the retail bank’s one-stop guide to journey mapping · the retail bank’s one-stop guide to...

TRANSCRIPT

CATALYST WHITEPAPER

The Retail Bank’s One-Stop Guide to Journey Mapping

How to Select, Create and Measure Customer Journeys

TARA LITCHFIELD | DIRECTOR OF EXPERIENCE DESIGN

The Retail Bank’s One-Stop Guide to Journey Mapping Page 2

TABLE OF CONTENTSExecutive Summary .................................................................................................................................3

Why Does Customer Experience Matter for Retail Banks? .........................................................................3

Why Invest in Customer Journey Maps? ...................................................................................................4

What Is a Customer Journey Map? .........................................................................................................5

Who Uses Customer Journey Maps? ......................................................................................................5

Can Your Bank Benefit Financially from a Journey Map? .........................................................................6

How to Create a Journey Map That Drives Measurable Results .................................................................9

How Can I Get Started? ..........................................................................................................................14

About the Author ...................................................................................................................................15

About Catalyst .......................................................................................................................................15

The Retail Bank’s One-Stop Guide to Journey Mapping Page 3

EXECUTIVE SUMMARY

Although retail banks have long been at the forefront of customer experience improvement, customers’ banking needs are changing at lightning speed – almost as fast as the role of fintech. Customers have high expectations for their bank, partly because so many leading traditional and virtual banks have made significant investments in these areas.

To embrace innovative digital changes and bring them into the retail bank’s customer experience, banks must first learn how different customer segments want to engage with them across different channels of the customer’s life cycle. The best way to study and document customer experience opportunities across channels and life cycle is through qualitative research and customer journey maps.

WHY DOES CUSTOMER EXPERIENCE MATTER FOR RETAIL BANKS?

To retain customers and cross-sell other bank products, banks must offer a great customer experience worthy of a high Net Promoter Score. EY has asserted, based on their research, that trust is strongly associated with higher Net Promoter Scores for banks, and trust is often based on how banks treat and communicate with their customers. Younger, digitally savvy customers are more willing to switch banks than ever, and overall, customers are buying fewer products from their primary bank.

Source: Winning through customer experience, EY Global Consumer Banking Survey 2014, http://www.ey.com/Publication/vwLUAssets/EY_-_Global_Consumer_Banking_Survey_2014/$FILE/EY-Global-Consumer-Banking-Survey-2014.pdf

Relationship between trust and advocacy in primary provider

Very likely to recommend

Neutral or unlikely to recommend

Likely to recommend

68%20%

3%

50%

13%

30%

84%27%5%

Moderate trust Minimal trust or no trust

Complete trust

The Retail Bank’s One-Stop Guide to Journey Mapping Page 4

WHY INVEST IN CUSTOMER JOURNEY MAPS?

Companies in all industries are investing in customer journey maps, using them as tools to increase customer satisfaction and improve their customer experience. According to The Gartner Group, 89% of marketers expect customer experience to be their primary differentiator in 2017.

An example of a company using customer journey maps successfully is Citi’s Credit Card Business. Citi redirected resources toward delivering superior customer experiences. After using customer journey maps for 18 months, Citi has increased Net Promoter Score 1800 basis points overall and improved payments experience by 31%. Citi Card’s Chief Customer & Digital Experience Officer explains in a two-part article what a dramatic effect customer journey mapping has had on the company’s customer experience.

Clarbridge – compiled research on customer experience that provides clear evidence linking customer experience improvements to increased revenue and customer loyalty.

And McKinsey & Company has found that end-to-end customer journey satisfaction is a better indicator of customer experience than the performance of individual touch points.

With the competitive landscape tightening and changing so rapidly for retail banks, there is mounting pressure to optimize the customer experience now … or risk becoming obsolete.

Reasons for having complete trustFinancial stability

Ability to withdraw money

Their security procedures

The size of the company

The way I am treated

How they communicate with me

Quality of advice provided

My relationship with certain employees

The fees I pay

Interest rates I earn on my accounts

Interest rates I pay on my loans

Stories from friends or relatives

Their decision to open or close branches

Recent articles or news stories

Institutional stability

Customer experience

Fees and rates

Other

60%54%

51%42%

56%44%

41%38%

19%26%

24%20%

14%9%

8%

Source: Winning through customer experience, EY Global Consumer Banking Survey 2014, http://www.ey.com/Publication/vwLUAssets/EY_-_Global_Consumer_Banking_Survey_2014/$FILE/EY-Global-Consumer-Banking-Survey-2014.pdf

The Retail Bank’s One-Stop Guide to Journey Mapping Page 5

WHAT IS A CUSTOMER JOURNEY MAP?

A customer journey map is a visualization tool that shows the process a customer experiences when accomplishing a goal. The customer journey is shown over time and across multiple touch points. It is a form of storytelling that uses qualitative customer research to help businesses understand what their customers are thinking, feeling and doing during the process. Most journey maps visually show customer emotion and/or pain points associated with different needs during the process. Opportunities to meet customers’ needs are documented as part of the process.

The goal of a customer journey map is to teach a company about its customers, inventory high and low points in the customer experience and identify opportunities for business improvement.

WHO USES CUSTOMER JOURNEY MAPS?

Almost everyone in a company can use customer journey maps to guide day-to-day decisions to improve customer experience. But different maps may serve different audiences better.

A single customer journey map can be used for multiple audiences, but retail banks need to consider how the maps will be delivered and the density of the information included in the map. Maps with too much information that don’t visually tell a story will be harder for different audiences to digest and remember.

So, keep it as simple and visual as possible.

Maximizing satisfaction with customer journeys,

AND

increase customer satisfaction by

can lift revenue by up to

and lower the cost of serving customers by as much as

86%of buyers will pay more for a better customer experience

1%of customers feel that vendors consistently meet their expectations

BUT ONLY

89%Of consumers have stopped doing business with a company after experiencing poor customer service

vs

A customer is 4 times more likely to buy from a competitor if the problem is service related vs. price or product related

Source: The Top 14 Customer Experience (CX) Stats of 2016, http://www.clarabridge.com/blog/the-top-14-customer-experience-cx-stats-of-2016/

The Retail Bank’s One-Stop Guide to Journey Mapping Page 6

CAN YOUR BANK BENEFIT FINANCIALLY FROM A JOURNEY MAP?

Several things need to be in place in order for a journey map to drive business results:

Journey Maps Require Qualitative Research

Customer journey maps are not helpful for all companies all the time. A bank that does not want to invest in qualitative research should not attempt to create journey maps, because journey maps are based on what actual customers report that they are thinking, feeling and doing. Quantitative customer data tells us what customers are doing but not why they are doing it. Understanding the “why” is key when improving customer experiences.

WHO WHAT MAP GOALS

Project Managers and Marketers

• Evaluate touch points

• Define KPIs

• Identify low-performing CX areas

• Associate quantitative data with qualitative data

• Provide clear, actionable opportunities

Product Managers• Make important investment decisions

• Identify new features to build

• Prioritize new features based on research

• Plan design and development based on opportunities

Executives• Set a yearly roadmap

• Secure appropriate funding

• Build a business case with customer data

• Plan design and development based on opportunities

Sales AssociatesDesignersDevelopersWritersCustomer Service Representatives

• Better understand customers

• Help decision-making

• Improve daily work outputs

• Deliver customer-friendly communications

• Create customer-centered workflows and UI designs

The Retail Bank’s One-Stop Guide to Journey Mapping Page 7

Journey Maps Require Segmentation Data and Personas

A retail bank that doesn’t understand its customer segmentation should start there and develop customer personas before it develops journey maps. Not every customer’s journey will be the same across all touch points. Within segments and personas there will be fluctuations, but there should be common goals, needs and patterns of behavior for groups of customers.

It is important to understand this when mapping customer journeys. Journey maps work best when they are paired with customer personas, so the retail bank can understand the journey relative to the needs and goals of a specific group of customers. Before creating customer journey maps, researchers will need to review customer segmentation data, personas and other customer experience baseline metrics, like customer satisfaction scores and Net Promoter Scores.

Carli’s Story

Carli is a full-time mom who enjoys being out and about often during the day with her two young children. Her husband owns a landscaping company, so sometimes she runs errands for him. Since she is very busy, she doesn’t spend much time in front of a computer screen at home. She is a former corporate accountant, so she likes to take an active role in the family’s finances. She loves her new Bank of America mobile app and prefers to use it for most of her banking needs. If she does have a question or a problem on her account, she will call customer service or stop by her local branch to get assistance.

Banking Preference

Payment Preference

NUMBER OF FINANCIAL PRODUCTS

Context of Use

LOW HIGH

ATM USE

LOW HIGH

CASH USE

LOW HIGH

TECHNICAL SKILL

LOW HIGH

CarliMobile Free Spirit

AGE

OCCUPATION

MARITAL STATUS

LOCATION

30

STAY-AT-HOME MOM

MARRIED

RICHMOND, CA

NEW BANK

OTHER BANKS

BANK OF AMERICA

WELLS FARGO, FIDELITY

“I opened a new bank account because I was tired of the lack of locations by my current bank, so I wanted to have more convenience when it came to banking and a better user experience with the mobile app.”

Yoga, Exercising, Gardening, Swimming, Travel, Blogging

Interests

Friendly Active Easygoing

Customer Service Channel Preference

LIVE CHAT ON MY MOBILE APP

CALLING BY PHONE

TEXT OR EMAIL REPLY

ONLINE PLATFORM & VIDEO CONFERENCE

IN PERSON IN THE BRANCH

Mobile Banking

Digital Wallet orCredit Card

Biggest Opportunity

Mobile Live Chat

CONVENIENCEConvenient banking when and how I need it, including mobile, ATM, and branch banking

SELF-SERVICEEasy-to-use mobile app for basic tasks like viewing balances, depositing checks, paying bills, and transferring money

TRANSPARENCY OF COSTClear communications on fees, rates, discounts, and bank product options

Banking Goals

The Retail Bank’s One-Stop Guide to Journey Mapping Page 8

The Company Must Be Committed to Solving Experience Problems

If a company doesn’t have well-defined customer experience goals that its executives are committed to solving, customer journey maps are a wasted effort. Customer experience changes are often long-term commitments that span multiple departments. Customer experience opportunities discovered during journey mapping may require the breakdown of organizational silos and the transformation of internal processes.

Retail banks need to assign ownership of performance improvements to individuals or a department based on journey map findings. Time and money need to be set aside to pilot improvement projects with the assigned departments. If the current research and development departments do not have the capabilities or the bandwidth to address the recommended customer experience changes, the retail bank must create an investment plan to address them or postpone journey mapping until resources are secured.

Eric’s Story

Eric is a lawyer who specializes in corporate law. He represents many large companies and must travel often on assignment. He has been at his firm for a few years and has almost paid off his student loans. His daughter Jayla was born this past year, and he made it a priority to start saving for her future. He did a lot of online research before he found his new high-interest savings account. He is confident that he made the right decision now but will reevaluate his decision over time. He owns his own home and is paying a mortgage but likes to keep that and his student loans separate from his savings and checking accounts. He trusts the bank with his money and information, but he likes to make his own decisions when it comes to investing his money and opening accounts.

Banking Preference

Payment Preference

SELF-SERVICEEasy-to-use online platform that allows me to take care of all my banking online without going to a branch

EASY PRODUCT & RATE COMPARISONFinding the best financial products and rates for my needs

QUICK CUSTOMER SERVICEQuick and convenient remote customer service options

Banking Goals

NUMBER OF FINANCIAL PRODUCTS

Context of Use

LOW HIGH

ATM USE

LOW HIGH

CASH USE

LOW HIGH

TECHNICAL SKILL

LOW HIGH

EricTech-Savvy Researcher

AGE

OCCUPATION

MARITAL STATUS

LOCATION

37

LAWYER

MARRIED

CINCINNATI, OH

NEW BANK

OTHER BANKS

CAPITAL ONE 360

NRL MORTGAGE, CHASE

“I determined I needed an interest-bearing account for all the savings I was accumulating and my new account gives me a high 1.1% interest rate.”

Classic Cars, Working Out, Politics, and Current Affairs

Interests

Highly Educated Analytical Proactive

Customer Service Channel Preference

LIVE CHAT

CALLING BY PHONE

EMAIL REPLY

ONLINE PLATFORM & VIDEO CONFERENCE

IN PERSON IN THE BRANCH

Online Banking

Credit Card to maximize points

Biggest Opportunity

Interactive Online Self-Service Tools

The Retail Bank’s One-Stop Guide to Journey Mapping Page 9

Don’t Map What You Can’t Measure

A company needs to have a customer experience measurement program in place or a plan to execute one after a customer journey map is complete. Baseline analytics, customer satisfaction scores, Net Promoter Scores, and call center data should be in place for all the journey’s pain points and/or opportunities in order to select pilot programs and measure their effectiveness. Journey maps can help point retail banks in the right direction for improvement, but only through iterative change and measurement will a company be able to confirm customer experience improvement and the associated results.

Most important elements needed prior to creation of a customer journey map:

• Defined business goal or goals related to the journey

• Defined target customer group for the journey (marketing segment or customer persona)

• Assumed customer goal or goals for the journey

• Documented journey stages

• Inventoried journey touch points

• Assumed customer pain point areas related to low performance in quantitative data

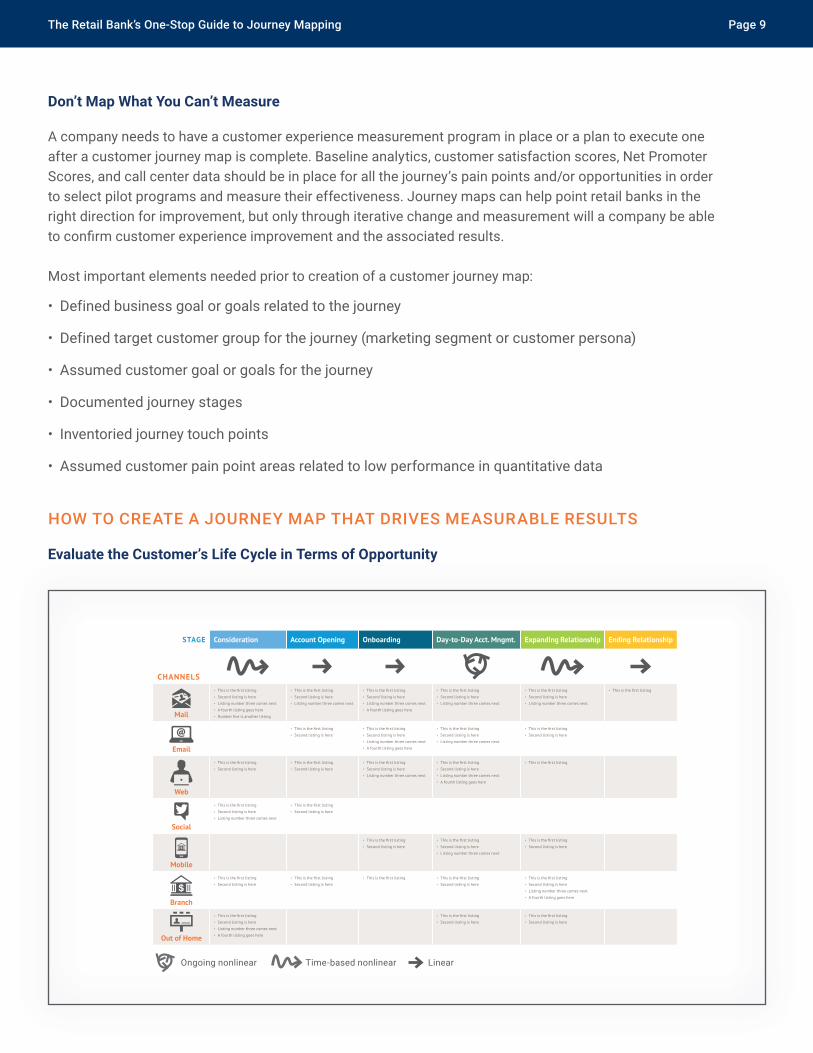

HOW TO CREATE A JOURNEY MAP THAT DRIVES MEASURABLE RESULTS

Evaluate the Customer’s Life Cycle in Terms of Opportunity

STAGE Consideration Account Opening Onboarding Day-to-Day Acct. Mngmt. Expanding Relationship Ending Relationship

CHANNELS

•

• Second listing is here

• Listing number three comes next

• A fourth listing goes here

•

•

• Second listing is here

• Listing number three comes next

•

• Second listing is here

• Listing number three comes next

• A fourth listing goes here

•

• Second listing is here

• Listing number three comes next

•

• Second listing is here

• Listing number three comes next

•

•

• Second listing is here

•

• Second listing is here

• Listing number three comes next

• A fourth listing goes here

•

• Second listing is here

• Listing number three comes next

•

• Second listing is here

Web

•

• Second listing is here

•

• Second listing is here

•

• Second listing is here

• Listing number three comes next

•

• Second listing is here

• Listing number three comes next

• A fourth listing goes here

•

Social

•

• Second listing is here

• Listing number three comes next

•

• Second listing is here

Mobile

•

• Second listing is here

•

• Second listing is here

• Listing number three comes next

•

• Second listing is here

Branch

•

• Second listing is here

•

• Second listing is here

• •

• Second listing is here

•

• Second listing is here

• Listing number three comes next

• A fourth listing goes here

Out of Home

•

• Second listing is here

• Listing number three comes next

• A fourth listing goes here

•

• Second listing is here

•

• Second listing is here

Ongoing nonlinear Time-based nonlinear Linear

The Retail Bank’s One-Stop Guide to Journey Mapping Page 10

Start the journey mapping process by reviewing your service blueprint or by conducting a touch point inventory for the target customer segment and selected journey. If you don’t have much process documentation, the researcher will need to conduct business stakeholder interviews. Stakeholder interviews extract process information about the journey’s triggers, touch points and channels. The researcher will also review the quantitative data for the different customer segments, touch points and channels, and look for opportunities across the customer’s life cycle. This evaluation will help focus the retail bank’s journey map process by providing a customer experience inventory.

Choose the Customer Journeys to Research

To determine which customer journeys to explore, retail banks should look at areas that have the largest pain points and lowest performance from a revenue and cost perspective, particularly for their highest-value customers. After reviewing analytics, usability data, call center data, customer satisfaction surveys, and Net Promoter Scores, it should be clear where the most promising areas of opportunity are.

ASK YOUR TEAM THESE FOUR QUESTIONS:

• What do we intend to solve by creating a journey map?

• Why do we need to solve those problems?

• What are we hoping to achieve?

• Who will use the journey map and how will they use it?

Some retail banks evaluate direct competitors during the journey map selection process to help decision-making. Take the results of this analysis and select a couple of customer journeys to focus on that align well with their immediate roadmap goals. The selection process usually happens in a workshop that includes the team of internal stakeholders and any outside researchers. Typically, customer journey maps are more successful in driving immediate results when they focus on micro journeys and not on macro journeys that span more than a couple life cycle stages.

Recruit Participants and Conduct Research

Choose research methods that will get you qualitative information in the most efficient way. If you want to study offline processes, ethnographic studies may be warranted; however, processes that are mostly digital can be conducted through remote interviews. Recruit customers that fit your target audiences and screen them with the touch points and channels that you want to study. Create a discussion guide for the research; include a combination of open and closed questions for each of the journey’s stages. Schedule the participants and conduct the research. Stakeholders should try to attend some research sessions to get a feel for the customer’s point of view firsthand.

The Retail Bank’s One-Stop Guide to Journey Mapping Page 11

Analyze and Document the Customer Journey

Analysis of the research typically takes longer than conducting the research. The researcher will compare findings across segments and look at the frequency of customer pain points to determine the size of the opportunities. The researcher will document the findings in terms of what customers were thinking, feeling and doing for each of the life cycle stages and the opportunities associated with them. Document the customer persona goals and/or guiding principles related to the customer’s journey. Pull sample customer quotes or audio/video files to exemplify pain points or opportunities. Associate pain points and unmet needs with related qualitative data to establish key performance indicators that can be measured over time.

Collaborate in a Workshop

After the researcher has finished documenting the customer’s journey, a collaboration workshop should be scheduled. During a full-day workshop, the researcher will share the study’s findings and walk the team through the customer’s journey and the associated opportunities. Business stakeholders and designers can brainstorm and sketch potential solutions to address opportunities.

During the workshop, business stakeholders, technology officers and data analysts will need to determine the data sources for measurement and evaluate the benefits and costs associated with different opportunities. Opportunity prioritization should be based on those parts of the journey that can be measured effectively to assess future improvements. The culled opportunities and their associated KPIs should be included in a customer experience roadmap that is owned by an assigned program manager or department.

Account Opening Follow-Up Self-Service Long-Term Advice

Tech-Savvy Researchers

MobileFree Spirits

Trusted CommunityMembers

+feeling

_feeling

The Retail Bank’s One-Stop Guide to Journey Mapping Page 12

Create a Visual Map and Connect It to KPIs

Create a visual user interface of the map from the skeleton of the customer journey that has been documented. The map should tell a story immediately, without requiring the user to read lots of detail. The map can be an interactive tool and include live quantitative data, or it can be static and paired with customer journey dashboards. Static maps can be updated every few years or after the customer journey significantly changes.

Carli’s Bank Onboarding Journey

ACCOUNT OPENING

FEEL

ING

OP

PO

RTU

NIT

IES

–

DO

ING

+TH

INKI

NG

Quick & Convenient Account Opening

MOBILE FREE SPIRIT – WANTS CONVENIENCE

Easy Access to InformationUsing My Phone

Easy-to-Use Mobile App &Quick 24/7 Customer Service

Mobile App AdviceI Can Follow Up On When Ready

FOLLOW-UP SELF-SERVICE & PROBLEM RESOLUTION LONG-TERM ADVICE

STARTDAY 1

DAY 90

DAY 7

DAY 14 DAY 30

Took longer than expected to open account at the branch

Logs in to mobile app Throws out welcome kit–

prefers digital documents

Bank sales associate calls and leaves product offer message on voicemail

Deposits checks and transfers money using the mobile app

“Online account sign-up just makes everything a lot quicker and more efficient. I don’t have to hear a sales pitch, I don’t have to spell anything out.”

“Sharing personal information - it's part of the process when signing up. I have no problem sharing any of this information. I guess I would rather share it in the beginning.”

“Actually, the kit was unhelpful I tossed it in the garbage. With the whole world online, I felt it was unnecessary.”

“If I need a service I don't need the bank to send me info. I would research it on my own then if I want the service I would call the bank.”

“I believe the bank's platform should have video demos.”

“I like chat and instant messaging to get answers to any questions.”

“I am generally looking for deals or cashback promotions that I can go ahead and add it to my account online as well as detailed graphs on my spending and a quick screenshot of all my account information.”

“I like to do both an in person and online process. In person I can ask questions, I can go over things. It's more personable. Online I can do my own search and explore every bit of a service.”

“I would prefer to do a credit card online. It’s hassle free and I feel confident in the bank's security.”

Uses live chat on the mobile app to understand a charge

Long wait time on customer service line to stop a check

Receives mobile app alert to transfer funds to avoid an overdraft

Receives email promotion about cash back credit card

Responds to email to ask about the credit card offer

Frustrated - online account openingwould be more convenient

Annoyed - communications shouldbe digital

Satisfied - I can use the mobile appfor most of my banking needs

Hopeful - looks like my bank has other great products and offers

• Account opening by phone or online

• Ask for information that can help personalize financial advice during the account opening process

• Account managers shouldn’t press new customers to add products, just offer options and explain the benefits

• Digital welcome kit

• An assigned account manager with direct contact details

• Follow-up communications by email, text, or mobile app

• Video demos of product features

• Mobile app that allows you to make wire transfers to different banks

• 24/7 live chat accessible via mobile app

• Mobile alerts that help you avoid unnecessary charges

• ATM locator on mobile app

• Ability to schedule appointments with bank associates

• Money management tools built into the mobile app

• Product recommendations and advice built into the mobile app experience

• Online product sign-up

Bank associate tries to push other product sign-up

No ATM locator on mobile app

GO

ALS

The Retail Bank’s One-Stop Guide to Journey Mapping Page 13

Deploy the Customer Journey Maps

A large journey map should be printed and mounted at a size that is large enough to be read easily. In addition, several copies of the final map should be digitally distributed to each stakeholder for reference. The journey maps should be presented to stakeholders in a workshop setting, where they can ask questions and discuss the findings.

Across the organization, journey maps should be digitally distributed and discussed. Employees should be able to ask questions and provide feedback. Some of their feedback may be integrated into the roadmap documentation. Executives may determine that there is organizational change needed to address journey map opportunities. Managers can offer suggestions and gather feedback on how to systematically use the journey maps to produce departmental change that will benefit the customer’s experience. Designers, developers, marketers, and product managers should have journey maps handy so they can regularly refer to them when making decisions.

After the maps have been in use for a while, ask employees to rate their usefulness, share examples of how they have used them and talk about how they can be improved.

Banking Customer Experience Map

PURCHASE ADVOCATE

CUST

OM

ER J

OUR

NEY

Step

s

• Identify the need for a new financial account• Assess financial institutions and account types available

• Choose a financial institution and account type(s)• Open account(s)• Receive confirmation and account numbers

• Set up online or mobile banking services• Set up direct deposit• Order checks• Receive ATM/debit/credit card

• Deposit money• Withdraw money• Check balances• Pay bills

• Monitor financial health• Identify the need for new financial services• Learn about products or services available• Add or change account products/services

• Identify the steps necessary to move financial assets• Close account with financial institution

Doin

g View mail promotion

View advertisements Call a representative

Call representative

Visit branch

Visit branch Receive materials in the mail

Send direct deposit info

Sign up for online banking

Call a rep

Visit website Apply online

Speak with arepresentative

Fill outapplication

Receive account opening documents

Receive account opening documents

Withdraw money

Pay bills

Receive paperwork to sign

Check rates online

Talk with friendsVisit branchReceive account

opening documentsFax/email signed paperwork to bank

Log in

Download mobile app

Deposit money

Receive statements and alerts

Evaluate financial situation

Learn about new services View cross-sell promotions

Receive account closing paperwork

Add account

Research products/services

Initiate account closing

Transfer money and check balances

THIN

KIN

G

• Who do my friends and family bank with? • How do I choose the best account for my needs?• Does the bank offer the services and technology I need?• How close are the nearest branches and ATMs?• How do fees and rates compare to other banks?• How big is the bank’s presence (local, national, international)?• Does this bank take an interest in my community?• How helpful and knowledgeable are the bank employees? • Will the bank help me grow and progress financially?

• Will it be difficult to open a new account?• Will I qualify for the account(s) that I want? • What does the fine print mean?• Will I be able to talk to a real person?• Will the branch representatives take care of all the paperwork?

Acquisition• What should I expect when my account is taken over by the bank?• Will I be able to continue working with my advisor from my old bank?• What will happen to the employees at my local branch?

• What services and features are offered with my new account(s)?• Will I be able to understand how to use my account?• Will I have problems logging in to my account online or

on my mobile device?• Will all of my bank accounts transition smoothly?

• Will I be able to reach someone at the bank easily if I have a question or a problem?

• Is my bank looking out for my best interests?• Are my banking activities and identity secure?• Can I easily access my accounts wherever and whenever I need to?

• What are these new features all about (e.g., mobile banking)? Are they useful?

• Will it be easy to add a new account?• Is there a branch nearby where I can talk to someone about adding

an account?• Are there any benefits to switching the account(s) that I have with

the bank?• Will the bank monitor my account(s) and let me know when I should consider

a change?

• Can I trust my current bank?• Are there banks with better interest rates?• Can I find a bank that doesn’t charge as many fees?• Will other banks move faster (e.g., refinancing)?• Is another bank’s promotion worth switching for?• How difficult and painful will it be to switch banks?• Can I find a knowledgeable financial team to work for me?• Are there any loyalty benefits for sticking with the bank?• Can I live with the frustrations that I have with my bank’s technology?

FEEL

ING

Pos

itive

Comfortable — I’ve done my research Happy — the bank does a lot of great things for the local communityConfident — my friends/family have recommended the bank Excited to open my first account Respected — branch representatives sat down with me and explained options and servicesConvinced — switching will deliver a better experience than my current bank

Happy — the reps are here to help me open an accountThankful — the bank was willing to lend me money Special — as if my transaction were the only thing happening in the branch

AcquisitionWelcomed during the takeover Comfortable — the bank knows what is going on and I can ask for help

Empowered to build our home knowing that the bank was backing us Informed — the site is very comprehensive and explained all of the benefits that come with the account Comfortable — bank employees don’t make me feel stupid or behind the times when I ask questions about new technology Pleased — I have met all of the requirements to receive my promotional offer for opening an accountLucky — I had a smooth transition to the bank. Others did not

Valued — when I am recognized in the branch Secure — I am alerted when changes are made to my online account Comfortable — I can reach someone at the branch or by phone if I have a problem with my accountRelieved and happy — it isn’t a fight to get a problem solved Confident — my questions will be answered by friendly bank personnelPleased — my bank supports my community

Valued — when a teller or other employee suggests an option that will earn more interest or have lower fees Fortunate — the bank is looking out for my best interests Respected — the bank doesn’t push accounts/services that I don’t want

Intrigued by higher interest rates for checking accounts at other banksInterested in cash offers to open an account elsewhere

Indi

ffer

ent Confused — how do offers differ from bank to bank?

Concerned — will I be taking a step backwards, since the bank doesn’t have a global presence?

Worried — will it be difficult? It’s been a long time since I changed accounts Pleased — I wasn’t rushed and that the process was not stalledGlad to have it done — one more thing crossed off my to-do list

AcquisitionIndifferent — I didn’t actually choose the bankConcerned — will I lose access to my money?

Satisfied — my online issues have been dealt with quickly by phone reps Anonymous — I’m just a number after all the papers are signed

Acquisition Confused — I didn’t feel like everything was as clear as it could be Ignored — no communication from the bank since my accounts were transitioned

Easy to keep my money in the same place it has been since I was a kidOK — as long as everything is handled correctlyIndifferent — my bank is just a place to make payments; I’m a numberUnimportant — they haven’t taken the opportunity or time to approach me and find out what they can do for me

Unsure about some services like mobile banking and overdraft protection and whether they will benefit meAnonymous — the promotions I receive are generic Indifferent — I don’t really feel like I have a relationship with the bank

Lazy — I don’t feel like jumping through all the hoops to switch my account(s) Unappreciated — no one has contacted me or helped me learn how to maximize my banking relationshipImpatient — our mortgage refinancing is taking foreverUnfulfilled — I need a bank with an international presence

Dis

satis

fied

Distrustful of large banks that are sneaky and rude Impatient — waited a long time in a crowded, smelly waiting area Insecure — branch personnel were not super knowledgeable

Acquisition Burdened — I had to figure out how to switch some things on my ownUnappreciated — the bank is cold, impersonal and untrustworthyFrustrated and annoyed — many missteps and fees along the way

Upset — I can’t transfer funds to a friend immediately, even though he has a the bank account

Acquisition Unsettled — I didn’t have the tools to access my accountUnimportant — ATM/debit cards and new checks were not reissued when promised Foolish — I was told that my banking service would be the same and it has not turned out that way

Dissatisfied — I feel disconnected; I’d like a better relationshipFrustrated — I keep getting locked out of my online banking account — especially when the Customer Contact Center is closed! Irritated — I’ve requested that my email address be changed multiple times and it still hasn’t been doneAnnoyed — my online account history displays only 90 days of transactionsUnappreciated — I am not rewarded for my loyalty. Why do new customers get all the perks? Irked — it’s hard to get in touch with my advisor

Disappointed — the bank has not analyzed my patterns and reviewed changes that could benefit me. I’m left to do this work on my ownUninformed — I don’t receive information about promotions or products Annoyed by the constant promotional mailings that I receive from the bank Impatient — tellers at the bank try to upsell me when I’m in a hurry — I’m there for a specific reason

Angry — my bank made a mistake with my bank accountVulnerable — I felt like my accounts had been compromised Embarrassed — a customer service representative made me feel dumb, instead of trying to help Deceived — the bank’s financial practices don’t seem straightforward, and extra fees keep getting added to my account(s) Exasperated — when I can’t log in to my online account and the Customer Contact Center is closed

OPP

OR

TUN

ITIE

S

• Create personal connections with prospective customers• Make it easy to understand and differentiate between account options• Share stories from advocates

• Create flexible and customizable account options• Make account opening simple and straightforward• Provide customer support at each step of the process• Welcome and guide acquired customers through conversion

• Follow up on all new customers with personalized communications• Identify and honor customer communication preferences• Provide educational tools• Assign acquired customers to a bank counselor

• Form a relationship with each customer• Be available to customers• Encourage and reward loyalty

• Work for each customer’s financial well-being• Make it easy to grow the relationship• Provide customized messaging and promotions online

• Provide prompt, expeditious responses to customer concerns• Follow up personally on all account errors• Match competitor offers

Consideration Account Opening Onboarding Day-to-Day Account Management Expanding Relationship Ending Relationship

CONSIDER AND EVALUATE

The path to purchase and beyondCustomer life cycle stages

Opportunities for improvement

Customer thinking Illustration of customer journey

The Retail Bank’s One-Stop Guide to Journey Mapping Page 14

Measure and Plan Improvements

Post-customer journey mapping, the bank needs to start migrating qualitative data from different sources into one measurement tool, either dashboards associated with customer journeys or the journey map itself. If baseline data is needed for different journey touch points, that data will first need to be collected. After the measurement tool and data are in place, you can build out a detailed roadmap for the design, development and measurement of the selected customer journey map improvements. The roadmap document will provide a brief description of each initiative, planned timing, success measurements, and business goals. The more detailed the roadmap from a project management and business goal perspective, the easier it will be to execute and gauge the effectiveness of the solutions.

HOW CAN I GET STARTED?

Before a company can get started, it needs to assess its organizational capabilities and its capacity to create customer journey maps with in-house resources. If your company needs additional support and has a need for significant product or process improvements over the next year, give Catalyst a call. We can schedule a consultation to help you determine whether customer journey maps can help drive results for your bank and create a plan to help get you there.

The Retail Bank’s One-Stop Guide to Journey Mapping Page 15

ABOUT THE AUTHOR

TARA LITCHFIELD Director of Experience Design

MORE ABOUT CATALYST

Catalyst (www.catalystinc.com) is a marketing agency that helps retail bankers develop more profitable customer relationships. By combining our intellectual curiosity and inquisitiveness with hard-core analytics and measurement, we create acquisition, retention, CRM, and CX programs that improve the customer experience at every stage of the life cycle, from account opening through onboarding through relationship expansion.

We call it Science + Soul.

It’s a powerful combination that results in a measurable increase in new accounts, deposits, upsell and cross-sell opportunities, and increased customer lifetime value.

TO LEARN HOW CATALYST CAN HELP YOUR RETAIL BANKING BUSINESS,

CONTACT:

Christian Banach at 585.453.8313 or email: [email protected]

or

Mike Osborn at 585.453.8331 or email: [email protected]

As Catalyst’s director of experience design, Tara develops engaging and effective experiences for our clients’ customers. She leads research initiatives to uncover new insights, then translates those insights into optimized customer experiences.

Her tool kit includes personas, journey maps and touch point analyses to help clients understand their customers in new ways, which leads to new business opportunities. She is an experienced UX designer who creates information architecture, workflow diagrams, detailed wireframes, interactive prototypes, user experience requirement documentation, content strategy, and heuristic evaluations to develop detailed customer-focused creative solutions. She conducts in-depth usability studies to validate and measure a solution’s effectiveness.

Tara holds an MA in visual arts and a BS in psychology. She has worked with a variety of Fortune 500 clients, including American Express, Honeywell, Kaspersky Lab, Paychex, Sears, Anthropologie, Carpet One, Reebok, Verizon, and Campbell’s Soup, among others.

800.836.7720 | www.catalystinc.com | [email protected] Facebook Twitter LinkedIn © 2017 Catalyst