“the optical market - astoria.noticierotextil.net · “the optical market: gfk ......

TRANSCRIPT

“The Optical Market:

GfK - Growth from Knowledge

1

“The Optical Market:developments, trends and

opportunities”

Paris, 26th September 2013Giampaolo Falconio, Cècile PouletGfK Global Optics

2

GfK belongs to the top five market research companies

3

Sales in mio. dollars

North America

US

Canada

APAC + JAPAN

Japan China (10 Cities)

South Korea

Malaysia

Taiwan

Singapore

13 countries

Europe

APAC 6

GfK Optics Panels: Worldwide Countries Portfolio

4Existing Portfolio

Hong Kong

North America

US

Canada

APAC + JAPAN

Japan China (10 Cities)

South Korea

Malaysia

Taiwan

Singapore

13 countries

Europe

APAC 6

Czech RepublicUkraine

GfK Optics Panels: future expansion

5

Saudi Arabia

UAE

Turkey

Brasil

Existing Portfolio New Openings

Indonesia

IndiaChile

Argentina Australia

Hong Kong

GfK Optics Panels: how does it work?

Track Sell OutTrack Sell Out

First: understand the market structureFirst: understand the market structure

6

Track Sell OutTrack Sell Out

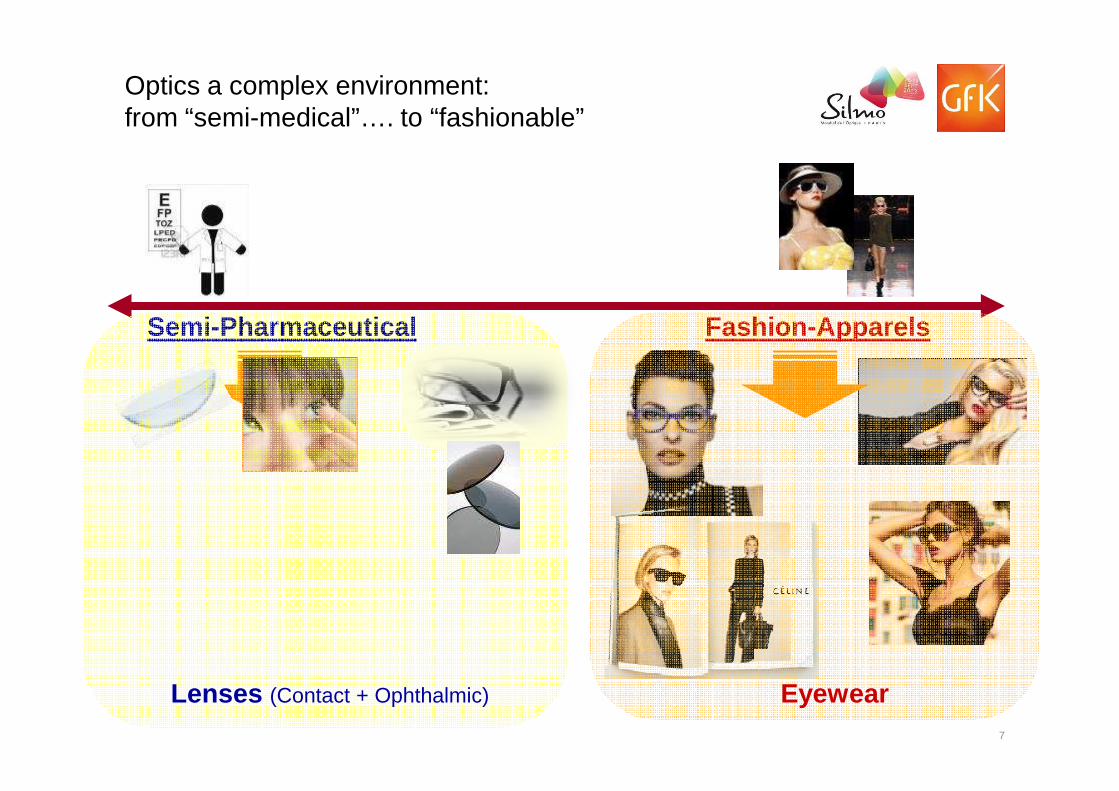

Semi-Pharmaceutical Fashion-Apparels

Optics a complex environment:from “semi-medical”…. to “fashionable”

7

Lenses (Contact + Ophthalmic) Eyewear

Impossibile v isualizzare l'immagine. La memoria del computer potrebbe essere insufficiente per aprire l'immagine oppure l'immagine potrebbe essere danneggiata. Riavviare il computer e aprire di nuovo il file. Se v iene visualizzata di nuovo la x rossa, potrebbe essere necessario eliminare l'immagine e inserirla di nuovo.

CONTACTLENSES + CARE

56,5

9,8

1Half 2013

Spectacle Glasses Spectacle Glasses

Europe 4 Optics market in 1H 2013Optician Turnover Breakdown

8

LENSES + CARE

OPHTHALMICLENSES

SPECTACLEFRAMES

SUNGLASSES

11,8

21,9

7,3 bio €

Spectacle Glasses Core Business

78 %

Spectacle Glasses Core Business

78 %

Gross Domestic Product

9Source: Eurostat http://epp.eurostat.ec.europa.eu/portal/page/portal/eurostat/home//

Private expenses

10Source: Eurostat http://epp.eurostat.ec.europa.eu/portal/page/portal/eurostat/home//

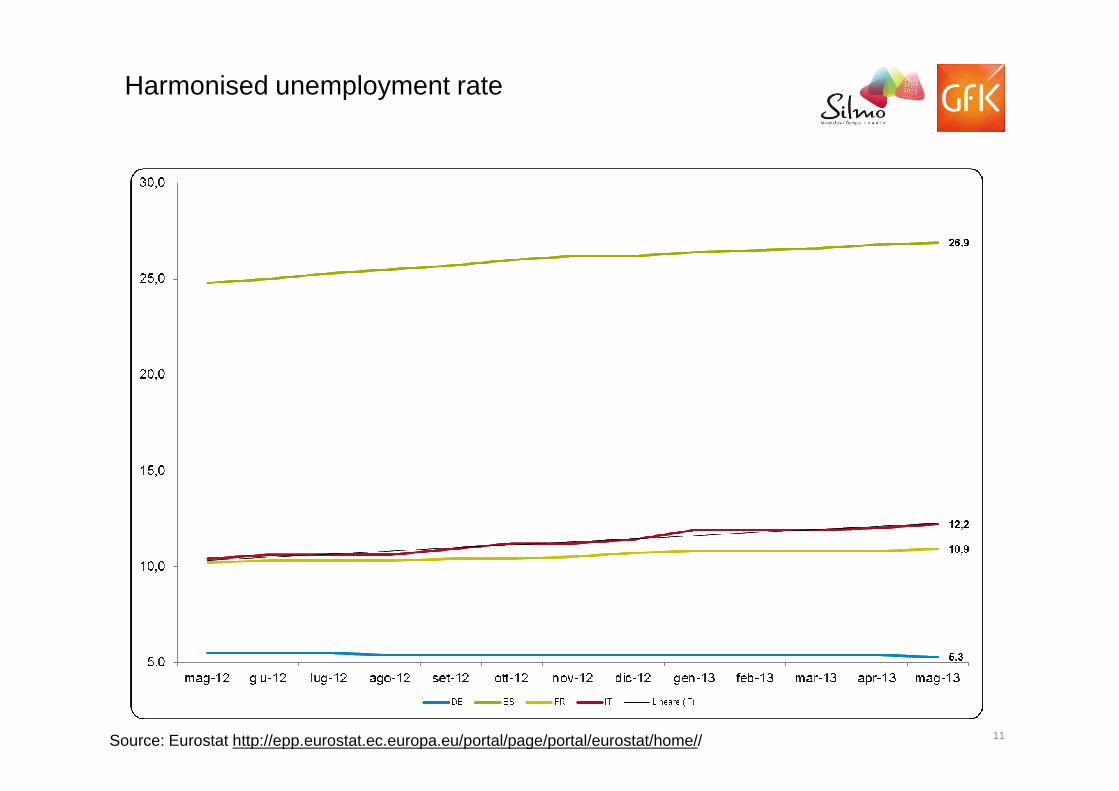

Harmonised unemployment rate

11Source: Eurostat http://epp.eurostat.ec.europa.eu/portal/page/portal/eurostat/home//

1,1 -48,7 -9,7 9,3 -24,4 -43 -33,9 -6,9

36,2 -57,4 -20,2 -25,2 -31,5 -43,7 -41,5 -3,2

36,5 -42,2 -29,5 -49 -25,8 -43,2 -29,6 11,6

Economic Expectations

Income Expectations

Willingness

European consumers in Europe:More shadows than sunshine…

12

36,5 -42,2 -29,5 -49 -25,8 -43,2 -29,6 11,6Willingness to buy

� Poor economic data and High unemployment continue to keep Europe on tenterhooks. The financial and economic crisis has not yet been overcome.

� In most countries, it drives the consumers income expectations & willingness to buy low, though those indicators are stabilizing.

� France is an exception, with pessimism gaining ground, and some of the worst indicators of all Europe.

Source : GfK Consumer Climate – July 2013Methodology : sample between 1000 & 3000 persons according to the countryIndex : balanced score between positive and negative answers on a 5 point scale

1H 2013 vs 1H 2012

Impossibile v isualizzare l'immagine. La memoria del computer potrebbe essere insufficiente per aprire l'immagine oppure l'immagine potrebbe essere danneggiata. Riavviare il computer e aprire di nuovo il file. Se v iene visualizzata di nuovo la x rossa, potrebbe essere necessario eliminare l'immagine e inserirla di nuovo.

CONTACTLENSES + CARE

0%

4%56,5

9,8

1Half 2013

Total Optics Total Optics

Europe4 Optics market in 1H 2013Market Composition and trend - Value

13

LENSES + CARE

OPHTHALMICLENSES

SPECTACLEFRAMES

SUNGLASSES

4%

-2%

-7%

11,8

21,9

7,3 bio €

Total Optics +0.7%

Total Optics +0.7%

+4,0% EU (60% of opticians revenues)

14

Progressive Vs Monofocal EU sales ratio (30/70) is stable

…despite a steady price 2 times higher than the monofocal one!

EU4 frames -2%

↓Licenses (-7%) & House brands↑ Trade brands (19%)

(↑ 120€-149€ & ↑ 150€-199€)

4

15

+14% +6 Licenses+18 House Brands+39 Trade brands

Hipsters style

Opportunity?

180

200

220

240

260

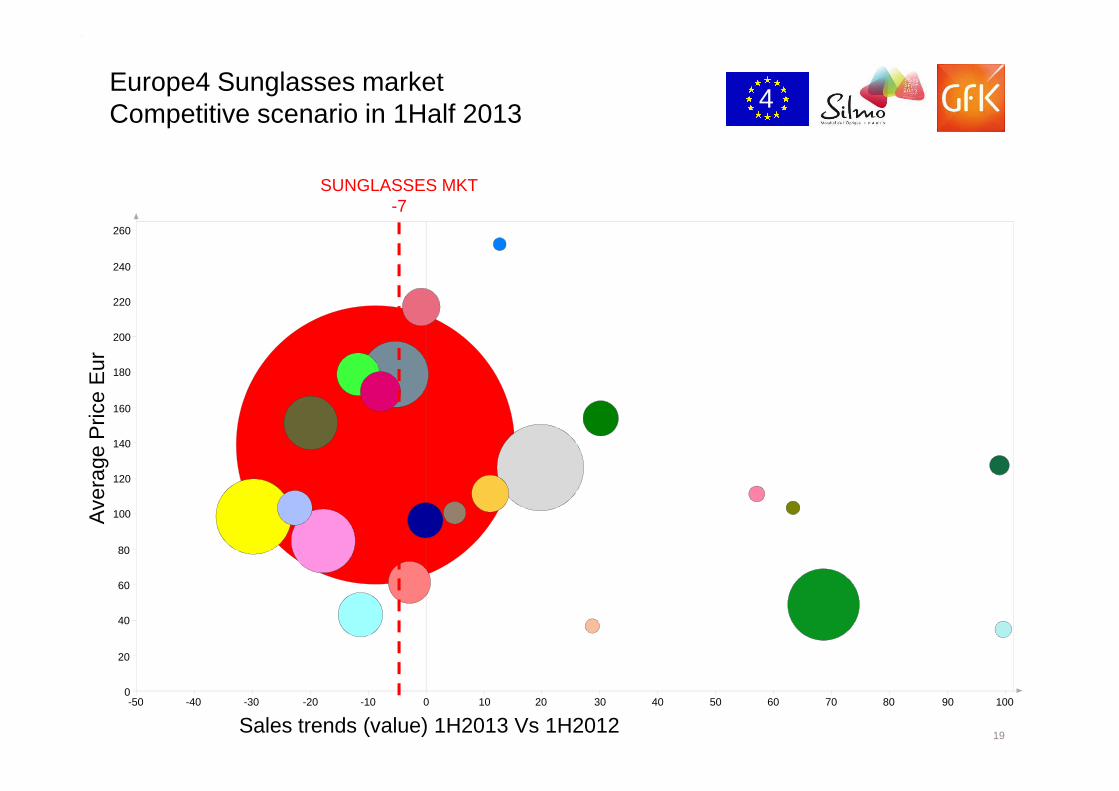

SUNGLASSES MKT-7

Europe4 Sunglasses marketCompetitive scenario in 1Half 2013

Pric

e E

ur4

16

-50 -40 -30 -20 -10 0 10 20 30 40 50 60 70 80 90 100

Sales trends (value) 1H2013 Vs 1H2012

0

20

40

60

80

100

120

140

160

Ave

rage

Pric

e

180

200

220

240

260

SUNGLASSES MKT-7

4P

rice

Eur

Europe4 Sunglasses marketCompetitive scenario in 1Half 2013

17

-50 -40 -30 -20 -10 0 10 20 30 40 50 60 70 80 90 1000

20

40

60

80

100

120

140

160

Sales trends (value) 1H2013 Vs 1H2012

Ave

rage

Pric

e

180

200

220

240

260

SUNGLASSES MKT-7

4P

rice

Eur

Europe4 Sunglasses marketCompetitive scenario in 1Half 2013

18

-50 -40 -30 -20 -10 0 10 20 30 40 50 60 70 80 90 1000

20

40

60

80

100

120

140

160

Sales trends (value) 1H2013 Vs 1H2012

Ave

rage

Pric

e

180

200

220

240

260

SUNGLASSES MKT-7

4P

rice

Eur

Europe4 Sunglasses marketCompetitive scenario in 1Half 2013

19

-50 -40 -30 -20 -10 0 10 20 30 40 50 60 70 80 90 1000

20

40

60

80

100

120

140

160

Sales trends (value) 1H2013 Vs 1H2012

Ave

rage

Pric

e

180

200

220

240

260

SUNGLASSES MKT-7

4P

rice

Eur

Europe4 Sunglasses marketCompetitive scenario in 1Half 2013

20

-50 -40 -30 -20 -10 0 10 20 30 40 50 60 70 80 90 1000

20

40

60

80

100

120

140

160

Sales trends (value) 1H2013 Vs 1H2012

Ave

rage

Pric

e

-10

0

10

2012201220092009 2011201120102010

Consumer Confidence Index (CCI)

20132013

21

-50

-40

-30

-20

Source: Consumer Confidex Index http://epp.eurostat.ec.europa.eu/

1

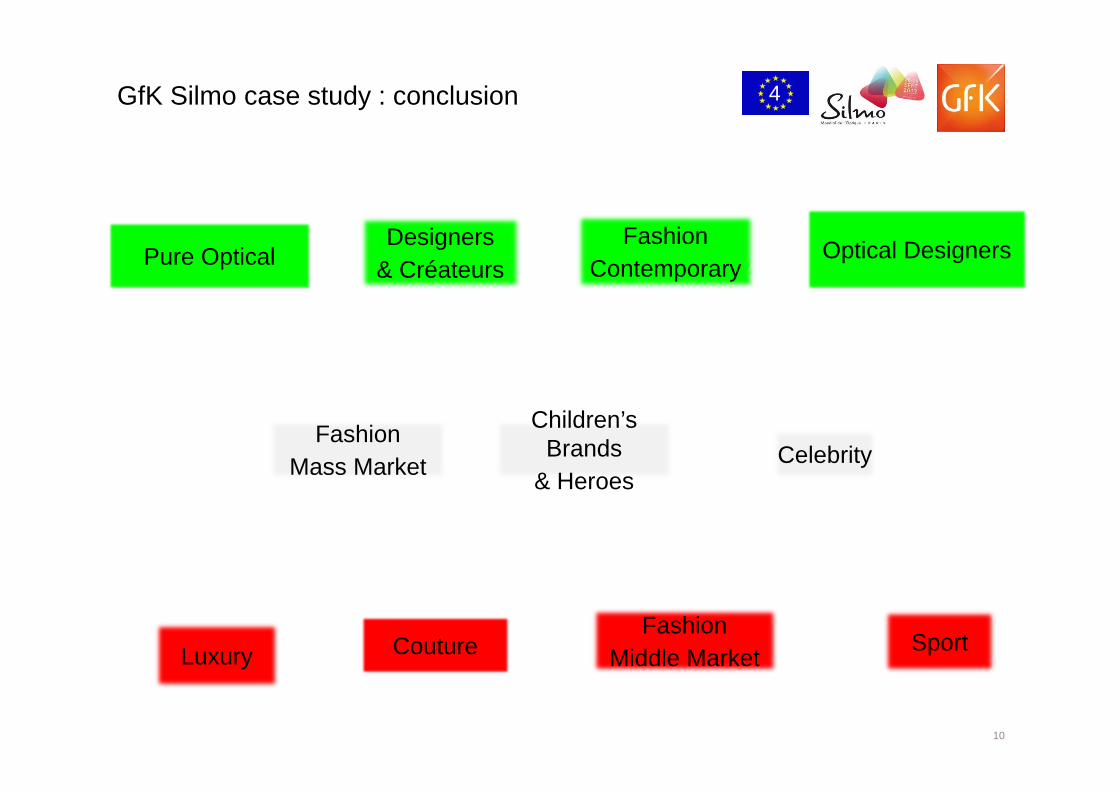

Case studyEyewear Brands segmentation

2

Eyewear in France : the long tail phenomenon

0 200 400 600 800 1000 1200 1400

3

Couture

Pure Optical

Optical Designers

Non complete list

11 brands segmentation ranked by Turnover

MAT June 13

1

2 3

FashionContemporary

FashionMiddle Market

LuxuryFashion

Mass MarketChildren’s Brands

& HeroesCelebrity

Designers & Créateurs Sport

4 5 6 7

8 9 10 11

4

=50% market

4© GfK 2013 - All rights reserved | 9/2013

-40 -30 -20 -10 0 40 50 60100

120

140

160

180

200

220

240

260

280

300

320

Optical Designers

FashionContempory (3,6)

Fashion MiddleMarket (3,7)

Designers & Createurs (3,7)

Luxury (1,7)

Fashion MassMarket (1,5)

Children's Brands and Heroes (0,9)

Celebrity (0,2)

Evol % Sales Value

Sport (3,0)

10 20 30

Top 3 segments

Optical Designers is the only segment growing in €

MAT 2013

Pure Optical

CoutureAver

age

pric

ein

clVA

T

Stable

av price 125€

+2,7% 217€

-18% 190€

5

Children's Brands Heroes

Celebrity

© GfK 2013 - All rights reserved | 9/2013

-40 -30 -20 -10 0 10 20 30 40 50 60-40

-30

-20

-10

0

10

20

30

40

50

60

Couture

Optical Designers

Fashion Contemporary

Fashion MiddleMarket

Designers & Createurs

Luxury

Fashion Mass Market

Evol % Sales Value

Evol

% S

ales

Uni

ts

Sport

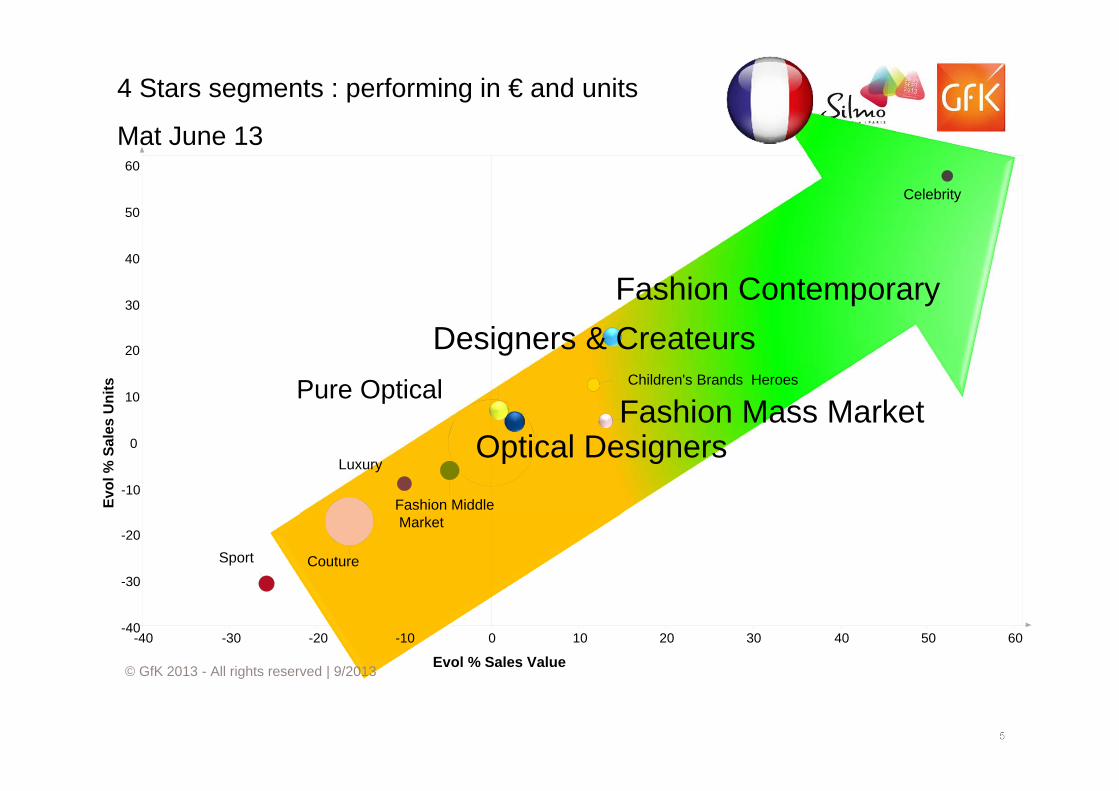

4 Stars segments : performing in € and units

Mat June 13

Pure Optical

6

35 48

55 52

35 42 36

39 40

76 47

<100 EUR 100 - 150 EUR 150-200 EUR >200 EUR

Each segment has its own price positioning

Sales units% by price class

7© GfK 2013 - All rights reserved | 9/2013PRJ 65001 - RG 3727206 - RP 19714204 - ID 390146088

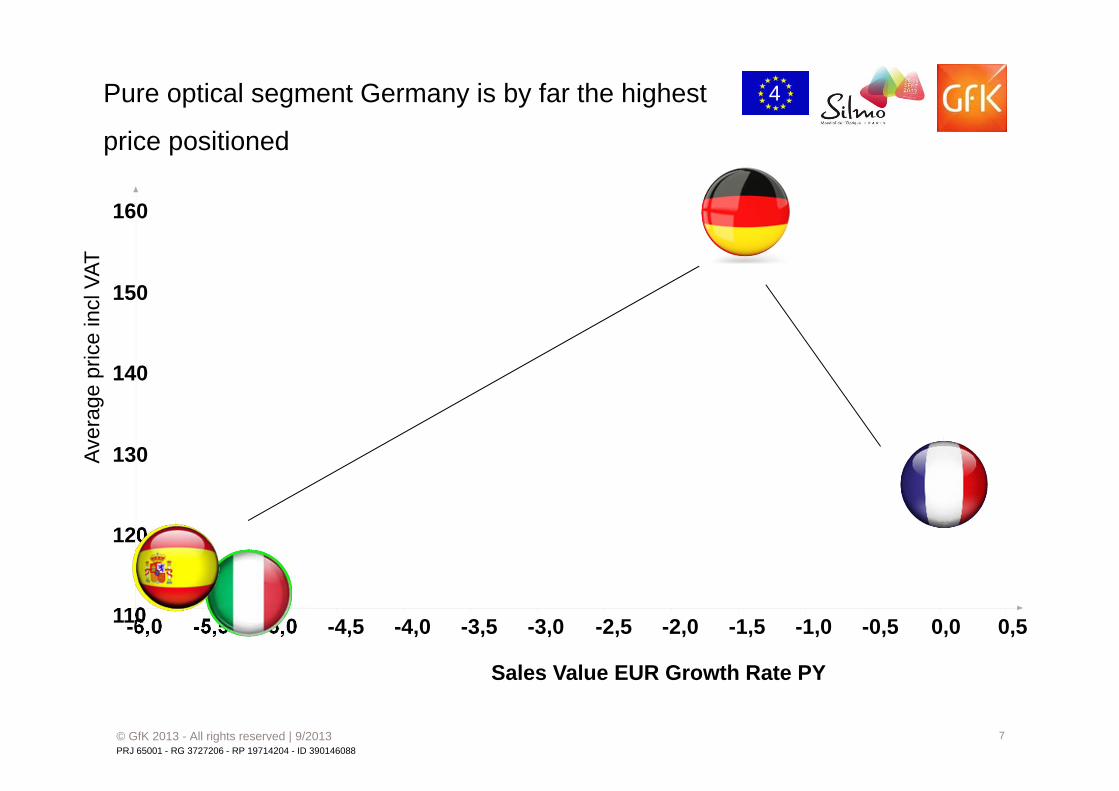

-6,0 -5,5 -5,0 -4,5 -4,0 -3,5 -3,0 -2,5 -2,0 -1,5 -1,0 -0,5 0,0 0,5

Sales Value EUR Growth Rate PY

110

120

130

140

150

160

Pure optical segment Germany is by far the highest

price positioned

4Av

erag

epr

ice

incl

VAT

8

Couture : France, native country, is challenging

Germany but suffering more than Italy

© GfK 2013 - All rights reserved | 9/2013

-18 -17 -16 -15 -14 -13 -12Sales Value EUR Growth Rate PY

145

150

155

160

165

170

175

180

185

190

195

4Av

erag

epr

ice

incl

VAT

9

Designers segments : optical designers are clearly

drivers

-10 -8 -6 -4 -2 0 2 4 6 8 10 12 14 16 18 20 22 24 26 28 30 32

Sales Value EUR Growth Rate PY

120

140

160

180

200

220

240

Optical Designers (

Optical Designers ()

Optical Designers (

Optical Designers

Designers & Createurs

Designers & Createurs

Designers & Createurs 2)

Designers & Createurs

4Av

erag

epr

ice

incl

VAT

10

Couture

FashionContemporary

FashionMiddle Market

Pure Optical

Luxury

FashionMass Market

Children’sBrands

& HeroesCelebrity

Optical Designers Designers & Créateurs

Sport

GfK Silmo case study : conclusion 4

11

THANK YOU

Giampaolo Falconio, Cécile Poulet