the state of biomanufacturing capacity – do we finally have …€¦ · 2008 – 29+ commercial...

TRANSCRIPT

The State of Biomanufacturing Capacity –Do We Finally Have Enough?

Howard L. Levine, Ph.D.IBC’s 10th International

Production and Economics of Biopharmaceuticals Boston, MA

September 19 – 22, 2005

From Clone to Clinic®

Biopharmaceutical Industry Growth Through 2015

$-

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Year

Tota

l Sal

es ($

B)

Biopharma Total Pharma

Sources for BPTC Estimate: IMS Health, Arthur D. Little, and Woods-Mackenzie

2004 sales approaching 10% of almost $450B pharmaceutical market, growing to approximately 15% by 2015Biopharmaceutical sales growth approximately double that of the pharmaceutical marketAt 85% gross margin manufacturing sector forecast to grow to $30B by 2015

From Clone to Clinic®

Biomanufacturing Market Segmentation

CommercialMicrobial:2004 – 162008 – 19

Clinical Microbial:2004 – 25

2008 – 29+

Commercial Cell Culture:2004 – 162008 – 19

Clinical Cell Culture:2004 – 23

2008 – 25+

Product Development Companies (PDC)

From Clone to Clinic®

Biomanufacturing Market Segmentation

CommercialMicrobial:2004 – 72008 – 8

Clinical Microbial:2004 – 312008 – 34

Commercial Cell Culture:

2004 – 82008 – 10

Clinical Cell Culture:2004 – 352008 – 38

Contract Manufacturing Organizations (CMO)

From Clone to Clinic®

Biopharma CMO Market Growth

Biopharma$29 B

Biopharma CMO$1 B

Total pharma market$390 B

Biopharma CMO$3 B

Biopharma$70 B

Total pharma market$690 B

2001 2007

Sources for BPTC Estimate: IMS Health, Arthur D. Little, and Woods-Mackenzie

Outsourcing of commercial manufacturing accounts for approximately 3.5% of biopharmaceutical product revenuesCMO percentage of market to remain relatively flat through 2007

From Clone to Clinic®

Mammalian Cell Culture Capacity

Amgen8%

Biogen Idec14%

Genentech32%Novartis

10%

Wyeth8%

Others28%

Boehringer Ingelheim

40%

Abgenix8%

Baxter Biosciences

8%

Lonza22%

Diosynth6%

Others16%

Distribution by Company – 2004

Contract ManufacturersTotal installed capacity ~400,000 L

Product Development Cos.Total installed capacity ~950,000 L

Will decrease with sale of

NIMO & NICO

From Clone to Clinic®

Cell Culture Bioreactor Capacity Distribution

Current expansion projects are adding larger volume bioreactorsat current manufacturersBy 2008, over 10 companies will have >100,000 L installed capacity

0

5

10

15

20

<1000 L 1000L - <10000L 10000L - 100000L >100000L

Total Reactor Volume

Num

ber o

f Com

pani

es

CMO (2004) CMO (2008) PDC (2004) PDC (2008)

From Clone to Clinic®

BPTC Approach to Capacity Analysis

Bottom-up methodology• Plant-by-plant estimation of capacity “supply”• Product-by-product and dose-driven estimation of

“demand”Probability weighting factors• Accounting for multiple products targeting same

indication• Assumptions for probability of success and time to

marketMarket differentiation• Microbial and mammalian cell culture markets• Clinical and commercial markets

Apply Monte-Carlo analysis to quantify probability of predicted outcomes

From Clone to Clinic®

Microbial Volume Capacity – Existing and Forecast

Clinical supply represents approximately 7- 12% of installed capacityPDCs control the majority of total installed capacity• Approximately 80% in 2003• Contracting to approximately 70% by 2009

0

200

400

600

800

1000

1200

Estim

ated

Inst

alle

d Fe

rmen

ter V

olum

e('0

00 L

)

2003 2004 2005 2006 2007 2008 2009Year

PDCCMO

From Clone to Clinic®

Cell Culture Volume Capacity – Existing and Forecast

Perfusion capacity adjusted to equivalent fed-batch capacityClinical supply represents approximately 5 – 10% of installed capacityPDCs control the majority of total installed capacity• Approximately 80% in 2003• Moderate growth to approximately 85% by 2009

0

500

1000

1500

2000

2500

3000

3500

Estim

ated

Inst

alle

d B

iore

acto

r Vol

ume

('000

L)

2003 2004 2005 2006 2007 2008 2009Year

PDCCMO

From Clone to Clinic®

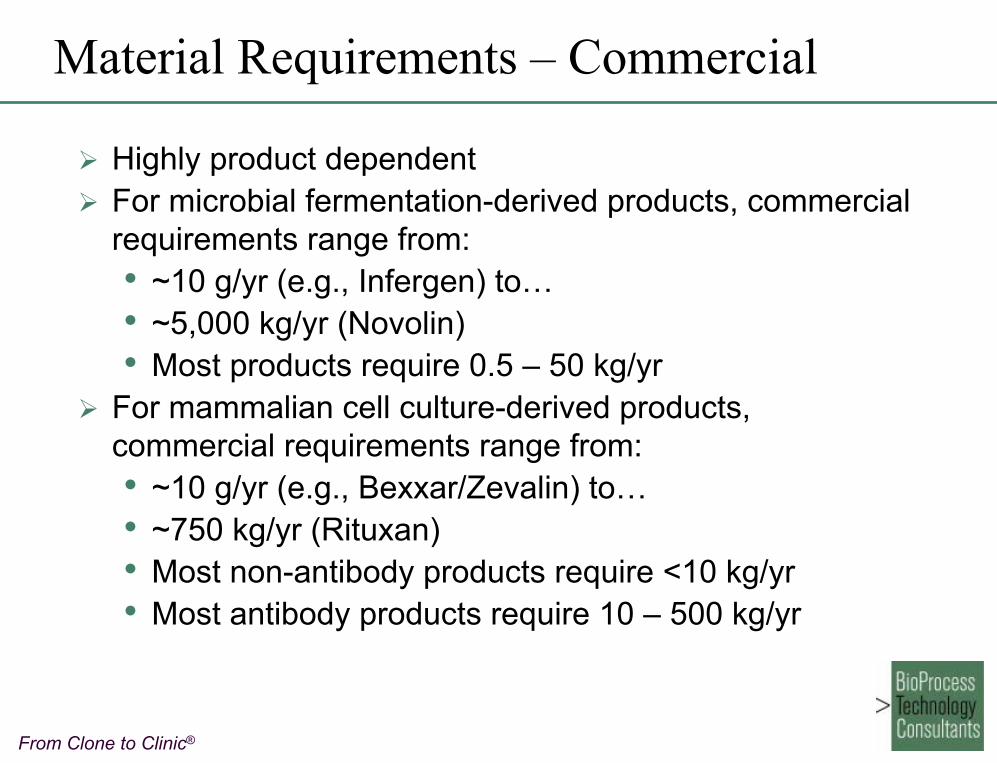

Material Requirements – Commercial

Highly product dependentFor microbial fermentation-derived products, commercial requirements range from:• ~10 g/yr (e.g., Infergen) to…• ~5,000 kg/yr (Novolin)• Most products require 0.5 – 50 kg/yr

For mammalian cell culture-derived products, commercial requirements range from:• ~10 g/yr (e.g., Bexxar/Zevalin) to…• ~750 kg/yr (Rituxan)• Most non-antibody products require <10 kg/yr• Most antibody products require 10 – 500 kg/yr

From Clone to Clinic®

Trends in Commercial Product Requirements

Fastest growing segment is monoclonal antibodies• Growth rate > 40% per year

Trend for commercial products is from agonists to antagonists• Larger volume, less expensive ($/g) products

2004 Sales by Mfg Technology/Prod Type

Mammalian Mab, $13.1

Mammalian rProtein, $17.8

Microbial rProtein, $15.4

Mammalian Products

0.0

500.0

1000.0

1500.0

2000.0

2500.0

3000.0

Amount Required (kg/yr) N Ave. Sales Price ($/mg)

rProteinsMAbs

From Clone to Clinic®

Product-by-Product Analysis Methodology: Commercial Products

Product sales (2004 WW sales $/yr)Source: Industry and co. financial reports

Product pricing ($/mg)Source: 2004 Red Book

Product amount required (kg/yr)

Expression level/overall yield (g/L)Source: Published data and estimates Cell Culture volume required (L/yr)

Mfg site determined where possibleTechnology for manufactureSource: Literature and internal evaluation

Per patient dosing (g/pt/yr)Source: Prescribing info, reg. documents

Treatment population (pt/yr)

}}

Inputs Outputs

From Clone to Clinic®

2004 Bulk Product Requirements (Kg/yr) –Mammalian Commercial Products

Total estimated bulk product requirements for mammalian cell culture commercial products (2004):

• All mammalian products – 2,875 kg/yr• Monoclonal antibodies – 2,810 kg/yr• rProteins – 65 kg/yr

Significant growth in monoclonal antibody product requirements:• Approximately 65% per year over last 3 years • ~ 1,000 kg/yr (2002); ~ 1,700 kg/yr (2003)

Estimated requirements for top selling biopharmaceutical products:• Rituxan 784 Kg• Remicade 615 Kg• Enbrel 577 Kg• Herceptin 287 Kg• Avastin 150 Kg• Erbitux 107 Kg• All others (38) 357 Kg

From Clone to Clinic®

0

500

1,000

1,500

2,000

2,500

3,000

3,500

Ritu

xan

Enb

rel

Her

cepti

n

Rem

icade

*

Erb

itux

Rec

ombin

ate

Ava

stin

Pulm

ozym

e

Kog

enate

* A

ll othe

rs (3

5)

Product

Estd

CC

Vol

200

4 ('0

00 L

/yr)

2004 Cell Culture Volume Requirements –Mammalian Commercial Products

Total estimated cell culture volume requirements for mammalian cell culture commercial products (2004):

• All mammalian products – 11.2 M L/yr• Monoclonal antibodies – 9.0 M L/yr• rProteins – 2.2 M L/yr

Significant growth from previous years:• Approximately 35% per year over last 3 years • ~ 6.2 M L/yr (2002); ~ 8.5 M L/yr (2003)

* Perfusion adjusted to equivalent batch/fed batch volume

From Clone to Clinic®

Growth of Current Commercial Cell Culture Products

Worldwide sales shown for each productAverage CAGR for products on market 3 years or more is >45%Growth of existing products represents significant driver for future capacity demand

$-

$500

$1,000

$1,500

$2,000

$2,500

$3,000

2000 2001 2002 2003 2004

Year

Sale

s ($

M)

EnbrelRituxanRemicadeHerceptinRecombinateAvastinSynagisHumiraErbitux

From Clone to Clinic®

Forecast Cell Culture Volume Requirements –Existing Commercial Products Only

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

2005 2006 2007 2008 2009 2010

Year

Cel

l Cul

ture

Vol

ume

(ML/

yr)

Capacity shown based on equivalent fed-batch basis for perfusion productsBase analysis assumes no changes in current volumetric productivitiesPotential 3X process improvements for Enbrel, Erbitux, and Rituxan could result in 35% decrease in demand by 2010• 29.4 ML (no improvement) vs. 19.0 ML (predicted improvement)

Further process improvements in other products could decreasedemand for existing products even further

From Clone to Clinic®

Why Invest in Process Improvement?

Regulatory environment becoming more supportive• Risk-based GMP initiatives• Comparability protocols• Increasing number of post-approval process changes

Significant technical advances enable dramatic increases in volumetric productivities for mammalian cell culture processes• High expressing cell lines• Media development and optimization• Improvements in downstream processing• Increases in basic operating efficiencies can improve

volumetric productivities without requiring major process changes

From Clone to Clinic®

Why Invest in Process Improvement?

Financial returns are compelling for improvements to older large volume processes• At $400/g, manufacturing costs for a 500 kg/yr MAb

represent $200 Million per year or more• A significant increase in volumetric productivity can

easily be expected to provide savings of 20% or more− 3X process improvements could lower bioreactor

capacity demand by 35%• Payback time for a successful $30 Million

comparability program to implement a higher yielding process could be less than one year.

From Clone to Clinic®

Product-by-Product Analysis Methodology: Pipeline (Phase II/III) Products

* Launch date & probability weight determined by development phase -BPTC estimates

Inputs OutputsPer patient dosing (g/pt/yr)Source: Literature, databases, press releases

Indication Prevalence (pt/yr)Source: Databases

Product amount required post-launch* (kg/yr)

Expression level/overall yield (g/L)Source: Published data and estimates

Cell Culture volume required post-launch* (L/yr)

Technology for manufactureSource: Literature and internal evaluation

Market Penetration (% prev/yr)Based on indication & # products per indication

}

}

From Clone to Clinic®

Success Rate and Turnover Data

90%

64%

45%

86%

30%

40%

100%

56%

56%

0% 20% 40% 60% 80% 100% 120%

BLA

Phase III

Phase II

Success rate (to next stage)

2004 Performance2003 performanceBPTC model values

Turnover statistics (2003/2004)No BLA products remained in the same stage• All either approved or rejected

60 – 65% of Phase III products remained in Phase III• ≤40% moved forward or failed

61 – 67% of Phase II products remained in Phase II

From Clone to Clinic®

Distribution of Pipeline by Production Technology

Pipeline Number of Products

0

10

20

30

40

50

60

70

Market BLA Phase III Phase II Phase I

Stage

Num

ber o

f Pro

duct

s

MammalianMicrobial

Pipeline Fraction MAb-based

0%10%20%30%40%50%60%70%80%90%

100%

Market BLA Phase III Phase II Phase I

Stage

Perc

ent M

Ab-

base

d

MammalianMicrobial

Pipeline is 70% mammalian cell cultureSignificant trend towards antibody-based products is leveling off at ~ 85% of mammalian cell culture pipelineSuccess of Fabs coupled with improvements in antibody expression in microbial systems may shift balance

From Clone to Clinic®

Forecast Cell Culture Volume Requirements –Commercial and Pipeline Products

Top 5 pipeline drivers fail:46.8 ML

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

2004 2005 2006 2007 2008 2009

Year

CC

Vol

ume

Req

d (M

L/y

r)

Commercial Pipeline

Other factors that may affect future demand include variation in time to approval, market penetration, and process yield

Top 5 pipeline drivers succeed:68.5 ML~ 50% demand

from new products

From Clone to Clinic®

Comparison Mammalian Cell Culture Supply & Demand

2004 2005 2006 20072008 2009

2010

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

Inst

alle

d R

xr V

olum

e ('0

00 L

)

Year

Forecast Demand (Y+1) Forecast Supply

From Clone to Clinic®

Cell Culture Supply & Demand – Conclusions

Slight excess of supply for coming 2 – 3 yearsAccess to capacity may cause temporary isolated shortagesPotential shortages may occur in 2009 and beyond if additional capacity is not installed or processes improvedUnusually high success or fail rates may result in dramatic fluctuations in supply and demand

From Clone to Clinic®

Capacity Utilization Scenarios – 2009 Forecast

112%92%76%No commercial process yield improvements

95%75%59%

Commercial yield improvement for three large volume products

Top 5 Pipeline Volume Drivers

Succeed

MostProbable

Case

Top 5 Pipeline Volume Drivers

FailScenario

From Clone to Clinic®

Monte Carlo Simulation – Assumptions and Methods

Using data from most probable scenario as starting point, calculate a probable range of output scenarios based on 3,000 independent calculations using random values from within the defined probability ranges for each of the following input variables

• Approval - Yes/No− Yes frequency based on stage of development

• Overall Yield− Includes expression level and purification yield− Normal distribution using standard deviation

• Patient population− Normal distribution with increasing standard deviation

year to yearOutput shows distribution of total capacity demand foreach year based on selected variables

From Clone to Clinic®

Total Capacity Demand – Distribution By Year

3,000 5,000

2,400 4,000

1,800 3,000

1,200 2,000

600 1,000

0 0

2002 2003 2004 2005 2006 2007 2010

Annual Pipeline Mean

+/- Standard Dev (nml)

Projected Supply

Rea

ctor

Vol

ume

(‘000

L)

Year

5,000

4,000

3,000

2,000

1,000

0

2003 projection2005 projection

From Clone to Clinic®

What’s Next?10 Year Forecast Requires a Different Approach

totalpatients

year#doses

Patient/yeargramsdose

Lgramx % patients

treated x x x

time

L/gm

time

Dose/Pt/yr

PER INDICATION

time

%biol

Vs. total %biol

Product-by-product approach unlikely to successfully predict outcome:• 10 years ago (1995), OKT-3 and ReoPro were the only approved

antibody products• Most meaningful products from a manufacturing capacity

perspective were in pre-clinical/early clinical developmentDevelop new model based on indication and treatment prevalence to forecast manufacturing requirements over a longer time horizon

From Clone to Clinic®

Overall ConclusionsSupply expansion will result in more large-scale players with a broader distribution of capacity• PDCs retain approximately 75 – 80% of total industry

capacityAs volumetric productivities increase, bioreactor capacity may no longer be throughput-limiting in many facilities• Future efforts should focus on improving downstream

processingOverall, the demand for cell culture volumetric capacity will likely continue to grow for the foreseeable future• Process improvements will act to reduce demand• Sales growth and new product approvals will act to increase

demand• On industry-wide aggregate basis, capacity supply meets

demand requirements; however, absent significant process yield improvements, utilization industry-wide is likely to increase

From Clone to Clinic®

Overall ConclusionsThe range of supply-demand scenarios over the next 5 – 10 years is significant, influenced by:

− Process yields− Time to approval−Market penetration− Success rates−Operational efficiency

Development of effective manufacturing strategies requires methods for defining the risk of supply shortages and anticipating demand increases• Monte Carlo simulations provide one means of

defining this risk

From Clone to Clinic®

Acknowledgements

Tom Ransohoff

• Supply/demand analysis; production yields

James Blackwell, PhD

• Supply/demand analysis; Monte-Carlo simulations

Susan Dana Jones, PhD

• Patient populations; market penetration

Robert Mittendorff, II, MBA, MD

• Monte-Carlo simulations

Richard Stock, PhD (BioPharm Services)

• Clinical products database