the truth about n sel -...

TRANSCRIPT

ABOUT NSELTHE TRUTH

Issued in the Interest of Public Information by National Spot Exchange Limited (NSEL)

FEBRUARY 2015

PART-1

How Financial Technologies, which created an extensive ecosystem of exchange institutions across

Asia and Africa, is demonised and systematically demolished for payment defaults at one of its subsidiaries

owing to abrupt action by the Ministry of Consumer Affairs on the ill-advice of the Forward Markets Commission

• National Spot Exchange Limited (NSEL) came into being to fulfil a vision/aspiration of the Government to create a common Indian market for trading of commodities. NSEL has germinated out of this purpose and had been conducting its operations within this framework due to which several State Governments granted it an e-Market registration | approval under APMC Act against the backdrop of the Model APMC Act. In the five years of its functioning, NSEL has had several achievements that are mentioned subsequently in this paper.

• However, the brokers had offered a trading strategy on one of the products to the well informed, highly sophisticated, qualified and high networth traders. NSEL strongly believed that the problem that arose could have been mitigated with a more calibrated and mature response from the Forward Markets Commission (FMC) | Department of Consumer Affairs (DCA) in the Ministry of Consumer Affairs, and had the FMC/DCA not acted in a manner that ultimately proved detrimental to the prospects of a common market, but also the potential of NSEL to play a much more meaningful role.

• The outcome of the sudden and abrupt action by the DCA has been extremely destructive that led to huge erosion of value and prospects of further development of spot exchanges in the country and will prove to be a major deterrent in creation of a national agricultural market. For NSEL it has been extremely painful. The share of the problem were put entirely on NSEL's parent company FTIL while the FMC | DCA chose to overlook the role and contribution of other players and instead focused only on FTIL, with a wide range of punitive actions, penalties and punishment.

• It is this unfair treatment that compelled NSEL to communicate with the wider public on various issues leading to the problem at NSEL and developments thereafter.

• The Paper explains the NSEL's point of view on various aspects regarding the problem. It also articulates the concerns of its parent company FTIL, which has faced unnecessary pain and punishment for no fault of it. Moreover, the 63000 shareholders of FTIL are being made the scapegoat for the sins of others. The information used in the preparation of this Paper is drawn from NSEL as also from FTIL, wherever it was found relevant and required.

• FTIL, however, is not associated with any aspect of the paper and thus not responsible for any points of view made in this Paper.

Pg 2

Pg 3

ABOUT NSELTHE TRUTH

How Financial Technologies, which created an extensive ecosystem of exchange institutions across

Asia and Africa, is demonised and systematically demolished for payment defaults at one of its subsidiaries

owing to abrupt action by the Ministry of Consumer Affairs on the ill-advice of the Forward Markets Commission

Conspiracies that undermine the importance of institutions might sub serve the vested interests of a few, but will compromise the value that could belong to the majority including the nation as a whole. Discrimination against institutions by way of bias, unfair treatment, undue harassment and punishment could only dent and adversely affect the prospects for sustained growth that could otherwise add strength to the nation’s value. What could be solved through a collective approach, if distorted and subjected to undue pressures and penalties could undermine the nation’s interests in more than one way. Financial Technologies Group, despite its stellar contributions to the growth of Indian financial markets, has been subjected to a series of stringent actions in the last one and half years depriving it the due share for its utmost commitment in creating the state of the art financial market infrastructure that India can take pride in.

FTIL had the distinction of perhaps the fastest growing financial infrastructure group with exchanges spread across multiple geographies. It stood the scrutiny of stringent regulation of major international financial centers in which the group established exchanges. In a short time of less than a decade, it made Indian exchanges stand among the top league of global exchanges. The innovations in exchange development made by the FTIL group have become case studies for authorities planning similar development endeavors and strategies in several other emerging markets.

All this was wasted by certain people working for narrow interests, waiting for a minor accident to happen that they could turn into a major crisis and take this as an alibi to launch a massive assault against the Financial Technologies Group. An accident that happened at NSEL, arising from sudden stoppage of further issuance of certain commodity trading contracts by the regulatory authorities, that were made popular by brokers for their sophisticated and well informed traders and clients. In a similar situation anywhere in the world, regulatory institutions extend support including temporary liquidity provision as may be required to overcome the crisis. India too witnessed such support to institutions in the aftermath of the global financial crisis. Whereas in the case of NSEL/FTIL, it was like vengeance unleashed by certain officials with rash actions and harsh punishments, when the investigations were still going on and certain key issues were under consideration of the courts. Launch of investigations by multiple agencies, prescription of a series of punitive actions, subjecting the group executives to punishments and vilification campaigns in the public platforms to sully and destroy the image of the Group which through hard work, dedication and commitment created huge market infrastructure and ecosystem in India.

Who benefited from all this? Only the egos of a couple of officials, who were keen to destroy the group. But the claims of traders and clients remained unsettled. The recovery efforts which could have been given a big push as a collaborative endeavor are solely left to NSEL to deal with. Thousands of people who were depending on the group directly or indirectly lost jobs and incomes. The punitive actions and punishments directed against the promoters and key officials of the group have further eroded its ability to quickly respond and recover. The market activity greatly diminished. The opportunities for growth greatly marginalized. Ultimately, it is the nation that lost a great deal at the cost of keeping a couple of officials happy.

Can India afford such officials who could undermine national interest? How history will consider their actions is yet to be decided, but destroying value in pursuit of protecting the limited interests of a few competitors and in this process destroying the ability and capability of others will surely cost the nation a great deal.

It is time to reflect on what the country needs, who can deliver it and how certain people can make it vulnerable. And also how to protect Indian financial system from vested interests.

The Danger from Discrimination

Pg 4

THE CONTOURS OF A CONSPIRACYDECEMBER 19, Dr. K. P. Krishnan (KPK), the then joint secretary in the Union Ministry of Finance (MoF), had recommended that two state-owned institutions LIC and Nabard should be asked to divest their stakes in NCDEX (a rival of MCX) in favour of NSE (a private sector company) so that NCDEX can provide "credible competition" to MCX (ANX-1). The decision was questioned by MCX in a complaint to DCA in July 2012 (ANX-2). "it is because of this complaint that KPK all along had a personal vendetta against the group companies" the NSEL affidavit submitted to the Mumbai High Court Challenging the Ministry of Corporate Affairs draft proposal for the merger of NSEL with FTIL mentions.

FTIL sets up MCX-SX as the third national stock exchange in India. It began with trading in currency futures and applied for full licence to commence trading in equities/bonds/and other approved market segments. Till MCX-SX began operations, currency trading, volumes in India were meager. With MCX-SX currency trading volumes in the country began to increase. The rival exchange adopted zero pricing for transactions in currency futures that deprived the new exchange (i.e. MCX-SX) of any revenue. MCX-SX had to seek the intervention of Competition Commission of India to redress its grievance that ultimately led to the rival exchange having to face penalty for unfair pricing practices by the Commission. Later MCX-SX application for stock market segments was rejected by the SEBI. MCX-SX had to seek the intervention of the Bombay High Court to obtain licence to trade in equity markets segments.

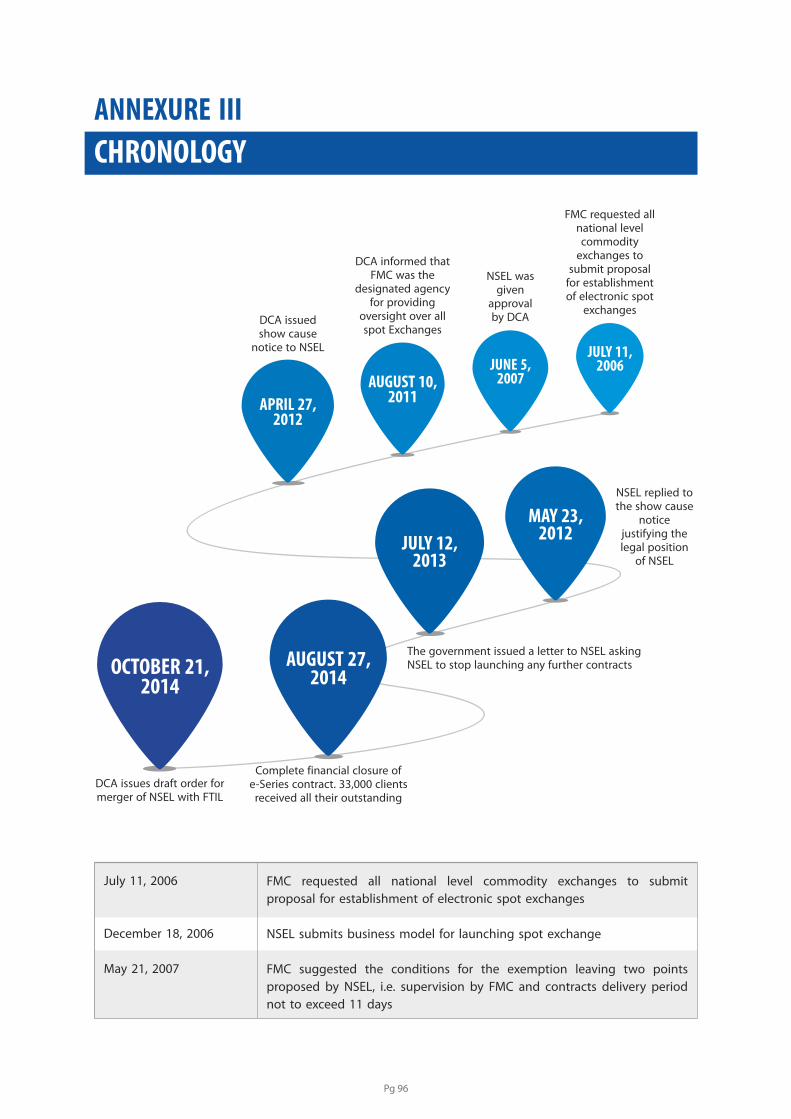

• APRIL 27: Department of Consumer Affairs issued a show cause notice to NSEL on certain aspects of its operation (ANX-3).

• MAY 23: NSEL responded to the notice promptly by its reply dated May 23, 2012 (ANX-4) and made further follow up on the response to the DCA again on August 11, 2012 (ANX-5).

• There was no reply or action from the Department of Consumer Affairs for more than a year, which is believed to have been satisfied on the issues raised in the notice.

• OCTOBER 3: NSEL issued communication to all members with copy of same posted on company website giving details of communication received from the DCA and replies given by NSEL (ANX-6).

• MAY 13: FMC wrote to DCA specifying the penalties that can be imposed under FCRA for violation of provision of FCRA. However, no penalty was ever levied on NSEL (ANX-7).

• JULY 12: Department of Consumer Affairs issued a letter to NSEL to stop issuing fresh contracts. Such a letter which should have been held in utmost confidence between two institutions was leaked to the press (ANX-8).

• JULY 12 AND 22: NSEL wrote to Department of Consumer Affairs on July 12, 2013 (ANX-9) and July 22, 2013 (ANX-10) stating that any abrupt and sudden measures of stoppage of contracts would severely dislocate and disintegrate the market functioning that could adversely affect the payment obligations.

• JULY 19: FMC wrote to DCA that the exemption granted to NSEL was silent whether the exemption is applicable to all or specific provisions of the FCRA, thus, impliedly endorsing the legality of NSEL’s contracts (ANX-11). This dispels the view expressed by the former Finance Minister that business at NSEL was illegal.

• JULY 31: All exchange operations of NSEL had to be stopped due to the panic created in the market by the DCA’s action (ANX-12).

• AUGUST 4: FMC had a meeting with the defaulters about the stocks in position and payment obligations and received positive confirmation from them to the material and money involved (ANX-13).

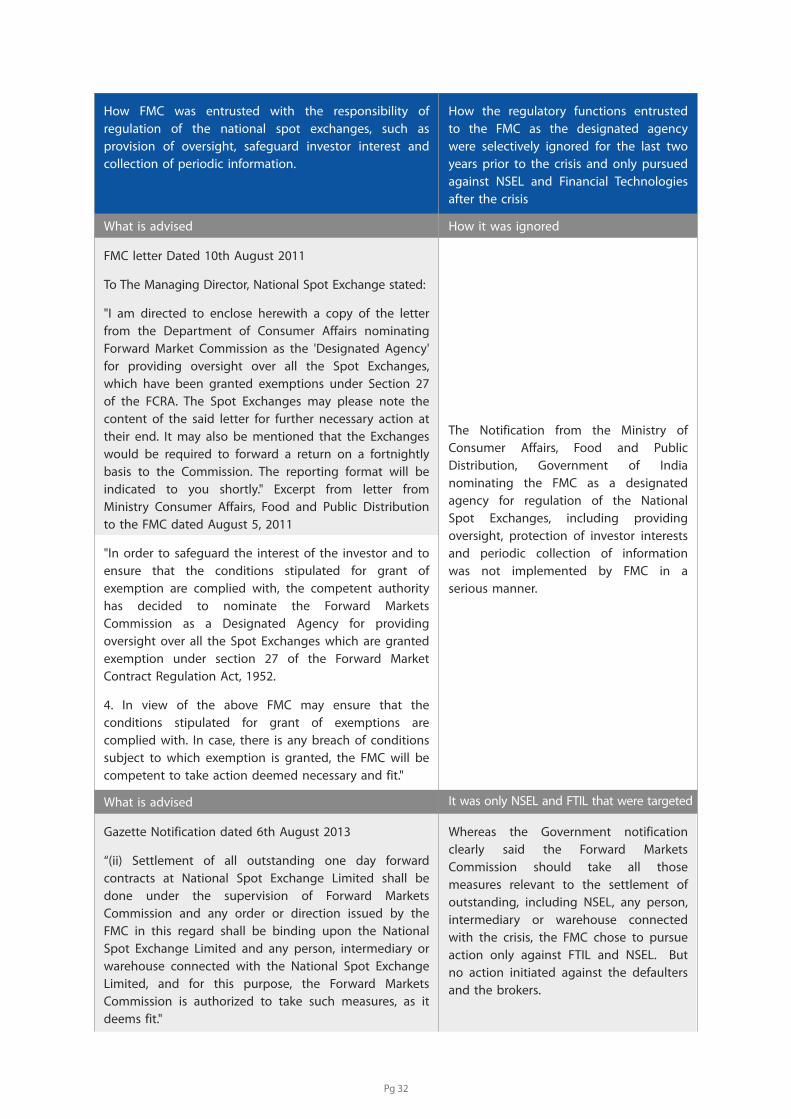

• AUGUST 6: DCA authorized FMC to take such measures as deemed fit against “any person, intermediary or warehouse connected with NSEL” (ANX-14). Whereas the entire focus and action of FMC since then has been solely directed against FTIL | NSEL conveniently ignoring the other players i.e. the Defaulters & brokers.

• AUGUST 12: FMC wrote to DCA stating there is an urgent need to secure the warehouse stocks and verify their quantity and quality (ANX-15). However, no required actions were taken in this regard by FMC later on.

• DECEMBER 17: FMC declares FTIL as unfit to hold more than 2% equity in a recognized commodities exchange in India thus forcing FTIL to reduce its stakes in MCX from 26 percent to 2 percent.

• AUGUST 18: Regulator FMC recommended the Government to consider merger of the spot commodity exchange with its promoter FTIL, followed by a second recommendation on October 17, 2014.

• SEPTEMBER 19: GOI issued notification withdrawing exemptions given under Section 27 of FCRA to NSEL and other spot exchanges (ANX-16). The notification said that the exemption of June 5, 2007 was from the operation of the provisions of the said Act, thereby confirming NSEL stand that it is a general exemption from the Act.

• OCTOBER 21: The Centre announced the NSEL would have to merge with its holdings company, FTIL. The Ministry of Corporate Affairs issued a draft order invoking Section 396 of the Companies Act for the merger.

• NOVEMBER 13: FTIL challenges the Government order.

2007

2008

-10

2012

2013

2014

Pg 5

THE TRUTH ABOUT NSEL: A PRIMER

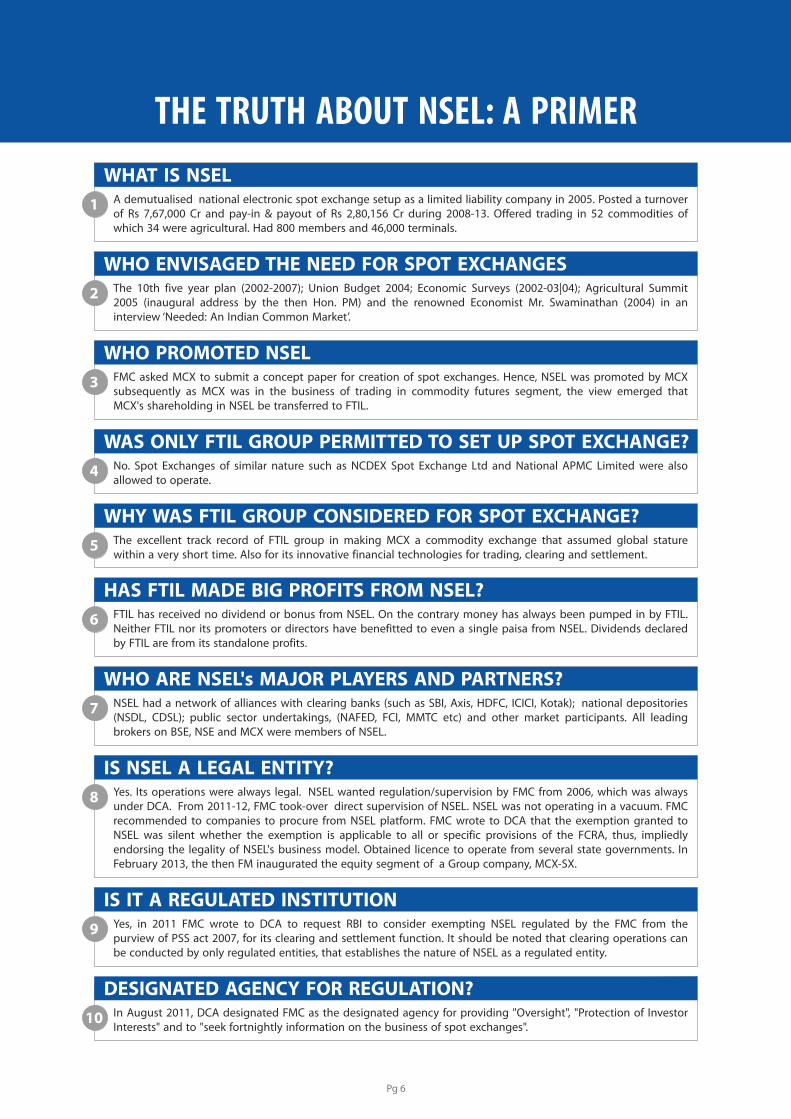

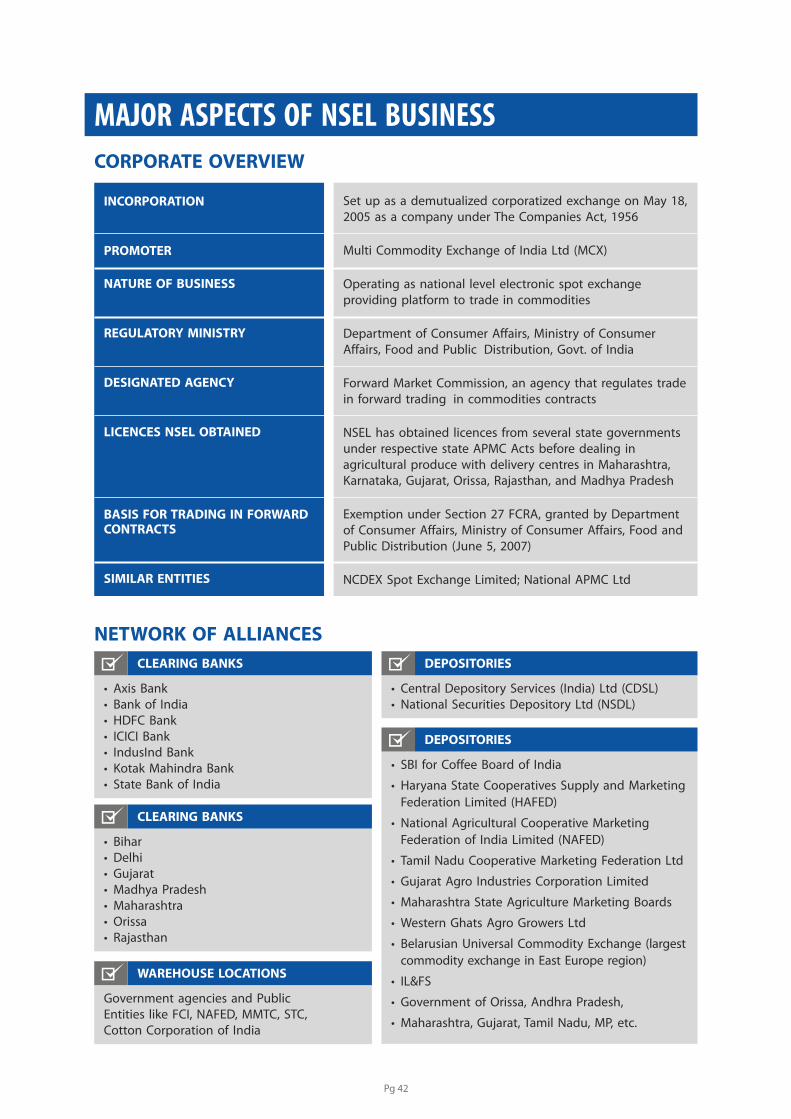

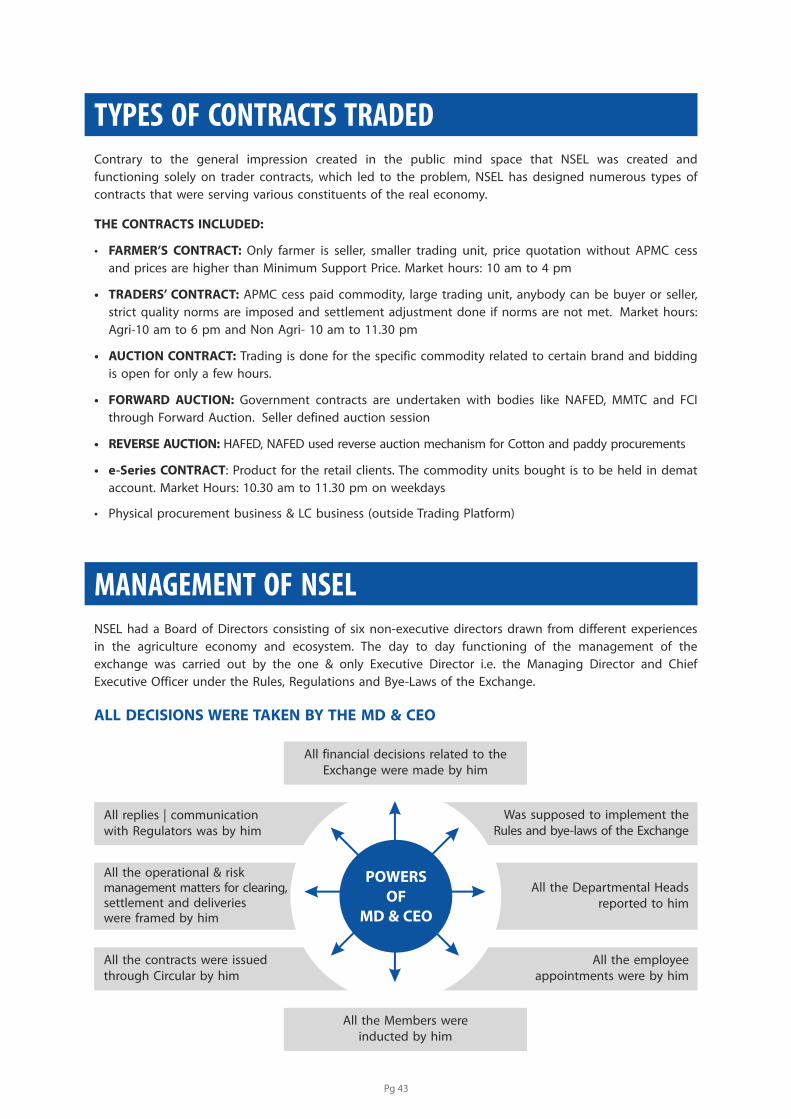

WHAT IS NSELA demutualised national electronic spot exchange setup as a limited liability company in 2005. Posted a turnover of Rs 7,67,000 Cr and pay-in & payout of Rs 2,80,156 Cr during 2008-13. Offered trading in 52 commodities of which 34 were agricultural. Had 800 members and 46,000 terminals.

1

WHO ENVISAGED THE NEED FOR SPOT EXCHANGESThe 10th five year plan (2002-2007); Union Budget 2004; Economic Surveys (2002-03|04); Agricultural Summit 2005 (inaugural address by the then Hon. PM) and the renowned Economist Mr. Swaminathan (2004) in an interview ‘Needed: An Indian Common Market’.

2

WHO PROMOTED NSELFMC asked MCX to submit a concept paper for creation of spot exchanges. Hence, NSEL was promoted by MCX subsequently as MCX was in the business of trading in commodity futures segment, the view emerged that MCX's shareholding in NSEL be transferred to FTIL.

3

WAS ONLY FTIL GROUP PERMITTED TO SET UP SPOT EXCHANGE?No. Spot Exchanges of similar nature such as NCDEX Spot Exchange Ltd and National APMC Limited were also allowed to operate.

4

WHY WAS FTIL GROUP CONSIDERED FOR SPOT EXCHANGE?The excellent track record of FTIL group in making MCX a commodity exchange that assumed global stature within a very short time. Also for its innovative financial technologies for trading, clearing and settlement.

5

HAS FTIL MADE BIG PROFITS FROM NSEL?FTIL has received no dividend or bonus from NSEL. On the contrary money has always been pumped in by FTIL. Neither FTIL nor its promoters or directors have benefitted to even a single paisa from NSEL. Dividends declared by FTIL are from its standalone profits.

6

WHO ARE NSEL's MAJOR PLAYERS AND PARTNERS?NSEL had a network of alliances with clearing banks (such as SBI, Axis, HDFC, ICICI, Kotak); national depositories (NSDL, CDSL); public sector undertakings, (NAFED, FCI, MMTC etc) and other market participants. All leading brokers on BSE, NSE and MCX were members of NSEL.

7

IS NSEL A LEGAL ENTITY?Yes. Its operations were always legal. NSEL wanted regulation/supervision by FMC from 2006, which was always under DCA. From 2011-12, FMC took-over direct supervision of NSEL. NSEL was not operating in a vacuum. FMC recommended to companies to procure from NSEL platform. FMC wrote to DCA that the exemption granted to NSEL was silent whether the exemption is applicable to all or specific provisions of the FCRA, thus, impliedly endorsing the legality of NSEL's business model. Obtained licence to operate from several state governments. In February 2013, the then FM inaugurated the equity segment of a Group company, MCX-SX.

8

IS IT A REGULATED INSTITUTIONYes, in 2011 FMC wrote to DCA to request RBI to consider exempting NSEL regulated by the FMC from the purview of PSS act 2007, for its clearing and settlement function. It should be noted that clearing operations can be conducted by only regulated entities, that establishes the nature of NSEL as a regulated entity.

9

DESIGNATED AGENCY FOR REGULATION?In August 2011, DCA designated FMC as the designated agency for providing "Oversight", "Protection of Investor Interests" and to "seek fortnightly information on the business of spot exchanges".

10

Pg 6

THE TRUTH ABOUT NSEL: A PRIMER

HOW NSEL COMPLIED WITH REGULATIONSince November 2011, NSEL provided fortnightly information to FMC as prescribed including details of commodity stocks. Replied to all communications from the DCA | FMC from time to time.

11

WHAT IS THE NATURE OF ACCIDENT THAT HAPPENED AT NSEL?DCA | FMC abruptly stopped NSEL from further issuance of fresh contracts. Sudden and rash measures led to migration of commodities. NSEL not given any regulatory support to address the issue.

12

THE GENESIS OF THE PROBLEM Creation of structured products by brokers for buying and selling of commodities followed by aggressive marketing. Lower returns in stock markets in 2011 | 12 induced the brokers to focus more on such contracts to derive revenue and returns.

13

ARE FTIL AND THE BOARD OF NSEL RESPONSIBLE?FTIL, its board or the Board of NSEL is not even remotely connected with any of the brokers, clients or traders. No red flags raised either by the auditors of the NSEL or of the brokers or of the PSUs or by FMC or the brokers who visited warehouses more than 50 times.

14

HAS NSEL CREATED ANY SYSTEMIC CRISIS?Reports of the RBI | Government reiterated that there is no systemic crisis from the NSEL problem. The clients were sophisticated, well informed of high net worth and they were buying and selling commodities as a part of business and booking income accordingly.

15

THE UNIVERSE OF CLIENTS AFFECTEDClaims of 33000 e-Series clients settled successfully. 7000 clients with claims exposure below Rs 10 lakh received 50% of the total settlement. 7 defaulters own upto 85% of the claim amount. NSEL has privity of contract with only 71 brokers. Only 6% of the clients account for 69% of the claim.

16

IMMEDIATE RESPONSE OF NSEL | FTILFTIL provided without prejudice a loan of Rs 179 cr to NSEL to pay the dues of small trading clients. Changed the management of NSEL and reconstituted its Board. It is extending legal, financial, infrastructure, personnel support to NSEL. Extending complete cooperation to the authorities.

17

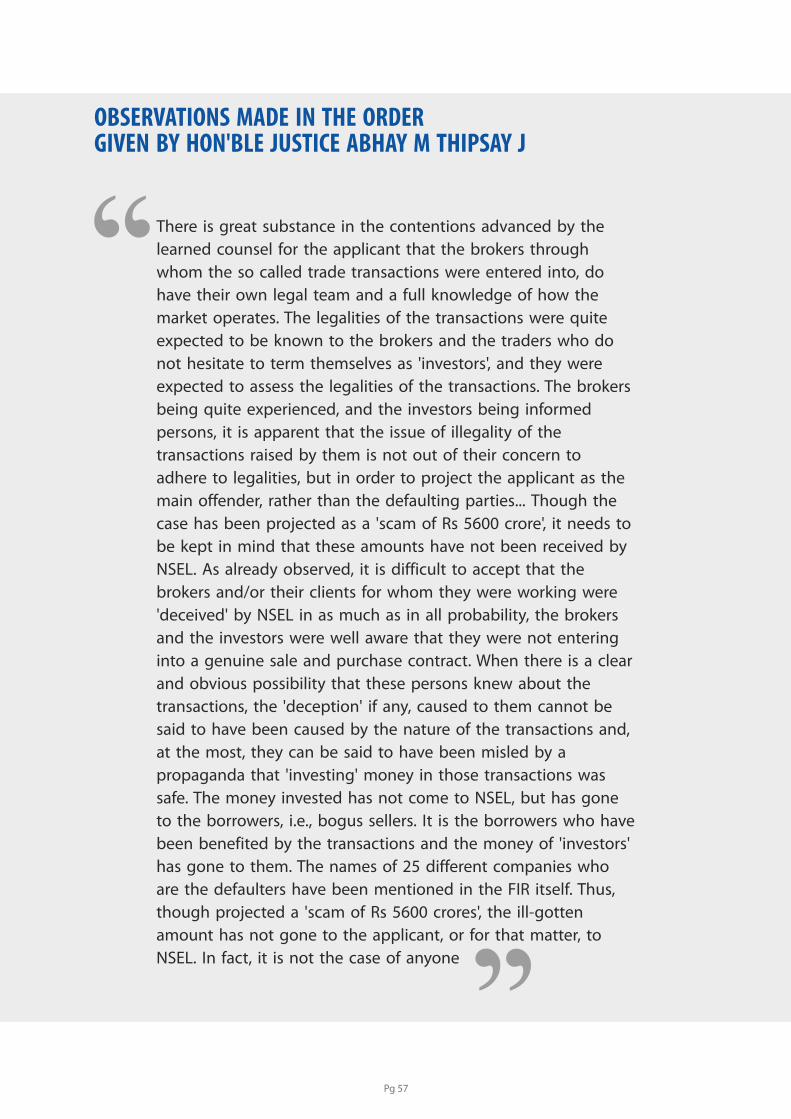

WHAT IS THE JUDICIAL VIEW ON AFFECTED CLIENTS?"The legalities of the transactions were quite expected to be known to the brokers and traders... The brokers were quite experienced... It is difficult to accept that the brokers and their clients were deceived by NSEL" -High Court of Mumbai in its order dated 22-08-2014.

18

IS THERE ANY CONSPIRACY BEHIND THE PROBLEM There is a defined plan of action as evident abundantly in the execution to undermine the image of the FTIL and sabotage its reputation and future growth to favour competition. (See the next page)

19

HOW THE CONSPIRACY WAS PLANNEDDCA | FMC issued a show cause notice to NSEL in April 2012. NSEL promptly responded in May 2012 and followed up in August 2012. No action from DCA | FMC for over a year. No order issued to the show cause. Through a letter in July 2013 DCA | FMC ordered stoppage of issuance of fresh contracts that led to suspension of trading.

20

Pg 7

HOW A FAST GROWING FINANCIAL INFRASTRUCTURE GROUP FROM INDIA IS DEMOLISHED AND DESTROYED BY

THE CONSPIRACY OF A FEW VESTED INTERESTS

WHO ACCENTUATED THE PROBLEMDCA | FMC with abrupt actions. Brokers by mis-selling. Defaulters by diverting stocks after the problem broke out. Auditors of brokers who inspected the stocks several times failed to raise red flags. Field level functionaries of NSEL for lack of due diligence. Misinformation campaigns by vested interests.

21

FORCES BEHIND THE CONSPIRACYCertain officials including the erstwhile Additional Secretary, DEA, MOF; the Chairman, FMC who thwarted orderly management of the problem by NSEL | FTIL by rash measures, while the investigations were still on, that further deepened the extent of the problem.

22

HOW THE GLOBAL REGULATORS ADDRESSED MARKET ACCIDENTSThe financial crisis of 2008 witnessed accidents of much larger scale and dimension but regulators showed great maturity and restraint in not destroying the ecosystem and ensured recovery of markets in an orderly manner.

23

WHAT HAS BEEN THE APPROACH OF INDIAN REGULATORSSudden and abrupt measures. Weakening of the institutions. No focus on recovery. No collaborative effort. Rash and damaging measures. Target only one group leaving the real offenders untouched.

24

IMPACT OF THE APPROACH OF GLOBAL REGULATORSThe markets recovered soon and so the institutional strength. Institutions in problem were given support that made resolution quicker. Institutions were given various types of support to overcome the crisis and resume growth.

25

THE IMPACT OF THE APPROACH OF INDIAN REGULATORSMarket has lost severely. Institutions that reached global league tables lost the privilege and position. Market momentum has diminished. Severe doubts and questions on the integrity of regulators and its approach have been raised.

26

HAS THE NATION BENEFITTED ANYTHING FROM THE OUTCOME?The nation as a whole suffered huge loss in its march towards emerging as a global player in multi-asset-class exchanges, as also bringing financial inclusion through spread of markets.

27

HAS THE MARKET BENEFITTED ANYTHING FROM THE OUTCOME? India lost its sheen as the most promising country with innovations in exchange infrastructure that FTIL pioneered and promoted in last two decades.

28

WHAT MESSAGE HAS IT SENT TO ENTERPRISES?Response mechanism to crisis tend to be biased, not planned properly, abrupt and sudden and targeting a few leaving untouched others who have played a major role in the problem.

29

WHAT MESSAGE HAS IT SENT TO GLOBAL MARKETS?Lack of maturity in dealing with complex problems. Biased and vindictive approach of penalizing without any efforts towards market recovery or client protection. Resort to measures inconsistent with global corporate laws.

30

Pg 8

HOW A FAST GROWING FINANCIAL INFRASTRUCTURE GROUP FROM INDIA IS DEMOLISHED AND DESTROYED BY

THE CONSPIRACY OF A FEW VESTED INTERESTS

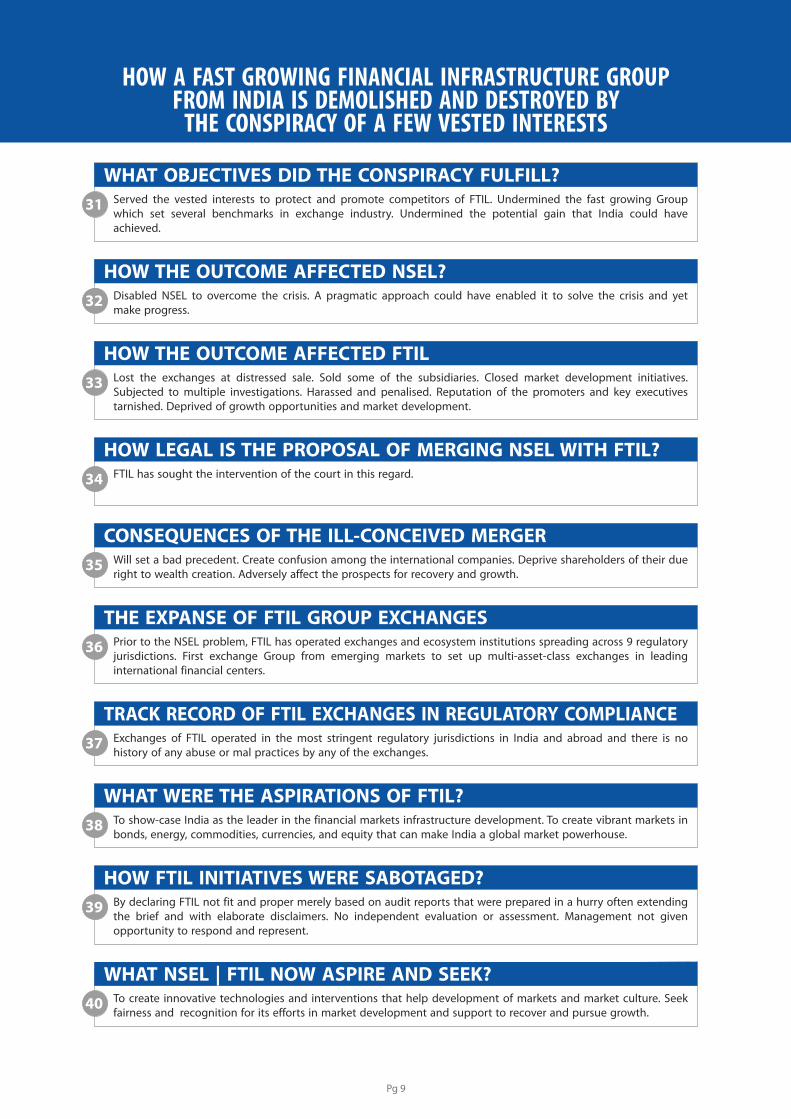

WHAT OBJECTIVES DID THE CONSPIRACY FULFILL?Served the vested interests to protect and promote competitors of FTIL. Undermined the fast growing Group which set several benchmarks in exchange industry. Undermined the potential gain that India could have achieved.

31

HOW THE OUTCOME AFFECTED NSEL?Disabled NSEL to overcome the crisis. A pragmatic approach could have enabled it to solve the crisis and yet make progress.

32

HOW THE OUTCOME AFFECTED FTILLost the exchanges at distressed sale. Sold some of the subsidiaries. Closed market development initiatives. Subjected to multiple investigations. Harassed and penalised. Reputation of the promoters and key executives tarnished. Deprived of growth opportunities and market development.

33

HOW LEGAL IS THE PROPOSAL OF MERGING NSEL WITH FTIL?FTIL has sought the intervention of the court in this regard. 34

CONSEQUENCES OF THE ILL-CONCEIVED MERGERWill set a bad precedent. Create confusion among the international companies. Deprive shareholders of their due right to wealth creation. Adversely affect the prospects for recovery and growth.

35

THE EXPANSE OF FTIL GROUP EXCHANGESPrior to the NSEL problem, FTIL has operated exchanges and ecosystem institutions spreading across 9 regulatory jurisdictions. First exchange Group from emerging markets to set up multi-asset-class exchanges in leading international financial centers.

36

TRACK RECORD OF FTIL EXCHANGES IN REGULATORY COMPLIANCEExchanges of FTIL operated in the most stringent regulatory jurisdictions in India and abroad and there is no history of any abuse or mal practices by any of the exchanges.

37

WHAT WERE THE ASPIRATIONS OF FTIL?To show-case India as the leader in the financial markets infrastructure development. To create vibrant markets in bonds, energy, commodities, currencies, and equity that can make India a global market powerhouse.

38

HOW FTIL INITIATIVES WERE SABOTAGED?By declaring FTIL not fit and proper merely based on audit reports that were prepared in a hurry often extending the brief and with elaborate disclaimers. No independent evaluation or assessment. Management not given opportunity to respond and represent.

39

WHAT NSEL | FTIL NOW ASPIRE AND SEEK?To create innovative technologies and interventions that help development of markets and market culture. Seek fairness and recognition for its efforts in market development and support to recover and pursue growth.

40

Pg 9

The Dangers from DiscriminationThe Contours of A ConspiracyThe Truth About NSEL: A Primer

Distinction of Pioneering and Path-Breaking Contribution to Indian Financial Market

NSEL is committed to Expedite Recovery from the Defaulters, to Resolve the Crisis

Overlooking Principles of Fairness to Unjustly Punish the Financial Technologies Group

Abrupt Stoppage of Contracts by DCA | FMC

WHY THIS PAPER?

FINANCIAL TECHNOLOGIES

OUR PRIORITY

PRINCIPLES AND PRACTICE

THE BEGINNING AND THE BUSINESS OF NSEL

THE CAUSE OF THE CRISIS

The Real Picture on the Background of the Crisis

The PioneerThe Path-Breaking ContributionThe Spin-Off Effects of the Financial Technologies GroupAn Exchange Industry MNC from IndiaDistinctionsExtensive EcosystemNSEL CrisisRising to the ChallengeSubjected to Unfair TreatmentLooking Ahead

A Positive Action from the FMC could have led to a Productive Outcome

If it is a Private Market Problem, Why Excessive Regulatory Zeal?Regulation: Can be it Discretionary or should it be Mandatory?Unfair Comparison with Earlier CrisesPuzzling Attitude of Pick and ChooseQuestionable Application of 'Fit and Proper’FTIL is the VictimThe Money TrailShould a Payment Crisis only Lead to Closing Down of the Exchange?Why the Approach Needs to ChangeAvoid Measures that could be Counter-Productive

ExemptionsThe Business of NSELMajor Aspects of NSEL BusinessTypes of Contracts TradedManagement of NSELOrganisational ChartNSEL: The Bright Side

FMC | DCABrokersManagementMisconception that NSEL was set up to defraud peopleMissing Stocks: How it could have Happened?Role of Employees

14

16

17181819202121222223

24

28

456

30

31313333343535363737

3841414243434444

48

495050525454

1

3

4

5

2

CONTENT

Pg 10

68

69

82

83

88

8990

92

70

58

6061626364646566

74

777778808080

949596

100102104106

5456

6

7

8

9

10

11

12

13

No Red Flags to The BoardBrokers and Trading Clients

The Multiple of Audits...and the AberrationsWhat is Good Regulation?Designated AgencyPoints of Contact and CommunicationThe Show Cause to NSELThe NSEL ReplyTaking a Partisan View

A Mature Way of Solving the Crisis

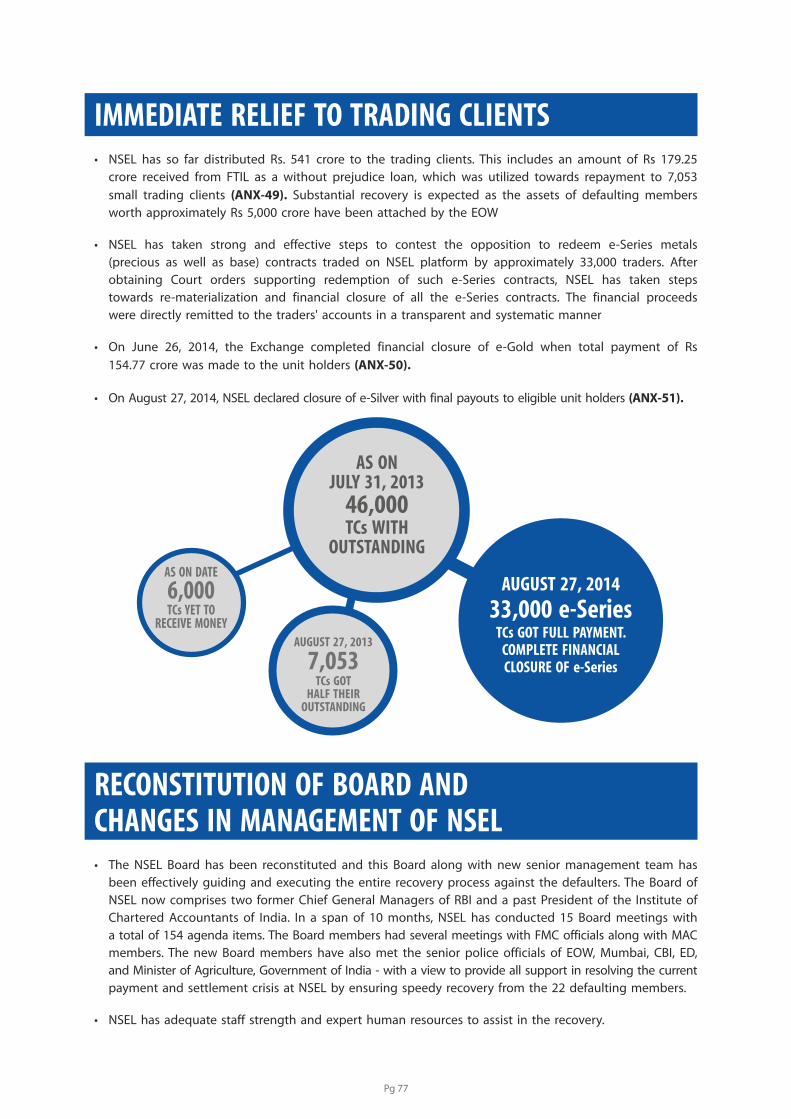

Immediate Relief to Trading ClientsReconstitution of Board and Changes in Management of NSELOther Efforts towards RecoveryComplete Cooperation to Investigating AgenciesPeriodic Briefings to Government and Regulatory AuthoritiesRecovery Efforts and Pursuing Defaulters

NSEL Responses to Specific Comments of the Chairman, FMC

Why Merger Should Not Be Allowed to HappenSupersession of Management: Depriving Due Credit

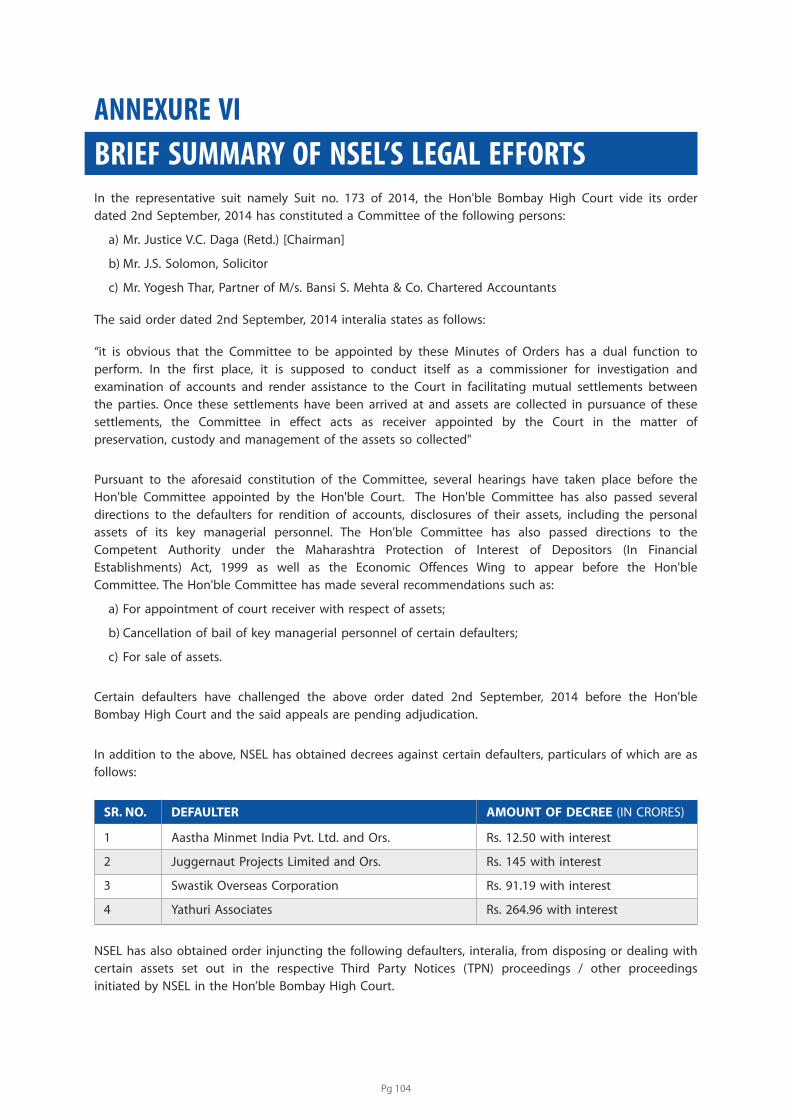

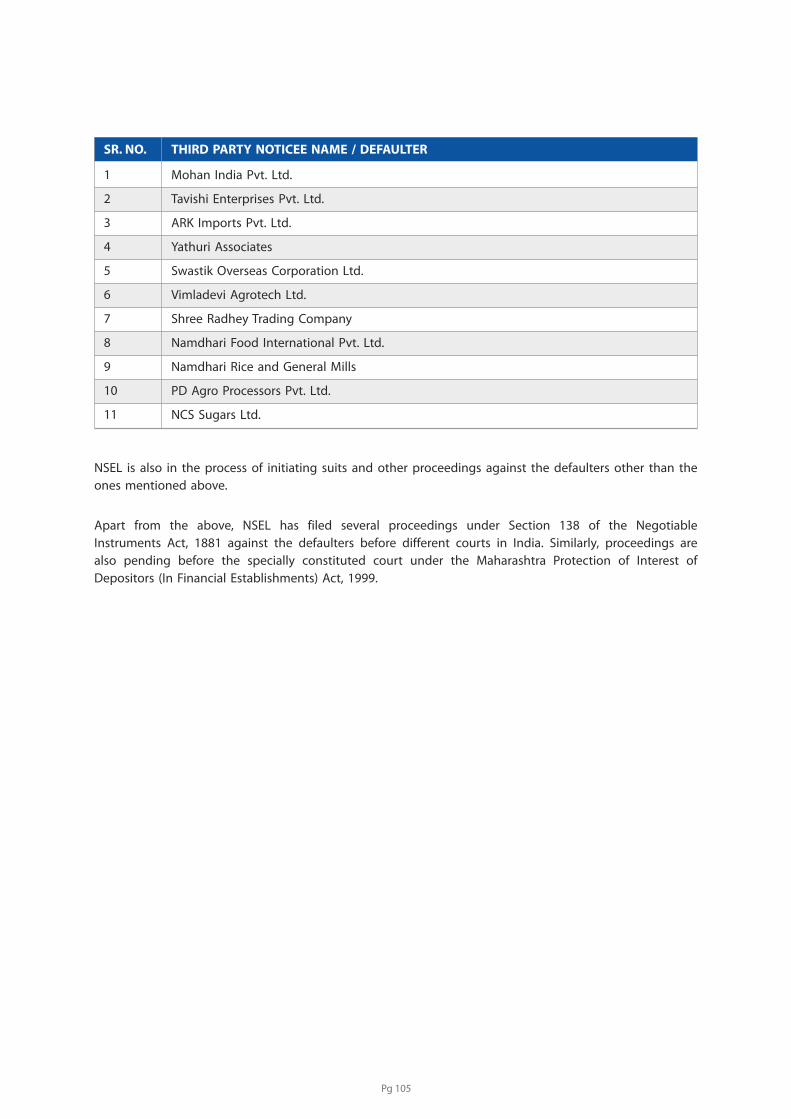

Contracts In Dispute: Settlement Defaults at NSEL: What really happened?Delivery ProcessChronologyGuidelines for Members for Conduct of BusinessRecovery Efforts by NSELBrief Summary of NSEL's legal effortsAn Unhealthy Misinformation and Misunderstanding: How NSEL Crisis was Misinterpreted and Misunderstood

SHORTCOMINGS OF THE REGULATOR

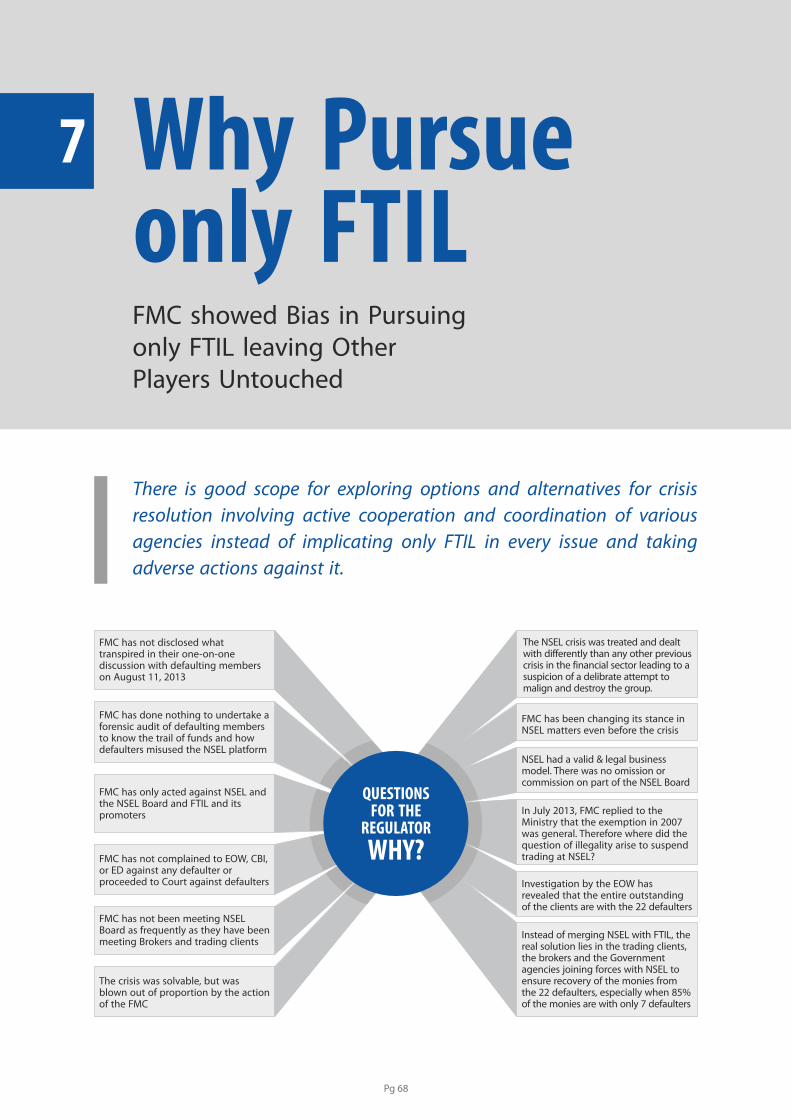

WHY PURSUE ONLY FTIL

APPROACH OF OTHER REGULATORS

NSEL CLARIFIES

CONTESTABLE PROPOSALS

LOOKING BACK

ANNEXURE

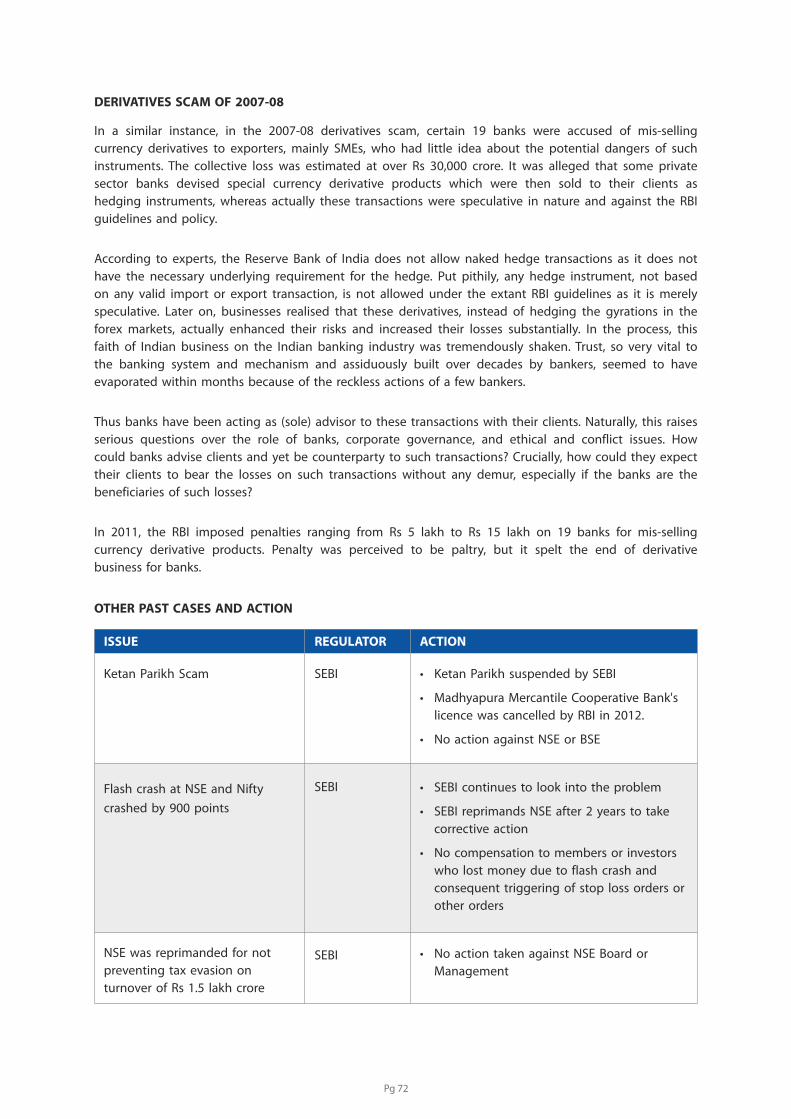

Failures of Regulatory Agency

FMC showed Bias in Pursuing only FTIL leaving Other Players Untouched

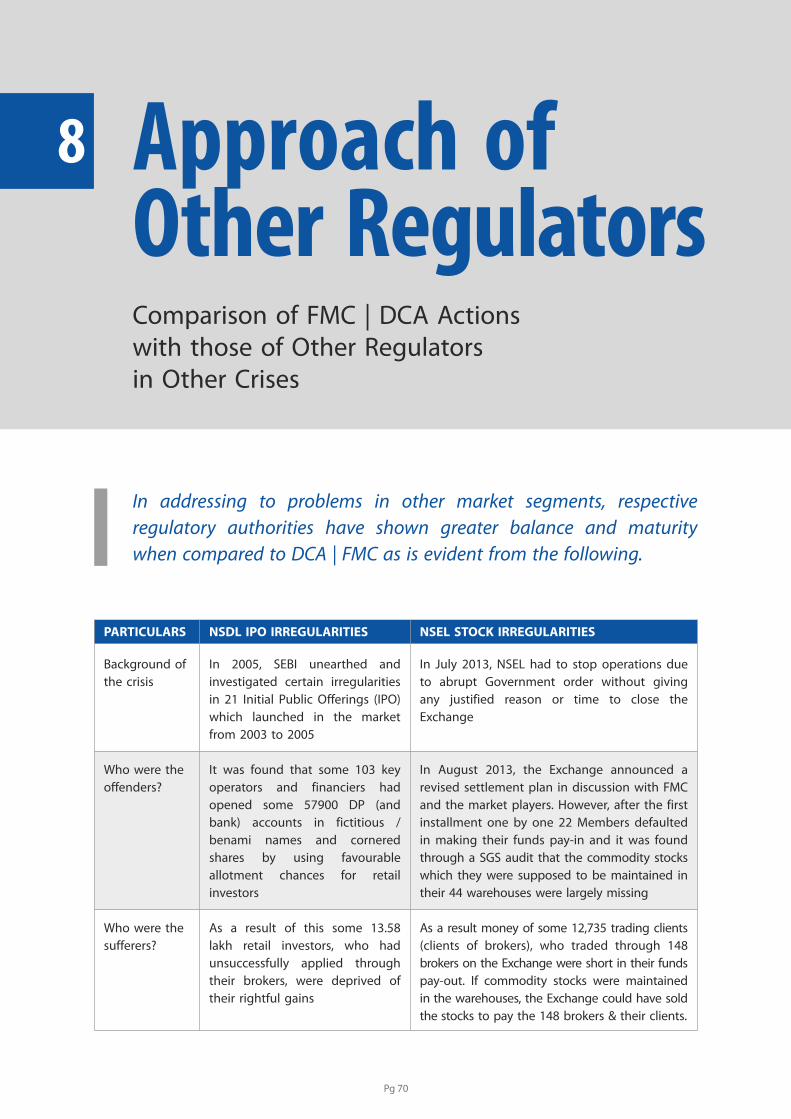

Comparison of FMC | DCA Actions with those of Other Regulators in Other Crises

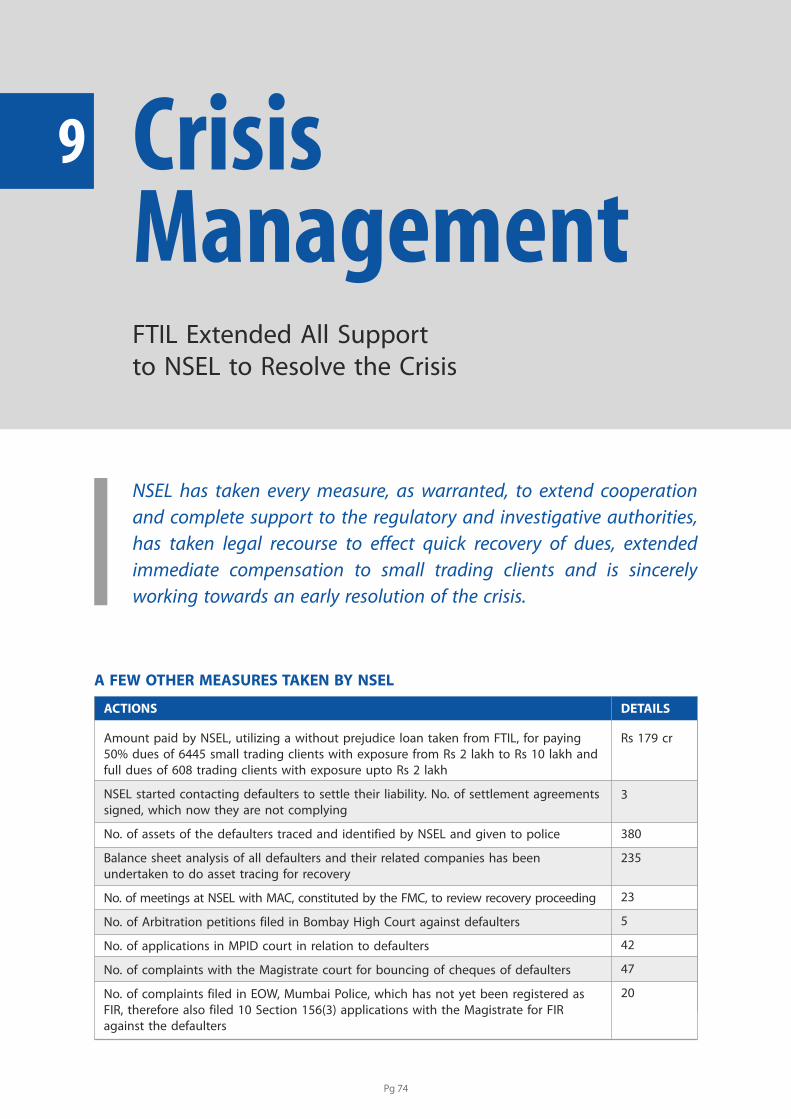

FTIL Extended All Support to NSEL to Resolve the Crisis

Clarifications on the Comments of the Chairman, FMC, on NSEL

Merger of NSEL with FTIL Proposed by FMC Not Consistent with Corporate Laws

How the problem could have been better resolved.

CRISIS MANAGEMENT

Pg 11

Agricultural Produce Market CommitteeComptroller and Auditor General of IndiaCentral Bureau of InvestigationCentral Depository Services (India) LtdCredit Information Bureau (India) LimitedDepartment of Consumer AffairsEnforcement DirectorateEconomic Offences WingFood and Agriculture Organization of the United NationsFood Corporation of IndiaForward Contracts (Regulation) Act, 1952Forward Markets CommissionGovernment of IndiaHaryana State Cooperatives Supply and Marketing Federation LimitedThe Institute of Chartered Accountants of IndiaLetter of CreditMonitoring and Auction CommitteeMinistry of Corporate AffairsMaharashtra Protection of Interest of Depositors (MPID) ActNational Agricultural Cooperative Marketing Federation of IndiaNational Securities Depository LtdPrevention of Money Laundering Act, 2002Payment and Settlement Systems Act, 2007Trading ClientsDepartment of Economic AffairsMinistry of FinanceAnnexureThese Annexures are available in separate book named PART-2

Disclaimer:

The purpose of this note is to explain the NSEL | FTIL side of the story and views on the whole episode of the NSEL crisis. It is not intended either to undermine or disparage the work of various authorities involved in resolution of the crisis or to comment upon subjudice matters. It is also not an attempt to cover or camouflage the real reasons behind the crisis or to escape from the obligations. It is just to explain the whole incident from the way NSEL | FTIL looks at it. FTIL and its Group companies, the previous and the present Boards and the management of the Group and its companies disclaim any responsibility arising from this Paper.

The Paper is a collective feeling of the constituents, shareholders and beneficiaries productively engaged with the vast ecosystem of the group who are keen that the world be told the company side of the story, which the Paper would, hopefully do.

The Financial Technologies Group holds no grudge against any authority, government or others who were involved in various aspects of investigation and finding resolution to the crisis. While seeking application of fairness and lawful measures, NSEL | Financial Technologies has extended complete cooperation to all the authorities.

APMCCAGCBICDSLCIBILDCAEDEOWFAOFCIFCRA (1952)FMCGoIHAFEDICAILCMACMCAMPID ActNAFEDNSDLPMLA ActPSSTCsDEAMoFANX

ABBREVIATIONS

Pg 12

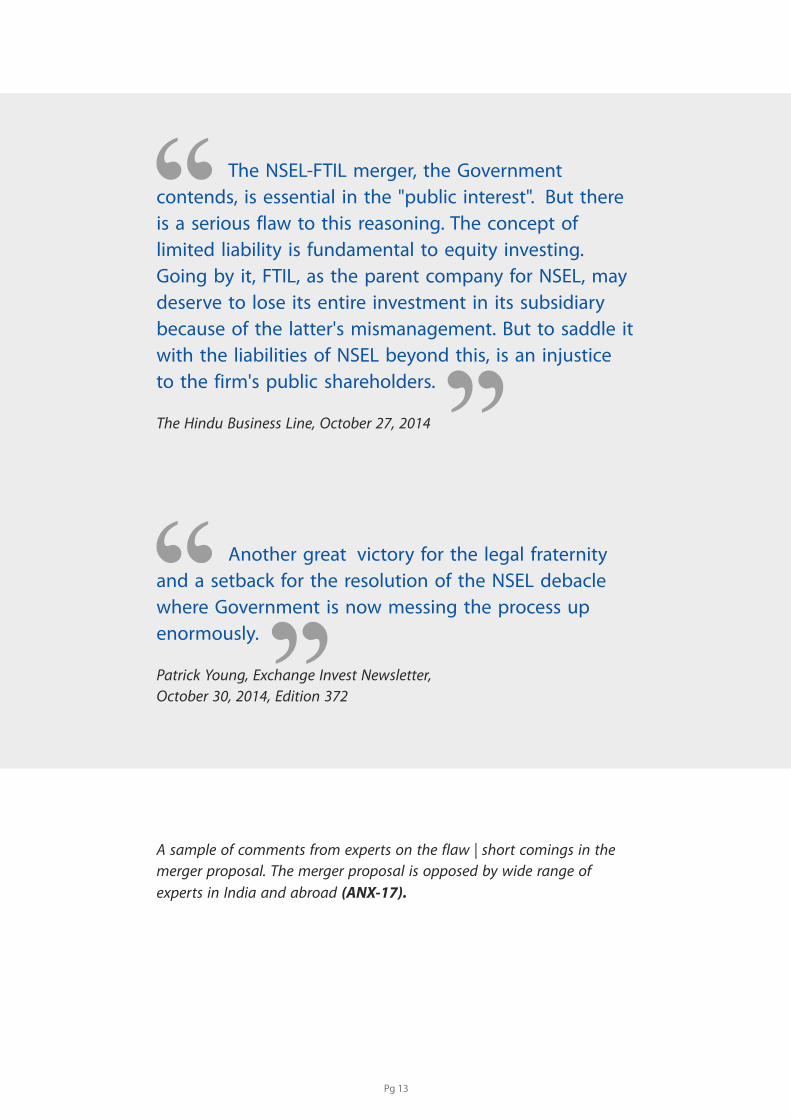

The Hindu Business Line, October 27, 2014

Patrick Young, Exchange Invest Newsletter, October 30, 2014, Edition 372

A sample of comments from experts on the flaw | short comings in the merger proposal. The merger proposal is opposed by wide range of experts in India and abroad (ANX-17).

The NSEL-FTIL merger, the Government contends, is essential in the "public interest". But there is a serious flaw to this reasoning. The concept of limited liability is fundamental to equity investing. Going by it, FTIL, as the parent company for NSEL, may deserve to lose its entire investment in its subsidiary because of the latter's mismanagement. But to saddle it with the liabilities of NSEL beyond this, is an injustice to the firm's public shareholders.

Another great victory for the legal fraternity and a setback for the resolution of the NSEL debacle where Government is now messing the process up enormously.

Pg 13

WHY THIS PAPER?The Real Picture on the Background of the Crisis

It is not to avoid responsibility. It is neither an effort to undermine the importance of obligations nor an argument to comment on the authorities for which we have greatest respect and extended best of our cooperation and compliance, from the beginning and will continue to do so.

The Financial Technologies Group, is a large group that promoted nine multi-asset-class exchanges spread across Asia, Africa and the Middle East, many of them in collaboration with pedigree institutions and global and domestic investors. MCX-SX, the third national stock exchange and the first to be promoted by private enterprise had majority of the shareholders representing the government owned financial institutions.

Similar to any large financial group spread across different geographies and various market segments, FTIL too faced problem with one of its subsidiaries, the National Spot Exchange Ltd (NSEL). The causes behind the crisis and those who contributed to it are still under investigation.

However, as things have unfolded, it appears that the crisis is a result of a wide range of factors. Members | brokers who paired the commodities trading contracts and the regulator not analysing the data provided to them every fortnight by the exchange. The crisis emerged when the government stopped, in July 2013, with immediate effect, further issuance of new contracts by NSEL that led to liquidity pressures and settlement problem.

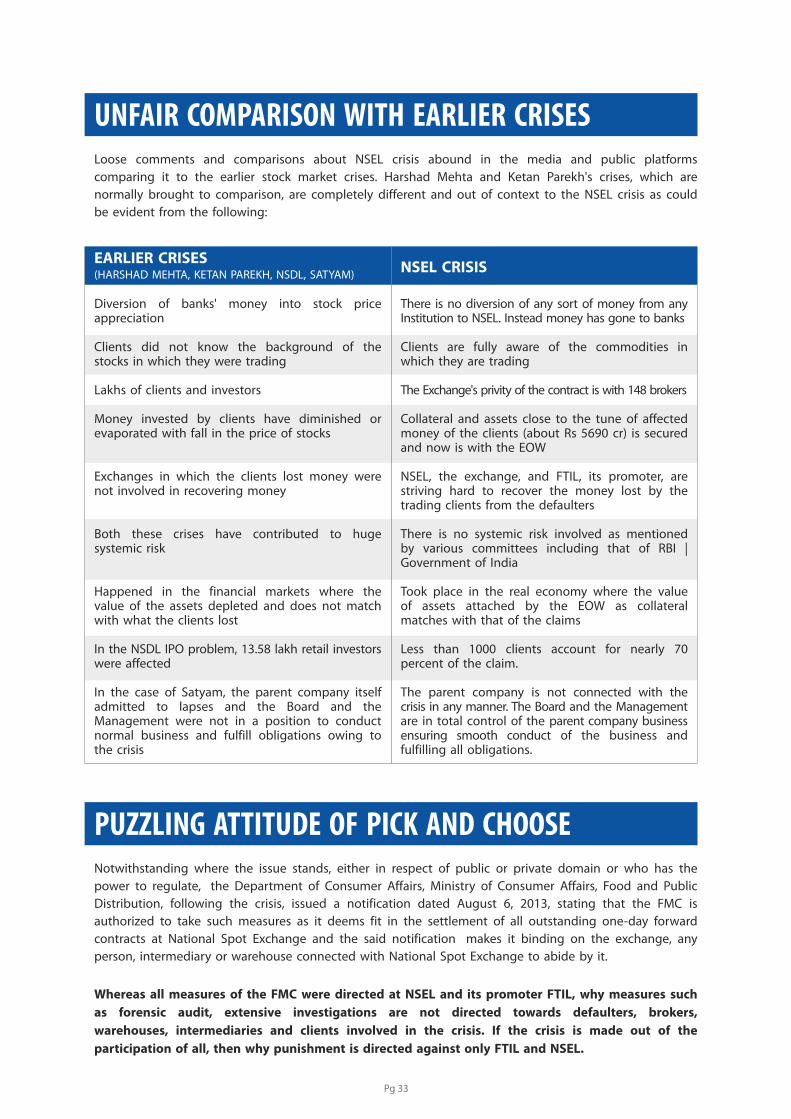

This time, the very nature of crisis is entirely different. There is no systemic risk, and it is about 13,000 trading clients and 24 defaulters who were caught up in the liquidity problem. Nearly 85 percent of the settlement obligation is from seven defaulter members and about 6 percent of 13000 trading clients currently account for 69 percent of the claim. The trading clients dealing with NSEL were all well informed, well educated, highly qualified, and of high net-worth. The trading took place between willing buyers and sellers, both sides being fully aware of the intricacies of trading along with associated risks and rewards.

The accident at NSEL was manageable. Nearly Rs 5,000 crore of assets of the defaulters that have been frozen and remain with the investigative agencies, (this is nearly as much as the settlement value of Rs 5,690 crore), is available for disposal and distribution among the trading clients once investigations are complete and clarity on legal process emerges.

The reactions to the crisis, however, remained one sided, all of which have been directed against the Financial Technologies Group. FTIL has nothing to do with any of the trading clients and never met any of them with regards to NSEL business. It was going by the briefings and reports as provided to the NSEL Board, by NSEL's management, that all was well and the minutes of which were noted in the FTIL Board meetings with effect from March 2011 when NSEL became a material subsidiary of FTIL. Immediately after the crisis, NSEL came out with an interim plan to support the small trading clients, with exposure less than Rs 10 lakh, utilising the without prejudice loan of Rs 179 crore granted by FTIL as a goodwill gesture. NSEL reconstituted the Board and revamped the management. It extended complete support to investigating agencies.

It is NSEL's parent company FTIL that suffered the most from the crisis. It has lost all its exchanges at substantial losses that it passionately built and incubated over a long period, even before the investigations in the matter are complete. FTIL and its promoter were declared not 'Fit and Proper'

Pg 14

though pioneering role was played by them in creating the state-of-the-art exchanges and ecosystem not seen even in the developed markets. The punitive actions even extended to custodial interrogation though whatever was asked was provided regularly.

The silent and sincere efforts of the Group in trying in every manner to resolve the crisis, within the four corners of the law, were overawed by the barrage of criticism, accusations, aspersions, all based on misinformation and misunderstanding that came from all over with no responsible authority trying to explain the real situation.

That is why it is thought that the NSEL | FTIL side of the story needs to be told to the world. For the accident originated | engineered by FMC | DCA and then to payment default (post August 4, 2013) committed by defaulters at one of its subsidiaries, the entire Group is paying the price. Not only injustice was meted on the FTIL, but added to it are other painful measures such as the hurry to declare promoters not 'fit and proper', the vilification campaign, unverified rumours, which have pushed the Group into a corner gasping for a little justice.

The merger of NSEL with FTIL which the Ministry of Corporate Affairs, on recommendation of the FMC, has proposed in a draft plan, is a complete contradiction to the democratic system and against the tenets of corporate law. Thousands of shareholders of FTIL will be deprived to enjoy the benefits of wealth creation and the very business that stood against the global competition and sustained success will wither away. Any measures of supersession of the management will expose the company to a quagmire of confusion and indecision that will surely decimate the prospects for an otherwise robust company having a clear vision for growth.

As things stand today, assets close to the settlement in dispute are frozen and available with the investigative agencies for early resolution of the crisis which shows that the trading clients money has not gone into thin air and is completely collateralized with real assets. NSEL, with all the required support from its parent, FTIL, is striving its best to recover the trading clients money from the 24 defaulters and even found success in full recovery of amount from two members with outstanding dues, which has already been distributed among the trading clients.

So far you have heard the side of the story that has unjustly punished the Group. We now seek your indulgence in spending a few minutes to listen to the hitherto "untold" story behind the crisis and what have been our efforts and intentions to resolve the crisis.

FTIL has always strived to make its growth a story for India to take pride in. Our exchanges and ecosystem institutions have demonstrated this spirit more than adequately.

We should now be given a fair chance to explain our stand, to recover and rebuild. It will be such a waste to demolish all that this Group has built in the interest of the country and its financial system, just to fulfill the wishes of a few, a minority who in the first place are the reason why the crisis took place.

Pg 15

Financial TechnologiesDistinction of Pioneering and Path-Breaking Contribution to Indian Financial Market

1

The engagement of FTIL in global and domestic exchange industries and ecosystem development prior to the crisis is very extensive and comprehensive.

FTIL pioneered multi-asset-class trading technologies that enabled markets in India spread their reach and access across the country. The exchanges and ecosystem that the Group created in the last one decade stand out for their superior standards in the design and development of financial markets infrastructure that are not seen even in some of the developed markets.

FINANCIAL TECHNOLOGIES GROUP: The Ecosystem of Markets and Economic Empowerment

Ÿ Farmers Ÿ Trading Houses Ÿ TradersŸ Corporates Ÿ Fund Managers Ÿ Retail investorsŸ Member brokers Ÿ High net worth investors Ÿ Manufacturers and Producers Ÿ Exporters Ÿ Institutional investors intermediariesŸ Importers Ÿ Hedgers

MARKET PARTICIPANTS

• Farmers• Producers, Consumers, intermediaries and

investors• Shareholders• Financial Institutions• Employees• Market Regulators• Revenue Authorities• State and Central Government• Catalyst for Innovation and entrepreneurship

at local level• Community employment programme• Skilled development and self employment for

local youth• Agri sector and SME development• Agri extensions and Marketing Board• Media and communication Professionals• Vendors• Contractors

STAKEHOLDERS

MCX-SXIndia’s New Stock Exchange is promoted

FTIL and MCX, but now owned upto 89% by Banks and Financial Institutions

• Multi-assets Exchanges and support institutions

• Development of local markets APMCs and Marketing Boards

• Clearing corporation• Depository institutions• Regulatory infrastructure and support

institutions• Banks and lending Institutions• Software and Systems Architecture• Trading and Technology solutions• Warehousing Infrastructure• Quality and Accrediting institutions and

delivery stations• Research and advisory firms• Information dissemination infrastructure and

network• Transportation other physical infrastructure

MARKET INFRASTRUCTURE

CAPACITY BUILDING• Enhancing financial literacy and • Market education at Under • Knowledge development and

financial inclusion graduate and graduate level documentation• Financial Advisors • Market professionals for support • Media services

services• Research Analysts • Software Developers• Market communication• Trainers and Educators • Hardware Manufacturers

Pg 16

For India, the decade of the 1990s was a turning point. A new wave of economic liberalization that has dawned in the country after five decades of controlled policy environment unleashed an upsurge of enterprise and entrepreneurship for which India was known for centuries. It is around the same time that new-generation information technology companies, which made India as brand equity for global outsourcing, began to take shape. and form. It was also the time when stock markets in India, which functioned under the closed confines of broker-dominated exchanges, began to emerge as corporate entities with greater focus on moving towards electronic trading and trade transparency.

India is a large country with vast geographic proportions and has the potential to create markets of big size and significance. However, for long, the country faced the limitations of logistics to spread the market activity across the nation. The technologies prevailing at that time, mostly from the global multinational corporations were prohibitively expensive, which made thousands of brokerage firms in India, many of them smaller in size, not being able to afford expensive technologies

It is at that time the pioneering role of FTIL came into finest display, which amazed even the developed markets. A small team led by Mr. Jignesh Shah, B.E. (Electronics), Mr. Dewang Neralla, B.E. (Computer Science) and Mr. Ghanshyam Rohira, B.E. (Computer Science), harnessing the skills they earned as engineers and a strong urge to place India on the map of the global capital markets, came out with trading technology through which brokers could trade multiple products in different exchanges using just one desktop. It was like a sort of revolution in trading technology in India where virtually every exchange, broker, sub-broker, and market intermediary have courted this product and vouched for its best performance. In securities industry, "ODIN" trading solution is like an i-Phone which everyone wanted. The only difference is that FTIL made it affordable to thousands of broking firms, small and big, individual and corporate, across the length and breadth of the country.

The trading technology that FTIL has developed had to meet the toughest standards. It has to match with the best that the competition was offering in terms of quality and robustness. It should be useful to thousands of broking firms. It has to clear the regulatory standards. It should be found acceptance by the exchanges. If it were to be extensively used, it needed to carry out enormous capacity building.

FTIL, with great focus and thrust on quality, robustness and cost effectiveness, has met all these challenges with great commitment. Very soon it emerged as the market leader (Number 1 in India and number 2 in the world) in trading technology, which even competitors used to hold in high regard. It has held leadership position for the past 15 years.

The optimally prized and process-efficient trading technology that FTIL has so passionately developed has enabled Indian stock markets to make a big leap in terms of expanding operations through the country and gaining access to millions of investors and institutions. The very fact that Indian stock markets have about half a million trading terminals, most of which are run on the technology provided by FTIL, spread across nearly 3000 towns and cities is a testimony to the immense contribution the company has made in India in making Indian stock markets truly national.

THE PIONEER

Pg 17

THE PATH-BREAKING CONTRIBUTIONA pioneer in technology solutions soon became a path breaker in the exchange industry. Even till early 2000s markets in India meant just stock markets. One or two products were traded on the exchanges that hardly reported volume of any size or significance. India was nowhere in the vicinity of globally recognized exchanges. It was an opportunity for FTIL to repeat the distinction that it achieved in creating world class products in exchange technology. Exchanges are the natural progression for the company as it has excelled in providing technology solutions that enabled transaction intensity and the presence spread across the geography. It then explored to enter into the exchange industry to set up state-of-the-art exchanges that India can take pride in.

It is this aspiration that led the Group to set up a wide range of exchanges in India. Not only setting up the exchanges, the Group is credited with the distinction of developing exchange - traded derivatives markets in virtually every sphere that India has witnessed in the post-reform period, which helped millions of businesses and enterprises to protect their business and growth from price risk.

Multi Commodity Exchange of India (MCX) was the first exchange from the Financial Technologies Group. MCX was given licence to trade in commodity futures, which it obtained based on the excellent track record of the promoters and the professional expertise to run modern financial market infrastructure institutions. FTIL got the licence for MCX purely on merit of their track record against intense competition from other players. Very soon MCX has brought back the glory that India once enjoyed in the leadership of commodity trading. India being the 'Sone ki Chidiya' was the attraction that pulled Columbus to Vasco da Gama to the East India Company to India. Mr. Jignesh Shah dreamt of making India, once again, "the commodity trading hub between Tokyo and London". The success of MCX has become a standard for exchange industry development in many emerging markets. Governments from various countries have approached the Financial Technologies Group to set up such successful financial markets infrastructure in their respective countries. At its peak, MCX had more than 2000 members with about 4.5 lakh trading terminals spread across 1500 cities and towns with an average daily trading to the tune of Rs 500 billion.

THE SPIN-OFF EFFECTS OF THE FINANCIAL TECHNOLOGIES GROUP

ECONOMIC BENEFITS TECHNOLOGY BENEFITS SOCIAL BENEFITS

• Efficient price discovery process

• Diverse hedging products

• Extensive market infrastructure

• Market penetration across towns and cities

• Collateral and risk management products

• Indigenously developed cost-effective technologies

• Low-cost real-time information dissemination

• Innovative payment solutions

A nationwide study (A Million Jobs & A Million Opportunities) conducted by MCX and Tata Institute of Social Sciences, TISS, brought out numerous social benefits contributed by the Group that include:

• Employment opportunities across the country

• Increased scope for self-employment opportunities

• Financial access to local communities

• Increased participation of the local talent and expertise

• Growth of local entrepreneurship

Pg 18

AN EXCHANGE INDUSTRY MNC FROM INDIAFrom the success of MCX came out the international forays of the Group in setting up exchanges in leading international financial centres covering important geographies of Africa, South East Asia and the Middle East. Dubai Gold and Commodities Exchange was set up in a joint venture with the Government of United Arab Emirates. It is for the first time that the Government of United Arab Emirates has entered into a joint venture with a private sector institution outside the country. DGCX, as it is known, very soon emerged as a major multi-commodity exchange in the Gulf region, a position it enjoys even now. Then followed a series of multi-asset-class exchanges in leading international financial centres. Singapore Mercantile Exchange within the regulatory jurisdiction of Monetary Authority of Singapore has emerged as a well-known exchange in South East Asia. Global Board of Trade, which was under the regulatory supervision of Financial Services Commission, Mauritius, was meant to be the gateway for growth opportunities in the fast-growing Africa region. On the eve of the launch of the Global Board of Trade in Mauritius, Navinchandra Ramgoolam GCSK, FRCP, Prime Minister of Mauritius was very gracious in thanking the Financial Technologies Group for "showing confidence in Mauritius and adding an entirely new dimension to our financial system by bringing knowledge, technologies, businesses and know-how that are generally found in the big financial centres of the world. To operate in Mauritius might be a relatively small step for GBOT, but this was a big stride in our economy." Global Board of Trade is now merged with Bourse Africa that the Group has set up in Botswana as a business strategy to focus on the entire Africa region, with its headquarters now located in Mauritius. Bahrain Financial Exchange under the regulatory jurisdiction of the Central Bank of Bahrain was envisaged for developing trading in various sukuk-based and Islamic capital market products that are assuming importance and prominence in a number of countries. Within a very short time the imprints of the Financial Technologies Group spread far and across multiple geographies and multi-asset-classes.

Exchanges promoted by FTIL are located in leading international financial centres, such as Singapore, Mauritius, Dubai, Botswana and Bahrain, in addition to Mumbai and Delhi, making it the first ever multinational company from emerging markets to hold exchanges across major geographic regions.

Back home, further innovations continued. One of the major problems affecting the Indian industry was electricity. Indian Energy Exchange was set up to create market-based solutions for price discovery and trading of electricity. MCX-SX, India's new stock exchange was established to offer a basket of stock market products so as to increase retail participation in the stock markets, which has been abysmally low. Further, NSEL was set up to create and develop a common market for agricultural produce by providing a nationwide electronic trading platform. Thus FTIL has created a unique basket of exchanges for all major asset classes, which is unique in global finance.

THE EXTENSIVE UNIVERSE OF EXCHANGESAND ECOSYSTEM INSTITUTION CREATED

BYFINANCIAL TECHNOLOGIES

EQUITIES

ENER

GY

COMMODITY

CURRENCIES

BONDS

Pg 19

DISTINCTIONS§ MCX was ranked by the Futures Industry Association as the 3rd biggest commodity exchange in terms

of number of contracts traded. MCX is the first listed exchange in India, which received phenomenal success by mobilizing US$ 7 billion for an issue size of US$132 million. It won the NASSCOM Social Innovation Honors 2010 for its flagship CSR Project Gramin Suvidha Kendra, the rural facilitation centre set up in a joint venture with India Post.

§ Growth and Inclusion was the theme on which exchanges of the Financial Technologies Group were conducting business.

§ MCX-SX was ranked at the 1st biggest exchange in terms of number of currency futures contracts traded by the World Federation of Exchanges.

§ Indian Energy Exchange is the biggest energy exchange in India in terms of electricity traded. The exchange was reported as leading to a second industrial revolution by a lead story in Economic Times (July 9, 2011).

§ NBHC was the largest collateral and warehouse management company in the private sector in India. It rose to become the largest facilitator of bank credit against agricultural commodities through warehouse receipt based finance.

§ Dubai Gold and Commodities Exchange even now enjoys the distinction of a premier exchange in the entire GCC region.

§ Atom had the distinction of being India's leading digital transaction platform, which received the India SME Innovation Award for 'An Innovative Payment Solution for SMEs'.

§ All exchanges of the Financial Technologies Group were widely held, consisting of pedigree investors from domestic and international markets. The Group exchanges had predominant shareholding of the public sector financial institutions. For instance, banks and financial institutions held 88.8 percent of the shareholding of MCX Stock Exchange promoted by the Group. The group had the benefits of several visionaries, senior bureaucrats, independent professionals, academicians serving in the Board, with every institution run by a team of independent professionals.

for INDIAof INDIA to INDIAby INDIA in INDIA

MCX: A MISSION FOR THE NATION

The underlying of commodity futures traded on the exchanges are all important aspects of the Indian economy. Be it agricultural commodities, bullion, metals, or energy, all are essential for the growth of the nation. Commodity exchanges help in efficient price

Unlike capital markets, commodity markets in India are not driven by either foreign institutional investors or companies. The entire ecosystem of constituents of commodity markets, including farmers, corporations, traders, producers,

The development of the entire commodity futures market is solely shouldered and driven by Indian enterprises and professionals, and these markets are run and managed by Indian talent. Traders, investors, technology professionals, brokers, bankers,

Commodity exchanges are playing a pivotal role in the Indian economy. They offer a variety of benefits to a large number of stakeholders through efficient price discovery, price risk management through hedging, and effective planning of production and consumption. They directly benefit millions of producers and consumers,

All the progress and development of commodity exchanges take place and stay in India. Pricing, trading, hedging, research, employment, income generation, and job creation take place in India, benefitting millions who are gainfully employed either in business or jobs or numerous enterprises. A major

Pg 20

§ Mr Jignesh Shah, promoter of FTIL is the only Asian to be recognized as ‘Dominant Financial & Futures Industry Leaders’, by the Futures Industry Association (US), a glory that he shared with the likes of US Treasury Secretary, Tim Geithner, CME’s Craig Donohue and Terry Duffy, ICE’s Jeffrey Sprecher and BATS’ Joe Ratterman.

§ He brought the first FII investment in MCX, and then listed it with an outstanding success. Honoured as ’Young Global Leader’ by the World Economic Forum, ‘Entrepreneur of the Year’ by E&Y and the ‘Exchange Industry Person of the Decade’ at the India International Gold Convention.

§ His focus on development of ‘Social Business enterprises’ generated over a million jobs that blended social interest with inclusive growth, and yet ensuring highest returns to shareholders.

§ He was keen on putting India on top of the map of the global exchange industry.

To be successful, exchanges require support in the form of capacity building, which FTIL has carried out in a unique manner. Exclusive arrangements for providing these support systems were made. National Bulk Handling Corporation was providing risk and collateral management facilities. TicketPlant was providing cost effective and customized real time data support and solutions to the exchange industry community. FTKMC was engaged in the development of extensive domain knowledge development and management across various stakeholders, including regulatory institutions, exchanges and intermediaries, corporates, banks and financial institutions, investors and the academia. Atom was providing innovative payment solutions. The ecosystem institutions so thoughtfully designed were contributing services to not only the exchanges of the Group but also other institutions from India and a number of emerging markets.

It might be ironical, but it was not FTIL that mooted the proposal of the spot exchange. FTIL was only keen on developing exchange industry solutions and setting up multi-asset-class exchanges. The idea of National Spot Exchange came in the context of the keen desire of the Government of India to create a nationwide common market for commodities (see Page no. 39). The Government invited various institutions for consultations on setting up of electronic spot exchange to which MCX responded by submitting a proposal.

EXTENSIVE ECOSYSTEM

NSEL CRISIS

discovery as well as offer risk management alternatives to producers and consumers of these commodities.

consumers, and other stakeholders, are based and residing in India.

intermediaries, and so on reflect Indian talent and skills and represent the most successful story of market development in post-independent India.

which include farmers, entrepreneurs, traders, individuals, SMEs, corporations, and investors. They also indirectly benefit millions of ecosystem partners like warehouse operators, collateral management services, logistic support providers, information vending services, and other service providers.

contributor to the revenue of the state and Central governments as stamp duty, service tax, professional tax, and income tax, these exchanges support the rural development programmes of the government and strengthen its financial inclusion strategies.

Pg 21

The Government gave the responsibility of regulation in respect of oversight, protection of investor interests and provision of periodic information by commodities exchanges on all major operational aspects to the FMC. On several platforms, MCX has been advocating amendment to the FCRA Act to further widen the scope of the commodity derivatives markets as also sought a complete regulatory framework for the spot exchanges by the Forward Markets Commission.

These developments more than adequately dispel rumours spread by certain vested interests, that NSEL was created by FTIL with the sole purpose of defrauding the people. (Please refer to Chapter 5)

The accident at NSEL happened when trading clients sequenced certain commodity trading contracts to maximise return. When the Government instructed NSEL to stop all contracts, immediately, market intermediaries | trading clients were caught in a liquidity problem, disrupting the smooth settlement programme that had been going on since the inception of the exchange.

FTIL extended all support to NSEL to resolve the crisis. As an interim measure, without prejudice loan of Rs 179 crore was given to NSEL to pay the smaller trading clients with exposure upto Rs 10 lakh. The NSEL Board was reconstituted and the management revamped. NSEL extended full cooperation to the investigating authorities, including EOW, CBI, ED as also the Committees that the Government has set up to study the NSEL crisis. FTIL has been supporting NSEL through financial and human resource support to explore various avenues of crisis resolution that are legally possible. NSEL, with support from FTIL, has been taking all measures required legally to proceed against defaulters to recover the money.

FTIL did all what was expected from a responsible corporate when one of its subsidiaries came into a problem.

RISING TO THE CHALLENGE

While action was taken against NSEL and FTIL for its sincere efforts to find a solution to the crisis, was most unjust and unfair, all other players responsible for the crisis such as the defaulters and brokers were left out. FMC has focused only on NSEL and FTIL, with actions that proved detrimental to FTIL, and was put at risk prospects and fortunes of thousands of investors, employees and other stakeholders. These actions, which

• Investigation by multiple agencies in the same issues

• Though investigations are not complete and the promoters not held guilty, they are subjected to excessive harassment

• Rumours that have no basis and far from reality

• Relief and recovery measures of the FTIL are not recognized

• Continuous threats in terms of mergers and change of the Management of FTIL which are adversely affecting the recovery process and crisis resolution

• Loss of Exchanges and ecosystem ventures at distress that FTIL has pioneered and so passionately developed

• Closure/sale of companies

• Loss of business growth

• Job losses in group companies affecting hundreds of families

• Decline in the commodity exchange business after the exit of the promoters

• Loss to scores of small businesses that depended on the FTIL group for various support services

SUBJECTED TO UNFAIR TREATMENT

FTIL IS THE MAJOR VICTIM

Pg 22

were never heard or seen as any time in the past when a company was extending its fullest cooperation to resolve the crisis, included custodial interrogation of the promoter and key governing and managerial personnel of the exchanges, declaring the promoter as not fit and proper, threatening with the mergers and supersession of management, which are not consistent with the corporate conduct of civil societies in democracies.

The immature manner in which FMC handled the accident at NSEL only highlighted its own shortcomings and led to NSEL and FTIL becoming even more aggrieved party than these were before.

In the outrage that emerged after the crisis and the intense lobbying by certain sections of brokers and trading clients, a few major facts about NSEL are being completely side-stepped. The contracts in dispute formed just 17 percent of the total business of NSEL since inception. Except the contracts that faced problem, the settlement of e-series contracts was conducted smoothly and successfully. When the exchange was abruptly stopped by the DCA | FMC to issue further contracts and the operations were closed, the exchange had a total of 46,000 clients with outstanding dues. Claims of 33,000 clients of e-Series contracts were settled successfully. Clients with exposure below Rs 10 lakh whose number is 7,000 received 50 percent of their claims. The claims of 6,000 clients are under the process of settlement. Of the Rs 5,690 crore of settlement, seven defaulters own upto 85 percent and six percent of the clients, which is equivalent to 781 clients who traded through 71 brokers with whom the exchange has privity of contract, (the clients have their own client-broker agreements with brokers under the Rules, Regulations and Bye-Laws), account for 69 percent of the claim.

The accident at NSEL has affected FTIL in the worst possible manner. The Group lost exchanges, profitable businesses, and growth opportunities. Its ability to create world class institutions is severely eroded and dented.

Our parent company FTIL is fully seized of the problem at NSEL and is committed to extend fullest cooperation and support in an early resolution of the crisis.

We urge and request all those who believe in enterprise and the potential of India to lead the financial markets development to appreciate the relevant concerns and extend their support and cooperation in overcoming this crisis.

WE EARNESTLY REQUEST THAT:

The actions of the Government be spread across all the entities that have contributed to the crisis, including the Forward Markets Commission, the then Additional Secretary, DEA, brokers, trading clients and defaulters. NSEL has been needlessly punished and so has the Financial Technologies Group.

Assets of the defaulters worth Rs 5,000 crore have been seized for attachment by the EOW, which is close to the Rs 5,690 crore settlement due. The Government should take all the measures possible to dispose of these assets in order to bring an early resolution to the crisis.

FTIL and the managerial professionals be absolved from the not 'Fit and Proper' declaration by the FMC, which was made without proper examination and investigation of all factors concerned and without considering the judicial process currently in progress.

The focus should be on the recovery of dues from the defaulters rather than taking vengeful measures against FTIL group that will destroy the ecosystem of exchanges and benefit competing exchange groups.

NSEL should be allowed to take every measure to resolve the crisis without undermining its power and potential by hasty measures of merger with FTIL or supersession of FTIL management, which can actually prove counter-productive in solving the problem.

LOOKING AHEAD

Pg 23

OurPriorityNSEL is committed to Expedite Recovery from the Defaulters, to Resolve the Crisis

2

FTIL by itself has not committed any breach of governance standards or market abuses. It is a well-run company, with close to 60,000 public shareholders, an accomplished Board and a dynamic management, that has steered this company from being a start-up in early 2000s to one of the most respected and widely regarded technology solutions company that pioneered multi-asset-class trading segments, which stood the tests of competition from global majors such as IBM. Cost-effective and efficient technology solutions enabled Indian financial markets to expand the reach and access nationwide, benefiting millions, including financial institutions, intermediaries, investors and other stakeholders.

Since its inception, FTIL has not received any complaint from exchanges or intermediaries, which are its biggest clients and customers. Even competing institutions used to buy technology solutions from FTIL, which is a testimony for its integrity and business ethics. There was never any regulatory action of any sort though the exchange and ecosystem ventures of the Financial Technologies Group were operating in several regulatory jurisdictions in India and abroad.

NSEL is committed to taking all the steps required and extending complete cooperation for an early resolution to the crisis through recovery of trading clients' money from the defaulters. FTIL has already provided ad-hoc without prejudice relief to NSEL to support small trading clients with exposure upto Rs 10 lakh and is helping the exchange with financial, infrastructure and personnel support to speed up the recovery process from the defaulters.

Pg 24

FTIL never received any subsidy, land or financial or fiscal support from any state or Central government. It has contributed significantly to tax generation in the form of corporate income tax, service tax, transaction tax, stamp duty and other levies and charges from various institutions from time to time.

FTIL is a first-generation enterprise that created new standards and benchmarks on potential and possibility of financial markets development.

Despite FTIL being in the private sector, it has contributed significantly to the growth of public capital markets. FTIL is the one that took India to the global league tables in regard to exchange operations in major segments, such as commodities, currencies and energy.

It enabled several key and strategic sectors, working with a wide range of commodities to hedge, manage risk and discover prices to promote efficient production, procurement, sales and distribution.

A nationwide study by a leading research institution, Tata Institute of Social Sciences (TISS), described MCX one of the erstwhile Financial Technologies Group Companies in one catch line: "A Million Jobs and a Million More Opportunities".

The Financial Technologies Group has expanded its operations and sphere of influence and in this process conceived and created some of the best exchange and ecosystem ventures, which stand out as a distinct achievement and accomplishment from any emerging market economy in the world.

As it was expanding its sphere of influence across various asset classes in new market segments coming up in different geographies across the world, it engaged in numerous businesses connected with technology and exchange industry and in the process set up several subsidiaries, one of which was National Spot Exchange Limited (NSEL).

The genesis of NSEL came in the background of the desire of public policy and the Government of India to create a common commodities market in which a nation wide electronic platform for spot trading in commodities assumes significance. Reports of the Government have often mentioned the need for such an institutional mechanism to provide transparent and market-determined process to the producers of commodities. MCX, the flagship commodity futures exchange of the Financial Technologies Group, had several rounds of discussion with the Government in taking forward the spot exchange initiative. It is worthwhile to note that NSEL was not set up by FTIL but by MCX in 2005. it was only later on that shares held by MCX and its nominees in NSEL were transferred to FTIL as the current legislation was not conducive to commence greenfield spot trading and agriculture being a subject governed by different state governments with a Model APMC legislation, having promulgated by the Union Government and adopted by 16 state governments. Subsequently, an exemption was granted by the Ministry of Consumer Affairs, Food & Public Distribution, Government of India, to NSEL to conduct nationwide trading in one-day forward contracts. This was not a privilege extended to just NSEL, as similar exemptions were granted to all the other exchanges running similar platforms such as NCDEX promoted NSPOT and NMCE promoted National APMC.

While several agencies of regulation, government and investigation are currently involved in examination and study of various issues leading to the payment crisis, the MCA has suddenly come up with a proposal to merge NSEL with FTIL in contravention of the long established conventions of corporate law and conduct. Subsequently, newspaper reports hinted that the MCA is contemplating supersession of the management of FTIL, which is again a contravention of the established norms of economic freedom.

Pg 25

THE PERTINENT QUESTIONS THAT EMERGE IN THIS CONTEXT ARE:

WHY CANNOT:

• Is it fair to impose harsh and unjust actions on FTIL for payment defaults at one of its subsidiaries?

• Is it consistent with the local legislative and legal framework?

• Is it in accordance with the established conventions and practices?

• Is it in the good spirit of domestic and global corporate law?

• Has the regulator | government contemplated similar initiatives for companies that have experienced crisis that are much more grave and serious?

• Is the regulator | government succumbing to the demands of vested interests and a minority against a large majority of thousands of shareholders, employees and other stakeholders of FTIL justifiable?

• Are the proposed and management supersession aimed at only to settle the claims of a few high networth trading clients against, the livelihoods of scores of people and families that directly or indirectly depend on the success of the FTIL justifiable?

• Is it fair for the government to deprive FTIL genuine investors/shareholders their due share in the progress of the company?

If the Government is keen on settling the claims of a few high networth trading clients and a few brokers whose demand and persistence is leading it to take such unusual measures as considering merger and supersession of the FTIL Board and management, why cannot it direct its efforts to any of the following actions?

• The Government extend help and support to the three-member Committee set up by the Bombay High Court to dispose of the confiscated assets of the defaulters and utilise proceeds for the settlement?

• The brokers who have large role in the marketing, selling and trading of the defaulted contracts be investigated and forensic audit of their entire chain of operations be conducted?

• Strict action be taken against defaulter members who are evading payment?

• A fast track Court be set up to expedite recovery of dues from the defaulters and liquidate their assets?

• The PMLA (Prevention of Money Laundering Act 2002) be amended to enable proceeds of assets attached by the ED to go to the trading clients rather than the Government?

The amount close to the claim amount is already available in the form of collateral with the investigating agencies. It is expected that the Government, regulatory authorities and investigating agencies will sell the confiscated assets first towards settlement of the claims of the trading clients.

The Financial Technologies Group has created millions of new stakeholders in the financial system, giving opportunities to earn, grow, and seek sustainable livelihoods. It created and nurtured new market segments and expanded the product ranges to serve a multitude of purposes such as investing, hedging and seeking newer opportunities for wealth creation. Governments, regulators and other development institutions from various countries used to visit the Financial Technologies Group to know and learn how it was able to create such a success story of sustainable financial market infrastructure growth and

Pg 26

development with such an extensive ecosystem and a large engagement of numerous stakeholders. Countries were keen to partner with the Financial Technologies Group to replicate the success that the Financial Technologies Group has managed in India, in their respective countries. The whole country expectantly looked at the Financial Technologies Group for leading to new directions of growth and maturity in Capital and Financial markets.

All this came to an abrupt halt just because of payment defaults at one of its subsidiaries. Government and regulatory authorities could have surely recognized the power of enterprise that the Financial Technologies Group has built, the impeccable record of conduct it has displayed in public markets, the unblemished achievement of enriching thousands of its shareholders with uninterrupted dividend payout for 36 consecutive quarters, getting accolades and recognition from global and domestic institutions, including multilateral institutions such as UNCTAD, FAO, and should have extended a helping hand to the Financial Technologies Group to overcome the crisis, which could have enabled it to solve the settlement crisis quickly and take the country towards the next generation of growth and development in the financial markets. The world over it is not uncommon for the Government to give temporary and ad-hoc support to institutions in crisis. If the US and European regulators and governments would have adopted the same stance as that of the Indian Government and the FMC, there would not have been anything of US or European finance left by now. Globally, Governments and crisis-hit institutions have always worked hand in hand in solving the problem and enabled both to reach recovery within a short time, which proved helpful to investors, customers and other constituents of the economy and finance. Unfortunately in the case of the Financial Technologies Group, it was nothing but vilification and witch-hunt from all sides, be it the government or the regulator or the agencies that have pressed it into a corner disabling its power to recover and redress quickly.

Even without assistance and support and despite being under constant and continuous harassment, NSEL is determined to get itself out of the crisis and redress grievances of the claims of trading clients. It is extending cooperation and actively coordinating with the courts and other agencies towards realization of dues from the defaulters that could lead to an early settlement. In all these efforts, FTIL is fully supporting NSEL, both with personnel and finance.

FTIL and NSEL are not allowed to do even this in a planned and orderly manner with continuous threats of mergers and supersessions, which are not only unjust but could best be ascribed as measures of plain expropriation of a successful enterprise.

Pg 27

It is surprising to note that the FMC has never let NSEL management handle recovery with focus

and never partnered NSEL's recovery effort. In fact, the FMC kept taking decisions to destabilize

recovery and keep defaulters away from being the focal point.

If the DCA had accepted NSEL's suggestion of orderly closure of the market in July 2013, this

episode would not have happened. This fact is being stated not for pointing fingers but to clarify

to those who have alleged that this model was deliberately wrongly designed, which is far from

truth.

Globally, post-global market crisis, it called for creation of stability and isolation of risk whereas

despite Financial Stability and Development Council (FSDC) being in place, the FMC through its

various actions in fact has enhanced and accentuated the risk for the FTIL Group due to its hurried

decision on declaring FTIL as not Fit and Proper. Overtime, enough evidence was there which clearly

proved this point but by then NSEL had been disadvantaged.

From July 2013 to September 13, 2013 the Board at NSEL was trying to come to grips with the

problem and understand the problem caused by the defaulters. By August 2013, NSEL filed its

complaint against defaulters with the EOW. Later, the EOW registered the complaint of the trading

clients. On December 13, 2013, the FMC declared FTIL and key officials of the FTIL Group, including

the promoter of FTIL, CEOs of MCX and MCX-SX as not 'Fit and Proper' without proper hearing and

consideration, which was ritualistically followed by SEBI (in case of MCX-SX) and Central Electricity

Regulatory Authority (in case of IEX) despite regulatory compliance in both these exchanges being

of the highest order, with an instruction for the FTIL Group to sell its stake in respective exchanges.

This was also followed by each regulatory institution organizing forensic audit in each of the

exchanges (i.e., NSEL, MCX, IEX and MCX-SX). Meanwhile, NSEL was busy making settlement

agreements with defaulters to recover money or obtain collaterals, but the FMC refused to approve

the agreements provoking the aggrieved parties moving to the MPID court for ratification of

agreements, which later got embroiled in litigations. Finally, NSEL got court order in such cases and