the story of three children‘s hospitals in various stages of captive development

TRANSCRIPT

The Story of Three Children‘s Hospitals in Various Stages of

Captive Development

Moderated by:

Todd HagemeierAlliant Insurance Services, Inc.

Managing Director, Executive Vice President

Keith LindloffChildren‘s Health

Director Insurance Services

Children‘s HealthOur transition to a

Risk Bearing Captive Story

Children’s Insurance Company(CIC)

• Parent Organization: Children’s Medical Center of Dallas

• Independent pediatric hospital

• Two full service hospitals, total of 442 beds in operation

• 3 subsidiary physician organizations employing appx 100 physicians

• Level I Trauma Center; Level III NICU

• Affiliated with UT Southwestern Medical School

Children’s Insurance Company (CIC)

• Captive created in 1990 to provide access to reinsurance markets, esp. Employers’ Reinsurance

• Domiciled in Vermont due to Board concerns about public perception

• Issued policies for excess Professional & General Liability, 100% reinsured

• Retained no risk for first 25 years

Children’s Insurance Company (CIC)

• Children’s Medical Center has been a very conservative organization with regard to risk as well as finance

• Children’s Medical Center has been a financially strong organization – well-supported by community; favorable reimbursement structure

• Successful tort reform in Texas lowered the temperature regarding Professional Liability

Children’s Insurance Company (CIC)

• Challenge: Developing the organizational will to assume more risk

• Elements that came together: – New Strategies– Continued increase in primary HPL premium despite

excellent loss history– New CFO– Desire to remove costs from Operations budget

Children’s Insurance Company (CIC)

• Jan. 1 2014 – Assumed primary Professional and General Liability in CIC

• Near term plans:– Add employed physicians – Issue ‘deductibles’ policy to consolidate budgeting for all

losses within deductibles– Review of all coverages with an eye to utilizing CIC

Karen A. WardellCook Children‘s Health Care

SystemAssociate General Counsel

Cook Children‘sOur Captive Success

Story

Cook Children‘s Health Care System

enter picture

Cook Children’s Health Care System is a not-for-profit, pediatric health care organization based in Fort Worth, Texas

Cook Children’s Health Care System

W.I. Cook

Foundation, Inc.

Cook Children’s Health Care

System

Cook Children’sHome Health

Cook Children’sPhysician Network

Cook Children’sMedical Center

Cook Children’s NE Hospital,

LLC

Cook Children’s Surgical Center,

LLC [Plano]

Cook Children’sHealth Plan

Cook Children’sIndemnity Company

Cook Children’s Health Services,

Inc.

Rosedale Office

Building, Inc. 501(c)(2)

Cook Children‘s Indemnity Company

• CCIC was licensed & capitalized in 2002 in response to a hardening insurance market

• CCMC historically maintained a self-insured trust for its HPL and purchased excess insurance

• Its physician group purchased first dollar coverage• In the early 2000’s, we started seeing declining capacity for

medical malpractice • Carriers abandoned the market and/or refused to insure certain

medical specialties• In 2002, the cost of insuring our 200 employed physicians was

over $5M• Primary purpose was to provide a vehicle to self-insure the

medical malpractice exposure of Cook Children’s Health Care System & its employed physicians

Coverage and Limits

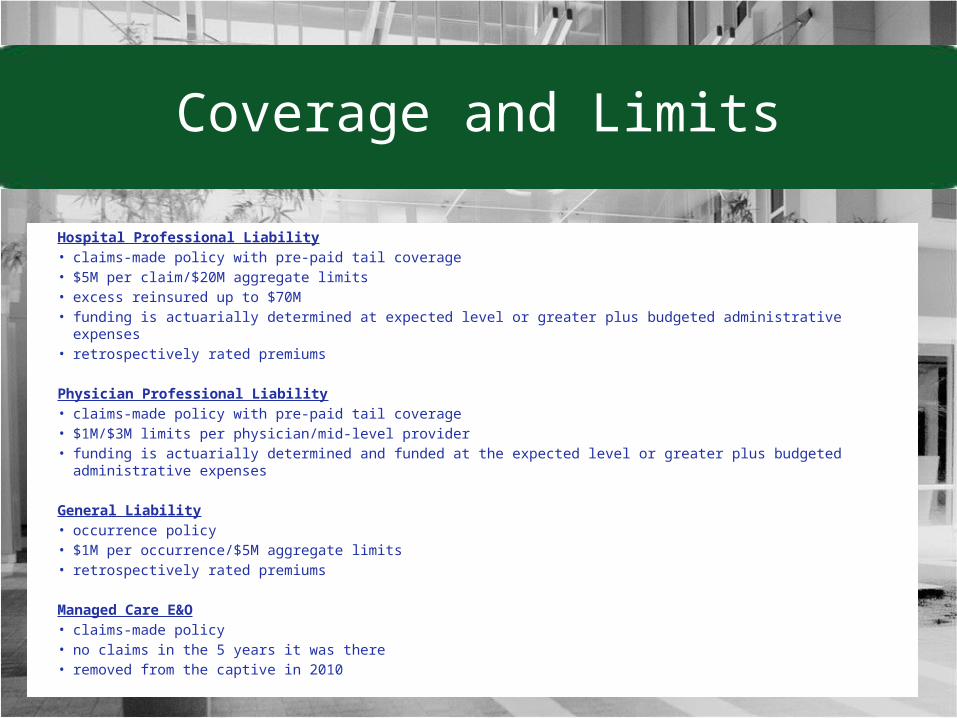

Hospital Professional Liability• claims-made policy with pre-paid tail coverage• $5M per claim/$20M aggregate limits• excess reinsured up to $70M• funding is actuarially determined at expected level or greater plus budgeted administrative expenses • retrospectively rated premiums

Physician Professional Liability• claims-made policy with pre-paid tail coverage• $1M/$3M limits per physician/mid-level provider• funding is actuarially determined and funded at the expected level or greater plus budgeted

administrative expenses

General Liability• occurrence policy• $1M per occurrence/$5M aggregate limits• retrospectively rated premiums

Managed Care E&O• claims-made policy• no claims in the 5 years it was there• removed from the captive in 2010

• Premium paid to CCIC since December 2002 - $92M

• Premium net of reinsurance - $80M (Amount actuaries say we should have paid)

• Total paid losses to date - $6.8M

• Dividend/retrospective premium returned to System - $68M

HOW?

• Medical malpractice tort reform enacted in Texas in 2003 made it easier to accurately predict future costs

non-economic damages caps at $250,000 per occurrence for any and all non-institutional health care providers (most commonly, physicians) with a second $250,000 cap per occurrence for each health care institution with a limit of $500,000 total for all health care institutions

2 year statute of limitations

10 year statute of repose

all wrongful death damages remained capped at an indexed cap, which is about $1.8M and includes punitive damages

• Apology & disclosure policy developed and implemented

See Lee Taft, Apology & Medical Mistake: Opportunity or Foil?, 14 Annals of Health Law 55 (2005).

Melissa MurrahTexas Children‘s HospitalDirector – Risk Management

Texas Children’s Our Super Captive

Insurance Company Story

Overview of Texas Children‘s Hospital

• Groundbreaking ceremonies were held on May 23, 1951 for a three story, 106 bed pediatric hospital

• Teaching affiliation established at that time with Baylor College of Medicine that is still in place

• Neurological Research Institute, the world’s first basic research institute dedicated to childhood neurological diseases, opened in 2010

• The Pavilion for Women, providing women, mothers and babies with a full continuum of high quality healthcare, opened in 2011

• EPIC installed system wide in 2012• In 2013, Texas Children’s had 3.2 million patient encounters and

performed 26,000 surgeries• Today - 644 beds and 230 employed physicians

Overview of TCH Insurance Company, Ltd. (“TCHICO”)

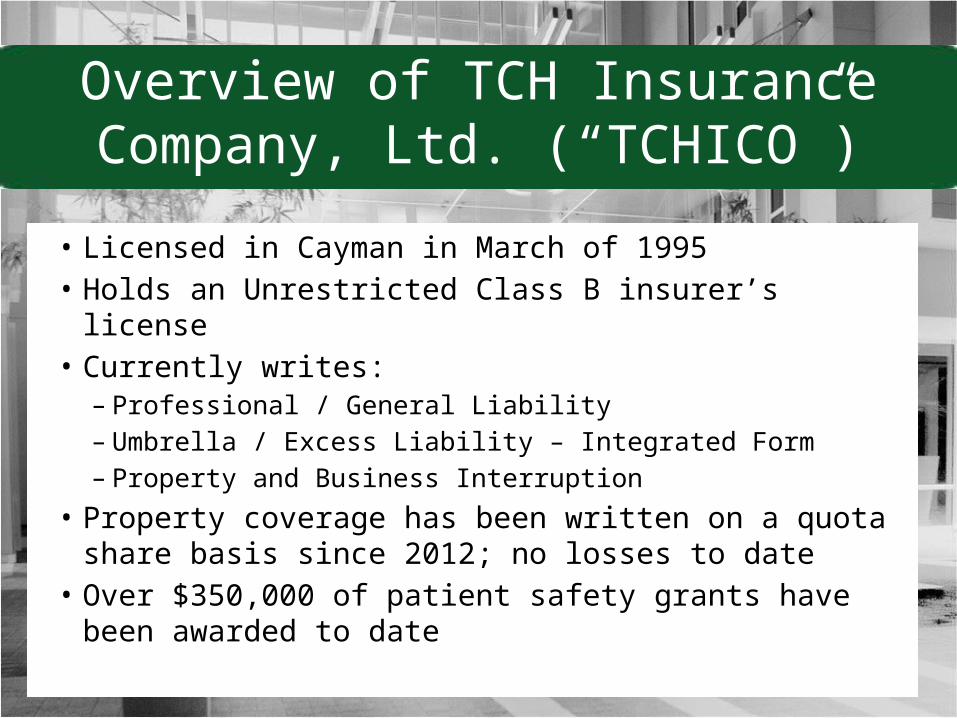

• Licensed in Cayman in March of 1995• Holds an Unrestricted Class B insurer’s license• Currently writes:– Professional / General Liability– Umbrella / Excess Liability – Integrated Form– Property and Business Interruption

• Property coverage has been written on a quota share basis since 2012; no losses to date

• Over $350,000 of patient safety grants have been awarded to date

Texas Children’s ERM Initiative

• Texas Children’s has a very robust and interactive ERM initiative that started in 2012

• Board oversight of our ERM initiative is provided by the Chairman of our Risk Management & Insurance Committee

• Our ERM protocol involves the use of a Risk Register, a Heat Map and Aggregate Risk Scores that lead to a red, yellow or green ranking for each enterprise risk that is identified

• We are tracking fifty-two enterprise risks, including a “Fine Fifteen”

• TCHICO is an integral part of our Risk Mitigation Strategy and Action Plan and the possible utilization is always a part of our analysis

Sample ERM Risk RegisterHeat Map

Heat Map

Like

lihoo

d of

Occ

urre

nce

AlmostCertain

Likely

Moderate

Unlikely

Rare

Insignificant Minor Moderate Major Severe

Potential Impact to TCH(Financial Value & Organizational Reputation/Regulatory Compliance/Operational Status)

ERM Risk Category

ERM Risk Detail

ERM Risk Definition

ERM Risk Owner

Inherent Risk Score

Risk Management/Mitigation

Activities

Risk Management/Mitigation

Measurements

IndividualResidual Risk

Score

AggregatedResidual

Risk Score Activities/Tasks2014 20142014

What are the key applications of people, process or technology used to manage / mitigate / monitor the risk?

What is the objective measurement criteria used to measure the effectiveness of each management / mitigation activity?

Where is the actual risk today?

What actions are needed to enhance management, mitigation or monitoring efforts?

Other Possible Risk Areas for TCHICO Being Investigated

• HMO Reinsurance• Medical Stop Loss• Biomedical Maintenance• Property and Casualty Deductibles• Regulatory (Billing E&O) Risk• Property (Higher Limits)• ROCIP Coverages– Builder’s Risk– Primary Casualty– Excess Liability

Questions