the ric report - merrill lynch ric report ... leading global indicators suggest that earnings growth...

TRANSCRIPT

BofA Merrill Lynch does and seeks to do business with issuers covered in its research reports. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. Refer to important disclosures on page 35 to 36. 11718828

The RIC Report Beyond our borders

14 March 2017

Scaling up our forecasts We’ve raised our year-end forecast for the S&P500, and now expect three Fed rate hikes this year, including one on March 15.

Japan favorite developed equity market We believe that favorable economic growth and inflation in Japan along with coordinated monetary and fiscal policy will drive domestic demand and boost Japanese equity prices. The weakening in the yen vs the dollar that we expect should favor cyclical stocks.

Europe in holding pattern Leading global indicators suggest that earnings growth among European companies should accelerate over the remainder of this year. Earnings should also benefit from recovering commodity prices, disciplined capital spending and expanding margins. However, risk that the political landscape becomes more unstable from upcoming elections in the Netherlands, France and Germany keeps us neutral for now.

Maintain favorable view on Emerging Market stocks Emerging Market central banks appear more synchronized with the US, reducing the risk of currency depreciation. The earnings picture has improved with expanding operating margins and free cash flow. However, Asia has near-term challenges, as China balances growth with financial stability amid talk of trade conflicts with the US. We prefer Russia and Brazil.

Limited appeal of bonds outside the US We believe that bond market allocations outside the US should be concentrated in dollar-denominated sovereign and corporate Emerging Markets, but even that market we would approach with caution for the near-term.

Disruptive trends add excitement to auto sector Four trends that are disrupting the auto sector—electrification, autonomous driving, connectivity and shared mobility—are likely to forge a paradigm shift to a future where cars are greener, safer, faster, and available on-demand. See the ideas section, page 11.

Investment Strategy Global

Table of Contents

Financial markets recap 2

Beyond our borders 3

The market’s message to the Fed 9

The future of autos 11

RIC asset class views 17

Fixed Income, Economics, Commodities,

Currencies: views and risks 18

Global equity markets: views and risks 19

Asset allocation for individual investors 20

US Equity Strategy Sector Views 25

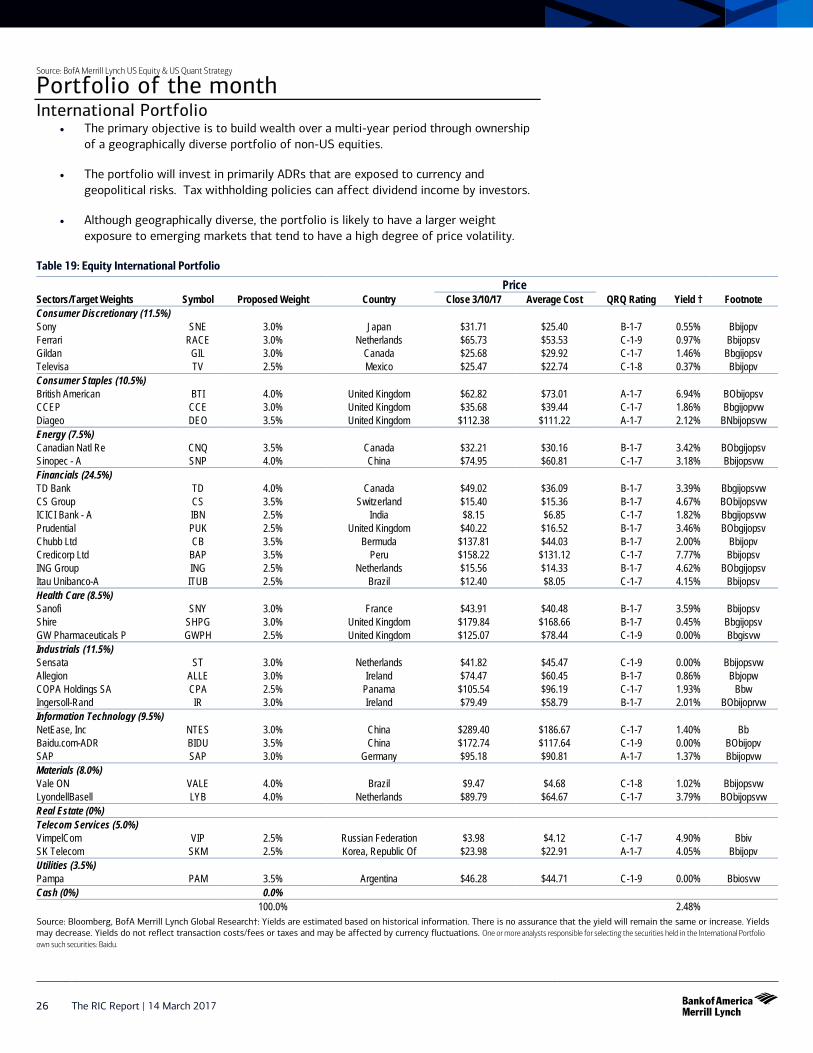

Portfolio of the month 26

Stock lists 27

US economic forecast summary 31

Global economic forecast summary 32

Interest rate forecast summary 32

FX rate forecast summary 32

Research Analysts 36

Research Investment Committee MLPF&S

Martin Mauro Fixed Income Strategist MLPF&S

Cheryl Rowan Portfolio Strategist MLPF&S

Matthew Trapp, CFA Investment Strategist MLPF&S

See Team Page for List of Analysts

Timestamp: 14 March 2017 12:01AM EDT

2 The RIC Report | 14 March 2017

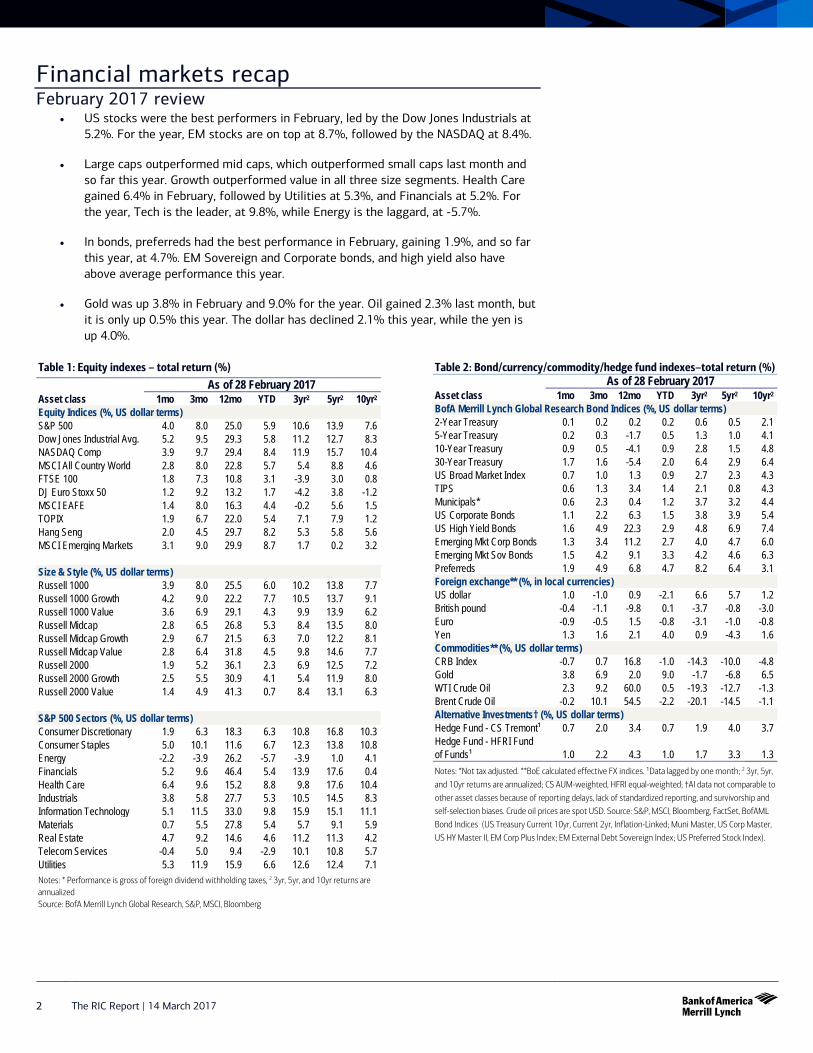

Financial markets recap February 2017 review

• US stocks were the best performers in February, led by the Dow Jones Industrials at5.2%. For the year, EM stocks are on top at 8.7%, followed by the NASDAQ at 8.4%.

• Large caps outperformed mid caps, which outperformed small caps last month andso far this year. Growth outperformed value in all three size segments. Health Caregained 6.4% in February, followed by Utilities at 5.3%, and Financials at 5.2%. Forthe year, Tech is the leader, at 9.8%, while Energy is the laggard, at -5.7%.

• In bonds, preferreds had the best performance in February, gaining 1.9%, and so farthis year, at 4.7%. EM Sovereign and Corporate bonds, and high yield also haveabove average performance this year.

• Gold was up 3.8% in February and 9.0% for the year. Oil gained 2.3% last month, butit is only up 0.5% this year. The dollar has declined 2.1% this year, while the yen isup 4.0%.

Table 1: Equity indexes – total return (%) As of 28 February 2017

Asset class 1mo 3mo 12mo YTD 3yr2 5yr2 10yr2 Equity Indices (%, US dollar terms) S&P 500 4.0 8.0 25.0 5.9 10.6 13.9 7.6 Dow Jones Industrial Avg. 5.2 9.5 29.3 5.8 11.2 12.7 8.3 NASDAQ Comp 3.9 9.7 29.4 8.4 11.9 15.7 10.4 MSCI All Country World 2.8 8.0 22.8 5.7 5.4 8.8 4.6 FTSE 100 1.8 7.3 10.8 3.1 -3.9 3.0 0.8 DJ Euro Stoxx 50 1.2 9.2 13.2 1.7 -4.2 3.8 -1.2MSCI EAFE 1.4 8.0 16.3 4.4 -0.2 5.6 1.5 TOPIX 1.9 6.7 22.0 5.4 7.1 7.9 1.2 Hang Seng 2.0 4.5 29.7 8.2 5.3 5.8 5.6 MSCI Emerging Markets 3.1 9.0 29.9 8.7 1.7 0.2 3.2

Size & Style (%, US dollar terms) Russell 1000 3.9 8.0 25.5 6.0 10.2 13.8 7.7 Russell 1000 Growth 4.2 9.0 22.2 7.7 10.5 13.7 9.1 Russell 1000 Value 3.6 6.9 29.1 4.3 9.9 13.9 6.2 Russell Midcap 2.8 6.5 26.8 5.3 8.4 13.5 8.0 Russell Midcap Growth 2.9 6.7 21.5 6.3 7.0 12.2 8.1 Russell Midcap Value 2.8 6.4 31.8 4.5 9.8 14.6 7.7 Russell 2000 1.9 5.2 36.1 2.3 6.9 12.5 7.2 Russell 2000 Growth 2.5 5.5 30.9 4.1 5.4 11.9 8.0 Russell 2000 Value 1.4 4.9 41.3 0.7 8.4 13.1 6.3

S&P 500 Sectors (%, US dollar terms) Consumer Discretionary 1.9 6.3 18.3 6.3 10.8 16.8 10.3 Consumer Staples 5.0 10.1 11.6 6.7 12.3 13.8 10.8 Energy -2.2 -3.9 26.2 -5.7 -3.9 1.0 4.1 Financials 5.2 9.6 46.4 5.4 13.9 17.6 0.4 Health Care 6.4 9.6 15.2 8.8 9.8 17.6 10.4 Industrials 3.8 5.8 27.7 5.3 10.5 14.5 8.3 Information Technology 5.1 11.5 33.0 9.8 15.9 15.1 11.1 Materials 0.7 5.5 27.8 5.4 5.7 9.1 5.9 Real Estate 4.7 9.2 14.6 4.6 11.2 11.3 4.2 Telecom Services -0.4 5.0 9.4 -2.9 10.1 10.8 5.7 Utilities 5.3 11.9 15.9 6.6 12.6 12.4 7.1 Notes: * Performance is gross of foreign dividend withholding taxes, 2 3yr, 5yr, and 10yr returns are annualized Source: BofA Merrill Lynch Global Research, S&P, MSCI, Bloomberg

Table 2: Bond/currency/commodity/hedge fund indexes–total return (%) As of 28 February 2017

Asset class 1mo 3mo 12mo YTD 3yr2 5yr2 10yr2 BofA Merrill Lynch Global Research Bond Indices (%, US dollar terms) 2-Year Treasury 0.1 0.2 0.2 0.2 0.6 0.5 2.1 5-Year Treasury 0.2 0.3 -1.7 0.5 1.3 1.0 4.1 10-Year Treasury 0.9 0.5 -4.1 0.9 2.8 1.5 4.8 30-Year Treasury 1.7 1.6 -5.4 2.0 6.4 2.9 6.4 US Broad Market Index 0.7 1.0 1.3 0.9 2.7 2.3 4.3 TIPS 0.6 1.3 3.4 1.4 2.1 0.8 4.3 Municipals* 0.6 2.3 0.4 1.2 3.7 3.2 4.4 US Corporate Bonds 1.1 2.2 6.3 1.5 3.8 3.9 5.4 US High Yield Bonds 1.6 4.9 22.3 2.9 4.8 6.9 7.4 Emerging Mkt Corp Bonds 1.3 3.4 11.2 2.7 4.0 4.7 6.0 Emerging Mkt Sov Bonds 1.5 4.2 9.1 3.3 4.2 4.6 6.3 Preferreds 1.9 4.9 6.8 4.7 8.2 6.4 3.1 Foreign exchange** (%, in local currencies) US dollar 1.0 -1.0 0.9 -2.1 6.6 5.7 1.2 British pound -0.4 -1.1 -9.8 0.1 -3.7 -0.8 -3.0Euro -0.9 -0.5 1.5 -0.8 -3.1 -1.0 -0.8Yen 1.3 1.6 2.1 4.0 0.9 -4.3 1.6 Commodities** (%, US dollar terms) CRB Index -0.7 0.7 16.8 -1.0 -14.3 -10.0 -4.8Gold 3.8 6.9 2.0 9.0 -1.7 -6.8 6.5 WTI Crude Oil 2.3 9.2 60.0 0.5 -19.3 -12.7 -1.3Brent Crude Oil -0.2 10.1 54.5 -2.2 -20.1 -14.5 -1.1Alternative Investments† (%, US dollar terms) Hedge Fund - CS Tremont¹ 0.7 2.0 3.4 0.7 1.9 4.0 3.7 Hedge Fund - HFRI Fund of Funds¹ 1.0 2.2 4.3 1.0 1.7 3.3 1.3 Notes: *Not tax adjusted. **BoE calculated effective FX indices. ¹Data lagged by one month; 2 3yr, 5yr,

and 10yr returns are annualized; CS AUM-weighted, HFRI equal-weighted; †AI data not comparable to

other asset classes because of reporting delays, lack of standardized reporting, and survivorship and self-selection biases. Crude oil prices are spot USD. Source: S&P, MSCI, Bloomberg, FactSet, BofAML

Bond Indices (US Treasury Current 10yr, Current 2yr, Inflation-Linked; Muni Master, US Corp Master,

US HY Master II, EM Corp Plus Index; EM External Debt Sovereign Index; US Preferred Stock Index).

The RIC Report | 14 March 2017 3

Beyond our borders

Cheryl Rowan Portfolio Strategist MLPF&S

Martin Mauro Fixed Income Strategist MLPF&S

Matthew Trapp, CFA Investment Strategist MLPF&S

With all the potential tax and regulatory changes from the new leadership in Washington, investors may be paying too little attention to events and markets outside the US. In equities, we broadly favor Japanese and Emerging Markets, while we wait for more clarity on the political situation in Europe before becoming more enthusiastic there. In bonds, we favor Emerging Market dollar-denominated debt, both sovereign and corporate.

Stepped up Fed rate hikes, higher US stock market target The US economic picture has been improving. Job gains have averaged 209,000 during the past three months, the manufacturing ISM index has been above 50% for the past six months, and consumer sentiment has been moving higher. US Economist Michelle Meyer now expects the Fed to raise rates three times this year, with the first move coming on March 15. These moves would probably not rattle the markets. The bond market is already priced for a March 15 move and expects at least three rate hikes this year.

Since we expect yields to move higher in the coming months, we recommend a defensive approach to bond positioning. We favor ladders and barbells. We also suggest areas where coupon rates would likely rise as the Fed hikes rates. Fixed-to-floating rate preferreds fit this description, although in many cases the floating period does not begin until the early 2020s. Senior loans are another choice for investors who can accept low credit quality.

Savita Subramanian, head of US Equity Strategy, recently raised her year-end S&P 500 target to 2450 from 2300. The change reflects a lowering of her year-end equity risk premium assumption and a lowering of her fair value model weight in favor of her sentiment model. Subramanian sees increasing likelihood that we are entering the typical later stages of a bull market during which the fundamentals typically take a back seat to sentiment and technicals.

With strong relative performance from US markets and these forecast changes, it’s easy to understand why investors would be focused solely on the US. But that ignores opportunities in other parts of the world, as we highlight below.

Europe in a holding pattern but runway in sight It appears that the era of Quantitative Easing by the European Central Bank (ECB) is winding down. That’s because Europe seems to be on a solid path toward higher inflation. Data for growth, inflation and earnings are beating expectations. Our economists expect 2017 to be the trough for economic growth at 1.4%. Exports are a significant portion of the European economy, and global growth continues to improve. Nonetheless, the political risks surrounding the upcoming elections including what those outcomes may mean for the sustainability of the Eurozone keep us neutral.

Several reasons to be more inclined to add to European equities The reflation theme keeps gaining traction in Europe, and evidence of rising inflation globally has exceeded expectations, particularly in Germany, the UK and China. Manufacturing survey price indicators suggest that cyclical inflationary pressures are building and the rise in several commodity prices confirms this data. Leading global indicators are hitting levels associated with European EPS growth in the teens (Chart 2).

4 The RIC Report | 14 March 2017

Bond yields are rising again, and European Equity Strategist James Barty thinks, after years of negative rates, there is room for yields to back up further before they create a risk to equity market valuations. This is an important positive for banks, given their sensitivities to the short end of the yield curve. Barty notes that banks’ price returns and valuation are most highly correlated to rising rates and inflation expectations.

Our strategists forecast higher earnings growth in Europe, led by a synchronized upturn in the global economic cycle (Chart 1). Barty believes earnings have bottomed and are poised to deliver double digit (11%) growth for the first time since 2010. This view is based on recovering commodity prices, low margins, a disciplined approach to capital spending and a modest currency tailwind. Further, the region looks inexpensive in relation to US stocks, based on both normalized price/earnings and price/book ratios. Our strategists currently favor banks, oils and chemicals along with the defensive health care and utilities sectors.

Chart 1: European earnings closely correlated with global GDP Europe trailing EPS growth vs World GDP

Source: BofA Merrill Lynch Global Research, Datastream, IBES. Note: GDP for 2017 based on BofAML forecast

Chart 2: Rising PMIs point to upside risks for growth and earnings

Source: BofA Merrill Lynch Global Research, Datastream, IBES

Political risks keep us on the sidelines for longer In our view, the key downside risk for Europe is that the political landscape becomes more unstable and fears of a Eurozone breakup gain momentum. The market is focused on elections in the Netherlands and Germany, and especially the election of a new president in France. A victory by Front National candidate Marine Le Pen could, according to Barty, potentially reignite fears that the Eurozone disintegrates, as Le Pen advocates a referendum on this topic and reversal of some economic reforms. Barty estimates a Le Pen victory could lead to a selloff in European equities of 13-23%. The election’s first round will be held April 23 with any run-off election on May 7.

German elections follow later in the year (September 24), so we expect market volatility to be higher than normal as that date approaches. The political situation in Italy remains complicated, but it looks likely that elections there will not occur until 2018. We do not think national elections will occur in Spain this year, but do not rule it out.

It is possible that an improving growth outlook for European equities could offset political concerns. It is also possible that reform-minded candidates could win elections and bring more stability to European politics. However, we prefer to remain neutral on markets at least until the situation in France becomes clearer.

Underweight UK as economic growth likely to slow We remain underweight on UK equities. We believe that the UK economy will slow more than the market expects as the country begins to implement its exit from the Eurozone—or Brexit. Q4 2016 economic growth was better than expected, but for the full year, the economy showed the slowest growth rate since 2012. Consumer spending accounted for all of UK economic growth in 2016 (Chart 3). However, real income growth (a key driver of consumption) has halved since the Brexit vote and consumer confidence has fallen. The gap

-1%

1%

3%

5%

7%

-50%

-30%

-10%

10%

30%

50%

Q496 Q499 Q402 Q405 Q408 Q411 Q414 Q417MSCI Europe 12m trail EPS (IBES) World GDP (right)

-60

-40

-20

0

20

40

60

30

35

40

45

50

55

60

65

01/98 01/01 01/04 01/07 01/10 01/13 01/16ISM / Euro PMI manuf avg (advanced 9m)MSCI Europe EPS € (trailing yoy, RHS)

The RIC Report | 14 March 2017 5

between wages and retail sales cannot last, in our view. We also expect a currency-induced rise in inflation in coming months. Further, the vast majority of UK growth since the financial crisis has come from expansion of the labor force, so a slowdown in immigration—likely as Brexit is implemented—suggests a downside risk to growth. Investors may want to limit their exposure to the UK consumer; our equity strategists are underweight retailing and travel/leisure stocks.

Chart 3: Contributions to yoy GDP growth: the consumer is the last leg left standing

Source: BofA Merrill Lynch Global Research, ONS.

It’s all coming together in Japan We favored Japan equities last year and we are even more convinced of our overweight stance for 2017. Japan Economist Izumi Devalier has an upbeat view of the Japanese economy, with a forecast of 1.5% GDP growth and an expectation of favorable inflation of 1.0%. Her view is predicated on an alignment of monetary and fiscal policy from the government, along with a recovery in domestic demand driven by consumption and industrial capital spending. Japanese Equity Strategist Shusuke Yamada expects the yen to weaken to 117 at year-end (from about 115 currently) and that should favor Japanese cyclicals.

The main catalyst for Japan’s recovery, according to Devalier, has been the pickup in global growth and the improvement in the global industrial cycle. Japan’s manufacturing sector has responded favorably—exports have been recent leaders. In 2017, expectations are high for domestic demand to drive the Japanese economy and stock market. Wage and full-time employment growth has stimulated consumption. Devalier believes the re-acceleration of wage growth could provide one of the biggest macro surprises for Japan in 2017. The combination of tight labor supply and stronger demand is forecast to lift nominal wage growth to around 1.4% in FY2017, and close to 2% in FY2018, up from the 0-0.5% pace of the past three years (Chart 4). This should support consumption.

The Bank of Japan is likely to be on hold for much of the year—allowing for a natural acceleration in growth. Inflation appears headed higher over the next two years, led by higher oil prices and a more hawkish Fed in the US, which should lead to a weaker yen by year-end.

-3-2-1012345

2014 2015 2016Consumption Capex & underlying stocksNet exports & valuables GovernmentContribution from… "the rest" GDP % yoy

6 The RIC Report | 14 March 2017

Chart 4: Steady labor market tightening points to wage growth ahead

Source: BofA Merrill Lynch Global Research, MHLW

Yamada believes that Japanese equities are attractively valued and thinks the economic environment favors a shift to cyclicals. He favors the domestic demand-driven cyclicals that could benefit from increases in consumption, along with financials (banks and insurance) that benefit from a pickup in inflation.

Maintaining a favorable view of Emerging Market stocks There are several cross currents facing emerging markets (EM); we maintain an overweight stance even though we acknowledge the potential for those stocks to pull back in the near term. Monetary policy has become more hawkish, suggesting less risk of currency devaluation, and the earnings picture looks favorable, particularly for Asian markets. Further, fund manager allocations do not appear aggressive (Chart 5). But China’s ability to maintain financial stability is still in question, potential trade conflicts with the US are worrisome, and expectations for strong global growth may already be built into stock prices.

The comeback in EM asset prices and reflation theme coincides with a shift in EM monetary policy, according to EEMEA Strategist David Hauner. Rather than diverging with the US Federal Reserve’s tightening policy, EM central banks appear to be more in sync with the US. Based on market expectations, 10 out of 15 EM countries are pricing in some probability of tightening rates over the next year. This is likely due to recovery in manufacturing Purchasing Managers’ Indices (PMIs) in Asia and EMEA and an acceleration in Chinese imports that is spilling over to broader Asia demand, and is reflected in our forecasts for steeper yield curves in much of EM this year.

EM Equity Strategist Ajay Kapur believes that a sharp decline in capital spending in key EM countries is likely to lead to expanding operating margins and a doubling of free cash flow in Asia ex-Japan by 2018. That should allow for approximately 20% growth in EPS for the region in 2017. He also thinks that EM valuations are reasonable and currencies are undervalued. But Kapur has become cautious in the near term, as he believes that China’s monetary conditions index may be rolling over and suggests exiting the more cyclical stocks.

China Equity Strategist David Cui is also cautious, as he thinks that China’s government may struggle to maintain both growth and financial stability and thinks that the market underestimates the potential of China-US trade conflicts. Financial deregulation has largely run its course and, according to Cui, if the currency is allowed to free float and devalues, it could trigger broad-based asset price deflation.

We are maintaining our positive view on EM and suggest that investors focus on markets such as Russia and Brazil. The Russian economy is on a recovery path and appears strong enough that the central bank has become less inclined to lower rates, which should support the currency. As long as oil prices are stable to rising they, along with removal of sanctions, should support the market. We expect Brazil to continue on the path toward reform. The

-3

-2

-1

0

1

2

3

-2.5

-2.0

-1.5

-1.0

-0.5

0.0

1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015 2017

FT job offers-total applicants gap Hourly wage-all workers 12MMA %YoY (RHS)

The RIC Report | 14 March 2017 7

central bank will likely continue to lower rates and that should help the economy recover from its severe recession. Investors are still under allocated, according to LatAm Equity Strategist Felipe Hirai. Earnings estimates are showing signs of improving and strong oil/commodities markets also support Brazilian equity prices.

The broad trade-weighted US dollar has moved lower since the start of the year, which has helped EM stocks rally (Chart 6). We are closely watching the dollar for signs of it moving higher again, as a significantly stronger dollar would be a negative headwind for EM equities. Two data points we are monitoring are the prospect of Congress enacting a Border Adjustment Tax, which we believe would lead to a stronger dollar, and the path for Fed rate hikes.

Chart 5: Net % fund managers say they are OW GEM equities

Source: BofA Merrill Lynch Global Fund Manager Survey

Chart 6: US broad trade-weighted dollar The dollar has moved lower since the start of the year

Source: BofA Merrill Lynch Global Research, Bloomberg

Bonds: dollar-denominated EM with caution We believe that bond market allocations outside the US should be concentrated in dollar-denominated sovereign and corporate Emerging Markets, but even that market we would approach with caution for the near term. We do not favor bonds in developed markets outside the US because yields are low, and we believe that dollar strength and rising rates will eat into returns.

EM bonds stumbled in the weeks after the election but have since more than recouped their losses. The rise in commodity prices (Chart 7) is helping most EM countries, as is the rise in manufacturing activity over much of Asia and EMEA. Yields have been declining since the middle of December as Chart8 below right shows.

The main positive for EM debt is the favorable economic growth outlook for most of the countries for the next two years. Our economists expect GDP among EM nations to grow by 4.6% this year and 5.1% next year, compared to 2.1% and 2.5% in the US.

100105110115120125130135

US Trade Weighted Broad Dollar Index

8 The RIC Report | 14 March 2017

Chart 7: CRB Commodity Price Index (1967=100)

Source: Commodity Research Bureau, Bloomberg

Chart 8: Emerging market bond yields %

Source: BoA Merrill Lynch Global Bond Indexes

Dollar-denominated sovereign debt The strong recent performance of EM bonds has made finding value more difficult. Jane Brauer, Global EM fixed-income quantitative strategist, is moderately cautious on EM external (dollar-denominated) debt. The biggest positives she sees revolve around the demand among investors for duration and the still-low yields and shortage of bonds with credit exposure in developed countries. Although spreads of EM dollar-denominated sovereigns to US Treasuries have narrowed to their lowest level in three years, they have not narrowed as much as US corporate and high yield bonds.

One risk for EM debt in Brauer’s view is that the recent outperformance in risk assets may have run ahead too quickly. Also, a rise in global rates would reduce the appeal of EM bonds. Other risks are a potential decline in commodity prices, an appreciation in the dollar (which would have a negative influence on commodity prices) and protectionist policies in the US and a significant slowdown in China.

EM corporates: some near-term positives EM corporate bonds, most of which are denominated in dollars, have also fared well this year, but here again valuations are moving toward extremes. The yield spread vs US governments is the narrowest since before the financial crisis. Anne Milne, head of Global EM Credit Research, believes that spreads can remain tight for the near term.

One positive is the near-term cash flow outlook. Maturing issues and coupon payments will total $20 billion in March and $26 billion in April. Those are funds that could be plowed back into the market. Also, EM corporate bonds are benefitting from new institutional allocations and increased retail interest. Finally, commodity producers are benefiting from higher prices. The risks for EM corporate, in Milne’s view, are the potential border adjustment tax in the US, the potential for more aggressive path of Fed rate hikes.

Enter the market gradually Investors need to balance the favorable long-term growth prospects for EM debt with the near-term risks that we cited, as well as the less attractive valuations resulting from the decline in yields in recent months. We suggest committing to the market gradually over the course of the next several months, especially on weakness. .

We favor dollar-denominated debt, both sovereign and corporate, over local currency debt in order to mitigate the currency risk that US investors would face if the dollar appreciates as we expect.

390395400405410415420425430435440

4.004.204.404.604.805.005.205.405.605.806.00

Jul-16 Aug-16 Sep-16 Oct-16 Nov-16 Dec-16 Jan-17 Feb-17

Series1 Corporate

The RIC Report | 14 March 2017 9

The market’s message to the Fed Shyam S.Rajan Rates Strategist MLPF&S

The bond market’s focus in early March was on the Fed’s message to the market. The coordinated attack by Fed officials on the probabilities that the market attached to a March 15 rate hike resulted in a re-pricing of near-term expectations. But even more interesting was the market’s response to the Fed. Despite the 60% increase in near-term Fed hike probabilities, stocks are higher, credit spreads are tighter, interest rate volatility and the VIX are lower. While this has allowed the Fed to have its cake and eat it too at the March meeting, in our view there could be a bigger sign from the markets to the Fed: financial conditions could be at the cusp of signaling that policy is behind the curve. Ultimately, financial conditions that fail to tighten in response to a hawkish Fed could raise concerns of a more hawkish policy stance (higher dots and/or active balance sheet talk). This could translate to higher risk premium in the front end and a steeper skew.

Chart 9: The broken link between financial conditions and the Fed

Source: BofA Merrill Lynch Global Research

Hikes vs financial conditions: going back to Dudley 2015 Consider the argument put forth by NY Fed President Dudley in 2015. In an interview in June 2015 he said, “If you actually look at what actually happened to financial conditions over that period — 2004 to 2007 — the Fed wasn’t really effective in tightening financial conditions, so the Fed didn’t really achieve its objective. My point in the footnote was basically to say this was probably a period where the Fed should have done a bit more because we probably should have been tightening financial conditions over that period.”

The above failure to tighten financial conditions in the 2004 cycle relative to the 1994 cycle is best illustrated through Chart 10 and Chart 11. The charts plot the Chicago Fed financial conditions index with the second Eurodollar contract yield in both these cycles (Eurodollars are interest bearing bank deposits denominated in US Dollars and held at banks outside of the United States). Clearly, Fed hikes translated to tighter financial conditions in the former and barely moved conditions in the latter. Fast forward to today, Chart 9 shows the same failure in 2004 has repeated so far in the current cycle.

-1.5

-1

-0.5

0

0.5

1

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1/3/2010 1/3/2011 1/3/2012 1/3/2013 1/3/2014 1/3/2015 1/3/2016 1/3/2017

2nd Eurodollar contract yield Chicago Fed financial conditions index (RHS)

10 The RIC Report | 14 March 2017

Chart 10: 1994 hiking cycle: financial conditions vs. short term rates

Source: BofA Merrill Lynch Global Research

Chart 11: 2004 hiking cycle: financial conditions vs. short term rates

Source: BofA Merrill Lynch Global Research

Doing a 180: from policy misstep to policy catch-up The above shift, while subtle, is an important one. Not too long ago, markets were stuck in a negative feedback loop: Good US data and a persistently hawkish Fed in the face of weaker global growth led to a much stronger dollar and fed back into lower inflation expectations. This not so merry-go-around (illustrated by our economists here) was evident in September 2013 (taper tantrum), June 2015 (Dollar rally in March), September 2015 (China deval) and January 2016 (post hike China concerns).

The first week of March marks the first phase of the transition: a market that loosened financial conditions in response to a hawkish Fed. While this has likely been treated as a welcome development so far, that judgment could be called into question, especially if global growth continues to accelerate and fiscal stimulus remains in the cards. Ultimately, loose financial conditions in the face of a hawkish Fed could embolden a more hawkish/braver policy stance. At the very least, it should raise repeated concerns of the dots shifting higher or the Fed using its balance sheet as an active tool.

-1.2

-1

-0.8

-0.6

-0.4

-0.2

0

3

4

5

6

7

8

9

2nd Eurodollar contract yield

Chicago Fed financial conditions index (RHS)

-1-0.9-0.8-0.7-0.6-0.5-0.4-0.3-0.2-0.10

0

1

2

3

4

5

6

2nd Eurodollar contract yield

Chicago Fed financial conditions index (RHS)

The RIC Report | 14 March 2017 11

The future of autos Beijia Ma, CFA >> Equity Strategist MLI (UK)

Sarbjit Nahal >> Equity Strategist MLI (UK)

The global transportation sector is a behemoth with US$6.8 trillion in annual output and 1.2 billion vehicles globally, generating US$2.1 trillion in annual light vehicle sales and another US$4+ trillion in supplies and ancillary services (source: Roland Berger, Navigant). We believe that the sector is ripe for a defining disruptive moment as it moves toward more sustainable ways to tap into transport demand, while evolving toward next-generation solutions using limited resources. Transport in the future will be greener, safer, faster, on-demand, and personalized for the user.

Urbanization, demographics, congestion, pollution, emissions, safety and cost are all challenging the existing vehicle ownership model. The traditional auto ownership model is grossly inefficient, with 95% of cars parked at any one point (source: Donald Shoup 2005, Kenworthy & Laube, IEA). Population growth is projected to add 2.5 billion people to the planet by the middle of this century, with 70% of the planet living in urban settings (source: UN), adding to congestion on the roads. The rising financial, social and environmental costs of transportation are unsustainable, and demand a fundamental rethink of mobility.

Please see the comprehensive primer on future mobility that much of this article is based on: Thematic Investing: Overdrive – Global Future Mobility Primer 16 February 2017

31% of urban land is used for parking, 30% of all traffic is looking for spots Parking accounts for 31% of the central business districts in global cities (source: Kenworthy & Laube). For cities like Los Angeles, 59-66% of land is car-related, consisting of either sidewalks, streets, or parking (source: Transportation and parking for tomorrow’s cities, Smith). In fact, 30% of all traffic flow in urban centers across the world is looking for parking spots (source: Shoup et al). Furthermore, 40% of fuel in cities is wasted looking for parking (source: Casualty Actuarial Society). Liberating space otherwise wasted on parking via replacement by fewer autonomous vehicles (AVs) could allow more people to live in city centers.

Congestion wastes time and fuel – slower than a pig in London Traffic congestion globally has been rising in all urban areas in both DMs and EMs. In the US, commuters in urban areas lost 8bn hours or 50 hours of extra travel time per person in 2015, or nearly 3x the 18 hours in 1982. This wasted 19 gallons per person, up from four gallons in 1982. London has some of the worst traffic within the developed world in terms of wasted time in traffic (source: TomTom Traffic Index, INRIX 2016). The average traffic speed in central London has been declining steadily, from 10.9mph in 2003 to 7.8mph by 2016, or 30% slower than a pig (source: Inrix, Transport for London, Speed of Animals).

Moving to a new transportation paradigm The confluence of electric, autonomous, shared, and connected cars will give rise to an entirely new transportation paradigm. From a technology perspective, we have entered the exponential age, whereby Moore’s law is enabling the rise of sensor content, Big Data, artificial intelligence (AI), cloud analytics, and the broader Internet of Things (IoT) ecosystem. While many sectors are already undergoing the IoT transformation, we believe the automotive industry is the next to be upended. Four trends disrupting the transport sector right now – electrification, autonomous driving, connectivity and shared mobility – will forge a paradigm shift from a vehicle-centric to a platform-centric model. Future Mobility – including an

12 The RIC Report | 14 March 2017

integrated, on-demand electric fleet of autonomous taxis – can generate US$3.8tn of cumulative positive impact over the next 10 years.

These changes will unbundle the automobile, shift revenue pools, change consumer mobility behavior, and introduce new competition and cooperation. We believe the impact will reverberate well beyond vehicles, with significant ramifications for oil and electricity demand, insurance, real estate and jobs.

Chart 12: Macro factors driving shift in mobility paradigm

Source: BofA Merrill Lynch Global Research based on cited sources

Moving toward zero emissions Transport accounts for nearly a quarter of global energy-related emissions. Cars and trucks represent 75% of these (source: IEA). Electric Vehicles (EVs) are set to be a critical component of the global fight against climate change with CO2 emissions 40% lower than internal combustion engines (ICEs) today. The move to EVs will mirror a global move to de-carbonize the economy and double the share of renewable power generation in the next 25 years.

New energy vehicles are expected to reach 26% of global sales (31mn vehicles) by 2030E, 35% by 2040E, and up to 50% in a shared transport scenario (source: BofAML Global Autos team, Bloomberg New Energy Finance). This includes pure EVs, plug-in hybrids (PHEVs), mild hybrids (MHVs), and fuel cells. We see the early 2020Es as the inflection point for pure EV uptake as costs come down to parity vs. the traditional internal combustion engine.

Consumers are demanding fuel-efficient vehicles for cost and environmental reasons, with close to 40% of US adults interested in buying an EV. Levels of interest in EVs are up to 70% with younger US millennials (source: Consumer Federation of America). Barriers to widescale adoption today include cost of vehicle ownership, vehicle range, recharge time, and consumer awareness, each of which are coming down rapidly.

We see several drivers of an expected pick-up in adoption, particularly for EVs:

• EV range improving: Range has been an important consumer consideration holdingback wider EV adoption so far (range anxiety). In our view, EVs will be more widelyadopted if they offer a drive range of 200-250 miles on a single charge. This shouldbe possible in the next 10 years.

The RIC Report | 14 March 2017 13

• Price: The incremental cost of pure EV vs ICE is $12,500 today, but this is set todecline to parity by 2030E, and 2022E with subsidies. In a scenario where thesharing economy takes off and utilization rates double, the parity point could comeas early as 2018.

• Expansion of charging infrastructure

• EV performance catching up: Performance is no longer a reason for consumers toavoid EVs. For example, Toyota’s Prius, the best-selling hybrid, has a maximum speedof 112 mph (well above the legal limit in most countries) and reaches 0-60mph in adecent ~10 seconds.

• Regulatory emission deadlines drawing closer: In particular, 2020 and 2021 arekey hard stop years in terms of CO2 reduction for OEMs in several markets – Europe,China and Japan. Without a materially higher share of hybrid or fully EVs in theirsales mix by then, most OEMs will be unable to achieve these reductions.

The rise of the robo-cars Autonomous vehicles (AVs), otherwise known as self-driving cars, are a vision of the not-too-distant future in which a vehicle can drive itself from A to B without human input. This will be made possible through the use of various sensors, lasers, radars, cameras, advanced driver assistance systems, software, GPS, mapping data, and wireless data communication systems. The data picked up by these sensors must be interpreted by ultra-high-speed computer processors to provide real-time route guidance, navigation, and obstacle detection.

In addition to consumer cars, there are two other types of autonomous vehicles being developed: high passenger-density urban transport and heavy-duty trucks. There has been rapid progress on both.

AV technology is set to create a US$87bn solutions market for OEMs, parts suppliers, and technology companies by 2030E, with software taking the largest share at 29% of the total (source: Lux Research). We think that the large-scale rollout of autonomous cars will likely occur by 2020E, with cars with partial autonomous features set to reach 12-13% penetration by 2025E (source: BCG). Fully autonomous cars will reach 32% global penetration or 21mn units by 2030E, and rise to 75mn units by 2040E (source: IHS 2016).

There are numerous potential benefits from AV technology including:

• Improved safety: There are 6mn car crashes every year in the US, causing 3.9mninjuries, damaging 24mn cars, and leading to 40,000 traffic deaths. Worryingly, 95%of accidents are caused by human error (source: NHTSA). According to the USDepartment of Transportation, as many as 80% of all crashes could be avoided usingself-driving technology.

• Less congestion and pollution: AVs can improve fuel economy by 4-10% just byaccelerating and decelerating more smoothly than human drivers (source: RAND).Platooning – AVs driving together resembling a train – can increase road capacityand reduce highway fuel use by up to 20% (source: KPMG). This makes start-and-stop traffic a thing of the past.

• Greater productivity: Given an average commute of 25 minutes, around 80% of theUS workforce loses 50 minutes of potential productivity every workday (source:KPMG). If the freed-up time were used for work-related activities, this wouldtranslate into a 10-15% productivity increase assuming an eight-hour hour workday

14 The RIC Report | 14 March 2017

Chart 13: Progression toward autonomous driving

Source: Continental

Some hurdles to adoption Despite the conversation on autonomous vehicle adoption reaching the tipping point, several hurdles remain to full commercial adoption:

• Regulation/ Insurance: Fully autonomous driving systems, where no interventionwould be required by the driver, will require changes to regulation for determiningfault in the event of an accident (ie, the driver, OEM, or supplier).

• Cost: The cost of a fully autonomous vehicle features is expected to be aroundUS$5,000-10,000 at introduction in 2025 (source: BCG 2015, Valeo, Delphi). Whilethis is feasible for affluent premium-car consumers, costs will have to fall for widerglobal adoption.

• Ethics: Widespread adoption of driverless cars will involve OEMs tackling somedifficult ethical issues. How should the car be programmed to act in the event of anunavoidable accident? Should it minimize the loss of life, even if it means sacrificingthe occupants, or should it protect the occupants at all costs? The answers to thesequestions will have a significant impact on the way self-driving cars are accepted insociety (ie, would consumers buy a car programmed to sacrifice the owner?).

Shared autonomous EVs the optimal mode of transport The sharing economy is expected to change traditional vehicle ownership models more in the next 5-10Y than in the last 50Y (source: GM). In the long run, a shared vehicle that replaces its internal combustion engine with electric, and replaces its human driver with AI, will be the cheapest, fastest and most flexible form of transport. Today, a fleet of autonomous EVs on the Tesla Network would cost around US$0.42-0.49/mile, including charging, insurance, and maintenance. This is 70-85% cheaper than ride-hailing, up to 50% cheaper than car ownership, and even 35-65% cheaper than car-sharing (source: Chen et al 2016). Many studies show that the long-term cost of a robo-taxi could be as low as US$0.17-0.30/mile as infrastructure, R&D, and other start-up costs fall (source: Chen et al 2016, BCG 2016, KPMG, BNEF/McKinsey, Rock Mountain Institute). This is 40-70% cheaper than ownership, and could even be cost competitive compared with mass transit at a rate of two passengers, but with a 40% lower commute time (source: BCG).

The RIC Report | 14 March 2017 15

Existing modes of multimodal transport – including ride-hailing (Uber), ride-sharing (Commutr), and car-sharing (Zipcar) – are already economical in many situations vs ownership and public transport. For someone traveling 4,000 miles or less per year in the US, ride-hailing would be cheaper than buying and operating a new car. This is often the case for urbanites with shorter commutes. For those travelling 5,000 miles or less per year, using multimodal transport would be around 24% cheaper than a new car, without any sacrifice to time or convenience (source: McKinsey).

Internet of Cars: more cars than phones getting connected Connectivity is an enabler of future mobility and a feature that consumers are increasingly demanding. The Internet of Things (IoT) is one of the biggest disruptors of our age with 25bn connected devices today and an estimated 50bn by 2020E (source: Ericsson, Cisco). IoT is now reaching the automobile, creating the Internet of Cars (IoC). Consultant Chetan Sharma noted that in 1Q16, there were more automobiles getting connected to the network in US than smartphones. In Europe, six out of 10 (59%) of consumers say that connected features influenced their decision to buy a vehicle, and one in three (32%) says it is an important criteria that influenced their decision (source: TNS and the BearingPoint Institute).

The auto-tech arms race For tech giants, the US$5tn transport sector presents a major growth area. Connected cars will drive growth of the global automotive semiconductor market, which is projected to reach US$36bn by 2018E (9% of the total industry, +6.4% CAGR from 2016) (source: BofAMLe). Average semi content stands at US$345 per car today (+40% higher vs 2009), and is set to grow to over US$1000. Infotainment is one of the largest auto semis clusters today at US$5bn, and growing 7% pa. Semis are helping to redefine auto architecture into an integrated cockpit, with OEMs, suppliers and tech enablers aiming for a fully configurable, touch-free experience using gesture control, voice recognition, and eye detection, etc. The next stepwise changes will be led by EVs and AVs. EVs can take semi content up to US$700, while autonomous driving will represent another US$550 of incremental content.

New opportunities The average autonomous car is expected to generate 4,000GB of data per day by 2020E, compared with the 6-700MB per day for the average human now (source: Intel, Cisco). The data generated could help create new business models that, if fully realized, can form a service economy worth US$450-750bn by 2030E (source: McKinsey). Tech companies and other new entrants can have a major role in sifting through the data flood, in order to generate value-added knowledge. Their fundamental models for value creation revolve around generating direct revenues, reducing costs and improving safety and security.

Future mobility stock list The following covered companies were identified as publicly traded participants in the future mobility market in the February 16, 2017 BofA Merrill Lynch Global Future Mobility Primer.

In the full report, the thematic investing team mapped opportunities across 4 entry points for investors wishing to invest in the Future Mobility theme including: 1) electrification; 2) autonomous driving; 3) Internet of Cars (IoC); and 4) shared mobility. We outline these areas in much greater detail throughout our Primer report. For each company, we have estimated the level and materiality of companies’ exposure to future mobility-related themes – and the role of future mobility as a long-term growth driver. For each company, we have characterised their future mobility exposure as follows:

• Low – Future Mobility-related products, technologies, services, and solutions are notmaterial to global revenues and/or growth but are one factor, among others, for thebusiness model, strategy & R&D of the company.

• Medium – Future Mobility -related products, technologies, services, and solutions arean important factor for the business model, strategy and R&D of the company;material to sales and/or growth.

16 The RIC Report | 14 March 2017

• High – Future Mobility -related technologies, services, and solutions are core to thebusiness model, strategy and R&D of the company; material sales and/or growthdriver; pure play (i.e., 100% of sales).

Although it is difficult to accurately gauge the link between such exposure and share price performance (as many factors outside the scope of this analysis are likely to play a role in short- and long-term price development), we still consider future mobility exposure as an important and positive point to track given that future mobility is a global “Transforming World” theme with a long lifespan.

Table 3: Future mobility stock universe

Company BofAML Ticker Price 3/10/2017 Mkt. Cap US$m Q-R-Q Country

Future Mobility Sub-Sector

Future Mobility Exposure

Autonomous Alphabet C GOOG 843.25 588,864 B-1-9 United States Technology Medium Baidu.com-ADR BIDU 172.74 59,925 C-1-9 China Technology Low Delphi DLPH 77.09 20,781 C-3-7 United Kingdom Autoparts Supplier Medium Ford Motor F 12.53 49,798 C-2-7 United States Automaker Medium General Motors GM 36.83 55,170 C-2-7 United States Automaker Medium Gentex GNTX 21.52 6,183 C-3-7 United States Autoparts Supplier Medium Intel INTC 35.91 169,782 B-1-7 United States Tech Hardware Low Magna Intl MGA 42.71 16,326 C-3-7 Canada Autoparts Supplier Medium Nvidia NVDA 99.12 58,382 C-1-7 United States Tech Hardware Medium QUALCOMM QCOM 58.64 86,614 B-1-7 United States Semiconductors Medium Sensata ST 41.82 7,146 C-1-9 United States Autoparts Supplier Low TE Connectivity Ltd. TEL 74.61 26,508 C-1-7 United States Autoparts Supplier Medium Tesla TSLA 243.69 39,397 C-3-9 United States Automaker Medium Texas Instr. TXN 80.33 80,301 B-1-7 United States Semiconductors Low Toyota Motor TM 112.66 183,805 B-2-7 Japan Automaker Low Electric Vehicles BorgWarner BWA 41.79 8,888 C-3-7 United States Autoparts Supplier Medium Delphi DLPH 77.09 20,781 C-3-7 United Kingdom Autoparts Supplier Medium FMC FMC 60.05 8,028 B-3-7 United States Battery Materials Low General Motors GM 36.83 55,170 C-2-7 United States Automaker Low Parker Hannifin PH 157.32 20,970 B-1-7 United States Battery Materials Low Sensata ST 41.82 7,146 C-1-9 United States Autoparts Supplier Low SQM SQM 32.99 9,027 C-2-8 Chile Battery Materials Medium TE Connectivity Ltd. TEL 74.61 26,508 C-1-7 United States Autoparts Supplier Medium Tesla TSLA 243.69 39,397 C-3-9 United States Automaker High Toyota Motor TM 112.66 183,805 B-2-7 Japan Automaker Low Connected Alphabet C GOOG 843.25 588,864 B-1-9 United States Technology Medium Amazon.com AMZN 852.46 406,769 B-1-9 United States Technology Low Analog Devices ADI 82.20 25,417 C-1-7 United States Semiconductors Low Apple Inc. AAPL 139.14 730,004 B-1-7 United States Technology Low Broadcom AVGO 226.35 90,848 C-1-7 Singapore Semiconductors Low Delphi DLPH 77.09 20,781 C-3-7 United Kingdom Autoparts Supplier Medium Intel INTC 35.91 169,782 B-1-7 United States Tech Hardware Medium Microsoft Corp MSFT 64.93 501,749 B-1-7 United States Technology Low Nvidia NVDA 99.12 58,382 C-1-7 United States Tech Hardware Medium ON Semiconductor ON 15.22 6,386 C-1-9 United States Semiconductors Medium QUALCOMM QCOM 58.64 86,614 B-1-7 United States Semiconductors Medium TE Connectivity Ltd. TEL 74.61 26,508 C-1-7 United States Semiconductors Medium Texas Instr. TXN 80.33 80,301 B-1-7 United States Semiconductors Medium Xilinx XLNX 59.55 14,824 C-3-7 United States Semiconductors Low Shared Alphabet C GOOG 843.25 588,864 B-1-9 United States Technology Medium Ford Motor F 12.53 49,798 C-2-7 United States Automaker Low General Motors GM 36.83 55,170 C-2-7 United States Automaker Low Tesla TSLA 243.69 39,397 C-3-9 United States Automaker Medium Source: BofA Merrill Lynch Global Research. This screen is not a recommended list either individually or as a group of stocks. Investors should consider the fundamentals of the companies and their own individual circumstances/objectives before making any investment decisions.

The RIC Report | 14 March 2017 17

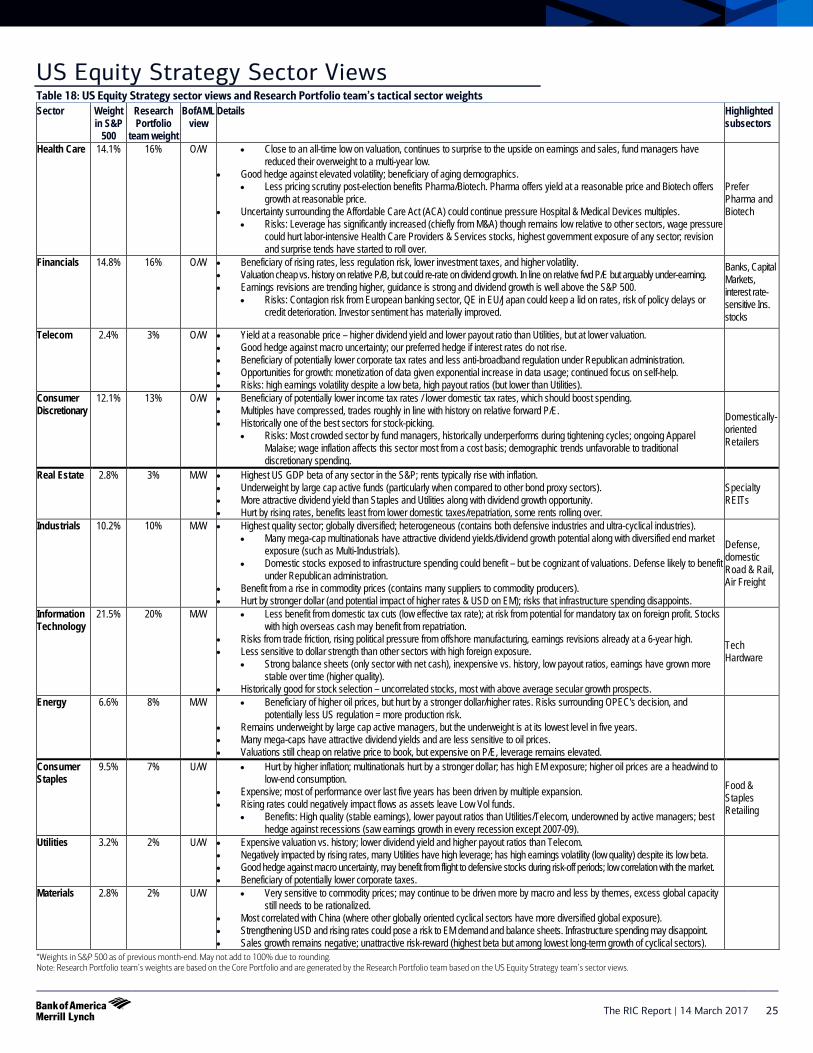

RIC asset class views Table 4: Research Investment Committee asset class views Asset Class RIC view Comments

(+ / = / –) Equity markets

US equities + Low but rising rate expectations, modest inflation and a strong dollar are good for stocks Also EPS and sales growth are favorable. But we have concerns about high valuations and potential for disappointment if policy implementation is delayed. Prefer dividend growers.

Consumer Discretionary + Principally domestic orientation, so less exposed to global trade concerns; beneficiary of lower proposed income taxes (increased spending) and corporate taxes, and improved confidence. Watch rising labor costs as economy heats up.

Consumer Staples – High quality stocks but vulnerable to higher dollar and higher inflation. Global sector that would be hurt by restrictions on trade; still expensive. Energy = Oil price forecast suggests upside, but would be hurt by stronger dollar and higher rates. We remain concerned about production risk.

Financials + Key beneficiary of rising rates, steeper yield curve, higher volatility. Attractive valuations (P/B) and earnings revisions are improving. Banks, brokers, insurers likely beneficiaries of reduced regulation.

Health Care + Should get less pricing scrutiny under new administration; earnings and sales improving and PMs have reduced exposure. Prefer managed care and biotech, pharma for yield; watch exposure to hospitals and devices if ACA gets revised/repealed.

Industrials = Highest quality sector, beneficiary of higher commodity prices and improving global growth; benefits from infrastructure and defense spending. Information Technology = Repatriation would benefit but other tax plans less helpful. Vulnerable to trade friction issues. Balance sheets strong, inexpensive. Materials – Benefits from commodity price strength and “buy American,” but most exposed sector to China and still has excess capacity. Real Estate = Most GDP-sensitive sector; good combination of dividend yield plus dividend growth. Hurt by rising rates but can lead to better property cash flows. Telecom Services + Yield at a reasonable price; beneficiary of less anti-broadband regulation and lower corporate taxes; opportunities for growth as data usage rises. Utilities – Expensive and hurt by rising rates; leverage and earnings volatility are both high. Should benefit from lower corporate tax rates.

Growth – Growth may lose momentum as profits growth accelerates, but it is cheap and we like exposure to selected Technology and Industrials. Prefer “half growth, half yield” stocks.

Value + Value tends to outperform when profits are accelerating as we believe they are today. Value indices have high exposure to Energy and Financials.

Small cap + Should benefit from pro-growth policy action and lower corporate taxes. Less vulnerable to global trade friction but valuation to large cap near extremes.

Large cap = Prefer high quality stocks with good dividend growth potential.

Europe (ex. UK) = Expect 11% growth in EPS in 2017 on better growth, as long as euro stays weak and commodity prices recover. PMIs hitting multi-year highs. Take balanced sector approach between cyclicals/defensives. O/W energy, banks, pharmaceuticals, utilities.

United Kingdom − Brexit fallout is GBP weakness and slower economic growth. Current growth looks unsustainable. Avoid domestic UK stocks.

Japan + We think yen weakens in 2017 (shifting spending to services). BoJ monetary policy, as well as fiscal policy, endorses reflation. Expect GDP growth forecasts to rise. Like cyclicals/exporters along with domestic demand beneficiaries. Favor financials.

Asia Pac (ex. Japan) + Valuations attractive. Fundamentals strong due to competitive currencies and global growth/commodity strength. Expect improving cash flow/EPS.

Emerging markets + Beneficiary of rising global growth and rising inflation expectations in DM. China debt service stability and shift to inflation should deflect pessimism. Currencies competitive but “too strong” dollar a risk. China, Russia, Taiwan, Korea, Brazil favored.

Fixed income markets Treasuries –- Treasuries will benefit from risk-off trades as they occur, but we see better yield opportunities elsewhere. The big risk is fiscal stimulus. Agencies / MBS = Historically, MBS have had a good mix of returns and volatility. TIPS = Inflation will likely rise modestly in the coming 12-18 months, but the market appears to be priced for much of that. US IG Corporates + Investment grade (IG) debt offers a good yield pickup over Treasuries, while still high quality. US HY Corporates – High debt levels, narrowing spreads, and weak earnings pose a risk, but potentially better growth and higher energy prices are a positive. Preferred securities = Favor QDI payers and fixed-to-floating structures. Non-US DM Sovereigns – Yields remain low and are likely to rise. A stronger dollar is a risk. EM $ Sovereigns = Economic growth is likely to outpace that in developed nations, but the market has rallied and spreads have narrowed. EM local currency Sovereigns = Favorable growth, fiscal, and current account prospects. Rising dollar is a risk.

Commodities/FX Gold = We expect the price to be $1400/oz at year end, on average in 2018. Fed rate hikes are the key obstacle to a sustained bull market. Oil + We forecast Brent Crude oil to rise to $70/bbl by mid-year, and to average between $50-$70/bbl through 2022. US dollar = We expect the US dollar to rise modestly against most currencies. Source: BofA Merrill Lynch Global Research

Notes to RIC views Ratings designations are as follows: (+) favorable view; (=) neutral view; (-) unfavorable view. Ratings reflect the Research Investment Committee’s view for an investment time horizon of 12 months. Typically, the RIC view will agree with regional/product strategists, but at times there may a difference of opinion based on investor suitability or time frame.

18 The RIC Report | 14 March 2017

Fixed Income, Economics, Commodities, Currencies: views and risks Table 5: Regional strategist views and associated risks

Views Risks Global Economics (Ethan Harris) • We expect 2% growth from 1Q to 3Q as growth momentum is slowed by policy uncertainty. However,

by late in the year we expect moderate fiscal stimulus to kick in moving growth higher. This should allow the Fed to hike in March, then twice more in Sep and Dec.

• The UK is likely to skirt a recession following Brexit, but we expect growth to slow to 1.4% this year. Euro area growth should fall more modestly to 1.5%, with external developments posing the greatest risks to the forecast.

• We take a pause from our structural EM bullishness as we think spreads are too tight ahead of the major uncertainty around US tax reform and French elections in April. However, we would buy the dip as we ultimately expect spreads to revisit their 2012 lows. EM remains supported by improving data, rising commodity prices and strong equity sentiment in the US. Focus on relative value, short duration and idiosyncratic trades.

• Downside risks: the main risk comes from polices driven by populism. This includes trade protectionism in the US and a move toward anti-EU parties in Europe.

• Upside risks: stronger animal spirits after the US election lift spending and investment, and US fiscal expansion could be larger than expected. Better growth in EM is another upside risk.

Global Rates (Shyam Rajan, Ralf Preusser) • US: The sweep election outcome is a game changer. Fiscal stimulus would clear the path for expectations of

faster Fed hikes and bring more front-end supply, giving the 5y sector in the US a lot more room to underperform. We expect 10y rates to test 3% and the 5s-30s curve to bear flatten.

• Europe: Politics have taken over as main driver of European rates, with short positioning in core EUR rates now reduced and positioning in the periphery turning negative. While higher US rates, shorter German QE purchases and rising inflation prints support a bearish bias, investors may remain close to neutral until political risks recede.

• US: The biggest risk to our higher rates view is extended expectations in risk assets and the upcoming election cycle in Europe.

• Europe: A large selloff in US rates could drive EUR rates higher despite existing political risks. Reduced risks associated with French elections could also lead to a significant selloff in rates, especially as headline inflation continues rising.

Global Commodities (Francisco Blanch) • Oil: OPEC agreed to cut crude oil output by 1.2mn b/d with key non-OPEC producers indicating a 600k

b/d curb, a first since 1998. Country quotas and an independent production monitoring committee are also part of the deal, so we expect firmer compliance. We see Brent crude oil averaging $61/bbl in 2017 and hitting $70 by mid-year on the seasonal ramp-up in demand.

• Gold: The outcome of the US presidential elections has changed gold market dynamics. A sharp push higher in nominal and real yields is a headwind to gold. For gold to rise, inflation needs to pick up so real yields stabilize. This may happen through 2017.

• We see EM oil demand expanding by 1.2mn b/d in 2017 but acknowledge downside risks on the back of higher US rates.

• OPEC's action won't propel prices much above our $70 mid-year target. Longer term, we estimate global oil demand will increase by 1.2mn b/d per year over five years at $55-75, and by 1.7mn b/d at $30/bbl.

Global Credit (Michael Contopoulos, Hans Mikkelsen) • We expect US high grade spreads to tighten to 105bp in 2017. • We are bullish on high grade spreads due to continued positive technicals and improving fundamentals. We

expect supply to decline 17% in 2017 while demand remains strong. Also earnings are rebounding for companies with considerable foreign sales exposure, and releveraging activity is declining.

• We expect HY to return 6% this year, driven by continued outperformance from lower quality names over the next several months. However, we think this will ultimately give way to an underwhelming 2nd half of the year.

• In our view, the likely catalyst for a weaker 2nd half is the eventual realization that the promise for tax and infrastructure reform underwhelms and is likely delayed. The month leading up to the August recess is the time period to watch out for, as investors will likely expect concrete plans with signs of passage.

• The biggest risk to US investment grade is the possibility of wider credit spreadsfollowing a rates shock, likely prompted by a rebound in the global economy, leading to fund outflows and institutional repositioning.

• The biggest risk to high yield at the moment is a strong pickup in inflation, which could potentially be caused by fiscal reform via a Border Adjustment Tax. We also think oil falling to the $40 range and remaining there for an extended period of time poses a strong risk to high yield corporates.

Municipals (Philip Fischer) • The muni market grew very little in the fourth quarter of 2016, though international demand has

steadily grown. P&C muni holdings steady as a percent of their assets. • The House Republican plan to repeal and replace Obamacare passed two House Committees by

Thursday after lengthy debates. The American Health Care Act makes significant changes to Medicaid that will likely decrease federal funding over time, and increase budget pressures on the states. Medicaid makes up roughly one-third of state budgets.

Global FX (David Woo) • A clean sweep for the Republicans at the US election provides the green light for fiscal loosening and a

stronger USD. Our highest conviction is for a higher USD/JPY given its interest rate sensitivity and as Japan domestic flows turn JPY negative. Politics will be an important theme for EUR.

• The ECB has extended QE but at a slower pace, consistent with our view that the market increasingly will focus on the potential end of QE, pushing EUR/JPY higher. In the near term we do not preclude some pullback in the USD given its aggressive moves and stretched positioning.

• EM: We are starting to see divergence in EM FX. In particular, we are seeing real signs of reflation in CEE FX, which makes PLN and CZK the most likely candidates for appreciation given their more hawkish central banks. In LatAm, we forecast weaker FX vs USD with MXN and BRL to remain volatile, while PEN and CLP and ARS, to a lesser extent, are more resilient, driven by local dynamics.

• An upside surprise to persistently low US inflation could induce expectations of faster Fed normalization, higher yields and thereby a higher USD.

• Downside risk for EUR-USD comes from the possibility of more aggressive QE moves from the ECB and falling oil prices.

• EM: A slowdown in China, higher US rates and policy uncertainty in the US remains a major risk for global trade, with direct implications for Mexico and Asia.

Source: BofA Merrill Lynch Global Research

The RIC Report | 14 March 2017 19

Global equity markets: views and risks Table 6: Regional strategist views and associated risks

Views Risks Global Equities (Michael Hartnett) • Peak liquidity, peak globalization and peak inequality suggest peak returns, but also big rotation in 2017. • Asset allocation: long stocks, real estate, commodities, US dollar and short bonds. • 2017 expected returns: double digits for Japan, Europe, UK stocks, and oil; single digits for US stocks,

commodities, the USD & Emerging Markets; low/negative returns for corporate & government bonds. • We expect inflation & interest rates to surprise to the upside in 2017, leading to a rotation from “deflation” to

“inflation”, from “ZIRP winners” to “ZIRP losers”, from Wall Street to Main Street. • We believe fiscal stimulus accelerates, trade and immigration policies tighten, and wage growth

accelerates, boosting domestic demand across the G7. • Disruptive technology and aging demographics remain powerful secular forces; they won’t likely prevent a

cyclical pick-up in inflation; but they are likely to constrain the magnitude of the rise in rates and inflation.

• Boom-bust scenario where Fed is forced to respond to macro inflation via bear flattening of yield curve, inducing wider credit spreads, forced liquidation and a bond crash (see Orange County/Mexico 1994).

• US protectionism (global trade war) + weaker-than-expected US growth (policy disappointment) could lead to elevated volatility and stagflationaryreturns.

United States (Savita Subramanian) • Our 2017 year-end S&P 500 target is 2450 and our long-term (year-end 2025) S&P 500 target is 3500. Our

target reflects the increasing likelihood that we are entering the typical later stages of a bull market, during which fundamentals typically take a back seat to sentiment and technicals.

• We forecast 2016 EPS of $118.50 (flat y/y), 2017 EPS of $129 (+9% y/y), and 2018 EPS of $137 (+6% y/y). • Valuations are above historical levels across most metrics, but most metrics are far from stretched, and

stocks still look attractive relative to bonds. • We favor large caps and small caps to mid caps, value over growth, and div. growth to high div. yield.• Overweight Health Care, Financials, Telecom, and Cons. Discr. Underweight: Materials, Utilities and

Consumer Staples. • Post-US election, we believe that tax reform beneficiaries could outperform, whereas fiscal stimulus

beneficiaries could disappoint. See 2017 Theme Screens report for details.

• Risks: protectionism and trade wars crimp growth and squeeze margins,sales growth fails to materialize, global growth disappoints, economic shock tied to credit, global recession; a slowdown in corporate buybacks is not offset by rotation out of fixed income into equities.

• We expect volatility to remain elevated in 2017 as the likelihood of meaningful growth policies wax and wane with political rhetoric.

Europe (James Barty) • We are constructive on European equities especially the earnings cycle given accelerating nominal global

growth. We forecast 11% EPS growth this year and have 5% upside to our 12m Stoxx 600 rolling target of 390.

• Longer-term we think Europe can outperformance the US if Le Pen doesn’t win the French election as uncertainty is priced out of European equities allowing them to re-rate and flows to return.

• We are watching rising in rates closely. We see 30-50bp runway for inflation breakevens to rise back to longer term levels before real rates lead the move, which is typically equity negative.

• Our sector allocation is framed around four themes: 1) skew to reflation beneficiaries with o/w Banks on the short duration side. 2) preference for beneficiaries of rising energy prices / inflation (o/w Oils & Chems, u/w Autos, Construction), 3) avoid UK consumer sectors (u/w Retail and Travel), 4) value preference in Defensives (Utilities and Pharma overweight vs Food & Beverage underweight).

• Political risks likely to dominate into elections in Holland, France: downside from populism gaining further ground; upside if reformers come to power.

• Escalation of US trade policy risks causing risk-off move or upside surprise to tax reform/ fiscal spending expectations causing dollar / US rates overshoot.

• More hawkish ECB policy and / or sharp rise in bond yields without a complementary pick-up in growth and inflation expectations would put pressure on periphery yields in particular.

• Chinese growth or financial stability concerns resurface.

Japan (Shusuke Yamada) • We expect USD/JPY to rise to 122 in 1H17 and the Nikkei 225 index to end the year at 21,000. • Constructive on Japanese equity for five reasons. 1) Contrarian resumption of JPY weakness to end

Japanese deflation. We expect $/¥ to rise back to 120 this year. 2) A policy return to nominal reflation with the new economic package closing much of the existing GDP gap and the BoJ's September policy meeting strengthening the sustainability of monetary policy. 3) Portfolio rebalancing by Japanese investors. 4) Stretched pessimism over undervaluation of Japanese shares. 5) Long-term chart technical remain bullish with a long-term technical objective of 28,500 for the Nikkei.

Risks: • Heightened US protectionism and a weak dollar policy. • Adverse effects from rising interest rates.• RMB and oil weakening.

Asia-Pac ex-Japan (Ajay Kapur) • We turned tactically neutral on Asia ex-Japan (AxJ) on account of the global equity risk-love sentiment

reaching euphoric levels. However, we continue to remain structurally bullish on the region based on reasonable valuations, undervalued currencies, good macro fundamentals and an expected torrent of free cash flow (FCF). We expect FCF in AxJ to more than double from 2016 to 2018. The projected FCF-to-sales ratio is likely to hit close to a record high of 5.8% by 2018 from 3.2% at end-2016.

• Leading indicators of AxJ earnings growth - world trade, US ISM, asset price growth indicator (which has an opinion on global growth), China monetary conditions and earnings revisions suggest 20% Asia ex-Japan earnings growth in 2017. The Street has EPS growth at 15% for 2017.

• Overweight: China, Korea and Taiwan; Underweight: The Philippines, India, Malaysia and Hong Kong.

Downside risks • Stronger USD• Protectionism• China policy tightening• European politics

Emerging Markets (Ajay Kapur)• We are tactically neutral on Emerging Markets on account of the global equity risk-love sentiment reaching

euphoric levels.). However, our structural bullishness on EMs remains intact. EM valuations are reasonable, currencies are competitive, EM financial vulnerability is at a 10-year low, while a slew of indicators are suggesting nominal global growth is likely to continue to pick up.

• EEMEA cross asset strategist David Hauner has a long-term positive stance on EEMEA but believes March may bring a pullback in EEMEA equities. Our LatAm strategist Felipe Hirai, is positive on LatAm equities.

• Overweight: Russia, China, Korea, Taiwan and Turkey; Underweight: The Philippines, India, Malaysia, South Africa, and Mexico.

Downside risks • Policy tightening in China. • Stronger USD. • US growth is weaker and inflation is higher than what consensus expects.

Source: BofA Merrill Lynch Global Research

20 The RIC R

eport | 14 March 2017

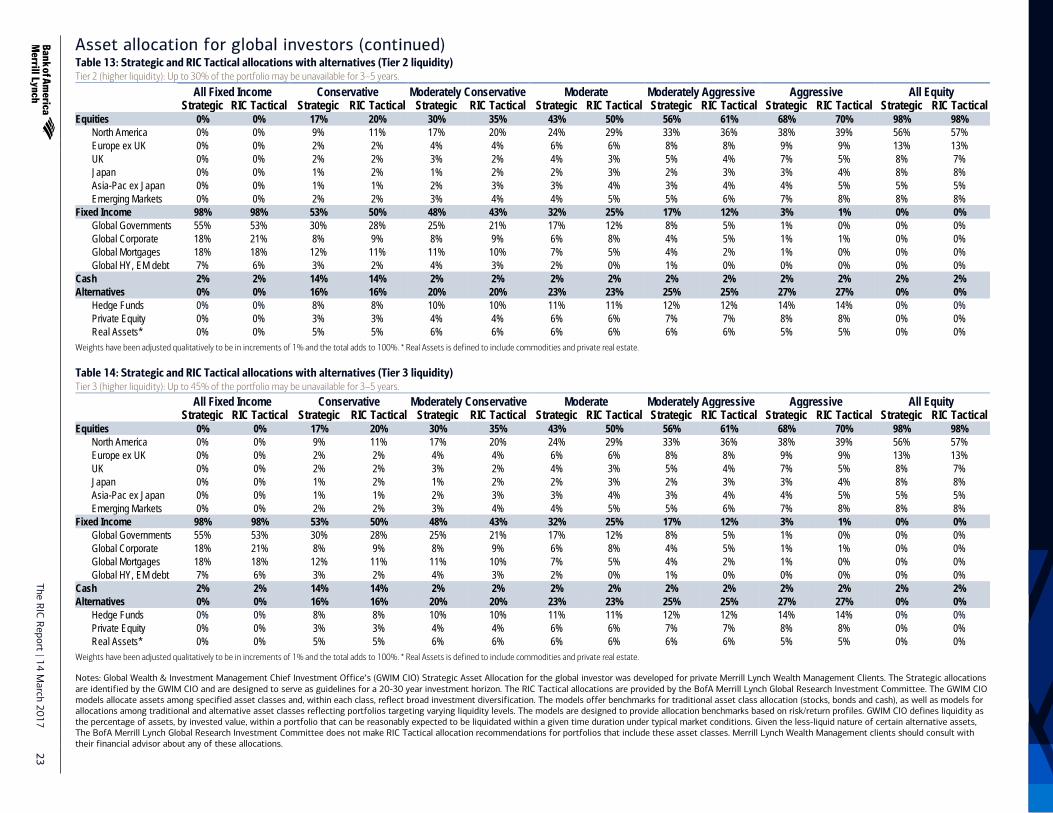

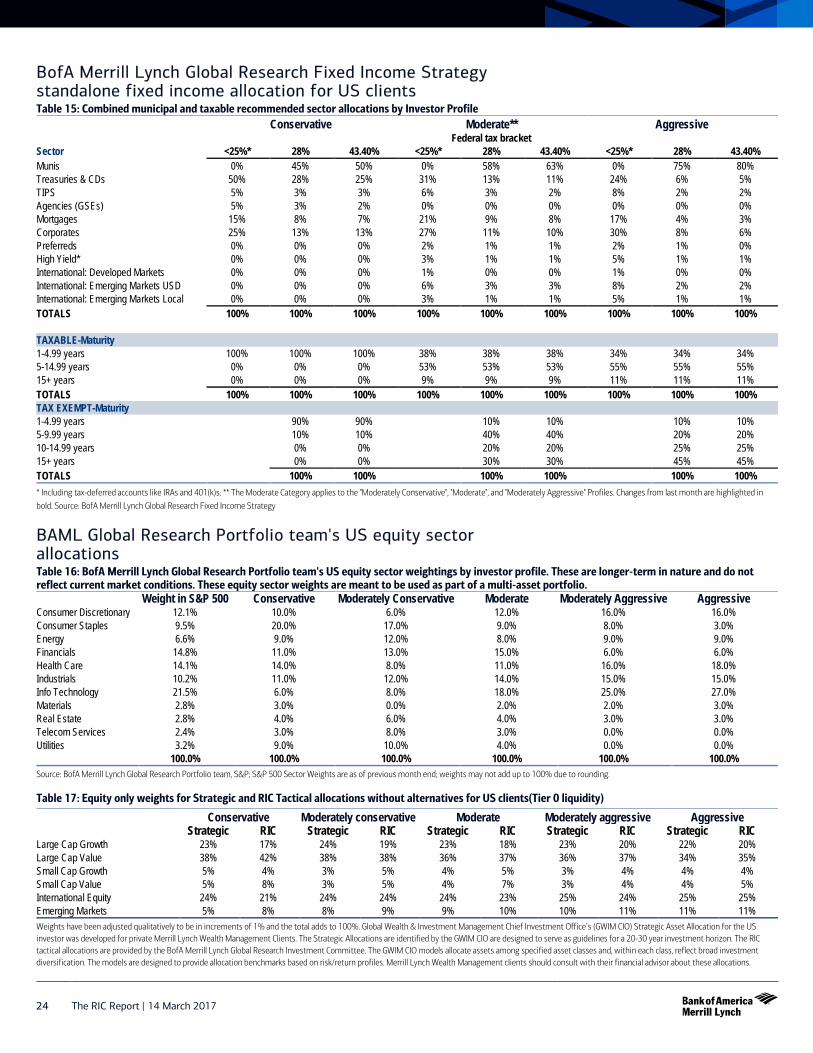

Asset allocation for individual investors The tables below represent asset allocation recommendations by investor profile (Conservative – Aggressive). Strategic allocations are designed to be long-term, 20- to 30-year benchmarks developed by the Global Wealth & Investment Management Chief Investment Office (GWIM CIO). RIC Tactical allocations have a 12-month horizon,and are provided by the BofA Merrill Lynch Global Research Investment Committee. Both Strategic and RIC Tactical allocations are intended for individual investors.

Asset allocation for US clients Table 7: Strategic and Tactical allocations without alternative assets (Tier 0 liquidity) Tier 0 (highest liquidity): Highest liquidity needs with none of the portfolio invested in less liquid alternative asset categories.

All Fixed Income Conservative Moderately Conservative Moderate Moderately Aggressive Aggressive All Equity Strategic RIC Tactical Strategic RIC Tactical Strategic RIC Tactical Strategic RIC Tactical Strategic RIC Tactical Strategic RIC Tactical Strategic RIC Tactical

Equities 0% 0% 21% 24% 37% 42% 53% 60% 69% 74% 84% 89% 98% 98% Large Cap Growth 0% 0% 5% 4% 9% 8% 12% 11% 16% 15% 19% 18% 23% 22% Large Cap Value 0% 0% 8% 10% 14% 16% 19% 22% 25% 27% 29% 31% 36% 36% Small Cap Growth 0% 0% 1% 1% 1% 2% 2% 3% 2% 3% 3% 4% 3% 3% Small Cap Value 0% 0% 1% 2% 1% 2% 2% 4% 2% 3% 3% 4% 4% 5% International Equity 0% 0% 5% 5% 9% 10% 13% 14% 17% 18% 21% 22% 24% 24% Emerging Markets 0% 0% 1% 2% 3% 4% 5% 6% 7% 8% 9% 10% 8% 8%

Fixed Income 98% 98% 55% 52% 61% 56% 45% 38% 29% 24% 14% 9% 0% 0% Governments 28% 27% 17% 15% 17% 14% 14% 10% 9% 6% 5% 2% 0% 0% Mortgages 23% 23% 12% 11% 15% 14% 11% 9% 7% 6% 3% 2% 0% 0% Corporates 24% 28% 10% 12% 15% 17% 14% 16% 9% 10% 4% 5% 0% 0% High Yield 7% 5% 4% 3% 5% 3% 4% 2% 3% 2% 1% 0% 0% 0% Intl Fixed Income 16% 15% 12% 11% 9% 8% 2% 1% 1% 0% 1% 0% 0% 0%

Cash 2% 2% 24% 24% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% Weights have been adjusted qualitatively to be in increments of 1% and the total adds to 100%.

Table 8: Strategic and Tactical allocations with alternative assets (Tier 1 liquidity) Tier 1 (higher liquidity): Up to 15% of the portfolio may be unavailable for 3–5 years.

All Fixed Income Conservative Moderately Conservative Moderate Moderately Aggressive Aggressive All Equity Strategic RIC Tactical Strategic RIC Tactical Strategic RIC Tactical Strategic RIC Tactical Strategic RIC Tactical Strategic RIC Tactical Strategic RIC Tactical

Equities 0% 0% 19% 22% 35% 40% 50% 57% 66% 71% 80% 82% 98% 98% Large Cap Growth 0% 0% 4% 4% 8% 7% 11% 10% 16% 15% 18% 16% 23% 22% Large Cap Value 0% 0% 7% 9% 13% 15% 18% 21% 24% 26% 28% 29% 36% 36% Small Cap Growth 0% 0% 1% 1% 1% 2% 1% 2% 2% 3% 3% 4% 3% 3% Small Cap Value 0% 0% 1% 2% 1% 2% 2% 4% 2% 3% 3% 4% 4% 5% International Equity 0% 0% 5% 5% 9% 10% 13% 14% 16% 17% 20% 20% 24% 24% Emerging Markets 0% 0% 1% 1% 3% 4% 5% 6% 6% 7% 8% 9% 8% 8%

Fixed Income 98% 98% 55% 52% 50% 45% 33% 26% 17% 12% 3% 1% 0% 0% Governments 28% 27% 18% 16% 14% 11% 10% 6% 6% 3% 1% 0% 0% 0% Mortgages 23% 23% 12% 11% 13% 12% 8% 6% 4% 3% 1% 0% 0% 0% Corporates 24% 28% 9% 10% 13% 14% 10% 12% 5% 6% 1% 1% 0% 0% High Yield 7% 5% 4% 3% 4% 3% 3% 1% 1% 0% 0% 0% 0% 0% Intl Fixed Income 16% 15% 12% 12% 6% 5% 2% 1% 1% 0% 0% 0% 0% 0%

Cash 2% 2% 15% 15% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% Alternatives 0% 0% 11% 11% 13% 13% 15% 15% 15% 15% 15% 15% 0% 0%

Hedge Funds 0% 0% 8% 8% 10% 10% 11% 11% 11% 11% 11% 11% 0% 0% Private Equity 0% 0% 0% 0% 0% 0% 0% 0% 0% 0% 0% 0% 0% 0% Real Assets* 0% 0% 3% 3% 3% 3% 4% 4% 4% 4% 4% 4% 0% 0%

Weights have been adjusted qualitatively to be in increments of 1% and the total adds to 100%. * Real Assets is defined to include commodities and private real estate.

The RIC Report | 14 M

arch 2017 21

Asset allocation for US investors (continued) Table 9: Strategic and RIC allocations with alternative assets (Tier 2 liquidity) Tier 2 (moderate liquidity): Up to 30% of the portfolio may be unavailable for 3–5 years.

All Fixed Income Conservative Moderately Conservative Moderate Moderately Aggressive Aggressive All Equity Strategic RIC Tactical Strategic RIC Tactical Strategic RIC Tactical Strategic RIC Tactical Strategic RIC Tactical Strategic RIC Tactical Strategic RIC Tactical

Equities 0% 0% 17% 20% 32% 37% 46% 53% 60% 65% 73% 75% 98% 98% Large Cap Growth 0% 0% 4% 4% 7% 6% 10% 9% 14% 13% 16% 14% 23% 22% Large Cap Value 0% 0% 6% 8% 12% 14% 16% 19% 21% 23% 26% 27% 36% 36% Small Cap Growth 0% 0% 1% 1% 1% 2% 2% 3% 2% 3% 3% 4% 3% 3% Small Cap Value 0% 0% 1% 2% 1% 2% 2% 4% 2% 3% 3% 4% 4% 5% International Equity 0% 0% 4% 4% 8% 9% 12% 13% 15% 16% 18% 18% 24% 24% Emerging Markets 0% 0% 1% 1% 3% 4% 4% 5% 6% 7% 7% 8% 8% 8%

Fixed Income 98% 98% 55% 52% 51% 46% 35% 28% 19% 14% 3% 1% 0% 0% Governments 28% 27% 18% 16% 15% 12% 11% 7% 6% 3% 1% 0% 0% 0% Mortgages 23% 23% 12% 11% 13% 12% 8% 6% 5% 4% 1% 0% 0% 0% Corporates 24% 28% 9% 10% 12% 13% 11% 13% 5% 6% 1% 1% 0% 0% High Yield 7% 5% 4% 3% 4% 3% 3% 1% 2% 1% 0% 0% 0% 0% Intl Fixed Income 16% 15% 12% 12% 7% 6% 2% 1% 1% 0% 0% 0% 0% 0%

Cash 2% 2% 16% 16% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% Alternatives 0% 0% 12% 12% 15% 15% 17% 17% 19% 19% 22% 22% 0% 0%

Hedge Funds 0% 0% 6% 6% 8% 8% 9% 9% 9% 9% 11% 11% 0% 0% Private Equity 0% 0% 2% 2% 3% 3% 4% 4% 6% 6% 7% 7% 0% 0% Real Assets* 0% 0% 4% 4% 4% 4% 4% 4% 4% 4% 4% 4% 0% 0%

Weights have been adjusted qualitatively to be in increments of 1% and the total adds to 100%. * Real Assets is defined to include commodities and private real estate.

Table 10: Strategic and RIC allocations with alternative assets (Tier 3 liquidity) Tier 3 (lower liquidity): Up to 45% of the portfolio may be unavailable for 3–5 years.

All Fixed Income Conservative Moderately Conservative Moderate Moderately Aggressive Aggressive All Equity Strategic RIC Tactical Strategic RIC Tactical Strategic RIC Tactical Strategic RIC Tactical Strategic RIC Tactical Strategic RIC Tactical Strategic RIC Tactical

Equities 0% 0% 17% 20% 32% 37% 46% 53% 60% 65% 73% 75% 98% 98% Large Cap Growth 0% 0% 4% 4% 7% 6% 10% 9% 14% 13% 16% 14% 23% 22% Large Cap Value 0% 0% 6% 8% 12% 14% 16% 19% 21% 23% 26% 27% 36% 36% Small Cap Growth 0% 0% 1% 1% 1% 2% 2% 3% 2% 3% 3% 4% 3% 3% Small Cap Value 0% 0% 1% 2% 1% 2% 2% 4% 2% 3% 3% 4% 4% 5% International Equity 0% 0% 4% 4% 8% 9% 12% 13% 15% 16% 18% 18% 24% 24% Emerging Markets 0% 0% 1% 1% 3% 4% 4% 5% 6% 7% 7% 8% 8% 8%

Fixed Income 98% 98% 55% 52% 51% 46% 35% 28% 19% 14% 3% 1% 0% 0% Governments 28% 27% 18% 16% 15% 12% 11% 7% 6% 3% 1% 0% 0% 0% Mortgages 23% 23% 12% 11% 13% 12% 8% 6% 5% 4% 1% 0% 0% 0% Corporates 24% 28% 9% 10% 12% 13% 11% 13% 5% 6% 1% 1% 0% 0% High Yield 7% 5% 4% 3% 4% 3% 3% 1% 2% 1% 0% 0% 0% 0% Intl Fixed Income 16% 15% 12% 12% 7% 6% 2% 1% 1% 0% 0% 0% 0% 0%

Cash 2% 2% 16% 16% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% Alternatives 0% 0% 12% 12% 15% 15% 17% 17% 19% 19% 22% 22% 0% 0%

Hedge Funds 0% 0% 6% 6% 8% 8% 9% 9% 9% 9% 11% 11% 0% 0% Private Equity 0% 0% 2% 2% 3% 3% 4% 4% 6% 6% 7% 7% 0% 0% Real Assets* 0% 0% 4% 4% 4% 4% 4% 4% 4% 4% 4% 4% 0% 0%