the path to ind as conversion - deloitte us | audit, … · · 2018-02-24the path to ind as...

TRANSCRIPT

Circulation Only March 2015

The path to Ind AS conversion

May 2015

2

Contents

MCA Notification on Ind AS adoption 3

Summary 6

1. Your Roadmap to Ind AS Conversion 7

2. Overcoming challenges in the Ind AS journey 9

3. Impact of complex standards 13

4. Impact on information technology 18

5. Impact on collateral activities 22

6. Elements to a successful conversion 24

7. Time for action 25

The path to Ind AS conversion 3

MCA Notification on Ind AS adoption

On 16 February 2015, the Ministry of Corporate Affairs (MCA) notified the Companies (Indian Accounting

Standards) Rules, 2015 (the ‘Rules’) (pending publication in the Gazette of India).

Applicability

Mandatory adoption

The following class of companies need to comply with the Ind AS in preparation of the financial statements:

For the accounting period beginning on or

after 1 April 2016 (Phase 1)

For the accounting period beginning on or

after 1 April 2017 (Phase 2)

The following companies will have to adopt Ind

AS for financial statements from the above

mentioned date:

Companies whose equity or debt securities

are listed or are in the process of listing on

any stock exchange in India or outside India

(listed companies) and having net worth of

Rs.500 crores or more

Unlisted companies having a net worth of

Rs.500 crores or more

Holding, subsidiary, joint venture or

associate companies of the listed and

unlisted companies covered above

The following companies will have to adopt Ind

AS for financial statements from the above

mentioned date:

Listed companies having net worth of less

than Rs.500 crore

Unlisted companies having net worth of

Rs.250 crore or more but less than Rs.500

crore

Holding, subsidiary, joint venture or

associate companies of the listed and

unlisted companies covered above

Comparative for these financial statements will

be periods ending 31 March 2016 or

thereafter.

Comparative for these financial statements will

be periods ending 31 March 2017 or thereafter.

Once a company starts following the Ind AS mandatorily on the basis of the criteria specified above, it will be

required to follow the Ind AS for all the subsequent financial statements even if any of the criteria specified do

not subsequently apply to it.

Companies to which Ind AS are applicable should prepare their first set of financial statements in accordance

with the Ind AS effective at the end of its first Ind AS reporting period i.e., companies preparing financial

statements applying the Ind AS for the accounting period beginning on 1 April 2016 should apply the Ind AS

effective for the financial year ending as on 31 March 2017.

The path to Ind AS conversion 4

Voluntary adoption

Companies may voluntarily adopt Ind AS for financial statements for accounting periods beginning on or after

1 April 2015, with the comparatives for the periods ending on 31 March 2015 or thereafter. Once a company

opts to follow Ind AS, it will be required to follow the Ind AS for all the subsequent financial statements (the

option is irrevocable). Once the option to voluntary follow Ind AS is adopted, companies will not be required

to prepare another set of financial statements in accordance with Accounting Standards specified in

Annexure to Companies (Accounting Standards) Rules, 2006.

Non-applicability

The roadmap will not be applicable to:

Companies whose securities are listed or in the process of listing on SME exchanges as referred to in

Chapter XB or on the Institutional Trading Platform without initial public offering in accordance with the

provisions of Chapter XC of the Securities and Exchange Board of India (Issue of Capital and Disclosure

Requirements) Regulations, 2009.

Companies not covered by the roadmap in the “Mandatory adoption” categories above.

Note: SME Exchange to have the same meaning as assigned to it in Chapter XB of the Securities and

Exchange Board of India (Issue of Capital and Disclosure Requirements) Regulations, 2009.

These companies should continue to apply existing Accounting Standards prescribed in the Annexure to the

Companies (Accounting Standards) Rules, 2006, unless they opt for voluntary adoption.

Net Worth

Definition

The definition of "net worth" is as per section 2(57) of the Companies Act, 2013. As per that section, net

worth means the paid-up share capital + reserves created out of the profits (excludes reserves created out of

revaluation of assets, write-back of depreciation and amalgamation) + securities premium account –

accumulated losses – deferred expenditure – miscellaneous expenditure not written off as per the audited

balance sheet.

Dates for consideration of net worth

Net worth to be calculated in accordance with the standalone financial statements of the company as on

31 March 2014 or the first audited financial statements for an accounting period which ends after that date.

For companies that are not in existence on 31 March 2014 or an existing company falling under any of

thresholds specified under 'Mandatory adoption' for the first time after 31 March 2014, the net worth should

be calculated on the basis of the first audited financial statements ending after that date in respect of which

it meets the thresholds. Such companies meeting the specified thresholds for the first time at the end of an

accounting year shall apply Ind AS from the immediate next accounting year.

Example:

Companies covered under Mandatory adoption (Phase 1) for all companies – listed as well as unlisted – with

net worth of Rs.500 crores or more:

Net worth of Rs.500 crores or more met for the first time based on audited

standalone financial statements as at:

31 March 2014 31 March 2015 31 March 2016 31 March 2017

Transition

date

1 April 2015 1 April 2016

Comparative

period

1 April 2015 to 31 March 2016 1 April 2016 to 31 March 2017

Reporting

Period

1 April 2016 to 31 March 2017 1 April 2017 to 31 March 2018

The path to Ind AS conversion 5

Companies covered under Mandatory adoption (Phase 2) for listed companies with net worth of less than

Rs.500 crores and unlisted companies with net worth of Rs.250 crores or more but less than Rs.500 crores:

Net worth of less than Rs.500 crores for listed companies and net worth

of Rs.250 crores or more but less than Rs.500 crores for unlisted

companies met for the first time based on audited standalone financial

statements as at:

31 March

2014

31 March

2015

31 March

2016

31 March

2017

31 March

2018

Transition date 1 April 2016 1 April 2017

Comparative

period

1 April 2016 to 31 March 2017 1 April 2017

to 31 March

2018

Reporting Period 1 April 2017 to 31 March 2018 1 April 2018

to 31 March

2019

Companies who voluntarily adopt:

Company not covered under Phase 1 or Phase 2 of the roadmap, voluntarily

adopting Ind AS:

From 1 April 2015 From 1 April 2016 From 1 April 2017 From April 1 2018

Transition date 1 April 2014 1 April 2015 1 April 2016 1 April 2017

Comparative

period

1 April 2014 to

31 March 2015

1 April 2015 to

31 March 2016

1 April 2016 to

31 March 2017

1 April 2017 to

31 March 2018

Reporting Period 1 April 2015 to

31 March 2016

1 April 2016 to

31 March 2017

1 April 2017 to

31 March 2018

1 April 2018 to

31 March 2019

Applicability to standalone/consolidated financial statements

Once the Ind AS are required to be complied with, they will apply to both standalone financial statements and

consolidated financial statements.

An overseas subsidiary, associate, joint venture, and other similar entity of an Indian company may prepare

its standalone financial statements in accordance with the requirements of the specific jurisdiction. However,

the Indian parent will have to mandatorily prepare its consolidated financial statements in accordance with

the Ind AS if it meets the criteria specified above.

An Indian company which is a subsidiary, associate, joint venture, and other similar entity of a foreign

company should prepare its financial statements in accordance with Ind AS if it meets the criteria specified

above.

Companies to which Ind AS are applicable should prepare their first set of consolidated financial statements

in accordance with the Ind AS effective at the end of its first Ind AS reporting period unless otherwise

specified e.g., companies preparing consolidated financial statements for the accounting period beginning on

or after 1 April 2016 will be required to apply the Ind AS effective for financial year ending on 31 March 2017.

Roadmap for banks, NBFCs, and Insurance companies

Insurance companies, banking companies, and non-banking finance companies will not be required to apply

Ind AS for preparation of their financial statements either voluntarily or mandatorily.

The path to Ind AS conversion 6

Summary

Your Ind AS conversion is a strategic issue. You would need to develop your own roadmap by

considering the key points along the items shown in the diagram below. The board of directors and

management need to explain to the stakeholders on changes and impact arising from the Ind AS

conversion.

Lessons learnt

You can learn the following lessons based on Deloitte’s experience globally in Ind AS/ IFRS conversion

carried out over the past few years.

Most investors believe Ind AS will improve the quality of standalone and consolidated financial

statements.

Large companies that rely more heavily on equity financing perceive the benefits of Ind AS to be

greater than other companies.

Larger companies typically convert earlier and devote considerable resources to educating and

training their boards, staff, and investors.

There is widespread agreement that Ind AS will make financial statements easier to compare across

countries and competitors.

Treat Ind AS not as a purely technical exercise, but a strategic one which requires organisational

commitment.

Effort to convert is often underestimated.

Lead time from announcement to reporting date is short.

Late start to converting often results in escalation of costs.

Striving to achieve “stable” state for Ind AS reporting is important. Change is continuous.

Companies need to take a holistic approach towards Ind AS conversion resulting in an effective

conversion effort.

Impacts of Ind AS conversions are often underestimated.

The conversion process extends beyond accounting to process, people, controls, and technology.

The path to Ind AS conversion 7

1. Your Roadmap to Ind AS Conversion

From our perspective, there are 3 distinct stages to Ind AS implementation: assess your individual situation

and requirements, complete the conversion activities, and sustain ongoing Ind AS reporting.

A successful conversion effort that can stand up to the scrutiny of regulators and analysts will require a

lengthy exercise and commitment.

If there is one thing you can take from reading this document, it is: Develop your Ind AS implementation

roadmap soon.

To kick off this roadmap, we suggest that you ask your team a few preliminary questions. The answers to

these questions should help you gauge the potential effect of Ind AS on your company. For example:

Have we identified main differences between Ind AS and Indian GAAP?

How would an Ind AS conversion affect our business? Would we need to review existing business

contracts?

How many of our business units already understand Ind AS and its related impacts – the skill sets from

which can be leveraged?

How will our financial statements look on a pro forma basis, once converted to Ind AS?

How might our access to capital be affected by an Ind AS conversion?

Do we have a major ERP or finance transformation project which is currently ongoing or envisaged?

Are we involved in or considering a major acquisition?

What is the level of Ind AS knowledge within a company, both domestically and globally?

Have we assessed the cost and benefits of adopting Ind AS?

Do we need to revise the controls framework in order to continuously meet the risk management

objective?

Your Ind AS implementation roadmap will be significantly more detailed than merely addressing these few

questions. Given the far-reaching scope of Ind AS, your roadmap should include assessing the potential

effect on each department in your organisation, including:

Finance

Human Resources

Tax

Legal

Information Technology

Investor Relations

• Analyse impact of Ind AS on standalone and consolidated reporting and accounting policies

• Determine tax implications of Ind AS adoption

• Analyse impact on functional and business processes and controls

• Evaluate the impact on financial systems

• Assess magnitude of

change on organisation

Assess

• Convert to Ind AS at the consolidated and/or standalone reporting level

• Develop a judgment framework for documenting and resolving issues

• Perform tax conversion • Design Ind AS

accounting, reporting, consolidation, and reconciliation processes and controls

• Design future state IT systems to incorporate Ind AS reporting

• Develop change management strategy and revised operating model

• Configure, test, and deliver production environment and monitor system enhancements

• Execute change management activities and implement revised operating model

• Deploy the future state accounting, reporting, consolidation, and reconciliation processes and controls

• Continue monitoring and application of the changing standards environment

• Facilitate knowledge transfer for ongoing Ind AS reporting

Determine vision for Ind AS adoption

Convert Sustain

Perform Comprehensive Ind AS Conversion

Enable continued Ind AS reporting and perform

knowledge transfer

The path to Ind AS conversion 8

Other stakeholders may also be involved, including the board, audit committee, shareholders, your external

and internal auditors and your regulators.

A carefully designed roadmap may empower your company to convert smoothly and effectively. By taking a

measured and informed approach, you increase the likelihood of identifying values in the exercise that

otherwise may be reactive and solely compliance driven. The value may show itself in the form of:

Reduced costs of implementation

Standardisation and centralisation of statutory reporting activities and related controls

Greater consistency of accounting policy application

Possibly core finance transformation

The path to Ind AS conversion 9

2. Overcoming challenges in the Ind AS journey

Potential Ind AS impacts: Key questions for consideration

Ind AS may impact many aspects of a company’s business; there are several questions that companies

should consider, such as:

Governance and controls

What is an appropriate governance model for monitoring Ind AS application?

How will the internal control structure be impacted?

Will additional work be required for internal financial controls reporting?

Information technology

Can the financial systems of the company and its subsidiaries accommodate Ind AS

accounting and reporting requirements? Do they capture the correct data attributes necessary

under Ind AS?

Can the systems handle multi-ledger reporting? During the transition years, both Indian GAAP

and Ind AS financial statements will be required.

Policy and process

How should company best develop and implement a new set of accounting policies that

requires significantly more judgment than Indian GAAP and facilitates consistent application?

Can a company leverage its finance operating model to gain efficiency and effectiveness in

financial reporting?

How will projections, forecasts and budgets and the people that rely on them be impacted?

What are the impacts to the legal contracts, revenue arrangements, contingent consideration

arrangements, bonus plans, debt covenants, and other financing arrangements that have

metrics based on reported numbers?

The path to Ind AS conversion 10

Organisation and people

How will compensation arrangements based on Indian GAAP financial results be impacted

and how should the company best educate people about the change to Ind AS?

How should the company train its employees and educate investors, business partners and

analysts about Ind AS and its impacts?

What are the impacts on other functional areas (e.g., treasury, HR, investor

communications, legal)?

Tax

What will be the impact of differences between Ind AS and Income Computation and

Disclosure Standards (notified by the Central Board of Direct Taxes) on deferred taxes?

Will any of the tax planning structures be impacted?

What will be the impact on the effective tax rate?

When a foreign subsidiary adopts Ind AS, will the value of the net assets fall below

capitalisation requirements for that country?

How are the dividend requirements affected at the subsidiary level?

The path to Ind AS conversion 11

Ind AS conversions – Start Preparing

The earlier you plan for the Ind AS conversion, the more prepared you would be to address the challenges

and reap benefits such as strengthening controls and formulating your policies and procedures. Companies

may consider the following challenges or points of focus in their roadmap to conversion.

Challenges or Points to Focus Leading practices

• Companies will have to convert within a short-

lead time

• Late start often results in escalation of costs

• Do not wait for regulatory mandate to start

preparing

• Train early and build awareness

• Effort necessary is often underestimated

• On the transition date, objective should be to

adopt Ind AS without any disruptions and

therefore achieve “business as usual”

• Adopt an integrated approach — Consider

collateral effects

• Communicate with auditors/other stakeholders

frequently

• Consider effects on tax structures and debt

covenants

• Have a full-time dedicated PMO

• Adopt a multidisciplinary strategic approach

• Align with other finance transformation projects

• Focus should not be to minimise accounting

differences

• Consider accounting substance versus the

easier short-term route

• Post-adoption, companies can leverage

benefits of Ind AS implementation

• Consider using Ind AS now to:

Improve controls over reporting,

More efficiently use resources,

Better manage cash, and

Possibility to use Ind AS financial

statements in other markets due to minimal

carve outs.

• Cultural bias could often impact consistent

application in a global group involving foreign

components

• Standardise policies at the group level

• Set a strong tone at the top

• Issues can be missed if the implementation

focuses solely on resolving identified GAAP

differences

• Be aware of a potential bias to “find” existing

“Indian GAAP” answers within the Ind AS

framework

• Focus on the Ind AS standards as a whole

including the basis for conclusions contained in

IFRS for how the conclusions were drawn

• Consider implementation guidance and similar

material

• Achieve an understanding of the standards as

a whole

• Scoping and developing a roadmap is an

important step in the process but much of the

effort and complexity results from the “Convert”

and “Sustain” activities

• Move from theory to practical application of Ind

AS standards to company-specific transactions

as soon as possible

• Approach transition from multiple angles

• Identify significant transactions from prior years

which required significant accounting analysis

and re-analyse the entire transaction under Ind

AS

The path to Ind AS conversion 12

Challenges or Points to Focus Leading practices

• Maximise use of Ind AS 101 exemptions and

exceptions

• The fair value as deemed cost exemption

should not be underestimated. However the

exemption to use carrying values on the date of

transition to Ind AS for Property, Plant and

Equipment is a big relief

• Careful study of all exemptions required to

understand limitations and applicability

• Financial statement presentation and

disclosure issues should not be

underestimated

• Develop mock first annual and first interim

financial statements early in process

• Include in your plans a strategy for re-mapping

accounts to specific financial statement line

items once the Ind AS compliant financial

statement format is finalised

• Internal management reporting changes

shouldn’t be overlooked

• Communications across the organisation

needs to be very effective

• Personnel outside finance should be integrated

in the conversion process

• Develop specific training for non-finance

personnel

• Establish a formal communication plan to keep

key people outside finance (legal, tax, IT,

investor relations) updated regarding key

deadlines and deliverables

The path to Ind AS conversion 13

3. Impact of complex standards

Ind AS poses technical accounting challenges to companies, particularly for standards like Revenue from Contracts with Customers (Ind AS 115), Financial Instruments (Ind AS 109), Business Combinations (Ind AS 103), Consolidated Financial Statements (Ind AS 110), Joint Arrangements (Ind AS 111), etc. which are more complex than existing standards under Indian GAAP. The following section highlights some of the common accounting issues that are particularly important:

Key Areas Challenges What can companies do?

Revenue from Contracts

with Customers (Ind AS

115) (“new revenue

recognition standard”)

• Timing of revenue and profit

recognition may be

significantly affected by the

new revenue recognition

standard

• Management will need to

exercise significant

judgment particularly in:-

– Identification of

performance obligations

– Allocation of revenue to

each performance

obligation

– Whether revenue should

be recognised at a point

in time or over a period

of time

– Impact of variable

revenues requires

judgment and estimation

Important for companies to

consider how the new

standard specifically applies

to them so that they can

prepare for any changes in

revenue recognition patterns.

• Increased judgment in

determining revenue

recognition policies; an overall

approach to revenue

recognition will need to be

developed, focusing on a

judgment framework

• Ensure consistency of

judgments throughout

organisation

• To comply with the new

standard, companies will have

to gather and track information

that they may not have

previously monitored

• The systems and processes

associated with such

information may need to be

modified to support the capture

of additional data elements

• For internal financial controls

reporting purposes,

management may want to

assess whether it should

implement additional controls

• Companies may also need to

begin aggregating essential

data from new and existing

contracts since many of these

contracts will most likely be

subject to Ind AS 115

• Company-wide training and

communication

• Document basis for

judgments/estimates

(Adequacy of audit trail)

The path to Ind AS conversion 14

Key Areas Challenges What can companies do?

Financial Instruments (Ind AS

109) – Beware of the devil in the

details

• All derivatives must be

recognised in the balance

sheet at fair value

• Financial assets will be

measured either at amortised

cost or at fair value

• Specific requirements for

recognising and measuring

impairment of financial assets

• Specific guidance on the

classification of financing

arrangements as either

shareholders’ equity or debt

on the balance sheet

• Elimination of cost-method

investments subject to certain

exemptions

• Increased disclosures of

companies’ financial risks and

how these are being

measured and managed

• Need to discount expected

cash flows when measuring

impairment for group of loans

• Need to apply hedge

accounting rules, including

maintaining documentation to

meet hedging requirements

• Able to apply netting only if

certain conditions are met

• Need to apply multi-step

model for de-recognition of

financial assets, focusing on

the risk and rewards of

ownership

• Not all financial instruments can

have easily measurable fair

values and therefore valuation

may not be a straight-forward

exercise – build in-house

valuation expertise for simple

valuations and take help from

experts for complex

instruments

• Impairment provisions will

require far more thorough

analysis, including the use of

historic default ratios

• Build internal financial reporting

controls and risk management

processes and systems for

recording fair values

• Impact on systems, processes

and controls will need to be

assessed simultaneously

• Ensure consistency of

judgments throughout

organisation

• To comply with the new

standard, companies will have

to gather and track information

that they may not have

previously monitored

• The systems and processes

associated with such

information may need to be

modified to support the capture

of additional data elements.

• Company-wide training and

communication

• Document basis for

judgments/estimates

(Adequacy of audit trail)

The path to Ind AS conversion 15

Key Areas Challenges What can companies do?

Business

Combinations (Ind

AS 103)

• Fair value measurement of

assets acquired and

liabilities assumed is

complex

• Accounting of acquired tax

contingencies/uncertainties

may impact income tax

calculation

• Processes and data capture for

business combinations may be

more detailed leading to possible

information system changes

• Ensure consistency of judgments

throughout organisation (e.g., fair

value measurement of assets

acquired and liabilities assumed)

• For internal financial controls

reporting purposes, management

may want to assess whether it

should implement additional

controls

• Document basis for

judgments/estimates (adequacy

of audit trail)

• Training at appropriate levels

Consolidated

Financial

Statements (Ind

AS 110) and Joint

Arrangements

(Ind AS 111)

• More judgment in

determining the entities to be

consolidated and the date

when control / joint control

was obtained

• More judgment in

determining whether the

entities are joint operations

or joint ventures

• May trigger acquisition

accounting because of a

decision to consolidate

which may pose challenges

in determining the fair value

of assets and liabilities on

the acquisition date

• Processes and data capture

for disclosures may be more

detailed leading to possible

information system changes

• Efforts needed to align

accounting policies across

subsidiaries

• The need to conform to the

accounting policies and

reporting dates may lead to

changes in financial

information systems and

data capture processes for

controlled entities

• To comply with the new

standard, companies will have to

gather and track information that

they may not have previously

monitored

• The systems and processes

associated with such information

may need to be modified to

support the capture of additional

data elements

• Facilitate consistency of

judgments throughout

organisation

• Documenting the basis for

judgments/estimates (adequacy

of audit trail)

• For internal financial controls

reporting purposes, management

may want to assess whether it

should implement additional

controls

• Organisation-wide training and

communication

The path to Ind AS conversion 16

Key Areas Challenges What can companies do?

Impairment of

Assets (Ind AS

36)

• Increased judgment around

the level at which assets are

tested for impairment

• Processes and controls

around the reversal of

impairment charges will

need to be developed

• Differences in the timing and

amount of impairment

charges may have an impact

on income taxes

• Data capture for an asset’s

recoverable amount may be

more detailed leading to

possible information system

changes

• To comply with the new

standard, companies will have to

gather and track information that

they may not have previously

monitored

• The systems and processes

associated with such information

may need to be modified to

support the capture of additional

data elements

• Documenting the basis for

judgments/estimates (adequacy

of audit trail)

Employment

Benefits (Ind AS

19)

• Accounting for actuarial

gains and losses requires

increased judgment

• Asset celling test is complex

• Don’t forget the timing and

amount of pension costs

impact on income-taxes

• Data capture and processes

for pension plans

disclosures may be more

detailed

• To comply with the new

standard, companies will have to

gather and track information that

they may not have previously

monitored

• The systems and processes

associated with such information

may need to be modified to

support the capture of additional

data elements

• For internal financial controls

reporting purposes, management

may want to assess whether it

should implement additional

controls

Inventory (Ind AS

2)

• Calculation and reversals of

impairments required may

be complex

• Ensuring consistency of

judgments throughout

organisation is vital– for

computing net realisable

value

• The systems and processes

associated with such information

may need to be modified to

support the capture of additional

data elements

• Document basis for

judgments/estimates (Adequacy

of audit trail

Leases (Ind AS

17)

• Determining whether an

arrangement contains a

lease is complex and

requires significant judgment

thereby impacting the

classification of lease

• Processes and data capture for

leases may be more detailed

leading to possible information

system changes

• Evaluate contracts and assess

whether any changes are

required

The path to Ind AS conversion 17

Key Areas Challenges What can companies do?

Property, plant

and equipment

(Ind AS 16)

• Optimum selection of choices

available for cost or

revaluation method

• Componentisation and

calculation of residual values

is time consuming and

complex

• Componentisation and

revaluation may pose specific

challenges for calculating book

tax differences

• Increased judgment (e.g.,

depreciable lives for individual

components)

• To comply with the new

standard, companies will have to

gather and track information that

they may not have previously

monitored

• The systems and processes

associated with such information

may need to be modified to

support the capture of additional

data elements

• Facilitate consistency of

judgments throughout

organisation (e.g.,

componentisation, residual

values)

• Documenting the basis for

judgments/estimates (adequacy

of audit trail)

• Consider cost segregation

studies to maximise tax benefits

associated with component

approach

• For internal financial controls

reporting purposes, management

may want to assess whether it

should implement additional

controls

The path to Ind AS conversion 18

4. Impact on information technology

When addressing the technical accounting challenges, companies may find the Ind AS related issues

such as changes to information technology a challenge. In the roadmap to conversion, companies

should consider areas of overlap with an Ind AS conversion throughout the implementation process

and evaluate the interdependencies in the assessment phase. We have laid down below some of the

common areas of focus and the suggested activities which companies should consider as part of their

assessment on changes required to information technology.

Common areas of focus Suggested activities as part of assessment

Chart of accounts (COA)

structure

• Understand what additional COA may be required under Ind AS

• Understand if there is certain COA detail that might ultimately

facilitate or simplify disclosure requirements under Ind AS

• Map the Ind AS sub ledger impacts to system functionality

• Facilitate COA rationalisation effort so that it is consistent with the

dual reporting approach in the transition phase

New entities potentially

requiring consolidation

• Assess existing legal entity structure and COA under Ind AS

• Consider legal entity structure changes for entities that could

potentially be consolidated under Ind AS

Dual reporting strategy • Develop a dual reporting

• Create journal entry methods/templates to accommodate new

requirements

Ledger interfaces • Understand that the differences in the accounting treatment between

Indian GAAP and Ind AS will likely drive changes to general ledger

design

• Facilitate the conformity of the legal entity structure and the account

structure to accommodate Ind AS reporting

Timeline/roadmap for

implementation

• Mapping/integration of systems and Ind AS roadmaps

The path to Ind AS conversion 19

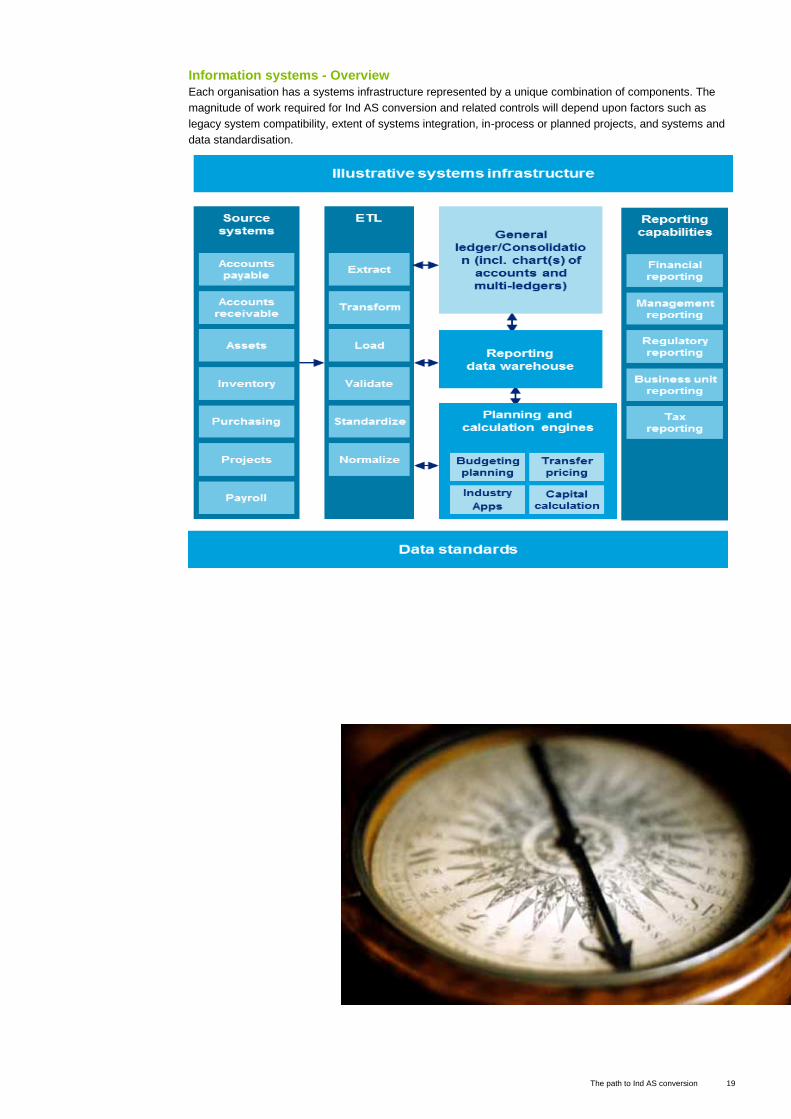

Information systems - Overview

Each organisation has a systems infrastructure represented by a unique combination of components. The

magnitude of work required for Ind AS conversion and related controls will depend upon factors such as

legacy system compatibility, extent of systems integration, in-process or planned projects, and systems and

data standardisation.

The path to Ind AS conversion 20

The potential impact of the four key components on technology is highlighted below.

Upstream — Source

systems and

transformation layer

General ledger and

consolidation

Financial data

warehouse and

processing engines

Downstream —

output, reporting and

decision support

Differences in the

accounting treatment

between Indian GAAP

and Ind AS will create a

need for new input data

Current data and

transactions may not have

all needed attributes or

qualities

Sub-ledgers within the

ERP system may have

additional functionality to

support Ind AS which is

currently not being utilised

and could be

implemented

Transformation layer may

need to be adjusted

Over time the potential for

acquisitions of companies

using Ind AS will increase;

altering ETL tools

(“Extract, transform, load”)

to provide required data

elements could make

integrations more efficient

Differences in the

accounting treatment

between Indian

GAAP and Ind AS

will likely drive

changes to general

ledger design

Companies may

ultimately assess a

need to re-develop

their general ledger

platforms to enable

compliance with

multiple financial

reporting

requirements

(statutory and tax)

Multi-ledger

accounting

functionality within

newer releases of

ERP may be

considered for long-

term solutions

Changes to Ind AS

will likely necessitate

redesigned

accounting,

reporting,

consolidation, and

reconciliation

processes, which

may impact

configuration

Ind AS has more

extensive

disclosure

requirements,

typically requiring

regular reporting

and usage of

financial data that

may not be

standardised in

current data

models

Increased need for

documented

assumptions;

sensitivity analyses

may expand the

scope of

information

managed by

financial systems

Reporting

warehouse feeds

to calculation

engines may need

to be adjusted in a

standardised way

to support

reporting

processes

The differences that

arise in the accounting

treatment between

current accounting

standards and Ind AS

will create a need for

changes in reporting

Assumption changes

from period to period

may require detailed

support for derivation

and rationale for

changes, requiring

additional reports

External reporting

templates will likely

require revisions to

reflect Ind AS

requirements

Changes to data

structures may impact

Key Performance

Indicators (KPI)

production and

balanced scorecards

New information

delivery tools may be

required to meet all

requirements

The path to Ind AS conversion 21

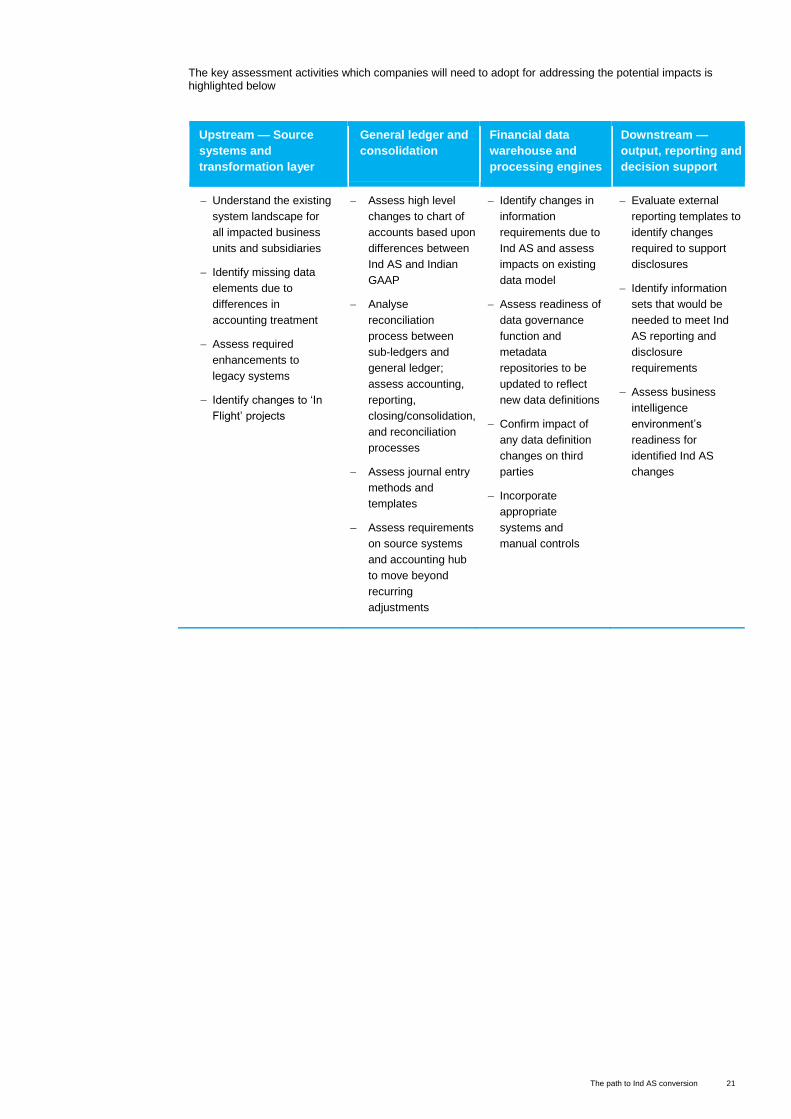

The key assessment activities which companies will need to adopt for addressing the potential impacts is highlighted below

Upstream — Source

systems and

transformation layer

General ledger and

consolidation

Financial data

warehouse and

processing engines

Downstream —

output, reporting and

decision support

Understand the existing

system landscape for

all impacted business

units and subsidiaries

Identify missing data

elements due to

differences in

accounting treatment

Assess required

enhancements to

legacy systems

Identify changes to ‘In

Flight’ projects

Assess high level

changes to chart of

accounts based upon

differences between

Ind AS and Indian

GAAP

Analyse

reconciliation

process between

sub-ledgers and

general ledger;

assess accounting,

reporting,

closing/consolidation,

and reconciliation

processes

Assess journal entry

methods and

templates

Assess requirements

on source systems

and accounting hub

to move beyond

recurring

adjustments

Identify changes in

information

requirements due to

Ind AS and assess

impacts on existing

data model

Assess readiness of

data governance

function and

metadata

repositories to be

updated to reflect

new data definitions

Confirm impact of

any data definition

changes on third

parties

Incorporate

appropriate

systems and

manual controls

Evaluate external

reporting templates to

identify changes

required to support

disclosures

Identify information

sets that would be

needed to meet Ind

AS reporting and

disclosure

requirements

Assess business

intelligence

environment’s

readiness for

identified Ind AS

changes

The path to Ind AS conversion 22

5. Impact on collateral activities

Companies may find Ind AS related issues such as changes to financial performance management,

management reporting and budgeting a challenge. In the roadmap, companies should consider the

potential impacts on these areas in the implementation process

Key Areas Potential impacts What can companies do?

Aligning financial

performance

management

Many management incentive

payments could be based on

“responsibility” reports that

track metrics by business unit

or geography

Results may turn out

differently when prepared

according to Ind AS, which

in turn may affect incentive

and bonus outcomes

Incentive plans may need

to be recalibrated

Compensation plans

(commissions, bonus pools,

etc.) may require realignment

Changes to the technical

accounting process may

require a detailed review of

existing compensations

metrics with potential updates

Companies may want to identify Indian

GAAP to Ind AS differences and

understand impacts on metrics, plans,

and the overall compensation structure

Consider conducting stakeholder

impact analysis

Consider revising incentive plan metrics

based on Ind AS reported results

Consider developing a communication

plan and implementation roadmap for

updates

Aligning management

reporting

An Indian GAAP to Ind AS

reconciliation process is

needed for accurate analysis

and comparison of

management reports, metrics

and projected earnings prior

to transition

We believe new management

reporting KPIs, metrics and

reports may need to be

defined and the changes

communicated

Companies can identify current

accounts and related management

reports impacted by Ind AS

Companies should consider defining

the future state of management

reporting strategy

Companies should understand gaps in

current process to identify additional

management reporting needs (i.e., new

KPIs, metrics, analyses, reports, etc.)

Coordinate with budgeting and

forecasting processes to make

alignment of budget v/s actual reporting

Identify potential implications on how

changes in reporting systems transfer

over to tax systems

The path to Ind AS conversion 23

Key Areas Potential impacts What can companies do?

Aligning budgeting and

financing processes

Planning accounts may need

to be updated and new

business rules may need to

be created for existing

applications

Treatment for certain

accounting areas may require

new operational drivers for

planning purposes

Substantial updates may be

required for the planning

technologies, and multiple

scenarios may be needed to

compare historical plans

(Indian GAAP) and future

plans (Ind AS)

We believe that because the

technical accounting process

will change, tax systems and

process could potentially be

impacted as well

Companies should identify current

budgeting and forecasting processes

impacted by Ind AS conversion

May consider defining an overall

approach and level of detail for the

future budgeting and forecasting

processes (i.e., level that adjustment

are made, changes to corporate and

segment planning, etc.)

May want to revise budgets and

forecasts based on projected Ind AS

financial statement impact

The path to Ind AS conversion 24

6. Elements to a successful conversion

In order to remain focused for a successful conversion, you may want to take note of the following

suggestions:

Identify existing projects you can leverage on

If you are already going through or recently completed an enterprise resource planning (ERP), compliance or a finance transformation project, it may be a good time to consider Ind AS adoption.

Recent versions of major ERP systems conformed data or systems are designed or modified to accommodate Ind AS, which can be mapped in and results in significant cost savings.

Ind AS offers the opportunity to implement standardised frameworks and processes to enhance the overall control environment

Conduct a trial run

If you have many reporting companies or companies located in different countries:

Start a trial run with a single country or reporting company

Use existing reporting requirements to your advantage

Learn from this initial conversion exercise

Apply the lessons learned to your group-wide rollout

Consider shared services centres

Ind AS provides a compelling reason to establish shared services centres so that the geographically-

dispersed finance offices could be:

reduced for a centralised finance function

strategically located to take advantage of tax incentives, payroll savings, and facilitating cost reductions

Re-visit your policies

Ind AS conversion drives the need to re-visit:

Revenue recognition

Impairment

Consolidated Financial Statements and Joint Arrangements

Share-based payments

Cost capitalisation

Other accounting policies It provides a refresh exercise for accounting policy implementation, with the aim for more accurate and timely financial reporting.

The path to Ind AS conversion 25

7. Time for action

The challenge of Ind AS conversion projects will usually be very significant, as the differences between

Indian GAAP and Ind AS are many. With many stakeholders involved, and given the combination of

marketing, financial reporting, human resources, IT, process, controls, tax and risk management issues,

change needs to be managed.

You have a choice: either sit back and wait for it to happen (with all the resultant uncertainty and risk), or

mobilise your company to ensure that you maximise the benefits and minimise the obstacle.

We however feel that, it’s time for leadership. By starting early, you will likely spread out your costs, get

the jump on your competition, and rein in scarce talent before it vanishes. You can improve your

processes and systems. You can integrate with other initiatives, such as an ERP upgrade or a merger or

acquisition. Most importantly, you can do it at a pace that suits your company and its circumstances.

There are major demands on financial and human resources in companies. An Ind AS conversion

project cannot be a distraction from the primary activities of your business. It must be integrated,

coordinated, and aligned. It should start soon with some preliminary questions and a carefully drawn

roadmap. Whether the journey from here to there is rocky or smooth may be entirely up to you.

The path to Ind AS conversion 26

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by

guarantee (“DTTL”), its network of member firms, and their related entities. DTTL and each of its member firms

are legally separate and independent entities. DTTL (also referred to as “Deloitte Global”) does not provide

services to clients. Please see www.deloitte.com/about for a more detailed description of DTTL and its

member firms.

This material and the information contained herein prepared by Deloitte Touche Tohmatsu India Private Limited

(DTTIPL) is intended to provide general information on a particular subject or subjects and is not an exhaustive

treatment of such subject(s) and DTTIPL, Deloitte Touche Tohmatsu Limited, its member firms, or their related

parties (collectively, the “Deloitte Network”) is not, by means of this publication, rendering accounting, business,

financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for

such professional advice or services, nor should it be used as a basis for any decision or action that may affect

your business. Before making any decision or taking any action that might affect your personal finances or

business, you should consult a qualified professional adviser.

No entity in the Deloitte Network shall be responsible for any loss whatsoever sustained by any person who

relies on this material.

© 2015 Deloitte Touche Tohmatsu India Private Limited. Member of Deloitte Touche Tohmatsu Limited