the time value of money time value of money is the term used to describe today’s value of a...

TRANSCRIPT

The Time value of Money

• Time Value of Money is the term used to describe today’s value of a specified

amount of money to be receive at a certain time in future. Thus, the saying “GH¢1

today is worth more than GH¢1 promised sometime in the future”. This is because

of one or combination of the following factors

The return you can earned on it if invested now

The erosion of its purchasing power caused by inflation

The risk of not getting the money due to default or the death of the one making the

promised.

• Basically it helps to indicate how much our investments today will be worth in the

future (future value), and also today’s worth of future proceeds of our current

investments (present value).

1Prepared by Alhaj Nuhu Abdulrahman

CHAPTER 4: INTRODUCTION TO VALUATION AND TIME VALUE OF MONEY

Future Value and Compounding

• Future value refers to how much an amount of money, invested today at a given

interest rate will amount to at the end of a specified period.

• Single period investment:

• Assume you have invested GH¢200 in an investment account for one year that pays

12% interest. How much will the investment, amount at the end of the year?

• It will amount to: (200 x 0.12) + 200 = 24 + 200 = GH¢224. This can be

mathematically expressed as; FV = P(1 + r)t called future value factor.

• So 200(1.12)1 = GH¢224. This computation is called simple interest.

Multi-period investments:

• If the GH¢200 is invested for two years, the future value will be: (200 x 0.12) +

(224 x 0.12) + 200 = 24 + 26.88 +200 = GH¢250.88.

2Prepared by Alhaj Nuhu Abdulrahman

TIME VALUE OF MONEY

• This can as well be mathematically expressed as; FV = P(1 + r)t. So 200(1.12)2 =

GH¢250.88. This computation is called compound interest.

• Present Value and Discounting:

• The concept of present value refers to today’s value (worth) of expected amount

over a certain period. It also helps to answer the question; how much money must I,

invest today at a certain interest rate to generate a desired amount at a certain future

period? Thus

i) What is the current value of GH¢224 expected in a year’s time at 12% interest rate?

ii) What is the current value of GH¢250.88 expected in two years at 12% interest rate?

iii) How much do I need to invest now at 12% interest rate to generate GH¢224 by the end of the year? (Single period)

iv) How much do I need to invest now at 12% interest rate to generate GH¢250.88 by the end of two years (multi-period)?

3Prepared by Alhaj Nuhu Abdulrahman

TIME VALUE OF MONEY Multi-period investments:

Present value (PV) = , which can also be expressed as; PV = FV x .

Solution: i & iii)

Present value of GH¢224 at 12% interest rate for a year = = GH¢200

or 224 x = 200.

Solution: ii & iv)

The present value of GH¢250.88 after two years = = GH¢200

or 250.88 x

4Prepared by Alhaj Nuhu Abdulrahman

TIME VALUE OF MONEY

Suppose you deposited GH¢200 today in an investment account that promises 12%

per annum. After a year you deposited GH¢250 and at the end of the second year you

again deposited GH¢350. How much will the investment amount to at the end of the

second year?

Solution: Future = Pv x (1 + r)t

= GH¢200 x (1.12)2 = GH¢250.88

= GH¢250 x (1.12)1 = GH¢280.00

= GH¢350 x (1.12)0 = GH¢350.00

Total FV = GH¢880.88

How much will the above investment amount to at the end of the third year if the

account had a beginning balance of GH¢150?

5Prepared by Alhaj Nuhu Abdulrahman

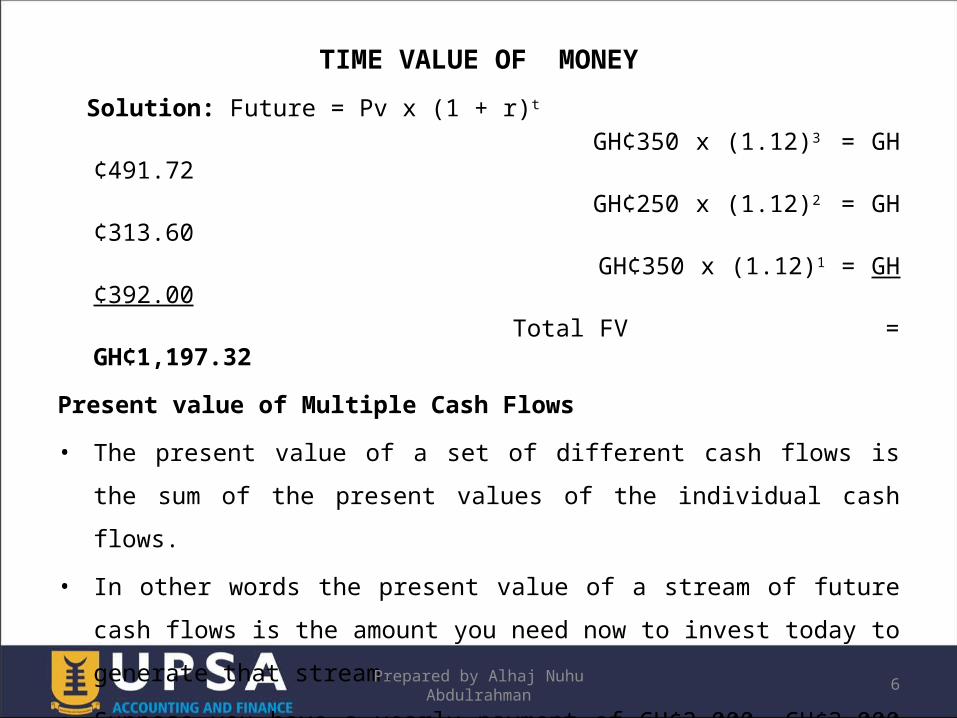

TIME VALUE OF MONEY Future value of Multiple Cash Flows

Solution: Future = Pv x (1 + r)t

GH¢350 x (1.12)3 = GH¢491.72

GH¢250 x (1.12)2 = GH¢313.60

GH¢350 x (1.12)1 = GH¢392.00

Total FV = GH¢1,197.32

Present value of Multiple Cash Flows

• The present value of a set of different cash flows is the sum of the present values of

the individual cash flows.

• In other words the present value of a stream of future cash flows is the amount you

need now to invest today to generate that stream.

• Suppose you have a yearly payment of GH¢2,000, GH¢3,000 and GH¢4,000.

• How much do you need to invest today in a bank account at 12% interest per

annum to enable you make these payments?

6Prepared by Alhaj Nuhu Abdulrahman

TIME VALUE OF MONEY

Solution: Present value =

=

=

= 1,786 + 2,392 + 2,847

= GH¢7,025

This can be rearranged in tabular form as follows;

Year Cf(GH¢) x PVF@12% = PV(GH¢)

1 2,000 0.8929 1,786

2 3,000 0.7972 2,392

3 4,000 0.7118 2,847

Total Present value GH¢7,025

7Prepared by Alhaj Nuhu Abdulrahman

TIME VALUE OF MONEYPresent value of Multiple Cash Flows

Exercises

1. Stanbic Bank developed and introduced an investment product that promises GH

¢3,000, GH¢4,000, GH¢6,000 and GH¢8,000 for the years one, to four

respectively. If the bank’s investment rate is 15%, how much will be the required

investment deposit now?

2. Suppose you approached a car dealer to purchase a car and he gives you the

following two alternative payment plans.

i) Pay GH¢15,000 now and pick the car or

ii) Make down payment of GH¢4,000 now and make instalment payments of GH

¢3,000 each year for 4 years.

8Prepared by Alhaj Nuhu Abdulrahman

TIME VALUE OF MONEYPresent value of Multiple Cash Flows

Question 1: How much do you need to invest now at an interest rate 12% to generate

the streams of 4 payments? Which of the alternatives deals is a better

one?

Question 2: Prepare a 4-year investment and instalment payment schedule

Solution 1: Year Cf(GH¢) x PVF@12% = PV(GH¢) 0 4,000 1.00 4,000 1 3,000 0.8929 2,679 2 3,000 0.7972 2,392 3 3,000 0.7118 2,135 4 3,000 0.6355 1,907 Required investment deposit 13,113

The second paying plan is better because instead of paying GH¢15,000 outright, you will

rather deposit GH¢13,113 now out of which the GH¢4,000 required down payment will

be made. So the actual investment deposit is (GH¢13,113 - GH¢4,000) GH¢9,113.

9Prepared by Alhaj Nuhu Abdulrahman

TIME VALUE OF MONEYPresent value of Multiple Cash Flows

Solution 2: Four-year investment and instalment payment schedule

Year Opening - Payment = Remaining + 12% earned = Closing

Balance Balance Interest Balance

0 13,113 4,000 9,113 1,094 10,207

1 10,207 3,000 7,207 865 8,072

2 8,072 3,000 5,072 609 5,681

3 5,681 3,000 2,681 322 3,003

4 3,003 3,000 3 0.36 3.36

10Prepared by Alhaj Nuhu Abdulrahman

TIME VALUE OF MONEYPresent value of Multiple Cash Flows

• An annuity is the equal (level) stream of regular payments for a fixed period of

time. Types of annuity:

• Ordinary annuity: This involves payments at the end of each period.

• Examples include loan payments and pension contributions.

• Annuity due: This involves payment at the beginning of each period.

• Examples include rent, mortgage and lease payments.

Valuation of annuities: Ordinary annuity:

• Present Value of Annuity (PVA) = C or

11Prepared by Alhaj Nuhu Abdulrahman

TIME VALUE OF MONEY Annuities

12Prepared by Alhaj Nuhu Abdulrahman

TIME VALUE OF MONEY Annuities

• Illustration: Assume you have just entered into a loan agreement with your bank

that requires monthly repayment of GH¢350 over a three-year period. The loan

facility attracts an annual interest rate of 18% (1.5% per month). What is the

amount of the loan facility?• Present value of Annuity = 350 x or

= =

= 350 x (27.66) = GH¢9,681

• Exercise: Suppose you realized you can afford to make monthly payment of GH

¢632 towards buying a new car in two years. Your bank has agreed to lend you the

amount you need now at the rate 1% per month. How much should be the borrowed

amount? Check it will be GH¢24,000

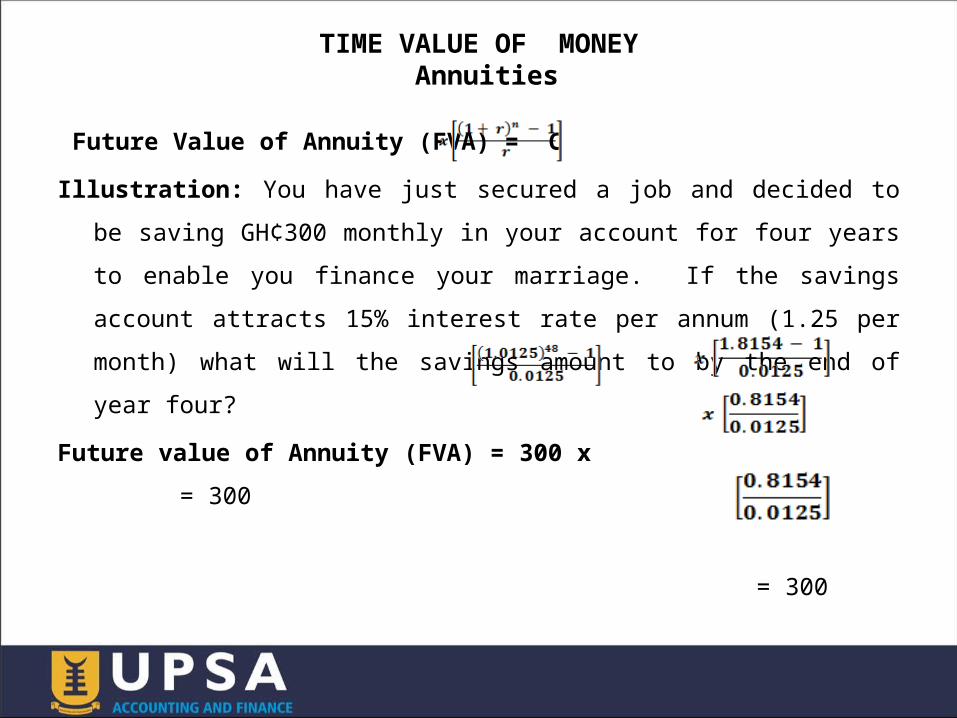

Future Value of Annuity (FVA) = C

Illustration: You have just secured a job and decided to be saving GH¢300 monthly in

your account for four years to enable you finance your marriage. If the savings

account attracts 15% interest rate per annum (1.25 per month) what will the savings

amount to by the end of year four?

Future value of Annuity (FVA) = 300 x = 300

= 300

= 300 x

= 300 x 65,232

= GH¢19,569.6

TIME VALUE OF MONEY Annuities

Exercise: Suppose you have a pension plan for which you deposit GH¢2,000 every

year into a retirement account that pays 8% interest per annum. If you retire in 30

years, how much will you have? Check; GH¢226,566

Values of Annuity Due:

• Calculating the present or future of an annuity due involves two steps:

• Calculate the present or future of ordinary annuity

• Multiply the answer by (1 + r), where r is the discount rate

• Now assume all the annuity payments discussed above were made at the beginning

of each period. Then their present and future values will be calculated as follows.

14Prepared by Alhaj Nuhu Abdulrahman

TIME VALUE OF MONEY Annuities

Present Value of Annuity (PVA) (1 + r)

= (1.015)

= GH¢9,681 x (1.015) = GH¢9,826

Future Value of Annuity (FVA) = c (1 + r)

= 300 x (1.0125)

= GH¢19,569.6 (1.0125)

= GH¢19,814.22

15Prepared by Alhaj Nuhu Abdulrahman

TIME VALUE OF MONEY Annuities

• Perpetuity refers to the equal stream of payments that continue forever. Perpetuities

are also called consols in Canada and the United Kingdom. An example of

investment with perpetuity payment is preference shares. Another example is a

particular British government Bonds called consols.

• The present value of perpetuity =

• Illustration: A company issued preference shares for GH¢50 each with fixed

dividend rate of 20% per annum. If your investment in this security is GH¢1,000

and you require a return of 8%, what is the value of this investment?

The yearly dividend payment will be 20% x GH¢1,000 = GH¢200.

• Thus, present value = = GH¢2,500

16Prepared by Alhaj Nuhu Abdulrahman

TIME VALUE OF MONEYPerpetuities

• Whenever a lender approves a loan facility, provisions will be made for repayment

of both the principal and agreed interest over the agreed period. • The three basic types of loans and their repayment plans are:

Pure Discount loans

Interest-only loans

Amortized loans

• Pure Discount loans: This type of loan involves the borrower receiving money

now, but repays a single sum at future agreed period. So if you borrow GH¢100 at

10% interest rate and to pay a single sum at the end of the year, becomes a pure

discount loan. The single sum will be (1.10) 100 = GH¢110.

• Suppose as a lender you agree to grant a loan at 12% interest rate per annum for

five years, which requires the borrower to pay GH¢25,000 at the end of the 5 th

years. How much should you give? This requires application of present value (PV)

at 12% for five years.

17Prepared by Alhaj Nuhu Abdulrahman

Loan Types and Repayment Plans

Thus, PV = = = = GH¢14,186 Treasury bills are typical examples of pure discount loans.

• Interest-only loans: This type of loan requires the borrower to pay only interest at

each agreed interval period and repay the loan amount (principal) at the end of the

agreed future time.

• For example, if a loan of GH¢1,000 for three years is to pay only 10% interest per

annum, what will be the repayment schedule?

• Interest payment for each of years 1 & 2 = Principal x interest rate

= GH¢1,000 x

0.10 = GH¢100

• Final payment at the end of year 3 = GH¢1,000 (1.10) = GH¢1,100

• Corporate bonds are examples of this type of loans.

18Prepared by Alhaj Nuhu Abdulrahman

Loan Types and Repayment Plans

=

• Amortized loans: With amortised loan parts of the principal and interest on

outstanding principal balance are paid by regular instalments, till the loan is fully

paid off. The process of paying off the loan by regular principal reductions is called

amortizing the loan or loan amortization.

• The two basic types of loan amortization are:

Declining total payments

Fixed total payments

The declining total payments: Under this payment plan, a fixed part of the principal

is paid along with interest amounts at regular intervals calculated on the

outstanding principal balances, resulting in declining total instalment payments.

19Prepared by Alhaj Nuhu Abdulrahman

Loan Types and Repayment Plans

• Illustration: A business borrowed GH¢6,000 from its bank for one year at 18%

interest per annum, which requires monthly total payments, comprising a monthly

fixed part principal and interest on outstanding monthly principal balances.

Steps for calculating the declining total payments

1st payment:

Step1 - monthly principal payment (PP) = Principal (P)/number of payments (n)

PP = = = GH¢500

Step2 – monthly interest = P x monthly rate (r) = GH¢6,000 x 0.015 = GH¢90

Step3 – total payment = GH¢500 + GH¢90 = GH¢590

2nd payment: Principal balance is (GH¢6,000 - GH¢500) GH¢5,500.

So second interest is GH¢5,500 x 0.015 = GH¢82.50

Thus, second total payment is GH¢500 + GH¢82.50 = GH¢582.50.

20Prepared by Alhaj Nuhu Abdulrahman

Loan Types and Repayment Plans

Amortisation schedule for 12 months declining total paymentsMonth Beginning Total Principal Interest Ending

Balance Payment Payment Payment Balance (GH¢) (GH¢) (GH¢) (GH¢) (GH¢)

1 6,000 590.00 500 90.00 5,500

2 5,500 582.50 500 82.50 5,000

3 5,000 575.00 500 75.00 4,500

4 4,500 567.50 500 67.50 4,000

5 4,000 560.00 500 60.00 3,500

6 3,500 552.50 500 52.50 3,000

7 3,000 545.00 500 45.00 2,500

8 2,500 537.50 500 37.50 2,000

9 2,000 530.00 500 30.00 1,500

10 1,500 522.50 500 22.50 1,000

11 1,000 515.00 500 15.00 500

12 500 507.50 500 7.50 0

6,585.00 6,000 585.00•

21Prepared by Alhaj Nuhu Abdulrahman

Loan Types and Repayment Plans

• Fixed total payments: Under this payment method, each period payment is

composed of increased part principal amount and decreased interest amount

calculated on outstanding principal balances. Since the periodic payments are fixed

it is a form of ordinary annuity, thus the ordinary annuity equation will be used to

determine the periodic payment amount (PP). The interest amount = P x r.

Thus, P = PP – Interest amount

Illustration: Supposing the GH¢6,000 loan facility discussed above is to be

amortised by fixed total payments, the amortization schedule look as follows:

Steps for calculating the fixed total payments

• Since monthly payment is equal the present value ordinary annuity formula is used.

PV = , 6,000 = , 6,000 = , 6,000 =

6,000 = C x 10.9087,

C = = GH¢550.12

22Prepared by Alhaj Nuhu Abdulrahman

Loan Types and Repayment Plans

Amortization Schedule for 12 monthly fixed total installmentsMonth Beginning Total Principal Interest Ending

Balance Payment Payment Payment Balance (GH¢) (GH¢) (GH¢) (GH¢) (GH¢)

1 6,000.00 550.12 460.12 90.00 5,539.88 2 5,539.88 550.12 467.12 83.00 5,072.76 3 5,072.76 550.12 474.12 76.00 4,598.64 4 4,598.64 550.12 481.14 68.98 4,117.50 5 4,117.50 550.12 488.36 61.76 3,629.14 6 3,629.14 550.12 495.69 54.43 3,133.45 7 3,133.45 550.12 503.12 47.00 2,630.33 8 2,630.33 550.12 510.67 39.45 2,119.66 9 2,119.66 550.12 518.33 31.79 1,601.33 10 1,601.33 550.12 526.12 24.00 1,075.21 11 1,075.21 550.12 533.99 16.13 542.21 12 542.21 550.12 541.99 8.13 0.22 6,601.44 6,000.77 600.67

23Prepared by Alhaj Nuhu Abdulrahman

Loan Types and Repayment Plans