the uk nuclear market. paul lester ceo lord mandelson secretary of state for business, innovation...

Post on 22-Dec-2015

215 views

TRANSCRIPT

The UK Nuclear Market

Paul LesterCEO

Lord MandelsonSecretary of State for Business, Innovation and Skills

Q & A Session

John ChubbManaging Director, Environment

The Global Nuclear Market Today and 2014

(Source: URENCO, NDA, Areva, British Energy. UK spend includes T1 expenditure)

£2bn £12bn £2.5bn £5.5bn£3.5bn

Market:£0.25bn2009

2014

ENRICHMENTFUEL

FABRICATIONREACTOR BUILDAND SERVICES

REPROCESSINGWASTE

MANAGEMENTDECOMMISSIONING

&£0.5bn £2bn

£1.25bn £0.5bn £2.5bn

Current Business Performance

Revenue £65m

Profit contribution £4.5m

Margin 7%

Investment net of cash £33.8m

NuclearCapability Nuclear

Engineering450 engineers

Project Management

Safety Case /Specialist Consultancy

Waste Management and Characterisation

Radiometric InstrumentationDesign and through life service

Radiological Analysis

VT has a broad range of nuclear capabilities in a market where supply is becoming increasingly stretched

World Leading Capabilities

• Graphite decommissioning - support to EDF

• Programme management - support to EBRD

• Waste retrieval projects - major Sellafield projects: B29, B30

• Reprocessing technology - support to Japan Nuclear Fuel Ltd

• Radiological analysis - Sellafield & security services

Strategic Repositioning -Markets

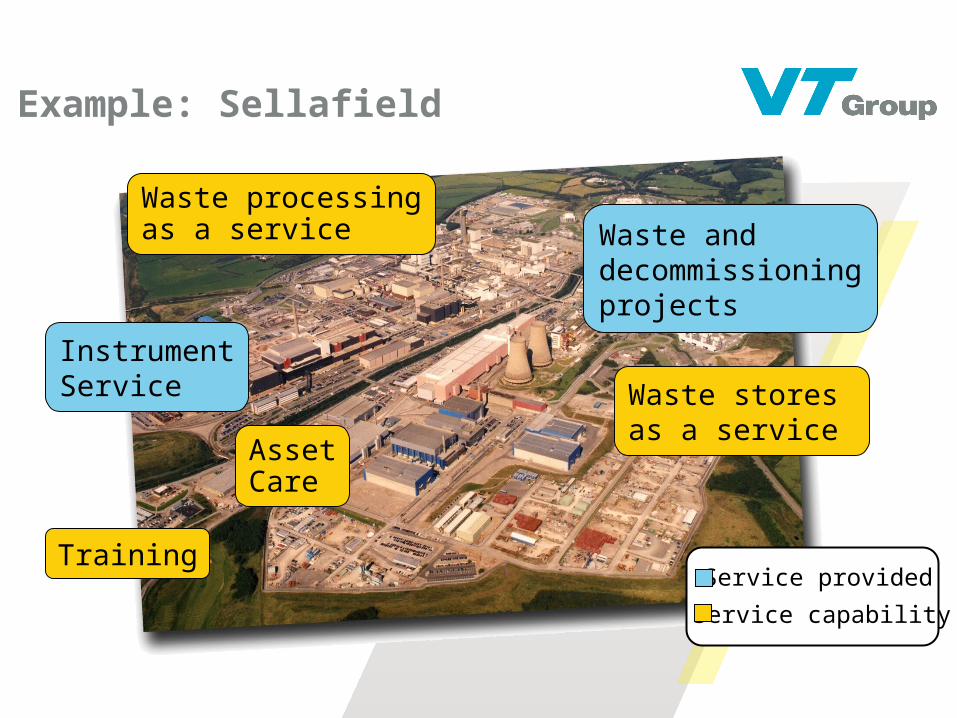

Example: Sellafield

InstrumentService

Waste processingas a service

Waste stores as a service

Waste anddecommissioningprojects

TrainingService provided

Service capability

AssetCare

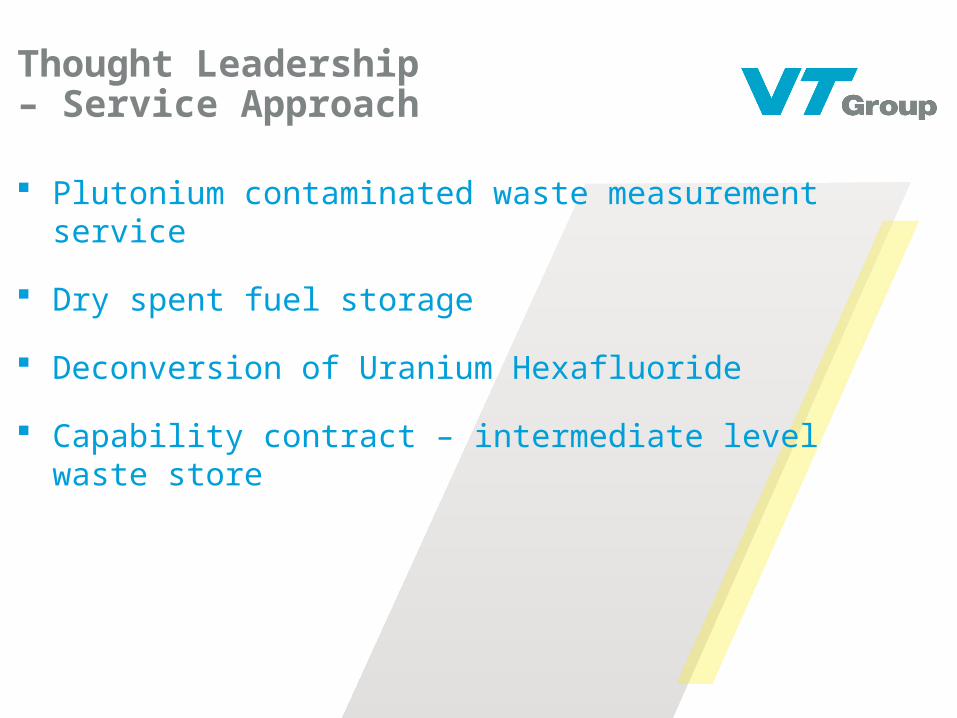

Thought Leadership – Service Approach

Plutonium contaminated waste measurement service

Dry spent fuel storage

Deconversion of Uranium Hexafluoride

Capability contract – intermediate level waste store

Where we work Dounreay

Sellafield

Hunterston

Chapelcross

Wylfa

BerkeleySizewell

Capenhurst

OldburyHinkley

Dungeness

Bradwell

LLWR DriggHartlepool

Heysham

Trawsfynydd

Harwell

Aldermaston

Torness

Major Customers

Capability Comparison

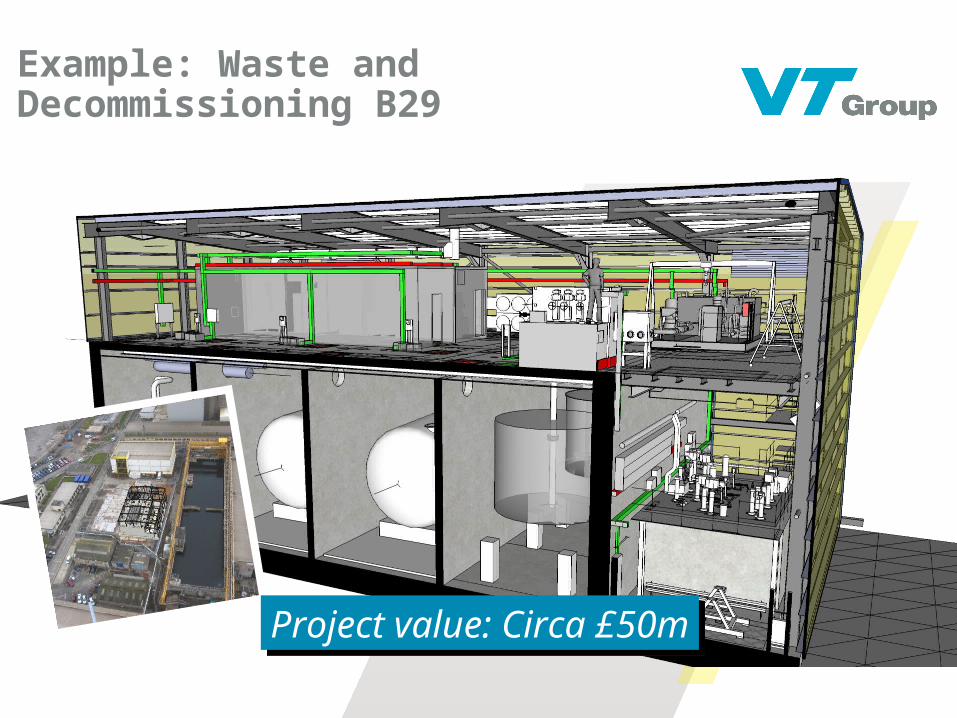

Example: Waste and Decommissioning B29

Project value: Circa £50mProject value: Circa £50m

Example: Waste and Decommissioning B29

Project value: Circa £50mProject value: Circa £50m

ProjectManagement

ConceptDesign

WasteCharacterisation

Operation

Procurement

Structure of the New Build market

International Utility, eg: EDF

Utility orReactor Vendor

Reactor Vendor eg: Westinghouse

Non-nuclearIsland

eg: Turbine

NuclearIsland

eg: Reactor

GeneralSupport

eg: Licensing

Developer

PrimeContractor

TechnologyProvider

Specialist Contractors

VT can provide supportto all of these sectors

Early Traction: NII Frameworks Reactor components Expert support to reactor

vendor Ongoing discussions with

utilities and reactor vendors

Example: New Build Opportunity

Total cost of a new build station will be in excess of £2bn per unit: ~15% is currently addressable by VT Group

Nuclear Island

£900mNon-Nuclear Island

£700m

General Support: £400mGeneral Support: £400m

Design for Decommissioning

Radwaste Plant

Engineering Validation/Inspection

Specialist Manufacturing

Source: IBM

General EngineeringSupport

Safety Case/ Environmental

Impact Assessments

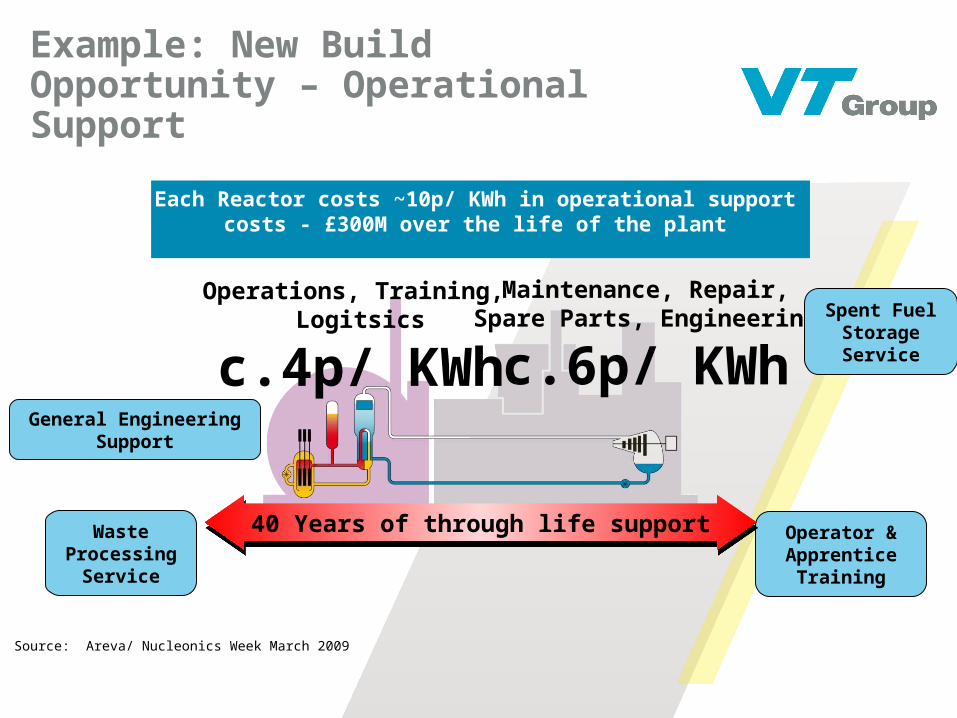

Example: New Build Opportunity – Operational Support

Each Reactor costs ~10p/ KWh in operational support costs - £300M over the life of the plant

Operations, Training, Logitsics

c.4p/ KWh

Maintenance, Repair,Spare Parts, Engineering

c.6p/ KWhGeneral Engineering

Support

Waste Processing

Service

Spent FuelStorage Service

Operator &Apprentice

Training

Source: Areva/ Nucleonics Week March 2009

40 Years of through life support40 Years of through life support

Summary

Strong nuclear engineering and technical capability

Bringing the VT Group customer-critical service delivery model to the nuclear sector

Broadening into adjacent sectors of the nuclear market with long-term potential

Positive feedback from early engagement with customers on this new approach

Q & A Session