the state of alternative investments: a global view investments.pdf · the state of alternative...

TRANSCRIPT

The State of Alternative

Investments: A Global View

Keith Black, PhD, CFA, CAIA

Showcase your Knowledge @CAIA_Keith Black @CAIAAssociation

State of Alternative Investment – 2

About CAIA Association

The global leader in alternative investment education

Non-profit established in 2002, based in Amherst, MA, with

offices in Hong Kong, Singapore, Geneva, and London

Over 8,700 current charterholders in more than 85 countries

28 vibrant chapters located in financial centers around the

world

More than 150 educational and networking events each year

Excellence in AI education through the CAIA designation and

the Fundamentals of Alternatives certificate program

State of Alternative Investment – 3

Alternative Investment Education

Alternatives currently represent over $14 trillion in assets

under management, while assets in liquid alternatives

have grown substantially.

The CAIA Association Mission: Establish the CAIA designation as the benchmark for alternative

investment education worldwide

Promote professional development through continuing education,

innovative research and thought leadership

Advocate high standards of professional ethics

Connect industry professionals globally

State of Alternative Investment – 4

The CAIA Charter Designation

Globally recognized credential for professionals

managing, analyzing, distributing, or regulating

alternative investments.

Highest standard of achievement in alternative

investment education.

Comprehensive program comprised of a two-tier

exam process: Level I assesses understanding of various alternative asset classes

and knowledge of the tools and techniques used to evaluate the

risk-return attributes of each one.

Level II assesses application of the knowledge and analytics

learned in Level I within a portfolio management context.

Both levels include segments on ethics and professional conduct.

State of Alternative Investment – 5

Fundamentals of Alternative Investments

The Fundamentals of Alternative Investments certificate program provides a foundation of core concepts in alternative investments.

Fundamentals fills a critical education gap for those who need to understand the evolving landscape of alternative investments.

Online, 20-hour, self-paced course

Earns CE hours for the CIMA®, CIMC®, CPWA®, CPA ®, and CFP® designations

Understand the core concepts in alternative investments

Gain confidence in discussing and positioning alternatives

State of Alternative Investment – 6

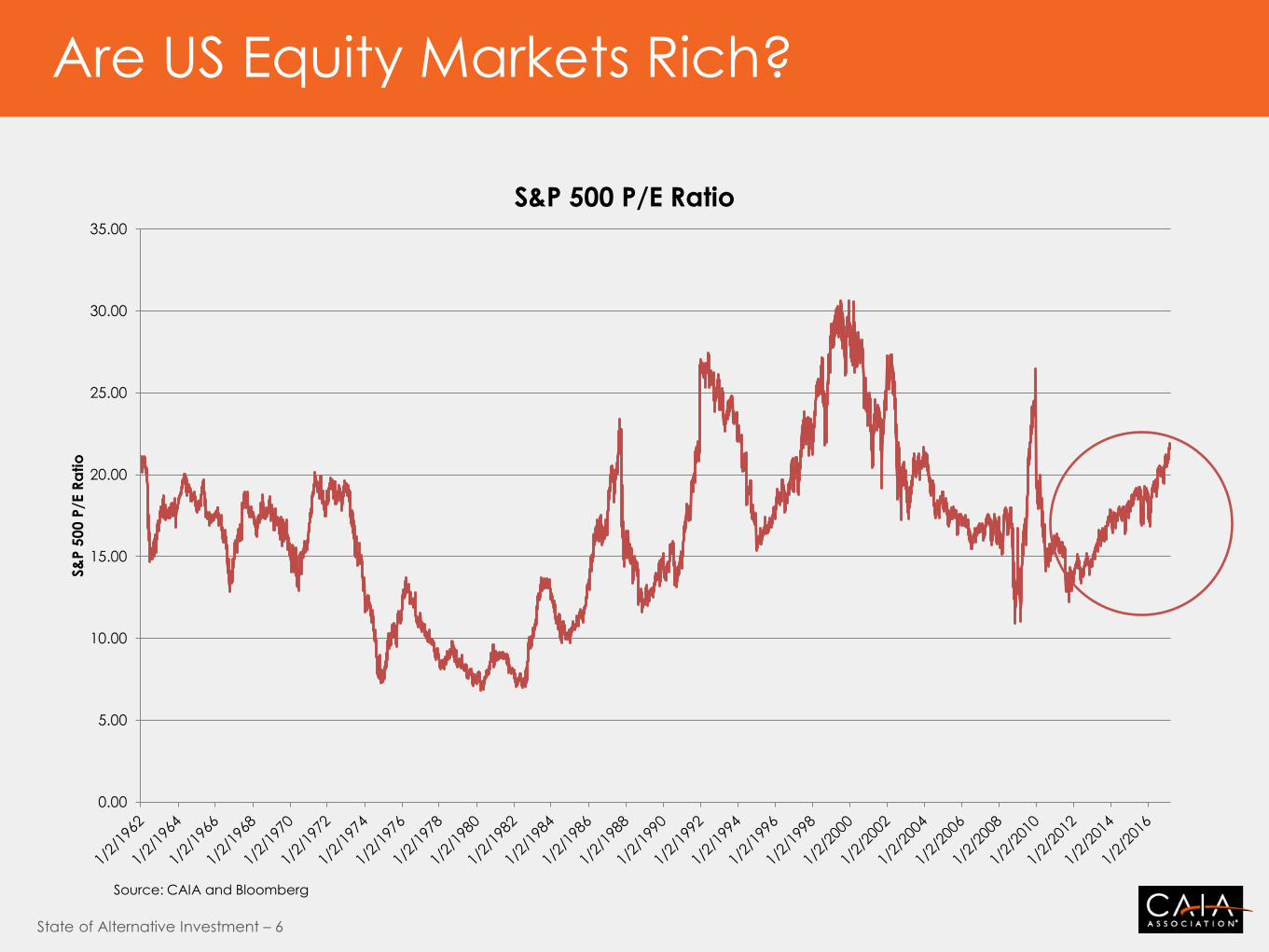

Are US Equity Markets Rich?

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

S&

P 5

00

P/E

Ra

tio

S&P 500 P/E Ratio

Source: CAIA and Bloomberg

State of Alternative Investment – 7

Fixed Income 30+ Year Bull Market

-2

0

2

4

6

8

10

12

14

16

18

Yie

ld

German Bund 10 Year US 10 Year

Source: CAIA and Bloomberg

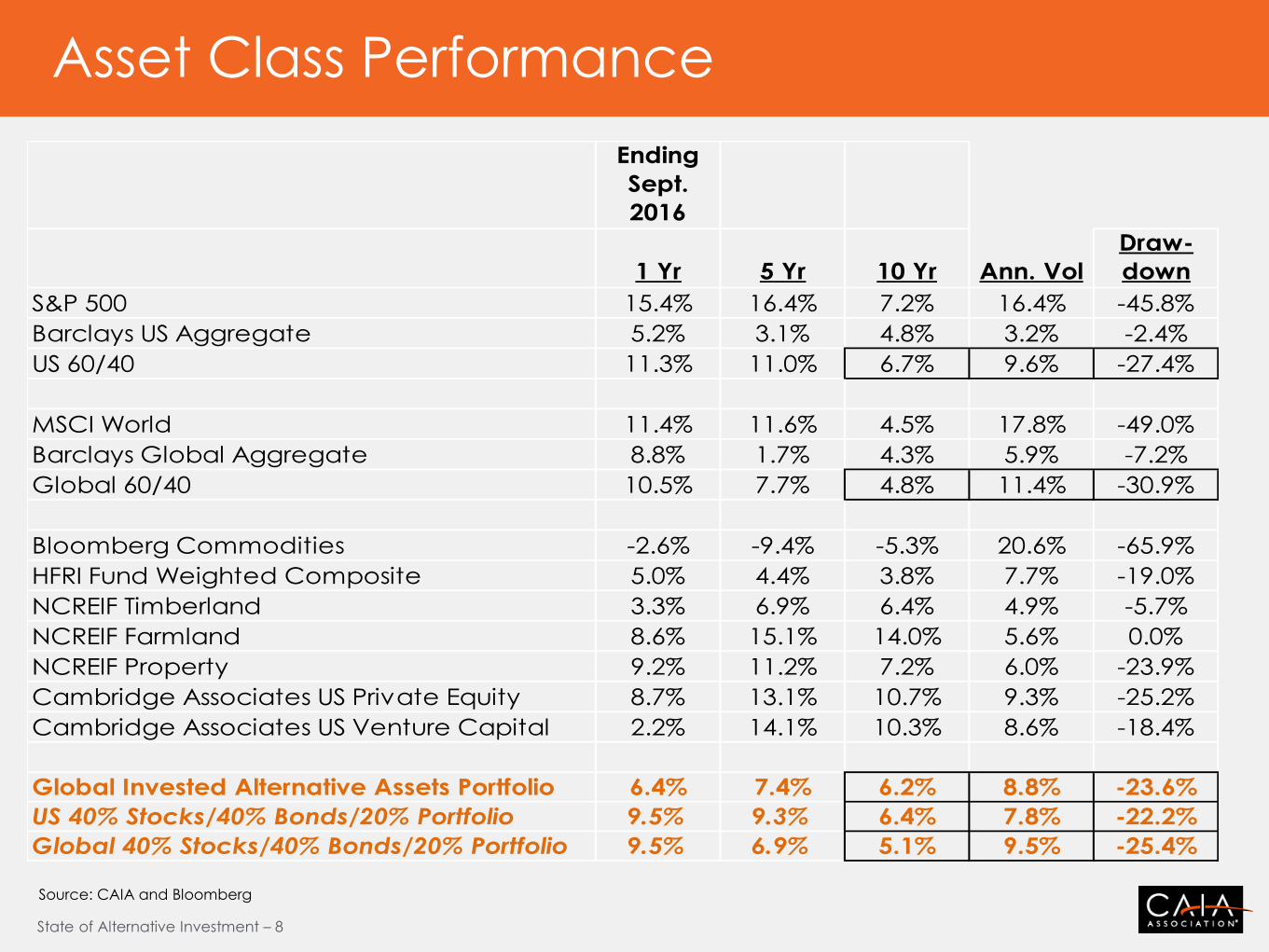

State of Alternative Investment – 8

Ending

Sept.

2016

1 Yr 5 Yr 10 Yr Ann. Vol

Draw-

down

S&P 500 15.4% 16.4% 7.2% 16.4% -45.8%

Barclays US Aggregate 5.2% 3.1% 4.8% 3.2% -2.4%

US 60/40 11.3% 11.0% 6.7% 9.6% -27.4%

MSCI World 11.4% 11.6% 4.5% 17.8% -49.0%

Barclays Global Aggregate 8.8% 1.7% 4.3% 5.9% -7.2%

Global 60/40 10.5% 7.7% 4.8% 11.4% -30.9%

Bloomberg Commodities -2.6% -9.4% -5.3% 20.6% -65.9%

HFRI Fund Weighted Composite 5.0% 4.4% 3.8% 7.7% -19.0%

NCREIF Timberland 3.3% 6.9% 6.4% 4.9% -5.7%

NCREIF Farmland 8.6% 15.1% 14.0% 5.6% 0.0%

NCREIF Property 9.2% 11.2% 7.2% 6.0% -23.9%

Cambridge Associates US Private Equity 8.7% 13.1% 10.7% 9.3% -25.2%

Cambridge Associates US Venture Capital 2.2% 14.1% 10.3% 8.6% -18.4%

Global Invested Alternative Assets Portfolio 6.4% 7.4% 6.2% 8.8% -23.6%

US 40% Stocks/40% Bonds/20% Portfolio 9.5% 9.3% 6.4% 7.8% -22.2%

Global 40% Stocks/40% Bonds/20% Portfolio 9.5% 6.9% 5.1% 9.5% -25.4%

Asset Class Performance

Source: CAIA and Bloomberg

State of Alternative Investment – 9

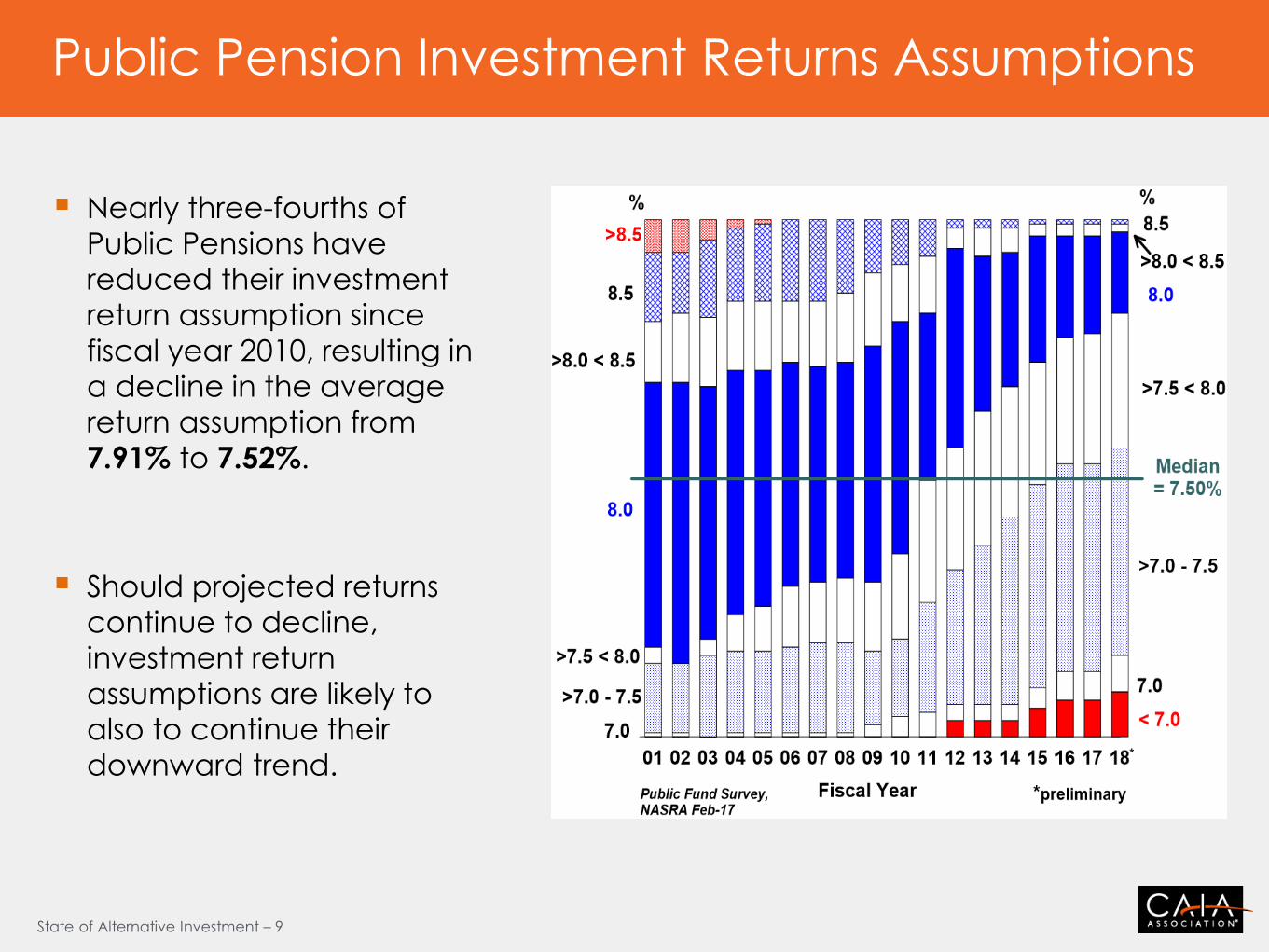

Public Pension Investment Returns Assumptions

Nearly three-fourths of

Public Pensions have

reduced their investment

return assumption since

fiscal year 2010, resulting in

a decline in the average

return assumption from

7.91% to 7.52%.

Should projected returns

continue to decline,

investment return

assumptions are likely to

also to continue their

downward trend.

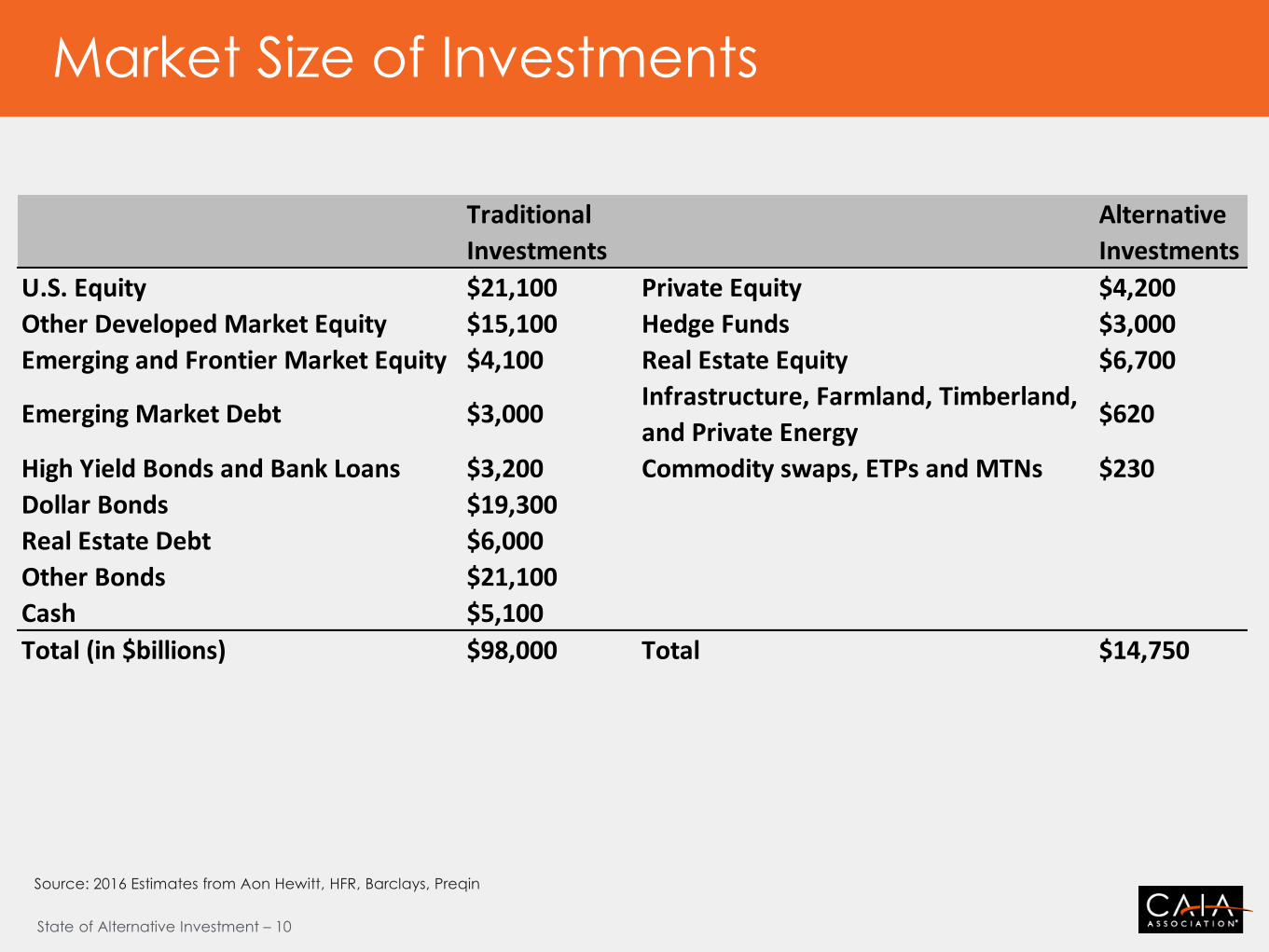

State of Alternative Investment – 10

Market Size of Investments

Source: 2016 Estimates from Aon Hewitt, HFR, Barclays, Preqin

Traditional

Investments

Alternative

Investments

U.S. Equity $21,100 Private Equity $4,200

Other Developed Market Equity $15,100 Hedge Funds $3,000

Emerging and Frontier Market Equity $4,100 Real Estate Equity $6,700

Emerging Market Debt $3,000 Infrastructure, Farmland, Timberland,

and Private Energy$620

High Yield Bonds and Bank Loans $3,200 Commodity swaps, ETPs and MTNs $230

Dollar Bonds $19,300

Real Estate Debt $6,000

Other Bonds $21,100

Cash $5,100

Total (in $billions) $98,000 Total $14,750

State of Alternative Investment – 11

Participation In Alternatives

Source: Preqin

State of Alternative Investment – 12

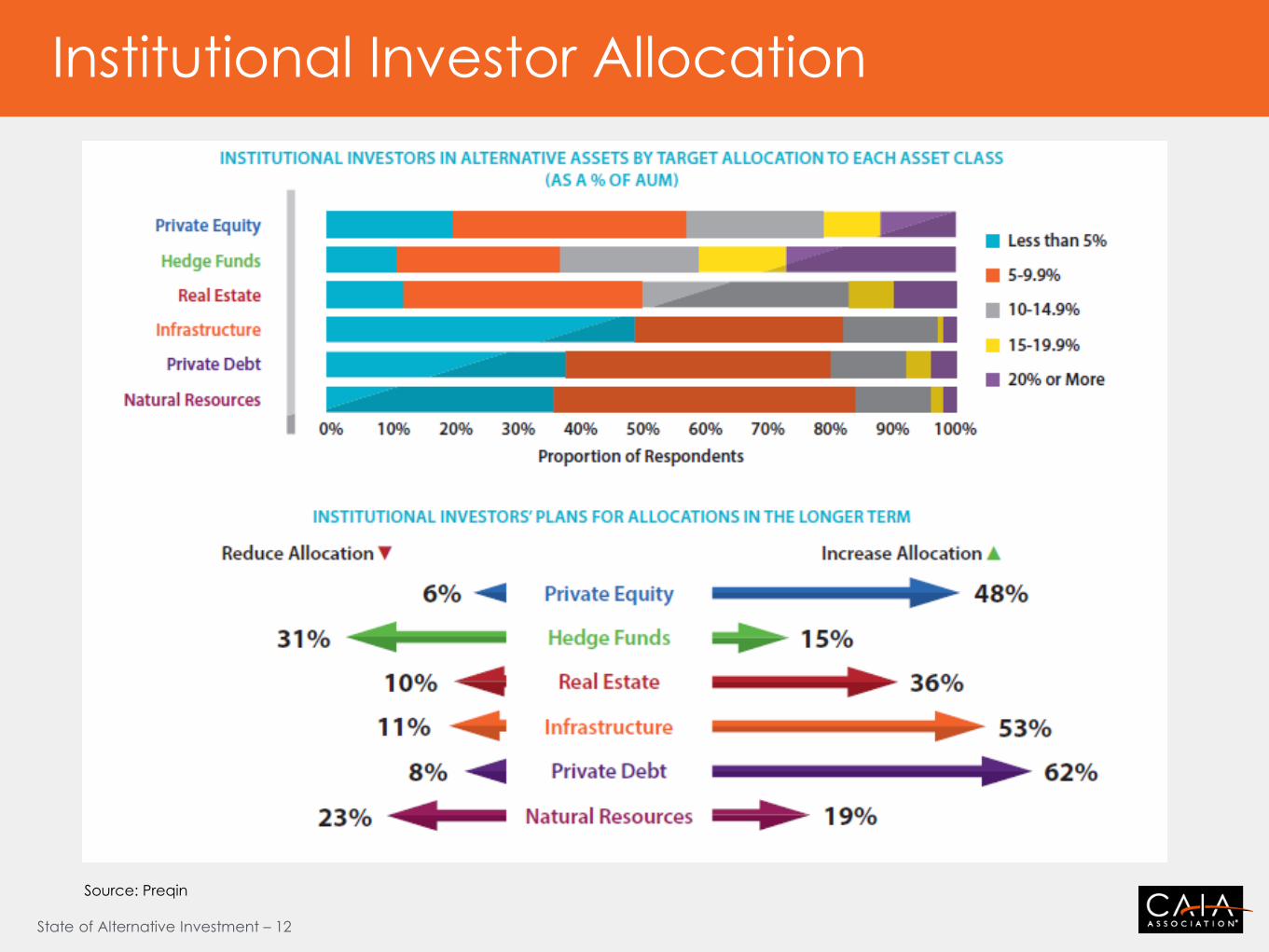

Institutional Investor Allocation

Source: Preqin

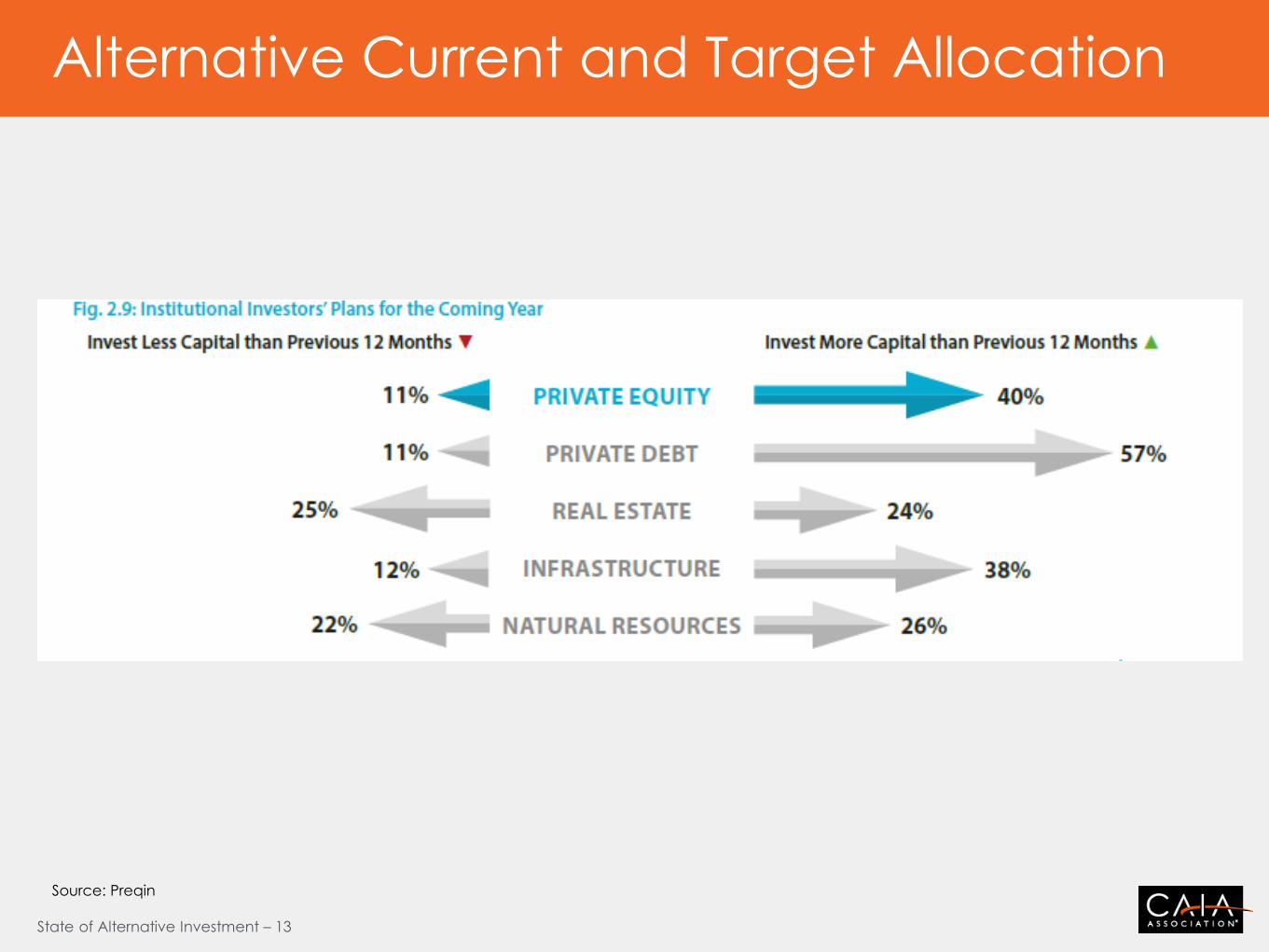

State of Alternative Investment – 13

Alternative Current and Target Allocation

Source: Preqin

State of Alternative Investment – 14

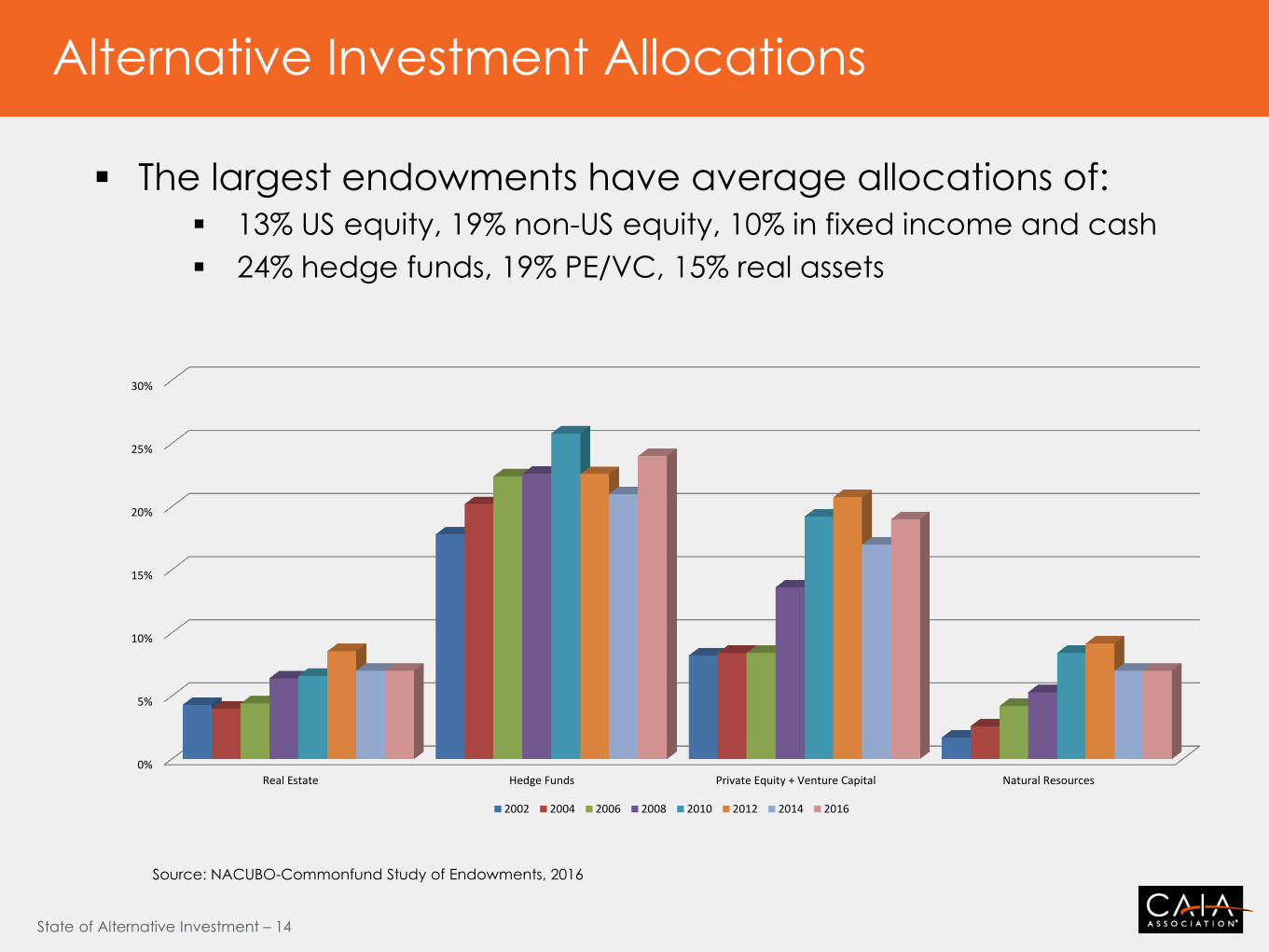

Alternative Investment Allocations

The largest endowments have average allocations of: 13% US equity, 19% non-US equity, 10% in fixed income and cash

24% hedge funds, 19% PE/VC, 15% real assets

Source: NACUBO-Commonfund Study of Endowments, 2016

0%

5%

10%

15%

20%

25%

30%

Real Estate Hedge Funds Private Equity + Venture Capital Natural Resources

2002 2004 2006 2008 2010 2012 2014 2016

State of Alternative Investment – 15

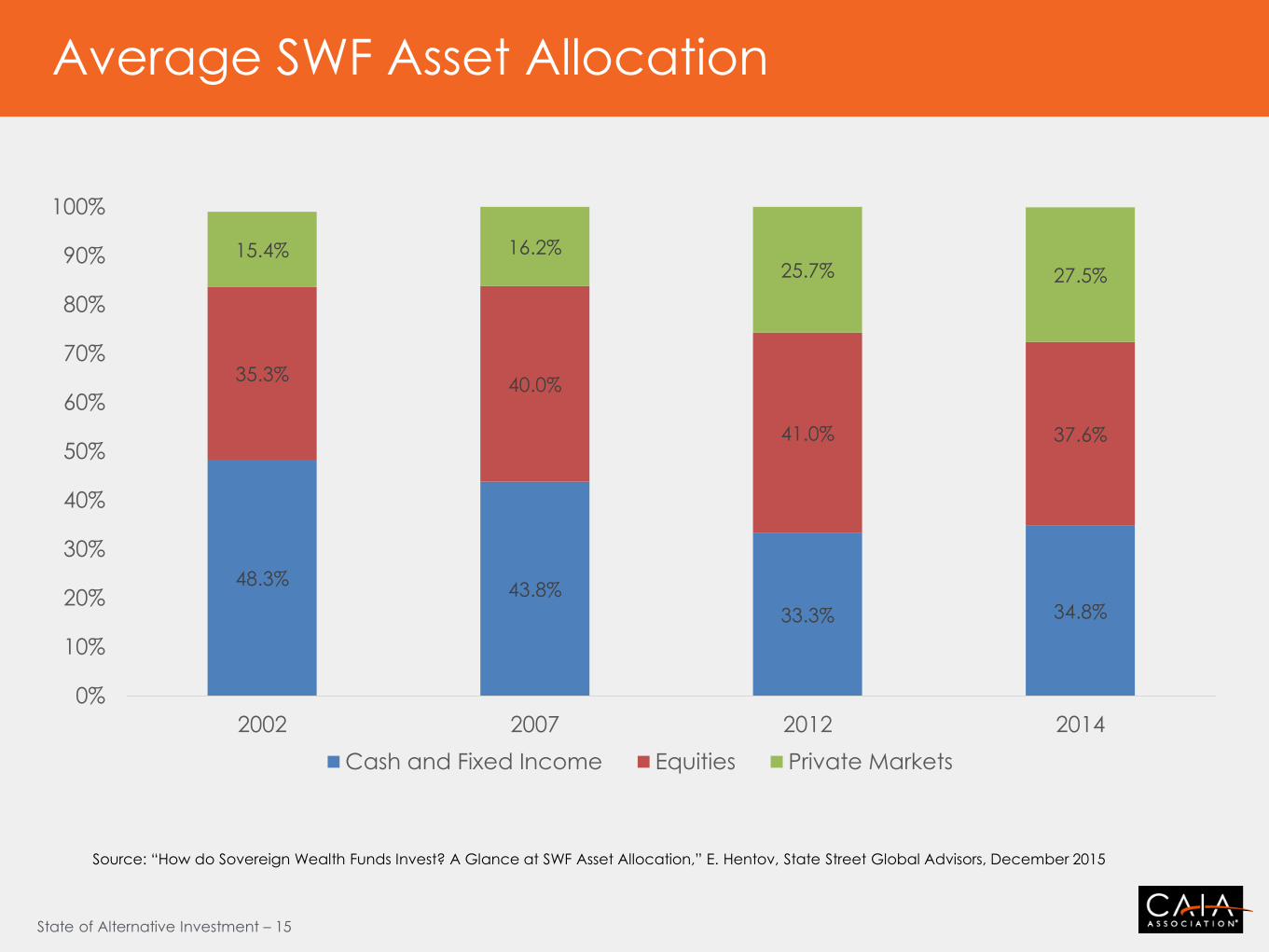

Average SWF Asset Allocation

Source: “How do Sovereign Wealth Funds Invest? A Glance at SWF Asset Allocation,” E. Hentov, State Street Global Advisors, December 2015

48.3% 43.8%

33.3% 34.8%

35.3% 40.0%

41.0% 37.6%

15.4% 16.2% 25.7% 27.5%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2002 2007 2012 2014

Cash and Fixed Income Equities Private Markets

State of Alternative Investment – 16

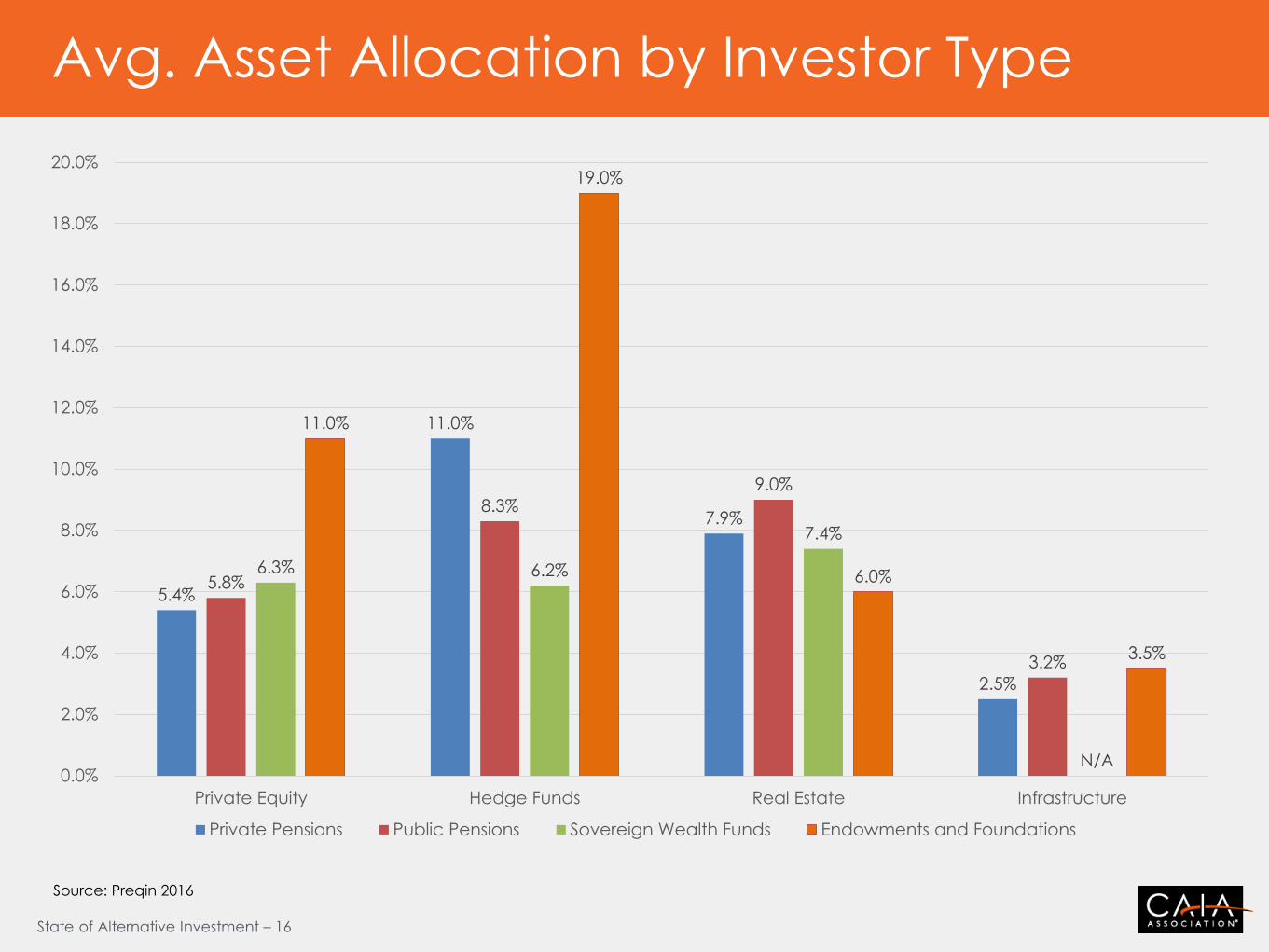

Avg. Asset Allocation by Investor Type

Source: Preqin 2016

5.4%

11.0%

7.9%

2.5%

5.8%

8.3%

9.0%

3.2%

6.3% 6.2%

7.4%

N/A

11.0%

19.0%

6.0%

3.5%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

20.0%

Private Equity Hedge Funds Real Estate Infrastructure

Private Pensions Public Pensions Sovereign Wealth Funds Endowments and Foundations

State of Alternative Investment – 17

Alternative Current and Target Allocation

10.3%

9.6% 9.5% 9.6% 9.6%

11.0%

10.6% 10.7% 10.7% 10.7%

8.5%

9.0%

9.5%

10.0%

10.5%

11.0%

11.5%

2013 2014 2015 2016 2017 YTD

Average Allocation to Private Equity (As a % of AUM)

Average Current Allocation Average Target Allocation

13.0%

13.3%

13.8%

13.1%

14.7%

13.8%

14.1%

14.4%

13.7%

13.5%

12.0%

12.5%

13.0%

13.5%

14.0%

14.5%

15.0%

2013 2014 2015 2016 2017 YTD

Average Allocation to Hedge Funds (As a % of AUM)

Average Current Allocation Average Target Allocation

9.3% 9.2%

9.3%

9.9%

9.0%

10.5% 10.3% 10.4%

10.6% 10.6%

8.0%

8.5%

9.0%

9.5%

10.0%

10.5%

11.0%

2013 2014 2015 2016 2017 YTD

Average Allocation to Real Estate (As a % of AUM)

Average Current Allocation Average Target Allocation

3.6%

4.3% 4.3%

3.9% 4.2%

5.1%

5.7% 5.7%

5.2% 5.4%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

2013 2014 2015 2016 2017 YTD

Average Allocation to Infrastructure (As a % of AUM)

Average Current Allocation Average Target Allocation

Source: Preqin

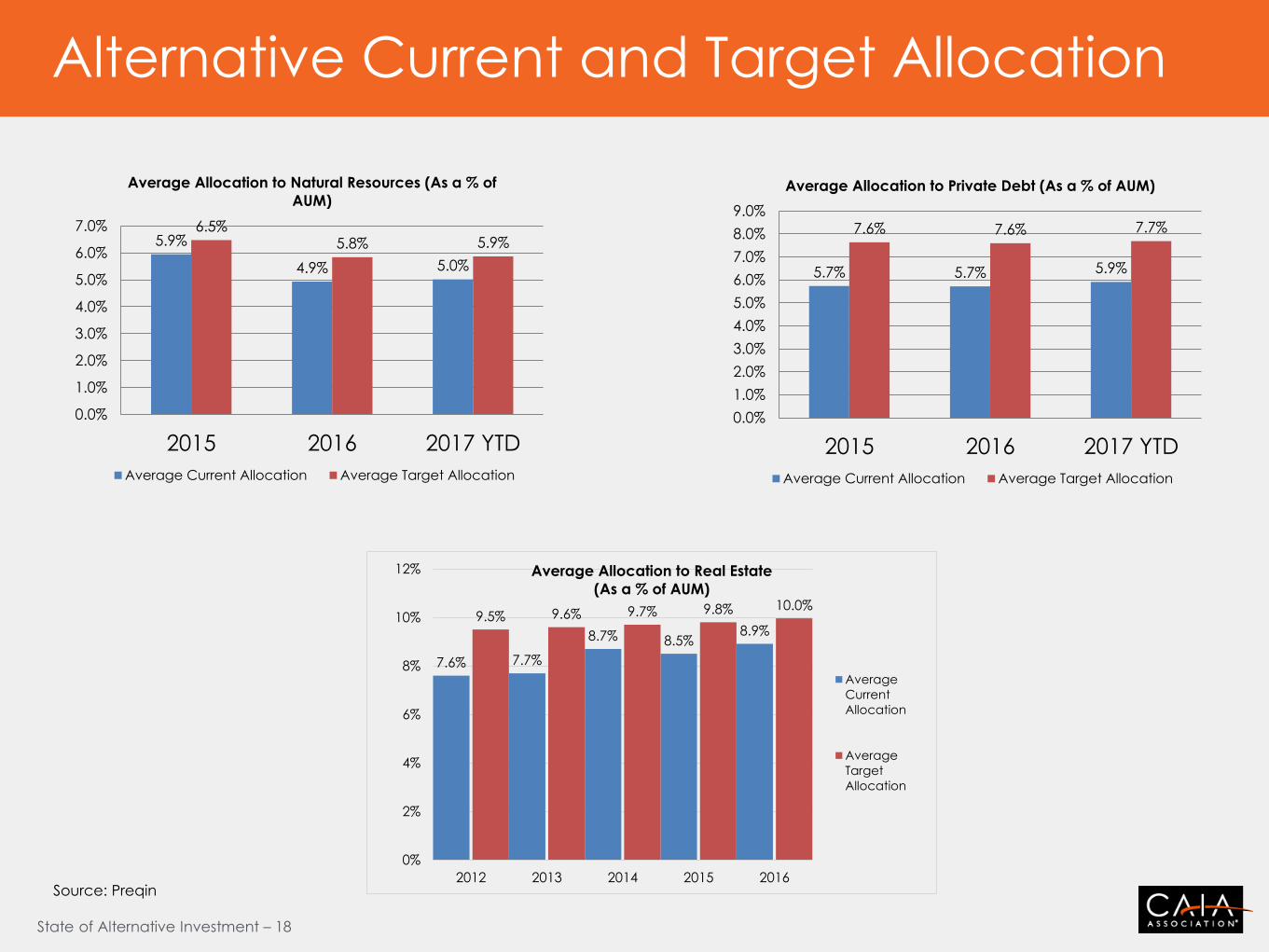

State of Alternative Investment – 18

Alternative Current and Target Allocation

5.9%

4.9% 5.0%

6.5% 5.8% 5.9%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

2015 2016 2017 YTD

Average Allocation to Natural Resources (As a % of

AUM)

Average Current Allocation Average Target Allocation

5.7% 5.7% 5.9%

7.6% 7.6% 7.7%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

2015 2016 2017 YTD

Average Allocation to Private Debt (As a % of AUM)

Average Current Allocation Average Target Allocation

Source: Preqin

7.6% 7.7%

8.7% 8.5% 8.9%

9.5% 9.6% 9.7% 9.8% 10.0%

0%

2%

4%

6%

8%

10%

12%

2012 2013 2014 2015 2016

Average Allocation to Real Estate

(As a % of AUM)

Average

Current

Allocation

Average

Target

Allocation

State of Alternative Investment – 19

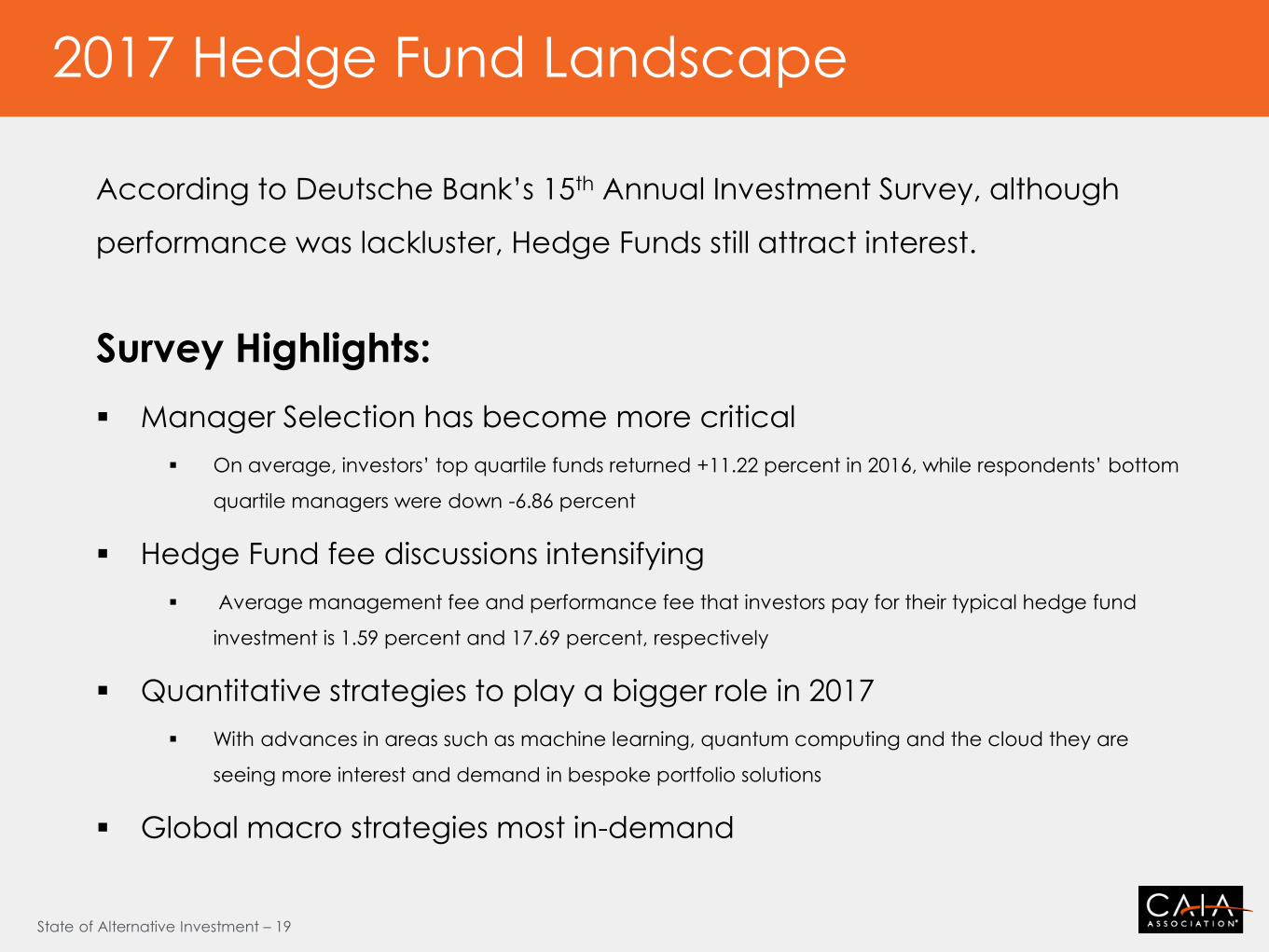

2017 Hedge Fund Landscape

According to Deutsche Bank’s 15th Annual Investment Survey, although

performance was lackluster, Hedge Funds still attract interest.

Survey Highlights:

Manager Selection has become more critical

On average, investors’ top quartile funds returned +11.22 percent in 2016, while respondents’ bottom

quartile managers were down -6.86 percent

Hedge Fund fee discussions intensifying

Average management fee and performance fee that investors pay for their typical hedge fund

investment is 1.59 percent and 17.69 percent, respectively

Quantitative strategies to play a bigger role in 2017

With advances in areas such as machine learning, quantum computing and the cloud they are

seeing more interest and demand in bespoke portfolio solutions

Global macro strategies most in-demand

State of Alternative Investment – 20

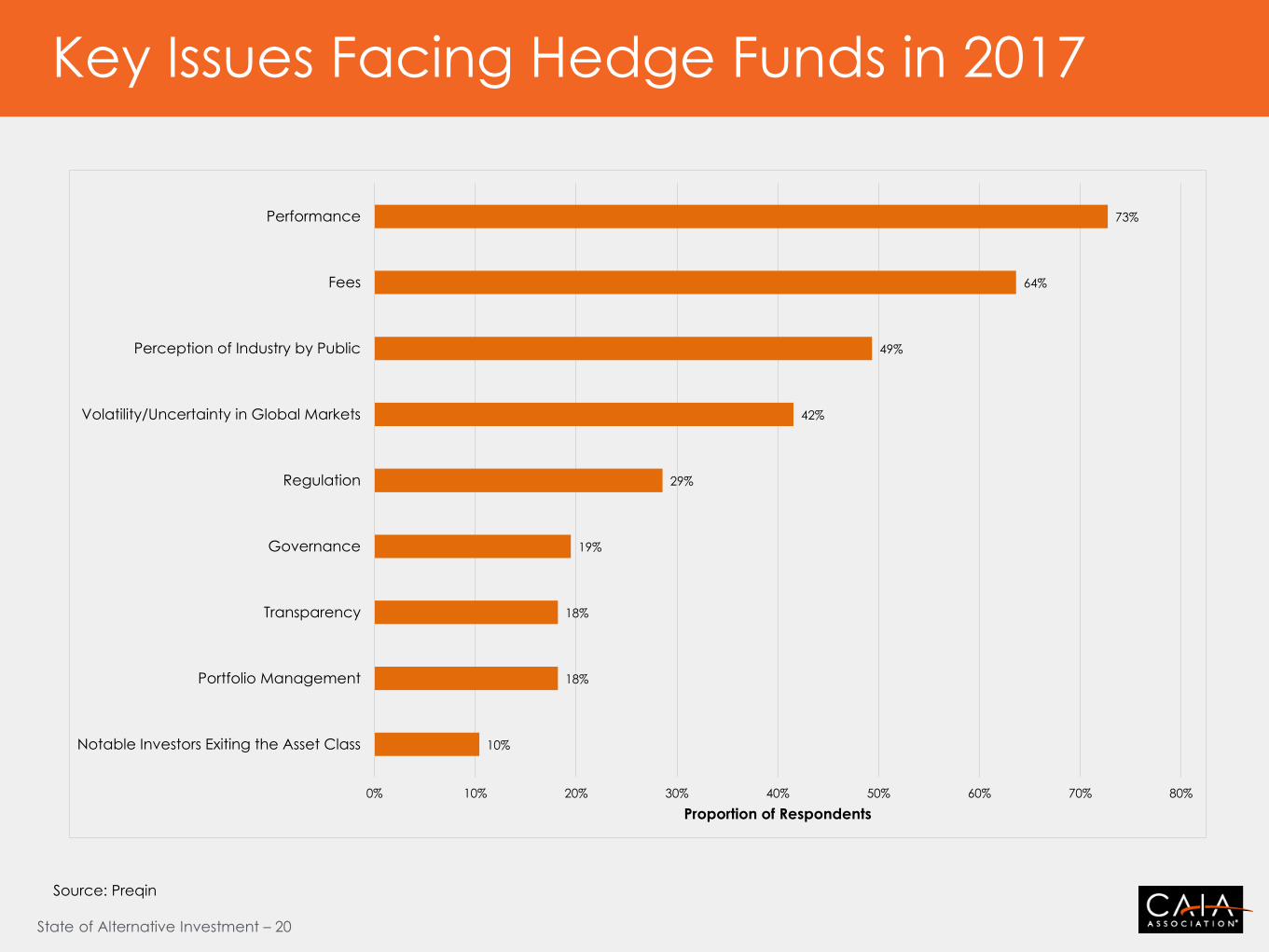

Key Issues Facing Hedge Funds in 2017

10%

18%

18%

19%

29%

42%

49%

64%

73%

0% 10% 20% 30% 40% 50% 60% 70% 80%

Notable Investors Exiting the Asset Class

Portfolio Management

Transparency

Governance

Regulation

Volatility/Uncertainty in Global Markets

Perception of Industry by Public

Fees

Performance

Proportion of Respondents

Source: Preqin

State of Alternative Investment – 21

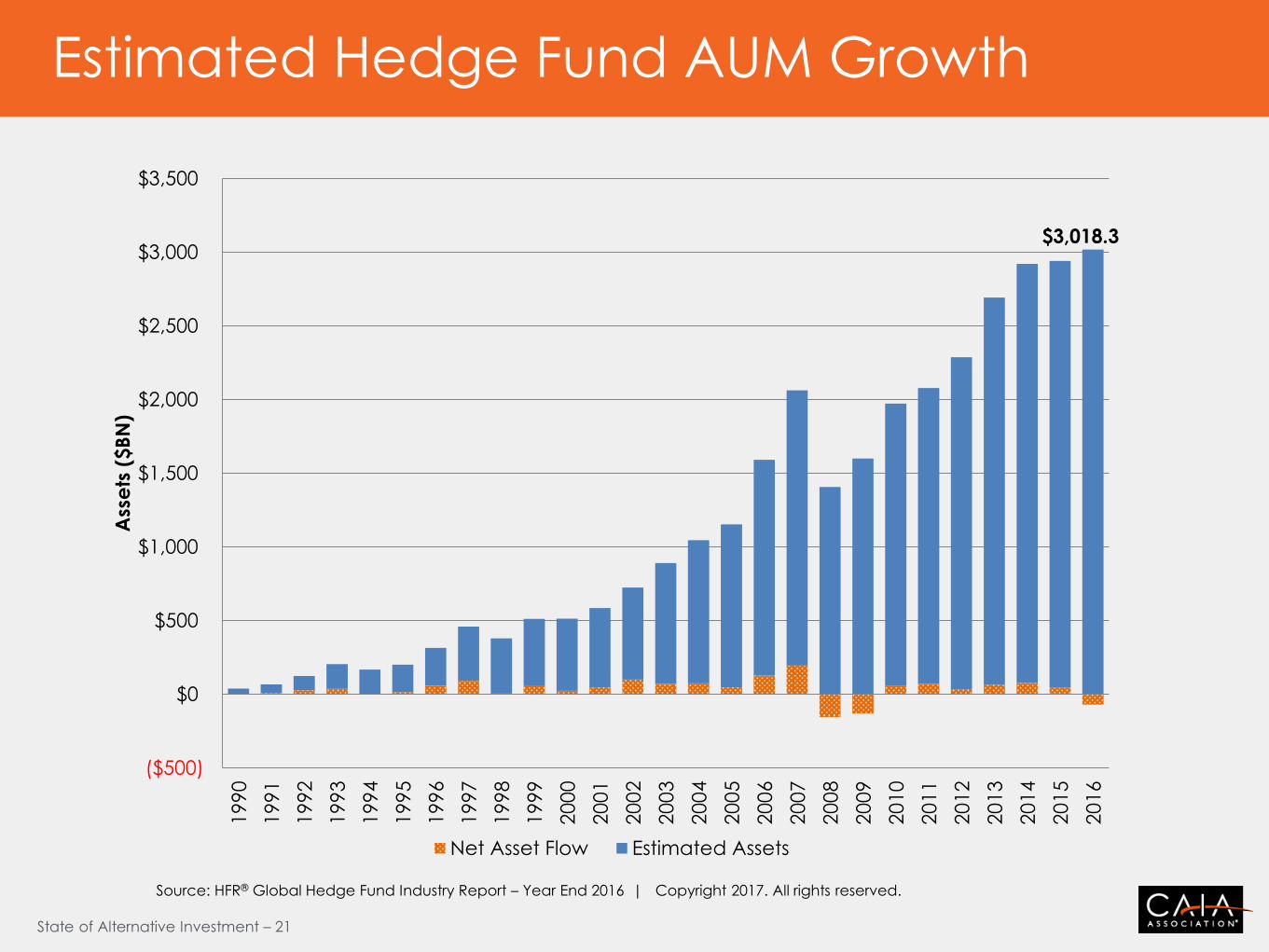

Estimated Hedge Fund AUM Growth

$3,018.3

($500)

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

Ass

ets

($B

N)

Net Asset Flow Estimated Assets

Source: HFR® Global Hedge Fund Industry Report – Year End 2016 | Copyright 2017. All rights reserved.

State of Alternative Investment – 22

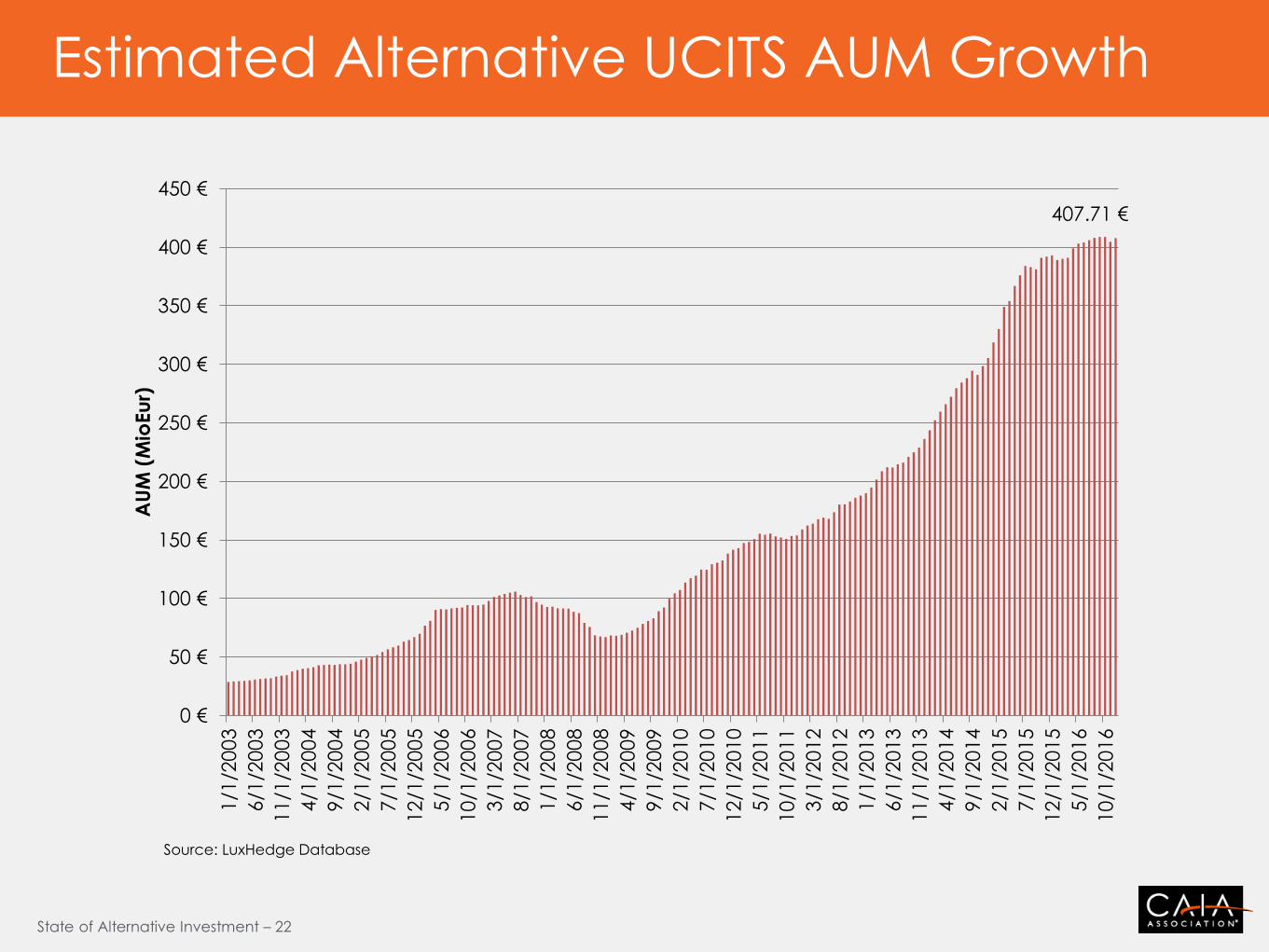

Estimated Alternative UCITS AUM Growth

407.71 €

0 €

50 €

100 €

150 €

200 €

250 €

300 €

350 €

400 €

450 €

1/1

/20

03

6/1

/20

03

11

/1/2

003

4/1

/20

04

9/1

/20

04

2/1

/20

05

7/1

/20

05

12

/1/2

005

5/1

/20

06

10

/1/2

006

3/1

/20

07

8/1

/20

07

1/1

/20

08

6/1

/20

08

11

/1/2

008

4/1

/20

09

9/1

/20

09

2/1

/20

10

7/1

/20

10

12

/1/2

01

0

5/1

/20

11

10

/1/2

011

3/1

/20

12

8/1

/20

12

1/1

/20

13

6/1

/20

13

11

/1/2

013

4/1

/20

14

9/1

/20

14

2/1

/20

15

7/1

/20

15

12

/1/2

015

5/1

/20

16

10

/1/2

016

AU

M (

Mio

Eu

r)

Source: LuxHedge Database

State of Alternative Investment – 23

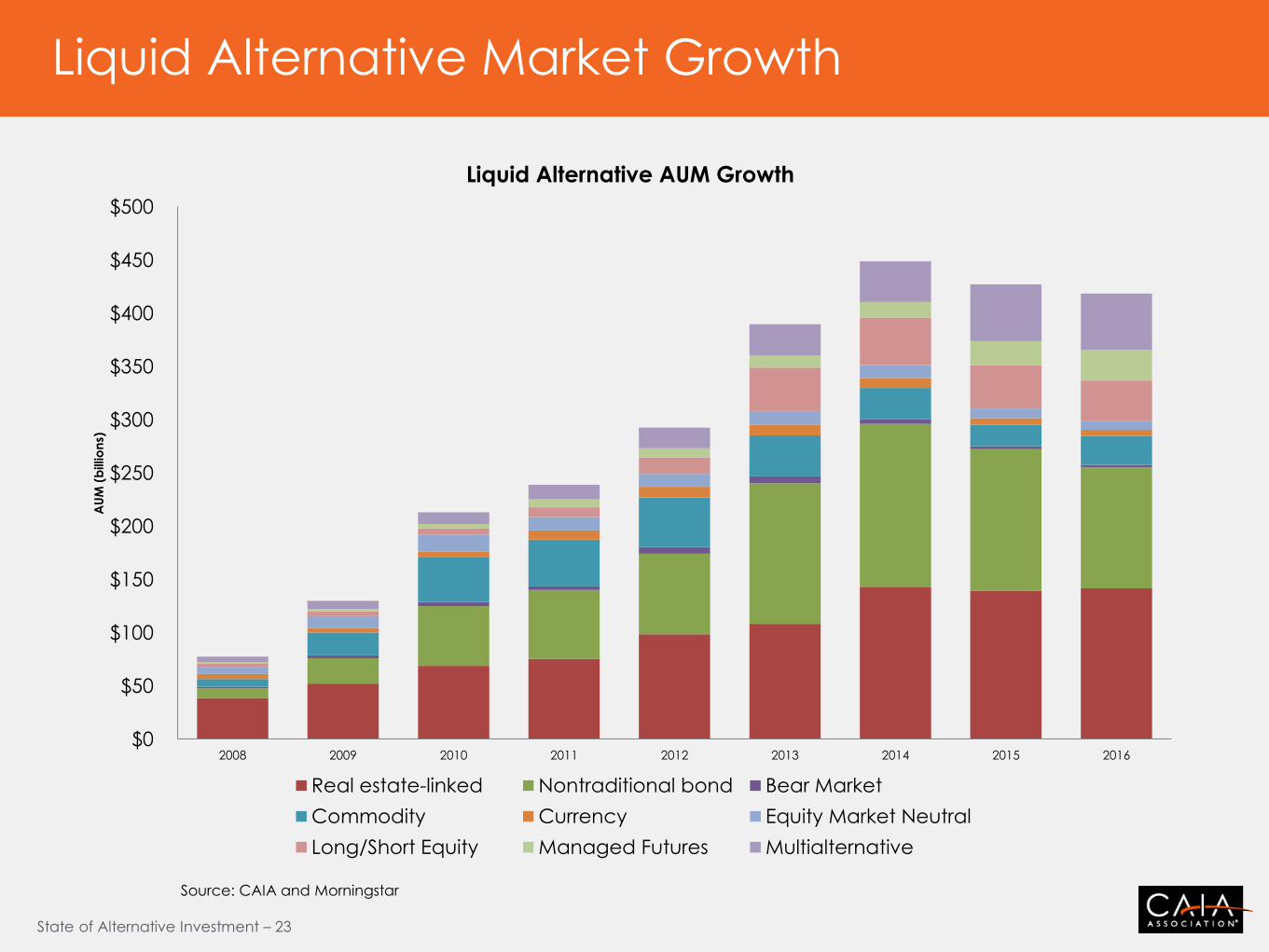

Liquid Alternative Market Growth

$0

$50

$100

$150

$200

$250

$300

$350

$400

$450

$500

2008 2009 2010 2011 2012 2013 2014 2015 2016

AU

M (

billio

ns)

Liquid Alternative AUM Growth

Real estate-linked Nontraditional bond Bear Market

Commodity Currency Equity Market Neutral

Long/Short Equity Managed Futures Multialternative

Source: CAIA and Morningstar

State of Alternative Investment – 24

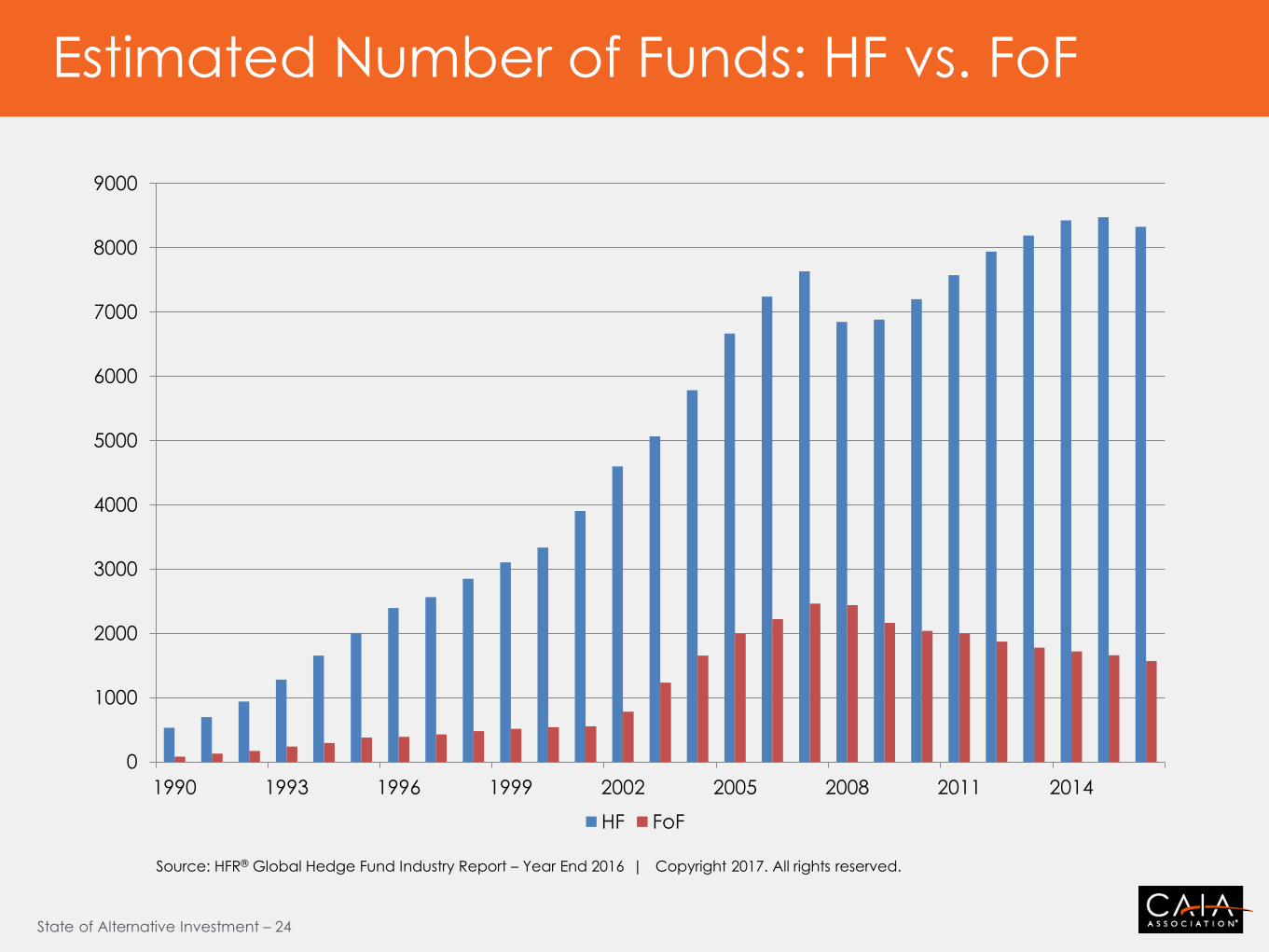

Estimated Number of Funds: HF vs. FoF

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

1990 1993 1996 1999 2002 2005 2008 2011 2014

HF FoF

Source: HFR® Global Hedge Fund Industry Report – Year End 2016 | Copyright 2017. All rights reserved.

State of Alternative Investment – 25

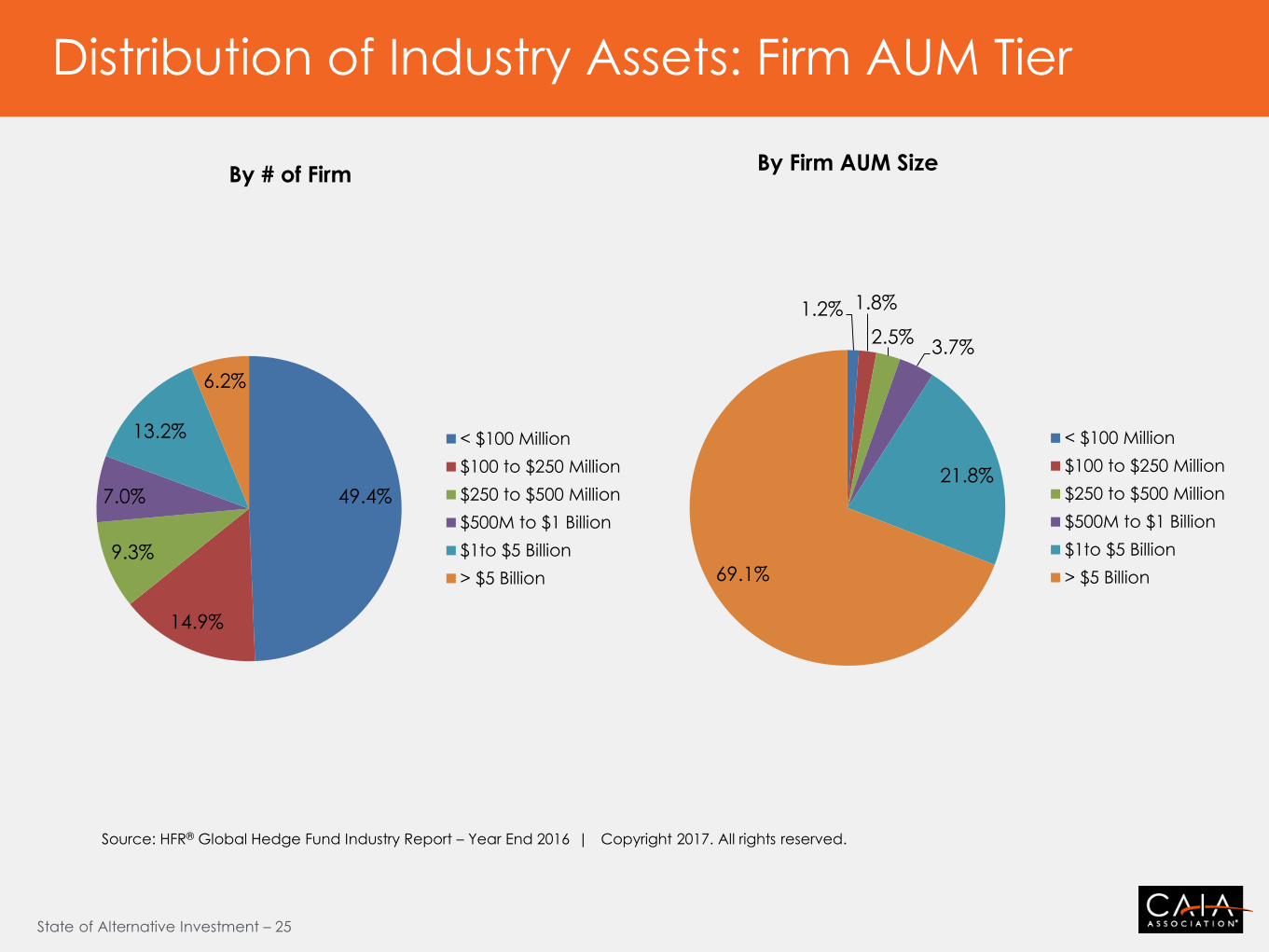

Distribution of Industry Assets: Firm AUM Tier

49.4%

14.9%

9.3%

7.0%

13.2%

6.2%

By # of Firm

< $100 Million

$100 to $250 Million

$250 to $500 Million

$500M to $1 Billion

$1to $5 Billion

> $5 Billion

1.2% 1.8%

2.5% 3.7%

21.8%

69.1%

By Firm AUM Size

< $100 Million

$100 to $250 Million

$250 to $500 Million

$500M to $1 Billion

$1to $5 Billion

> $5 Billion

Source: HFR® Global Hedge Fund Industry Report – Year End 2016 | Copyright 2017. All rights reserved.

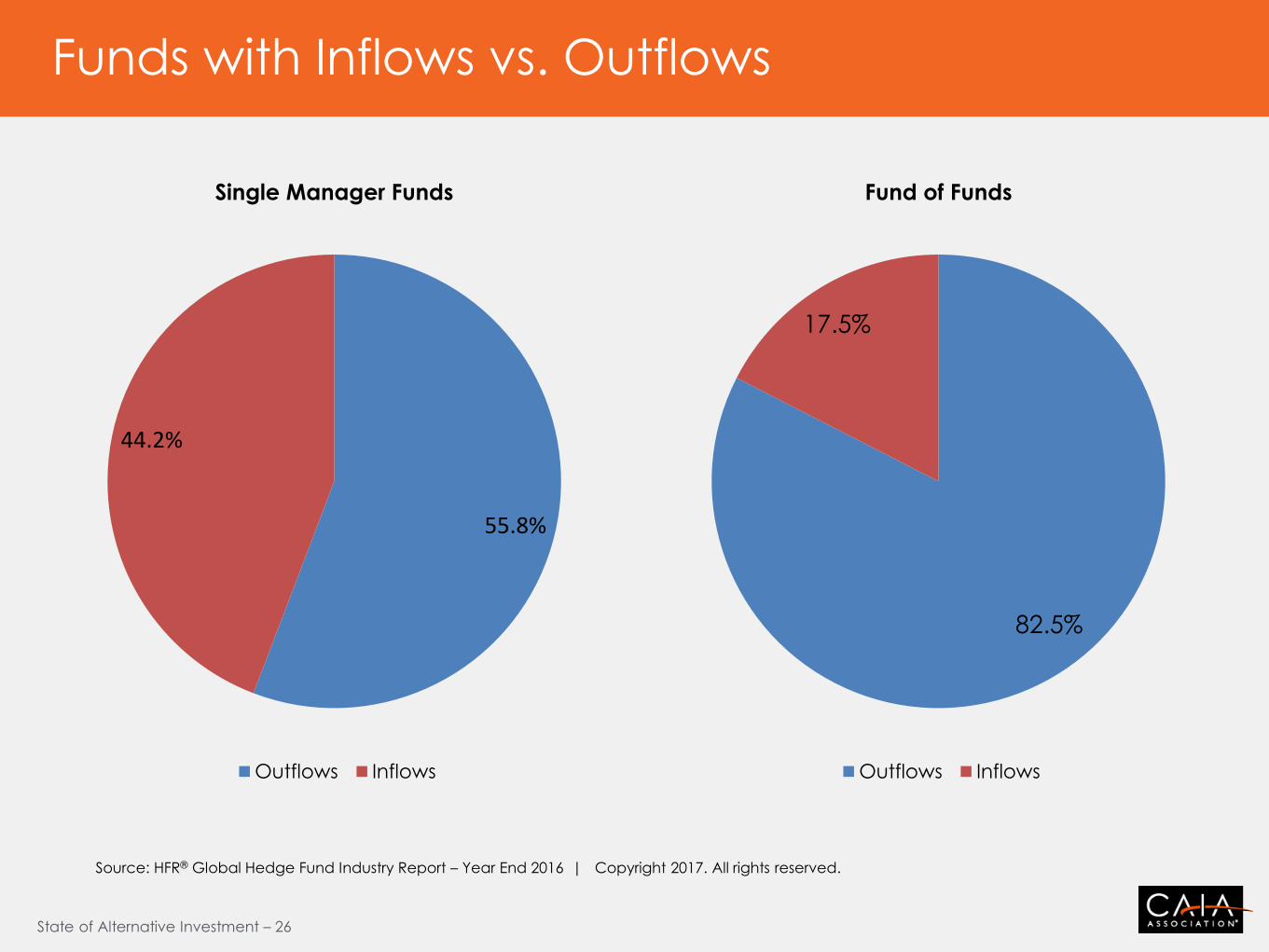

State of Alternative Investment – 26

Funds with Inflows vs. Outflows

55.8%

44.2%

Single Manager Funds

Outflows Inflows

82.5%

17.5%

Fund of Funds

Outflows Inflows

Source: HFR® Global Hedge Fund Industry Report – Year End 2016 | Copyright 2017. All rights reserved.

State of Alternative Investment – 27

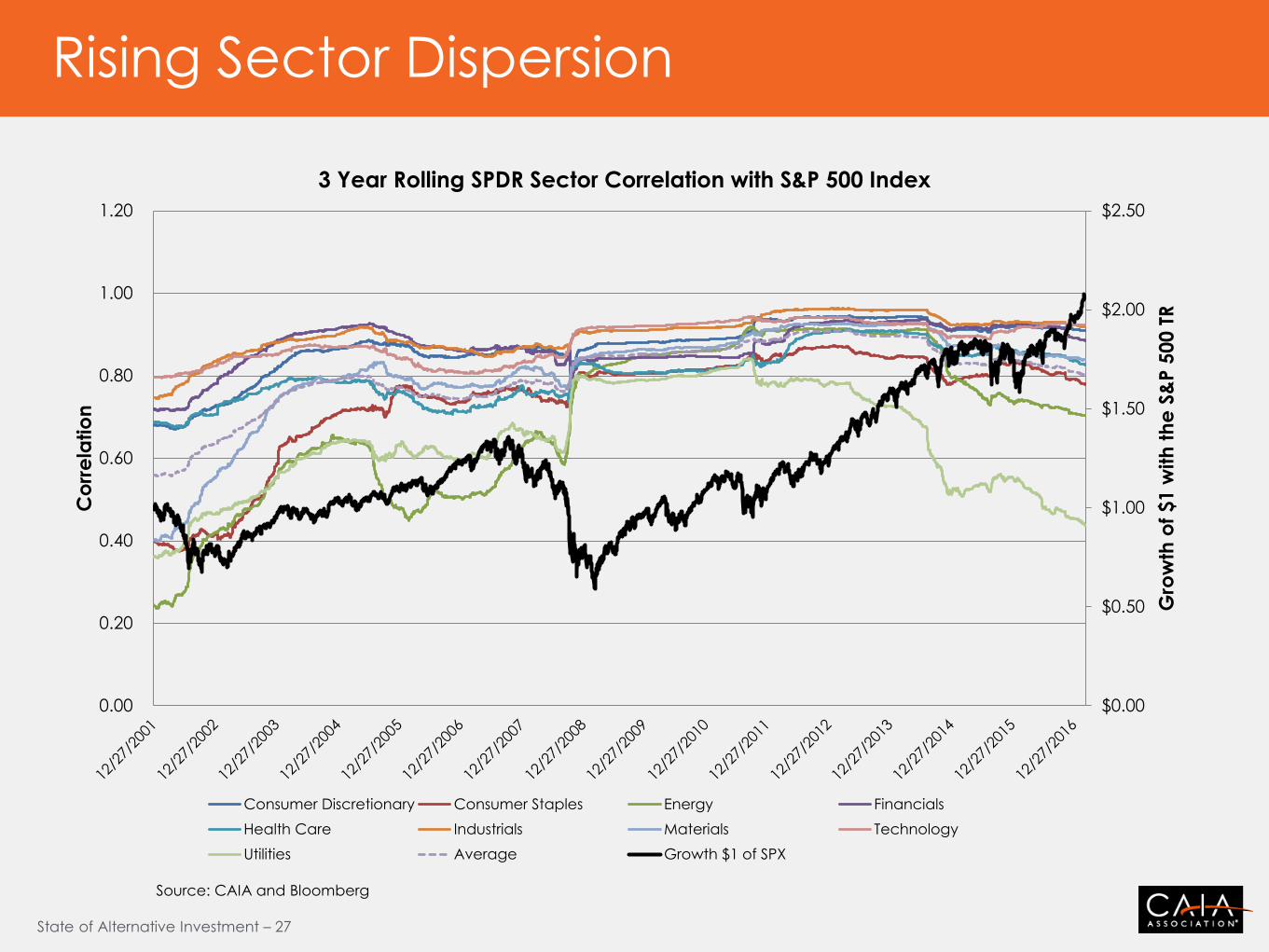

Rising Sector Dispersion

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

0.00

0.20

0.40

0.60

0.80

1.00

1.20

Gro

wth

of

$1 w

ith

th

e S

&P 5

00 T

R

Co

rre

latio

n

3 Year Rolling SPDR Sector Correlation with S&P 500 Index

Consumer Discretionary Consumer Staples Energy Financials

Health Care Industrials Materials Technology

Utilities Average Growth $1 of SPX

Source: CAIA and Bloomberg

State of Alternative Investment – 28

Private Capital AUM by Asset Class

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

De

c-0

5

De

c-0

6

De

c-0

7

De

c-0

8

De

c-0

9

De

c-1

0

De

c-1

1

De

c-1

2

De

c-1

3

De

c-1

4

De

c-1

5

Ju

n-1

6

Ass

ets

un

de

r M

an

ag

em

en

t ($

bn

)

Private Equity Private Debt Real Estate Infrastructure Natural Resources

Source: Preqin Online Products

State of Alternative Investment – 29

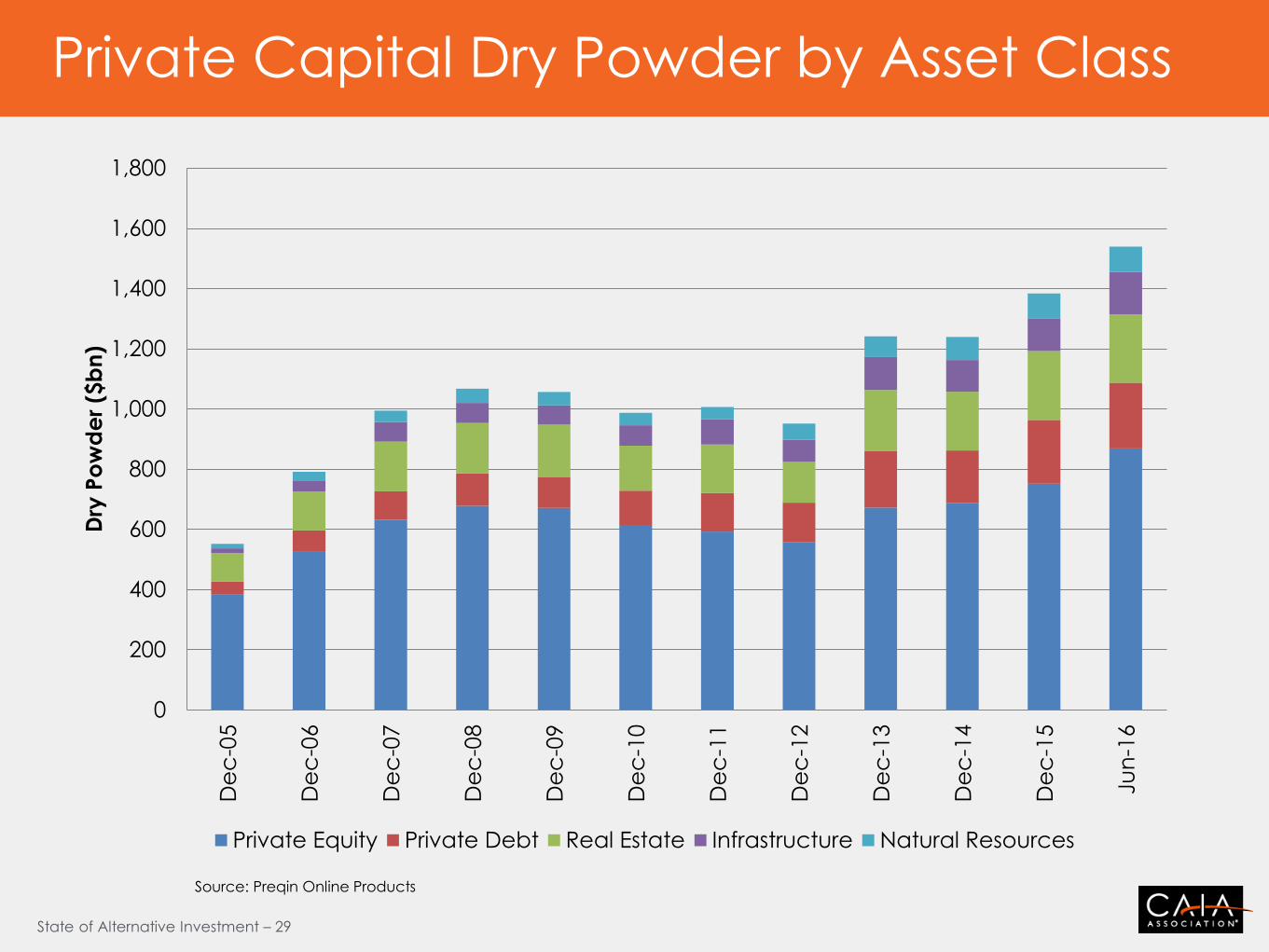

Private Capital Dry Powder by Asset Class

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

De

c-0

5

De

c-0

6

De

c-0

7

De

c-0

8

De

c-0

9

De

c-1

0

De

c-1

1

De

c-1

2

De

c-1

3

De

c-1

4

De

c-1

5

Ju

n-1

6

Dry

Po

wd

er

($b

n)

Private Equity Private Debt Real Estate Infrastructure Natural Resources

Source: Preqin Online Products

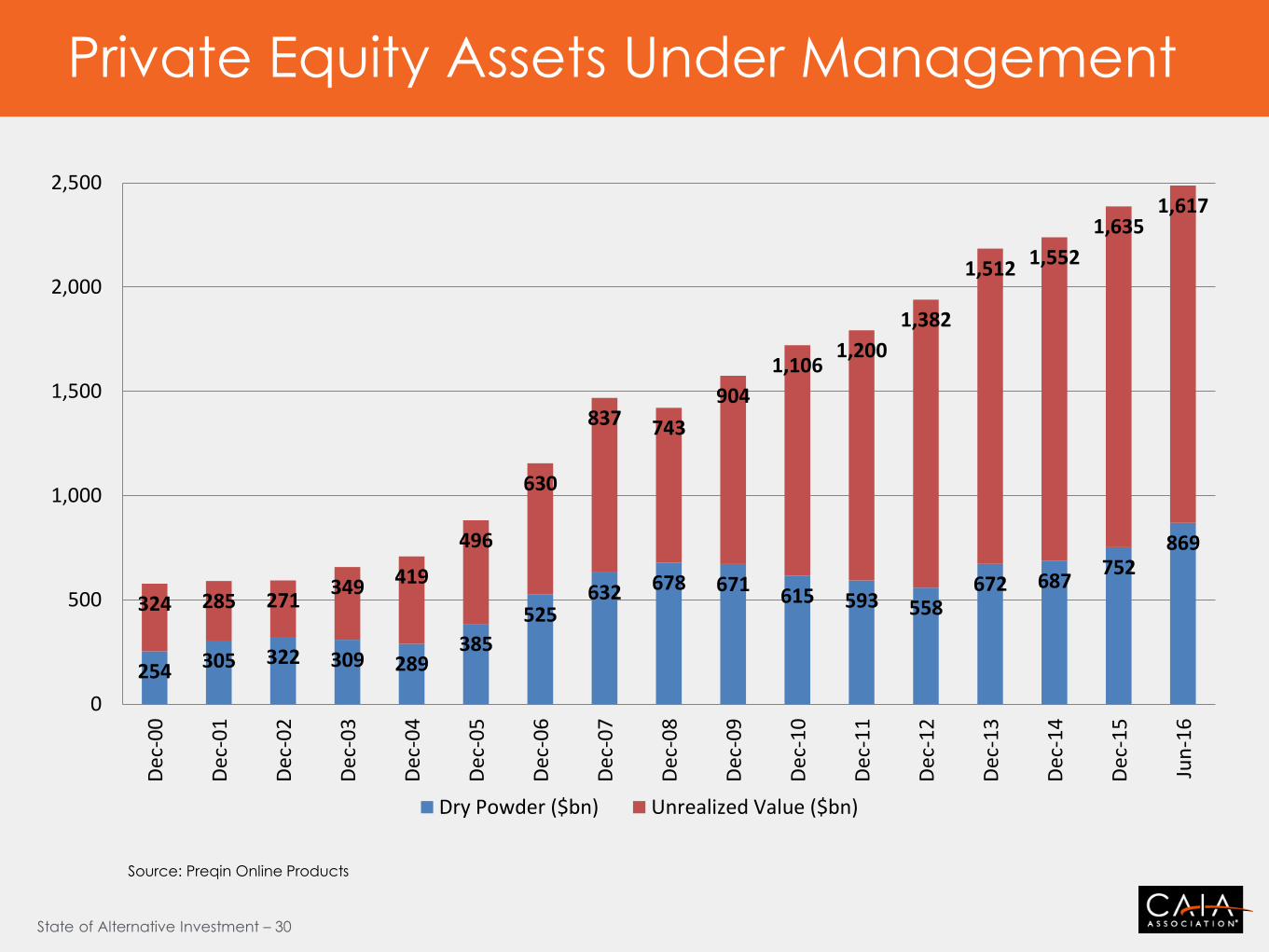

State of Alternative Investment – 30

Private Equity Assets Under Management

254 305 322 309 289 385

525 632 678 671

615 593 558 672 687

752 869

324 285 271 349 419

496

630

837 743

904

1,106 1,200

1,382

1,512 1,552

1,635 1,617

0

500

1,000

1,500

2,000

2,500D

ec-0

0

Dec

-01

Dec

-02

Dec

-03

Dec

-04

Dec

-05

Dec

-06

Dec

-07

Dec

-08

Dec

-09

Dec

-10

Dec

-11

Dec

-12

Dec

-13

Dec

-14

Dec

-15

Jun

-16

Dry Powder ($bn) Unrealized Value ($bn)

Source: Preqin Online Products

State of Alternative Investment – 31

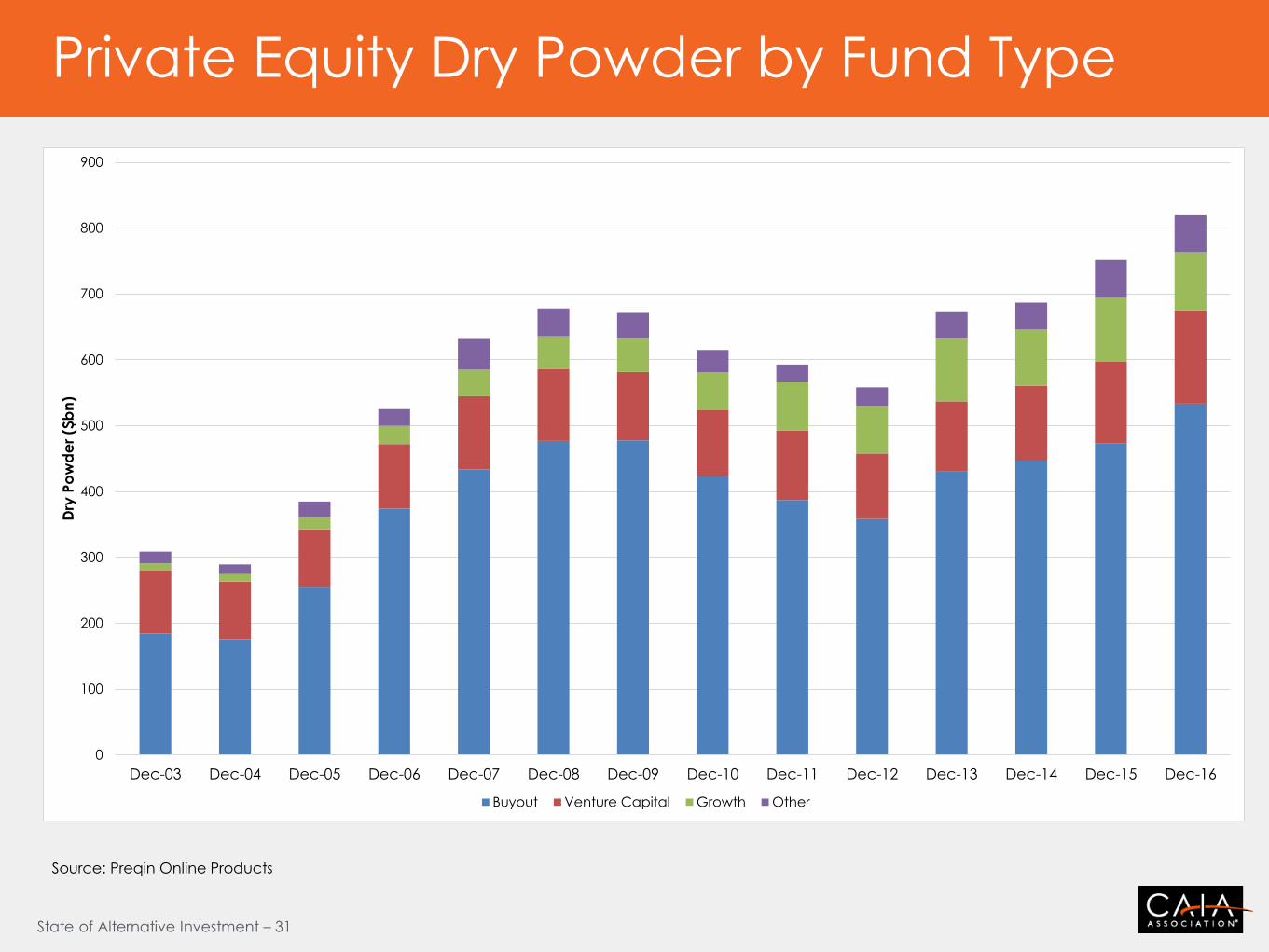

Private Equity Dry Powder by Fund Type

0

100

200

300

400

500

600

700

800

900

Dec-03 Dec-04 Dec-05 Dec-06 Dec-07 Dec-08 Dec-09 Dec-10 Dec-11 Dec-12 Dec-13 Dec-14 Dec-15 Dec-16

Dry

Po

wd

er

($b

n)

Buyout Venture Capital Growth Other

Source: Preqin Online Products

State of Alternative Investment – 32

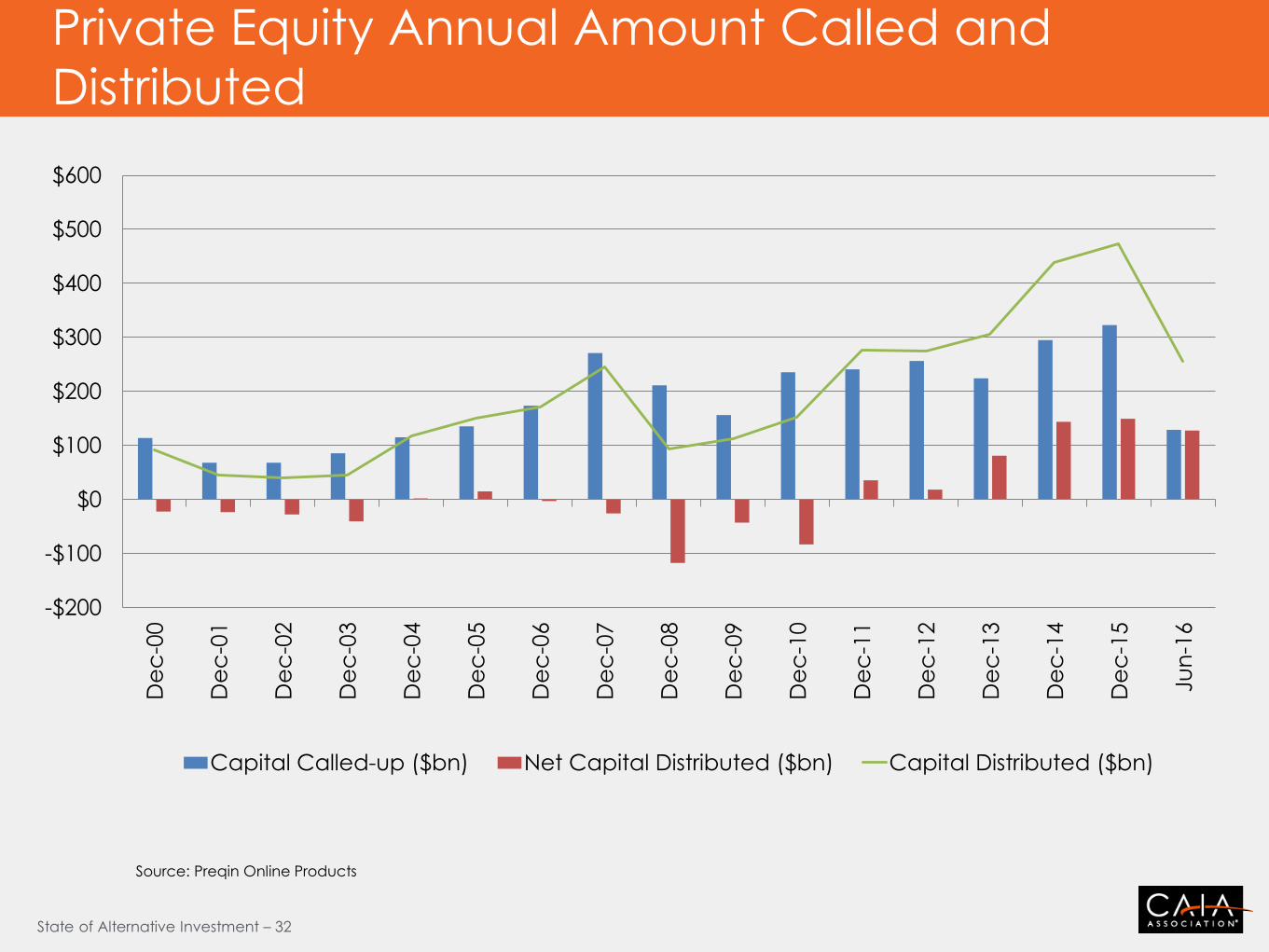

Private Equity Annual Amount Called and

Distributed

-$200

-$100

$0

$100

$200

$300

$400

$500

$600D

ec

-00

De

c-0

1

De

c-0

2

De

c-0

3

De

c-0

4

De

c-0

5

De

c-0

6

De

c-0

7

De

c-0

8

De

c-0

9

De

c-1

0

De

c-1

1

De

c-1

2

De

c-1

3

De

c-1

4

De

c-1

5

Ju

n-1

6

Capital Called-up ($bn) Net Capital Distributed ($bn) Capital Distributed ($bn)

Source: Preqin Online Products

State of Alternative Investment – 33

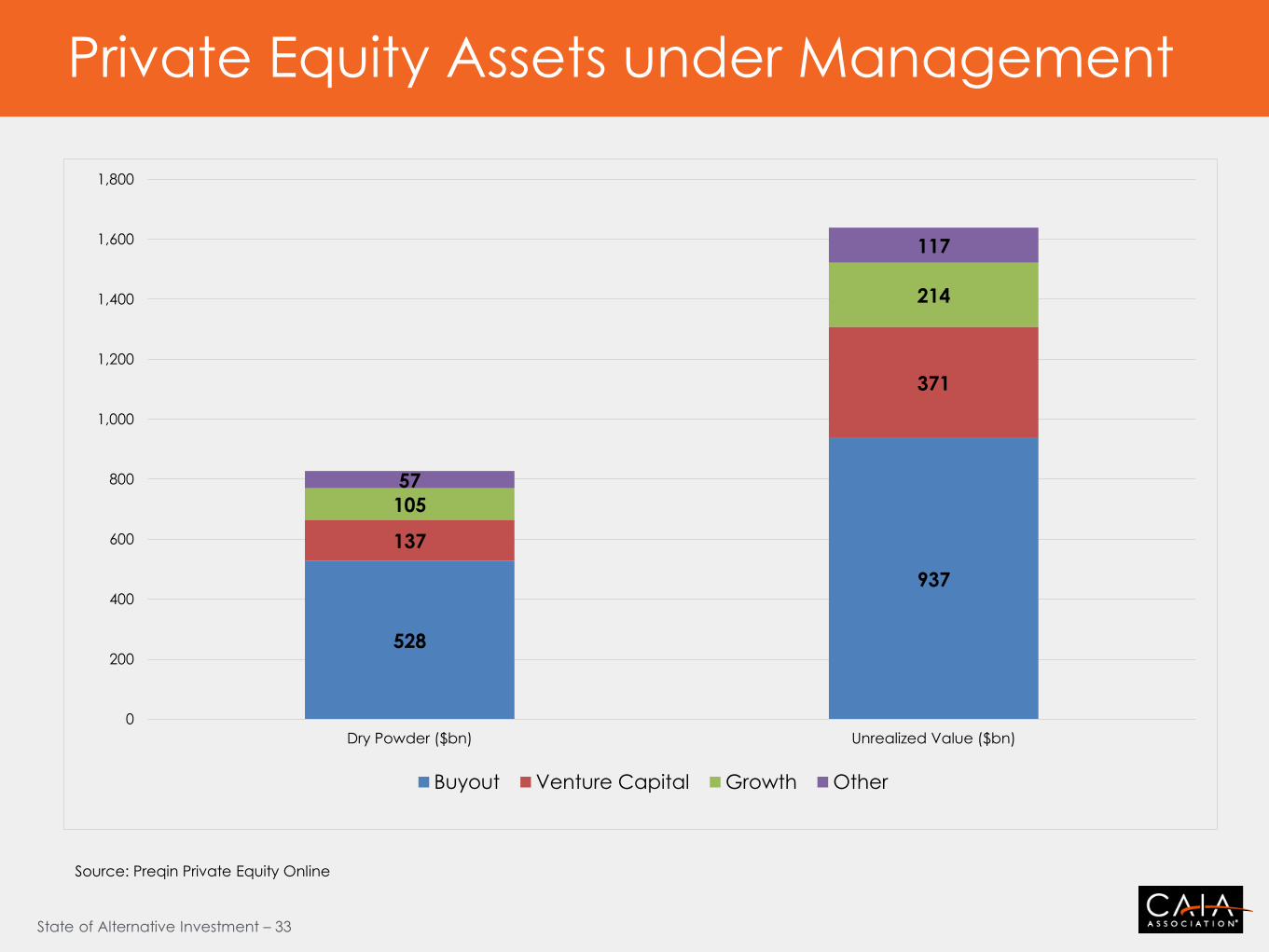

Private Equity Assets under Management

528

937

137

371

105

214

57

117

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

Dry Powder ($bn) Unrealized Value ($bn)

Buyout Venture Capital Growth Other

Source: Preqin Private Equity Online

State of Alternative Investment – 34

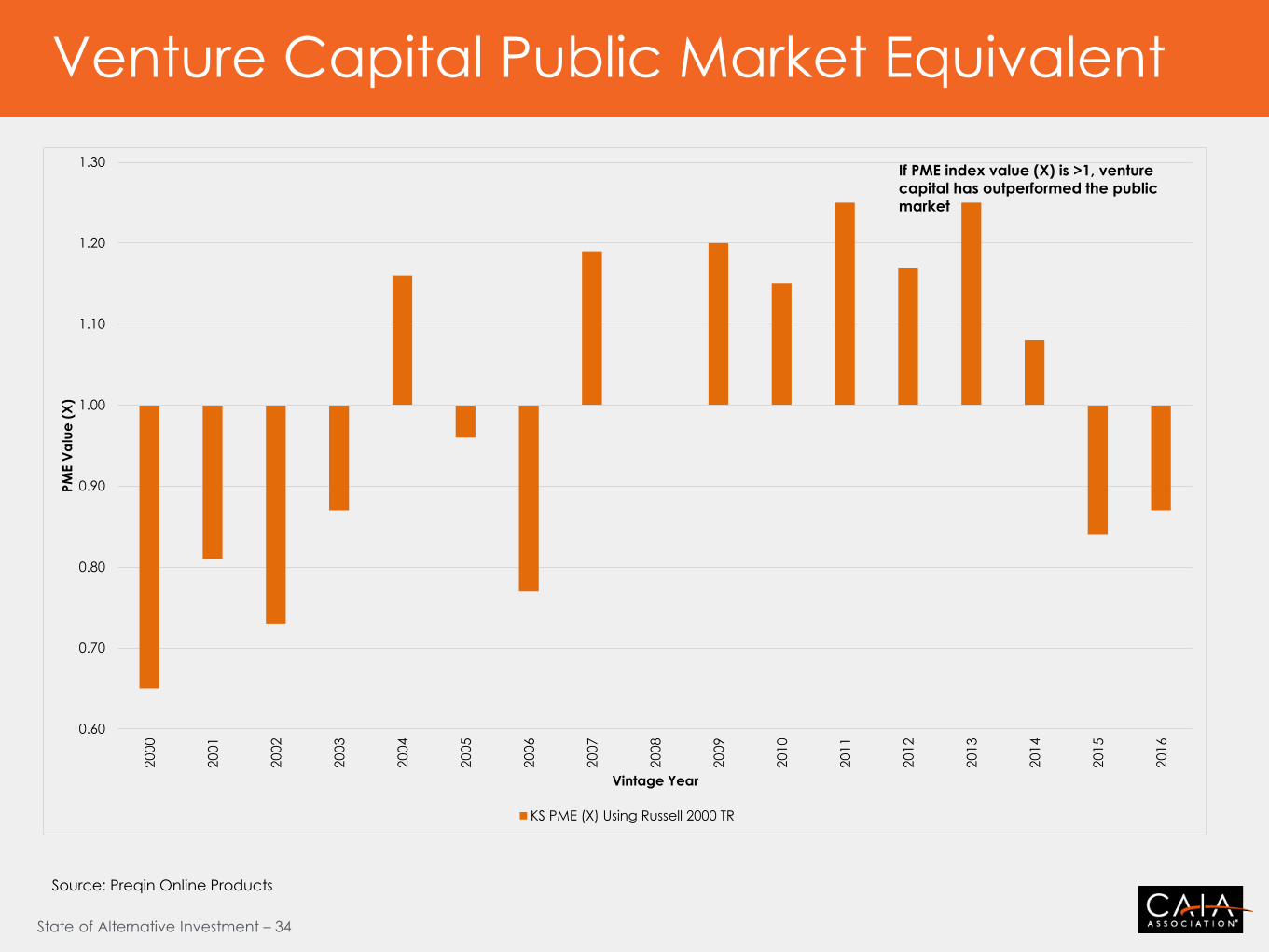

Venture Capital Public Market Equivalent

0.60

0.70

0.80

0.90

1.00

1.10

1.20

1.302

000

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

PM

E V

alu

e (

X)

Vintage Year

KS PME (X) Using Russell 2000 TR

If PME index value (X) is >1, venture

capital has outperformed the public

market

Source: Preqin Online Products

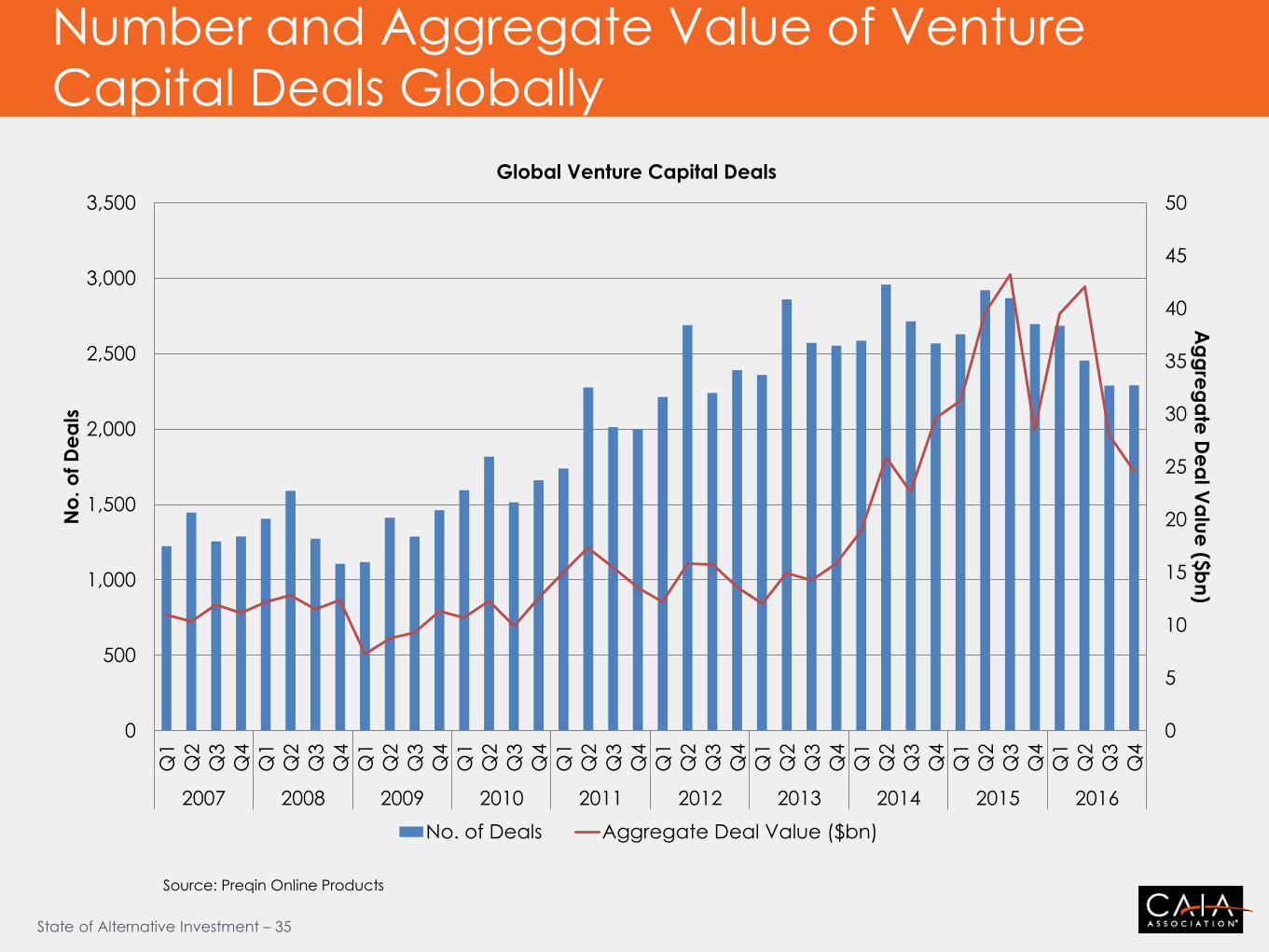

State of Alternative Investment – 35

Number and Aggregate Value of Venture

Capital Deals Globally

0

5

10

15

20

25

30

35

40

45

50

0

500

1,000

1,500

2,000

2,500

3,000

3,500

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Ag

gre

ga

te D

ea

l Va

lue

($b

n)

No

. o

f D

ea

ls

Global Venture Capital Deals

No. of Deals Aggregate Deal Value ($bn)

Source: Preqin Online Products

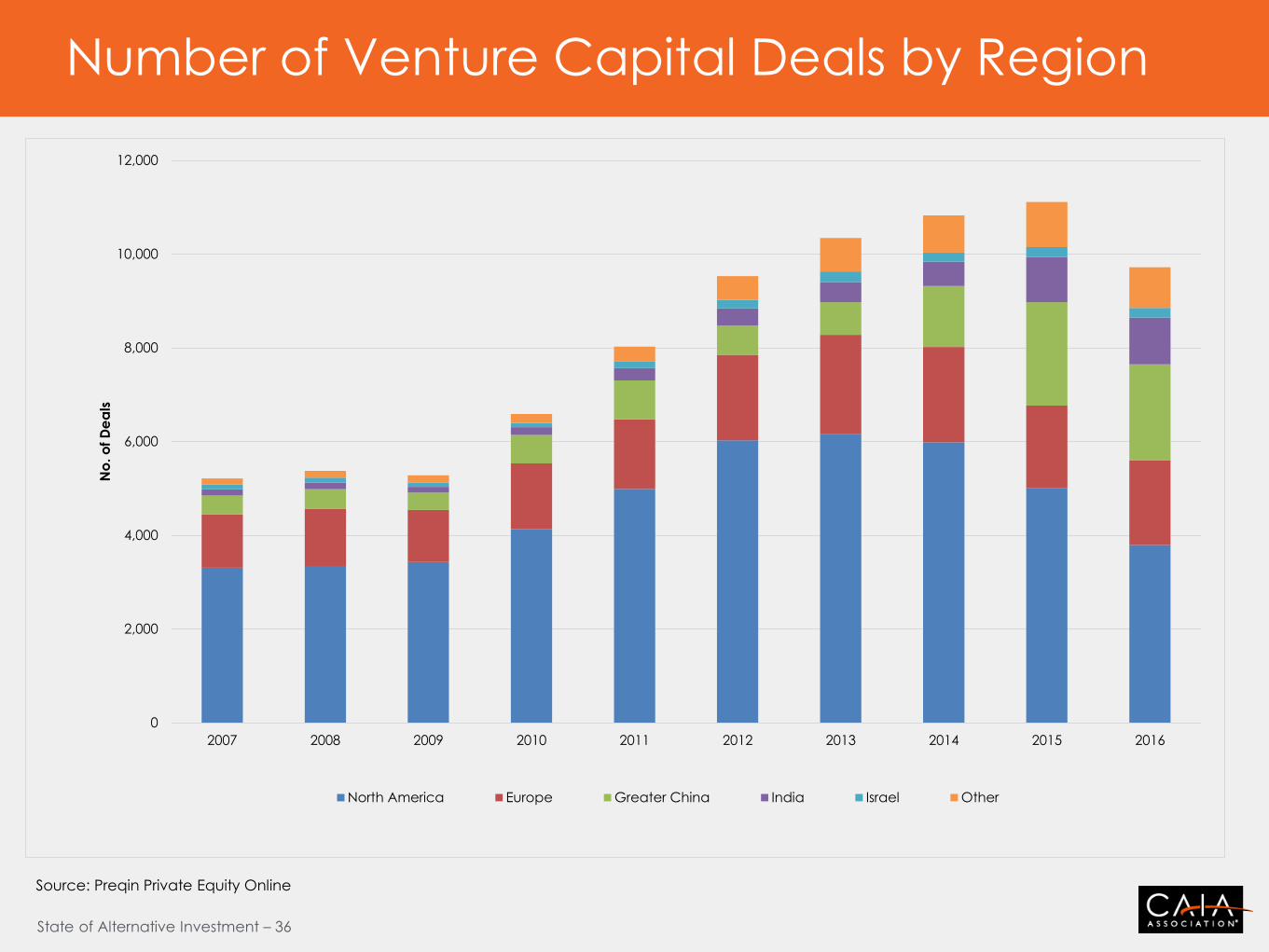

State of Alternative Investment – 36

Number of Venture Capital Deals by Region

0

2,000

4,000

6,000

8,000

10,000

12,000

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

No

. o

f D

ea

ls

North America Europe Greater China India Israel Other

Source: Preqin Private Equity Online

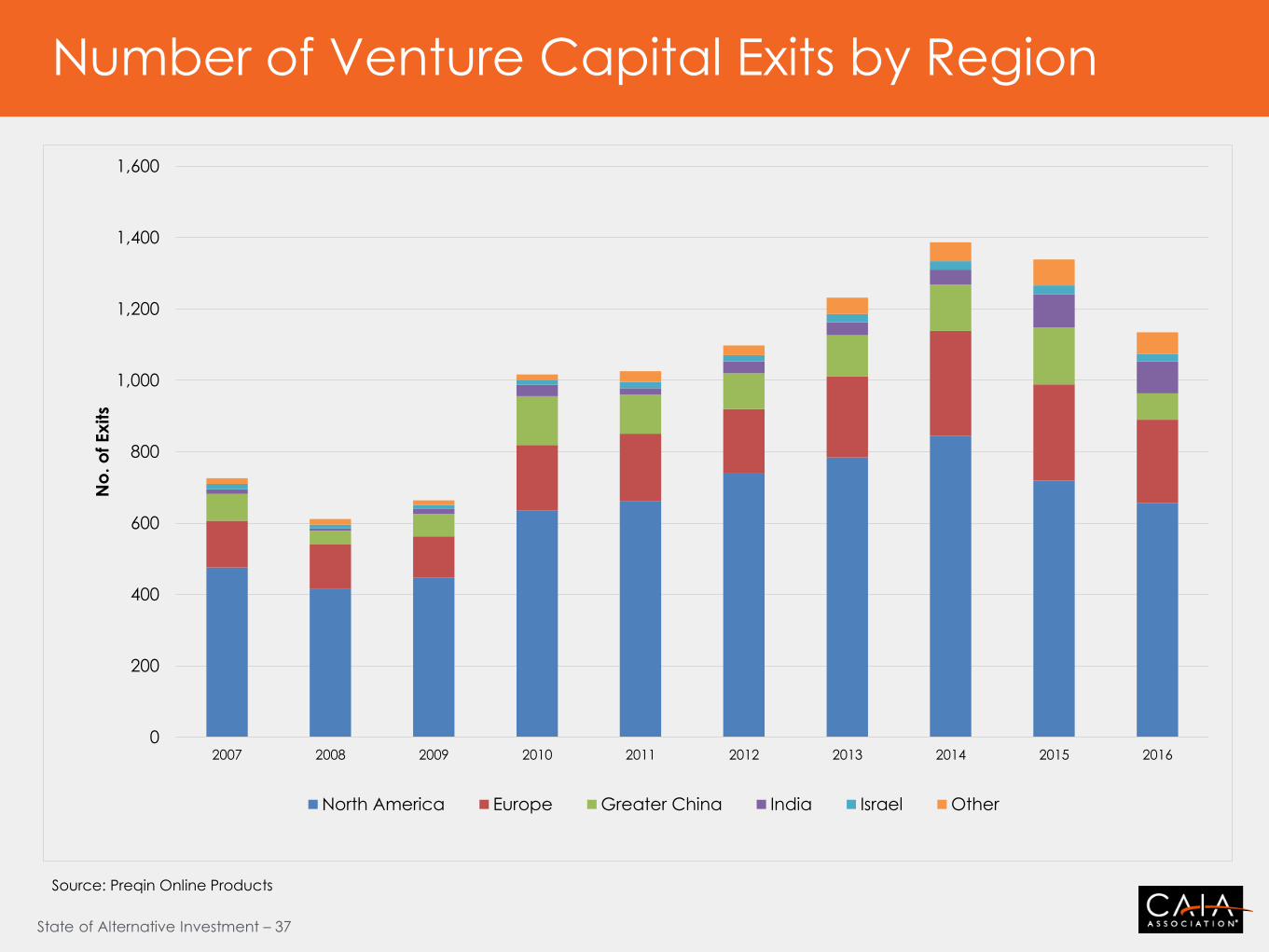

State of Alternative Investment – 37

Number of Venture Capital Exits by Region

0

200

400

600

800

1,000

1,200

1,400

1,600

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

No

. o

f Ex

its

North America Europe Greater China India Israel Other

Source: Preqin Online Products

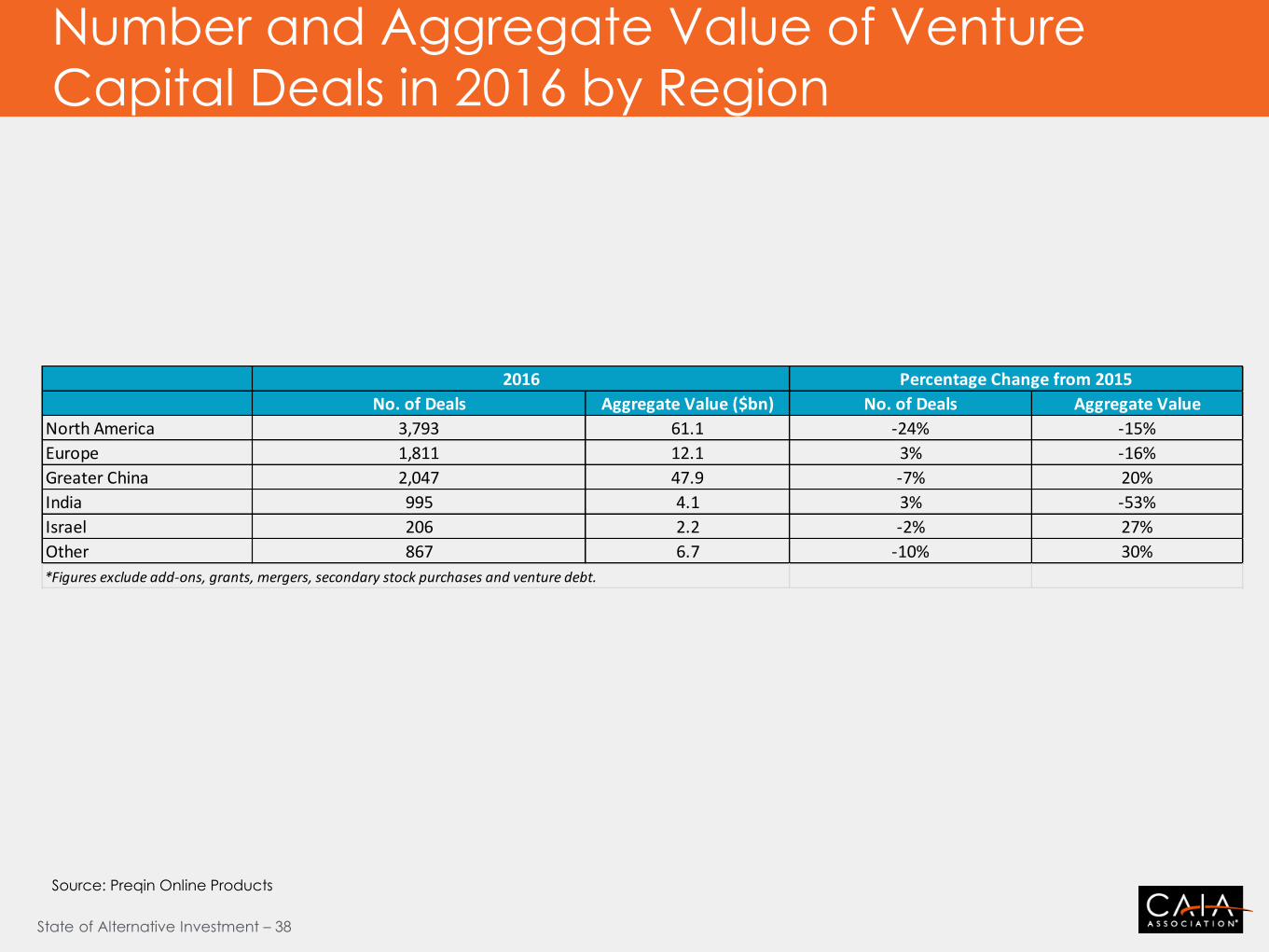

State of Alternative Investment – 38

Number and Aggregate Value of Venture

Capital Deals in 2016 by Region

No. of Deals Aggregate Value ($bn) No. of Deals Aggregate Value

North America 3,793 61.1 -24% -15%

Europe 1,811 12.1 3% -16%

Greater China 2,047 47.9 -7% 20%

India 995 4.1 3% -53%

Israel 206 2.2 -2% 27%

Other 867 6.7 -10% 30%

*Figures exclude add-ons, grants, mergers, secondary stock purchases and venture debt.

2016 Percentage Change from 2015

Source: Preqin Online Products

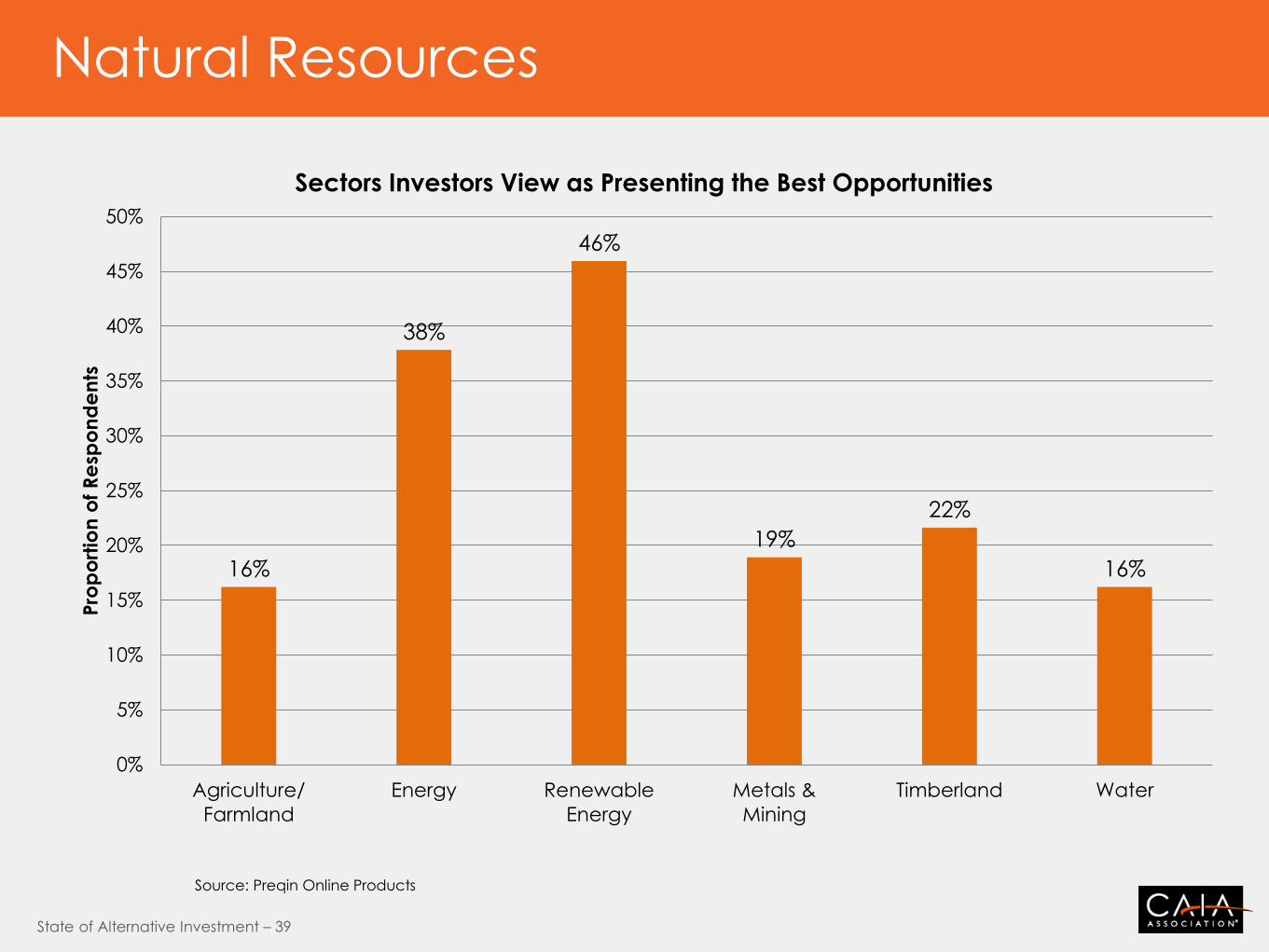

State of Alternative Investment – 39

Natural Resources

16%

38%

46%

19%

22%

16%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

Agriculture/

Farmland

Energy Renewable

Energy

Metals &

Mining

Timberland Water

Pro

po

rtio

n o

f R

esp

on

de

nts

Sectors Investors View as Presenting the Best Opportunities

Source: Preqin Online Products

State of Alternative Investment – 40

Natural Resources

5%

14%

16%

21%

23%

30%

37%

77%

5%

9%

23%

32%

16%

36%

30%

77%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

Brexit Vote

Stock Market Volatility

Currency Market Volatility

Low Interest Rates

Central Bank Intervention

Geopolitical Landscape

Slowdown in China's Economy

Commodity Price Volatility

Proportion of Respondents

Investor Views on the Macroeconomic Factors that Had the Biggest Impact on Their Natural Resources Portfolios in 2016 vs. Predictions for 2017

2016 2017

Source: Preqin Online Products

State of Alternative Investment – 41

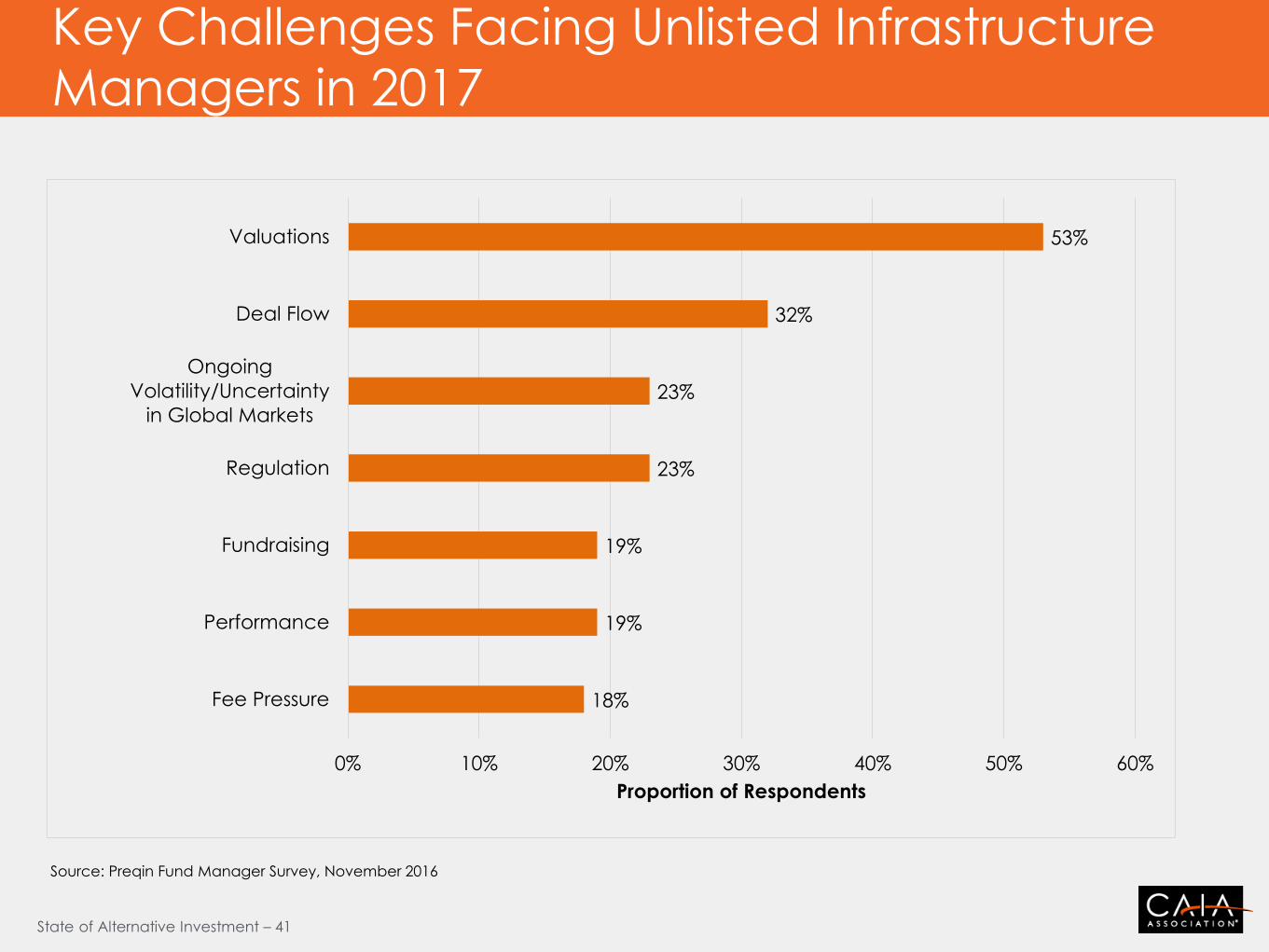

Key Challenges Facing Unlisted Infrastructure

Managers in 2017

18%

19%

19%

23%

23%

32%

53%

0% 10% 20% 30% 40% 50% 60%

Fee Pressure

Performance

Fundraising

Regulation

Ongoing

Volatility/Uncertainty

in Global Markets

Deal Flow

Valuations

Proportion of Respondents

Source: Preqin Fund Manager Survey, November 2016

State of Alternative Investment – 42

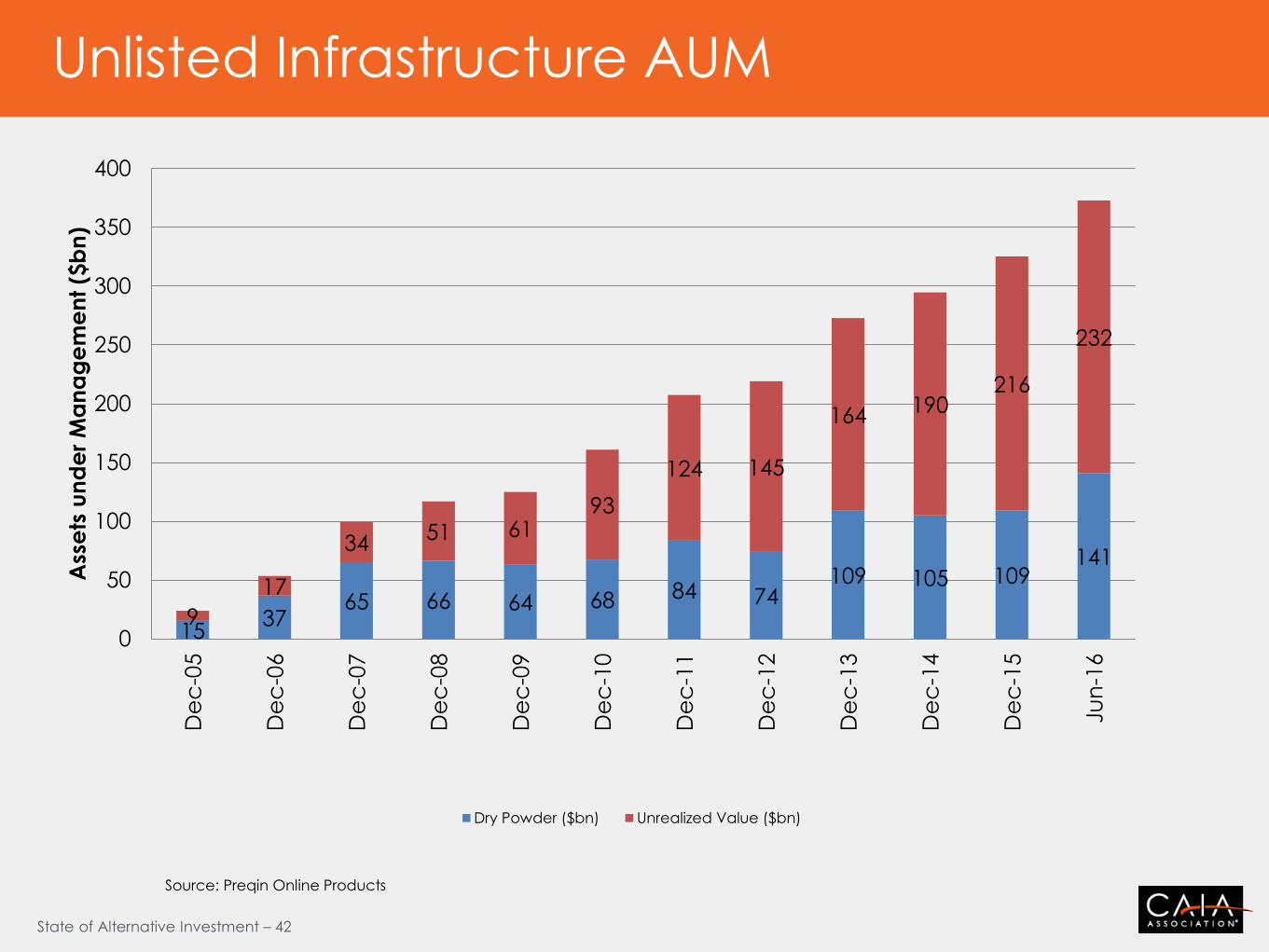

Unlisted Infrastructure AUM

15 37

65 66 64 68 84 74 109 105 109

141

9

17

34 51 61

93

124 145

164 190 216

232

0

50

100

150

200

250

300

350

400D

ec

-05

De

c-0

6

De

c-0

7

De

c-0

8

De

c-0

9

De

c-1

0

De

c-1

1

De

c-1

2

De

c-1

3

De

c-1

4

De

c-1

5

Ju

n-1

6

Ass

ets

un

de

r M

an

ag

em

en

t ($

bn

)

Dry Powder ($bn) Unrealized Value ($bn)

Source: Preqin Online Products

State of Alternative Investment – 43

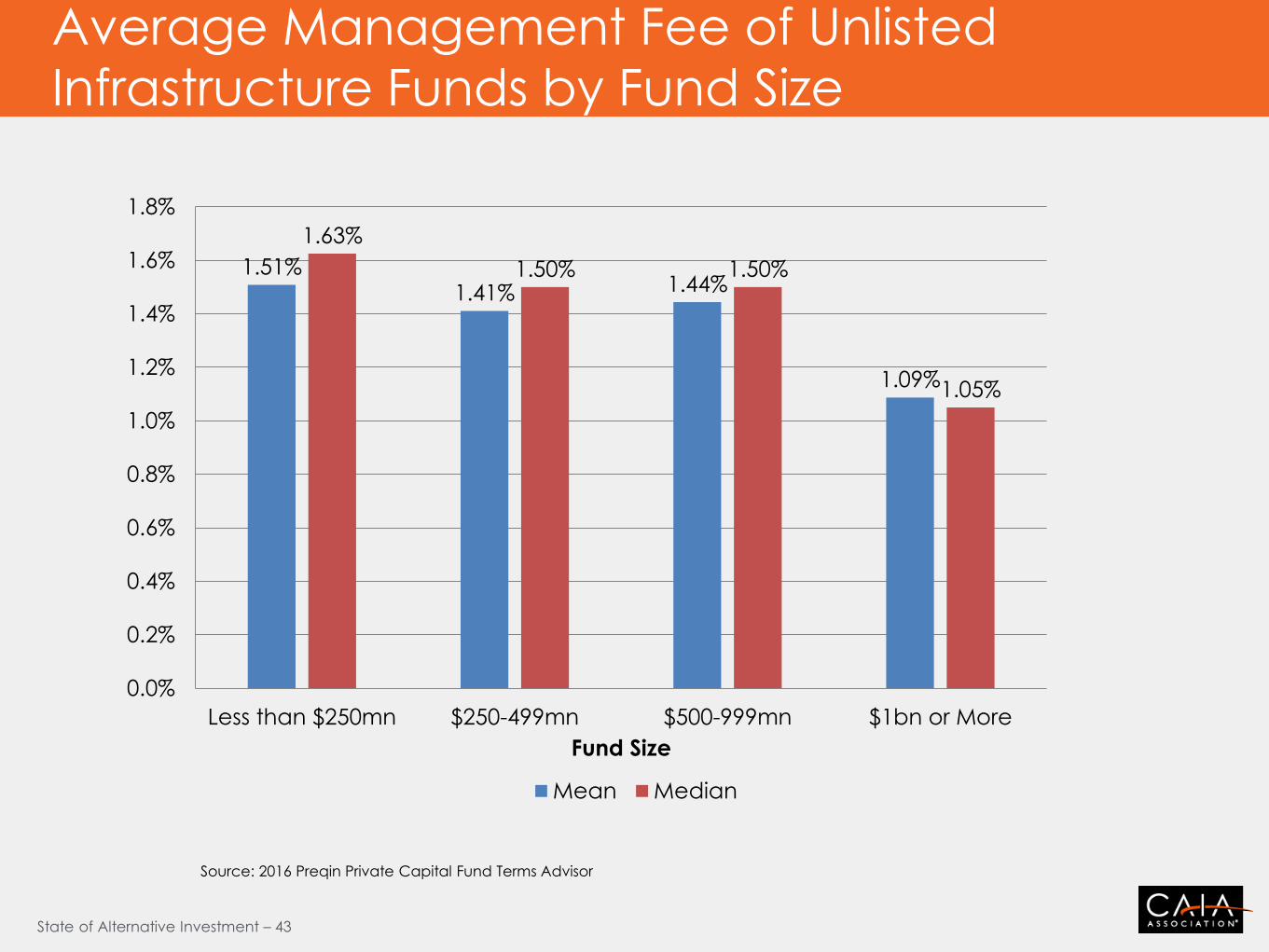

Average Management Fee of Unlisted

Infrastructure Funds by Fund Size

1.51% 1.41% 1.44%

1.09%

1.63%

1.50% 1.50%

1.05%

0.0%

0.2%

0.4%

0.6%

0.8%

1.0%

1.2%

1.4%

1.6%

1.8%

Less than $250mn $250-499mn $500-999mn $1bn or More

Fund Size

Mean Median

Source: 2016 Preqin Private Capital Fund Terms Advisor

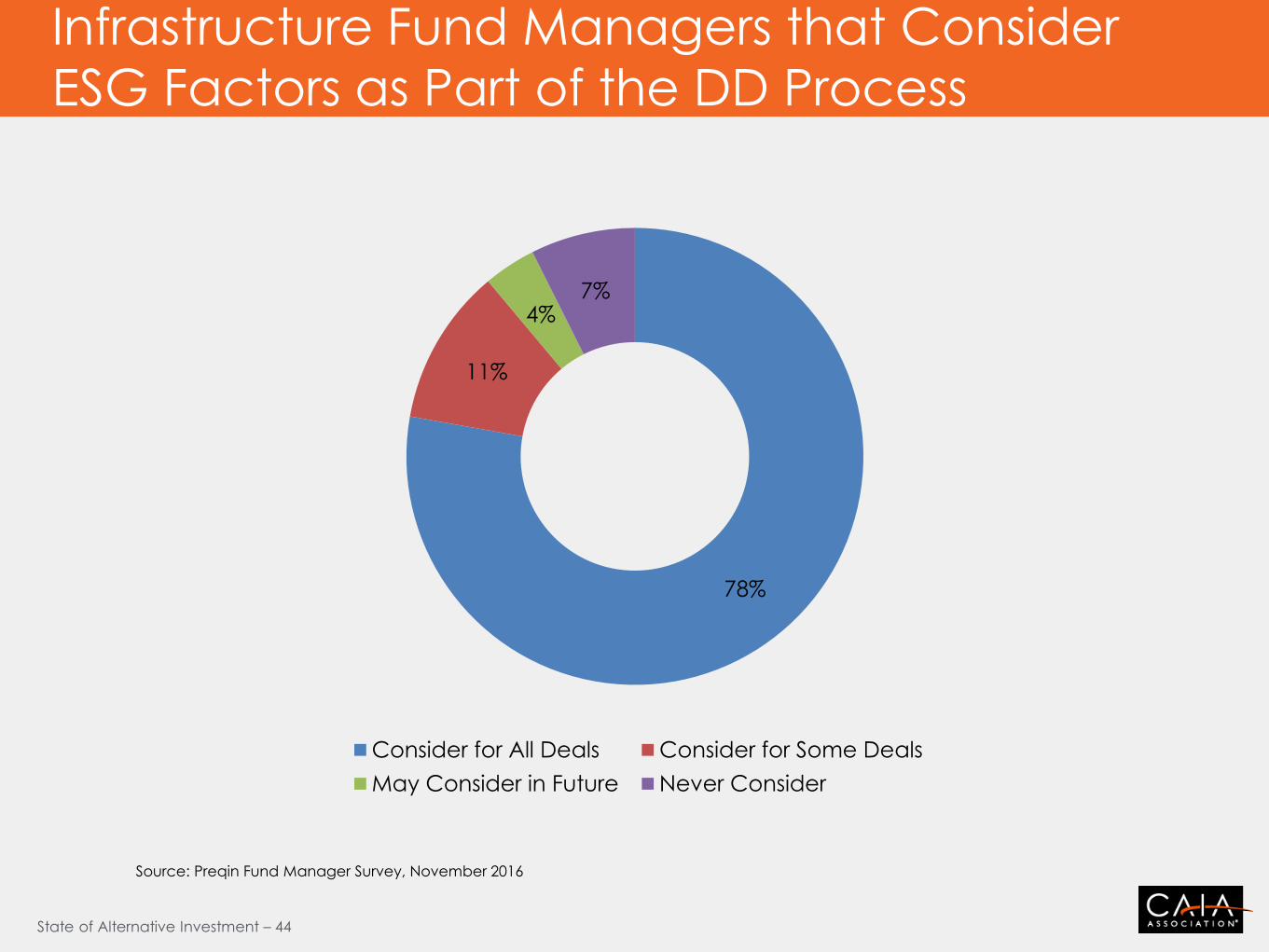

State of Alternative Investment – 44

Infrastructure Fund Managers that Consider

ESG Factors as Part of the DD Process

78%

11%

4% 7%

Consider for All Deals Consider for Some Deals

May Consider in Future Never Consider

Source: Preqin Fund Manager Survey, November 2016

State of Alternative Investment – 45

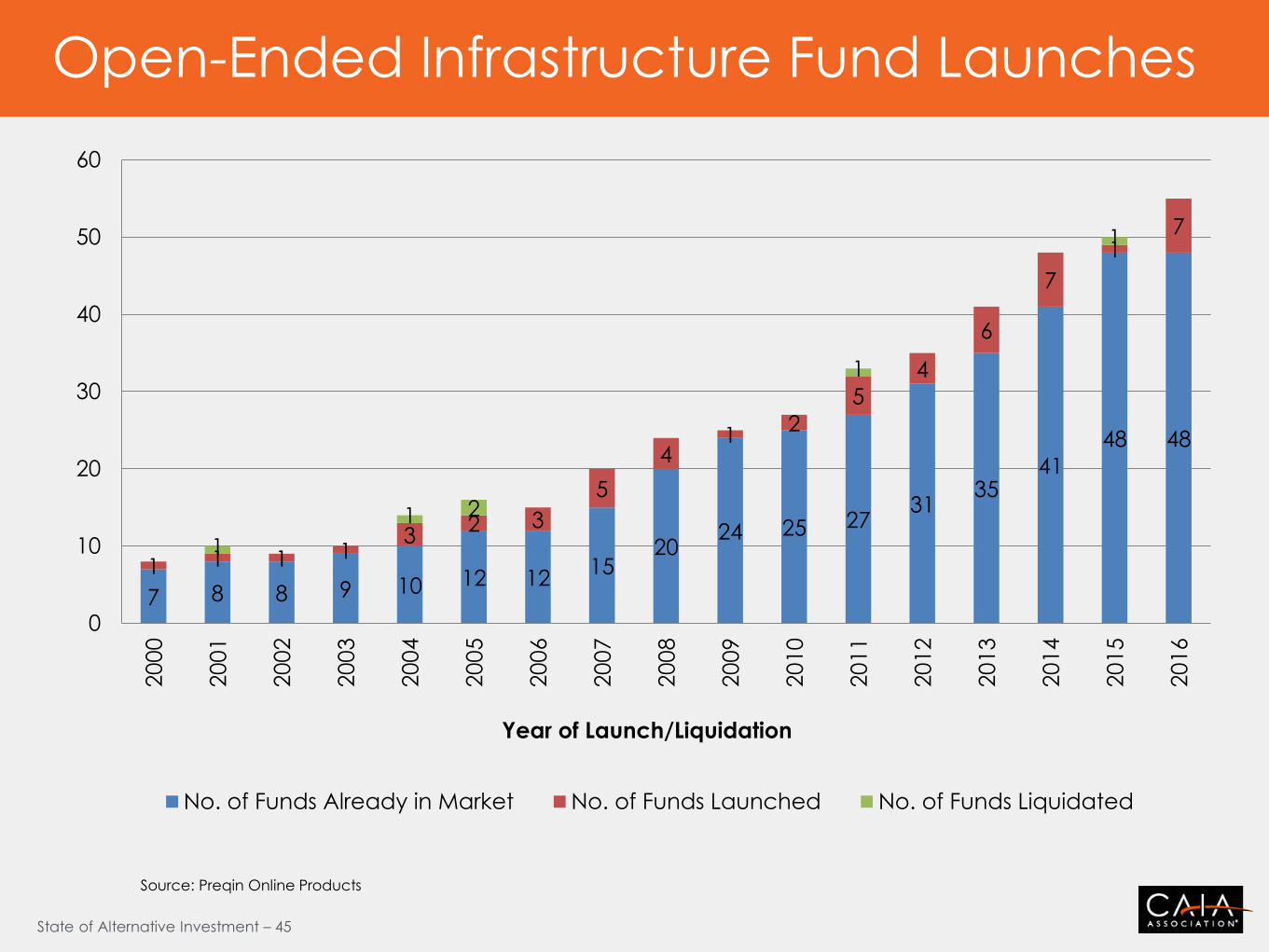

Open-Ended Infrastructure Fund Launches

7 8 8 9 10 12 12 15

20 24 25 27

31 35

41

48 48

1 1 1 1 3

2 3

5

4 1

2

5

4

6

7

1 7

1

1 2

1

1

0

10

20

30

40

50

602000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

Year of Launch/Liquidation

No. of Funds Already in Market No. of Funds Launched No. of Funds Liquidated

Source: Preqin Online Products

State of Alternative Investment – 46

Key Challenges Facing Private Real Estate

Managers in 2017

Source: Preqin Fund Manager Survey, November 2016

18%

7%

11%

14%

14%

22%

23%

26%

29%

37%

52%

0% 10% 20% 30% 40% 50% 60%

Other

Fee Pressure

Fulfilling Investor Demands

Regulation

Performance

Exit Environment

Availability/Pricing of Debt Financing

Deal Flow

Fundraising

Volatility/Uncertainty in Global Markets

Valuations

Proportion of Respondents

State of Alternative Investment – 47

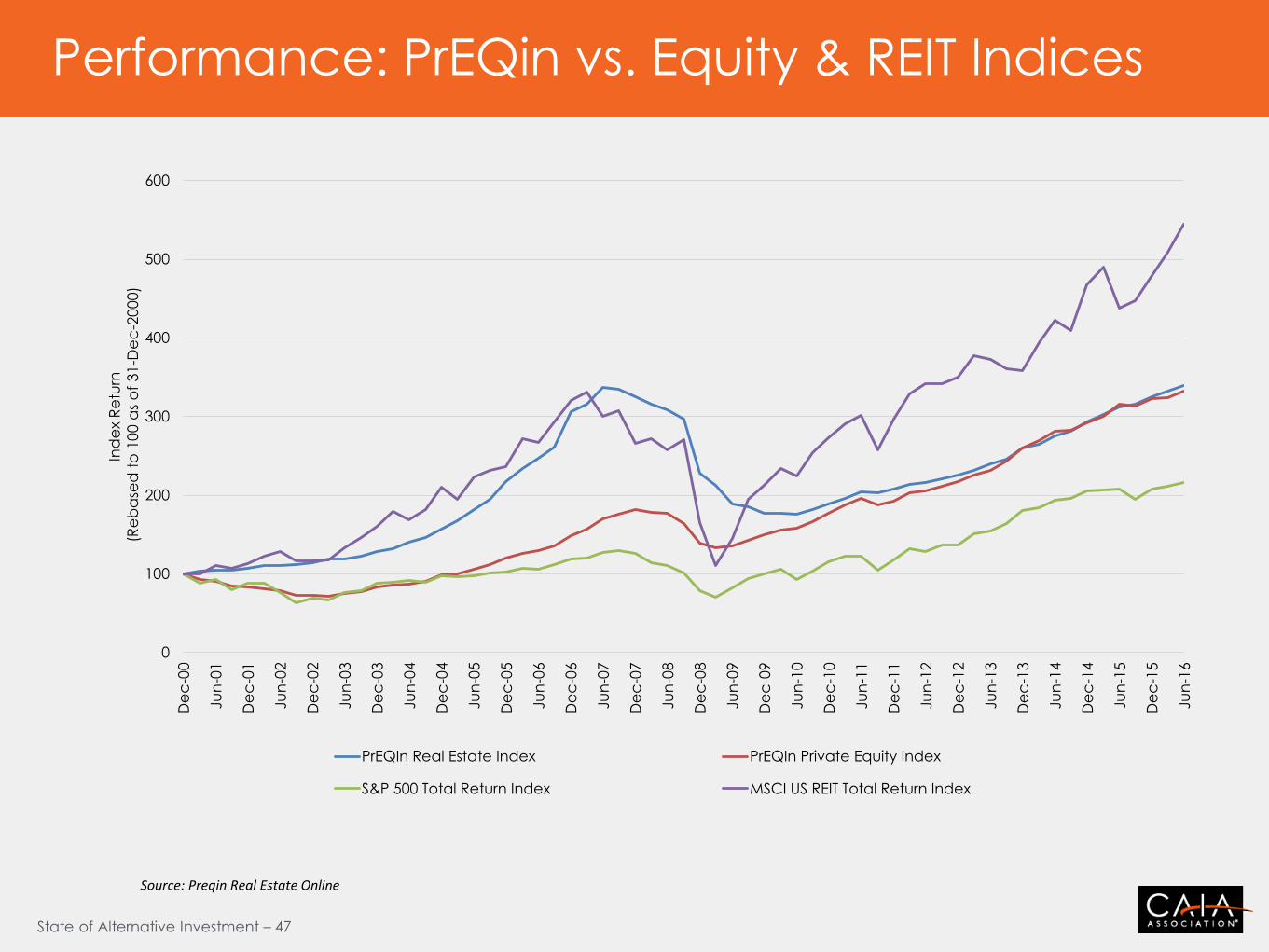

Performance: PrEQin vs. Equity & REIT Indices

Source: Preqin Real Estate Online

0

100

200

300

400

500

600D

ec

-00

Ju

n-0

1

De

c-0

1

Ju

n-0

2

De

c-0

2

Ju

n-0

3

De

c-0

3

Ju

n-0

4

De

c-0

4

Ju

n-0

5

De

c-0

5

Ju

n-0

6

De

c-0

6

Ju

n-0

7

De

c-0

7

Ju

n-0

8

De

c-0

8

Ju

n-0

9

De

c-0

9

Ju

n-1

0

De

c-1

0

Ju

n-1

1

De

c-1

1

Ju

n-1

2

De

c-1

2

Ju

n-1

3

De

c-1

3

Ju

n-1

4

De

c-1

4

Ju

n-1

5

De

c-1

5

Ju

n-1

6

Ind

ex R

etu

rn

(R

eb

ase

d t

o 1

00 a

s o

f 31

-De

c-2

000)

PrEQIn Real Estate Index PrEQIn Private Equity Index

S&P 500 Total Return Index MSCI US REIT Total Return Index

State of Alternative Investment – 48

Real Estate: Public Market Equivalent (PME)

Source: Preqin Real Estate Online

0.5

0.6

0.7

0.8

0.9

1.0

1.1

1.2

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

PM

E V

alu

e (

X)

Vintage Year

KS PME Using MSCI US REIT

KS PME Using S&P 500 TR

If PME value (X) is >1, private real

estate has outperformed the

public market

State of Alternative Investment – 49

US Average Cap Rate vs. US 10 Year Yield

Source: CAIA and Bloomberg

0

2

4

6

8

10

12

1/1

/20

01

5/1

/20

01

9/1

/20

01

1/1

/20

02

5/1

/20

02

9/1

/20

02

1/1

/20

03

5/1

/20

03

9/1

/20

03

1/1

/20

04

5/1

/20

04

9/1

/20

04

1/1

/20

05

5/1

/20

05

9/1

/20

05

1/1

/20

06

5/1

/20

06

9/1

/20

06

1/1

/20

07

5/1

/20

07

9/1

/20

07

1/1

/20

08

5/1

/20

08

9/1

/20

08

1/1

/20

09

5/1

/20

09

9/1

/20

09

1/1

/20

10

5/1

/20

10

9/1

/20

10

1/1

/20

11

5/1

/20

11

9/1

/20

11

1/1

/20

12

5/1

/20

12

9/1

/20

12

1/1

/20

13

5/1

/20

13

9/1

/20

13

1/1

/20

14

5/1

/20

14

9/1

/20

14

1/1

/20

15

5/1

/20

15

9/1

/20

15

1/1

/20

16

5/1

/20

16

9/1

/20

16

1/1

/20

17

Yie

ld

Spread US Avg. Cap Rate US 10 Year Yield

State of Alternative Investment – 50

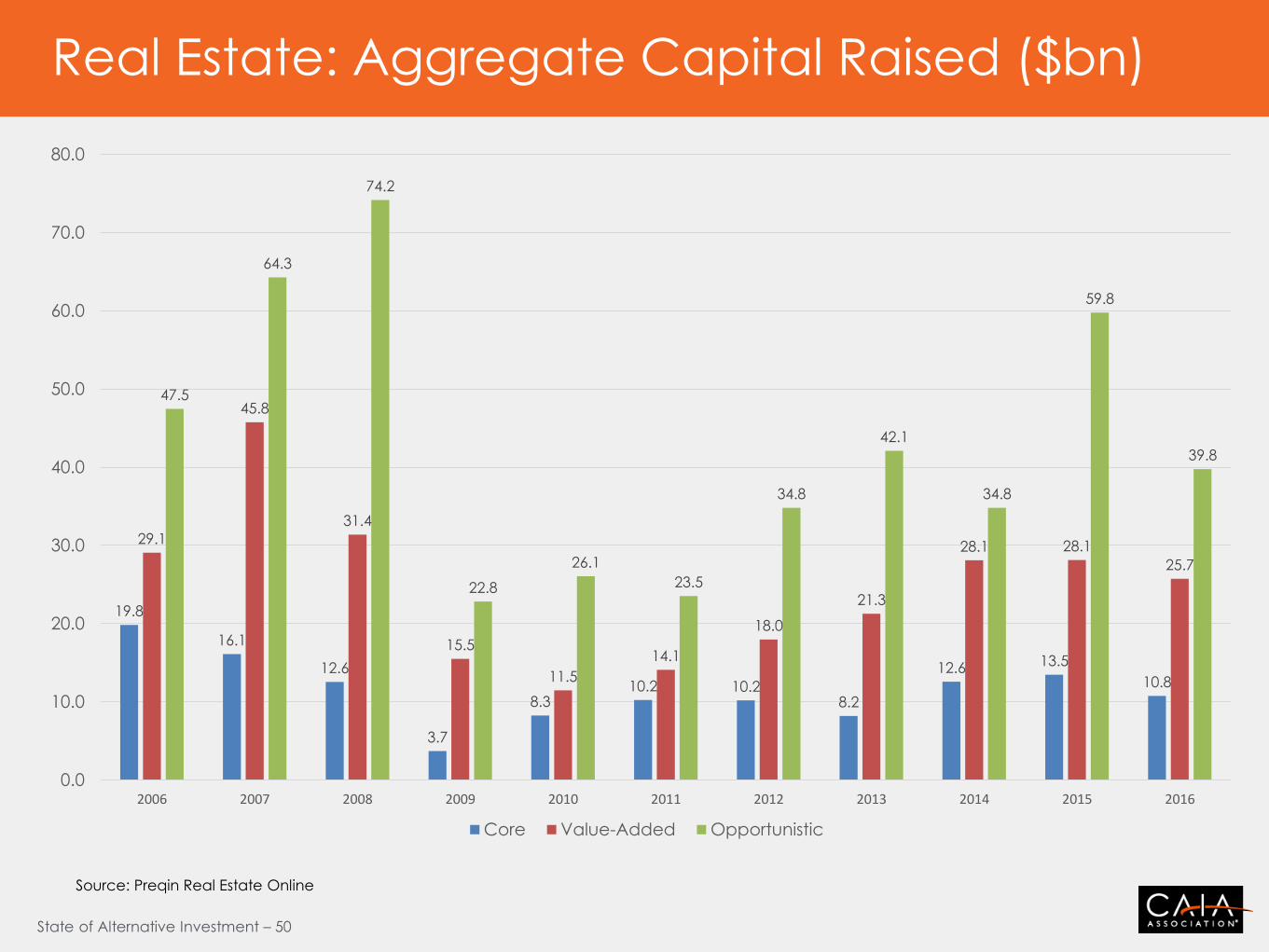

Real Estate: Aggregate Capital Raised ($bn)

19.8

16.1

12.6

3.7

8.3 10.2 10.2

8.2

12.6 13.5

10.8

29.1

45.8

31.4

15.5

11.5

14.1

18.0

21.3

28.1 28.1

25.7

47.5

64.3

74.2

22.8

26.1

23.5

34.8

42.1

34.8

59.8

39.8

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Core Value-Added Opportunistic

Source: Preqin Real Estate Online

State of Alternative Investment – 51

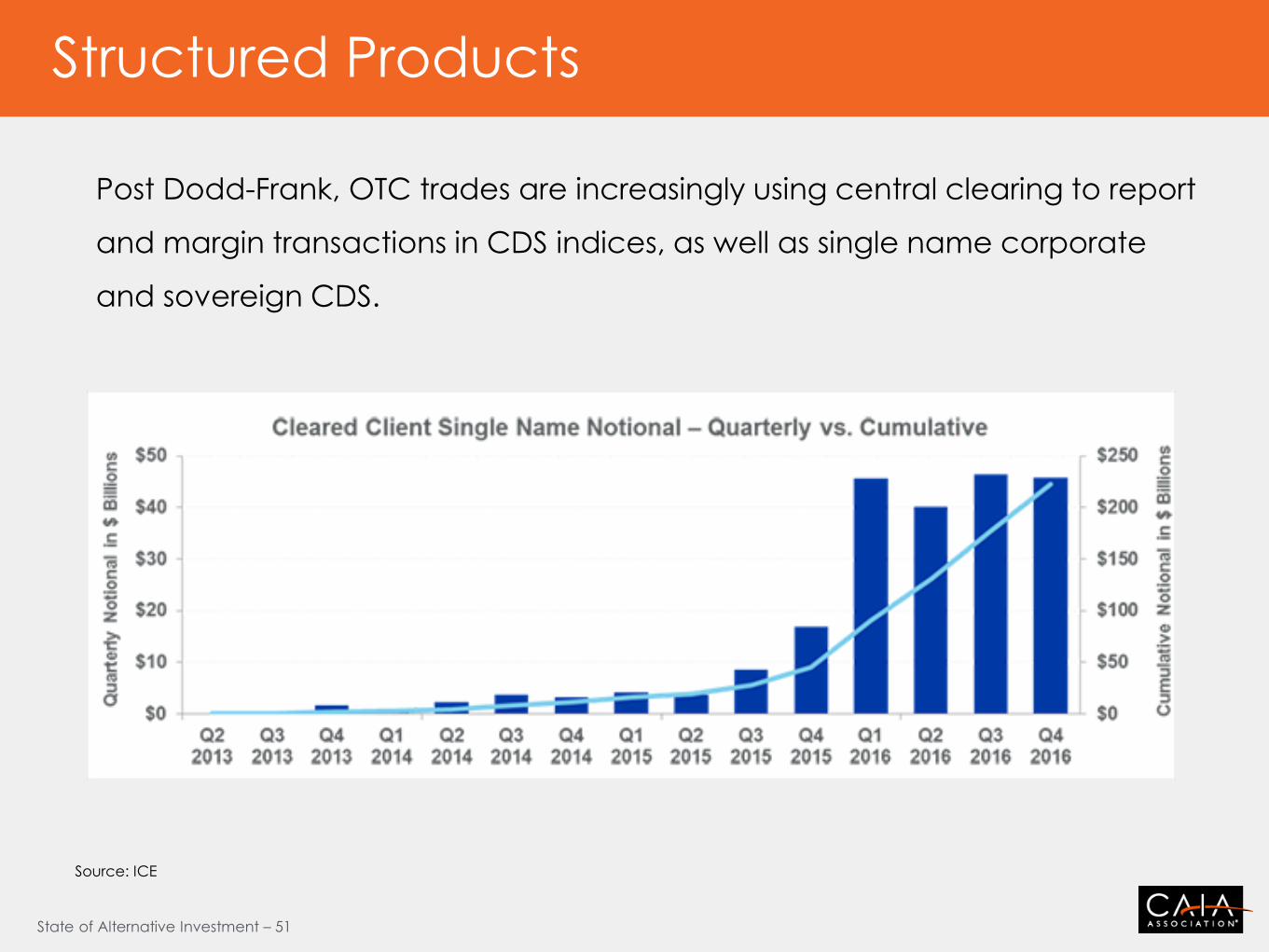

Structured Products

Post Dodd-Frank, OTC trades are increasingly using central clearing to report

and margin transactions in CDS indices, as well as single name corporate

and sovereign CDS.

Source: ICE

State of Alternative Investment – 52

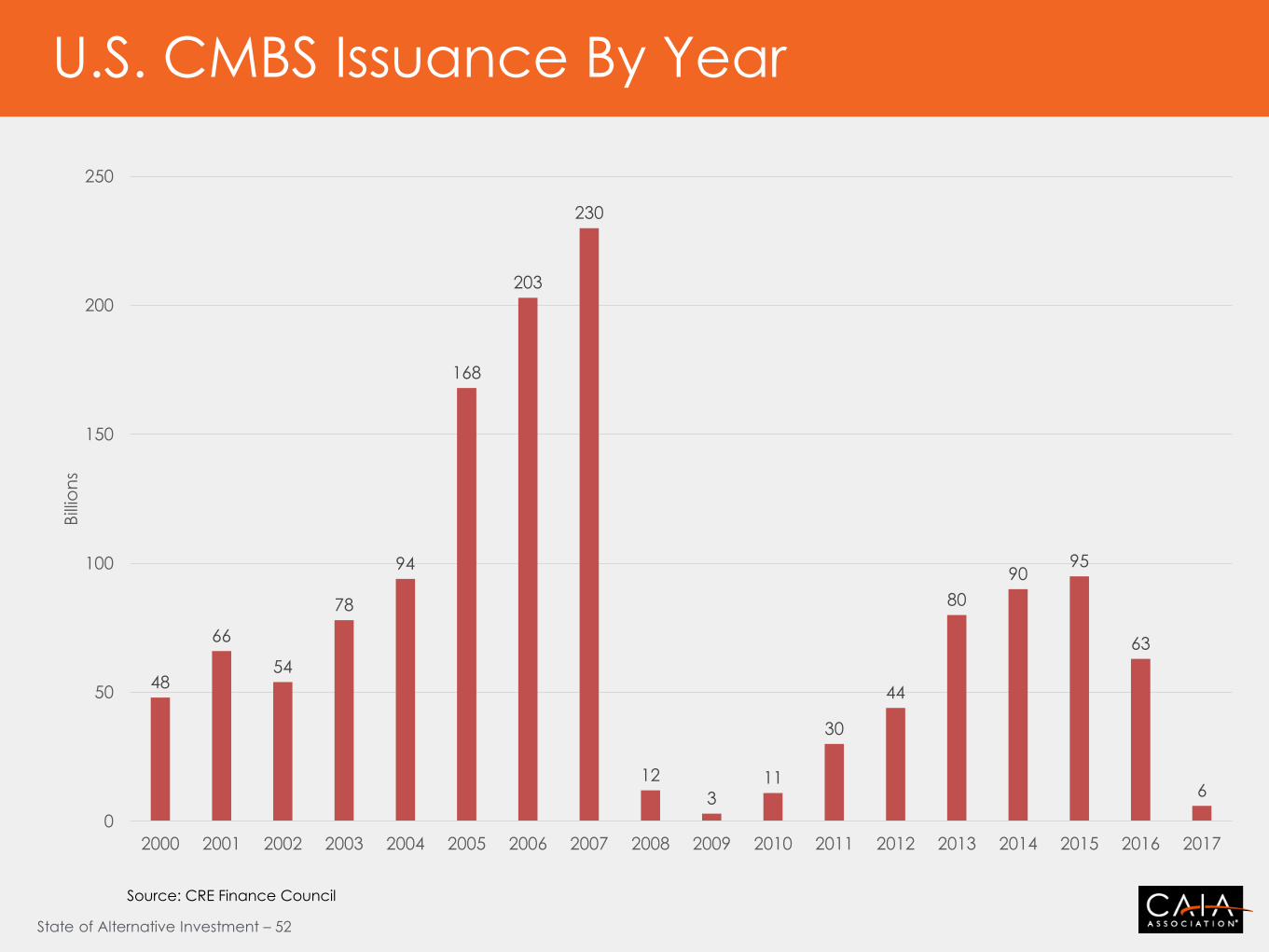

U.S. CMBS Issuance By Year

Source: CRE Finance Council

48

66

54

78

94

168

203

230

12

3 11

30

44

80

90 95

63

6

0

50

100

150

200

250

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Bill

ion

s

State of Alternative Investment – 53

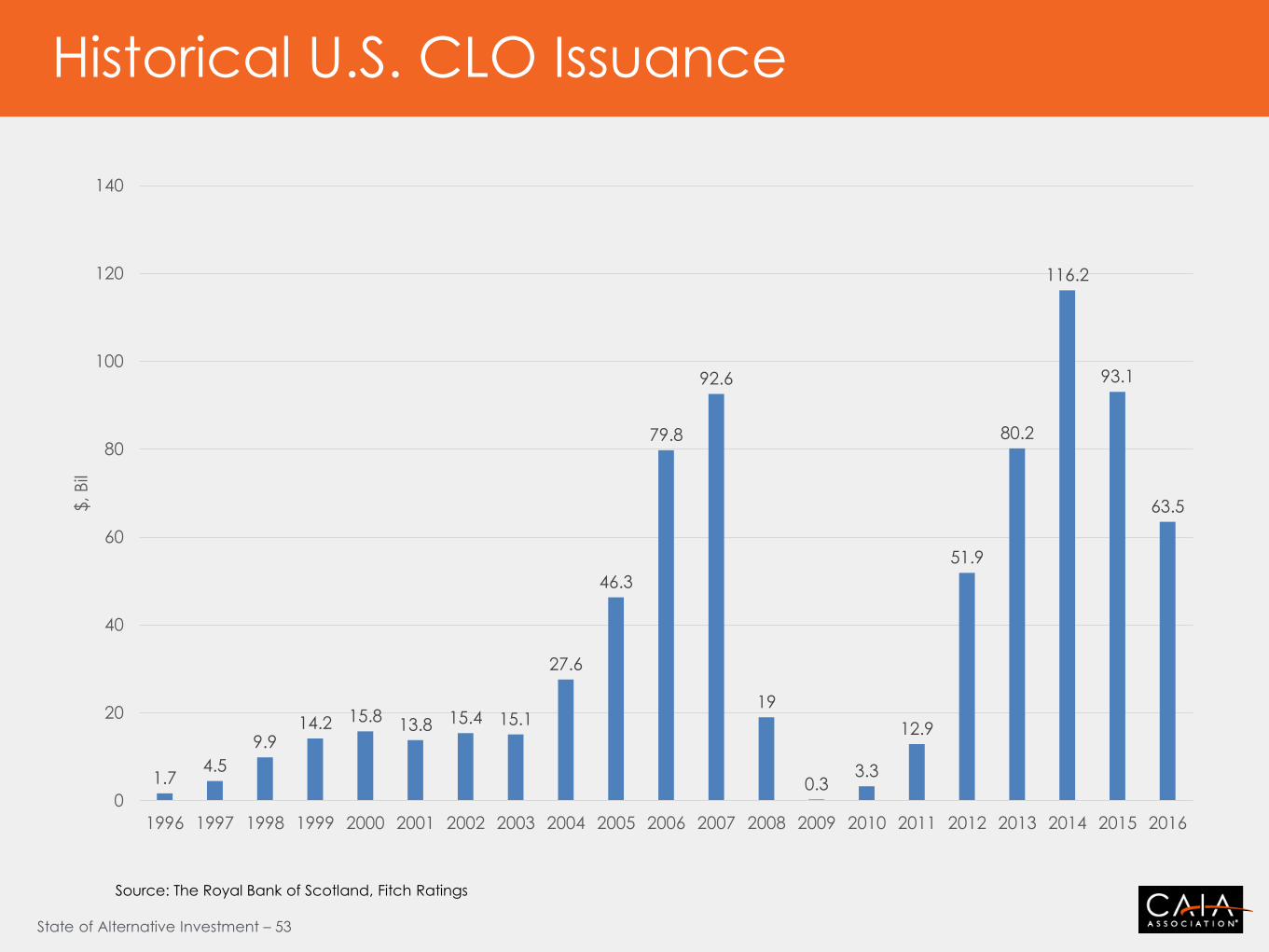

Historical U.S. CLO Issuance

Source: The Royal Bank of Scotland, Fitch Ratings

1.7 4.5

9.9 14.2 15.8

13.8 15.4 15.1

27.6

46.3

79.8

92.6

19

0.3 3.3

12.9

51.9

80.2

116.2

93.1

63.5

0

20

40

60

80

100

120

140

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

$, B

il

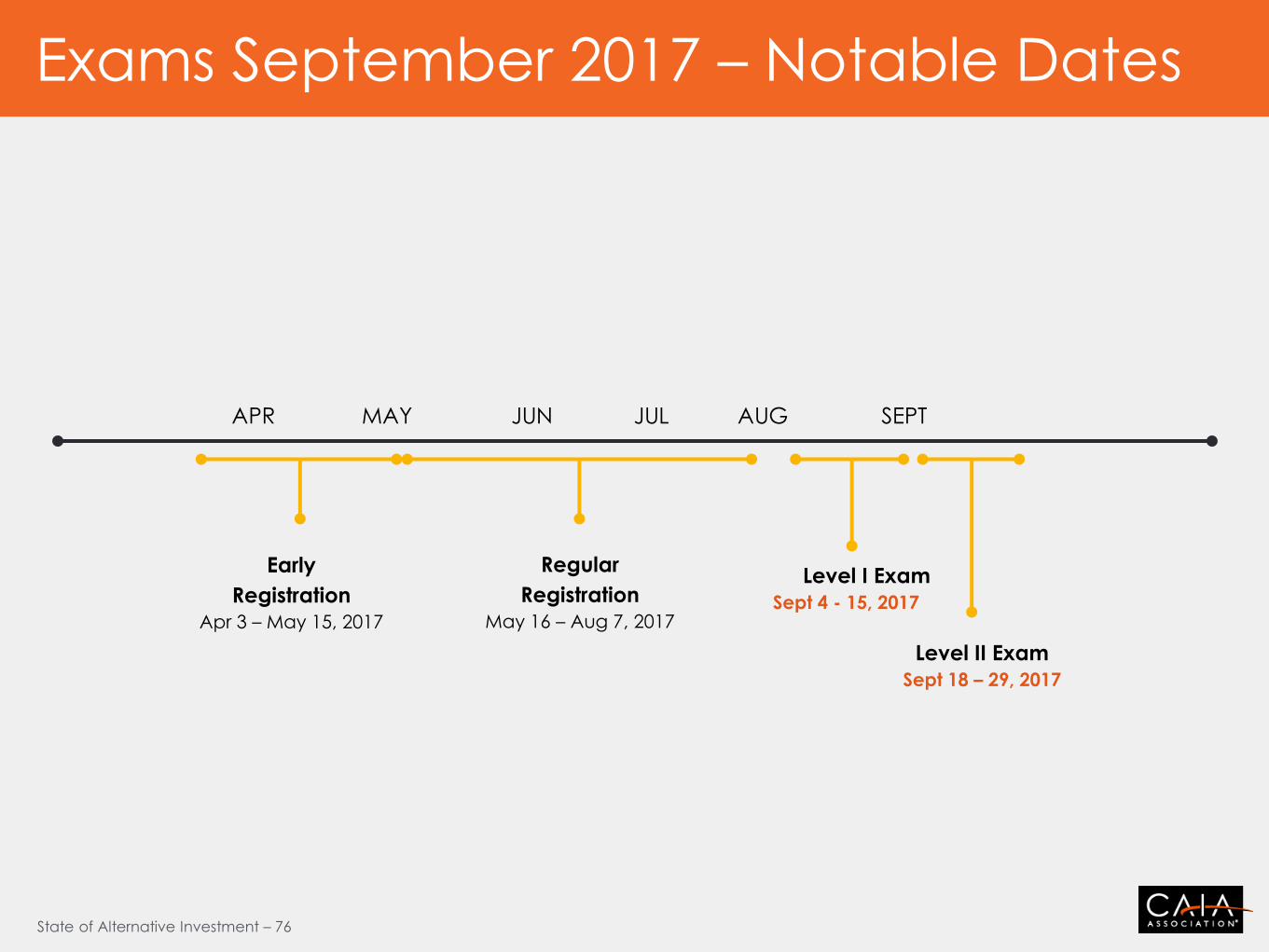

September 2017 Exam

The Global Benchmark In Alternative

Investment Education

The CAIA Charter

State of Alternative Investment – 55

Global Presence

State of Alternative Investment – 56

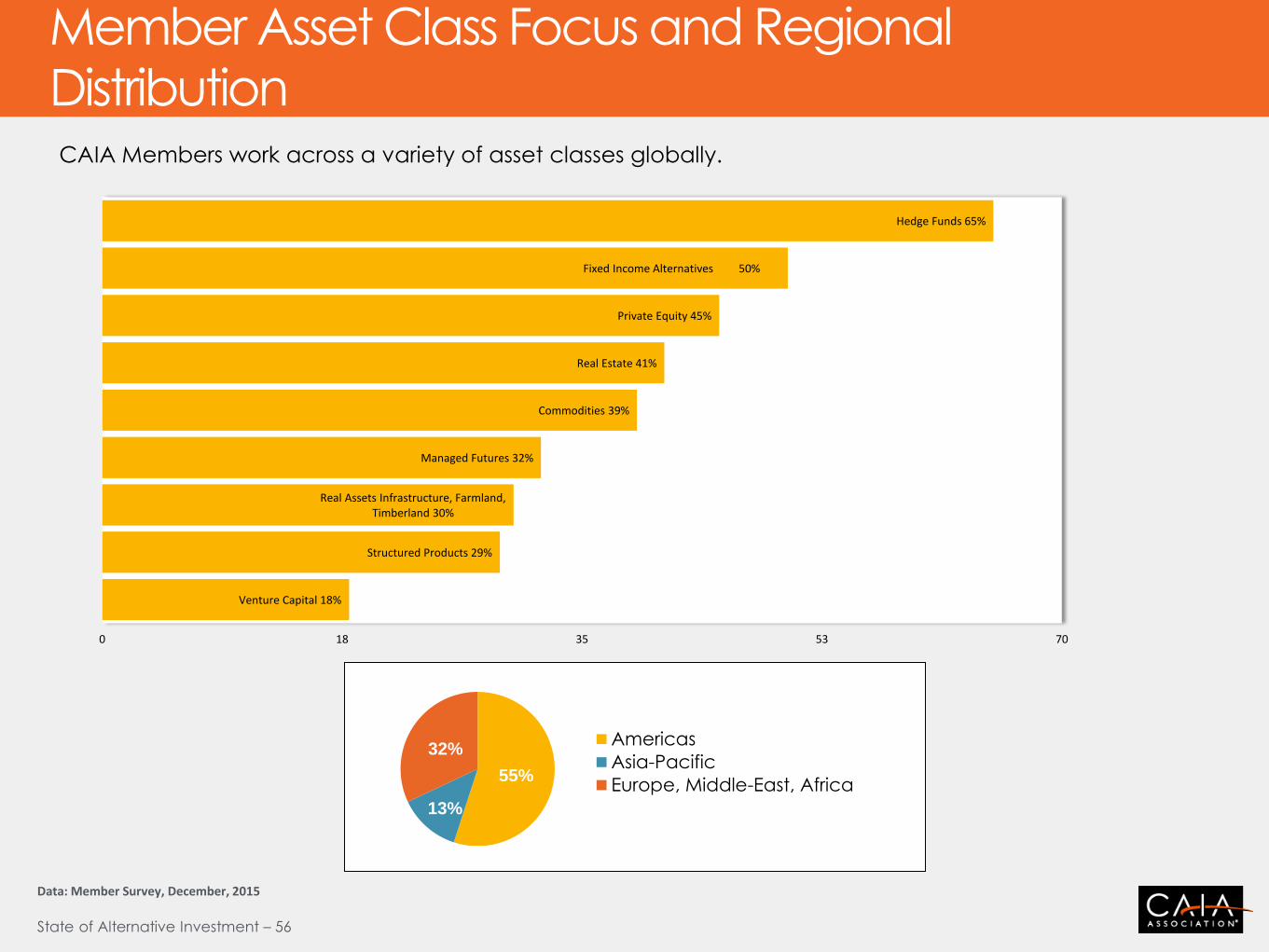

Member Asset Class Focus and Regional

Distribution

Data: Member Survey, December, 2015

Hedge Funds 65%

Fixed Income Alternatives 50%

Private Equity 45%

Real Estate 41%

Commodities 39%

Managed Futures 32%

Real Assets Infrastructure, Farmland, Timberland 30%

Structured Products 29%

Venture Capital 18%

0 18 35 53 70

55%

13%

32% Americas

Asia-Pacific

Europe, Middle-East, Africa

CAIA Members work across a variety of asset classes globally.

State of Alternative Investment – 57

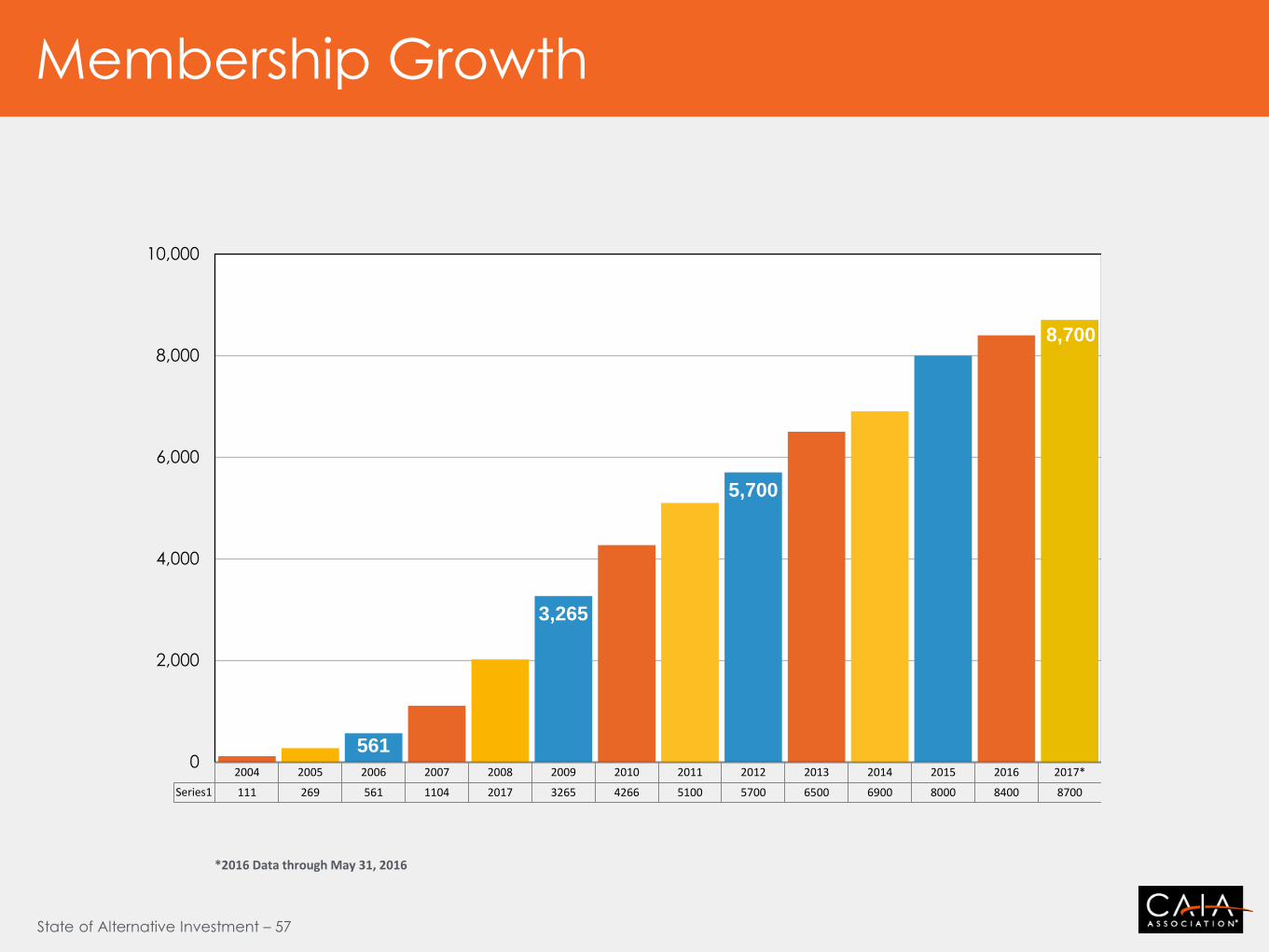

Membership Growth

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017*

Series1 111 269 561 1104 2017 3265 4266 5100 5700 6500 6900 8000 8400 8700

561

3,265

5,700

8,700

0

2,000

4,000

6,000

8,000

10,000

*2016 Data through May 31, 2016

State of Alternative Investment – 58

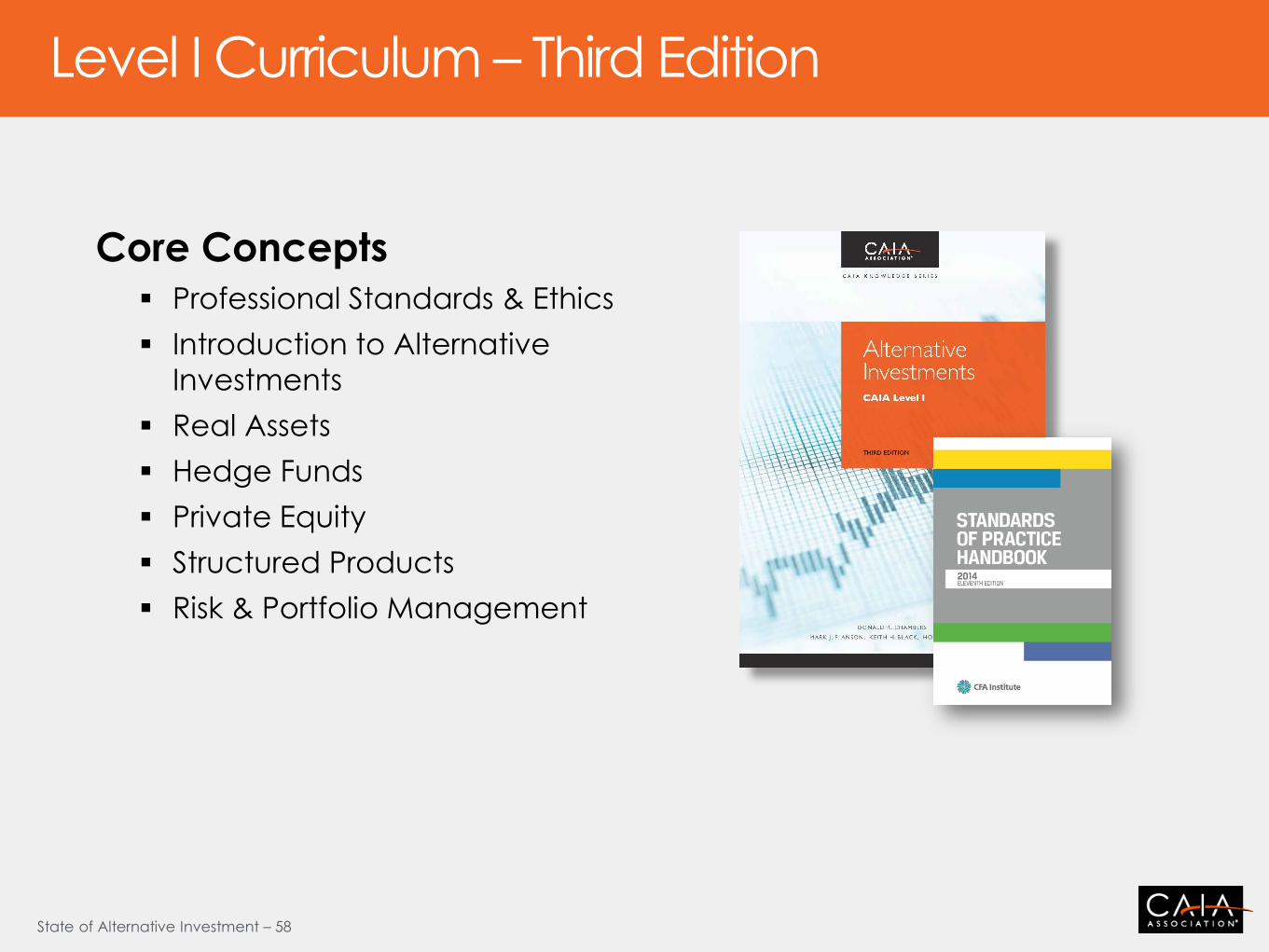

Level I Curriculum – Third Edition

Core Concepts

Professional Standards & Ethics

Introduction to Alternative

Investments

Real Assets

Hedge Funds

Private Equity

Structured Products

Risk & Portfolio Management

State of Alternative Investment – 59

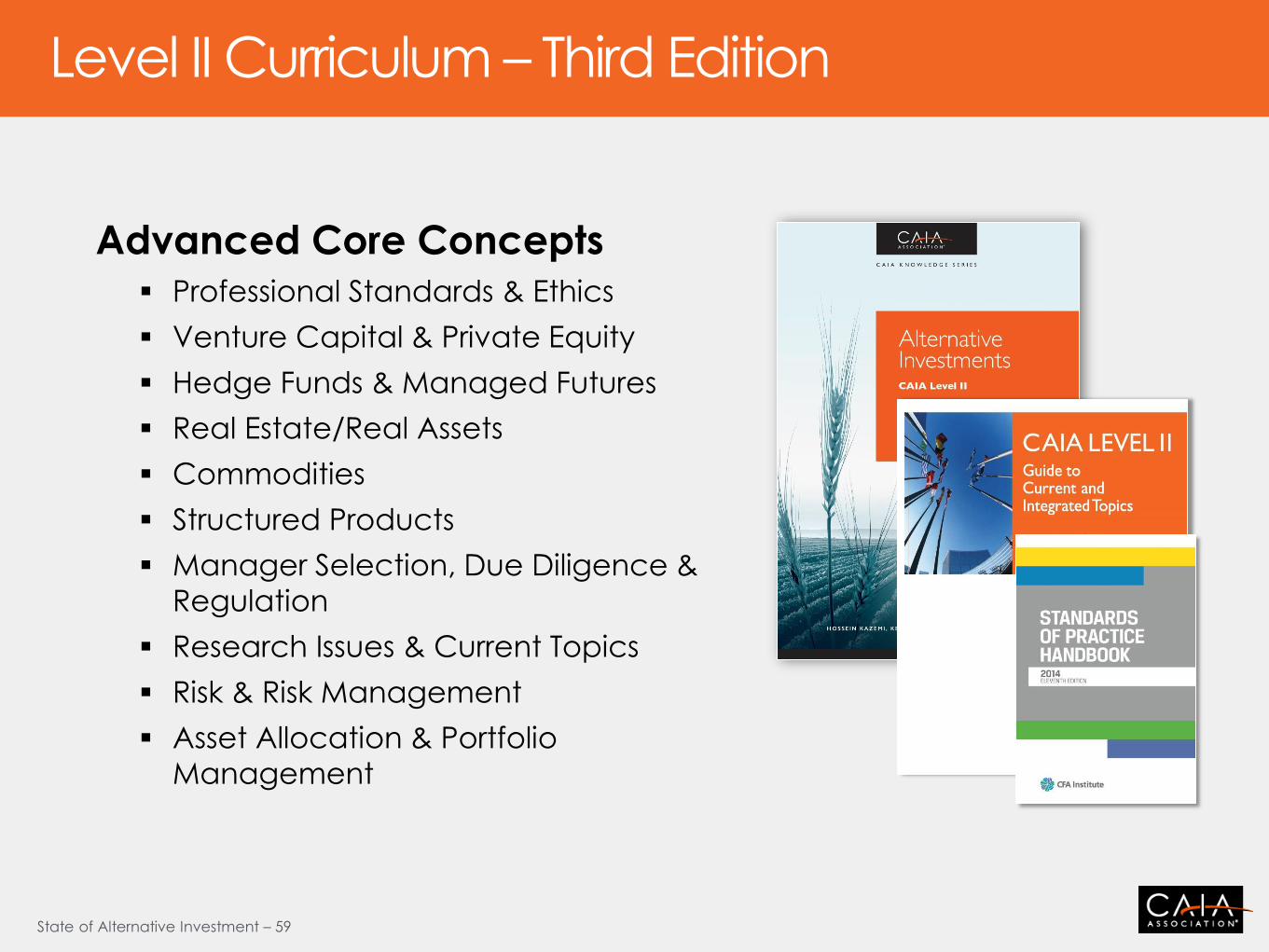

Level II Curriculum – Third Edition

Advanced Core Concepts

Professional Standards & Ethics

Venture Capital & Private Equity

Hedge Funds & Managed Futures

Real Estate/Real Assets

Commodities

Structured Products

Manager Selection, Due Diligence &

Regulation

Research Issues & Current Topics

Risk & Risk Management

Asset Allocation & Portfolio

Management

State of Alternative Investment – 60

Level II Curriculum Recent Changes

The 3rd Edition of the CAIA Level II textbook provides comprehensive data

models, due diligence processes, analysis, and strategies to keep you current

and relevant in the field of alternative investments.

New or Updated Topic Areas

Enhanced coverage of:

• Family offices and sovereign wealth funds.

• Alternative investment groups, such as structured products and

infrastructure

• Private equity

• Real assets

• Hedge funds including credit strategies and operational due diligence

• Structured products – featuring two sections focused on fixed-income

derivatives and asset-backed securities, and insurance-linked products

and hybrid securities

State of Alternative Investment – 61

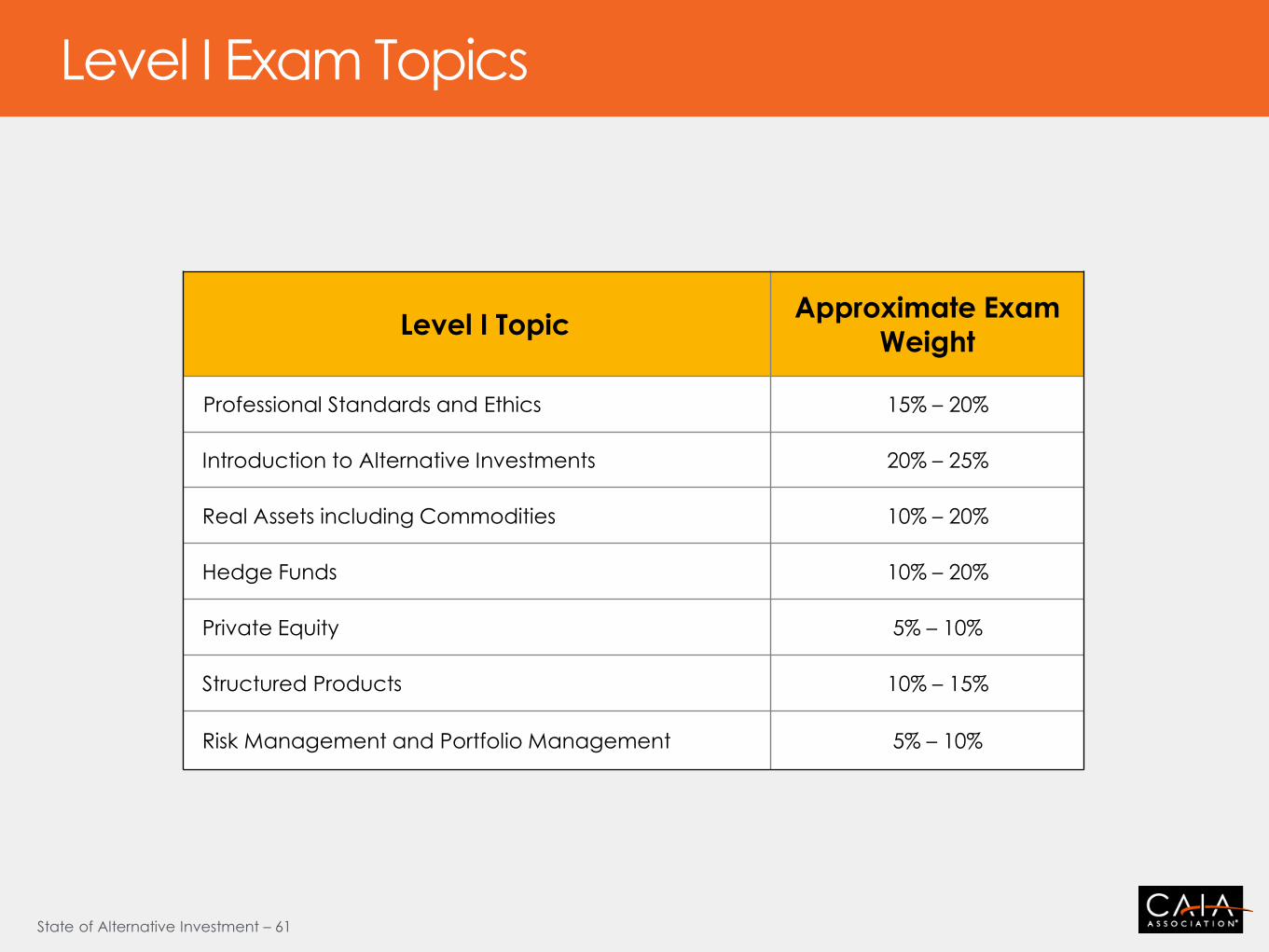

Level I Topic Approximate Exam

Weight

Professional Standards and Ethics 15% – 20%

Introduction to Alternative Investments 20% – 25%

Real Assets including Commodities 10% – 20%

Hedge Funds 10% – 20%

Private Equity 5% – 10%

Structured Products 10% – 15%

Risk Management and Portfolio Management 5% – 10%

Level I Exam Topics

State of Alternative Investment – 62

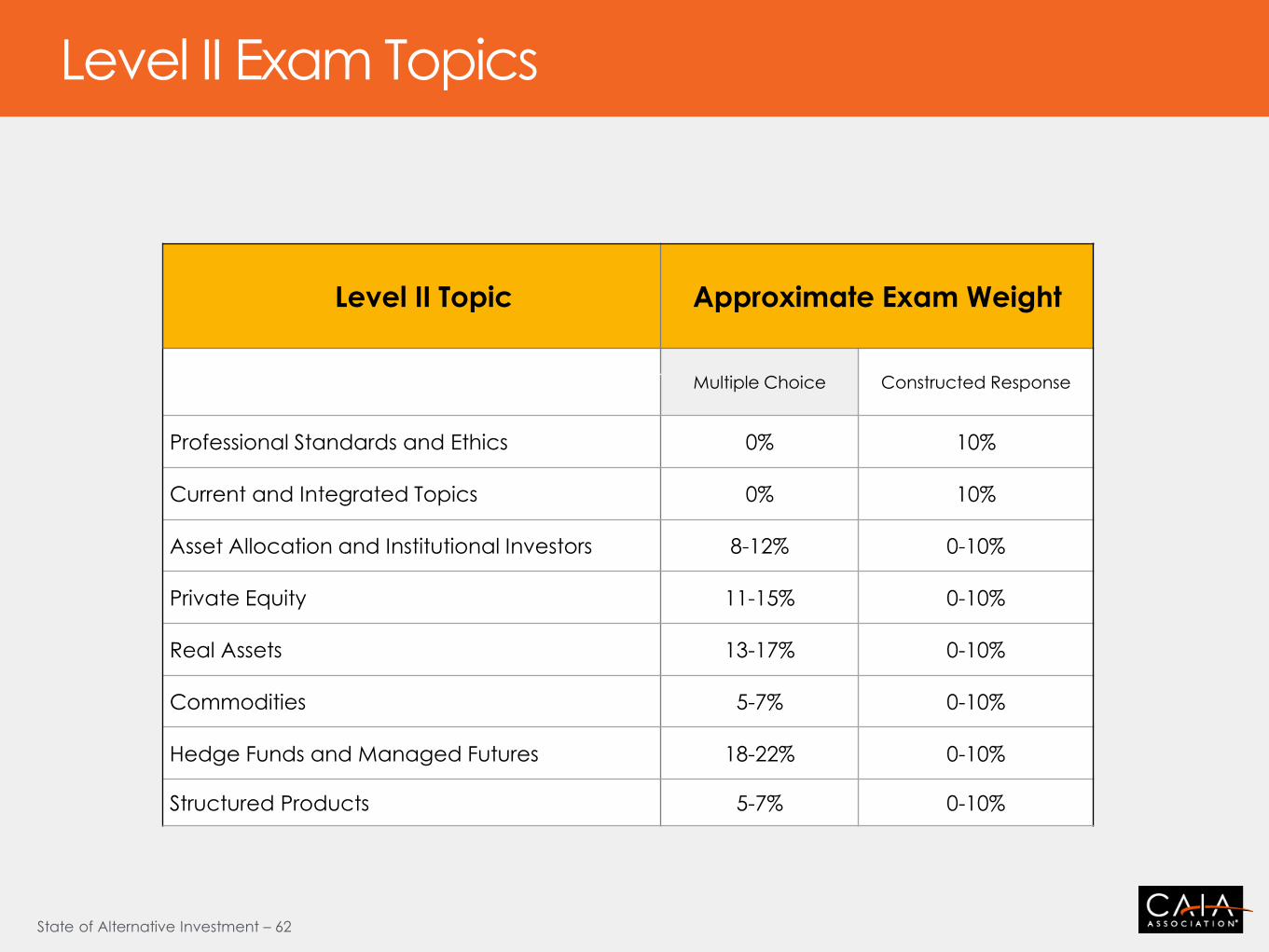

Level II Topic Approximate Exam Weight

Multiple Choice Constructed Response

Professional Standards and Ethics 0% 10%

Current and Integrated Topics 0% 10%

Asset Allocation and Institutional Investors 8-12% 0-10%

Private Equity 11-15% 0-10%

Real Assets 13-17% 0-10%

Commodities 5-7% 0-10%

Hedge Funds and Managed Futures 18-22% 0-10%

Structured Products 5-7% 0-10%

Level II Exam Topics

State of Alternative Investment – 63

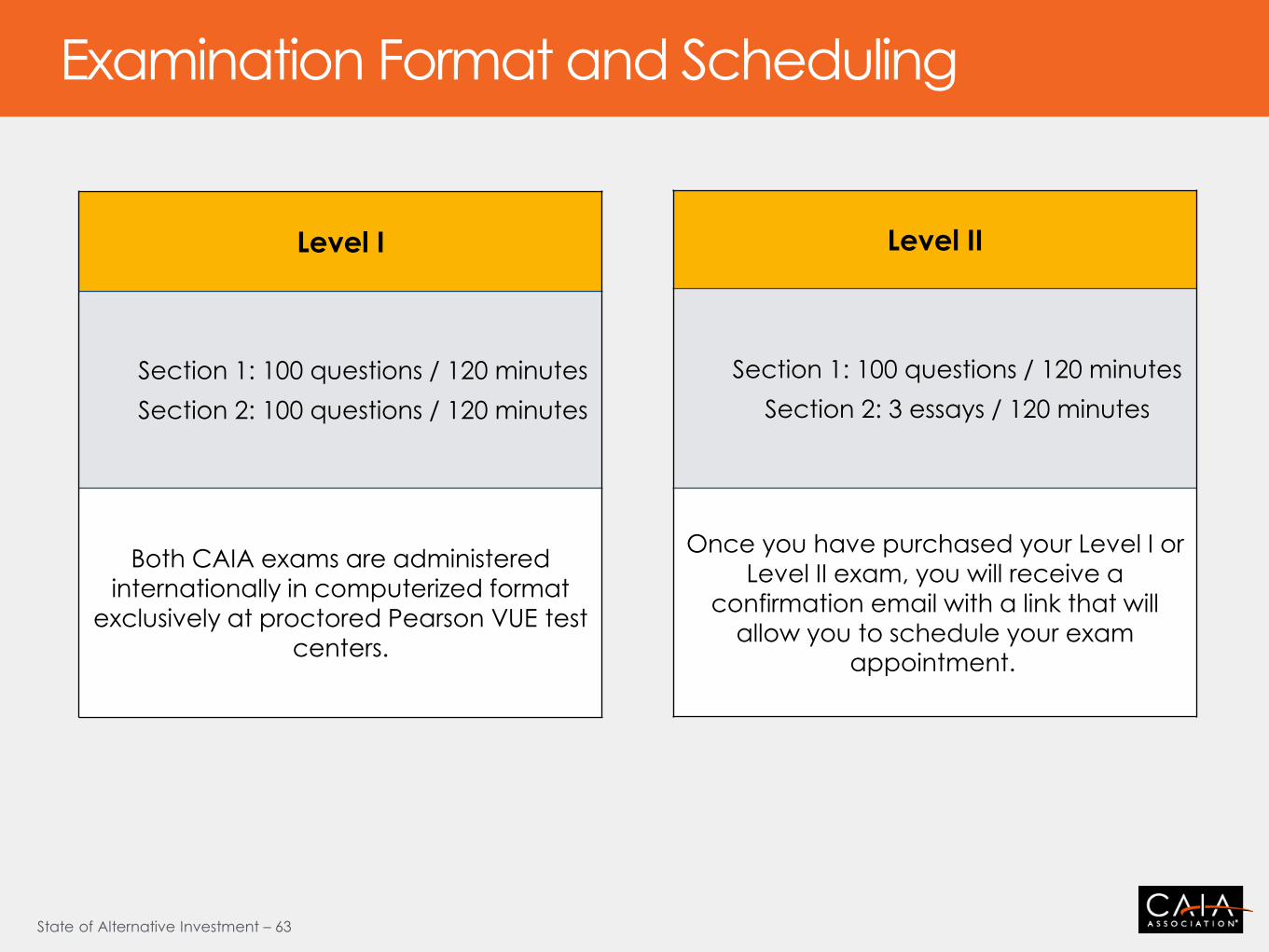

Examination Format and Scheduling

Level I

Section 1: 100 questions / 120 minutes

Section 2: 100 questions / 120 minutes

Both CAIA exams are administered

internationally in computerized format

exclusively at proctored Pearson VUE test centers.

Level II

Section 1: 100 questions / 120 minutes

Section 2: 3 essays / 120 minutes

Once you have purchased your Level I or

Level II exam, you will receive a

confirmation email with a link that will

allow you to schedule your exam appointment.

State of Alternative Investment – 64

Study guides outlining keywords and learning objectives

Workbooks with sample exercises

Candidate orientation sessions

Study calculator to plan your course of study

Third-party preparatory course and programs

Level I & Level II sample exams

Candidate Support/Tools

State of Alternative Investment – 65

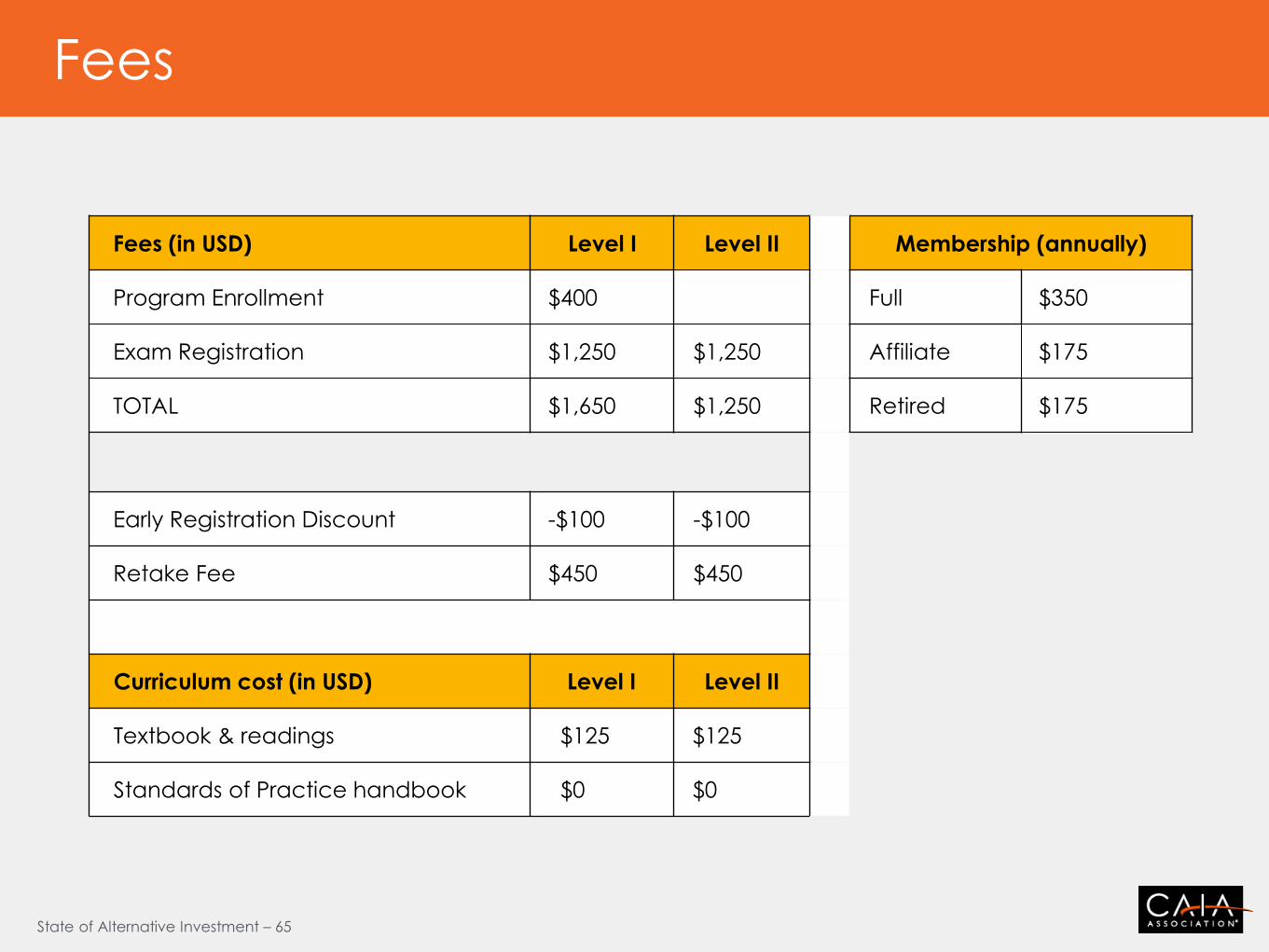

Fees (in USD) Level I Level II Membership (annually)

Program Enrollment $400 Full $350

Exam Registration $1,250 $1,250 Affiliate $175

TOTAL $1,650 $1,250 Retired $175

Early Registration Discount -$100 -$100

Retake Fee $450 $450

Curriculum cost (in USD) Level I Level II

Textbook & readings $125 $125

Standards of Practice handbook $0 $0

Fees

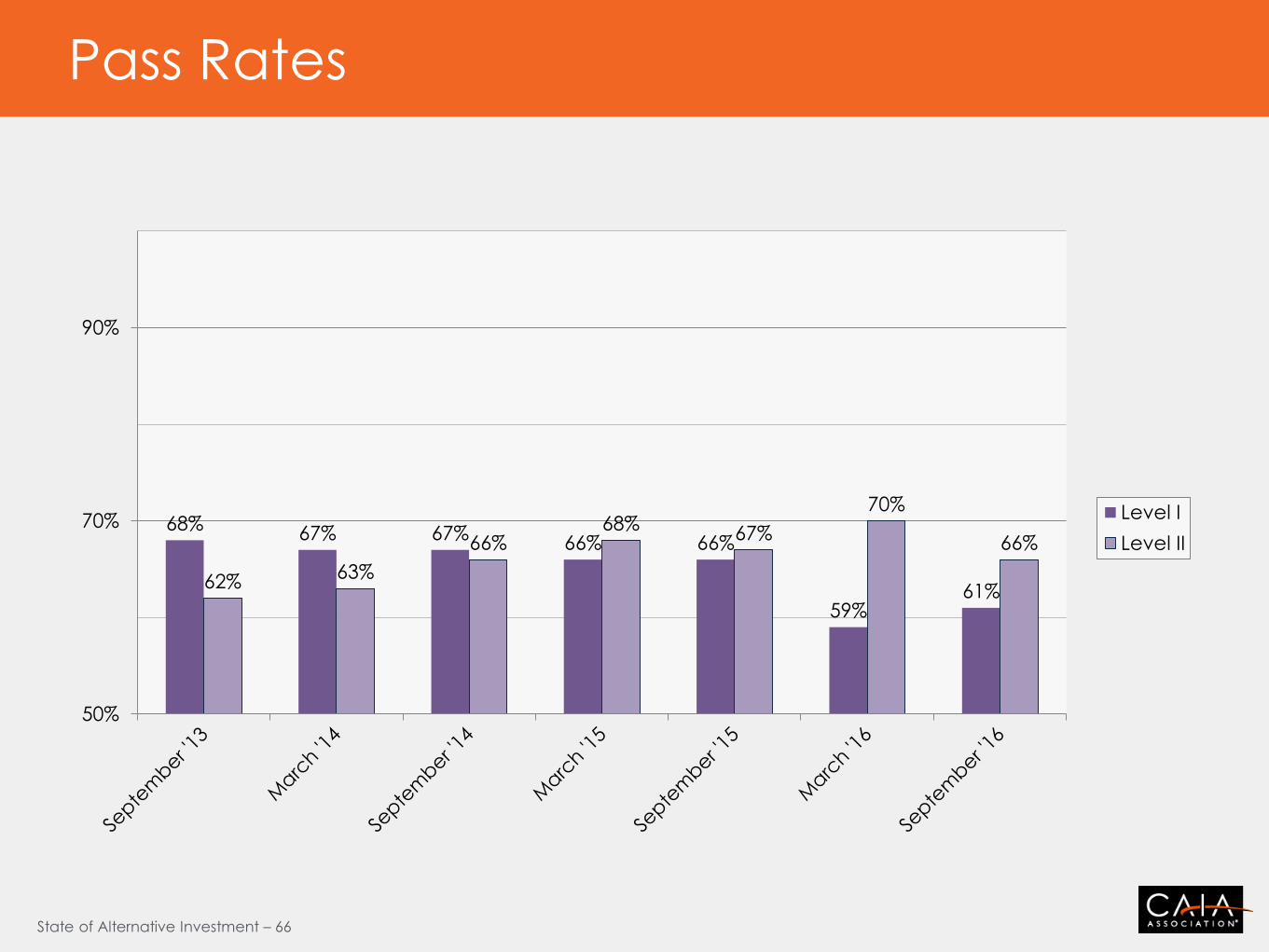

State of Alternative Investment – 66

68% 67% 67%

66% 66%

59% 61%

62% 63%

66% 68%

67%

70%

66%

50%

70%

90%

Level I

Level II

Pass Rates

State of Alternative Investment – 67

CAIA Charter

State of Alternative Investment – 68

Academic Partnerships - Americas

State of Alternative Investment – 69

A complete list of CAIA’s academic

partners globally can be found at caia.org.

Academic Partnerships - EMEA

State of Alternative Investment – 70

Academic Partnerships - APAC

A complete list of CAIA’s academic partners globally can be found at caia.org.

State of Alternative Investment – 71

Association Partnerships

State of Alternative Investment – 72

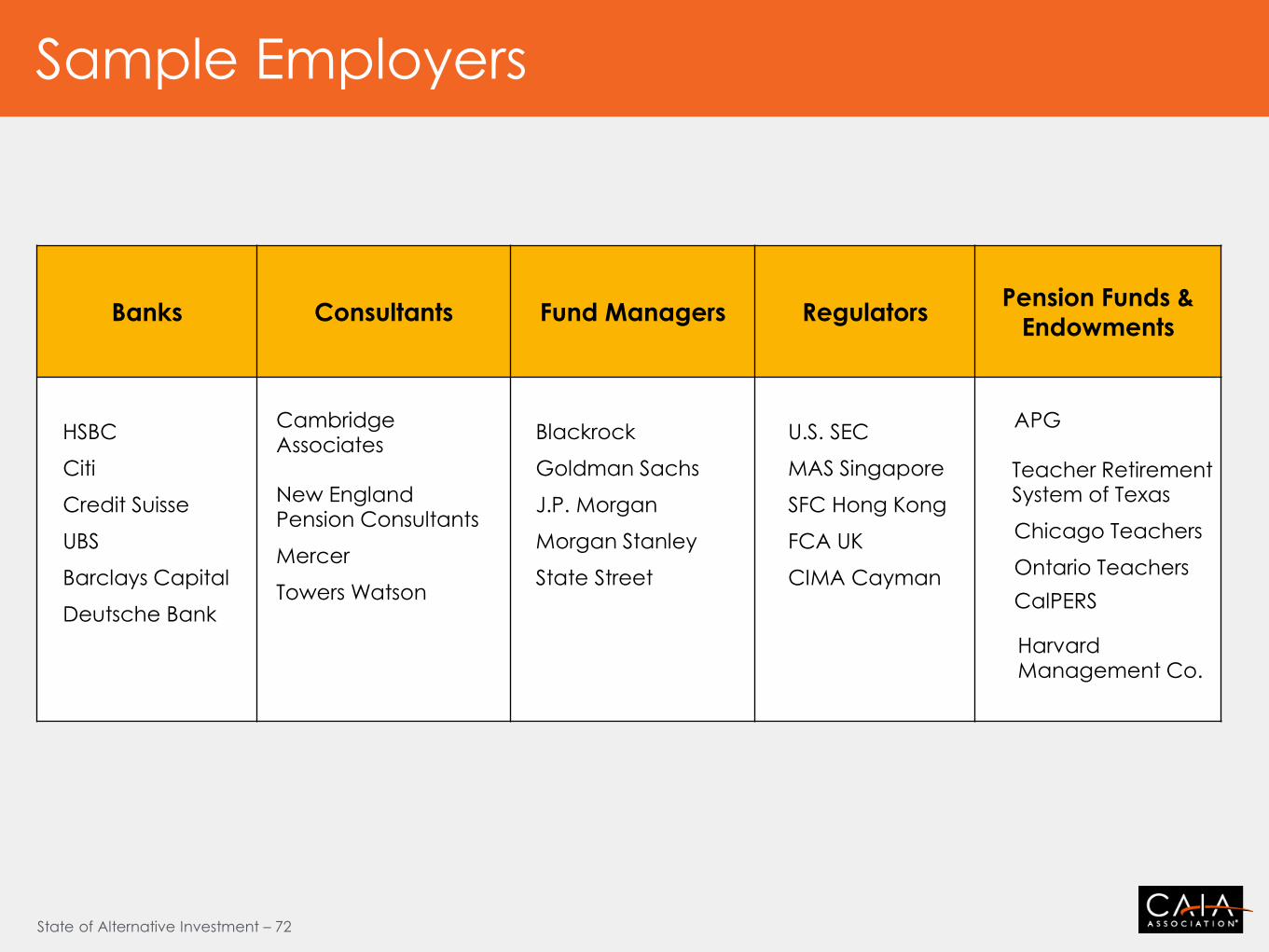

Banks Consultants Fund Managers Regulators Pension Funds &

Endowments

HSBC

Citi

Credit Suisse

UBS

Barclays Capital

Deutsche Bank

Cambridge Associates New England Pension Consultants

Mercer

Towers Watson

Blackrock

Goldman Sachs

J.P. Morgan

Morgan Stanley

State Street

U.S. SEC

MAS Singapore

SFC Hong Kong

FCA UK

CIMA Cayman

APG

Teacher Retirement System of Texas

Chicago Teachers

Ontario Teachers

CalPERS Harvard Management Co.

Sample Employers

State of Alternative Investment – 73

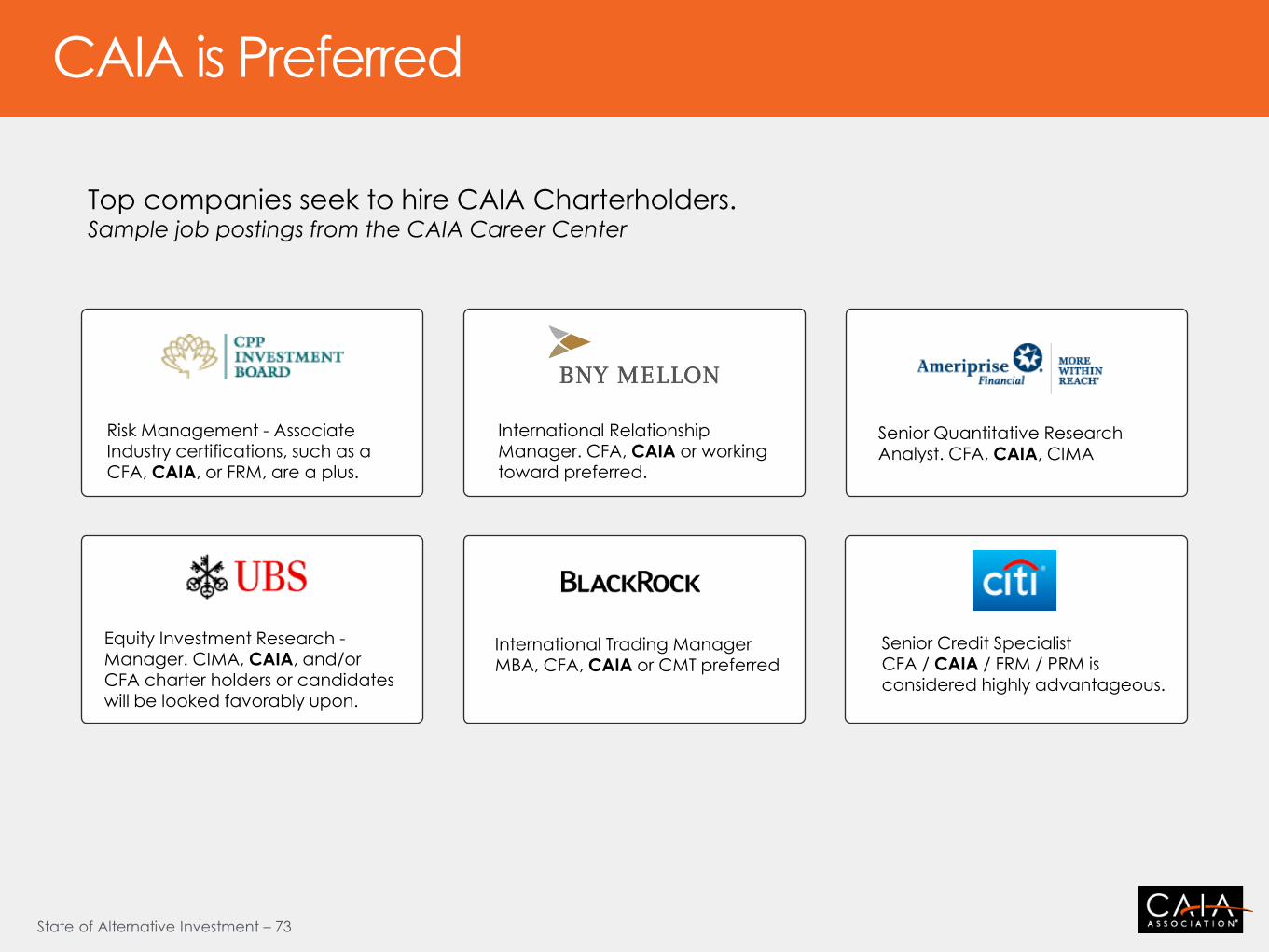

Top companies seek to hire CAIA Charterholders. Sample job postings from the CAIA Career Center

International Relationship Manager. CFA, CAIA or working toward preferred.

Equity Investment Research -

Manager. CIMA, CAIA, and/or CFA charter holders or candidates will be looked favorably upon.

International Trading Manager MBA, CFA, CAIA or CMT preferred

CAIA is Preferred

Senior Quantitative Research Analyst. CFA, CAIA, CIMA

Senior Credit Specialist CFA / CAIA / FRM / PRM is considered highly advantageous.

Risk Management - Associate Industry certifications, such as a CFA, CAIA, or FRM, are a plus.

State of Alternative Investment – 74

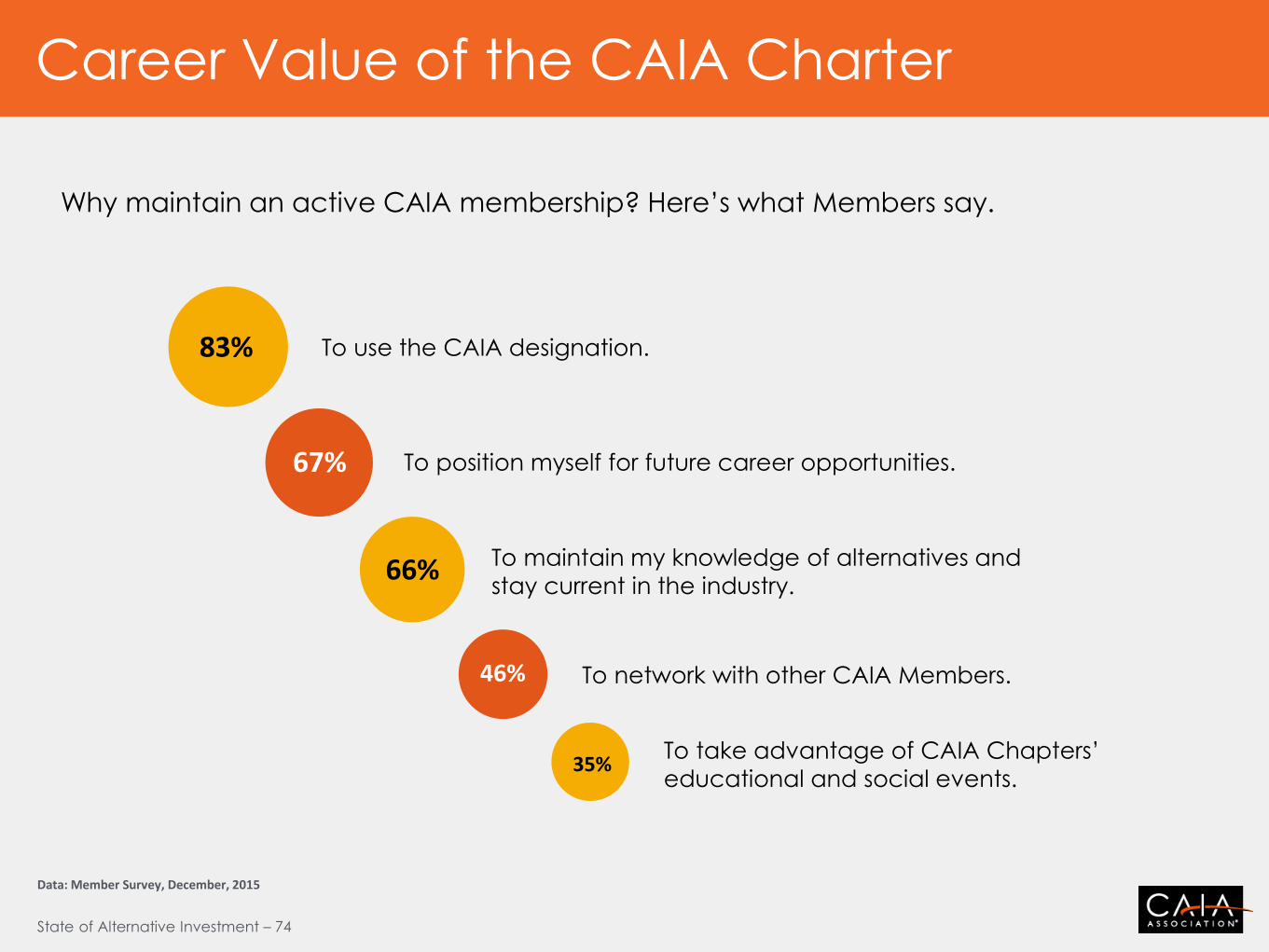

Why maintain an active CAIA membership? Here’s what Members say.

67%

83%

66%

46%

35%

Data: Member Survey, December, 2015

To use the CAIA designation.

To position myself for future career opportunities.

To maintain my knowledge of alternatives and

stay current in the industry.

To network with other CAIA Members.

To take advantage of CAIA Chapters’

educational and social events.

Career Value of the CAIA Charter

State of Alternative Investment – 75

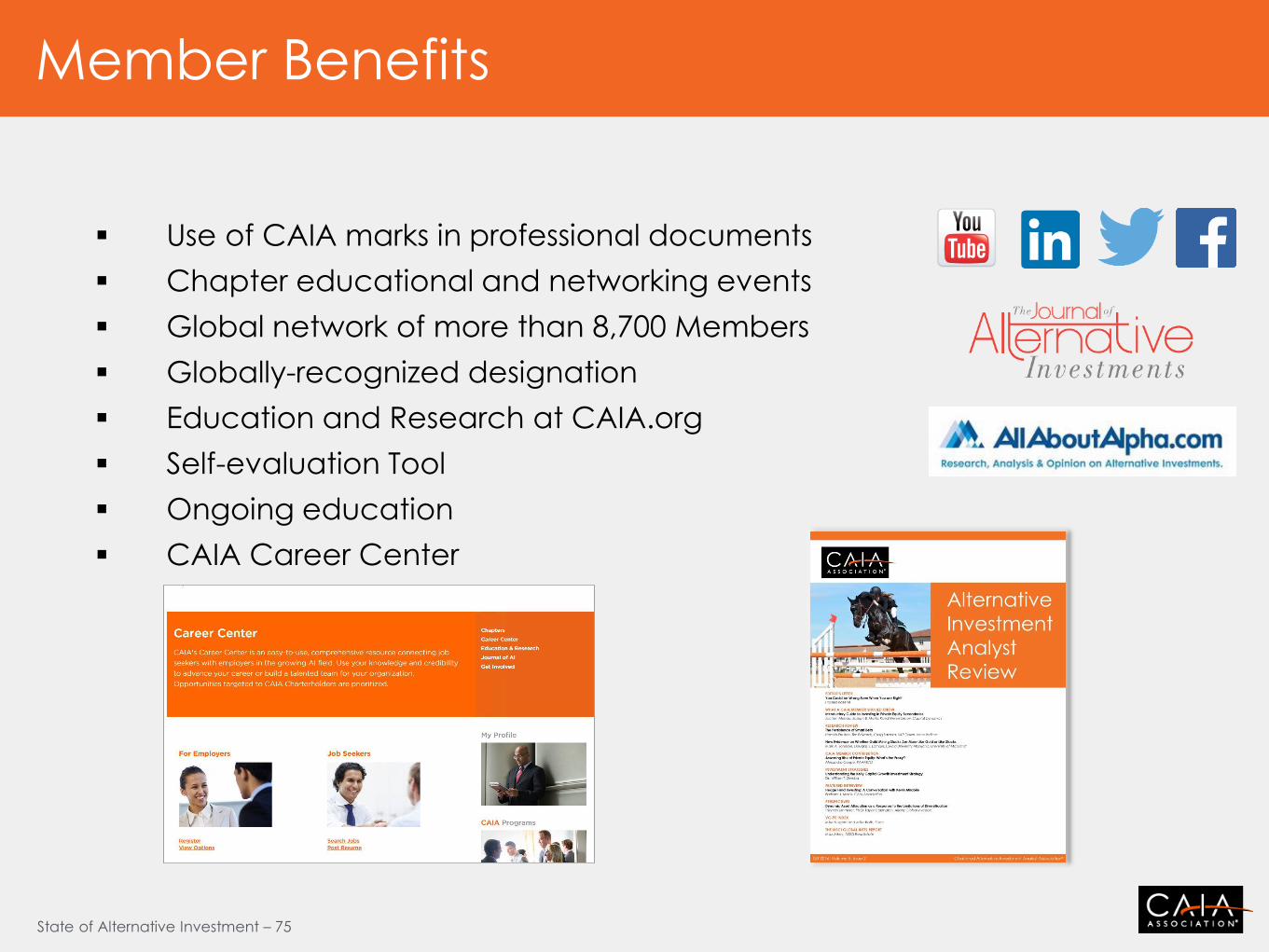

Use of CAIA marks in professional documents

Chapter educational and networking events

Global network of more than 8,700 Members

Globally-recognized designation

Education and Research at CAIA.org

Self-evaluation Tool

Ongoing education

CAIA Career Center

Member Benefits

State of Alternative Investment – 76

Early

Registration

Apr 3 – May 15, 2017

Regular

Registration

May 16 – Aug 7, 2017

Level I Exam

Sept 4 - 15, 2017

Level II Exam

Sept 18 – 29, 2017

APR MAY JUN JUL AUG SEPT

Exams September 2017 – Notable Dates

State of Alternative Investment – 77

AMERICAS

Millissa Allen, CAIA Amherst Managing Director of Business Development direct: +1 413 549 3324 [email protected]

Cody Durant Amherst Business Development Manager direct: +1 413 549 3313 [email protected]

EUROPE, MIDDLE-EAST, AFRICA

Laura Merlini, CAIA Geneva Managing Director of Business Development direct: +41 796 154 491 [email protected]

Tammy Johnston London Global Business Development Associate [email protected]

ASIA-PACIFIC

Joanne Murphy Hong Kong Managing Director, APAC direct: +852 3752 0495 [email protected]

Wendy Leung Hong Kong Assistant Director, APAC direct: +852 3752 0495 [email protected]

Peter Douglas, CAIA Singapore

Principal direct: +65 6536 4241 [email protected]

Global Business Development Contacts

www.caia.org

The Global Benchmark In Alternative

Investment Education

The CAIA Charter