the uncertainty, complexity and cost of ‘employee’ status · the uncertainty, complexity and...

TRANSCRIPT

The uncertainty, complexity and cost of ‘employee’ status in Australia

Associate Professor Brett Freudenberg Griffith University, Australia

E: [email protected] T: +61 7 373 58071 R: http://ssrn.com/author=498263

2

Initial thoughts

What does it mean for the economy if employment (and employing someone) is:

» too uncertain;

» too complex; and

» too administratively costly?

Small businesses are important to the economy:

» Many do not employ and could be seen as pseudo employees themselves;

» Others do employ but face challenges with regressive compliance cost, member-management and finance; and

» Are a large proportion of the service sector which accounts for approximately 80% of Australia’s gross value added to the economy.

“Employment” consequences

Employer

Employee

• Wages taxed at marginal rates: • 0%: $0 - $18.2 K (£10.6K) • 19%: $18.2- $37K (£21.5K)

• 32.5%: $37 - $87K (£50.5K)

• 37%: $87 - $180K (£105K)

• 47% > $180K (£105K) • Plus 2% Medicare levy • Able to claim work related

deductions • Not assessed on fringe

benefits (but RFBA) • Not assessed on super

(retirement) (but RSC)

Liable for ….

9.5% Superannuation Guarantee (retirement)

49% Fringe Benefits Tax on benefits provided

5 - 7% Payroll Tax (?) - State

5% (up to 15%) WorkCover insurance - State

20 days AL; 10 days SL; 13 days PH & LSL?

25 – 28%

Obligations for ….

PAYG – Withholding on wages

Super payment (1/4ly) and reporting

Wages & conditions: Fair Work Act 2009

Workplace Health & Safety

Non-discrimination

Record keeping

“Contractor” consequences

Business Business/ Contractor

• Need an Australian Business Number (enterprise)

• GST (VAT) registered if turnover >$75K (£45K)

• Liable for GST (?) @10% • Taxed on amount:

• Individual: marginal rates 47% > $180,000 AUD (£105,000) + 2% Medicare levy

• Corporation: 30% (if small <$2M 28.5%; <$10 27.5%)

• Partnership: partners • Trust: beneficiaries (inc

corp b’ee) or Trustee @ 49%

• Able to claim business related deductions (loss rules)

• Optional to make own super payments (deductible)

Liable for ….

? 9.5% Superannuation Guarantee (retirement) – only if contractor (individual) providing ‘labour’ or ‘paid to perform’ (i.e. musician)’

? 5 - 7% Payroll Tax (?) – State – only if contractor (individual) providing ‘services’

Able to claim GST input tax credit

Obligations for ….

PAYG – Withholding (Optional) – Mandatory if non-ABN

Unfair Contracts: Independent Contractors Act

Workplace Health & Safety

Non-discrimination

Record keeping

Mandatory for ‘taxi travel’ suppliers to register for GST – regardless of turnover. Uber BV v FCT (2017): uberX driver was taxi travel as supplying travel that involved transporting passengers for fares.

“Contractors” & Personal Services Income

Business

Business/ Contractor

Comp;

Trust,

P’ship /

ST

‘reward for personal efforts or skill of an individual’ • would not include selling goods; • would not include granting right to intellectual

property; • would not include using income producing asset; • would not include business with substantial

assets &/ employees Tax Office concerns with Professional Firms (such as Accounting and Law) – that fall outside these rules [compared to a sole pracitioner]

2015: $2,995,669,747 (£2,000,000,000)

“Contractors” & Personal Services Income

Business

Business/ Contractor

RESULTS TEST

Is at least 75% of PSI produce to: (a) To achieve a specified result, AND (b) Supply own Plant & Equip, AND (c) Liable to rectify IF NOT THEN:

Is < 80% of PSI from 1 source AND (a) Unrelated Client Test ; OR (b) Employment Test; OR (c) Business Premises Test.

OR

Is > 80% of PSI from 1 source AND Commissioner Determination for unusual circumstances

Comp;

Trust,

P’ship /

ST

Income attributed and deductions reduced

‘reward for personal efforts or skill of an individual’

Compared with being paid per hour

7

Terms used

Income Tax Legislation (Federal):

» Employee: not defined so common law meaning. (But for withholding extended definition to include such things as directors, religious practitioners…)

» Business: includes any profession, trade, employment, vocation or calling, but does not include occupation as an employee.

» Personal Exertion Income: exertion means income consisting of earnings, salaries, wages, commissions, fees, bonuses, pensions, superannuation allowances, retiring allowances and retiring gratuities, allowances and gratuities received in the capacity of employee or in relation ….

» Personal Services Income: as ordinary or statutory income that is gained mainly as a reward for the personal efforts and skills of an individual.

8

Terms used

Fringe Benefits Tax Legislation (Federal):

» Employee: not defined. (But extended definition to include such things as directors, religious practitioners…)

» Covers employee’s associates & past, future and present employers.

GST Legislation (Federal):

» Enterprise: includes ‘business’; leasing.. but excludes ‘employee’.

9

Terms used

Superannuation Legislation (Federal):

» Employee: defined as have their “ordinary meaning” but expanded by subsections (2) to (11).

» Covers ‘deemed’ employees: such as:

a person engaged under a contract that is wholly or principally for labour (ATO: Does not extend to people operating through corporations/or trusts; & not if ‘paid to produce a result’).

person who is paid to perform or to participate in the performance of presentation …

Directors….

10

Terms used

Payroll Tax (State):

» Employee: not defined.

» Deemed employees (Qld): the person performs work in relation to which services are supplied OR gives goods to individuals for work to be performed by those individuals in respect of the goods and for the goods to be re-supplied.

WorkCover (State):

» Uses the term ‘worker’ – which is then defined as a person who works under a contract and, in relation to the work, is an employee for the purpose of assessment for PAYG withholding under the Taxation Administration Act 1953 (Cth), schedule 1, part 2-5. (s 11 of the Act).

But exclusions and additions.

11

Terms used

Fair Work Act (Federal):

» Employee: not defined – ordinary meaning (s 11).

Independent Contractors Act (Federal):

» Independent Contractor: Applies to “service contracts”, which are defined as “contracts for services”. But no definitions of: ‘employee’, ‘contractor’ or ‘contracts for services’– but not limited to natural persons.

12

Reasons for uncertainty

Mixed policy objectives by governments:

Protection of employees (and small businesses):

Labour law; Superannuation Guarantee; WorkCover

Insurance.

Tax administration ease (self assessment system):

Self Assessment; PAYG Withholding, Super Guarantee;

Fringe Benefits Tax.

Employees as a sign of wealth:

Payroll tax.

Tax arbitrage:

‘Human’ capital excluded from ‘capital’ tax concessions.

Capital income (in the traditional economic sense)

includes interest and dividend income, property rental

income, royalties, capital gains, imputed rental income of

owner-occupied housing and net business income.

An important mechanism for collecting tax, being estimated to be over $182 billion in the 2016-2017 year out of total government income tax revenue estimated to be $278 billion

13

Reasons for uncertainty

Inspector General of Taxation (2016) concluded:

That a single definition may not be possible – instead

aim for harmonisation across agencies.

Australian Taxation Office could provide a higher

degree of certainty in the form of binding advice to

workers through a Voluntary Certification System

(VCS). A VCS would, in effect, be an extension of the

existing ruling and advice framework but would be

based on information provided independently by each

party.

Uncertainty is a cost and adds to complexity, and

provides opportunity for tax arbitrage.

14

Evidence of complexity

Board of Taxation (2007) study that found that rather than

“tax” per se, the application of other regulations can

increase overall compliance cost burden, such as:

» employment issues,

» superannuation,

» occupation health and safety, and

» workplace relations legislation.

It was concluded that some of the factors that drive up

tax compliance costs for small businesses are

employment of staff, inconsistent law applying across

taxing jurisdictions and use of tax system for non-tax

measures.

15

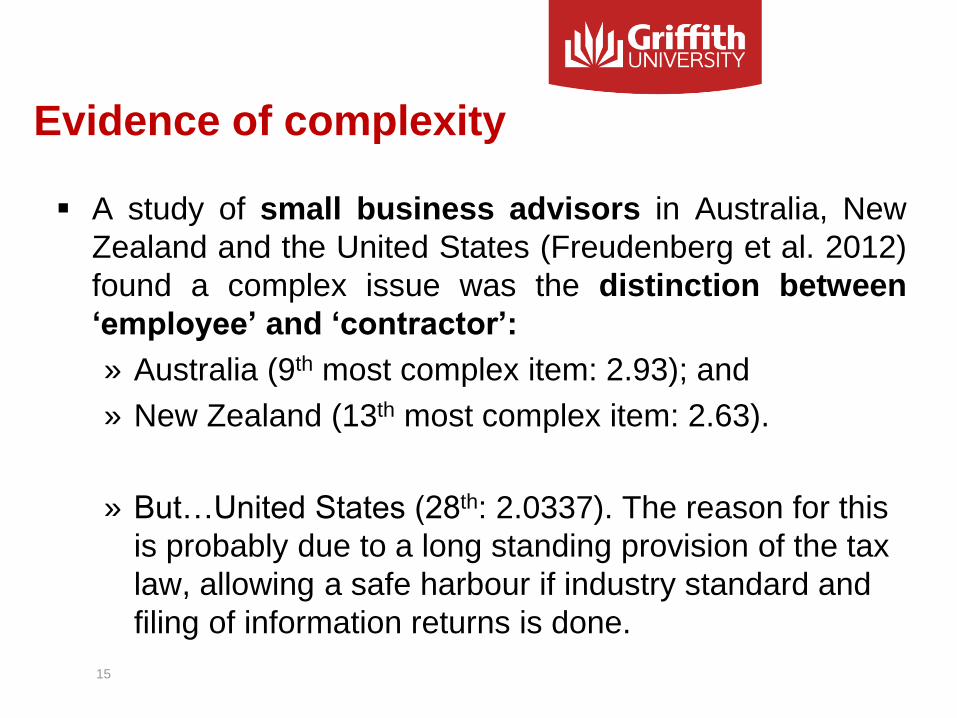

Evidence of complexity

A study of small business advisors in Australia, New

Zealand and the United States (Freudenberg et al. 2012)

found a complex issue was the distinction between

‘employee’ and ‘contractor’:

» Australia (9th most complex item: 2.93); and

» New Zealand (13th most complex item: 2.63).

» But…United States (28th: 2.0337). The reason for this

is probably due to a long standing provision of the tax

law, allowing a safe harbour if industry standard and

filing of information returns is done.

16

Evidence of complexity

Lignier et al. (2014) conducted a large-scale survey of

10,000 SME firms in Australia

Type of tax Micro

(hrs)

Small

(hrs)

Medium

(hrs)

GST 15.8 66.6 148.5

Income tax (exc CGT) 15.7 35.0 55.4

Employee withholding tax 2.4 21.4 54.5

Employee superannuation 1.4 13.2 46.2

Payroll tax 0 1.1 35.6

Total 37.5 143.6 482.2

10% 25% 28%

17

Evidence of complexity

When compared to the study by Evans et al. (1995)

twenty years earlier, evident that the time spent on

employee-related taxes has grown significantly

Type of tax Evans et al 1995 (hrs) Lignier, Evans and

Tran-Nam, 2013 (hrs)

GST NA 68.8

Income tax (exc CGT) 25.6 33.4

Employee withholding tax 6.0 35.8

Employee superannuation 3 18.6

Payroll tax 0 10.8

Total 40.1 185.4

23% 35%

18

Conclusion

It is not good for the economy if employment (and employing someone) is:

» too uncertain;

» too complex; and

» too administratively costly.

Need greater consistency and harmonisation of what is

an ‘employee’ and a re-think of how ‘human capital’

should be taxed.

Brett Freudenberg

Griffith Business School

The uncertainty, complexity and

cost of ‘employee’ status

in Australia

Any questions?

Griffith Business School