the road to namas - center for clean air policyccap.org/assets/the-road-to-namas_ccap.pdf · by...

TRANSCRIPT

The Road To NaMas

G lo b a l Sto r i e S o f S u cc e SS f u l c l i m at e ac t i o n S

abouT CCaPSince 1985, CCAP has been a recognized world leader in climate

and air quality policy and is the only independent, non-profit think

tank working exclusively on those issues at the local, national, and

international levels. Headquartered in Washington, D.C., CCAP

helps policymakers around the world to develop, promote and

implement innovative, market-based solutions to major climate, air

quality and energy problems that balance both environmental and

economic interests.

The Road To NaMasGlobal StorieS of SucceSSful climate actionS

aCkNowledgeMeNTsThese success stories were researched as part of the Center for Clean

Air Policy’s Mitigation Action Implementation Network (MAIN) program.

The primary authors of this report are Leila Yim Surratt, Tim Williams,

and Stacey Davis of CCAP. Significant contributions were provided

by Catherine Leining, Justine Sefton, Sonia Florian, Tomas Wyns, Julie

Cerqueira, Barry Elkinton, Kelly Clonts, and Michael Turner. A special

thanks to Brad Johnson, Ubaldo Inclan, Chuck Kooshian, Ignacio

Santelices, Anmol Vanamali, and Steve Winkelman for their input and

editorial assistance. This report was edited by Lisa Palmer and produced

by Star Dodd and Katy Nally.

This work was made possible by the generous support for the MAIN

program from Germany International Climate Initiative, Environment

Canada, the Kingdom of Denmark and other funders. CCAP is solely

responsible for the content of this report.

Table of CoNTeNTs4

6

8

14

20

26 32

38

44

50

56 62

MaP of suCCess sToRies

iNTRoduCTioN

baNgladeshDhaka’s Integrated Municipal Solid Waste Program

ChileTaking Initiative on Energy Efficiency

ChiNaExpanding Access to Energy Efficiency Finance Through the Use of Credit Guarantees

ColoMbiaReducing Traffic Congestion in Bogotá Through Bus Rapid Transit and Non-Motorized Transport

geRMaNy & ThailaNdAccelerating Renewable Energy Deployment with Feed-in-Tariffs

MexiCoPromoting Sustainable Growth in the Residential Sector

siNgaPoReImproving Building Efficiency with the Green Mark Scheme

swedeNDriving Industrial Energy Efficiency Through Energy Tax Rebates

ThailaNdRevolving and ESCO Funds for Renewable Energy and Energy Efficiency Finance

uNiTed sTaTesSmartWay Program Reduces Emissions from Freight Transport

p56

p20

p44

p8

p50

p32

p26

p14

p62

p38

UNITED STATES

MEXICO

COLOMBIA

CHILE

BRAZIL

NAMIBIA

SPAIN

BELGIUM

SWITZERLAND

GERMANY

SWEDEN

BULGARIA

PORTUGAL

SINGAPORE

MALAYSIABANGLADESH

INDIA

JAPANSOUTH KOREA

AUSTRALIA

THAILAND

CHINA

MaP of suCCess sToRies

4 the road to namas GLOBAL STORIES OF SUCCESSFUL CLIMATE ACTIONS 5

seCToRs

renewable enerGy

waSte

induStrial enerGy efficiency

buildinG enerGy efficiency

tranSport

In this publication

daRk blue

lighT blue

Read more stories online at www.ccap.org/road-to-namas

GLOBAL STORIES OF SUCCESSFUL CLIMATE ACTIONS 76 the road to namas

be designed to make the most of international financial support by spurring private sector investment. As a result of this work, we believe that NAMAs will be evaluated based on several core elements, including:

• The anticipated effectiveness of the NAMA, including the expected level of ambition in reducing greenhouse gas emissions, but also the expected sustainable development outcomes and plans to monitor, report and verify the actual results.

• The ability of the country to implement the NAMA, including strong leadership that has committed itself to the action, but also sufficient staff capacity and good planning.

• The size of the expected impact relative to the contributing country’s financial investment. The impact can be particularly high where funds are used to mitigate risks and overcome barriers that ripen conditions for private sector investments. Other considerations include careful budgeting that demonstrates funds will be managed and used effectively, commitment of a domestic financial contribution to the NAMA, and avoiding actions that are already supported as Clean Development Mechanism projects and where emissions reduced could be double counted.

In addition to thinking through the different design elements of a NAMA, a key aspect of our work has been harvesting and sharing the best examples of NAMA-like mitigation actions from around the world, with the idea that the NAMA framework can foster replication of the best examples. It is often the case that other countries faced similar policy, market, technical or financial barriers and have found successful solutions. One focus has been to identify and share examples where financing structures were used effectively to leverage donor funds by attracting private sector investment.

This body of work has helped our developing country partners identify and develop NAMAs, some of which are now entering the point where they can be considered for financial support. At the same time, our work has assisted the readiness of contributing countries preparing to invest in NAMAs.

exaMPles of suCCessful CliMaTe aCTioNs

The ten stories showcased in this book include examples from around the world where countries have implemented NAMA-like policies that have successfully reduced greenhouse gas emissions while contributing to measurable sustainable development outcomes. In conducting the research for this book, mitigation actions in both developed and developing countries were considered, specifically those within the five sectors: renewable energy, industrial energy efficiency, building energy efficiency, transport, and waste. The programs outlined in this book are particularly relevant for developing countries, utilize effective financial mechanisms that leveraged donor funds, and ultimately serve as good examples for a potential NAMA.

The stories in this book represent only a portion of the success stories we found from around the world. We encourage you to visit our website (www.ccap.org) to search through our more extensive database of climate action success stories.

We hope these success stories inspire policy makers to consider and identify new opportunities for reducing emissions in the context of sustainable development.

The UNFCCC Bali Action Plan (2007) called on developing countries to consider taking enhanced action on climate change mitigation through nationally appropriate mitigation actions (NAMAs). Central to the NAMA concept is that the actions should be in the context of sustainable development, and will be supported and enabled by international financing, technology, and capacity building.

At the UNFCCC conferences in Copenhagen in 2009 and Cancún in 2010, developed countries committed to mobilize USD 100 billion per year by 2020 to help developing countries reduce greenhouse gas emissions and adapt to the consequences of climate change. And also in 2010, the UNFCCC established the Green Climate Fund as a mechanism to deliver climate finance. While the Green Climate Fund is conceivably several years away from being fully operational, support for NAMA implementation is already starting to emerge through bilateral funding sources and multilateral institutions, and developing countries are now starting down the road to NAMAs.

The NAMA framework presents a critical opportunity to achieve broad-based emissions reductions in developing countries that lead to clear shifts in the emissions trajectory below business-as-usual levels. Rather than selling the lowest cost emission reduction opportunities to compliance buyers in developed countries (as in the case of the Clean Development Mechanism), through NAMAs, developing countries can take advantage of the available low cost opportunities to support achievement of their own voluntary pledges. Further, in undertaking NAMAs, developing countries will build experience in implementing mitigation actions and gain a better sense of the emissions reductions that are achievable in different sectors, informing their future deliberations on the scale of action that could be committed under a future climate agreement.

The UNFCCC opted not to create a formal definition for NAMAs, leaving the door wide open for developing countries to advance climate actions that are appropriate for their national circumstances. At the same time, this high level of flexibility creates some uncertainty over what might qualify as a NAMA and the parameters for accessing international support.

In this context, CCAP launched the Mitigation Action Implementation Network (MAIN) program in 2011 with initial funding from the German International Climate Initiative and with additional funding from Environment Canada and the Kingdom of Denmark. MAIN is increasing the capacity of developing countries in Latin America and Asia to design and develop ambitious NAMAs that can leverage contributing-country funds to achieve both greenhouse gas reduction and sustainable development goals. CCAP provides direct support to governments on the design of NAMAs and, through regional and global dialogues, engages policymakers and climate negotiators from both developing and contributing countries to build a shared understanding of NAMA opportunities and best practices.

As part of the MAIN program, CCAP has been working to educate stakeholders on the different components of a NAMA; how NAMAs might be evaluated; how monitoring, reporting, and verification can be used to build domestic political support while also demonstrating the action is taking place as planned and achieving progress in reducing greenhouse gas emissions; and on how NAMAs can

iNTRoduCTioN

9banGladeShbanGladeSh

wasTe

the bangladesh capital city develops an integrated municipal solid waste program

beyoNd wasTe

By some estimates, Bangladesh’s densely populated capital, Dhaka, is projected to generate more than 5,000 tons of waste each day by 2015—a 47 percent rise from its 2004 baseline of 3,400 tons per day.1,2 Rapid urban population growth and rising incomes have accelerated waste production, exceeding the government’s capacity to adequately manage the waste. Insufficient tax revenue, lax enforcement of the existing waste regulatory framework, and weak inter-agency coordination have further eroded the city’s waste management capacity. Dhaka has experienced a number of adverse impacts including high prevalence of disease, contaminated ground water and poor air quality. The waste sector in Bangladesh is also a significant contributor to greenhouse gas emissions because it generates methane, which is twenty-five times more potent as a greenhouse gas than carbon dioxide (CO

2).3 Excluding carbon

dioxide, this sector produced 17 million metric tons of CO2-equivalent in 2005, or 27

percent of the nation’s total non-CO2 emissions.4 By 2020, waste related emissions are

projected to increase by 22 percent, to 20 million metric tons.5

With financial and technical assistance from the Japan International Cooperation Agency, Dhaka designed a Solid Waste Master Plan in 2005 that set out to transform the municipal solid waste management system by 2015. The Plan sought to develop a participatory waste management program, build government capacity to collect and transport waste, modernize and expand disposal sites, and improve administration and financial management.

TRaNsfoRMiNg ThRough CooRdiNaTioN

The Master Plan manages municipal solid waste throughout its lifecycle and encourages public and private sector participation as cross-cutting themes.

waste Reduction: A National 3R (Reduce, Reuse, Recycle) Strategy was passed in 2010 establishing a 3R Wing at the Ministry of Environment and Forests to implement waste prevention activities, and an inter-ministerial committee to coordinate activities across ministries. To stimulate private sector investment in waste recycling and treatment plants, the strategy calls for the government to provide tax holidays, soft loans, and land to site the facilities. It also calls for research and development of resource-efficient products and processes that minimize chemical and energy waste. The strategy proposes public grants for educational and research institutions; and tax incentives, green industrial parks, and business incubators for industry.

dhaka’s integrated municipal Solid waste program

10 the road to namas 11banGladeSh

administration and financial Management: Each component of Dhaka’s solid waste management system was implemented by separate government offices. Without an overlaying regulatory framework or unifying authority, harmonizing plans and operations proved challenging. Therefore, a Waste Management Department was created to oversee waste operations. The Waste Management Department ultimately became responsible for coordinating the community-based collection efforts and overseeing the Landfill Management Unit. Another administrative challenge was insufficient tax revenue, which weakened the government’s capacity to support solid waste management. In response, The Plan created and implemented an integrated solid waste management cost accounting system, generating monthly cost figures to help the government better plan its waste expenditures and revenue stream to make the system financially sustainable.

wiNNiNg The wasTe baTTle

Implementation of the solid waste management system was successful despite significant delays in a number of areas including: establishing the Waste Management Department; securing sufficient government funding for the development of the Amin Bazar landfill; managing service providers under various departments; and overcoming a central government requirement to remove waste containers from main roads and collect and transport waste at night.10 The two semi-aerobic sanitary landfills, Matuail and Amin Bazar, are now in operation and managing 2,700 to 3,000 tons of waste per day.11

The Matuail landfill received Clean Development Mechanism (CDM) approval for methane recovery and utilization, and was projected to reduce 99,000 tons of CO

2-equivalent per year, directly and indirectly, in 2012.12 The city’s composting

facility was the first ever to receive CDM approval, and was projected to reduce 177,000 tons of CO

2-equivalent per year upon completion. The facility is also

expected to create up to 1,000 new jobs.13 Both CDM projects were financed by a Dutch corporation. The community-based approach to waste collection engaged residents to expand and improve services and improved the working conditions of service providers, thereby reducing occupational health hazards. Increased rates of collection and disposal have improved water and air quality, and expansion of the solid waste management system created opportunities for employment.

The Clean Dhaka Master Plan budgeted USD 44 million for development and capital costs, and USD 7.3 million per year for operations and maintenance (estimate for 2015).14,15 The Japanese government funded much of Dhaka’s waste management fleet—the Environmental Grant Aid Program donated 100 vehicles, valued at USD 5 million.16 The Japanese government also cancelled the debt incurred by Bangladesh for the purchase of 27 container carriers through the Debt Cancellation Fund. The Debt Cancellation Fund also financed the construction of the Matuail and Amin Bazar landfills. The Japan International Cooperation Agency provided technical support for designing and implementing the program.

The integrated solid waste management plan has spurred the development of a much needed waste-related regulatory framework, inspired replication across the country, and led to innovative measures of managing waste. Public and private infrastructure and services have continued to be expanded. Two wards are now receiving private collection and transportation services, and new landfill sites are being planned under the Dhaka Metropolitan Development Plan. The Dhaka model is being replicated in five other metropolitan cities across Bangladesh, financed by the Asian Development Bank’s Urban Public and Environmental Health Sector Development project. The six major cities established a secretariat to facilitate sharing of best practices through conferences, to prepare technical guidelines and to provide input to national solid waste management strategies and policies.

Regarding implementation efforts thus far, the government has established a tax holiday for all waste recycling and treatment plants for up to 10 years, reduced excise and import duties on relevant equipment, and eliminated sales tax on compost.6 Additionally, Dhaka implemented source separation of organic waste to reduce the amount of total waste that must be processed, and built a large scale commercial composting facility to convert 700 tons per day of organic waste to compost. Existing policies, such as a 2002 ban on polythene bags, have further supported waste reduction efforts.

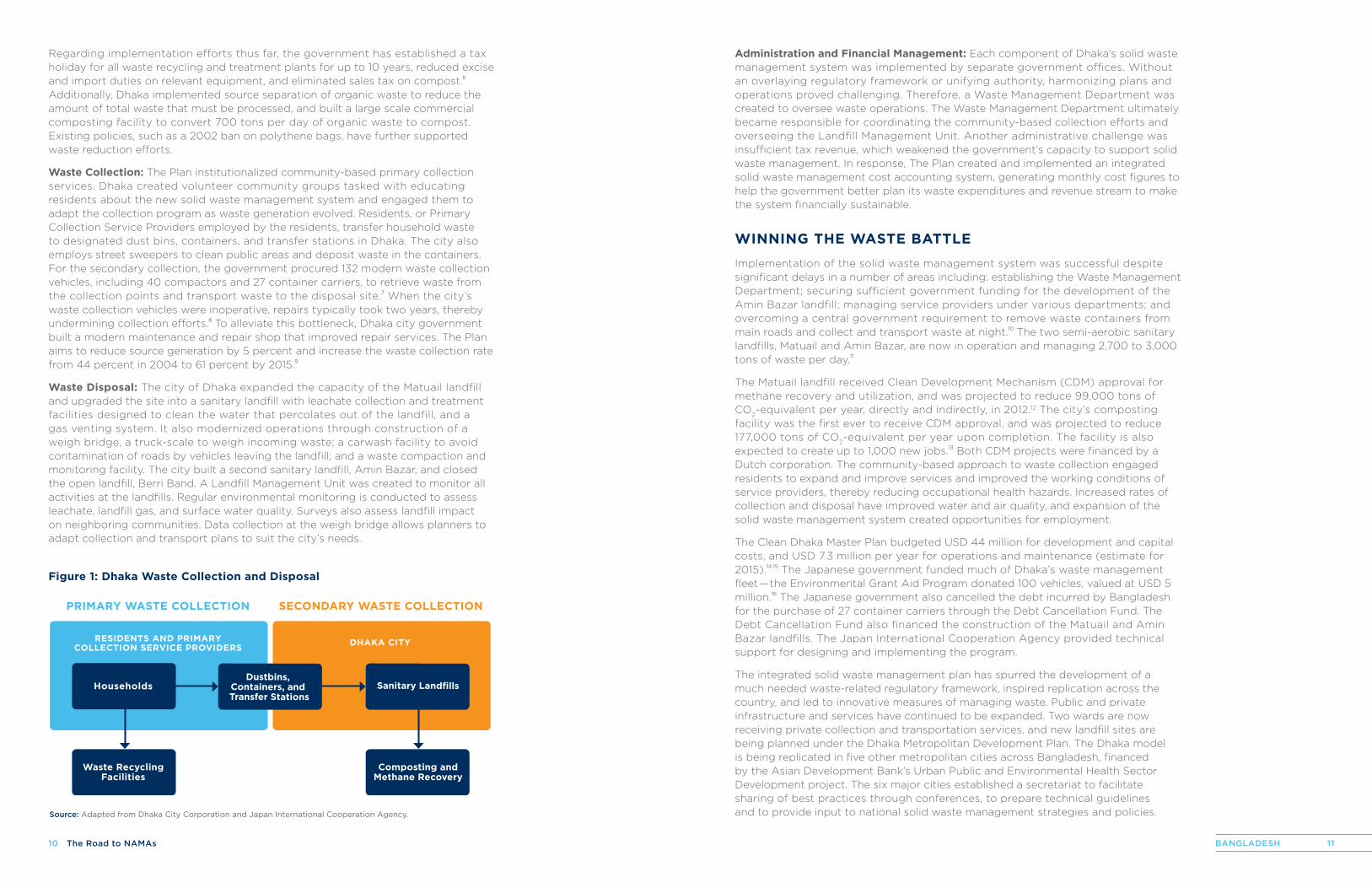

waste Collection: The Plan institutionalized community-based primary collection services. Dhaka created volunteer community groups tasked with educating residents about the new solid waste management system and engaged them to adapt the collection program as waste generation evolved. Residents, or Primary Collection Service Providers employed by the residents, transfer household waste to designated dust bins, containers, and transfer stations in Dhaka. The city also employs street sweepers to clean public areas and deposit waste in the containers. For the secondary collection, the government procured 132 modern waste collection vehicles, including 40 compactors and 27 container carriers, to retrieve waste from the collection points and transport waste to the disposal site.7 When the city’s waste collection vehicles were inoperative, repairs typically took two years, thereby undermining collection efforts.8 To alleviate this bottleneck, Dhaka city government built a modern maintenance and repair shop that improved repair services. The Plan aims to reduce source generation by 5 percent and increase the waste collection rate from 44 percent in 2004 to 61 percent by 2015.9

waste disposal: The city of Dhaka expanded the capacity of the Matuail landfill and upgraded the site into a sanitary landfill with leachate collection and treatment facilities designed to clean the water that percolates out of the landfill, and a gas venting system. It also modernized operations through construction of a weigh bridge, a truck-scale to weigh incoming waste; a carwash facility to avoid contamination of roads by vehicles leaving the landfill; and a waste compaction and monitoring facility. The city built a second sanitary landfill, Amin Bazar, and closed the open landfill, Berri Band. A Landfill Management Unit was created to monitor all activities at the landfills. Regular environmental monitoring is conducted to assess leachate, landfill gas, and surface water quality. Surveys also assess landfill impact on neighboring communities. Data collection at the weigh bridge allows planners to adapt collection and transport plans to suit the city’s needs.

figure 1: dhaka waste Collection and disposal

Composting andMethane Recovery

Waste RecyclingFacilities

Sanitary LandfillsDustbins,

Containers, and Transfer Stations

Households

DHAKA CITYRESIDENTS AND PRIMARYCOLLECTION SERVICE PROVIDERS

PRIMARY WASTE COLLECTION SECONDARY WASTE COLLECTION

Source: Adapted from Dhaka City Corporation and Japan International Cooperation Agency.

12 the road to namas 13banGladeSh

RefeReNCes

Yousuf, Tariq Bin. 2011. “Clean Dhaka Master Plan: An Experience of ODA in Municipal Solid Waste Management.” International Solid Waste Association—Publications. Web. September 2012. <http://www.iswa.org/en/76/publications.html>

Dhaka City Corporation and Japan International Cooperation Agency. October 2007. “Implementation of Clean Dhaka Master Plan: Progress Report 1.” Web. September 2012. <http://www.dhakacity.org/cleandhaka/Documents/progress1.pdf>

Dhaka City Corporation and Japan International Cooperation Agency. 2005. “Clean Dhaka Master Plan: Final Report.” Web. September 2012. <http://www.dhakacity.org/cleandhaka/Documents/CleanDhakaMasterPlanMain.pdf>

eNdNoTes

1 Dhaka City. 2005. “State of the Environment 2005.” Web. September 2012. <http://www.rrcap.unep.org/pub/soe/dhaka-soe-05/3-4dhaka-noise.pdf>

2 Yousuf, Tariq Bin. 2011. “Clean Dhaka Master Plan: An Experience of ODA in Municipal Solid Waste Management.” International Solid Waste Association - Publications. Web. September 2012. <http://www.iswa.org/en/76/publications.html>

3 Intergovernmental Panel on Climate Change. 2007. “Working Group I Fourth Assessment Report: The Physical Science Basis. Chapter 2.” IPCC Working Group I. Web. September 2012. <https://www.ipcc-wg1.unibe.ch/publications/wg1-ar4/wg1-ar4.html>

4 Excludes emissions from land-use, land-use change and forestry.

5 U.S. Environmental Protection Agency. 2011. “Emissions and Projections of Non-CO

2Greenhouse Gases from Developing

Countries: 1990-2030.” Web. August 21, 2012. <http://www.epa.gov/climatechange/EPAactivities/economics/nonco2projections.html>

6 Hasnat, Abu and Maqsood Sinha. “Public-Private Partnership and Decentralized Composting Approach in Dhaka, Bangladesh.” Waste Concern presentation at IPLA Global Forum 2012 on Empowering Municipalities in Building Zero Waste Society—A Vision for the Post-Rio-20 Sustainable Urban Development. Seoul, Republic of Korea, September 5-6, 2012. Web. September 2012. <http://www.uncrd.or.jp/env/ipla/doc/120905Sinha-Waste%20Concern-Bangladesh.pdf>

7 Yousuf, 2011, op cit.

8 Ibid.

9 Dhaka City Corporation and Japan International Cooperation Agency. 2005. “Clean Dhaka Master Plan: Final Report.” Web. September 2012. <http://www.dhakacity.org/cleandhaka/Documents/CleanDhakaMasterPlanMain.pdf>

10 Dhaka City Corporation and Japan International Cooperation Agency. October 2007. “Implementation of Clean Dhaka Master Plan: Progress Report 1.” Web. September 2012. <http://www.dhakacity.org/cleandhaka/Documents/progress1.pdf>

11 Communication from DCC dated May 31, 2012.

12 Government of Bangladesh. 2004. “CDM Project Design Document: Landfill Gas Extraction and Utilization at the Matuail landfill site Dhaka, Bangladesh.” Web. September 2012. <http://cdm.unfccc.int/Projects/projsearch.html>

13 Government of Bangladesh. 2004. “CDM Project Design Document: Composting of Organic Waste in Dhaka.” Web. September 2012. <http://cdm.unfccc.int/Projects/projsearch.html>

14 Currency exchange rate of Bangladesh Taka 81.5 = USD 1 converted on August 22, 2012.

15 Dhaka City Corporation and Japan International Cooperation Agency, 2005, op cit.

16 Currency exchange rate of Japan Yen 78.0 = USD 1 converted on September 30, 2012.

17 Alam, Helemul. “Power from garbage: Govt-run plant to generate 50MWelectricity using garbage of Dhaka city.” The Daily Star, August 8, 2012. Web. September 2012. <http://www.bangladeshnews24.com/thedailystar/2012/08/18/power-from-garbage-govt-run-plant-to-generate-50mw-electricity-using-garbage-of-dhaka-city-11555.htm>

figure references

figure 1: dhaka waste Collection and disposalAdapted from Dhaka City Corporation and Japan International Cooperation Agency.

Dhaka is building on its success by initiating a waste-to-energy project on a “build, own, operate, transfer” basis. A private firm will build an incineration plant and an anaerobic digestion plant on two landfill sites in Dhaka. The power plants will initially have a generating capacity of 10 megawatts and will process 1,000 tons of waste per day, with plans to scale up each facility to 50 megawatts at a processing rate of 5,000 tons of waste per day within three years.17

15chilech ile

chile accelerates its energy efficiency efforts

effeCTive leadeRshiP

As a nation with only modest fossil fuel resources, Chile has carved out a reputation as one of Latin America’s strongest actors on energy efficiency. In 2005, in response to earlier shortages of natural gas imports and droughts which limited hydropower generation, Chile redefined its energy strategy, stressing energy efficiency as a core national priority and establishing a National Energy Efficiency Program.1 Since then, the importance of energy efficiency in Chile has grown substantially, which has been reflected in the federal budget. From 2006 to 2009, the annual budget of the National Energy Efficiency Program increased from USD 1 million to more than USD 34 million.2

Chile reformed its institutional framework for energy efficiency over the last decade and in November 2010 it established the Chilean Energy Efficiency Agency to take over the implementation of energy efficiency policies and initiatives. The Chilean Energy Efficiency Agency is structured as an independent, nonprofit organization which draws on resources from the public as well as private sectors to support the competitiveness and sustainable development of Chile.3 In its role as a public-private institution, it also coordinates and informs the actions of relevant stakeholders at the local, national, and global levels. In 2012, Chile featured energy efficiency as the first component of its National Energy Strategy for 2012 to 2020, which has set an ambitious goal to reduce 2020 projected energy demand by 12 percent through improved energy efficiency.4

a RaNge of eNeRgy effiCieNCy MeasuRes

Since the outset of its energy efficiency efforts in 2005, Chile has initiated a number of significant programs, including:

Chilean energy efficiency standards and labeling Program: This program established a regulatory and labeling framework for electrical products sold in the country. The aim is to provide consumers with clear information about the efficiency of a range of appliances and equipment, and to offer a metric for product comparison. Following the lead of other Latin American countries which have implemented labeling practices, the program requires International Organization for Standardization test procedures to be used. Labeling is mandatory for incandescent and compact fluorescent light bulbs, as well as certain appliances such as refrigerators, microwaves, air conditioning units, and televisions.5

taking initiative on energy efficiency

iNdusTRial eNeRgy effiCieNCy

buildiNg eNeRgy effiCieNCy

16 the road to namas 17chile

conservation. This outreach complemented Chile’s other efforts and helped to reduce the nation’s energy intensity while sustaining economic growth. In 2008, net energy demand in the grid serving 93 percent of the population declined by 1.2 percent despite economic growth of 3.2 percent.22

Over the next decade, Chile plans to continue pursuing energy efficiency successes by introducing stronger regulations and new financial mechanisms to expand credit access. The country is developing regulations on minimum energy performance standards for appliances. Chile is also looking to expand credit access for energy efficiency measures by partnering with the Global Environment Facility to implement a partial credit guarantee program. This program will overcome financial barriers by reducing the risk of lending to energy service companies through guaranteeing payments in the event of a loan default.

light up good energy: Through this initiative, Chile purchased and distributed compact fluorescent light bulbs (CFLs) to residents within the most vulnerable 40 percent of the population. Purchases were made through the state procurement agency, ChileCompra.6 The CFLs, which are up to five times more efficient than traditional incandescent bulbs, allow families to save up to 25 percent on their monthly electricity bills.7 The program commenced in 2008 with the distribution of 1.5 million CFLs, and was extended in 2009 through early 2010 with the distribution of an additional 1.4 million CFLs. Over its duration, Light up Good Energy resulted in the distribution of 2.9 million CFLs at a total cost of USD 8.8 million.8

subsidy on electric Motors: Chile’s industrial and mining sectors account for about 38 percent of primary energy consumption in the country.9 These sectors, particularly the mining industry, are heavily dependent on small motors to generate on-site power for various tasks. In 2009, Chile initiated a program to encourage the replacement of traditional motors with higher-efficiency motors, which are up to 12 percent more energy efficient.10 The program, which ran through 2010 and had a total budget of USD 2.5 million, subsidized the purchase of efficient electric motors at a rate which attempted to match their cost with the cost of purchasing a standard motor.11,12 The subsidy, which was available to efficient motors ranging from 1 to 10 horsepower, resulted in the replacement of over 5,000 motors in 2009 and 2010.13,14

Pre-investment in energy efficiency: In 2006, Chile launched a program to facilitate the implementation of energy efficiency measures in the private sector, particularly small and medium sized enterprises. It works towards this goal by providing technical and financial assistance to these firms to help them minimize their energy consumption. Financial assistance is provided through a direct subsidy for consulting services, which are used to assess potential energy savings, create implementation plans, and conduct financial analyses for energy efficiency measures. Companies with annual net sales up to USD 33 million are eligible for support, with the condition that services are carried out by an accredited consultant. The program covers up to 70 percent of the total consultation costs, up to a maximum of USD 10,000.15 From the launch of this program through December 2009, 154 contracts were approved, of which 110 had completed their final report.16

energy efficiency Credit line: In 2008, a new credit line was introduced with resources provided by the Chilean Economic Development Agency and the German development bank KfW, with a goal to finance energy efficiency measures in businesses. The credit line is available to a variety of sectors and can be used to finance a range of projects, including procurement of machinery and equipment, construction, and engineering and assembly services.17 Credit is disbursed through commercial banks with a maximum of USD 1 million, provided at a preferential fixed interest rate with payment terms of two to 12 years and grace periods of up to 18 months.18 Chile’s energy efficiency credit line supports companies, production cooperatives, and associations with annual net sales up to USD 33 million.19

eNeRgy effiCieNCy gaiNs

Chile has received international praise for its efforts to improve energy efficiency. In 2010, the Alliance to Save Energy, a leading nonprofit organization that promotes energy efficiency worldwide, honored Chile with its EE Visionary Award, which showcases the world’s best practices in energy efficiency policy and implementation.20

From 2005 to 2011, Chile consistently reduced its energy intensity, achieving a reduction of over 10 percent, as shown in Figure 1.21 Chile’s achievements were possible because of the high level of support for energy efficiency from the public as well as political leaders. Several public education and awareness campaigns by the Chilean government highlighted the importance of energy efficiency and

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

0.160

0.150

0.140

0.130

0.120

0.1 10

0.100

0.1

56

0.1

48

0.1

43

0.1

37

0.1

39

0.1

36

0.1

40 0.1

48

0.1

48

0.1

59

0.1

53

0.1

45

0.1

47

0.1

43

0.1

44

0.1

40

0.1

36

0.1

31

0.1

30

0.1

30

0.1

24

0.1

25

figure 1: Chile energy intensity 1990–2011

Source: Enerdata. “Global Energy Statistical Yearbook 2012.”

*US dollars at constant exchange rate, price and purchasing power parities of the year 2005

kto

e p

er

un

it o

f G

dp

(u

Sd

20

05

*)

18 the road to namas 19chile

RefeReNCes

Chilean Energy Efficiency Agency. “About Program.” Web. September 2012. <http://www.acee.cl/576/propertyvalue-13094.html>

International Energy Agency. 2009. “Chile Energy Policy Review: 2009.” Web. September 2012. <http://www.iea.org/textbase/nppdf/free/2009/chile2009.pdf>

Lutz, Wolfgang et al. July 2011. “The National Energy Efficiency Standards and Labeling Program of Chile.” CLASP and LBNL. Web. September 2012. <http://www.scribd.com/doc/92222448/National-EE-S-L-Program-of-Chile-Review>

eNdNoTes

1 Chilean Energy Efficiency Agency. “About Program.” Web. September 2012. <http://www.acee.cl/576/propertyvalue-13094.html>

2 International Energy Agency. 2009. “Chile Energy Policy Review: 2009.” Web. September 2012. <http://www.iea.org/textbase/nppdf/free/2009/chile2009.pdf>

3 Mellado, Pamela M. “Public Buildings Energy Efficiency Program (PEEEP) National Agency for Energy Efficicency.” Chilean Energy Efficiency Agency. Web. September 2012. <http://www.jiko-bmu.de/files/basisinformationen/application/pdf/11-pamela_mellado,_chile.pdf>

4 Ministry of Energy, Chile. February 2012. “National Energy Strategy 2012-2020.” Web. September 2012. <http://pds.kallman.com/shows/iftenergy_2012/pdfs/Energy-for-the-Future-Chile’s-National-Energy-Strategy-2012-2030-English.pdf>

5 Lutz, Wolfgang et al. July 2011. “The National Energy Efficiency Standards and Labeling Program of Chile.” CLASP and LBNL. Web. September 2012. <http://www.scribd.com/doc/92222448/National-EE-S-L-Program-of-Chile-Review>

6 Ibid.

7 Ibid.

8 Institute of Energy Economics, Japan. “Compendium of Energy Efficiency Policies of APEC Economies.” Web. September 2012. <http://www.ieej.or.jp/aperc/CEEP/Chile.pdf>

9 Asia-Pacific Economic Cooperation. April 14, 2009. “Peer Review on Energy Efficiency in Chile – Final Report.” Web. September 2012. <http://www.ieej.or.jp/aperc/PREE/PREE_Chile.pdf>

10 Institute of Energy Economics, Japan, op cit.

11 Lutz, Wolfgang et al, 2005, op cit.

12 Cancino, Paola Andrea Martínez. April 2010. “Análisis del Recambio de Refrigeradores Energéticamente Eficientes como Medida de Eficiencia Energética y Propuestas de Implementación.” Universidad de Chile. Web. September 2012. <http://www.tesis.uchile.cl/tesis/uchile/2010/cf-martinez_pc/pdfAmont/cf-martinez_pc.pdf>

13 Chilean Energy Efficiency Agency. “Incentivo a la introducción de motores eléctricos eficientes en la industria: ‘Usa motores eficientes’.” Web. September 2012. <http://www.acee.cl/576/article-58878.html>

14 Institute of Energy Economics, Japan, op cit.

15 Chilean Energy Efficiency Agency. “Programa de Preinversión en Eficiencia Energética.” Web. September 2012. <http://www.acee.cl/576/article-59194.html>

16 Global Environment Fund. October 2010. “Request for CEO endorsement/approval. GEFSEC Project ID: 4176.” Web. October 2012. <http://www.thegef.org/gef/sites/thegef.org/files/documents/document/11-04-2010-ID4176%20Council%20doument.pdf>

17 Chilean Energy Efficiency Agency. “Crédito CORFO Eficiencia Energética.” Web. October 2012. <http://www.acee.cl/576/article-59200.html>

18 Global Environment Fund, 2010, op cit.

19 Ibid.

20 Alliance to Save Energy. May 6, 2010. “International Energy Efficiency ‘Visionaries’ from Four Continents to Be Honored May 11 at EE Global Forum.” Alliance to Save Energy. Web. October 2012. <http://ase.org/news/international-energy-efficiency-%E2%80%98visionaries%E2%80%99-four-continents-be-honored-may-11-ee-global-forum>

21 Enerdata. “Global Energy Statistical Yearbook 2012.” Web. October 2012. <http://yearbook.enerdata.net/#/energy-intensity-GDP-by-region.html>

22 Maxwell, Amanda. 2010. “At the EE Global Forum, ASE Prize Highlights Chile’s Efficiency Achievements.” Switchboard, May 13, 2010. Web. October 2012. <http://switchboard.nrdc.org/blogs/amaxwell/at_the_ee_global_forum_ase_pri.html>

figure references

figure 1: Chile energy intensity 1990–2011Enerdata. “Global Energy Statistical Yearbook 2012.” Web. October 2012. <http://yearbook.enerdata.net/#/energy-intensity-GDP-by-region.html>

iNdusTRial eNeRgy effiCieNCy

Due to its rapid economic growth, China’s burgeoning energy demand has created significant challenges to its energy security and sustainable development. In the face of this dual challenge, leaders have emphasized energy efficiency as a top priority for the country. From 1980 to 2000, China reduced its energy intensity, as measured by energy use per unit of gross domestic product, by an average rate of about 5 percent per year.1 It achieved these results mainly through subsidies and regulations geared toward its substantial industrial sector.2 However, by the early 2000s this trend had reversed due to a number of factors, including: rising domestic energy consumption; a rapid increase in the production and export of energy-intensive goods; and an expansion in construction.

China worked to increase private sector investment in energy efficiency, but had limited success because financial institutions lacked experience in dealing with energy efficiency projects. Lending decisions were based mostly on the value of

figure 1: Chuee Program design

ESCOs,Utilities,Vendors

Banks

CHUEE

IndustrialEnergy Users

Equipment andEngineering Services

TechnicalAssistance

TechnicalAssistance

Loan Guarantees andTechnical Assistance

Loans

Loans

CorporateAgreements

Source: Independent Evaluation Group, World Bank.

21chinachinaexpanding access to energy efficiency finance through the use of credit Guarantees

china develops a market for energy efficiency

gReeN loaNs To iNdusTRial ClieNTs

22 the road to namas 23china

asset collateral (balance sheet financing) rather than on expected project-based cash flow (project financing), which hindered the ability of energy service companies to access credit.3

In 2004, China turned to the International Finance Corporation for help in designing a new private-sector based finance initiative for energy efficiency. This effort led to creation of the China Utility-Based Energy Efficiency Finance Program (CHUEE), a new risk-sharing mechanism meant to increase the availability of private investment for energy efficiency projects. (Figure 1). Although the program was originally expected to focus on a gas utility, the design changed due to geographic and strategic differences between the gas utility and participating banks. The design that ultimately materialized focused on large banks with industrial clients, rather than small clients supported by lending through the gas utility. It was rolled out in two phases beginning in 2006, with a third phase currently in planning. CHUEE set an initial target to reduce emissions by 8.6 million tons of carbon dioxide (CO

2) per year

by 2012 under a base case scenario, which was later increased to 13.6 million tons of CO

2 per year by the end of the second phase in 2015.4

Chuee iMPleMeNTed To oveRCoMe PeRCeived Risk iN eNeRgy effiCieNCy PRojeCTs

CHUEE supports the implementation of energy efficiency improvements in two major ways. First, it provides a risk-sharing facility through partial credit guarantees to local banks for qualified energy efficiency loans. Second, it provides technical assistance to relevant stakeholders, including banks, energy service companies, and end-users. In addition to these two major activities, CHUEE engages in market outreach through information dissemination.

Through the first two phases of the program, the International Finance Corporation committed USD 207 million for the risk-sharing facility.5 This support is leveraged by a USD 16.5 million grant from the Global Environment Facility to cover the initial losses (“first loss tranche”) of the guarantee, as well as by donations from the Government of Finland (USD 4 million) and the Government of Norway (USD 3 million).6 The funds are used to support three major private financial institutions in China. The Industrial Bank was the first bank to participate. Its focus is on lending to large industrial corporations and has been the primary recipient of CHUEE guarantees. The Bank of Beijing and the Shanghai Pudong Development Bank also joined the pool of private investors in 2007 and 2009, respectively.

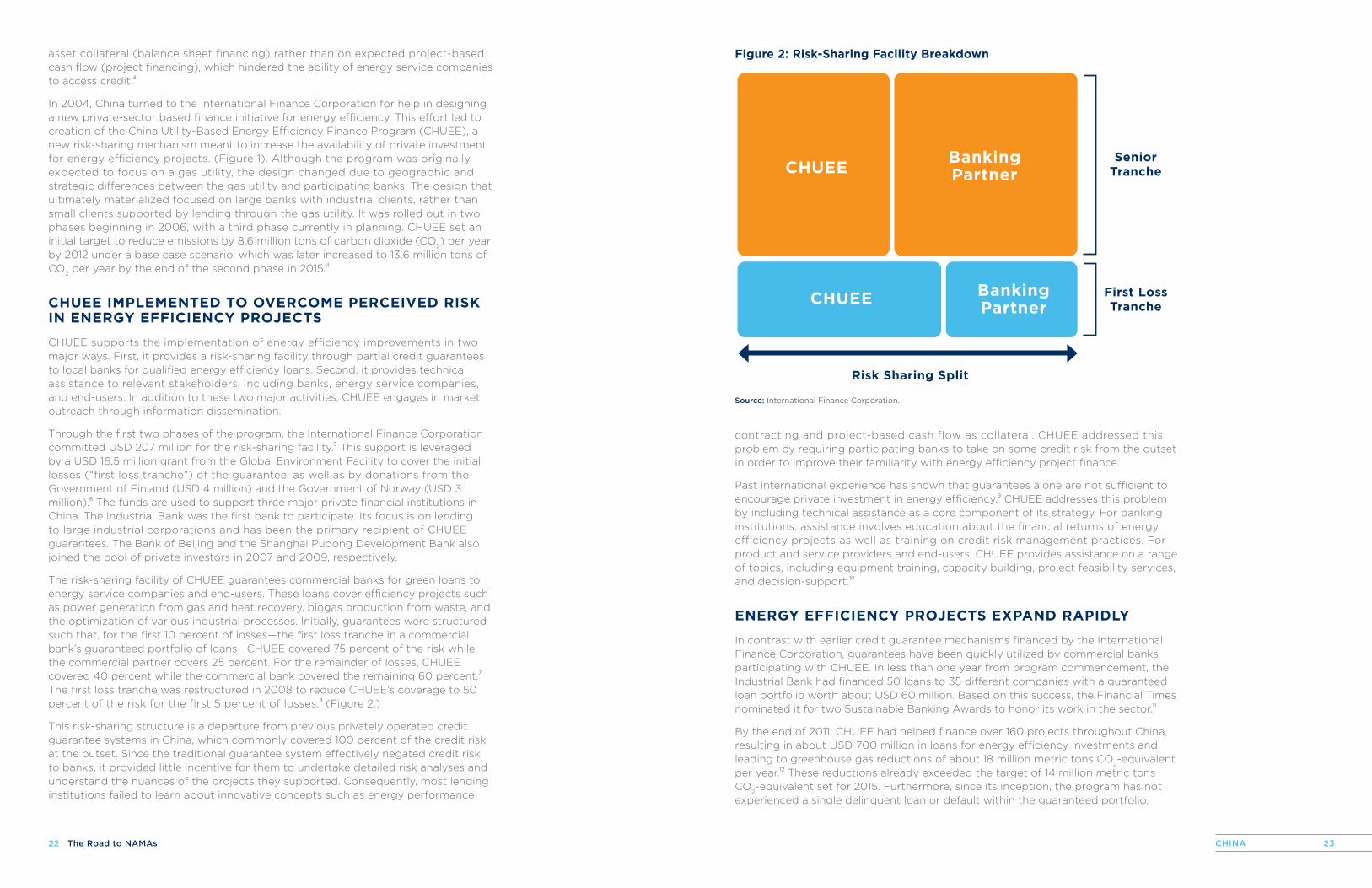

The risk-sharing facility of CHUEE guarantees commercial banks for green loans to energy service companies and end-users. These loans cover efficiency projects such as power generation from gas and heat recovery, biogas production from waste, and the optimization of various industrial processes. Initially, guarantees were structured such that, for the first 10 percent of losses—the first loss tranche in a commercial bank’s guaranteed portfolio of loans—CHUEE covered 75 percent of the risk while the commercial partner covers 25 percent. For the remainder of losses, CHUEE covered 40 percent while the commercial bank covered the remaining 60 percent.7 The first loss tranche was restructured in 2008 to reduce CHUEE’s coverage to 50 percent of the risk for the first 5 percent of losses.8 (Figure 2.)

This risk-sharing structure is a departure from previous privately operated credit guarantee systems in China, which commonly covered 100 percent of the credit risk at the outset. Since the traditional guarantee system effectively negated credit risk to banks, it provided little incentive for them to undertake detailed risk analyses and understand the nuances of the projects they supported. Consequently, most lending institutions failed to learn about innovative concepts such as energy performance

contracting and project-based cash flow as collateral. CHUEE addressed this problem by requiring participating banks to take on some credit risk from the outset in order to improve their familiarity with energy efficiency project finance.

Past international experience has shown that guarantees alone are not sufficient to encourage private investment in energy efficiency.9 CHUEE addresses this problem by including technical assistance as a core component of its strategy. For banking institutions, assistance involves education about the financial returns of energy efficiency projects as well as training on credit risk management practices. For product and service providers and end-users, CHUEE provides assistance on a range of topics, including equipment training, capacity building, project feasibility services, and decision-support.10

eNeRgy effiCieNCy PRojeCTs exPaNd RaPidly

In contrast with earlier credit guarantee mechanisms financed by the International Finance Corporation, guarantees have been quickly utilized by commercial banks participating with CHUEE. In less than one year from program commencement, the Industrial Bank had financed 50 loans to 35 different companies with a guaranteed loan portfolio worth about USD 60 million. Based on this success, the Financial Times nominated it for two Sustainable Banking Awards to honor its work in the sector.11

By the end of 2011, CHUEE had helped finance over 160 projects throughout China, resulting in about USD 700 million in loans for energy efficiency investments and leading to greenhouse gas reductions of about 18 million metric tons CO

2-equivalent

per year.12 These reductions already exceeded the target of 14 million metric tons CO

2-equivalent set for 2015. Furthermore, since its inception, the program has not

experienced a single delinquent loan or default within the guaranteed portfolio.

figure 2: Risk-sharing facility breakdown

Source: International Finance Corporation.

SeniorTranche

First LossTranche

Risk Sharing Split

CHUEEBankingPartner

CHUEE BankingPartner

24 the road to namas 25china

In addition to the CHUEE program, other government policies supporting energy efficiency measures also contributed to the rapid uptake of energy efficiency projects in China. For example, China’s state-owned banks provide direct loans for energy efficiency projects to large state-owned enterprises and public banks were banned from lending to the steel and cement industry unless the loans were for energy efficiency projects.13 These policies led to a surge of lending by the public sector banks for energy efficiency.

Despite the success of CHUEE, the program has received some criticism for failing to accommodate small to medium-sized enterprises, as had originally been intended. Although the program envisioned that over half of the loans would be in the USD 200,000 range, by 2010 these loans only accounted for about 10 percent of the total, and the actual average loan size was USD 5.7 million.14 Small to medium-sized enterprises continue to present challenges to private investors due to higher transaction costs and higher risks compared to larger firms. However, the newest phase of CHUEE is addressing this problem by developing innovative mechanisms geared towards local financial institutions with larger shares of small to medium-sized clients. These mechanisms may involve non-traditional financial partners, such as large energy service companies or property developers, which could play a role in sharing first loss risks.

CHUEE has been a valuable program to help private banks develop the institutional capacity for energy efficiency lending. In particular, a World Bank study found that private banks involved in the program became much more likely to accept project-finance based collateral than non-participating banks. Furthermore, loans with CHUEE backing had longer maturities on average than loans without backing.15 The CHUEE model has since been replicated in the Philippines, and there are new efforts to expand the mechanism to promote water savings in addition to energy efficiency.16

RefeReNCes

International Finance Corporation. “China Utility-Based Energy Efficiency Finance Program (CHUEE): Frequently Asked Questions.” Web. October 2012. <http://www1.ifc.org/wps/wcm/connect/regprojects_ext_content/ifc_external_corporate_site/home_chuee/about+us/faqs/faqs?RSF>

Independent Evaluation Group, World Bank. 2010. “Assessing the Impact of IFC’s China Utility-based Energy Efficiency Finance Program.” Web. October 2012. <https://openknowledge.worldbank.org/bitstream/handle/10986/2480/555490PUB0Ener1EPI1992912801PUBLIC1.pdf?sequence=1>

eNdNoTes

1 Wang Can and Lu Xuedu. “Mitigation potentials in China and perspectives on cooperation opportunities.” Tsinghua University presentation, Dialogue on Future International Actions to Address Global Climate Change and Clean Development Mechanism . Paris, France, April 19-22, 2006. Web. October 2012. <http://www.ccap.org/docs/resources/266/Can_Xuedu-China_Mitigation_potential_and_cooperation_opportunities-Joint_Dialogue.pdf>

2 Independent Evaluation Group, World Bank. 2010. “Assessing the Impact of IFC’s China Utility-based Energy Efficiency Finance Program.” Web. October 2012. <https://openknowledge.worldbank.org/bitstream/handle/10986/2480/555490PUB0Ener1EPI1992912801PUBLIC1.pdf?sequence=1>

3 Ellis, Jennifer. May 2010. “Energy Service Companies (ESCOs) in Developing Countries.” International Institute for Sustainable Development. Web. October 2012. <http://www.iisd.org/pdf/2009/bali_2_copenhagen_escos.pdf>

4 Independent Evaluation Group, World Bank, 2010, op cit.

5 Ibid.

6 International Finance Corporation. “Cooperation Agreement on CHUEE II with Norad Signed in Beijing.” Web. October 2012. <http://www1.ifc.org/wps/wcm/connect/regprojects_ext_content/ifc_external_corporate_site/home_chuee/news/events/event7>

7 Institute for Industrial Productivity. “China Utility-Based Energy Efficiency Finance Program (CHUEE).” Web. October 2012. <http://www.iipnetwork.org/sites/iipnetwork.org/files/file_attachments/resources/IIP-11.%20FinanceCaseStudyA.pdf>

8 Independent Evaluation Group, World Bank, 2010, op cit.

9 Ibid.

10 International Finance Corporation. “China Utility-Based Energy Efficiency Finance Program (CHUEE): Frequently Asked Questions.” Web. October 2012. <http://www1.ifc.org/wps/wcm/connect/regprojects_ext_content/ifc_external_corporate_site/home_chuee/about+us/faqs/faqs?RSF>

11 International Finance Corporation. “China Utility-based Energy Efficiency Finance Program (CHUEE): One Finance Solution to Climate Change.” Web. October 2012. <http://www.nengyuanguanli.com/uploadFiles/files/201001/UPFI201001060932485776.pdf>

12 International Finance Corporation. “China Utility-based EnergyEfficiency Finance Program (CHUEE).”Web. October 2012. <http://www1.ifc.org/wps/wcm/connect/0f680e004a9ad992af9fff9e0dc67fc6/Chuee+brochure-English-A4.pdf?MOD=AJPERES>

13 Independent Evaluation Group, World Bank, 2010, op cit.

14 Ibid.

15 Ibid.

16 Ibid.

figure references

figure 1: Chuee Program designIndependent Evaluation Group, World Bank. 2010. “Assessing the Impact of IFC’s China Utility-based Energy Efficiency Finance Program.” Web. October 2012. <https://openknowledge.worldbank.org/bitstream/handle/10986/2480/555490PUB0Ener1EPI1992912801PUBLIC1.pdf?sequence=1>

figure 2: Risk-sharing facility breakdownInternational Finance Corporation. “China Utility-based Energy Efficiency Finance Program (CHUEE): One Finance Solution to Climate Change.” Web. October 2012. <http://www.nengyuanguanli.com/uploadFiles/files/201001/UPFI201001060932485776.pdf>

27colombiacolombia

TRaNsPoRT

rapid transit and routes for human-powered transportation are key to addressing traffic congestion in bogotá, colombia

sTeeRiNg CleaR of CoNgesTioN

Bogotá’s bus rapid transit system and network of non-motorized transport infrastructure has become the exemplar for nations grappling with congested roadways, growing urban populations, and rising transport-related greenhouse gas emissions. Centered around the TransMilenio Bus Rapid Transit, the city’s multimodal transit system and innovative policies have made inroads in reducing traffic congestion, accidents, crime, and air pollution. For example, before TransMilenio, commutes averaged 1.5 hours in each direction, with private vehicles accounting for less than one-fifth of trips yet occupying 95 percent of roads.1 Now, average commute times in Bogotá have been cut by 20 minutes, air quality has improved by 40 percent, and accidents have decreased by 79 percent.2,3 While problems still exist, such as crime and traffic congestion, Bogotá remains a commonly cited success story of comprehensive transportation planning.

In the early 1990’s, Bogotá Mayor Antanas Mockus initiated a Citizen Culture campaign with the intention of changing public behavior towards community and civility. Using unorthodox techniques such as mimes, Mockus was able alter how residents viewed the relationship between motor vehicles and pedestrians, thereby laying the foundation for investment in a pioneering public transport system. The subsequent administration, led by Mayor Enrique Peñalosa, responded to the transit crisis with a Mobility Strategy that prioritized public transit and non-motorized transport modes, reduced private vehicle use, and induced a

behavioral shift towards the use of alternative transport options. The national government has since built upon Bogotá’s success by expanding comprehensively planned transit systems to eight other cities. Colombia is also considering implementing a Sustainable Urban Development Nationally Appropriate Mitigation Action (NAMA) to focus real estate development

reducing traffic congestion in bogotá through bus rapid transit and non-motorized transport

TransMilenio station and express lanes

28 the road to namas 29colombia

through local fuel taxes (46 percent), national government grants (20 percent), a World Bank loan (6 percent) and other local funds (28 percent).6 Phase II cost USD 545 million (USD 13 million per km) and was financed through the national government (66 percent) and a local fuel surcharge (34 percent).7 Unlike many public transport systems, the TransMilenio does not receive any operational subsidies. Bogotá is also moving forward with its first metro rail system; funding has been approved by the World Bank and detailed engineering studies have begun.

Finally, Bogotá implemented an education campaign to generate awareness and demand for the new system. Partially funded by a private bank, the city held community and business meetings, advertisements and events, and offered three weeks of free service on the TransMilenio.

easiNg The CoMMuTe, ReduCiNg gReeNhouse gases

The Mobility Strategy has successfully shifted residents to non-motorized and public transportation. At a cost of USD 147,000 per km, the bicycle routes are utilized by 200,000 to 285,000 people per day, quadrupling bike ridership since their inception.8,9 In addition, over one million riders are estimated to use the temporary bike paths each weekend.10 Car restrictions coupled with easy access to transport alternatives have caused 9 percent of car owners to shift to public transport. Before the TransMilenio, buses traveled at average speeds of 17 km per hour, with some corridors below five km per hour. Bogotá’s policies increased average bus speed to 26 km per hour, reducing the average commute time by 32 percent (20 minutes). Of Bogotá’s 8.5 million residents, the TransMilenio moves 47,000 passengers per hour per direction, or over 1.5 million riders each day.11,12

One of the most significant challenges in implementing the Bus Rapid Transit system was resistance from existing bus operators who feared loss of business and hesitated to use new processes such as awarding concessions through open bidding. They were also concerned about financial risks from investments in a new fleet and government capacity to build planned infrastructure and eliminate current operators. These challenges were overcome by prioritizing existing operators in the bidding process, establishing a fund to offset negative impacts to the operators, and including these companies in a dialogue with the city during the planning and implementation phases.13

around high-quality transit systems supported by pedestrian-accessible land use. The NAMA would create a framework to overcome financial and procedural barriers to transit-oriented development with pilot launches in two Colombian cities and national policy and capacity-building to expand sustainable urban development in cities across Colombia.

huMaN PoweRed aNd CaR-fRee

Bogotá implemented four notable projects to promote non-motorized mobility. The city built a 344 km city-wide network of bicycle routes for daily commuting. On Sundays and holidays, the government also closes 121 km of roads to create temporary bike paths for recreational use from 7 am to 2 pm. A citizen ballot consultation on vehicle use lead to the establishment of an annual Car Free Day the first Thursday of every February, during which private vehicle use is prohibited across the city. Walking is an important mode of transportation for many—especially the urban poor—thus the city created a 17 km pedestrian corridor that connects low-income neighborhoods with commercial and business districts.

To reduce the use of private vehicles, Bogotá created a roadway restriction based on license plate numbers. Vehicles with license plates ending in odd numbers are prohibited from using roadways on odd-numbered days, and those with plates ending in even numbers are prohibited from using roadways on even-numbered days. The restriction is in effect during morning and evening weekday commuting hours.4

The keystone of Bogotá’s Mobility Strategy is the TransMilenio Bus Rapid Transit system. The TransMilenio operates 87 km of trunk corridors that receive passengers from an integrated feeder system. The system increased efficiency through pre-boarding automated fare collection, free transfers, raised platforms for quick boarding and exiting, high occupancy vehicles (160 to 260 passengers), segregated bus lanes, and express routes. A single fare cross-subsidizes the poor, who often live on the city periphery. All buses comply with Euro II emission standards and are equipped with GPS that allows a centralized management system to respond in real-time to contingencies and re-route buses to meet demand. Pedestrian and bike pathways are integrated into the system, with free bike parking available at many terminals.

TransMilenio is a public-private partnership. The government entity TransMilenio S.A. is comprised of technical experts and was created specifically to plan, manage, and control the Bus Rapid Transit system. A consolidated management structure allows companies to compete through an open bidding process for concessions to supply and operate the bus fleet and the fare collection and validation system. Infrastructure costs are paid for by the city and national government, and operational costs are assumed by the private sector. The government retains control over the operation schedule, thereby shifting demand risk to the private sector.

Phase I of the TransMilenio became operational in 2001. Phase II came on-line in 2006, and became the first transportation project to receive approval as a Clean Development Mechanism. To meet monitoring, reporting and verification requirements, a special unit under the supervision of TransMilenio S.A. collects, reports, and stores all data. Passenger surveys supply information on prior transport mode, fuel type, and fuel efficiency to determine emissions abatement through modal shifts.

Ultimately, Bogotá expects to build a total of 388 km of corridors at a cost of USD 5 million per km.5 Phase I and II are complete and Phase III, which will extend the corridors an additional 36 km, is currently under construction. Phase I of the TransMilenio cost USD 240 million (USD 5.9 million per km) and was financed

Temporary weekend bike Paths

30 the road to namas 31colombia

eNdNoTes

1 Martinez, Astrid. “Energy Efficiency in Massive Public Transport Systems —Transmilenio: A Study Case.” Presentation at the UN Forum on Energy Efficiency and Energy Security, December 18, 2007. Web. August 2012. <http://www.un.org/esa/sustdev/sdissues/energy/op/forum_dec07/presentations/S51_ortiz.pdf>

2 Center for Clean Air Policy. January 2012. “Case Study: Colombia’s Bus Rapid Transit Development and Expansion.” Web. August 2012. <http://www.ccap.org/docs/resources/1080/Colombia-case%20study-final.pdf>

3 United Nations Development Program. “Bogotá, Colombia Bus Rapid Transit Project—TransMilenio Case Study.” Web. August 2012. <http://www.ncppp.org/undp/bogota.html>

4 City Government of Bogotá, Colombia. Pico y Placa website. Web. July 25, 2012. <http://www.movilidadbogota.gov.co/?sec=410>

5 United Nations Framework Convention on Climate Change. October 3, 2012. “Clean Development Mechanism Project Design Document—Bogotá, Colombia: TransMilenio Phase II to IV v5.4.” Web. October 2012. <http://cdm.unfccc.int/Projects/DB/DNV-CUK1159192623.07/view >

6 U.S. Department of Transportation. 2006. “Applicability of Bogotá’s TransMilenio BRT System to the United States.” Web. October 2012. <http://www.fta.dot.gov/documents/Bogota_Report_Final_Report_May_2006.pdf>

7 Ibid.

8 NYC Global Partners. May 4, 2011. “Best Practice: Largest Bicycle Path Network.” Web. September 2012. <http://www.nyc.gov/html/unccp/gprb/downloads/pdf/Bogota_CycleRoute.pdf>

9 City Government of Bogotá, Colombia. Web. July 30, 2012. <http://www.movilidadbogota.gov.co/?sec=71>

10 City Government of Bogotá. Web. July 26, 2012. <http://www.bogota.gov.co/portel/libreria/php/frame_detalle_scv.php?h_id=24777>

11 Penalosa, Enrique. “Equity and Mobility.” New Statesman. February 23, 2012. Web. August 2012. <http://www.newstatesman.com/transport/2012/02/mobility-cars-city-bus-cities>

12 City Government of Bogotá, Colombia. Transmilenio website. Web. July 26, 2012. <http://www.transmilenio.gov.co/WebSite/Contenido.aspx?ID=TransmilenioSA_TransmilenioEnCifras_EstadisticasGenerales>

13 Center for Clean Air Policy, 2012, op cit.

14 TransMilenio, S.A. February 2012. “Informe de Gestión 2011.” Web. August 2012. <http://www.transmilenio.gov.co/AdmContenidoUpload/administrador.contenido/Documents/Informe%20de%20Gesti%C3%B3n%202011.pdf>

15 Center for Clean Air Policy. January 14, 2010. “Transportation NAMAs: A Proposed Framework.” Web. August 2012. <http://ccap.org/docs/resources/924/CCAP_Transport_NAMA.pdf>

16 Rosenthal, Elisabeth. “Buses May Aid Climate Battle in Poor Cities.” New York Times, July 9, 2009. Web. August 2012. <http://www.nytimes.com/2009/07/10/world/americas/10degrees.html?_r=2>

17 United Nations Development Program, op cit.

18 Ibid.

19 The World Bank. 2010. “From Chaos to Order: Implementing High-Capacity Urban Transport Systems in Colombia.” Web. August 2012. <http://siteresources.worldbank.org/NEWS/Resources/Colombia_mass_transit_4-23-10.pdf>

figure references

figure 1: benefits achieved by bogotá’s Mobility strategyAdapted from the United Nations Development Program, the World Bank, and the City Government of Bogotá, Colombia.

The TransMilenio’s impact on emissions has been significant: from 2001 to 2010, the Bus Rapid Transit system abated 1.9 million metric tons of CO

2-equivalent, with

an annual average of 144,000 tons under Phase I alone (2001-2005) and 236,000 tons under Phases I and II combined (2006-2010).14 This greenhouse gas estimate is likely conservative due to multiplier effects from transit-oriented development that enhance non-motorized transport and reduce trip lengths.15 Moving forward, Colombia is pursuing a national sustainable urban development policy and NAMA to further amplify these benefits.

By 2009, Bogotá was able to decommission 7,000 small private buses from its roads, reducing the use of bus fuel by more than 59 percent.16 According to the United Nations Development Program, the system has reduced air pollutants by 40 percent; and decreased fatalities by 92 percent, injuries by 75 percent, and collisions by 79 percent along its trunk lines.17 Robberies at traffic stops have also been reduced by 83 percent.18 The Bus Rapid Transit system has successfully formalized a portion of the transport sector by awarding contracts for the operation of the TransMilenio fleet and related services to select, legal companies; and integrating bus operators and drivers from the informal sector into the new system. This has resulted in shorter work days for bus drivers, from 14 to 8 hours; the provision of social security benefits for employees; and securing tax contributions from bus operators.19 Other co-benefits include temporary jobs created by infrastructure development, a 15 to 20 percent increase in property values along the main trunk route, improved health outcomes from clean air and exercise, and overall improved quality of life.

RefeReNCes

Hidalgo, Dario and Graftieaux, Pierre. “A Critical Look at Major Bus Improvements in Latin America and Asia: Case Study TransMilenio, Bogotá, Colombia.” World Bank. Web. August 2012. <http://siteresources.worldbank.org/INTURBANTRANSPORT/Resources/Hidalgo-Graftieaux-BOGOTA.pdf>

Deutsche Gesellschaft für Internationale Zusammenarbeit (GIZ). May 2007. “The CDM in the Transport Sector—Sustainable Transport: A Sourcebook for Policy-makers in Developing Cities.” Web. August 2012. <https://www.giz.de/Themen/en/SID-9DEECDB1-4ECE4077/dokumente/en-cdm-transport-sector-2007.pdf>

Center for Clean Air Policy. January 2012. “Case Study: Colombia’s Bus Rapid Transit Development and Expansion.” Web. August 2012. <http://www.ccap.org/docs/resources/1080/Colombia-case%20study-final.pdf>

Pico y Placa website. <http://www.movilidadbogota.gov.co/?sec=410>

TransMilenio website. <http://www.transmilenio.gov.co/WebSite/Default.aspx>

figure 1: benefits achieved by bogotá’s Mobility strategy

benefitS achieved by boGotá’S mobility StrateGy

• commute times reduced by 32%

• bus driver work days shortened by 6 hours

• air quality improved by 40%

• GhGs reduced by 2 million tonnes co2-equivalent

• bus fuel use reduced by 59%

• collisions along trunk lines decreased by 79%

• fatalities along trunk lines decreased by 92%

• injuries along trunk lines decreased by 75%

• robberies at traffic stops decreased by 83%

• property values along trunk lines increased by 15-20%

• improved health outcomes from reduced pollution and exercise

• overall improved quality of life for residents

Source: Adapted from the United Nations Development Program, the World Bank, and the City Government of Bogotá, Colombia.

33Germany & thailand

Germany &thailand

The Feed-in tariff (FIT) is a policy mechanism that requires electric utilities to purchase electricity from renewable energy producers at predetermined rates. This, in turn, guarantees a market for the electricity produced by renewable energy sources, such as wind and solar, and makes an attractive return on investment for renewables.

Since the 1990s, FITs have stimulated renewable energy investments, particularly in Europe, but also in many other regions throughout the world. They are the most widely used policy tool for accelerating the deployment of renewable energy. By 2012, 65 countries and 27 states and provinces around the world will have put FIT policies into effect.1

When a country or municipality implements a FIT policy, the predetermined electricity rates generally involve an added premium above the market rates. Either the government pays the premium, or the ratepayers do, through surcharges on utility bills. The rates are typically set by long-term contracts with renewable generators, which usually include guarantees for generators to have access to the grid. In most FIT regimes, rates are set to reflect the costs of various renewable energy technologies, with higher rates offered for more expensive technologies. Technology-specific rates allow countries to leverage all of their renewable energy resources regardless of the technology’s maturity. Countries can also prioritize certain technologies to meet national objectives for energy development.

FITs can be tailored to provide support on a fixed basis, or can vary depending on the spot-market electricity price. The two options, known respectively as a fixed-price tariff and a premium-price tariff, each have strengths and weaknesses, and can have significantly different impacts on a market’s uptake of renewable energy projects.

A fixed-price tariff:

• Sets a constant price per unit of energy through the duration of a contract.

• Provides stability for expected future revenues, which reduces risk to investors and therefore reduces project financing costs.2

• Can be a challenge for policymakers to implement. Tariffs set too low may be ineffective at encouraging investment, while tariffs set too high may be overly generous, potentially leading to over-subscription and budgetary constraints.

accelerating renewable energy deployment with feed-in-tariffs

ReNewable eNeRgy

fit policies are versatile and used worldwide

sTiMulaTiNg ReNewable eNeRgy

34 the road to namas 35Germany & thailand

reached 91 TWh. (Figure 1). FITs have helped overcome many barriers to renewable energy deployment in Germany, including:7

• A distorted ‘playing field’ due to existing infrastructure and support measures for conventional sources of energy;

• High initial capital costs for renewable technologies;

• Lack of legal framework for independent power producers;

• Difficulty in gaining access to the grid;

• Perceived technology performance uncertainty and risk.

Due to strong growth in electricity generated from renewable sources, the cost of the policy increased from under USD 5 billion in 2004 to approximately USD 20 billion in 2011.8 In 2008, an average German household paid a surcharge of about 5 percent of their total electricity bill. However, the surcharge is expected to decline over the next two decades due to declining costs of renewable technologies coupled with rising prices for conventional energy.9

In 2006, energy producers supported by the German FIT system generated revenue totaling over USD 17 billion, which represented over 60 percent of total domestic renewable energy revenue. From 2004 to 2008, the number of jobs in the German renewable energy industry increased 75 percent, from about 160,000 in 2004 to 280,000 in 2008.10 Furthermore, shifts in electricity generation resulting from the FIT helped reduce greenhouse gas emissions by approximately 70 million metric tons in 2011.11

As the cost of renewable technologies like solar and wind continues to decline, Germany is lowering its FIT rates for new contracts according to a schedule which accounts for their improved competitiveness and declining costs. Due to the rapid uptake of solar power, Germany has further scaled back support in this area. It recently added a maximum size limit of 10 megawatts (MW); changed eligibility such

that only 90 percent of electricity from commercial-scale producers can receive the FIT; and set an overall 52 gigawatt (GW) cap on FIT support for solar power.12,13 Germany also added a new FIT option, which allows renewable energy producers to sell electricity at market prices and receive a variable adder premium in place of a fixed-price tariff. The new option is designed to help renewable energy producers become comfortable with electricity markets and ultimately increase their participation in the wholesale marketplace.

ThailaNd offeRs suPPoRT To sMall PRoduCeRs of ReNewable eNeRgy

A key component of Thailand’s strategy involves incentivizing and removing barriers to renewable generation by small power producers with generation capacities up to 90 MW.14 Thailand supports renewable and non-conventional energy producers with fixed adder rates for electricity generation.15 Energy producers are categorized as Very Small Power Producers with capacities less than 10 MW, and Small Power

A premium-price tariff:

• Sets a price equal to the spot-market electricity price plus an additional premium, known as an ‘adder’.

• Has two basic options for the adder: a fixed adder or a variable adder that depends on the spot-price. A fixed adder is easier to implement; the FIT payments are simply the sum of the spot-market electricity price and the adder. However, fixed adder FITs do not address instability in spot-prices and can result in large swings in project revenue if the market is volatile. A variable adder provides a larger subsidy when the spot-price is low, and tapers off the subsidy when the spot-price increases. Although more complex to implement, this method can create stable investment conditions while ensuring that renewable projects are profitable.

FITs are feasible in a range of political and institutional contexts, and a large number of them have been put into effect around the world. Two countries that showcase the success of FITs in very different circumstances are Germany and Thailand:

germany employs fixed-price tariffs for a range of technologies. FITS are central to its goal of obtaining 35 percent of its electricity from renewable sources by 2020.

Thailand uses a fixed adder tariff to encourage small renewable energy producers. Thailand’s FIT policies support its target to increase the share of renewable energy from about 9 percent of total energy consumption in 2011 to 25 percent in 2021.

In both cases, the goal of the FIT is to remove barriers to investment by improving the competitiveness and cash flow certainty of renewable energy projects. Each country’s approach is discussed in greater detail below.

geRMaNy PioNeeRs NaTioNal fiT PoliCy

Germany implemented the first national FIT policy in Europe in 1991, allowing renewable energy producers to sell their electricity to utilities at a fixed percentage of the retail electricity price. This system was effective at deploying coastal wind and hydropower electricity, but failed to encourage investment in more cutting-edge technologies such as solar generation. To address this problem, Germany shifted to a model based on the actual costs of renewable energy generation rather than a market-based rate. This cost-based framework offers a competitive advantage to a variety of renewable technologies with varying generation capacities, and remains one of the most important elements of successful FIT policies.3

In the German system, rates are set in 20-year contracts to cover the cost of renewable energy production plus a profit of 5 to 7 percent for developers.4 Although utilities pay the developers directly for their power, they pass on the costs of the tariffs to their electricity customers via a surcharge on electricity bills. Therefore, the program remains independent of government budgets and subsidies.

The FIT program in Germany has resulted in a sharp increase in the production of renewable energy, which grew from 3 percent of total energy production in 1990 to 20 percent by the first half of 2011.5 Electricity generation from projects supported by FITs grew from approximately 38.5 terawatt hours (TWh) in 2004 to about 75 TWh in 2009—about 79 percent of all renewable electricity generated that year.6 In 2011 this figure

figure 1: sample Rates under germany fiT Program as of october 2012 (usd/kwh)*

*Rates vary by size of installation. Cited rates do not include special bonuses for project-specific attributes. Conversion rate: 1 EUR = 1.3 USD; from oanda.com on 10/22/2012

Source: Lang, Matthias and U. Mutschler.

hydro 0.04-0.17

biomaSS 0.08-0.19

wind 0.05-0.20

Solar 0.17-0.24

Ge

rm

an

y f

it p

ro

Gr

am

Renewable energy deployment with feed-in-Tariffs

36 the road to namas 37Germany & thailand

RefeReNCes

Couture, T. D., Cory, K., Kreycik, C., & Williams, E. 2010. “A Policymaker’s Guide to Feed-in Tariff Policy Design [Technical Report No. NREL/TP-6A2-44849].” U.S. National Renewable Energy Laboratory.

Fulton, Mark and Reid Capalino. September 2012. “The German Feed-in-Tariff: Recent Policy Changes.” DB Research, Deutsche Bank. <http://www.dbresearch.com/PROD/DBR_INTERNET_EN-PROD/PROD0000000000294376/The+German+Feed-in+Tariff%3A+Recent+Policy+Changes.pdf>

Tongsopit, Sopitsuda and Chris Greacen. “Thailand’s Renewable Energy Policy: FiTs and Opportunities for International Support.” WRI-ADB Workshop on Feed-in Tariffs. Manila, Phillippines, February 21-23, 2012. <http://pdf.wri.org/wri_fair_fit_workshop_presentation_thailand_tongsopit_greacen.pdf>

eNdNoTes

1 Renewable Energy Policy Network for the 21st Century. 2012. “Renewables 2012 Global Status Report. Paris, France: REN21.” Web. October 2012. <http://www.ren21.net/>

2 Cory, Karlynn, Toby Couture and Claire Kreycik. March 2009. “Feed-in Tariff Policy: Design, Implementation, and RPS Policy Interactions.” U.S. National Renewable Energy Laboratory.

3 Couture, T. D., Cory, K., Kreycik, C., & Williams, E. 2010. “A Policymaker’s Guide to Feed-in Tariff Policy Design (Technical Report No. NREL/TP-6A2-44849).” U.S. National Renewable Energy Laboratory.

4 Stokes, Bruce. “What, Exactly, Is a Feed-In Tariff?” National Journal, April 25, 2009. Web. October 2012. <http://www.nationaljournal.com/njmagazine/nj_20090425_3763.php>

5 EU Climate Policy Tracker 2011. Web. October 2012. <http://www.climatepolicytracker.eu/>

6 Bundesministerium fur Umwelt, Naturschutz und Reaktorsicherheit (BMU). 2009. “Electricity from Renewable Energy Sources: What does it cost?” Web. October 2012. <https://www.bmu.de/english/renewable_energy/downloads/publ/36865.php>

7 World Future Council. 2007. “Feed-In Tariffs: Boosting Energy for our Future. A guide to one of the world’s best environmental policies.” Hamburg, Germany: WFC. Web. October 2012. <www.hermannscheer.de/en/images/stories/pdf/WFC_Feed-in_Tariffs_jun07.pdf>

8 Bundesministerium fur Umwelt, Naturschutz und Reaktorsicherheit (BMU). July 2012. “Development of renewable energy sources in Germany 2011.” 2012 Graphics and tables based on statistical data from the Working Group on Renewable Energy-Statistics (AGEE-Stat). Web. October 2012. <http://www.erneuerbare-energien.de/files/english/pdf/application/pdf/ee_in_deutschland_graf_tab_en.pdf>

9 Bundesministerium fur Umwelt, Naturschutz und Reaktorsicherheit (BMU), 2009, op cit.

10 Motl, B. 2011. “Reconciling German-Style Feed-In Tariffs with PURPA.” Wisconsin International Law Journal, 28(4), 742–767.

11 Bundesministerium fur Umwelt, Naturschutz und Reaktorsicherheit (BMU), 2012, op cit.

12 Lang, Matthias and U. Mutschler. “German Feed-in Tariffs 2012.” German Energy Blog. Web. October 19, 2012. <http://www.germanenergyblog.de/?page_id=8617>

13 Fulton, Mark and Reid Capalino. September 2012. “The German Feed-in-Tariff: Recent Policy Changes.” DB Research, Deutsche Bank.Web. October 2012. <http://www.dbresearch.com/PROD/DBR_INTERNET_EN-PROD/PROD0000000000294376/The+German+Feed-in+Tariff%3A+Recent+Policy+Changes.pdf>

14 Ruangrong, P. 2008. “Thailand’s Approach to Promoting Clean Energy in the Electricity Sector.” Paper presented at the Forum on Clean Energy, Good Governance and Regulation, Singapore, March 16-18, 2008. Web. October 2012. <http://electricitygovernance.wri.org/files/egi/Thailand.pdf>

15 Ibid.

16 Tongsopit, Sopitsuda and Chris Greacen. 2012. “Thailand’s Renewable Energy Policy: FiTs and Opportunities for International Support.” WRI-ADB Workshop on Feed-in Tariffs. Manila, Phillippines, February 21-23, 2012. Web. October 2012. <http://pdf.wri.org/wri_fair_fit_workshop_presentation_thailand_tongsopit_greacen.pdf>