the reform process and regulatory commissions in the ... · prayas-focus event on power sector...

TRANSCRIPT

Prayas-Focus Event on Power Sector Reforms

1

The Reform Process and Regulatory Commissionsin the Electricity Sector:

Developments in Different States of India

A Compilation of Selected Papers and Presentationsmade during the

‘Event on the Power Sector Reforms’organized by

Prayas and Focus on the Global South

[December 2000, Mumbai, India]

Prayas-Focus Event on Power Sector Reforms

2

The Reform Process and Regulatory Commissionsin the Electricity Sector:

Developments in Different States of India

Contents

Introduction

Part I: Papers on State Reform Processes

Maharashtra Prayas Energy Group

Andhra Pradesh Dr. M. Thimma Reddy

Orissa Ms. Sudha Mahalingam

Harayana Dr. Surinder Kumar

Kerala Mr. Abey George, Mr. K. Ramachandran

Uttar Pradesh Dr. Rahul Pandey

Phillipines Ms. Jenina Joy Chavez

Part II: Presentations during Consultation and Panel Discussion

Prof. A. K. N. Reddy Former President, International Energy Initiative

Dr. Madhav Godbole Former Home Secretary, Government of India andChairman, Energy Review Committee (GoM)

Mr. P. Subramaniam Chairman, Maharashtra Electricity RegulatoryCommission

Mr. Venkat Chary Member, Maharashtra Electricity RegulatoryCommission

Mr.Sanjeev Ahluvalia Former Secretary, Central Electricity RegulatoryCommission

Prayas-Focus Event on Power Sector Reforms

3

Introduction

The Indian power sector has been in the limelight since the reforms and restructuring of this sector beganin earnest in the latter half of 1990s. The reforms in the sector have gradually become the issue ofacrimonious debate in the academic, policy, and political circles. After the strike by employees of theUttar Pradesh State Electricity Board (UPSEB) in March 2000 and stalling of sector reforms (mainlyprivatization) in Haryana, the theatre of action shifted to the southern part of the country. In AndhraPradesh, electricity tariff hike and, hence, power sector reforms have become major issues even in themainstream electoral politics resulting in widespread political turmoil and even loss of life. InMaharashtra, after the five-day long strike in July 2000, trade unions of the employees of MaharashtraState Electricity Board (MSEB) were successful in eliciting a promise that the state government wouldnot privatize the state electricity board (SEB) and would consult the unions before unbundling.

The ongoing reforms involve fundamental legal, governance and ownership changes in the sector, withlong-term and, at time, irreversible implications. The reforms have engendered the independentregulatory commissions, which constitute a new institutional structure. This new institution is evolvedwith a view to ensure that the privatized power sector utilities do not take undue advantage of themonopoly over the sector and to ensure that the sector is able to meet the stated goal of supplying goodquality electricity at reasonable tariff. The regulatory commissions have been established in many states.In several states, the regulatory process has picked up speed with the commissions issuing tariff orders,releasing discussion papers, and deliberating on the other important issues such as capacity addition andstandards of consumer service.

This situation requires intense and urgent efforts on the part of the public-interest organizations to takeup challenges thrown up by the reform process in general and the regulatory processes in particular.Many individuals and organizations working for protection of public interest have been striving to takeup these challenges and are engaged in analysis, political as well as legal actions, and regulatoryinterventions. However, these individuals and organizations do suffer from paucity of information,analytical as well as legal skills, and human as well as financial resources. Hence, in response to theincreased pace of the reform and regulatory processes, it is necessary that these individuals andorganizations should come together, share experiences, and learn from each other. It must, however, beremembered that there is considerable diversity in the functioning of the state regulatory commissionsand even in the techno-economic, political, institutional, and historical contexts in different states.

Against this background, Prayas, in collaboration with Focus on Global South organized an event inorder to initiate a process of dialogue and, sharing of experiences among the individuals andorganizations working or planning to work for protection of public interest in the context of power sectorreforms and regulatory process. The event took place during 6th to 9th December 2000 at Mumbai.

Prayas (Energy Group), based in Pune, has been working in the electricity sector on activities includingresearch, information dissemination, policy activism, and regulatory intervention. Established in 1995,Focus on the Global South, based in Thailand is dedicated to regional and global policy analysis, micro-macro issues linking and advocacy. The India program of Focus (established in 1996) has beenundertaking studies, capacity building activities and facilitating dialogues amongst people’sorganizations, trade unions, and grassroots groups on specific issues falling under the realm ofliberalization, privatization and globalization.

The focus of deliberations during the four-day event was on reforms/restructuring processes in the statepower sectors with a special emphasis on the regulatory processes in the states. The main objectiveunderlying the event was to provide an opportunity to the participants to share experiences and to learnfrom each other on strategic as well as substantive issues.

The four-day event was divided in the five major components. The first component of the event was the‘Training Seminar’ lasting for about one and half days. In the ‘Training Seminar,’ along with thehistorical review of the Indian electricity sector, basic topics on techno-economic, legal, and institutionalaspects of the reform and regulatory processes were covered. The second component of the program,

Prayas-Focus Event on Power Sector Reforms

4

lasting for another day and the half, was entirely devoted to the invited presentations on updates andanalysis of the state-level processes. The third component of the event that took place on evening of thethird day was devoted to strategizing and planning for future activities.

The fourth component involved consultation on the topic “Sharing of Concerns and Expectationsbetween Regulators and Civil Society Institutions”. This was attended by Dr. Madhav Godbole (formerHome Secretary, Government of India), Mr. Venkat Chary (Member, Maharashtra Electricity RegulatoryCommission), Mr. Phillipose Matthai (Chairman, Karnataka Electricity Regulatory Commission), andMr. Sanjeev Ahluvalia (then Secretary, Central Electricity Regulatory Commission). The consultationwas chaired by Prof. AKN Reddy (former President, International Energy Initiative). The last componentwas the panel discussion on the topic “Electricity Sector: What Difference the Regulators can make?”which was open to public. The panelist included Prof. Reddy, Mr. Matthai, Mr. Ahluvalia and Mr. PSubrahmanyam (Chairman, Maharashtra Electricity Regulatory Commission). Dr. Godbole chaired thediscussion.

The invited presentations on the analysis of reform process in each state were the mainstay of the event,which sparked off intense discussions. In all, twelve presentations were made on the basis of analysis ofreform process in eleven states. In addition, an analytical note was circulated to participants on thereform process in Punjab. Further Ms. Jenina Joy Chavez-Malaluan of Focus on Global South presenteda similar case-study on the electricity sector reforms in Philippines.

In order to facilitate the comparison among the states and the process of drawing conclusions, thespeakers were requested to follow a common pre-decided framework in their presentations. Thesepresentations covered the broad contours of the reform/regulatory processes in the state, actions ofgovernments and regulators, responses of other players and the lessons the public interest organizationscould learn.

This volume is a compilation of selected papers presented during the event. The first part of the volumecontains papers discussing the reform process in six states namely Orissa, Andhra Pradesh, Harayana,Uttar Pradesh, Kerala, and Maharashtra. In the case of Kerala, excerpts from two presentations arepresented in this volume. It also contains a paper on electricity sector reforms in Philippines. Part II ofthe compilation contains presentations, remarks, and observations by some of the regulators and panelistswho attended the last two sessions. It was felt that these observations would provide deeper insights inthe subject under deliberations. The annexures contain the other details of the event including the list ofparticipants.

We wish to take this opportunity to thank all the participants in the four-day event including theregulators, panelists and chairmen of the sessions on the last day. We are especially thankful to thoseparticipants who patiently cooperated with us in revising their papers. We also wish to sincerelyapologize for the delay in coming out with compilations. We are sure that, despite this delay, thiscompilation would be useful to researchers, activists, media-persons, academics, and members of public.

Sincerely yours,

Minar Pimple Subodh Wagle(for Focus on Global South) (for Prayas Energy Group)

Prayas-Focus Event on Power Sector Reforms

5

Electricity Reforms in Maharashtra: An Analytical Overview

Prayas Energy Group

1. History of Power Sector in Maharashtra

1.1. A mix of ownership structures and retail competition since four decades

Maharashtra State Electricity Board (MSEB) was established in 1961. It soon acquired(after expiry of licenses) many small private power companies in the state. Since then,MSEB has monopoly over the generation, transmission, and distribution of electricityin the state except the Mumbai metropolitan region. Mumbai is served by three utilities,viz., Bombay Electricity Supply and Transport (BEST), Bombay Suburban ElectricitySupply (BSES) Ltd., and Tata Electric Companies Ltd. (TEC). BEST is MumbaiMunicipal Corporation’s undertaking and has a license to distribute power to a part ofthe city of Mumbai. BSES is a public limited company in which Reliance group has ashareholding of around 30% while financial institutions such as LIC, UTI, and GeneralInsurance Corporation hold around 37% equity. BSES distributes power to suburbanarea of Mumbai and also owns and operates a 500 MW coal thermal power plant. TECis a TATA group company supplying power to BEST and BSES from its 1774 MWpower plants. TEC also purchases power from MSEB to supplement its own generationfor meeting Mumbai's demand. Apart from this, TEC's license also allows it to sellpower directly to consumers in the areas licensed to BEST and BSES, provided thedemand is above 1 MW. Before BSES's plant at Dahanu came online in 1995, TEC'scapacity was being fully utilized. TEC has only recently started actively seekingconsumers from service areas of BEST and BSES. “Mula Pravara Electric Co-operativeSociety” is the only co-operative electricity distribution utility in the state. “MulaPravara” serves nearly 200 villages in Ahmadnagar district. Thus, it can be seen thatMaharashtra has a mix of different patterns of utility ownership and retail competitionin the Mumbai area since four decades. Table 1 lists some salient features of these fiveutilities to indicate the relative scale of operation.

Table 1: Salient Features of Power Utilities in Maharashtra

S r . No.

Parameter MSEB TEC BSES BEST M u l a -Pravara

1. Installed GenerationCapacity (MW)

9,096 # 1,774 500 Nil Nil

2. No. of consumers 1.3 Cr. 300 lakh 20.6 lakh 8.4 lakh 1.3 lakh3. Sales (MU) 42,000 9,000 5,415 3,000 4803. Annual revenue (Cr.) 14,500 ~ 2500 2,158 1,400 454. Service area (sq. km.) 3,08,000 438 384 78 1,880

Notes:1. Cr.=crores=10 million & lakh = 100,0001.2. Numbers given above are approximate.2.3. TEC sales includes sales to BSES and BEST

Prayas-Focus Event on Power Sector Reforms

6

3.4. # Apart from this MSEB, also has a share of around 1800 MW from central sectorgeneration such as NTPC and Nuclear Power Corporation. Additionally, DabholPower Company has commissioned Phase I of 728 MW and Phase II of 1444 MW.

1.2 Remarkable growth in physical infrastructure

Since its creation in 1961, MSEB has made remarkable progress in terms of expandingthe physical infrastructure. In terms of installed capacity and revenue, it is the largestelectricity board in the country. MSEB achieved 100% village electrification (~ 40,000villages) in 19891 and serves nearly 22 lakh agricultural consumers. In domestic,commercial, and industrial categories of consumers, around 65% consumption is fromurban areas. Commensurate with the national-level power policies and like many otherstates, this growth in physical infrastructure was facilitated by four major policychoices, which are briefly described below.

i.) Self-reliance and import substitution: In order to build national capability and toavoid dependence on imported equipment and fuel, emphasis was given ondevelopment of coal-thermal and hydro power stations.

ii.) Budgetary Support: The power sector is a highly capital-intensive sector,requiring huge investment with very long repayment horizons of around 10-15 years.To address such needs of the power sector, both central and state governmentsallocated significant portions of the plan expenditure for development of the powersector. Fox example, in 1980-81 annual plan, nearly 34% of the plan outlay wasearmarked for power sector. The governments provided this capital to the SEBs onconcessional interest rate with long repayment period2.

iii.) Centralized supply and grid expansion: Power sector relied almost exclusively onexpansion of centralized grid system for village electrification and on large centralizedgeneration schemes such as Chandrapur (2340 MW), Koradi (1110 MW), and Koyna(1920 MW).

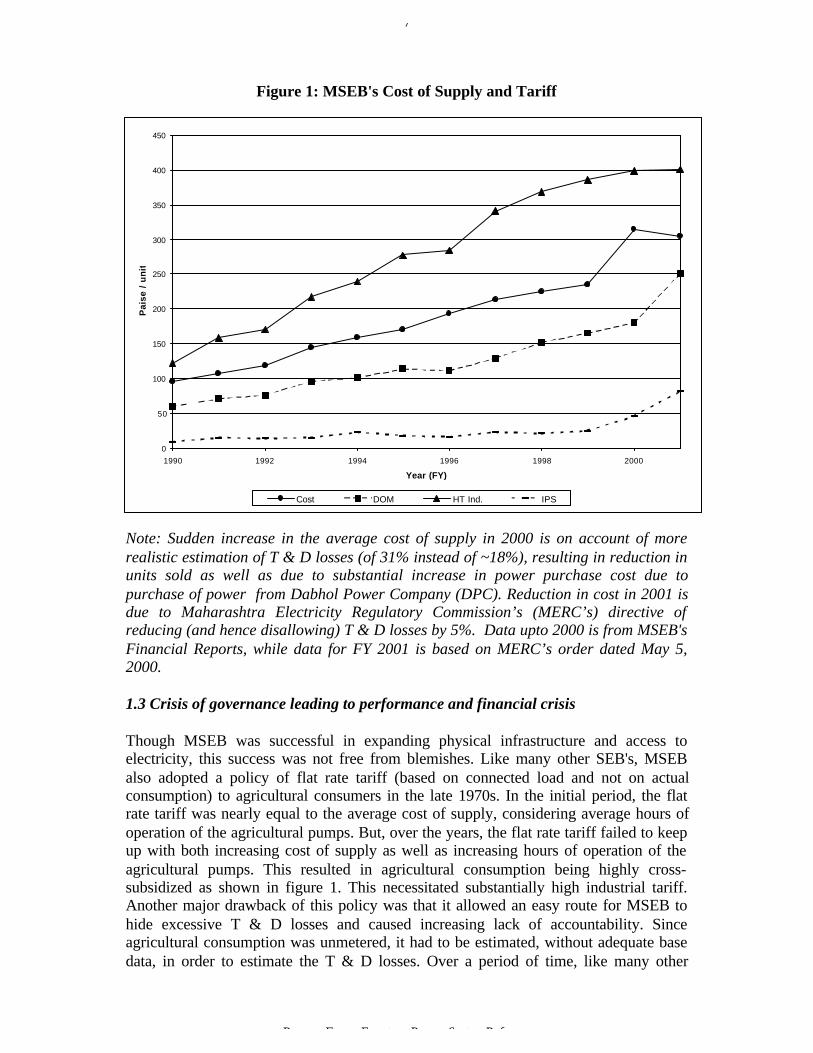

iv.) Cross-subsidy: Realizing that many poor households and farmers cannot afford topay full cost of electricity and remaining in line with the mainstream political thinkingat that time, the government adopted a policy of cross-subsidy. This involved chargingindustrial and commercial consumers more than the cost of supply and chargingdomestic and agricultural consumers lower than the cost of supply. Figure 1 shows thetariff of three major categories as well as the average cost of supply, i.e., total revenue(amounts billed) divided by total sales.

1 Similar to the other states, MSEB also declares a village "electrified" even if it manages tosupply power to just one household or one street light in the village. Some of these villages areconsidered electrified even if there are few solar PV based streetlights. As a result, even thoughMaharashtra has achieved 100% village electrification, actual household electrification is justabout one-third.2 Since 1991, budgetary support is also becoming as expensive as commercial loans with highinterest rates.

Prayas-Focus Event on Power Sector Reforms

7

Figure 1: MSEB's Cost of Supply and Tariff

Note: Sudden increase in the average cost of supply in 2000 is on account of morerealistic estimation of T & D losses (of 31% instead of ~18%), resulting in reduction inunits sold as well as due to substantial increase in power purchase cost due topurchase of power from Dabhol Power Company (DPC). Reduction in cost in 2001 isdue to Maharashtra Electricity Regulatory Commission’s (MERC’s) directive ofreducing (and hence disallowing) T & D losses by 5%. Data upto 2000 is from MSEB'sFinancial Reports, while data for FY 2001 is based on MERC’s order dated May 5,2000.

1.3 Crisis of governance leading to performance and financial crisis

Though MSEB was successful in expanding physical infrastructure and access toelectricity, this success was not free from blemishes. Like many other SEB's, MSEBalso adopted a policy of flat rate tariff (based on connected load and not on actualconsumption) to agricultural consumers in the late 1970s. In the initial period, the flatrate tariff was nearly equal to the average cost of supply, considering average hours ofoperation of the agricultural pumps. But, over the years, the flat rate tariff failed to keepup with both increasing cost of supply as well as increasing hours of operation of theagricultural pumps. This resulted in agricultural consumption being highly cross-subsidized as shown in figure 1. This necessitated substantially high industrial tariff.Another major drawback of this policy was that it allowed an easy route for MSEB tohide excessive T & D losses and caused increasing lack of accountability. Sinceagricultural consumption was unmetered, it had to be estimated, without adequate basedata, in order to estimate the T & D losses. Over a period of time, like many other

0

50

100

150

200

250

300

350

400

450

1990 1992 1994 1996 1998 2000

Year (FY)

Pai

se /

un

it

Cost DOM HT Ind. IPS

Prayas-Focus Event on Power Sector Reforms

8

SEB's, MSEB also started overestimating the agricultural consumption to show"reasonable" figures for T & D losses. Figure 2 shows how, in spite of substantialgrowth in T & D network and rural electrification, MSEB managed to show nearlysame percentage of T & D losses, year after year, while showing rapid increase inagricultural consumption.

Figure 2: Increasing Un-metered Energy and Inflated Agricultural Consumption

This route of hiding excessive T & D losses helped many quarters. MSEB officialscould, on one hand, absolve their responsibility of preventing theft and excessive T &D losses and, on the other hand, could brag about growing agricultural consumption asa symbol of its "social commitment", politicians could patronize constituencies byclaiming highly subsidized agricultural tariff and growing agricultural consumption,agricultural consumers also benefited from this policy as they had become used to apre-defined power tariff not linked to consumption. As a result of this "arrangement ofconvenience" for a array of influential actors, increase in theft of power and technical(T & D) losses was ignored and continued to be camouflaged under the agriculturalconsumption. As indicated by the last year’s data in Figure 2, the real agriculturalconsumption was far lower than claimed3. Speaking in the gross terms, these excessiveT & D losses and theft of power amounted to nearly Rs. 2500 Cr. This loss waspartially funded by higher tariff to industrial and commercial consumers and partly byway of government subsidy to MSEB.

Though excessive T & D losses and theft of power form the most significant parts ofoverall inefficiency in MSEB, they are not the only ones. There are several other areaswhere MSEB's performance could be improved. For example, during the first tariffrevision case before MERC, MSEB claimed that, though the availability of its thermalpower plants was about 85%, it could not generate full power due to poor quality of 3 As explained in section on regulatory process the real level of T & D loses and agriculturalconsumption was exposed during the first tariff revision process for the year 1999-2000.

Composition of Un-metered Energy

0%

10%

20%

30%

40%

50%

1975 1980 1985 1990 1995 2000

% o

f Ene

rgy

Ava

ilabl

e

T&D loss Agri. Unmetered Share

Prayas-Focus Event on Power Sector Reforms

9

coal and claimed that the loss of generation capacity on this account was about 670MW. Similarly, nearly 500 MW (out of 920 MW) of MSEB's gas station at Uran couldnot be effectively utilized due to unavailability of gas. MSEB's performance in terms ofbilling and metering is equally dismal. During the tariff revision process, it wasrevealed that even for consumers from domestic, commercial, and industrial categories(which have been metered), around 50% bills issued are not based on the actualconsumption due to reasons such as faulty meters and average billing or minimumconsumption bills. The other areas where MSEB's performance needs to be improvedsubstantially are quality of electricity supplied and service to consumers. However, inthe absence of adequate studies and proper data, these aspects cannot be elaborated.Table 2 shows MSEB's performance for the last decade.

Table 2: MSEB's Sales and Revenue

Year < - - - - - Sales (MU) - - - - - - - - --- > < - Revenue (Rs. Cr.)- >Domestic Total TotalHT

I n d u -stry

Agric-ulture

Sale ofPower

Government.Subs--idy

R a t e ofReturn%

1990 2594 9050 5950 26973 2249 272 25871991 2839 9706 6404 27958 2923 0 2995 2.61992 3148 9746 8177 30472 3336 199 3626 3.01993 3549 10083 7839 30962 4343 0 4484 5.21994 3772 10771 8703 34562 5244 0.01 5464 4.81995 3962 11671 11453 37763 6151 0.03 6444 4.71996 4424 12776 13332 41619 7115 630 8016 4.51997 4897 12856 13867 42698 8573 258 9074 4.51998 5341 12635 15382 43894 9242 305 9829 4.51999 5915 12622 15968 46327 10121 355 10891 4.52000 6454 12756 10293 41981 10625 2084 13215 4.5Note: Rate of return is the return on net fixed assets in use.

2. Status of Independent Power Producers (IPPs) in Maharashtra

2.1 Reliance’s Patalganga Project

In the mid 1990s, MSEB signed Power Purchase Agreements (PPAs) with three majorindependent (private) power producers (or IPPs). In 1990, MSEB had invitedcompetitive bids for two power stations, viz., Khaperkheda Coal-Thermal (420 MW)and Nagothane Gas-Thermal (820 MW). After several changes in the locations andcapacity of the plants and deliberations by committees, MSEB finally signed a PPAwith Reliance Patalganga Power Ltd. in 1996 for a power station at Patalganga withcapacity of 447 MW. Though the process of inviting bids was initiated before theGovernment of India (GoI) opened up the power generation sector for privateinvestments, tariff of this project is on the lines of GoI tariff guidelines announced in1991. The project will use natural gas (to be diverted from MSEB's share of natural gasfrom Bombay High) and naphtha as fuels. Subsequently, the PPA was amended in

Prayas-Focus Event on Power Sector Reforms

10

February 2000. This was done after the establishment of MERC, but without MERC'sprior approval. The Government of Maharashtra (GoM) approved allocation of “escrowcover” for the project in early 2001. Prayas filed a petition before MERC, raising thisissue and requesting MERC to declare this amendment in the agreement as null andvoid. Mr. Prakash Hogade of Janata Dal (Secular) had also filed a petition regardingthis issue apart from the other issues such as load shedding. In response to this petition,MERC directed that MSEB need to take a prior approval for any PPA or foramendments to the same and declared that the said agreement was of "doubtful legalvalidity". As a result of this order by MERC (dated 17th May 2001), ReliancePatalganga Power and MSEB will have to approach MERC and get its approval for thePPA amendments. As per the techno-economic clearance (dated 22nd January 1998)from Central Electricity Authority (CEA), the approved capital cost of the project is US$ 320 million plus Rs. 246 Cr.. Apart from a small controversy regarding diverting ofMSEB's share of gas for this project, there is no major controversy or litigationsurrounding this project as yet, mainly due to relatively (compared to Enron project)small size of the project and very initial stage of development.

2.2 Bhadrawati Project

MSEB signed with M/S Central India Power Company (an IPP promoted by the Ispatgroup) a MoU in 1993 and a PPA in 1998. This is a coal-based project with a capacityof 1082 MW and located near Bhadrawati in Chandrapur district. This is one of theeight power projects that were granted the ‘fast-track’ status as well as the counter-guarantees’ by the central government. Though the project secured CEA's techno-economic clearance in 1994 (with a capital cost of Rs. 5187 Cr.), it has not movedmuch beyond the planning stage. This project is marred by several controversies mainlyrelating to fuel supply and cost. The project will use coal mined from a nearby captivemine to be owned and operated by a sister company. There were several allegations andcourt cases on the issue of coal cost. Similarly, it was suggested that the proposedproject would pose threat to national security as the proposed captive mine was close toone ordnance depot. Last year, Electricite de France (EDF) withdrew from the projectdue to delays and due to the unresolved issues relating to coal supply, cost, and theescrow cover. After the report of Energy Review Committee (Godbole Committee),considering the changed demand-supply situation as well as learning from the Enronepisode, the GoM has decided to keep the project on hold. Also, due to several changesand delays in finalizing various contracts, it is expected that the PPA will have to beamended, which would require approval of MERC.

2.3 Enron's DPC project

The power project of Dabhol Power Company promoted by Enron Corporation is oneof the most controversial IPP projects in the country. In response to GoI's decision toopen power generation for foreign private companies and following a visit by a high-level GoI delegation to Houston, USA, Enron Corporation decided to set up a powerproject based on imported LNG of capacity of around 2000 MW. In 1993, it signed aPPA with MSEB. As per the PPA, the project was to come up in two phases, the firstphase was of 695 MW and second phase was of 1255 MW. As envisaged in the PPAsigned in 1993, the first phase would run on liquid fuel (either distillate or naphtha) and

Prayas-Focus Event on Power Sector Reforms

11

the second phase (to be run on imported LNG) was optional, i.e., was not binding onMSEB and a Go / No-Go decision could be taken in future without any liability. Sincethe beginning, the project has been shrouded in many controversies on aspects such aslack of competitive bidding, high capital cost and tariff, and larger than neededcapacity. In 1995, the state government led by two part coalition of BJP and Shiv-Sena,which had opposed the project as one of the main election plank, came to power in thestate assembly. Immediately after forming the government, it appointed a committeeunder the chairmanship of then Deputy Chief Minister Mr. Gopinath Mundhe to reviewthe project and, based on recommendations of the committee, cancelled the project thathad purportedly attained financial closure in February 1995. In response to GoM'sdecision to repudiate the contract, Enron filed an arbitration claim in London followingthe provisions in the PPA. The state government also filed a suit in the Bombay HighCourt and alleged that the PPA was null and void on account of alleged corruptioninvolved. But, subsequently the Sena-BJP government did a somersault and appointedan "expert committee" to renegotiate the project. The terms of reference of thecommittee required it to negotiate both the phases of the project. The committeeworked with lightning speed and submitted its report within just 11 days, few daysahead of its term. Based on the report of the committee, the project was revived,making both phases as well as purchase of large quantity of LNG (take-or-pay contractequivalent to 90% PLF of the 2184 MW plant) binding on MSEB and stategovernment. The revised PPA was signed in 1996, which was again amended in 1998.The project being one of the eight ‘fast-track’ projects enjoys counter-guarantee fromthe central government (for Phase I) as well as the guarantee from the state governmentand “escrow cover”. The first phase of the project started production in May 1999 andopened eyes of the politicians and MSEB alike when bills started coming in. The costof Dabhol power is around Rs. 5 / kWh, with intermittent peak tariff of as much as Rs.7.80 / kWh in July 2000 due to the limited off-take by MSEB and high naphtha prices.

By this time, it had become clear that neither MSEB nor even the Maharashtra Statecould afford the Enron project. MSEB earns around Rs. 12,000 Cr. from its consumersAs against this, when Phase 2 of the project was scheduled to be commissioned in early2002, annual payments to DPC from MSEB would shoot to over Rs. 6,500 Cr., makingit simply impossible for MSEB to bear the burden. In this event, it was evident thateven the GoM, which has guaranteed the payments to DPC, would also not be able tobear such a large burden, year after year, due to the more precarious financial situationof the state.

This stark financial reality, on one hand, and the aggressive stand taken by someconstituents of the ruling coalition, viz., Democratic Front, the state governmentdecided to appoint a review committee under the chairmanship of Dr. MadhavGodbole. The committee submitted its report in April 2000. The report is highly criticalof the manner in which the project was negotiated and approved in 1993 as well as in1995. The committee also concluded that the project was not desirable for the state ofMaharashtra right from initial design in 1993. The committee concluded that the DPCproject would be unsustainable even if MSEB were to function in an efficient manner.The committee recommended several structural changes in the project such as:separating LNG facility and harbor from the project, drastic reduction in theprofitability of the promoters as well as in the interest rates of the loans extended by

Prayas-Focus Event on Power Sector Reforms

12

financial institutions supporting the project so as to reduce the tariff and make theproject viable.

The report of the committee revealed that, apart from the losses due to fundamentalfactors such as the need for project and reasonability of capital cost, MSEB could havesaved Rs. 930 Cr. per year only by negotiating in a better manner, the provisionsrelated to sharing of harbor and regasification costs, O & M costs, and heat rate. Thecommittee also pointed out several lacuna and shortcomings in the decision-makingprocess that led to the present state of affairs and observed that "This failure ofgovernance has been broad, across different governments at different points of time, atboth the state and the central level and across different agencies associated withexamining the project, and at both the administrative and political levels".

Two members of the committee, viz., Dr. Godbole and Dr. E.A.S. Sarma, alsorecommended institution of a judicial commission of inquiry to investigate the issueand to make those responsible for such "governance failure" accountable.Subsequently, the GOM has asked the same committee to conduct negotiations with theDPC on the lines of its own recommendations. Several rounds of negotiations betweenthe committee and DPC took place but the issue could not be resolved. The committeehas submitted its report on these negotiations to the state government, which is yet tobe made public. As per press reports, the committee has concluded that the DPC tariffshould not be more than Rs. 2.40 /unit. Considering that the tariff as per current PPAworks out to around Rs. 3.6 / unit, effectively the committee has concluded that areduction of around Rs. 2000 Cr./ yr. in payments to DPC is required and feasible. Atthe time of writing of this report, the Government of Maharashtra has announced that itwill institute such a Commission of Inquiry.

Alongside these developments, the MSEB also adopted aggressive legal stand towriggle out of this unsustainable liability. MSEB realized that the DPC plant wasunable to supply full power within three hours of start-up as promised in the projectreport submitted to CEA as well as in the PPA. MSEB, as per the provisions of thePPA, charged DPC a penalty of nearly Rs. 400 Cr. for one such instance. As expected,DPC rejected this claim and chose to invoke the international arbitration process as perthe provisions in the PPA. MSEB responded to this by filing a petition before theMERC claiming that MERC has the exclusive jurisdiction on resolving disputesbetween utilities following endorsement of the Electricity Regulatory Commission'sAct 1998 in October 2000 by GoM, which delegated powers of dispute resolution toMERC. In the meanwhile, MSEB also rescinded PPA by citing the issue ofmisdeclaration of plant's capabilities and has stopped purchasing power from DPC.DPC has obviously not accepted this claim. On MSEB's petition, MERC gave aninterim order and stopped DPC from proceeding further in the international arbitrationcase filed by DPC. DPC refused to accept MERC's jurisdiction on "dispute resolution"and filed an appeal in the Bombay High Court. The Bombay High Court ordered thatthe MERC should first hear the matter and decide on its jurisdiction. DPC appealed onthis order of the high court in the Supreme Court. The Supreme Court then directed theBombay High Court to decide on the issue of MERC's jurisdiction. During the hearingin the Supreme Court, apart from other legal issues, DPC also alleged that one memberof the MERC, viz., Mr. Jayant Deo had been biased against DPC. In support of these

Prayas-Focus Event on Power Sector Reforms

13

allegations, DPC quoted extensively from Mr. Deo's writings on DPC project in 1995-96 in his capacity as the Research Director of a consumer organization, ‘MumbaiGrahak Panchayat’. As things stand at the time of writing this report, the case ispending before the Bombay High Court on the issue of MERC's jurisdiction to arbitrateand resolve dispute between MSEB and DPC.

The Enron episode has highlighted the ruinous financial impact on MSEB because ofthe wrong contracts with IPPs. The Godbole committee also pointed out similar flawsin the design of other two IPPs in the state, viz., Reliance and Bhadrawati. As a resultof these developments, MSEB has decided not to pursue these projects at this stage.Also, both Reliance and Bhadrawati projects will have to approach MERC for seekingits approval for their PPAs before they can attain financial closure, which is a key pre-condition and a milestone for any IPP to start construction. It is expected that crucialissues such as need for power, the least-cost nature of these projects, and tariff of powerfrom the same will be debated in a transparent manner during the proceedings beforethe MERC.

Apart from these major IPPs, GoM / MSEB had initiated the process of contractingwith seven small IPPs (liquid fuel based) through competitive bidding in the mid1990's. Though promoters were selected, due to several constraints relating to fuelsupply and escrow agreements, the PPAs have not been signed and these projects arealso shelved in the current situation.

3. The Regulatory Process

In 1995-96, the financial situation of MSEB worsened and the government was forcedto provide a subsidy of Rs. 630 Cr. so as to enable MSEB to achieve the mandated rateof return of 4.5% of net fixed assets. Also the World Bank, which was providing a loanto MSEB under its “Second Maharashtra Power Project” threatened and later actuallypulled out of the project and declined to disburse the remaining amount. This was donein response to failure of MSEB and GoM to adhere to certain loan covenants such asachievement of a minimum of 4.5% return on net fixed assets, reduction in receivablesto the level of 2.5 months, and increasing agricultural tariff. These developmentsprompted the GoM to appoint an expert committee under the Chairmanship of Shri.V.G. Rajadhyaksha. Apart from several recommendations to improve the functioningof the MSEB, the committee also suggested an establishment of the state regulatorycommission. Like many other recommendations of the committee, thisrecommendation was also not followed by the government.

In September 1998, MSEB effected substantial tariff hike mainly for industrial andcommercial consumers. Some industrial associations filed a petition in the MumbaiHigh Court against this tariff increase. By the time this petition came up for hearing,the GoI had enacted the Electricity Regulatory Commissions Act 1998. This Actprovided for establishment of state regulatory commissions and articulated proceduresfor selection of the regulatory commissioners as well as functions and authorities of thecommissions. The decision of whether to establish the regulatory commission was leftto the discretion of the respective state governments. During the hearing on the petitionfiled by the industry associations, the High Court directed the GoM to establish the

Prayas-Focus Event on Power Sector Reforms

14

Maharashtra Electricity Regulatory Commission, however, the MERC was constitutedin August 1999. MERC is a three-member body consisting of two retired seniorgovernment officers (from the Indian Administrative Service or IAS) and one privatesector consultant.

3.1 First Tariff Revision Process before the MERC

Soon after MERC was established, MSEB filed a tariff revision application before it inNovember 1999 (Case 1 of 1999) based on the revenue requirement for the financialyear 1999-2000. In response to this, MERC issued a public notice inviting commentsand made available copies of MSEB's tariff proposal (at the price of Rs. 200/-) in theoffices of all Executive Engineers of MSEB across the state. The proposal submitted byMSEB was sketchy and lacked adequate data and information. In response, Prayas fileda separate petition before the MERC (Case 2 of 99) demanding that MERC shoulddirect MSEB to make available to public substantial quantity of more data andinformation on matters such as details of fuel cost, power purchase cost, and estimationof T &D loss and agricultural consumption. This petition also demonstrated that how,in the absence of this data, it was not possible for public or the MERC to justify andevaluate reasonableness of costs claimed by MSEB to the tune of Rs. 1900 Cr. Thiswas much more than the tariff increase of Rs. 1219 Cr. demanded by MSEB. Afterhearing the petition, MERC directed MSEB to make all data requested by Prayas to bemade public. MERC also directed MSEB to reply individually to each objectionreceived on the proposal. MERC held public hearings at the headquarters of all the sixrevenue divisions in the state. During the hearing, in addition to those who had filedaffidavits, other interested persons were also allowed to comment on the proposal afteradministering proper oath. After the public hearings were over, the Commissiondecided to hold "technical sessions" on MSEB's proposal. Citing MERC's conduct ofbusiness regulations, which stipulated that all proceedings before the commissionwould be public, Prayas requested the commission to allow consumer groups toparticipate in such sessions. The MERC accepted this suggestion and invited consumergroups to participate in these sessions. During the technical sessions, the proposal andadditional data submitted by MSEB, was scrutinized in detail. In this process, severalinconsistencies and shortcomings in the proposal were exposed and MSEB was forcedto modify the proposal as well as affidavits several times. At the end of this process, itbecame clear that the revenue shortfall claimed by MSEB (based on existing tariff) wasfar less than reality and in order to bridge the revenue gap far higher tariff increasewould be required. Apart from this, the original proposal had undergone substantialchanges on many other accounts, such as T & D losses, agricultural consumption, andsales to industrial consumers. Table 3 summarizes these changes.

Also, by this time, the financial year 1999-2000 was nearly over, as technical sessionsextended upto February 2000. Considering these aspects, the commission directedMSEB to submit revised proposal based on revenue requirement for the year 2000-01.The commission also directed the MSEB to take note of findings during the technicalsessions, which had indicated far higher T & D losses. Using the analysis of dataobtained from MSEB in Case 2 of 99 and its own previous work on agriculturalconsumption, during the technical sessions, Prayas was able to conclusively prove thatT & D loss figure of about 18 % as claimed by MSEB in its original proposal was

Prayas-Focus Event on Power Sector Reforms

15

highly understated and that the real T & D losses would be in the range of 28 to 33%.On suggestion from Prayas, MERC also directed MSEB to send revised proposal to allthose who had commented on the earlier proposal, i.e., to over 100 groups andindividuals. The rationale was that this was the same case and the need for revisedproposal had arisen mainly due to inconsistencies and shortcomings in the MSEB'soriginal proposal. MSEB submitted its revised tariff proposal for the FY 2000-01 andadmitted that T & D losses were 27%. In the new proposal, MSEB estimated that, atexisting tariff, the revenue shortfall would be Rs. 2018 Cr. and proposed an equivalenttariff increase. Considering that the process had extended over a long time, thecommission decided to hold public hearing only at Bombay. The commission finallycame out with the tariff order on 5th May 2000.

Table 3: Changes in the MSEB's Tariff Proposal During Technical Sessions

Item October 99 10th Feb2000

16th Feb2000

28th Feb 2000

Total revenue requirement 13,859 13,592 13,011 12,995Revenue at present tariff 12,640 12,486 10,912 11,206Revenue gap at present tariff 1,219 1,106 2,099 1,789Revenue at proposed tariff 13,859 13,592 11,972 12,344

Revenue gap at proposedtariff

0 0 1,039 651

Connected load of Agri.pumps (LT Unmetered) HP

9,175,803 7,291,464 8,619,475 8,464,420

Connected load of Agri.pumps (HT Unmetered) HP

579,088 326,950 307,647 522,788

Number of power looms 373,718 631,108 631,108 631,108Assumed hours of operationof flat rate looms

2,598 3,650 3,650 3,650

Net power generation byMSEB plants

~ 42000 43,297 40,793 42,073

Power purchase MU 19,469 19,470 18,470 17,610HT industrial consumption 15,333 15,191 12,436 12,920

Notes:HT industrial consumption = HTP I + HTP II + HTP BP + HTP X (mines)

This order concluded that the T&D losses of MSEB (including theft) were 31%. Theorder gave a tariff hike amounting to revenue increase of about Rs 600 Cr. against thedemanded increase of Rs 2018 Cr.. It asked MSEB to generate additional revenue ofRs. 600 Cr. through reduction in T&D losses by 5%. It also asked MSEB to reduceexpenses by Rs. 256 Cr. for power purchase, and Rs. 69 Cr. for power generation.

There were many positive features in the order. The order asked MSEB to strictlyfollow “merit order dispatch” 4. It ordered that all the new connections would have to 4 Merit order dispatch implies generating power from lowest variable cost plants first and to useplants with highest variable cost minimal (after all low variable cost generation is exhausted).

Prayas-Focus Event on Power Sector Reforms

16

be metered and asked MSEB to evolve a master plan for metering in order to completemetering of all consumers within the next three years. MERC has plans to reviewperformance of MSEB on the key operational parameters, like metering plan. This wasa welcome step. The order also directed MSEB to introduce Time of the Day (TOD)tariff for industrial consumers giving incentive for load shift to off-peak period, it alsoincluded incentive for power factor improvement. The order gave a very stiff tariff hiketo agricultural consumers (60% immediately, followed by another 200% for the largeagricultural consumers, considering metered tariff and compulsory metering). TheCommission also expressed its intent to remove cross-subsidy within five years.

After the tariff order by MERC, MSEB as well as some consumers (mainlyagricultural) groups filed review petitions before the MERC. MSEB's main points forreview petition were plea for not to disallow transit loss of coal (around Rs. 150 Cr.),nearly halve the targets for T & D loss reduction, increase in thermal PLF andreduction in thermal heat rate. The main pleas from consumers were to reduce tariff,especially of large irrigation pumps owned by co-operative lift irrigation schemes.After similar process including public hearings, the commission virtually rejected allthese review applications and maintained earlier decisions.

3.2 Other major cases before the MERC

Apart from the tariff revision case, MERC has addressed several other major issues /cases. Table 4 shows the nature of cases filed before the MERC and petitioners.

Table 4: Petitions before the MERC

Party No. of Cases Name ofthe Party

Details

Utility 8Tariff 4 MSEB 1998, 00-01 *, FOCA *, Mula

CoopDispute 2 Tata-BSES, MSEB-DPC *PPAs 2 MSEB-Cogen PPAs *Govt 1 About SubsidyIndustry 12Own Tariff 7 Bulk discount, billing demandNTPC directSupply

4 Steel export industry

Supply conditions 1 With AGPNGOs 6Transparency 2 Prayas MSEB data, PPA documentsPPA invalidity 1 Prayas Reliance PPA being voidGovernment role 1 MGP Restraining governmentSupply conditions 1 AGP Challenging MSEB comm. CircularsMSEB efficiency 1 Individual Challenging MSEB plant dispatchPolitical Party 1PPA invalidity 1 JD (s) Reliance PPA being voidNote: Review petitions not included

Prayas-Focus Event on Power Sector Reforms

17

Soon after the tariff order, the GoM announced concession in tariff for agricultural andpower-loom consumers without assuring adequate compensation to MSEB for this lossof revenue. After consumer groups raised this issue in the Commission AdvisoryCommittee, the GoM approached MERC with a request to allow reduction in tariff andfiled an affidavit to provide MSEB around Rs. 800 Cr. to compensate the revenue loss.MERC agreed with this proposition and directed GoM to release the said amountbefore October 2001, i.e., before finalization of MSEB's accounts for FY 2000-01.

As mentioned in Section 2 above, the MERC ruled positively on the petition filed byPrayas as well as Shri. Hogade and declared PPA amendment between Reliance andMSEB of "doubtful legal validity".

Shri. Paranjape, former Director, Kalpakkam Atomic Power Station filed a case beforethe MERC alleging that the MSEB violated MERC's tariff order dated May 5, 2000which directed MSEB to purchase power from Enron strictly on the principle of "meritorder dispatch". Several hearings were held on this petition with the final hearing beingheld in April 2001. MERC has not issued its final order in this case as yet.

MERC has, after duly inviting public comments and conducting public hearing,approved MSEB's application for fuel and other costs adjustments (FOCA) formula.The other major cases pending before the MERC are dispute between TEC and BSESregarding stand-by charges, a tariff revision application by Mula-Pravara Co-operativeSociety, and MSEB's application for resolution of dispute between MSEB and DPC.Recently, MSEB approached MERC for approval of PPAs for several bagasse-basedco-generation plants. MSEB and project promoters claimed that they be allowed a tariffof Rs. 2.25 / unit (1995 level) with annual escalation of 5% as per GoM policy. MERCopined that GoM cannot give a "policy directive" specifying tariff, as the ERC Act1998 specifies that tariff determination is the exclusive domain of ERCs, and decidedto look into cost components of these projects. These cases are still in initial stage oftechnical validation and preliminary hearing. MERC plans to hold public hearingsbefore approval of the PPAs.

In October 2000, Prayas had filed a petition before the MERC with a view to enhancetransparency in the sector. Prayas requested MERC to obtain copies of severaldocuments (such as clearances and project construction, operation and maintenance andfinancing agreements of IPPs ) and to make the same available to consumers and otherpublic. As a result of this petition, MSEB has made several documents public withhitherto "confidential" information. This includes information / documents such ascomputer model of DPC's tariff calculation, evaluation report of the competitivebidding process through which Patalganga project was awarded to Reliance. But, due toDPC's claimed confidentiality, MSEB refused to make public the agreements related toproject construction and project financing. Prayas filed second petition objecting to thisnon-compliance. The final hearing on this petition was held on 18th July 2001. MERCgave its order on 31st July 2001 and, notwithstanding MSEB's claims of confidentiality(arising out of its contractual obligation under the PPA), directed MSEB to makeavailable all documents demanded by Prayas.

Prayas-Focus Event on Power Sector Reforms

18

3.3 Salient observations about the regulatory process in Maharashtra

In many other states, the regulatory commissions were created, as part of the overallreform package, usually under active coaxing from the World Bank (WB) or AsianDevelopment Bank (ADB). As against this, in Maharashtra, MERC was established inresponse to peoples’ initiative and without any external pressure related to the overallreform. In less than two years of its existence, MERC, through its regulatory process,has been instrumental in substantially improving the transparency and publicparticipation in the decision-making and regulation functions in the sector. This couldbe attributed to three major factors, viz., MERC's positive approach, absence ofexternal pressures, and strong public intervention. For example, in the last two years,access for public to data and information has substantially increased and severaldocuments and information are now easily accessible to public. This included data suchas detailed monthly bills from DPC, PPAs and related clearances and contracts of IPPs,MSEB's metering and billing performance, hourly demand, load shedding and plant-wise generation. In line with its ‘Conduct of Business Regulations’, MERC has ensuredthat all proceedings before it are "actually" public and all notices of MERC are sent toits registered consumer groups. This has allowed consumer groups and general publicto witness all proceedings before the commission.

Apart from these process-related gains, in terms of substantive issues, the regulatoryprocess has also proved useful. Maharashtra is perhaps the only state, where an attemptis being made to estimate real T & D losses, without pressures from the WB or ADB.The Reliance PPA amendment case and the directive to GoM for timely disbursementof subsidy to MSEB has also demonstrated that such regulatory process can helprestrain both private and government sectors, provided there is strong publicintervention.

Though these are the positive aspects of regulatory process in Maharashtra, within thepresent legal and institutional framework, several more things need to be done toensure sustained effectiveness of the regulatory process for protecting and promotingthe "public interest". In the Electricity Regulatory Commission's Act 1998, powers ofstate electricity regulatory commissions (SERCs) are spit in two sub-sections, 22.1 and22.2. Powers under section 22.1 are not discretionary and but governments have choiceof delegating powers under section 22.2 to the SERCs. GoM has still not delegated fullpowers under section 22.2 to MERC. As a result, the MERC still has no authority toapprove investments of utilities or licensing. Apart from this, another factor affectingefficacy of the MERC is the lack of adequate financial and human (technical and legal)resources. Till now, MERC has very few technical staff and no legal staff at all. Suchlack of crucial resources is likely to hamper MERC's ability to take proper decisions ina time-bound manner and affect the in-depth scrutiny of various techno-economic aswell as legal aspects. Though MERC's conduct of business regulations stipulate that allrecords of the commission are public, a proper public information system is yet toevolve. In order to operationalise various transparency and public participation relatedprinciples articulated in the law and regulations, it is essential to institute proper"information disclosure systems" which would facilitate easy access to regulatoryinformation. For example, if the MERC institutes a system of monthly newsletter,listing all proceedings before the MERC in that month (along with a summary of each

Prayas-Focus Event on Power Sector Reforms

19

hearing and list of documents / records available to the commission), then it would befar easier for public to access commission's records and participate in the process. Aweekly email newsgroup version of this newsletter can further shorten the time lag andimprove benefits.

Compared to other states, the public awareness in Maharashtra about the regulatoryprocess is much better. However, considering the complexity and scale of regulatoryprocess, it is essential to have sustained efforts for enhancing public awareness andcapabilities of the civil society groups to effectively participate in the process.

In terms of substantive issues, there are some major challenges before the regulatoryprocess. MERC, in its first tariff order in May 2000, declared its intention to remove allcross-subsidy within five years. How agricultural economy can cope with this change isa big question as for the last two decades, large infrastructure as well as cropping andirrigation practices have been developed on the assumption of continued supply ofcheap, unmetered electricity. In the absence of comprehensive approach aimed atpumping efficiency improvements and at gradual changes in cropping and irrigationpatterns and practices, it is likely that agricultural economy will suffer badly. Asanother outcome of attempts of rapid reduction in cross-subsidy, GoM might be forcedto bear the subsidy burden, resulting in just transferring burden of cross-subsidy fromelectricity consumers to taxpayers. Large T & D losses and the Enron imbroglio areother major issues that need to be resolved with out affecting public interest in theMaharashtra's power sector.

4. The Reform Process

As mentioned in Section 3, the GoM appointed a committee under the Chairmanship ofShri. V.G. Rajadhyaksha in 1995-96. Dr. Madhav Godbole, Pradip Shah (CRISIL), andShri. M.G. Varade (Ex. Director, MSEB) were other members of the committee. One ofthe major recommendations of this committee was to privatize distribution. Based onthis recommendation, the GoM initiated measures to privatize power distribution insome urban industrial areas adjacent to Mumbai. These actions and recommendationsof the Rajadhyaksha Committee resulted in strong protests from trade unions of MSEBemployees. The unions opposed any move towards privatization and demanded thatMSEB should be allowed to function with adequate autonomy. They also demanded a"code of conduct" to avoid government interference in MSEB's functioning. But theseprotests failed to change GoM's thinking in any significant way. It announced decisionto privatize distribution in the New Bombay area (predominantly urban, industrialarea). The ‘Infrastructure Leasing and Financial Services’ (IL & FS) was appointed forthe study of various aspects related to the formation of a joint venture companybetween MSEB, CIDCO (a nodal urban infrastructure authority for the region, ownedby GoM) and a private company. The GoM also assured MSEB unions, in the process,that it would consult unions before any final decision. IL & FS submitted its report inMarch 1999 and it was circulated to MSEB unions for their comments. However, in themeanwhile, elections for the Legislative Assembly in Maharashtra were held in 1999and a new coalition of Congress, Nationalist Congress and some other smaller partiescame to power. Apparently, this change in government and opposition from the MSEB

Prayas-Focus Event on Power Sector Reforms

20

unions resulted in putting this proposal on the back-burner and not much progress wasmade in this regards.

The second impetus for reform came in the mid-2000. During this period, the ChiefMinister (CM) and some of his cabinet colleagues went to US. During this visit, theyalso met the President and other officials of the World Bank. Immediately afterreturning from the US, the CM announced plans for power sector restructuring on theline of the Orissa Model, i.e., unbundling and privatization. GoM appointed‘Administrative Staff College of India’ (ASCI) to prepare a draft of reform Act, knownas Maharashtra Electricity Reform Bill 2000. This bill is very similar to reform Act ofAndhra Pradesh and Orissa. GoM’s decision to adopt the WB model of power sectorreforms resulted in strong protests. Over a dozen unions of MSEB went on indefinitestrike from July 25, 2000 with only one demand of canceling privatization. The strikereceived wide support from MSEB’s workers and engineers alike and over 95%workforce joined the strike. Though in terms of workers unity the strike was successful,striking workers were at the receiving end of the public wrath due to the large-scaledisruption in electricity supply and the resultant inconvenience to general public. Apartfrom MSEB unions, many organizations such as Prayas, and Akhil Bharatiya GrahakPanchayat also opposed government’s approach to power sector privatization. Afterfour days of strike, a compromise was struck between unions and government. Thecompromise agreement is peculiar. It is a Marathi agreement, reading that thegovernment would withdraw the proposed bill and new bill will be introduced afterapproval of unions, but in bracketed English it says “after consultation” with unions !The events during the strike revealed how MSEB and its workers have little credibilityin the public eye. One of the major shortcomings in the process was the failure ofunions to create public awareness about dangers of privatization and to demonstratetheir commitment to improve MSEB’s performance and consumer service. The revisedversion of the Bill (not materially different from the first version) was tabled in theAssembly in November 2000. But due to growing internal realization that untilcrushing liability of Enron is taken care of, reforms cannot move ahead as well as dueto the growing opposition to Enron project (which needed immediate remedial action),the government did not press for passing of the bill. Instead, the government announcedits decision to appoint an expert committee to review Enron Project.

After much delay and skirmishes over the Chairmanship of the Committee, theCommittee was finally appointed in February 2001 under the Chairmanship of Dr.Madhav Godbole. Other members of the committee were Dr. E.A.S. Sarma (formerHome Secretary, GoI), Mr. Deepak Parekh (Chairman, Infrastructure Development andFinance Corporation), Dr. R.K. Pachauri (Director, Tata Energy Research Institute),Mr. V. M. Lal (Energy Secretary, GoM) and Dr. Kirit Parikh (Professor Emirates,Indira Gandhi Institute of Development Research). After a controversy over Dr. KiritParikh's involvement in the earlier committee to renegotiate Enron project, he chose notto participate in the functioning of the committee citing his prior commitments. Apartfrom reviewing Enron and other IPPs in Maharashtra, the Terms of Reference of thecommittee also required the committee to make recommendations for reforming powersector in Maharashtra. This Part II of the committee’s report was submitted to thegovernment on July 11, 2001 and was made public subsequently. The committee hasrecommended unbundling and privatization of generation and distribution. As per the

Prayas-Focus Event on Power Sector Reforms

21

report, separate companies should be created for thermal and hydro generation plantsand nearly a dozen companies (equivalent to present zones of MSEB) should be createdfor distribution. The committee has outlined a time-line of five years for privatizationof distribution and seven years for that of thermal generation. It has furtherrecommended surcharge of one paise / unit for funding expenditure of the RegulatoryCommission. Because, currently, the issue of DPC is attracting full attention of policymakers as well as general public, there has been little debate or action on the report ofthis committee as yet.

5. Conclusion

Due to several reasons, developments of power sector in Maharashtra till now are muchdifferent than many other reforming states. Ruinous financial impacts as well as strongpublic opinion against the Enron project have forced MSEB / GoM to look for ways ofavoiding this crushing liability. Only legal and techno-economic innovations as well asstrong political will would succeed in relieving people of Maharashtra and other statestoo (as there are efforts to sell Enron power to other states) from the unwarranted andhigh-cost Enron power. The Enron experience has also resulted in rethinking aboutother IPPs in the state. Though a couple of attempts were made by the GoM in the lasttwo to three years, the privatization and unbundling have remained on paper. This wasdue to several factors such as, the large and unbearable burden of Enron PPA, strongopposition by unions and some public groups, and relatively better financial situation ofMSEB (in the pre-Enron period). The regulatory process in the state is also muchdifferent when compared to other states. Due to strong public intervention and sectoralexigencies, the MERC had to handle several important cases such as amendments toPPA, subsidy by government, tariff revision and merit order dispatch. The regulatoryprocess in the state has resulted in substantial improvement in the transparency andpublic participation but, at the same time, several further actions (e.g., operationalisingtransparency and civil society capability building) are needed to ensure that the processbecomes sustainable and effective in protecting and promoting “public interest” in thelong term. One of the major fallout of the Enron controversy has been lack of concertedefforts to improve the performance of MSEB. Fortunately, after appointment of thecurrent Chairman of MSEB, since November 2000, several steps have been initiated toimprove MSEB’s performance (such as design and implementation of proper energyaudit, management information systems, and strong drive for recovery of arrears andtheft reduction). These measures have started yielding some results in terms ofreduction in arrears and better estimation of theft and identification of high theft areas.Of course, the success of these efforts depend on co-operation of MSEB’s workers andengineers and strong public pressure to ensure that the top management of MSEB isgiven free hand to deal sternly with erring staff and consumers alike and is madeaccountable for performance of MSEB.

Documents and Web-sites Referred

MSEB's annual Administrative and Financial Reports

Report of the Energy Review Committee (Godbole Committee) - 2001

Prayas-Focus Event on Power Sector Reforms

22

Report of the Rajadhyaksha Committee - 1996

MERC's tariff order dated May 5, 2000

MSEB's tariff proposal before MERC in November 1999 and March 2000

www.mercindia.com

www.msebindia.com

www.bses.com

www.bestundertaking.com

www.tata.com

_________0_________

Prayas-Focus Event on Power Sector Reforms

23

Development in the Power Sector in Andhra Pradesh

M. Thimma Reddy,Convener, Peoples’ Monitoring Group on Electricity Regulation (PMGER)

Introduction

In a span of four decades since its inception in 1959 APSEB increased power generationcapacity by 36 times, power handled by 59 times, service connections by 40 times, andrevenue by 747 times. During this period APSEB achieved 100 per cent electrification oftowns and villages. 65 per cent of the hamlets, 85 percent of the backward classes coloniesand 92 per cent of the Scheduled Castes’ colonies are electrified.

Table 1: Power Position in Andhra Pradesh

Item 1959 1999Generation Capacity 200MW 7330MWPeak Demand 146MW 6480MWService Connections 2.7 lakhs (i.e., hundred thousands) 1.1 croreAgriculture Connections 18,000 18.85 lakhsPower supplied 686MU 40,574MUAnnual Revenue Rs. 6.6 crore Rs. 4932 crore

Source: Power Development in AP – 1998-99.

Financial Position of Andhra Pradesh State Electricity Board (APSEB)

Losses incurred by APSEB are shown as one of the main reasons for restructuring thepower sector in Andhra Pradesh. But these losses have surfaced only recently. Both thestate government and the World Bank concede this fact. In 1994-95 APSEB earned profitsof Rs.87.25 crores. But during the very next year, i.e., 1995 - 96 losses stood atRs.1244.68 crores. These losses climbed to Rs.1533.04 crores in 1996 - 97. One maywonder how losses of such magnitude surfaced so suddenly. According to the white paperpublished by the state government of AP on power sector in the past also the boardincurred losses but they were compensated by additional mobilisation of resources by thestate government. Additional resources worth Rs. 130.25 crores were mobilised in 1992 -93, and Rs. 275.25 crores were mobilised in 1993 - 94. In 1994 -95 the state governmenthas written off its equity of Rs. 944.11 crores in APSEB. After that, according to thegovernment, there is no other way of compensating losses incurred by the APSEB.

During the same period revenues of APSEB were moving up. Revenues increased fromRs. 1935.5 crores in 1992 -93 to Rs. 3007.87 crores in 1996 - 97. The revenues of theboard are not enough to cover the mounting costs. Fuel purchase, payments towardselectricity purchased from other electricity boards and interest payments are importantcomponents of the costs incurred by the APSEB. Because of rise in prices of petroleumproducts in recent times and difficulties encountered in production and transport of coalled to fuel cost escalation. In order to balance supply and demand of power in the state

Prayas-Focus Event on Power Sector Reforms

24

APSEB resorted to purchase of power from other boards. The cost on this count increasedfrom Rs. 591.66 crores in 1992 - 93 to Rs. 888.18 crores in 1996 - 97. Besides this,purchase price paid by the board is also above the national average. While the nationalaverage purchase price stood at 110.01 paise (i.e. one hundredth of a Rupee) per unit ofpower, APSEB paid 114.12 paise. On the debt front, in 1992 -93 APSEB paid Rs. 330.36crore towards interest payments, it increased to 1106.93 crores in 1996 - 97. This showsthat one third of the Board’s income is going to meet interest payments. At the end ofMarch 1996 the outstanding loans stood at Rs.4851.02 crores. Added to this, theincreasing burden of interest payments formed 20.31 per cent of the expenditure of theBoard. It increased to 32.23 per cent in 1996 -97.

Table 2: Financial Position of APSEB (Rs. Crores)

1992-93 1993-94 1994-95 1995-96 1996-97Provi’nal Estimate

1. Total Income 1935.50 2303.15 3220.44 2407.28 3007.862. Expenditure on Fuel 484.66 608.75 719.09 1000.94 1306.443. Expenditure on purchaseof power

591.46 742.75 940.29 954.68 888.18

4. Total expenditure 1542.69 1914.14 2597.39 2991.79 3433.975. Operational Income (1-4) 392.81 389.01 623.05 -584.51 -426.116. Interest Payments 313.36 302.02 535.80 660.17 1106.937. Net surplus / Deficit (5-7) 79.45 86.99 87.25 -1244.68 -1533.04

Source : Finances of APSEB. APSEB, June - 1996

Table 3: Distribution of Electricity (in MU)

Category 1 9 8 0 -81

1 9 9 0 -91

1 9 9 5 -96

1 9 9 6 -97

1 9 9 7 -98

1 9 9 8 -99

P o w e r Distributed

6915 20233 29457 32092 36358 38721

Industry Total 3363 7042 7798 8207 8595 8655% 8.63 34.80 26.47 25.57 23.64 22.35

Agriculture Total 915 6285 11399 7835 9336 9866% 13.23 31.06 38.70 24.41 25.67 25.48

Domestic Total 546 2079 3276 3801 4535 5090% 7.90 10.28 11.12 11.84 12.47 13.15

T&D Losses Total 1523 3978 5551 10281 12020 12312% 22.03 19.67 18.85 32.04 33.06 31.80

Source: Power Development in Andhra Pradesh - 1998-99.

APSEB and Agriculture Sector

Whenever the issue of losses crop up the government and APSEB officials point theiraccusing finger at the agriculture sector. They argue that because of the subsidies given tothe agriculture sector the Board has landed in losses. While the agriculture sector isconsuming more power than any other sector, it provides least proportion of revenues. The

Prayas-Focus Event on Power Sector Reforms

25

losses are mounting as power is being diverted from industrial sector to agriculture sector.In 1985 -86 while agriculture sector consumed 28.8 per cent of power distributed,industrial sector consumed 54.8 per cent. In 1994 -95 while power consumed by theagriculture sector increased to 47.8 per cent, that of the industrial sector declined to 29.1per cent. Subsidies to the agriculture sector cost Rs. 162.3 crores in 1985 -86. Thisincrease to Rs. 1626.8 crores in 1995 - 96. But the question is how far these figures arereliable. Power supplied to the agriculture sector is not metered. All the power supplied,after deducting the power consumed by industrial and household sectors is shown as beingconsumed by agriculture sector. But this includes losses in transmission and distribution,and also power theft. If these losses are taken in to account then the proportion of powerconsumed by the agriculture sector will be low, lower than 47.8 per cent. M. HariprasadRao estimated that the government overestimated the number of pump sets by 25 per cent,working hours (1620 hours) in an year by 33 per cent and power consumption by one 5HPmotor (4.55 units) by 20 per cent. Because of all these power consumed by the agriculturesector was shown to be two times more than its actual consumption (The Hindu,September, 5, 1997).

This overestimation of the agricultural consumption continued with the recent tariffhike exercise. According to the ‘Tariff Proposals for Retail Power Supply’ (pageNo.17) “ for the purpose of developing the ERC/ARR projections, APTRANSCO hasadopted an estimate of agricultural consumption of 1200 hours This calculation isbased on supply of power for six hours daily for 200 days in an year. But in actualexperience it never crossed five hours. APTRANSCO has taken 9,815 MU asagricultural consumption for the year 2000-01. Actually this would not be more than6600 MU. This means that more than 3200MU of power is wrongly attributed toagriculture. This fact is also conceded by APTRANSCO when it submitted beforeAPERC that its “sample was not representative and it is likely that the extrapolatedconsumption derived from such sample metering is on the higher side”(p.16).

According to the official white paper released in 1999, while cost per unit of power atLT end was about 201.84 paise in 1997-98 the electricity board received only 16.12paise from agriculture while supplying 9336MU of power; and as a result of it incurreda loss of Rs. 1,733.88 crore. But if we take 5398 MU as the actual consumption in theagricultural sector per unit income from this sector will be 28 paise and loss incurredwill be Rs 938.40 crore. Industrial and commercial consumers are cross subsidisingagricultural and domestic consumption. While the average cost of power supply is Rs.2.29 per unit the industrial consumers are paying about Rs 3.19 per unit andcommercial consumers are paying Rs 3.69 per unit. As a result of this additionalincome accruing to the board is about Rs 907.8 crore (Rs 778.02 crore from industryand Rs 129.79 crore from commercial). This amounts to Rs 31.4 crore effective subsidyprovided by the state government/APSEB. Even if we add subsidy of about Rs 163.25crore provided to domestic consumers the total subsidy will not cross Rs 200 crore.This show that subsidies to agriculture in particular are not the main cause of financialproblems because the losses on this account are more than compensated by surplusfrom the industrial and commercial consumers.

Transmission and Distribution (T&D) Losses: Fudged Figures

Prayas-Focus Event on Power Sector Reforms

26

While subsidy to agriculture is treated as villain, the T&D losses are escaping theattention it should have received. In fact effective addressing of this problem will solvethe problems of the power sector. A substantial proportion of T&D losses were shownas being consumed by the agriculture sector on the pretext that it being non-meteredsector it is difficult to measure its consumption properly. So after assuming a notionalquantity of T&D losses the remaining quantity is attributed to agriculture. From1982while T&D losses steadily declined as if showing improved efficiency in T&D,agricultural consumption was shown to be increasing, symbolising unbridledconsumption in the wake of heavily subsidised power supply. But truth was otherwise.There were technical limitations to such an increase in agriculture sector powerconsumption, which include limited hours of supply, poor quality of supply anddeclining water table. At the same time commercial losses signifying theft of powerwas spreading alarmingly. But from 1996-97 the year in which power sector reforms inAP began to take a firm shape T&D losses were shown to be suddenly increasing, to 32percent from 18.85 percent of the previous year. With the initiation of AP Power SectorRestructuring Programme extensive investments began to be made in transmission anddistribution. Since the onset of reforms in 1995 more than Rs. 2000 crore were spent onimproving transmission and distribution systems. Even then T&D losses instead ofdeclining are increasing. According to the Power Development in Andhra Pradesh1998-99 published by APSEB T&D losses during 1998-99 stood at 31.8%. In a writtenreply in Lok Sabha (i.e., the Parliament) on 17th April 2000 the minister for state forpower stated that T&D losses in AP are 31.76%. But for the same year according to theARR submitted by the APTRANSCO these losses were shown as 38.10%. This showsthat the figures are fudged to their convenience. Substantial proportions of these lossesare because of commercial losses/thefts. These could be and should be stopped withoutmuch investment. The Document released by the APERC “Issues in Tariff Philosophy”in October 1999 for public discussion has specifically mentioned, “APTRANSCO hasalready initiated programmes to alleviate these problems. Energy audit was conductedin October 1996 to assess a realistic level of non-metered agricultural consumption.Almost 7 lakhs of defective meters were replaced in 1997-98. Meter terminal coverswere sealed for majority of services. Investigation of energy theft has been intensifiedin the last two years, and bill collections at the LT level has increased to 91.8% in thelast year. All these measures have contributed to reduction of T&D losses and anincrease in revenue of APTRANSCO to a small extent” (page No.4). This means thatreducing these losses is within reach, provided will to achieve it is there.

Evolution of Reforms

It can be said that the reform process in AP started with the constitution of a high levelcommittee under the chairmanship of Hiten Bhaya to suggest reforms to be introduced inthe power sector. This committee was constituted in January 1995 and submitted its reportin June 1995. The important proposals made by the Hiten Bhaya committee include,fixing of tariff structure to cover production costs, to separate generation, transmission anddistribution activities and keep them in the hands of different companies, to keep thesecompanies as subsidiaries of APSEB, to run them on commercial lines, to privatise powerdistribution companies gradually, to retain the Board only as a holding company in chargeof long-term sector planning, supervision and co-ordination of the subsidiaries, monitoringof reform implementation and provision of policy advice to be with the government,

Prayas-Focus Event on Power Sector Reforms

27

setting up a regulatory commission to fix tariff structure, keeping licensing powers withthe state government.

The World Bank team which subsequently assessed the sector pointed out that though themeasures proposed by the Hiten Bhaya committee are in the right direction, they are notcomprehensive and need to be further developed. According to them some shortcomingsof the Hiten Bhaya committee are:

1. The proposal that ABSEB continue as a holding company for the new companieswould continue to expose APSEB and consequently its subsidiaries to politicalpressure, and the power sector would not be insulated from short-term politicalexpediencies. This would undermine the main objective of the reform programme.

2. The committee defines the role of the regulatory commission narrowly: to deal withretail tariffs. The responsibilities of the commission should be broadened to includeregulation of the bulk supply tariffs, distribution tariffs, and connection charges. Inaddition, the regulator should also grant licenses to all transmission and distributioncompanies and enforce them.

3. The committee recognised the need for new legislation only for the establishment ofthe regulating system. Unbundling APSEB and creating separate companies are majorchanges that could be achieved only through new legislation dealing also with transferof assets, staff and interests.

4. The committee’s recommendation that all power generating assets be transferred to asingle company that will also procure power from independent producers. This modelwould limit competition, reduce expected efficiency gains, and make the regulatorregime too complex to administer.

The only way out of the present predicaments in the power sector in the opinion of theWorld Bank team is to implement all encompassing reforms. Some important componentsof the reform proposed by the World Bank are:

1. Define a structure for the sector consistent with privatisation of distribution andprivate sector development in generation.

2. Corporatise the power utilities and ensure that they operate without governments’interference.

3. Create an independent and transparent regulatory system for the sector with broadrange of responsibilities including granting licenses and enforcing them.

4. Enact comprehensive reform legislation to establish the new regulatory frameworkand implement the restructuring measures.

5. Increase the tariff rate to agriculture to at least 50 paise/kWh in the near term.Continue to adjust tariffs to cover costs and reduce cross subsidies.

Prayas-Focus Event on Power Sector Reforms

28

The government of Andhra Pradesh released its power sector policy statement on June 14,1997. According to it the aims of the state government are: