the mcgraw-hill series

TRANSCRIPT

The McGraw-Hill Series Economics

ESSENTIALS OF ECONOMICS

Brue, McConnell, and FlynnEssentials of EconomicsSecond Edition

MandelEconomics: The BasicsFirst Edition

SchillerEssentials of EconomicsSeventh Edition

PRINCIPLES OF ECONOMICS

ColanderEconomics, Microeconomics,and MacroeconomicsSeventh Edition

Frank and BernankePrinciples of Economics,Principles of Microeconomics,Principles of MacroeconomicsFourth Edition

Frank and BernankeBrief Editions: Principles ofEconomics, Principles ofMicroeconomics, Principles ofMacroeconomicsFirst Edition

McConnell, Brue, and FlynnEconomics, Microeconomics,and MacroeconomicsEighteenth Edition

McConnell, Brue, and FlynnBrief Editions: Economics,Microeconomics,MacroeconomicsFirst Edition

MillerPrinciples of MicroeconomicsFirst Edition

Samuelson and NordhausEconomics, Microeconomics,and MacroeconomicsEighteenth Edition

SchillerThe Economy Today, The MicroEconomy Today, and The MacroEconomy TodayEleventh Edition

SlavinEconomics, Microeconomics,and MacroeconomicsNinth Edition

ECONOMICS OF SOCIAL ISSUES

GuellIssues in Economics TodayFourth Edition

Sharp, Register, and GrimesEconomics of Social IssuesEighteenth Edition

ECONOMETRICS

Gujarati and PorterBasic Econometrics Fifth Edition

Gujarati and PorterEssentials of Econometrics Fourth Edition

MANAGERIAL ECONOMICS

BayeManagerial Economics and BusinessStrategySixth Edition

Brickley, Smith, and ZimmermanManagerial Economics andOrganizational ArchitectureFifth Edition

Thomas and MauriceManagerial EconomicsNinth Edition

INTERMEDIATE ECONOMICS

Bernheim and WhinstonMicroeconomicsFirst Edition

Dornbusch, Fischer, and StartzMacroeconomicsTenth Edition

FrankMicroeconomics and BehaviorSeventh Edition

ADVANCED ECONOMICS

RomerAdvanced MacroeconomicsThird Edition

MONEY AND BANKING

CecchettiMoney, Banking, and FinancialMarketsSecond Edition

URBAN ECONOMICS

O’SullivanUrban EconomicsSeventh Edition

LABOR ECONOMICS

BorjasLabor EconomicsFourth Edition

McConnell, Brue, and MacphersonContemporary Labor EconomicsEighth Edition

PUBLIC FINANCE

Rosen and GayerPublic FinanceEighth Edition

SeidmanPublic FinanceFirst Edition

ENVIRONMENTAL ECONOMICS

Field and FieldEnvironmental Economics:An IntroductionFifth Edition

INTERNATIONAL ECONOMICS

Appleyard, Field, and CobbInternational EconomicsSixth Edition

King and KingInternational Economics,Globalization, and Policy: A ReaderFifth Edition

PugelInternational EconomicsFourteenth Edition

guj75772_IFC.qxd 01/08/2008 10:06 AM Page 2

Basic Econometrics

Fifth Edition

Damodar N. GujaratiProfessor Emeritus of Economics,United States Military Academy, West Point

Dawn C. PorterUniversity of Southern California

Boston Burr Ridge, IL Dubuque, IA New York San Francisco St. LouisBangkok Bogotá Caracas Kuala Lumpur Lisbon London Madrid Mexico CityMilan Montreal New Delhi Santiago Seoul Singapore Sydney Taipei Toronto

guj75772_fm.qxd 05/09/2008 11:15 AM Page i

BASIC ECONOMETRICS

Published by McGraw-Hill/Irwin, a business unit of The McGraw-Hill Companies, Inc., 1221 Avenue of theAmericas, New York, NY, 10020. Copyright © 2009, 2003, 1995, 1988, 1978 by The McGraw-Hill Companies,Inc. All rights reserved. No part of this publication may be reproduced or distributed in any form or by anymeans, or stored in a database or retrieval system, without the prior written consent of The McGraw-HillCompanies, Inc., including, but not limited to, in any network or other electronic storage or transmission, orbroadcast for distance learning.

Some ancillaries, including electronic and print components, may not be available to customers outside theUnited States.

This book is printed on acid-free paper.

1 2 3 4 5 6 7 8 9 0 VNH/VNH 0 9 8

ISBN 978-0-07-337577-9MHID 0-07-337577-2

Publisher: Douglas ReinerDevelopmental editor: Anne E. HilbertEditorial coordinator: Noelle FoxAssociate marketing manager: Dean KarampelasLead Project manager: Christine A. VaughanFull-service project manager: Michael Ryder, ICC Macmillan Inc.Lead production supervisor: Carol A. BielskiDesign coordinator: Joanne MennemeierMedia project manager: Srikanth Potluri, Hurix Systems Pvt. Ltd.Cover design: Brittany SkwierczynskiTypeface: 10/12 TimesNewRomanPSCompositor: ICC Macmillan Inc.Printer: R. R. Donnelley

Library of Congress Cataloging-in-Publication Data

Gujarati, Damodar N.Basic econometrics / Damodar N. Gujarati, Dawn C. Porter. — 5th ed.

p. cm.Includes bibliographical references and index.ISBN-13: 978-0-07-337577-9 (alk. paper)ISBN-10: 0-07-337577-2 (alk. paper)1. Econometrics. I. Porter, Dawn C. II. Title.

HB139.G84 2009330.01�5195—dc22

2008035934

www.mhhe.com

guj75772_fm.qxd 05/09/2008 11:15 AM Page ii

About the AuthorsDamodar N. GujaratiAfter teaching for more than 25 years at the City University of New York and 17 years in theDepartment of Social Sciences, U.S. Military Academy at West Point, New York, Dr. Gujaratiis currently Professor Emeritus of economics at the Academy. Dr. Gujarati received hisM.Com. degree from the University of Bombay in 1960, his M.B.A. degree from theUniversity of Chicago in 1963, and his Ph.D. degree from the University of Chicago in 1965.Dr. Gujarati has published extensively in recognized national and international journals, suchas the Review of Economics and Statistics, the Economic Journal, the Journal of Financialand Quantitative Analysis, and the Journal of Business. Dr. Gujarati was a member of theBoard of Editors of the Journal of Quantitative Economics, the official journal of the IndianEconometric Society. Dr. Gujarati is also the author of Pensions and the New York City FiscalCrisis (the American Enterprise Institute, 1978), Government and Business (McGraw-Hill,1984), and Essentials of Econometrics (McGraw-Hill, 3d ed., 2006). Dr. Gujarati’s bookson econometrics have been translated into several languages.

Dr. Gujarati was a Visiting Professor at the University of Sheffield, U.K. (1970–1971), aVisiting Fulbright Professor to India (1981–1982), a Visiting Professor in the School ofManagement of the National University of Singapore (1985–1986), and a Visiting Professorof Econometrics, University of New South Wales, Australia (summer of 1988). Dr. Gujaratihas lectured extensively on micro- and macroeconomic topics in countries such asAustralia,China, Bangladesh, Germany, India, Israel, Mauritius, and the Republic of South Korea.

Dawn C. PorterDawn Porter has been an assistant professor in the Information and Operations Manage-ment Department at the Marshall School of Business of the University of SouthernCalifornia since the fall of 2006. She currently teaches both introductory undergraduateand MBA statistics in the business school. Prior to joining the faculty at USC, from2001–2006, Dawn was an assistant professor at the McDonough School of Business atGeorgetown University, and before that was a visiting professor in the psychology depart-ment at the Graduate School of Arts and Sciences at NYU. At NYU she taught a number ofadvanced statistical methods courses and was also an instructor at the Stern School ofBusiness. Her Ph.D. is from the Stern School in Statistics.

Dawn’s areas of research interest include categorical analysis, agreement measures,multivariate modeling, and applications to the field of psychology. Her current research ex-amines online auction models from a statistical perspective. She has presented her researchat the Joint Statistical Meetings, the Decision Sciences Institute meetings, the InternationalConference on Information Systems, several universities including the London School ofEconomics and NYU, and various e-commerce and statistics seminar series. Dawn is alsoa co-author on Essentials of Business Statistics, 2nd edition, McGraw-Hill Irwin, 2008.Outside of academics, Dawn has been employed as a statistical consultant for KPMG, Inc.She has also worked as a statistical consultant for many other major companies, includingGinnie Mae, Inc., Toys R Us Corporation, IBM, Cosmaire, Inc., and New York University(NYU) Medical Center.

iii

guj75772_fm.qxd 05/09/2008 11:15 AM Page iii

For Joan Gujarati, Diane Gujarati-Chesnut,

Charles Chesnut, and my grandchildren,

“Tommy” and Laura Chesnut.

—DNG

For Judy, Lee, Brett, Bryan, Amy, and Autumn Porter.

But especially for my adoring father, Terry.

—DCP

guj75772_fm.qxd 05/09/2008 11:15 AM Page iv

Brief ContentsPreface xviAcknowledgments xix

Introduction 1

PART ONESingle-Equation Regression Models 13

1 The Nature of Regression Analysis 15

2 Two-Variable Regression Analysis: Some Basic Ideas 34

3 Two-Variable Regression Model: TheProblem of Estimation 55

4 Classical Normal Linear RegressionModel (CNLRM) 97

5 Two-Variable Regression: IntervalEstimation and Hypothesis Testing 107

6 Extensions of the Two-Variable Linear Regression Model 147

7 Multiple Regression Analysis: TheProblem of Estimation 188

8 Multiple Regression Analysis: TheProblem of Inference 233

9 Dummy Variable Regression Models 277

PART TWORelaxing the Assumptions of the Classical Model 315

10 Multicollinearity: What HappensIf the Regressors Are Correlated? 320

11 Heteroscedasticity: What Happens Ifthe Error Variance Is Nonconstant? 365

12 Autocorrelation: What Happens Ifthe Error Terms Are Correlated? 412

13 Econometric Modeling: ModelSpecification and Diagnostic Testing 467

PART THREETopics in Econometrics 523

14 Nonlinear Regression Models 525

15 Qualitative Response Regression Models 541

16 Panel Data Regression Models 591

17 Dynamic Econometric Models:Autoregressive andDistributed-Lag Models 617

PART FOURSimultaneous-Equation Models and TimeSeries Econometrics 671

18 Simultaneous-Equation Models 673

19 The Identification Problem 689

20 Simultaneous-Equation Methods 711

21 Time Series Econometrics: Some Basic Concepts 737

22 Time Series Econometrics: Forecasting 773

APPENDICESA A Review of Some

Statistical Concepts 801

B Rudiments of Matrix Algebra 838

C The Matrix Approach to Linear Regression Model 849

D Statistical Tables 877

E Computer Output of EViews, MINITAB, Excel, and STATA 894

F Economic Data on the World Wide Web 900

SELECTED BIBLIOGRAPHY 902

v

guj75772_fm.qxd 05/09/2008 11:15 AM Page v

vi

ContentsPreface xviAcknowledgments xix

Introduction 1

I.1 What Is Econometrics? 1I.2 Why a Separate Discipline? 2I.3 Methodology of Econometrics 2

1. Statement of Theory or Hypothesis 32. Specification of the Mathematical Model

of Consumption 33. Specification of the Econometric Model

of Consumption 44. Obtaining Data 55. Estimation of the Econometric Model 56. Hypothesis Testing 77. Forecasting or Prediction 88. Use of the Model for Control

or Policy Purposes 9Choosing among Competing Models 9

I.4 Types of Econometrics 10I.5 Mathematical and Statistical Prerequisites 11I.6 The Role of the Computer 11I.7 Suggestions for Further Reading 12

PART ONESINGLE-EQUATION REGRESSIONMODELS 13

CHAPTER 1The Nature of Regression Analysis 15

1.1 Historical Origin of the Term Regression 151.2 The Modern Interpretation of Regression 15

Examples 161.3 Statistical versus Deterministic

Relationships 191.4 Regression versus Causation 191.5 Regression versus Correlation 201.6 Terminology and Notation 211.7 The Nature and Sources of Data for Economic

Analysis 22Types of Data 22The Sources of Data 25The Accuracy of Data 27A Note on the Measurement Scales of Variables 27

Summary and Conclusions 28Exercises 29

CHAPTER 2Two-Variable Regression Analysis: SomeBasic Ideas 34

2.1 A Hypothetical Example 342.2 The Concept of Population Regression

Function (PRF) 372.3 The Meaning of the Term Linear 38

Linearity in the Variables 38Linearity in the Parameters 38

2.4 Stochastic Specification of PRF 392.5 The Significance of the Stochastic

Disturbance Term 412.6 The Sample Regression Function (SRF) 422.7 Illustrative Examples 45

Summary and Conclusions 48Exercises 48

CHAPTER 3Two-Variable Regression Model: TheProblem of Estimation 55

3.1 The Method of Ordinary Least Squares 553.2 The Classical Linear Regression Model: The

Assumptions Underlying the Method of Least Squares 61

A Word about These Assumptions 683.3 Precision or Standard Errors

of Least-Squares Estimates 693.4 Properties of Least-Squares Estimators:

The Gauss–Markov Theorem 713.5 The Coefficient of Determination r2:

A Measure of “Goodness of Fit” 733.6 A Numerical Example 783.7 Illustrative Examples 813.8 A Note on Monte Carlo Experiments 83

Summary and Conclusions 84Exercises 85Appendix 3A 92

3A.1 Derivation of Least-Squares Estimates 923A.2 Linearity and Unbiasedness Properties

of Least-Squares Estimators 923A.3 Variances and Standard Errors

of Least-Squares Estimators 93

guj75772_fm.qxd 05/09/2008 11:15 AM Page vi

Contents vii

3A.4 Covariance Between β1 and β2 933A.5 The Least-Squares Estimator of σ2 933A.6 Minimum-Variance Property

of Least-Squares Estimators 953A.7 Consistency of Least-Squares Estimators 96

CHAPTER 4Classical Normal Linear Regression Model (CNLRM) 97

4.1 The Probability Distribution of Disturbances ui 97

4.2 The Normality Assumption for ui 98Why the Normality Assumption? 99

4.3 Properties of OLS Estimators under the Normality Assumption 100

4.4 The Method of Maximum Likelihood (ML) 102Summary and Conclusions 102Appendix 4A 103

4A.1 Maximum Likelihood Estimation of Two-Variable Regression Model 103

4A.2 Maximum Likelihood Estimation of Food Expenditure in India 105Appendix 4A Exercises 105

CHAPTER 5Two-Variable Regression: IntervalEstimation and Hypothesis Testing 107

5.1 Statistical Prerequisites 1075.2 Interval Estimation: Some Basic Ideas 1085.3 Confidence Intervals for Regression

Coefficients β1 and β2 109Confidence Interval for β2 109Confidence Interval for β1 and β2

Simultaneously 1115.4 Confidence Interval for σ2 1115.5 Hypothesis Testing: General Comments 1135.6 Hypothesis Testing:

The Confidence-Interval Approach 113Two-Sided or Two-Tail Test 113One-Sided or One-Tail Test 115

5.7 Hypothesis Testing: The Test-of-Significance Approach 115

Testing the Significance of RegressionCoefficients: The t Test 115Testing the Significance of σ2: The χ2 Test 118

5.8 Hypothesis Testing: Some Practical Aspects 119The Meaning of “Accepting” or “Rejecting” aHypothesis 119

The “Zero” Null Hypothesis and the “2-t” Ruleof Thumb 120Forming the Null and Alternative Hypotheses 121Choosing α, the Level of Significance 121The Exact Level of Significance: The p Value 122Statistical Significance versus PracticalSignificance 123The Choice between Confidence-Intervaland Test-of-Significance Approachesto Hypothesis Testing 124

5.9 Regression Analysis and Analysis of Variance 124

5.10 Application of Regression Analysis: The Problem of Prediction 126

Mean Prediction 127Individual Prediction 128

5.11 Reporting the Results of Regression Analysis 129

5.12 Evaluating the Results of Regression Analysis 130

Normality Tests 130Other Tests of Model Adequacy 132

Summary and Conclusions 134Exercises 135Appendix 5A 143

5A.1 Probability Distributions Related to the Normal Distribution 143

5A.2 Derivation of Equation (5.3.2) 1455A.3 Derivation of Equation (5.9.1) 1455A.4 Derivations of Equations (5.10.2)

and (5.10.6) 145Variance of Mean Prediction 145Variance of Individual Prediction 146

CHAPTER 6Extensions of the Two-Variable LinearRegression Model 147

6.1 Regression through the Origin 147r2 for Regression-through-Origin Model 150

6.2 Scaling and Units of Measurement 154A Word about Interpretation 157

6.3 Regression on Standardized Variables 1576.4 Functional Forms of Regression Models 1596.5 How to Measure Elasticity: The Log-Linear

Model 1596.6 Semilog Models: Log–Lin and Lin–Log

Models 162

guj75772_fm.qxd 05/09/2008 11:15 AM Page vii

viii Contents

How to Measure the Growth Rate: The Log–Lin Model 162The Lin–Log Model 164

6.7 Reciprocal Models 166Log Hyperbola or Logarithmic ReciprocalModel 172

6.8 Choice of Functional Form 1726.9 A Note on the Nature of the Stochastic Error

Term: Additive versus MultiplicativeStochastic Error Term 174Summary and Conclusions 175Exercises 176Appendix 6A 182

6A.1 Derivation of Least-Squares Estimatorsfor Regression through the Origin 182

6A.2 Proof that a Standardized Variable Has Zero Mean and Unit Variance 183

6A.3 Logarithms 1846A.4 Growth Rate Formulas 1866A.5 Box-Cox Regression Model 187

CHAPTER 7Multiple Regression Analysis:The Problem of Estimation 188

7.1 The Three-Variable Model: Notationand Assumptions 188

7.2 Interpretation of Multiple Regression Equation 191

7.3 The Meaning of Partial RegressionCoefficients 191

7.4 OLS and ML Estimation of the Partial Regression Coefficients 192

OLS Estimators 192Variances and Standard Errors of OLS Estimators 194Properties of OLS Estimators 195Maximum Likelihood Estimators 196

7.5 The Multiple Coefficient of Determination R2

and the Multiple Coefficient of Correlation R 196

7.6 An Illustrative Example 198Regression on Standardized Variables 199Impact on the Dependent Variable of a UnitChange in More than One Regressor 199

7.7 Simple Regression in the Context of Multiple Regression: Introduction toSpecification Bias 200

7.8 R2 and the Adjusted R2 201Comparing Two R2 Values 203

Allocating R2 among Regressors 206The “Game’’ of Maximizing R

–2 2067.9 The Cobb–Douglas Production Function:

More on Functional Form 2077.10 Polynomial Regression Models 2107.11 Partial Correlation Coefficients 213

Explanation of Simple and Partial Correlation Coefficients 213Interpretation of Simple and Partial Correlation Coefficients 214

Summary and Conclusions 215Exercises 216Appendix 7A 227

7A.1 Derivation of OLS EstimatorsGiven in Equations (7.4.3) to (7.4.5) 227

7A.2 Equality between the Coefficients of PGNP in Equations (7.3.5) and (7.6.2) 229

7A.3 Derivation of Equation (7.4.19) 2297A.4 Maximum Likelihood Estimation

of the Multiple Regression Model 2307A.5 EViews Output of the Cobb–Douglas

Production Function in Equation (7.9.4) 231

CHAPTER 8Multiple Regression Analysis: The Problemof Inference 233

8.1 The Normality Assumption Once Again 2338.2 Hypothesis Testing in Multiple Regression:

General Comments 2348.3 Hypothesis Testing about Individual

Regression Coefficients 2358.4 Testing the Overall Significance of the Sample

Regression 237The Analysis of Variance Approach to Testing theOverall Significance of an Observed MultipleRegression: The F Test 238Testing the Overall Significance of a MultipleRegression: The F Test 240An Important Relationship between R2 and F 241Testing the Overall Significance of a MultipleRegression in Terms of R2 242The “Incremental” or “Marginal” Contributionof an Explanatory Variable 243

8.5 Testing the Equality of Two RegressionCoefficients 246

8.6 Restricted Least Squares: Testing LinearEquality Restrictions 248

The t-Test Approach 249

guj75772_fm.qxd 05/09/2008 11:15 AM Page viii

Contents ix

The F-Test Approach: Restricted Least Squares 249General F Testing 252

8.7 Testing for Structural or Parameter Stability of Regression Models: The Chow Test 254

8.8 Prediction with Multiple Regression 2598.9 The Troika of Hypothesis Tests: The

Likelihood Ratio (LR), Wald (W), andLagrange Multiplier (LM) Tests 259

8.10 Testing the Functional Form of Regression:Choosing between Linear and Log–LinearRegression Models 260Summary and Conclusions 262Exercises 262Appendix 8A: Likelihood Ratio (LR) Test 274

CHAPTER 9Dummy Variable Regression Models 277

9.1 The Nature of Dummy Variables 2779.2 ANOVA Models 278

Caution in the Use of Dummy Variables 2819.3 ANOVA Models with Two Qualitative

Variables 2839.4 Regression with a Mixture of Quantitative

and Qualitative Regressors: The ANCOVA Models 283

9.5 The Dummy Variable Alternative to the Chow Test 285

9.6 Interaction Effects Using Dummy Variables 288

9.7 The Use of Dummy Variables in SeasonalAnalysis 290

9.8 Piecewise Linear Regression 2959.9 Panel Data Regression Models 2979.10 Some Technical Aspects of the Dummy

Variable Technique 297The Interpretation of Dummy Variables in Semilogarithmic Regressions 297Dummy Variables and Heteroscedasticity 298Dummy Variables and Autocorrelation 299What Happens If the Dependent Variable Is a Dummy Variable? 299

9.11 Topics for Further Study 3009.12 A Concluding Example 300

Summary and Conclusions 304Exercises 305Appendix 9A: Semilogarithmic Regressionwith Dummy Regressor 314

PART TWORELAXING THE ASSUMPTIONS OF THECLASSICAL MODEL 315

CHAPTER 10Multicollinearity: What HappensIf the Regressors Are Correlated? 320

10.1 The Nature of Multicollinearity 32110.2 Estimation in the Presence of Perfect

Multicollinearity 32410.3 Estimation in the Presence of “High”

but “Imperfect” Multicollinearity 32510.4 Multicollinearity: Much Ado about Nothing?

Theoretical Consequences of Multicollinearity 326

10.5 Practical Consequences of Multicollinearity 327

Large Variances and Covariances of OLS Estimators 328Wider Confidence Intervals 330“Insignificant” t Ratios 330A High R2 but Few Significant t Ratios 331Sensitivity of OLS Estimators and TheirStandard Errors to Small Changes in Data 331Consequences of Micronumerosity 332

10.6 An Illustrative Example 33210.7 Detection of Multicollinearity 33710.8 Remedial Measures 342

Do Nothing 342Rule-of-Thumb Procedures 342

10.9 Is Multicollinearity Necessarily Bad? MaybeNot, If the Objective Is Prediction Only 347

10.10 An Extended Example: The Longley Data 347Summary and Conclusions 350Exercises 351

CHAPTER 11Heteroscedasticity: What Happens Ifthe Error Variance Is Nonconstant? 365

11.1 The Nature of Heteroscedasticity 36511.2 OLS Estimation in the Presence

of Heteroscedasticity 37011.3 The Method of Generalized Least

Squares (GLS) 371Difference between OLS and GLS 373

11.4 Consequences of Using OLS in the Presence of Heteroscedasticity 374

guj75772_fm.qxd 05/09/2008 11:15 AM Page ix

x Contents

OLS Estimation Allowing for Heteroscedasticity 374OLS Estimation Disregarding Heteroscedasticity 374A Technical Note 376

11.5 Detection of Heteroscedasticity 376Informal Methods 376Formal Methods 378

11.6 Remedial Measures 389When σ2

i Is Known: The Method of WeightedLeast Squares 389When σ2

i Is Not Known 39111.7 Concluding Examples 39511.8 A Caution about Overreacting

to Heteroscedasticity 400Summary and Conclusions 400Exercises 401Appendix 11A 409

11A.1 Proof of Equation (11.2.2) 40911A.2 The Method of Weighted Least

Squares 40911A.3 Proof that E(σ 2) �σ2 in the Presence

of Heteroscedasticity 41011A.4 White’s Robust Standard Errors 411

CHAPTER 12Autocorrelation: What Happens If the ErrorTerms Are Correlated? 412

12.1 The Nature of the Problem 41312.2 OLS Estimation in the Presence

of Autocorrelation 41812.3 The BLUE Estimator in the Presence

of Autocorrelation 42212.4 Consequences of Using OLS

in the Presence of Autocorrelation 423OLS Estimation Allowing for Autocorrelation 423OLS Estimation Disregarding Autocorrelation 423

12.5 Relationship between Wages and Productivityin the Business Sector of the United States,1960–2005 428

12.6 Detecting Autocorrelation 429I. Graphical Method 429

II. The Runs Test 431III. Durbin–Watson d Test 434IV. A General Test of Autocorrelation:

The Breusch–Godfrey (BG) Test 438Why So Many Tests of Autocorrelation? 440

12.7 What to Do When You Find Autocorrelation:Remedial Measures 440

12.8 Model Mis-Specification versus PureAutocorrelation 441

12.9 Correcting for (Pure) Autocorrelation: The Method of Generalized Least Squares (GLS) 442

When ρ Is Known 442When ρ Is Not Known 443

12.10 The Newey–West Method of Correctingthe OLS Standard Errors 447

12.11 OLS versus FGLS and HAC 44812.12 Additional Aspects of Autocorrelation 449

Dummy Variables and Autocorrelation 449ARCH and GARCH Models 449Coexistence of Autocorrelationand Heteroscedasticity 450

12.13 A Concluding Example 450Summary and Conclusions 452Exercises 453Appendix 12A 466

12A.1 Proof that the Error Term vt inEquation (12.1.11) Is Autocorrelated 466

12A.2 Proof of Equations (12.2.3), (12.2.4),and (12.2.5) 466

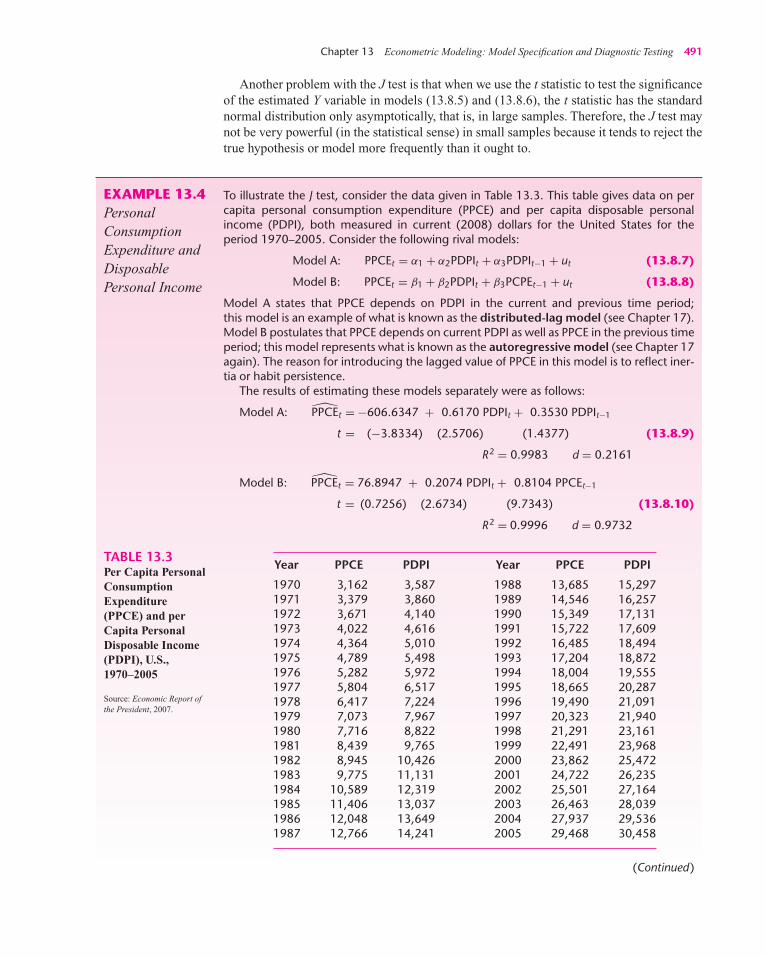

CHAPTER 13Econometric Modeling: Model Specification and Diagnostic Testing 467

13.1 Model Selection Criteria 46813.2 Types of Specification Errors 46813.3 Consequences of Model Specification

Errors 470Underfitting a Model (Omitting a RelevantVariable) 471Inclusion of an Irrelevant Variable (Overfitting a Model) 473

13.4 Tests of Specification Errors 474Detecting the Presence of Unnecessary Variables(Overfitting a Model) 475Tests for Omitted Variables and IncorrectFunctional Form 477

13.5 Errors of Measurement 482Errors of Measurement in the DependentVariable Y 482Errors of Measurement in the ExplanatoryVariable X 483

13.6 Incorrect Specification of the Stochastic Error Term 486

guj75772_fm.qxd 05/09/2008 11:15 AM Page x

Contents xi

13.7 Nested versus Non-Nested Models 48713.8 Tests of Non-Nested Hypotheses 488

The Discrimination Approach 488The Discerning Approach 488

13.9 Model Selection Criteria 493The R2 Criterion 493Adjusted R2 493Akaike’s Information Criterion (AIC) 494Schwarz’s Information Criterion (SIC) 494Mallows’s Cp Criterion 494A Word of Caution about Model Selection Criteria 495Forecast Chi-Square (χ2) 496

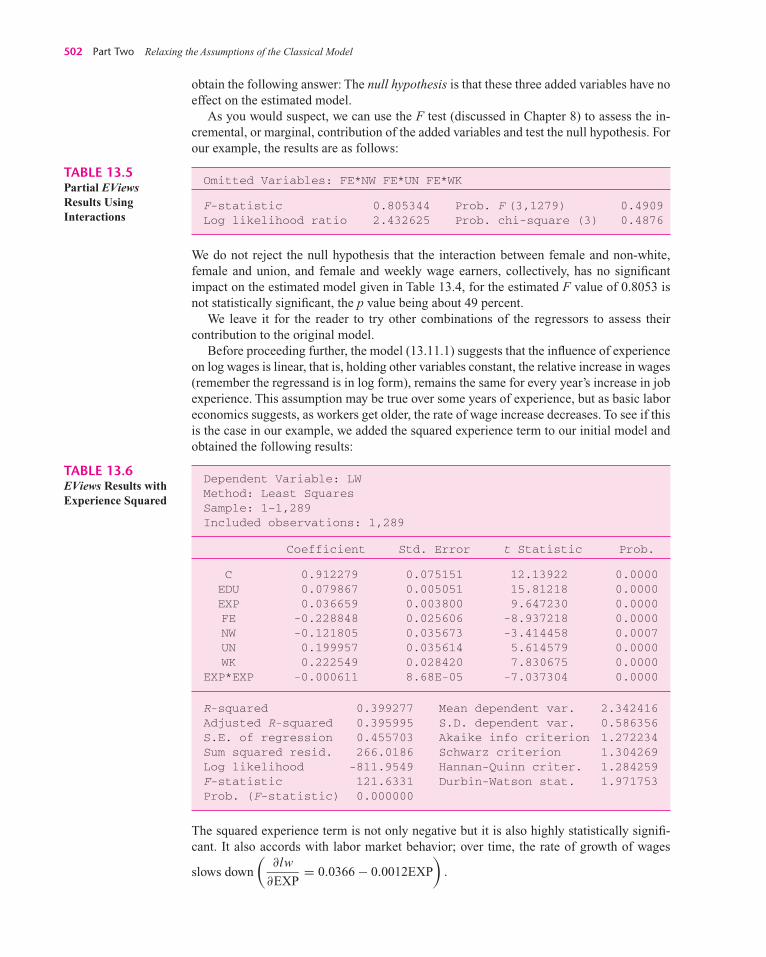

13.10 Additional Topics in Econometric Modeling 496

Outliers, Leverage, and Influence 496Recursive Least Squares 498Chow’s Prediction Failure Test 498Missing Data 499

13.11 Concluding Examples 5001. A Model of Hourly Wage Determination 5002. Real Consumption Function for the United

States, 1947–2000 50513.12 Non-Normal Errors and Stochastic

Regressors 5091. What Happens If the Error Term Is Not

Normally Distributed? 5092. Stochastic Explanatory Variables 510

13.13 A Word to the Practitioner 511Summary and Conclusions 512Exercises 513Appendix 13A 519

13A.1 The Proof that E(b1 2) = β2 + β3b3 2

[Equation (13.3.3)] 51913A.2 The Consequences of Including an Irrelevant

Variable: The Unbiasedness Property 52013A.3 The Proof of Equation (13.5.10) 52113A.4 The Proof of Equation (13.6.2) 522

PART THREETOPICS IN ECONOMETRICS 523

CHAPTER 14Nonlinear Regression Models 525

14.1 Intrinsically Linear and IntrinsicallyNonlinear Regression Models 525

14.2 Estimation of Linear and NonlinearRegression Models 527

14.3 Estimating Nonlinear Regression Models: The Trial-and-Error Method 527

14.4 Approaches to Estimating NonlinearRegression Models 529

Direct Search or Trial-and-Error or Derivative-Free Method 529Direct Optimization 529Iterative Linearization Method 530

14.5 Illustrative Examples 530Summary and Conclusions 535Exercises 535Appendix 14A 537

14A.1 Derivation of Equations (14.2.4) and (14.2.5) 537

14A.2 The Linearization Method 53714A.3 Linear Approximation of the Exponential

Function Given in Equation (14.2.2) 538

CHAPTER 15Qualitative Response Regression Models 541

15.1 The Nature of Qualitative Response Models 541

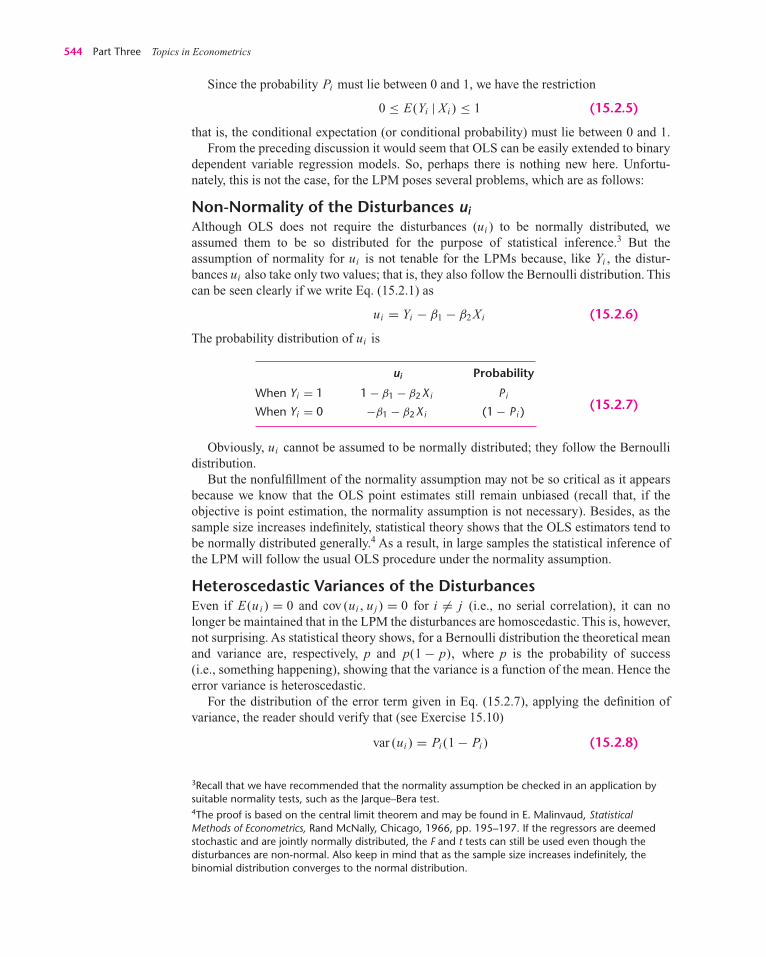

15.2 The Linear Probability Model (LPM) 543Non-Normality of the Disturbances ui 544Heteroscedastic Variances of the Disturbances 544Nonfulfillment of 0 ≤ E(Yi | Xi) ≤ 1 545Questionable Value of R2 as a Measureof Goodness of Fit 546

15.3 Applications of LPM 54915.4 Alternatives to LPM 55215.5 The Logit Model 55315.6 Estimation of the Logit Model 555

Data at the Individual Level 556Grouped or Replicated Data 556

15.7 The Grouped Logit (Glogit) Model: ANumerical Example 558

Interpretation of the Estimated Logit Model 558

15.8 The Logit Model for Ungrouped or Individual Data 561

15.9 The Probit Model 566Probit Estimation with Grouped Data: gprobit 567The Probit Model for Ungrouped or Individual Data 570The Marginal Effect of a Unit Change in the Value of a Regressor in the VariousRegression Models 571

guj75772_fm.qxd 09/09/2008 12:15 PM Page xi

xii Contents

15.10 Logit and Probit Models 57115.11 The Tobit Model 574

Illustration of the Tobit Model: Ray Fair’s Model of Extramarital Affairs 575

15.12 Modeling Count Data: The Poisson Regression Model 576

15.13 Further Topics in Qualitative ResponseRegression Models 579

Ordinal Logit and Probit Models 580Multinomial Logit and Probit Models 580Duration Models 580

Summary and Conclusions 581Exercises 582Appendix 15A 589

15A.1 Maximum Likelihood Estimation of the Logitand Probit Models for Individual (Ungrouped)Data 589

CHAPTER 16 Panel Data Regression Models 591

16.1 Why Panel Data? 59216.2 Panel Data: An Illustrative Example 59316.3 Pooled OLS Regression or Constant

Coefficients Model 59416.4 The Fixed Effect Least-Squares Dummy

Variable (LSDV) Model 596A Caution in the Use of the Fixed Effect LSDV Model 598

16.5 The Fixed-Effect Within-Group (WG)Estimator 599

16.6 The Random Effects Model (REM) 602Breusch and Pagan Lagrange Multiplier Test 605

16.7 Properties of Various Estimators 60516.8 Fixed Effects versus Random Effects Model:

Some Guidelines 60616.9 Panel Data Regressions: Some Concluding

Comments 60716.10 Some Illustrative Examples 607

Summary and Conclusions 612Exercises 613

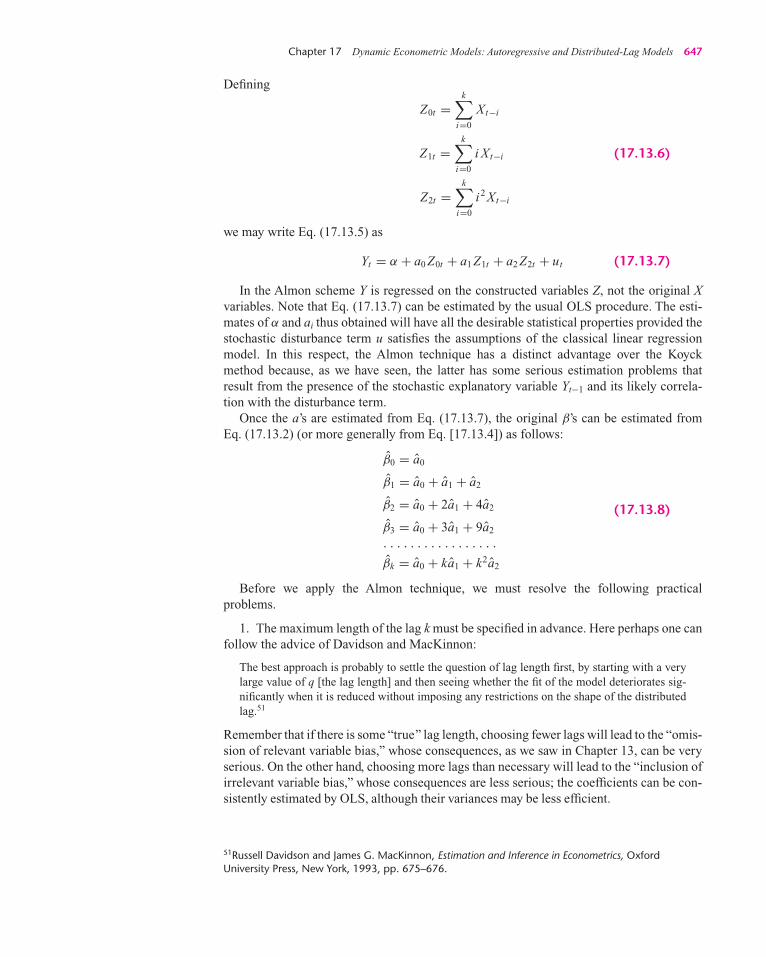

CHAPTER 17 Dynamic Econometric Models:Autoregressiveand Distributed-Lag Models 617

17.1 The Role of “Time,’’ or “Lag,’’in Economics 618

17.2 The Reasons for Lags 622

17.3 Estimation of Distributed-Lag Models 623Ad Hoc Estimation of Distributed-Lag Models 623

17.4 The Koyck Approach to Distributed-LagModels 624

The Median Lag 627The Mean Lag 627

17.5 Rationalization of the Koyck Model: TheAdaptive Expectations Model 629

17.6 Another Rationalization of the Koyck Model: The Stock Adjustment, or Partial Adjustment,Model 632

17.7 Combination of Adaptive Expectationsand Partial Adjustment Models 634

17.8 Estimation of Autoregressive Models 63417.9 The Method of Instrumental

Variables (IV) 63617.10 Detecting Autocorrelation in Autoregressive

Models: Durbin h Test 63717.11 A Numerical Example: The Demand for

Money in Canada, 1979–I to 1988–IV 63917.12 Illustrative Examples 64217.13 The Almon Approach to Distributed-Lag

Models: The Almon or Polynomial DistributedLag (PDL) 645

17.14 Causality in Economics: The GrangerCausality Test 652

The Granger Test 653A Note on Causality and Exogeneity 657

Summary and Conclusions 658Exercises 659Appendix 17A 669

17A.1 The Sargan Test for the Validity of Instruments 669

PART FOURSIMULTANEOUS-EQUATION MODELS AND TIME SERIESECONOMETRICS 671

CHAPTER 18Simultaneous-Equation Models 673

18.1 The Nature of Simultaneous-Equation Models 673

18.2 Examples of Simultaneous-Equation Models 674

18.3 The Simultaneous-Equation Bias:Inconsistency of OLS Estimators 679

guj75772_fm.qxd 09/09/2008 12:15 PM Page xii

Contents xiii

18.4 The Simultaneous-Equation Bias: A NumericalExample 682Summary and Conclusions 684Exercises 684

CHAPTER 19The Identification Problem 689

19.1 Notations and Definitions 68919.2 The Identification Problem 692

Underidentification 692Just, or Exact, Identification 694Overidentification 697

19.3 Rules for Identification 699The Order Condition of Identifiability 699The Rank Condition of Identifiability 700

19.4 A Test of Simultaneity 703Hausman Specification Test 703

19.5 Tests for Exogeneity 705Summary and Conclusions 706Exercises 706

CHAPTER 20Simultaneous-Equation Methods 711

20.1 Approaches to Estimation 71120.2 Recursive Models and Ordinary

Least Squares 71220.3 Estimation of a Just Identified Equation: The

Method of Indirect Least Squares (ILS) 715An Illustrative Example 715Properties of ILS Estimators 718

20.4 Estimation of an Overidentified Equation: The Method of Two-Stage Least Squares(2SLS) 718

20.5 2SLS: A Numerical Example 72120.6 Illustrative Examples 724

Summary and Conclusions 730Exercises 730Appendix 20A 735

20A.1 Bias in the Indirect Least-Squares Estimators 735

20A.2 Estimation of Standard Errors of 2SLSEstimators 736

CHAPTER 21 Time Series Econometrics:Some Basic Concepts 737

21.1 A Look at Selected U.S. Economic TimeSeries 738

21.2 Key Concepts 73921.3 Stochastic Processes 740

Stationary Stochastic Processes 740Nonstationary Stochastic Processes 741

21.4 Unit Root Stochastic Process 74421.5 Trend Stationary (TS) and Difference

Stationary (DS) Stochastic Processes 74521.6 Integrated Stochastic Processes 746

Properties of Integrated Series 74721.7 The Phenomenon of Spurious

Regression 74721.8 Tests of Stationarity 748

1. Graphical Analysis 7492. Autocorrelation Function (ACF)

and Correlogram 749Statistical Significance of AutocorrelationCoefficients 753

21.9 The Unit Root Test 754The Augmented Dickey–Fuller (ADF) Test 757Testing the Significance of More than OneCoefficient: The F Test 758The Phillips–Perron (PP) Unit Root Tests 758Testing for Structural Changes 758A Critique of the Unit Root Tests 759

21.10 Transforming Nonstationary Time Series 760Difference-Stationary Processes 760Trend-Stationary Processes 761

21.11 Cointegration: Regression of a Unit Root Time Series on Another Unit Root Time Series 762

Testing for Cointegration 763Cointegration and Error Correction Mechanism (ECM) 764

21.12 Some Economic Applications 765Summary and Conclusions 768Exercises 769

CHAPTER 22 Time Series Econometrics:Forecasting 773

22.1 Approaches to Economic Forecasting 773Exponential Smoothing Methods 774Single-Equation Regression Models 774Simultaneous-Equation Regression Models 774ARIMA Models 774VAR Models 775

guj75772_fm.qxd 05/09/2008 11:15 AM Page xiii

xiv Contents

22.2 AR, MA, and ARIMA Modeling of TimeSeries Data 775

An Autoregressive (AR) Process 775A Moving Average (MA) Process 776An Autoregressive and Moving Average (ARMA)Process 776An Autoregressive Integrated Moving Average (ARIMA) Process 776

22.3 The Box–Jenkins (BJ) Methodology 77722.4 Identification 77822.5 Estimation of the ARIMA Model 78222.6 Diagnostic Checking 78222.7 Forecasting 78222.8 Further Aspects of the BJ Methodology 78422.9 Vector Autoregression (VAR) 784

Estimation or VAR 785Forecasting with VAR 786VAR and Causality 787Some Problems with VAR Modeling 788An Application of VAR: A VAR Model of the TexasEconomy 789

22.10 Measuring Volatility in Financial Time Series: The ARCH and GARCH Models 791

What to Do If ARCH Is Present 795A Word on the Durbin–Watson d and the ARCHEffect 796A Note on the GARCH Model 796

22.11 Concluding Examples 796Summary and Conclusions 798Exercises 799

APPENDIX AA Review of Some Statistical Concepts 801

A.1 Summation and Product Operators 801A.2 Sample Space, Sample Points,

and Events 802A.3 Probability and Random Variables 802

Probability 802Random Variables 803

A.4 Probability Density Function (PDF) 803Probability Density Function of a DiscreteRandom Variable 803Probability Density Function of a ContinuousRandom Variable 804Joint Probability Density Functions 805Marginal Probability Density Function 805Statistical Independence 806

A.5 Characteristics of Probability Distributions 808

Expected Value 808Properties of Expected Values 809Variance 810Properties of Variance 811Covariance 811Properties of Covariance 812Correlation Coefficient 812Conditional Expectation and ConditionalVariance 813Properties of Conditional Expectationand Conditional Variance 814Higher Moments of Probability Distributions 815

A.6 Some Important Theoretical ProbabilityDistributions 816

Normal Distribution 816The χ2 (Chi-Square) Distribution 819Student’s t Distribution 820The F Distribution 821The Bernoulli Binomial Distribution 822Binomial Distribution 822The Poisson Distribution 823

A.7 Statistical Inference: Estimation 823Point Estimation 823Interval Estimation 824Methods of Estimation 825Small-Sample Properties 826Large-Sample Properties 828

A.8 Statistical Inference: Hypothesis Testing 831The Confidence Interval Approach 832The Test of Significance Approach 836

References 837

APPENDIX BRudiments of Matrix Algebra 838

B.1 Definitions 838Matrix 838Column Vector 838Row Vector 839Transposition 839Submatrix 839

B.2 Types of Matrices 839Square Matrix 839Diagonal Matrix 839Scalar Matrix 840Identity, or Unit, Matrix 840Symmetric Matrix 840Null Matrix 840Null Vector 840Equal Matrices 840

guj75772_fm.qxd 05/09/2008 11:15 AM Page xiv

Contents xv

B.3 Matrix Operations 840Matrix Addition 840Matrix Subtraction 841Scalar Multiplication 841Matrix Multiplication 841Properties of Matrix Multiplication 842Matrix Transposition 843Matrix Inversion 843

B.4 Determinants 843Evaluation of a Determinant 844Properties of Determinants 844Rank of a Matrix 845Minor 846Cofactor 846

B.5 Finding the Inverse of a Square Matrix 847B.6 Matrix Differentiation 848

References 848

APPENDIX CThe Matrix Approach to Linear RegressionModel 849

C.1 The k-Variable Linear Regression Model 849

C.2 Assumptions of the Classical LinearRegression Model in Matrix Notation 851

C.3 OLS Estimation 853An Illustration 855Variance-Covariance Matrix of β 856Properties of OLS Vector β 858

C.4 The Coefficient of Determination R2 in MatrixNotation 858

C.5 The Correlation Matrix 859C.6 Hypothesis Testing about Individual

Regression Coefficients in Matrix Notation 859

C.7 Testing the Overall Significance of Regression: Analysis of Variance in MatrixNotation 860

C.8 Testing Linear Restrictions: General F Testing Using Matrix Notation 861

C.9 Prediction Using Multiple Regression: MatrixFormulation 861

Mean Prediction 861Variance of Mean Prediction 862Individual Prediction 862Variance of Individual Prediction 862

C.10 Summary of the Matrix Approach: AnIllustrative Example 863

C.11 Generalized Least Squares (GLS) 867C.12 Summary and Conclusions 868

Exercises 869Appendix CA 874

CA.1 Derivation of k Normal or SimultaneousEquations 874

CA.2 Matrix Derivation of Normal Equations 875CA.3 Variance–Covariance Matrix of � 875CA.4 BLUE Property of OLS Estimators 875

APPENDIX DStatistical Tables 877

APPENDIX EComputer Output of EViews, MINITAB,Excel, and STATA 894

E.1 EViews 894E.2 MINITAB 896E.3 Excel 897E.4 STATA 898E.5 Concluding Comments 898

References 899

APPENDIX FEconomic Data on the World Wide Web 900

Selected Bibliography 902

Name Index 905

Subject Index 909

guj75772_fm.qxd 05/09/2008 11:15 AM Page xv

PrefaceObjective of the Book

The first edition of Basic Econometrics was published thirty years ago. Over the years,there have been important developments in the theory and practice of econometrics. Ineach of the subsequent editions, I have tried to incorporate the major developments in thefield. The fifth edition continues that tradition.

What has not changed, however, over all these years is my firm belief that econometricscan be taught to the beginner in an intuitive and informative way without resorting tomatrix algebra, calculus, or statistics beyond the introductory level. Some subject materialis inherently technical. In that case I have put the material in the appropriate appendix orrefer the reader to the appropriate sources. Even then, I have tried to simplify the technicalmaterial so that the reader can get an intuitive understanding of this material.

I am pleasantly surprised not only by the longevity of this book but also by the fact thatthe book is widely used not only by students of economics and finance but also by studentsand researchers in the fields of politics, international relations, agriculture, and healthsciences. All these students will find the new edition with its expanded topics and concreteapplications very useful. In this edition I have paid even more attention to the relevance andtimeliness of the real data used in the text. In fact, I have added about fifteen new illustra-tive examples and more than thirty new end-of-chapter exercises. Also, I have updatedthe data for about two dozen of the previous edition’s examples and more than twentyexercises.

Although I am in the eighth decade of my life, I have not lost my love for econometrics,and I strive to keep up with the major developments in the field. To assist me in thisendeavor, I am now happy to have Dr. Dawn Porter, Assistant Professor of Statistics at theMarshall School of Business at the University of Southern California in Los Angeles, asmy co-author. Both of us have been deeply involved in bringing the fifth edition of BasicEconometrics to fruition.

Major Features of the Fifth Edition

Before discussing the specific changes in the various chapters, the following features of thenew edition are worth noting:

1. Practically all of the data used in the illustrative examples have been updated.

2. Several new examples have been added.

3. In several chapters, we have included extended concluding examples that illustrate thevarious points made in the text.

4. Concrete computer printouts of several examples are included in the book. Most of theseresults are based on EViews (version 6) and STATA (version 10), as well as MINITAB(version 15).

5. Several new diagrams and graphs are included in various chapters.

6. Several new data-based exercises are included in the various chapters.

7. Small-sized data are included in the book, but large sample data are posted on the book’swebsite, thereby minimizing the size of the text. The website will also publish all of thedata used in the book and will be periodically updated.

xvi

guj75772_fm.qxd 05/09/2008 11:15 AM Page xvi

Preface xvii

8. In a few chapters, we have included class exercises in which students are encouraged toobtain their own data and implement the various techniques discussed in the book. SomeMonte Carlo simulations are also included in the book.

Specific Changes to the Fifth Edition

Some chapter-specific changes are as follows:

1. The assumptions underlying the classical linear regression model (CLRM) introducedin Chapter 3 now make a careful distinction between fixed regressors (explanatoryvariables) and random regressors. We discuss the importance of the distinction.

2. The appendix to Chapter 6 discusses the properties of logarithms, the Box-Cox trans-formations, and various growth formulas.

3. Chapter 7 now discusses not only the marginal impact of a single regressor on thedependent variable but also the impacts of simultaneous changes of all the explanatoryvariables on the dependent variable. This chapter has also been reorganized in the samestructure as the assumptions from Chapter 3.

4. A comparison of the various tests of heteroscedasticity is given in Chapter 11.

5. There is a new discussion of the impact of structural breaks on autocorrelation inChapter 12.

6. New topics included in Chapter 13 are missing data, non-normal error term, andstochastic, or random, regressors.

7. A non-linear regression model discussed in Chapter 14 has a concrete application ofthe Box-Cox transformation.

8. Chapter 15 contains several new examples that illustrate the use of logit and probitmodels in various fields.

9. Chapter 16 on panel data regression models has been thoroughly revised and illus-trated with several applications.

10. An extended discussion of Sims and Granger causality tests is now included in Chap-ter 17.

11. Stationary and non-stationary time series, as well as some of the problems associatedwith various tests of stationarity, are now thoroughly discussed in Chapter 21.

12. Chapter 22 includes a discussion on why taking the first differences of a time seriesfor the purpose of making it stationary may not be the appropriate strategy in somesituations.

Besides these specific changes, errors and misprints in the previous editions have been cor-rected and the discussions of several topics in the various chapters have been streamlined.

Organization and Options

The extensive coverage in this edition gives the instructor substantial flexibility in choos-ing topics that are appropriate to the intended audience. Here are suggestions about howthis book may be used.

One-semester course for the nonspecialist: Appendix A, Chapters 1 through 9, anoverview of Chapters 10, 11, 12 (omitting all the proofs).

One-semester course for economics majors: Appendix A, Chapters 1 through 13.

guj75772_fm.qxd 05/09/2008 11:15 AM Page xvii

xviii Preface

Two-semester course for economics majors: Appendices A, B, C, Chapters 1 to 22.Chapters 14 and 16 may be covered on an optional basis. Some of the technical appen-dices may be omitted.

Graduate and postgraduate students and researchers: This book is a handy refer-ence book on the major themes in econometrics.

Supplements

A comprehensive website contains the following supplementary material:

–Data from the text, as well as additional large set data referenced in the book; the datawill be periodically updated by the authors.

–A Solutions Manual, written by Dawn Porter, providing answers to all of thequestions and problems throughout the text.

–A digital image library containing all of the graphs and figures from the text.

For more information, please go to www.mhhe.com/gujarati5e

guj75772_fm.qxd 05/09/2008 11:15 AM Page xviii

AcknowledgmentsSince the publication of the first edition of this book in 1978, we have received valuableadvice, comments, criticism, and suggestions from a variety of people. In particular, wewould like to acknowledge the help we have received from Michael McAleer of theUniversity of Western Australia, Peter Kennedy of Simon Frazer University in Canada,Kenneth White, of the University of British Columbia, George K. Zestos, of ChristopherNewport University, Virginia, and Paul Offner, of Georgetown University, Washington, D.C.

We are also grateful to several people who have influenced us by their scholarship. Weespecially want to thank Arthur Goldberger of the University of Wisconsin, WilliamGreene of New York University, and the late G. S. Maddala. We continue to be grateful tothe following reviewers who provided valuable insight, criticism, and suggestions forprevious editions of this text: Michael A. Grove at the University of Oregon, Harumi Itoat Brown University, Han Kim at South Dakota University, Phanindra V. Wunnava atMiddlebury College, and Andrew Paizis of the City University of New York.

Several authors have influenced the writing of this text. In particular, we are grateful tothese authors: Chandan Mukherjee, director of the Centre for Development Studies,Trivandrum, India; Howard White and Marc Wuyts, both at the Institute of Social Studiesin the Netherlands; Badi H. Baltagi, Texas A&M University; B. Bhaskara Rao, Universityof New South Wales, Australia; R. Carter Hill, Louisiana University; William E. Griffiths,University of New England; George G. Judge, University of California at Berkeley; MarnoVerbeek, Center for Economic Studies, KU Leuven; Jeffrey Wooldridge, Michigan StateUniversity; Kerry Patterson, University of Reading, U.K.; Francis X. Diebold, WhartonSchool, University of Pennsylvania; Wojciech W. Charemza and Derek F. Deadman, both ofthe University of Leicester, U.K.; and Gary Koop, University of Glasgow.

A number of very valuable comments and suggestions given by reviewers of the fourthedition have greatly improved this edition. We would like to thank the following:

xix

Valerie BencivengaUniversity of Texas–Austin

Andrew EconomopoulosUrsinus College

Eric EideBrigham Young University

Gary FerrierUniversity of Arkansas–Fayetteville

David GarmanTufts University

David HarrisBenedictine College

Don HolleyBoise State University

George JakubsonCornell University

Bruce JohnsonCentre College of Kentucky

Duke KaoSyracuse University

Gary KruegerMacalester College

Subal KumbhakarBinghamton University

Tae-Hwy LeeUniversity of California–Riverside

Solaiman MiahWest Virginia State University

Fabio MilaniUniversity of California–Irvine

Helen NaughtonUniversity of Oregon

Solomon SmithLangston University

Kay StrongBowling Green State University

Derek TittleGeorgia Institute of Technology

Tiemen WoutersenJohns Hopkins University

guj75772_fm.qxd 05/09/2008 11:15 AM Page xix

xx Acknowledgments

We would like to thank students and teachers all over the world who have not only usedthis book but have communicated with us about various aspects of the book.

For their behind-the-scenes help at McGraw-Hill, we are grateful to Douglas Reiner,Noelle Fox, and Anne Hilbert.

Finally, but not least important, Dr. Gujarati would like to thank his daughters, Joan andDiane, for their constant support and encouragement in the preparation of this and the pre-vious editions.

Damodar N. GujaratiDawn C. Porter

guj75772_fm.qxd 05/09/2008 11:15 AM Page xx

1

I.1 What Is Econometrics?

Literally interpreted, econometrics means “economic measurement.” Although measure-ment is an important part of econometrics, the scope of econometrics is much broader, ascan be seen from the following quotations:

Econometrics, the result of a certain outlook on the role of economics, consists of the applica-tion of mathematical statistics to economic data to lend empirical support to the modelsconstructed by mathematical economics and to obtain numerical results.1

. . . econometrics may be defined as the quantitative analysis of actual economic phenomenabased on the concurrent development of theory and observation, related by appropriatemethods of inference.2

Econometrics may be defined as the social science in which the tools of economic theory,mathematics, and statistical inference are applied to the analysis of economic phenomena.3

Econometrics is concerned with the empirical determination of economic laws.4

The art of the econometrician consists in finding the set of assumptions that are both suffi-ciently specific and sufficiently realistic to allow him to take the best possible advantage of thedata available to him.5

Econometricians . . . are a positive help in trying to dispel the poor public image of economics(quantitative or otherwise) as a subject in which empty boxes are opened by assuming theexistence of can-openers to reveal contents which any ten economists will interpret in11 ways.6

The method of econometric research aims, essentially, at a conjunction of economic theoryand actual measurements, using the theory and technique of statistical inference as a bridgepier.7

1Gerhard Tintner, Methodology of Mathematical Economics and Econometrics, The University of ChicagoPress, Chicago, 1968, p. 74.2P. A. Samuelson, T. C. Koopmans, and J. R. N. Stone, “Report of the Evaluative Committee for Econo-metrica,” Econometrica, vol. 22, no. 2, April 1954, pp. 141–146.3Arthur S. Goldberger, Econometric Theory, John Wiley & Sons, New York, 1964, p. 1.4H. Theil, Principles of Econometrics, John Wiley & Sons, New York, 1971, p. 1.5E. Malinvaud, Statistical Methods of Econometrics, Rand McNally, Chicago, 1966, p. 514.6Adrian C. Darnell and J. Lynne Evans, The Limits of Econometrics, Edward Elgar Publishing, Hants,England, 1990, p. 54.7T. Haavelmo, “The Probability Approach in Econometrics,” Supplement to Econometrica, vol. 12,1944, preface p. iii.

Introduction

guj75772_intro.qxd 23/08/2008 10:29 AM Page 1

2 Basic Econometrics

I.2 Why a Separate Discipline?

As the preceding definitions suggest, econometrics is an amalgam of economic theory,mathematical economics, economic statistics, and mathematical statistics. Yet the subjectdeserves to be studied in its own right for the following reasons.

Economic theory makes statements or hypotheses that are mostly qualitative in nature.For example, microeconomic theory states that, other things remaining the same, a reduc-tion in the price of a commodity is expected to increase the quantity demanded of that com-modity. Thus, economic theory postulates a negative or inverse relationship between theprice and quantity demanded of a commodity. But the theory itself does not provide anynumerical measure of the relationship between the two; that is, it does not tell by how muchthe quantity will go up or down as a result of a certain change in the price of the commod-ity. It is the job of the econometrician to provide such numerical estimates. Stated differ-ently, econometrics gives empirical content to most economic theory.

The main concern of mathematical economics is to express economic theory in mathe-matical form (equations) without regard to measurability or empirical verification of thetheory. Econometrics, as noted previously, is mainly interested in the empirical verificationof economic theory. As we shall see, the econometrician often uses the mathematicalequations proposed by the mathematical economist but puts these equations in such a formthat they lend themselves to empirical testing. And this conversion of mathematical intoeconometric equations requires a great deal of ingenuity and practical skill.

Economic statistics is mainly concerned with collecting, processing, and presentingeconomic data in the form of charts and tables. These are the jobs of the economic statisti-cian. It is he or she who is primarily responsible for collecting data on gross nationalproduct (GNP), employment, unemployment, prices, and so on. The data thus collectedconstitute the raw data for econometric work. But the economic statistician does not go anyfurther, not being concerned with using the collected data to test economic theories. Ofcourse, one who does that becomes an econometrician.

Although mathematical statistics provides many tools used in the trade, the econometri-cian often needs special methods in view of the unique nature of most economic data,namely, that the data are not generated as the result of a controlled experiment. The econo-metrician, like the meteorologist, generally depends on data that cannot be controlleddirectly. As Spanos correctly observes:

In econometrics the modeler is often faced with observational as opposed to experimentaldata. This has two important implications for empirical modeling in econometrics. First, themodeler is required to master very different skills than those needed for analyzing experimen-tal data. . . . Second, the separation of the data collector and the data analyst requires the mod-eler to familiarize himself/herself thoroughly with the nature and structure of data in question.8

I.3 Methodology of Econometrics

How do econometricians proceed in their analysis of an economic problem? That is, whatis their methodology? Although there are several schools of thought on econometricmethodology, we present here the traditional or classical methodology, which still domi-nates empirical research in economics and other social and behavioral sciences.9

8Aris Spanos, Probability Theory and Statistical Inference: Econometric Modeling with Observational Data,Cambridge University Press, United Kingdom, 1999, p. 21.9For an enlightening, if advanced, discussion on econometric methodology, see David F. Hendry,Dynamic Econometrics, Oxford University Press, New York, 1995. See also Aris Spanos, op. cit.

guj75772_intro.qxd 23/08/2008 10:29 AM Page 2

Introduction 3

Broadly speaking, traditional econometric methodology proceeds along the followinglines:

1. Statement of theory or hypothesis.

2. Specification of the mathematical model of the theory.

3. Specification of the statistical, or econometric, model.

4. Obtaining the data.

5. Estimation of the parameters of the econometric model.

6. Hypothesis testing.

7. Forecasting or prediction.

8. Using the model for control or policy purposes.

To illustrate the preceding steps, let us consider the well-known Keynesian theory ofconsumption.

1. Statement of Theory or HypothesisKeynes stated:

The fundamental psychological law . . . is that men [women] are disposed, as a rule and onaverage, to increase their consumption as their income increases, but not as much as theincrease in their income.10

In short, Keynes postulated that the marginal propensity to consume (MPC), the rate ofchange of consumption for a unit (say, a dollar) change in income, is greater than zero butless than 1.

2. Specification of the Mathematical Model of ConsumptionAlthough Keynes postulated a positive relationship between consumption and income,he did not specify the precise form of the functional relationship between the two. Forsimplicity, a mathematical economist might suggest the following form of the Keynesianconsumption function:

Y = β1 + β2 X 0 < β2 < 1 (I.3.1)

where Y = consumption expenditure and X = income, and where β1 and β2, known as theparameters of the model, are, respectively, the intercept and slope coefficients.

The slope coefficient β2 measures the MPC. Geometrically, Equation I.3.1 is as shownin Figure I.1. This equation, which states that consumption is linearly related to income, isan example of a mathematical model of the relationship between consumption and incomethat is called the consumption function in economics. A model is simply a set of mathe-matical equations. If the model has only one equation, as in the preceding example, it iscalled a single-equation model, whereas if it has more than one equation, it is known as amultiple-equation model (the latter will be considered later in the book).

In Eq. (I.3.1) the variable appearing on the left side of the equality sign is called thedependent variable and the variable(s) on the right side is called the independent, orexplanatory, variable(s). Thus, in the Keynesian consumption function, Eq. (I.3.1), con-sumption (expenditure) is the dependent variable and income is the explanatory variable.

10John Maynard Keynes, The General Theory of Employment, Interest and Money, Harcourt BraceJovanovich, New York, 1936, p. 96.

guj75772_intro.qxd 23/08/2008 10:29 AM Page 3

4 Basic Econometrics

3. Specification of the Econometric Modelof Consumption

The purely mathematical model of the consumption function given in Eq. (I.3.1) is of lim-ited interest to the econometrician, for it assumes that there is an exact or deterministicrelationship between consumption and income. But relationships between economic vari-ables are generally inexact. Thus, if we were to obtain data on consumption expenditure anddisposable (i.e., aftertax) income of a sample of, say, 500 American families and plot thesedata on a graph paper with consumption expenditure on the vertical axis and disposable in-come on the horizontal axis, we would not expect all 500 observations to lie exactly on thestraight line of Eq. (I.3.1) because, in addition to income, other variables affect consump-tion expenditure. For example, size of family, ages of the members in the family, familyreligion, etc., are likely to exert some influence on consumption.

To allow for the inexact relationships between economic variables, the econometricianwould modify the deterministic consumption function in Eq. (I.3.1) as follows:

Y = β1 + β2 X + u (I.3.2)

where u, known as the disturbance, or error, term, is a random (stochastic) variable thathas well-defined probabilistic properties. The disturbance term u may well represent allthose factors that affect consumption but are not taken into account explicitly.

Equation I.3.2 is an example of an econometric model. More technically, it is an exam-ple of a linear regression model, which is the major concern of this book. The economet-ric consumption function hypothesizes that the dependent variable Y (consumption) islinearly related to the explanatory variable X (income) but that the relationship between thetwo is not exact; it is subject to individual variation.

The econometric model of the consumption function can be depicted as shown inFigure I.2.

FIGURE I.1Keynesian consumption function.

Con

sum

pti

on e

xpen

dit

ure

XIncome

1

2 = MPCβ

1β

Y

guj75772_intro.qxd 23/08/2008 10:29 AM Page 4

Introduction 5

FIGURE I.2Econometric modelof the Keynesianconsumption function.

Con

sum

pti

on e

xpen

dit

ure

X

Y

Income

u

4. Obtaining DataTo estimate the econometric model given in Eq. (I.3.2), that is, to obtain the numericalvalues of β1 and β2, we need data. Although we will have more to say about the crucialimportance of data for economic analysis in the next chapter, for now let us look at thedata given in Table I.1, which relate to the U.S. economy for the period 1960–2005. TheY variable in this table is the aggregate (for the economy as a whole) personal consumptionexpenditure (PCE) and the X variable is gross domestic product (GDP), a measure ofaggregate income, both measured in billions of 2000 dollars. Therefore, the data are in“real” terms; that is, they are measured in constant (2000) prices. The data are plottedin Figure I.3 (cf. Figure I.2). For the time being neglect the line drawn in the figure.

5. Estimation of the Econometric ModelNow that we have the data, our next task is to estimate the parameters of the consumptionfunction. The numerical estimates of the parameters give empirical content to the con-sumption function. The actual mechanics of estimating the parameters will be discussed inChapter 3. For now, note that the statistical technique of regression analysis is the maintool used to obtain the estimates. Using this technique and the data given in Table I.1, weobtain the following estimates of β1 and β2, namely, −299.5913 and 0.7218. Thus, theestimated consumption function is:

Yt = −299.5913 + 0.7218Xt (I.3.3)

The hat on the Y indicates that it is an estimate.11 The estimated consumption function (i.e.,regression line) is shown in Figure I.3.

11As a matter of convention, a hat over a variable or parameter indicates that it is an estimated value.

guj75772_intro.qxd 23/08/2008 10:29 AM Page 5

6 Basic Econometrics

Year PCE(Y) GDP(X)

1960 1597.4 2501.81961 1630.3 2560.01962 1711.1 2715.21963 1781.6 2834.01964 1888.4 2998.61965 2007.7 3191.11966 2121.8 3399.11967 2185.0 3484.61968 2310.5 3652.71969 2396.4 3765.41970 2451.9 3771.91971 2545.5 3898.61972 2701.3 4105.01973 2833.8 4341.51974 2812.3 4319.61975 2876.9 4311.21976 3035.5 4540.91977 3164.1 4750.51978 3303.1 5015.01979 3383.4 5173.41980 3374.1 5161.71981 3422.2 5291.71982 3470.3 5189.31983 3668.6 5423.81984 3863.3 5813.61985 4064.0 6053.71986 4228.9 6263.61987 4369.8 6475.11988 4546.9 6742.71989 4675.0 6981.41990 4770.3 7112.51991 4778.4 7100.51992 4934.8 7336.61993 5099.8 7532.71994 5290.7 7835.51995 5433.5 8031.71996 5619.4 8328.91997 5831.8 8703.51998 6125.8 9066.91999 6438.6 9470.32000 6739.4 9817.02001 6910.4 9890.72002 7099.3 10048.82003 7295.3 10301.02004 7577.1 10703.52005 7841.2 11048.6

TABLE I.1Data on Y (PersonalConsumptionExpenditure) andX (Gross DomesticProduct, 1960–2005),both in 2000 Billionsof Dollars

Source: Economic Report ofthe President, 2007, Table B–2,p. 230.

guj75772_intro.qxd 23/08/2008 10:29 AM Page 6

Introduction 7

As Figure I.3 shows, the regression line fits the data quite well in that the data points arevery close to the regression line. From this figure we see that for the period 1960–2005 theslope coefficient (i.e., the MPC) was about 0.72, suggesting that for the sample period anincrease in real income of one dollar led, on average, to an increase of about 72 cents in realconsumption expenditure.12 We say on average because the relationship between con-sumption and income is inexact; as is clear from Figure I.3, not all the data points lieexactly on the regression line. In simple terms we can say that, according to our data, theaverage, or mean, consumption expenditure went up by about 72 cents for a dollar’sincrease in real income.

6. Hypothesis TestingAssuming that the fitted model is a reasonably good approximation of reality, we have todevelop suitable criteria to find out whether the estimates obtained in, say, Equation I.3.3are in accord with the expectations of the theory that is being tested. According to “posi-tive” economists like Milton Friedman, a theory or hypothesis that is not verifiable byappeal to empirical evidence may not be admissible as a part of scientific enquiry.13

As noted earlier, Keynes expected the MPC to be positive but less than 1. In our exam-ple we found the MPC to be about 0.72. But before we accept this finding as confirmationof Keynesian consumption theory, we must enquire whether this estimate is sufficiently

12,00010,000800060004000

GDP (X)

20001000

2000

3000

4000P

CE

(Y

)

8000

7000

6000

5000

FIGURE I.3Personal consumptionexpenditure (Y ) inrelation to GDP (X),1960–2005, in billionsof 2000 dollars.

12Do not worry now about how these values were obtained. As we show in Chapter 3, the statisticalmethod of least squares has produced these estimates. Also, for now do not worry about thenegative value of the intercept.13See Milton Friedman, “The Methodology of Positive Economics,” Essays in Positive Economics,University of Chicago Press, Chicago, 1953.

guj75772_intro.qxd 23/08/2008 10:29 AM Page 7

8 Basic Econometrics

below unity to convince us that this is not a chance occurrence or peculiarity of the partic-ular data we have used. In other words, is 0.72 statistically less than 1? If it is, it may sup-port Keynes’s theory.

Such confirmation or refutation of economic theories on the basis of sample evidence isbased on a branch of statistical theory known as statistical inference (hypothesis testing).Throughout this book we shall see how this inference process is actually conducted.

7. Forecasting or PredictionIf the chosen model does not refute the hypothesis or theory under consideration, we mayuse it to predict the future value(s) of the dependent, or forecast, variable Y on the basis ofthe known or expected future value(s) of the explanatory, or predictor, variable X.

To illustrate, suppose we want to predict the mean consumption expenditure for 2006.The GDP value for 2006 was 11319.4 billion dollars.14 Putting this GDP figure on theright-hand side of Eq. (I.3.3), we obtain:

Y2006 = −299.5913 + 0.7218 (11319.4)

= 7870.7516(I.3.4)

or about 7870 billion dollars. Thus, given the value of the GDP, the mean, or average, fore-cast consumption expenditure is about 7870 billion dollars. The actual value of the con-sumption expenditure reported in 2006 was 8044 billion dollars. The estimated modelEq. (I.3.3) thus underpredicted the actual consumption expenditure by about 174 billiondollars. We could say the forecast error is about 174 billion dollars, which is about1.5 percent of the actual GDP value for 2006. When we fully discuss the linear regressionmodel in subsequent chapters, we will try to find out if such an error is “small” or “large.”But what is important for now is to note that such forecast errors are inevitable given thestatistical nature of our analysis.

There is another use of the estimated model Eq. (I.3.3). Suppose the president decidesto propose a reduction in the income tax. What will be the effect of such a policy on incomeand thereby on consumption expenditure and ultimately on employment?

Suppose that, as a result of the proposed policy change, investment expenditure in-creases. What will be the effect on the economy? As macroeconomic theory shows, thechange in income following, say, a dollar’s worth of change in investment expenditure isgiven by the income multiplier M, which is defined as

M = 1

1 − MPC(I.3.5)

If we use the MPC of 0.72 obtained in Eq. (I.3.3), this multiplier becomes about M = 3.57.

That is, an increase (decrease) of a dollar in investment will eventually lead to more than athreefold increase (decrease) in income; note that it takes time for the multiplier to work.

The critical value in this computation is MPC, for the multiplier depends on it. And thisestimate of the MPC can be obtained from regression models such as Eq. (I.3.3). Thus, aquantitative estimate of MPC provides valuable information for policy purposes. KnowingMPC, one can predict the future course of income, consumption expenditure, and employ-ment following a change in the government’s fiscal policies.

14Data on PCE and GDP were available for 2006 but we purposely left them out to illustrate the topicdiscussed in this section. As we will discuss in subsequent chapters, it is a good idea to save a portionof the data to find out how well the fitted model predicts the out-of-sample observations.

guj75772_intro.qxd 23/08/2008 10:29 AM Page 8

Introduction 9

8. Use of the Model for Control or Policy PurposesSuppose we have the estimated consumption function given in Eq. (I.3.3). Suppose furtherthe government believes that consumer expenditure of about 8750 (billions of 2000 dollars)will keep the unemployment rate at its current level of about 4.2 percent (early 2006). Whatlevel of income will guarantee the target amount of consumption expenditure?

If the regression results given in Eq. (I.3.3) seem reasonable, simple arithmetic willshow that

8750 = −299.5913 + 0.7218(GDP2006) (I.3.6)

which gives X = 12537, approximately. That is, an income level of about 12537 (billion)dollars, given an MPC of about 0.72, will produce an expenditure of about 8750 billiondollars.

As these calculations suggest, an estimated model may be used for control, or policy,purposes. By appropriate fiscal and monetary policy mix, the government can manipulatethe control variable X to produce the desired level of the target variable Y.

Figure I.4 summarizes the anatomy of classical econometric modeling.

Choosing among Competing ModelsWhen a governmental agency (e.g., the U.S. Department of Commerce) collects economicdata, such as that shown in Table I.1, it does not necessarily have any economic theory inmind. How then does one know that the data really support the Keynesian theory of con-sumption? Is it because the Keynesian consumption function (i.e., the regression line)shown in Figure I.3 is extremely close to the actual data points? Is it possible that anotherconsumption model (theory) might equally fit the data as well? For example, MiltonFriedman has developed a model of consumption, called the permanent income

Estimation of econometric model

Econometric model of theory

Economic theory

Data

Forecasting or prediction

Using the model forcontrol or policy purposes

Hypothesis testing

Mathematical model of theory

FIGURE I.4Anatomy ofeconometric modeling.

guj75772_intro.qxd 23/08/2008 10:29 AM Page 9

10 Basic Econometrics

hypothesis.15 Robert Hall has also developed a model of consumption, called the life-cyclepermanent income hypothesis.16 Could one or both of these models also fit the data inTable I.1?

In short, the question facing a researcher in practice is how to choose among competinghypotheses or models of a given phenomenon, such as the consumption–income relation-ship. As Miller contends:

No encounter with data is [a] step towards genuine confirmation unless the hypothesis does abetter job of coping with the data than some natural rival. . . . What strengthens a hypothesis,here, is a victory that is, at the same time, a defeat for a plausible rival.17

How then does one choose among competing models or hypotheses? Here the advice givenby Clive Granger is worth keeping in mind:18

I would like to suggest that in the future, when you are presented with a new piece of theory orempirical model, you ask these questions:

(i) What purpose does it have? What economic decisions does it help with?

(ii) Is there any evidence being presented that allows me to evaluate its quality compared toalternative theories or models?

I think attention to such questions will strengthen economic research and discussion.

As we progress through this book, we will come across several competing hypothesestrying to explain various economic phenomena. For example, students of economics arefamiliar with the concept of the production function, which is basically a relationshipbetween output and inputs (say, capital and labor). In the literature, two of the best knownare the Cobb–Douglas and the constant elasticity of substitution production functions.Given the data on output and inputs, we will have to find out which of the two productionfunctions, if any, fits the data well.

The eight-step classical econometric methodology discussed above is neutral in thesense that it can be used to test any of these rival hypotheses.

Is it possible to develop a methodology that is comprehensive enough to includecompeting hypotheses? This is an involved and controversial topic. We will discuss it inChapter 13, after we have acquired the necessary econometric theory.

I.4 Types of Econometrics

As the classificatory scheme in Figure I.5 suggests, econometrics may be divided into twobroad categories: theoretical econometrics and applied econometrics. In each category,one can approach the subject in the classical or Bayesian tradition. In this book theemphasis is on the classical approach. For the Bayesian approach, the reader may consultthe references given at the end of the chapter.

15Milton Friedman, A Theory of Consumption Function, Princeton University Press, Princeton, N.J.,1957.16R. Hall, “Stochastic Implications of the Life Cycle Permanent Income Hypothesis: Theory andEvidence,” Journal of Political Economy, vol. 86, 1978, pp. 971–987.17R. W. Miller, Fact and Method: Explanation, Confirmation, and Reality in the Natural and SocialSciences, Princeton University Press, Princeton, N.J., 1978, p. 176.18Clive W. J. Granger, Empirical Modeling in Economics, Cambridge University Press, U.K., 1999, p. 58.

guj75772_intro.qxd 23/08/2008 10:29 AM Page 10

Introduction 11

Theoretical econometrics is concerned with the development of appropriate methods formeasuring economic relationships specified by econometric models. In this aspect, econo-metrics leans heavily on mathematical statistics. For example, one of the methods usedextensively in this book is least squares. Theoretical econometrics must spell out theassumptions of this method, its properties, and what happens to these properties when oneor more of the assumptions of the method are not fulfilled.

In applied econometrics we use the tools of theoretical econometrics to study somespecial field(s) of economics and business, such as the production function, investmentfunction, demand and supply functions, portfolio theory, etc.

This book is concerned largely with the development of econometric methods, theirassumptions, their uses, and their limitations. These methods are illustrated with examplesfrom various areas of economics and business. But this is not a book of applied economet-rics in the sense that it delves deeply into any particular field of economic application. Thatjob is best left to books written specifically for this purpose. References to some of thesebooks are provided at the end of this book.

I.5 Mathematical and Statistical Prerequisites

Although this book is written at an elementary level, the author assumes that the reader isfamiliar with the basic concepts of statistical estimation and hypothesis testing. However, abroad but nontechnical overview of the basic statistical concepts used in this book is pro-vided in Appendix A for the benefit of those who want to refresh their knowledge. Insofaras mathematics is concerned, a nodding acquaintance with the notions of differentialcalculus is desirable, although not essential. Although most graduate level books in econo-metrics make heavy use of matrix algebra, I want to make it clear that it is not needed tostudy this book. It is my strong belief that the fundamental ideas of econometrics can beconveyed without the use of matrix algebra. However, for the benefit of the mathematicallyinclined student, Appendix C gives the summary of basic regression theory in matrixnotation. For these students, Appendix B provides a succinct summary of the main resultsfrom matrix algebra.

I.6 The Role of the Computer

Regression analysis, the bread-and-butter tool of econometrics, these days is unthinkablewithout the computer and some access to statistical software. (Believe me, I grew up in thegeneration of the slide rule!) Fortunately, several excellent regression packages are com-mercially available, both for the mainframe and the microcomputer, and the list is growingby the day. Regression software packages, such as ET, LIMDEP, SHAZAM, MICROTSP, MINITAB, EVIEWS, SAS, SPSS, STATA, Microfit, PcGive, and BMD have mostof the econometric techniques and tests discussed in this book.

Econometrics

Theoretical

Classical Bayesian

Applied

Classical Bayesian

FIGURE I.5Categories ofeconometrics.

guj75772_intro.qxd 23/08/2008 10:29 AM Page 11

12 Basic Econometrics