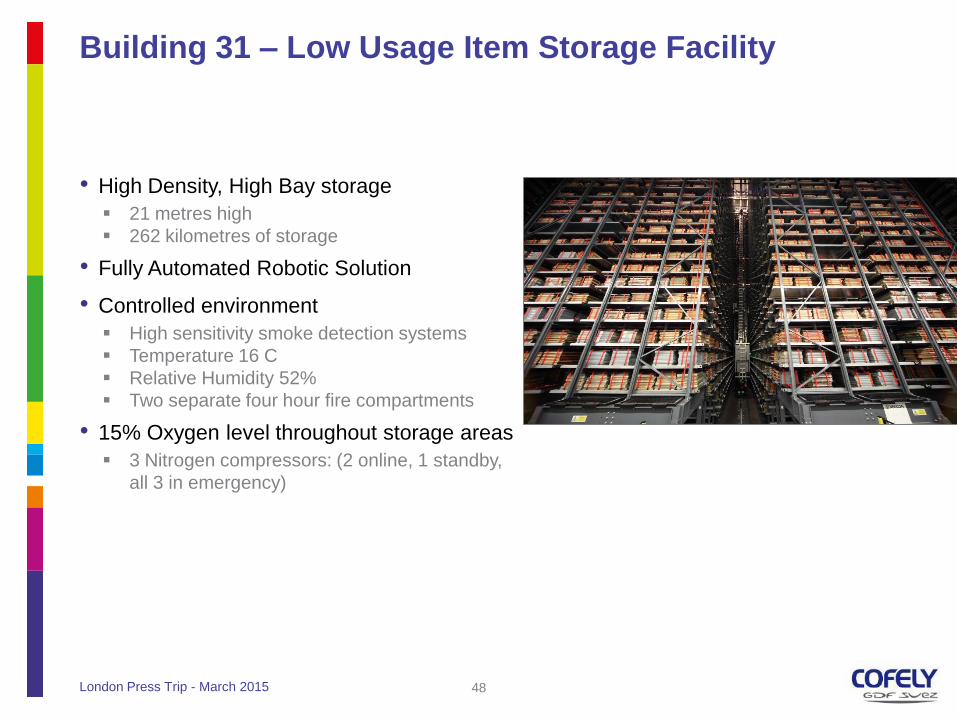

Building 31 – Low Usage Item Storage Facility

• High Density, High Bay storage

21 metres high

262 kilometres of storage

• Fully Automated Robotic Solution

• Controlled environment

High sensitivity smoke detection systems

Temperature 16 C

Relative Humidity 52%

Two separate four hour fire compartments

• 15% Oxygen level throughout storage areas

3 Nitrogen compressors: (2 online, 1 standby,

all 3 in emergency)

48

London Press Trip - March 2015

Challenges of Working with the Heritage Sector

The sector presents a number of common challenges

and unique characteristics:

• Predominantly old, list buildings (including grade I & II)

• Strict atmospheric parameters for preservation of collections

Humidity and Temperature control to critical environments

Collection care, UK Government Indemnity Scheme Requirements

• Public access buildings with unique user & profiles and intense usage

• Funding issues

Government targets for carbon reduction of up to 25%

49

London Press Trip - March 2015

Other Museums & Galleries Experience - UK

• National Portrait Gallery

• Royal Museums, Greenwich

• Imperial War Museum

• Kew Gardens

• Science Museum

• Museum of London

• V&A Museum

• Cabinet War Rooms

50

The United Kingdom,

a major development area for energy services

LONDON PRESS TRIP

March 2015