the newsletter about reforming economies beyond transition · beyond transition • april — june...

TRANSCRIPT

Beyond TransitionThe Newsletter About Reforming Economies

April — June 2006 • Volume 17, No. 2 http://www.worldbank.org/transitionnewsletter

Theme of the Issue: Energy

Interview with Kenneth Rogoff: “No country should plan onUS$70 oil ... forever” 3

World Crude Oil Markets: Monetary Policy and the RecentOil ShockNoureddine Krichene 5

The Oil Supply Potential of the CISRudiger Ahrend and William Tompson 7

Insert: The Resource Curse and Media FreedomSergey Guriev, Konstantin Sonin and Georgy Egorov 8

Management of Energy Resources in ChinaJiang Kejun 9

Caspian Oil: Changing the World's Energy Outlook Yadviga Semikolenova 11

Interview with Vladimir Milov: “The state should leave theenergy sector” 12

Human Capital and the “Resource Curse” Natalia Volchkova and Elena Suslova 14

New Findings

Energy Poverty in Macedonia and the Czech RepublicStefan Buzar 15

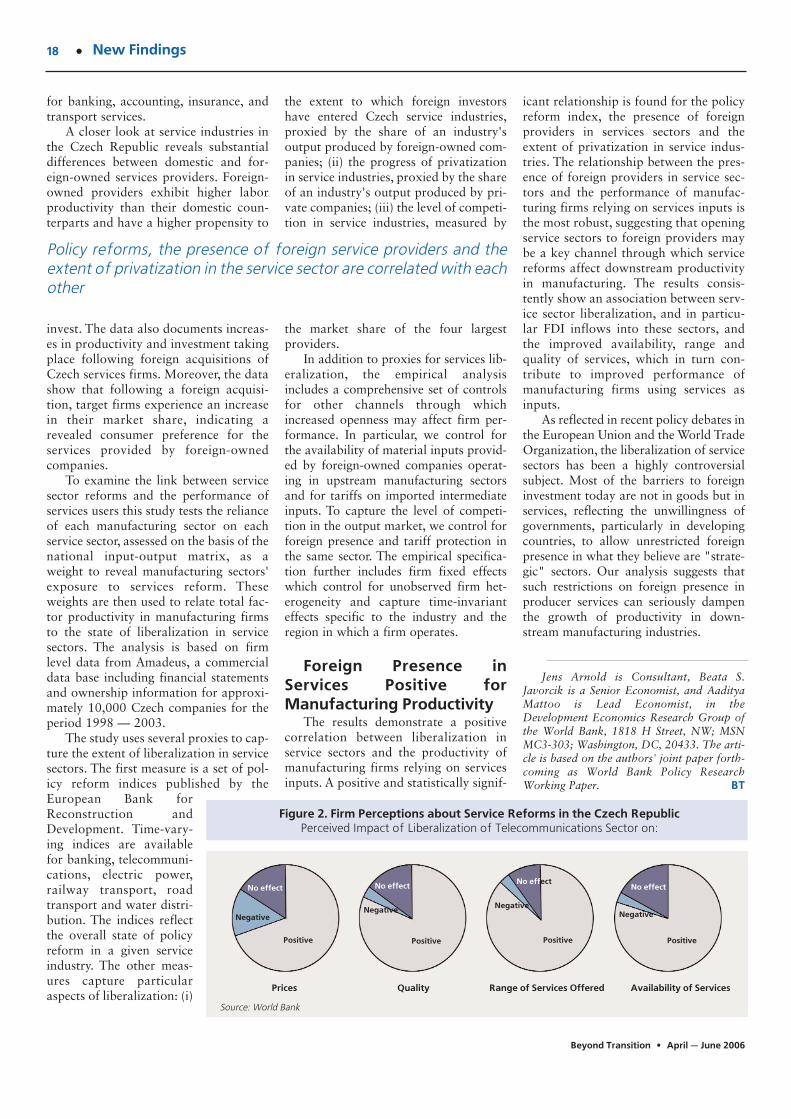

The Productivity Effects of Services Liberalization in theCzech Republic Jens Arnold, Beata S. Javorcik and Aaditya Mattoo 17

The Media's Effect on Corporate Governance in RussiaAlexander Dyck, Natalya Volchkova and Luigi Zingales 19

Is there a "Glass Ceiling" in the Czech Republic?Stepan Jurajda and Teodora Paligorova 21

Foreign Ownership vs. Production EfficiencyValentin Zelenyuk 23

Russia and the WTO: The "Gravity" of Outsider StatusBogdan Lissovolik and Yaroslav Lissovolik 24

World Bank Agenda 25

New Books and Working Papers 27

Conference Diary 30

www.cefir.ru

Global Oil Demand Growth thousand barrels per day

Europe FSU

Middle East

North America

Latin America

Africa

Asia809

88 197

212�4 6 170 47 47

402 324 332

1279

414 470

275133 117

98 83 68

Source: IEA, www.iea.org/2004/2005/2006

37148P

ublic

Dis

clos

ure

Aut

horiz

edP

ublic

Dis

clos

ure

Aut

horiz

edP

ublic

Dis

clos

ure

Aut

horiz

edP

ublic

Dis

clos

ure

Aut

horiz

edP

ublic

Dis

clos

ure

Aut

horiz

edP

ublic

Dis

clos

ure

Aut

horiz

edP

ublic

Dis

clos

ure

Aut

horiz

edP

ublic

Dis

clos

ure

Aut

horiz

ed

Beyond Transition • April — June 2006

2 ·

Dear Reader,

High and highly volatile oil prices over the last few years pose different problems for energyexporting and importing countries. On the face of it oil importers would seem to suffer more.Kenneth Rogoff, however, argues in his interview to BT that in fact oil exporters face much big-ger challenges than importers. Rogoff believes, and his view is supported by evidence presented inNoureddline Krichene's article, that the 1970s output decline was due to monetary policy ratherthan oil shocks. In the last 30 years, oil importing countries have strengthened their financial sys-tems, and improved monetary policy. As a result, they have good chances to withstand currentprice rises without big output losses. Moreover, the current price highs, like all the previous ones,will not last forever. According to Rogoff, we will see oil prices decline within the next five toseven years and this will certainly lead to economic turmoil in oil exporting countries, whosefinancial systems and macroeconomic policies are not strong enough to adapt to lower prices.

One way to make oil exporting countries less vulnerable, according to Rogoff, is to increase private sector participation in theoil sector. Instead we have been observing the increase of state control in oil and gas in many oil producing countries. The ener-gy-rich CIS countries, such as Russia and Kazakhstan, which had previously relied to a large extent on private or foreign own-ership, are now going in the same direction of increased state control in the energy sector. As shown by Ahrend and Tompson,this strategy immediately resulted in the sharp decline of output growth and investment rates. Major problems are awaiting thesecountries in the future, as state owned companies have proved to be much less efficient in developing new fields than the privateones. For example, Gazprom, the Russian natural gas monopoly, has not developed a single large gas deposit in the past 15 years(Milov).

Even state-owned companies can have incentives to increase efficiency if they face strong competition. Recently built pipelines,which bypass Russia, will certainly intensify competition between the oil and gas producing companies of the CIS region. In termsof competition the bad news is that Azerbaijan seems to be increasingly out of the game, as its oil reserves proved to be muchsmaller than was expected (Semikolenova).

In contrast to developed oil consuming countries, which according to Rogoff are well prepared for the current price rise, manydeveloping countries find the current situation very challenging. For China, whose fast-growing economy is widely believed tohave contributed to increased oil prices, the situation is extremely complicated. To be able to continue its fast and robust devel-opment it has to develop a comprehensive energy management strategy. Jiang Kejun provides different scenarios for China'sfuture demand and supply, and suggests policies needed to moderate the current demand growth rate.

At the G8 meeting, which takes place in St.Peterburg in mid July, energy security will be a major topic to be discussed. The arti-cles in this volume demonstrate that the best way to achieve energy security in both oil exporting and oil importing countries isto improve institutions. The first step in this direction may be to secure media freedom, which will help improve control overreform implementation by bureaucrats (Guriev, Sonin, and Egorov) and also improve corporate governance in private firms(Dyck, Volchkova, Zingales). Building better services, particularly in the finance sector, is another important step in the rightdirection. As argued by Arnold, Javorcik and Mattoo, the liberalization of this sector for foreign direct investments is one of thefastest ways to get results.

Ksenia Yudaeva, Managing Editor

From the Editor:

BT: Oil today trades at over US$70per barrel and prices are expected to stayhigh in the near future. Are we anywherenear an oil crisis similar to the one backin the 1970s?

No, I do not think it is a crisis situa-tion, in the sense that a global recession isimminent. High oil prices are an impor-tant issue in the global economy first andforemost because they imply huge gainsfor oil exporters and huge costs for oilconsumers. However, a significant part ofthe past few years' price growth has beendriven by a strong global growth, asopposed to actual or prospective supplyinterruptions.

In fact, academic researchers havelong doubted oil's reputed role as themain culprit for the low productivitygrowth and high inflation years of the1970s in industrialized countries. Overthe past ten years especially, academicwork has reached a broad consensus thatweak monetary policy was a much big-ger factor. During 1971—72, the FederalReserve increased the money supply byover 30% in an effort to boost demand,and help US President Richard Nixon's1972 re-election bid. Even without theoil shock, the Fed would have beenforced to undo part of this massiveincrease to avoid having inflation go intothe stratosphere. So a post-election reces-sion was on the cards long before OPECdecided to break free from Western con-trol of oil prices. The oil increase mag-nified the recession but was not the pri-mary driver.

BT: Is today's global economy betteradapted to high energy prices than it wasin the 1970s?

The most important change is thatcentral banks can be more patient whenoil prices rise than used to be the case.Over the past twenty years we have been

living in an era which economists call"the Great Moderation". Volatility hasbeen going down and financial marketshave improved, goods and labor marketshave become more flexible. Thanks toglobalization and more independentinflation-minded central banks, mone-tary policy has distinctly improved.Monetary authorities do not have toraise interest rates quite as quickly asthey used to, when inflation rose due toenergy price hikes.

It also helps that the share of energyin the industrialized countries' outputhas decreased almost by 50% since the1970s. Equally important, oil use is nowmuch more concentrated in transporta-tion rather than manufacturing. Thus oilprice hikes do not have the same knock-on effects through the economy that theyused to.

All this is not to say that we shouldbe totally calm about high prices. Oneimportant issue is the effect of oil priceson the already huge United States cur-rent account deficit, which has nowtopped 6% of US income. The IMF esti-mates that 50% of the increase in the UScurrent account deficit over the past twoyears has been due to oil imports. Giventhat a disorderly adjustment of the US

current account poses significant risks tothe global economy, and that the prob-lem is being exacerbated by oil pricerises, there is a chance that this recent oilprice cycle may not have a happy ending.

BT: Which countries are more vul-nerable to oil shocks?

I am actually far more concernedabout the oil-exporting countries than theoil-importing ones right now. High pricesare great for them, but part of this rise iscyclical and the question is how they willreact when lower prices hit. Most of theoil-exporting countries have very weakfinancial systems, making it hard forthem to deal with macroeconomic volatil-ity. High prices also make it difficult tosustain important structural reforms todiversify their economies. Because ofthese obstacles, most oil-exporting coun-tries have not enjoyed "the GreatModeration" to nearly the same degree asthe industrialized countries.

Russia, in particular, is certainly stillextremely vulnerable to oil price volatili-ty. Its financial system is still dominatedby state banks, with other forms offinance being woefully undersized. Inorder for it to develop better financialmarkets, it will need greater transparency,stronger institutions and stronger gover-nance. Russia has a lower degree of cen-tral bank independence than would bedesirable over the longer term for anchor-ing inflation and the economy. It has notjoined the WTO yet. So on all these frontsRussia is more vulnerable than sayCanada, another G8 energy exporter.

The bottom line is that despite thetrend for increasing prices in oil, thanksto India and China, no country shouldplan on US$70 oil being around forever.At some point in the next five to sevenyears, we will surely have at least a briefperiod of US$20 oil.

· 3Theme of the Issue: Energy

The World Bank & CEFIR

Kenneth Rogoff: “No country shouldplan on US$70 oil ... forever”Kenneth Rogoff is Thomas D. Cabot Professor of Public Policy and Professor of Economics at HarvardUniversity. He has extensively published on international finance, including exchange rates and cur�rent accounts, central bank design, and financial globalization, and is currently working on a book "Oiland the Global Economy". He shared his findings and views with BT's Olga Mosina during his recentvisit to Moscow

·4 Theme of the Issue: Energy

Beyond Transition • April — June 2006

I should also note that there arecountries in Africa that spend 15% oftheir GDP on oil and energy imports, soobviously high oil prices mean a hugecost to them. However, some of thesecountries are still making out all rightthanks to the fact they export other com-modities whose prices have also beensoaring.

BT: What policies could help to miti-gate macroeconomic risks resulting fromoil price volatility?

For oil-producing countries there area host of issues. At the most basic level,they need deeper financial markets tohelp handle all kinds of volatility,including oil volatility. The ability tointernationally diversify some of theirrisks would also help. Unfortunately, thenationalization of oil companies makesit very difficult to diversify the risk;roughly 70% of the world's oil reservesare in the hands of national oil compa-nies. State-owned oil companies couldachieve some diversification throughfinancial contracts, but they cannotcarry this approach very far without

effectively giving up ownership. Havinga more flexible exchange rate wouldhelp a little, though diversification is thebig issue.

By the way, there are those who arguethat oil wealth is a "curse." This idea wascoined by the Harvard economic historianDavid Landes, who argued that when agovernment can tap a lot of naturalresource wealth it is under much lessimmediate pressure to develop a middleclass to generate economic growthbecause it can get growth from the natu-ral resources. But I think this idea hasbeen grossly oversold. The United Stateshas lots of natural resource wealth, so doCanada, Australia and New Zealand. So ifI was asked whether I would like to havemineral resources in the country where Ilive, I would take a chance and say "yes."The key is to have good institutions.

BT: What about oil-consuming coun-tries?

Most oil-consuming countries havedone a lot of homework already, and are

reaping the benefits today. They havedeeper financial markets, better regula-tion, and better monetary policy. If oil-exporting countries were able to achievethe same, they would surely face far lessdifficulties.

BT: Do these include the new EUmembers?

No, those countries still face a lot ofissues and high oil prices pose a lot ofproblems. The new EU members still use alot of oil in manufacturing which, as I havealready noted, causes far bigger knock-oneffects for the economy than when oil isconcentrated in transportation.

BT: Coming back to nationalization,how do you explain the recent string ofnationalizations in the oil and gas indus-tries?

It has been a long trend, and the situ-ation differs by region. Middle Eastcountries are rich in some dimensionsbut very underdeveloped in many others.They are still very much developingcountries working on building institu-

tions and decentralizing the economy.When these countries took over controlof their oil wealth from foreign oil com-panies a few decades ago, most of theircitizens surely benefited enormously. Butthat day is past and now they need tothink about how to expand their privatesectors.

Russia is clearly a different case.Russia's chaotic privatization in the1990s ended up in giving away a lot ofthe country's riches to a small number ofpeople. This virtual theft of nationalresources has created all kinds of legiti-macy and governance problems. Thepresent-day government's desire toredress some of the resulting problems isvery understandable, though reversion tostate control is not a solution, either. Iagree with Illarionov [former economicpolicy advisor to President Putin], whohas made the point many times thatcountries with privately-owned oil tendto do better.

BT: How would you comment on therecent events in Venezuela and Bolivia?

In Latin America it is really hard tosee any upside to the recent nationaliza-tions. In Venezuela, oil output is now60% of what it was before Chavez tookcontrol. It would have been better toimprove the redistribution of income andenforcement of tax laws than to nation-alize the oil companies. Bolivia's case isalso problematic. It is a classic expropri-ation of foreign assets with a short-termgain but potentially very big long-termcosts. Unfortunately, the recent national-izations of energy resources in LatinAmerica is a giant step backwards thatwill likely haunt the region for decadesto come.

BT: There is much discussion inRussia today about what to do with thestabilization fund, which has accumulat-ed over US$60 bln. How do you thinkthe fund should be best dealt with?

In general it is a good idea to set asidea portion of windfall gains from tem-porarily high oil prices. I hope the gov-ernment ultimately finds a way to redi-rect some of its higher revenues towardsachieving growth in some of the poorerregions, where infrastructure, health andeducation are all weak. Unfortunately, ashas so often been the case throughRussian history, a lot of money is endingup in Moscow, with a bit spilling over toSt. Petersburg.

BT: One of the main argumentsagainst using the funds is the risk ofhigher inflation…

In fact, saving money in an oil fundtakes pressure off inflation, because itpulls resources out of the economy.Anyway, a faster rate of ruble apprecia-tion would go a long way to solvingRussia's double digit inflation problems,which are among the worst in the world.Many in Russia have the view thatexchange rate intervention has beenhelpful in keeping the real exchange ratelow, but I doubt the cumulative effect onthe real exchange rate has been morethan 10 — 15%. Instead, the main effecthas been to force inflation to carry theburden of real exchange rate adjustment.This is not a desirable trade-off. By pur-suing its current policy of very low nom-inal appreciation, all Russia gets is highinflation. Russia could get just as goodgrowth by allowing the nominalexchange rate to appreciate. BT

In Latin America it is really hard to see any upside to the recentnationalizations

· 5

The World Bank & CEFIR

Crude oil prices rapidly increasedfrom around US$30/barrel (bbl) in 2004to close to US$70/bbl in September2005, equivalent to an increase of about133%. In spite of this rapid priceincrease, crude oil supply has beenalmost stagnant at 84 — 85 million bbla day, implying that crude oil productionhas been seriously constrained byresources availability.

Oil price volatility was also high dur-ing the period. The implied volatilityfrom crude oil call options reached highlevels between February 2005 andSeptember 2005, averaging about 30%and showing that the market was experi-encing major uncertainty regardingexpected price developments (see Figure1). Volatility increased even further, ris-ing to 40%, indicating that markets hadbecome very sensitive to small shocksand to news. For instance, after tempo-rary damage to U.S. oil refineries in theGulf of Mexico caused by hurricaneKatrina in September 2005, oil pricessoared beyond the $70/bbl mark.

Inelastic Demand, RigidSupply

What are the basic properties of oilmarkets that cause high volatility in oilprices?

A simultaneous equations modelapplied quarterly (for 1984Q1 —2005Q2) and annually (for 1970 —

2005) provides data supporting thehypothesis of low short-run price demandelasticity (ranging between -0.02 and -0.03), implying that changes in oil priceshave a small partial effect on demand forcrude oil. The volatility of oil markets andtheir vulnerability to small shocks is thusexplained by the fact that energy con-sumption is determined in the short-runby fixed equipment and prevailing tech-nologies and offers limited scope for sub-stantial variation in relation to pricemovements. The long-run demand forcrude oil is also price inelastic. Eventhough the long-run demand price elastic-ity is higher than the short-run one, it isstill low, ranging between -0.03 and -0.08.

Short-run income elasticity rangesbetween 0.12 and 0.19, clearly demon-strating that oil demand is responsive tochanges in economic activity. Highereconomic activity would entail anincrease in demand for oil.

Both the short-run and the long-rundemand for crude oil are negativelyrelated to the U.S. dollar nominal effec-tive exchange rate (NEER). The NEERelasticity ranges between -0.03 and -0.09: an appreciation of the U.S. dollarwould tend to make oil more expensiveand would reduce the demand for crudeoil. The interest rate tends to act nega-tively on the demand for crude oil; anincrease in the interest rate would act toreduce the demand for crude oil andvice-versa. Changes in interest rates are

not transmitted instantaneously to theeconomic activity and prices; their effectis known to work with a delay.

The short-run supply of crude oil isprice inelastic. Producers do not expandoutput in the face of a price increasebecause of short-run capacity con-straints, quota fixation, or to preservesignificant price increases. Similarly, pro-ducers do not reduce output in the faceof large declines in prices. In some cir-cumstances of depressed oil prices, oilproducers may supply more than thequotas in order to generate badly neededbudgetary revenues. Short-run crude oilsupply is significantly influenced by nat-ural gas production. Short-run elasticityranges between 0.11 and 0.26. For thisreason, an increase in natural gas pro-duction may be accompanied by anexpansion in crude oil production.

Long-run price elasticity remains lowat 0.08, implying that long-run oil sup-ply is determined by technological fac-tors and discoveries, and is less respon-sive to prices. Natural gas continues toplay an important role in the supply ofcrude oil. These two products were per-fectly correlated over 1970 — 2005.

Thus the basic properties of the oilmarkets are the combination of lowprice, high income elasticities, and rigidsupply that explains high and persistentvolatility in the oil markets and the mar-ket power of producers.

Two�Way CausalityDuring 1970 — 2005, three epochs

can be distinguished:• The oil supply shocks of 1970 —

1986, with the oil price peaking atUS$41/bbl in 1980. As a result, worldinflation rose to two-digit levels, averag-ing 10.1% during 1974 — 81. Monetarypolicy had to be deployed to cope withthe oil shock and the oil-induced infla-tionary pressure. Interest rates kept chas-ing oil prices and peaked only after oilprices had reached a peak. Indeed, thefederal funds rate peaked at 19.08% in1981. Because of high interest rates, the

World Crude Oil Markets: MonetaryPolicy and the Recent Oil Shock

Noureddine Krichene

An oil demand shock, caused by record low interest rates, led to the exorbitant price increases in 2004�2005

Figure 1: Crude Oil Implied Price Volatility, February — August, 2005

45

40

35

30

25

20

15

10

5

0

Imp

lied

Vo

lati

lity

10.02.2005

24.02.2005

10.03.2005

24.03.2005

07.04.2005

21.04.2005

05.05.2005

19.05.2005

02.06.2005

16.06.2005

30.06.2005

14.07.2005

28.07.2005

·6 Theme of the Issue: Energy

Beyond Transition • April — June 2006

NEER appreciated significantly, makingoil more expensive. Ultimately, world eco-nomic growth contracted sharply to ameager average growth rate of 0.8% dur-ing 1980 — 1982, forcing a sustaineddecline in both crude oil prices and theworld inflation rate during 1981 — 1986.

• The period of relative oil pricestability and stationary NEER during1986 — 1999. Interest rates were, how-ever, highly nonstationary, implying thatmonetary policy remained active andwas mainly geared toward maintainingthe growth and price stability momen-tum.

• The period of record low interestrates and a depreciating NEER during1999 — 2005. Interest rates were ostensi-bly taking the lead over crude oil prices.The federal funds rate was maintained at1% during 2003 — 2004. Crude oil pricesstarted rising rapidly, exceeding the markof US$70/bbl in September 2005.

The relationship between crude oilprices, interest rates, and the NEER ischaracterized by a two-way causality,depending on the type of shock. Duringan oil supply shock, oil prices affect inter-est rates; whereas during a demand shock,interest rates affect crude oil prices.

Tight Monetary PolicyHelps to Stabilize Oil Markets

During the oil supply shock period of1974 — 1981, under stable oil demandconditions, oil prices led interest rates.Monetary policy was deployed to pushoil prices down by forcing a downwardadjustment in the demand for oil com-mensurate with the supply disturbances.Such an adjustment was brought aboutby substantial increases in real interestrates through targeting non-borrowedreserves. Interest rates increase by six per-centage points for each 100% increase inoil prices. Indeed, the data show that

crude oil prices went up fromUS$11.17/bbl to US$40.97/bbl during theperiod, while the federal funds rate wentup from 4.61% to 19.1%. During thedeclining phase of oil prices in 1982 —1986 monetary policy was progressivelyeased in response to the abatement of therise in oil prices.

During the oil supply shock period,powerful actions on interest rates had tobe undertaken to choke off oil priceincrease, thereby causing a severe con-traction of world economic growth.These actions were reinforced by othermeasures that were simultaneouslyadopted to curb oil prices, such as hightaxes on petroleum consumption, energysubstitution and conservation, and tech-nological change oriented toward higherenergy efficiency.

During the demand shock of recentyears, under stable oil supply conditions,interest rates led oil prices. Low interestrates caused excess demand for crude oilwhich fed into higher prices. Consequent-ly, an important increase in real interestrates, similar to those experienced duringthe oil supply shock, might be required tobring demand in line with supply and con-tain the inflationary effect of high oilprices. This may cause a temporary con-traction in world economic growth.

The model predicts that a 1% increasein income leads to an increase in crude oiloutput by 0.49% and crude oil price by2.8%. Thus, an expansion of world eco-nomic growth could exert a strongupward pressure on oil prices. For naturalgas production, a 1% increase leads to anincrease of 0.30% in the crude oil pro-duction and a decline in oil price of

1.47%. An increase in the interest rateleads in the long-run to a decline in bothcrude oil demand and prices.

Thus, monetary policy, conductedthrough changes in interest rates and mon-etary aggregates, has a significant and pro-tracted effect on aggregate demand forgoods and services as well as on asset

prices such as exchange rates, housing andstock prices. The sustained pressure on oilprices observed in 2004 — 2005 can beexplained by an excessively expansionarymonetary policy, with interest rates fallingto record levels in an integrated interna-tional capital market. Stimulated by lowinterest rates and a depreciating U.S. dol-lar, demand for oil has expanded fasterthan supply. Given the short-run priceinelasticity of both oil demand and supply,equilibrium is obtained through a largeincrease in oil prices.

The main conclusion is that the stabi-lization of oil markets requires a tighten-ing of monetary policy and an increase inex-ante real interest rates. Based on datafor 1970 — 86, the degree of monetarytightening to rein in oil prices and theirinflationary implications may be sub-stantial and may involve a trade-offbetween inflation and output. In thesame vein, based on data for 1986 —2000, sustained noninflationary worldeconomic growth would require a degreeof stability in oil markets.

Noureddine Krichene is an Economist atthe IMF. The full paper can be accessed at:http://www.imf.org/external/pubs/cat/lon-gres.cfm?sk=18890.0. The views expressed inthe article are those of the author and do notnecessarily represent those of the IMF. BT

The stabilization of oil markets requires a tightening of monetarypolicy and an increase in real interest rates

Quarterly World Oil Demand Quarterly World Oil Supply

87868584838281807978

mb

/d

1Q2004

2Q2004

3Q2004

4Q2004

1Q2005

2Q2005

3Q2005

4Q2005

1Q2006

2Q2006

3Q2006

4Q2006

86

85

84

83

82

81

80

mb

/d

1Q2004

2Q2004

3Q2004

4Q2004

1Q2005

2Q2005

3Q2005

4Q2005

1Q2006

81,882,4

83,384,2

83,784,4 84 84,2

84,8

Source: IEA, http://omrpublic.iea.org/

82,681,3

82,2

84,2 84,6

82,583,3

84,285

85,5

87,7

86,4

· 7

The World Bank & CEFIR

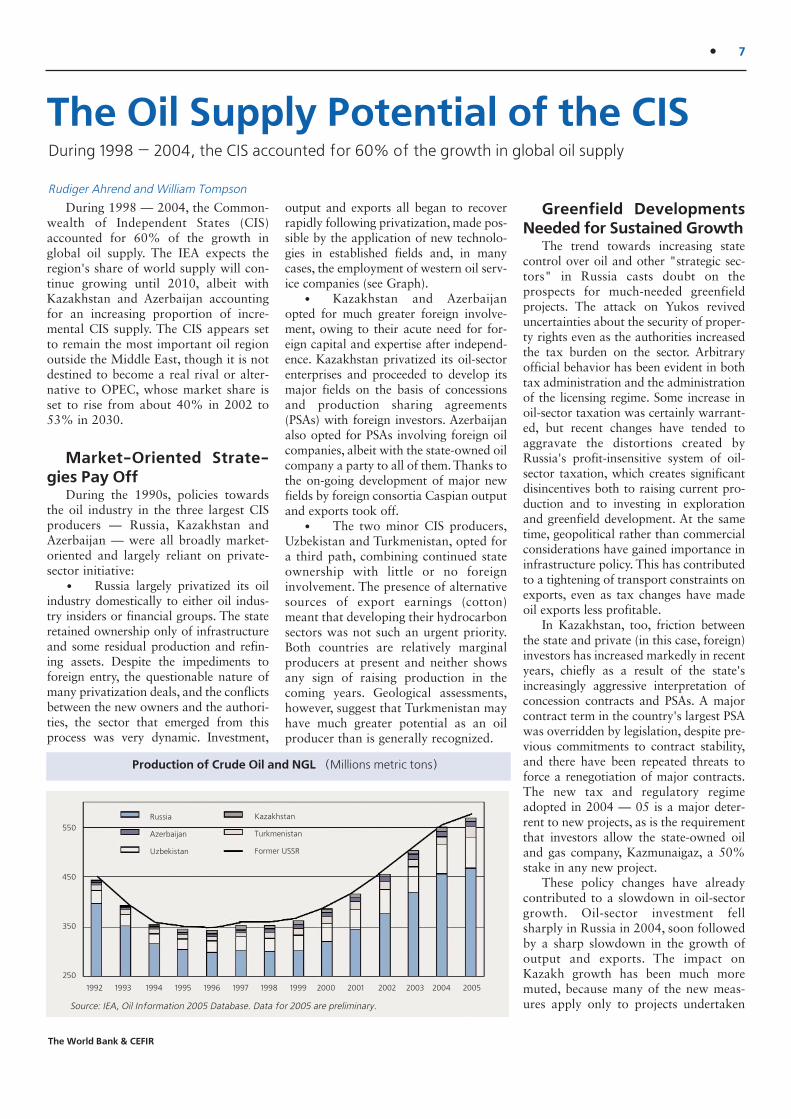

The Oil Supply Potential of the CIS

Rudiger Ahrend and William Tompson

During 1998 — 2004, the Common-wealth of Independent States (CIS)accounted for 60% of the growth inglobal oil supply. The IEA expects theregion's share of world supply will con-tinue growing until 2010, albeit withKazakhstan and Azerbaijan accountingfor an increasing proportion of incre-mental CIS supply. The CIS appears setto remain the most important oil regionoutside the Middle East, though it is notdestined to become a real rival or alter-native to OPEC, whose market share isset to rise from about 40% in 2002 to53% in 2030.

Market�Oriented Strate�gies Pay Off

During the 1990s, policies towardsthe oil industry in the three largest CISproducers — Russia, Kazakhstan andAzerbaijan — were all broadly market-oriented and largely reliant on private-sector initiative:

• Russia largely privatized its oilindustry domestically to either oil indus-try insiders or financial groups. The stateretained ownership only of infrastructureand some residual production and refin-ing assets. Despite the impediments toforeign entry, the questionable nature ofmany privatization deals, and the conflictsbetween the new owners and the authori-ties, the sector that emerged from thisprocess was very dynamic. Investment,

output and exports all began to recoverrapidly following privatization, made pos-sible by the application of new technolo-gies in established fields and, in manycases, the employment of western oil serv-ice companies (see Graph).

• Kazakhstan and Azerbaijanopted for much greater foreign involve-ment, owing to their acute need for for-eign capital and expertise after independ-ence. Kazakhstan privatized its oil-sectorenterprises and proceeded to develop itsmajor fields on the basis of concessionsand production sharing agreements(PSAs) with foreign investors. Azerbaijanalso opted for PSAs involving foreign oilcompanies, albeit with the state-owned oilcompany a party to all of them. Thanks tothe on-going development of major newfields by foreign consortia Caspian outputand exports took off.

• The two minor CIS producers,Uzbekistan and Turkmenistan, opted fora third path, combining continued stateownership with little or no foreigninvolvement. The presence of alternativesources of export earnings (cotton)meant that developing their hydrocarbonsectors was not such an urgent priority.Both countries are relatively marginalproducers at present and neither showsany sign of raising production in thecoming years. Geological assessments,however, suggest that Turkmenistan mayhave much greater potential as an oilproducer than is generally recognized.

Greenfield DevelopmentsNeeded for Sustained Growth

The trend towards increasing statecontrol over oil and other "strategic sec-tors" in Russia casts doubt on theprospects for much-needed greenfieldprojects. The attack on Yukos reviveduncertainties about the security of proper-ty rights even as the authorities increasedthe tax burden on the sector. Arbitraryofficial behavior has been evident in bothtax administration and the administrationof the licensing regime. Some increase inoil-sector taxation was certainly warrant-ed, but recent changes have tended toaggravate the distortions created byRussia's profit-insensitive system of oil-sector taxation, which creates significantdisincentives both to raising current pro-duction and to investing in explorationand greenfield development. At the sametime, geopolitical rather than commercialconsiderations have gained importance ininfrastructure policy. This has contributedto a tightening of transport constraints onexports, even as tax changes have madeoil exports less profitable.

In Kazakhstan, too, friction betweenthe state and private (in this case, foreign)investors has increased markedly in recentyears, chiefly as a result of the state'sincreasingly aggressive interpretation ofconcession contracts and PSAs. A majorcontract term in the country's largest PSAwas overridden by legislation, despite pre-vious commitments to contract stability,and there have been repeated threats toforce a renegotiation of major contracts.The new tax and regulatory regimeadopted in 2004 — 05 is a major deter-rent to new projects, as is the requirementthat investors allow the state-owned oiland gas company, Kazmunaigaz, a 50%stake in any new project.

These policy changes have alreadycontributed to a slowdown in oil-sectorgrowth. Oil-sector investment fellsharply in Russia in 2004, soon followedby a sharp slowdown in the growth ofoutput and exports. The impact onKazakh growth has been much moremuted, because many of the new meas-ures apply only to projects undertaken

During 1998 — 2004, the CIS accounted for 60% of the growth in global oil supply

550

450

350

250

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

Source: IEA, Oil Information 2005 Database. Data for 2005 are preliminary.

Russia

Azerbaijan

Uzbekistan

Kazakhstan

Turkmenistan

Former USSR

Production of Crude Oil and NGL (Millions metric tons)

·8 Theme of the Issue: Energy

Beyond Transition • April — June 2006

from 1 January 2004. Even so, tougherregulatory policies do appear to haveconstrained production growth.Azerbaijan has arguably remained themost investor-friendly of the three states,and production there has boomed sincethe opening of the Baku-Tbilisi-Ceyhanpipeline in 2005. However, its long-termsustainability is in doubt, as a number ofprojects have been wound up after fail-ing to find the anticipated volumes ofcommercially recoverable reserves.

Looking to the FutureThe growing openness of both

Uzbekistan and Turkmenistan to greaterforeign involvement in their respectivehydrocarbon sectors reflects a welcomeawareness that they will need outsideinvestment and technology to realizetheir potential. At present, both foreignpolicy considerations and the weaknessof the investment environment suggestthat this role will be played increasinglyby Russian state-controlled companiesand by the national oil companies offast-growing consumer countries likeChina and India, which have been seek-ing to expand into the CIS and the rest ofthe developing world.

The trend in Russia and Kazakhstanis towards higher taxation, greater stateownership of oil-sector assets, andincreasingly aggressive and arbitrary

administration of licensing and otherregulatory regimes. Russia is now work-ing to address the distortions created byits profit-insensitive system of oil-sectortaxation, but the long awaited — andbadly needed — reform of subsoil legis-lation has stalled. Greater state interven-tion is likely to result in more confusionand delay when it comes to major deci-sions, such as exploration and invest-ment in greenfield projects. A commonfeature in both countries has been theweakness of the administrative, regulato-ry and rule enforcement capacities ofboth states, and the authorities' frustra-tion at their inability to capture oil rentsin an environment of very high prices.Yet it is far from clear that greater stateownership will ensure that the state doescapture these rents. It may simply lead totheir dissipation via poor performanceand rent-seeking by insiders.

In late 2003, state-controlled compa-nies in Russia accounted for about 17%of crude production. This figure hassince more than doubled and could reach45% by the time Yukos's assets are soldoff. Given the poor performance of mostRussian state companies with respect tocost control, productivity, corporate gov-ernance and innovation, this bodes ill forthe future. Moreover, greater state own-ership of oil-producing assets is likely todistort the incentives facing the remain-

ing private oil companies, because theyfear unfair treatment when competingwith large state-owned producers.

Given the sums already committed toexisting projects, Kazakhstan is still wellplaced to deliver strong growth over theyears ahead. However, major new proj-ects are unlikely under the present taxand regulatory regime, and it is far fromcertain that the country will triple outputby 2015 as planned, not least because ofconflict with investors over the develop-ment of export infrastructure. Russia isanother matter. It accounts for almost80% of CIS production today and hasconsiderable potential for further, albeitundramatic, growth. However, it faces amuch greater risk than Kazakhstan ofstagnating or even falling output over themedium term if significant new green-field projects are not developed in atimely manner.

Rudiger Ahrend is an Economist andWilliam Tompson is a Senior Economist atthe OECD Economics Department. The arti-cle is based on the author's paper "Realizingthe oil supply potential of the CIS: the impactof institutions and policies", available at:http://www.olis.oecd.org/olis/2006doc.nsf/linkto/ECO-WKP(2006)12. The opinionsexpressed in the article are those of the authorsand do not necessarily reflect the views of theOECD or its member states. BT

The Resource Curse and Media FreedomIn 1985, Mikhail Gorbachev faced a difficult dilemma.

Without allowing free speech, the reforms of the highly ineffi-cient bureaucracy and the command economy seemed all butimpossible. At the same time, free flow of information wouldthreaten the foundations of the Communist Party's rule.

Such a dilemma is quite typical for any autocratic ruler. Innon-democratic societies, the ruler needs independent sourcesof information on the outcomes of his policies, such as freemedia. Otherwise he cannot provide incentives to the bureau-cracy, which may result in poor economic performance andmay eventually cost him his job. The ruler may choose toallow media freedom; however, independent media will pro-vide all (even negative) information to citizens, therebyincreasing risks of overthrowing the ruler. Alternatively, theruler may build a secret service that would report on thebureaucracy directly to him. In this case, there is a risk of col-lusion between the monitoring organization and bureaucrats.

The trade-off between incentives for bureaucracy and theneed to "divide-and-rule" via suppressing information flowsis especially visible in developing countries with abundantnatural resources. On average, such countries perform less

successfully than resource-poor countries. There is now anemerging consensus that the major reason for the resource-rich countries' slowdown in economic growth is institutions.Our theoretical model predicts a negative relationship, whichshould be especially strong in less democratic countries,between resource abundance and media freedom. In the pres-ence of abundant resources, it becomes less important to pro-vide proper incentives for bureaucrats, which in turn reducesthe ruler's willingness to have free media.

The empirical analysis confirms theoretical implications:using Freedom House data on media freedom, Polity IVscores for democracy and autocracy, and BP data on oilreserves, we find that, controlling for the level of develop-ment and democracy, media are less free in oil-rich countries.The effect of natural resources on media freedom is especial-ly strong in less democratic countries, while mature democ-racies are relatively safe from the adverse effect of oil.

Sergey Guriev is Associate Professor and Rector of New EconomicSchool (NES), Moscow. Konstantin Sonin is Assistant Professor at NES.Georgy Egorov is a Ph.D. student at Harvard University. The piece isbased on the working paper available at:http://www.cefir.ru (#63). BT

· 9

The World Bank & CEFIR

Management of Energy Resourcesin China

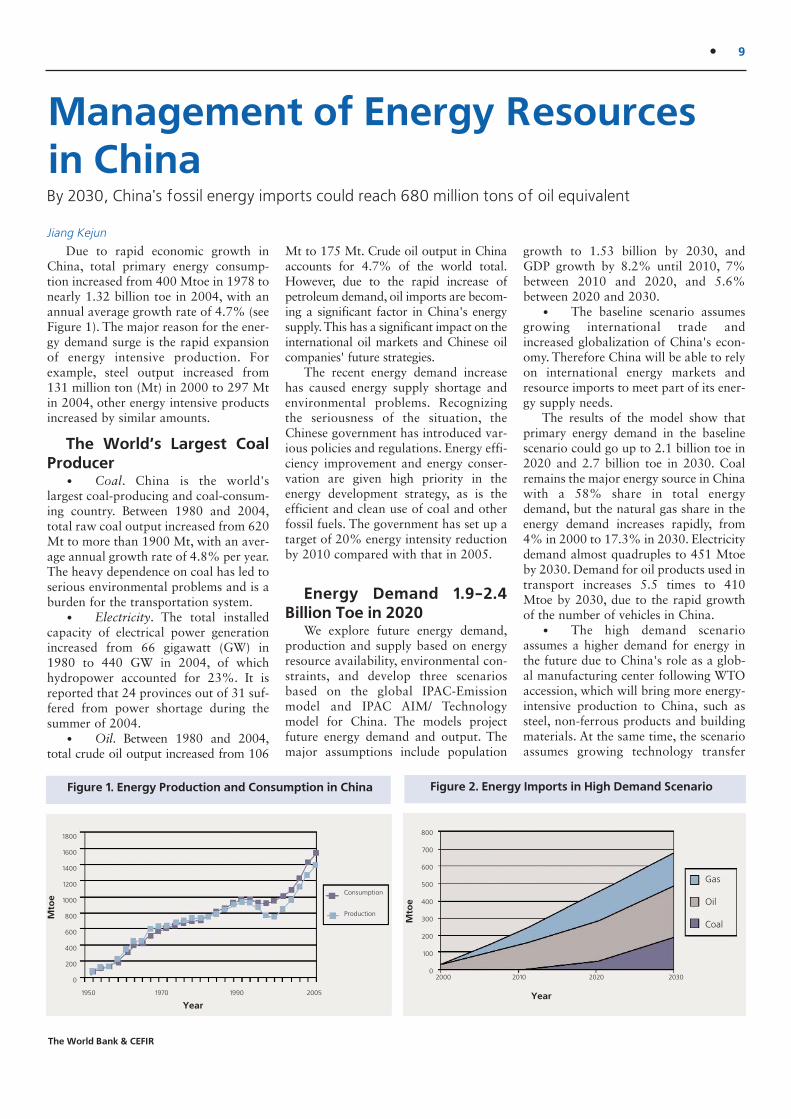

Jiang Kejun

Due to rapid economic growth inChina, total primary energy consump-tion increased from 400 Mtoe in 1978 tonearly 1.32 billion toe in 2004, with anannual average growth rate of 4.7% (seeFigure 1). The major reason for the ener-gy demand surge is the rapid expansionof energy intensive production. Forexample, steel output increased from131 million ton (Mt) in 2000 to 297 Mtin 2004, other energy intensive productsincreased by similar amounts.

The World’s Largest CoalProducer

• Coal. China is the world'slargest coal-producing and coal-consum-ing country. Between 1980 and 2004,total raw coal output increased from 620Mt to more than 1900 Mt, with an aver-age annual growth rate of 4.8% per year.The heavy dependence on coal has led toserious environmental problems and is aburden for the transportation system.

• Electricity. The total installedcapacity of electrical power generationincreased from 66 gigawatt (GW) in1980 to 440 GW in 2004, of whichhydropower accounted for 23%. It isreported that 24 provinces out of 31 suf-fered from power shortage during thesummer of 2004.

• Oil. Between 1980 and 2004,total crude oil output increased from 106

Mt to 175 Mt. Crude oil output in Chinaaccounts for 4.7% of the world total.However, due to the rapid increase ofpetroleum demand, oil imports are becom-ing a significant factor in China's energysupply.This has a significant impact on theinternational oil markets and Chinese oilcompanies' future strategies.

The recent energy demand increasehas caused energy supply shortage andenvironmental problems. Recognizingthe seriousness of the situation, theChinese government has introduced var-ious policies and regulations. Energy effi-ciency improvement and energy conser-vation are given high priority in theenergy development strategy, as is theefficient and clean use of coal and otherfossil fuels. The government has set up atarget of 20% energy intensity reductionby 2010 compared with that in 2005.

Energy Demand 1.9�2.4Billion Toe in 2020

We explore future energy demand,production and supply based on energyresource availability, environmental con-straints, and develop three scenariosbased on the global IPAC-Emissionmodel and IPAC AIM/ Technologymodel for China. The models projectfuture energy demand and output. Themajor assumptions include population

growth to 1.53 billion by 2030, andGDP growth by 8.2% until 2010, 7%between 2010 and 2020, and 5.6%between 2020 and 2030.

• The baseline scenario assumesgrowing international trade andincreased globalization of China's econ-omy. Therefore China will be able to relyon international energy markets andresource imports to meet part of its ener-gy supply needs.

The results of the model show thatprimary energy demand in the baselinescenario could go up to 2.1 billion toe in2020 and 2.7 billion toe in 2030. Coalremains the major energy source in Chinawith a 58% share in total energydemand, but the natural gas share in theenergy demand increases rapidly, from4% in 2000 to 17.3% in 2030. Electricitydemand almost quadruples to 451 Mtoeby 2030. Demand for oil products used intransport increases 5.5 times to 410Mtoe by 2030, due to the rapid growthof the number of vehicles in China.

• The high demand scenarioassumes a higher demand for energy inthe future due to China's role as a glob-al manufacturing center following WTOaccession, which will bring more energy-intensive production to China, such assteel, non-ferrous products and buildingmaterials. At the same time, the scenarioassumes growing technology transfer

By 2030, China's fossil energy imports could reach 680 million tons of oil equivalent

Figure 1. Energy Production and Consumption in China

1800

1600

1400

1200

1000

800

600

400

200

0

1950 1970 1990 2005

Consumption

ProductionMto

e

Year

Figure 2. Energy Imports in High Demand Scenario

2000 2010 2020 2030

800

700

600

500

400

300

200

100

0

Gas

Oil

CoalMto

e

Year

·10 Theme of the Issue: Energy

Beyond Transition • April—June 2006

and the application of energy efficiencytechnologies.

This model results in primary energydemand reaching 2.9 billion toe by2030, which is 250 Mt higher than thebaseline scenario. Of the total primaryenergy demand, coal provides 59.1%, oil16.1%, natural gas 17.8%, and nuclearenergy 1.2%. Because this scenarioassumes better integration in interna-tional markets, there is greater relianceon imported natural gas and oil.

• The policy scenario assumes theimplementation of various energy andemission control policies and a lowerenergy demand, which reflects energysupply and environmental constraints.The policies include: end use technologyefficiency promotion; introduction ofenergy efficiency standards for buildings;vehicle and energy taxes; renewable ener-gy development; increasing share of pub-lic transport in cities; transport efficiencyimprovement and use of fuel-efficientvehicles; increased efficiency of coal firedpower plants; enhancement of natural gassupply; and nuclear power development.

Compared to the baseline scenario,the energy demand would be lower bynearly 280 Mtoe by 2030. In order toachieve such a reduction in demand, thisscenario requires timely implementationof the policies mentioned above.

Abundant AlternativeEnergy Resources

As for the energy resources, coal isexpected to continue playing a key role inproviding energy security for the country,but it will perhaps take a smaller share inthe total fossil fuel resources compared tothe current share of 96%. Natural gashas historically received less attention,but in the past two years three very largenatural gas fields were discovered in

mainland China. Regarding hydropower,transmission from the hydro resource-rich south-west of China to the easternpart, and small-scale hydropower devel-opment are the main priorities. Chinaalso has good prerequisites for develop-ing nuclear power. These include produc-ing energy, supplying nuclear fuel, pro-cessing used fuels, and having the neces-sary technologies at hand.

As for alternative energy resources,biomass resources from agriculture,forestry and timber industries, andmunicipal waste have the potential forplaying a decisive role in China's energysupply, with, as one example, wastesfrom agriculture potentially yieldingnearly 80 billion m3 of biogas. With alarge land mass and long coastline,China has relatively abundant windresources for the further development oflarge-scale wind power. According toestimates by the China MeteorologyResearch Institute, land-based andocean-based exploitable wind resourcesrepresent a potential power generationcapacity of about 1,000 GW. China isalready tenth in the world in terms oftotal installed wind power capacity andhas 40 wind farms established.

Energy Supply ScenariosHaving simulated future energy pro-

duction in China, we find that • Coal production could reach

1.48 billion toe by 2030. Coal demand,therefore, could exceed domestic coalproduction in China.

• Oil production is projected toreach 175 Mt by 2030.

• Natural gas production is expect-ed to reach 312 billion m3 by 2030.

• Nuclear power generation willincrease quickly in the future reaching344 TWh by 2030 (compared with 16.7TWh in 2000), but will still represent a

small share of the total energy produc-tion, because of its high cost.

• Hydropower output willincrease from 224 TWh in 2000 to 722TWh by 2030, with capacity reaching201 GW by 2030.

Consequently, the need for future fos-sil energy imports in the baseline scenariois 375 Mtoe annually by 2020 and 562Mtoe by 2030. As a comparison, in 2000,the USA imported 870 Mtoe. Oil will topthe energy imports, but even coal needs tobe imported after 2020, with 129 milliontons of coal needed annually.

In the high demand scenario, energyimports are much bigger (see Figure 2).Total fossil energy import will be 445Mtoe by 2020 and 680 Mtoe by 2030.Even more coal needs to be imported inthis scenario.

To ease the pressure on energy sup-ply, well-designed energy strategiesshould be developed. These includedevelopment of new generation tech-nologies, use of energy tax, resource taxand export tax for energy-intensiveproducts in order to promote energy sav-ing, development of renewable energyand the establishment of a diversifiedenergy supply. Clean coal technologyshould be emphasized in order to miti-gate emission form coal combustion.Due to low production costs China islikely to become the global manufactur-ing center relying on energy andresource-intensive production. This trendshould be carefully controlled, and exter-nal costs to the environment should beincluded in production costs.

Jiang Kejun is a Research Professor atEnergy Research Institute. The full text of thepaper can be accessed at: http://siteresources.worldbank.org/INTDECABCTOK2006/Resources/Kejun_Energy_China.pdf BT

Coordinated efforts by the international community canplay a significant role in promoting energy security. An agen-da for action could include the following key elements:

• Actively promoting more efficient use of energy inall economies through developing programs to agree broadsets of objectives and international benchmarking, and facil-itate exchange of information and technologies;

• Facilitating the access and security of cross borderenergy investment and transit, so as to allow global andnational fuel and supplier diversity;

• Building on the G8 commitment at Gleneagles to alow carbon economy and adaptation to climate change byintegrating this with the energy security agenda;

• Supporting and strengthening initiatives by interna-tional institutions and others to support the poorest coun-tries in their adjustment to short term energy price shocks,and, in the longer run, to make healthy, clean affordableenergy available to all their citizens;

• Promoting transparency about energy resources, useand production through the whole energy chain, especially inthe critical oil market, by supporting and supplementing cur-rent initiatives and approaches as needed.

Source: World Bank briefing paper: Energy Security Issues,http://siteresources.worldbank.org/INTRUSSIANFEDERATION/Resources/Energy_Security_eng.pdf BT

· 11

The World Bank & CEFIR

Caspian Oil: Changing the World's Energy Outlook

Yadviga Semikolenova

After the collapse of the Sovietempire, the Caspian states of Azerbaijanand Kazakhstan managed to generate agreat deal of excitement over wildcatexploration of its poorly researched oiland gas fields. Despite falling oil prices,uncertain reserve sizes and a non-exis-tent legal framework, an extraordinaryvolume of international investmentpoured into the region in 1997 — 1998.By 1999, over 20 oil exploration con-tracts were signed in Azerbaijan alone,which represented over US$30 billion inlong-term capital investment with someUS$2.5 billion in committed investment.In Kazakhstan, direct foreign investmentin oil and gas amounted to US$2 billionfor 1991 — 1996. It was widely expect-ed that the poorly explored, but high-potential Caspian oil reserves wouldchange the world energy market and pro-vide an alternative to Middle Eastern oil.

However, the expectations overCaspian oil turned out to be quite exag-gerated and soon the Caspian hype wasover. Most of the projects failed to findenough reserves to justify commercialdevelopment of the fields. After 1999,most contracts were either closed or puton hold; and, two oil companies, Arcoand Conoco, decided to exit the region.

Caspian Oil Boom 1997�98:Information Herding?

The mid 1990s Caspian frenzy is dif-ficult to explain.

• The size of the Caspian provenreserves was not significant enough toattract such a massive investment flow insuch a short period of time. Azerbaijanand Kazakhstan's proven oil reserveswere 3.6 and 10 billion barrels respec-tively, which were much smaller than,say, Russia's 56 billion barrels.

• The potential size of Caspianreserves was quite uncertain for prospec-tive investors. The estimates of the upperboundary of probable reserves variedfrom the US Department of the Interior'sapproximation of 13.2 billion barrels inAzerbaijan to the estimate of 27 billion

barrels by the US State Department.• World oil prices were falling

when most oil companies entered theCaspian exploration projects in 1997 —1998. By the time the oil prices recoveredin 2000, the Caspian frenzy had died.

However, the dynamics of theCaspian frenzy may be explained byinformation herding. A lot of investorscould have come to the Caspian region asa part of the herd that was created byavailable public information, such asinvestment decisions by first-comers tothe region, the results of the first drillings,and various reports of credible agencies.The majority of the companies came tothe region in 1997 — 1998, after the USDepartment of State released its high esti-mates of Caspian potential reserves, andafter the first project moved to the devel-opment stage in November. The frenzywas over after the news of empty wellsand closed projects became available inlate 1998 and early 1999.

BTC: A New Energy Order?Everything changed, however, in the

spring of 2006 when the Baku-Tbilisi-Ceyhan (BTC) pipeline, connectingCaspian oil with the Turkish port ofCeyhan, became operational. A few daysearlier natural gas began passingthrough the newly completed SouthCaucasus Pipeline (SCP), which willdeliver gas to the Georgian and Turkishmarkets.

The talks about the possibility of anoil transit route bypassing Russia startedas early as 1994. As part of a ProductionSharing Agreement between Azerbaijanand BP signed in 1994, foreign investorswere supposed to find an export route forland-locked Azeri oil. Several possibleroutes were looked at, included the Baku-Novorossiysk pipeline through Russia,Baku-Supsa to the Georgian Black Seaport, and BTC to Turkey.

Before 2003, none of the bypassesseemed threatening enough to affect theRussian regional monopoly on oil trans-portation. According to experts, the

existing Baku-Supsa route together withthe Russian route to Novorossiysk couldonly have been expanded to transport450,000 barrels of Caspian oil a day, notenough to transport Caspian crude whenAzerbaijan’s fields of Azeri, Chirag anddeepwater Guneshli (AIOC contract leadby BP) would come to full productionstage in 2007 — 2010 averaging700,000 — 800,000 barrels per day.Thus, before 2003, it looked quite likelythat after AIOC moved to the full pro-duction stage Russian pipelines would bethe only export solution for the Azeri oil.

However, in late 2003 the threat of abypass became much more credible. Asoil prices were going up, the BTCPipeline Company, formed in 2002 andled by BP, found enough investors to goon with the project. The following year,Azeri and Kazakh officials launchedtalks on directing Kazakh oil flowsthrough BTC. In the fall of 2005 thepipeline was completed and in June2006, the first BTC oil reached theCeyhan terminal.

The competition of the Baku-Tbilisi-Ceyhan and the South Caucasus pipelinesis a huge milestone marking the end ofRussian dominance on the European ener-gy markets. The pipelines will re-shapeenergy consumption and the geopolitics ofthe region. First, they will decreaseRussian near-monopoly on energy transitfrom the Caspian states to global markets.Second, Russia will have to adapt to inter-national competition, but the way it doesso is difficult to predict. Third, Europeanconsumers now have access to Caspianenergy avoiding Russia all together, bothas an energy producer and transporter.Finally, Turkey will gain an importantposition on the European energy marketas a new energy crossroads.

Yadviga Semikolenova is AssistantProfessor at Division of Economics andBusiness, Colorado School of Mines. Thisarticle is based on two working papers thatare available upon request by contacting theauthor: [email protected] BT

Competition from two new pipelines marks the end of Russian dominance on European energy markets

·12 Theme of the Issue: Energy

Beyond Transition • April — June 2006

Vladimir Milov: "The state shouldleave the energy sector”

BT: Energy security will be one of thekey topics at the G8 Summit in St.Petersburg this year. What do Russia as awhole and Gazprom in particular, meanby energy security?

Because energy resources are highlyunevenly distributed among differentcountries, it is fair to say that the conceptof energy security varies from country tocountry depending on their resources ortheir access to resources in other coun-tries. The term itself appeared in import-dependent developed countries after theArab oil embargo in the 1970s, but a con-sensus understanding of energy securityhas never been achieved. Although Russiaproposed the theme of energy security forthe G8 summit a year ago I regret to saythat during the past year the world hasnot moved any nearer to common under-standing. Preparation for the summit hasbeen an intellectual debacle and Russia,unfortunately, has only been able to offerthe world a set of cliches that areremoved from the real situation. Indeed,by our practical actions we merely com-pounded the uncertainty in this sphere.

BT: Why should countries be inter-ested in achieving a consensus?

President Putin quite rightly wrote inhis article in The Wall Street Journal lastFebruary that energy egoism does notpay. About three quarters of world energyresources are concentrated in some tencountries which produce a little over 5%of world GDP in purchasing power pari-ty. The countries which produce morethan 70% of world GDP own only 10%of oil and gas resources, which are gradu-ally being depleted. Such a global imbal-ance is fraught with serious conflicts.Unless humanity creates a system thatguarantees the stable supply of energyresources in required amounts from sev-eral resource-rich countries, we will faceresource wars. I think it will depend in the

first place on the situation in such coun-tries as Russia, Saudi Arabia and Iran.

The role of Russia in oil is not asglobal as that of Saudi Arabia, however,Russia controls more than a third of theworld's proven gas resources and, ifadding yet-to-be-found resources, thenthis figure may rise to almost 50%. Theglobal gas demand will only be increas-ing: over the past 15 years gas consump-tion has been growing much faster thanthat of any other fuels in practically allthe regions of the world.

At present, especially now that thestate has gained control over keyresources, primarily over Gazprom,Russia is behaving in a rather selfish wayand claims special terms for the energysupplies into international markets. Thisviolates a kind of tacit understandingwith the West dating back to the times ofthe Soviet Union: we provide you withenergy in return for very good money, anarrangement that earned the country thereputation of a reliable supplier. NowRussia wants something more. Today theRussian authorities say that they want togain access to distribution networks inEuropean countries in exchange foraccess to Russian resources. But whatwill they demand tomorrow? If all theresource-rich countries start behavinglike this a serious situation may arise.

Energy security can be approached ina different way, namely, by finding abasis for a global consensus and offeringlong-term guarantees to resource-richcountries that they would be able toinvest in energy with a minimum risk.

BT: What guarantees do you see?Long-term contracts?

I wouldn't like to speak about con-crete mechanisms, there are many, andlong-term contracts are the simplest ofthem. What is important is to recognizethat producing countries need somecommercially attractive terms for devel-oping their resources, while the import-ing countries need guarantees that theywill get enough resources on marketterms. And no country will try to usurpresources or claim any special politicalprivileges in the international arena.

BT: Many experts and investors areworried about declining production inGazprom's main fields in WesternSiberia. But its CEO recently struck anoptimistic note at the world gas congresswhen he said that "in 2005 Gazpromregistered the largest growth of gasresources since 1993." How justified arethe fears of a possible shortage of gasand how serious can the consequences befor internal and external consumers?

The problem is not that Russia has noreserves in the ground: at current levels ofproduction, the resources will last morethan 80 years. There is a huge problemwith the economic system and incentivesto ensure timely extraction of the reservesfrom the ground and their delivery tomarket. In 1992, when Gazprom was cre-ated, the idea was mooted of creating sev-eral private independent gas companiesthat would compete among themselves.In the event, the advocates of a central-ized system prevailed, their main argu-ment being that only a powerful vertical-

Vladimir Milov is President of the Energy Policy Institute in Moscow and a former Deputy Minister ofEnergy of the Russian Federation. He shared his views on energy security and the problems of theRussian gas sector with BT’s Olga Mosina

· 13

The World Bank & CEFIR

ly integrated company could develop thegiant gas fields. It is true that Russia hasvery large deposits, for example, just twoof them on the Yamal Peninsula, accountfor more than 10% of all proven Russiangas resources. The problem is that 15years later, Gazprom has only developeda draft feasibility study for one of thedeposits, which was rejected last yearbecause of the inferior quality of thematerials. In my opinion, that is anindictment of Gazprom.

The very large gas condensate fieldsput into operation in the Soviet times,such as the Urengoy and Yamburg, whichtoday provide the bulk of Russian output,are rapidly being depleted. All Gazpromcan do in the near future in order to pre-vent a slump in production is to put near-by satellite fields into operation. But thatpotential will be quickly exhausted.

Gazprom's accrued investments ingas field development over the past sevenyears, amount to a mere US$12.5 billionin current prices. As a comparison,investments in oil production reachedUS$37 billion between 1999 and 2004,and the growth of oil production inrecent years has truly been an investmentgrowth. Gazprom, by contrast, prefers toinvest in other projects. In previous yearsit prioritized pipeline construction (main-ly export pipelines), and the purchase ofassets in oil, power and petrochemistryindustries.

Gas shortage is not a "prospect", it isalready here. Because gas demand ishighly seasonal, the shortage is visibleonly during peak periods, in winter. Allconsumers, both Russian and foreign,suffered during the last winter chills. Thesupply of gas to the power industry (themain consumer of gas in Russia) in sev-eral energy zones dropped to 15% of theagreed amounts on certain days. At thesame time Gazprom could not provideenough gas for Ukrainian and Europeanconsumers. The Ukrainians, who havefirst access to the pipeline, could tap intogas supplies, but the Europeans missedout on substantial volumes of gas.

BT: Are Gazprom's real interests notin extracting gas, but its export, process-ing and sale?

Gazprom prefers to invest instrengthening its monopoly power. Thecompany only has an annual budget anddoes not do long-term financial plan-ning. Implementing long-term risky proj-

ects runs counter to the economic logicof the very existence of the company.Gazprom looks exclusively to short-termtransactions, and it views borrowing notas a source of financing new projects butas a means to cover the cash gaps. Onecould perhaps understand Gazprom'sdifficulty in balancing the budget attimes of payment arrears by Russianconsumers and low gas prices in Europe.But today, with soaring prices in Europe

and a threefold increase of domestic realprices in the last six years, the companyis still barely making ends meet. In myopinion, it proves that Gazprom's eco-nomic system has no economic andinvestment logic, but is merely a tool inthe hands of external and internal lobby-ists. As a result, Gazprom invests inthose projects that may bring profits toinsiders or may increase its monopolypower and bring quick returns.

BT: What do you think of Gazprom'sstatements about exchanging assets withEuropean companies?

It is a natural way of integratingRussian business into international busi-ness. Russian oil and gas companiesestablished through privatization in theearly 1990s are not competitive in theinternational market. They need accessto new technologies and expertise ininvesting in complex long-term projectsthat large international corporationspossess. The value of integration inwhich the interests of various nationsintertwine lays the foundation for non-political, effective, and stable interactionbetween resource-rich and resource-poorcountries. Integration with Europeancompanies would have been possible ifour leaders did not meddle in pursuit oftheir own personal interests or attemptto control everything.

BT: Should the Europeans, then, beafraid of Gazprom investments in theirgas distribution networks?

Gazprom is not perceived as the bestagent for cooperation. First, the companyhas a host of internal problems and mas-sive inefficiencies, which impedes the cre-ation of alliances based on commercialconsiderations. Second, Gazprom is a

state-owned company and it is feared forpolitical reasons. But Russia itself behavesin a similar way. For example, the state-owned Chinese CNPC was blocked fromthe Slavneft auction in 2002.

Gazprom brags about its agreementwith BASF/Wintershall to sell a share inthe South-Russian field, but so far it hasbeen a one-off case and most probablyan exception from the rule, especiallysince Wintershall has a long history of

relations with some Gazprom insiders.Gazprom has no other examples of suc-cessful partnership, and has so far beenunable to agree with the German EON-Ruhrgas, Italy's ENI and Enel. The mainreason for failing partnerships isGazprom's political background.

BT: Could asset exchange lead todividing up Gazprom? Or, because youare skeptical about cooperation as such,what future awaits the company?

I think Gazprom's future is even worsethan the Soviet Union's in the late 1980s.I don't want to be a prophet of gloom anddoom, but I think we will see a completedisintegration of the sector with verygrave consequences for the gas market.

Gazprom holds licenses for hugefields which are not being developed.The sale of licenses or an equity share incompanies that develop the fields to out-side investors could solve the problem ofGazprom's accumulated debt and enableits restructuring. At the same time, out-side investors could have an opportunityto quickly develop the fields.

In the meantime, Gazprom is insistingon keeping the controlling stake in everyproject which, given its present financialsituation, decision-making process andgeneral effectiveness, makes equityfinancing of major projects impossible.

The development of oil fields by pri-vate foreign investors, for example theSakhalin-1 and Sakhalin-2 projects, hasshown that assets that fall into privatehands are already yielding returns. Theseprojects seem to be fairly successful,unlike other major Sakhalin projects inwhich the state has chosen to be in thedriving seat and where nothing has beenhappening. The state must leave the ener-gy sector and open it up to foreign com-panies if there is to be any progress. BT

Gazprom prefers to invest in strengthening its monopoly powerand looks exclusively to short�term transactions

·14 Theme of the Issue: Energy

Human Capital and the "Resource Curse"

Natalia Volchkova and Elena Suslova

One of the main issues on Russia’sdevelopment agenda is accelerating eco-nomic growth and creating an infrastruc-ture capable of sustaining that growth.The so-called "resource curse", whichrefers to an empirical regularity suggest-ing that the economies of resource-richcountries on average grow more slowlythan those of resource-poor countries,can be a major obstacle along that road.

Three Channels Modern economics has three main

groups of hypotheses regarding the chan-nels through which the "curse" is spread:

• The macroeconomic channel isconnected with the high resource pricevolatility in the world markets and theresulting volatility of GDP and nationalrevenues of resource-rich countries, whichmay be a serious obstacle to achievingsustained long-term economic growth.

• The most frequently discussedmicroeconomic channel is the so-called"Dutch disease", which refers to the flowof production factors from the manufac-turing industry into the sectors that pro-duce goods exclusively for the internalmarket (primarily, the service sector) andextractive sectors, in response to growingincomes in the extractive sectors. Howe-ver, empirical studies of many resource-dependent countries do not bear out thehypothesis of the negative correlationbetween the rate of long-term growth andvolatility of trade terms, nor of the nega-tive impact of the size of the extractivesector of industry on the size of the man-ufacturing sector. Studies of the dynamicsof the extractive and manufacturing sec-tors in the Russian economy over the past15 years has not provided any evidence ofa "Dutch disease" in Russia.

• More and more scholars areinclined to think that the main obstacleto further development of resource-dependent countries are insufficientlydeveloped institutions. However, in com-modity-oriented economies, because ofthe high economic rent created in theextractive industries, institutional back-wardness may make economic policymeasures aimed at stimulating the econ-

omy counter-productive, still furtherincreasing the country's dependence onraw materials.

A combination of a significantresource rent, poor property rights pro-tection, undeveloped and imperfect mar-kets and a poor legal system may be verydestructive to economic development.Many of the civil conflicts in the 20thcentury stemmed from attempts to seizecontrol of the rent; the fight for the rententails corruption in business and thestate, which substantially distortsresource allocation in the economy.

The availability of vast resources andthe constant flow of revenue they generateare not conducive to creating incentivesfor the state to carry out economic reform,the streamlining of public administrationand improving the quality of institutions.In other words, vast stocks of resourcecapital squeeze out the social capital.

Underdeveloped HumanCapital ?

Our analysis of 44 countries and 11sectors in the period between 1980 and1990 warrants some conclusions regard-ing the development of human capital inresource-dependent economies and itsimpact on economic growth.

The hypothesis about the existence ofthis channel for the spread of the"resource curse", as a part of the institu-tional channel, is based on two premises.First, many studies point out that re-source-rich economies sometimes tend tounderinvest in human capital comparedwith resource-poor economies. Resource-intensive sectors in the economy absorbthe bulk of investments in the economywithout creating highly skilled jobs. Thisis a disincentive for both private and pub-lic sectors to invest in education.

Second, both the classical and newgrowth theories stress the importance ofaccumulating human capital for generat-ing long-term economic growth. So, onecan expect that resource-rich countrieslose out to resource-poor countries interms of the rate of growth becausehuman capital in the former is not suffi-ciently developed.

Our approach to the study of the"resource curse" is based on the "differ-ence-in-difference" method, whichmakes it possible to track down the dif-ference in the growth rates of varioussectors of industry in various countrieswhile controlling for country and sec-toral variables. Sectors of industry areranged according to the particular sec-tor's demand for human capital at a cer-tain level, and countries are orderedaccording to the availability of naturalresources.

Human Capital�IntensiveIndustries Suffer

Analysis has shown that the differ-ence in the growth rates of the sectorsthat need a large number of workerswith a high human capital level and thesectors that have less need for suchworkers is less in countries with a highshare of primary exports. In otherwords, in the resource-rich countries thesectors that rely more on workers with ahigh level of human capital — and theseare the petrochemical industry, engineer-ing (other than electronics) etc. — are ina less favorable position compared, forexample, with the food industry, than inresource-poor countries. The result hasalso been confirmed for yet another cri-terion of resource wealth, the productionof oil and other hydrocarbons.

Summing up,• Intensive use of natural

resources suppresses growth in sectorsthat need workers with a high level ofhuman capital;

• The more a sector depends onhuman capital the more it loses out at thehands of natural resource development.

The results undoubtedly stress therole of investments in education as amechanism for overcoming the"resource curse".

Natalia Volchkova is a Senior Economistat the Centre for Economic and FinancialResearch (CEFIR) in Moscow. Elena Suslovais a graduate student at New EconomicSchool. The paper is forthcoming as CEFIRworking paper at www.cefir.org. BT

Intensive use of natural resources depresses growth in sectors employing workers with a high level ofhuman capital

Beyond Transition • April — June 2006

Energy Poverty in Macedonia andthe Czech Republic

Energy poverty is a condition wherehouseholds are living in inadequatelyheated homes, which can mean that eitherthe average daytime indoor temperature isbelow the biologically determined limit of21°C, or that the amount of warmth inthe home is lower than the subjective min-imum which allows an individual to per-form his/her everyday life.

Many countries in Central andEastern Europe and the former SovietUnion have undertaken significant energyprice increases, with the aim of removingthe inherited price structure. As most gov-ernments have been unable to develop thenecessary social safety net to protect vul-nerable households from price increases,there is a danger that energy poverty mayaffect millions of households in the region

leaving them with no option other than tocut back on energy purchase.

Energy poverty may create, and beperpetuated by, vicious circles betweeninvestment patterns, politics, and socialdeprivation. This is because the level offinal useful warmth in the home is relat-ed to the energy efficiency of the builtfabric, energy distribution installations,and domestic appliances. Patterns ofenergy poverty are thus contingent onlevels of investment and maintenance ofthese capital stocks. In the countrieswhere energy reforms have been slower,one of the reasons for the persistence ofcross-subsidies is the fear that energyprice increases may push significantnumbers of households into domesticenergy deprivation, thus causing socialand political unrest. But the maintenanceof below-cost pricing in the residentialsector hampers investment in the capitalstocks of energy efficiency, while encour-aging wasteful energy practices.

The study of the institutional, spatialand social underpinnings of energy pover-ty in Macedonia and the Czech Republicrelies on semi-structured interviews with

policy-makers, professionals, and house-holds in the two countries, as well as ana-lyzes of income and expenditure patterns,subjective perceptions of well-being, andassessments of housing quality.

Macedonia: Energy Povertyis a Lower� and Middle�ClassPhenomenon

One of the main aims of recentMacedonian economic policies was therestructuring of the state-owned ElectricPower Company of Macedonia thatmanaged all of the country's electricitygeneration, transmission and distribu-tion facilities. In order to prepare thestate-owned electricity monopoly for pri-vatization, household electricity tariffs

and disconnection rates were more thandoubled during the 1990s. Yet the coun-try failed to develop a comprehensiveenergy efficiency investment program inthe residential sector. So far Macedonialacks an adequate legal and institutionalframework for the formulation andimplementation of energy efficiency poli-cies, as well as effective mechanisms toregulate the thermal efficiency of newhousing. This is despite the fact thatnearly all housing in Macedonia is pri-vate and owner-occupied.

The emergence of the energy povertyproblem has transpired against the back-drop of a rapid increase in general pover-ty. The percentage of the population livingunder the relative poverty line now standsat nearly 30%, up from 4% in 1991. YetMacedonia still lacks a targeted energypoverty-amelioration policy. The onlymechanism is a relaxed disconnection pol-icy tacitly implemented by energy utilities,who often allow residential consumers tocontinue using electricity or district heat-ing despite months of non-payment. As awhole, these developments have led to ashift towards biomass (mainly wood) in

the national residential energy balance, sothat approximately 70% of the popula-tion currently relies on it for domesticheating, especially in rural areas. Districtheating networks outside of the capital,Skopje, are almost completely nonexist-ent. In medium-sized towns without dis-trict heating, households have been forcedto rely on electricity for heating, and thenumber of such households has grown toapproximately 30%.

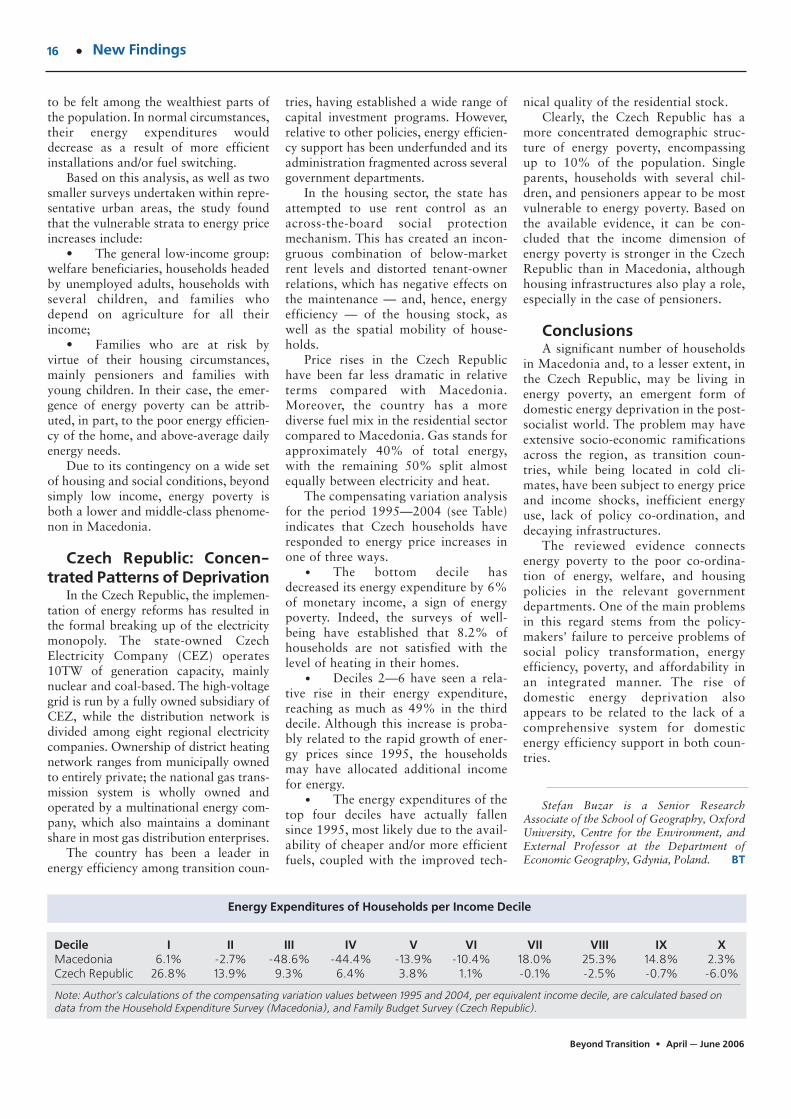

The demographic extent of energypoverty remains unknown, as there havebeen no direct surveys on the subject.However, the size of the problem can beestimated with the aid of the "compen-sating variation," which is applicable tonational household expenditure surveys.This method quantifies the percentage bywhich household incomes would havehad to change in 2004 in order for themto be able to retain the same ratio ofenergy expenditure relative to thenational average in 1995, when energyprices were still relatively low.

It transpired that the 60% of house-holds with lowest incomes would have toreceive additional funds ranging between27% and 1% of total equivalent income.At the same time, income would have tobe "taken away" from the top 30% ofhouseholds in order for their energyexpenditure ratios to remain the same in2004 and 1995. This means that the rela-tive energy expenditures of better-offhouseholds have increased in comparisonto the 1995 level, while the bottom 60%have been forced to cut back on theirenergy purchases (see Table).