the north montney - progress energy canada ltd. north montney daniel topolinsky executive vice...

TRANSCRIPT

The North MontneyDaniel Topolinsky

Executive Vice President,

Exploration & Development

Jim Stannard

Senior Vice President, Development

22

North MontneyEstablished as a World Class Gas Play

Q3 - 2008

• First vertical test

Q1 - 2009

• First horizontal test

Q1 - 2010

• First commercial developments

2011

• 80 producing horizontal wells

• 8 commercial developments

• 3 International joint ventures

Why the Global Interest?

• 300 m gas charged column

• Top tier economics

• Access to North American market & LNG

CYPRESS

FARRELL

TOWNCARIBOU

KOBES

SEPTIMUS

GROUNDBIRCH

DAWSON

SWAN

PARKLAND

3333

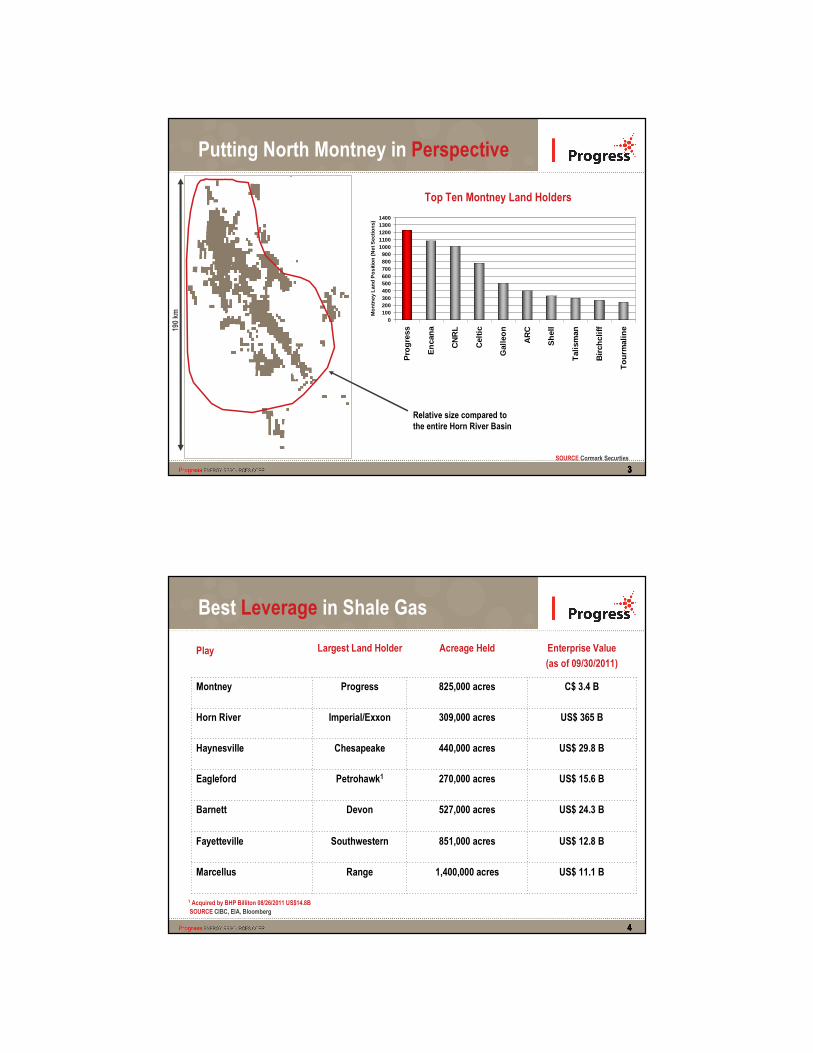

Putting North Montney in Perspective

Relative size compared to the entire Horn River Basin

Top Ten Montney Land Holders

190 km

SOURCE Cormark Securties

0100200300400500600700800900

10001100120013001400

Pro

gre

ss

En

can

a

CN

RL

Cel

tic

Gal

leo

n

AR

C

Sh

ell

Tal

ism

an

Bir

chcl

iff

To

urm

alin

e

Mo

ntn

ey L

and

Po

sitio

n (N

et S

ectio

ns)

190 km

4444

Best Leverage in Shale Gas

Play Largest Land Holder Acreage Held Enterprise Value

(as of 09/30/2011)

Montney Progress 825,000 acres C$ 3.4 B

Horn River Imperial/Exxon 309,000 acres US$ 365 B

Haynesville Chesapeake 440,000 acres US$ 29.8 B

Eagleford Petrohawk1 270,000 acres US$ 15.6 B

Barnett Devon 527,000 acres US$ 24.3 B

Fayetteville Southwestern 851,000 acres US$ 12.8 B

Marcellus Range 1,400,000 acres US$ 11.1 B

1 Acquired by BHP Billiton 08/26/2011 US$14.8B

SOURCE CIBC, EIA, Bloomberg

5

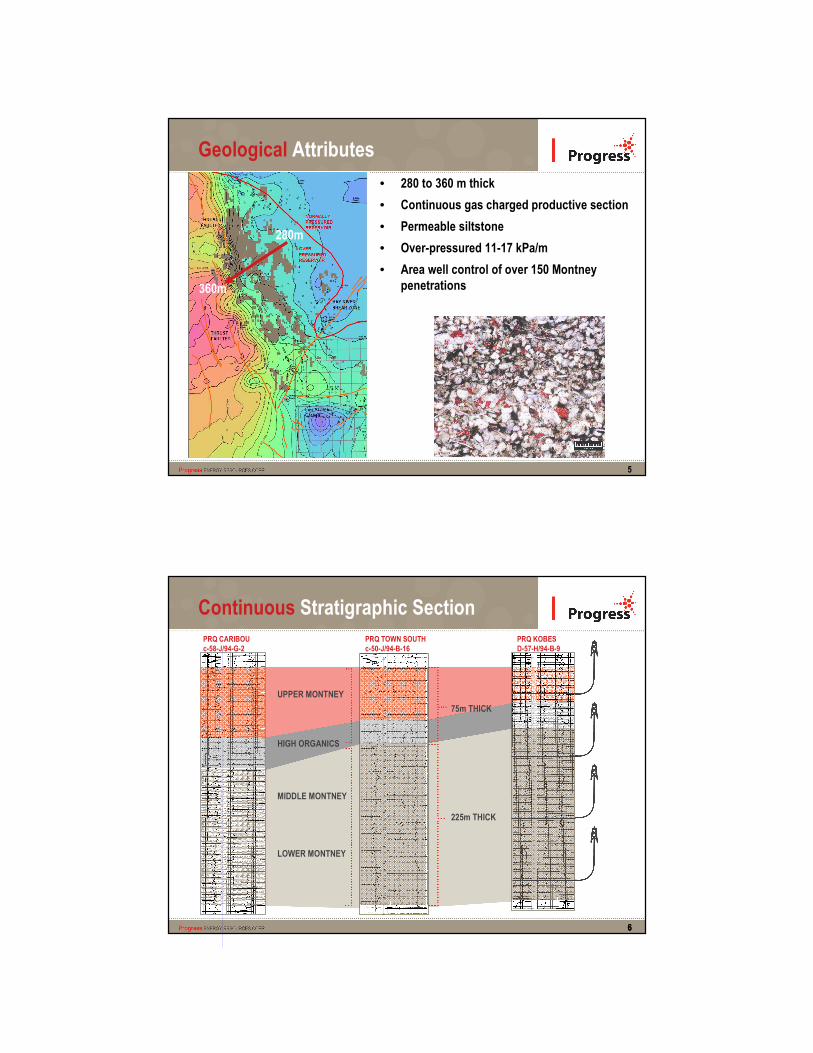

Geological Attributes

• 280 to 360 m thick

• Continuous gas charged productive section

• Permeable siltstone

• Over-pressured 11-17 kPa/m

• Area well control of over 150 Montneypenetrations

280m

360m

66

Continuous Stratigraphic Section

PRQ CARIBOUc-58-J/94-G-2

PRQ TOWN SOUTHc-50-J/94-B-16

PRQ KOBESD-57-H/94-B-9

1940.00

2240.00

1880.00

2240.00

LOWER MONTNEY

UPPER MONTNEY

HIGH ORGANICS

225m THICK

75m THICK

MIDDLE MONTNEY

7777

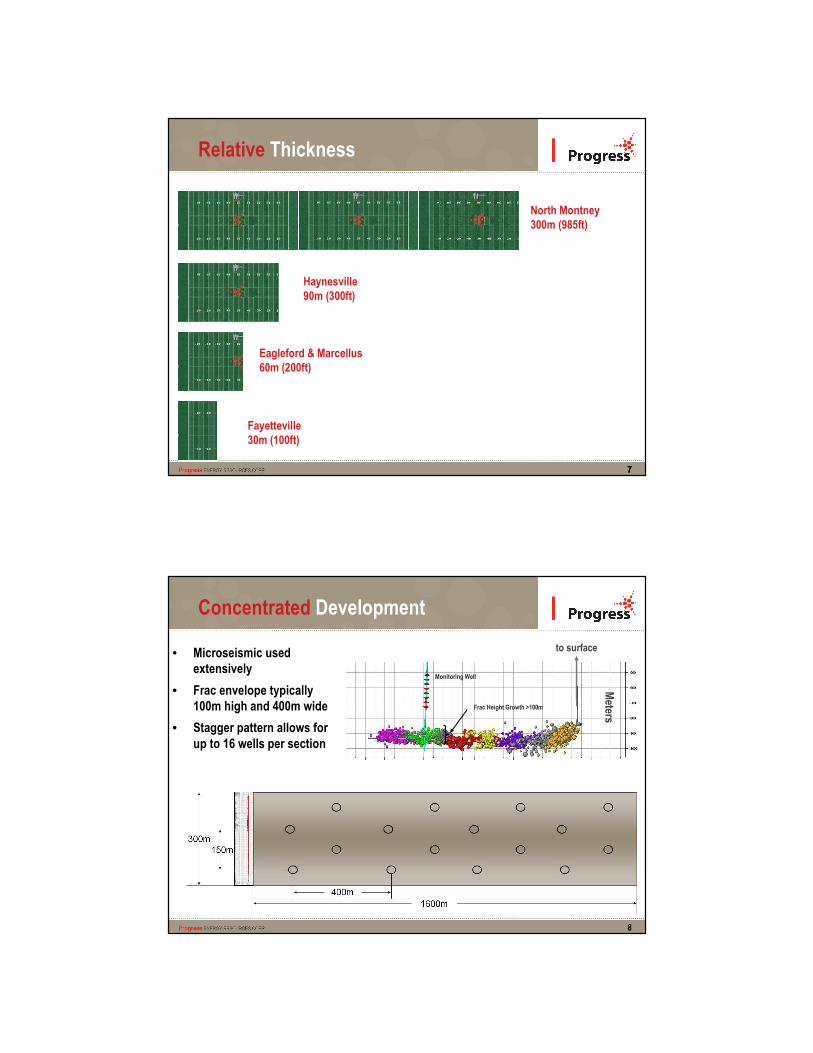

Relative Thickness

North Montney300m (985ft)

Haynesville90m (300ft)

Eagleford & Marcellus60m (200ft)

Fayetteville30m (100ft)

Concentrated Development

Frac Height Growth >100m

Monitoring Well

Meters

to surface• Microseismic used extensively

• Frac envelope typically 100m high and 400m wide

• Stagger pattern allows for up to 16 wells per section

8

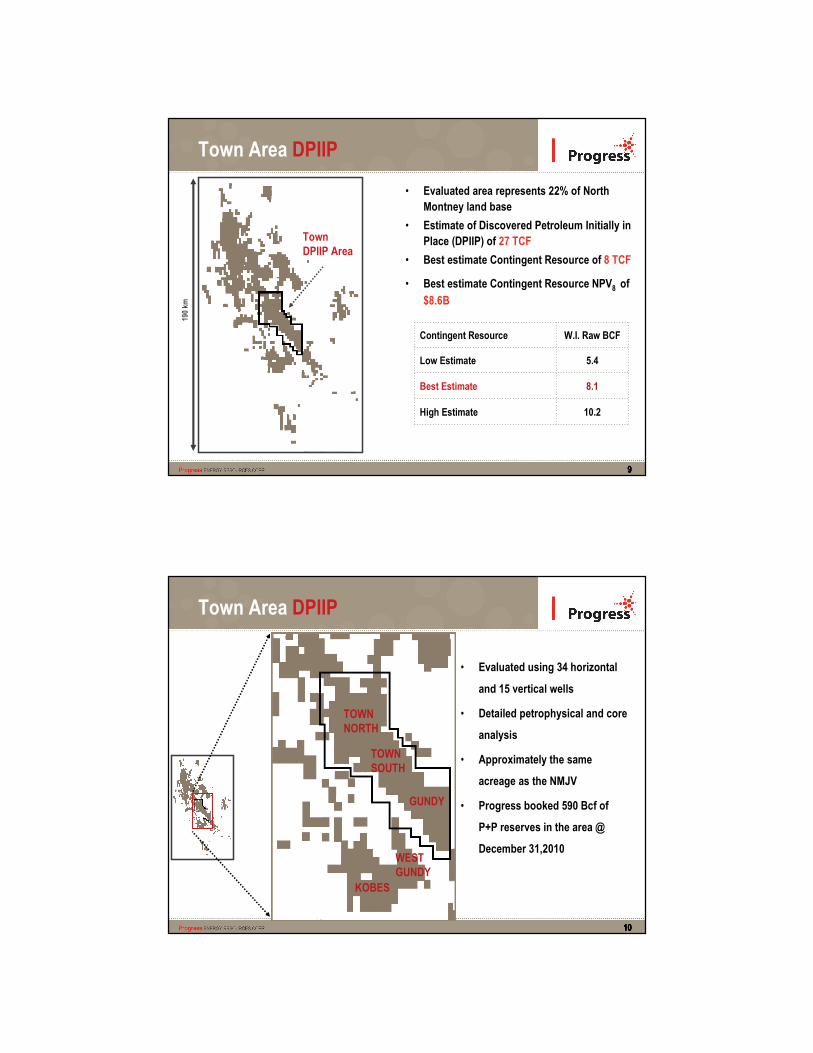

9999

• Evaluated area represents 22% of North

Montney land base

• Estimate of Discovered Petroleum Initially in

Place (DPIIP) of 27 TCF

• Best estimate Contingent Resource of 8 TCF

• Best estimate Contingent Resource NPV8 of

$8.6B

Contingent Resource W.I. Raw BCF

Low Estimate 5.4

Best Estimate 8.1

High Estimate 10.2

TownDPIIP Area

Town Area DPIIP

190 km

10101010

TOWN NORTH

TOWN SOUTH

GUNDY

• Evaluated using 34 horizontal

and 15 vertical wells

• Detailed petrophysical and core

analysis

• Approximately the same

acreage as the NMJV

• Progress booked 590 Bcf of

P+P reserves in the area @

December 31,2010

Town Area DPIIP

KOBES

WESTGUNDY

1111

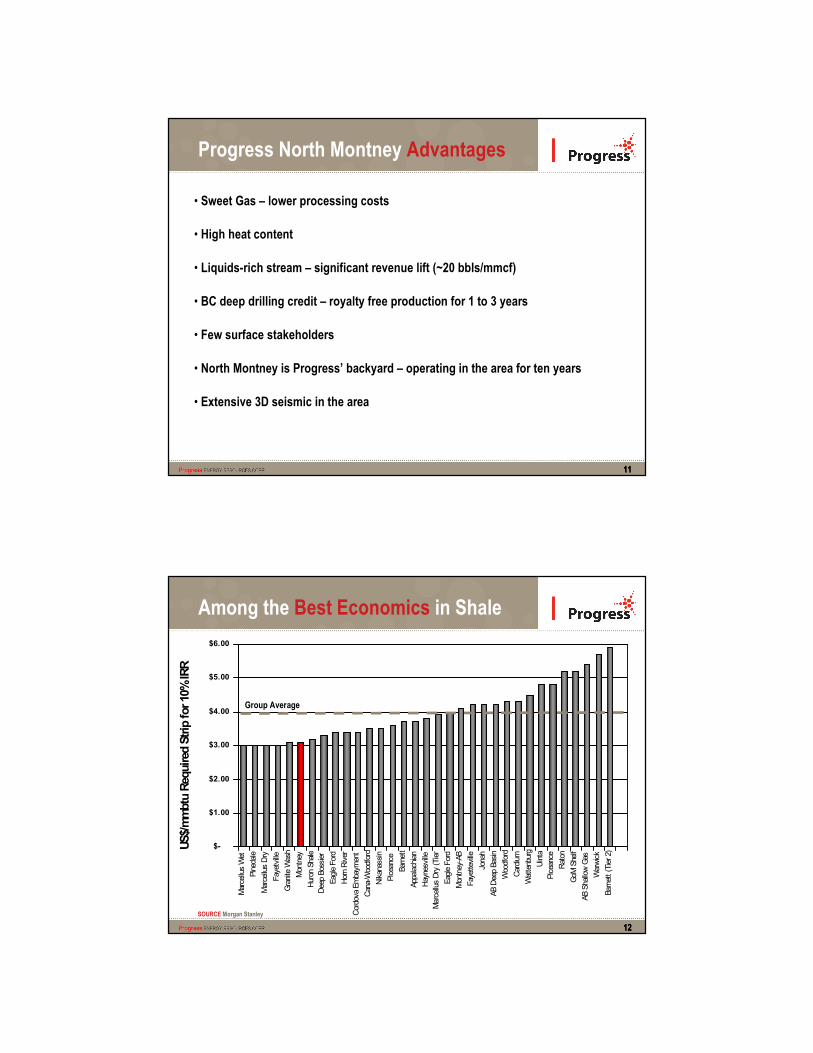

Progress North Montney Advantages

• Sweet Gas – lower processing costs

• High heat content

• Liquids-rich stream – significant revenue lift (~20 bbls/mmcf)

• BC deep drilling credit – royalty free production for 1 to 3 years

• Few surface stakeholders

• North Montney is Progress’ backyard – operating in the area for ten years

• Extensive 3D seismic in the area

1212

Among the Best Economics in Shale

SOURCE Morgan Stanley

$-

$1.00

$2.00

$3.00

$4.00

$5.00

$6.00

US$/mmbtu Required Strip for 10% IRR

Marcellus Wet

Pinedale

Marcellus Dry

Fayetville

Granite Wash

Montney

Huron Shale

Deep Bossier

Eagle Ford

Horn River

Cordova Embayment

Cana-Woodford

Nikanassin

Piceance

Barnett

Appalachian

Haynesville

Marcellus Dry (Tier

Eagle Ford

Montney-AB

Fayetteville

Jonah

AB Deep Basin

Woodford

Cardium

Wattenburg

Uinta

Piceance

Raton

GoM Shelf

AB Shallow Gas

Warwick

Barnett (Tier 2)

Group Average

1313

North Montney has Strong Economics

SOURCE Peters & Co. Limited estimates. Liquids are converted at 6:1.

$-

$1.00

$2.00

$3.00

$4.00

$5.00

Hzl

Mo

ntn

ey B

reak

even

Pri

ces-

Hal

f C

yle

(C$/

mcf

)

Kay

bo

b

PR

Q T

ow

n S

ou

th

Daw

son

/Par

klan

d

Gre

ater

To

wn

Ko

bes

Po

uce

Co

up

e

Sw

an

Gro

un

db

irch

141414

B.C. Deep Drilling Credit

EAST/WEST ROYALTY LINE

• East/West line to account for higher cost to the West

• Progress receives a credit of ~$2MM per well on the

West side

• Results in 1-3 years of royalty free production

• East Montney credit is ~$0.8-1MM per well

• Majority of Progress’ developments qualify for the

higher West credit

1515

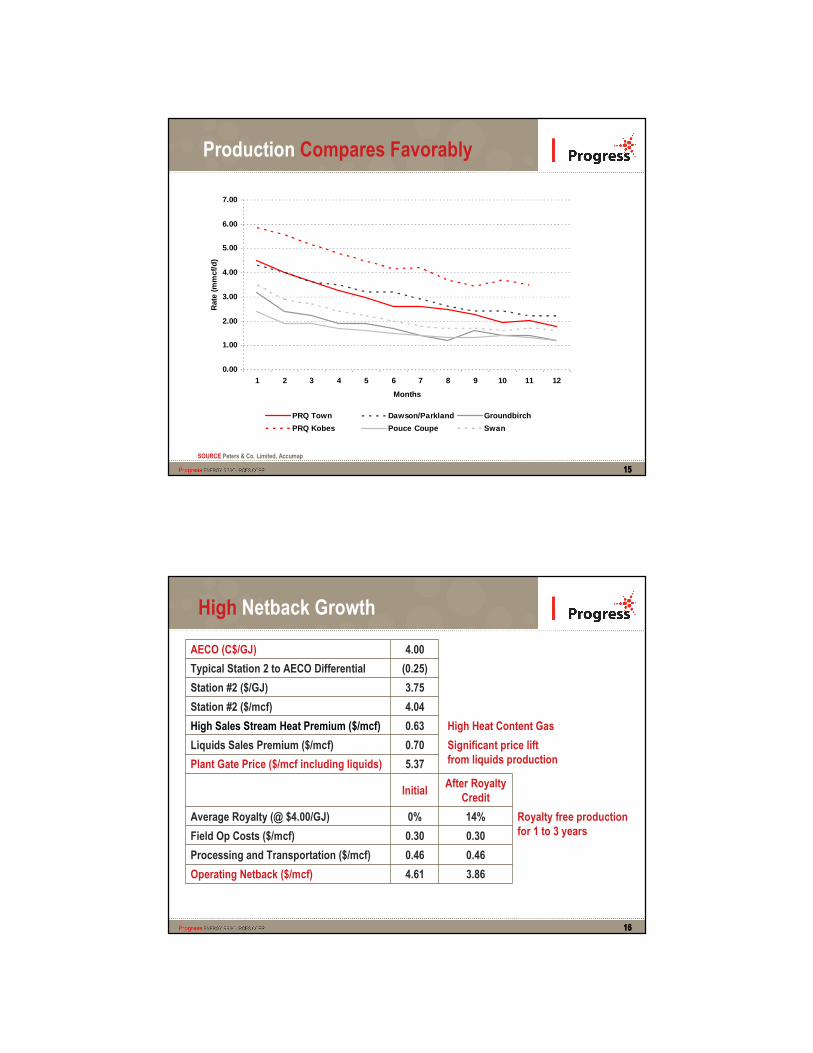

Production Compares Favorably

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

1 2 3 4 5 6 7 8 9 10 11 12

Months

Rat

e (m

mcf

/d)

PRQ Town Dawson/Parkland Groundbirch

PRQ Kobes Pouce Coupe Swan

SOURCE Peters & Co. Limited, Accumap

1616

High Netback Growth

3.75Station #2 ($/GJ)

AECO (C$/GJ) 4.00

Typical Station 2 to AECO Differential (0.25)

Station #2 ($/mcf) 4.04

High Sales Stream Heat Premium ($/mcf) 0.63

Liquids Sales Premium ($/mcf) 0.70

Plant Gate Price ($/mcf including liquids) 5.37

InitialAfter Royalty

Credit

Average Royalty (@ $4.00/GJ) 0% 14%

Field Op Costs ($/mcf) 0.30 0.30

Processing and Transportation ($/mcf) 0.46 0.46

Operating Netback ($/mcf) 4.61 3.86

High Heat Content Gas

Significant price lift from liquids production

Royalty free production for 1 to 3 years

1717

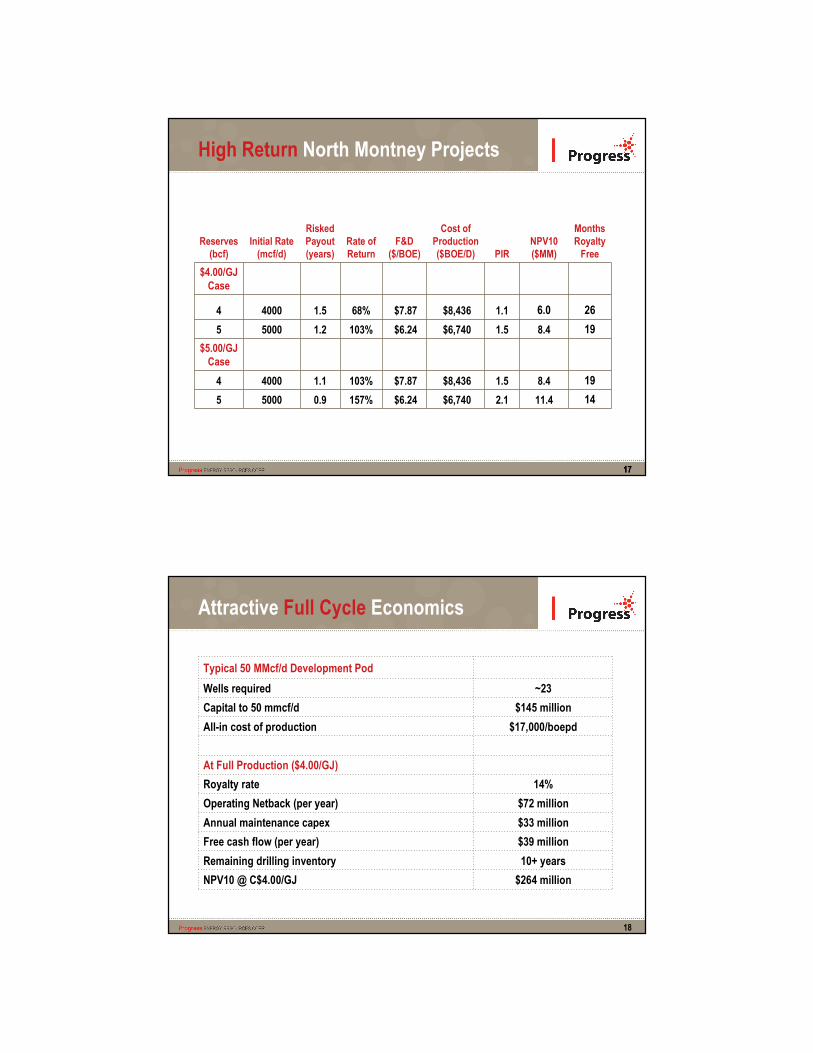

High Return North Montney Projects

Reserves (bcf)

Initial Rate (mcf/d)

Risked Payout(years)

Rate of Return

F&D ($/BOE)

Cost of Production ($BOE/D) PIR

NPV10($MM)

Months Royalty Free

$4.00/GJ Case

4 4000 1.5 68% $7.87 $8,436 1.1 6.0 26

5 5000 1.2 103% $6.24 $6,740 1.5 8.4 19

$5.00/GJ Case

4 4000 1.1 103% $7.87 $8,436 1.5 8.4 19

5 5000 0.9 157% $6.24 $6,740 2.1 11.4 14

18

Attractive Full Cycle Economics

Typical 50 MMcf/d Development Pod

Wells required ~23

Capital to 50 mmcf/d $145 million

All-in cost of production $17,000/boepd

At Full Production ($4.00/GJ)

Royalty rate 14%

Operating Netback (per year) $72 million

Annual maintenance capex $33 million

Free cash flow (per year) $39 million

Remaining drilling inventory 10+ years

NPV10 @ C$4.00/GJ $264 million

0

20

40

60

80

100

120

No

v-08

Jan

-09

Mar

-09

May

-09

Jul-

09

Sep

-09

No

v-09

Jan

-10

Mar

-10

May

-10

Jul-

10

Sep

-10

No

v-10

Jan

-11

Mar

-11

May

-11

Jul-

11

Sep

-11

Gro

ss P

rod

uct

ion

(m

mcf

)

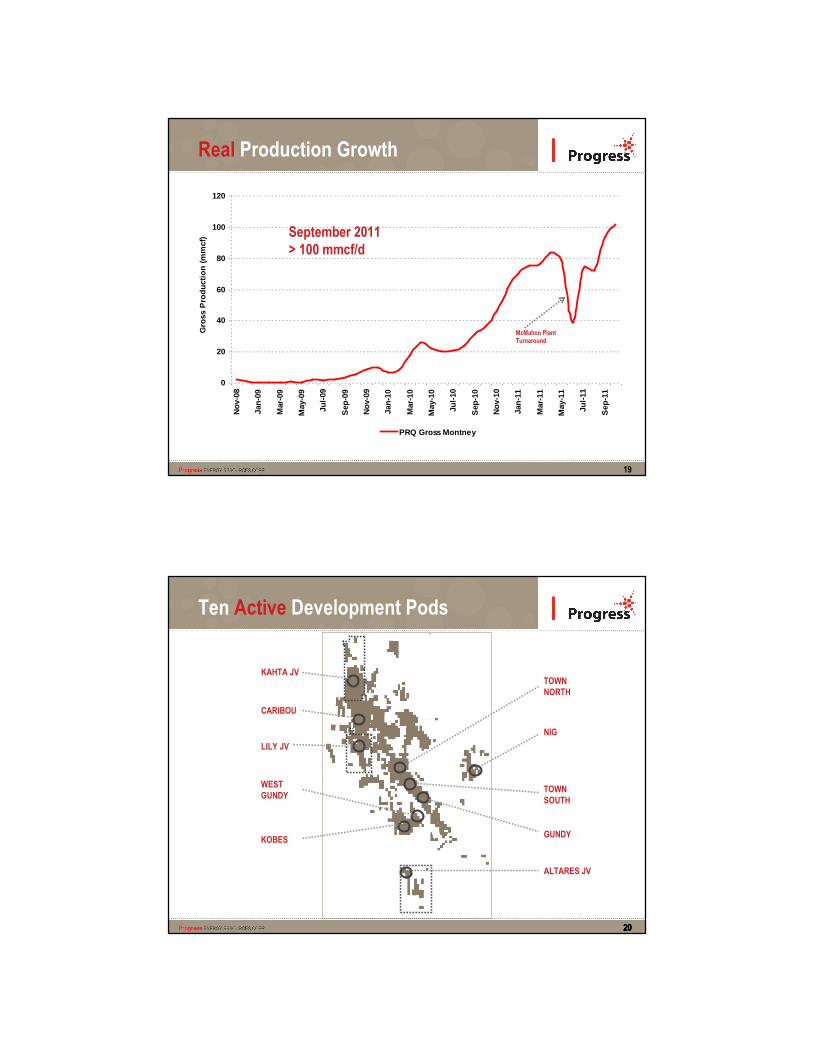

PRQ Gross Montney

19

Real Production Growth

McMahon Plant Turnaround

September 2011> 100 mmcf/d

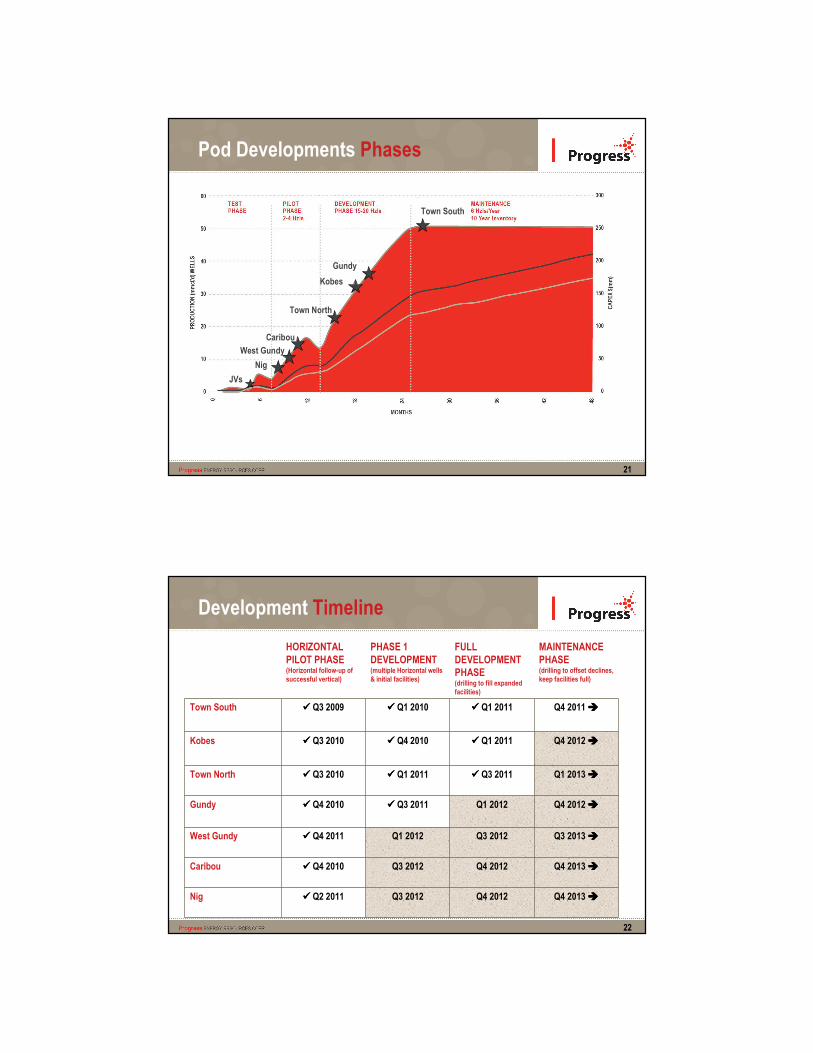

20202020

TOWN NORTH

CARIBOU

KOBES

Ten Active Development Pods

TOWN SOUTH

WEST GUNDY

GUNDY

NIG

KAHTA JV

LILY JV

ALTARES JV

21

Pod Developments Phases

Town South

Kobes

Gundy

Town North

Caribou

West Gundy

Nig

JVs

22

Development Timeline

HORIZONTALPILOT PHASE(Horizontal follow-up of successful vertical)

PHASE 1 DEVELOPMENT(multiple Horizontal wells & initial facilities)

FULL DEVELOPMENT PHASE(drilling to fill expanded facilities)

MAINTENANCE PHASE(drilling to offset declines, keep facilities full)

Town South ���� Q3 2009 ���� Q1 2010 ���� Q1 2011 Q4 2011 ����

Kobes ���� Q3 2010 ���� Q4 2010 ���� Q1 2011 Q4 2012 ����

Town North ���� Q3 2010 ���� Q1 2011 ���� Q3 2011 Q1 2013 ����

Gundy ���� Q4 2010 ���� Q3 2011 Q1 2012 Q4 2012 ����

West Gundy ���� Q4 2011 Q1 2012 Q3 2012 Q3 2013 ����

Caribou ���� Q4 2010 Q3 2012 Q4 2012 Q4 2013 ����

Nig ���� Q2 2011 Q3 2012 Q4 2012 Q4 2013 ����

232323

2012 Development Wells

End 2011 2012 Drills

Town North 10 2

Town South 21 7-9

Gundy 11 8-11

West Gundy 1 8-12

Kobes 7 4

Total 50 35

TOWNNORTH

Number of Horizontal Wells

TOWNSOUTH

KOBES

WESTGUNDY

GUNDY

2424

Town South Development Pod

0

10

20

30

40

50

60

1 91 181

271

361

451

541

631

721

Days

Pro

du

ctio

n (

mm

cf)

0

5

10

15

20

25

Wells

Rate Wells on Production

Target Actual

Total cost ($MM) 145 166

Prod Cost ($/boepd) 16,667 19,137

252525

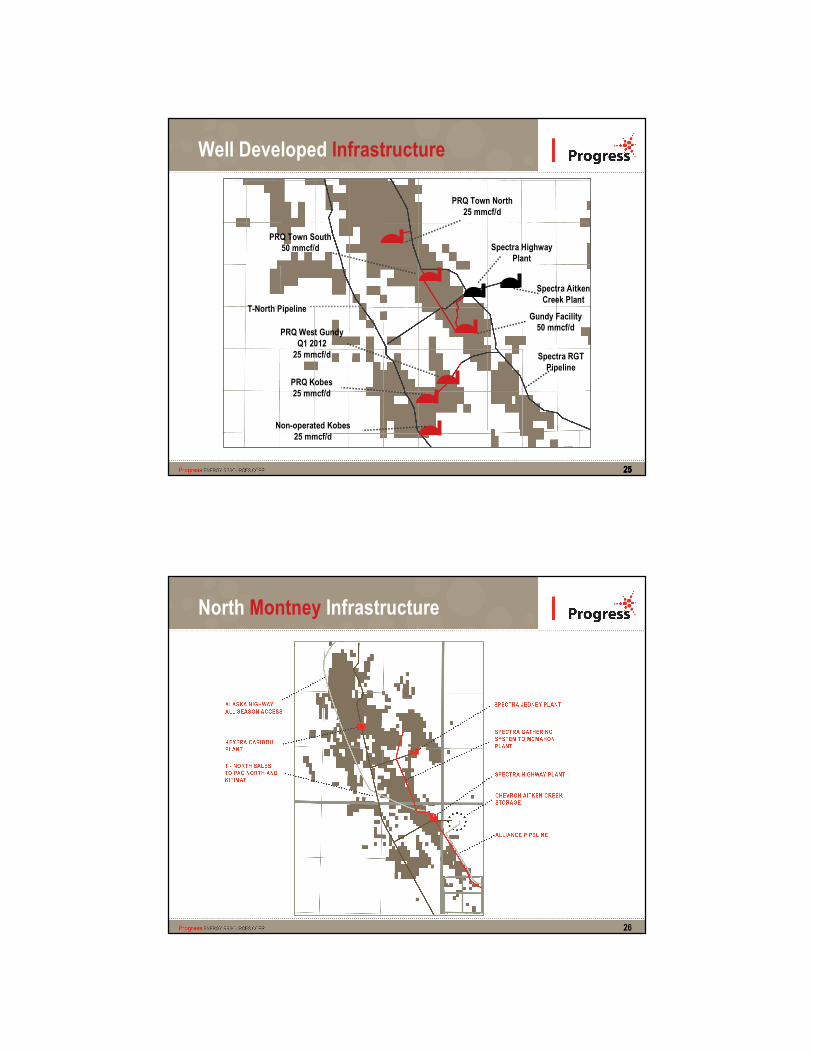

Well Developed Infrastructure

PRQ Kobes25 mmcf/d

PRQ West Gundy Q1 2012

25 mmcf/d

PRQ Town North25 mmcf/d

PRQ Town South 50 mmcf/d

Gundy Facility50 mmcf/d

Spectra RGTPipeline

T-North Pipeline

Non-operated Kobes25 mmcf/d

Spectra Highway Plant

Spectra AitkenCreek Plant

26

North Montney Infrastructure

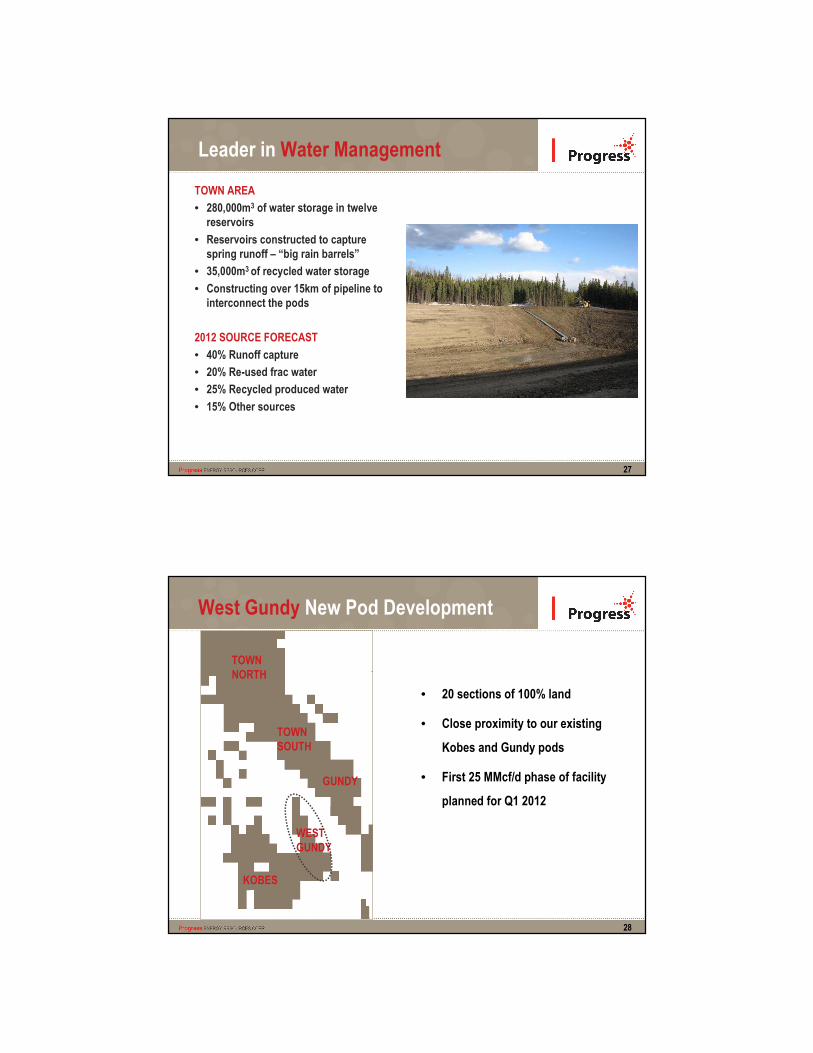

Leader in Water Management

TOWN AREA

• 280,000m3 of water storage in twelve reservoirs

• Reservoirs constructed to capture spring runoff – “big rain barrels”

• 35,000m3 of recycled water storage

• Constructing over 15km of pipeline to interconnect the pods

2012 SOURCE FORECAST

• 40% Runoff capture

• 20% Re-used frac water

• 25% Recycled produced water

• 15% Other sources

27

28

West Gundy New Pod Development

• 20 sections of 100% land

• Close proximity to our existing

Kobes and Gundy pods

• First 25 MMcf/d phase of facility

planned for Q1 2012

TOWNNORTH

TOWNSOUTH

KOBES

WESTGUNDY

GUNDY

29

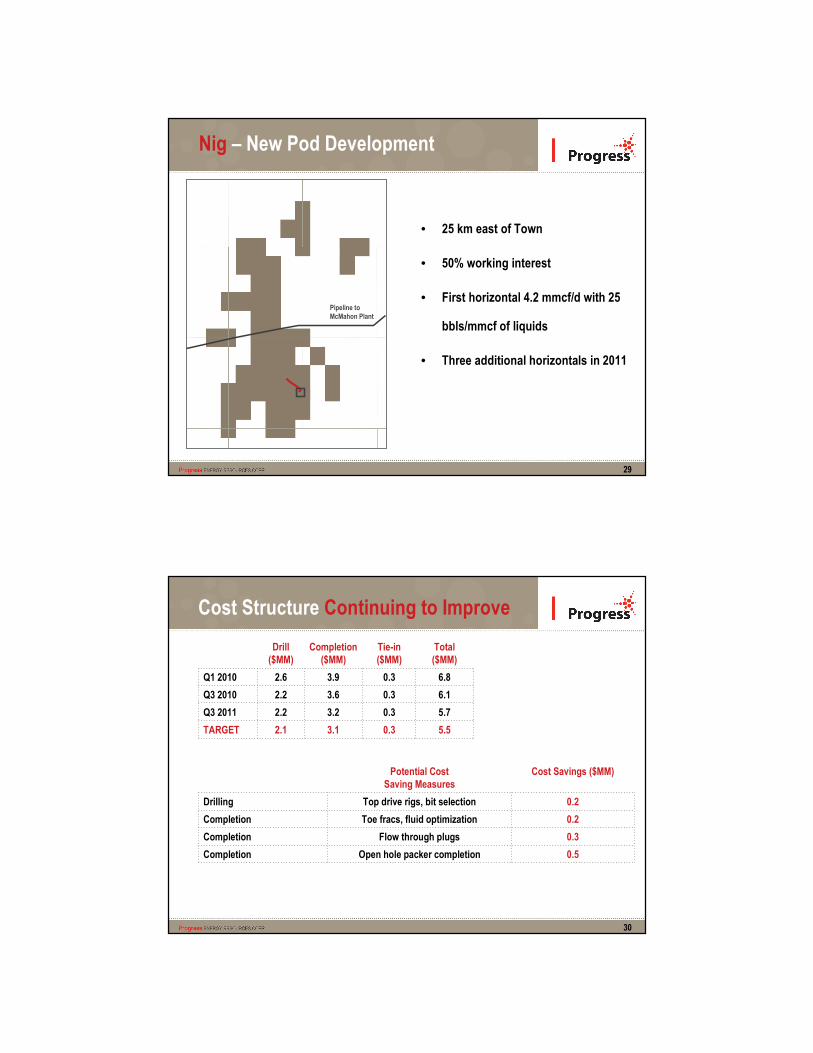

Nig – New Pod Development

• Updated graphic• 25 km east of Town

• 50% working interest

• First horizontal 4.2 mmcf/d with 25

bbls/mmcf of liquids

• Three additional horizontals in 2011

Pipeline to McMahon Plant

30

Cost Structure Continuing to Improve

Drill ($MM)

Completion ($MM)

Tie-in ($MM)

Total ($MM)

Q1 2010 2.6 3.9 0.3 6.8

Q3 2010 2.2 3.6 0.3 6.1

Q3 2011 2.2 3.2 0.3 5.7

TARGET 2.1 3.1 0.3 5.5

Potential CostSaving Measures

Cost Savings ($MM)

Drilling Top drive rigs, bit selection 0.2

Completion Toe fracs, fluid optimization 0.2

Completion Flow through plugs 0.3

Completion Open hole packer completion 0.5

313131

Managing Cost Inflation

• Long term relationships with service companies

- Working together through the best and worst times

• Load levelled program

- Maintain an active program

• Continuous improvement

- Detailed tracking of costs and results

• Repeatable model for facilities and well design

- Improvement through repetition

• Developing New Solutions

- Centralized frac water handling

32

Progress North Montney Expertise

• Microseismic

- Over 160 fracs monitored

• 3-D Seismic

- 3,300 square kilometres to date with 650 planned for H1 2012

• Completions practices

- Over 400 fracs

• Facilities Construction

- 15 compressor stations constructed over 10 years

• Water handling

- Setting new standards for the Canadian industry

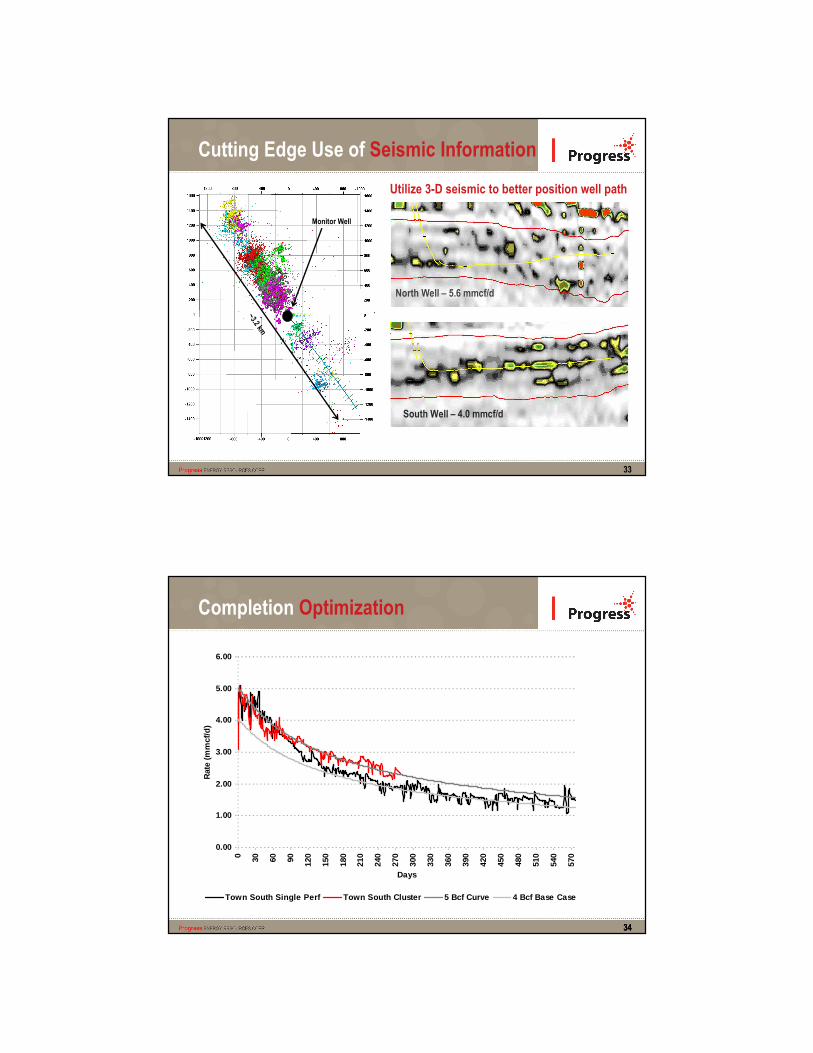

Monitor Well

~3.2 km

North Well – 5.6 mmcf/d

South Well – 4.0 mmcf/d

Cutting Edge Use of Seismic Information

Utilize 3-D seismic to better position well path

33

3434

Completion Optimization

0.00

1.00

2.00

3.00

4.00

5.00

6.00

0 30 60 90 120

150

180

210

240

270

300

330

360

390

420

450

480

510

540

570

Days

Rat

e (m

mcf

/d)

Town South Single Perf Town South Cluster 5 Bcf Curve 4 Bcf Base Case

35

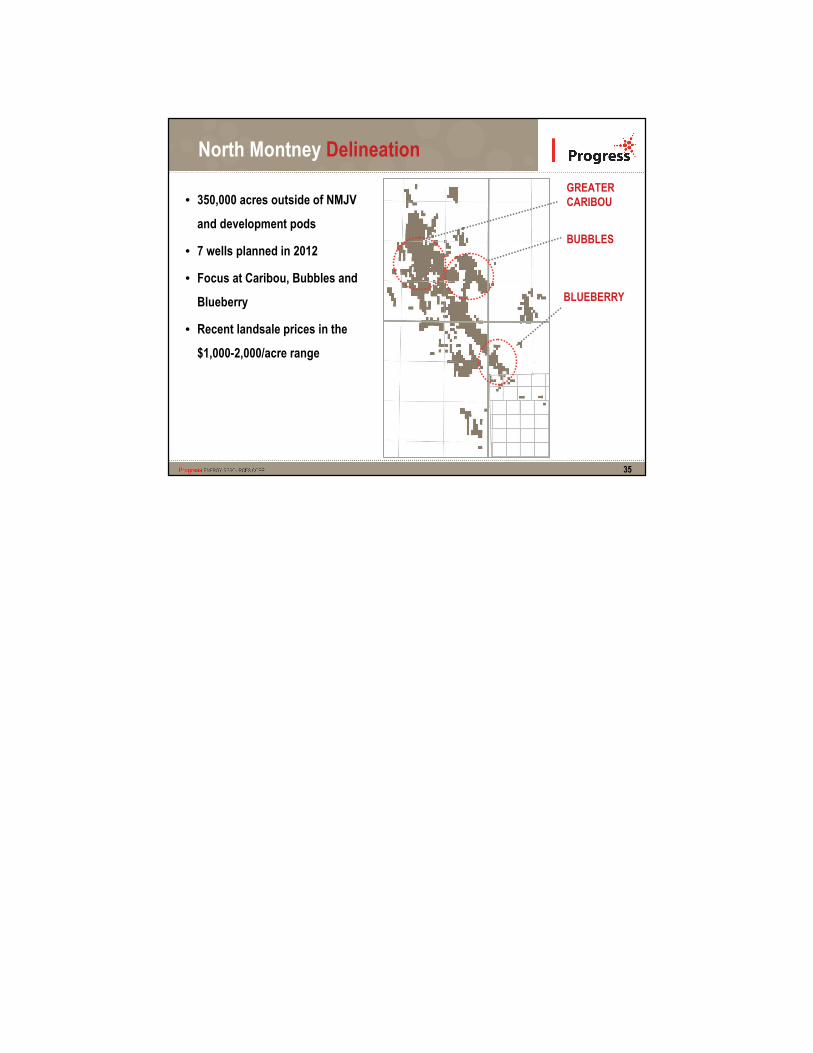

North Montney Delineation

GREATERCARIBOU

BUBBLES

BLUEBERRY

• 350,000 acres outside of NMJV

and development pods

• 7 wells planned in 2012

• Focus at Caribou, Bubbles and

Blueberry

• Recent landsale prices in the

$1,000-2,000/acre range