the outstanding mineral endowment of the central andes ... · the outstanding mineral endowment of...

TRANSCRIPT

The Outstanding

Mineral Endowment

of the Central Andes

(Peru-Chile)

Miguel CardozoAlturas Minerals Corp - CP Group S.A.C

José CabelloMineralium

Top Mining

Perumin 2015 , Arequipa

Central Andes: Perú - Chile (north & central)

4.000 km length

300 km average width

1.740.000 km2 area

45 Million inhabitants

US$ 461 billion PBI

US$ 55 billion mining PBI� Highlights of a regional

US$ 55 billion mining PBI

12% of PBI from mining

� Highlights of a regional

approach rather than a

country by country

analysis

� Mineral endowment of

the Central Andes has a

significant geopolitical

importance

Metal

Commodities

Production

(t)

Production Value

(Mill US$)

World prod.

(%)

World

ranking

Copper 7,151,641 35,937 39 1

Gold 203 7,342 7 5

Zinc 1,381,032 2,449 10 3

Silver 4,848 2,202 19 1

Molybdenum 56,855 1,535 21 3

Tin 23,668 385 1 2

Metals – Yearly Production

Tin 23,668 385 1 2

Lead 228,671 384 4 4

TOTAL PRODUCTION 50,234 17

• Copper is largely the main commodity followed by gold

• In a not distant future, the region could exceed the 50% of world’s copper output

• Polymetallic nature of the Central Andes allows convenient diversification of risk

Source:

Others

Commodities

Production

(t)

Production Value

(Mill US$)

World prod

(%)

World

ranking

Rhenium 27 81 54 1

Diatomite 151,999 46 7 4

Arsenic 10,000 7 27 3

Indium 10 7 1 9

Other commodities – Yearly Production

Selenium 110 6 5 8

Cadmium 695 1 3 3

Mercury 19,325 1 1 4

Total Production 149 8

• Other commodities are also produced and the region produces 8% of

the total world’s output of this commodities

Source:

Industrial

Minerals

Production

(t)

Production Value

(Mill US$)

World prod.

(%)

World

Ranking

Phosphates 14,857,263 1,337 6 5

Iodine 20,656,000 785 63 1

Potassium 1,158,403 846 3 7

Borates 806,528 508 15 3

Lithium 60,646 400 36 2

Industrial Minerals – Yearly Production

Lithium 60,646 400 36 2

Salt 6,576,960 362 2 8

Nitrates 759,000 200 100 1

Total Production 4,438 6

• Largest world producers of iodine, lithium and nitrates

• The region produces 6% of the industry minerals in the world

revisar nitratosSource:

Mining Value Prod

(Mill US$)

Percentage Total

(%)

Metals 50,234 91.6

Industrial Minerals 4,438 8.1

Other 149 0.3

Peru-Chile Central Andes

Mining Value Production Summary

Other 149 0.3

Total (US $ Mill) 54,821

• The bulk of the mining production comes from metals

• Industrial minerals represent a small percentage of the mineral production

reflecting the still incipient industrial development of the region

Source:

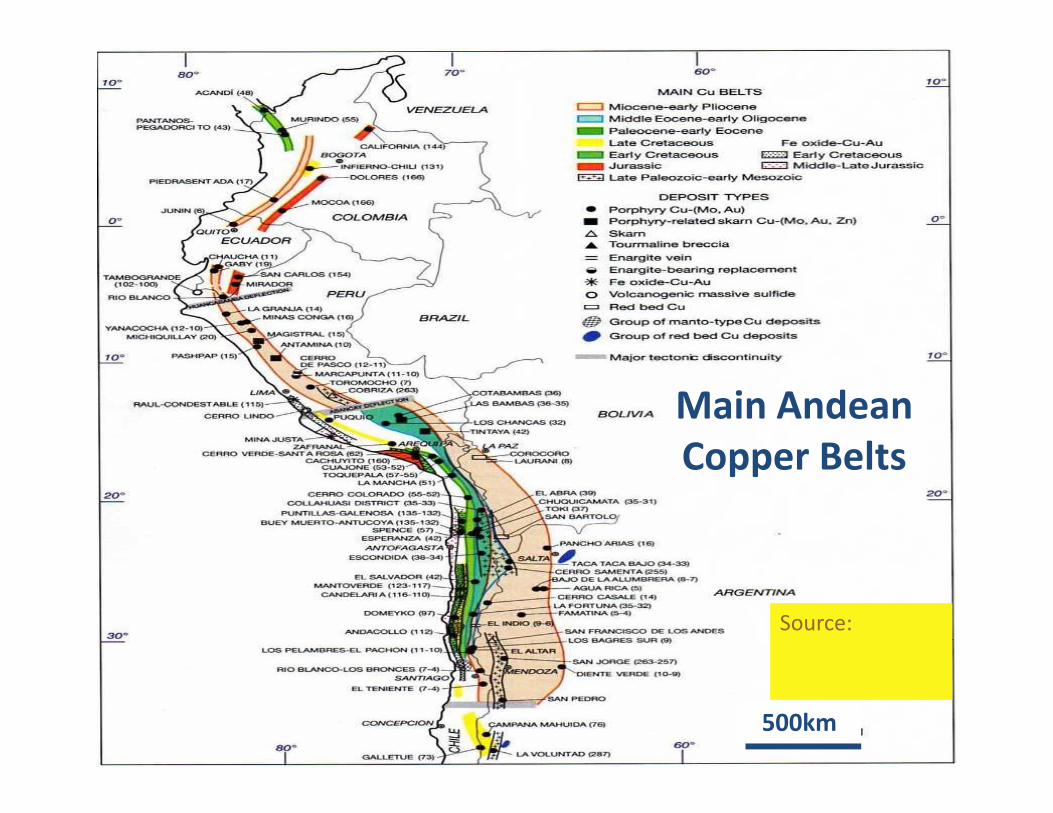

The Peruvian Chilean Andes today

• The topographic expression of the Peruvian-Chilean Andes shows an

intrincate structure that is the result of the interaction of a complex

basement history with active subduction and changing geometry

through time.through time.

• As a result ,different subordinated segments have been recognized,

with distinctive characteristics.

Main AndeanMain Andean

Copper Belts

Source:

500km

QuechuaPhases

Incaic Phases

Peruvian Phose

Mochica Phose

QUATERNARY

TERTIARY

CRETACEDUS

JURASSIC

TRIASSIC

PLIOCENE

MIOCENE

OLIGOCENE

PALEOCENE

UPPER

LOWER

MALM

DOGGER

LIAS

UPPER

LOWER

EOCENE

0

50

100

150

200

Volcanic

Limestone

Coarse clastic

Fine clastic

A thick, mainly late

Pz–Up.K, marine

sed.-volc. sequence.

Followed by a

terrestrial clasticLate HercynianPhoss

Early HercynianPhase

COSTAWESTERN

CORDILLERAALTIPLANO

EASTERN

CORDILLERA

SUBANDEAN

REGION

PERMIAN

CARBONI-

FEROUS

DEVONIAN

SILURIAN

ORDOVICIAN

CAMBRIAN

PRE - CAMBRIAN

PENNSYL-VANIAN

MISSISSIP-PIAN

0 100 200 300 km

250

300

350

400

450

500

550

600

2000

Intense, episodic

magmatism occurred

in the Cordilleran

region. Intrusives range

from deep batholithic

to subvolcanic settings

Source:

M. Cardozo, PDAC 2013

terrestrial clastic

sequence and intense

sub-aereal volcanism

Source:

QuechuaPhases

Incaic Phases

Peruvian Phose

Mochica Phose

QUATERNARY

TERTIARY

CRETACEDUS

JURASSIC

TRIASSIC

PERMIAN

PLIOCENE

MIOCENE

OLIGOCENE

PALEOCENE

UPPER

LOWER

MALM

DOGGER

LIAS

UPPER

LOWER

EOCENE

0

50

100

150

200

Cu Skarn

Cu-Zn VMS

Cu Porphyry

Cu-Au Porphyry

MVT

Peruvian Andean

Metallogenesis

Cu VMS

IOCG

Late HercynianPhoss

Early HercynianPhase

COSTAWESTERN

CORDILLERAALTIPLANO

EASTERN

CORDILLERA

SUBANDEAN

REGION

PERMIAN

CARBONI-

FEROUS

DEVONIAN

SILURIAN

ORDOVICIAN

CAMBRIAN

PRE - CAMBRIAN

PENNSYL-VANIAN

MISSISSIP-PIAN

0 100 200 300 km

250

300

350

400

450

500

550

600

2000

Cu-Zn Skarn

Cu Skarn

Polymet Replac.

Polymet Veins

Mesothermal Au

Epithermal

Geological

diversity

Source:

M. Cardozo, PDAC 2013

QuechuaPhases

Incaic Phases

Peruvian Phose

Mochica Phose

QUATERNARY

TERTIARY

CRETACEDUS

JURASSIC

TRIASSIC

PERMIAN

PLIOCENE

MIOCENE

OLIGOCENE

PALEOCENE

UPPER

LOWER

MALM

DOGGER

LIAS

UPPER

LOWER

EOCENE

0

50

100

150

200

Iron.

Copper

Copper-Gold

Zinc

Polymetallic

Copper-Zinc

Peruvian Andean

Commodity Base

Late HercynianPhoss

Early HercynianPhase

COSTAWESTERN

CORDILLERAALTIPLANO

EASTERN

CORDILLERA

SUBANDEAN

REGION

PERMIAN

CARBONI-

FEROUS

DEVONIAN

SILURIAN

ORDOVICIAN

CAMBRIAN

PRE - CAMBRIAN

PENNSYL-VANIAN

MISSISSIP-PIAN

0 100 200 300 km

250

300

350

400

450

500

550

600

2000

Polymetallic

Tin + Other

Tungsten + Other

Gold-Silver

Polymetallic

Endownment

Source:

M. Cardozo, PDAC 2013

Porphyry systems

Base of lithocap

High-sulfidation Au-Cu

Intermediate sulfidation

Au-Ag (Pb-Zn)

Distal Pb-Zn

Sillitoe, 2010

Economic Geology

Porphyry Cu-Au Proximal Cu-

Au skarn

Pb-Zn skarn

Replacement Zn-Pb-Ag

THIS GEOLOGICAL

FRAMEWORK EXPLAINS

OVER 85% OF THE

MINERAL PRODUCTION

OF PERU

Central Andes (Perú-Chile) Ore Models (17)Deposit Types Relevant Examples

Peru Chile

MVT San Vicente

VMS Tambogrande, Cerro Lindo

Porphyry Cu Toquepala Chuquicamata

Porphyry Au Cerro Corona Marte-Lobo

Porphyry Mo Pashpap Copaquire

Epithermal HS Yanacocha El Indio

Epithermal LS Ares, Antapite El Peñon

Epithermal IS Arcata, OrcopampaEpithermal IS Arcata, Orcopampa

IOCG Mina Justa Candelaria

Polymetallic Replacement Cerro de Pasco

Tin veins San Rafael

Skarn Tintaya, Antamina

Manto type Cu-Ag Arqueros

Mesothermal Au veins Pataz and Nazca-Ocoña districs

W veins Pasto Bueno

Li rich brines Salar de Atacama

Nitrate fields Oficina Victoria

revisar

Andean Countries: Exploration Potential

Largest Copper Reserves in the World

Source: USGS, 2013

Metal

Commodities

Production

% of world’s total

Resources

% of world’s total

Copper 40 40

Gold 7 11

Zinc 10 13

Production and Resources of the Central Andes

Metals

Zinc 10 13

Silver 19 33

Molybdenum 21 20

Tin 10 2

Lead 5 8

Source: USGS, 2015

Other

Commodities

Production

% of World’s total

Resources

% of World’s totalRhenium 54 52

Diatomite 7 -

Arsenic 27 -

Production and Resources of the Central Andes

Other commodities

Arsenic 27 -

Indium 1 -

Selenium 5 32

Cadmium 3

Mercury 1 3

Source: USGS, 2015

Industrial

Minerals

Production

% of world’s total

Resources

% of world’s total

Phosphates 6 1

Iodine 66 24

Potassium 3 52

Production and Resources of the Central Andes

Industrial Minerals

Potassium 3 52

Borates 15 17

Lithium 36 55

Salt 2 3

Nitrates 100 100Revisar

nitratosSource: USGS, 2015

Peru and Chile received 12% of 2014 Exploration

Investment: US$ 1,368 Mill

20

Chile

Peru

Source: (SNL Metals & Mining)

29% of 2014 Copper Exploration Investment

21

Chile

Peru

20%

9%

Source: (SNL Metals & Mining)

45% of 2014 Exploration Investment directed

to Latin America

25%

6%Colombia

Mexico

22

Chile 25%

Peru 20% 11%Brasil

Source: (SNL Metals & Mining)

Production and Resources of the Central Andes

Number of

Projects

Investment

US$Mill

Production

Fine Cu (t)

PERU 29 39,000 3,700,000

CHILE 30 74,000 5,200,000

Total 59 11,3000 8,900,000

Source: USGS, 2015Source: USGS, 2015

Number of

Projects

Investment

US$Mill

Production

Fine Au (t)

PERU 4 5,400 29

CHILE 10 17,000 103

Future Investment in Gold Projects

(2015-2023)

CHILE 10 17,000 103

Total 22,400 132

Source: USGS, 2015

Investment

US$ billion

Share

(%)

Canada 117 15

Australia 100 13

Russia 74 9

Chile 69 9

Brazil 57 7

Peru 49 6

United States 45 6

South Africa

Mining Project Investment by Country, 2013

Source: E&MJ’s Annual Survey of Global

Metal Mining Investment -2014

South Africa 25 3

Mexico 18 2

The Philippines 17 2

TOTAL 571 72

Chile - Peru 118 15

• In 2013, Chile and Peru together account for the largest mining project

investment of the world with US$118 million, more than the planned

investment in Canada and Australia

26• This position is still maintained in 2015

Source:

MAIN DISCOVERIES

(1995-2014)

PERU CHILEMinas Conga (Au, Cu) Spence (Cu, Mo)

Pierina (Au) Gabriela Mistral (Cu, Mo)

Rio Blanco (Cu, Mo) Pascua Lama (Au)

Antapaccay (Cu,Mo) Caserones (Cu, Mo)

Las Chancas (Cu, Mo) Toki (Cu, Mo)

Alto Chicama (Au) El Volcan (Au)Alto Chicama (Au) El Volcan (Au)

Mina Justa (Cu, Au) Caspiche (Au)

Tia Maria (Cu, Mo) Encuentro

Haquira (Cu, Mo) Pampa Escondida

El Galeno (Cu, Mo) Sulfatos (Cu, Mo)

• In 2013, Chile and Peru together account for the largest mining project

investment of the world with US$118 million, more than the planned

investment in Canada and Australia

CONCLUDING REMARKS

• In spite of the current somehow depressed metals market it can be

predicted that the Perú-Chile Central Andes will remain as one of the most

important regions regarding mining ,development and exploration activities

for the foreseeable future.

• Investments will continue to materialize into the region stimulated by the

tremendous success of past mining and exploration achievements.

• Viewed in perspective, these mining, development and exploration

activities have generated significant increase in the Central Andes mineral

resources as well as in production levels with a substantial to the economic resources as well as in production levels with a substantial to the economic

development of Peru and Chile and the creation of new jobs.

• It has also improved technological and service capabilities, as well as the

related infrastructure (access roads, metallurgical plants, smelters, port

facilities and so forth).

• The region appeal is based on several factors: excellent geological

prospectivity, size and grade of deposits still attractive even in critical metals

and minerals price cycles, balanced environmental laws coupled with

gradually improving infrastructure conditions and adequate political-

economic stability despite of increasing internal social and political noisse.

CONCLUDING REMARKS

CONCLUDING REMARKS

• The region appeal is based on several factors: excellent geological prospectivity, size and grade of deposits viable with critical metals and minerals price deposits viable with critical metals and minerals price cycles, balanced environmental laws coupled with gradually improving infrastructure conditions and adequate political-economic stability.

CONCLUDING REMARKS

• As copper prices remain broadly stable or improve, it can be expected that the region discovery record over the next decade will be important at a global scale. the next decade will be important at a global scale.

• And the already discovered resources will remain as one of the key elements affecting worldwide mineral production rates and price.