the soda report (volume 1, 2016); 2016-17 forecast

TRANSCRIPT

From the SoDA Board Chair

Tony QuinChairman of the Board, SoDA & CEO, IQ

Welcome to the first 2016 edition of The SoDA Report, our organization’s biannual trend publication released in May and December each year.

As The SoDA Report enters its 7th year, it continues to be one of the most viewed digital trends publication in the world, with nearly half a million views and downloads per year. In this latest issue, SoDA’s elite membership, partners and other industry leaders once again provide insight into the latest digital trends and innovations for brands amid the confluence of digital marketing, customer experience and product design.

2016 finds the SoDA organization going from strength to strength. Building on our wildly successful inaugural SoDA Academy in New York last October, we will once again be bringing together director-level leaders from digital agencies around the world for remarkable master-classes and peer-to-peer collaboration on November 14th & 15th in New York City at the Museum of the Moving Image. Find out more about how to qualify for this invitation-only event.

With over 100 handpicked member companies on 6 continents, SoDA remains the preeminent network of digital agencies and creative companies in the world. Membership requires the highest standards of work, innovation, reputation and culture. So much so that only 14% of agencies considered are elected as members. The resulting commitment to leadership and innovation that members bring to SoDA has enabled the organization to continue to grow its influence and value in the digital world.

I hope you find this edition of The SoDA Report valuable and enjoyable. Take the time to explore our primary website at www.sodaspeaks.com, where you can also sign up for our mailing list and stay informed about what’s coming next from SoDA.

Best wishes,Tony QuinChairman of the Board, SoDACEO, IQ Agency

For the full 2016 SoDA Report, Vol. 1, please visit www.sodareport.com

Note from the Editor-in-Chief

Chris BuettnerEditor-in-Chief and Executive Director, SoDA

Welcome to the latest edition of The SoDA Report. In this volume of our biannual trend publication, we explore the theme of Evolution. Agencies, consultancies, brands and other industry thought leaders largely agree that 2016 is shaping up to be an evolve-or-die year. Or, to put a positive spin on it, we might say it’s a year to thrive through intelligent adaptation. While some agencies are going the way of the dinosaur, a forward-thinking cross-section of shops are reporting increased revenues and profits by partnering with clients in new and innovative ways, by bringing their own IP to market and more. Other industry players need to evolve as major shifts in the way consumers use technology, consume media and engage with the world around them are forcing massive changes.

Throughout the 2016 editions of The SoDA Report, we’ll explore top trends and behaviors that leading practitioners in our industry won’t be able to ignore as the year unfolds, and we’ll cast a spotlight on brands, agencies and individuals who are flourishing in this environment.

Within Modern Marketer, Industry Insider and via our Digital Outlook Study (conducted in partnership with Forrester Research for the first time), we’ll also explore how the landscape of creativity and the modus operandi for agency-client relationships are shifting in radical ways. Spurred by rapidly changing consumer expectations and behaviors, agency-client partnerships are expanding in incredibly exciting ways beyond the marketing realm to include business strategy, R&D, product development and customer service.

We are so proud of the growth and development of The SoDA Report over the past year. Our 2015 editions have received over 400,000 views and downloads. In 2016, we’ll also be expanding the special report series we initiated last year under “The SoDA Report on…” moniker, with editions either in development or already published around top-of-mind topics such as the state of agency workflows, future-forward project management methods, experience design trends and the future of media.

I want to thank our Section Editors, our Partners at Forrester Research and all of our contributing authors from around the world. The production of this report is truly a global effort. In fact, in this edition, you’ll discover original artwork that we commissioned from illustrators in Taiwan, Uruguay, South Africa and the UK via Behance to help bring the feature articles to life.

I want to thank Barcelona-based SoDA member, Vasava, for translating our editorial theme of Evolution into a stunning visual metaphor for the cover of this edition. The

allusion to mysticism is an apt one, as the changes taking place in our industry also involve a constellation of distinctive practices, discourses, institutions, traditions and experiences aimed at human transformation.

To become a subscriber of The SoDA Report, please email SoDA and we’ll make sure you have priority access to the release of upcoming editions. We hope you enjoy this issue and, as always, we welcome your feedback, ideas and contributions for future editions.

Saludos,Chris BuettnerEditor-in-Chief and Executive Director, SoDA

For the full 2016 SoDA Report, Vol. 1, please visit www.sodareport.com

Team & Partners

Chris BuettnerManaging Editor of The SoDA ReportSoDA Executive Director

After a career on the digital agency and publisher side that spanned 15+ years, Chris Buettner now serves as Managing Editor of The SoDA Report. He is also the Executive Director of SoDA where he is charged with developing and executing the organization’s overall strategic vision and growth plan. And with roots in journalism, the transition to lead SoDA has been a welcome opportunity to combine many of his talents and passions. After living in Brazil and Colombia for years, Chris is also fluent in Spanish and Portuguese and is an enthusiastic supporter of SoDA’s initiatives to increase its footprint in Latin America and around the world. Chris lives in Atlanta with his wife and two daughters.

Brigitte MajewskiVice President, Research Director Serving B2C Marketing Professionals, Forrester

A graduate of Emory University, Lakai Newman comes to SoDA from a NY-based digital agency where he focused on creating compelling content for a number of blue-chip brands. He serves as SoDA’s primary steward and contact for communications, social media and marketing efforts. Lakai also serves as head of production for The SoDA Report, SoDA’s biannual trend publication that features primary research, thought leadership, and case studies from top digital agencies, production companies, and client-side digital marketing executives from around the world. He considers himself a natural “creative” that is passionate about global travel, cooking, pop-culture, and all things digital.

Melissa ParrishVice President, Principal Analyst Serving B2C Marketing Professionals, Forrester

As vice president and principal analyst at Forrester Research, Melissa serves B2C Marketing Professionals and is a leading expert on social and digital marketing strategy. In her research, Melissa explores how marketers use evolving technologies and platforms to create and deepen the bonds between them and their ever-changing customers. Melissa earned a B.A. in drama and philosophy from Loyola University, New Orleans, an M.A. in liberal studies from The New School, and an M.F.A. in dramaturgy and script development from Columbia University.

Research Team

Sarah SikowitzPrincipal Analyst Serving B2C Marketing Professionals, Forrester

Sarah serves B2C Marketing Professionals at Forrester Research. Sarah’s chief role is to help marketing leaders navigate the needs from and relationships with the agencies that serve them. She analyzes the role of agencies as a part of the post-digital landscape, including agency portfolio management and in-house agency strategy. Sarah has a bachelor’s degree in American studies from Wesleyan University and an MBA in marketing from Kellogg School of Management. She lives in Cambridge, MA with her husband and two children.

PARTNERS

Research Partner

Lead Organizational Sponsors

Content & Production Data Graphics Provided By

Cover Design

(Founding Organizational Partner)

The opinions and viewpoints expressed in the articles in this publication are those of the authors, and do not necessarily represent or reflect the opinions or viewpoints of SoDA.

The SoDA Report Production Team

Lakai Newman, Head of ProductionA graduate of Emory University, Lakai Newman comes to SoDA from a NY-based digital agency where he focused on creating compelling content for a number of blue-chip brands. He serves as SoDA’s primary steward and contact for communications, social media and marketing efforts. Lakai also serves as head of production for The SoDA Report, SoDA’s biannual trend publication that features primary research, thought leadership, and case studies from top digital agencies, production companies, and client-side digital marketing executives from around the world. He considers himself a natural “creative” that is passionate about global travel, cooking, pop-culture, and all things digital.

Jessica Ongko, Production DesignerSince joining the operation team in 2014, Jessica has been deeply involved with strengthening SoDA’s brand and visual identity while collaborating with agencies around the world to design and create publications, event signage, and digital/physical assets related to the work of SoDA. A graduate of the graphic design program from advertising portfolio school, The Creative Circus, you’ll often find Jessica trotting the globe and working out of airports during long layovers.

The responsive version of The SoDA Report was developed with a variety of solutions from the Adobe Creative Cloud.

0 Introduction to the Digital Outlook Study1 Respondent Overview2 Agency Ecosystems in 20163 The State of the Agency-Client Relationship4 The Outlook for Agencies5 Modern Marketer6 Talent and Advocacy

T A B L E O F C O N T E N T S

Introduction to the Digital Outlook Study

The respondent base for this year’s study proves once again that digital is on the minds of business leaders and key decision makers. Client-side respondents were just as experienced as those who responded last year with 86% at the level of director of marketing or above. These high-level business leaders also command substantial marketing budgets: 64% have $5 million to $100 million or more to spend; and 30% were at the high end of this spectrum with budgets of $50 million or more.

With this kind of money on the table, one might expect clients to be increasing investment in digital initiatives — and one would be right. While 11% report decreasing their budgets for this year, which is statistically even versus last year, 55% of client-side respondents expect to increase their spend in some way, either by an increase in overall marketing dollars or an increase in the digital allocation of a steady overall budget. This eight-point uptick year-on-year is likely due to optimism around the performance of digital programs, as opposed to excitement around emerging tech and creative strategies as we’ve seen in years past. For proof, just look to the areas in which large majorities of clients plan to increase their spend:

• Digital experiences (82%)• Content development (76%)• Digital projects (71%)

One of the most significant changes we see this year is essentially a total turnaround of what clients value most in their agency partners. Market or marketing research was the No. 1 most valued skill in clients’ relationship with their agencies — an option that was at the very bottom of the list last year. The least valued this year? Strategic leadership and marketing creativity, which adds fuel to the idea that clients are prioritizing execution over big ideas when it comes to agency relationships. Considering that emerging technologies topped the list last year, we believe this may also point to a trend of getting back to digital fundamentals, where clients are remembering that trendy tech is fun to talk about but may not be as successful at helping them reach their goals as solid data-driven strategy.

The good news is that agencies agree that these are the skills and services that are most valued by their clients. The bad news is that that’s where the agreement between agencies and their clients ends. Disconnects between marketers and their partners is a common topic, but when particular discrepancies in priorities and perceptions persist, as they do for the third year in our study, they demand a deeper look.

We asked respondents on both sides whether clients’ organizational structures hinder For the full 2016 SoDA Report, Vol. 1, please visit www.sodareport.com

or facilitate innovation. Forty-eight percent of client-side respondents said it helps while 51% of agency respondents said it hinders. A more startling disconnect emerges when it comes to perceived strengths within those organizational structures. Agency respondents believe that clients are very weak in the areas of executive management, user experience, and technology, while clients said their companies had little to no gap at all in these areas.

Even more important is the continued discrepancy between the reasons agencies think they were fired and the reasons clients cite for ending their relationships. Agency respondents said that changes in management were the No. 1 reason they were fired, just as they did last year. However, this year, this response was chosen by 56% versus 33% last year — a whopping 23-percentage-point increase. According to clients, the primary reason they fired their agencies was pricing or value, a new option this year, which garnered 37% of responses. Perhaps even more telling is the distribution of the rest of the responses on the client side. While cost overruns were second in last year’s study, this year that response is eighth, behind each of the following choices, which received between 20% and 24% of responses:

• Unhappy with creative • Unhappy with strategy• Unhappy with project management/account management• Mismatched agency size/ability• Understaffed/Underexperienced

This generalized dissatisfaction adds context to similarly lukewarm client satisfaction on agency programs. This year we asked clients to rate their satisfaction with each of the key services for which they turn to agencies. On a scale of one to five, not a single service scored better — or worse — than the mid-threes. Considering that this includes those services for which clients plan to increase investment, it points to the possibility of even greater churn in client-agency pairings as marketers look for new partners to deliver at a higher level on their increased hopes and expectations.

While 53% of agency respondents believe that working relationships with their clients are improving overall, it’s clear that there’s still lots of room for improvement. And with so much optimism — and investment — around digital it’s crucial to turn this general malaise and discomfort around. Otherwise, the trend for agencies with digital roots to be the lead among all agency partners — which 76% of agency respondents agree is becoming more likely — will never be the norm.

For the full 2016 SoDA Report, Vol. 1, please visit www.sodareport.com

Respondent OverviewOrganization TypeKEY INSIGHT:

• Client participation in the Digital Outlook Study reached an all-time high in 2016, representing a broad array of industry verticals.• Consultancies, once the new kids on the block in digital, have solidified their presence within the community of influencers examining and shaping digital marketing trends.

For the full 2016 SoDA Report, Vol. 1, please visit www.sodareport.com

The share of client-side marketers responding to the SoDA/Forrester Digital Outlook Survey rose 24% in 2016 on a year-over-year basis. This increase likely stems from the fact that brands are scaling their in-house digital operations and growing their leadership teams by recruiting executives with deep digital expertise — often from the agency side.

The share of consultancies in the respondent mix fell slightly in 2016 (from 10% to 8%), but still stands at double the level of SoDA’s 2014 study. The rise of consultancies focusing on digital transformation via their own homegrown efforts and through M&A activity is no longer a nascent trend, but rather a prevalent movement within the global ecosystem of digital service providers. First-movers Deloitte Digital and Accenture Interactive have been joined by PwC, McKinsey, KPMG, IBM, Perficient, and others in a mad dash to bolster their digital chops and capture a larger share of growing budgets in areas such as customer experience, UX, digital product and platform development, and interaction design. Brands are anxious to understand what the “digital transformation” mantra should mean for their businesses and how they need to evolve to better serve connected consumers.

For the full 2016 SoDA Report, Vol. 1, please visit www.sodareport.com

Job TitleKEY INSIGHT:

• Senior-level executives are showing unprecedented levels of interest in digital marketing research and insights as evidenced by their participation in the SoDA/Forrester study.• Ninety-two percent of respondents were key decision makers (C-level, senior executives, VPs, and directors).

(continued below)

For the full 2016 SoDA Report, Vol. 1, please visit www.sodareport.com

(continued below)

For the full 2016 SoDA Report, Vol. 1, please visit www.sodareport.com

A record 92% of all respondents (up from 88% in 2015 and 82% in 2014) were key decision makers and influencers at their companies (C-level, senior executives, VPs, and directors).

The share of respondents at the senior-most levels (VP and above) was largely consistent on the client and agency sides (62% for agencies and 60% for client-side marketers).

For the full 2016 SoDA Report, Vol. 1, please visit www.sodareport.com

Geographic Region

Just over three out of five respondents to this year’s study derive the majority of their revenue from the North American market. However, participants from Europe and Asia are growing in numbers and importance.

Internationalization — in terms of both the respondent mix and SoDA as a whole — will no doubt continue given the groundbreaking digital work coming out of so many established and emerging economies in Europe, LatAm, and the APAC region.

In fact, 27% of SoDA’s member company offices are now in Latin America, Africa, and Asia, up from 20% in 2015 and 13% in 2014. Globally, SoDA members are present in 42 countries, with almost half (49%) located outside the U.S. and Canada.

For the full 2016 SoDA Report, Vol. 1, please visit www.sodareport.com

Marketing Budgets

The experience of client-side respondents in 2016 surpassed the already high level registered in 2015, with 86% at the level of director or above. These business leaders also control significant marketing budgets. Nearly two in three have US$5 million or more to spend, with 30% at the high end of that spectrum (i.e., budgets of US$50 million or more).

The client marketers surveyed represent a wide range of industry verticals, including financial services, insurance, healthcare, media and entertainment, pharmaceuticals, professional services, retail, telecommunications, travel and hospitality, automotive, consumer electronics and consumer packaged goods.

With digital transformation efforts and disruption taking place across every industry vertical, it’s not surprising that the client-side mix of leaders paying attention to digital trends is the most diverse we’ve seen since initiating this research study back in 2009.

For the full 2016 SoDA Report, Vol. 1, please visit www.sodareport.com

Agency Types

On the agency side, respondents included a mix of full-service digital shops, agencies handling both traditional and digital assignments, and niche players in areas such as experience design, social, mobile, and content marketing.

The share of agencies identifying as “Full-service (digital only)” was higher than anticipated given the large number of SoDA member companies dedicated to niche focus areas, including specialization in place-based digital experiences, product development, user experience, and social, among other fields. However, the respondent base includes a broad mix of member and non-member agencies, with SoDA members comprising only 25% of all agency respondents.

For the full 2016 SoDA Report, Vol. 1, please visit www.sodareport.com

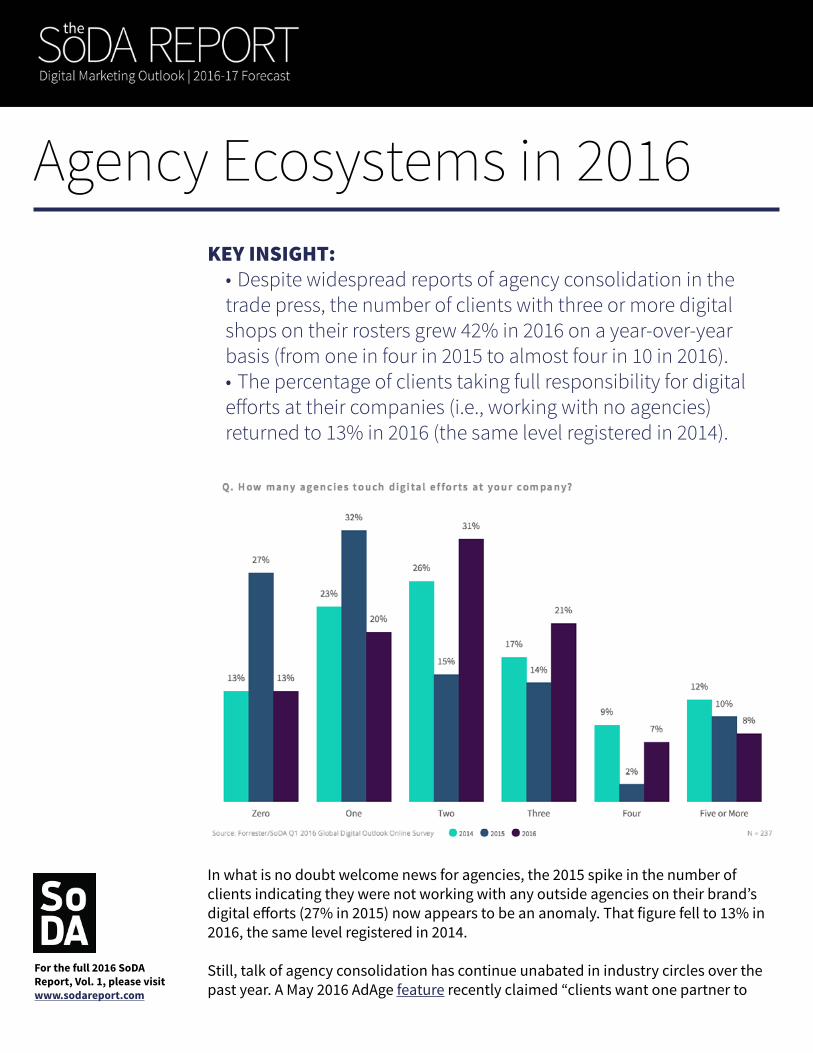

Agency Ecosystems in 2016KEY INSIGHT:

• Despite widespread reports of agency consolidation in the trade press, the number of clients with three or more digital shops on their rosters grew 42% in 2016 on a year-over-year basis (from one in four in 2015 to almost four in 10 in 2016).• The percentage of clients taking full responsibility for digital efforts at their companies (i.e., working with no agencies) returned to 13% in 2016 (the same level registered in 2014).

In what is no doubt welcome news for agencies, the 2015 spike in the number of clients indicating they were not working with any outside agencies on their brand’s digital efforts (27% in 2015) now appears to be an anomaly. That figure fell to 13% in 2016, the same level registered in 2014.

Still, talk of agency consolidation has continue unabated in industry circles over the past year. A May 2016 AdAge feature recently claimed “clients want one partner to

For the full 2016 SoDA Report, Vol. 1, please visit www.sodareport.com

simplify the fragmentation and data.”

In part, the data in the 2016 SoDA/Forrester Digital Outlook Survey supports the core assertion of the AdAge piece that consolidation is on the rise. More than 50% of the client-side respondents work with only one or two digital agencies, up from 47% in 2015.

While it’s true that some agencies are going the way of the dinosaur (and others are being absorbed into holdings companies, consultancies, media companies, and tech firms), a forward-thinking cross-section of independent shops are reporting increased revenues and profits by partnering with clients in new and innovative ways in niche areas.

In fact, there is a parallel and significant counter-trend toward specialization in our 2016 study. The number of clients with three or more digital shops on their rosters grew 42% in 2016 on a year-over-year basis (from about one in four in 2015 to almost four in ten in 2016).

Other research studies conducted by SoDA in 2016 underscore that the overall state of the business for top digital shops is strong. Sixty-two percent of all respondents to SoDA’s latest “Quick Strike” financial health survey indicated that their profit margins grew in the most recent quarter (versus the same quarter in 2015). And of those reporting profit margin growth, nearly half were in the extremely high growth category (25% profit margin growth or higher).

For the full 2016 SoDA Report, Vol. 1, please visit www.sodareport.com

Innovation EffortsKEY INSIGHT:

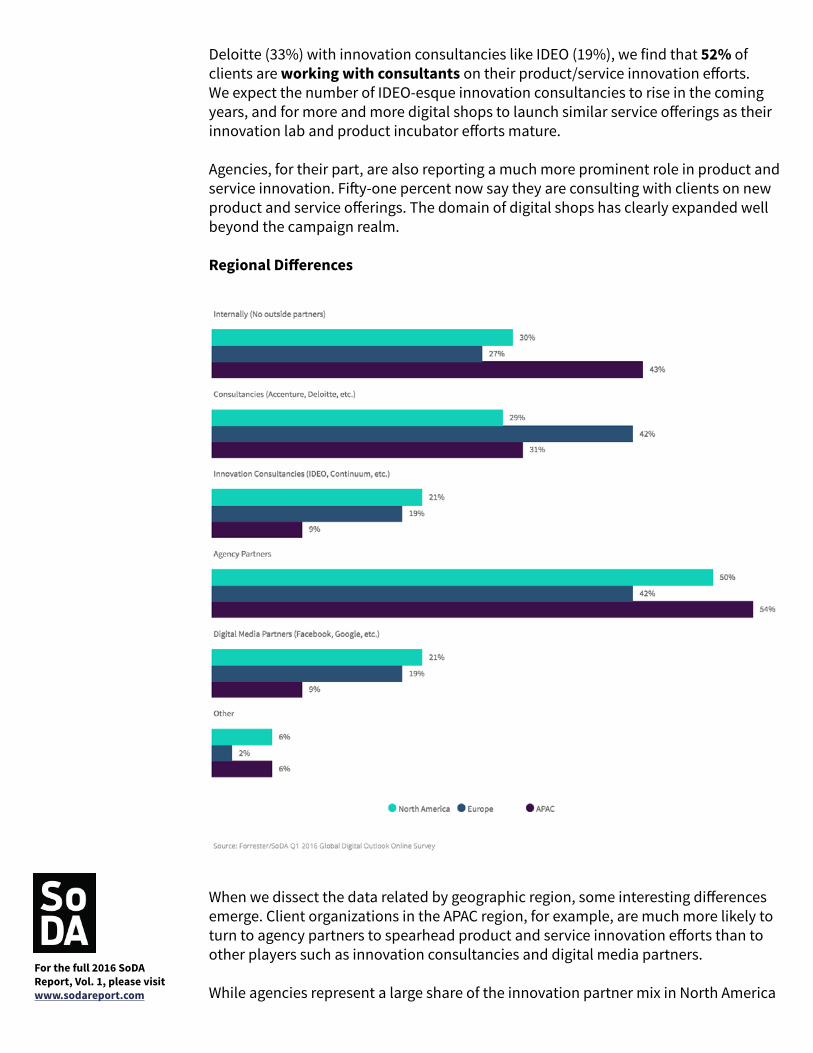

• When it comes to innovating product and service offerings, the two most important partners for clients are agencies (50%) and consultancies (52%).

In 2016, agency partners clearly have a seat at the table when it comes to partnering with clients on product and service innovation. Even a cursory review of the Showcase Section of this survey edition underscores that fact. A whopping 50% of clients said they are now partnering with agencies in the product and service innovation realm. In 2015, that figure was 20%, although full disclosure — the question was structured as a single select question versus multiple select as was the case in the 2016 study.

The prominent role of consultancies in the area of innovation was also clear in this year’s results. Combining professional service consultancies like Accenture and

For the full 2016 SoDA Report, Vol. 1, please visit www.sodareport.com

Deloitte (33%) with innovation consultancies like IDEO (19%), we find that 52% of clients are working with consultants on their product/service innovation efforts. We expect the number of IDEO-esque innovation consultancies to rise in the coming years, and for more and more digital shops to launch similar service offerings as their innovation lab and product incubator efforts mature.

Agencies, for their part, are also reporting a much more prominent role in product and service innovation. Fifty-one percent now say they are consulting with clients on new product and service offerings. The domain of digital shops has clearly expanded well beyond the campaign realm.

Regional Differences

When we dissect the data related by geographic region, some interesting differences emerge. Client organizations in the APAC region, for example, are much more likely to turn to agency partners to spearhead product and service innovation efforts than to other players such as innovation consultancies and digital media partners.

While agencies represent a large share of the innovation partner mix in North America

For the full 2016 SoDA Report, Vol. 1, please visit www.sodareport.com

(50%), their participation in innovation efforts in Europe is less prevalent (42%). In Europe, consultancies have a much more prominent role in the innovation partner mix, with more than two in five clients saying they partner with consultancies such as Accenture, Deloitte, McKinsey, and others to drive innovation.

For the full 2016 SoDA Report, Vol. 1, please visit www.sodareport.com

The Value of Innovation Labs

The SoDA Report theme for this year is Evolution. To put a positive spin on it, we’re specifically exploring how companies in our industry are thriving through intelligent adaptation. Nowhere is that more evident than in the realm of product development. More and more digital shops are transforming their revenue models and bringing their own products and IP directly to market as a growth engine for their companies and as a hedge against the commoditization and in-housing of some digital services.

These innovation and product development efforts are reaching a maturation point that we have not seen in previous studies. Almost four in 10 agency respondents (38% to be exact) have had an innovation lab in place for three or more years. In 2015, that figure was only 29%.

For agencies whose innovation labs are three or more years old, nearly one in five reported that their efforts had resulted in a company spin-off, VC investment, or significant funding; three in four said their innovation lab efforts contributed directly to new business wins, and almost two in five indicated increased revenue from their product incubation efforts. Talent retention and new business development maintained their position in 2016 as

For the full 2016 SoDA Report, Vol. 1, please visit www.sodareport.com

the two most salient benefits overall (53% and 55%, respectively), regardless of the age of the innovation lab.

Driving substantial revenue growth, however, takes time. After three years, nearly four in 10 agencies (38%) indicate that their product incubators and innovation labs are driving significant growth for the company. That figure falls to 18% if the lab has only been in existence for one to two years, and into the single digits if it is 12 months old or younger.

Clearly, moving from a service-based model to product development leaves agencies and production companies with a steep learning curve, which takes time to flatten.

KEY INSIGHT: • While fewer than one in 10 agencies cite revenue growth as a benefit of newly formed (under one year old) innovation labs, that percentage quadruples for shops that have three or more years of product incubation experience under their belts.

Q. What benefits has your innovation lab/product incubator produced? (select all that apply)

For the full 2016 SoDA Report, Vol. 1, please visit www.sodareport.com

For the full 2016 SoDA Report, Vol. 1, please visit www.sodareport.com

KEY INSIGHT: • Agency leaders say the impact of product incubators and innovation labs on business development more than triples after year 1.

Q. What benefits has your innovation lab/product incubator produced? (select all that apply)

(continued below)

For the full 2016 SoDA Report, Vol. 1, please visit www.sodareport.com

For the full 2016 SoDA Report, Vol. 1, please visit www.sodareport.com

What Types of Digital Shops Are Clients Hiring?KEY INSIGHT:

• Despite all the talk about nearshoring and offshoring, only a small percentage of clients are forging offshore production partnerships directly. However, more than one in five agencies are leveraging such relationships.

* Survey question posed for first time in 2016-2017 Digital Outlook Study

While there is a lot of talk about the rise of nearshoring and offshoring as a potential threat to agencies in developed markets, only a minuscule percentage of clients (1%) are opting to offshore production to other markets while keeping digital strategy with a lead agency.

Many agencies, however, are finding (and contracting with) strong and sophisticated digital production partners in developing economies, allowing them to maintain healthy margins despite the demand for rapid-fire innovation and the growing complexities of client work across an ever-expanding array of screens and consumer touchpoints. In our study, over one in five agencies (22%) were leveraging nearshoring and offshoring services for digital production. For the full 2016 SoDA

Report, Vol. 1, please visit www.sodareport.com

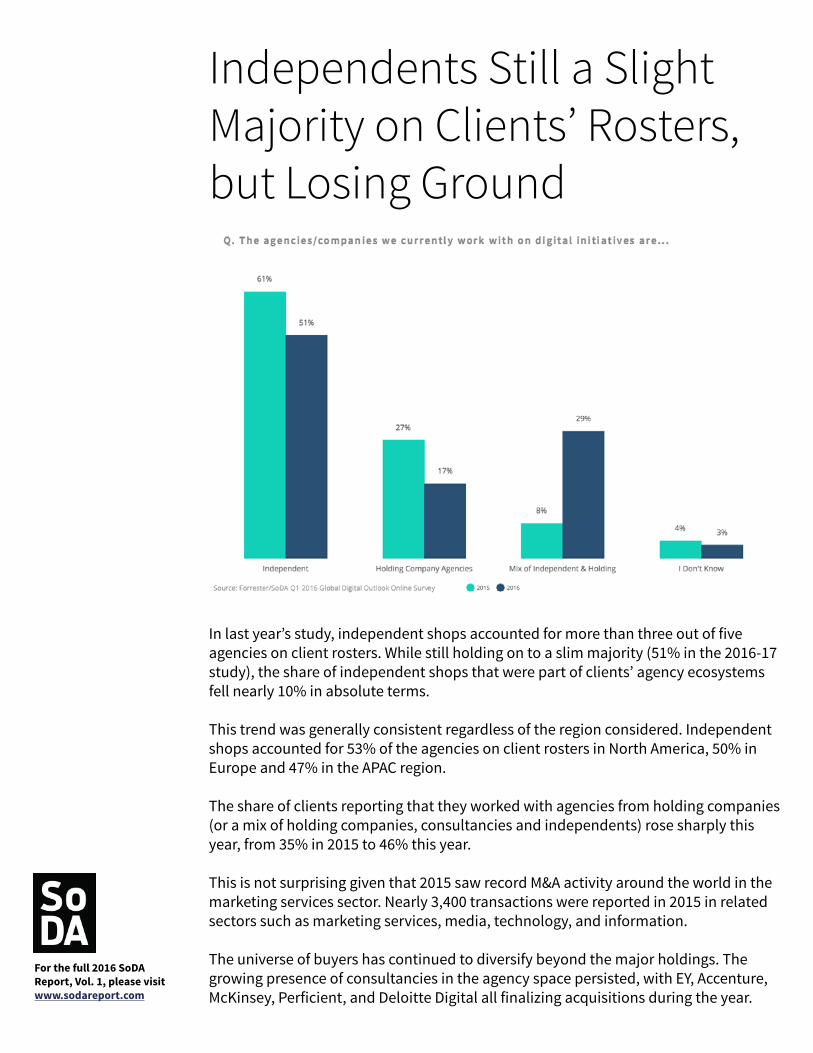

Independents Still a Slight Majority on Clients’ Rosters, but Losing Ground

In last year’s study, independent shops accounted for more than three out of five agencies on client rosters. While still holding on to a slim majority (51% in the 2016-17 study), the share of independent shops that were part of clients’ agency ecosystems fell nearly 10% in absolute terms.

This trend was generally consistent regardless of the region considered. Independent shops accounted for 53% of the agencies on client rosters in North America, 50% in Europe and 47% in the APAC region.

The share of clients reporting that they worked with agencies from holding companies (or a mix of holding companies, consultancies and independents) rose sharply this year, from 35% in 2015 to 46% this year.

This is not surprising given that 2015 saw record M&A activity around the world in the marketing services sector. Nearly 3,400 transactions were reported in 2015 in related sectors such as marketing services, media, technology, and information.

The universe of buyers has continued to diversify beyond the major holdings. The growing presence of consultancies in the agency space persisted, with EY, Accenture, McKinsey, Perficient, and Deloitte Digital all finalizing acquisitions during the year.

For the full 2016 SoDA Report, Vol. 1, please visit www.sodareport.com

New types of holdings have also emerged. Tokyo-based Hakuhodo DY Holdings, for example, has acquired an extremely prestigious lineup of digitally savvy companies in the past 12 months, including IDEO, Sid Lee, and Digital Kitchen.

Independent shops still hold a slim majority on client rosters, and we continue to believe that the most forward-thinking and innovative shops have a very bright future. In fact, the independents themselves are more bullish than their holding company counterparts about their prospects for 2016. When asked how confident they were that 2016 would be better than 2015 in terms of profitable growth (on a scale of 1 to 10), the average response for independents was a healthy 7.1, 16% higher than the holding company average of 6.1.

For the full 2016 SoDA Report, Vol. 1, please visit www.sodareport.com

Ch-Ch-Changes in Client Engagement ModelsKEY INSIGHT:

• Over half of all agency respondents report consulting with clients on new product and service offerings.

* Survey question posed for first time in 2016-2017 Digital Outlook Study

What is particularly revealing about the statistics above is the linear decline in the number of respondents indicating there were “no changes” in their engagement models with clients. The status quo is clearly not reigning supreme.

Those respondents indicating “no change” has declined steadily from 22% in 2013 to 12% in 2016. In other words, almost nine in 10 agency respondents are seeing (and

For the full 2016 SoDA Report, Vol. 1, please visit www.sodareport.com

sometimes pursuing) a transformation in how they work with clients. If we flip the data (visualizing the number of agencies who are seeing changes), the trend becomes even more salient.

More agencies are providing education and training services to clients (over one in three) as well as embedding specialized resources at client sites (almost one in four). Clients are moving full steam ahead developing in-house digital capabilities, a fact that has bolstered the training and staff augmentation trend in agency-client relationships.

Over the past few years, in-house digital teams on the client side have focused on areas such as community management or maintaining digital platforms developed by external partners, but these internal teams are now becoming much more sophisticated and innovation-focused.

Agencies are also beginning to realize they can’t do it all, particularly given the pace of technological advancements and the rising demand for highly specialized skill sets, including advanced data science capabilities. In fact, over one in four respondents indicated they were going to market with external third parties to round out their offerings.

As previously mentioned, there is also a growing number of agencies that are turning to nearshoring and offshoring for digital production work as a hedge against shrinking margins and the growing complexities of digital work. Twenty-one percent of agency respondents indicated they were now working with nearshore and offshore partners for digital production, while maintaining strategy and UX work in-house.

For the full 2016 SoDA Report, Vol. 1, please visit www.sodareport.com

The State of the Agency-Client Relationship

After a positive turn in 2015, the client/agency dynamic has hit a roadblock with the number of agencies reporting relationship improvements falling from 70% to 53%. This is likely due to an increasingly competitive landscape, where clients work across multiple agencies and are feeling more and more pressure to not only produce successful marketing campaigns, but to also “out-innovate” their competitors in areas that are still relatively new, like digital products and experiences, as well as marketing creativity and strategy.

The Client/Agency Dynamic

Agency respondents have a decidedly less optimistic outlook on their relationships with clients than in 2015, when 70% agreed that the dynamic was improving. This isn’t surprising as clients are pushing for diverse and innovative work from partners and

For the full 2016 SoDA Report, Vol. 1, please visit www.sodareport.com

aren’t particularly loyal to one shop (see Agency Ecosystems).

When we dug deeper, we saw that agencies that provide both traditional and digital services were more likely to have cause for concern than agencies that provide digital services only. This is likely due to the changes that these agencies, as well as their clients, have had to undergo to adjust to the always-evolving digital landscape. This transformation can be painful, resulting in a negative impact on the client/agency dynamic.

Even agencies that are experimenting with new types of engagement such as alternative compensation models or embedded resources did not feel particularly bullish compared with those agencies that are following more traditional models. 55% of agencies trying new engagement models agreed that the dynamic was improving versus 52% of their traditional counterparts.

This may indicate that new engagement models aren’t going to save these relationships. Instead, agencies and clients need to come back to an agreed upon value exchange and invest as much in the relationship as they do in the latest technology or consumer trend.

For the full 2016 SoDA Report, Vol. 1, please visit www.sodareport.com

What Clients WantThis year’s Digital Outlook Study revealed a greater imbalance between the skill sets that clients and agencies believe bring the most value to their relationship.

To gauge YOY trends, we asked both clients and agencies to rank the areas of expertise they believe to be the most valuable for client organizations. Here’s what they said:

Q. (Agencies) Generally speaking, what do your clients value most in their relationship with your organization? (Rank 1-9, with 1 being the highest)

Q. (Clients) Generally speaking, what do you value most in agency relationships? (Rank 1-9, with 1 being the highest)

For the full 2016 SoDA Report, Vol. 1, please visit www.sodareport.com

Before we get into the results, it’s important to note that, while the agency response shows a significant spread, the client results cluster in the middle — indicating that clients are having difficulty prioritizing what’s really important (everything is!). Agencies, on the other hand, seem to have prioritized services like strategic leadership and creativity over others.

Clients rank strategic leadership and marketing creativity in their top two —which agencies also agree are the same level of importance.

The similarities, however, end there. In 2015, clients and agencies aligned on five of the seven skill sets, while this year, we only see agreement on four out of nine. Clients are still seeking the fundamentals of customer-focused strategy and creativity from their agencies, along with basics like project management and measurement. Agencies, however, are putting more weight on expertise in emerging trends and technology capabilities. We can’t blame them though —clients ranked expertise in emerging trends highest in 2015!

Most notable is the gap between customer-centric marketing, which clients rank as the third most valuable skill set that an agency can bring. Agencies rank it sixth. With the proliferation of media channels and, now, brand experiences, the idea of providing utility to the customer can often get lost. This is an opportunity for agencies to start focusing more on the customer rather than the technology or channel when coming up with ideas.

For the full 2016 SoDA Report, Vol. 1, please visit www.sodareport.com

Why Clients LeaveMiscommunication is usually a root cause of any bad relationship — even at the end. And it’s no different with clients and agencies. Clients continue to leave for myriad reasons, but agencies continue to blame it on management changes. Not only is this incorrect, but it doesn’t break the top five termination reasons for clients.

Yet agencies continue to attribute client termination to new management. In fact, the percentage of agencies that blame client management changes jumped from 33% in 2015 to 56% in 2016 — a full 19 percentage points higher than the next most prevalent reason cited by agencies. This isn’t to say that it isn’t rising in significance for clients, who are often at the mercy of a new CMO or business lead under pressure to drive growth. Management changes jumped for clients as well from 11% in 2015 to 18% in 2016. Even with this jump, however, it still ranks seventh.

New to the survey this year is the pricing/value category, which clients and agencies wholeheartedly agree on! Thirty-seven percent on both sides attribute the end of their relationship to this common issue. This is not surprising, as agencies struggle to prove the impact of their work through measurement and clients feel increasing pressure to prove the ROI of agency investments. Agencies owned by holding companies feel this more acutely with 48% selecting pricing/value as a reason for termination versus 35% of independent agencies. This could be because holding company agencies are often sitting on bigger budgets and clients expect greater efficiencies.

After pricing/value, the client-side response clustered around unhappiness with strategy, creative and project management — the bread and butter of most client and agency relationships. As we saw in the What Clients Want section, these areas are of utmost importance and when agencies don’t meet expectations, clients are going to jump ship. Agencies that turn a blind eye to why their clients are really leaving will fail to address key improvement areas. The dysfunctional circle will continue until a new entrant comes along to disrupt the cycle.

Another big change from 2015 is the impact understaffing or inexperience can have on an agency’s chances of survival. In 2015, only 6% of clients listed this as a reason for termination; it jumped to 21% in 2016. As agencies struggle to stay competitive and meet client needs, they are sacrificing talent and sufficient skill development — and clients are starting to notice.

We expect inexperience to be an increasingly prevalent causal factor in agency-client relationships going south, as the percentage of agencies who indicated they are not providing any training to their staff almost tripled in 2016, growing from 5% to 14%.

Overall, client expectations are increasing across the board and agencies haven’t caught up yet. And they aren’t always bringing their business to other agencies. Many are also taking it in-house, which came out in the color commentary provided by respondents.

(continued below)For the full 2016 SoDA Report, Vol. 1, please visit www.sodareport.com

Q. (Clients) Thinking about your most recent experience with terminating an agency, why did that relationship end?

Q. (Agencies) Thinking about your most recent experience with being terminated by a client, why did that relationship end?

For the full 2016 SoDA Report, Vol. 1, please visit www.sodareport.com

Clients on Their Agency Partners: Everything is… Just OKKEY INSIGHT:

• Over half of all agency respondents report consulting with clients on new product and service offerings.

Last year, we asked clients to answer how likely they were to recommend their agency partners to a friend or colleague. We saw a general level of dissatisfaction for both digital and non-digitally-focused agencies.

We didn’t ask the same question this year because we wanted to dive into satisfaction levels for various digital agency services. We found a general feeling of “blah” from our client respondents regardless of the service. We did, however, see pockets of difference based on the type of client respondent.

Most notably, B2B marketers were the most dissatisfied (when compared to their B2C and B2B2C counterparts) with their agencies’ abilities in strategy, digital products, and customer insights. This represents an opportunity for agencies with expertise in these areas and B2B marketing.

User experience, content, and app development received the lowest marks from all marketers.

For the full 2016 SoDA Report, Vol. 1, please visit www.sodareport.com

Are Clients Organized for Innovation?For the second year, SoDA asked both clients and agencies for their opinion on clients’ organizational structure and whether those structures facilitate or hinder their ability to innovate and spur positive change. 2016 results follow the same patterns as 2015, but the gaps are wider. Here’s what they said:

(continued below)

For the full 2016 SoDA Report, Vol. 1, please visit www.sodareport.com

As we saw in 2015, clients and agencies have very different perceptions of how clients are positioned to drive innovation. 2016, however, reveals even larger gaps and less uncertainty. In 2015, 17% of clients reported that their organization hindered their ability to innovate. This jumps to 29% in 2016.

Clients picked sides on this issue in 2016, as evidenced by the fact that the share of noncommittal respondents (i.e., those indicating their organization neither facilitates nor hinders innovation) shrank from 41% to 23%. The percentage of clients responding that their organization facilitates innovation saw a slight increase from 42% to 48%.

Meanwhile, agencies are feeling less optimistic — with the percentage reporting that their clients’ current organizational structures facilitate innovation dropping from 15% to 12% and those that think client org structures hinder rising from 44% to 51%.

As the term innovation broadens and companies are feeling pressure to remain competitive, many organizations are devoting greater resources and time to innovation (or not), which is why clients are more likely to pick a side. Agencies, however, may find that working with these newly formed innovation teams or processes is even more cumbersome — bringing more process and red tape into projects that used to move quickly under the oversight of a rogue innovation team.For the full 2016 SoDA

Report, Vol. 1, please visit www.sodareport.com

Clients and Agencies Assess Their Digital SavvyQ: How do you rate your organization on the following? 1-5 with 1 being the weakest and 5 being the strongest (Clients, Agencies, Prodcos and other consultants were evaluating themselves on the three attributes listed below)

(continued below)For the full 2016 SoDA Report, Vol. 1, please visit www.sodareport.com

Similar to 2015, agencies continue to rank themselves higher than their marketing counterparts in these three key areas: user-centric design, emerging technology, and digital innovation. The gap, however, is lessening and clients are feeling more confident than agencies in their ability to drive digital innovation and incubate new products.

The real story here is the difference between agencies, production companies/studios, and other service providers that may identify as consultants. With the exception of user-centric design, agencies rank themselves lower than the other service providers in terms of emerging trends and digital/product innovation. Production companies/studios, as well as consultants, may be tasked with special projects focused solely on digital product innovation or emerging technology.

Agencies, on the other hand, are still tasked with the traditional tasks of an agency, which can include more traditional, but necessary, marketing tactics like creative development, campaign execution, and website updates.

For the full 2016 SoDA Report, Vol. 1, please visit www.sodareport.com

The Outlook for AgenciesFor many agencies, the decision on whether to specialize or broaden services remains a conundrum. The need for digital shops to determine their best path forward is becoming more acute, as traditional agencies and consultants continue to move into “digital agency territory.”

Regardless, agencies are positive about the future and are investing in the experiences and digital tools that their clients are clamoring for (and can’t yet build themselves). But while these areas are growing, agencies must combat cheaper alternatives like nearshoring or offshoring, as well as the growing number of clients taking agency services in-house. Agencies are also grappling with a general feeling that their impact on their clients’ businesses is lessening.

To remain differentiated, agencies will need to focus resources on the strategies and services that will deliver the most value to their clients. It also means exploring different working arrangements (embedded services, training, staff augmentation) and partnerships, both with other agencies and with consultants and clients.

Agencies’ Outlook is Positive, but Must Combat CommoditizationAgency respondents remain optimistic that shops with “digital roots” are well positioned to lead among a team of various agency partners. That being said, the percentage of respondents that agree with this statement has stalled at the same level as 2015. This is quite different than the year-over-year surge registered from 2014 to 2015. In last year’s study, the share of respondents who believed digital shops were rising to a preeminent position within agency ecosystems jumped 10%.

Why doesn’t a higher percentage of respondents agree this year? Maybe because traditional agencies and other service providers, like consultancies, are catching up. As digital has become not only prevalent, but pervasive, the players that have previously been in the driver’s seat, like consultants or traditional brand agencies, have developed a deeper digital skill set so that they don’t lose their leadership position.

(continued below)For the full 2016 SoDA Report, Vol. 1, please visit www.sodareport.com

For the full 2016 SoDA Report, Vol. 1, please visit www.sodareport.com

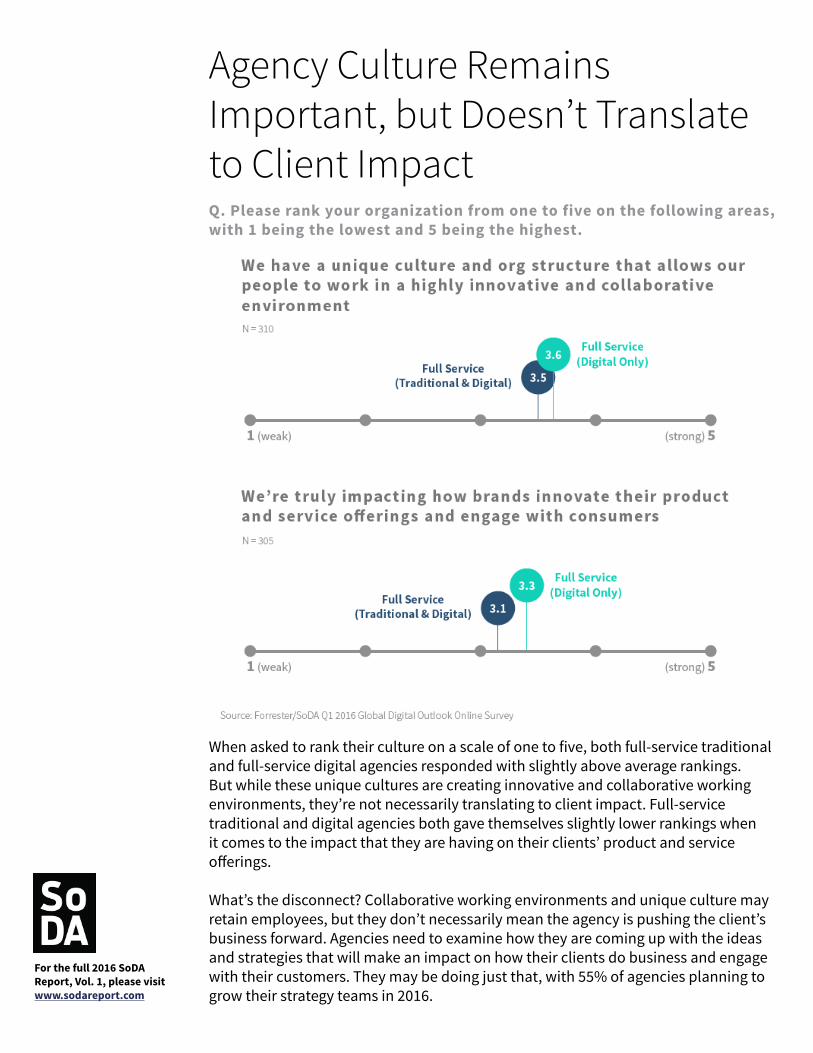

Agency Culture Remains Important, but Doesn’t Translate to Client ImpactQ. Please rank your organization from one to five on the following areas, with 1 being the lowest and 5 being the highest.

When asked to rank their culture on a scale of one to five, both full-service traditional and full-service digital agencies responded with slightly above average rankings. But while these unique cultures are creating innovative and collaborative working environments, they’re not necessarily translating to client impact. Full-service traditional and digital agencies both gave themselves slightly lower rankings when it comes to the impact that they are having on their clients’ product and service offerings.

What’s the disconnect? Collaborative working environments and unique culture may retain employees, but they don’t necessarily mean the agency is pushing the client’s business forward. Agencies need to examine how they are coming up with the ideas and strategies that will make an impact on how their clients do business and engage with their customers. They may be doing just that, with 55% of agencies planning to grow their strategy teams in 2016.

For the full 2016 SoDA Report, Vol. 1, please visit www.sodareport.com

Agencies Build Experiences and Tools… and Their Business

Agencies are increasingly positive about the benefits of building experiences and tools for clients. Eighty-three percent of respondents agreed with the above assertion, up from 80% in 2015.

Why is this happening? We think it is the result of two primary factors:

1. The broader need of clients to create experiences beyond advertising, which we see in their budgeting decisions. Eighty-two percent are increasing budgets for digital experiences (e.g., websites, mobile web) and 71% are increasing budgets for digital products (i.e., non-marketing-related platforms, applications, tools, and services). 2. The increase in qualified talent and less expensive, faster technology, which allow agencies to scale their product development efforts with less financial risk.

(continued below)For the full 2016 SoDA Report, Vol. 1, please visit www.sodareport.com

Agencies are less excited about specialization. Only 50% agree that it’s the best route to growth. Drilling down farther, full-service digital shops are more bullish on specialization and may even consider themselves specialists. Meanwhile, only 38%

For the full 2016 SoDA Report, Vol. 1, please visit www.sodareport.com

of agencies that handle both traditional and digital think that specialization is a solid growth strategy.

Most clients are maintaining a specialized agency roster — which is no doubt why certain agencies still see specialization as a growth engine. In fact, 58% of clients still leverage a full roster of specialized agencies or a handful specialized shops in partnership with their full-service agencies.

For the full 2016 SoDA Report, Vol. 1, please visit www.sodareport.com

2016 Hiring Trends

Agencies are investing in content, customer insights and UX staff, in addition to growing their teams focused on the development of digital experiences (e.g., websites, mobile web). This makes sense, as clients are laser focused on understanding their customers in order to deliver highly relevant content and experiences.

To beef up their human resources in these areas, agencies anticipate hiring a mix of full-time staff and contractors. The categories with the highest percentage of freelance resources are app development, content, social, and UX. Agencies may consider these areas more scalable and nimble versus an area like strategy, where the teams tend to be smaller, but the work requires someone who is deeply embedded in the agency and client business.

For the full 2016 SoDA Report, Vol. 1, please visit www.sodareport.com

Full-Service Agencies Competing with Specialized Shops and In-House Client TeamsSpecialized agencies still reign supreme when it comes to app development and building immersive digital experiences. The skill sets needed to be competitive in these areas remain beyond the domain of many full-service agencies.

Many clients allocate strategy, content, and social marketing to both specialized and integrated agencies, but a growing cross-section of brands handle these functions internally. Twenty-six percent of clients report handling content development in-house, while 24% use a specialized agency and 18% use an integrated agency. This aligns with the growing trend of brands bringing content development under their own roof in order to increase the speed of development while keeping costs down.

Customer insights also tends to live in-house as clients want to be closer to their data. Control is also an issue. With so many agencies in the mix, it’s often smarter for the client to aggregate the massive amounts of data coming from a variety of sources rather than relying on an agency partner to do so.

Q. What types of companies do you currently work with on the following initiatives?

For the full 2016 SoDA Report, Vol. 1, please visit www.sodareport.com

For the full 2016 SoDA Report, Vol. 1, please visit www.sodareport.com

For the full 2016 SoDA Report, Vol. 1, please visit www.sodareport.com

For the full 2016 SoDA Report, Vol. 1, please visit www.sodareport.com

For the full 2016 SoDA Report, Vol. 1, please visit www.sodareport.com

Agencies Continue to Struggle with Data ScienceSimilar to last year, both agencies and production companies still think they are average when it comes to insights and data. It’s hard to say which came first, but 26% of clients now have this handled by an internal team (second only to content development). Remaining mediocre in these areas may not be sustainable for agencies given how critical a detailed understanding of the customer is for marketing strategy. Additionally, measurement is the only reliable way for an agency to prove its value, which could alleviate the complaints that we heard from clients who felt compelled to let agencies go because of their inability to track ROI.

Q. Please rank your organization from one to five on the following areas, with one being the lowest and five being the highest.

For the full 2016 SoDA Report, Vol. 1, please visit www.sodareport.com

Modern MarketerKEY INSIGHT:

• Marketers have fully embraced digital innovation, changing expectations for ecosystem partners. Anticipate less evangelizing and more strategy, execution, and optimization.• Complexity is inherent to this world of full-on digital and marketers feel ready for it. But is their confidence borderline hubris? Marketers admit only meager skill gaps, a mismatch to today’s inconsistent marketing. • Innovation comes from ideas and ideas from people. While marketers offer attractive talent retention tools, they fall short on promoting programs that build diverse skills and supply challenging projects.

InnovationKEY INSIGHT:

• More marketers than ever perceive themselves to be innovative. Expect this self-reported identification — be it authentic or biased — to stress future expectations of agencies.

(continued below)

For the full 2016 SoDA Report, Vol. 1, please visit www.sodareport.com

The Age of Confidence

We’ve entered the age of confidence — at least if you ask a marketer about her own digital innovation efforts. In an incredible 12-percentage-point jump over 2015, 27% of our client respondents feel they are “very innovative” when it comes to digital marketing. This shift in improved self-perception indicates that clients are ready to tackle the complexities of modern marketing, to move from thinking about it to doing it. But caution remains: this year the biggest slice of respondents, 38%, feel only “somewhat innovative,” showing a balance of room to grow but also a sense of accomplishment. Respondents feeling “not very innovative” or “not at all innovative” dropped to a mere 8%, meaning fewer marketers than ever consider themselves neophytes.

We expect a ripple effect throughout the marketing ecosystem as brands push their own innovation boundaries. As our data shows, clients will look for new types of partners for innovation support, including a broader array of internal stakeholders, agencies, consultancies, and digital media partners. They will seek new services from existing partners. And most importantly, as they traverse the learning curve, clients will get smarter faster, making it harder for partners to stay the step ahead to bring — and charge for — unique value.

For the full 2016 SoDA Report, Vol. 1, please visit www.sodareport.com

Technology is Key to Evolving Brand Value…to a PointKEY INSIGHT:

• Marketers appreciate the value technology can bring to brand positioning, but they keep it in check — as the brand promise enabler, not a panacea.

While marketers are feeling more innovative, they’re stabilizing in terms of pursuing technology innovation as a part of their brand’s positioning. More than 70% of respondents believe that being perceived as an early adopter of technology is “key” or “important” to their brand positioning, a high percentage but a slight dip from 2015 levels.

Marketers recognize how technologies such as mobile and the internet of things are transforming the concept of brand value. Early adopters of technology seize the first mover advantage to retrofit existing services so that they are faster, easier, and more valuable: Think of an airline that lets you control your flight reservation via its brand app. But more exciting is the chance to rethink your brand’s positioning entirely, such as the sports gear brand whose social-enabled workout app connects enthusiasts for community-driven incentives. For marketers who can reimagine their brand beyond the product on the shelf, technology can help deliver a new brand experience.

For the full 2016 SoDA Report, Vol. 1, please visit www.sodareport.com

We believe the recent leveling off is a good thing: it indicates that marketers understand that technology is not a panacea. A brand’s value proposition starts with understanding the customer’s experience and the unique way(s) the brand can fit into that experience. Technology is the enabler, not the end in and of itself.

For the full 2016 SoDA Report, Vol. 1, please visit www.sodareport.com

Added Complexity is the Price of InnovationKEY INSIGHT:

• More marketers than ever expect complexity in their industry, and more than half think they are quite or very prepared for it

Even in their bullish state, marketers have no illusion that digital transformation is easy. Pacing with their appreciation of technology is the understanding of the complexity that comes with such a world. In just a year, the percentage of marketers who agree that the level of complexity facing their profession over the next five years will be “high” or “very high” jumped from 74% to 84%.

Expect this practical perspective to fuel adoption of new business models, ecosystems, and collaboration processes that cut out unnecessary layers and reimagine how work can get done for better, faster, more cost-effective results. Consider new entrant Tongal, which connects brands to a global community of filmmaking talent for a choice advantage when it comes to producing original video content. Marketers and partners who are open to these new workflows will have a strategic lead in converting complexity to opportunity.

(continued below)For the full 2016 SoDA Report, Vol. 1, please visit www.sodareport.com

The good news is that marketers feel more prepared than ever to handle such complexity. Fifty-six percent, over half of marketers polled, feel “quite” or “very prepared,” a jump of 26 percentage points over 2015. This increase further supports the notion that marketers are entering a new mental state in terms of handling digital and will seek different types of digital support compared to the past. Still, 39% are feeling “only somewhat prepared” or less, a group that is likely composed of late entrants into the digital foray.

We see further evidence of burgeoning confidence with digital given that 1 in 5 client respondents feel that their organization is “excellent” at forecasting and adapting to new technology trends, and 41% feel they are “good” at it. As marketers feel more prepared to handle the complexity of their profession, agencies are relieved of that responsibility. Agencies will have to become uber-innovation resources to exceed what clients are now able to do for themselves — a possible but difficult task that requires strategic investment. More importantly, agencies will need to double down on the marketing strategy, creative, and customer-centricity — yes, their original value drivers — that work with these new technology trends. These are areas that new entrants such as consultancies struggle to master.

For the full 2016 SoDA Report, Vol. 1, please visit www.sodareport.com

Minor Innovations Get You Only So FarKEY INSIGHT:

• Marketing progress starts with minor innovations, but respondents are split on whether minor or major innovations are sufficient for the future.

Today, 46% of our client respondents claim that their organization relies on “minor innovations” to innovate their products and services or to engage with customers in new ways, versus 29% of respondents citing “major innovations” for the same goal. The emphasis on minor change makes sense: Organizations are often willing to commit to roadmaps of incremental steps versus risking it all for a massive transformation.

But minor improvements get you only so far. When it comes to projecting the level of change needed to innovate projects and services or to engage with consumers in new ways in the next one to two years, our respondents bifurcated strongly. Thirty-eight percent believe that “minor innovations” are sufficient to survive and grow while a similar number (40%) say “major innovations” are needed for their organizations to stay alive and prosper.

This disagreement speaks to the fact that different businesses need different approaches. Companies burdened with legacy culture, inefficient processes, and

For the full 2016 SoDA Report, Vol. 1, please visit www.sodareport.com

antiquated technologies will need radical change to survive and grow. A century-old insurance firm with risk-avoidance baked into its very DNA will struggle to fully embrace the agile “fail fast, fail often” mentality that is pervasive in the start-up community. When the low hanging fruit is gone, brands will have to make difficult decisions regarding change — or be forced into such changes by the market.

For the full 2016 SoDA Report, Vol. 1, please visit www.sodareport.com

The Skill Gap Mirage: Digital Confidence Risks Self-DeceptionKEY INSIGHT:

• Marketers acknowledge few internal skill gaps — a questionable mindset given today’s pace of constant change.

But where is the most improvement needed? Again, marketers’ confidence is at an all-time high, with more than 50% stating that they are “Experienced” or an “Expert” across almost every single digital skill set included in the study, with the highest being “use of data to drive digital marketing effectiveness”. The one area showing some self-doubt: place-based digital experiences. Uncertainty here makes sense given that this skill set brings together diverse, cutting-edge disciplines including mobile, design, engineering, architecture, and real-time data.

Q. (Clients) Where are the most significant skill gaps in your organization with respect to digital marketing?

Our respondents chose “User Experience” as one of the two areas where they are most likely to be experiencing significant gaps with respect to digital marketing. More than one in five respondents claimed talent gaps in this area. Executive management was the only other area where respondents indicated such a major gap in digital marketing preparedness. But this perceived deficiency is still relatively low. In fact, more than 30% of respondents said they had no gaps at all in any of the categories about which we inquired. The concession of only minor gaps across the board

For the full 2016 SoDA Report, Vol. 1, please visit www.sodareport.com

(ranging from 30% to 40% of respondents) further reflects respondents’ confidence in their digital capabilities.

Given the self-reported nature of this data and the inconsistent brand experiences we have all seen as consumers, we have to question whether marketers’ confidence has ventured into hubris. Is it truly possible that a brand would have no gap at all in content marketing? Marketers will be best served by taking a hard look at internal processes, organization, and technology to assess their true skills gaps and avoid being blindsided by their own skill set mirage.

For the full 2016 SoDA Report, Vol. 1, please visit www.sodareport.com

Innovation Relies on Talent and Talent Relies on InspirationKEY INSIGHT:

• Marketers offer a variety of talent retention tools but miss the mark on options that bring skill-building opportunities.

Q. (Clients) What does your organization do to retain talent?

Innovation relies on getting and nurturing great ideas. Ideas come from people. To truly be innovative, marketers must find, build, and sustain top-notch teams in a highly competitive talent environment. Marketers have been incredibly bullish on their own innovation profile, skills sets, and learning agenda across this survey. But where the equation does not add up is when we asked about talent retention. While marketers provide a broad array of retention tools, their focus is light on skill-building initiatives such as rotation programs and participation in innovation labs or hack-a-thons. After sabbaticals, these two employee benefits showed the lowest incidence rates at 14% and 16%, respectively. While flexible work schedules (47%) and financial incentives (42%) are key, modern managers must inspire the modern workforce with cutting-edge projects that incite problem solving and a sense of accomplishment if they want to keep the best talent.

For the full 2016 SoDA Report, Vol. 1, please visit www.sodareport.com

Clients Increasingly Bullish on Digital Despite Modest Global Growth

The global economy is expected to grow a modest 3.2% in 2016, essentially on par with 2015 and down 0.2% from the January 2016 forecast (Source: IMF, April 2016). However, growth prospects are expected to improve in 2017 and beyond, bolstered primarily by emerging markets. Specifically, the projected recovery in 2017 is predicated on stronger growth in countries contending with harsh economic conditions in 2015-16 (including Russia, Brazil, and some countries in Latin America and the Middle East). The full IMF report is available here.

Despite lackluster growth in many parts of the world (and a contraction of economic output in major markets such as Russia and Brazil), 55% of client-side respondents expect to increase their spend in some way in 2016, either by an increase in overall marketing dollars or an increase in the digital allocation of a steady overall budget. As Melissa Parrish points out in her introduction to this year’s study, the eight-point rise year-over-year is arguably due to the fact that clients’ expectations are being buoyed by the strong performance of digital programs, rather than being driven by excitement around emerging tech as we’ve seen in previous years. While we expect new technologies such as VR to drive increased spending on digital

For the full 2016 SoDA Report, Vol. 1, please visit www.sodareport.com

in the medium-to-long term (particularly as the requisite hardware becomes more widely available and affordable), large majorities of clients are planning to increase their spending in 2016 in more foundational areas, such as:

• Digital experiences (e.g., websites, mobile web) (82%)• Content development (76%)• Digital products (e.g., non-marketing-related platforms, applications, tools

and services) (71%)

A smaller, albeit still sizeable, share of clients is increasing spending on app development. As responsive website technologies continue to advance, more and more clients and agency partners are moving away from OS-specific development. Globally, 55% of respondents indicated they were either 1) reallocating more budget into digital from their existing marketing spend or 2) increasing digital budgets while also increasing their overall marketing spend. That’s up significantly from 47% in 2015. In the 2015 study, there were larger variances between regions, with a far lower percentage of clients in Europe, for example, projecting increased spending on digital. That has changed in 2016 as the European economic outlook has improved, albeit to a limited degree and not unilaterally across all markets. In the 2016 study, 50% of respondents from Europe expect to increase digital spending (with 27% increasing the share allocated to digital without increasing its overall marketing spend, and 23% increasing both the digital and overall spend). By contrast, only 28% of clients expected to increase digital spending in last year’s study. Clients in the APAC region and North America are more in line with the global average when it comes to projected spending increases on digital in 2016 (54% and 55% respectively).

For the full 2016 SoDA Report, Vol. 1, please visit www.sodareport.com

Clients Are Also Prioritizing Content, Digital Products, and Data Science

Increased spending on digital is not limited to campaign buys. In fact, budgets are growing most dramatically for insight-driven content strategy and development that turns audiences into brand advocates. Digital products outside of the marketing realm (including platforms, applications, tools, and services) ranked second in 2016. Agencies and software development companies who have expertise in digital product creation (both bringing their own IP to market as well as developing digital products on behalf of clients) clearly stand to benefit from the growing budget priority among clients’ organizations. Social and email marketing rounded out the top five. Digital areas where clients indicated lower spending priorities included: app development, user experience testing, standalone strategy, video, display media, and mobile.

For the full 2016 SoDA Report, Vol. 1, please visit www.sodareport.com

KEY INSIGHT: • Agencies drastically shift their training strategies — some shortsightedly cutting education overall, others switching to more scalable channels, but do near-term gains sacrifice long-term skill development?• Agencies and clients majorly disagree on client skill gaps, stressing the evolving relationship. • Talent wars worsen as clients join the fray, looking to staff in-house initiatives.

Staff Training

While Offering Less Training Overall, Agencies Diversify Educational Methods

Between 2015 and 2016, the percentage of agencies who do not provide any training to their staff almost tripled, growing from 5% to 14%. With shrinking margins

Talent and Advocacy

For the full 2016 SoDA Report, Vol. 1, please visit www.sodareport.com

pervasive in the industry, it’s not surprising to see agencies cut non-client-facing investments. For the agencies who continue to provide training, delivery methods have diversified drastically in 2016, with an emphasis on lower cost channels. Formal corporate training grew incrementally, increasing six percentage points, while scalable formats increased significantly, particularly webinars and conferences.

Despite the drop in training, many respondents — on both the agency and client sides — listed education as a primary issue that requires industry advocacy. One marketer requested “even more online webinars,” while another called out the “importance of investing in staff recruitment and retention.”

Agencies face increasing uncertainty as clients move capabilities in-house. While education may not seem like a top priority, squeezing investments in training saves short-term budgets at the expense of long-term capability growth. Clients and agencies alike are facing a talent war — often against each other as clients poach agency talent for in-house staffing. The best talent will go where they can learn the most; cutting or diluting training signals the de-prioritization of talent development and risks a talent drought.

For the full 2016 SoDA Report, Vol. 1, please visit www.sodareport.com

Talent GapsQ. (Agencies) Where are the most significant gaps in talent on the client side with respect to digital marketing? Q. (Clients) Where are the most significant gaps in talent in your organization with respect to digital marketing?

Clients are feeling increasingly confident about the talent they’ve brought on and fostered in recent years. The percentage of clients saying they have no talent gap at all increased year-over-year across every single category, most notably in technology, research, and brand management. Agencies very rarely agreed with clients on this, indicating in all categories that clients’ major talent gaps have grown, with the lone exception of eCommerce. This divergence represents a critical pain point in agency-client relationships given that agencies are often called in to supplement client skill gaps.

The biggest disparity: user experience (UX). For the third consecutive year, agency respondents identified UX as the most significant talent gap on the client side at 52%, a ten-point gain over last year. As noted in the Modern Marketer section, clients recognize a gap in user experience as well, a concern given User Experience’s critical contribution to manifesting brand promises across all channels. Although not everyone agrees — one agency respondent called UX “just another bandwagon to hop on.”

Clients and agencies also disagree when it comes to clients’ technology talent gap.

For the full 2016 SoDA Report, Vol. 1, please visit www.sodareport.com

While 41% of agencies believe there is a major talent gap on the client side, the same percentage of clients report having no talent gap at all. The same pattern can be seen in research, where 35% of agencies think there is a major gap on the client side and clients report no gap.

For the full 2016 SoDA Report, Vol. 1, please visit www.sodareport.com

Client EducationTrends from 2015 Continue into 2016

Key:Thought Leadership = We develop and deliver thought leadership, research, and analysis as part of our planning or client service offering.Playbooks = It is a standard practice to create “playbooks” and other guidelines that help our clients effectively operate the campaigns, content, and platforms we create.Only When Asked = We offer educational or training services only when clients ask for briefings on a topic or help building a capability in-house.

In 2016, agency-to-client education patterns stayed mostly the same from previous years. Thought leadership embedded as part of agencies’ planning or client service offerings continues to grow, a promising outlook to help bridge some of the talent gaps highlighted earlier. A higher percentage of agencies also provide Playbooks than in previous years, enabling clients to execute work on their own.

Consultants and agency respondents pointed to significant areas where they see client education lagging, in contrast to the confidence portrayed by clients in the Modern Marketer section. One consultant wrote, “I don’t feel clients fully understand how to navigate the digital marketplace.” She continues, “Social channels are quickly changing and marketers today have a broad understanding, but tactically, they can’t keep up with changes.”

Many respondents also focused on clients’ understanding (or lack thereof) of digital: from the basic (“lack of awareness of the benefits of digital”) to the tactical (“integrating digital across silos”) and the strategic (“developing a digital-first mind set”). While clients report feeling confident and innovative, their agencies paint a very different picture — causing further strain in the agency-client relationship.

For the full 2016 SoDA Report, Vol. 1, please visit www.sodareport.com

While agencies’ increasing use of playbooks indicates they are pushing more guides and how-tos to their clients, it won’t be enough to fill the gaps identified by agency respondents. Understanding the benefits of digital, applying digital across teams, and building a comprehensive strategy all require buy-in far beyond the marketing team or owner of the client-agency relationship. Agencies would be well served to consider other means, such as hands-on workshops or thought leadership engagements to deliver value to clients. In the age of personalization, agencies should follow suit and aim to be a partner in breaking down marketing silos and encouraging cross-team collaboration. One respondent wrote, “There’s still a huge need for education in the C-Suite. So many companies don’t understand the impact that great digital marketing can and should have on their business.”

For the full 2016 SoDA Report, Vol. 1, please visit www.sodareport.com