“the price of lust : the case of ipo lawsuits against vc ... · pdf filethe case of ipo...

TRANSCRIPT

Doctoral Track and Conference

ENTREPRENEURSHIP, CULTURE, FINANCE AND ECONOMIC DEVELOPMENT

“The Price of Lust : The Case of IPO Lawsuits against VC-Backed Firms,” Mark D. Griffiths*, Jill R. Kickul** and Philip Drake*** * Prof. Mark D. Griffiths, Jack Anderson Professor of Finance, (Miami University, Farmer School of Business –USA) [email protected] ** Professor, Director Stewart Satter Program in Social Entrepreneurship, NYU – Stern School of Business [email protected]

THE PRICE OF LUST:THE CASE OF IPO LAWSUITS AGAINST VC-

BACKED FIRMS

Mark D. Griffiths, Ph.D.Jack Anderson Professor of Finance

Farmer School of BusinessMiami University

Jill R. Kickul, Ph.D., DirectorStewart Satter Program in

Social EntrepreneurshipNYU – Stern School of Business

Philip Drake, Ph.D.Arizona State University

Babson 2008Griffiths, Kickul & Drake

THE PRICE OF LUST . . .

“There are strange things done in the midnight sun

By the men who moil for gold;…”

The Cremation of Sam McGee

(Robert W. Service)

Babson 2008Griffiths, Kickul & Drake

Why SHOULD We Care?

The initial public offering is supposed to be the exit strategy for the VC Fund.

If the firm gets sued over the IPO, something went horribly wrong!

Are there differences between VC-backed and non-VC-backed sued IPOs?

Are there other characteristics that determine the likelihood of being sued?

What can we learn from the worst case scenario?

Babson 2008Griffiths, Kickul & Drake

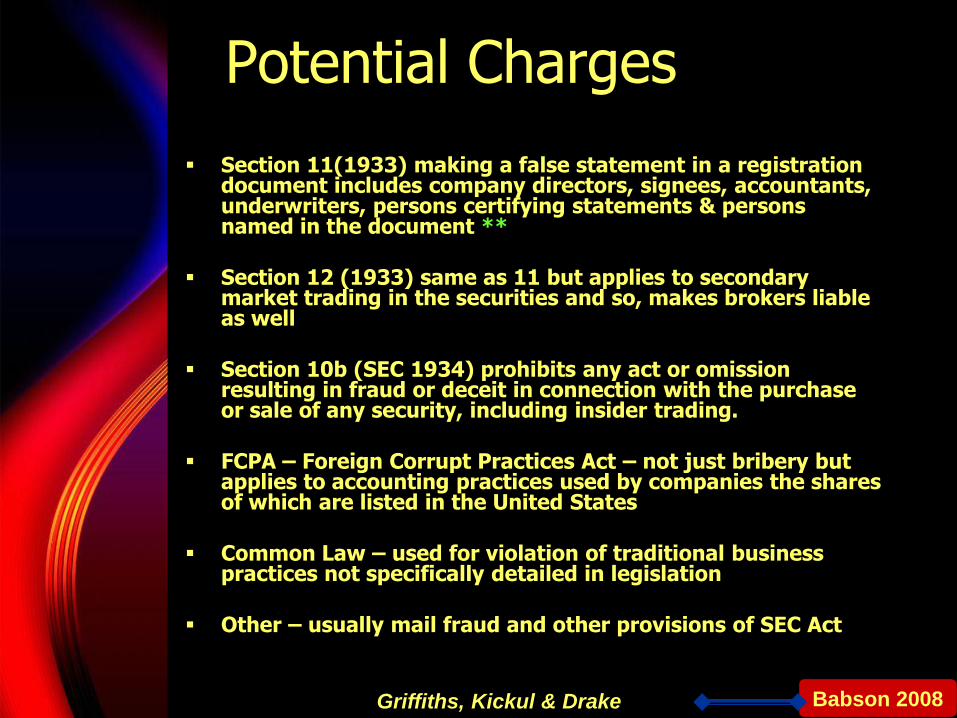

Potential Charges

Section 11(1933) making a false statement in a registration document includes company directors, signees, accountants, underwriters, persons certifying statements & persons named in the document **

Section 12 (1933) same as 11 but applies to secondary market trading in the securities and so, makes brokers liable as well

Section 10b (SEC 1934) prohibits any act or omission resulting in fraud or deceit in connection with the purchase or sale of any security, including insider trading.

FCPA – Foreign Corrupt Practices Act – not just bribery but applies to accounting practices used by companies the shares of which are listed in the United States

Common Law – used for violation of traditional business practices not specifically detailed in legislation

Other – usually mail fraud and other provisions of SEC Act

Babson 2008Griffiths, Kickul & Drake

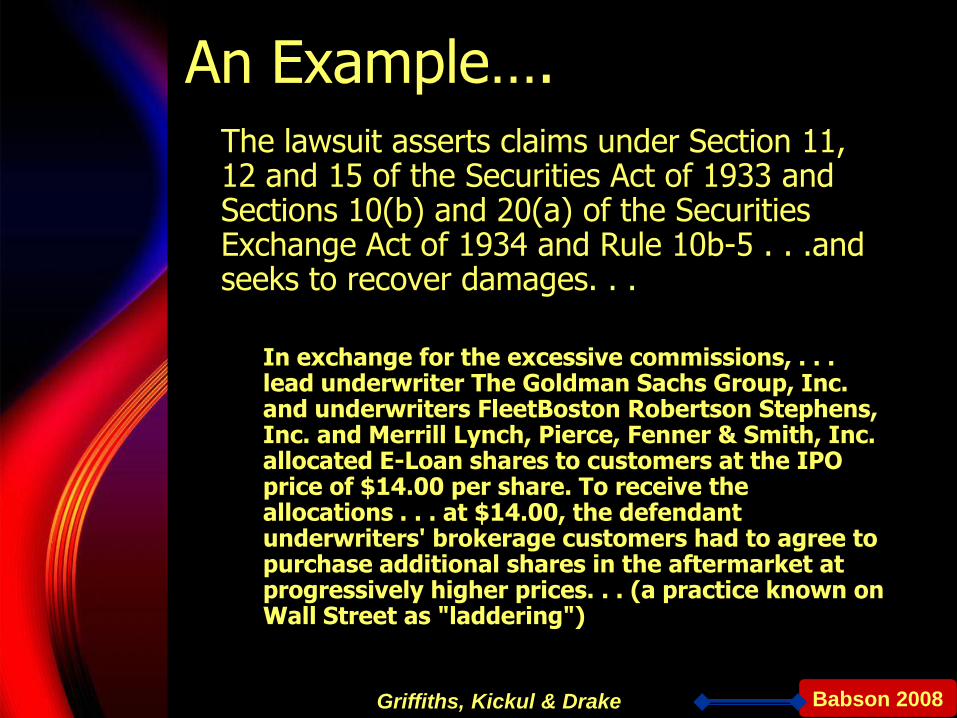

An Example….The lawsuit asserts claims under Section 11, 12 and 15 of the Securities Act of 1933 and Sections 10(b) and 20(a) of the Securities Exchange Act of 1934 and Rule 10b-5 . . .and seeks to recover damages. . .

In exchange for the excessive commissions, . . . lead underwriter The Goldman Sachs Group, Inc. and underwriters FleetBoston Robertson Stephens, Inc. and Merrill Lynch, Pierce, Fenner & Smith, Inc. allocated E-Loan shares to customers at the IPO price of $14.00 per share. To receive the allocations . . . at $14.00, the defendant underwriters' brokerage customers had to agree to purchase additional shares in the aftermarket at progressively higher prices. . . (a practice known on Wall Street as "laddering")

Babson 2008Griffiths, Kickul & Drake

An Example…

This artificial price inflation, . . . enabled both the defendant underwriters and their customers to reap enormous profits by buying E-Loan stock at the $14.00 IPO price and then selling it later for a profit at inflated aftermarket prices, which rose as high as $51.00 during its first day of trading. . .

the complaint alleges, the defendant underwriters required their customers to "kick back" some of their profits in the form of secret commissions. . . sometimes calculated . . . on how much profit . . . had (been) made (on the) IPO stock allocation. . .

The complaint further alleges that . . . the Prospectus distributed to investors and the Registration Statement filed with the SEC . . . contained material misstatements regarding the commissions that the underwriters would derive from the IPO and failed to disclose the additional commissions and "laddering" scheme discussed above.”

Babson 2008Griffiths, Kickul & Drake

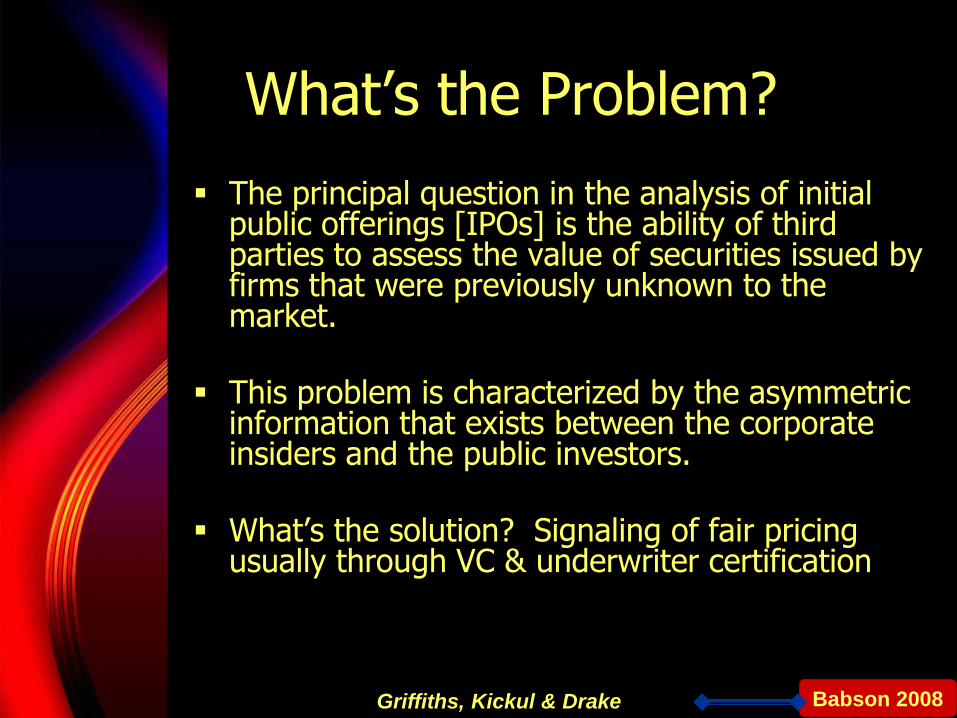

What‟s the Problem?

The principal question in the analysis of initial public offerings [IPOs] is the ability of third parties to assess the value of securities issued by firms that were previously unknown to the market.

This problem is characterized by the asymmetric information that exists between the corporate insiders and the public investors.

What‟s the solution? Signaling of fair pricing usually through VC & underwriter certification

Babson 2008Griffiths, Kickul & Drake

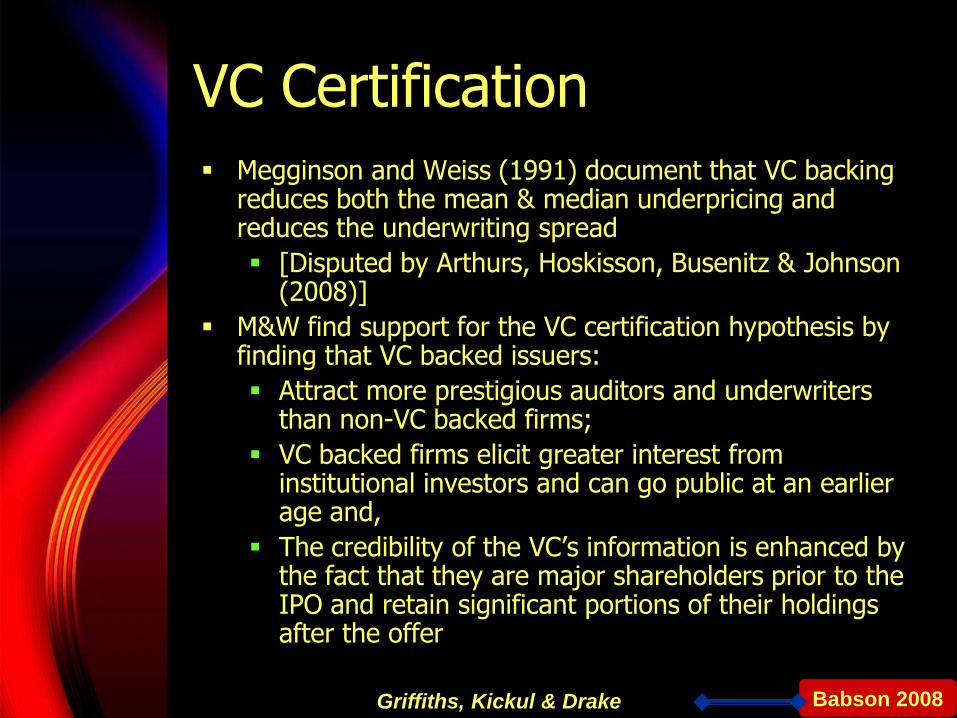

VC Certification

Megginson and Weiss (1991) document that VC backing reduces both the mean & median underpricing and reduces the underwriting spread

[Disputed by Arthurs, Hoskisson, Busenitz & Johnson (2008)]

M&W find support for the VC certification hypothesis by finding that VC backed issuers:

Attract more prestigious auditors and underwriters than non-VC backed firms;

VC backed firms elicit greater interest from institutional investors and can go public at an earlier age and,

The credibility of the VC‟s information is enhanced by the fact that they are major shareholders prior to the IPO and retain significant portions of their holdings after the offer

Babson 2008Griffiths, Kickul & Drake

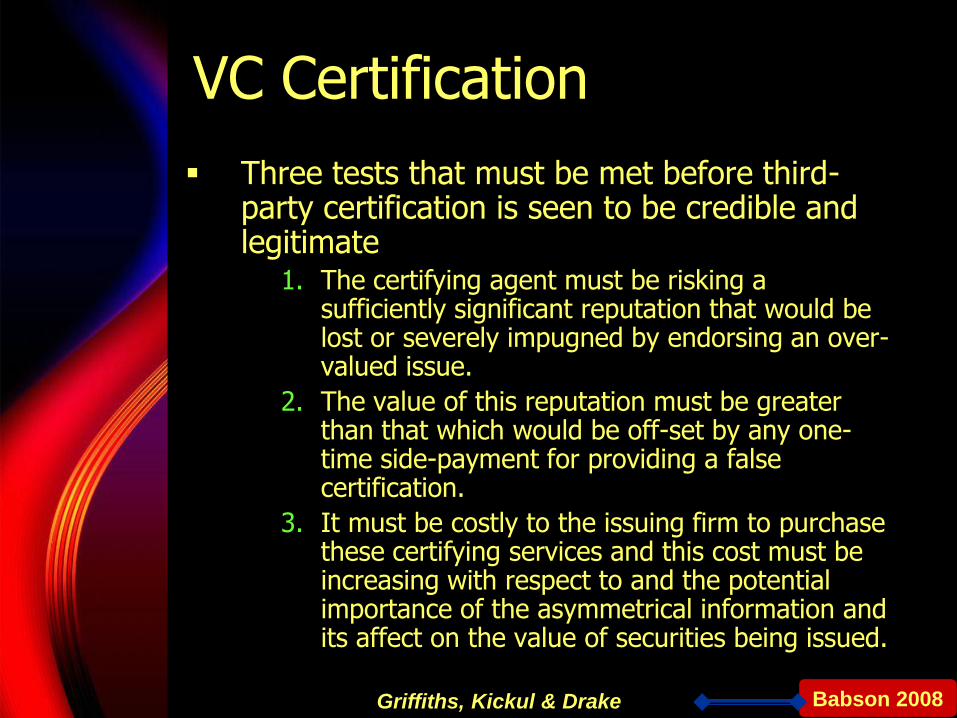

VC Certification

Three tests that must be met before third-party certification is seen to be credible and legitimate

1. The certifying agent must be risking a sufficiently significant reputation that would be lost or severely impugned by endorsing an over-valued issue.

2. The value of this reputation must be greater than that which would be off-set by any one-time side-payment for providing a false certification.

3. It must be costly to the issuing firm to purchase these certifying services and this cost must be increasing with respect to and the potential importance of the asymmetrical information and its affect on the value of securities being issued.

Babson 2008Griffiths, Kickul & Drake

Analyst Lust Loughran and Ritter (2004) introduce the analyst

lust hypothesis to describe IPO underpricing where influential analysts are engaged to take the firm public creating incentives to seek underwriters with a reputation for severe underpricing.

We test the Loughran and Ritter hypotheses on underpricing as well as the Lowry & Shu (2002) finding that greater underpricing leads to lower litigation risk. This is essentially an insuranceargument

We also investigate both the VC-backed success hypothesis (Jain & Kini, 2000) and the Huneycutt & Wibker (1992) wisdom of “sue the party with the deepest pockets.”

Babson 2008Griffiths, Kickul & Drake

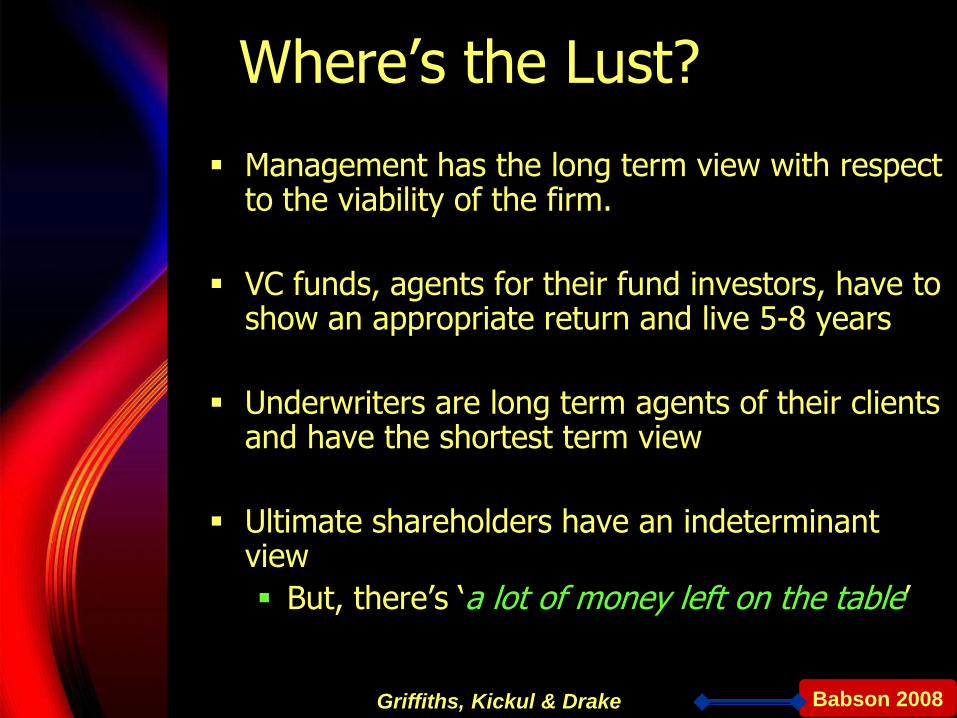

Where‟s the Lust?

Management has the long term view with respect to the viability of the firm.

VC funds, agents for their fund investors, have to show an appropriate return and live 5-8 years

Underwriters are long term agents of their clients and have the shortest term view

Ultimate shareholders have an indeterminant view

But, there‟s „a lot of money left on the table‟

Babson 2008Griffiths, Kickul & Drake

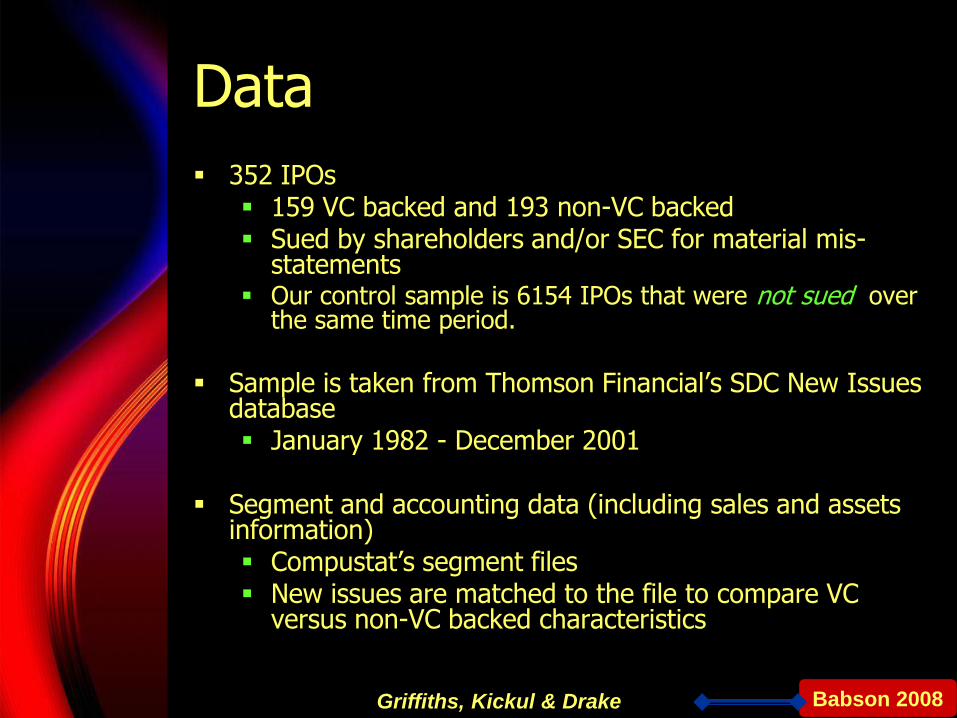

Data

352 IPOs 159 VC backed and 193 non-VC backed Sued by shareholders and/or SEC for material mis-

statements Our control sample is 6154 IPOs that were not sued over

the same time period.

Sample is taken from Thomson Financial‟s SDC New Issues database January 1982 - December 2001

Segment and accounting data (including sales and assets information) Compustat‟s segment files New issues are matched to the file to compare VC

versus non-VC backed characteristics

Babson 2008Griffiths, Kickul & Drake

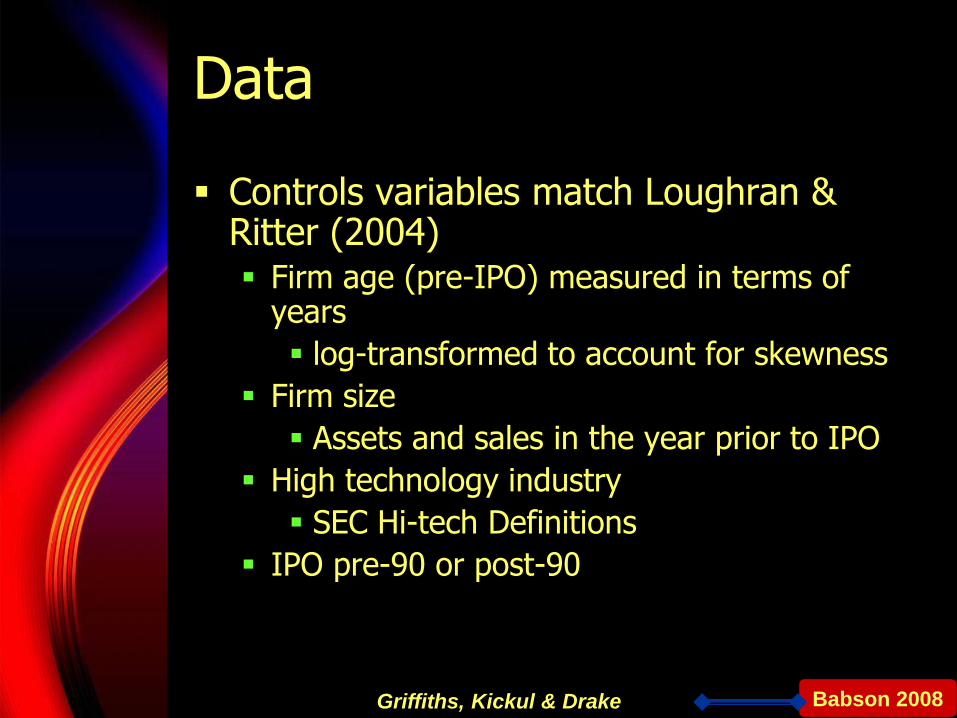

Data

Controls variables match Loughran & Ritter (2004) Firm age (pre-IPO) measured in terms of

years

log-transformed to account for skewness

Firm size

Assets and sales in the year prior to IPO

High technology industry

SEC Hi-tech Definitions

IPO pre-90 or post-90

Babson 2008Griffiths, Kickul & Drake

Data

A dummy variable was created to indicate whether a firm had received venture capital backing or not.

A dummy variable was created to indicate the number of times certain VC funds were sued within the sample.

Dummy variable =1 if VC was sued 5 or more times and zero if sued less than 5 times over the sample period

Babson 2008Griffiths, Kickul & Drake

Data

Underpricing

% change in stock price during the first day of trading for the IPO

((closing price – offer price)/offer price)

Offer price revision

Divide the final offer price by the mid-point of the initial offer price range & subtract one. The range is stated in the IPO prospectus.

Carter & Manaster underwriter rankings . . . . . .

Babson 2008Griffiths, Kickul & Drake

Analysis of LustDescriptives and Underpricing

1. Distribution of IPO Firms Over 20-year period

2. Identification of number of VC Firms Sued

3. Comparative Descriptive Statistics

1. VC-Backed, Non-VC Backed, Sued, Not Sued IPO Firms

4. Two-stage least-squares regression analyses

1. Predictors: Controls variables are: (1) Underwriter Rank and VC-Backed (2)

2. Dependent Variable: Underpricing

Babson 2008Griffiths, Kickul & Drake

5. Three-stage Logit Model Estimation

Predictors: Controls (stage 1), Underpricing (stage 2), and Underwriter Rank & VC-Backed (stage 3)

Dependent Variable: Sued

Analysis of LustProbability of Being Sued

Babson 2008Griffiths, Kickul & Drake

6. Descriptive statistics for charge legitimacy and settlement size (by VC)

7. Least-square regression analyses

Predictors: Underwriter Rank, VC-Backed, Underpricing

Dependent Variable: Settlement Size

8. Comparative Descriptive Statistics

VC sued infrequently/frequently by charge legitimacy and settlement

Analysis of LustCharge Legitimacy and Settlement

Analysis of Lust

Descriptives and Underpricing

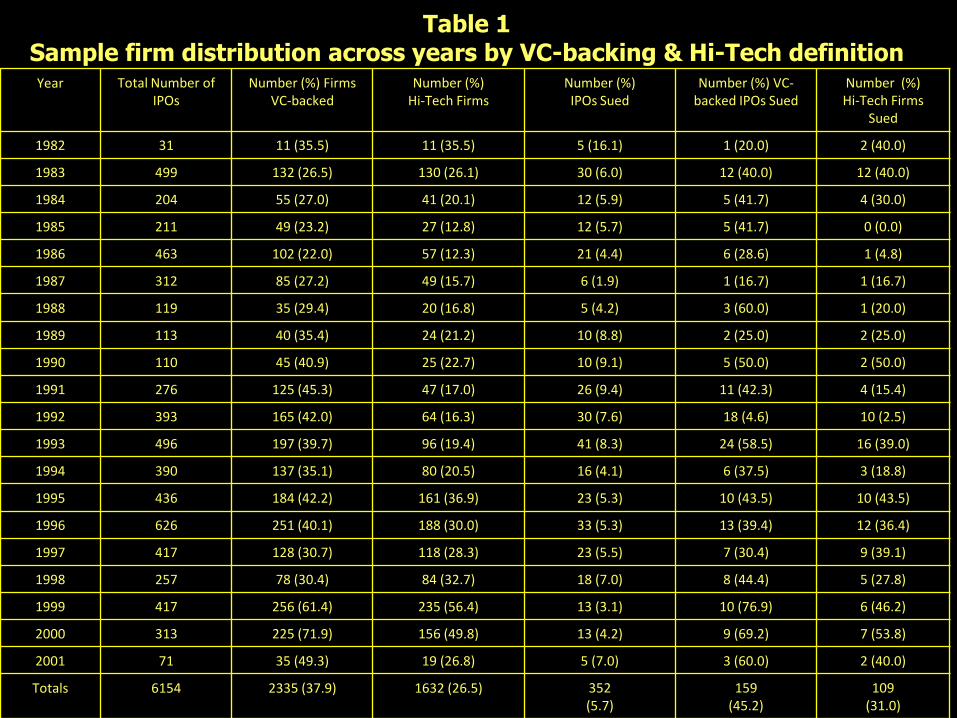

Year Total Number of IPOs

Number (%) FirmsVC-backed

Number (%) Hi-Tech Firms

Number (%)IPOs Sued

Number (%) VC-backed IPOs Sued

Number (%)Hi-Tech Firms

Sued

1982 31 11 (35.5) 11 (35.5) 5 (16.1) 1 (20.0) 2 (40.0)

1983 499 132 (26.5) 130 (26.1) 30 (6.0) 12 (40.0) 12 (40.0)

1984 204 55 (27.0) 41 (20.1) 12 (5.9) 5 (41.7) 4 (30.0)

1985 211 49 (23.2) 27 (12.8) 12 (5.7) 5 (41.7) 0 (0.0)

1986 463 102 (22.0) 57 (12.3) 21 (4.4) 6 (28.6) 1 (4.8)

1987 312 85 (27.2) 49 (15.7) 6 (1.9) 1 (16.7) 1 (16.7)

1988 119 35 (29.4) 20 (16.8) 5 (4.2) 3 (60.0) 1 (20.0)

1989 113 40 (35.4) 24 (21.2) 10 (8.8) 2 (25.0) 2 (25.0)

1990 110 45 (40.9) 25 (22.7) 10 (9.1) 5 (50.0) 2 (50.0)

1991 276 125 (45.3) 47 (17.0) 26 (9.4) 11 (42.3) 4 (15.4)

1992 393 165 (42.0) 64 (16.3) 30 (7.6) 18 (4.6) 10 (2.5)

1993 496 197 (39.7) 96 (19.4) 41 (8.3) 24 (58.5) 16 (39.0)

1994 390 137 (35.1) 80 (20.5) 16 (4.1) 6 (37.5) 3 (18.8)

1995 436 184 (42.2) 161 (36.9) 23 (5.3) 10 (43.5) 10 (43.5)

1996 626 251 (40.1) 188 (30.0) 33 (5.3) 13 (39.4) 12 (36.4)

1997 417 128 (30.7) 118 (28.3) 23 (5.5) 7 (30.4) 9 (39.1)

1998 257 78 (30.4) 84 (32.7) 18 (7.0) 8 (44.4) 5 (27.8)

1999 417 256 (61.4) 235 (56.4) 13 (3.1) 10 (76.9) 6 (46.2)

2000 313 225 (71.9) 156 (49.8) 13 (4.2) 9 (69.2) 7 (53.8)

2001 71 35 (49.3) 19 (26.8) 5 (7.0) 3 (60.0) 2 (40.0)

Totals 6154 2335 (37.9) 1632 (26.5) 352 (5.7)

159(45.2)

109(31.0)

Table 1Sample firm distribution across years by VC-backing & Hi-Tech definition

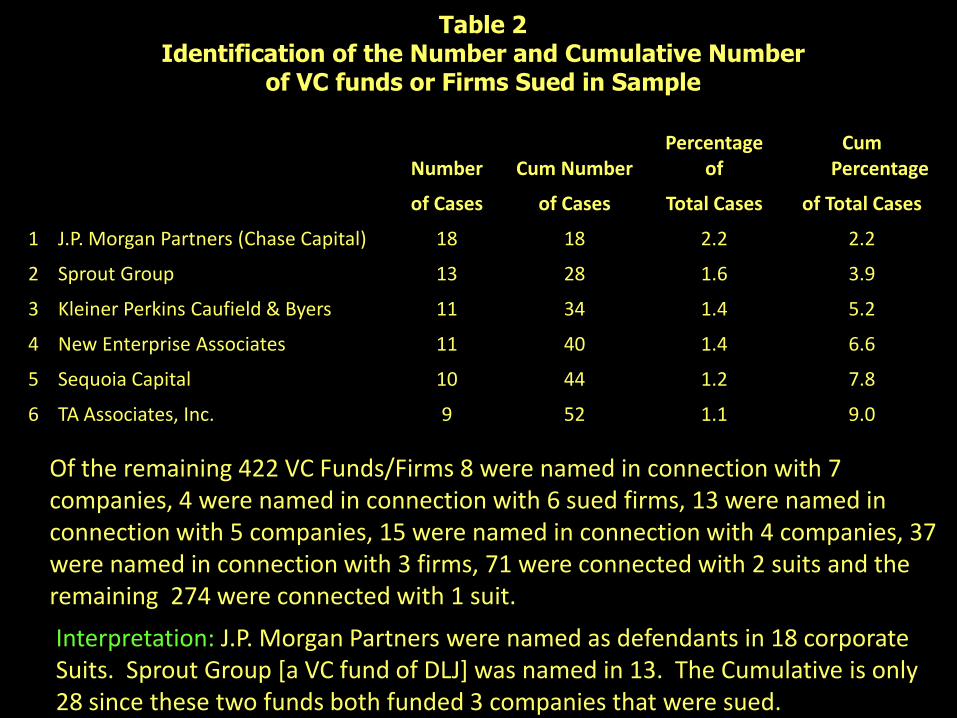

Number Cum NumberPercentage

of Cum

Percentage

of Cases of Cases Total Cases of Total Cases

1 J.P. Morgan Partners (Chase Capital) 18 18 2.2 2.2

2 Sprout Group 13 28 1.6 3.9

3 Kleiner Perkins Caufield & Byers 11 34 1.4 5.2

4 New Enterprise Associates 11 40 1.4 6.6

5 Sequoia Capital 10 44 1.2 7.8

6 TA Associates, Inc. 9 52 1.1 9.0

Table 2Identification of the Number and Cumulative Number

of VC funds or Firms Sued in Sample

Of the remaining 422 VC Funds/Firms 8 were named in connection with 7 companies, 4 were named in connection with 6 sued firms, 13 were named in connection with 5 companies, 15 were named in connection with 4 companies, 37 were named in connection with 3 firms, 71 were connected with 2 suits and the remaining 274 were connected with 1 suit.

Interpretation: J.P. Morgan Partners were named as defendants in 18 corporateSuits. Sprout Group [a VC fund of DLJ] was named in 13. The Cumulative is only28 since these two funds both funded 3 companies that were sued.

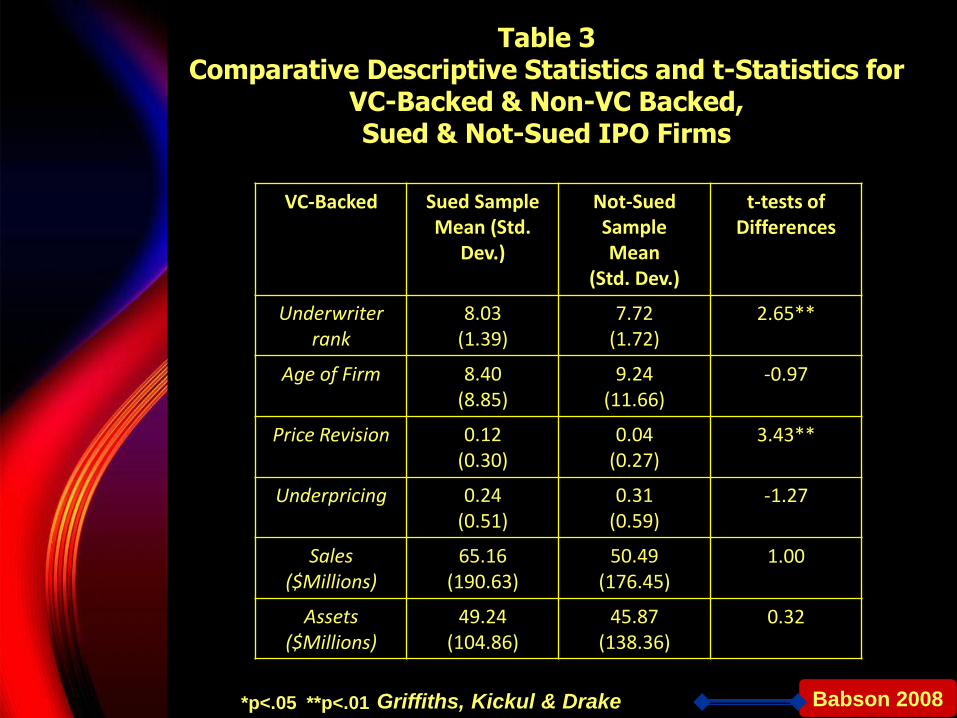

Babson 2008Griffiths, Kickul & Drake*p<.05 **p<.01

Table 3Comparative Descriptive Statistics and t-Statistics for

VC-Backed & Non-VC Backed, Sued & Not-Sued IPO Firms

VC-Backed Sued SampleMean (Std.

Dev.)

Not-Sued SampleMean

(Std. Dev.)

t-tests of Differences

Underwriter rank

8.03 (1.39)

7.72 (1.72)

2.65**

Age of Firm 8.40 (8.85)

9.24 (11.66)

-0.97

Price Revision 0.12 (0.30)

0.04 (0.27)

3.43**

Underpricing 0.24 (0.51)

0.31 (0.59)

-1.27

Sales ($Millions)

65.16 (190.63)

50.49(176.45)

1.00

Assets ($Millions)

49.24(104.86)

45.87(138.36)

0.32

Babson 2008Griffiths, Kickul & Drake*p<.05 **p<.01

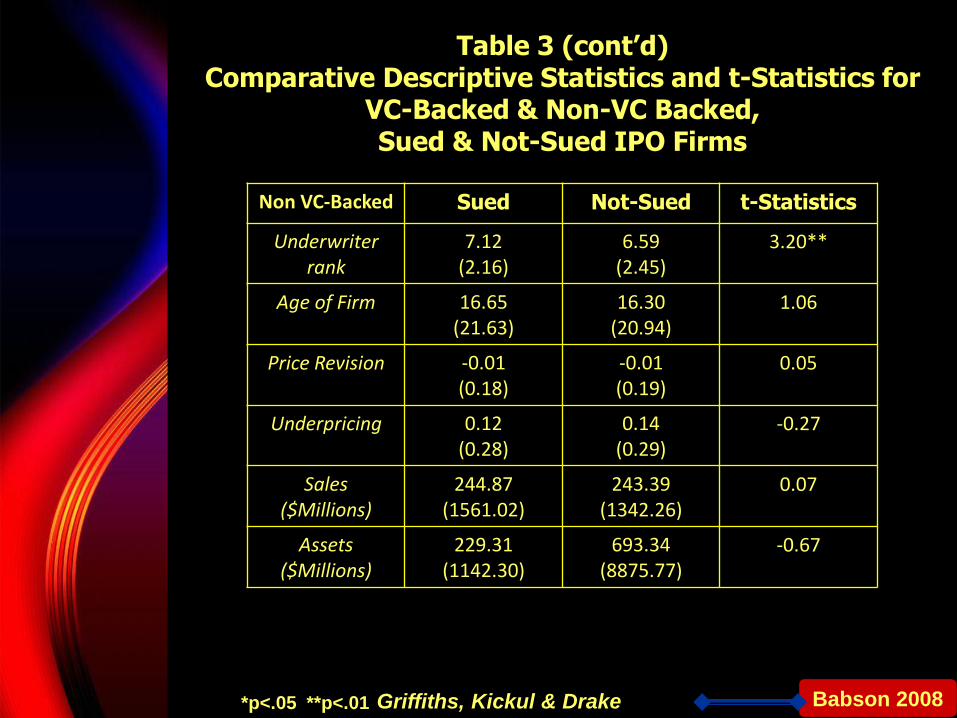

Table 3 (cont’d)Comparative Descriptive Statistics and t-Statistics for

VC-Backed & Non-VC Backed, Sued & Not-Sued IPO Firms

Non VC-Backed Sued Not-Sued t-Statistics

Underwriter rank

7.12 (2.16)

6.59(2.45)

3.20**

Age of Firm 16.65 (21.63)

16.30(20.94)

1.06

Price Revision -0.01 (0.18)

-0.01(0.19)

0.05

Underpricing 0.12(0.28)

0.14(0.29)

-0.27

Sales ($Millions)

244.87(1561.02)

243.39(1342.26)

0.07

Assets ($Millions)

229.31(1142.30)

693.34(8875.77)

-0.67

Babson 2008Griffiths, Kickul & Drake*p<.05 **p<.01

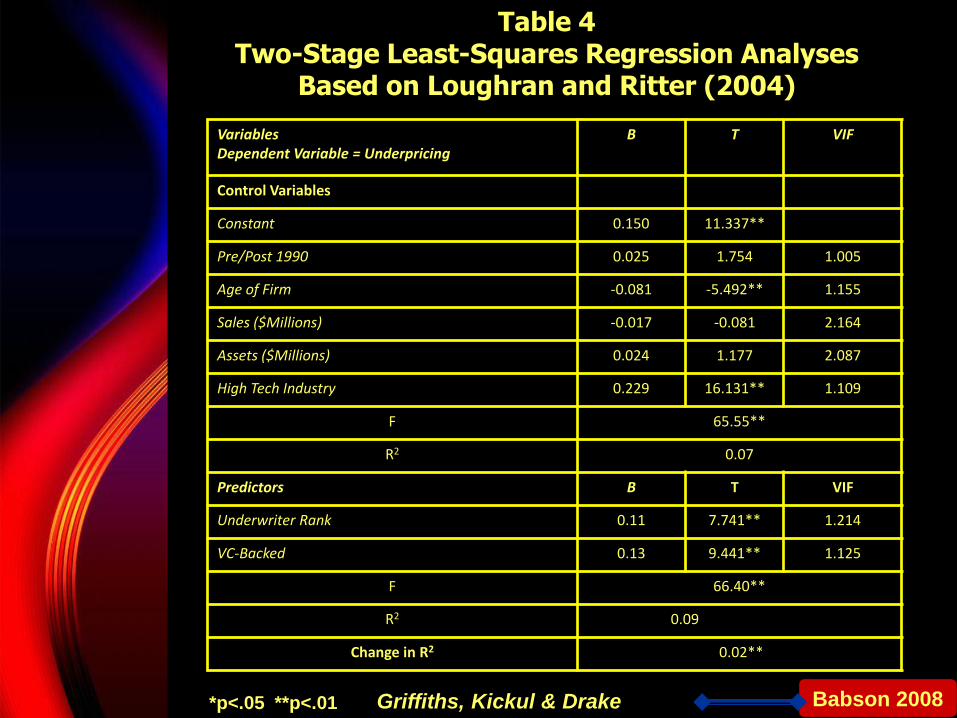

Table 4Two-Stage Least-Squares Regression Analyses

Based on Loughran and Ritter (2004)

VariablesDependent Variable = Underpricing

B T VIF

Control Variables

Constant 0.150 11.337**

Pre/Post 1990 0.025 1.754 1.005

Age of Firm -0.081 -5.492** 1.155

Sales ($Millions) -0.017 -0.081 2.164

Assets ($Millions) 0.024 1.177 2.087

High Tech Industry 0.229 16.131** 1.109

F 65.55**

R2 0.07

Predictors B T VIF

Underwriter Rank 0.11 7.741** 1.214

VC-Backed 0.13 9.441** 1.125

F 66.40**

R2 0.09

Change in R2 0.02**

Analysis of Lust

Probability of

Being Sued

Babson 2008Griffiths, Kickul & Drake

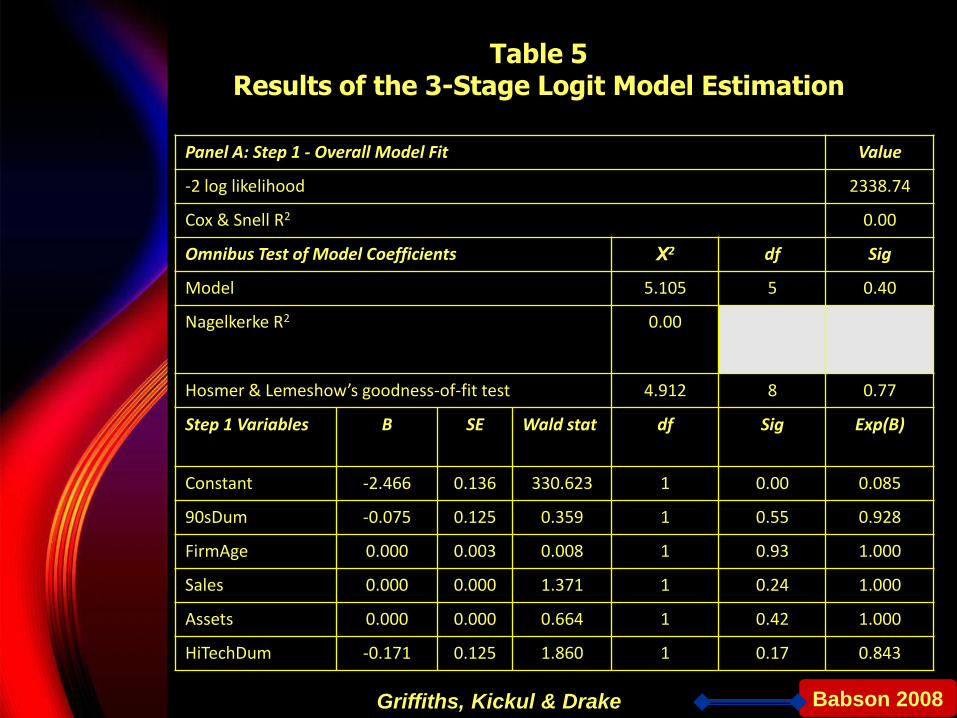

Table 5Results of the 3-Stage Logit Model Estimation

Panel A: Step 1 - Overall Model Fit Value

-2 log likelihood 2338.74

Cox & Snell R2 0.00

Omnibus Test of Model Coefficients Χ2 df Sig

Model 5.105 5 0.40

Nagelkerke R2 0.00

Hosmer & Lemeshow’s goodness-of-fit test 4.912 8 0.77

Step 1 Variables B SE Wald stat df Sig Exp(B)

Constant -2.466 0.136 330.623 1 0.00 0.085

90sDum -0.075 0.125 0.359 1 0.55 0.928

FirmAge 0.000 0.003 0.008 1 0.93 1.000

Sales 0.000 0.000 1.371 1 0.24 1.000

Assets 0.000 0.000 0.664 1 0.42 1.000

HiTechDum -0.171 0.125 1.860 1 0.17 0.843

Babson 2008Griffiths, Kickul & Drake

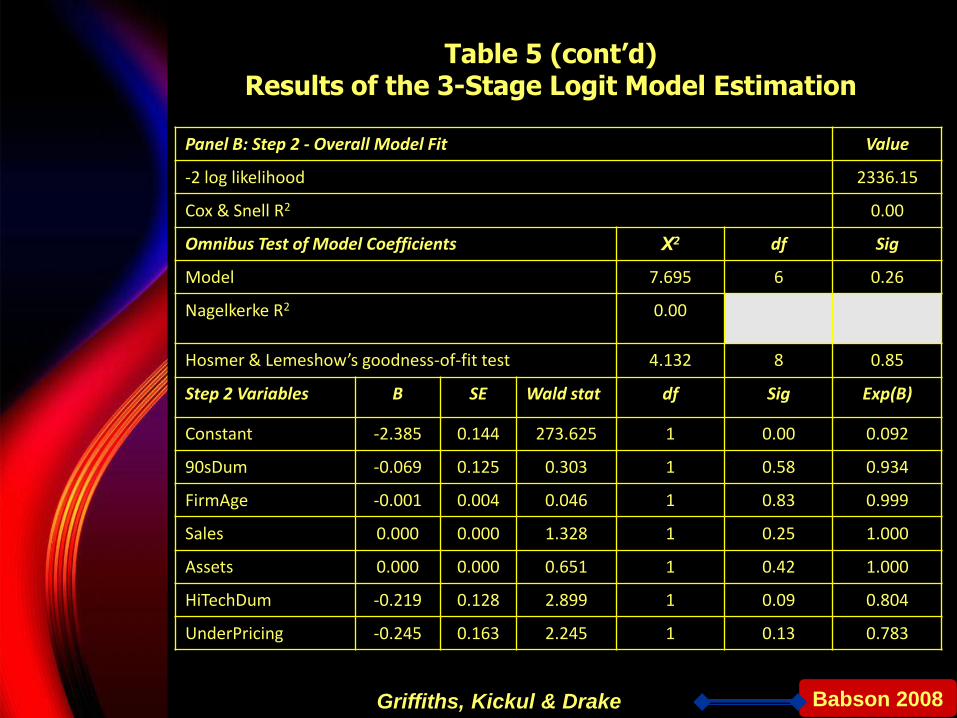

Table 5 (cont’d)Results of the 3-Stage Logit Model Estimation

Panel B: Step 2 - Overall Model Fit Value

-2 log likelihood 2336.15

Cox & Snell R2 0.00

Omnibus Test of Model Coefficients Χ2 df Sig

Model 7.695 6 0.26

Nagelkerke R2 0.00

Hosmer & Lemeshow’s goodness-of-fit test 4.132 8 0.85

Step 2 Variables B SE Wald stat df Sig Exp(B)

Constant -2.385 0.144 273.625 1 0.00 0.092

90sDum -0.069 0.125 0.303 1 0.58 0.934

FirmAge -0.001 0.004 0.046 1 0.83 0.999

Sales 0.000 0.000 1.328 1 0.25 1.000

Assets 0.000 0.000 0.651 1 0.42 1.000

HiTechDum -0.219 0.128 2.899 1 0.09 0.804

UnderPricing -0.245 0.163 2.245 1 0.13 0.783

Babson 2008Griffiths, Kickul & Drake

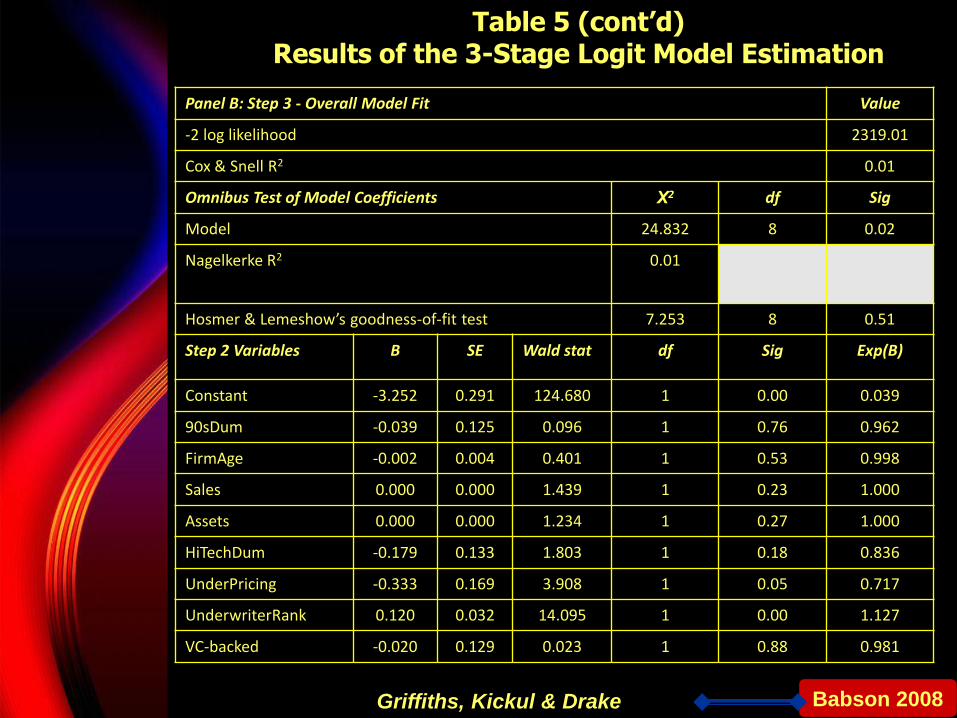

Table 5 (cont’d)Results of the 3-Stage Logit Model Estimation

Panel B: Step 3 - Overall Model Fit Value

-2 log likelihood 2319.01

Cox & Snell R2 0.01

Omnibus Test of Model Coefficients Χ2 df Sig

Model 24.832 8 0.02

Nagelkerke R2 0.01

Hosmer & Lemeshow’s goodness-of-fit test 7.253 8 0.51

Step 2 Variables B SE Wald stat df Sig Exp(B)

Constant -3.252 0.291 124.680 1 0.00 0.039

90sDum -0.039 0.125 0.096 1 0.76 0.962

FirmAge -0.002 0.004 0.401 1 0.53 0.998

Sales 0.000 0.000 1.439 1 0.23 1.000

Assets 0.000 0.000 1.234 1 0.27 1.000

HiTechDum -0.179 0.133 1.803 1 0.18 0.836

UnderPricing -0.333 0.169 3.908 1 0.05 0.717

UnderwriterRank 0.120 0.032 14.095 1 0.00 1.127

VC-backed -0.020 0.129 0.023 1 0.88 0.981

Analysis of Lust

Charge Legitimacy

and Settlement

Babson 2008Griffiths, Kickul & Drake

*p<.05 **p<.01

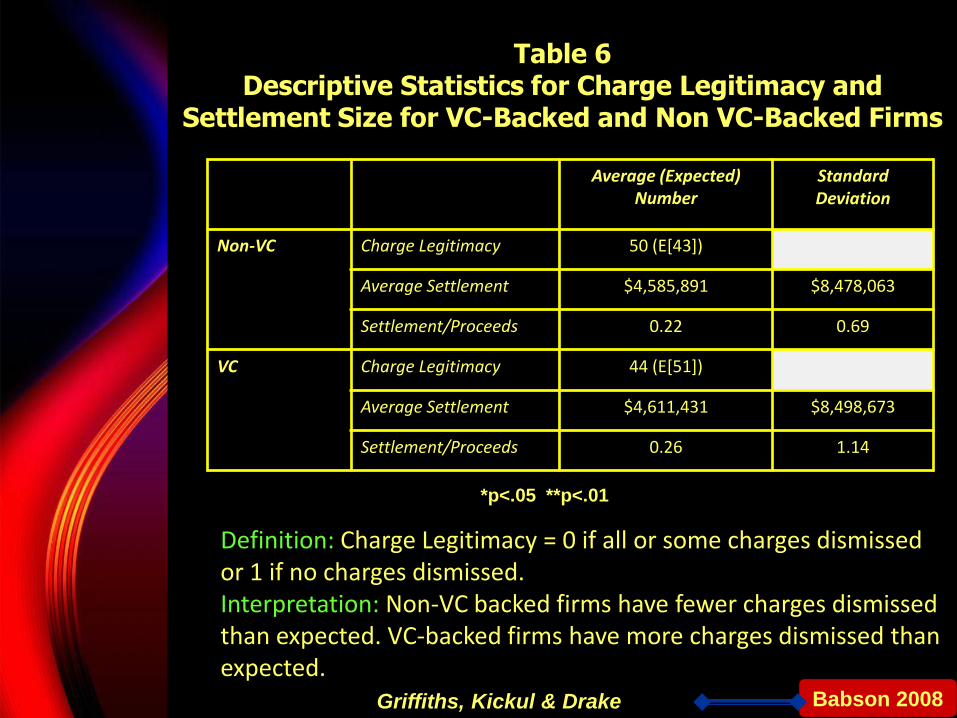

Table 6Descriptive Statistics for Charge Legitimacy and

Settlement Size for VC-Backed and Non VC-Backed Firms

Average (Expected) Number

StandardDeviation

Non-VC Charge Legitimacy 50 (E[43])

Average Settlement $4,585,891 $8,478,063

Settlement/Proceeds 0.22 0.69

VC Charge Legitimacy 44 (E[51])

Average Settlement $4,611,431 $8,498,673

Settlement/Proceeds 0.26 1.14

Definition: Charge Legitimacy = 0 if all or some charges dismissedor 1 if no charges dismissed. Interpretation: Non-VC backed firms have fewer charges dismissedthan expected. VC-backed firms have more charges dismissed thanexpected.

Babson 2008Griffiths, Kickul & Drake

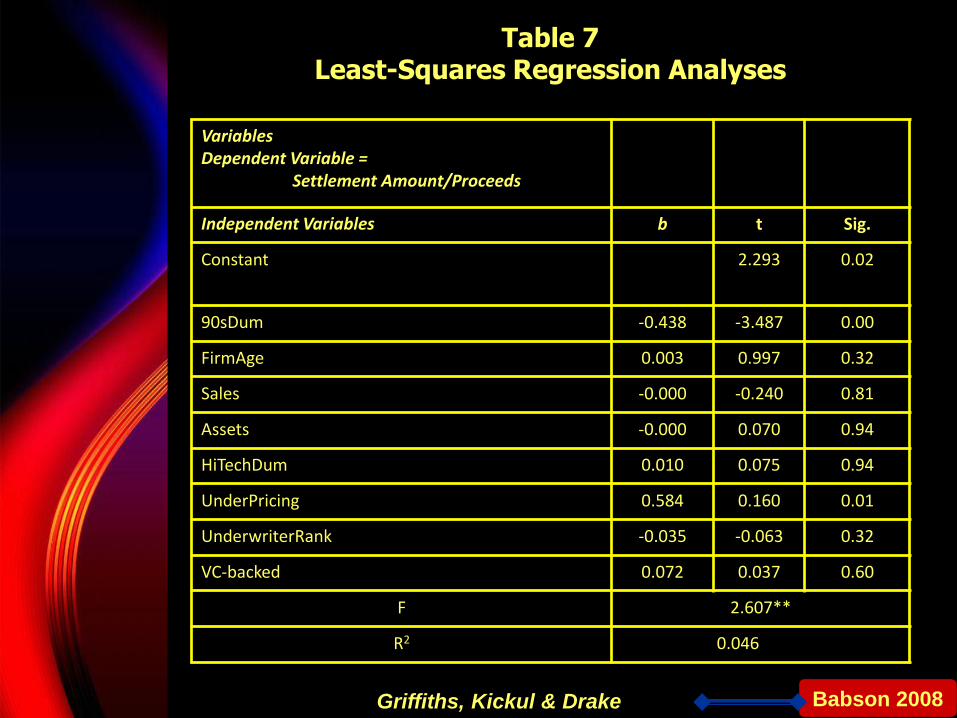

Table 7Least-Squares Regression Analyses

VariablesDependent Variable =

Settlement Amount/Proceeds

Independent Variables b t Sig.

Constant 2.293 0.02

90sDum -0.438 -3.487 0.00

FirmAge 0.003 0.997 0.32

Sales -0.000 -0.240 0.81

Assets -0.000 0.070 0.94

HiTechDum 0.010 0.075 0.94

UnderPricing 0.584 0.160 0.01

UnderwriterRank -0.035 -0.063 0.32

VC-backed 0.072 0.037 0.60

F 2.607**

R2 0.046

Babson 2008Griffiths, Kickul & Drake

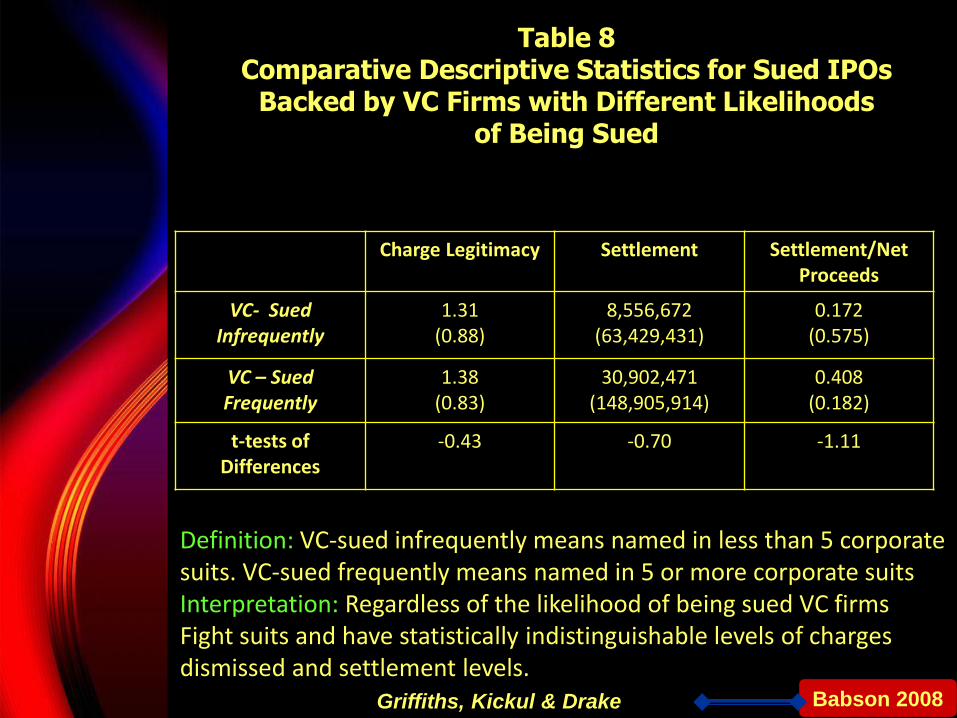

Table 8Comparative Descriptive Statistics for Sued IPOs

Backed by VC Firms with Different Likelihoods of Being Sued

Charge Legitimacy Settlement Settlement/Net Proceeds

VC- Sued Infrequently

1.31(0.88)

8,556,672(63,429,431)

0.172(0.575)

VC – Sued Frequently

1.38(0.83)

30,902,471(148,905,914)

0.408(0.182)

t-tests of Differences

-0.43 -0.70 -1.11

Definition: VC-sued infrequently means named in less than 5 corporatesuits. VC-sued frequently means named in 5 or more corporate suitsInterpretation: Regardless of the likelihood of being sued VC firmsFight suits and have statistically indistinguishable levels of chargesdismissed and settlement levels.

Babson 2008Griffiths, Kickul & Drake

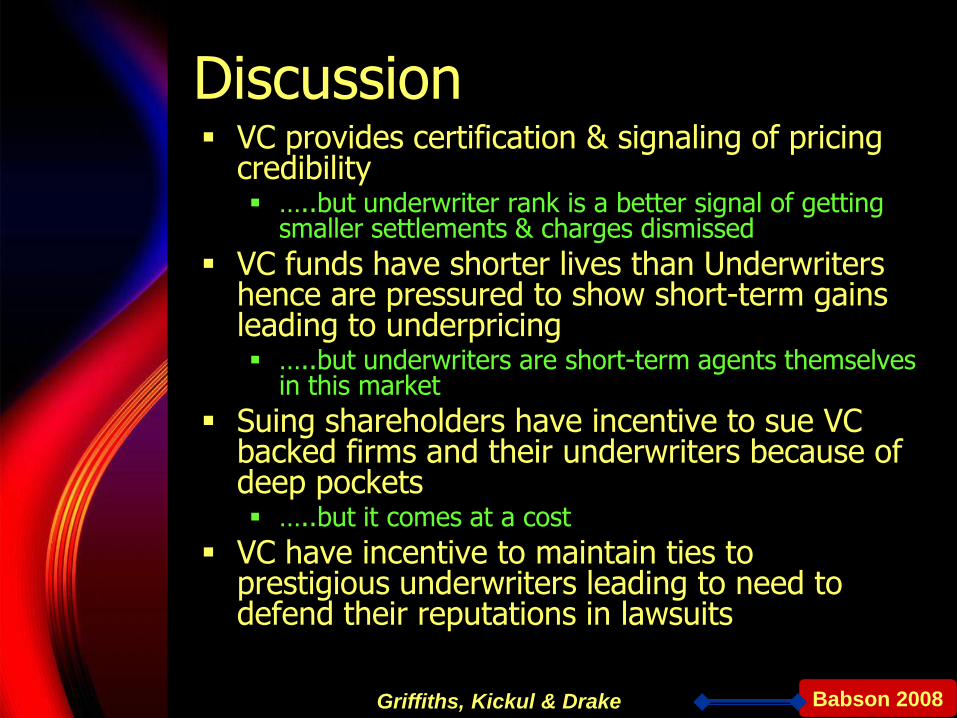

Discussion VC provides certification & signaling of pricing

credibility …..but underwriter rank is a better signal of getting

smaller settlements & charges dismissed

VC funds have shorter lives than Underwriters hence are pressured to show short-term gains leading to underpricing …..but underwriters are short-term agents themselves

in this market

Suing shareholders have incentive to sue VC backed firms and their underwriters because of deep pockets …..but it comes at a cost

VC have incentive to maintain ties to prestigious underwriters leading to need to defend their reputations in lawsuits