the royal bank of scotland group plc annual report · pdf filethe royal bank of scotland group...

TRANSCRIPT

THE ROYAL BANK OF SCOTLAND GROUP plc

ANNUAL REPORT ON FORM 20-FFOR THE YEAR ENDED SEPTEMBER 30, 1999

CONTENTS

Item Item Caption Page

Presentation of Information ............................................................................................ 2

Exchange Rates ............................................................................................................ 3

1 Description of Business ................................................................................................. 4

Description of Assets and Liabilities ............................................................................ 10

Competition ............................................................................................................ 23

Monetary Policy ...................................................................................................... 23

Supervision and Regulation........................................................................................ 25

2 Description of Property.................................................................................................. 27

3 Legal Proceedings......................................................................................................... 27

4 Control of Registrant ..................................................................................................... 27

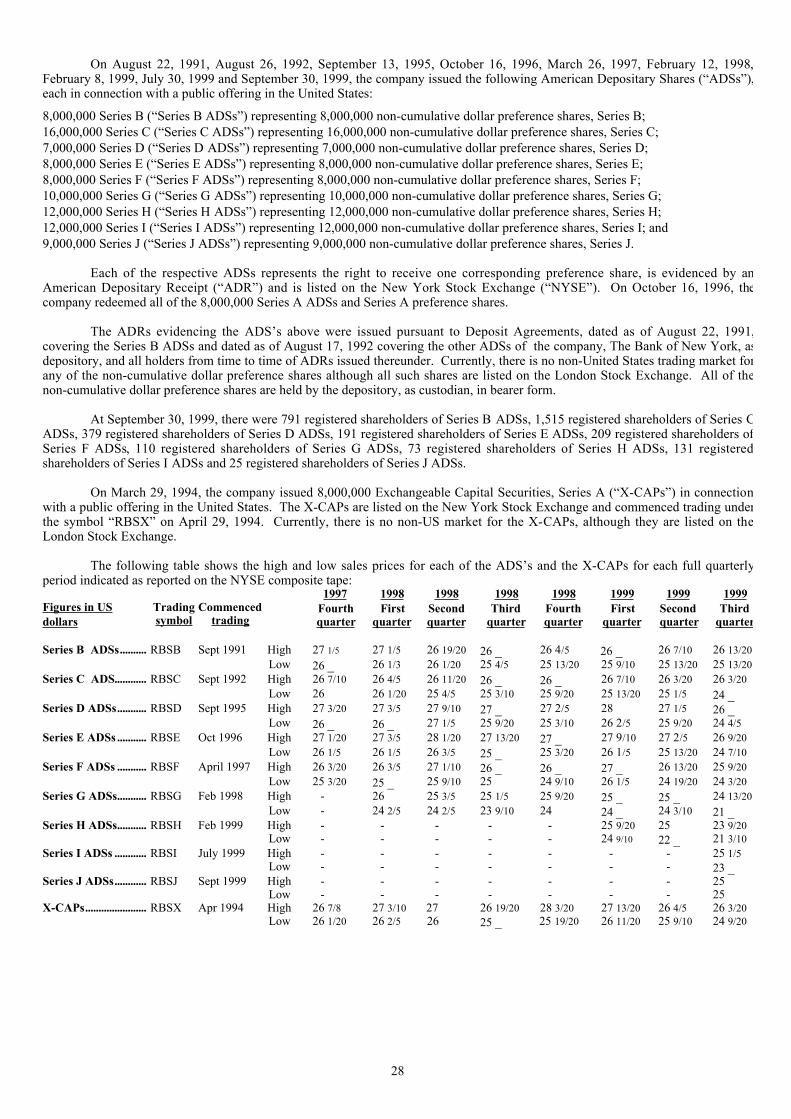

5 Nature of Trading Market............................................................................................... 28

6 Exchange Controls and Other Limitations Affecting Security Holders..................................... 29

7 Taxation ..................................................................................................................... 30

8 Selected Consolidated Financial Data ............................................................................... 34

9 ManagementÕs Discussion and Analysis of Financial Condition and Results of Operations.......... 37

Divisional Analysis .................................................................................................. 38

Results of Operations of the Group.............................................................................. 48

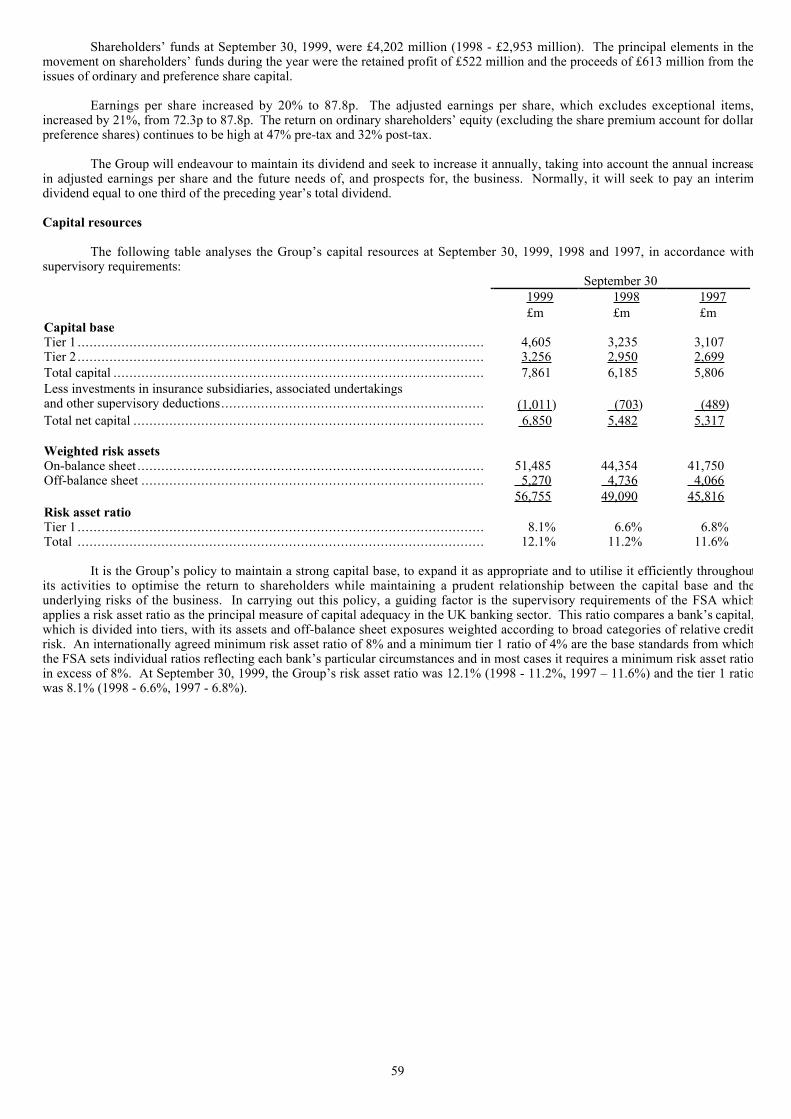

Capital Resources .................................................................................................... 59

Quantitative and Qualitative Disclosures about Market Risk............................................. 60

10,11,12 Directors and Officers of Registrant; Remuneration of Directors and Officers; Options to

Purchase Securities from Registrant or Subsidiaries ........................................................ 66

13 Interest of Management in Certain Transactions.................................................................. 72

14 Description of Securities to be Registered.......................................................................... *

15 Defaults upon Senior Securities ....................................................................................... *

16 Changes in Securities and Changes in Security for Registered Securities ................................. *

17 Financial Statements ..................................................................................................... *

18 Financial Statements ..................................................................................................... 73

19 Exhibits ...................................................................................................................... *

Signatures ................................................................................................................... 143

* Not applicable or the answer is in the negative.

2

PRESENTATION OF INFORMATION

In this Report, ÒcompanyÓ means The Royal Bank of Scotland Group plc and ÒGroupÓ means the company and itssubsidiaries.

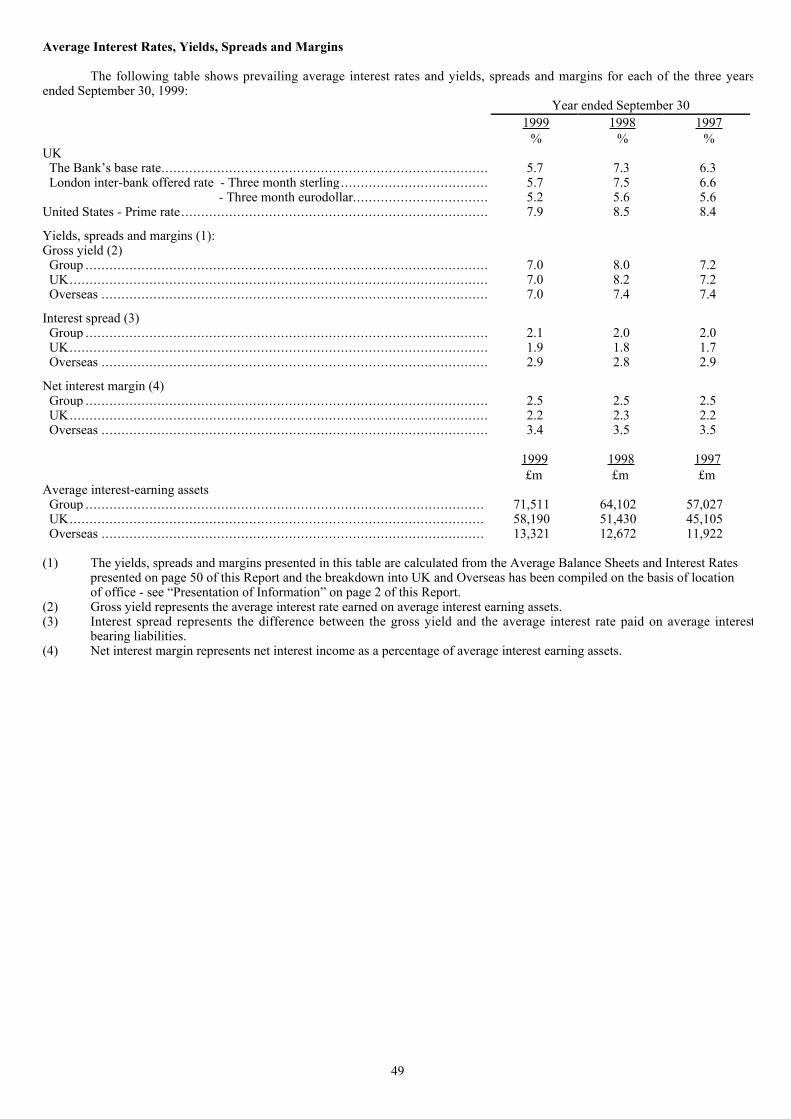

Certain financial and statistical information in this Report is presented separately for domestic and foreign activities. Theterm ÒForeign activitiesÓ refers to transactions in which the debtor or customer is domiciled outside the United Kingdom (ÒUKÓ).ÒForeign activitiesÓ are further divided into ÒForeign-UK basedÓ, ÒContinental EuropeÓ, ÒUnited StatesÓ and ÒRest of the WorldÓ.The term ÒForeign-UK basedÓ refers to those Foreign activities conducted by offices in the UK. Foreign activities allocated toÒContinental EuropeÓ, ÒUnited StatesÓ or ÒRest of the WorldÓ involve transactions in which the customer is domiciled in thecountries included in these respective categories. For purposes of such financial and statistical information, the UK includes theChannel Islands and the Isle of Man. The separate presentation of domestic and foreign activities reflects allocations of loan capitalinterest, certain centralised expenditure and taxes that in some cases are necessarily subjective and to an extent arbitrary.

The breakdown into UK and overseas sectors contained in the Average Interest Rates, Yields, Spreads and Marginspresented on page 49 of this Report and the Average Balance Sheets and tables of Interest Rates presented on page 50 of this Reporthave been compiled on the basis of location of office. We believe that the presentation of the Average Balance Sheets and Inte restRates on such a basis provides more useful information on the yields, spreads and margins of the GroupÕs activities in the UK andoverseas. Presenting the Average Balance Sheets and Interest Rates on the basis of the domestic and foreign activities analysis usedelsewhere in this Report would not provide useful information because the average assets and liabilities arising from ÒForeign - UKbasedÓ activities do not match. In its UK branch network, the Bank attracts more deposits from customers domiciled outside the UKthan it lends to such customers; therefore, the interest spreads and margins obtained from an analysis into domestic and foreignwould be distorted to the extent of this imbalance. Ignoring the effect of this distortion would result in materially different yields,spreads and margins for the foreign sector.

Where average balances are shown in this Report, cleared balances are used in the case of The Royal Bank of Scotland plc(the ÒBankÓ), the UK clearing bank subsidiary of the company. Cheques deposited in an account by a customer which are awaitingclearance are therefore not included in these balances. In addition, where arrangements exist with a customer under which loans toand deposits from the customer are netted for the purpose of determining interest due to or from the customer, such loans anddeposits are similarly netted for the purpose of computing average balances. As a result, the average balances shown are lower thanthey would be if the book values of customersÕ accounts were used. Average balances, where used, are based upon daily averagesfor the Bank and Citizens Financial Group (ÒCFGÓ) and averages not less frequent than monthly for other Group operations. Allsuch balances are considered to be fairly representative of the operations of the Group.

The Group prepares its Consolidated Financial Statements on the basis of a fiscal year beginning on October 1 and endingon September 30 of the following year. References to a year in this Report are, unless otherwise indicated, references to the GroupÕsfiscal year ending on September 30 of such year.

The Group publishes its Consolidated Financial Statements in pounds sterling (Ò£Ó or ÒsterlingÓ). In this Report, referencesto ÒUS dollarsÓ, Ò$Ó or ÒcentsÓ are to United States currency and references to Òpounds sterlingÓ, ÒsterlingÓ, Ò£Ó, ÒpenceÓ or ÒpÓ areto UK currency.

Forward-looking statements

Certain statements in this document may be considered to be Òforward-looking statementsÓ as that term is defined in theUnited States Private Securities Litigation Reform Act of 1995, such as statements that include the words ÒexpectÓ, ÒestimateÓ,ÒprojectÓ, ÒanticipateÓ, ÒshouldÓ, ÒintendÓ, ÒprobabilityÓ, ÒriskÓ, ÒVaRÓ, ÒtargetÓ, ÒgoalÓ, ÒobjectiveÓ and similar expressions orvariations on such expressions. In particular, this document includes forward-looking statements relating, but not limited, to theGroupÕs potential exposures to various types of market risks, such as interest rate risk, foreign exchange rate risk and commodity andequity price risk. See ÒLiquidity riskÓ, ÒMarket riskÓ, ÒValue at RiskÓ elsewhere in this document. Such statements are subject tocertain risks and uncertainties. For example, certain of the market risk disclosures are dependent on choices about key modelcharacteristics and assumptions and are subject to various limitations. See ÒMarket RiskÓ and ÒValue at RiskÓ. By their nature,certain of the market risk disclosures are only estimates and could be materially different from what actually occurs in the future. Asa result, actual future gains and losses could materially differ from those that have been estimated. Other factors that could causeactual results to differ materially from those estimated by the forward-looking statements contained in this document include, but arenot limited to: general economic conditions in the UK and in other countries in which the Group has significant business activities orinvestments, including the United States and Spain; the monetary and interest rate policies of the Bank of England, the Board ofGovernors of the Federal Reserve System and other G-7 central banks; inflation; deflation; unanticipated turbulence in interest rates,foreign currency exchange rates, commodity prices and equity prices; the effects of non-linear market behaviour that cannot becaptured by linear statistical models such as the Value at Risk model used by the Group; changes in UK and foreign laws,regulations and taxes; changes in competition and pricing environments; natural disasters; the inability to hedge certain riskseconomically; the adequacy of loss reserves; acquisitions or restructurings; technological changes; changes in consumer spendingand saving habits; and the success of the Group in managing the risks involved in the foregoing.

The forward-looking statements contained in this document speak only as of the date of this report, and the Group does notundertake to update any forward-looking statement to reflect events or circumstances after the date hereof or to reflect the occurrenceof unanticipated events.

EXCHANGE RATES

3

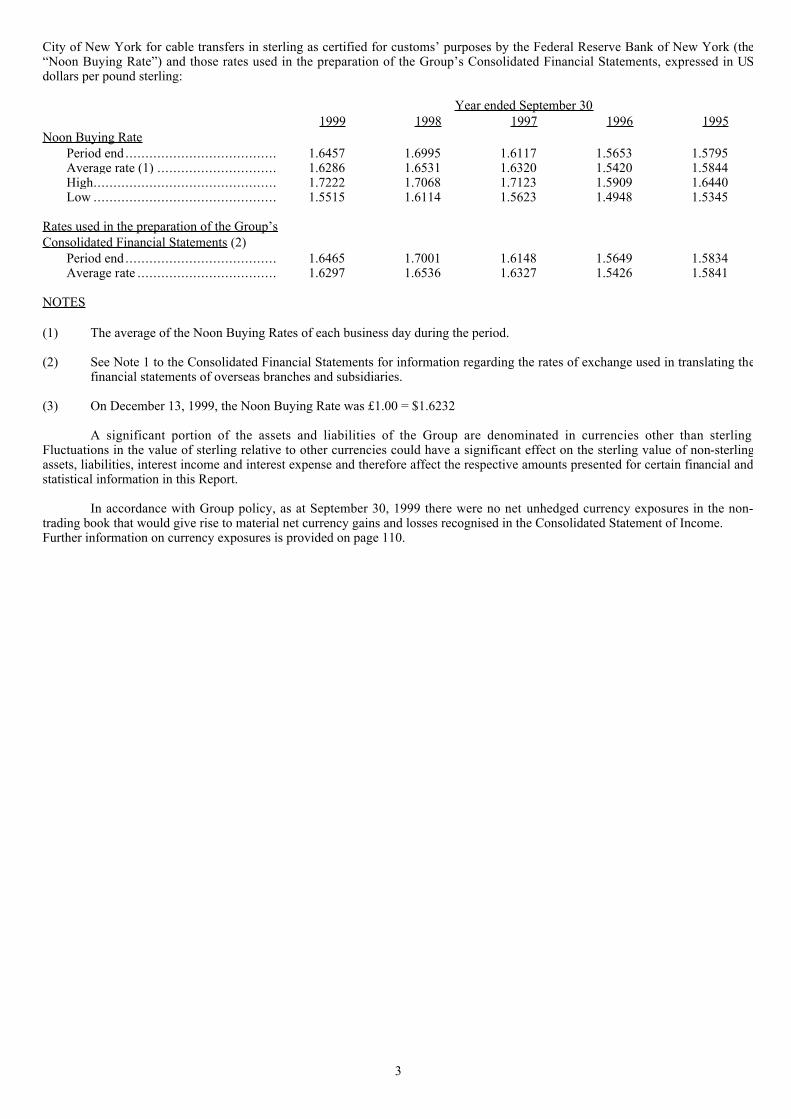

City of New York for cable transfers in sterling as certified for customsÕ purposes by the Federal Reserve Bank of New York (theÒNoon Buying RateÓ) and those rates used in the preparation of the GroupÕs Consolidated Financial Statements, expressed in USdollars per pound sterling:

Year ended September 30 1999 1998 1997 1996 1995

Noon Buying RatePeriod end ...................................... 1.6457 1.6995 1.6117 1.5653 1.5795Average rate (1) .............................. 1.6286 1.6531 1.6320 1.5420 1.5844High.............................................. 1.7222 1.7068 1.7123 1.5909 1.6440Low .............................................. 1.5515 1.6114 1.5623 1.4948 1.5345

Rates used in the preparation of the GroupÕs Consolidated Financial Statements (2)

Period end ...................................... 1.6465 1.7001 1.6148 1.5649 1.5834Average rate ................................... 1.6297 1.6536 1.6327 1.5426 1.5841

NOTES

(1) The average of the Noon Buying Rates of each business day during the period.

(2) See Note 1 to the Consolidated Financial Statements for information regarding the rates of exchange used in translating thefinancial statements of overseas branches and subsidiaries.

(3) On December 13, 1999, the Noon Buying Rate was £1.00 = $1.6232

A significant portion of the assets and liabilities of the Group are denominated in currencies other than sterlingFluctuations in the value of sterling relative to other currencies could have a significant effect on the sterling value of non-sterlingassets, liabilities, interest income and interest expense and therefore affect the respective amounts presented for certain financial andstatistical information in this Report.

In accordance with Group policy, as at September 30, 1999 there were no net unhedged currency exposures in the non-trading book that would give rise to material net currency gains and losses recognised in the Consolidated Statement of Income.Further information on currency exposures is provided on page 110.

4

ITEMÊ1.ÊDESCRIPTIONÊOFÊBUSINESS

Introduction

The Group is a diversified financial services group engaged in a wide range of banking, financial and finance-relatedactivities in the UK and overseas. The GroupÕs operations are principally centered in the UK. At and for the year ended September30, 1999, based on domicile of customer, no country outside the UK or the United States accounted for more than 10% of total assetsor net income available for ordinary shares of the Group - see Note 50 to the Consolidated Financial Statements. At September 30,1999, the Group had total assets of £88.9 billion (1998 - £79.7 billion), total deposits of £61.6 billion (1998 - £55.1 billion) andshareholdersÕ equity of £4,202 million (1998 - £2,953 million). At September 30, 1999, the Group employed 32,670 staff (1998 Ð31,680).

The Bank is the companyÕs principal operating subsidiary and it controls, directs and promotes the operations of thesubsidiary companies. The Bank is a major UK clearing bank whose predecessors date back to 1727. At September 30, 1999, theBank had 634 branches in the UK. The Bank was created by the merger in 1985 of the former The Royal Bank of Scotland plc, thelargest of the Scottish clearing banks, and Williams & GlynÕs Bank plc, a wholly-owned English clearing bank subsidiary of thecompany.

The Group is organised by division, each focusing on a key market segment. The UK Bank provides banking and otherrelated financial services to individuals and small to medium-sized corporate clients through a UK-wide branch network, certaincentralised banking services and various subsidiary companies. It also provides banking and other related financial services to largercorporate and institutional clients in the UK and internationally. Angel Trains acquires rolling stock from manufacturers and leasesit to train operating companies. RBS Cards provides credit and debit card services and holds credit card receivables. The RoyalBank of Scotland International Limited provides offshore banking services to local and international customers. Investor Servicesprovided investment administration solutions to institutional investors until the date of its sale on October 31, 1999. Direct LineInsurance principally provides automobile and household insurance. CFG constitutes the GroupÕs North American division. Thevarious new businesses started by the Group in recent years are grouped together in a separate classification, New Retail FinancialServices Businesses. Support is provided by central functions dealing with finance, strategy, legal and regulatory matters andexternal affairs.

The UK Bank

The operations of the UK Bank comprise three divisions, Retail Banking, Corporate and Institutional Banking and Serviceand Operations which are described below.

Retail Banking

Through its UK branch network and certain centralised banking services, Retail Banking provides a wide range of banking,insurance and other related financial services to individuals and to small business clients. It also operates direct banking telephoneservices and has complementary subsidiary businesses covering life assurance and pensions, and private banking.

In the personal banking market, Retail Banking offers money transmission, savings and loan facilities (comprisingmortgages, consumer loans and overdraft facilities). It also acts as a point of sale for credit cards on behalf of RBS Cards. In itssmall business banking market, Retail Banking provides a range of services which includes money transmission and cashmanagement, short, medium and long-term finance and retail and wholesale deposit taking products. Through the operations ofRoyal Scottish Assurance (ÒRSAÓ), Retail Banking provides a wide range of life assurance, pension and unit linked investmen tproducts, together with discretionary portfolio management.

Private Banking

Adam & Company PLC, which is a wholly owned subsidiary of the Bank, provides private banking services in Scotlandand England.

RSA

RSA was established as a joint venture to offer a wide range of life, pensions and investment products through the BankÕsUK branch network. Initially, the Bank held an 80% shareholding in RSA. In May 1997, the Bank acquired the remaining 20% ofRSA from Scottish Equitable plc and then later that month sold a 30% interest in RSA to Scottish Widows Fund and Life AssuranceSociety (ÒScottish WidowsÓ), resulting in a 70% shareholding held by the Bank. Scottish Widows provides administration,processing, investment management and other services to RSA. On November 26, 1999, it was announced that the Group and CGUplc had entered into a memorandum of understanding for the provision of life, pensions and investment products to the RBS Group.CGU has agreed to acquire a 50% interest in RSA and will replace Scottish Widows in this venture.

5

Corporate and Institutional Banking

Corporate and Institutional Banking provides commercial banking and other financial services to the BankÕs corporate andinstitutional clients selling a wide range of products to meet their financial needs. It consists of the following businesses:

Corporate and Commercial Banking

Corporate and Commercial Banking focuses on the needs of the BankÕs corporate customers and financial institutions. Dueto their size and complexity, these customers demand a wide range of corporate banking skills which can best be provided by aseparate dedicated business. Corporate and Commercial Banking provides a number of products and services including clearing,money transmission, syndicated lending and corporate finance. The Bank is committed to the concept of Òrelationship bankingÓwhere each customer has one principal point of contact within the Bank. To achieve this, Corporate and Commercial Banking hassmall teams of managers in each of the BankÕs major centres (London, Edinburgh and Manchester) which are devoted exclusively tostrengthening and deepening the BankÕs involvement with these customers.

Treasury and Capital Markets

The BankÕs Treasury and Capital Markets operation, based in London, Edinburgh and Manchester, is responsible for thefunding and liquidity position of the Bank and for managing the BankÕs foreign exchange risk. Treasury and Capital Markets alsooffers a wide product range to an expanding customer base serviced from dealing rooms in London, Edinburgh and Manchester.Dealing operations are also located in New York and Singapore. The Bank operates in foreign exchange markets, sterling marketsand the Eurocurrency deposit markets. The London operation controls all positions, both in the money markets and foreignexchange markets, within constraints established either by the applicable regulatory authorities or the BankÕs senior management asappropriate. Treasury and Capital Markets participates in the derivative markets to meet the financing needs of customers, to reducethe BankÕs exposure to fluctuations in exchange and interest rates and as an integral part of its trading activities. SeeÒManagementÕs Discussion and Analysis of Financial Condition and Results of Operations - Risk ManagementÓ.

Investment Finance

The principal business units within Investment Finance are Leveraged Finance and Royal Bank Development CapitalLimited.

Leveraged Finance has established itself as one of the leading debt providers in the UK market. It has capabilities inarranging funds for acquisitions, for management buy-ins and buy-outs and for other situations requiring the arrangement ofleveraged debt facilities. During 1998 RBS Mezzanine Limited, a mezzanine capital business, was launched and is already provingprofitable and, during 1999, Leveraged Finance expanded into Europe, opening offices in Paris and Frankfurt. In July 1999, theGroup formed a 50% joint venture company, Caledonian Capital Limited, with the Bank of Scotland to provide a single independentEuropean underwriting capability for high value senior debt financing to leveraged buy-out transactions.

Royal Bank Development Capital Limited provides equity finance for companies that have little or no access to capitalmarkets. The companyÕs activities cover start-ups, development capital situations, management buy-outs and buy-ins and sharerestructurings.

Structured Finance

The constituent areas of this business are loan syndications, leasing, project and export finance, shipping, structured tradefinance and structured asset finance. It also has a specialist team to provide finance under the UK GovernmentÕs Private FinanceInitiative.

Royal Bank Leasing Limited provides asset based finance for large capital equipment projects. Over the past few years, ithas concentrated on developing its reputation for providing individual financing solutions. Royal Bank Leasing Limited generatesnew business from its offices in London, Glasgow and its head office in Cheltenham.

The Shipping unit provides mortgage finance together with corporate and personal banking services to the worldÕs majorshipping companies and high net worth individuals connected with the sector, from its two operational centres in London andPiraeus.

Loan syndications within the Bank are managed by a dedicated team which is involved in the arrangement, structuring andunderwriting of major corporate facilities and is acknowledged as a top ranking arranger/co-arranger of UK corporate debttransactions.

The project and export finance group is active in a wide range of UK based and international project finance businesses andhas a dedicated export credit team. A global mandate is pursued through its representation in London, Edinburgh, Singapore,Sydney and New York.

UK and International Banking Services

UK and International Banking Services is the BankÕs domestic and international payments and cash management business.

Service and Operations

6

Service and Operations provides banking services, property and facilities management and technology for the UK Bank. Italso provides support to the UK Bank through a network of Service Centres, Cash Centres and the Mortgage Centre in Greenock,Scotland.

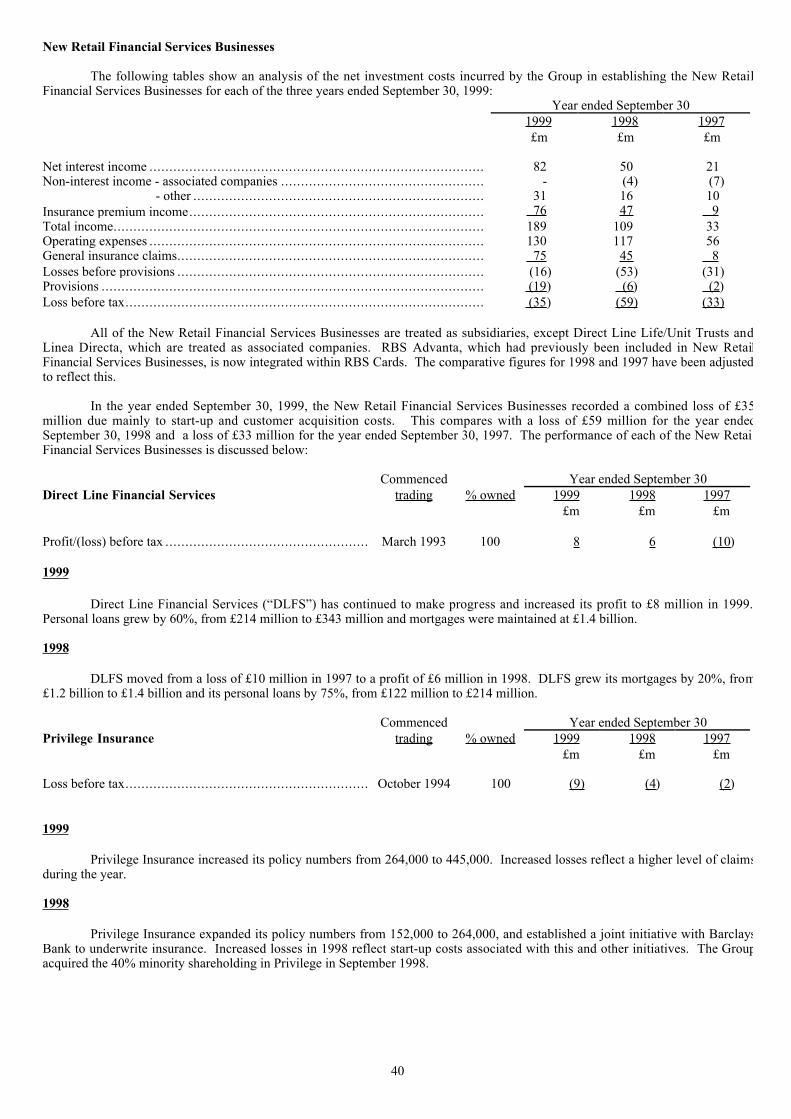

New Retail Financial Services Businesses

In recent years, the Group has established various new retail businesses to extend and complement its existing financialservices to customers.

Direct Line Financial Services Limited was established in 1993 to provide personal financial services using a telephonebased delivery system. The company offers mortgages, personal loans and savings products and recently launched its own low costcredit card. At September 30, 1999, the company had over 130,000 accounts.

Privilege Insurance was established in 1994 and provides non-standard motor insurance through a telephone based deliverysystem and motor and household insurance through affinity schemes with third parties. At September 30, 1999, the company had445,000 policies in-force.

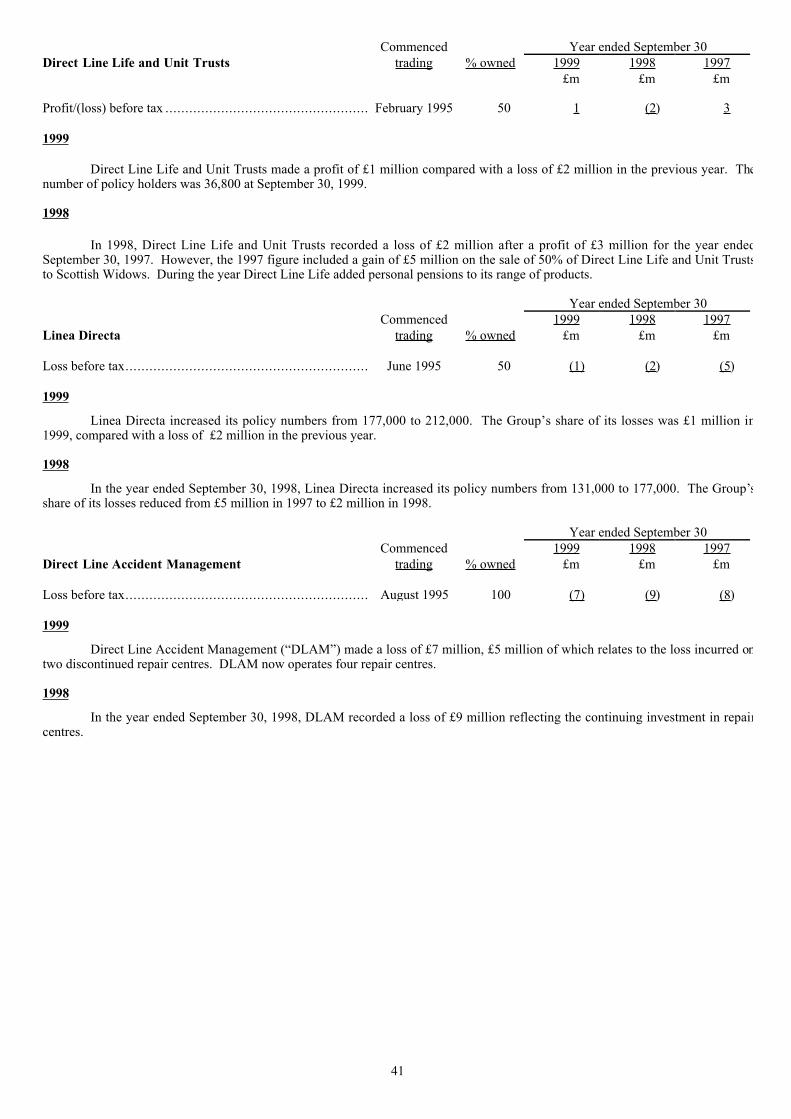

In 1994, Direct Line Group Limited entered into a joint venture agreement with Bank Inter S.A., a Spanish bank, to set up adirect marketing automobile insurance operation in Spain. The joint venture company, Linea Directa Aseguradora S.A., is 50%owned by Direct Line Group Limited. At September 30, 1999, there were 212,000 in-force policies (September 1998 Ð 177,000).

In July 1997, a partnership between Direct Line and Scottish Widows resulted in the formation of a 50% joint venture.Through two subsidiary companies of Direct Line Life Holdings Ltd, the joint venture holding company, life insurance, personalpensions, Individual Savings Accounts and unit trust investment products are offered directly to the public by telephone.

Direct Line Accident Management had four accident repair centres operational at September 30, 1999, having closed twocentres during the year.

In July 1997, the Group established a joint venture in financial services with Tesco PLC, one of the UKÕs leadingsupermarket groups. The new venture, Tesco Personal Finance Group Limited, allies the strengths of the Group with TescoÕs largecustomer base.

In October 1997, the Group established a joint venture with Virgin Direct, Virgin Direct Personal Finance Limited. A 24hour telephone based bank account, with a mortgage element, the Virgin One Account, was launched to VirginÕs own customers inOctober 1997 and more broadly in May 1998.

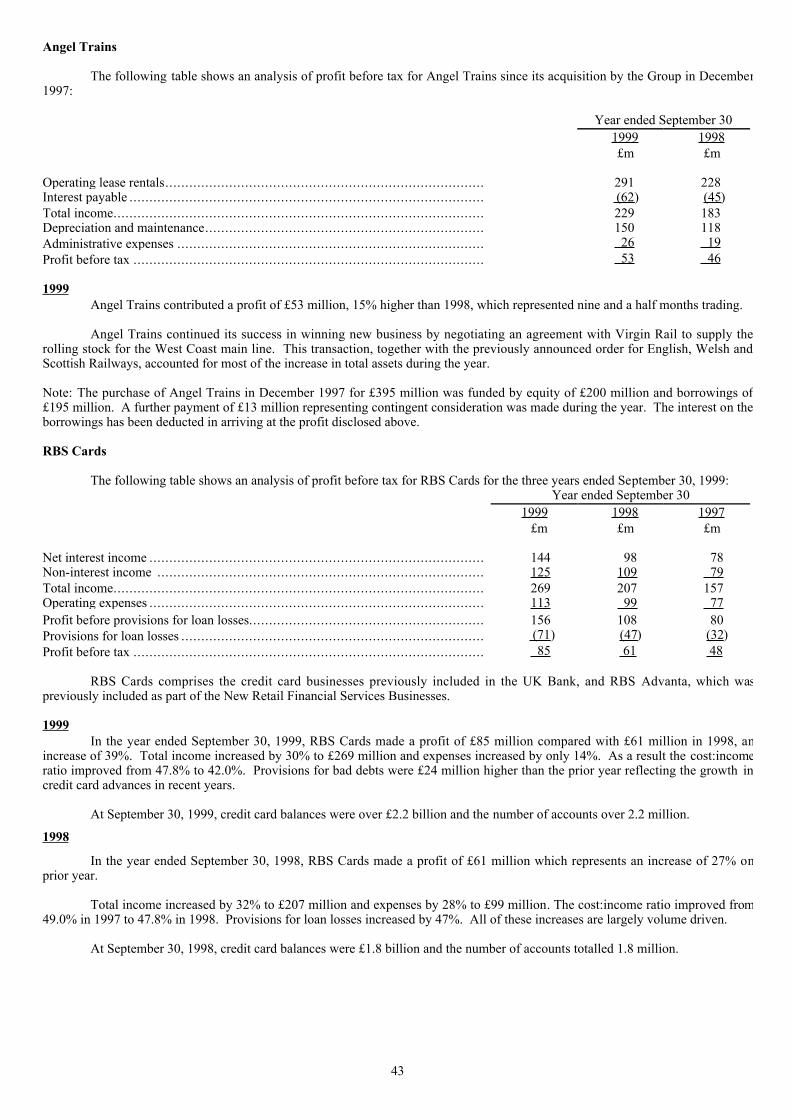

Angel Trains

Angel Trains was acquired by the company in December 1997. It is one of the three rolling stock leasing companies in theUK which were privatised in 1996. Angel Trains acquires rolling stock from manufacturers, leases the rolling stock to train operatingcompanies and sub-contracts the maintenance of the rolling stock.

During 1999, Angel Trains won the contract to invest in 53 new high-tech ÔAdvanced Tilting TrainsÕ to be leased to VirginRail Group for use on the West Coast main line.

RBS Cards

RBS Cards provides credit and debit card services including its own low cost, no fee MasterCard and Visa credit cards andthe BankÕs multi-functional Highline debit cards, which can be used in every ATM in the UK. These debit cards incorporate theCirrus and Maestro facilities which provide the ability to use both ATMÕs and debit card facilities worldwide.

The BankÕs card services business has expanded in recent years with a series of joint ventures. In 1997, a new company,RBS Cards Limited, was created to lead the development of new products. Its first launch, the AU Gold MasterCard, offers lowrates of interest to its target market of low-risk customers.

In May 1995, a joint venture, RBS Advanta, was entered into with the Advanta Corporation of Pennsylvania (ÒAdvantaCorporationÓ) to promote and service credit cards in the UK. In July 1998, the Bank acquired Advanta CorporationÕs 49% minorityshareholding to become sole shareholder of RBS Advanta.

At September 30, 1999, credit card balances were over £2.2 billion and the number of accounts over 2.2 million.

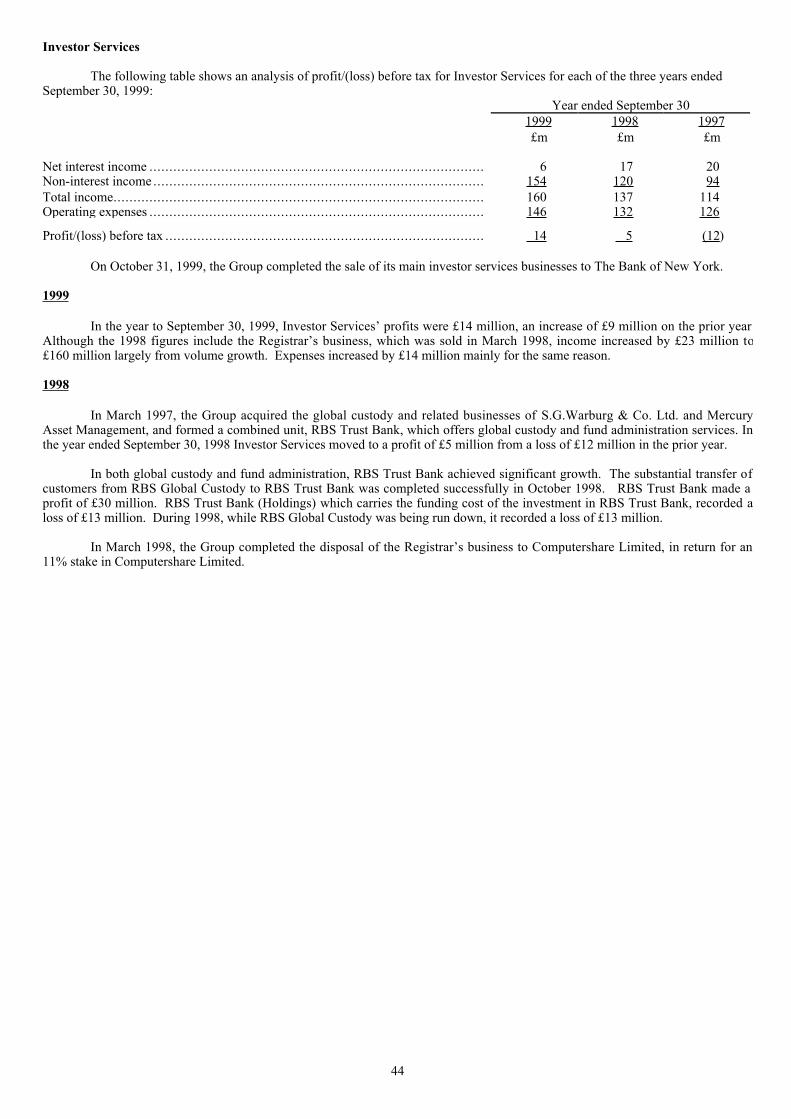

Investor Services

On October 31, 1999, the Group completed the sale of its main investor services businesses to The Bank of New York.

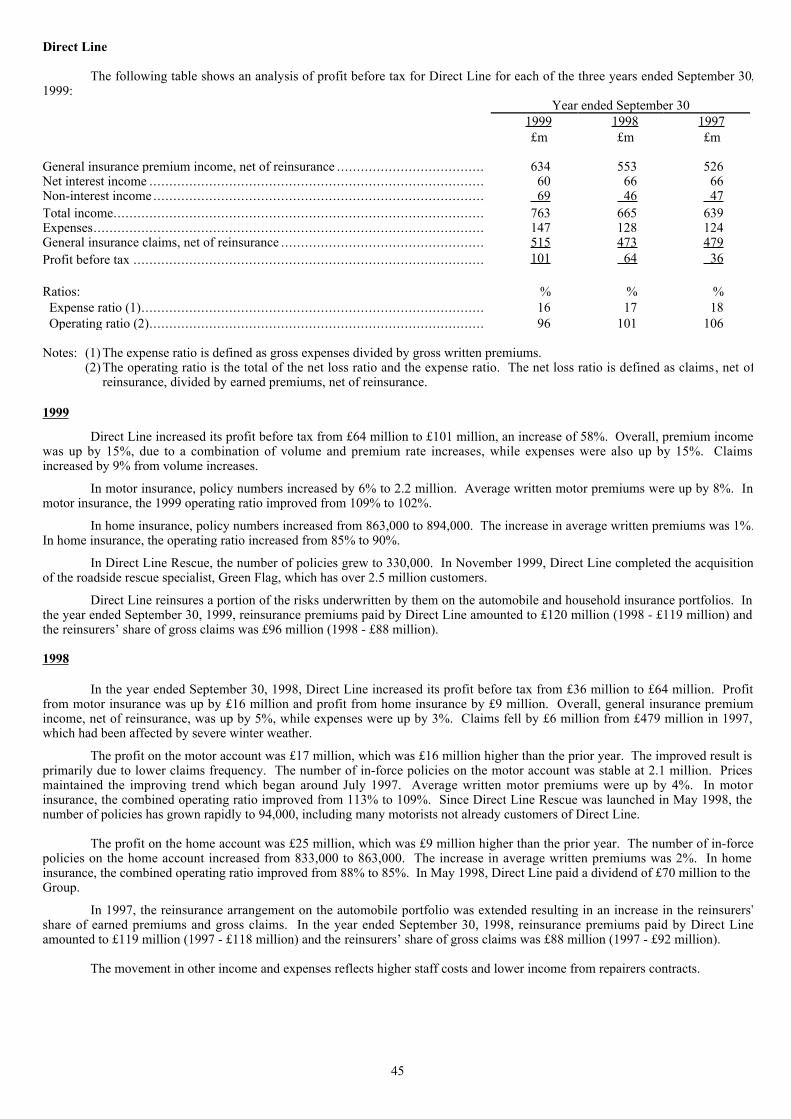

Direct Line Insurance

7

p ( ) g pdomestic household insurance policies. Direct Line sells insurance by telephone directly to customers and does not use insurancebrokers or other intermediaries. Direct Line operates with its head office and South of England regional office in Croydon and hasregional offices in five other major cities in the UK.

In the automobile insurance market Direct Line has increased the number of in-force motor policies by 6% to approximately2.2 million at September 30, 1999 (1998 - 2.1 million), ranking it as one of the largest underwriters of private automobile insurancepolicies in the UK.

Direct Line continued to expand its household insurance portfolio (including buildings, contents and personal possessions)with nearly 894,000 in-force policies at September 30, 1999 (1998 - 863,000 policies). Direct Line also offers creditor insurance topersonal loan and credit card customers of the Bank and Direct Line Financial Services Limited, offering protection to thosecustomers against inability to service debt due to unemployment, sickness or accident. It also offers travel and pet insurance andcertain other ancillary services to its customers, including the arrangement of roadside assistance and recovery.

In November 1999, Direct Line completed the acquisition of the roadside rescue specialist, Green Flag, which, with therapidly growing Direct Line Rescue business, will make Direct Line the UKÕs third largest operator in this business sector, withalmost three million customers.

Citizens Financial Group (ÒCFGÓ)

Citizens Financial Group, Inc. is a US bank holding company incorporated in 1984, the principal banking subsidiaries ofwhich are Citizens Bank of Rhode Island, Citizens Bank of Connecticut, Citizens Bank of Massachusetts and Citizens Bank NewHampshire (ÒCBNHÓ). CFG has 280 branches covering Rhode Island, Connecticut, Massachusetts and New Hampshire and is thesecond largest bank in New England.

CFG provides a range of retail and corporate banking services. Approximately half of its loan portfolio relates to personalbanking, including residential mortgages and home equity loans, and half to corporate lending. See ÒDescription of Assets andLiabilities - Lending ConcentrationsÓ on page 11 of this Report. In addition, CFG engages in a wide variety of consumer lendingactivities, ATM and debit card services, trust services and retail investment services. CFG also operates subsidiaries primarilyengaged in equipment lease financing.

On April 26, 1996, the Group and Bank of Ireland completed the merger of their US banking operations in New England.This transaction involved the merger of CFG and Bank of Ireland First Holdings, the holding company of CBNH, and resulted in theGroup retaining a holding of 76.5% of CFGÕs enlarged share capital, with the remaining 23.5% being held by Bank of Ireland. InSeptember 1998, the Bank acquired the Bank of IrelandÕs 23.5% minority shareholding in CFG for a cash consideration of $750million.

On October 16, 1998, CFG completed the acquisition of four branches from Branford Savings Bank, a subsidiary of NorthFork Bancorp, for a premium of $6 million over net assets acquired, payable in cash.

On October 1, 1999, CFG completed the acquisition of the major part of the commercial banking business of State StreetCorporation for a cash premium of $350 million over net assets acquired. This business has commercial loans totalling $2.3 billionand deposits of $1.1 billion.

On June 21, 1999, it was announced that CFG had entered into an agreement to acquire the entire issued share capital ofUST Corp. of Boston, Massachusetts (ÒUSTÓ) for a consideration of approximately $1.4 billion. As at March 31, 1999, UST hadassets of $5.9 billion and deposits of $4.2 billion. The consideration will be payable in cash at completion, which is expected to takeplace in early 2000, subject to obtaining the consent of Federal and State regulators in the US.

At September 30, 1999, CFG had total assets of $19.5 billion (including total loans of $11 billion and a securities portfolioof $7 billion), total customer deposits of $14 billion and stockholdersÕ equity of $1.5 billion. All figures are stated in accordancewith UK GAAP unless stated otherwise.

8

The Royal Bank of Scotland International Limited (ÒRBSIÓ)

RBSI provides a wide range of offshore banking services to local and international customers through its subsidiaries in theChannel Islands, the Isle of Man, the Bahamas and Gibraltar. These offshore banking services include corporate banking, custod y,treasury and personal banking.

In October 1999, RBSI completed the sale of 30% of its investor services businesses to The Bank of New York.

Central items

Central items include the GroupÕs principal associated undertakings, head office department costs (excluding thoserecharged to other divisions) and income from surplus capital less central financing costs.

Relationship with Banco Santander Central Hispano, S.A.

In October 1988, the Group and Banco Santander entered into an agreement (Òthe agreementÓ) whereby the Group andBanco Santander and its subsidiaries agreed to co-operate in certain banking and financial services activities in Europe, includingrepresentation in each otherÕs bank branches to service their respective customers, offshore and investment banking, technologydevelopment, operational co-operation and the development of representation in Europe and the Far East. In January 1999, BancoSantander announced its intention to merge with Banco Central Hispanoamericano, another Spanish banking group. This merge rwas completed in April 1999 and the merged entity is called Banco Santander Central Hispano, S.A. (ÒBSCHÓ).

At September 30, 1999, the Group held 2.23% of BSCHÕs capital stock. The total cost of this shareholding is £160 millionand the market value as at September 30, 1999 was £514 million. During the year ended September 30, 1998 the Group sold 3.6million shares in Banco Santander realising a gain of £57 million. At September 30, 1999, BSCH held 9.64% of the companyÕsordinary shares.

The Group also has a 12.8% shareholding in Banco Santander, Portugal S.A., with the remainder of the shares being held byBSCH.

Recent events

On November 29, 1999, the Group announced that it had made an offer to acquire National Westminster Bank Plc(ÒNatWestÓ). The company has offered new ordinary shares and loan notes in exchange for NatWest ordinary shares in proportionssuch that existing shareholders in the company would hold approximately 38% of the issued share capital of the enlarged groupfollowing the offer, whilst NatWest shareholders would hold approximately 62%.

9

Staff involvement

At September 30, 1999, the Group employed 32,670 people. The Group encourages staff involvement by a process ofcommunication and consultation. This takes the form of the provision of information through normal management channels, internalpublications, video communication, regular dialogue with staff representatives and an opportunity for staff to voice their views in aconfidential manner via an annual staff opinion survey.

Significant developments to enhance staff involvement in the last year have included the introduction of a training andcommunication network which allows employees to participate in interactive training sessions from their place of work via theirpersonal computer. Also launched within the last year was the BankÕs Intranet which gives employees electronic access toinformation including policies, employment information, job vacancies, news, publications and departmental information.

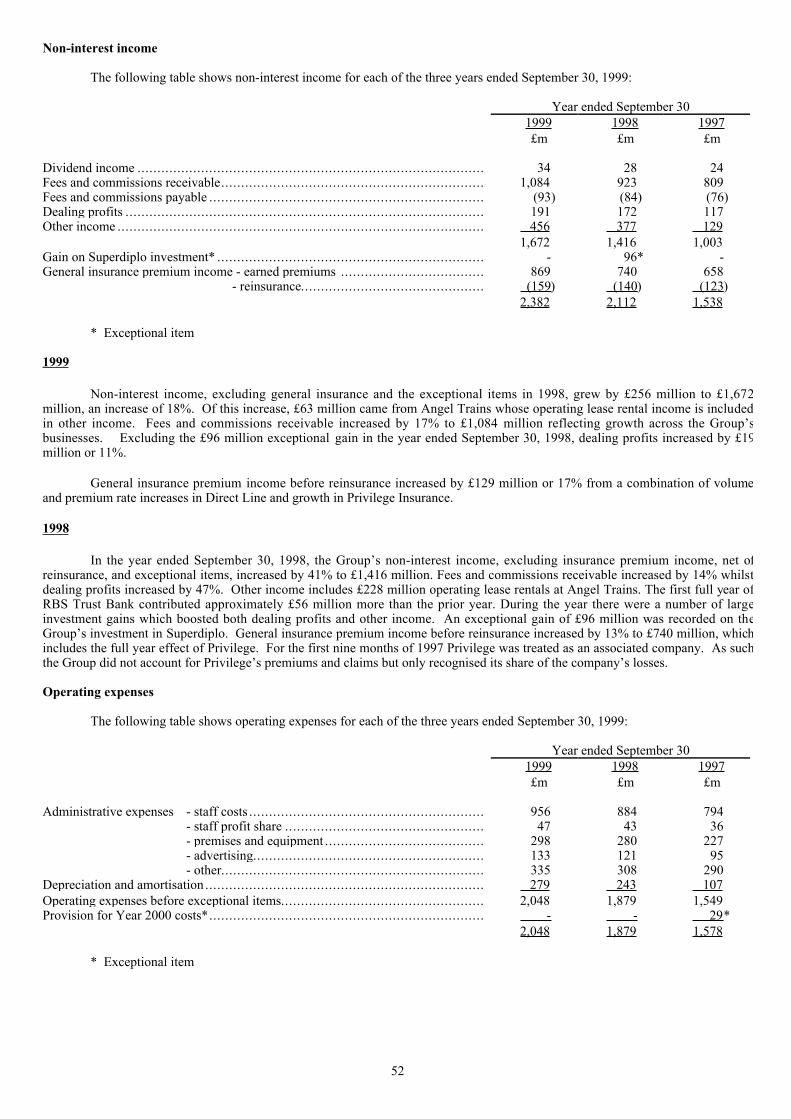

Profit sharing schemes have existed since 1980 and these have included the opportunity to acquire shares in the company.Included in expenses for the year ended September 30, 1999 are sums totalling £47 million for payments to staff eligible toparticipate in the GroupÕs profit sharing schemes (1998 - £43 million).

Staff option schemes were introduced in 1986. On June 3, 1999, options were granted over 3,525,518 ordinary shares, at aprice of 1085p per share, under the companyÕs sharesave scheme. On December 7, 1998, March 4 and June 3, 1999, options weregranted over 935,209 ordinary shares, at prices of 943p, 1205.5p and 1291p per share respectively, under the companyÕs executiveshare option scheme.

Equal opportunities

The company is committed to providing equality of opportunity. The employment practices of companies in the Groupfollow the best practice of each country in which they operate. In the recruitment of staff and their subsequent career development,individuals are considered solely on the basis of their aptitude and ability, irrespective of sex, marital status, race, age, sexualorientation, religion or disability.

The number of women in management positions continues to grow and women now make up almost 37% of middlemanagement and over 11% of senior management. For serving employees who become disabled, every help is given to ensure theircontinued employment and to arrange rehabilitative training. An Occupational Health Service provides in-house expertise on suchrehabilitation programmes. The Bank is a member of the EmployerÕs Forum on Disability and is committed to action to improve theposition of disabled people both as valued employees and as customers of the Bank. The Bank is also a member of Race forOpportunity and is committed to eliminating racism in the workplace.

Environmental issues

The Group recognises that environmental and social responsibility is integral to the way we do business. Environmentaland social imperatives are shaping all our futures and the diversity and flexibility of our businesses enable us to anticipate andrespond to those changes. Our philosophy is that business excellence, of necessity, requires that we meet changing customerexpectations and needs.

The Group recognises this challenge and has adopted policies and management regimes which reinforce these wider humanand material concerns. Our Values, Balanced Scorecard, Change Management, Staff Development, Equal Opportunities, EmployeeAssistance, Health, Safety and Environment programmes all reinforce these wider business principles. The objective is not only tomanage the obvious direct operational impacts on the environment, such as energy, raw material, waste and transport, but also tointegrate environmental and social concerns into all of our financial services activities.

10

Description of Assets and Liabilities

Assets

Loan Portfolio

The GroupÕs loan portfolio consists of loans (including overdraft facilities) and instalment credit and finance leasereceivables. The BankÕs overdraft facilities provide the customer with a demand deposit account and demand credit facilitycombined in a single checking (current) account. An overdraft is effected whenever a customerÕs drawings on a demand depositaccount exceed the credit balance of the account, the balance of which may alternate between debit and credit. While overdrafts arecontractually repayable on demand unless a fixed term has been agreed, in practice customers will from time to time make deposi tsinto the account, thereby reducing indebtedness or increasing a credit balance in accordance with their business requirements.Borrowing limits on the overdraft facility are established, and full repayment is required only if the customer fails to honour theconditions on which the limit was granted or his financial position has so deteriorated that it is necessary to take protective action.Overdraft facilities are usually reviewed at least annually. Interest is generally calculated on the daily outstanding balance byreference to the BankÕs base rate and is typically charged monthly. Overdrafts accounted for approximately 10.8% of the BankÕstotal domestic loan portfolio at September 30, 1999 and 12% at September 30, 1998.

Analysis of Loans to Customers by Geographical Area and Type of Customer

The following table analyses loans (including instalment credit and finance lease receivables) by geographical area and typeof customer at September 30 for each of the five years ended September 30, 1999. The domestic categories of customer are based onthe asset classification requirements of the Bank of England.

SeptemberÊ301999 1998 1997 1996 1995£m £m £m £m £m

Domestic:Central and local government............................. 150 78 116 90 112Manufacturing................................................. 2,715 2,075 1,739 1,732 1,682Construction ................................................... 648 543 404 530 471Finance.......................................................... 2,891 2,197 3,100 3,173 3,231Service industries............................................. 5,585 4,968 4,660 3,374 3,296Agriculture, forestry and fishing ......................... 673 643 613 493 473Property......................................................... 3,668 2,935 2,617 1,525 1,263Business and other services................................ 2,477 2,011 2,140 2,715 2,384Individuals - home mortgages........................... 9,544 8,317 7,371 6,532 6,201

- other.......................................... 6,283 4,550 3,530 2,713 2,319Instalment credit and other loans......................... 1,059 900 856 630 660Finance leases ................................................. 2,555 2,587 2,569 2,333 1,623

Total domestic loans ...................................... 38,248 31,804 29,715 25,840 23,715

Foreign:Foreign Ð UK based ......................................... 2,799 2,248 1,880 1,403 1,178Continental Europe .......................................... 1,046 484 426 408 350United States .................................................. 6,807 5,811 6,063 5,416 3,942Rest of the World............................................. 1,177 1,303 981 853 572

Total foreign loans ........................................ 11,829 9,846 9,350 8,080 6,042

Total loans ................................................... 50,077 41,650 39,065 33,920 29,757 Less allowance for loan losses ......................... (737 ) (633 ) (459 ) (474 ) (540 )

Loans to customers (net of provisions) ................. 49,340 41,017 38,606 33,446 29,217

Analysis of foreign loans by type of borrower:

Governments and official institutions................... 225 179 24 125 99Other financial institutions................................. 47 78 79 93 31Commercial and industrial................................. 7,692 5,834 4,873 3,895 2,943Other............................................................. 3,865 3,755 4,374 3,967 2,969

Total foreign loans ........................................ 11,829 9,846 9,350 8,080 6,042

For further information regarding the GroupÕs operations by geographical area, see Note 50 to the Consolidated FinancialStatements.

11

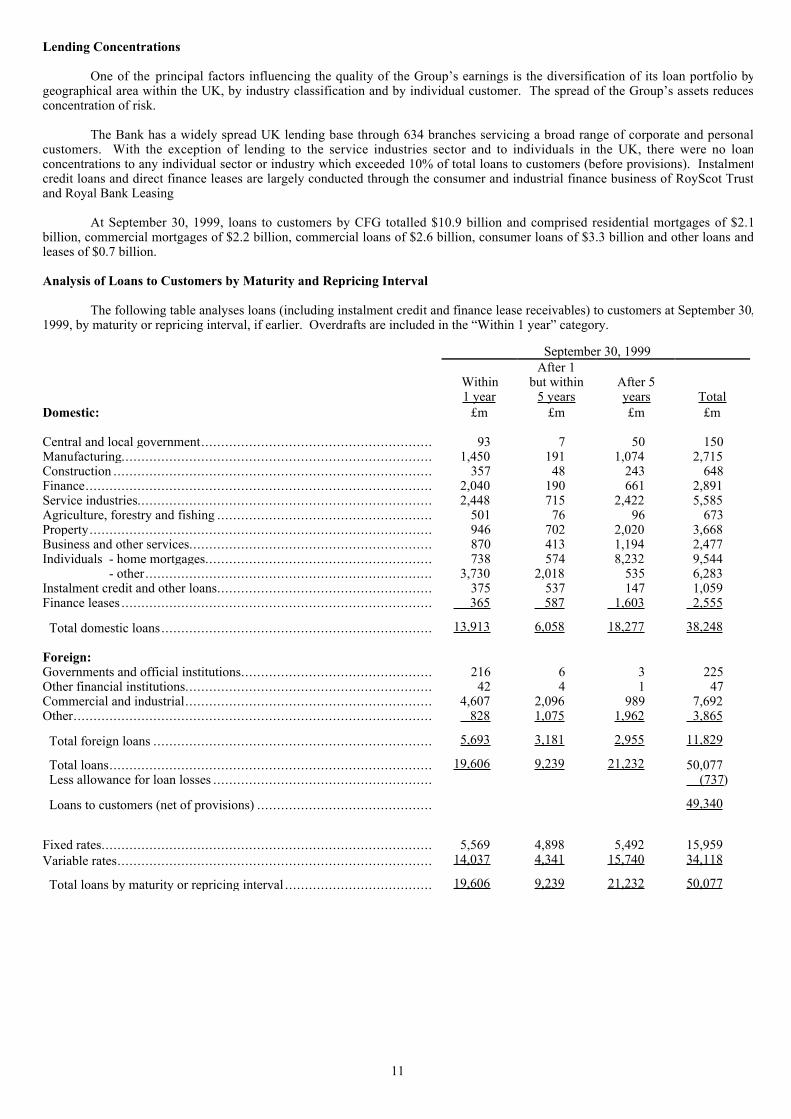

Lending Concentrations

One of the principal factors influencing the quality of the GroupÕs earnings is the diversification of its loan portfolio bygeographical area within the UK, by industry classification and by individual customer. The spread of the GroupÕs assets reducesconcentration of risk.

The Bank has a widely spread UK lending base through 634 branches servicing a broad range of corporate and personalcustomers. With the exception of lending to the service industries sector and to individuals in the UK, there were no loanconcentrations to any individual sector or industry which exceeded 10% of total loans to customers (before provisions). Instalmentcredit loans and direct finance leases are largely conducted through the consumer and industrial finance business of RoyScot Trustand Royal Bank Leasing

At September 30, 1999, loans to customers by CFG totalled $10.9 billion and comprised residential mortgages of $2.1billion, commercial mortgages of $2.2 billion, commercial loans of $2.6 billion, consumer loans of $3.3 billion and other loans andleases of $0.7 billion.

Analysis of Loans to Customers by Maturity and Repricing Interval

The following table analyses loans (including instalment credit and finance lease receivables) to customers at September 30,1999, by maturity or repricing interval, if earlier. Overdrafts are included in the ÒWithin 1 yearÓ category.

SeptemberÊ30, 1999After 1

Within but within After 51Êyear 5Êyears years Total

Domestic: £m £m £m £m

Central and local government.......................................................... 93 7 50 150Manufacturing.............................................................................. 1,450 191 1,074 2,715Construction ................................................................................ 357 48 243 648Finance....................................................................................... 2,040 190 661 2,891Service industries.......................................................................... 2,448 715 2,422 5,585Agriculture, forestry and fishing ...................................................... 501 76 96 673Property...................................................................................... 946 702 2,020 3,668Business and other services............................................................. 870 413 1,194 2,477Individuals - home mortgages......................................................... 738 574 8,232 9,544

- other........................................................................ 3,730 2,018 535 6,283Instalment credit and other loans...................................................... 375 537 147 1,059Finance leases .............................................................................. 365 587 1,603 2,555

Total domestic loans.................................................................... 13,913 6,058 18,277 38,248

Foreign:Governments and official institutions................................................ 216 6 3 225Other financial institutions.............................................................. 42 4 1 47Commercial and industrial.............................................................. 4,607 2,096 989 7,692Other.......................................................................................... 828 1,075 1,962 3,865

Total foreign loans ...................................................................... 5,693 3,181 2,955 11,829

Total loans................................................................................. 19,606 9,239 21,232 50,077 Less allowance for loan losses ....................................................... (737 )

Loans to customers (net of provisions) ............................................ 49,340

Fixed rates................................................................................... 5,569 4,898 5,492 15,959Variable rates............................................................................... 14,037 4,341 15,740 34,118

Total loans by maturity or repricing interval ..................................... 19,606 9,239 21,232 50,077

12

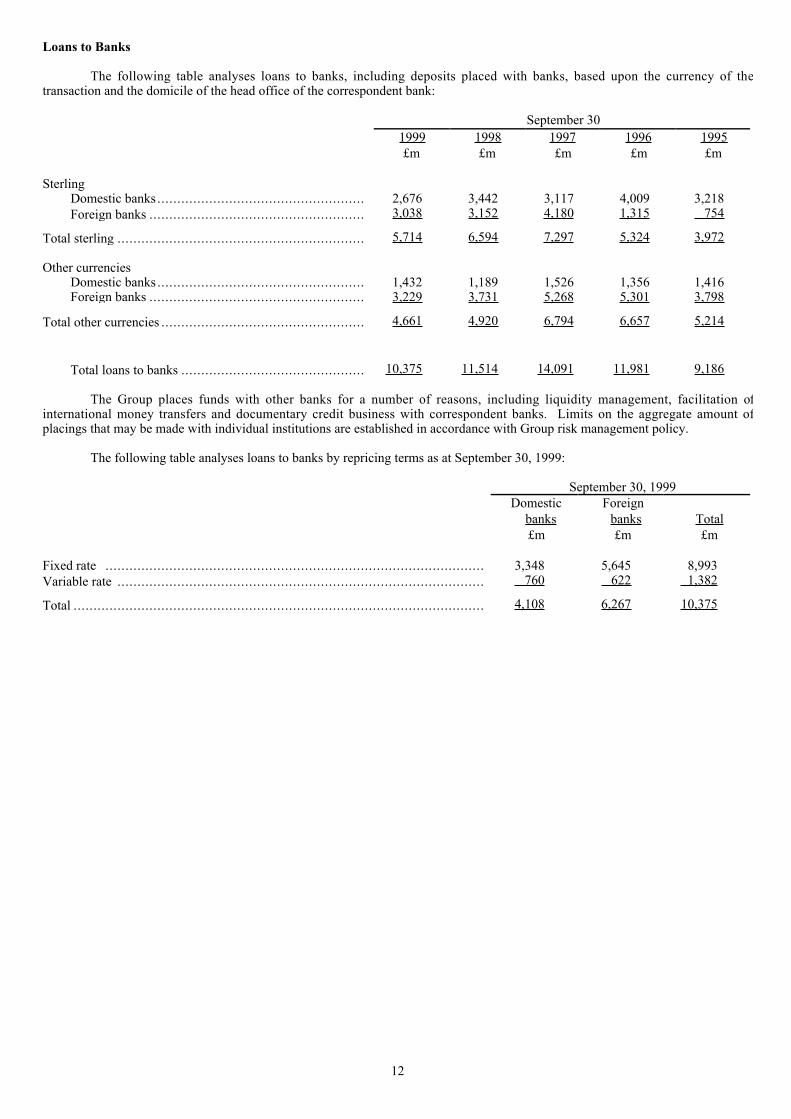

Loans to Banks

The following table analyses loans to banks, including deposits placed with banks, based upon the currency of thetransaction and the domicile of the head office of the correspondent bank:

SeptemberÊ301999 1998 1997 1996 1995 £m £m £m £m £m

SterlingDomestic banks .................................................... 2,676 3,442 3,117 4,009 3,218Foreign banks ...................................................... 3,038 3,152 4,180 1,315 754

Total sterling .............................................................. 5,714 6,594 7,297 5,324 3,972

Other currenciesDomestic banks .................................................... 1,432 1,189 1,526 1,356 1,416

Foreign banks ...................................................... 3,229 3,731 5,268 5,301 3,798

Total other currencies ................................................... 4,661 4,920 6,794 6,657 5,214

Total loans to banks .............................................. 10,375 11,514 14,091 11,981 9,186

The Group places funds with other banks for a number of reasons, including liquidity management, facilitation ofinternational money transfers and documentary credit business with correspondent banks. Limits on the aggregate amount ofplacings that may be made with individual institutions are established in accordance with Group risk management policy.

The following table analyses loans to banks by repricing terms as at September 30, 1999:

September 30, 1999Domestic Foreign

banks banks Total£m £m £m

Fixed rate ............................................................................................... 3,348 5,645 8,993Variable rate ............................................................................................ 760 622 1,382

Total ....................................................................................................... 4,108 6,267 10,375

13

Cross-Border Outstandings

Cross-border outstandings consist of loans to banks and customers, instalment credit and finance lease receivables,acceptances and other monetary assets, including non-local currency claims of overseas offices on local residents. The Groupmonitors the geographical breakdown of outstandings based on the country of domicile of the borrower or guarantor of ultimate risk.CFG has no material amount of cross-border outstandings.

Cross-Border Outstandings in Excess of 1% of Total Assets

The following table identifies countries where the GroupÕs cross-border outstandings to borrowers exceeded 1% of totalassets and acceptances:

Banks Commercial,As % of and other Governments industrial and

total financial and official other privateassets (1) Total institutions institutions sector

% £m £m £m £mSeptember 30, 1999United States .............................................. 3.8 3,452 1,482 264 1,706Germany.................................................... 3.5 3,135 2,880 39 216France ....................................................... 1.9 1,722 1,567 37 118

September 30, 1998Germany.................................................... 3.5 2,810 2,679 - 131United States .............................................. 3.1 2,481 675 145 1,661France ....................................................... 2.5 2,022 1,932 - 90Japan......................................................... 1.3 1,043 999 - 44Spain......................................................... 1.2 1,001 832 46 123

September 30, 1997United States .............................................. 4.3 3,139 1,363 410 1,366France ....................................................... 2.5 1,863 1,766 - 97Japan......................................................... 1.5 1,135 1,100 - 35Belgium..................................................... 1.4 1,056 1,050 - 6Germany ................................................... 1.1 796 717 - 79

NOTE

(1) Assets comprise total assets, as reported in the Consolidated Balance Sheet, and acceptances, which together totalled£89,746 million at September 30, 1999 (September 30, 1998 - £80,700 million, September 30, 1997 - £73,464 million).

Cross-Border Outstandings Between 0.75% and 1% of Total Assets

At September 30, 1999, cross-border outstandings totalling £2,434 million to borrowers in Belgium, Canada and Spaineach amounted to between 0.75% and 1% of total assets.

At September 30, 1998, cross-border outstandings totalling £2,608 million to borrowers in Canada, Belgium, theNetherlands and Italy each amounted to between 0.75% and 1% of total assets.

At September 30, 1997, cross-border outstandings totalling £1,327 million to borrowers in the Netherlands and Italy eachamounted to between 0.75% and 1% of total assets.

14

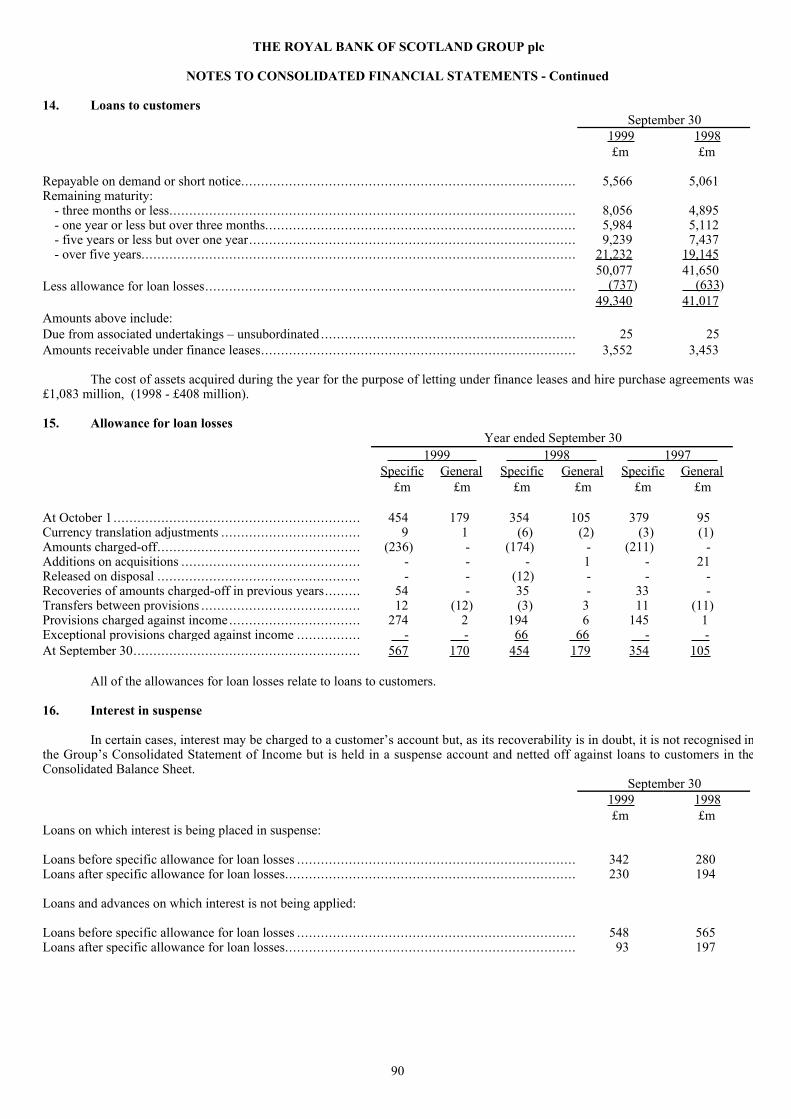

Provision and Allowance for Loan Losses

Provisioning Policy

Within the Bank and those of its subsidiaries engaged in banking (excluding CFG - see below), loan officers regularlyreview the quality of loans for which they are responsible. Specific provisions are made against loans when, as a result of a detailedappraisal of the loan portfolio, it is considered that recovery is doubtful, which depends in each case on the individual circumstancesof the loan, including, among other things, the adequacy of any collateral securing the loan. Provisions made during a year (lessamounts released and recoveries of amounts charged-off in previous years) are charged against income. Interest receivable ondoubtful loans is brought into the Consolidated Statement of Income as it accrues only so long as its collectibility is not subject tosignificant doubt. Loans classified as bad debts are charged-off to their estimated net realisable value when there is no realisticprospect of recovery.

In addition, general provisions are maintained at levels considered appropriate by management to cover losses from loanswhich have not been separately identified but are known from experience to be present in any portfolio of bank loans. Reviews ofthe level of general provisions are conducted throughout the year. A factor in establishing the level of general provisions is thescope and detail of the specific provisioning procedures in place at the time of the review.

There are differences between the provisioning policies of banks in the UK and the United States. In the UK loans andrelated accrued interest are charged-off only when, as a matter of banking judgement, there is no realistic prospect of recovery.When management determines that a charge-off is appropriate, the principal amount and accrued interest on the obligation arewritten down to estimated net realisable value. Interest receivable on loans is recognised as income as it accrues provided that itscollectibility is not subject to significant doubt. In contrast, banks in the United States (including CFGÕs bank subsidiaries) typicallystop accruing interest when loans become overdue by 90 days and recovery is doubtful, and charge-off loans more rapidly. Thecumulative effect of the GroupÕs policies is to increase the relative size of the GroupÕs loan portfolio and the allowance for loanlosses compared with those of US banks, which has the effect of increasing the GroupÕs loan loss allowance ratios compared withthose which would result from the application of US bank provisioning policies. The GroupÕs policies do not, however, result in asignificant adjustment to the GroupÕs net income, shareholdersÕ funds and total assets for restatement under US GAAP. See Note 52to the Consolidated Financial Statements.

CFG

Loan officers in CFG evaluate the adequacy of the allowance for possible credit losses by performing reviews of certainindividual loans and leases, analysing changes in the composition and size of the portfolio, reviewing previous loss experience andconsidering current and anticipated economic factors. The allowance is established through charges to earnings in the form of aprovision for credit losses and is maintained at a level which management considers adequate based on the results of this evaluation.Amounts determined to be uncollectable are deducted from the allowance and subsequent recoveries, if any, are added to theallowance.

Non-performing loans and leases consist of (a) non-accrual loans and leases and (b) accruing loans which are contractuallypast due 90 days or more. Loans and leases are generally placed on non-accrual when 90 days or more past due, or earlier whenmanagement deems the probability of collection to be insufficient to warrant further accrual. Certain loans, primarily consumercredits, remain on accrual when contractually past due 90 days or more if considered by management to be collectible.

15

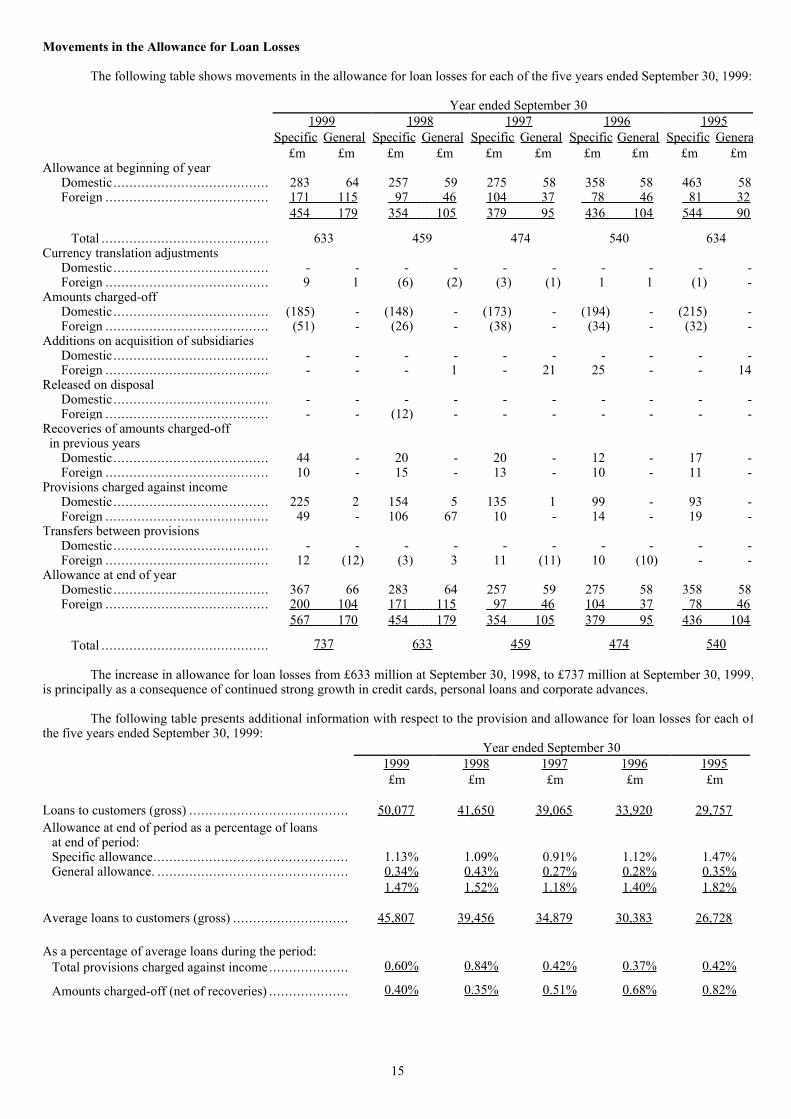

Movements in the Allowance for Loan Losses

The following table shows movements in the allowance for loan losses for each of the five years ended September 30, 1999:

YearÊendedÊSeptemberÊ301999 1998 1997 1996 1995

Specific General Specific General Specific General Specific General Specific Genera£m £m £m £m £m £m £m £m £m £m

Allowance at beginning of yearDomestic....................................... 283 64 257 59 275 58 358 58 463 58Foreign ......................................... 171 115 97 46 104 37 78 46 81 32

454 179 354 105 379 95 436 104 544 90

Total .......................................... 633 459 474 540 634Currency translation adjustments

Domestic....................................... - - - - - - - - - -Foreign ......................................... 9 1 (6) (2) (3) (1) 1 1 (1) -

Amounts charged-offDomestic....................................... (185) - (148) - (173) - (194) - (215) -Foreign ......................................... (51) - (26) - (38) - (34) - (32) -

Additions on acquisition of subsidiariesDomestic....................................... - - - - - - - - - -Foreign ......................................... - - - 1 - 21 25 - - 14

Released on disposalDomestic....................................... - - - - - - - - - -Foreign ......................................... - - (12) - - - - - - -

Recoveries of amounts charged-off in previous years

Domestic....................................... 44 - 20 - 20 - 12 - 17 -Foreign ......................................... 10 - 15 - 13 - 10 - 11 -

Provisions charged against incomeDomestic....................................... 225 2 154 5 135 1 99 - 93 -Foreign ......................................... 49 - 106 67 10 - 14 - 19 -

Transfers between provisionsDomestic....................................... - - - - - - - - - -Foreign ......................................... 12 (12) (3) 3 11 (11) 10 (10) - -

Allowance at end of yearDomestic....................................... 367 66 283 64 257 59 275 58 358 58Foreign ......................................... 200 104 171 115 97 46 104 37 78 46

567 170 454 179 354 105 379 95 436 104

Total .......................................... 737 633 459 474 540

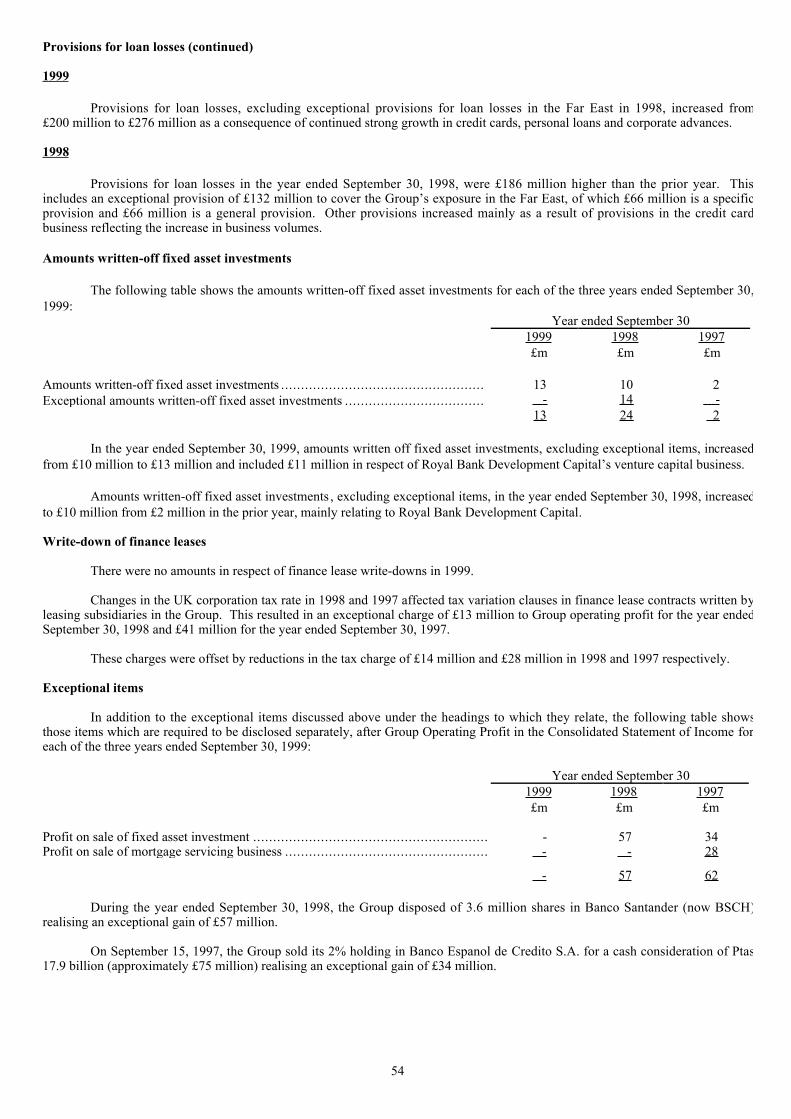

The increase in allowance for loan losses from £633 million at September 30, 1998, to £737 million at September 30, 1999,is principally as a consequence of continued strong growth in credit cards, personal loans and corporate advances.

The following table presents additional information with respect to the provision and allowance for loan losses for each ofthe five years ended September 30, 1999:

YearÊendedÊSeptemberÊ301999 1998 1997 1996 1995 £m £m £m £m £m

Loans to customers (gross) ........................................ 50,077 41,650 39,065 33,920 29,757Allowance at end of period as a percentage of loans

at end of period:Specific allowance................................................. 1.13% 1.09% 0.91% 1.12% 1.47%General allowance. ................................................ 0.34% 0.43% 0.27% 0.28% 0.35%

1.47% 1.52% 1.18% 1.40% 1.82%

Average loans to customers (gross) ............................. 45,807 39,456 34,879 30,383 26,728

As a percentage of average loans during the period:Total provisions charged against income.................... 0.60% 0.84% 0.42% 0.37% 0.42%

Amounts charged-off (net of recoveries) .................... 0.40% 0.35% 0.51% 0.68% 0.82%

16

Charge-offs and Recoveries

The following table shows amounts charged-off for each of the five years ended September 30, 1999:

Charge-offs YearÊendedÊSeptemberÊ301999 1998 1997 1996 1995 £m £m £m £m £m

Domestic:Manufacturing........................................................ 4 11 5 10 10Construction .......................................................... 5 5 11 10 9Finance ................................................................. 1 2 1 7 4Service industries.................................................... 22 35 58 56 51Agriculture, forestry and fishing................................. 1 2 1 3 2Property ................................................................ 4 4 7 12 18Business and other services....................................... 16 6 21 23 31Individuals - home mortgages ................................... 9 5 3 4 1 - others.................................................. 117 74 63 63 71Finance leases and instalment credit............................ 6 4 3 6 18

Total domestic............................................... 185 148 173 194 215Foreign .................................................................... 51Ê 26 38 34 32

Total charge-offs ........................................... 236 174 211 228 247

Charge-offs increased from £174 million in the year ended September 30, 1998 to £236 million in the current year. Theincrease in ÔIndividuals Ð othersÕ was due to the increase in credit card lending. This increase was partly offset by a decrease of £13million in Service industries.

The following table shows recoveries of amounts charged-off in previous years for each of the five years ended September30, 1999:

Recoveries YearÊendedÊSeptemberÊ301999 1998 1997 1996 1995 £m £m £m £m £m

Domestic:Manufacturing........................................................ 2 1 1 - -Construction .......................................................... 1 3 3 - -Finance ................................................................. 8 1 1 - -Service industries.................................................... 4 5 8 5 7Property ................................................................ - 1 1 1 4Business and other services ....................................... - 1 - - -Individuals - home mortgages ................................... 1 - - - -

- others ................................................ 28 8 6 6 6

Total domestic............................................... 44 20 20 12 17

Foreign .................................................................... 10 15 13 10 11

Total recoveries ............................................. 54 35 33 22 28

For a discussion of the factors considered in determining the amount of the provision for loan losses, see ÒProvision forLoan LossesÓ on page 53.

17

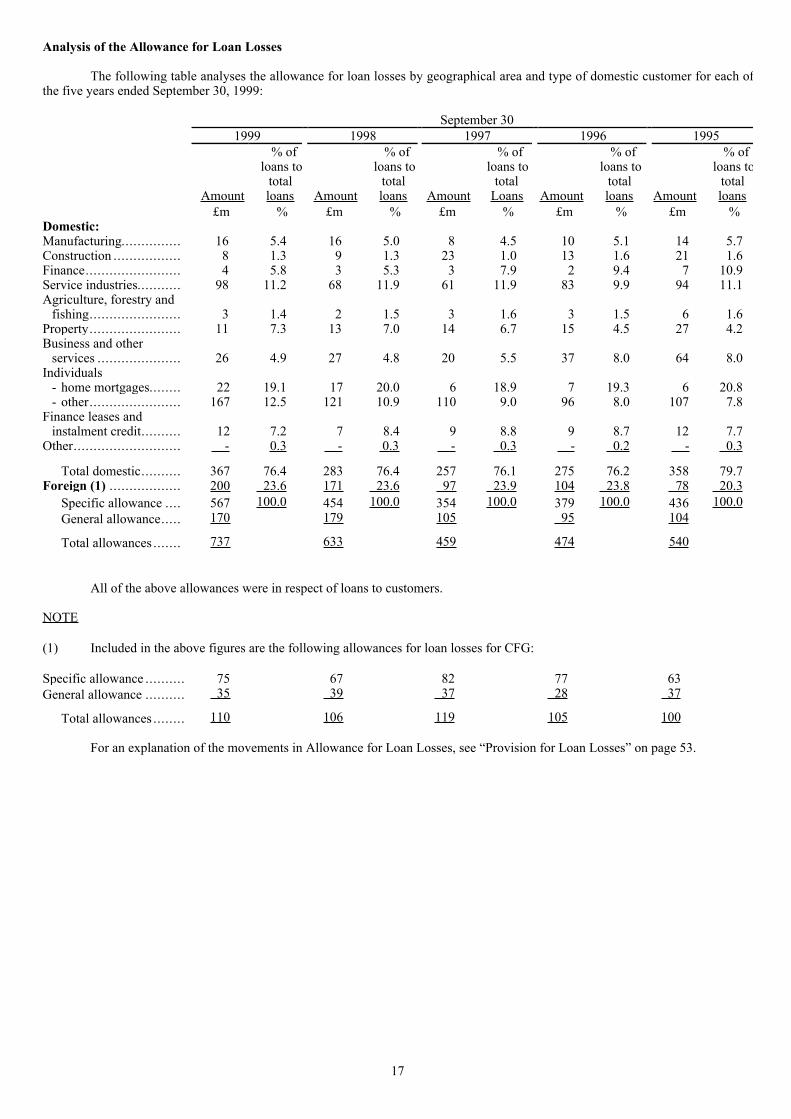

Analysis of the Allowance for Loan Losses

The following table analyses the allowance for loan losses by geographical area and type of domestic customer for each ofthe five years ended September 30, 1999:

September 301999 1998 1997 1996 1995

% of % of % of % of % ofloans to loans to loans to loans to loans to

total total total total totalAmount loans Amount loans Amount Loans Amount loans Amount loans

£m % £m % £m % £m % £m %Domestic:Manufacturing............... 16 5.4 16 5.0 8 4.5 10 5.1 14 5.7Construction ................. 8 1.3 9 1.3 23 1.0 13 1.6 21 1.6Finance........................ 4 5.8 3 5.3 3 7.9 2 9.4 7 10.9Service industries........... 98 11.2 68 11.9 61 11.9 83 9.9 94 11.1Agriculture, forestry and

fishing....................... 3 1.4 2 1.5 3 1.6 3 1.5 6 1.6Property....................... 11 7.3 13 7.0 14 6.7 15 4.5 27 4.2Business and other

services ..................... 26 4.9 27 4.8 20 5.5 37 8.0 64 8.0Individuals

- home mortgages........ 22 19.1 17 20.0 6 18.9 7 19.3 6 20.8- other....................... 167 12.5 121 10.9 110 9.0 96 8.0 107 7.8

Finance leases andinstalment credit.......... 12 7.2 7 8.4 9 8.8 9 8.7 12 7.7

Other........................... - 0.3 - 0.3 - 0.3 - 0.2 - 0.3

Total domestic.......... 367 76.4 283 76.4 257 76.1 275 76.2 358 79.7Foreign (1) .................. 200 Ê23.6 171 23.6 97 23.9 104 23.8 78 20.3

Specific allowance .... 567 100.0 454 100.0 354 100.0 379 100.0 436 100.0General allowance..... 170 179 105 95 104

Total allowances ....... 737 633 459 474 540

All of the above allowances were in respect of loans to customers.

NOTE

(1) Included in the above figures are the following allowances for loan losses for CFG:

Specific allowance .......... 75 67 82 77 63General allowance .......... 35 39 37 28 37

Total allowances ........ 110 106 119 105 100

For an explanation of the movements in Allowance for Loan Losses, see ÒProvision for Loan LossesÓ on page 53.

18

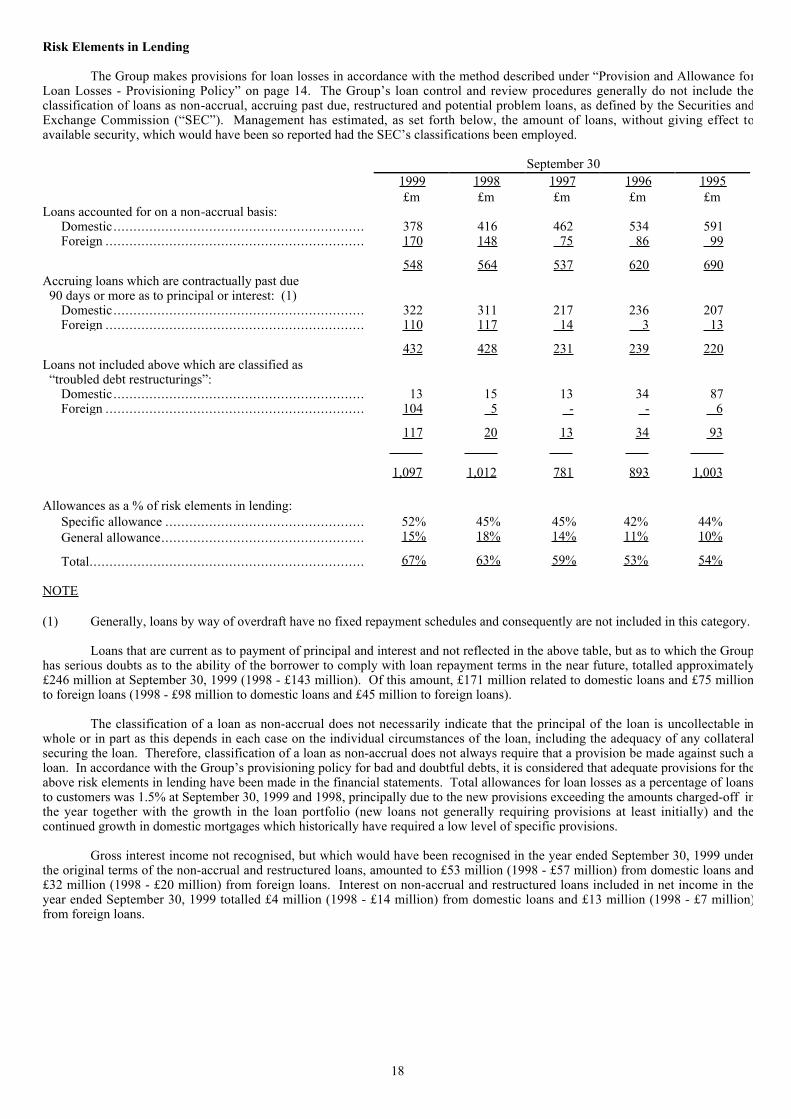

Risk Elements in Lending

The Group makes provisions for loan losses in accordance with the method described under ÒProvision and Allowance forLoan Losses - Provisioning PolicyÓ on page 14. The GroupÕs loan control and review procedures generally do not include theclassification of loans as non-accrual, accruing past due, restructured and potential problem loans, as defined by the Securities andExchange Commission (ÒSECÓ). Management has estimated, as set forth below, the amount of loans, without giving effect toavailable security, which would have been so reported had the SECÕs classifications been employed.

SeptemberÊ301999 1998 1997 1996 1995 £m £m £m £m £m

Loans accounted for on a non-accrual basis:Domestic............................................................... 378 416 462 534 591Foreign ................................................................. 170 148 75 86 99

548 564 537 620 690Accruing loans which are contractually past due 90 days or more as to principal or interest: (1)

Domestic............................................................... 322 311 217 236 207Foreign ................................................................. 110 117 14 3 13

432 428 231 239 220Loans not included above which are classified as Òtroubled debt restructuringsÓ:

Domestic............................................................... 13 15 13 34 87Foreign ................................................................. 104 5 - - 6

117 20 13 34 93ÊÊÊÊÊÊÊÊÊÊ ÊÊÊÊÊÊÊÊÊÊ ÊÊÊÊÊÊÊ ÊÊÊÊÊÊÊ ÊÊÊÊÊÊÊÊÊÊ

1,097 1,012 781 893 1,003

Allowances as a % of risk elements in lending:Specific allowance .................................................. 52% 45% 45% 42% 44%General allowance................................................... 15% 18% 14% 11% 10%

Total..................................................................... 67% 63% 59% 53% 54%

NOTE

(1) Generally, loans by way of overdraft have no fixed repayment schedules and consequently are not included in this category.

Loans that are current as to payment of principal and interest and not reflected in the above table, but as to which the Grouphas serious doubts as to the ability of the borrower to comply with loan repayment terms in the near future, totalled approximately£246 million at September 30, 1999 (1998 - £143 million). Of this amount, £171 million related to domestic loans and £75 millionto foreign loans (1998 - £98 million to domestic loans and £45 million to foreign loans).

The classification of a loan as non-accrual does not necessarily indicate that the principal of the loan is uncollectable inwhole or in part as this depends in each case on the individual circumstances of the loan, including the adequacy of any collateralsecuring the loan. Therefore, classification of a loan as non-accrual does not always require that a provision be made against such aloan. In accordance with the GroupÕs provisioning policy for bad and doubtful debts, it is considered that adequate provisions for theabove risk elements in lending have been made in the financial statements. Total allowances for loan losses as a percentage of loansto customers was 1.5% at September 30, 1999 and 1998, principally due to the new provisions exceeding the amounts charged-off inthe year together with the growth in the loan portfolio (new loans not generally requiring provisions at least initially) and thecontinued growth in domestic mortgages which historically have required a low level of specific provisions.

Gross interest income not recognised, but which would have been recognised in the year ended September 30, 1999 underthe original terms of the non-accrual and restructured loans, amounted to £53 million (1998 - £57 million) from domestic loans and£32 million (1998 - £20 million) from foreign loans. Interest on non-accrual and restructured loans included in net income in theyear ended September 30, 1999 totalled £4 million (1998 - £14 million) from domestic loans and £13 million (1998 - £7 million)from foreign loans.

19

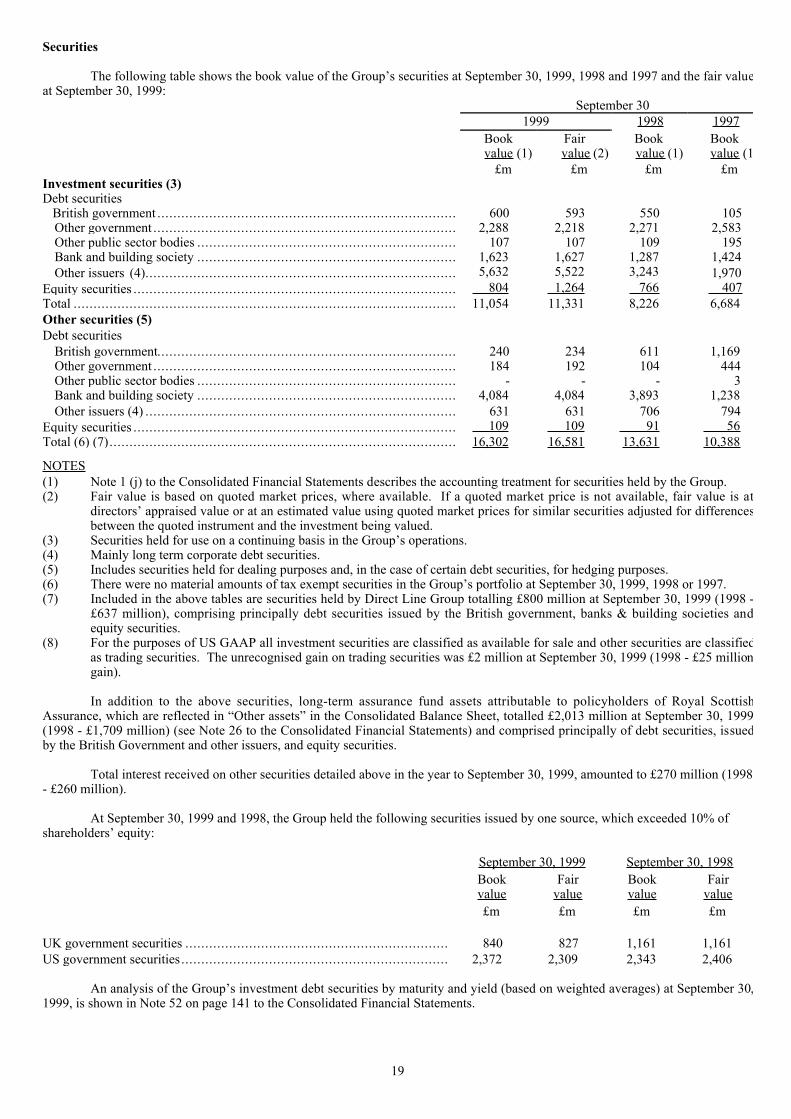

Securities

The following table shows the book value of the GroupÕs securities at September 30, 1999, 1998 and 1997 and the fair valueat September 30, 1999:

SeptemberÊ301999 1998 1997

Book Fair Book Bookvalue (1) value (2) value (1) value (1

£m £m £m £mInvestment securities (3)Debt securities British government ........................................................................... 600 593 550 105

Other government ............................................................................ 2,288 2,218 2,271 2,583Other public sector bodies ................................................................. 107 107 109 195Bank and building society ................................................................. 1,623 1,627 1,287 1,424Other issuers (4).............................................................................. 5,632 5,522 3,243 1,970

Equity securities ................................................................................. 804 1,264 766 407Total ................................................................................................ 11,054 11,331 8,226 6,684Other securities (5)Debt securities British government........................................................................... 240 234 611 1,169

Other government ............................................................................ 184 192 104 444Other public sector bodies ................................................................. - - - 3Bank and building society ................................................................. 4,084 4,084 3,893 1,238Other issuers (4) .............................................................................. 631 631 706 794

Equity securities ................................................................................. 109 109 91 56Total (6) (7)....................................................................................... 16,302 16,581 13,631 10,388

NOTES(1) Note 1 (j) to the Consolidated Financial Statements describes the accounting treatment for securities held by the Group.(2) Fair value is based on quoted market prices, where available. If a quoted market price is not available, fair value is at

directorsÕ appraised value or at an estimated value using quoted market prices for similar securities adjusted for differencesbetween the quoted instrument and the investment being valued.

(3) Securities held for use on a continuing basis in the GroupÕs operations.(4) Mainly long term corporate debt securities.(5) Includes securities held for dealing purposes and, in the case of certain debt securities, for hedging purposes.(6) There were no material amounts of tax exempt securities in the GroupÕs portfolio at September 30, 1999, 1998 or 1997.(7) Included in the above tables are securities held by Direct Line Group totalling £800 million at September 30, 1999 (1998 -

£637 million), comprising principally debt securities issued by the British government, banks & building societies andequity securities.

(8) For the purposes of US GAAP all investment securities are classified as available for sale and other securities are classifiedas trading securities. The unrecognised gain on trading securities was £2 million at September 30, 1999 (1998 - £25 milliongain).

In addition to the above securities, long-term assurance fund assets attributable to policyholders of Royal ScottishAssurance, which are reflected in ÒOther assetsÓ in the Consolidated Balance Sheet, totalled £2,013 million at September 30, 1999(1998 - £1,709 million) (see Note 26 to the Consolidated Financial Statements) and comprised principally of debt securities, issuedby the British Government and other issuers, and equity securities.

Total interest received on other securities detailed above in the year to September 30, 1999, amounted to £270 million (1998- £260 million).

At September 30, 1999 and 1998, the Group held the following securities issued by one source, which exceeded 10% ofshareholdersÕ equity:

September 30, 1999 September 30, 1998Book Fair Book Fairvalue value value value£m £m £m £m

UK government securities .................................................................. 840 827 1,161 1,161US government securities................................................................... 2,372 2,309 2,343 2,406

An analysis of the GroupÕs investment debt securities by maturity and yield (based on weighted averages) at September 30,1999, is shown in Note 52 on page 141 to the Consolidated Financial Statements.

20

Liabilities

Deposits

A substantial portion of the GroupÕs assets are funded by deposits, principally current accounts and various types of interestbearing deposit accounts, collected through the BankÕs UK branch network, CFG and RBSI. The remainder of the assets of theBank, CFG and RBSI are funded by wholesale deposits, debt securities in issue, loan capital and shareholdersÕ equity.

At September 30, 1999, 1998 and 1997, approximately 8.9%, 11% and 14.4% respectively, of domestic deposits were innon-interest bearing current accounts. At September 30, 1999, 1998 and 1997, approximately 57.8%, 56.0% and 52.4% respectively,of domestic deposits were interest bearing deposits repayable on demand. Interest bearing demand deposits are current accountswith credit balances and retail deposits repayable on demand, obtained primarily through the BankÕs UK branch networks, andwholesale deposits repayable on demand, booked mainly within the BankÕs treasury operation. Interest rates applicable to suchdeposits are generally calculated on the basis of a margin under the BankÕs base rate. Deposits in currencies other than sterling arecollected principally by Corporate and Institutional Banking, CFG and RBSI. The former raises most of its deposits through thewholesale markets whereas CFGÕs and RBSIÕs deposits are principally demand and savings deposits.

Savings deposits are specific products which are designed to attract larger savings from personal customers who do notrequire withdrawals on demand and therefore in general offer better rates of return than interest bearing demand deposits. AtSeptember 30, 1999, 1998 and 1997, approximately 7.5%, 10.0% and 8.7% respectively, of the BankÕs domestic deposits were insavings deposits.

Other time deposits are collected centrally from the money market to bridge the gap between retail resources and sterlingassets. Chief sources of wholesale deposits are the inter-bank market, corporations and non-bank financial institutions which placefunds on the inter-bank market, and issuance of certificates of deposit and medium term notes. All are priced in relation to moneymarket rates. Rate considerations and the ability to provide funds in the maturity periods required by the Bank to fulfil its liquiditymanagement objectives affect the choice of instrument. Customers are offered rates related to inter-bank market rates for the term ofthe deposit depending on the amounts and term. Larger deposits (typically £1 million and over) earn the money market rates paid inthe inter-bank market, and smaller amounts earn progressively wider spreads under the money market rate. Rates are centrallycommunicated throughout the Bank by the BankÕs central treasury operation. While competitive rates influence the quantity ofdeposits obtained through the branch network, the branch network enables a wide variety of local depositor sources to be accessed.

Analysis of Deposits

The following table shows the distribution of deposits by banks and customer accounts by sterling and other currencies atSeptember 30, 1999, 1998 and 1997:

SeptemberÊ301999 1998 1997£m £m £m

Deposits by banks Sterling .................................................................................................. 3,347 1,958 1,217 Other currencies....................................................................................... 3,071 2,479 4,178

Total deposits by banks........................................................................... 6,418 4,437 5,395

Customer accounts Sterling .................................................................................................. 36,663 33,785 30,827 Other currencies (1).................................................................................. 18,517 16,900 16,755

Total customer accounts......................................................................... 55,180 50,685 47,582

Total deposits....................................................................................... 61,598 55,122 52,977

NOTE

(1) Includes non-sterling deposits in CFG of £8,919 million at September 30, 1999 (1998 - £8,065 million, 1997 - £8,300 million).

21

Average Deposits and Average Interest Rates

The following table shows details of the GroupÕs average deposits in each of the past three years:

Year ended SeptemberÊ30ÊÊÊÊÊÊÊÊÊÊÊÊÊÊ1999ÊÊÊÊÊÊÊÊÊÊÊÊÊ ÊÊÊÊÊÊÊÊÊÊÊÊÊÊ1998ÊÊÊÊÊÊÊÊÊÊÊÊÊ ÊÊÊÊÊÊÊÊÊÊÊÊÊÊ1997ÊÊÊÊÊÊÊÊÊÊÊÊÊAverage Average Average Average Average Averagebalance rate balance rate balance rate

£m % £m % £m %Domestic offices Interest free demand ................................. 1,899 - 1,920 - 1,858 - Deposits by banks .................................... 5,344 5.4 4,144 6.6 3,935 5.8 Customer accounts Demand................................................ 20,370 3.8 18,912 5.2 16,156 4.3 Savings ................................................ 8,783 4.9 4,136 6.0 2,819 5.0 Other time............................................. 10,622 5.8 12,265 7.2 10,769 6.1

Total domestic office deposits ................. 47,018 4.9 41,377 5.8 35,537 4.8

Foreign offices Interest free demand ................................. 1,111 - 957 - 858 - Deposits by banks .................................... 1,038 4.6 1,289 5.7 1,583 5.4 Customer accounts Demand................................................ 995 1.6 2,131 5.1 1,840 3.8 Savings ................................................ 6,441 4.0 6,253 4.1 5,963 4.4 Other time............................................. 1,272 5.1 348 5.0 327 4.9

Total foreign office deposits ................... 10,857 3.6 10,978 4.2 10,571 4.1

Total average deposits ........................... 57,875 4.3 52,355 5.4 46,108 4.7

Certificates of Deposit and Other Time Deposits

The following table shows details of the GroupÕs certificates of deposit issued and other time deposits over £50,000 (or theequivalent of $100,000 for currencies other than sterling) by time remaining until maturity:

SeptemberÊ30,Ê1999Over 3 but Over 6 but

Within within 6 within 12 Over 123Êmonths months months months Total

£m £m £m £m £mUK based companies and branches

Certificates of deposit .................................. 2,798 811 367 65 4,041Other time deposits...................................... 14,639 1,061 173 601 16,474

Overseas based companies and branchesCertificates of deposit .................................. 516 9 3 - 528Other time deposits...................................... 2,032 293 200 141 2,666

Total ....................................................... 19,985 2,174 743 807 23,709

22

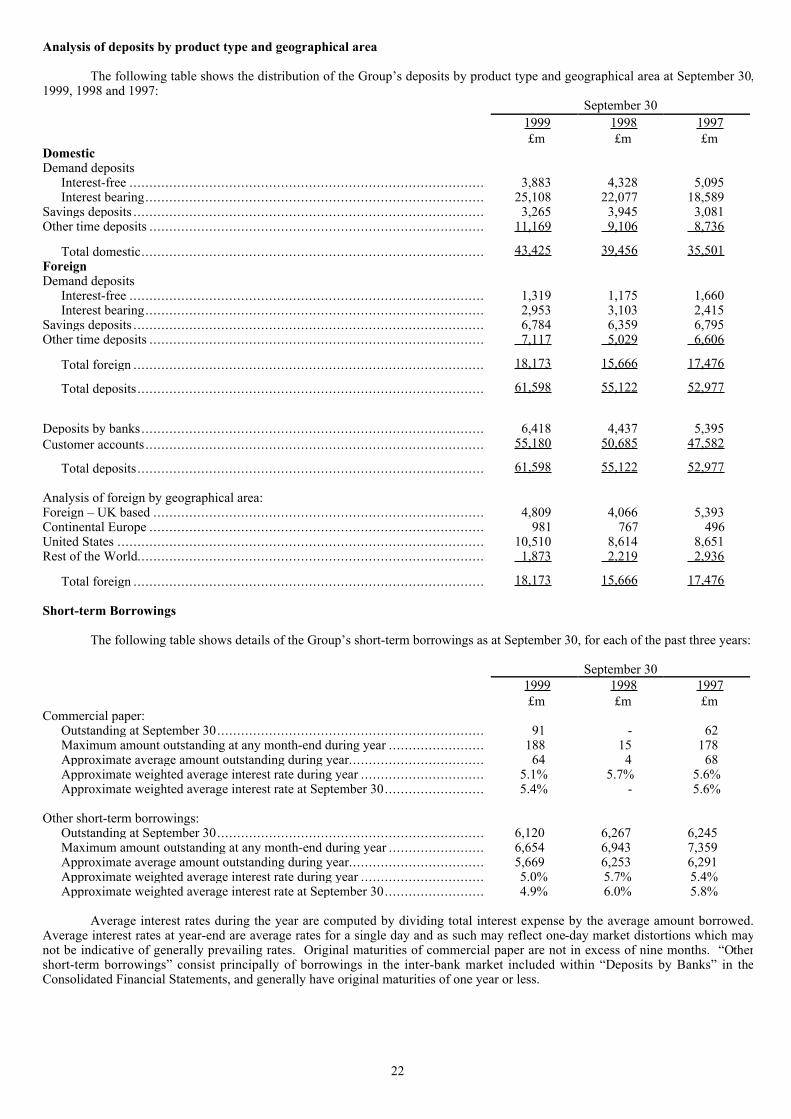

Analysis of deposits by product type and geographical area

The following table shows the distribution of the GroupÕs deposits by product type and geographical area at September 30,1999, 1998 and 1997:

SeptemberÊ301999 1998 1997£m £m £m

DomesticDemand deposits

Interest-free ......................................................................................... 3,883 4,328 5,095Interest bearing..................................................................................... 25,108 22,077 18,589

Savings deposits ........................................................................................ 3,265 3,945 3,081Other time deposits .................................................................................... 11,169 9,106 8,736