the relationship between the european union and mercosur

TRANSCRIPT

This article was downloaded by: [The University of British Columbia]On: 27 April 2013, At: 09:46Publisher: RoutledgeInforma Ltd Registered in England and Wales Registered Number: 1072954 Registered office: Mortimer House,37-41 Mortimer Street, London W1T 3JH, UK

The International Spectator: Italian Journal ofInternational AffairsPublication details, including instructions for authors and subscription information:http://www.tandfonline.com/loi/rspe20

The Relationship between the European Union andMercosurSheila Page aa Research Fellow at the Overseas Development Institute, LondonVersion of record first published: 29 Apr 2008.

To cite this article: Sheila Page (1999): The Relationship between the European Union and Mercosur, The InternationalSpectator: Italian Journal of International Affairs, 34:3, 91-108

To link to this article: http://dx.doi.org/10.1080/03932729908456879

PLEASE SCROLL DOWN FOR ARTICLE

Full terms and conditions of use: http://www.tandfonline.com/page/terms-and-conditions

This article may be used for research, teaching, and private study purposes. Any substantial or systematicreproduction, redistribution, reselling, loan, sub-licensing, systematic supply, or distribution in any form toanyone is expressly forbidden.

The publisher does not give any warranty express or implied or make any representation that the contentswill be complete or accurate or up to date. The accuracy of any instructions, formulae, and drug doses shouldbe independently verified with primary sources. The publisher shall not be liable for any loss, actions, claims,proceedings, demand, or costs or damages whatsoever or howsoever caused arising directly or indirectly inconnection with or arising out of the use of this material.

THE INTERNATIONAL SPECTATORVOLUME XXXIV, No, 3, July - September 1999

The Relationship between theEuropean Union and Mercosur

Sheila Page

Sheila Page is Research Fellow at the OverseasDevelopment Institute, London.1

The relations between the European Union and Mercosur (the Common Market ofthe South2) are part of a complex nexus of linkages and also of approaches to in-ternational economic policy. The regions are traditional trading partners, but theyalso have other links: economic (investment, services, etc.), historic and political.And their relations do not exist in a vacuum. For the EU, Mercosur has to be seenin the context of

its internal economic policies, especially in agriculture;its expansion to the East;its other ties to Latin America;its relations with other middle-income countries;its relations with the US;the evolution of its approach to other regions.

For Mercosur, its relations with the EU have to be balanced against

• its relations to the rest of Latin America;• its relations to the US;• its own accelerating integration and evolving external policies.

Beyond these, there are influential external events such as the development of theworld trading system and, most recently, the Brazilian financial crisis.

This article will try first to sketch the context of EU-Mercosur relations, then tosummarise their current trade and investment flows, and finally to look at how a EUpolicy to Mercosur could fit into the other EU and Mercosur policies and priorities.

1 This article is a revised version of a paper prepared for the IAI's International Affairs Laboratory. Theopinions expressed do not necessarily correspond to those of the firms participating in the Laboratory.

2 Full members: Argentina, Brazil, Paraguay and Uruguay; associate members: Bolivia and Chile.

91

Dow

nloa

ded

by [

The

Uni

vers

ity o

f B

ritis

h C

olum

bia]

at 0

9:46

27

Apr

il 20

13

THE RELATIONSHIP BETWEEN THE EU AND MERCOSUR

EU-Latin America relations

Background

European policy towards Latin America in the 1970s and 1980s emphasised aidand cooperation for democracy (and, at times, conflict prevention) more thantrade. The trade seen as important was trade within Latin America. Although LatinAmerica has always received a much lower proportion of total European aid thanthe more recent ex-colonies - the African, Caribbean and Pacific (ACP) countries- the EU has been a major donor in Latin America and, as such, has a potentiallysignificant voice. Up to the mid-1990s, EU aid, including both bilateral and Commis-sion aid, accounted for 40 percent of aid to Latin America. The principal declaredpriority of the EU's Latin American programmes, which distinguishes them fromthose of other donors, has always been the promotion of regionalism. CommonEuropean assistance to Latin America began with the first European Commu-nity/Latin America Joint Committee in 1970, following which the EC established di-rect relations with the Andean Pact.3 This was regarded by the Commission aspotentially similar to itself, and therefore received substantial assistance. It is prob-able that EU assistance kept the Pact alive through the late 1970s and 1980s whenthere was little active local integration.

The second and third generation agreements with Latin American countrieswere also with regional arrangements (hereinafter referred to as "regions"), and de-signed to encourage integration both formally and through infrastructure. The impor-tance of regions is mentioned in all EU agreements with Latin American countries andregions, and most make provisions for technical assistance in implementation.

There are, however, strict limits to the geographical scope of the regionalismpromoted by the agreements. The agreement with Mexico explicitly mentions onlyexisting regional agreements (which would include those with other Latin Ameri-can countries, but not, at the time of agreement, the North American Free TradeAssociation - NAFTA),4 and both the Brazil and the Paraguay agreements explic-itly encourage agreements only in their region. It seems clear that this regionalismis intended to exclude arrangements with the US. The underlying argument is thatagreements with the US (but not with the EU?) would reduce member countries' in-terest in purely Latin American agreements, and thus potentially reduce the bene-fits of these.

European interest in Latin America increased in the 1990s, some years afterthe accession of Spain and Portugal to the EU: while their entry clearly increased

3 Andean membership has varied, but the EU has always had relations with the group, not individualcountries. Members: Peru, Colombia, Ecuador, Bolivia; Chile was a member at the beginning buthas left; Venezuela has now joined.

4 Commission of the European Communities, "Towards Closer Relations between the European Un-ion and Mexico". Communication from the Commission to the Council and the European Parlia-ment, Brussels, 2 August 1995 (mimeo).

92

Dow

nloa

ded

by [

The

Uni

vers

ity o

f B

ritis

h C

olum

bia]

at 0

9:46

27

Apr

il 20

13

SHEILA PAGE

the number of countries with an interest in the area, it was not the cause of eitherthe rise in interest or its timing. The economic interests of France and the UK werealready a century old; there was a long tradition of Italian interest, particularly inSouth America; and Germany has become a major investor.

The third generation agreements signed in the 1990s with the Central Ameri-can, Andean, and Mercosur countries were much broader than the 1970s and1980s agreements, and for the first time had a private sector component, with sup-port for investment. The coverage includes industry and agriculture, financial,transport and communications services, and energy, but also the environment, in-vestment, science and technology, intellectual property, industrial standards, andmonetary policy, indicating how far they have moved beyond simple internationaltransactions.

From 1989, for the first time, some Latin American countries were given extratrade preferences. Following the very political tradition of European assistance toLatin America, these were neither for the poorest nor for those most likely to im-port from the EU, but for the drug producing Andean countries (this, again, was anagreement with the regional group); the intention was to promote stability by offer-ing alternative exports.

The agreements of the fourth generation, starting with Mercosur in 1995, thenChile in 1996 and Mexico in 1997, provide encouragement for regional integration,ministerial level consultation, and the possibility of reciprocal free trade.

In spite of this increased interest in Latin America, the level and the share ofaid going there fell, notably in 1997 after a peak in 1996. It now receives only 14percent of EU flows, behind the shares not only of Africa, but also of Asia. The re-ductions appear to reflect a shift to poorer areas, mainly Africa, and also the newflows to Eastern Europe. Within Latin America, there has been a shift from thericher to the poorer. In 1997, the Mercosur countries received only 14 percent ofthe total (although accounting for about half the Latin American economy), withthe Andean countries receiving 38 percent and Central America 30 percent.5 Asthe aid budget was redirected to other priorities, trade agreements became thecentral tool of EU relations with Latin America, especially Mercosur and Mexico.

EU-Mercosur

The emphasis on regions is most explicit in the agreement signed with Mercosur inDecember 1995,6 which emphasises the importance of regionalism in promotinginternational integration. It notes the common interests and experiences of the EUand Mercosur. It provides specifically for the EU to give technical assistance in theimplementation of Mercosur institutions. Assistance for countries attempting to

5 "Development Cooperation with Latin America: Will Europe's Role Diminish?", IRELA Briefing, 31March 1999, IRELA, Madrid.

6 Commission of the European Communities, "Acuerdo marco interregional de cooperación entre lacommunidad Euopea y sus estados miembros y el mercado común del sur y sus estados partes",1995.

93

Dow

nloa

ded

by [

The

Uni

vers

ity o

f B

ritis

h C

olum

bia]

at 0

9:46

27

Apr

il 20

13

THE RELATIONSHIP BETWEEN THE EU AND MERCOSUR

meet their regional commitments, for example the fiscal cost of reduced tariff re-ceipts in a free trade area, is potentially also important.

Preparing the conditions for an inter-regional association between Mercosurand the EU is one of the declared objectives of the agreement; mention is alsomade of the possibility for an EU-Mercosur free trade area. Along with the similarframework agreements signed with Mexico and Chile, this was the first example ofmoving from encouraging regions within Latin America to proposing agreementsbetween Latin American countries and Europe. The idea of free trade areas(FTAs) between the EU and Mercosur or EU and Mexico would be a significant ex-tension of inter-regional links, but it is not clear if this is feasible. As will be dis-cussed later, there are difficulties with sensitive products.

Chile is an associate member of Mercosur, making it impossible for the EU tosign a single agreement with Mercosur and Chile, but it is envisaged that negotia-tions with the two will be parallel and any agreements consistent.

EU relations to other regions

Its size, level of development, and - now - age have given the EU a particular role inrelation to other regions, not only as a model (or anti-model), but as a trading part-ner and aid donor with a strong commitment to a regional approach. The EU, as aregion itself, takes a strong view that economic linkages should be, perhaps need tobe, reinforced by institutional linkages. This means that it not only accepts regionsas trading partners or joint recipients for aid, but encourages their institutionalstrengthening. The EU also applies its interpretation of its own experience, that is,that forming a region promoted growth and efficiency as well as intra-regional secu-rity and peace, to other regions, and therefore sees this as a reason to encouragecountries to form regions. In a recent statement, the EU pointed out that it has en-couraged, partly by example, partly through direct support, many of the new re-gional groupings in the developing world, and "all major strategy documents andundertakings of the European Commission addressing the problems of developingcountries and the EU's relations with them, place a high priority on the support of re-gional initiatives".7 It is only since 1995, however, that this long-standing policy hasmoved beyond its encouragement of regional integration among developing coun-tries to promoting EU trading arrangements with developing regions.

Following the framework agreement with Mercosur in 1995, the EU startedregular regional official and ministerial meetings with ASEAN. This was not an ex-act parallel. The agreement only established a cooperation forum (more like theearly 1990s agreements with the Latin American countries). Interestingly (inview of what happened to the proposed EU-Mercosur summit) it was extended

7 Commission of the European Communities, "European Community Support for Regional EconomicIntegration Efforts among Developing Countries". Communication from the Commission, Brussels,16 June 1995, p. 1.

94

Dow

nloa

ded

by [

The

Uni

vers

ity o

f B

ritis

h C

olum

bia]

at 0

9:46

27

Apr

il 20

13

SHEILA PAGE

(because of pressure from other Asian countries) to a broader group than theASEAN preference area, which effectively precluded it from becoming the basisfor a region-to-region trade agreement.

The 1997 Green Paper on relations with the ACP countries followed the LatinAmerican precedents more closely. It proposed, as one of the options, signingtrade agreements with regions formed by the ACP countries. This had both ele-ments of the approach to the Latin American countries: first encouraging the for-mation or completion of trade agreements among developing countries, and thenchanging from EL) preferences to a reciprocal trading relationship. At the sametime, the proposals for reciprocity with countries, even if they are not a part of re-gional arrangements, was not confined to the Mexico negotiations; the EU hasnow signed a free trade agreement with South Africa (1999).

These developments mean that, contrary to the normal assumptions aboutFTAs, an EU-Mercosur agreement would not be a case of special treatment, except inthe sense that all the EU's bilateral arrangements are different. It would create one ofseveral FTAs, along with the EU's range of preferential agreements (the GeneralisedSystem of Preferences, the special arrangements for the Andean countries, Lome,the new special arrangements, for least developed countries, etc.).

Mercosur as a region

Equally, the agreement would not be special for Mercosur: Mercosur is also devel-oping a range of ties, including its association agreements with Chile and Bolivia,the regionalising of pre-existing bilateral arrangements between individual Merco-sur countries and the Andean countries, the speculative South American FreeTrade Area, and the negotiations for a Free Trade Area of the Americas (FTAA) toinclude the US. .

The Mercosur model of a customs union among four countries, with FTAs withothers, is different from that of the EU, which has expanded by requiring the wholeacquis to be adopted by any new member in its region. When the EU has estab-lished FTAs, these have been with clearly non-European countries. As Mercosur isstill young, it would be unwise to take its current intentions as irrevocable, but atpresent it appears to be assuming a regional identity permitting deep integrationamong four countries, contrasting with more limited interests in its relations withother trading partners. It is not clear how long the associate countries will acceptthis. Chile's original declared interests were entirely in trade access, not deeper in-tegration, but Chile and Bolivia are increasingly pressing for greater participation inall committees. Chile has joined in some of the working groups and joint initiatives,but is not formally a member because it did not want to raise its tariff (about 8 per-cent) to Mercosur's planned Common External Tariff (about 12 percent).

The 1997 Mercosur summit brought major steps toward greater integration. Atarget date for liberalising services was finally agreed, and there were the first dis-cussions of the possibility of transfer payments from the richer countries to thepoorer. This is normal in a customs union, and probably essential in a commonmarket. Chile was given observer status in the institutions, although still without a I = I

95

Dow

nloa

ded

by [

The

Uni

vers

ity o

f B

ritis

h C

olum

bia]

at 0

9:46

27

Apr

il 20

13

^ •?

THE RELATIONSHIP BETWEEN THE EU AND MERCOSUR

vote. Chile now no longer rules out full membership, and has sought Mercosursupport in trade disputes with the US outside current Mercosur obligations. InJanuary 1999, the Chilean foreign minister said Chile was willing to "consider acloser association with Mercosur in 1999, including possibly joining the customsunion".8

The Free Trade Area of the Americas

Of the new trade options open to Mercosur, the most obvious parallel or alterna-tive to an agreement with the EU is the US proposal for an FTAA. This would alsobe a way of securing preferential and guaranteed access to a major trading partnerand could be seen as an expression of a liberalising trade policy. But it is very dif-ferent in many ways. It would be a uniform agreement for the hemisphere (not spe-cial relationships tailored to partners). The proposed coverage goes beyond tradeto include services, investment, trading forms and practices. And the US, in pro-posing it, took no account of the existence of Mercosur (or other regions), unlikethe EU's specific proposal for a region-to-region agreement.

Although as initially proposed, creation of the FTAA was to be analogous to awidening of NAFTA, and the initial negotiations were in parallel with negotiationsfor Chile to enter NAFTA, Mercosur considered this politically unacceptable. Thenegotiations have now been restructured. It is an ambitious undertaking in num-bers alone. There is no precedent for an FTA forming with 34 members (or even 13if Mercosur, the Caribbean Community Common Market - CARICOM - and theCentral American Common Market - CACM - are counted as one member each),so the negotiations are likely to be prolonged. After initiation in 1994, the point ofdeciding to start trade negotiations was reached in 1998. But the US's ability to ne-gotiate is now in doubt without fast-track authority, and Mercosur, particularly Bra-zil, has been hesitant from the beginning. The FTAA would probably replace allthe existing bilateral arrangements and FTAs in Latin America because the pro-posed coverage would go beyond anything they include, unless they make new ar-rangements and rapid progress while FTAA negotiations proceed.

The negotiating questions for Mercosur as a customs union, however, aremore complicated, not only because it already covers (or is negotiating to cover)areas that go beyond the FTAA proposals (including, most notably, its common ex-ternal tariff), but because, unlike the careful EU distinction between an agreementwith Mercosur as a group and one with Chile as a country, the US proposal initiallytreated all countries individually, with no regard for the negotiating position of re-gions. On tariffs, it should have been obvious that for the customs unions, any tar-iff reductions would have to be agreed and implemented on a regional, not countrybasis. Nevertheless, the US initially opposed accepting the regions as competent

8 "Chile and the European Union: Prospects of Association", IRELA Briefing, 18 January 1999,IRELA, Madrid.

96

Dow

nloa

ded

by [

The

Uni

vers

ity o

f B

ritis

h C

olum

bia]

at 0

9:46

27

Apr

il 20

13

SHEILA PAGE

in the negotiations, and apparently tried to divide members of Mercosur. After thestart of negotiations, 11 working groups were formed, on a country basis. Joint ne-gotiation for regions was finally agreed in the first half of 1997; members of FTAsremained free to negotiate jointly or separately according to choice. Mercosur andCARICOM have declared that they will negotiate as groups, and Chile and Boliviaare increasingly negotiating with Mercosur. Chile has now committed itself to do-ing so in the FTAA. An alternative outcome would be for Mercosur's expansion tomove faster, taking in the Andean countries (or even the proposed South Ameri-can Free Trade Area - SAFTA); then all would negotiate with the NAFTA coun-tries, the CACM, and CARICOM as a group. NAFTA countries will negotiateindividually.

Integrated groups may need to negotiate together even on issues not yet cov-ered by their region, thus encouraging regional coordination, if not harmonisa-tion.9 The negotiations cover some subjects which are not included in Mercosur.On others, for example services, there are simultaneous negotiations in the FTAAand Mercosur.

The question of how to proceed on matters which are in process of integrationin both the region and FTAA is particularly acute for Mercosur. Is it necessary tointegrate at the sub-regional level first, in order to preserve a Mercosur identitywithin the FTAA, or are the advantages of larger-scale integration more impor-tant? The official view in Argentina and Brazil, at least, is that greater integrationat the Mercosur level should precede the FTAA.10 This helps to explain the effortsby Mercosur to slow FTAA negotiations by arguing over the sequence of integra-tion. It supports the view that Mercosur is seen as an important grouping for politi-cal reasons, not simply a vehicle for obtaining economic advantages fromintegration.

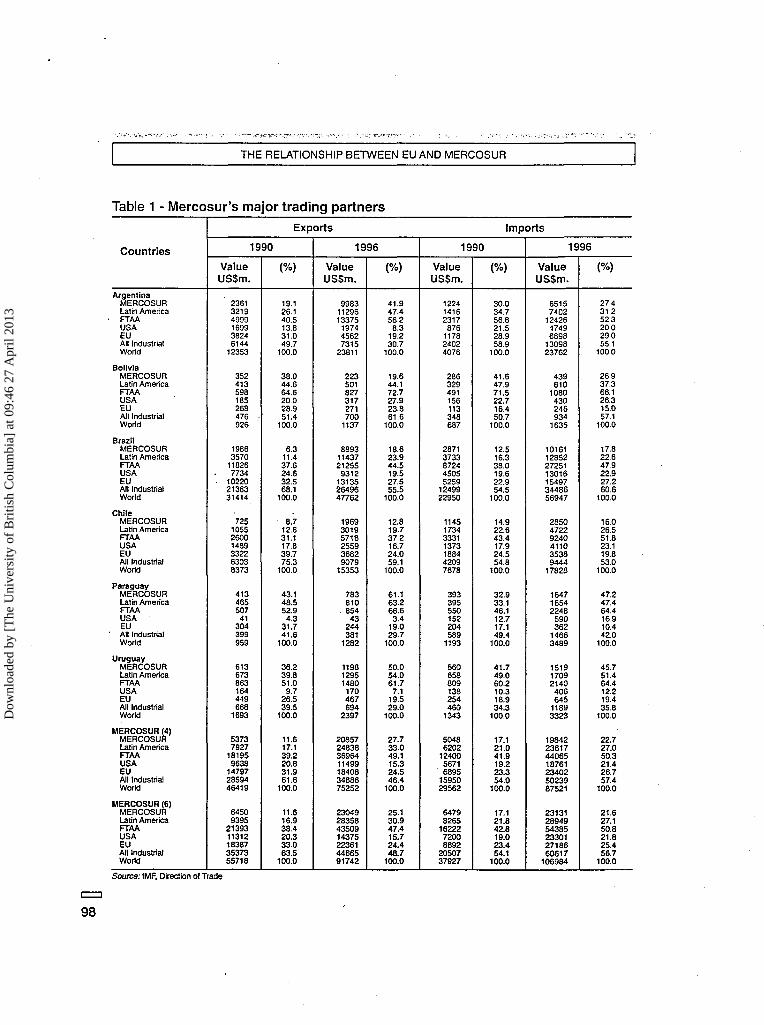

Trade flows

Tables 1 and 2 show the importance of the EU to Mercosur and of Mercosur to theEU. The EU is Mercosur's single most important trading partner and is important toall Mercosur members. What is striking (and obvious in both tables) is the shiftfrom a Mercosur surplus in trade with the EU in 1990 to a deficit by 1996, becauseof a tripling of Mercosur's imports from the EU, which has increased the EU'sshare in Mercosur imports from 23 percent to 27 percent. For the EU, of course,Mercosur is much less important. The surge in exports to Mercosur has shown upas a doubling in the share of this market, but all of Latin America is only 2 percentof EU trade, and Mercosur, 1 percent.

9 The obvious analogy is EC's parallel negotiations as group and countries in the Uruguay Roundwhich included tariffs (EC competence), investment (country), and services (mixed).

10 On 19 June 1997, during the Mercosur summit, Argentina's Secretary of International EconomicRelations, Jorge Campbell, stated that "the existence of negotiations on the FTAA requires us todeepen Mercosur in orderto survive with a real identity"; Mercosur (Madrid: IRELA, 1997) p. 27.

97

Dow

nloa

ded

by [

The

Uni

vers

ity o

f B

ritis

h C

olum

bia]

at 0

9:46

27

Apr

il 20

13

THE RELATIONSHIP BETWEEN EU AND MERCOSUR

Table 1 - Mercosur's major trading partners

Countries

ArgentinaMERCOSURLatin AmericaFTAAUSAEUAll IndustrialWorld

BoliviaMERCOSURLatin AmericaFTAAUSAEUAll IndustrialWorld

BrazilMERCOSURLatin AmericaFTAAUSAEUAll IndustrialWorld

ChileMERCOSURLatin AmericaFTAAUSAEUAll IndustrialWorld

ParaguayMERCOSURLatin AmericaFTAAUSAEUAll IndustrialWorld

UruguayMERCOSURLatin AmericaFTAAUSAEUAll IndustrialWorld

MERCOSUR (4)MERCOSURLatin AmericaFTAAUSAEUAll IndustrialWorld

MERCOSUR (6)MERCOSURLatin AmericaFTAAUSAEUAll IndustrialWorld

1990

ValueUSSm.

236132194999169938246144

12353

352413598185268476926

19863570

11826• 7734• 10220

2138331414

725105526001489332263038373

41346550741

304399959

613673863164449668

1693

53737927

181959638

147972859446419

64509395

2139311312183873537355718

Exports

(%)

19.126.140.513.831.049.7

100.0

38.044.664.620028.951.4

100.0

6.311.437.624.632.568.1

100.0

8.712.631.117.839.775.3

100.0

43.148.552.94.3

31.741.6

100.0

36.239.851.0

9.726.539.S

100.0

11.617.139.220.831.961.6

100.0

11.616.938.420.333.063.5

100.0

1996

ValueUS$m.

99831129613375

197445627315

23811

223501827317271700

1137

88931143721255

9312131352649647762

196930195718255936829079

15353

78381085443

244381

1282

119812951480

170467694

2397

20857248383696411499184083488675252

23049283584350914375223614466591742

(%)

41.947.456.2

8.319.230.7

100.0

19.644.172.727.923.861.6

100.0

18.623.944.519.527.555.5

100.0

12.819.737.216.724.059.1

100.0

61.163.266.6

3.419.029.7

100.0

50.054.061.7

7.119.529.0

100.0

27.733.049.115.324.546.4

100.0

25.130.947.415.724.448.7

100.0

1990

ValueUS$m.

122414162317

876117824024076

286329491156113348687

28713733872445055259

1249922950

1145173433311373188442097678

393395550152204589

1193

560658809138254460

1343

50486202

124005671

' 68951595029562

64798265

1622272008892

2050737927

Imports

(%)

30.034.756.821.528.958.9

100.0

41.647.971.522.716.450.7

100.0

12.516.338.019.622.954.5

100.0

14.922.643.417.924.554.8

100.0

32.933.146.112.717.149.4

100.0

41.749.060.210.318.934.3

100.0

17.121.041.919.223.354.0

100.0

17.121.842.819.023.454.1

100.0

1996

ValueUSSm.

65157402

1242617496898

1309823762

439610

1080430246934

1635

10161128522725113016154973448656947

285047229240411035389444

17828

164716542248

590362

14663489

151917092140

406645

11893323

19842236174406518761234025023987521

231312894954385233012718660617

106984

(%)

27.431252.320.029,055.1

100.0

26.937.366.126.315.057.1

100.0

17.822.647.922.927.260.6

100.0

16.026.551.823.119.853.0

100.0

47.247.464.416 910.442.0

100.0

45.751.464.412.219.435.8

100.0

22.727.050.321.426.757.4

100.0

21.627.150.821.825.456.7

100.0

Source: IMF, Direction of Trade

98

Dow

nloa

ded

by [

The

Uni

vers

ity o

f B

ritis

h C

olum

bia]

at 0

9:46

27

Apr

il 20

13

SHEILA PAGE

Table 2 - EU Trade with

Argentina

Bolivia

Brazil

Chile

Paraguay

Uruguay

MERCOSUR (4)

MERCOSUR (6)

Latin America

Developingcountries

World

Latin AmericaEU Exports

1990

ValueUS$m.,

1,668

185

5,077

1,750

229

305

7,279

9,214

27,097

257,181

1,492,200

(%)

0.11

0.01

0.34

0.12

0.02

0.02

0.49

0.62

1.82

17.24

100.0

1996

ValueUS$m.

7,319

251

14,522

3,429

408

868

23,117

26,797

49,745

449,032

2,041,600

(%)

0.36

0.01

0.71

0.17

0.02

0.04

1.13

1.31

2.44

21.99

100.0

Imports

1990

ValueUS$m.

4,526

328

12,352

3,400

544

512

17,934

21,662

36,566

281,016

1,543,000

(%)

0.29

0.02

0.80

0.22

0.04

0.03

1.16

1.40

2.37

18.21

100.0

1996

ValueUS$m.

5,087

222

13,340

3,719

189

527

19,143

23,084

41,844

409,851

1,953,200

(%)

0.26

0.01

0.68

0.19

0.01

0.03

0.98

1.18

2.14

20.98

100.0Source: IMF, Direction of Trade

Although Mercosur's trade flows within its own region and with the rest ofLatin America have increased sharply, these have remained roughly in balance.Mercosur's pattern with the US, however, is rather like that with the EU, with a fallin the share of exports, but a rise in imports, giving a move from surplus into defi-cit. The US is less important than the EU as a trading partner for almost all thecountries.

Even if we take the whole potential area of an FTAA - the US plus the rest ofLatin America and Canada - this would account for only about half of the Mercosurcountries' trade (less than the share of EU trade for EU countries, so not a very inte-grated region for its size). It would be higher for the smaller countries, but only abouthalf for Argentina, and under half for Brazil. For the Mercosur countries as a group,more than half their current exports to a potential FTAA go to Mercosur (Table 1);exports to the US are only about a third. As for imports, however, imports from theUS would account for as much as from the current Mercosur members, and muchmore than before the liberalisation within Mercosur occurred. This suggests that lib-eralising their trade to the US in an FTAA would be potentially much more difficultthan it has been within Mercosur: it would have a large impact on markets and tariffrevenues, made potentially more serious by the greater competitiveness.

Even for Brazil, the FTAA would take more than 50 percent of manufacturedexports. This reflects the different patterns of trade between Mercosur-EU andMercosur-US. The EU pattern is still much more one of exporting manufacturesand importing primary goods, while the US, as well as being, by virtue of its

99

Dow

nloa

ded

by [

The

Uni

vers

ity o

f B

ritis

h C

olum

bia]

at 0

9:46

27

Apr

il 20

13

THE RELATIONSHIP BETWEEN THE EU AND MERCOSUR

geography, less dependent on imports of primary goods, has shifted in all its tradewith developing countries more to imports of manufactures than has the EU. OfLatin America's 25 main export products to the EU in 1994, only motors (in 16thplace) and leather shoes (25th) (along with refined copper) could be classified asmanufactures.11 Only 35 percent of the total were manufactures, well below LatinAmerica's average of over a half. Chile follows the pattern of the rest of Mercosur,with 90 percent of its exports primary goods. This shows the importance of the EUpolicy on agricultural imports (half the total).

There are no good regional figures for trade in services, but it should be notedthat this sector is included now in Mercosur, and is under negotiation for inclusionin the FTAA. The picture for any agreement with the EU is less certain. Trade inservices has not been a major part of other regional agreements signed or pro-posed by the EU. As they are an important and growing part of the Mercosureconomies, failure to include them in an agreement with the EU could reduce therelative desirability of the EU compared to the FTAA.

Investment flows

European investment has returned to Latin America in the 1990s, increasing bothLatin America's share in European investment (estimated as a quarter of Euro-pean investment outside the Organisation for European Cooperation and Develop-ment - OECD - in 199512), and Europe's share in Latin America's inflows. OfEuropean investment in Latin America, 85 percent goes to South America, and twothirds of that to Mercosur (Table 3). Mercosur is also important to Japan: this sug-gests that we are observing high US investment in Mexico, rather than exceptionalinterest by the EU in Mercosur.

In Brazil, almost a third of investment in 1997 (and of stocks in that year) wasfrom the EU, compared to 29 percent (a quarter of stocks) from the US.13 But ofcourse no individual country was as important as the US, with France and theNetherlands the only countries approaching 10 percent, followed by Portugal andSpain. For Argentina and Chile, however, Spain, with 40 percent and 31 percent,respectively, outweighed the US, about 20 percent in both, with total EU invest-ment in 1997 about half the total. Table 4 shows how European importance toMercosur has increased relative to other developed country investors in the1990s. The principal investors are different from the world average: at the worldlevel, the UK and Germany, followed by France would be most important; amongEU investors to Mercosur, France is joining Germany as important, with Spain also

11 Closer European Union Links with Eastern Europe: Implications for Latin America (Madrid: IRELA,1997).

12 Latin America and Europe: Beyond the Year 2000, Dossier No. 65 (Madrid: IRELA, September1998).

13 Foreign Investment in Latin America and the Caribbean. 1998 Report (Santiago de Chile: CE-PAL/ECLAC, 1998).

100

Dow

nloa

ded

by [

The

Uni

vers

ity o

f B

ritis

h C

olum

bia]

at 0

9:46

27

Apr

il 20

13

SHEILA PAGE

Table 3 - FDI flows from Europe, the United States and Japan by sub-region,1990-96 (%)

Argentina

Brazil

Paraguay

Uruguay

MERCOSUR

Chile

Andean Group

Mexico

Central America

Latin America arid the Caribbean

1990-1996

Europe

19.1

34.2

0.2

2.1

55.6

7.7

20.0

13.7

0.1

100.0

USA

10.3

32.8

0.1

0.4

43.6

8.4

12.3

30.4

1.6

100.0

Japan

5.9

48.5

0.0

0.0

54.4

2.6

13.0

29.7

0.2

100.0

Source: IDB/lFtELA, Foreign Direct Investment in Latin America, Madrid 1998.

Table 4 - FDI flows

Austria.BelgiumDenmarkFinlandFranceGermanyItalyNetherlandsPortugalSpainSwedenUnited Kingdom

European Union

SwitzerlandEuropeUSJapanTotal

to MERCOSUR and to Latin America and the Caribbean,MERCOSUR

1980-89

0.000.490.000.164.87

11.214.813.340.002.410.05

17.99

45.33

0.0045.3342.9711.70

100.00

1990-96

0.120.800.120.174.826.230.795.860.874.250.449.05

33.50

1.6235.1360.624.25

100.00

1996

0.074.970.260.00

16.12-1.091.673.833.397.511.54

13.53

51.81 ..

1.6753.4839.117.42

100.00

1980-89

0.000.570.040.116.47.

10.753.712.680.004.90

-0.0817.52.

46.71

0.0046.7142.1611.17

100.00

Latin America

1990-96

0.060.890.160.243.424.394.544.590.416.220.307.32

28.47

1.5830.0566.233.71

100.00

1980-96 (%)

1996

0.043.240.270.14

11.42-0.871.032.381.738.840.81

11.03

40.04

2.1942.2353.40

4.37100.00

Source: IDB/IRELA, Foreign Direct Investment in Latin America, Madrid 1998.

101

Dow

nloa

ded

by [

The

Uni

vers

ity o

f B

ritis

h C

olum

bia]

at 0

9:46

27

Apr

il 20

13

THE RELATIONSHIP BETWEEN THE EU AND MERCOSUR

consistently important. The share of Italy has fallen, and in particular it did notshow the large surge in 1996 of the other investors. In flows to all of Latin America(excluding the offshore financial centres), the same pattern among Europeancountries can be seen, suggesting that it is not a Mercosur phenomenon (exceptthat Portuguese investment appears almost entirely confined to Mercosur).

Different national interests can be identified.14 For the service sector, Spain,France and Britain are important; for manufacturing, Germany and the Nether-lands. The services investments, in particular, are tied to supplying local markets,rather than for export, and have been greatly increased in recent years by the pri-vatisation programmes (especially in Brazil). The investment in manufactures hasbeen both for local consumption and for export, and for the regional (Mercosur)market and for Europe.

Mercosur and other EU interests

There were fears in the early 1990s that the negotiations to admit the EasternEuropean countries to the EU would reduce European interest in Latin America. Astudy in 1996 found that economically there was little direct effect, although therewere some negative changes.15 There was increased trade with Eastern Europe,and while economically this was not a "diversion", but rather a return to traditionalsuppliers, for the Latin American countries and products affected it was still a cost.But, like Latin America, these countries account for only a very small proportion ofEU trade so that the developments in other areas and in general EU trade policyare likely to be much more important influences in fact, if not in perceptions. Therewas apparently some switch of investment, but in the context of large increases inall European investment outside Europe, this did not (as seen) prevent a large in-crease also to Mercosur. There was a clear reduction in development assistanceto developing countries when assistance to Eastern Europe increased (althoughsome was "new money"). Within the total of development and Eastern Europe as-sistance, Latin America's share was therefore reduced, although only from 6.3percent in the 1980s to 6 percent in the 1990s. Italy shows a particularly sharpdrop, to providing only 2 percent of European aid to the region in 1997.16

Perhaps the more important risks, however, were expected to come in the fu-ture. The Eastern European countries have no historical or economic interests inLatin America, and therefore would on balance reduce the pressure for special re-lationships there. Their agricultural economies were expected to put pressure onthe Common Agricultural Policy (CAP). This could have led to major reform (andhelped all exporters of agriculture, including Mercosur), but it now seems morelikely that it will produce the minimum changes designed to accommodate them - if

14 IRELA, Latin America and Europe, p. 21.15 IRELA, Closer European Union Links with Eastern Europe.16 IRELA, "Development Cooperation with Latin America".

102

Dow

nloa

ded

by [

The

Uni

vers

ity o

f B

ritis

h C

olum

bia]

at 0

9:46

27

Apr

il 20

13

SHEILA PAGE

necessary, at the expense of other traders. These doubts mean that the EU must(if it is interested in improving relations with Mercosur) stress and demonstrate itsinterest and intentions more strongly than normal.

But the impression that it has been giving is of a weakening. The signature offramework agreements with Mercosur in December 1995 and with Chile in June1996 should have been followed by adoption of a negotiating mandate (as withMexico, where negotiations are in progress). The necessary preparations for ne-gotiations foreseen in the framework agreement (the drafting of an agreed data seton trade, tariffs, standards, and other trade information) had been completed, butthe Council did not adopt a negotiating mandate until 1999. Meanwhile, the FTAAnegotiations had started. The transformation of a proposed EU-Mercosur summitinto an EU-Latin American-Caribbean summit (held 28-29 June 1999 in Rio de Ja-neiro) reduced its value to Mercosur. It suggests that the EU's interests are now of ageneral trading nature on the continent, rather in establishing a special alliance withanother customs union or with a powerful potential counterweight to the US.

The negotiating mandate was finally presented by the Commission to theCouncil of Ministers in July 1998, after the vote of four commissioners (includingthe Agriculture Commission) against presenting it weakened the pressure for itsadoption. Adopting the mandate was also delayed so that advances on reform of theCAP and the conditions for entry of the Eastern European countries could be madebefore setting an agenda that would have to include agriculture. The agriculturalagreement in March 1999 removed part of the excuse for delay, although its inade-quacy made any negotiation difficult. The disruption to the Commission's activitiesbecause of the collective resignations then set all business back. Finally, at the June1999 Rio summit, it was agreed to start negotiations in November 1999, but discus-sion of tariffs was postponed until 2001. This was close to the minimum required tokeep EU-Mercosur negotiations in parallel with FTAA negotiations.

The facts that the negotiations with Mexico (which signed its frameworkagreement more than a year after Mercosur) were begun in November 1998, thatnegotiations on an FTA with South Africa were completed in March, and that theEU has proposed FTAs with all the countries currently under the Lome agreementsuggest that the EU is still interested in signing FTAs with its trading partners.Consequently, not negotiating with Mercosur would not merely mean refusing spe-cially favourable treatment, but offering below normal treatment.

"Normal" treatment is probably what Mercosur and the EU can aim for in theirrelations: the countries on both sides can, of course, muster historical reasons oreconomic examples to argue for special European interests in Mercosur, but anexamination of the agendas for EU-Caribbean, EU-African, EU-Mediterranean orany other EU negotiation shows that these are no more a guarantee of specialtreatment of Mercosur by the EU than of the EU by Mercosur.

EU-Mercosur negotiations

Both the FTAA negotiations and the EU-Mexico negotiations (the two obvious mod-els for an EU-Mercosur agreement) cover a wide range of subjects beyond tariff C=D

103

Dow

nloa

ded

by [

The

Uni

vers

ity o

f B

ritis

h C

olum

bia]

at 0

9:46

27

Apr

il 20

13

THE RELATIONSHIP BETWEEN THE EU AND MERCOSUR

reductions, including services, investment, competition policy, intellectual prop-erty - all areas either in or proposed for multilateral negotiations in the next roundof negotiations in the World Trade Organization (WTO). An agenda for EU-Mercosur, therefore, must either include these or take a deliberate decision to ex-clude them.

Up to now, however, most discussion has focussed on trade. Under WTOrules for regions (Article XXIV and the Understanding on Article XXIV adopted inthe Uruguay Round), an FTA among members of the WTO must include "substan-tially" all trade, and cannot entirely exclude any major sector. There is a limit of 10years on the transition period. No definition is given in the Article of "substantially",although it is now often assumed to be 90 percent. Any proposed region must bereferred to the WTO's Committee on Regions for appraisal, and report to the WTOCouncil, and as no region has yet completed this process, there is no legal rulingon the criteria.17 The European Commission appears to be introducing its own in-terpretation of the rules, not only assuming that 90 percent is a limit, but that it is90 percent of present trade, which is less rigorous than 90 percent of potentialtrade. Tariffs or other barriers reduce the share of any sensitive commodity, andthus make it easier for these to fall under 10 percent of recorded trade. It has alsoargued (in the EU-South Africa FTA, the most recent signed) that the 90 percent isan average across all the participants in an FTA, so that if one offers to liberalisemore than 90 percent, others can offer less.

This playing with numbers and rules suggests that the FTAs now being con-sidered are very different from those seen in the past. While the EU and Mercosur(and NAFTA) have all had some products excluded during (sometimes long) tran-sition periods, none has maintained permanent exclusions, and none has goneinto the negotiations with the intention of liberalising as little as possible to meetthe rules, even when the rules were much less enforceable than they are now.This suggests that the EU's new FTAs are being seen as preference arrange-ments, offering limited and carefully measured economic advantages to each side,rather than as conventional regional arrangments, where strong political motivesfor the region make the calculation of economic costs and benefits secondary.This supports the view that the EU-Mercosur FTA is to be seen in the normal run ofboth sides' trading arrangements, rather than as a special relationship.

Under this assumption, there is no reason for Mercosur or the EU not to pur-sue other trading arrangements at the same time, whether in the FTAA or withEastern Europe. Such simultaneous negotiations would be awkward if the primaryobjective is to gain an advantage relative to another area (e.g. for the EU to gainan advantage in Mercosur relative to the US or for Mercosur to gain an advantagein the EU relative to Asian or African countries). Both Mercosur and the EU should

17 The EU was notified under the easier regime of the 1950s, which required only that there not be aconsensus against it. Mercosur was also notified before the beginning of the WTO, although it is stillunder examination by the Committee.

104

Dow

nloa

ded

by [

The

Uni

vers

ity o

f B

ritis

h C

olum

bia]

at 0

9:46

27

Apr

il 20

13

SHEILA PAGE

avoid such an aim. Realistically, it must be expected that the liberalisation whicheither makes to the other is likely to be extended to other partners, first, becausethe debates over sensitive products will have been fought in the first liberalisationand, second, because the costs of liberalisation to one trade partner are greaterthan multilateral liberalisation as a result of the risks of trade diversion, importingfrom a less efficient trading partner.

This assessment that the negotiations should be seen as parallel, not in com-petition, could have implications for the timing of negotiations. If both sides wantto ensure that negotiations are coordinated with other trading partners (EasternEurope and the renegotiation of Lome for the EU, or the FTAA for Mercosur), thenEU-Mercosur negotiations are likely to follow the same 2000-2005 rhythm envis-aged for the others. It is also likely that all the negotiations will be held back by de-lays in each. (For Mexico, in contrast, its negotiations with the US are alreadycomplete, so negotiations with the EU are "catching up".)

What are the main products of interest? Cars are a major trading commodityfor both sides, and remain subject to important tariffs (and controls) even withinMercosur. Other industries particularly important for EU exports are capital goods,including computing. EC calculations suggest that the major gains would be forthe EU ($6.5 billion compared to $1.5 billion for Mercosur18), thus a continuation ofthe trading trends of the last six years. Some of this would come from trade diver-sion from other suppliers. It seems doubtful whether this would be acceptable toMercosur (or, even more so, to its other trading partners).

Mercosur gains would come from agriculture, in particular cereals, meat,dairy products, vegetables and wine. These account for about 40 percent of Mer-cosur exports to the EU, and for all of the 14 percent considered sensitive. Somemight be excluded, under the assumed 10 percent allowed, but this would furtherrestrict the relative gains for Mercosur. A Brazilian calculation (in 1997), on theassumption that any agreement with either the EU or the FTAA would be withoutexclusions, found larger gains from an agreement with the EU than with the US,but this was entirely from gains on agricultural exports.19 The issue is important toboth Argentina and Brazil. It may be slightly less so to Chile: the official Chileanestimate is that sensitive agricultural products are only 7 percent of their exportsto the EU,20 but these are the same sensitive goods found in Mercosur exports (ce-reals, meat, fruit, and wine). It would be disruptive to the FTA between Chile andMercosur to have different lists of exclusions for a Chile-EU FTA and a Mercosur-EU FTA. The EU has made it clear that it sees the negotiations with Chile as paral-lel to those with Mercosur, so this would be unlikely to permit a more rapid settle-ment with Chile. For the EU, the same goods are of interest in its exports to Chile,but the incentive to seek an FTA is much less, with tariffs on cars at about 11

18 "Mercosur and the European Union: Dynamics and Prospects of a Developing Association". IRELABriefing, 19 February1999, IRELA, Madrid.

19 Report by Getulio Vargas Institute, 1997.20 IRELA, "Chile and the European Union".

105

Dow

nloa

ded

by [

The

Uni

vers

ity o

f B

ritis

h C

olum

bia]

at 0

9:46

27

Apr

il 20

13

THE RELATIONSHIP BETWEEN THE EU AND MERCOSUR

percent instead of the 40 percent in Mercosur. This again suggests that there willnot be a separate settlement with Chile.

In the EU, the opposition to an agreement with Mercosur (and to approving anegotiating mandate) comes from the traditional agricultural producers, Germanyand France, and for some products, Spain and Italy (thus including countrieswhich otherwise have long-term interests in the area). While the EU imports fromMercosur would be small, any changes in the CAP to accommodate liberalisationto them would need to be extended to other countries, so that it is likely that the im-pact on these sectors would be much greater than the specific Mercosur marketgains available to European producers of cars and other manufactures. For Mer-cosur, while the gains from an FTAA would be less, because of the smaller impor-tance of agriculture and the lower shares of trade, it may be easier to reachagreement on negotiations. The US and Mercosur have already agreed to work to-gether in the WTO Millennium Round against the EU agricultural policy.21

On many of the non-trade relations, there would need to be the same prelimi-nary fact-finding stage that the EU and Mercosur organised for trade. None is animportant issue between the EU and Mercosur (as intellectual property was in rela-tion to Asia or investment was in the US negotiations with Mexico), so they are likelyto follow trade negotiations, and proceed very much in parallel with multilateralprogress.

The financial pressures on Brazil could affect negotiations in two ways. In theshort term, they make an agreement more risky for the EU (if Mercosur is seen asan unstable, devaluing partner) but more desirable for Mercosur (the EU is a grow-ing market; signing would be an indication of international approval). On the otherhand, Brazil's international and fiscal weakness make the costs of negotiating tar-iff cuts seem even greater. But the more serious effects could be in the longerterm if the crisis weakened the internal Mercosur links. At the worst stages of thecrisis, Brazil took action to protect imports and promote exports which could dam-age the rest of Mercosur, and took it without consultation, although this was re-versed (in contrast, when Mexico faced crisis in 1994, it exempted from thebeginning the US and Canada from the import surcharges it imposed). Brazil's de-valuation, undertaken without any consultation of its Mercosur trading partners,jeopardised the trade balances of its partners, while the retaliatory controls takenby Argentina threatened the integrity of the customs union. These problems wereresolved in ad hoc ways, but they mark the third occasion in Mercosur's short his-tory on which a devaluation by Argentina or Brazil has had serious internal effects.Stability of the partners is particularly important within a region because depend-ence is increased and because the temporary import controls available amongnon-members of regions are no longer (officially) available. For Mexico's partnersin 1994, this was less important because US trade with Mexico is much lower than

21 Agence France Press, 12 April 1999.

i—i

106

Dow

nloa

ded

by [

The

Uni

vers

ity o

f B

ritis

h C

olum

bia]

at 0

9:46

27

Apr

il 20

13

SHEILA PAGE

Mercosur countries' with Brazil. For the EU, there were no comparable strains inits first eight years.

Conclusions

The immediate need for the EU is to convince Mercosur that it is as important to theEU as other trading partners: not more important, which would not be credible, butnot less important and to be neglected either because it is neither sufficiently poor(for the new aid criteria) nor sufficiently near (to be admitted to the enlargement). Itis difficult to see how this can be done in the short term through general trade nego-tiations. There is not a strong EU interest in improving access to Mercosur markets,and Mercosur's own evolution is likely to lower average tariffs in these. There are,however, strong EU interests in preventing or at least postponing liberalisation inagriculture. There are many pressures that are likely to prevail eventually on theCAP: the EU budget, enlargement, and WTO negotiations. These are likely to bemore important than any negotiations with Mercosur. Mercosur would do better tolet others achieve this, while it bargains on more attainable aims.

The perception in Mercosur that the EU is losing interest in Mercosur isprobably too pessimistic, however, and it should be possible to rebut it. Mercosuris not a major trading partner, but it is more important to the EU than many smallercountries in Africa, for example, and it has completed its economic restructuring(unlike the Asian countries which are undergoing it now). With minor exceptions, itis secure and politically stable. It is important to the EU that Mercosur not see theFTAA as the only trading alliance open to it, although it is equally important thatneither Mercosur nor EU see an EU-Mercosur agreement as an alternative to theFTAA: the arguments for (and against) are the same for both - an opening to a sig-nificant trading partner, but a risk in terms of economic and administrative costsfrom trade discrimination. The EU must be as active in promoting practical work-ing groups as the FTAA, but it would be wrong to discourage Mercosur from partici-pating in the FTAA.

Two very different types of "regionalism" must be distinguished. The deep in-tegration within the EU or Mercosur and probably very few others makes them takeover national roles, both within the region and in relations with the rest of theworld. The cooperation of an FTAA or an EU-Mercosur agreement, like the Asian-Pacific Economic Community (APEC) or the various FTAs among Latin Americancountries will be more casual: a coming together for a particular purpose, with noexpectation that it will be a permanent or exclusive alliance against the rest of theworld or lead to a deep integration. As the competence of multilateral organisa-tions extends (trade in manufactures in the 1940s; energy in the 1970s; trade inagriculture, services, the environment and intellectual property in the UruguayRound; investment, labour conditions and perhaps migration, and company law incurrent negotiations) these matters are gradually removed from the possibleagenda for casual regional arrangements. Like preference areas faced with "prefer-ence erosion", purely trading regions are progressively weakened, and they must <==>

107

Dow

nloa

ded

by [

The

Uni

vers

ity o

f B

ritis

h C

olum

bia]

at 0

9:46

27

Apr

il 20

13

THE RELATIONSHIP BETWEEN THE EU AND MERCOSUR

find new subjects for cooperation (the details of trade facilitation, for example).Mercosur is still developing regional (and even national) company law and

standards, as well as business practices. The EU has the experience of adaptingall members, which already have the same legal tradition, to a common regime.Developing cooperation with Mercosur on this could both help Mercosur's owndevelopment and integration and give a stimulus to EU-Mercosur trade and invest-ment.

The type of regular consultation found in the OECD or in APEC will not lead toa regional group that acts together, but it will permit ideas to be advanced or differ-ences defused less formally than in the WTO. The WTO's achievements of universalcoverage and formal rules and dispute procedures are not always advantages inreaching rapid solutions. If the EU is to continue with its habit of emphasisingbilateral arrangements to supplement the multilateral, then Mercosur must be in-cluded. For Mercosur,.the EU also has a role as a balancing relationship, to keepit from becoming too dependent on the US.

Both Mercosur and the EU must also consider how to act as regions in themultilateral frameworks. The WTO has admitted the EU as a member: should thisbe the precedent for Mercosur? There is an urgent need to find a way for the WTOto deal with the fact that negotiations will be among different types of "customsareas", and Europe's common currency and Mercosur's almost-common financialcrisis suggest that international financial organisations also need to recognise therole of regions more formally. Mercosur and the EU, which are not only customsunions but have negotiated FTAs with others, also have a role in determining howFTAs should be treated.

In their relations with each other, the most important progress that Merco-sur and the EU are likely to make is in useful, but unglamorous areas of tradecooperation and administration. Trying to secure a more visionary approach byaiming for an FTA could be taking things too far beyond what economic interestscan support between areas which do not have the strong ties to each other thateach has with its members. If a broader approach is desirable, it may be easierto define at the international level, with the two major customs unions rethinkingthe world economic structure.

108

Dow

nloa

ded

by [

The

Uni

vers

ity o

f B

ritis

h C

olum

bia]

at 0

9:46

27

Apr

il 20

13