the pentecostal credit union ltd - 37th annual general meeting

TRANSCRIPT

37th Annual General MeetingThe Pentecostal Credit Union Ltd

from 6pm, 11 March 2017

venue Tooting Neighbourhood Centre28 Glenburnie Road London SW17 7PJ

The Pentecostal Credit Union is authorised by the Prudential RegulationAuthority and regulated by the Financial Conduct Authority and thePrudential Regulation Authority (FRN 213242).

The Pentecostal Credit Union Limited

15 Oldridge RoadBalhamLondon SW12 8PL

Phone 020 8673 2542

Email [email protected]

www.pcuuk.com

/pentecostalcreditunion

@PentecostalCU

AGM agenda

1. Welcome

2. Prayer

3. Hymn: How Great is Our God

4. Scripture: 1 Chronicles 29:11:13

5. Apologies

6. Minutes of last AGM: 19 March 2016

7. Matters arising

8. Directors’ report

9. Presentation from the Youth Shadow Board

10. Bank charges

11. Loan report

12. Audit Committee report

13. Nominations for the Board

14. PCU Financial Statements

• Directors’ report and recommendation of dividend

• Independent auditors’ report

• Accounts

15. Appointment of auditor

16. Raffle

17. Closing: A word from the founder – Rev. Carmel Jones

18. Hymn

19. Close in prayer

2

Prayer: St Francis of AssisiLord, make me an instrument of Thy peace;

Where there is hatred, let me sow love;

Where there is injury, pardon;

Where there is error, truth;

Where there is doubt, faith;

Where there is despair, hope;

Where there is darkness, light;

And where there is sadness, joy.

O Divine Master, Grant that I may not so much seek

To be consoled as to console;

To be understood as to understand;

To be loved as to love.

For it is in giving that we receive;

It is in pardoning that we are pardoned;

And it is in dying that we are born to eternal life.

3

How Great is Our GodThe splendour of the King,

Clothed in majesty

Let all the earth rejoice

All the earth rejoice

He wraps himself in Light,

And darkness tries to hide

And trembles at His voice

Trembles at His voice

How great is our God, sing with me

How great is our God, and all will see

How great, how great is our God

Age to age He stands

And time is in His hands

Beginning and the end

Beginning and the end

The Godhead Three in One

Father Spirit Son

The Lion and the Lamb

The Lion and the Lamb

Name above all names

Worthy of our praise

My heart will sing

How great is our God

How great is our God, sing with me

How great is our God, and all will see

How great, how great is our God

4

Scripture: 1 Chronicles 29: 11-13Thine, O Lord, is the greatness, and the power, and the glory, and thevictory, and the majesty: for all that is in the heaven and in the earth isthine; thine is the kingdom, O Lord, and thou art exalted as head aboveall. Both riches and honour come of thee, and thou reignest over all; andin thine hand is power and might; and in thine hand it is to make great,and to give strength unto all. Now therefore, our God, we thank thee,and praise thy glorious name.

5

Held on Saturday 19 March 2016 at 28 Glenburnie Road, London SW17 7JP

Directors presentLeslie Laniyan (Chair)

Chona Labor (Vice Chair)

Patricia Toussainte (Secretary)

Tracey Connage (Director)

Lorna Lynch (Director)

Michael Mathura (Director)

Ann Waugh (Chair, Audit Committee)

Staff in attendanceMr S Bowes (CEO)

Ms L Humphris (Loans and Business Administrator)

Ms E Bowes (Executive Assistant and Minute Taker)

Minutes of the 36th Annual GeneralMeeting of the Pentecostal Credit Union

WelcomeThe AGM convened at 6.30pm. Mr Leslie Laniyan, the Chair of the PCU,presided over the meeting and welcomed the members.

Prayer, hymn and scripture readingMrs Tracey Connage facilitated the'praise and worship' openingsession. She read the prayer of St Francis of Assisi, led themembership in the hymn –‘Standing on the Promises’ and read the scripture Psalm 16: Vs. 8-11.

ApologiesApologies were received from:

• Rev. Verona Richards – Director• Ms Veronica Palment• Rev. Geoffrey Folkes

6

Minutes of the last meetingMrs Patricia Toussainte, Secretary of the credit union, read the minutes ofthe last meeting.

Ms Veronica O'Connor noted an error in the date recorded for the dividendpayment. This should read 2013-14 and not 2014-15. This was acceptedto be rectified.

Mrs Johnson proposed that the minutes be accepted as a true record ofevents.

Mrs Douglas seconded the proposal. The minutes were accepted with nofurther changes or challenges.

Matters arisingThe Credit Union Expansion Project (CUEP)Mr Bowes updated the AGM on this government-sponsored scheme tomodernise the credit union sector in the UK. He informed the meetingthat CUEP is a 10-year scheme. PCU are due to begin transformation inAugust 2016.

Through CUEP, all 40 participating credit unions will share a core bankingplatform and a common computer system. They will also share bestpractice, knowledge and data. The project has a series of targets, whicheach credit union has to meet. There will be new, improved productsand services that everyone will benefit from.

Mr Howard Johnson suggested that CUEP might be a means for thegovernment to check on the financial dealings of credit union members.Mr Bowes assured him that this was not the case. Each credit union isautonomous and will have its own unique system within the commonplatform. Members’ personal data will not be shared with anyone.

The purpose of CUEP is to modernise the credit union sector and to makecredit unions more attractive to the population as a whole and especiallyto younger people. Credit unions only report to the government – HMRC– on accounts with levels of dividend payments in excess of £250 andthis is only reporting. No other details are shared.

7

Directors’ report to the membershipMr Chona Labor, Vice Chair of the credit union, presented the Directors’Report.

After playing the PCU promotional video – Sun in Rain – he highlightedthe following:

Strategic objectives• Growth, renewal and improvement are the PCU’s strategic objectives

to September 2017.• As well as revising existing targets, new targets were set this year in

the areas of lending, shareholding and income.• The rate of membership has more than doubled, with an average of

12 new members per month.

Marketing• The PCU has adopted a dynamic and multi-faceted marketing strategy.• Social media channels Facebook, Twitter, YouTube and LinkedIn have

helped to raise our profile and increase awareness of the PCU brand.The PCU YouTube channel, in particular, showcases our work throughvideo.

• The PCU is about to embark on a series of promotional Roadshows.

A new office• The refurbished offices are now operational.• The formal office opening is planned for April 2016. It will be

officiated by Bishop Delroy Powell and opened by the Deputy Mayorof Wandsworth.

Developing our young people• The PCU has plans to establish a Youth Shadow Board (YSB).• The YSB will consist of young savers aged 11-18 years.• Members were encouraged to support and promote the initiative.

8

PCU Shares• The PCU is now publishing a quarterly newsletter.• The first edition was recently circulated to all members.• PCU Shares enables the PCU to keep in touch with its members and

raise the profile of the organisation.

35th anniversary celebration• On 6 June 2015, we hosted a gala dinner and gospel show to celebrate

our 35th anniversary.• It was a resounding success, with over 300 guests attending and ‘A

list’ gospel artists performing.• The anniversary celebration was held to celebrate the great achievements

of this credit union, to honour the founding members, to mark thehistory and success of black enterprise in the UK and, most importantly,to promote the credit union, raise our profile and increase ourmembership. The event helped to do all of those things.

Welcome toour newnewsletterWe hope you like our newnewsletter, which is designed toshare our news, give you lots ofinformation about our services –and invite you to join us as avolunteer.

The newsletter is part of ourtransformation plans for PCU overthe coming year. It will allow us tokeep you up to date and pass onuseful information.

Leslie LaniyanChair of the PCU Board

Bright new office(& new services on the way)The refurbishment of our Balham offices is now complete,giving us a brighter reception area and better spaces forour staff and meetings.

pcusharesMarch 2016

Our newly updated offices reflect theway we’re working to transform theentire business – to provide ourmembers with a modern, accessibleservice that better meets their needs.

On 14 April, we will hold a smallopening event. Bishop Delroy Powellfrom the New Testament Assembly willlead a service to re-dedicate the buildingand the credit union to the ministryof providing financial services to thePentecostal faith community in the UK.

InsideMeet PCU’s staff 2

Church Credit Champions Network 2

Become a PCU Ambassador 3

Involving young people 3

Tips to stay on top of your finances 3

Focus on: Our YouTube channel 4

News from the Pentecostal Credit Union

Before (bottom left) and after (belowand right). Our tired offices are nowtransformed.

Key messages The Chair then summarised the key messages from the report as follows:

• He explained that marketing is extremely important to the PCU, asthis was the medium through which the credit union’s ambitions forgrowth would be achieved.

• He explained the importance of improving the individual loan portfolio,as the quicker this was done the quicker we could recommencemaking loans to churches.

• He continued that the key rationale for refurbishing the office was tocreate a positive and uplifting environment for everyone – staff andmembers. He invited members to visit the offices – they would bewelcomed by Shane and Lauren.

• The Chair welcomed feedback on the new newsletter, PCU Shares. Heexplained that the newsletter is to keep the membership informed andup to date about PCU operations and activities, and that we want tomake it something that the members are really proud of.

The Chair then invited questions on the Directors’ report.

Rev. Jones observed that the presentation of the Directors’ report was‘fantastic’, but asked if it could be improved by making better use ofvisual aids in presenting the reports, as well as a microphone. This couldbe implemented next year.

9

There were a range of questions and discussions about the YouthShadow Board – which the membership displayed full support for. MrsKatharine Johnson asked if the children had to be members of the PCU.Leslie Laniyan responded that this was the case.

Rev. Phil Forte commended the scheme and commented that the themeof getting young people to encourage and work with other young people,in the way outlined, would bolster them and provide them with a senseof direction. Leslie asked the members to encourage young people tojoin and come, as this would provide fantastic opportunities for them.

There was further discussion about the YSB. Rev. Jones added to thedebate the contribution of the Equiano Benevolent Fund Scheme (EBS)to the campaign to increase the membership of young people to thecredit union. EBS will provide £30 to any young person under the age of18 who wishes to open a credit union account. This gift will be the firstdeposit in the share account.

Bishop Eric Brown commented that he’d had the pleasure of visiting thePCU office some months ago and offered his congratulations to theBoard for the new office facilities now available to the staff andmembership. He continued that he’d had a conversation with Rev. Jonesabout EBS and that he wanted to commend the programme highly. Hefelt that it was important for the PCU to emphasise the EBS facility indiscussions with church leaders, to promote the organisation.

Loan reportThe Loan report was presented to the membership by the Loans andBusiness Administrator, Lauren Humphris. She reported that a total of£1,280,646 had been allocated in loans between 1 October 2014 and30 September 2015.

Shane Bowes commented that this was a substantial improvement onlast year’s outturn, partly because the previous moratorium on lendinghad impacted part of the 2013-14 financial year. But, more significantly,the increased target of £1.2m in loans (£100k per month) set by theBoard had driven the improvement. The target was overachieved bysome £80k.

He continued the explanation by adding that the CustomerSegmentation project that we commissioned researching the financialbehaviours of PCU members had greatly influenced our targeting andmarketing of loans.

Mr Ezra Parkin asked if the PCU would be offering different types of loansin future, particularly mortgages. Shane Bowes responded that thesegmentation research report would help to determine the types of loansthat we offer in future. He continued that the PCU does not have mortgagepermissions at the moment and it was unlikely that we would ventureinto the realm of mortgage lending given that we can only grant loansof up to £125k and you can’t buy any property – certainly not in theSouth East – for this amount of money. However, PCU can and doesprovide secured lending in the form of second charge mortgages. Wehave reduced the interest rates on larger loans like this to 5%.

Rev. Jones observed that that this was excellent news. Bishop Eric Brownadded that the PCU had been a real credit to our community. It shouldbe promoted and marketed as a very competitive and viable way ofaccessing resources and doing the things that we need to do.

10

He commended the Roadshow initiative and suggested that the PCUshould look into hosting Prayer Breakfasts with key church leaders. Headded that Bishops and church leaders had an important role to play inpromoting the PCU. As a District Bishop he has several churches withinhis remit and he would be pushing and promoting the PCU to hiscongregants. He added, finally, that members should take responsibilityfor promoting the organisation.

Report of the Audit CommitteeMs Ann Waugh, the Chair of the Audit Committee, presented her report.She began by explaining the role of the Audit Committee – which is tosafeguard the interests of the membership and to ensure that the Boardis compliant with legal and regulatory requirements. She furtherexplained that the Audit Committee works with an independentlycommissioned auditor, who audits the PCU’s operations in accordancewith an agreed Audit Plan. The Audit Committee is independent of theBoard and operates separately.

The purpose of her report was to inform the members of:

• New developments.• Results of Internal Audits during 2014-15.• Key lessons and emerging trends from internal audits.• The Board’s expertise and effectiveness.• Audit Plan for 2015-2016.

She summarised:

• Leroy Reid and Company Ltd had been appointed to conduct thePCU’s internal audit. February 2015 saw the start of our two-yearinternal audit contract.

• Seven out of 12 of the annual audits have been rated ‘reasonableassurance’. Four were rated as substantial assurance. One has yet tobe finalised and should be carried forward into next year’s scheduleof audits.

• The Audit Committee through the internal audit process aids the PCUto learn and grow from audits, feedback, collaboration and discovery.Members have a Board of Directors and a management team that areopen to learning and determined to improve. Improvements have beenmade to our marketing strategy, as well as to the managementinformation reports that the Board need to make decisions.

• The Board of Directors have the majority of the right competencies toaddress the company’s short-term and long-term issues, and a strongchairman. Overall attendance at Board meetings is 93%.

Finally she summarised the Audit plan for 2015-16.

Ann Waugh invited questions from the floor. Mr O’Connor asked for theterm ‘provisioning’ to be explained. Shane Bowes explained that everycredit union has to make provision for bad and doubtful debts and thiscredit union has a provisioning policy that ensures that all loans in arrearshave adequate provision for the length of time in arrears.

Mr Noel Bennett noted that Risk had not been completed in last year’saudit. Ann Waugh explained that the auditor had an emergency, so hewas not able to complete it in time for this report, but that it had beenadded to Quarter 1 in the audit plan for 2015-16.

Leslie Laniyan thanked Ann Waugh for her report.

11

Nominations for election to the BoardIn accordance with Rule 103, one-third of the Board had resigned and wereseeking re-election. In addition, the Chair of Audit had also completedher term and was seeking re-election. These directors were Lorna Lynch,Tracey Connage and Ann Waugh. These members were duly re-elected.

There were no other nominations from the floor.

Rev. Jones asked about the new regime for approved persons being broughtin by the Financial Conduct Authority (FCA). He observed that Directorsnow had to be appointed only if they had the necessary skills andcompetencies needed for the direction and management of the creditunion and that nominations and elections to the Board had to reflect this.

Shane Bowes confirmed Rev. Jones’s observations and explained the new‘Senior Managers Regime’ being implemented by the FCA, and that it is nowthe responsibility of the credit union to conduct their own due diligenceon elected Board members, with respect to ‘Fit and Proper’ – ie, financialand other checks – and to ensure that they have the right skills andcompetencies for the Board. In future, FCA approval would be forthcomingfor two senior people in the organisation – the Chair and the CEO.Authority in the form of Approved Persons Controlled Function 1.

The Rev. Richards was duly elected by the membership.

In addition, and in accordance with Rule 103, one-third of the Boardhad resigned and were seeking re-election. These directors were MichaelMathura and Chona Labor. These members were also duly re-elected.

There were no other nominations.

PCU financial statementsMs Lorna Lynch (Director) presented the accounts. She explained that thelarge capital withdrawals related to churches that had needed towithdraw funds to fund projects which the PCU were unable to financethrough loans because of the corporate lending restrictions.

Bishop Eric Brown asked about the new reduced level of protection ofthe Financial Services Compensation Schemes. Shane Bowes explainedthe new arrangements and that, due to EU changes, the level ofprotection that the government will provide for savings in a financialinstitution in the UK has reduced from £85k to £75k. Ms Lorna Jonesobserved that we were affected by this because of EU regulations.

The accounts were accepted by the membership.

DividendA dividend of 1.5% was recommended. The Chair reminded themembership that last year the Board had committed to paying anincrease in dividend, provided we were successful in recouping fundsthrough the legal case. As this had happened, the Board were in aposition to propose an increase of 50% on the dividend paid last year,which was 1%.

The members applauded the Board’s achievements in financialmanagement. Bishop Brown moved that the dividend be accepted andthis was unanimously agreed.

Appointment of the auditorLorna Lynch proposed that Thomas Westcott be re-appointed as ourAuditors for the coming year. Bishop Brown asked about costs. Lornaresponded that their costs amounted to £4,800. Bishop Brown movedthat we re-appoint Thomas Westcott as the PCU’s auditors. This wasseconded by Mr A Bartley.

RaffleMrs Jones presided over the raffle draw. She thanked the Board andcongratulated them for the very proficient way that they were runningthe business on behalf of the membership. Master Montelle Bartley drewthe raffle. The winners were:

• No. 131 – Patricia Toussainte – £150• No. 133 – Michael Mathura – £100• No. 150 – Sis. Logan – £100

12

Founder’s closing addressBefore Rev. Jones rose to give his address, Bishop Brown asked to make astatement. He stated that he had been a long-serving member andsupporter of the PCU and that Rev. Jones was the ‘Grand Father’ of thecredit union and as such should be recognised formally, not only as thefounder but for his contribution to the current success of the credit union.

He asked the Board to consider formal recognition of Rev. Jones’scredibility, in the form of a lifelong membership award. The Chair saidthat this will be the first order of business at the next Board meeting andwe will report back in the newsletter.

Rev. Jones then addressed the membership. He expressed his pride andpleasure at the achievements of the PCU Board and recognised thetransformation that had happened in the credit union. He commentedthat the Americans know how to applaud their people when they havedone well, yet, in the UK, we tend to belittle great achievement. Heasked the membership to applaud the Board and commented that thereshould be an hour of prayer dedicated to the leadership anddevelopment of the PCU every four months.

In closing, he led the membership in the hymn ‘Immortal Invisible’.

Bishop Eric Brown closed the proceedings in prayer.

13

14

The PCU organisational chartat 1 January 2017

PCUMembership

Board (governing body)

Mr Leslie Laniyan (Chair, SMF8)Mr Chona Labor (Vice Chair)

Ms Patricia Toussainte (Secretary)Mr Michael Mathura (Director)

Ms Lorna Lynch (Director)Mrs Tracey Connage (Director)Ms Verona Richards (Director)

Audit Committee

Ann WaughChair of Audit Committee(Non-Executive Director)

MarketingCommittee

Mr Chona Labor (Chair)Mr Leslie Laniyan

Ms Verona Richards Mr Shane BowesMs Elaine Bowes

RemunerationCommittee

Ms Patricia Toussainte (Chair)

Mr Michael MathuraMrs Tracey Connage

Mr Shane BowesMr Leslie Laniyan

Chief Executive Officer

Shane Bowes (SMF8)

Loans & BusinessOfficer

Lauren Humphris

Executive Assistant

Elaine Bowes

15

Dear members Another year has passed of both challenge and achievement for thePentecostal Credit Union. As we entered the final year of our currentstrategic planning cycle (PCU Business Plan 2014-2017), we havecontinued to raise the bar of expectations for achievement at the PCUand we are happy to announce that these initiatives are bearing fruit.

Strategic objectivesGrowth, renewal and improvement remain our three strategic/businessplan objectives up until September 2017 and, as you know, we setchallenging targets to achieve these objectives that are reviewed andrevised each year at the annual Board strategic planning workshop.

After the July 2016 review, we revised the targets upwards again toprovide even greater stretch in the areas of lending, membership andshareholding. We have shown growth in all these areas and we areespecially pleased with the continued growth in membership, running ata current (2017) average of 16 per month as compared with five in 2014,and placing us well on track to achieving this year’s target.

Lending for the financial year of 2015-16 was also above target at £1.65m.

Directors’ report to the membership

Membership growthThe growth in membership for the financial year of 2015-16 is set outon page 16. The increase in lending is outlined in the loans report onpage 25.

The table on the following page demonstrates the growth membershipfrom 2014 together with the six-month average trend.

16

In the final year of our strategic/business plan we are happy to announcethat we are on course to achieve all our overall objectives for growth,renewal and improvement, and to date have attained all but two of the28 specific targets that were designed to deliver the overall objectives.The Board will consider the full delivery report of the 2014-17 businessplan at the annual strategic planning workshop in July 2017.

Revision of PCU valuesAnother key area for revision at the Board strategic planning workshopwere the PCU values. The impetus for this change came from theindependent review of our business through the process to achieve theInvestors in People Award (see below).

The independent assessor observed that our (previous) values of:Transparency; Connecting with the members; Integrity and workingethically; Fairness; Customer first; and Flexibility ‘’...are lived and thatthere is transparency, integrity, fairness, a flexible service, acting withfairness, putting the customer first and connecting with members..’’

However, she further commented that these values are typical and canbe found in most all financial institutions. Indeed, they are expectedbehaviours from a regulatory standpoint. So they did not differentiatethe PCU from other credit unions – that is, they do not demonstrate ouruniqueness and our brand. She recommended a review.

We considered this carefully and, with the assistance of an independentfacilitator, we have adopted the following suite of values.

• Personality: An uncommon warmth and friendliness, with a sprinkleof light-hearted feistiness.

• Empowering: Through financial education of our current and futuremembers, so they proactively take control of their future.

• Faith-based: Our common bond is our faith in God, the Lord JesusChrist and in one another.

• Inspirational: Providing a path to security and prosperity for ourmembers, in an environment without judgement.

• Different: Dare to be different from the pack, fearless andcourageous, a leader and influential in our community.

At this ceremony, we surprised the Rev. Jones with the presentation of theLifetime Achievement Award for his unprecedented vision for the deliveryof financial services to the Pentecostal faith community in Great Britain,and his dedication and commitment to the delivery of that vision, and tomaking this credit union the success it is today. We salute you again, Sir!

17

Office opening and Founder’s Lifetime Achievement AwardAt the AGM last year, Bishop Eric Brown proposed, and the membershipunanimously agreed, that we should honour our founding member, the Rev.Carmel Jones, with a Lifetime Achievement Award. We listened and we did.

On 14 April 2016, we opened the refurbished offices with a re-dedicationceremony officiated by Bishop Delroy Powell from the New TestamentAssembly. The office was formally opened by the Mayor Elect ofWandsworth, Councillor Richard Field.

Supporting the PCU through prayerAnother proposal from the AGM last year was that there should beperiodic prayer meetings to strengthen the work of the PCU. On 14 July2016, the Rev. Jones hosted the first of these ‘PCU Lunch and Pray’events at our offices. He was joined by five senior pastors and leaders ofPentecostal churches, who are also members of the PCU.

The five who joined us for lunch and prayer were the Rev. Currie fromthe United Church of God, the Rev. Jean Pierre from the New TestamentAssembly, the Rev. Brown from the Assemblies of the First Born, the Rev.Bent from New Life Assemblies and Bishop Thomas from Faith Chapel.

The Lunch and Pray sessions will be an annual event at PCU.

18

Investor in People Bronze AwardIn March 2016, the PCU attained the Investor in People Bronze Award.To be recognised as an Investor in People, we have to show that we leadour staff well, offer them the right support and give them the chance toimprove their skills and our organisation.

However, IIP is not only about the staff, but about the health of theorganisation as a whole. The independent assessor commented “... witha supportive new Board, highly committed people and governmentpromoting and funding a credit union initiative, the organisation is in astrong position to expand. There are some significant challenges, howeverthese have been recognised. Notably, there is a great deal of knowledge,experience, passion and motivation in the organisation.

“Key strengths include:

A highly knowledgeable and dedicated CEO

Highly knowledgeable and active Board

Committed people

A culture of continuous learning

The values are lived”

We have implemented a programme to make the changes recommendedfor improvement, and will be aiming for Silver at the review in two years.

19

Achieving excellence in customer servicesOne of our most important objectives is to provide the very best servicesthat we can to you our members. In order to demonstrate that wegenuinely deliver on this commitment, we have commissioned theservices of an independent and expert research company called Accuityto survey all customers who use our services each month by becomingnew members or by taking out a loan.

Accuity provide us with high quality reports, complete with theirindependent and impartial analysis. These reports help us to improve ourservices and engage with you better. They give us better informationabout what you want and what it takes for you to be satisfied with ourservice. They also report back on how you found our performance andmake suggestions for improvement.

We began the process in October last year and it is running verysmoothly. Early reports are extremely positive, but we will report fully onthe year’s activity in the 2017-18 annual report.

Our campaign to increase ourengagement with young peopleMany of you will know that this has been a key focus this year and ourachievements here have been substantial. The motives for ourconcentrated effort in this area are numerous and meet a range ofneeds, for the business of the PCU itself, for our communities and forour young people more generally. Our programmes aim to:

• build loyal members and future customers• address PCU succession planning needs• increase membership• develop leaders for the future for our communities, and• teach good financial habits to improve the financial literacy of our

young people and our communities.

Gimme DatYou will recall that we established the Youth Shadow Board (YSB) lastyear. The YSB initiative is itself an ongoing leadership developmentprogramme in that it continually imparts leadership and financialcapability skills to our member young savers.

You will hear from them in a moment, but one of the first things theydid was to produce the music video Gimme Dat. This was their way ofbeginning a dialogue with other young people about youth materialism.Made with the help of Christian rapper Tneek, the film looks at howmaterialist young people can be. It encourages them to think againabout how they spend their money and become ‘money wise’ instead –because it’s wisdom, not wealth, that gets you through life successfully.It also serves to promote the PCU to a younger customer base. We wouldlike to thank the New Testament Assembly in Tooting, Chic Unique HairSalon in Brixton and Chicken World in Acre Lane Brixton for their help inmaking this video.

#Create AmazingGimme Dat was the focus of a roadshow of Moneywise workshopscalled ‘Let’s Talk about Money’ aimed at young people in Pentecostalchurches up and down the country. By November 2016, the YSBmembers had increased to 11 and youth membership was up by 20%.

In the autumn half term in October 2016, the PCU partnered with theNew Life Assembly Supplementary School (NLASS) to deliver a YouthLeadership and Entrepreneurship Development Programme for ourrespective youth groups. The PCU’s Youth Shadow Board and NLASSembarked on the #Create Amazing programme aimed at developingand empowering our next generation of leaders. The programme wasdesigned to help young people:

• build confidence• enhance their leadership skills• explore their vision and personal aspirations• help them overcome any limiting fears and anxieties, and • develop the right approaches and attitudes, so they can make the

next bold move to create the future they want, whether that be inbusiness, academia or a career.

20

The programme was delivered by RomeoEffs and his team at the Empire BuildersAcademy and consisted of four days ofworkshop tuition at South Bank University,with a final day of site visits, the highlightof which was a visit to Google head officesin Tottenham Court Road. They then hadthree months of 1-2-1 coaching.

PCU at BBC Songs of PraiseThe pinnacle of our work with young people last year was the invitationto take part in BBC Songs of Praise which was aired on 8 January thisyear. The BBC contacted us after they became aware of our work withyoung people through our social media and videos – particularly GimmeDat. They told us that they considered our financial education youthwork to be groundbreaking and, for us, the BBC exposure represented akey milestone in our marketing journey. Our thanks to New Life Assemblyin Dulwich for supporting us on this and enabling filming at their churchpremises.

Our exposure through Songs of Praise has resulted in a host ofinvitations from churches for our ‘Let’s Talk About Money’ workshops –which our evaluations show leads to increased membership.

The Equiano Benevolent Gift Scheme(EBGS)Members will recall that they elected to make a donation to thischaritable fund, run by a group of Christians, at the AGM in 2015. EBGShas been providing a gift of £30 to every young person under the age of18 who wants to open a credit union account. This gift provides the firstdeposit into their share accounts. EBGS has journeyed with us in ourcampaign to increase our engagement with young people and providedinvaluable support for our work. In all, 95% of all our new young saversthis year have come via EBGS. We want to thank the Trustees of thecharity for their remarkable contribution to our work.

21

InternshipsA new area for us has been in providing internships to young people. Aninternship is an opportunity offered by an employer to a studentinterested in the industry. An intern works at the company for a fixedperiod of time, from a week to six months.

Internships offer students a hands-on opportunity to work in theirdesired field. They learn how their course of study applies to the realworld and they build valuable experience that makes them strongercandidates for jobs after graduation. An internship can be an excellentway to ‘try out’ a certain career and, in some colleges, internships alsocount towards course credit.

In the past year we have provided three young people with internships:Emmanuel Sampah, a Finance and Economics undergraduate atBournemouth University; Jabril Issak, aiming for a career in investmentbanking; and, currently, Montelle Bartley, who is a veteran member ofour Youth Shadow Board.

22

The PCU marketing strategy Marketing is the key lynchpin of our growth objectives and we continueto learn and develop our approaches to raising awareness of the PCU inour ‘common bond’ community, building our brand and marketing ourproducts and services.

We have continued to develop our social media presence on YouTube,Facebook, Twitter and LinkedIn, and are developing a presence onInstagram aimed at younger people. We also have additional Facebookand Twitter accounts for our younger market – called PCU Money. Weare gaining approximately 150 new followers a month on Twitter andFacebook and we have 30 videos to view on line on YouTube,showcasing our work.

Our marketing plan is multi-faceted. As well as the social media strategy,we have regular radio advertising on Ruach Radio and occasional advertswith Premier. We have an active sponsorship programme where we canbuy not only advertising space, but also speaking opportunities at keyevents. We also make presentations about our work to church groupsand organisations, as well as the Moneywise roadshows.

Moneywise workshopsOne of the most effective tools for marketing this year has proven to bethe delivery of financial capability workshops to church groups acrossour common bond community, in a series of Roadshows.

In August 2016, the PCU gained accreditation from the National SkillsAcademy in Financial Services, to provide training in financial capability.We developed the concept of ‘Moneywise’ using the government’s edict(Credit Unions Act 1979) to credit unions to provide education to itsmembers in the ‘wise use of money’. Well, we have gone beyond justour members and we provide this service to our common bondcommunity generally – that is the Pentecostal Faith community – as avehicle to also promote our services.

‘Moneywise’ is a programme for adults and there is also a separateprogramme for young people – Let’s Talk About Money. They areinteractive events with case studies, group exercises and role plays. Ourworkshops provide financial capability training, grounded in biblicalprinciples, and we strongly believe that in developing the financialacumen of our membership and our congregations we are building theeconomic wealth of our churches and communities.

In our most recent evaluations on membership, the data shows thatmost people joining the credit union in the past two months have joinedas a result of attendance at a Moneywise workshop. We have plans todeliver these workshops in-house via webinar.

Testimonial“Elaine and Shane delivered a fantastic Let’s Talk About Money workshopto the youth in our church.

“They both were very knowledgeable and passionate about the topic. Bykeeping the workshop interactive, they encouraged interestingdiscussions amongst the attendees and kept them engaged throughout!Everyone learnt something new about being wise with money and we’vealready heard some testimonies from attendees on how they will applythis in their lives.

“The best thing about the workshop is that it was grounded in scriptureand biblical principles.

“PCU are doing a great thing in the UK Pentecostal community. We lookforward to developing a relationship with PCU in the future and heartilyrecommend the workshop to others.

“On behalf of Nu-Life church, I want to say thank you to Elaine, Shaneand the rest of the PCU!

“Thanks again for coming!

“God bless.”

Member developmentThe leadership programme for our young savers prompted a stream ofinterest from our adult members about similar programmes for them –in particular, business development workshops. Research suggests that acommunity’s generational economic empowerment is linked to itsentrepreneurial success. Therefore, if we are serious about improving ourcommunities, increasing our wealth and providing jobs, we mustadvance and strengthen our businesses.

In response to this we are exploring commissioning the delivery of businessdevelopment workshops for our members who are either consideringopening a business, have recently opened a business, or who are alreadybusiness owners but need help/support in developing their business.

If you are interested in being on this programme please let Elaine know,as access will eventually be on a first-come-first-served basis.

23

Independent review of governance at PCUAs part of our commitment to excellent governance we have commissionedan independent governance review to help us assess and evaluate ourgovernance practices and help determine key improvements. This is thefirst of our three, yearly, independent governance reviews, to complementthe yearly skills review and performance appraisal that directors undertake.The first stage of the review utilised the Association of British CreditUnion’s (ABCUL) Code of Governance for Credit Unions as the evaluationframework for our current governance practices. We scored a very goodoverall average of 80.25% in the areas of:

• compliance and continuity • integrity and accountability • skills and ability, and• structure and the principles of good governance.

Regulatory complianceIn accordance with regulatory requirements, we can inform themembership that the PCU has Fidelity Bond Insurance and Public LiabilityInsurance in place. We are also fully compliant with Single CustomerView requirements and we do not carry out any other additionalactivities other than those that we are approved to carry out.

Our thanks Finally, it remains for us to thank those people to whom we owe ourcontinued progress and success. Our staff team – Shane our ChiefExecutive and Lauren our Loans and Business Officer – both of whomremain committed to providing you with the best possible service and todeveloping the organisation to be a beacon credit union that you can beproud of. But most importantly we want to thank you – the members.Your commitment, prayers and devotion continue to be a pillar ofstrength to us. We remain utterly committed to your best interests andto providing you with the best financial services that we can deliver.

Best wishes from the Board of Directors• Leslie Laniyan: Chair• Chona Labor: Vice Chair• Patricia Toussainte: Secretary• Michael Mathura• Lorna Lynch• Verona Richards• Tracey Connage• Ann Waugh: Audit Committee Chair

24

25

Banking fees

The Pentecostal Credit Union (PCU) will be adopting transaction bankingas part of joining the Credit Union Expansion Project.

Transaction banking will allow a PCU member to make payments toanother person or business, or to receive payments from another person orbusiness, directly by logging in to their account. They will be able to dothis either via the PCU website, or by downloading an app that willaccompany the new banking facility at launch. The PCU is expected toroll out transaction banking to members by the end of the year.

A transaction fee of £0.40p will be levied against the PCU each time itremits funds to a member’s account or pays a beneficiary. Each timefunds are deposited into the bank account of the PCU by a memberpaying shares, loan repayments or other creditors, the PCU will becharged £0.01. These costs will represent a significant ongoing expenseto the credit union, which will increase over time as membership increases,and products and services diversify. Please see below for the projectedcosts of the new banking platform and software for the first three years.

We propose that adult members, aged 18 and above, contribute thesum of £2.50 per year as an annual service charge deduction from theirshare accounts, as a contribution towards the estimated annual costs.

£2.50 per year represents good value for money for transaction bankingfacilities, a new app and a new interactive website, with the newfunctionality. Members are, in effect, only making a small contributiontowards the costs of transactions that the credit union will have to pay.

Cost of transformation £ £ £

Cost of ownership Year 1 Year 2 Year 3

Membership/Joining fee 240 240 240

Per member per month fee 10,656 14,479 16,758

Agency banking set up andaccess fees

530 300 6,200

Refunded set up costs 6,200 - -

Product specific fees - creditdecisioning costs

2,946 3,093 3,248

Banking Transaction Fees 3,444 3,616 3,797

Other costs 528 30 331

Total cost of ownership £12,144 £21,759 £30,574

26

Loans report1 October 2015 to 30 September 2016

Month Loans granted (£) Total (£)

October 2015 119,000 119,000

November 2015 142,270 261,270

December 2015 82,050 343,320

January 2016 140,450 483,770

February 2016 86,750 570,520

March 2016 160,700 731,220

April 2016 51,800 783,020

May 2016 97,930 880,950

June 2016 104,750 985,700

July 2016 334,500 1,320,200

August 2016 128,300 1,448,500

September 2016 203,300 1,651,800

TOTAL 1,651,800 1,651,800

IntroductionThe Audit Committee exists to safeguard your interests and ensure theBoard meets all legal and regulatory requirements as well as financialprobity. We scrutinise and audit the Pentecostal Credit Union Limited’s(PCU) practices so that they safeguard your interests, treat you fairly andcomply with the law of the land.

We are not part of the Board and operate completely independently ofit; we are what are known in the sector as non-executive directors. Withthe Financial Conduct Authority (FCA), we have a controlled functionstatus. We are here for you the members.

Each financial year we set out the areas of focus, together with theBoard, based on challenges ahead, listening to members’ feedback,lessons learned from previous audits and new developments in the creditunion sector. The purpose of the Audit and Risk Committee’s Report is toinform the PCU’s members of:

• Results of internal audits during 2015-16• Key lessons and emerging trends from internal audits• Board’s expertise and effectiveness• Audit Plan for 2016-2017• The PCU’s impact

The result of internal audits during 2015-16Leroy Reid and Company Ltd, the internal auditor, covered 14 areas. TheAudit Committee, through the internal audit function, provided regularscrutiny of the PCU’s areas of operations. They work to an annual planthat ensures that the entire business undergoes full scrutiny during thefinancial year. They assess the PCU and score the organisation’sperformance against the policies and procedures in use. The PCU canachieve one of four ratings (which are illustrated in the appendix).

Table 1, on the next page, summarises the assessment ratings the PCUachieved over the financial year 2015-16.

In the 2016 AGM, there was one internal audit report that was overdue– looking at risk assessment and management. This was produced andpresented on 20 May 2016 and was rated ‘reasonable assurance’.

Nine out of 14 audits have been rated ‘substantial assurance’. Five wererated as ‘reasonable’ assurance. The Audit and Risk Committeerecognises that the PCU is doing what it sets out in the policy andprocedures manual and is monitoring itself effectively.

27

Audit Committee report to the AGM1 October 2015 to 30 September 2016

28

TABLE 1: Internal Audits – 2015-2016

Audit focus Assessment

1. Lending process – Q1 Substantial assurance

2. Risk management – Q1 Reasonable assurance

3. Treating customers fairly – Q1 Reasonable assurance

4. Segregation of duties – Q1 Reasonable assurance

5. Business Plan implementation – Q2 Reasonable assurance

6. Lending process – Q2 Substantial assurance

7. Marketing – Q2 Reasonable assurance

8. Provisioning – Q2 Substantial assurance

9. Lending process – Q3 Substantial assurance

10. Treasury management – Q3 Substantial assurance

11. Membership – Q3 Substantial assurance

12. Business Plan implementation – Q4 Substantial assurance

13. Lending process – Q4 Substantial assurance

12. Marketing – Q4 Substantial assurance

Key lessons and emerging trends frominternal auditsThe Audit Committee through the internal audit process aids the PCU tolearn and get better, and gives members reassurance that they are actingin your interests and complying with the law. We looked at how the PCUgoes about meeting your wishes and expectations through the creditunion laws and their own policies and procedures. We also scrutinise theappropriateness of decisions, considering the emerging trends andoriginal vision for the PCU. We also are mindful of the legacy we want topass on to the next generation – future and younger members.

I also consider the challenges organisations of our size and experience face.Thus, the Audit Committee have advised the Board to add two more risksto their radar. The number of risks have been expanded this year to reflectunique features of the UK church sector. The new risks include the PCU’srelationship and connection with stakeholders in the fast-growing segmentof Pentecostal churches in the UK.

In addition, members as a risk area has been added. Although there hasbeen double-digit growth since the PCU started digital marketing,combined with the Roadshow campaign, the growth in the customersegments that we want to attract requires continual management oversight.

Over the past two years, the Audit Committee has reviewed new areasincluding business plan implementation and marketing. The Board hascommissioned a review of governance by Gareth Evans, an independentconsultant. This audit is being overseen by the Remuneration Committee.The report on the PCU’s governance is due to come to a Board meetingby the end of Quarter 2 (2016-17).

The Audit Committee will review the report to ensure compliance. Thefinal report is being drafted, but the scores against the Association ofBritish Credit Union’s (ABCUL) Code of Governance framework indicate ahigh level of performance by the Board in governance at 80.25%. Thisverifies the findings of previous internal audit reports on governance,which scored the Board ‘substantial assurance’.

29

Board expertise and effectivenessBoard dynamics and leadership are critical in supporting a Board’s abilityto carry out its responsibilities effectively. Boards need the rightcombination of skills, experience and training — and to be alert to thefact that the ‘right’ combination changes over time.

High performing Boards need a chair who will ensure the Boardeffectively discharges its responsibilities, and one that uses a processwhich engages directors most productively.

Directors also need to demonstrate the right ‘mind-set’. In a recentreport on Board Effectiveness – what works best (by PwC), a directorcommented that “One of the biggest challenges for a director is beingcourageous — being willing to ask difficult or uncomfortable questions”.This Board of Directors has most of the right skills and tools to addressthe company’s short-term and long-term issues, and a strong chairman.Where possible, we contract in specific competencies such as socialmedia management and PR. The Board has undertaken training in socialmedia to better manage and oversee the PCU’s social media campaigns.

Director attendance at Board meetings 80% in 2015-16.

Audit Plan for 2016-2017Through discussions with the Chair and CEO, noting the news from theAssociation of British Credit Unions Ltd, and a review of the strategicgoals for the PCU, the Audit Committee has identified the follow areasfor review.

The new audit schedule for 2016-2017 is outlined below in Table 2. Theplan and schedule were approved at the September 2016 Board meeting.

Mind set Tool set

Skill set

TABLE 2: Audit Schedule for 2016-2017

Area Q1Oct-Dec

2016

Q2Jan-Mar

2017

Q3Apr-Jun2017

Q4Jul-Sept2017

1. Business plan implementation ü ü

2. Loans ü ü ü ü

3. Marketing & membership ü

4. Conduct of directors notcovered by SMF

ü

5. Provisioning ü

6. Risk assessment &management

ü

7. Segregation of duties ü

8. Treasury management ü

9. Single customer view ü

10. Transformation – softwarecompliance

ü

30

PCU impactOn a more personal note, it is heartening to see the PCU involved indeveloping the leadership skills and financial savviness of our youngpeople, delivering money workshops for better financial managementusing biblical principles and supporting endeavours that help vulnerablepeople through our corporate social responsibility programme.

ConclusionThe Audit Committee has a good professional relationship with theBoard. The Prudential Regulation Authority (PRA) is satisfied with ourwork and I hope you the members are too.

Ann Waugh Chair, the PCU Audit CommitteeFebruary 2017

Appendix 1

Assessment rating Definition

Substantial assurance Robust series of internal controls in place designed to achieve the systemobjectives and which are being consistently applied.

Reasonable assurance Series of internal controls in place, however there are some control improvementsthat would assist in ensuring the continuous and effective achievement of thesystem objectives.

Limited assurance The controls in place are not sufficient to ensure the continuous and effectiveachievement of the system objectives.

No assurance Fundamental breakdown or absence of core internal controls.

PENTECOSTAL CREDIT UNIONLIMITED

DIRECTORS' REPORT

AND FINANCIAL STATEMENTS

FOR THE YEAR ENDED30 SEPTEMBER 2016

FCA REGISTRATION NUMBER213242

COMPANY NUMBERIP00006C

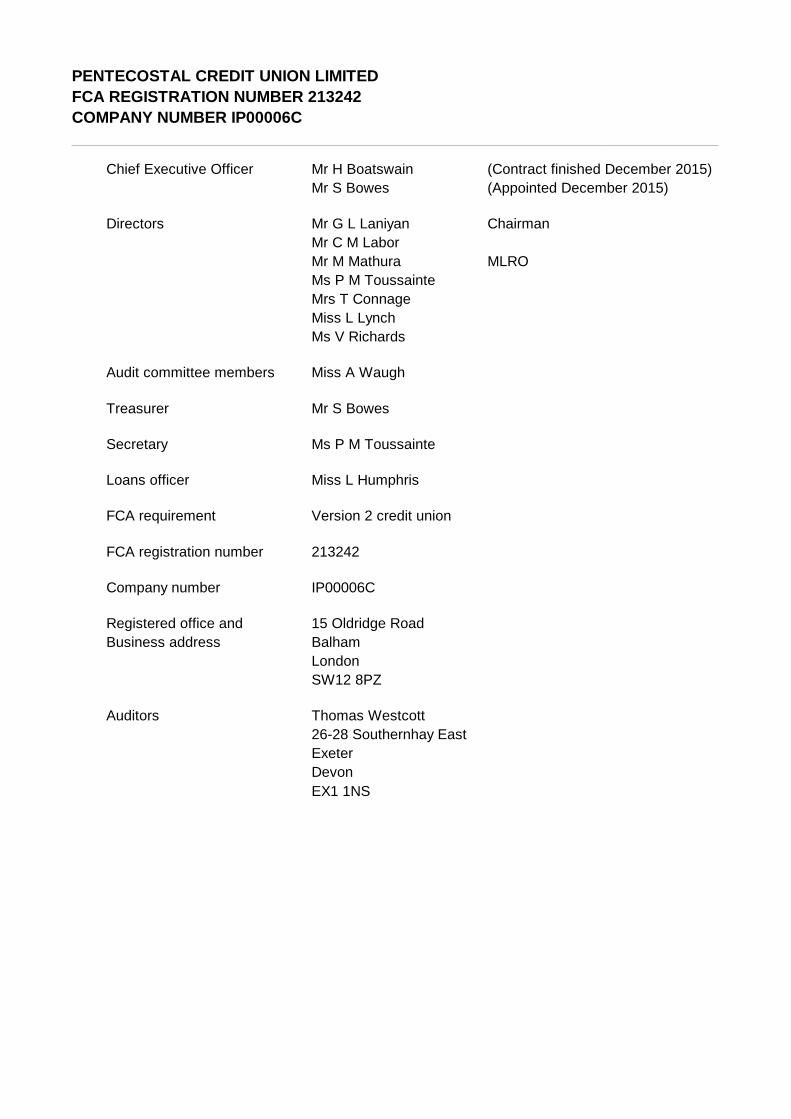

PENTECOSTAL CREDIT UNION LIMITEDFCA REGISTRATION NUMBER 213242COMPANY NUMBER IP00006C

Chief Executive Officer Mr H Boatswain (Contract finished December 2015)Mr S Bowes (Appointed December 2015)

Directors Mr G L Laniyan ChairmanMr C M LaborMr M Mathura MLROMs P M ToussainteMrs T ConnageMiss L LynchMs V Richards

Audit committee members Miss A Waugh

Treasurer Mr S Bowes

Secretary Ms P M Toussainte

Loans officer Miss L Humphris

FCA requirement Version 2 credit union

FCA registration number 213242

Company number IP00006C

Registered office and 15 Oldridge RoadBusiness address Balham

LondonSW12 8PZ

Auditors Thomas Westcott26-28 Southernhay EastExeterDevonEX1 1NS

PENTECOSTAL CREDIT UNION LIMITEDFCA REGISTRATION NUMBER 213242COMPANY NUMBER IP00006C

CONTENTS

Page

Directors' report 1 - 2

Auditors' report 3 - 4

Income and expenditure account 5 - 6

Balance sheet 7 - 8

Statement of changes in retained earnings 9

Notes to the financial statements 10 - 16

PENTECOSTAL CREDIT UNION LIMITEDFCA REGISTRATION NUMBER 213242COMPANY NUMBER IP00006C

DIRECTORS' REPORT

FOR THE YEAR ENDED 30 SEPTEMBER 2016

Page 1

The directors present their report and the financial statements for the year ended 30 September2016.

Principal activityPentecostal Credit Union Limited is regulated by the Financial Conduct Authority as a Version 2Credit Union. It was established for the promotion and encouragement of regular savings and thecreation of credit for the benefit of the members at fair and affordable rates of interest.

DirectorsThe Principal activity of the directors is to be responsible for the delivery of the business of thePentecostal Credit Union and legislative and regulatory compliance. To provide strategic direction tothe staff team and to ensure the best interests of the membership are met.The directors who served during the year are as stated below:

Mr G L Laniyan - ChairMr C M Labor - Vice ChairMs P M Toussainte - SecretaryMr M Mathura - DirectorMrs T Connage - DirectorMiss L Lynch - DirectorMs V Richards - Director

Non- Executive Director:

Miss A Waugh - Chair of Audit Committee

Statement of directors' responsibilitiesThe directors are responsible for preparing the Directors' Report and the financial statements inaccordance with applicable law and regulations.

Co-operative and Community Benefit Societies law requires the directors to prepare financialstatements for each financial year which give a true and fair view of the state of affairs of the creditunion and of the surplus/deficit of the credit union for that period.

In preparing these financial statements, the directors are required to:

- select suitable accounting policies and apply them consistently;- make judgements and estimates that are reasonable and prudent;- prepare the financial statements on the going concern basis unless it is inappropriate to presume

that the company will continue in business.

PENTECOSTAL CREDIT UNION LIMITEDFCA REGISTRATION NUMBER 213242COMPANY NUMBER IP00006C

DIRECTORS' REPORT

FOR THE YEAR ENDED 30 SEPTEMBER 2016

.................... continued

Page 2

The directors are responsible for keeping proper accounting records that are sufficient to show andexplain the credit union's transactions and disclose with reasonable accuracy at any time thefinancial position of the credit union and enable them to ensure that the financial statements complywith Co-operative and Community Benefit Societies Act 2014 and the Credit Union Act 1979. Theyare also responsible for safeguarding the assets of the credit union and hence for taking reasonablesteps for the prevention and detection of fraud and other irregularities.

Each of the persons who is a director at the date of approval of this report confirm that:- so far as each director is aware, there is no relevant audit information of which the credit union's

auditor is unaware; and- each director has taken all steps that they ought to have taken as a director to make themself

aware of any relevant audit information and to establish that the credit union's auditor is aware ofthat information.

This report was approved by the Board on .................................... and signed on its behalf by

Ms Patricia ToussainteSecretary

INDEPENDENT AUDITOR'S REPORT TO THE SHAREHOLDERS OFPENTECOSTAL CREDIT UNION LIMITEDFCA REGISTRATION NUMBER 213242COMPANY NUMBER IP00006C

Page 3

Independent auditors' report to the shareholders ofPentecostal Credit Union Limited

We have audited the financial statements of Pentecostal Credit Union Limited for the year ended 30September 2016 which comprise the income and expenditure account, the appropriation account,the balance sheet and the related notes. The financial reporting framework that has been applied intheir preparation is applicable law and United Kingdom Accounting Standards (United KingdomGenerally Accepted Accounting Practice).

This report is made solely to the Credit Union's members, as a body, in accordance with theCo-operative and Community Benefit Societies Act 2014 and the Credit Union Act 1979. Our auditwork has been undertaken so that we might state to the credit union's members those matters weare required to state to them in an auditors' report and for no other purpose. To the fullest extentpermitted by law, we do not accept or assume responsibility to anyone other than the Credit Unionand the Credit Union's members as a body, for our audit work, for this report, or for the opinions wehave formed.

Respective responsibilities of directors and the auditorsAs explained more fully in the Directors' Responsibilities statement on pages 1 to 2, the directorsare responsibile for the preparation of the financial statements which give a true and fair view. Ourresponsibility is to audit and express an opinion on the financial statements in accordance withapplicable law and International Standards on Auditing (UK and Ireland). Those standards requireus to comply with the Auditing Practices Board's (APB's) Ethical Standards for Auditors.

Scope of the audit of the financial statementsAn audit involves obtaining evidence about the amounts and disclosures in the financial statementssufficient to give reasonable assurance that the financial statements are free from materialmisstatement, whether caused by fraud or error. This includes an assessment of: whether theaccounting policies are appropriate to the credit union's circumstances and have been consistentlyapplied and adequately disclosed; the reasonableness of significant accounting estimates made bythe directors; and the overall presentation of the financial statements. In addition, we read all thefinancial and non-financial information in the director's report to identify material inconsistencies withthe audited financial statements and to identify any information that is apparently materially incorrectbased on, or materially inconsistent with, the knowledge acquired by us in the course of performingthe audit. If we become aware of any apparent material misstatements or inconsistencies weconsider the implications for our report.

Opinion on the financial statementsIn our opinion the financial statements:

- give a true and fair view of the state of the credit union's affairs as at 30 September 2016and of its income and expenditure for the year then ended; and

INDEPENDENT AUDITOR'S REPORT TO THE SHAREHOLDERS OFPENTECOSTAL CREDIT UNION LIMITEDFCA REGISTRATION NUMBER 213242COMPANY NUMBER IP00006C

...................continued

Page 4

- have been properly prepared in accordance with United Kingdom Generally AcceptedAccounting Practice, and with the Co-operative and Community Benefit Societies Act 2014and the Credit Union Act 1979.

Matters on which we are required to report by exceptionWe have nothing to report in respect of the following matters where the Co-operative andCommunity Benefit Societies Act 2014 requires us to report to you if, in our opinion:

- proper books of account have not been kept by the credit union in accordance with therequirements of the legislation,

- a satisfactory system of control over transactions has not been maintained by the creditunion in accordance with the requirements of the legislation,

- the income and expenditure account or the other accounts (if any) to which our reportrelates, and the balance sheet are not in agreement with the books of account of the creditunion,

- we have not obtained all the information and explanations necessary for the purposes ofour audit.

Shona Godefroy FCCA (senior statutory auditor)For and on behalf of Thomas WestcottChartered Accountants and Statutory Auditors26-28 Southernhay EastExeterDevonEX1 1NS

PENTECOSTAL CREDIT UNION LIMITEDREGISTRATION NUMBER 213242

REVENUE ACCOUNT

AND EXPENSES SCHEDULE

FOR THE YEAR ENDED 30 SEPTEMBER 2016

Page 5

2016 2015£ £ £ £

IncomeEntrance fees 735 570Income from loans to members 340,026 322,425Interest received on investments 109,656 69,419Bad debts recovered - 175,395Sundry income 1,996 1,862PCU 35th anniversary celebrations income - 7,754Expansion project income 27,707 3,277

Total income for the year 480,120 580,702

Administrative expensesAdministration expenses 169,569 135,771Data processing expenses 6,588 6,588Fidelity bond insurance 3,875 3,934Consultancy fees 8,460 30,375FCA fees 3,550 6,712Auditors remuneration 9,832 8,608Other legal and professional 70,933 135,407Affiliation fees 1,949 1,813Bank charges 766 675Investment management charges 5,987 -Bad debt provision )(38,606 )(33,788General expenses 73 473PCU 35th anniversary celebrations 3,610 35,991Depreciation of assets 16,887 16,368Profits/losses on disposal of investments 2,566 -Revaluation movement on investments 4,239 -

Total expenditure for the year 270,278 348,927

Surplus/ (Deficit) for the year before taxation 209,842 231,775Taxation 21,931 13,884

Surplus/ (Deficit) for year before appropriations 187,911 217,891

PENTECOSTAL CREDIT UNION LIMITEDREGISTRATION NUMBER 213242

REVENUE ACCOUNT

AND EXPENSES SCHEDULE

FOR THE YEAR ENDED 30 SEPTEMBER 2016

Page 6

Appropriations:Revenue reserve 187,911 217,891Dividend )(104,692 )(71,040

Total applied 83,219 146,851

There are no recognised gains or losses other than those included above.All figures included in the income and expenditure account relate to continuing activities.

PENTECOSTAL CREDIT UNION LIMITEDFCA REGISTRATION NUMBER 213242COMPANY NUMBER IP00006C

BALANCE SHEET

AS AT 30 SEPTEMBER 2016

The notes on pages 10 to 16 form an integral part of these financial statements.

Page 7

2016 2015Notes £ £ £ £

Fixed assetsTangible assets 4 567,701 504,340Investments 5 1,520,065 -

2,087,766 504,340

Members loans 6 5,041,221 4,508,310Less: provision for underperforming loans )(901,900 )(940,506

4,139,321 3,567,804

6,227,087 4,072,144Current assetsPrepayments and accrued income 6,274 6,709Investments 8 2,749,368 3,684,797Cash at bank and in hand 7 364,480 1,783,403

3,120,122 5,474,909

Total current assets 3,120,122 5,474,909

Total assets 9,347,209 9,547,053

LiabilitiesSubscribed share capitalOrdinary members shares 10 6,974,429 7,271,640Junior members shares 10 124,621 120,929Hold shares 10 190 190

7,099,240 7,392,759

Other payables 9 36,710 26,254Revaluation reserve 297,124 297,124Social and educational reserve 115,409 115,409Revenue reserve 518,132 434,913General reserve 1,280,594 1,280,594

Total liabilities 9,347,209 9,547,053

PENTECOSTAL CREDIT UNION LIMITEDFCA REGISTRATION NUMBER 213242COMPANY NUMBER IP00006C

BALANCE SHEET

AS AT 30 SEPTEMBER 2016

The notes on pages 10 to 16 form an integral part of these financial statements.

Page 8

The financial statements were approved by the directors on and signed on its behalf by

Ms P M Toussainte - Secretary

Mr G L Laniyan - Director

Mr C M Labor

PENTECOSTAL CREDIT UNION LIMITEDFCA REGISTRATION NUMBER 213242COMPANY NUMBER IP00006C

STATEMENT OF CHANGES IN RETAINING EARNINGS

FOR THE YEAR ENDED 30 SEPTEMBER 2016

The notes on pages 10 to 16 form an integral part of these financial statements.

Page 9

Revaluation General Revenue Social and reserve reserve reserve educational Total

£ £ £ £ £

At 1 October 2014 297,124 1,280,594 288,062 115,409 1,981,189Dividends paid - - )(71,040 - )(71,040Appropriation of surplus - - 217,891 - 217,891

At 30 September 2015 297,124 1,280,594 434,913 115,409 2,128,040

Dividends paid - - )(104,692 - )(104,692Appropriation of surplus - - 187,911 - 187,911

At 30 September 2016 297,124 1,280,594 518,132 115,409 2,211,259

PENTECOSTAL CREDIT UNION LIMITEDFCA REGISTRATION NUMBER 213242COMPANY NUMBER IP00006C

NOTES TO THE FINANCIAL STATEMENTS

FOR THE YEAR ENDED 30 SEPTEMBER 2016

Page 10

1. Accounting policies

1.1. Accounting conventionThe Credit Union is registered under the Co-operative and Community Benefit Societies Act2014. The financial statements have been prepared under the historical cost convention inaccordance with the Co-operative and Community Benefit Societies Act 2014 and the CreditUnion Act 1979 and comply with financial reporting standards of the the AccountingStandards Board.

In accordance with the regulatory environment for credit unions, deposits from members canbe made by subscription for redeemable shares, deferred shares and interest bearng shares.At present the Credit Union only has redeemable shares.

These financial statements have been prepared in accordance with FRS102, the financialreporting standard applicable in the UK and Republic of Ireland.

1.2. First-time adoption of FRS102These are Pentecostal Credit Union Limited's first financial statement to comply withFRS102. The date of transition to FRS102 is 1 October 2014.

There have been no changes required due the transition due to FRS102.

1.3. Interest All interest payable and receivable is accounted for on an accruals basis.

1.4. TaxationCorporation tax payable is provided on investment income at the current rate.

1.5. Tangible fixed assets and depreciationDepreciation is provided at rates calculated to write off the cost or valuationless residual value of each asset over its expected useful life, as follows:

Land and buildings - 2% reducing balanceFixtures, fittings and equipment- 25% reducing balance

Tangible fixed assets are stated at cost less accumulated depreciation.

PENTECOSTAL CREDIT UNION LIMITEDFCA REGISTRATION NUMBER 213242COMPANY NUMBER IP00006C

NOTES TO THE FINANCIAL STATEMENTS

FOR THE YEAR ENDED 30 SEPTEMBER 2016

.................... continued

Page 11

1.6. InvestmentsInvestments held as fixed assets are revalued at mid-market value at the balance sheet dateand the gain or loss taken to the profit or loss account.

Current asset investments are taken at the lower of cost and net realisable value.

1.7. Financial assets - loans and advances to membersLoans to members are financial assets with fixed or determinable payments, and are notquoted in an active market. Loans are recognised when cash is advanced to members andmeasured at amortised cost using the effective interest method.

Loans are derecognised when the right to recieve cash flows from the asset have expired,usually when all amounts outstanding have been repaid by the member.

1.8. Impairment reviewThe Credit Union assesses at each balance sheet date, if there is objective evidence that anyof its loans to members are impaired. The loans are assessed collectively in groups thatshare similar credit risk characteristics, because no loans are individually significant. Inaddition, if, during the course of the year, there is objective evidence that any individual loanis impaired, a specific loss will be recognised.

Any impairment losses are recognised in the revenue account, as the difference between thecarrying value of the loan and the net present value of the expected cash flows.

1.9. Financial liabilities - subscribed capitalMembers' shareholdings in the Credit Union are redeemable and therefore are classified asfinancial liabilities and described as subscribed capital. They are initially recognised at theamount of cash deposited and subsequently measured at amortised cost.

1.10. Juvenile depositorsJuvenile transactions are included within the financial statements unless specially shownotherwise.

1.11. Cash and cash equivalentsCash and cash equivalents comprise cash on hand and cash and loans and advances tobanks with maturity of less than or equal to three months.

PENTECOSTAL CREDIT UNION LIMITEDFCA REGISTRATION NUMBER 213242COMPANY NUMBER IP00006C

NOTES TO THE FINANCIAL STATEMENTS

FOR THE YEAR ENDED 30 SEPTEMBER 2016

.................... continued

Page 12

2. Auditors' remuneration2016 2015

£ £

External auditors' remuneration - audit of the financial statements 6,084 4,860Internal auditors' remuneration - internal audit services 3,748 3,748

In common with many other Credit Unions of our size and nature we use our auditors toprepare and submit returns to the tax authorities and to assist us with the preparation of thefinancial statements.

3. Tax on profit on ordinary activities

Analysis of charge in period 2016 2015£ £

Current taxUK corporation tax 21,931 13,884

PENTECOSTAL CREDIT UNION LIMITEDFCA REGISTRATION NUMBER 213242COMPANY NUMBER IP00006C

NOTES TO THE FINANCIAL STATEMENTS

FOR THE YEAR ENDED 30 SEPTEMBER 2016

.................... continued

Page 13

Land and Fixtures,4. Tangible fixed assets buildings fittings

freehold equipment Total£ £ £

CostAt 1 October 2015 607,504 48,693 656,197Additions 77,075 3,173 80,248

At 30 September 2016 684,579 51,866 736,445

DepreciationAt 1 October 2015 122,580 29,277 151,857Charge for the year 11,240 5,647 16,887

At 30 September 2016 133,820 34,924 168,744

Net book valuesAt 30 September 2016 550,759 16,942 567,701

At 30 September 2015 484,924 19,416 504,340

5. Fixed asset investments Listedinvestments Total

£ £Cost/revaluationAdditions 1,802,409 1,802,409Disposals )(278,105 )(278,105Revaluations )(4,239 )(4,239

At 30 September 2016 1,520,065 1,520,065

Net book valuesAt 30 September 2016 1,520,065 1,520,065

Historical cost at 30 September 2016 1,473,836

PENTECOSTAL CREDIT UNION LIMITEDFCA REGISTRATION NUMBER 213242COMPANY NUMBER IP00006C

NOTES TO THE FINANCIAL STATEMENTS

FOR THE YEAR ENDED 30 SEPTEMBER 2016

.................... continued

Page 14

6. Members loans 2016 2015£ £

Members loan accounts (see below) 5,041,221 4,508,310Provision for underperforming loans )(901,900 )(940,506

4,139,321 3,567,804

Members loans(including Juniors)

Balances brought forward from last year 4,508,310 4,649,819Repaid )(1,458,915 )(1,694,927Granted 1,651,800 1,235,805Interest charged 340,026 317,613Loans written off - -

5,041,221 4,508,310

7. Cash and cash equivalents 2016 2015£ £

Cash at bank and in hand 364,480 1,783,403

8. Current asset investments 2016 2015£ £

Cash held in investments 2,749,368 3,684,797

PENTECOSTAL CREDIT UNION LIMITEDFCA REGISTRATION NUMBER 213242COMPANY NUMBER IP00006C

NOTES TO THE FINANCIAL STATEMENTS

FOR THE YEAR ENDED 30 SEPTEMBER 2016

.................... continued

Page 15

9. Creditors: amounts falling due 2016 2015 within one year £ £

Trade creditors 14,779 12,371Corporation tax 21,931 13,883

36,710 26,254

10. Subscribed capital - financial liabilities 2016 2015(including Juniors) £ £

Balance brought forward from last year 7,392,759 7,778,177Shares saved and loans repaid 1,314,301 1,472,732Dividends paid 104,692 71,040Shares withdrawn )(1,712,512 )(1,929,190

7,099,240 7,392,759

Analysed as:Ordinary members shares 6,974,429 7,271,640Hold shares 190 190Junior members shares 124,621 120,929

7,099,240 7,392,759

11. Capital commitments 2016 2015£ £

Details of capital commitments at theaccounting date are as follows:

Contracted for but not provided in the financial statements - 39,269

PENTECOSTAL CREDIT UNION LIMITEDFCA REGISTRATION NUMBER 213242COMPANY NUMBER IP00006C

NOTES TO THE FINANCIAL STATEMENTS

FOR THE YEAR ENDED 30 SEPTEMBER 2016

.................... continued

Page 16

12. Related party transactions

Loans can be made to directors, as members of the Credit Union, in the course of businessand on the same terms as are available to other members, in accordance with therequirements of the Financial Conduct Authority.

During the year £48,099 (2015: £42,135) including Employers National Insurance was paid tokey management personnel in respect of remuneration.

During the year, Pentecostal Credit Union paid £43,995 (2015: £29,795) in consultancy feesto mother of a member of key management personnel.

13. Members numbers 2016 2015(including Juniors)

Members as at 30 September 1,691 1,574Junior members as at 30 September 34 29

Total 1,725 1,603

14. Transition to FRS102FRS102 was adopted by the Credit Union for the first time in these financial statements forthe year ended 30th September 2016. No transitional adjustments were required.

And Can it BeAnd can it be that I should gain

An int’rest in the Savior’s blood?

Died He for me, who caused His pain?

For me, who Him to death pursued?

Amazing love! how can it be

That Thou, my God, shouldst die for me?

Amazing love! how can it be

That Thou, my God, shouldst die for me?

2

’Tis mystery all! The Immortal dies!

Who can explore His strange design?

In vain the firstborn seraph tries

To sound the depths of love Divine!

’Tis mercy all! let earth adore,

Let angel minds inquire no more.

’Tis mercy all! let earth adore,

Let angel minds inquire no more.

3

He left His Father’s throne above,

So free, so infinite His grace;

Emptied Himself of all but love,

And bled for Adam’s helpless race:

’Tis mercy all, immense and free;

For, O my God, it found out me.

’Tis mercy all, immense and free;

For, O my God, it found out me.

4

Long my imprisoned spirit lay

Fast bound in sin and nature’s night;

Thine eye diffused a quickening ray,

I woke, the dungeon flamed with light;

My chains fell off, my heart was free,

I rose, went forth, and followed Thee.

My chains fell off, my heart was free,

I rose, went forth, and followed Thee.

5

No condemnation now I dread;

Jesus, and all in Him, is mine!

Alive in Him, my living Head,

And clothed in righteousness Divine,

Bold I approach the eternal throne,

And claim the crown, through Christ my own.

Bold I approach the eternal throne,

And claim the crown, through Christ my own.50

Office opening event 14 April 2016

51

Notes

52

37th Annual General MeetingThe Pentecostal Credit Union Ltd

from 6pm, 11 March 2017

venue Tooting Neighbourhood Centre28 Glenburnie Road London SW17 7PJ

The Pentecostal Credit Union is authorised by the Prudential RegulationAuthority and regulated by the Financial Conduct Authority and thePrudential Regulation Authority (FRN 213242).

The Pentecostal Credit Union Limited

15 Oldridge RoadBalhamLondon SW12 8PL

Phone 020 8673 2542

Email [email protected]

www.pcuuk.com

/pentecostalcreditunion

@PentecostalCU