the retail labour market - flinders university - adelaide ... · the retail labour market report by...

TRANSCRIPT

The Retail

Labour Market

Report by

National Institute of Labour StudiesProfessor Sue Richardson

for

Coles Myer Ltd

August 2003

Contents

Executive Summary................................................................................................................1

1. Introduction.......................................................................................................................6

2. Overview of Retail Employment....................................................................................7

3. Do Supermarkets Reduce Retail Employment?....................................................14

4. Productivity in the Retail Industry...............................................................................18

5. The Structure of the Retail Industry...........................................................................22

5.1 A Detailed Snapshot of the Retail Industry....................................................22

5.2 Changes over Time: Hours...............................................................................24

5.3 Changes over Time: Turnover...........................................................................24

5.4 Changes over Time: Size of Business............................................................28

6. Employment in the Retail Industry.............................................................................33

6.1 Total Employment................................................................................................34

6.2 Sectors within Retail Employment...................................................................35

6.3 Female and Male Employment.........................................................................36

6.3 Hours Worked......................................................................................................42

7. Earnings.........................................................................................................................44

References...........................................................................................................................49

List of Tables

Table 1: Characteristics of the Retail Labour Force, and a Comparisonwith the Total Australian Labour Force, February 2003 12

Table 2: Employment, and Wages as a Share of Business Activity, byType of Food Retail Business 17

Table 3: Output, Labour Input and Productivity in the Retail Sector, 1974-75 to 1998-99 (average annual rates of growth, per cent per year) 20

Table 4: Characteristics of Components of the Retail Industry, 1998-99 23

Table 5: Retail Group Share in Total Retail Turnover, 1982 and 2003

(per cent). .....................................................................................................27

Table 6: Numbers of People Employed in Retailing, 1984,1996and 2003 .......................................................................................................37

Figures and Diagrams

Diagram 1(b): Structure of All Businesses and Large Businesses,Australia and Retail, 2000-01 11

Figure 1: Retail Indexes of Output, Hours Worked and LabourProductivity, 1984-85 to 1998-99 (Index 1984-5 = 100) 21

Figure 2: Total Retail Turnover Adjusted for CPI, $m 26

Figure 3: Retail Turnover Trend Estimates, by Industry Group1982-2001 26

Figure 4: Food Retail Turnover 1982-2001 Adjusted for CPI 27

Figure 5a: Number of Retail Businesses by Employer Size Group,1983-84, 1988-2000 30

Figure 5b: Number of Retail Businesses by Employer Size Group,1983-84m, 1988-2000 (reported as deviations from thestarting value) 30

Figure 6: Employment in Small Retail Businesses as a Proportionof All Employment in Retail Trade, 1983-84, 1988-2000 31

Figure 7: Employment in Small Retail Businesses as a Proportionof All Employment in Retail Trade, 1983-84, 1988-2000 31

Figure 8: Non-employing Retail Businesses as a Proportion of AllRetail Businesses, 1983-84, 1988-2000 33

Figure 9: Number of People Employed in Australian Businesses,1983-84m, 1988-2000 (reported as deviations from thestarting value) 35

Figure 10: Number of Male and Female Employees in the RetailIndustry 1985-2001 38

Figure 11(a): Number of Employers in the Retail Industry 1985-2001 39

Figure 11(b): Male and Female Own-Account Workers in the RetailIndustry 1985-2001 40

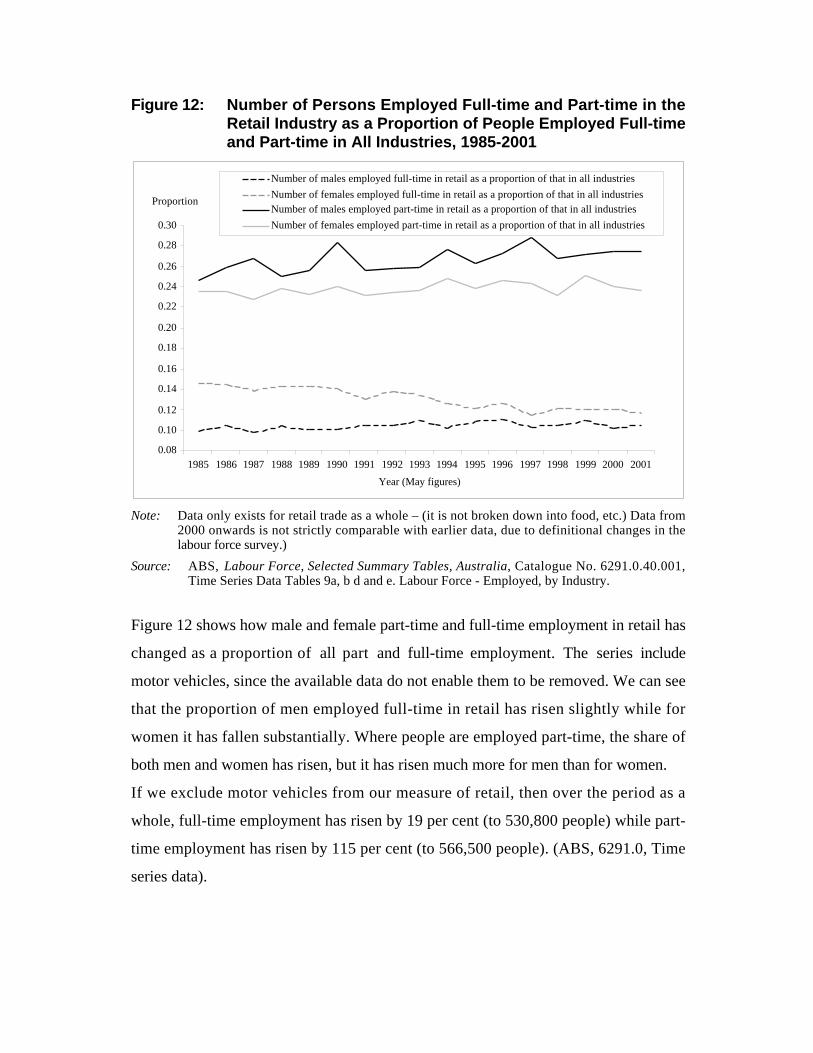

Figure 12: Number of Persons Employed Full-time and Part-timein the Retail Industry as a Proportion of People EmployedFull-time and Part-time in All Industries, 1985-2001 41

Figure 13: Hours Worked in the Retail Industry and a Proportion ofHours Worked in All Industries, 1985-2001 43

Figure 14: Real Average Weekly Earnings in Retail, 1984-2001,1989-90 = 100 45

Figure 15: Real Average Weekly Earnings, Full-time Adults in Retail,1984-2001, Base 1989-90 = 100 46

Figure 16: Average Weekly Earnings for All Persons Employedin the Retail Industry as a Proportion of the AverageWeekly Earnings for All Persons Employed in AllIndustries, 1984-2001 48

Figure 17: Average Full-time Weekly Earnings for Persons Employedin the Retail Industry as a Proportion of the AverageFull-time Weekly Earnings for All Persons Employedin All Industries, 1984-2001 48

Executive Summary

Retailing is a major economic activity and employs more people than any other

Australian industry. This report describes the character of employment in the retail

industry, how it compares with employment in other industries, how it has changed

over time, and how it differs between large and small retailers. This information is

placed in the context of developments in the economy as a whole. Changes in the

characteristics of employment over time are related to changes in the structure of the

retail industry. Part of the examination includes a direct look at the question of

whether growth in market share by the large retailers is detrimental to employment in

the retail industry.

In May 2003, retailing comprised about 5 per cent of the Australian GDP (compared

with 3% for agriculture) and employed 1.5 million people, or 15 per cent of all

employment. Like the rest of the economy, the retail industry has the characteristic

that most firms are small yet half of the workforce work in large firms. The handful of

large businesses accounted for 41 per cent of income. Retail symbolizes much of the

change that has been occurring in the Australian workplace over the past 25 years,

with a relatively small proportion of employees being full-time males and many

working on part-time and casual terms. More than half of retail workers are employed

part-time, two-thirds of whom are female. The workforce is also remarkably young,

which will pose a challenge for the industry as the cohort of young workers shrinks in

size over the coming decades.

The distinctive features of retail employment

The character of employment in retail is quite different from employment in the rest

of the economy. This is especially so if the sale and service of motor vehicles is

excluded: car retailing has a relatively masculine, full-time and higher paid workforce.

Compared with all employment, employment in retail has:

v a much higher proportion of part-time workers, and a higher proportion of women;

v a higher than expected number of employers, especially female employers;

v a very young workforce: half of employees aged 15-19 work in retail but only 11

per cent of those aged over 54;

v an occupational structure that is quite different from the workforce as a whole,

with few managers and administrators and two thirds of all people employed in

elementary clerical, sales and service jobs;

v a disproportionate number of people working part-time, including almost one third

of all people who work fewer than 16 hours per week;

v relatively low wages;

v a relatively low level of formal education among employees.

Does supermarket growth reduce employment?

We examine the question of whether an expansion of supermarkets at the expense of

smaller stores would reduce total retail employment. To do this, it is necessary to

compare supermarket employment with other areas of retail that are similar to

supermarkets in the service and products they provide, but differ in size. We find that

the employment per unit of sales and per unit of production is at least as high in the

large supermarkets/grocery stores as it is in the small greengrocers and liquor stores.

While the evidence is not conclusive, it provides no support for the view that the

transfer of business from the small stores to the large supermarkets would decrease

total employment or labour earnings.

Changes in retail over time

Over the 24 year period from 1974-5 to 1998-9, multifactor productivity in the retail

sector is estimated to have risen at an average rate of 0.3 per cent per annum. The

comparable figure for the whole market sector of the economy is 0.9. Multifactor

productivity in the retail sector is estimated to have fallen over the decade 1984-94,

then turned around to rise at a rate of 1.3 per cent for the remainder of the 1990s.

Labour inputs, which are measured as the number of hours worked, have grown over

the whole period, but at different rates. Growth was especially fast in the period

1984-5 to 1991-2 and continued to be quite strong for the rest of the 1990s. Labour

productivity, however, fell in the middle period, while growing strongly at the

beginning and end of the period.

There is considerable diversity within the retail sector in growth, productivity and

employment changes over time.

Supermarkets and grocery stores are the largest employers within the retail sector.

They saw a steady growth in output but fluctuating changes in employment over the

past quarter century , with no growth until after the recession of the early 1990s.

After a few years of employment growth, employment has remained steady and the

growth in output has been accomplished largely by an increase in output per hour

worked (labour productivity), rather than by an increase in employment.

Hours of employment have grown fastest (over 60 per cent) in Furniture, houseware

and appliances and in Other personal and household goods. They have fallen quite

substantially in Department stores and slightly in Clothing and soft goods. The growth

in labour hours is not systematically related to growth in output, which causes trends

in labour productivity to vary substantially across the sectors. The highest growth in

output (50 per cent or more) is in Other personal and household goods, Furniture,

houseware and appliances (the two sectors where employment has also grown

fastest) and Supermarkets and grocery stores.

The selling of food and groceries dominates the retail sector, accounting for 43 per cent

of the gross product of the industry. The relatively rapid growth in sales of food and

groceries has been in the supermarkets, rather than in the specialist food shops.

Supermarkets and grocery stores predominate in terms of output, but small specialised

food retailers provide almost as much employment, though at a lower level of annual

earnings. The level of annual earnings reflects both hourly rates of pay and number of

hours worked. These small food stores are relatively labour intensive, contributing

more to employment than their share of industry gross product would suggest.

As is shown in more detail in the report, the major changes over the past 18 years in

retail employment are:

v Total employment in retailing grew faster than in the economy as a whole, but a

little slower than employment in the private business sector;

v There has been a sizeable fall in the proportion of retail employment that is in

small (less than 20 workers) businesses;

v Self-employment in retail has fallen from 22 per cent to 14 per cent of all retail

employment with most of the fall occurring in the last decade;

v Part-time employment grew much faster than full-time employment (147%

compared with 27%);

v Employment in Food Retailing grew relatively fast (78%) ;

v The growth in part-time employment was especially strong (181%), and in full-

time employment especially weak (13%), in Food Retailing.

v By 2003, there were almost as many people employed in Food Retailing as in

Personal and Household Goods.

v Food Retailing has a high and rising ratio of part-time to full-time staff (1.6

compared with 0.8 for Personal and Household Goods in 2003).

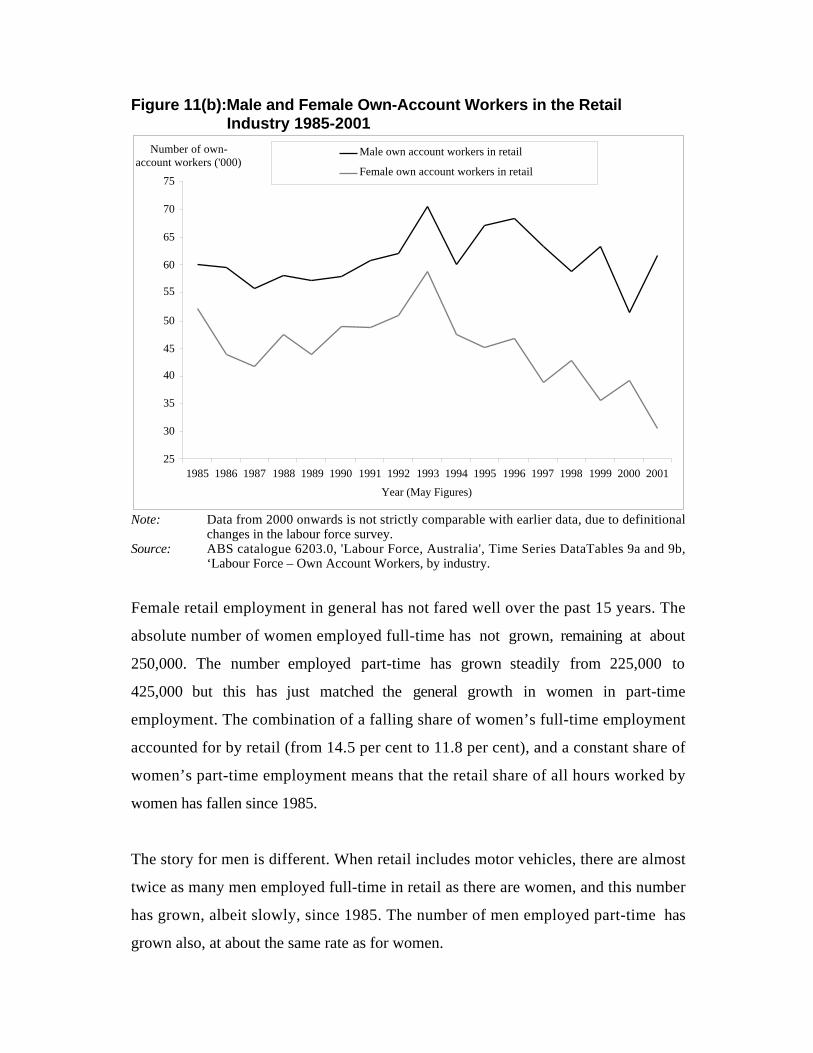

Female retail employment in general has not fared well over the past 15 years. The

absolute number of women employed full-time has not grown, remaining at about

250,000. The number employed part-time has grown steadily from 225,000 to

425,000 but this has just matched the general growth in part-time employment for

women. The combination of a falling share of women’s full-time employment

accounted for by retail (from 14.5 per cent to 11.8 per cent), and a constant share of

women’s part-time employment means that the retail share of all hours worked by

women has fallen since 1985.

While total hours worked by women in retail have been growing a little faster than

total hours worked by men, the hours growth for women has not matched that

occurring in other parts of the economy. Thus there are two trends. Within the retail

sector, the share of total hours worked by women has been rising. But for the

economy as a whole, the share of total hours worked in the retail sector, and especially

the share of women’s total hours worked in the retail sector, has been falling.

It is clear that over the past 15 or so years in retail there has been a trend towards

larger businesses and away from small and owner-operated businesses. While the

absolute number of small businesses has not fallen, their share of all businesses has.

Employment in small businesses has fallen substantially as a share of all retail

employment, to just under half, and this trend has been underway for the whole

period since the mid 1980s. Own account workers have also fallen substantially as a

proportion of all retail workers. But the fall in self-employment has been quite recent,

the downturn starting in the mid-1990s. It is not yet clear that this is part of a long-

term trend.

Retail employment is not well paid. The average adult full-time retail worker earns

about three-quarters of the amount earned by the average Australian adult full-time

worker. One reason for the relatively low pay is the high ratio of low paying

occupations, such as sales, to high paying occupations, such as professional and

managerial, in the retail sector. Relative pay for full-time women retail workers is

higher than it is for men and has fluctuated less. As for men, however, it has fallen

somewhat since the mid-1980s.

In brief, the composition of employment in the retail sector has been changing. The

self-employed are diminishing as a component of total retail employment and

becoming more masculine; employees are becoming more feminine; there has been a

rapid expansion of the role of part-time staff and increasingly people are employed by

large rather than small businesses.

1. Introduction1

Retailing is a major economic activity and a major employer. In May 2003, it

comprised about 5 per cent of the Australian GDP (compared with 3% for agriculture)

and employed 1.49 million people, or 15.6 per cent of all employment2. Indeed, it is

the biggest employer of all industries in Australia. Its output (ie, value added) rose in

real terms at 2.7 per cent per annum between 1984-5 and 1998-9, to $31.1 billion.3 It

has a structure much like that of the rest of the private sector, with small businesses

(employing fewer than 20 people) comprising 97 per cent of all businesses but only

38 per cent of total income. The fewer than one per cent of large businesses which

employ 200 people or more accounted for 41 per cent of income. It symbolizes much

of the change that has been occurring in the Australian workplace over the past 25

years, with a relatively small proportion of employees being full-time males and many

working on part-time and casual terms. More than half of retail workers are employed

part-time, two-thirds of whom are female. How retail employment is changing, and

whether it represents an exemplar of the future of work in general is a question of great

social interest.

The past 25 years has seen a large withdrawal of men from the labour force and a large

growth in the employment of married women. It has also seen a substantial

substitution of part-time and casual jobs for full-time and continuing jobs. These

changes have important implications for the way that families work, whether they are

formed at all and their capacity to provide secure and adequate incomes from working.

Employment in retailing has given many people their first work experience. It has been

less good at providing stable employment with reasonably predictable weekly earnings

and some prospects for career progression.

1 Members of the NILS team, particularly Lauren Miller Lewis and Skye Jacobi, have made substantialcontributions to this report.2 ABS Labour Force, catalogue number 6291.0.55.001, Table 4.3 Value added is the value of sales minus the value of purchased inputs: it is the same as wages andsalaries, plus depreciation, interest and profits. The source for these data is the ABS NationalAccounts. Note that ‘retail’ as defined by the ABS excludes the provision of services that are solddirect to consumers, such as hairdressing, real estate sales, house cleaning and trades. See Merrilees andMiller, 1996.

This report describes the character of employment in the retail industry, how this has

changed over time, and how it differs between large and small retailers. Where

possible, this information is placed in the context of developments in the economy as

a whole. Changes over time are related to changes in the structure of the retail

industry.

Part of the examination includes a direct look at the question of whether growth in

market share by the large retailers is detrimental to employment in the retail industry.

In answering this question, we believe it is necessary to consider the meaning of

“detrimental”. For example, if a given number of low paid, casual, deadend jobs was

replaced by a smaller number of better paid, more secure jobs with prospects of

advancement, that might be considered beneficial rather than detrimental. The quality

of jobs and the skills development of those who occupy them matters, as well as the

number of jobs.

Employment can be categorized in a number of ways. These include by type of

employment contract and by the types of people who are employed. We examine

both perspectives.

The report focuses on retailing in general, excluding car sales and service where

possible. To the extent possible with the available data, the report also looks

separately at food retailing and small and large businesses. Note that the usual measure

of retailing, and the one being used here, includes only the sale of goods direct to the

consumer, not of services.

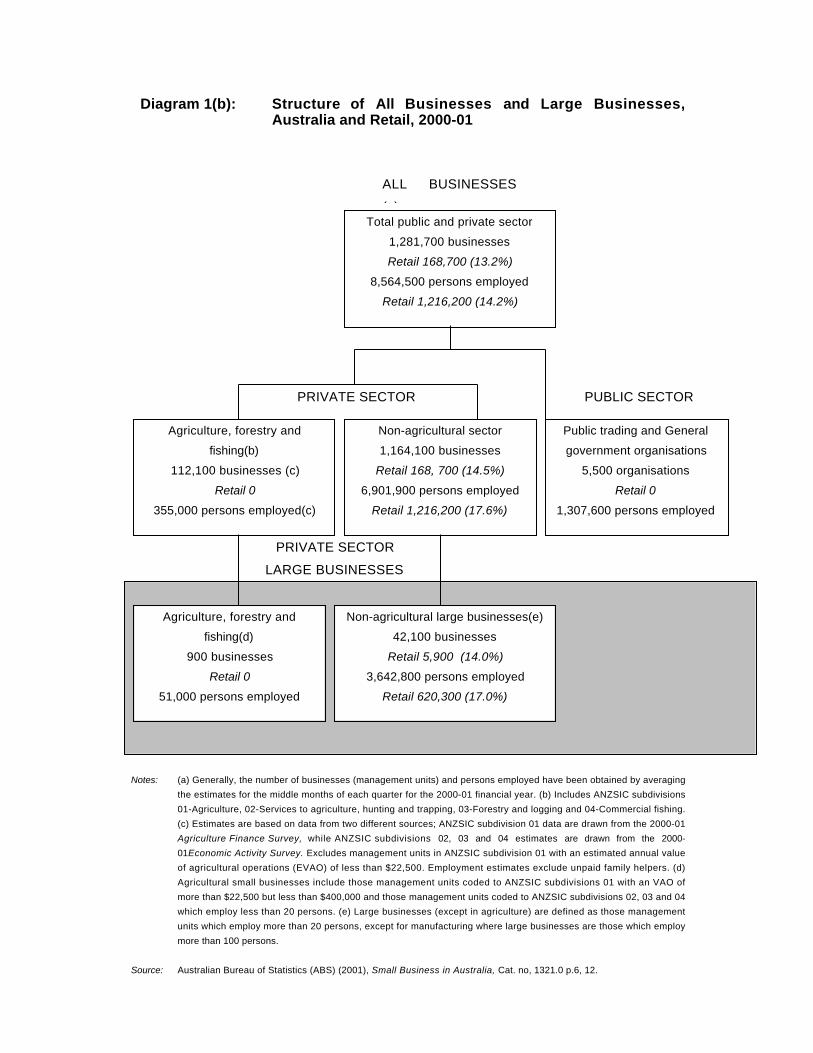

2. Overview of Retail Employment

We start with a picture of the structure of the retail sector, and a comparison with the

structure of Australian businesses as a whole. The retail sector described in the tree

diagram below is based on the definition of retail as used by the Australian Bureau of

Statistics, from where the data are drawn. The ABS defines retailing as comprising

businesses ‘—mainly engaged in the resale of new or used goods to final consumers for

personal or household consumption or in selected repair activities such as repair of

household equipment or motor vehicles.’ (ABS, 1993:157) The data include motor

vehicles sales and service, which constitute about 20 per cent of total retailing.

The structure of businesses and of employment in the Australian economy is set out

in the tree diagram, Diagram 1 below. Comparable data for the retail industry are

included in each box, in italics. The percentage that retail represents of the relevant

category is provided in parentheses. Thus, in 2000-01 there were 168,700 retail

businesses, employing 1,216,200 people. These represent 13.2 per cent and 14.2 per

cent (respectively) of all businesses and of all employment4. Diagram 1 (a) gives

additional data on small business, while Diagram 1 (b) focuses on large businesses.

Further down Diagram 1 (a) we see that there were 93,000 private sector non-

agricultural small retail businesses that employed staff, in which 501,100 people were

employed. This represented 17.2 per cent of such small employing businesses and

19.7 per cent of people employed in such small employing businesses.

We can learn a number of things from this diagram. The retail sector, at 14 per cent of

total employment, is a big employer. The average size of retail businesses (in terms of

employment) is similar to that for all businesses. This is indicated by the fact that the

share of retail in the number of businesses (13.2%) is almost the same as its share in

the number of persons employed (14.2%). Because all retail firms are in the private

sector, and none are in agriculture, forestry or fishing, then retail is a larger share of

non-agricultural private businesses (14.5%) and employment (17.6%). It does not

have an unusually large proportion of small businesses, since its share of non-

agricultural small businesses (14.5%) is the same as its share of all non-agricultural

businesses (14.5%). It has a somewhat lower than average number of non-employing

businesses and a larger number of small employing businesses. Among the small

employing businesses, it has a much higher proportion than other industries of people

who are working in their own business (23.6% of all such people) rather than working

as employees.

The picture for large businesses mirrors that of small retail businesses. Large retail

businesses are 14 per cent of all non-agricultural private sector large businesses—the

same share as small retail businesses. Like small businesses, their share of employment

exceeds their share of businesses. This implies that on average each large retail

business employs more people than the typical large business.

We next present a much more detailed look at the characteristics of the retail labour

force, and compare these with the national picture. When reading the right hand

column of the table below, it is helpful in most instances to keep in mind that 15 per

cent of all employed people were employed in retail, in 2003. Then we can see, for

example, that slightly over one third were employed in food retailing, and that retailing

employed much more than its share of workers aged 15-19 (50% of such workers,

compared with 15% of workers overall).

4 This is the latest date for which data in this form can be obtained. The difference between theseestimates of the size of retail and those given earlier are accounted for by minor differences in datasource and definition as used by the ABS.

Diagram 1 (a):Structure of Australian Business and the Retail Sector, 2000-01

Notes: (a) Generally, the number of businesses (management units) and persons employed have been obtained by averaging the estimates for the middle

months of each quarter for the 2000–2001 financial year. (b) Includes ANZSIC Subdivisions 01 – Agriculture, 02 – Services to Agriculture; Hunting

and Trapping, 03 – Forestry and Logging and 04 – Commercial fishing. (c) Estimates are based on data from two different sources; ANZSIC

Subdivision 01 data are drawn from the 1999–2000 Agricultural Finance survey, while ANZSIC Subdivisions 02, 03 and 04 estimates are drawn from

the 1999–2000 Economic Activity Survey. Excludes management units in ANZSIC Subdivision with an estimated annual value of agricultural

operations (EVAO) of less than $22,500. Employment estimates exclude unpaid family helpers. (d) Agricultural small businesses include those

management units coded to ANZSIC Subdivision 01 with an EVAO of more than $22,500 but less than $400,000, and those management units

coded to ANZSIC Subdivisions 02, 03 and 04 which employ less than 20 persons. (e) Small business (except in agriculture) are defined as those

management units which employ less than 20 persons.

Source: Australian Bureau of Statistics (ABS) (2001), Small Business in Australia, Cat. no, 1321.0 p.6, 12.

PRIVATE SECTORSMALL BUSINESSES

PRIVATE SECTOR

Total public and private sector1,281,700 businessesRetail 168,700 (13,2%)

8,564,500 persons employedRetail 1,216,200 (14.2%)

Agriculture, forestry and fishing(b)112,100 businesses (c)

Retail 0

355,000 persons employed(c)

Non-agricultural sector1,164,100 businesses

Retail 168, 700 (14.5%)

6,901,900 persons employedRetail 1,216,200 (17.6%)

Public trading and Generalgovernment organisations

5,500 organisationsRetail 0

1,307,600 persons employed

PUBLIC SECTOR

ALL BUSINESSES (a)

Agriculture, forestry andfishing(d)

111,200 businessesRetail 0

304,000 persons employed

Non-agricultural small businesses(e)1,122,000 businesses

Retail 162,800 (14.5%)

3,259,100 persons employedRetail 595,900 (18.3%)

Non-employing businesses582,100 businesses

Retail 69,800 (12.0%)

713,200 own account workersRetail 94,800 (13.3%)

Employing businesses539,900 businesses

Retail 93,000 (17.2%)

2,545,900 persons employedRetail 501,100 (19.7%)

Employers276,500 persons employed

in their own business

Retail65,200 (23.6%)

Employees(wage & salary earners)

2,269,400 persons employed

Retail435,900 (19.2%)

Diagram 1(b): Structure of All Businesses and Large Businesses,Australia and Retail, 2000-01

Notes: (a) Generally, the number of businesses (management units) and persons employed have been obtained by averaging

the estimates for the middle months of each quarter for the 2000-01 financial year. (b) Includes ANZSIC subdivisions

01-Agriculture, 02-Services to agriculture, hunting and trapping, 03-Forestry and logging and 04-Commercial fishing.

(c) Estimates are based on data from two different sources; ANZSIC subdivision 01 data are drawn from the 2000-01

Agriculture Finance Survey, while ANZSIC subdivisions 02, 03 and 04 estimates are drawn from the 2000-

01Economic Activity Survey. Excludes management units in ANZSIC subdivision 01 with an estimated annual value

of agricultural operations (EVAO) of less than $22,500. Employment estimates exclude unpaid family helpers. (d)

Agricultural small businesses include those management units coded to ANZSIC subdivisions 01 with an VAO of

more than $22,500 but less than $400,000 and those management units coded to ANZSIC subdivisions 02, 03 and 04

which employ less than 20 persons. (e) Large businesses (except in agriculture) are defined as those management

units which employ more than 20 persons, except for manufacturing where large businesses are those which employ

more than 100 persons.

Source: Australian Bureau of Statistics (ABS) (2001), Small Business in Australia, Cat. no, 1321.0 p.6, 12.

PRIVATE SECTOR

LARGE BUSINESSES

PRIVATE SECTOR

Total public and private sector

1,281,700 businesses

Retail 168,700 (13.2%)

8,564,500 persons employed

Retail 1,216,200 (14.2%)

Agriculture, forestry and

fishing(b)

112,100 businesses (c)

Retail 0

355,000 persons employed(c)

Non-agricultural sector

1,164,100 businesses

Retail 168, 700 (14.5%)

6,901,900 persons employed

Retail 1,216,200 (17.6%)

Public trading and General

government organisations

5,500 organisations

Retail 0

1,307,600 persons employed

PUBLIC SECTOR

ALL BUSINESSES

(a)

Agriculture, forestry and

fishing(d)

900 businesses

Retail 0

51,000 persons employed

Non-agricultural large businesses(e)

42,100 businesses

Retail 5,900 (14.0%)

3,642,800 persons employed

Retail 620,300 (17.0%)

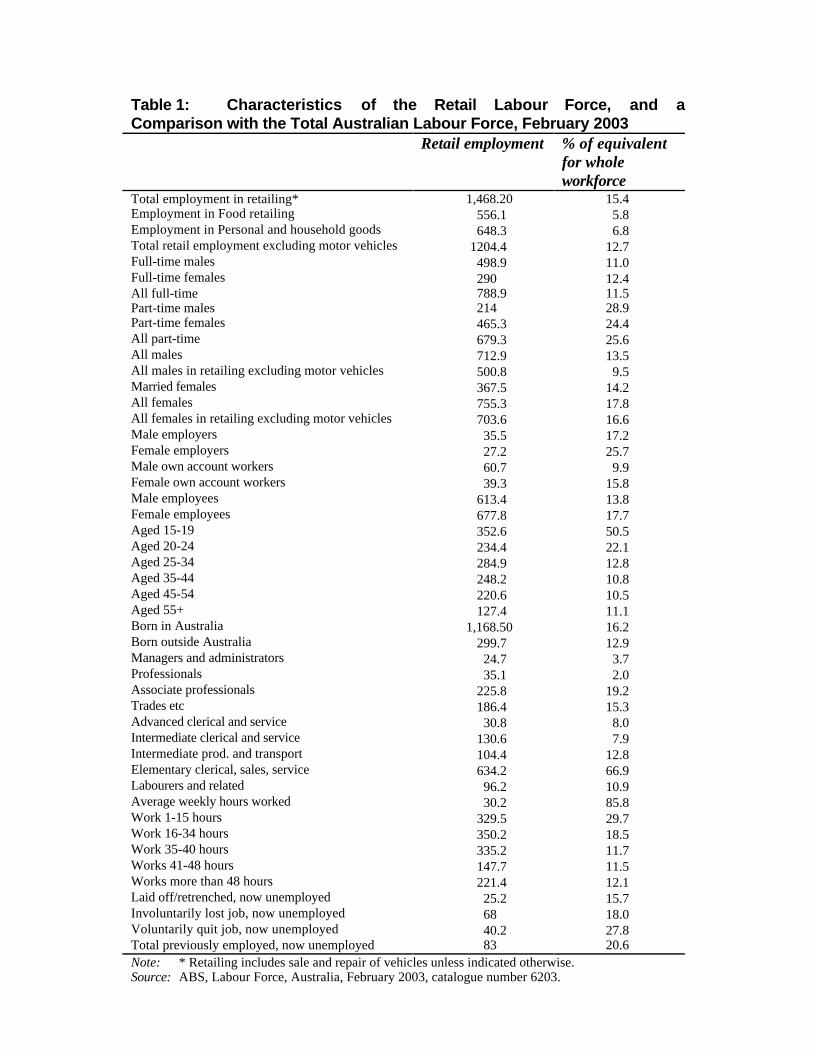

Table 1: Characteristics of the Retail Labour Force, and aComparison with the Total Australian Labour Force, February 2003

Retail employment % of equivalentfor wholeworkforce

Total employment in retailing* 1,468.20 15.4Employment in Food retailing 556.1 5.8Employment in Personal and household goods 648.3 6.8Total retail employment excluding motor vehicles 1204.4 12.7Full-time males 498.9 11.0Full-time females 290 12.4All full-time 788.9 11.5Part-time males 214 28.9Part-time females 465.3 24.4All part-time 679.3 25.6All males 712.9 13.5All males in retailing excluding motor vehicles 500.8 9.5Married females 367.5 14.2All females 755.3 17.8All females in retailing excluding motor vehicles 703.6 16.6Male employers 35.5 17.2Female employers 27.2 25.7Male own account workers 60.7 9.9Female own account workers 39.3 15.8Male employees 613.4 13.8Female employees 677.8 17.7Aged 15-19 352.6 50.5Aged 20-24 234.4 22.1Aged 25-34 284.9 12.8Aged 35-44 248.2 10.8Aged 45-54 220.6 10.5Aged 55+ 127.4 11.1Born in Australia 1,168.50 16.2Born outside Australia 299.7 12.9Managers and administrators 24.7 3.7Professionals 35.1 2.0Associate professionals 225.8 19.2Trades etc 186.4 15.3Advanced clerical and service 30.8 8.0Intermediate clerical and service 130.6 7.9Intermediate prod. and transport 104.4 12.8Elementary clerical, sales, service 634.2 66.9Labourers and related 96.2 10.9Average weekly hours worked 30.2 85.8Work 1-15 hours 329.5 29.7Work 16-34 hours 350.2 18.5Work 35-40 hours 335.2 11.7Works 41-48 hours 147.7 11.5Works more than 48 hours 221.4 12.1Laid off/retrenched, now unemployed 25.2 15.7Involuntarily lost job, now unemployed 68 18.0Voluntarily quit job, now unemployed 40.2 27.8Total previously employed, now unemployed 83 20.6Note: * Retailing includes sale and repair of vehicles unless indicated otherwise.Source: ABS, Labour Force, Australia, February 2003, catalogue number 6203.

From Table 1 we see that retail employment, compared with total employment for the

whole economy:

v When broadly defined, comprises 15.4% of total employment;

v When retailing excludes the sale and repair of cars, comprises 12.7% of totalemployment;

v Has a much higher proportion of part-time workers (about one quarter of all part-time employees), and a higher proportion of women;

v Has a higher than expected number of employers, especially female employers:they comprise one quarter of all female employers;

v Has a very young workforce: half of employees aged 15-19 work in retail but only11 per cent of those aged over 54;

v Has an occupational structure that is quite different from the workforce as awhole, with few managers and administrators and two thirds of all peopleemployed in elementary clerical, sales and service jobs;

v Has a disproportionate number of people working part-time, including almost onethird of all people who work fewer than 16 hours per week;

v Has a disproportionate number of former workers who are now unemployed—arelatively high proportion of whom quit their jobs voluntarily.

While not shown in the table, it is also true that employees in retail have less formal

education than the Australian workforce as a whole. For example, in 1997 28 per cent

of retail employees had post-school qualifications compared with 40 per cent for all

workers. Put another way, 9 per cent of workers with post-school education and 21

per cent of workers without post-school qualifications worked in retail. Between 1984

and 1997, the proportion of all workers without post-school qualifications who

worked in retail rose, from 18 per cent to 21 per cent. Retail employed a higher

proportion of such workers than any other sector (the next largest employer being

manufacturing, with 14 per cent)5.

The major characteristics of retail employment are not static. An examination of how

they have changed over the past 15 years shows that, between 1984 and 2003:

v Total employment in retail (excluding motor vehicle sales and service) has grownfrom 700,000 to 1,204,000, or by 72 per cent;

5 See Barnes, P, Johnson, R, Kulys, A and Hook, S, 1999, Productivity and the Structure of

Employment, Productivity Commission staff research paper, Ausinfo, Canberra, p.27

v This is faster than the rate of growth of all employment (58 per cent);

v Employment in personal and household goods has grown less rapidly than inretail as a whole and in food retailing;

v There has been a rise in the proportion of all employment that is accounted for byretail employment and by food retail employment, but no rise in the proportionemployed in personal and household goods;

v The number of people employed part-time has more than doubled for food andfor total retailing and has grown more slowly for personal and household goods;

v In consequence, part-time employment in food and in total retailing has grown, asa share of all part-time employment, especially for the former: it has fallen forpersonal and household goods retailing;

v There has been no growth in full-time employment in personal and householdgoods retailing and little in food or in total retailing;

v In consequence, full-time employment in total and in the main categories of retail(excluding motor) has fallen as a proportion of all full-time employment;

v Total hours worked in retail have grown by over 10 million, but they have fallenas a proportion of all hours worked, from 13.1% to 12.5%.

3. Do Supermarkets Reduce Retail Employment?

In this section we seek to establish whether the expansion of supermarkets at the

expense of small businesses is likely to reduce overall retail employment. It would do

so if the “labour content” of a unit of sales were higher if the goods were sold by a

small business than if the same goods were sold by a supermarket. By “labour

content” we mean the amount of worker time together with the wage paid for that

time. This is an empirical question. In order to answer it we draw on data from 1998-9

Retail Industry Census (the latest one available). Among other things, the census

contains information on:

v Turnover

v Cost of goods sold

v Wages and other costs of employing labour

v Interest, depreciation, rent, insurance and other expenses

v Number of employed persons

v Industry Gross Product.

It is not easy to establish whether small businesses are more labour intensive in their

operations than are larger firms. In principle, the share of labour costs in value added

(the difference between revenue and the cost of purchased inputs) is the best measure

of how labour intensive is a firm or industry. But many factors can affect labour’s

share of value added at a given moment of observation. In order to identify the effects

of firm size, we need to be able to compare firms that differ in size but otherwise are

the same. For example, they need to be selling the same sort of product, and located in

similar places. In a retail store, two things are being sold. One is the product. The

other is the service that surrounds the sale. Some products, such as spectacles,

inherently require more sales service than do others, such as milk. Some products,

such as fresh bread and takeaway food, are prepared on the premises and the labour

involved in preparation is indistinguishable from the labour involved in the selling. If

small firms specialise in the sale of products that require above average levels of

service or instore preparation, then the labour content of their value added will be

higher. In this case the high labour content is caused by the nature of the product sold

and not by the fact that the retail businesses are small.

In the table below, we examine two measures of the labour intensity of the retail

activity. The retail businesses are confined to those that sell food and groceries, in

order to make them as comparable as possible in their activities. The table

distinguishes supermarkets and grocery stores on the one hand and a range of

specialized food and drink stores on the other. It is not possible to separate

supermarkets from other grocery stores.

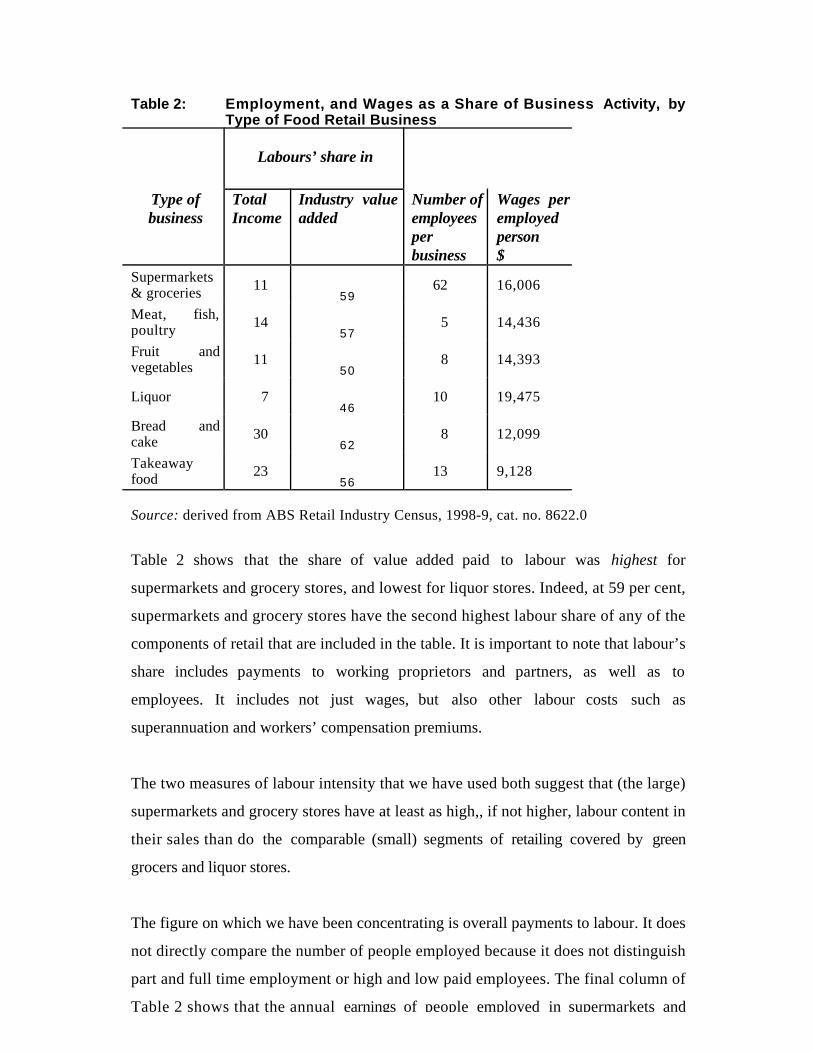

Table 2 shows that, compared with the value of goods purchased and other expenses,

the labour content of what is sold is particularly high for bread and cakes and high also

for takeaway food and meat, fish and poultry. It is lowest for liquor and low also for

supermarkets and groceries and greengrocers. Thirty per cent of total turnover goes to

paying wages for bread and cake shops, whereas only 7 per cent of turnover goes to

paying wages in the sale of liquor. This large difference in labour content occurs

despite the fact that the average size of business is about the same in the two types of

retail outlet. It is reasonable to conclude that the nature of what is sold is the key

factor driving the share of turnover accruing to wages, rather than the size of the

business. Where a product is partly or wholly produced on the premises, the labour

content of what is sold is naturally higher than when a business provides only a retail

service.

In terms of the type of retail product sold, perhaps the best match with supermarkets

is greengrocers and liquor stores. Clearly, the average greengrocer/liquor store (with 8-

10 workers) is much smaller than the average supermarket/grocer (with 62), so this

gives us an opportunity to see if there is a big difference in labour content according to

size.

If labour content is measured as labour costs as a fraction of turnover, the answer is

no: labour content is about the same for all three types of retail outlet, with liquor

stores having the lowest fraction.

An alternative measure of labour intensity is payments to labour as a share of industry

value added. Value added is defined by the ABS as ‘Turnover less purchases and

selected other expenses plus (or minus) the change in the value of stocks’. (ABS,

1994:46). The share of labour in value added indicates how labour intensive, as distinct

from capital or ‘shop space’ intensive, are the arrangements used for providing the

retail service.

Table 2: Employment, and Wages as a Share of Business Activity, byType of Food Retail Business

Labours’ share in

Type ofbusiness

TotalIncome

Industry valueadded

Number ofemployeesperbusiness

Wages peremployedperson$

Supermarkets& groceries 11

5962 16,006

Meat, fish,poultry 14

575 14,436

Fruit andvegetables 11

508 14,393

Liquor 746

10 19,475

Bread andcake 30

628 12,099

Takeawayfood 23

5613 9,128

Source: derived from ABS Retail Industry Census, 1998-9, cat. no. 8622.0

Table 2 shows that the share of value added paid to labour was highest for

supermarkets and grocery stores, and lowest for liquor stores. Indeed, at 59 per cent,

supermarkets and grocery stores have the second highest labour share of any of the

components of retail that are included in the table. It is important to note that labour’s

share includes payments to working proprietors and partners, as well as to

employees. It includes not just wages, but also other labour costs such as

superannuation and workers’ compensation premiums.

The two measures of labour intensity that we have used both suggest that (the large)

supermarkets and grocery stores have at least as high,, if not higher, labour content in

their sales than do the comparable (small) segments of retailing covered by green

grocers and liquor stores.

The figure on which we have been concentrating is overall payments to labour. It does

not directly compare the number of people employed because it does not distinguish

part and full time employment or high and low paid employees. The final column of

Table 2 shows that the annual earnings of people employed in supermarkets and

grocery stores tend to be higher than those of other food retail segments. (They much

higher than for takeaway food, where payments are well below average.) They are

slightly higher than payments to workers in greengrocers, and less than in liquor

stores. On this evidence, the size of the wage bill is a reasonable indicator of the

quantity of employment. Wages and salaries in supermarkets are the same or higher as

a share of turnover and of value added as they are in greengrocers and liquor stores.

This suggests that the employment per unit of sales and of production is at least as

high in the large supermarkets/grocery stores as it is in the small greengrocers and

liquor stores. The transfer of business from the small stores to the large supermarkets

would not, on this evidence, decrease total employment or labour earnings.

Thus there is nothing in Table 2 to support the view that the expansion of

supermarkets at the expense of smaller food retail outlets would reduce overall

employment.

4. Productivity in the Retail Industry

The changes summarized above have occurred in the context of an economy that has

had several major developments over the period since the mid-1980s. Overall, the

growth in output and productivity for the Australian economy has been robust,

compared with other developed countries. The 1980s saw a strong growth in

employment and output, but quite low productivity growth: this has been ascribed in

part to the success of the Accord in keeping wage growth low and in encouraging

employment. Broadly, the reverse occurred in the 1990s, with strong growth in

productivity and less success in increasing employment. In between, there was a

severe recession in 1990-1, which caused low productivity, output and employment

for a few years. Since this recession, macroeconomic conditions in Australia have seen

sustained and quite high levels of growth in output, if not so much in employment.

In the retail sector, output is measured by the Australian Bureau of Statistics (ABS) as

the difference between the value of sales and the cost of the goods sold (value added).

This measure assumes that the average level of service associated with the sale of

goods does not change over time. Productivity is measured as the ratio of the value of

output to the value of the inputs. Labour productivity is the value of output divided

by the number of labour hours. Capital productivity is the value of output divided by

the value of services from capital equipment. Multifactor productivity is the value of

output divided by the value of both the labour and capital inputs. Both the value of

output and the value of capital services are difficult to measure in ways that make

them comparable over time. Hence some caution should be exercised in interpreting

trend figures.

Over the 24 year period from 1974-5 to 1998-9, multifactor productivity in the retail

sector is estimated to have risen at an average rate of 0.3 per cent per annum. The

comparable figure for the whole market sector of the economy is 0.96. Multifactor

productivity in the retail sector is estimated to have fallen over the decade 1984-94,

then turned around to rise at a rate of 1.3 per cent for the remainder of the 1990s.

Multifactor productivity rises, by definition, when output rises faster than inputs.

Table 3 below shows the behaviour of the key productivity measures, for three

intervals over the period 1975-99.

The growth in output varied considerably over the three periods reflected in Table 3.

At 1.5 per cent per annum during 1984-5 to 1991-2, it was less than half the growth

that was achieved for the remainder of the decade (3.9 per cent pa). Productivity

growth tends to decline when output growth slows and vice-versa, and this is

apparent in the table. It is notable that when output growth was slowing, input

(particularly labour input) growth continued at a rapid rate. Labour inputs, which are

measured as the number of hours worked, have grown over the whole period, but at

different rates. Growth was especially fast in the period 1984-5 to 1991-2 and

continued to be quite strong for the rest of the 1990s. Labour productivity, however,

fell in the middle period, while growing strongly in the earlier and later periods.

6 This and subsequent productivity figures are taken from Johnson et al, 2000.

Table 3: Output, Labour Input and Productivity in the Retail Sector,1974-75 to 1998-99 (average annual rates of growth, percent per year)

1974-75 to1984-85

1984-85 to1991-92

1991-92 to1998-99

Output 2.8 1.5 3.9Total inputs 1.5 3.3 2.9Labour 0.6 2.4 1.7Labour productivity 2.2 -0.9 2.2Multifactor productivity 1.3 -1.7 1.0

Source: Estimates based on unpublished ABS data, Gretton and Fisher (1997).

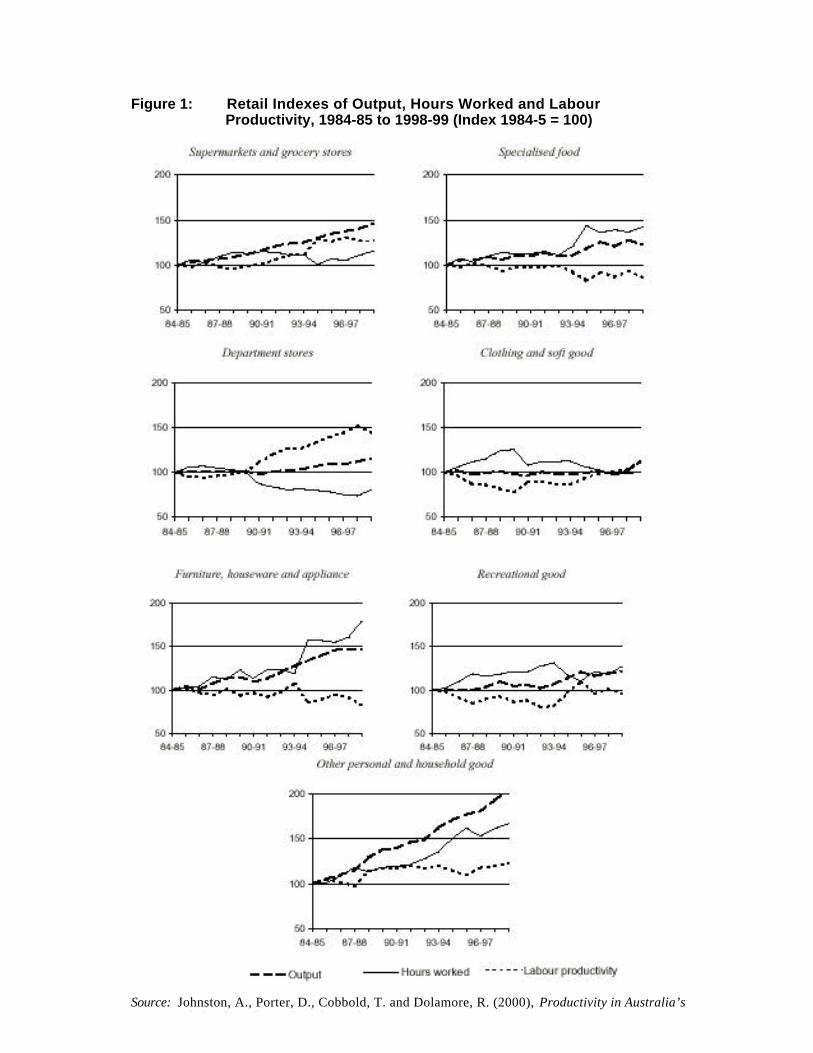

Figure 1, which is taken from Johnston et al (2000), shows the output, employment

and labour productivity trends in sub-sets of the retail industry, for the period from

1984-5 to 1998-9, using unpublished ABS data. It is interesting to see the variety of

experience across the different parts of retail. The data are able to exclude motor

vehicles, which represent about a quarter of retail industry output and 18 per cent of

employment.

Hours of employment have grown fastest (over 60 per cent) in Furniture, houseware

and appliances and in Other personal and household goods. They have fallen quite

substantially in Department stores and slightly in Clothing and soft goods. The growth

in labour hours is not systematically related to growth in output, which is why trends

in labour productivity vary so much across the sectors. The highest growth in output

(50 per cent or more) is in Other personal and household goods, Furniture, houseware

and appliances (the two sectors where employment has also grown fastest) and

Supermarkets and grocery stores. Interestingly, labour productivity has grown fastest

in Department stores, which is a sector that has seen slow growth in output. It

obtained the productivity increase (of 50 per cent) by substantially reducing the

number of hours employed. The next best productivity performer, Supermarkets and

grocery stores, had a substantial rise in output and obtained its productivity growth

by meeting this growing demand with only a modest growth in hours worked.

Figure 1: Retail Indexes of Output, Hours Worked and LabourProductivity, 1984-85 to 1998-99 (Index 1984-5 = 100)

Source: Johnston, A., Porter, D., Cobbold, T. and Dolamore, R. (2000), Productivity in Australia’sWholesale and Retail Trade, Productivity Commission.

5. The Structure of the Retail Industry

The retail industry covers the sale of a wide range of products, from flowers to boats

to fast food. The nature of businesses and of employment differs with the type of

product being sold. Butchers differ from department stores which in turn differ from

fast food outlets. In the analysis of changes in the structure of the retail industry, we

must rely on data from the Australian Bureau of Statistics. The ABS sub-divides the

retail industry into three main components. These components are Food, Personal

and household goods and Motor vehicle retailing and services. In what follows, Motor

vehicle retailing and services are excluded from the data, so that we refer only to Food

and Personal and household goods. Further subdivisions are made within each of

these components, but most data are published only at the more aggregated level.

5.1 A Detailed Snapshot of the Retail Industry

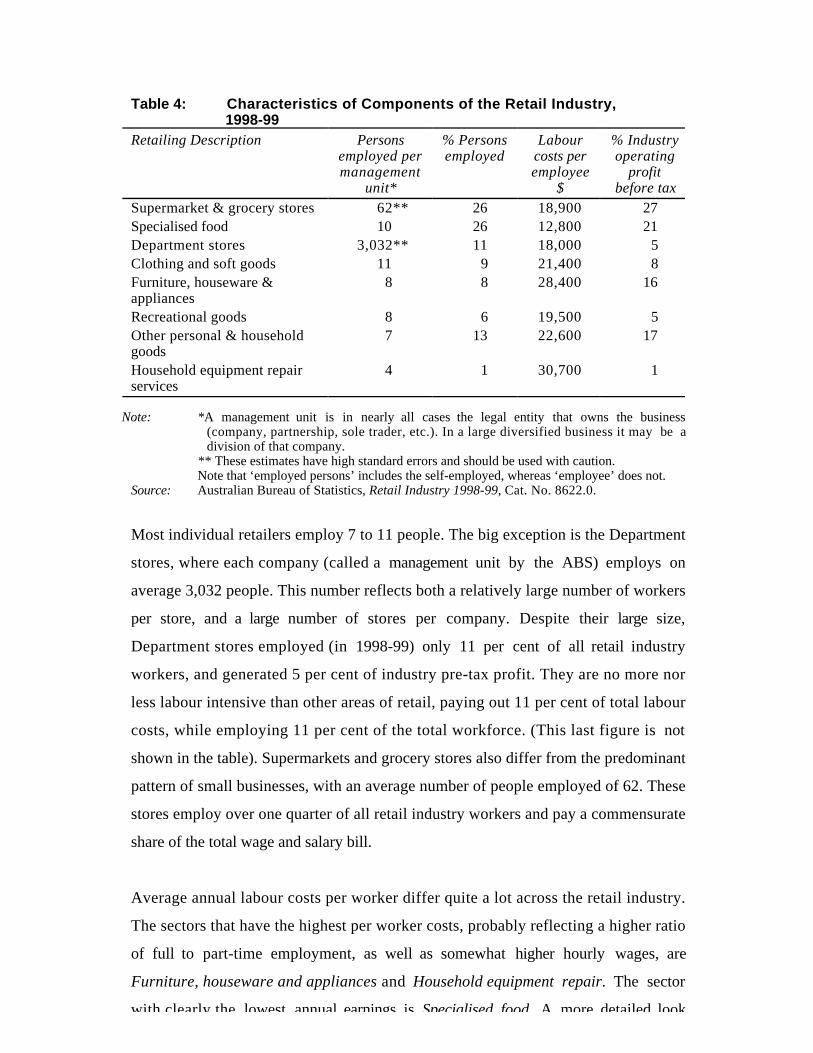

A census of the retail industry conducted by the ABS in 1998-9 (the last that has been

conducted) provides a snapshot look at the level of employment, number of

management units, wage bill and contribution to industry gross product by detailed

components of the retail industry. Table 4 below provides a summary of this

information.

The selling of food and groceries dominates the retail sector, accounting for 43 per cent

of the gross product of the industry. Supermarkets and grocery stores predominate in

terms of output, but small specialised food retailers provide almost as much

employment, though at a lower level of annual earnings. The level of annual earnings

reflects both hourly rates of pay and number of hours worked. These small food

stores are relatively labour intensive, contributing more to employment than their

share of industry gross product would suggest.

Table 4: Characteristics of Components of the Retail Industry,1998-99

Retailing Description Personsemployed permanagement

unit*

% Personsemployed

Labourcosts peremployee

$

% Industryoperating

profitbefore tax

Supermarket & grocery stores 62** 26 18,900 27Specialised food 10 26 12,800 21Department stores 3,032** 11 18,000 5Clothing and soft goods 11 9 21,400 8Furniture, houseware &appliances

8 8 28,400 16

Recreational goods 8 6 19,500 5Other personal & householdgoods

7 13 22,600 17

Household equipment repairservices

4 1 30,700 1

Note: *A management unit is in nearly all cases the legal entity that owns the business(company, partnership, sole trader, etc.). In a large diversified business it may be adivision of that company.

** These estimates have high standard errors and should be used with caution.Note that ‘employed persons’ includes the self-employed, whereas ‘employee’ does not.

Source: Australian Bureau of Statistics, Retail Industry 1998-99, Cat. No. 8622.0.

Most individual retailers employ 7 to 11 people. The big exception is the Department

stores, where each company (called a management unit by the ABS) employs on

average 3,032 people. This number reflects both a relatively large number of workers

per store, and a large number of stores per company. Despite their large size,

Department stores employed (in 1998-99) only 11 per cent of all retail industry

workers, and generated 5 per cent of industry pre-tax profit. They are no more nor

less labour intensive than other areas of retail, paying out 11 per cent of total labour

costs, while employing 11 per cent of the total workforce. (This last figure is not

shown in the table). Supermarkets and grocery stores also differ from the predominant

pattern of small businesses, with an average number of people employed of 62. These

stores employ over one quarter of all retail industry workers and pay a commensurate

share of the total wage and salary bill.

Average annual labour costs per worker differ quite a lot across the retail industry.

The sectors that have the highest per worker costs, probably reflecting a higher ratio

of full to part-time employment, as well as somewhat higher hourly wages, are

Furniture, houseware and appliances and Household equipment repair. The sector

with clearly the lowest annual earnings is Specialised food. A more detailed look

within Specialised food shows that the low labour costs per worker of this sector is

generated almost entirely in Takeaway food, which had an average per worker cost of

only $10,600. Low hourly wages, paid to youth, as well as a high level of part-time

employment undoubtedly both contribute to this outcome.

5.2 Changes over Time: Hours

In Figure 1 we showed how each of the sectors of the retail industry have evolved

between 1984-5 and 1998-9, in terms of output, hours worked and productivity. We

have already discussed the productivity aspects of these changes. Here we focus on

the changes in hours worked.

Substantial growth in hours worked is apparent for three sectors, namely Furniture,

houseware and appliances, Other personal and household goods and Specialised food.

The sector with the fastest growing employment was also the highest paying, namely

Furniture, houseware and appliances. It seems to have been largely unaffected by

technological change, as productivity per worker hour has fallen over the period. The

next fastest growing area of employment, Other personal and household goods, was

about average in terms of annual earnings. It experienced a rapid growth in output as

well as in employment, and modest labour productivity growth. The largest employer

of all, Supermarkets and grocery stores, saw a steady growth in output but fluctuating

changes in employment, with no growth until after the recession of the early 1990s.

After a few years of employment growth, employment has remained steady and the

growth in output has been accomplished by an increase output per hour worked

(labour productivity).

5.3 Changes over Time: Turnover

Developments in the retail industry can be viewed through a variety of lenses. These

include turnover, employment, value added, total wages and total profits. Here we

focus on turnover as a measure of size.

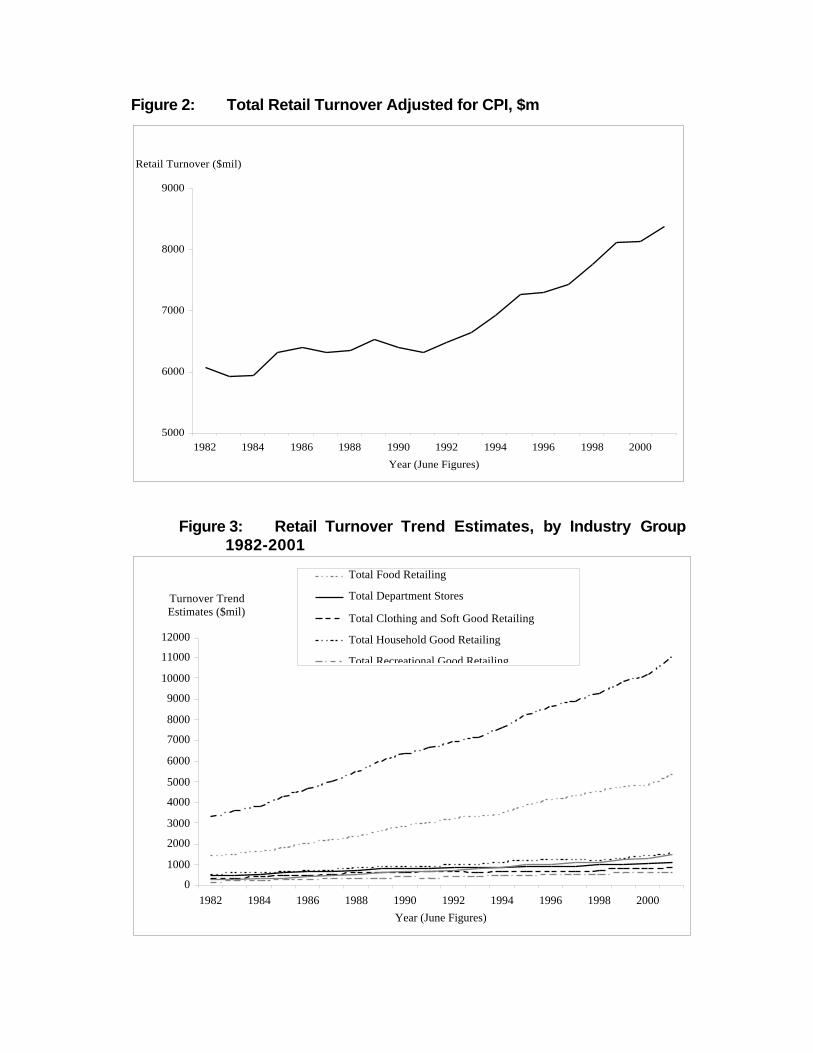

Figure 2 shows how the value of turnover in retail (excluding motor vehicles) has

grown over the period 1982-2001. The information is expressed in constant value

dollars: that is, the effects of inflation have been removed. It is clear that the real value

of retail spending is quite sensitive to the state of the business cycle. During the

downturns of the early 1980s and 1990s, real turnover fell. It rose in line with the

growth of the economy in the remaining years, accelerating in the later 1990s as rates

of economic growth increased.

In Figure 3 we show how different segments of retailing have grown since 1982. In this

figure, values are expressed as a proportion of the starting value, adjusted for inflation.

Thus the vertical axis measures the real growth from 1982. This figure shows, not

output, as presented in Figure 1, but turnover. Output measures value added, or the

difference between revenue and cost of goods. Turnover measures the value of sales.

Figure 3 also uses the current categories of the ABS, rather than those that prevailed in

1991. The data are presented in a way that makes it easy to compare the growth in the

different segments of retail. It can readily be seen that Food retailing, which by 2001

comprised almost half of all retailing, had the fastest growth, followed by ‘Other’.

Turnover in Department Stores, Clothing and soft goods, and Household goods grew

more slowly than average and thus these had a lower share at the end of the period

than at the beginning. Table 5 confirms these conclusions.

Figure 2: Total Retail Turnover Adjusted for CPI, $m

5000

6000

7000

8000

9000

1982 1984 1986 1988 1990 1992 1994 1996 1998 2000

Year (June Figures)

Retail Turnover ($mil)

Figure 3: Retail Turnover Trend Estimates, by Industry Group1982-2001

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

10000

11000

12000

1982 1984 1986 1988 1990 1992 1994 1996 1998 2000

Year (June Figures)

Turnover Trend Estimates ($mil)

Total Food Retailing

Total Department Stores

Total Clothing and Soft Good Retailing

Total Household Good Retailing

Total Recreational Good Retailing

Table 5: Retail Group Share in Total Retail Turnover, 1982 and 2003(per cent)

Components as % of total Jun-82 May-03Food Retailing 43 49Department Stores 15 10Clothing and Soft Good Retailing 11 8Household Good Retailing 17 16Recreational Good Retailing 6 5Other Retailing 9 12

Source: ABS 8501.0, online data

Food retailing, of course, is quite a diverse sector. On the one hand there are

supermarkets, which range from the dominant Woolworths and Coles to small

independents, and on the other hand there are owner-managed specialty shops such as

butchers and cake shops. Figure 4 shows how turnover has grown for the components

of the food sector—supermarkets and grocery stores, and other food retailing. Other

food retailing excludes takeaway food. Figure 4 strongly makes the point that the

relatively rapid growth in sales of food and groceries has been in the supermarkets,

rather than in the specialist food shops.

Figure 4: Food Retail Turnover 1982-2001 Adjusted for CPI

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

1982 1984 1986 1988 1990 1992 1994 1996 1998 2000

Year (June figures)

Turnover ($mil) Supermarkets and Grocery Stores

Other Food Retailing

Total food retailing (excluding Takeaway food)

5.4 Changes over Time: Size of Business

The size of a business can be measured in a variety of ways. Because the focus of this

report is on the labour market, we measure the size of business in terms of the number

of employees. It would be preferable to measure hours worked, since retail is an

industry in which many people work part-time, and part-time work is more prevalent

in some parts of the industry than in others. But suitable data that report hours

worked as a measure of firm size, and how this has changed over time, are not

available.

The retail industry has the characteristic that most firms are small yet most workers

work in large firms. In 2003, 97 per cent of firms were small (ie, employed no more

than 20 people) yet large employers accounted for slightly over half of total

employment.

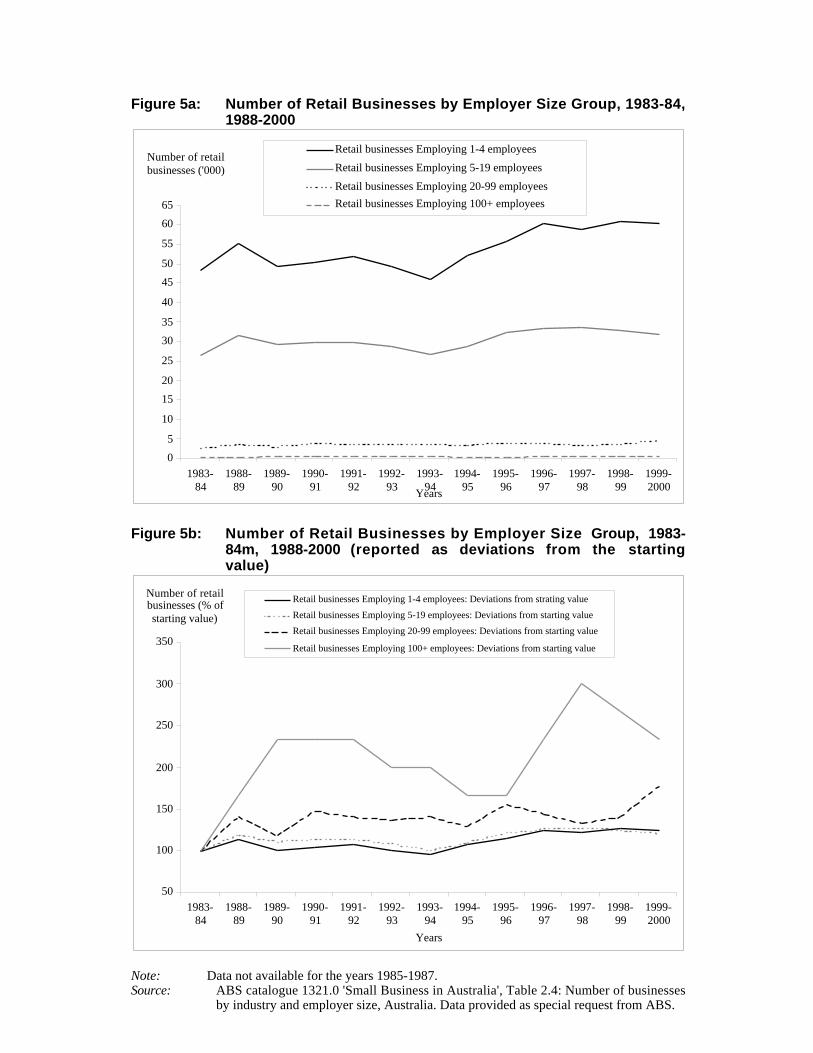

Figure 5 below shows the pattern of growth of firms of different size over the period

from 1983-4. Note that data are not available for the years 1985-87. The figure has

two panels. In the first, the absolute number of retail businesses of different size is

displayed. It is clear that there is a very small number of larger employers. In the

second, we show the percentage change in the number of businesses. This gives a

different view when the number of businesses in each category is very different.

Because there are only a small number of large firms, an increase of a few extra firms

appears in the second panel as a large percentage increase, but in the first panel is

hardly noticeable.

The very small number and proportion of businesses that employ over 100 people is

immediately apparent from the first panel. On the scale used in this figure, it is hard to

see whether there has been any change in the number of these businesses over the 16

years since 1983-4. Almost half of retail businesses employ fewer than 5 people and

most of the rest employ between 5 and 19 people. Most of the variation in business

numbers occurs among small businesses: indeed, the smaller the business, the larger the

numbers that come and go over the period. This is not surprising, Most new

businesses start out small, many small businesses do not survive for more than a few

years and the very successful ones often grow and move into a larger employment

category. Economic downturns have a disproportionate effect on the number of small

business failures and this can be seen in the decline in the numbers of small retail firms

during the recession and slow growth in the early part of the 1990s. Conversely, with

the increasing strength of the economy in the mid-1990s, there was a rebound in the

numbers of small retail firms. This rebound came to an end in 1996, and numbers have

been steady since then.

Panel b) of Figure 5 highlights the percentage change in the number of firms of given

size. On this perspective, the number of large firms looks to be more volatile than the

number of small firms. Note that the number of firms in a size category can change

because firms vary the size of their workforces, and in the process cross the arbitrary

boundary between the categories. Thus an increase in the number of large firms does

not necessarily mean that a new firm has arrived on the scene. Conversely, a fall in the

number of large firms does not necessarily mean that some firms have ceased operating

or been taken over: it may just mean that they have reduced the size of their workforce

below the threshold used for defining a firm as ‘large’.

A change in the proportion of small and large firms has implications for the workforce.

Working for a small employer is a different experience from working for a large

employer. There is also a concern that the expansion of large employers, such as

supermarkets, at the expense of small employers, such as greengrocers and corner

shops, will reduce the volume of employment generated by a given level of sales. We

examined this second issue in section 2 and concluded that there was no reason to

believe that such a shift would reduce overall employment.

In Figure 6, we show the ratio of employment in small retail firms to employment in

large retail firms. “Small” is defined as fewer than 20 employees. There has been a

clear downward trend in the proportion working in small retail businesses over the

past 16 years. At the beginning of the period, 58 per cent of workers were employed

in small businesses. By 2000, this had fallen almost ten percentage points to 49 per

cent.

Figure 5a: Number of Retail Businesses by Employer Size Group, 1983-84,1988-2000

0

5

10

15

20

25

30

35

40

45

50

55

60

65

1983-84

1988-89

1989-90

1990-91

1991-92

1992-93

1993-94

1994-95

1995-96

1996-97

1997-98

1998-99

1999-2000

Years

Number of retail businesses ('000)

Retail businesses Employing 1-4 employees

Retail businesses Employing 5-19 employees

Retail businesses Employing 20-99 employees

Retail businesses Employing 100+ employees

Figure 5b: Number of Retail Businesses by Employer Size Group, 1983-84m, 1988-2000 (reported as deviations from the startingvalue)

50

100

150

200

250

300

350

1983-84

1988-89

1989-90

1990-91

1991-92

1992-93

1993-94

1994-95

1995-96

1996-97

1997-98

1998-99

1999-2000

Years

Number of retail businesses (% of starting value)

Retail businesses Employing 1-4 employees: Deviations from strating value

Retail businesses Employing 5-19 employees: Deviations from starting value

Retail businesses Employing 20-99 employees: Deviations from starting value

Retail businesses Employing 100+ employees: Deviations from starting value

Note: Data not available for the years 1985-1987.Source: ABS catalogue 1321.0 'Small Business in Australia', Table 2.4: Number of businesses

by industry and employer size, Australia. Data provided as special request from ABS.

Figure 6: Employment in Small Retail Businesses as a Proportion of AllEmployment in Retail Trade, 1983-84, 1988-2000

0.46

0.48

0.5

0.52

0.54

0.56

0.58

1983-84

1988-89

1989-90

1990-91

1991-92

1992-93

1993-94

1994-95

1995-96

1996-97

1997-98

1998-99

1999-2000

Years

Proportion

Note: Data not available for the years 1985-1987.Source: ABS catalogue 1321.0 'Small Business in Australia', Table 2.3: Number of businesses

by industry and employer size, Australia. Data provided as special request from ABS.

Figure 7: Employment in Small Retail Businesses as a Proportion of AllEmployment in Retail Trade, 1983-84, 1988-2000

80

90

100

110

120

130

140

150

1983-84

1988-89

1989-90

1990-91

1991-92

1992-93

1993-94

1994-95

1995-96

1996-97

1997-98

1998-99

1999-2000

Years

Number of People Working in Retail (% of

starting value) Number of persons working in own retail business:Deviations from starting valueEmployment in all retail businesses: Deviations fromstarting value

Note: Data not available for the years 1985-1987.Source: ABS catalogue 1321.0 'Small Business in Australia', Table 2.3: Number of businesses

by industry and employer size, Australia. Data provided as special request from ABS.

At the same time that employment in small retail businesses has been falling, and total

employment in retail has been rising, the number of sole traders working in their own

retail business has fallen by about 10 per cent, to about 93,000. In round terms, own

account workers, who own their business and do not employ others, comprise about

10 per cent of all retail workers. A further 10 per cent consists of people who work in

their own their business and also employ others. Together, then, self-employed retail

workers comprise about one fifth of people working in a retail business. Figure 7

shows how the total number of people working in retail and the number working in

their own retail business have changed between 1983-4 and 1999-2000. The figures are

expressed as deviations from the value that each series had at the beginning of the

period, and hence can be read as percentage changes. Figure 7 shows that movements

in self-employment broadly followed those in total employment until 1994-5. In that

year, total employment began to accelerate and self-employment began to fall, until by

2000 self-employment was 15 per cent below it peak. The decline in self-employment

came later than the decline in overall employment in small retail businesses as shown

in Figure 6. As a result of these changes, self-employment in retail has fallen from 22

per cent to 14 per cent of all retail employment over the period. (ABS, catalogue no.

1321.0, unpublished data).

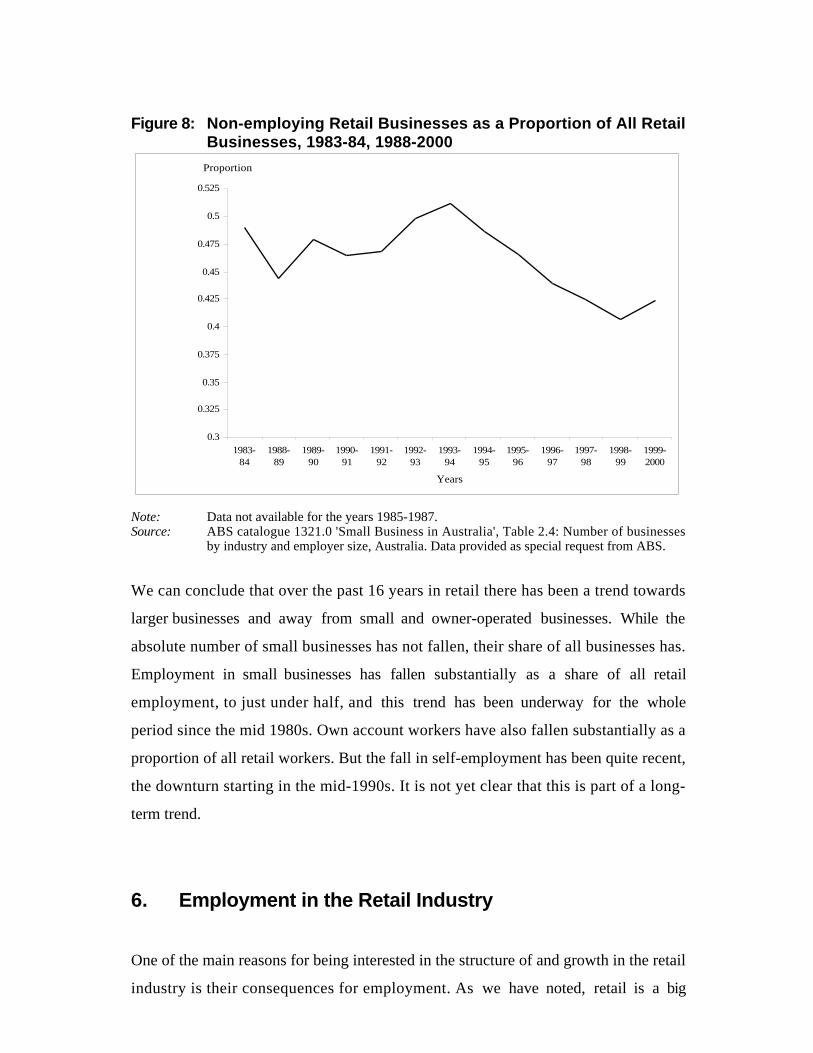

The pattern of change in the proportion of retail workers who are self-employed has

been largely matched by the changes in the proportion of all retail businesses that are

operated just by their owners (and perhaps family helpers). Figure 8 shows these non-

employing retail businesses as a proportion of all retail businesses. Their proportion

reached a peak, of a little over half, in 1993-4, but by 2000 had fallen to 43 per cent of

all retail businesses. Unlike the employment share, however, the most recent data

show a small upturn in their share.

Figure 8: Non-employing Retail Businesses as a Proportion of All RetailBusinesses, 1983-84, 1988-2000

0.3

0.325

0.35

0.375

0.4

0.425

0.45

0.475

0.5

0.525

1983-84

1988-89

1989-90

1990-91

1991-92

1992-93

1993-94

1994-95

1995-96

1996-97

1997-98

1998-99

1999-2000

Years

Proportion

Note: Data not available for the years 1985-1987.Source: ABS catalogue 1321.0 'Small Business in Australia', Table 2.4: Number of businesses

by industry and employer size, Australia. Data provided as special request from ABS.

We can conclude that over the past 16 years in retail there has been a trend towards

larger businesses and away from small and owner-operated businesses. While the

absolute number of small businesses has not fallen, their share of all businesses has.

Employment in small businesses has fallen substantially as a share of all retail

employment, to just under half, and this trend has been underway for the whole

period since the mid 1980s. Own account workers have also fallen substantially as a

proportion of all retail workers. But the fall in self-employment has been quite recent,

the downturn starting in the mid-1990s. It is not yet clear that this is part of a long-

term trend.

6. Employment in the Retail Industry

One of the main reasons for being interested in the structure of and growth in the retail

industry is their consequences for employment. As we have noted, retail is a big

employer. It also provides unusually high levels of opportunity for new entrants to

the labour force (young people and mothers returning to employment, though not

migrants) and for self-employment. So it is not just the total level of employment that

is interesting, but also the composition of that employment. We present below a

summary of developments in the main indicators of employment in the retail industry.

6.1 Total Employment

In Table 1 we saw that retail employment comprised 1,468,200 people in February

2003, or 15 per cent of total employment. This figure applies to a broad definition of

retail, and we will see later how this employment is divided among sub-sets of the

retail sector.

In this section, we examine how retail employment has changed over time, in total and

as a share of all employment.

Figure 9 shows how employment in retail businesses and in all businesses has changed

since the mid-1980s. Employment levels in 1983-4 are set as the starting value, and

employment in later years is expressed as a percentage of the starting value. From the

figure we can see that:

v Employment in all businesses grew by over 50 per cent by 1999-2000.

v Employment in total retail (including motor vehicles sales and service) grew more

slowly, at around 40 per cent, over the same period.

v Retail employment broadly tracked total business employment, but grew at a more

subdued rate.

v Where total business employment was unchanged over the five years from 1989-

90, in retail it fell over this period.

v Total business and retail employment each grew by around 15 per cent in the 6

years since the downturn of 1993-4.

Figure 9: Number of People Employed in Australian Businesses, 1983-84m, 1988-2000 (reported as deviations from the startingvalue)

80

90

100

110

120

130

140

150

160

170

1983-84

1988-89

1989-90

1990-91

1991-92

1992-93

1993-94

1994-95

1995-96

1996-97

1997-98

1998-99

1999-2000

Years

Number of people employed (% of starting value) Total employment in all retail businesses: Deviations

from starting value

Total employment in all businesses: Deviations fromstarting value

Note: Data not available for the years 1985-1987.Source: ABS catalogue 1321.0 'Small Business in Australia', Table 2.3: Number of businesses

by industry and employer size, Australia. Data provided as special request from ABS.

As a result of the flatter growth of retail employment, employment in retail businesses

as a share of employment in all businesses fell from 20 per cent at the beginning of the

period to 18 per cent at the end. All retail employment is in the private sector. If we

express private sector retail employment as a proportion of all private sector

employment, we find that the retail share has fluctuated around a central value of 18

per cent over the period since 1983-4. (ABS 1321.0, unpublished data).

6.2 Sectors within Retail Employment

Coles Myer Ltd is interested to know the changes in that part of the retail labour

market that are of most relevance to its own operations. The ABS publishes data at

different levels of detail, depending on the series and the topic of the data release. For

much of its labour force data, the industry breakdown is at a high level of aggregation,

and the retail sector is treated as a whole. For some series, the next level of

disaggregation is available, that divides the retail sector into food, personal and

household goods, and motor vehicle sales and service. In this section, we present

information on changes in retail employment that draws on this more disaggregated

data. We are thus able to exclude motor vehicle sales and service from the picture.

We start by giving an overview of the major changes in retail employment over the

past 15 years. Motor vehicle sales and service is included in the table in order to

enable its impact on the aggregate retail data to be seen.

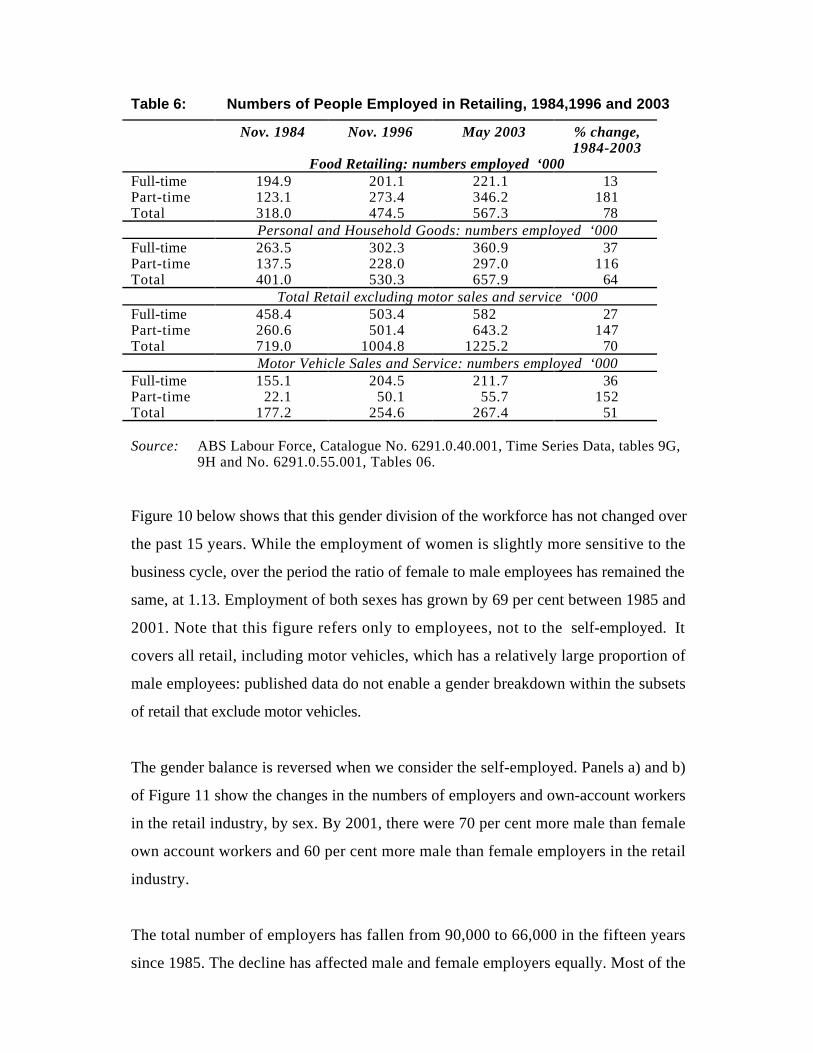

Table 6 tells us a great deal about recent developments in employment in the retail

sector. The key points are summarized below:

v Excluding motor vehicles, total employment in retail has grown by 70 per centover the past 18 years (which is faster than for the economy as a whole).

v Employment in Food Retailing grew faster (at 78%) than employment in Personaland Household Goods (at 64%).

v Part-time employment grew much faster than full-time employment (147%compared with 27%).

v The growth in part-time employment was especially strong (181%), and in full-time employment especially weak (13%), in Food Retailing. (Note that FoodRetailing does not include cafes and restaurants).

v By 2003, there were almost as many people employed in Food Retailing as inPersonal and Household Goods.

v Food Retailing has a high and rising ratio of part-time to full-time staff (1.6compared with 0.8 for Personal and Household Goods in 2003).

v Employment in Motor Vehicles Sales and Service rose more slowly than in theother two sectors of the retail industry, so that by 2003 it represented 18 per centof total retail employment.

6.3 Female and Male Employment

We saw in Table 1 that the retail industry employs a relatively large number of

women, especially if the sales and servicing of cars is excluded from the measure of

retail employment.

Table 6: Numbers of People Employed in Retailing, 1984,1996 and 2003

Nov. 1984 Nov. 1996 May 2003 % change,1984-2003

Food Retailing: numbers employed ‘000Full-time 194.9 201.1 221.1 13Part-time 123.1 273.4 346.2 181Total 318.0 474.5 567.3 78

Personal and Household Goods: numbers employed ‘000Full-time 263.5 302.3 360.9 37Part-time 137.5 228.0 297.0 116Total 401.0 530.3 657.9 64

Total Retail excluding motor sales and service ‘000Full-time 458.4 503.4 582 27Part-time 260.6 501.4 643.2 147Total 719.0 1004.8 1225.2 70

Motor Vehicle Sales and Service: numbers employed ‘000Full-time 155.1 204.5 211.7 36Part-time 22.1 50.1 55.7 152Total 177.2 254.6 267.4 51

Source: ABS Labour Force, Catalogue No. 6291.0.40.001, Time Series Data, tables 9G,9H and No. 6291.0.55.001, Tables 06.

Figure 10 below shows that this gender division of the workforce has not changed over

the past 15 years. While the employment of women is slightly more sensitive to the

business cycle, over the period the ratio of female to male employees has remained the

same, at 1.13. Employment of both sexes has grown by 69 per cent between 1985 and

2001. Note that this figure refers only to employees, not to the self-employed. It

covers all retail, including motor vehicles, which has a relatively large proportion of

male employees: published data do not enable a gender breakdown within the subsets

of retail that exclude motor vehicles.

The gender balance is reversed when we consider the self-employed. Panels a) and b)

of Figure 11 show the changes in the numbers of employers and own-account workers

in the retail industry, by sex. By 2001, there were 70 per cent more male than female

own account workers and 60 per cent more male than female employers in the retail

industry.

The total number of employers has fallen from 90,000 to 66,000 in the fifteen years

since 1985. The decline has affected male and female employers equally. Most of the

Figure 10: Number of Male and Female Employees in the Retail Industry1985-2001

300

350

400

450

500

550

600

650

1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

Year (May Figures)

Number of Employees ('000)

Number of Male employees in retail

Number of Female employees in Retail

Note: Data from 2000 onwards is not strictly comparable with earlier data, due to definitionalchanges in the labour force survey.

Source: ABS catalogue 6203.0, 'Labour Force, Australia', Time Series Data Tables 9a, 9b, and 9c ‘Labour Force – employees by industry.

decline has occurred since the mid-1990s, after an upturn following the recession of

1990-91.

Over the business cycle, changes to employment tend to lag changes to output. While