the statutory framework for financial...

TRANSCRIPT

922359 Page 1

THE STATUTORY FRAMEWORK FOR

FINANCIAL REPORTING

Discussion Document

September 2009

922359 Page 2

ISBN 978-0-478-33673-3 (PDF) ISBN 978-0-478-33674-0 (HTML) © Crown Copyright First Published September 2009 Competition, Trade and Investment Branch Ministry of Economic Development PO Box 1473 Wellington New Zealand http://www.med.govt.nz Permission to reproduce: The copyright owner authorises reproduction of this work, in whole or in part, so long as no charge is made for the supply of copies, and the integrity and attribution of the work as a publication of the Ministry is not interfered with in any way.

922359 Page 3

Table of Contents

Page Information for Submitters 5 Abbreviations 6 Questions for Submitters 7 Executive Summary 10 Introduction 17 Part 1: Objectives of the Review 18 Part 2: Problem definition 19 Part 3: Institutions and Statutory Responsibilities 20

3.1 Background 20 3.2 Options for Making Accounting and Auditing Standards 24 3.3 Options for Making Tiers of Financial Reporting 25

Part 4: Financial Reporting Principles and Indicators 27 4.1 Identifying the Principles and Indicators 27 4.2 Applying the Indicators to Preparation, Publication and Assurance 30 Part 5: The Application of the Indicators to For-Profit Entities 34

5.1 Background 34 5.2 For-Profit Entities and Public Accountability 35 5.3 For-Profit Entities and Economic Significance 35

5.3.1 Background 35 5.3.2 Applying the Economic Significance Indicator to For-

Profit Entities 36 5.4 For-Profit Entities and Management-Ownership Separation 38

5.4.1 The Application of the Indicators 38 5.4.2 Preparation by Small and Medium Companies 40

5.5 Conclusions on For-Profit Entities 42 Part 6: The Application of the Indicators to the Public Sector 43 Part 7: The Application of the Indicators to Private Non-Profit Entities 45

7.1 Background 45 7.2 Non-Profit Entities and Public Accountability 47 7.3 Non-Profit Entities and Economic Significance 48 7.4 Non-Profit Entities and Separation 49 7.5 The Implications for Small Non-Profit Entities 49 7.6 Conclusions on Non-Profit Entities 51

922359 Page 4

Part 8: The Application of the Indicators to Māori Asset Governance Entities 53 8.1 Background 53 8.2 Māori Trust Boards (Maori Trust Boards Act 1955) 53 8.3 Te Ture Whenua Māori Act Entities 54

8.3.1 Māori incorporations 55 8.3.2 Māori reservations 56 8.3.3 Māori land trusts 57

8.4 Conclusions on Māori Governance Entities 58 Part 9: Other Issues 59

9.1 Consequential Issues 59 9.1.1 Assurance standards enforcement 59 9.1.2 Changing monetary thresholds 62 9.1.3 The exemption powers in the FRA 62 9.1.4 Inactive entities 63 9.1.5 The solvency test 64

9.2 Other Issues 64 9.2.1 Parent company financial statements 64 9.2.2 Filing by contributory mortgage brokers 67 9.2.3 The filing deadline for companies 68 9.2.4 Remuneration disclosures in relation to key management 69 9.2.5 Out-of-date language in other legislation 71

Part 10: The New Zealand-Australia Implications 72 Appendix: A summary of MED’s proposals for each class of entity 77

922359 Page 5

Information for submitters

Queries about the review and submissions in response to this discussion document should be sent to:

Email: [email protected]

Post: Review of the Financial Reporting Framework Competition, Trade and Investment Branch Ministry of Economic Development PO Box 1473 Wellington

Phone 04 4742 914 or 04 4624 239 Fax: 04 4991 791 It would be useful if submissions sent in hard copy or faxed were also provided in electronic form (PDF, Microsoft Word 2000 or compatible format).

Questions in the discussion document are intended to provide a focus for the issues. Broader comment on the issues will also be welcomed.

The closing date for submissions is Friday 29 January 2010.

Publication of submissions, the Official Information Act and the Privacy Act

Other than submissions that may be defamatory, the Ministry intends publishing all submissions on its website http://www.med.govt.nz. The Ministry will not publish your submission on the internet if you have any objection to its publication. However, it will remain subject to the Official Information Act 1982 and may, therefore, be released in part or full. The Privacy Act 1993 also applies.

When making your submission, please state if you have any objections to the release of any information contained in your submission. If so, please identify which parts of your submission you are requesting to be withheld and the grounds under the Official Information Act 1982 for doing so (e.g. that it would be likely to unfairly prejudice the commercial position of the person providing the information).

Disclaimer

Views expressed in this discussion document are the preliminary views of the Ministry of Economic Development and do not reflect government policy.

Readers are advised to seek specific advice from an appropriately qualified professional before undertaking any action in reliance on the contents of this discussion document. The Crown does not accept any responsibility whether in contract, tort, equity, or otherwise any action taken or reliance placed on, any part, or all, of the information in this document, or for any error or omission from this document.

Acknowledgment

The Ministry would like to thank members of a steering group that provided MED with advice and a report which has contributed to the development of this discussion document. In particular, we would like to thank Joanna Perry, Kevin Simpkins, Bede Fraser, Patricia McBride, Vanessa Sealy-Fisher, Carole Greer and Kimberley Crook.

922359 Page 6

Abbreviations

AASB Australian Accounting Standards Board AIFRS Australian equivalents to International Financial Reporting Standards ASIC Australian Securities and Investments Commission ASRB Accounting Standards Review Board (NZ) AUASB Auditing and Assurance Standards Board (Australia) FASB Financial Accounting Standards Board (US) FDR Framework for Differential Reporting FRA Financial Reporting Act 1993 FRO Financial Reporting Order 1994 FRC Financial Reporting Council (Australia) FRS Financial Reporting Standards FRSB Financial Reporting Standards Board of the New Zealand Institute of

Chartered Accountants FTE Full time equivalent GAAP Generally accepted accounting practice GPFR General purpose financial reports IASB International Accounting Standards Board IASCF International Accounting Standards Committee Foundation ICAA Institute of Chartered Accountants in Australia ICANZ Act Institute of Chartered Accountants of New Zealand Act 1996 ICNPO United Nations International Classification of Nonprofit Organisations IFAC International federation of Accountants IFRS International Financial Reporting Standards IMF International Monetary Fund IOSCO International Organisation of Securities Commissions IPSASB International Public Sector Accounting Standards Board ISA International Standards on Auditing MED Ministry of Economic Development MOU The Trans-Tasman Memorandum of Understanding on the

Coordination of Business Law NZICA New Zealand Institute of Chartered Accountants (‘Institute’) NZ IFRS New Zealand equivalents to International Financial Reporting

Standards NZ Framework The New Zealand equivalent to the IASB Framework for the

Preparation and Presentation of Financial Statements NZ Preface New Zealand Preface to New Zealand equivalents to International

Financial Reporting Standards and Financial Reporting Standards PBE Public Benefit Entity PSB Professional Standards Board of the New Zealand Institute of

Chartered Accountants SEM Single Economic Market TTAASAG Trans-Tasman Accounting and Auditing Standards Advisory Group TTWMA Te Ture Whenua Māori Act 1993 XRB External Reporting Board (proposed for NZ)

922359 Page 7

Questions for submitters

Institutions and statutory responsibilities (Part 3)

Q1 What comments do you have on the proposal to transfer the Institute’s financial reporting and assurance standards responsibilities to a reconstituted ASRB?

Q2 What comments do you have on the proposals for the manner of setting the number of tiers and the qualifying criteria for each tier?

Financial reporting principles and indicators (Part 4)

Q3 What comments do you have on the Primary Principle and the Indicators of financial reporting? Should any other principles and/or indicators be considered?

Q4 What comments do you have on our broad conclusions in relation to preparation, publication and distribution; and assurance?

The application of the indicators to for-profit entities (Part 5)

Q5 What comments do you have on the tests (annual income, total assets and employee numbers) for determining whether a for-profit entity is economically significant? What comments do you have on the two-out-of-three test or the alternative “revenue plus one other” approach outlined in Section 5.3.1? What comments do you have on the current thresholds of $20m revenue, $10m assets and 50 FTE employees?

Q6 What comments do you have on the proposal to make no changes to the filing requirements for companies with 25% or more overseas ownership?

Q7 What comments do you have on the proposal to remove filing requirements for overseas-incorporated companies whose New Zealand businesses are not large?

Q8 What comments do you have on the preparation/opt-out and no-preparation/opt-in proposals for for-profit entities that meet the Separation Indicator only?

Q9 What comments do you have on the criteria we have used to illustrate the proposals described in the previous question (i.e. (a) 10 or more shareholders for identifying companies with a significant number of shareholders; (b) 5% of voting shares by value for opt-in; and (c) no vote against for opt-out and opt-down)?

Q10 What comments do you have on the proposal to remove the requirement for medium and small companies to prepare GPFR? What are the compliance cost implications?

Q11 What comments do you have on the Australian ‘grandfathering’ provision, exempting existing large companies at the time of the law change, from lodging financial statements with ASIC?

922359 Page 8

Q12 What comments do you have on the advantages and disadvantages of requiring large non-issuer companies (and other entities impacted) to file financial statements under a ‘grandfathering’ regime?

The application of the indicators to public sector entities (Part 6)

Q13 What comments do you have on the proposal to retain the requirements for all public sector entities to publish assured GPFR?

Q14 Do you consider that the changes outlined in Part 3 will provide an appropriate framework for public sector entity standards setting?

The application of the indicators to private non-profit entities (Part 7)

Q15 What comments do you have on the proposal to use annual operating expenditure as the means for determining whether a private non-profit entity is small, medium or large?

Q16 What comments do you have on the proposals to use annual operating expenditure of $20,000 and $20 million as the cut off points between small and medium, and medium and large respectively? If you consider that other criteria should be used, what are those criteria and what cut-off points should be used?

Q 17 What comments do you have on the proposal that financial reporting obligations outlined in this Part would not apply to gaming machine societies?

Q18 What are your views on the preparation, distribution, publication and assurance proposals appearing in Part 7.6 and the Appendix insofar as it relates to private non-profit entities?

The application of the indicators to Māori asset governance entities (Part 8)

Q19 What are your views on the proposal to make no changes in relation to Māori trust boards?

Q20 What are your views on the proposals appearing in Part 8.3.1 in relation to Māori incorporations as summarised in Part 8.4?

Q21 What are your views on the proposal to make no changes in relation to Māori reservations?

Q22 What are your views on the proposal for the Māori Land Court to continue to have the responsibility for setting financial record keeping and reporting obligations for Māori land trusts?

Q23 What are the advantages and disadvantages of requiring economically significant Maori land trusts to publish GPFR?

Consequential issues (Part 9.1)

Q24 What are your views on the advantages and disadvantages of giving assurance standards the force of law?

922359 Page 9

Q25 What are your views on the proposal to make it an offence to unduly influence, coerce, manipulate or mislead an auditor?

Q26 What are your views on the proposal to make it an offence to recklessly or knowingly include false or deceptive matters in an audit report?

Q27 What are your views on the proposal to introduce a requirement to change statutory monetary thresholds within a certain time period? What are your views on the ten year proposal?

Q28 What are your views on the proposals appearing in Part 9.1.3 concerning the three exemption powers?

Q29 What are your views on the proposed change to the solvency test?

Other issues (Part 9.2)

Q30 Do you consider that the parent company preparation and filing requirements should be retained, modified or removed? What are the compliance cost implications?

Q31 Assuming the parent company requirements were to be modified, what modifications should be made?

Q32 What are your views on the proposal to require contributory mortgage brokers and the broker’s nominee company to make GPFR available to investors?

Q33 Do you consider that the filing deadline for entities with publication requirements should be reduced? What are your views on the IMF suggestion of four months?

Q34 What are your views on the issues relating to remuneration disclosures for key management personnel?

New Zealand-Australia Single Economic Market (Part 11)

Q35 Do you have any comments on the proposals appearing in this document from a Single Economic Market perspective?

MED’s proposals for each class of entity (Appendix)

Q36 Do you have any comments on the proposals in the table in the Appendix?

General question

Q37 Do you have any other comments?

922359 Page 10

Executive summary

This discussion document should be read together with a companion discussion document released simultaneously by the ASRB entitled Proposed Application of Accounting and Assurance Standards under the Proposed New Statutory Framework for Financial Reporting.

The main purposes of the MED document are to propose changes to the standards-setting infrastructure and discuss which entities should have financial reporting obligations. The main purpose of the ASRB discussion document is to identify the changes that it would implement in the event that the changes that are outlined in the MED document were to be enacted. This division between the two documents is consistent with the division of responsibilities, which is as follows:

• The Government and Parliament should decide which entities will have reporting obligations (i.e. the “Who” question); and

• The ASRB should decide on the reporting obligations for each class of reporting entity (i.e. the “What” question).

The issues and the main preliminary conclusions in relation to the MED discussion document are summarised below.

Part 1: Objectives

The main objective is to create a financial reporting framework that is coherent, complete and consistent. There is also a need to balance the benefits of financial reporting against the compliance costs, to have a system that is as simple and clear as practicable and promote New Zealand-Australia financial reporting convergence.

Part 2: Problems

The discussion document identifies a large number of issues. The three major issues are as follows:

a. The inconsistencies between the financial reporting principles and the actual GPFR preparation, audit and publication requirements – in particular, some stakeholders have concerns about the current obligation on all companies to prepare GPFR;

b. The ASRB does not have the power to approve standards for some classes of entities that have statutory requirements to prepare financial statements. In particular, it cannot approve standards for Registered Charities. From a user perspective, this reduces the value of the financial information filed with the Charities Commission because the recognition and measurement principles and rules applied by the preparer may be unclear and the lack of consistency makes it more difficult for users of financial statements to compare entities; and

c. The allocation of statutory functions is inefficient, incomplete, inconsistent and, in some respects, opaque. For example, the standards setting functions are split between two bodies, there are no standards for Registered Charities, entities with similar user needs are treated differently and parts of the financial reporting system do not work in ways that would be expected based on a plain reading of the FRA.

922359 Page 11

Part 3: Institutions and statutory responsibilities There are three broad issues in relation to the financial reporting infrastructure. First, the FRA is silent about the responsibility for making financial reporting strategy-related decisions. This means that most strategic decisions are made by the FRSB or in an indirect way through the standards setting process. However, the ASRB is unable to initiate the process of making a standard. It must therefore seek to persuade the FRSB to make strategically important proposals to the ASRB. Corporate governance principles would suggest that the peak body (I.e. the ASRB) should be responsible for setting the strategic direction within the broader framework provided by the FRA. Secondly, the reporting system is not structured in the way that one would expect based on a plain reading of the Act. For example, the Act identifies two tiers of reporting. In fact, an intermediate tier was created by the two standards bodies, for very good reasons, by using a statutory power that was not obviously designed for such a purpose. Thirdly, the financial reporting standards-making responsibilities are split between the ASRB and the Institute. Assurance standards making is the sole responsibility of the Institute. These processes are inconsistent with the need for standards to be seen to be designed and approved in ways that are independent of the interests of the accounting profession. We are proposing to deal with these problems by consolidating all functions, along with the responsibility for making and approving assurance standards within a reconstituted ASRB, to be called the XRB. Thus, the XRB would be responsible for setting the strategy and designing and approving financial reporting and assurance standards. The other major issue addressed in this section relates to the processes for deciding the number of tiers of financial reporting and the qualifying criteria for each tier. Some of those decisions have been made by Parliament, others by the Government, and yet others jointly by ASRB and the FRSB. We conclude that there should be a single process for all such decision making. Our specific proposal is that the XRB should make recommendations to the Responsible Minister, who would decide to accept or reject them as a whole or refer them back to the XRB for further consideration. Part 4: Financial reporting principles and indicators Part 4 describes and discusses the purpose, principles and indicators of financial reporting. The overarching reason for imposing financial reporting obligations is to provide information to external users who have a need for an entity’s GPFR but are unable to demand them. There are three indicators that financial reporting is needed:

• Public accountability – Public accountability arises when an entity receives money direct from the public. The main examples are non-profit public sector entities, issuers of securities and charities;

922359 Page 12

• Economic significance – Large entities can have a significant impact on the national or regional economy if they fail. Therefore, there can be a broad societal interest. This is particularly important for suppliers who extend credit to facilitate sales, customers who prepay for goods and services and employees who have part of their compensation deferred; and

• The separation of ownership and management – There is a concern that managers of an entity may not manage owners’ and members’ money as well as the owners would themselves. Therefore, owners and members need access to financial information where there is a certain degree of ownership separation from management.

The remainder of Part 4 outlines our broad conclusions about what those indicators mean in terms of preparation, assurance and publication or distribution of GPFR. More detailed discussions of the application of the indicators appear in subsequent parts of the discussion as follows:

• Part 5: For-profit entities;

• Part 6: Public sector entities;

• Part 7: Private non-profit entities; and

• Part 8: Māori asset governance entities.

Appendix One summarises those parts by describing the status quo and outlining proposals for all entity forms in tabular form.

Part 5: The application of the indicators to for-profit entities

Preparation requirements for companies

The main issue in this section is whether every company should continue to be required to prepare financial statements annually. We note that none of the indicators of financial reporting apply to 98-99% of companies. We therefore conclude that the requirements to prepare financial statements should be removed for all but the 1-2% of companies that are issuers, large and/or do not have separation. The following points are also made:

• The requirement on all companies to keep proper accounting records should be retained;

• Even though small and medium companies would not be automatically required to prepare GPFR, shareholders should be able to require the company to prepare and, if so, have an assurance engagement completed; and

• While the requirement to prepare GPFR would be removed, special purpose reporting (e.g. for taxation purposes) would still involve the preparation of accrual-based financial reports to a minimum standard.

922359 Page 13

• Special rather than general purpose reporting is likely to substantially reduce compliance costs. Medium companies are likely to be able to reduce their use of sophisticated measure techniques (e.g. impairment tests), apply accounting policies that are targeted at the special purpose use (e.g. tax depreciation rates) and substantially reduce the number of notes to the accounts (i.e. both detailed breakdowns of major items and additional disclosures (e.g. directors’ remuneration and interests). There is also likely to be a reduced need for notes to financial reports prepared by small companies.

Filing by large non-issuer companies

Other large non-issuer companies and other for-profit entities are not required to file financial statements.1

We are seeking views on the approach adopted in Australia in regards to this issue. In 1995 the Australian Parliament introduced a requirement for new proprietary companies that were large to lodge GPFR with ASIC. However, proprietary companies that were incorporated prior to 1995 (that were either large at the time or subsequently became large) do not have to lodge. These “grandfathered” large proprietary companies only have to prepare GPFR and have them audited. This policy has had a significant impact over time and about 70% of large proprietary companies are now required to lodge GPFR with ASIC. However, large proprietary companies that now file financial statements make up a small proportion, just 0.3% in total, of the 1.6 million registered companies in Australia.

The application of the economic significance indicator to large non-issuer companies may mean that the companies GPFR help to contribute to good business decision-making, may ensure that financial disciplines that are placed on issuers are extended to non-issuer companies, and ensures, due to their economic significance, that creditors, employees and other stakeholders have good information about the company.

We are also seeking submitter views on the advantages and disadvantages of requiring large non-issuer companies (and other entities that may be impacted, such as not-for-profit entities or Maori Land Trusts that meet the economic significance indicator) to file financial statements.

Filing by overseas companies

This Part also addresses overseas company filing issues. The main issue relates to overseas-incorporated companies that carry on business in New Zealand, most of which are required to file GPFR with the Registrar of Companies. The discussion document concludes that overseas-incorporated companies that are not issuers and/or not large should no longer be required to file GPFR.

Part 6: The application of the indicators to public sector entities

The issues are straightforward for non-profit public sector entities. They are all publicly accountable because the great majority of their revenues are obtained from taxpayers and ratepayers. Therefore, they should all be required to publish assured GPFR.

1 An entity is large if it exceeds any two of the following: (i) total assets of $10 million; (ii) annual revenue

of $20 million; and (iii) 50 employees. See section 19 of the FRA.

922359 Page 14

We also conclude that all for-profit public sector entities should continue to be required to publish audited GPFR because it is the most effective way of ensuring that the ultimate owners (i.e. taxpayers and ratepayers) are able to obtain access to GPFR. In addition, a small number of for-profit entities that have majority public ownership (e.g. some port companies) are issuers. The private shareholders continue to need to have access to the GPFR.

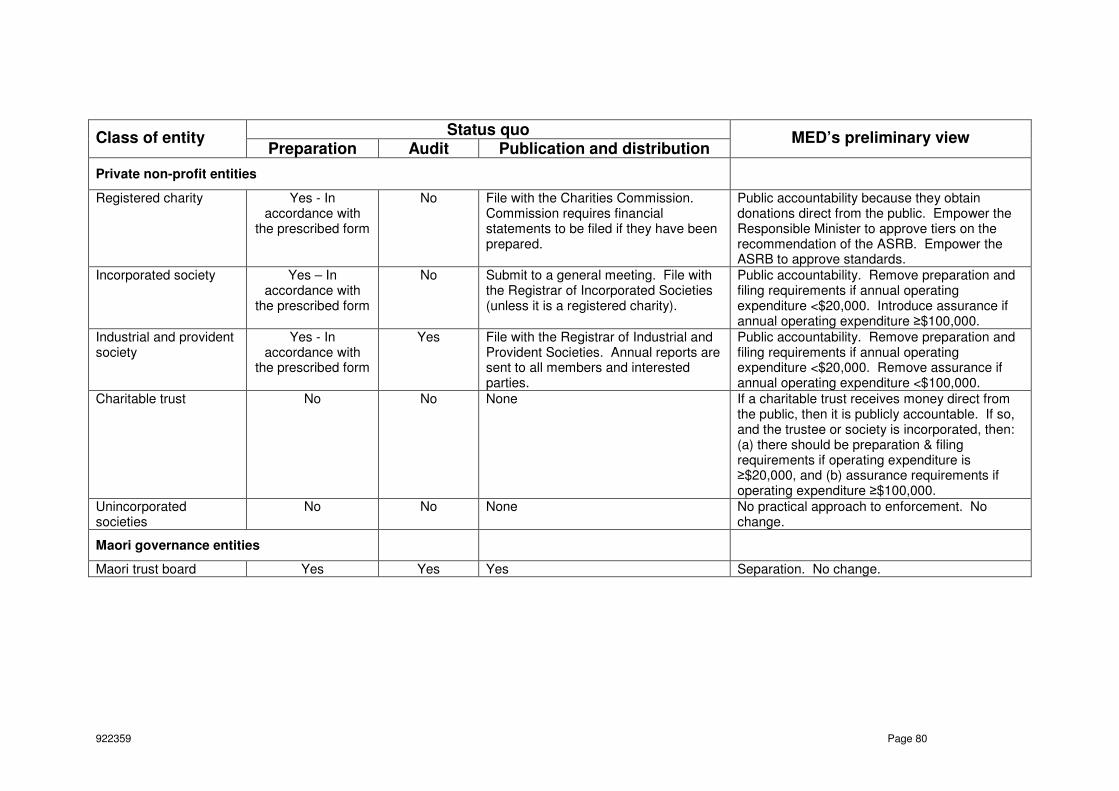

Part 7: The application of the indicators to private non-profit entities

The financial reporting obligations imposed on different classes of private non-profit entities are inconsistent among themselves and, in many respects, inconsistent with the indicators of financial reporting. For example, industrial and provident societies are required to have an audit completed but incorporated societies are not. There is no reason to treat them differently.

Another issue is that some non-profit entities, notably Registered Charities, are required to file financial information but there are no financial reporting standards underpinning the information that is filed. This creates uncertainty about the measurement and recognition principles and rules that have been used in preparing the information, which means that the information is of limited value to users.

Our main preliminary conclusions are that the following changes should be made in relation to private non-profit entities:

• The XRB should be empowered to make standards for all private non-profit entities with statutory obligations to prepare GPFR;

• Entities that accept donations from the public are publicly accountable. Nevertheless, the great majority of private non-profit entities should have no financial reporting obligations because they are too small to justify the preparation and distribution costs. Our preliminary conclusion is that only those with annual operating expenses of $20,000 or more should be required to prepare GPFR;

• Unincorporated societies (other than those that register with the Charities Commission) should have no financial reporting obligations because it is impractical to regulate and enforce regulation against those entities; and

• The Separation Indicator is likely to be met almost all of the time. Where only that indicator is met it should be for the members to decide whether the entity shall prepare GPFR and, if so, have an assurance engagement completed.

Part 8: The application of the indicators to Māori asset governance entities

The four classes of Māori asset governance entities (i.e. trust boards, reservation, incorporations and land trusts) are identified and the reporting issues are discussed. For the same reasons as discussed in relation to companies, MED has concluded that the non-large non-issuer Māori incorporations should no longer have to prepare GPFR. Likewise, shareholders should be able to require an incorporation to prepare and, if so, have an assurance engagement completed.

922359 Page 15

Part 9: Other issues

Ten secondary issues are discussed in this section. Five are issues that arise due to the application of the indicators and changing the financial reporting system outlined in Parts 3 and 5-8 of the discussion document. The other five issues would arise even if none of the changes proposed in this paper were to be made.

Of the five related issues, arguably the most important is the legal status of assurance standards approved by the XRB. Our preliminary conclusion is that assurance standards should not have the force of law because it could reduce audit quality. Our view is that it would provide incentives for auditors to take a very risk-averse box-ticking approach rather than exercising professional judgment. We note that this proposal would not change the current situation whereby the courts consider the requirements imposed under the standards in determining the duty of care owed in negligence and other civil cases.

We also express preliminary views to create the following audit-related offence provisions, which we consider would promote audit quality:

• To attempt to unduly influence, coerce, manipulate or mislead an auditor; and

• To recklessly or knowingly include false or deceptive matters in an audit report.

Of the five issues that are unrelated to the rest of the paper, arguably the most important is whether to retain the requirement for parent-only financial statements to be prepared. At present, a reporting entity that has one or more subsidiaries must prepare consolidated and parent-only GPFR. Consolidated statements are useful because they provide information about all of the assets, liabilities and activities under the parent company’s control. However, parent company statements only provide information about the parent’s investments in its subsidiaries. That information is only used by a subset of users, mainly those working in a credit risk assessment role. The issue is whether the additional costs associated with preparing parent-only financial statements are outweighed by the benefits to that subset of users. If not, the options would be to remove the requirement to prepare parent-only financial statements or require additional notes to the consolidated financial statements that would meet those users’ needs. We have not drawn any conclusions about this matter.

Part 10: The New Zealand-Australia Single Economic Market implications

There are major differences between the financial reporting frameworks applying in Australia and New Zealand. The proposals in the discussion document would bring the two countries’ reporting requirements and infrastructure much closer together. Consistency is important for the following reasons:

• To increase the opportunities for two countries’ standards bodies to remove existing differences between their standards, meaning that entities with reporting obligations in both countries would only need to prepare one set of GPFR;

• To make it easier for users in one country to interpret GPFR prepared in the other country; and

922359 Page 16

• To facilitate the creation of joint transTasman bodies at the strategic and/or standards setting level. The main driver of whether there should be separate or joint bodies is which option would maximise the two countries’ joint international influence. At present, this is achieved by the two countries having separate bodies. However, circumstances can change. Creating broad functional equivalence now would make it easier to implement mergers in the future.

922359 Page 17

Introduction

1. This MED discussion document and a companion discussion document prepared by the ASRB, entitled Proposed Application of Accounting and Assurance Standards under the Proposed New Statutory Framework for Financial Reporting, together address a number of problems with the statutory framework for financial reporting. MED addresses issues relating to the policy and law of financial reporting. The ASRB outlines how it would respond if Parliament were to enact the changes that are outlined by MED. The way that the issues are divided between the two documents is described in more detail below.

The MED discussion document

2. The MED discussion document outlines:

2.1. Proposals to rationalise the institutional arrangements and the allocation of statutory responsibilities;

2.2. A proposed statutory process for determining how the number of tiers of financial reporting and the qualifying criteria for each tier will be determined (Our preliminary view is that the ASRB should make recommendations on these matters to the Minister of Commerce, who would either accept or reject them in full, or refer them back for further consideration);

2.3. Preliminary views on whether each class of entity should be required to prepare financial statements and, if so, whether the statements will need to be audited and/or published or distributed in one way or another (e.g. filing with the Registrar of Companies); and

2.4. Some other issues with the financial reporting legal framework, such as whether the requirement to prepare parent-only financial statements should be retained.

The ASRB discussion document

3. The ASRB discussion document:

3.1. Makes proposals about the number of tiers and the qualifying criteria for each tier; and

3.2. Generally describes the nature of the financial reporting and assurance requirements tentatively proposed for each tier.

922359 Page 18

Part 1: Objectives of the Review

4. The main objective of the review is to produce a financial reporting system that works effectively and efficiently for all categories of entities in New Zealand. More specifically, the objectives are to produce a financial reporting system that:

• Is underpinned by coherent financial reporting principles;

• Weighs the benefits of financial reporting against the associated compliance costs. Those costs are as follows:

� The costs of preparing annual GPFR that would not otherwise be prepared;

� The costs of carrying out audits that would not otherwise be carried out;

� The costs associated with publishing financial statements; and

� The costs of developing and promulgating accounting and assurance standards.

• Is consistent. Entities with similar external user need characteristics should have similar financial reporting obligations;

• Is clear. The obligations that are imposed on each class of entities should be clearly defined. Clarity is needed both in terms of defining the tier of reporting an entity is included within and the resulting preparation, assurance and publication or distribution obligations that are imposed on it; and

• Facilitates the ability of the New Zealand and Australian standards setters to produce harmonised financial reporting standards. This would mean that an entity that has reporting obligations in both countries could produce a single GPFR that meets the legal requirements in both countries.

922359 Page 19

Part 2: Problem Definition

5. There are five broad sets of issues with the financial reporting system.

6. First, the allocation of responsibilities under FRA is incoherent, incomplete and, in many respects, opaque. In particular:

6.1. There is no clear rationale for the way that functions are allocated between the Government and the ASRB, with some being performed by the Institute;

6.2. The ASRB does not have the power to approve standards for some entities with financial reporting obligations (e.g. registered charities);

6.3. The FRA is silent about the allocation of the responsibility between the ASRB and the Institute for making decisions about the strategic direction of the New Zealand financial reporting system, and

6.4. Parts of the financial reporting system do not work in the way that would be expected based on a plain reading of the FRA.

7. Secondly, there are inconsistencies in the financial reporting obligations that are imposed on different entity types whose users have the same information needs. Although the principles underpinning financial reporting policy are recognised and used in many parts of the financial reporting system,2 they are not consistently applied. In many cases, the law prevents the standards setters from applying them in a fully effective manner, with some classes of entities consequentially having inappropriate reporting requirements. For example, there are no powers to make standards for Registered Charities.

8. Thirdly, the Institute has a major role in making financial reporting and assurance standards. This creates a perception that there is a lack of independence in the way that standards are set in New Zealand. In most overseas jurisdictions standards are designed and approved independently of the interests of the accounting profession.

9. Fourthly, some consequential issues arise due to the need to make changes in response to the problems outlined above. For example, if most companies were no longer required to produce GPFR there would need to be a change to the solvency test in the Companies Act, which refers to GPFR.

10. Finally, there are some other issues. For example, there is a discussion of whether the requirement to prepare parent company financial statements should be retained, modified or removed.

2 For example, they are discussed in the NZ Preface and the NZ Framework, and used in the FDR.

922359 Page 20

Part 3: Institutions and Statutory Responsibilities

PART 3.1: BACKGROUND

The status quo

Making and approving standards

11. Under the FRA:

11.1. The ASRB is responsible for reviewing and approving financial reporting standards submitted to it for approval. Standards approved by the ASRB have legal force;

11.2. The Institute is able to submit draft financial reporting standards and amendments to standards to the ASRB for approval. This function is carried out by an Institute board, the FRSB. The FRSB operates largely independently of the Institute Council and Executive Board.3 Much of the work is undertaken by Institute staff; and

11.3. Organisations and persons other than the Institute are able to submit draft standards to the ASRB for approval, but this rarely happens.

12. The FRSB and the Institute need to do many things to carry out the Institute’s standard-setting function. In particular, they expose draft IFRS and other standards for comment in New Zealand, analyse submissions, consider whether any changes are needed to make IFRS standards fit New Zealand’s needs, make submissions to the IASB and prepare standards where there is no IASB standard (e.g. the standard on prospective financial information, which is required to be applied by issuers and public sector entities).

13. There is also an international role for the FRSB. It generally liaises and seeks to influence the IASB and the IPSASB. It also has a very close relationship with the AASB.4

Setting the strategy

14. The FRA is silent about the responsibilities for making decisions that affect the broad direction of New Zealand financial reporting policy. In practice this function is split between the ASRB and the FRSB, with both making important decisions. For example, in 2002 the ASRB decided, after consulting with the FRSB, that New Zealand would adopt IFRS. The ASRB also issued Release 8 – The Role of the Accounting Standards Review Board and the Nature of Approved Financial Reporting Standards. The FRSB issued the NZ Framework and the NZ Preface, both of which are major operational strategy documents.

3 The FRSB’s high degree of autonomy means that standards design is more independent of the

interests of the profession than the FRA would suggest. 4 The FRSB and AASB agreed a protocol for cooperation in 2006, which provides the framework

for the transTasman coordination of operational strategies, policies and work programmes.

922359 Page 21

15. The absence of explicit provisions on strategy responsibilities means that many of the high level decisions are made through the standards approval process. Consequently, some major decisions have been made by the ASRB in response to proposals put to it by the FRSB. For example, when the ASRB issued Release 9 in 2007 (which delayed the adoption of IFRS for certain small entities pending the outcome of this review) it did so in response to a recommendation by the FRSB.

16. Thus, the ASRB has some powers to make major decisions about the direction of financial reporting in New Zealand. However, for the most part, the ASRB can only influence the strategic direction by encouraging the FRSB to submit proposals to it. This is not explicitly stated in the FRA and it is not readily inferred. Nor is it sensible. Governance principles would suggest that the peak body (i.e. the ASRB) should set the strategy.

Setting the medium term work programme

17. The standards work programme has two parts: the international agenda and the domestic agenda.

18. The international agenda for profit oriented entities is set by the IASB alone or jointly with the FASB. For public sector entities it is set by the IPSASB. National standards bodies, such as the FRSB and ASRB, need to fit in with the priorities, work programmes and deadlines set at the international level.

19. Under the scheme of the FRA, the domestic elements of the medium term work programme are largely under the control of the FRSB, but in practice the ASRB exercises influence in the way stated above in relation to strategy issues. In addition, due to the high levels of cooperation between the FRSB and AASB, including cross-membership, there is a high level of trans-Tasman work programme coordination.

The reporting tiers

20. There are three reporting tiers in New Zealand:

• Tier One: NZ IFRS;

• Tier Two: The FDR, which provides about 20 exemptions from the Tier One requirements for certain classes of entities.5 Most of the exemptions relate to disclosure. A small number are measurement-related; and

• Tier Three: Simple reporting requirements for small companies6 in accordance with the FRO.

5 An entity qualifies for the FDR if it is not publicly accountable and either has no separation

between owners and the governing body of the entity or is not large. An entity is large if it exceeds any two of the following: (i) total assets of $10 million; (ii) annual revenue of $20 million; and (iii) 50 employees. See Paragraphs 4.25 and 4.23 of the FDR.

922359 Page 22

21. Parliament established two tiers in the FRA. The top statutory tier comprises entities that are required to comply with GAAP (i.e. entities that fall within Tiers One and Two, as defined in the previous paragraph). The other statutory tier is Tier Three.

22. The FRA does not give explicit authority to the ASRB to create more tiers. Nevertheless, the two boards created Tier Two. The FRSB submitted the FDR for approval to the ASRB. The ASRB approved it by using a power in the FRA to give directions on the accounting policies that have authoritative support within the accounting profession.7 The FRSB then issued the FDR.

23. The boards could add more tiers in this way. However, they could not do so within the existing Tier Three because they do not have the power to design or approve standards for small companies.

24. There are consequential inconsistencies in the responsibilities for setting the thresholds that define which entities are in each tier. The ASRB and FRSB set the qualifying criteria that allow entities that would otherwise be in Tier One to report in accordance with the Tier Two requirements. Parliament set the qualifying criteria for Tier Three.8

Presentation and disclosure

25. There are inconsistencies in the ways that the presentation and disclosure requirements for entities within each tier are set. The requirements for Tier One appear in NZ IFRS, which are recommended by the FRSB and approved by the ASRB. The requirements for Tier Two appear in NZ IFRS and the FDR. The Tier Three requirements appear in the FRO. Thus, in a real sense, the government of the day set the Tier Three presentation and disclosure requirements.

Recognition and measurement

26. The recognition and measurement principles and rules are clearly set out for Tiers One and Two in NZ IFRS and the FDR. Clause 4 of the FRO outlines some basic measurement rules for Tier Three.

27. In theory, accountants should prepare small company financial statements in accordance with NZ IFRS and the FDR to the extent that they regard them relevant. However, our understanding is that most practitioners outside the Big 4 and the next level of accounting firms have little understanding of NZ IFRS and little reason to learn about them. In practice, most prepare financial statements based on their understanding of what is generally regarded as best practice by the profession.

6 A company is small if it meets two or more of the following tests: (i) total assets of no more than

$1million; (ii) annual revenue of no more than $2 million; and (iii) no more than five full-time equivalent employees. See section 6A of the FRA.

7 See section 24(1)(d) of the FRA.

8 See section 6 of the FRA.

922359 Page 23

Assurance standards

28. The Institute does not have explicit authority to make assurance standards. However, that role is implicitly provided through the ICANZ Act, because it empowers the Institute to regulate auditors. The PSB, which is a board of the Institute, submits draft standards for consideration by the Council of the Institute, which has responsibility for deciding whether to approve them. Approved assurance standards are mandatory for Institute members carrying out assurance engagements.

Responsibilities for administering statutes

29. There are close linkages between the FRA and ICANZ Act. However, the FRA is within the Commerce Portfolio and the ICANZ Act is within the Finance portfolio. In practice, the Minister of Commerce and MED have taken responsibility for matters covered by the ICANZ Act, such as the regulation of auditors.

Comment on the status quo

30. The legal framework for financial reporting is incoherent, incomplete, inconsistent and, in many respects, opaque. The best that can be said about it is that the ASRB, FRSB and the Institute have found ways to make it work, notwithstanding its obvious deficiencies. However, the status quo is unsustainable. The lack of clarity in relation to some statutory responsibilities, the misallocation of other responsibilities, the inability to make standards for some forms of entities, and the major differences between the way the system works in practice and the way it is described in law means that the FRA is inconsistent with at least three of the five principles of good regulatory practice.9

31. The main changes that are needed are:

31.1. To rationalise the institutional arrangements and clearly state where the responsibility for the statutory functions shall lie;

31.2. To remove the inconsistencies between the way the system works in practice and what would be expected based on a plain reading of the legislation; and

31.3. To empower the standards body to approve standards for all classes of entities which have statutory requirements to prepare financial statements.

9 Those principles are efficiency, effectiveness, transparency, clarity and equity.

922359 Page 24

PART 3.2: OPTIONS FOR MAKING ACCOUNTING AND AUDITING STANDARDS

32. Our preliminary view is that changes are needed with two aims in mind. First, efficiencies can be obtained by incorporating standards making and approval functions within a single body. Secondly, standards setting should be carried out and be seen to be carried out independently of the interests of the profession.

33. In our view there is only one feasible alternative to the status quo; to consolidate all standards-related responsibilities within the ASRB and rename it to reflect its broader responsibilities. The key features of this proposal are as follows:

33.1. The ASRB would be renamed as the XRB. As is the case with the ASRB, the XRB would be an independent crown entity;

33.2. The XRB would be responsible for setting the financial reporting strategy within the overall context provided by the new Act. The XRB would also have all responsibilities for designing and approving financial reporting standards and assurance standards;

33.3. XRB governance issues such as accountabilities and the process for making appointments to the board would be consistent with the template for independent crown entities in the Crown Entities Act 2004;

33.4. It would be within the powers of the XRB to establish committees to carry out any of its statutory functions. The XRB would consequentially be responsible for the oversight and governance of those committees in accordance with the provisions of the Crown Entities Act 2004;

33.5. The XRB would need staff to do the work that is currently carried out by the Institute;10

33.6. Approved financial reporting standards would continue to have the force of law;

33.7. At present assurance standards only apply to Institute members. Transferring responsibility for their design and approval to the XRB would make them mandatory for all audits that are required to be performed under Acts, Regulations and other statutes. The related enforcement issues are discussed in Part 9.1.1; and

33.8. The Institute would continue to regulate its members. Therefore, it would continue to set professional ethics and standards and impose the requirements for non-statutory assurance engagements.

10

The ASRB’s companion discussion document proposes a move away from the policy of sector neutrality, which would create a need to maintain more than one set of standards. This change might suggest a need for more staff and resources than is currently the case.

922359 Page 25

PART 3.3: OPTIONS FOR MAKING TIERS OF FINANCIAL REPORTING

34. As previously noted, there is no consistency in the responsibilities for making tiers and defining the qualifying criteria for each tier. We consider that there should be a single process in relation to these matters. This would allow for a fully consistent approach to be taken. We have identified the following options for determining the number of tiers and the qualifying criteria:

Option A: To include them in an Act of Parliament;

Option B: To include them in Statutory Regulations;

Option C: To assign the responsibilities to the XRB;

Option D: To assign the responsibilities to the XRB, subject to appeal to the High Court;

Option E: To assign the responsibilities to the XRB, subject to disallowance by the Regulations Review Committee of Parliament; and

Option F: To give the XRB the power to make recommendations to the Responsible Minister. The Responsible Minister would be able to accept or reject the recommendations, or refer them back to the XRB for further consideration within a specified time period (e.g. 30 working days).

35. We consider that the criterion for deciding the number of tiers and the qualifying criteria for each tier should be that the benefits to users are likely to outweigh the associated compliance costs for preparers regardless of which option is adopted.

Discussion of the options for making tiers of reporting

36. A disadvantage of Options A and B is that they would remove the formal linkages between determining which entities have to prepare and what they have to prepare. To illustrate why this is a problem, consider what would happen if a tier included two classes of reporting entity whose users had fundamentally different information needs. The XRB would be placed in the difficult position of having to decide whether to approve standards that did not fully meet one set of users’ needs, were too complex or detailed for the other set of users’ needs, or a combination of the two. However, this risk should not be overstated. Although the formal linkages would be absent, it would be reasonable to expect informal dialogue among the XRB, the Minister and officials.

37. An additional disadvantage with Option A is that good qualifying criteria that became suboptimal over time might not be changed until many years later because Parliamentary time is scarce and successive governments may regard changing them as a low priority.

922359 Page 26

38. Option C would deal with the problems associated with Options A and B. However, bearing in mind that the XRB would be exercising the coercive power of the State, Option C is unsatisfactory from an accountability perspective. Options D, E and F would provide accountability.

39. A feature of the High Court option (Option D) is that it would provide a higher degree of accountability because the XRB’s decisions would be scrutinised in considerably more detail. It is a matter of opinion whether this is an advantage or a disadvantage. A disadvantage of Option D is that it could add to the burdens of an already busy court system. In addition, appeals could be time consuming (compared with Options E and F) thereby creating unnecessary business uncertainty. Option D is also a much higher cost option than Options E and F.

40. Under Options E and F, strongly interested parties may lobby to veto a particular proposal, with a resultant risk that the lobbying power of interest groups could prevail over sound financial reporting principles. This would not matter so much if investors and other user groups that benefit from financial reporting were more powerful lobbyists than preparers. However, experience in New Zealand and overseas generally indicates that the reverse is true.

41. However, an advantage of Option F (compared with Option E) is that neither the XRB nor the Minister could act unilaterally. This should provide the XRB with a strong incentive to make high quality recommendations because it is very likely that any major problems would be drawn to the Minister’s attention.

42. Our preliminary view is that the lobbying risks would be manageable under Option F as long as it had the following features:

• The Minister would be required to apply the same criterion that the ASRB is required to use (i.e. whether the benefits to users exceed the costs to preparers); and

• The Minister could only reject a recommendation or refer it back for further consideration if he or she considered that the proposal was incomplete or not within the range of acceptable options.

43. To conclude, our preliminary view is to favour Option F because it combines the benefits of leaving the detailed analysis to the expert body and having an adequate level of accountability.

922359 Page 27

Part 4: Financial Reporting Principles and Indicators

PART 4.1: IDENTIFYING THE PRINCIPLES AND INDICATORS

Introduction

44. This Part identifies the two purposes, the main principle and the three indicators of financial reporting. The indicators are then applied to all types of entity and conclusions are drawn about the entities that should have reporting obligations. The indicators are applied to for-profit entities in Part 5, non-profit public sector entities in Part 6, private non-profit entities in Part 7 and Māori asset governance entities in Part 8. The Appendix summarises the status quo and our preliminary proposals for all entity forms.

The principle and the indicators

45. The primary principle and three indicators that financial reporting is needed are identified in Box One.

BOX ONE: FINANCIAL REPORTING PRINCIPLE AND INDICATORS

The Primary Principle

The overarching reason for financial reporting is to provide information to external users who have a need for an entity’s financial statements but are unable to

demand them

Indicators that an entity meets the primary principle

The major indicators that an entity should have financial reporting obligations are:

• Public accountability

• Economic significance

• The separation of ownership and management

The Primary Principle

46. GPFR are used for two purposes. One purpose is to promote accountability by entities to external users by requiring the disclosure of information about the entity’s financial performance and position. For example, GPFR promote accountability by:

• Public sector entities to taxpayers;

• Companies to shareholders; and

• Charities to donors.

922359 Page 28

47. The other purpose is to provide information that is useful to a wide range of users in making economic decisions. For example, GPFR provide information to investors, potential investors and their advisers that can contribute to decisions about whether to buy a business, buy the assets of a business or buy, hold or sell shares. In addition, GPFR can be a useful starting point for potential acquirers of the shares or assets of a business.

48. Some users are able to demand the financial information they need. For example, banks and other lending institutions impose financial information disclosure requirements, whether general or special purpose as a condition of lending money. Philanthropic and government entities do the same thing in relation to grants. However, most other users are unable to demand the information they need because they have little or nothing to give in exchange. As noted in the NZ Framework, many users have to rely on GPFR as their major source of financial information. The standards underlying GPFR should be designed with their needs in mind.11

The Public Accountability Indicator

49. Public accountability arises when an entity receives money directly from the public. The entities that are publicly accountable are:

• Non-profit public sector entities – Taxpayers and ratepayers provide the only or the predominant source of funding for the great majority of non-profit public sector entities (e.g. the government itself, government departments, crown entities and local authorities);12

• Issuers13 – Some entities seek funding through debt or equity instruments that are offered to the public. In addition banks, insurance companies, mutual funds and other entities take deposits from the public and/or hold assets in a fiduciary capacity for broad groups of outsiders. All money obtained in these ways is the public’s money; and

• Charities – Charities are publicly accountable because they receive donations and bequests directly from the public.

The Economic Significance Indicator

50. The idea underpinning economic significance as an indicator is the economic or social impact that a large entity is likely to have on the national or a regional economy if it fails. There is, therefore, a broader stakeholder interest in the financial position and performance of large entities even if they do not have public accountability.

51. In particular, groups other than equity investors and lenders provide resources as a consequence of their relationship with an entity, even though the contractual

11

NZ Framework, paragraph 6. 12

The flow-through of public money to another entity does not, in and of itself, mean that the recipient entity is publicly accountable. For example, a firm that provides consultancy services to a government department is not consequentially publicly accountable.

13 Comprising all registered banks, unit trusts, insurers, retirement villages, credit unions,

participatory securities and other entities that issue securities as defined in the Securities Act.

922359 Page 29

relationship is not that of a capital provider. For example, suppliers may extend credit to facilitate a sale. Customers may prepay for goods and services. Employees may have some of their compensation deferred for many years. To the extent that suppliers, customers, employees or other groups make decisions to provide resources to the entity in the form of credit, they are providers of capital.14

The separation of management and ownership indicator

52. The main idea underpinning this indicator is the concern that management may not manage other people’s money as well as the other people would themselves. This “principal-agent” problem explains the reason for corporate governance, which involves putting oversight systems and rules in place with the aim of modifying managerial behaviour and improving entity performance. Those systems and rules, which include the governance of financial resources, are imposed by parliaments, governments, regulators, boards, and owners or members.

53. At some point of separation, the principals need to be able to access GPFR to enable them to assess the financial performance, financial position and, in some cases, the cash flows of the entity.15 Our assessment of the separation indicator in relation to each of the broad categories of entities is as follows:

53.1. For-profit entities: The Separation Indicator applies to for-profit entities where significant numbers of owners of the business are not involved in its management. This is the case with some for-profit entities. However, it does not apply to most for-profit entities including sole traders, closely-held companies and most partnerships;

53.2. Public sector entities: The Separation Indicator applies to all public sector entities, whether non-profit or for-profit, because the ultimate owners are taxpayers and ratepayers. However, separation is only of academic interest to non-profit public entities because they are all publicly accountable; and

14

IASB, Exposure Draft of an improved Conceptual Framework for Financial Reporting, IASCF, May 2008, Paragraph OB6; and FASB, Exposure Draft – Conceptual Framework for Financial Reporting: The Objective of Financial Reporting and Qualitative Characteristics and Constraints of Decision-Useful Financial Reporting Information, Financial Accounting Series No 1570-100, 29 May 2008, Paragraph OB6.

15 NZ Preface, FRSB, March 2005, Paragraph 2(a).

922359 Page 30

53.3. Private non-profit entities: The Separation Indicator applies in different ways depending on the purpose of the entity:

53.3.1. The Separation Indicator applies to private non-profit entities whose purposes are to promote the interests of the members of the entity (e.g. sports clubs). It seems likely that the committee or board of most such entities would only be a small proportion of the total membership. Therefore, the separation indicator will almost always apply; and

53.3.2. The Separation Indicator applies in a different way in relation to private non-profit entities with charitable purposes. Arguably, the principals are the beneficiaries of such entities, in which case all such entities fit within the Separation Indicator. However, separation is only of academic interest because they are all publicly accountable.

PART 4.2: APPLYING THE INDICATORS TO PREPARATION, PUBLICATION AND

ASSURANCE

54. In this sub-part, we draw general conclusions about the application of the indicators and whether entities should therefore be required to prepare GPFR, have an assurance engagement completed and distribute or publish the GPFR. Those high level conclusions are then applied more specifically to each entity type in Parts 5-8 and the Appendix.

Applying the Indicators to preparation and publication or distribution

55. Preparation and publication/distribution are discussed together because preparation serves no purpose (in terms of accountability or economic decision making by external users) unless the preparer has obligations to ensure that the external users have access to the GPFR. In this context:

• “Publication” means a general requirement to make the GPFR available to the New Zealand public. Examples of publication are filing with a statutory officer (e.g. the Registrar of Companies or the Registrar of Incorporated Societies), forwarding them to a government department (e.g. the Ministry of Education in relation to schools and the Department of Internal Affairs for local authorities) and to forwarding them to a Minister of the Crown for tabling in Parliament (e.g. crown entities and government departments); and

• “Distribution” means, at minimum, making the user aware that the GPFR are available (e.g. alerting users by email that the GPFR appear on a specified website). It can also mean sending the GPFR to users by post, attaching them to an email or making them available at a meeting of the entity.

922359 Page 31

56. Our preliminary views in relation to preparation and publication or distribution are as follows:

56.1. For entities that are publicly accountable:

56.1.1. Issuers and public sector non-profit entities should be required to prepare and publish GPFR;

56.1.2. Private non-profit entities which have charitable purposes and are not small should be required to prepare and publish GPFR;

56.1.3. Small private non-profit entities which have charitable purposes should not have preparation requirements because the financial reporting costs outweigh the benefits to users; and

56.1.4. Unincorporated private non-profit entities which have charitable purposes should not have preparation requirements because enforcement is impractical.

56.2. Most economically significant entities should be required to prepare and publish GPFR;

56.3. The default position for entities with a significant degree of separation between management and the owners or members should be a requirement to prepare GPFR and to distribute them to owners or members. However, the owners or members should be able to opt out of the requirements to prepare; and

56.4. The default position for entities that do not fall within the definition of any of the Indicators should be to have no preparation requirements. However the owners or members of the entity should be able to require the preparation and distribution of GPFR and determine which tier of financial reporting standards will be used.

922359 Page 32

Applying the indicators to assurance

57. The purpose of an assurance engagement is to enhance the degree of confidence of intended users in the financial statements. This is achieved by the expression of an opinion by the auditor on whether the financial statements are prepared, in all material respects, in accordance with an applicable financial reporting framework.16 In general, misstatements, including omissions, are considered to be material if, individually, or in the aggregate, they could reasonably be expected to influence the economic decisions of users.17 In other words, without assurance GPFR are of less value because users do not know whether they can rely on them. Therefore their information needs are not being fully met.

58. There are two forms of assurance engagement. IFAC defines them as follows:

• Reasonable assurance (i.e. an audit): The objective is a reduction of assurance engagement risk to an acceptably low level in the circumstances of the engagement, as a basis for a positive form of expression of the practitioner’s conclusion; and

• Limited assurance (i.e. a review engagement): The objective is a reduction in assurance engagement risk to a level that is acceptable in the circumstances of the engagement but where that risk is greater than for a reasonable assurance engagement, as the basis for a negative form of the expression of the practitioner’s conclusion.18

59. Our preliminary views in relation to assurance are as follows:

59.1. Public sector and for-profit entities that are publicly accountable should be required to have an assurance engagement completed;

59.2. Private non-profit entities that are publicly accountable and have preparation requirements should be required to complete an assurance engagement unless their small size means that the assurance-related benefits to users are likely to be outweighed by the costs of a review engagement;

59.3. All economically significant entities should be required to have an assurance engagement completed;

59.4. Assurance should be the default position for entities with a significant degree of separation between management and the owners or members. However, the owners or members should be able to opt out;

16

“Overall Objectives of the Independent Auditor and the Conduct of an Audit in Accordance with International Standards on Auditing” (ISA 200) in Handbook of International Auditing, Assurance and Ethics Pronouncements¸ International Federation of Accountants, April 2009 edition, paragraph 3 , page 78.

17 ib id, page 79.

18 “Glossary of Terms”, IFAC, Handbook …, p18

922359 Page 33

59.5. If the owners or members of an entity that does not fall within the definition of any of the Indicators decide that the entity will prepare GPFR, then the owners or members will also be able to require an assurance engagement to be carried out. The owners or members will be able to specify either an audit or a review engagement; and

59.6. The XRB would determine the level of assurance (i.e. audit or review) that should apply to entities required to have an assurance engagement completed.

922359 Page 34

Part 5: The Application of the Indicators to For-Profit Entities

60. This Part is structured in the following way:

• Part 5.1 provides background information;

• Part 5.2 identifies for-profit entities that should have reporting obligations because they are publicly accountable;

• Part 5.3 identifies for-profit entities that should have reporting obligations because they are economically significant;

• Part 5.4 identifies for-profit entities that should have reporting obligations because there is separation of management and ownership; and

• Part 5.5 summarises our views on preparation, assurance and publication and distribution proposals for for-profit entities.

PART 5.1: BACKGROUND

61. The following for-profit entities are currently required to prepare and file audited GPFR and distribute them to the owners:

• Issuers;

• Overseas-incorporated companies that are carrying on business in New Zealand;

• Companies with 25% or more overseas ownership which are large;19

• Māori incorporations;20

• Non-issuer building societies; and

• Non-issuer friendly societies if the receipts, and payments and assets are greater than or equal to $20,000.

62. The following for-profit entities are currently required to prepare and distribute GPFR, but not file:

• All companies other than those covered by the previous paragraph;

• Limited partnerships; and

• Non-issuer friendly societies other than those listed in the previous paragraph.

19

An entity is large if it exceeds any two of the following: (i) total assets of $10 million; (ii) annual revenue of $20 million; and (iii) 50 employees. See section 19 of the FRA.

20 See Part 8.3.1 for a discussion of financial reporting for Māori incorporations.

922359 Page 35

PART 5.2: FOR-PROFIT ENTITIES AND PUBLIC ACCOUNTABILITY

63. Issuers of securities are publicly accountable because they invite the public to invest directly. It is clear that all issuers should continue to be required to prepare and file assured GPFR.

64. It can also be argued that there is public accountability by companies to creditors because the liability of the owners is limited. However, for cost-benefit reasons our view is that creditors’ interests are more appropriately considered from an economic significance perspective.

PART 5.3: FOR-PROFIT ENTITIES AND ECONOMIC SIGNIFICANCE

PART 5.3.1: BACKGROUND

65. We concluded in Part 4 that the financial reporting obligations for publicly accountable entities and economically significant entities should be no different. Both classes of entity should be required to prepare and publish assured GPFR. Therefore, our view is that economic significance only needs to be discussed in relation to large entities that are not publicly accountable.

66. At present, the economic significance indicator is only applied to companies with 25% or more overseas ownership. The relevant definition appears in section 19A of the FRA. It states that a company is large if it exceeds any two of the following tests: (i) consolidated assets of $10 million; (ii) consolidated annual revenue of $20 million; and (iii) 50 full time equivalent employees in the company and its controlled entities.

67. There is a possible risk with this approach in relation to overseas incorporated and owned companies. Some such companies may have substantial annual revenue but fall below both of the other thresholds. If so, then it might be better to modify the test so that a company would only be excluded from the definition of large if it was below the threshold for revenue, and one or both of the thresholds for assets or employees. To illustrate, a company with annual revenue of $25 million, assets of $5 million and 40 employees would not meet the extant definition but would meet the alternative definition of “large”.

68. As a starting point for discussion, we are seeking submitters’ views on whether asset values, annual revenue and numbers of employees are appropriate measures of economic significance, whether the two-out-of-three approach remains appropriate, and whether the current numbers in section 19A of the FRA should be retained.

69. Most economically significant for-profit non-issuer entities are companies. However, a small number of other entities, such as large partnerships within the professions are also economically significant.

922359 Page 36

70. 520,000-odd companies are registered in New Zealand and many other for-profit entities operate in New Zealand, including partnerships, trading trusts and sole traders. There are no reliable statistical data on the number of entities that meet the current test for defining a large company. However, Australia uses the same two-out-of-three approach for distinguishing between large and small proprietary companies and ASIC statistics may provide some guidance. The employee number test in Australia and New Zealand are the same (i.e. 50 employees) and the monetary tests are about 50% higher in Australia (A$12.5 million for assets and $A25 million for revenue) than New Zealand (NZ$10 million and NZ$20 million).

71. About 1.6 million companies are registered in Australia and about 33,000 entities are required to prepare GPFR comprising 20,000 public companies,21 7,000 registered schemes and 6,000 large proprietary companies. Thus, about one Australian company in 260 is a large proprietary company.

72. Due to the relative sizes of the Australian and New Zealand economies (about 6:1) we can reasonably assume that New Zealand companies are smaller than Australian companies across the size distribution. If it is assumed that the economy size factor and the lower thresholds for economic significance in New Zealand balance each other out, then 1:260 could be used to approximate the ratio of large non-issuer companies to total companies in New Zealand. This would suggest that there are about 2,000 economically significant non-issuer companies in New Zealand, using the current definition of “large” in the FRA.

73. We acknowledge that the number could be materially different in absolute terms (e.g. it might be half or double 2,000). However, that is unlikely to matter from a policy perspective. The key point is that only a very small proportion of non-issuer companies and other for-profit entities would have financial reporting obligations for economic significance reasons.

PART 5.3.2: APPLYING THE ECONOMIC SIGNIFICANCE INDICATOR TO FOR-PROFIT

ENTITIES

74. This section considers each of the following issues in relation to for-profit entities:

• Companies with 25% or more overseas ownership;

• Overseas-incorporated companies carrying on business in New Zealand; and

• All other economically significant companies and other for-profit entities.

21

The definition of “public company” in Australia is similar to the definition of “issuer” in New Zealand.

922359 Page 37

Companies with 25% or more overseas ownership that are not issuers

75. The requirements are already consistent with the Economic Significance Indicator for this class of companies. Under sections 19 and 19A companies with 25% or more overseas ownership are only required to file audited GPFR if they are large.

Overseas-incorporated companies carrying on business in New Zealand that are not issuers

76. Under section 19 of the FRA, an overseas-incorporated company carrying on business in New Zealand must file its financial statements and where relevant, consolidated financial statements, unless it is a subsidiary22 of another company that is required to file and has filed parent-only and consolidated financial statements. In addition, section 8(2) states that an overseas company that is required to file must also file financial statements for its New Zealand business as if that business were conducted by a company formed and registered in New Zealand.

77. The Economic Significance Indicator would suggest that the current filing obligations on overseas-incorporated companies are excessive. GPFR should only be required to be filed if the New Zealand business of the overseas company is large.

78. A non-indicator argument that has been put to us is that overseas-incorporated companies’ financial statements could be used for detecting money laundering and terrorist financing. We do not agree with this proposition. GPFR provide aggregated financial information, not information about individual transactions. It would seem very unlikely that they could be used to detect money laundering or terrorist financing.