the malta alternative investment funds - ey€¦ · 2 | the malta alternative investment funds •...

TRANSCRIPT

The Malta AlternativeInvestment FundsA technical guideJune 2016

It is my great pleasure to welcome you to our 2016 edition of“The Malta Alternative Investment Funds – A technical guide.”

Alternative Investment Funds are fast becoming one of Malta’s primary investment fund vehicle for all types of professional and sophisticated investors, which funds are a direct product of the AIFM directive. This directive aims to establish commonrequirements for the authorization and supervision of AIFs. It alsoprovides a harmonized regulatory framework for the activities within the EU of all AIFs.

A benefit of AIFs is the availability of marketing passportingprovisions introduced by the AIFM directive which substitutes theexisting EU member state’s national private placement regimeswhen marketing AIFs to professional investors within the EU. This directive has adopted a “one size fits all” approach under which a single set of rules shall govern AIFs which are not covered by the UCITS directive.

The local industry continues to enjoy the commitments of the localgovernment as well as the Malta Financial Services Authority which strive to preserve a leading regulatory and legislative regime that is attractive to foreign business while maintaining investor protection. The implementation of the regulatory agenda continues unabated, with much focus and discussion on depositary reform, remunerationpolicies and practices, the future of money market funds, extension of the AIFM directive passport to non-EU domiciled products and managers, and the likely impact of MiFID II all being in the headlines.

The purpose of this practical guide is to provide, in a clear and concise format, an overview of the AIF regime and how it fits withinthe scope of the AIFM directive. I hope you find this guide useful.

Our asset management advisory team looks forward to your feedback and in supporting you over the coming years so that wemay collectively realize the many opportunities offered by thisindustry.

Ronald AttardCountry Managing PartnerErnst & Young Limited +356 2134 2134 [email protected]

Fore

wor

d

| The Malta Alternative Investment Funds

s0102030405060708091011121314

Forward

In this report

Professional Investor Funds

Requirements of a PIF

Setting up and running a PIF

Investment Restrictions

Key service providers

Authorisation

Salient features of PIFs

Distribution of PIF products

PIF structures

Fund information and reporting obligations

Admissibility for Listing

Taxation

How can we help you?

Glossary

01 Altrnative investment funds

02 Requirements of an AIF

03Investment restrictions04Key service providers05Internally managed AIFs06Authorization07

Salient features of AIFs08Marketing under the AIFM directive09AIF structures10Transparency and reporting obligations11Admissibility for listing12Depositary13Valuation under the AIFM directive14

Setting up and running an AIF

4

6

8

14

18

22

30

32

34

38

42

46

48

54

Taxation15 56

How can we help you?16 58

Glossary17 60

Annex18 63

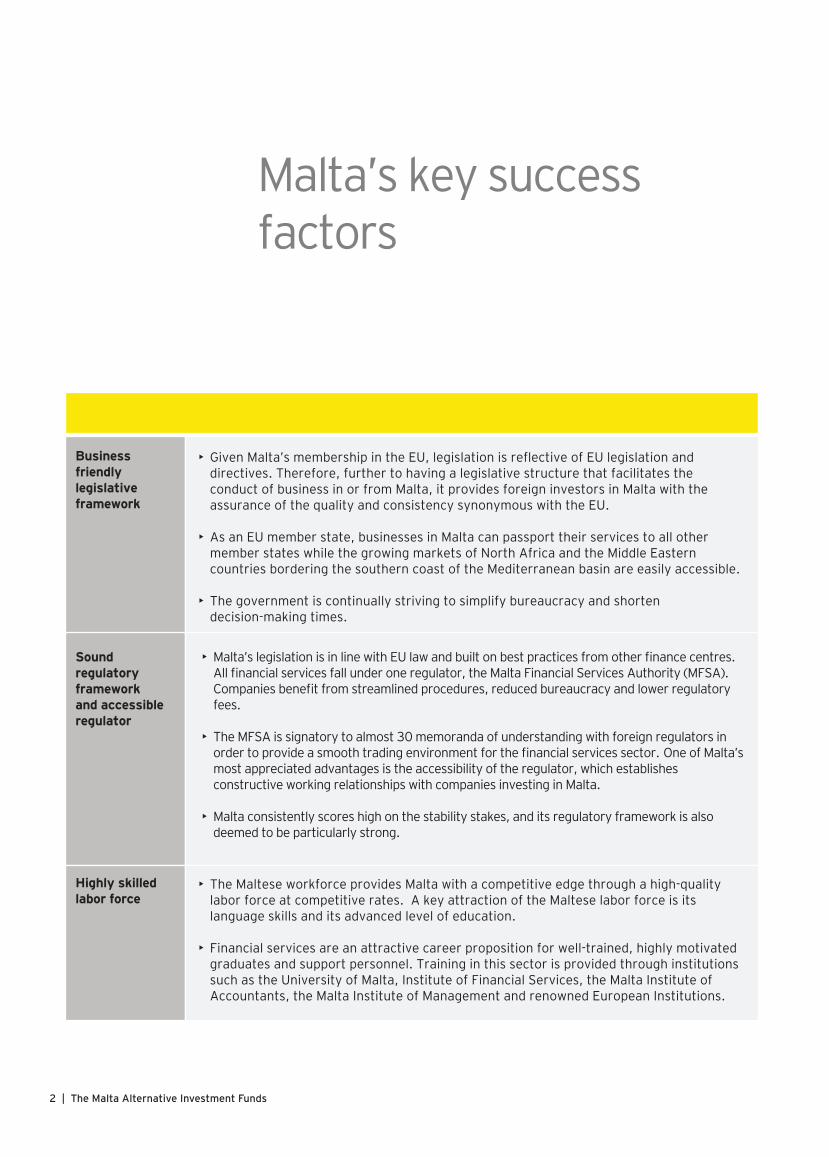

Malta’s key success factors 2

2 | The Malta Alternative Investment Funds

• The Maltese workforce provides Malta with a competitive edge through a high-quality labor force at competitive rates. A key attraction of the Maltese labor force is its language skills and its advanced level of education.

• Financial services are an attractive career proposition for well-trained, highly motivated graduates and support personnel. Training in this sector is provided through institutions such as the University of Malta, Institute of Financial Services, the Malta Institute of Accountants, the Malta Institute of Management and renowned European Institutions.

Highly skilledlabor force

• Given Malta’s membership in the EU, legislation is reflective of EU legislation and directives. Therefore, further to having a legislative structure that facilitates the conduct of business in or from Malta, it provides foreign investors in Malta with the assurance of the quality and consistency synonymous with the EU.

• As an EU member state, businesses in Malta can passport their services to all other member states while the growing markets of North Africa and the Middle Eastern countries bordering the southern coast of the Mediterranean basin are easily accessible.

• The government is continually striving to simplify bureaucracy and shorten decision-making times.

Businessfriendlylegislativeframework

Soundregulatoryframeworkand accessibleregulator

• Malta’s legislation is in line with EU law and built on best practices from other finance centres. All financial services fall under one regulator, the Malta Financial Services Authority (MFSA). Companies benefit from streamlined procedures, reduced bureaucracy and lower regulatory fees.

• The MFSA is signatory to almost 30 memoranda of understanding with foreign regulators in order to provide a smooth trading environment for the financial services sector. One of Malta’s most appreciated advantages is the accessibility of the regulator, which establishes constructive working relationships with companies investing in Malta.

• Malta consistently scores high on the stability stakes, and its regulatory framework is also deemed to be particularly strong.

Malta’s key successfactors

The Malta Alternative Investment Funds | 3

Small, activestock exchange

• Full member of International Organization of Securities Commissions (IOSCO) and the World Federation of Exchanges (WFE); following Malta’s accession to the EU, the Malta Stock Exchange, together with the exchanges of the other accession countries, was granted the status of full member of the Federation of European Securities Exchanges (FESE). Major sectors of the Maltese economy are represented on the lists of the Malta Stock Exchange.

• Since being set up in 1992, almost €3b worth of capital has been raised on the market for the private sector through the issue of corporate bonds and equity while a further €15b worth of government of Malta stocks and treasury bills have been issued and fully taken up. Investor base of over 75,000 individual investors, which is a significant number given Malta’s economic size and population. The focus of the Malta Stock Exchange is mostly domestic.

Cost competitiveenvironment

• Competitive labor costs, rental rates and general expenses compared to mainland Europe. Companies in Malta can benefit from an extensive network of double taxation treaties as well as from a number of business promotional incentives.

• Malta has excellent communication links with regular flights to main international airports as well as fully digitalized national telephone network. Malta boasts a truly modern infrastructure with one of the highest broadband access rates in the EU.

• International connectivity is ensured by two satellite stations and four submarine fiber-optic links to mainland Europe. A wide range of quality office and industrial space with commercial office space in purposely built developments or stand-alone blocks readily available at affordable prices.

Infrastructure

4 | The Malta Alternative Investment Funds

1 Directive 2011/61/EC of the European parliament and of the council of 8 June 2011 on Alternative Investment Fund Managers and amending directive 2003/41/EC and 2009/65/EC and regulations (EC) No 1060/2009 and (EU) No 1095/2010.

1.2 An investment fund adopted to any type of investment fund project

AIFs include:

• Hedge funds• Real estate funds• Loan funds (see Section 10.4)• Thematic funds such as AIF: • Investing in specific segments, such as environment • Investing in collectibles, such as luxury goods • Investing in intangible assets, such as patents • Meeting specific criteria, such as responsible investment criteria• Multiple-asset class AIF: AIF with multiple of sub-funds or compartments investing in different asset classes, sometimes with interlinked sub-funds or compartments (see Section 3.2)• Funds of AIF

1.1 The Alternative investment funds regime in brief

An Alternative Investment Fund (AIF) is a pan-European regulated branded investment fund forprofessional and sophisticated investors.

Some key characteristics of the AIF regime:

• A regulated EU structure under the Alternative Investment Fund Managers directive (AIFM directive)1

• Suitable for all investment strategies — including traditional and alternative — and all asset classes• Five different classifications — retail, experienced, professional, qualifying and extraordinary — depending on the proposed target investors (see Section 3.3)• Light diversification and leverage rules depending on target investor (see Section 4.1)• Single fund or multi-fund structure, combining different investment strategies or asset classes in different sub-funds• Possibility of internally managed (self-managed) AIFs (see Section 6)• Availability of marketing passporting of AIFs to all EU member states (see Section 9)

EY supports asset managers and investmentfund houses through the choice of investmentfund vehicle, the analysis of target markets,the definition of an efficient operating model and distribution strategy, and the selection of service providers.

01 Alternative investment funds

The Malta Alternative Investment Funds | 5

6 | The Malta Alternative Investment Funds

policy for the benefit of those investors, and which does not qualify as a UCITS in terms of the UCITSdirective.4

Every licence for an AIF is subject to standard licence conditions which are set in full in the investmentservices rules for Alternative Investment Funds.

2.2 Implications under the AIFM directive

The AIFM directive is the outcome of the recent financial difficulties experienced which have been viewed as being amplified by the activities of Alternative Investment Fund Managers (AIFMs). Itaims to establish common requirements for theauthorization and supervision of AIFMs and AIFs. It also provides a harmonized regulatory framework forthe activities within the EU of all AIFs including AIFMs that are not registered in any EU or EEA member state (non-EU AIFMs).

Its regulations have been transposed in the Act and constituent rules and regulations, and provide a harmonized regulatory framework among the EU member states for the regulation and supervision ofinvestment funds (excluding UCITS). It specifies the core features of such type of investment funds andimposes stringent regulation on AIFs and AIFMs suchas remuneration provisions and the requirement to appoint additional service providers (e.g., a depositary)however it has also introduced marketing passporting provisions for AIFMs to market AIFs to professional investors within the EU jurisdiction, which will eventually replace the current national private placement regime. This directive has adopted a “one size fits all” approach under which a single set of rulesshall govern AIFMs of AIFs which are not covered by the UCITS directive.

2.1 Investment services act

The Maltese Investment Services Act (the Act) provides the statutory basis for regulating investmentfunds constituted in or from Malta.2

AIFs are a special class of investment funds which fall within the provisions of the Act.3 The primary objective of an AIF must be the collective investment of capital acquired by means of an offer of units for subscription, sale or exchange and which has the following characteristics:

• The investment fund or arrangement operates according to the principle of risk spreading and either• The contributions of the participants and the profits or income out of which payments are to be made to them are pooled Or• At the request of the holders, units are or are to be re-purchased or redeemed out of the assets of the investment fund or arrangement, continuously or in blocks at short intervals Or• Units are, or have been, or will be issued continuously or in blocks at short intervals

An AIF that is not sold to retail investors may not havethe characteristic listed in paragraph (a) and shall onlybe deemed to be an investment fund if the AIF, in specific circumstances as established by regulationsunder the Act, is exempted from such requirement and satisfies any other conditions that may be prescribed.

The Act also classifies AIFs as investment funds whichraises capital from a number of investors, with a viewto investing it in line with a pre-defined investment

2 Investment Services Act, 19943 An investment fund, whether of the unit trust or open-ended investment company variety, falling within the scope of and authorised in terms of the UCITS directive.4 Directive 2009/65/EC of the European Parliament and of the Council of 13 July 2009 on the coordination of laws, regulations and administrative provisions relating to undertakings for collective investment in transferable securities (UCITS) (recast) and includes any implementing measures that have been or may be issued thereunder.

02 Requirements of an AIF

The Malta Alternative Investment Funds | 7

In terms of the AIFM directive, the following undertakings shall not be considered as AIFs:

• A holding company• An institution for occupational retirement provision which is covered by directive 2003/41/EC• Employee participation schemes or employee savings schemes• Securitization special purpose vehicles (SPV)• Insurance contracts and joint ventures• Supranational institutions• National central banks• National, regional and local governments and bodies or institutions which manage funds supporting social security and pension systems

2.3 The investment services rules for AIFs

Every license for an AIF is subject to standard license conditions which are set out in full in the investment services rules for Alternative Investment Funds issued by the MFSA. The investment services rules (the rules) describe the basic principles to which license holders must adhere in the provision of investment services or in the operation of an investment fund. In certain circumstances, the standard requirements can be tailored to meet specific circumstances. The rules also include the necessary forms to be completed by applicants for an investmentfund license.

8 | The Malta Alternative Investment Funds

articles of association; no more than 15% of theincome derived from securities are retained by thecompany.

SICAVs and INVCOs can operate as a multi-fundstructure, whereby the share capital may be divided into different classes of shares, with each class ofshares representing a distinct sub-fund of the AIF.

3.1.2 Contractual funds

Contractual funds are governed by the Act established by means of a deed of constitution entered into for such purpose by the manager and the custodian of such an AIF. They are not deemed to be a separate legal entity since they are established through a contractual obligation and can be licensed as a multi-fund or multi-class AIF. A contractual fund may set up one or more special purpose vehicle, which would be a company and through which the AIF maygain access to double taxation treaties.

3.1 AIFs structures

An AIF can be structured as an investment company (SICAV or INVCO), a contractual fund, unit trust or as a limited partnership.

3.1.1 Investment company

AIFs may be set up as limited liability companies andmay be established as open-ended investmentcompanies (SICAVs) or closed-ended investment companies (INVCOs).

A SICAV may be formed as a public or private company with variable share capital and is governedby the Companies Act.5, 6 A private company is restricted to the extent to which it can transfer sharesand is prohibited from issuing any invitation to the public to subscribe to any of the shares or debenturesof the company whilst a public company may offer itsshares or debentures to the public. SICAVs allow forthe introduction of additional investors without havingto wait for the liquidation of an existing investor. In anopen-ended AIF, the value of a share reflects the Net Asset Value of the AIF. SICAVs can be formed as Incorporated Cell Companies, in terms of the Companies Act having each incorporated cellwithin an incorporated cell company as a limited liability company endowed with its own legalpersonality.7

INVCOs are governed by the Companies Act and are public companies with a fixed share capital and its business is restricted to the investment of their fundsmainly in securities, or operating as a retirement fund.8

The activities of an INVCO are further restricted by the following requirements: the company’s holdings in any other company not being an investment companywith fixed share capital, does not exceed 15% by value of its investments; the distribution of the company’scapital profits is prohibited by its memorandum and

5 Investment Companies with Variable Share Capital6 Companies Act (Chapter 386 of the Laws of Malta)7 Companies Act (SICAV Incorporated Cell Companies) Regulations, 20108 Investment Companies with Fixed Share Capital

EY supports asset managers and investmentfund houses through the creation of an investment fund structure that meets the regulatory requirements and tax specifications.

03 Setting up and running an AIF

3.1.3 Unit trusts

AIFs can also be constituted by a trust deed between amanagement company and a trustee. They are governed by the Trusts and Trustees Act which Act enables both residents and non-residents to set up various trust structures such as constructive trusts,discretionary trusts, fixed interests trust and purpose trust.9 Trustees operating in Malta must be approved by the MFSA whilst trusts established in foreign jurisdictions may be recognized in Malta and it is therefore possible to set up an investment fund as a foreign law trust.

3.1.4 Limited partnerships

Limited Partnerships benefit from a similar legislative framework to the one offered to SICAVs and may be constituted as multi-class partnerships or as multi-fundpartnerships and the capital of the partnership can be divided into shares. Partnerships must have a registered office in Malta where they keep the personal information of all limited partners. In addition, a limited partnership requires general partners who are fully liable and both partners can be limited liability companies formed in any jurisdiction. Limited partnerships are governed by the Companies Act.

3.2 Multi-fund UCITS and unit classes

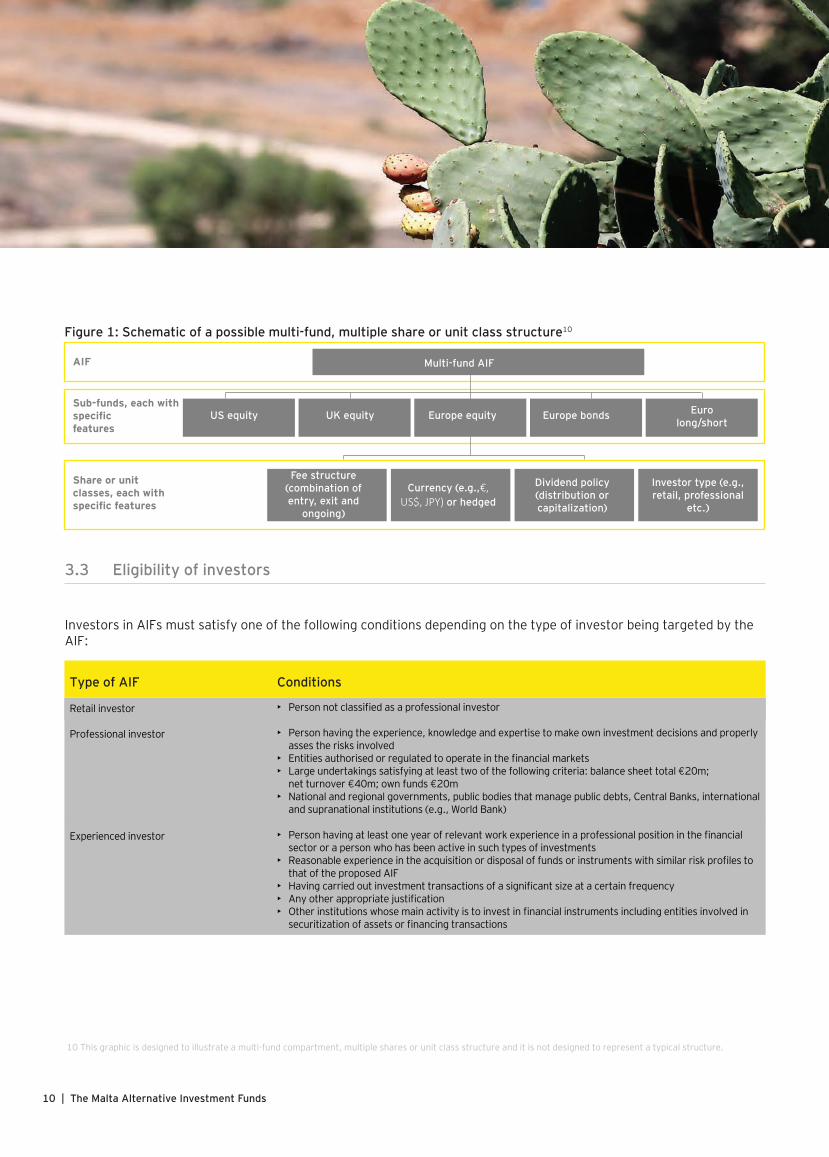

Multi-fund AIFs (otherwise known as umbrella funds) are single legal entities comprising two or more sub-funds or compartments, each with differentfeatures such as different investment policies and objectives, different asset class investments and different target clients.

Multi-fund AIFs may be created provided the constitutional documents expressly permit it and the offering documentation specifies the investment policy,

objectives and restrictions specific to each sub-fund. The multi-fund AIF may also elect, subject to relevant disclosure in its constitutional documents, to have the assets and liabilities of each sub-fund comprised in the AIF treated for all intents and purposes of law as a patrimony separate from the assets and liabilities ofeach other sub-fund of the AIF.

Investors may purchase shares or units in sub-funds which have different investment policies, objectives and restrictions, segregated assets and accounting records. Investors may, if permitted by the constitutional document or offering document, “switch”all or part of their investment from one compartmentto another, in principle without incurring significant charges. Promoters may consequently retain in the same AIF those investors who wish to change their investment strategy.

Multiple share or unit classes may be created within anAIF or, in the case of a multi-fund AIF, within a sub-fund.

While the investment objectives, policies and restrictions are defined at the level of the AIF or the sub-fund, share or unit classes permit the implementation of features, generally customized to one or more specific needs or preferences, such as a specific fee structure, currency of denomination, hedging policy, dividend policy, investor type or country of distribution.

Identification numbers (such as International SecurityIdentification Number (ISIN)) are attributed at the level of the share or unit class.

The graphic design featured on the following pageillustrates the flexibility of a multi-fund AIF.

9 Trust and Trustees Act (Chapter 331 of the Laws of Malta)

The Malta Alternative Investment Funds | 9

10 | The Malta Alternative Investment Funds

Figure 1: Schematic of a possible multi-fund, multiple share or unit class structure10

US equity UK equity Europe bonds Eurolong/short

Fee structure(combination ofentry, exit and

ongoing)

Currency (e.g.,€,US$, JPY) or hedged

Dividend policy(distribution orcapitalization)

Investor type (e.g.,retail, professional

etc.)

Sub-funds, each with specificfeatures

Share or unit classes, each withspecific features

AIF Multi-fund AIF

Europe equity

10 This graphic is designed to illustrate a multi-fund compartment, multiple shares or unit class structure and it is not designed to represent a typical structure.

Retail investor

Professional investor

Experienced investor

Type of AIF Conditions

3.3 Eligibility of investors

Investors in AIFs must satisfy one of the following conditions depending on the type of investor being targeted by the AIF:

• Person not classified as a professional investor

• Person having the experience, knowledge and expertise to make own investment decisions and properly asses the risks involved• Entities authorised or regulated to operate in the financial markets• Large undertakings satisfying at least two of the following criteria: balance sheet total €20m; net turnover €40m; own funds €20m• National and regional governments, public bodies that manage public debts, Central Banks, international and supranational institutions (e.g., World Bank)

• Person having at least one year of relevant work experience in a professional position in the financial sector or a person who has been active in such types of investments• Reasonable experience in the acquisition or disposal of funds or instruments with similar risk profiles to that of the proposed AIF• Having carried out investment transactions of a significant size at a certain frequency• Any other appropriate justification• Other institutions whose main activity is to invest in financial instruments including entities involved in securitization of assets or financing transactions

The Malta Alternative Investment Funds | 11

Qualifying investor

Extraordinary investor

Type of AIF Conditions

• Person (or entity) must have net assets in excess of €750,000. If the AIF is established as a trust, this condition applies to the net value of the trust’s assets. Individuals must meet this threshold either on their own, or jointly with their spouse. This is a mandatory condition• Reasonable experience in investment decisions on funds with a similar risk profile and in instruments of the proposed AIF• A senior employee or director of service providers to the AIF• A body corporate or partnership wholly owned by persons or entities satisfying any of these criteria that is used as an investment vehicle by such persons or entities• An entity with at least €3.75m under discretionary management investing on its own account• The investor is a AIF promoted to qualifying or extraordinary investors

• Person (or entity) must have net assets in excess of €7.5m. If the AIF is established as a trust, this condition applies to the net value of the trust’s assets. Individuals must meet this threshold either on their own, or jointly with their spouse. This is a mandatory condition• The investor is a AIF promoted to extraordinary investors• A senior employee or director of service providers to the AIF• A body corporate or partnership wholly owned by persons or entities satisfying any of these criteria that is used as an investment vehicle by such persons or entity

3.4 Regulatory characteristics and requirements

The following table presents a summary of other regulatory characteristics and requirements of AIFs

AIFs targetingexperienced investors

AIFs targetingqualifying investors

AIFs targetingextraordinary investors

Regulator

Authorization/ licensing procedure

Structures available

Eligible investors

Maximum number ofshareholders

Minimum number of shareholders

Minimum investment

MFSA

Prior to setup

• Investment companies• Limited partnerships• Unit trust• Contractual fund(Refer to Section 3.1)

Refer to Section 3.3

No limit

No minimum

€10,000/ $10,000 orequivalent

MFSA

Prior to setup

• Investment companies• Limited partnerships• Unit trust• Contractual fund(Refer to Section 3.1)

Refer to Section 3.3

No limit

No minimum

€75,000/ $75,000 or equivalent

MFSA

Prior to setup

• Investment companies• Limited partnerships• Unit trust• Contractual fund(Refer to Section 3.1)

Refer to Section 3.3

No limit

No minimum

€750,000/ $750,000 or equivalent

AIFs targetingexperienced investors

AIFs targetingqualifying investors

AIFs targetingextraordinary investors

12 | The Malta Alternative Investment Funds

Use of sub-funds

Multi share classes

Investment restrictions

Leverage restrictions

Cross Sub-Investments

Fees/expenses including performance and advisoryfees

Transferability of shares orunits

Information to investors

Regulator due diligencechecks

Listing possible

NAV calculation

Subscription and redemption price

Yes

Yes

Specific investmentrestriction (refer to Section 4.1)

Up to 100%

No

No restrictions given thatthey are duly disclosed inoffering document

• Generally freely transferable• Subject to informed investor qualifications

Offering documentation and financial statements

• Directors• Shareholders• Service Providers

Yes

NAV required

Subscription andredemption conditions laid down in the constitutionaldocuments

Yes

Yes

No restrictions – subject togeneral diversification requirements (refer to Section 4.1)

No

Yes• Allowed to invest up to 50% of its assets into any sub-fund within the same AIF• The target sub-fund/s may not themselves invest in the sub-fund which is to invest in the target sub-fund/s • When applicable avoid duplication of fees

No restrictions given that they are duly disclosed inoffering document

• Generally freely transferable• Subject to informed investor qualifications

Offering documentation andfinancial statements

• Directors• Shareholders• Service Providers

Yes

NAV required

Subscription and redemption conditions laiddown in the constitutional documents

Yes

Yes

No restrictions – subject togeneral diversification requirements (refer to Section 4.1)

No

Yes• Allowed to invest up to 50% of its assets into any sub-fund within the same AIF• The target sub-fund/s may not themselves invest in the sub-fund which is to invest in the target sub-fund/s • When applicable avoid duplication of fees

No restrictions given that they are duly disclosed inoffering document

• Generally freely transferable• Subject to informed investor qualifications

Offering documentation andfinancial statements

• Directors• Shareholders• Service Providers

Yes

NAV required

Subscription and redemption conditions laiddown in the constitutional documents

The Malta Alternative Investment Funds | 13

4.1 Investment restrictions

The MFSA’s rules for AIFs provides relevantinformation and clarifications on the investmentrestrictions that must be adhered to by AIFs depending on the type of investor being targeted.

Retail investors

The restrictions are to be complied with by each sub-fund in a multi-fund AIF structure.

The following is a summary of the investment restrictions applicable to AIFs targeting the differenttypes of investor:

Restriction

• The AIF may hold ancillary liquid assets irrespective of its investment objective and policy

• Up to 10% of its assets in securities which are not traded in or dealt on a market which: the depositary and the AIFM have agreed upon; is listed in the AIF’s offering documentation; is regulated, operates, recognized and open to public; has adequate liquidity and adequate transmission of income and capital and is not subject to MFSA restrictions• Up to 10% of its assets in securities issued by the same body. Derogation may be obtained to raise the limit to 35% or 100% subject to certain conditions• Up to 10% of any class of security issued by a single issuer• Up to 5% of the value of the AIF in nil paid or partly paid shares and subscribe for placing or underwriting provided certain restrictions are adhered to• The AIF is not to acquire sufficient instruments that give it the right to exercise control over 20% or more of the share capital or votes of a company or to enable it to exercise significant influence over the management of the issuer

• Up to 10% of the assets kept on deposit with any one body. This may be increased to 30% in case of money deposited with an EU credit institution or any other credit institution approved by the MFSA. Derogation may be obtained to raise the limit to 35% subject to certain conditions

Instrument

Ancillary liquid cash

Securities

Deposits with credit institutions

14 | The Malta Alternative Investment Funds

EY supports asset managers and investment houses through the structure and choice ofthe optimum investment fund structure coherent with the relevant investment objectives, policies and restrictions requirements.

04 Investment restrictions

The Malta Alternative Investment Funds | 15

Retail investors

Restriction

• May invest up to 20% of assets in any single investment fund• The AIFM shall waive all charges which it is entitled to charge for its own account in relation to subscription and redemption of units in the circumstances were the AIF invests in other investment funds managed by the same AIFM • Any commission received by the AIFM by virtue of an investment in Units of other investment funds on behalf of the AIF shall be paid into the AIF

• The AIF shall only hold FDIs or OTC-derivative instruments for the purposes of efficient portfolio management • Maximum potential loss to one counterparty in an OTC-derivative transaction is limited to 5% of the value of the AIF. This can be increased to 10% in case of the counterparty being a credit institution. Derogation may be obtained to raise the limit to 35% subject to certain conditions• Netting of the mark-to-market value of the OTC-derivative positions with the same counterparty is allowed only if the AIF has a contractual netting agreement with the counterparty• Derivatives performed on an exchange have a clearing house shall be deemed to be free of counterparty risk• The AIF is to hold the underlying instrument as cover in case where it holds an FDI which requires cash or physical settlement on maturity or exercise

• The AIF may not carry out uncovered sale of securities or other financial instruments

• The AIF may borrow up to 10% of its assets on a temporary basis subject to risk exposure not exceeding 110% of its assets

• The AIF cannot enter into cross sub-fund investments (if case the AIF is established as a multi-fund)

Instrument

Units in other investment funds

Financial derivative instruments

Uncovered sales

Borrowing

Others

16 | The Malta Alternative Investment Funds

Experienced investor

Restriction

• The AIF may hold ancillary liquid assets irrespective of its investment objective and policy

• Up to 20% of assets in securities issued by the same body. Limit may be increased to 35%/ 100% in the case where the money market instrument is issued or guaranteed by authorities in OECD or EU/EEA member states/EEA credit institutions• Limit may be increased to 35% in case of transferable securities traded or dealt on a regulated market

• Up to 30% of assets in money market instruments issued by the same body. Limit may increase to 35%/ 100% in case where the money market instrument is issued or guaranteed by authorities in OECD or EU/EEA member states/ EEA credit institutions

• Up to 35% of assets in deposits held with a single body

• No restriction applicable with respect to investment in a single investment funds provided it qualifies as a UCITS or other open-ended investment funds subject to the equivalent risk spreading requirements applicable to the AIF• Up to 30% of assets in any single investment not qualifying as UCITS or as other investment funds defined in the preceding point• The AIF is to invest in at least five hedge funds in case the AIF is a fund of hedge funds

• Exposure to a single counterparty limited to 20% of total assets; such exposure may be reduced if acceptable collateral is provided by the relevant counterparty • Netting of the mark-to-market value of the OTC-derivative positions with the same counterparty is allowed only if the AIF has a contractual netting agreement with the counterparty

• The Master AIF shall satisfy the leverage restrictions of the AIF in case it is setup as a Feeder Fund

• Up to 25% of assets – directly or indirectly (through an SPV) – in any one single immovable property• The AIF is to invest in at least five different properties in case it invest solely in immovable property • The AIF may invest up to 100% of total assets in any single property fund or SPV provided such fund or SPV complies with the investment, borrowing and leverage conditions applicable to AIFs targeting Experienced investors

• Allowed only if considered to be appropriate and in the best interest of investors and entails and acceptable levels of risk and investment is made in accordance with good market practice and involves the provision of adequate collateral

• Direct borrowing for investment purpose/ leverage via the use of derivatives is limited to 100% of the value of the AIF

• Aggregate maximum exposure to a single issuer/counterparty (through securities, money market instruments, deposits and OTC-derivatives) is limited to 40% of total assets• The AIF cannot enter into cross sub-fund investments (in case the AIF is established as a multi-fund)

Instrument

Ancillary cash

Securities

Money market instrument

Deposits

Units in investment funds

Financial derivative instruments

Feeder fund

Immovable property

Repurchase/reverse repurchase and stocklending or borrowing arrangements

Leverage

General

The Malta Alternative Investment Funds | 17

Professional investor/qualifying investor/extraordinary investor

Restriction

• The AIF may invest in units of one or more sub-funds within the same AIF subject to this being permitted in the constitutional documents and the Offering Memorandum of the said AIF• A sub-fund is allowed to invest up to 50% of its assets in another sub-fund within the same AIF• The target sub-fund may not itself invest in the sub-fund which is to invest in the target sub-fund• Where the AIFM of the sub-fund and the AIFM of the target sub-fund is the same (or in case affiliated), only one set of management (excl. performance fees), subscription and redemption fees shall be applicable

Instrument

Cross subfund investment

5.1 Typical organization of an AIF

This section outlines the typical organization of an AIF, summarizes the roles of the main service providers and outlines the factors impacting the choice

An AIF which has appointed an external assetmanager

18 | The Malta Alternative Investment Funds

of organizational model. As part of the formationprocedures of an AIF, several service providers mustbe appointed. The following diagrams show illustrative examples (however other models may be possible) of the organization of an AIF.

An AIF which has not appointed an external asset manager11

EY supports asset managers and investment fund houses with the selection of service providers having consideration to the target assets and organizational model of the investment fund.

11 Kindly refer to Section 6.0 for detailed information on internally managed/ self-managed AIFs.

Depositary

Prime broker

Auditor

Fund administrator,registrar, transfer

agent

Investment committee

Portfolio managersor

investment company

Depositary

Prime broker

Auditor

Fund administrator,resgistrar, transfer

agent

Third-partyinvestment manager

Investment advisors

Investment fund(board of directors)

Investment advisors

Valuer Asset manager

ValuerInternally managed

AIFboard of directors

05 Key service providers

The Malta Alternative Investment Funds | 19

The principle duties of the service providers are as follows:

5.2 Asset manager

An AIF may only appoint an AIFM, it terms of the AIFMdirective, as its asset manager to be responsible for the management and investment of its assets. TheAIFM is a delegate of the AIF and must be duly authorised to provide such services.

Management services of an AIFM include, in general, investment management, administration and marketing. In practice, many AIFMs delegate some ofthese functions. It shall however remain responsible for overseeing and supervising all delegated functions.

An AIFM may delegate, in part or full, the investmentmanagement function to a third-party investment company provided it is authorised to undertake such activity (e.g., an EU MiFID asset manager). The administrative function is ordinarily also delegated toan Administrator (see section 5.5)

The AIFM need not be domiciled and regulated where the AIF is domiciled. Not all AIFs are required to appoint an external asset manager (see Section 6).

5.3 Investment advisor

The investment advisor advices the AIF’s asset manager respect of transactions relating to financial instruments. The investment advisor will not have anydiscretion with respect to the investment and re-investment of the assets of the AIF.

AIFs ordinarily do not appoint an investment advisor. Furthermore, the investment advisor need not be based in the same jurisdiction as the AIF, but shall

have sufficient financial resources and liquidity at its disposal to enable it to conduct its business.

5.4 Depositary

The AIFM must appoint a single depositary for each AIF it manages. The depositary shall either be:

• A licensed EU credit institution • A licensed EU MiFID firm authorised to provide the services of safe-keeping of assets Or• Any other entity permitted to act as depositary pursuant to UCITS directive

The depositary need not to be domiciled in thejurisdiction of the AIF, at least until 22 July 2017.12

It must be independent from the asset manager and shall not be engaged as the valuer. The depositary may also act as prime broker, acting as counterparty to the AIF, subject to certain conditions being met.

While safekeeping of assets in which the AIF invests is the core function of the depositary, this party is also responsible for overseeing the AIFM compliance with the AIF’s constitutional documents and rules and to monitor the AIF’s cash flows.

The safe-keeping task is the only task that a depositary may delegate.

12 MFSA negotiated the derogation to Article 61(5) of the AIFM directive

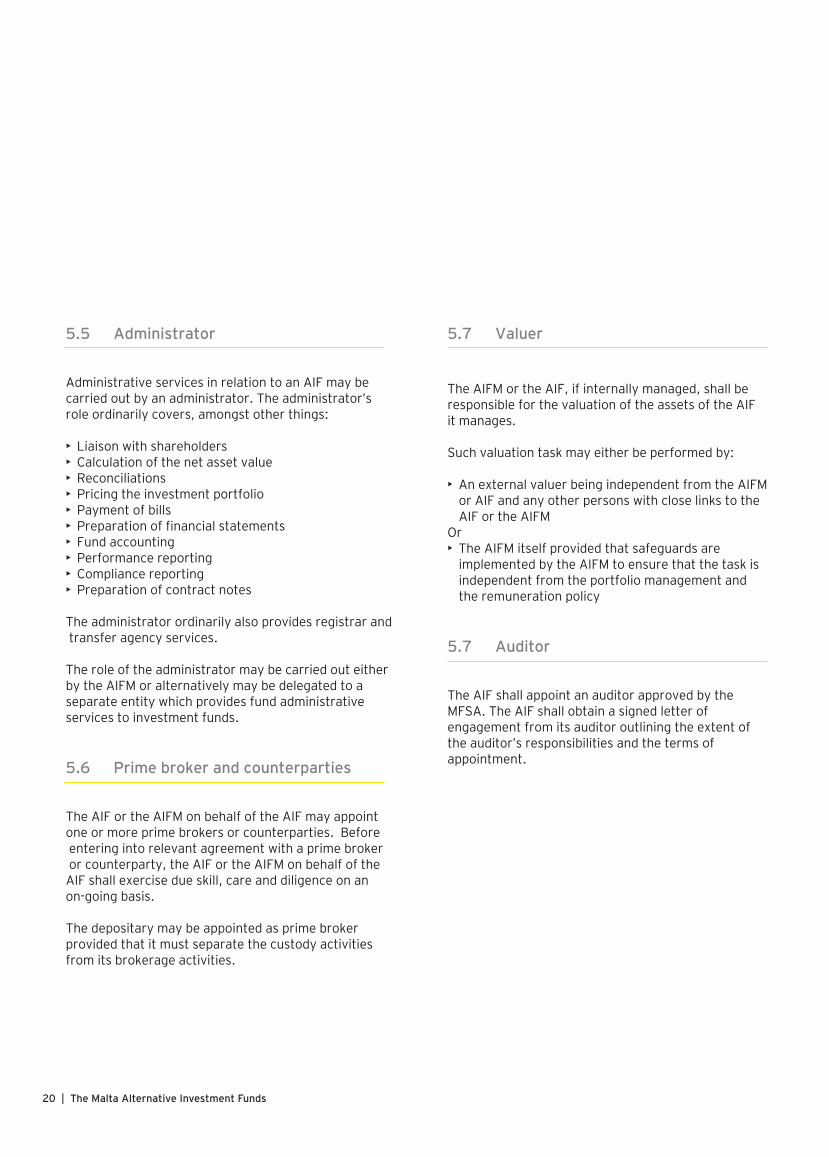

5.5 Administrator

Administrative services in relation to an AIF may be carried out by an administrator. The administrator’s role ordinarily covers, amongst other things:

• Liaison with shareholders• Calculation of the net asset value• Reconciliations• Pricing the investment portfolio• Payment of bills• Preparation of financial statements• Fund accounting• Performance reporting• Compliance reporting• Preparation of contract notes

The administrator ordinarily also provides registrar and transfer agency services.

The role of the administrator may be carried out either by the AIFM or alternatively may be delegated to a separate entity which provides fund administrative services to investment funds.

5.6 Prime broker and counterparties

The AIF or the AIFM on behalf of the AIF may appointone or more prime brokers or counterparties. Before entering into relevant agreement with a prime broker or counterparty, the AIF or the AIFM on behalf of the AIF shall exercise due skill, care and diligence on an on-going basis.

The depositary may be appointed as prime broker provided that it must separate the custody activities from its brokerage activities.

5.7 Valuer

The AIFM or the AIF, if internally managed, shall be responsible for the valuation of the assets of the AIF it manages.

Such valuation task may either be performed by:

• An external valuer being independent from the AIFM or AIF and any other persons with close links to the AIF or the AIFMOr• The AIFM itself provided that safeguards are implemented by the AIFM to ensure that the task is independent from the portfolio management and the remuneration policy

5.7 Auditor

The AIF shall appoint an auditor approved by theMFSA. The AIF shall obtain a signed letter of engagement from its auditor outlining the extent of the auditor’s responsibilities and the terms of appointment.

20 | The Malta Alternative Investment Funds

The Malta Alternative Investment Funds | 21

22 | The Malta Alternative Investment Funds

As such, the AIF may consider either of the following options:

• To integrate a fully fledged investment management function Or• To delegate either the investment management or risk management function to a third-party while retaining the other function

6.1 Introduction

An AIF may opt not to appoint an AIFM and thus the AIF will be carrying out internally the investment management function. In this regard, the AIF shall at least perform the portfolio management and risk management functions.

For the purpose of this section the term “AIF” shall be understood to refer to “internally managed AIF”. The term “investment management” shall refer to the “portfolio management and risk management functions”.

6.1 Operational arrangements

An AIF is to organise and control its affairs in a responsible manner and is to have adequate operational, administrative and financial procedures and controls to ensure compliance with all regulatoryrequirements.

The AIF would also need to have adequate and appropriate human and technical resources that arenecessary for the proper management and to effectively perform its activities.

6.1.1 Investment management

The AIF’s board of directors would be responsible forthe investment management function. In undertaking its activities, the AIF is to functionally separate thefunctions of portfolio management and riskmanagement. In that persons ordinarily engaged in either of the said functions are not to be supervisedby those responsible for the other operating units norare they to be engaged in other operating activities. Compensation to such persons should also be related solely to the performance of the function involved in.

EY supports asset managers and investmentfund houses with the organizational modeling,internal structuring and policies as well as anydelegation arrangements for internally managed investment funds.

06 Internally managed AIFs

The Malta Alternative Investment Funds | 23

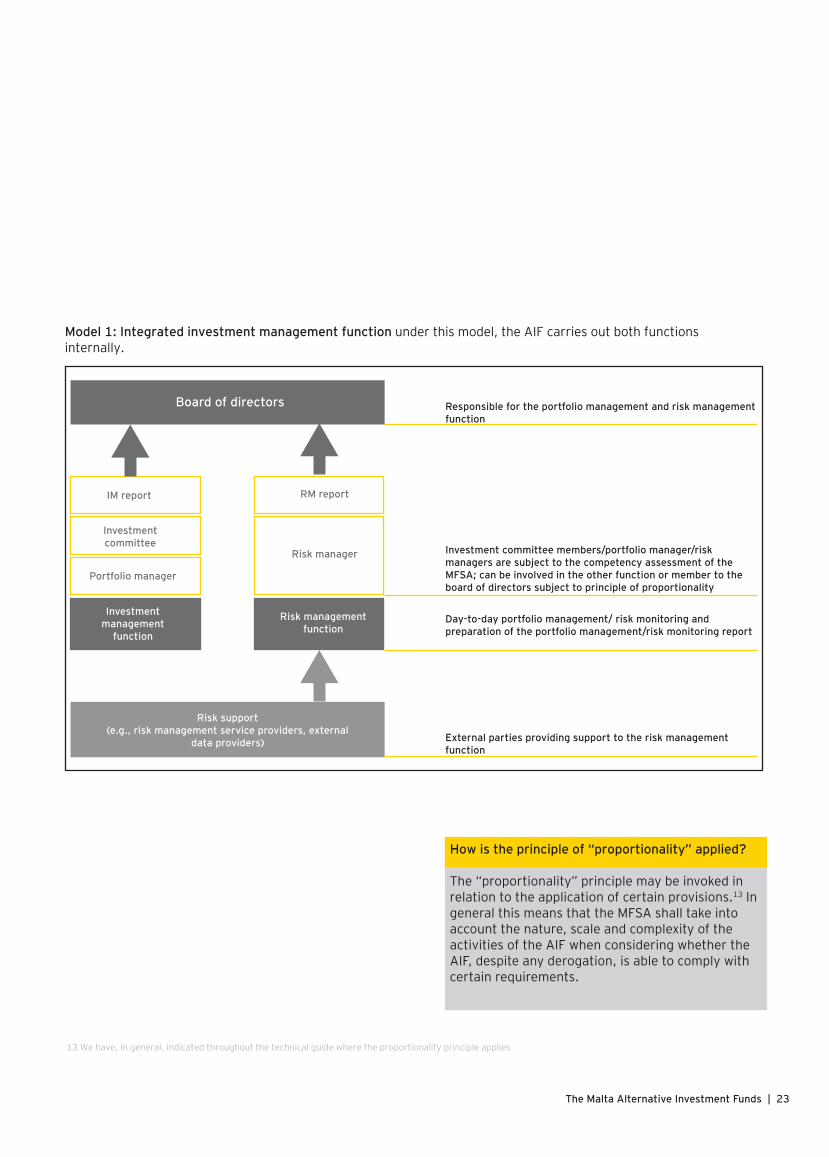

Model 1: Integrated investment management function under this model, the AIF carries out both functions internally.

IM report

Investmentmanagement

function

Board of directors

Investmentcommittee

Portfolio manager

Risk managementfunction

RM report

Risk manager

Risk support(e.g., risk management service providers, external

data providers)

Investment committee members/portfolio manager/risk managers are subject to the competency assessment of the MFSA; can be involved in the other function or member to the board of directors subject to principle of proportionality

Day-to-day portfolio management/ risk monitoring andpreparation of the portfolio management/risk monitoring report

External parties providing support to the risk management function

Responsible for the portfolio management and risk management function

How is the principle of “proportionality” applied?

The “proportionality” principle may be invoked in relation to the application of certain provisions.13 In general this means that the MFSA shall take into account the nature, scale and complexity of the activities of the AIF when considering whether the AIF, despite any derogation, is able to comply with certain requirements.

13 We have, in general, indicated throughout the technical guide where the proportionality principle applies

24 | The Malta Alternative Investment Funds

Model 2: Delegating of investment management function and retaining of risk management function

In this model, the AIF undertakes the risk management function through its own staff and delegates the portfolio management to a third-party, for example an EU-based MiFID compliant investment company.

Portfolio Manager

Risk support(e.g., risk management service providers, external

data providers)

Risk management function

RM report

Board of directors

Investment management team

IM delegated

IM reports

AIF EU MiFID entitiesor authorized delegate

The AIF is to establish procedures for the effective transfer of information to and from the delegate in line with the delegation provisions. External parties may also be appointed to provide support to the AIF risk management function. The board would still be responsible for both portfolio management and risk management functions. A variant to this model would be for the delegation of the risk management function instead of the investment management function.

RM reports

6.1.1.1 Portfolio management

The roles and duties pertaining to the portfolio management function are as follows:

6.1.1.2 Risk management

An AIF must also operate within a robust risk management framework to adequately manage riskalong its investment objectives and strategies. The AIF is to establish and maintain a permanent risk management function which proceedings are to be governed by a dedicated risk management policy. Therisk management function shall be functionally and hierarchically separated from operating units includingthe portfolio management, or, at least, specificsafeguards against conflicts of interest shall beimplemented to allow an independent performance of risk management activities.

The MFSA shall adopt a risk-metric approach proportional to the AIF’s size, internal organization and complexity of its activities in case the risk management function is not hierarchically and functionally independent from other units.

When is the risk management function “functionallyand hierarchically separated”?

• Individuals engaged in the risk management function are not supervised by those responsible for the operating units nor involved in such other units of the AIF. • Compensation of individuals involved the risk management function is related solely to such function. • The separation is ensured up to the board of directors of the AIF.

Board of directors

Portfoliomanager

EU MiFIDinvestmentcompany

Or

Investmentcommittee

The investment committee shall:• Monitor and review the investment policy of the AIF• Establish and review guidelines for the investment by the AIF• Issue rules and asset selection criteria• Setting up portfolio structure and allocation parameters• Make recommendations to the board of directors

Responsible for the overall management of the assets of the AIF

• Delegated the day-to-day portfolio management• Undertake the day-to-day portfolio management in line with the investment guidelines set by the investment committee and in accordance with the AIFs offering documents

The Malta Alternative Investment Funds | 25

26 | The Malta Alternative Investment Funds

The AIF may also elect to contractually delegate the risk management function to third parties (not being the depositary or a delegate of the depositary) for the purpose of a more efficient conduct of business provided that the AIF is able to demonstrate that: the third-party has the professional ability and capacity to perform such duties, is duly authorised or registered to perform such duties and its appointment is acceptable to the MFSA.

In doing so, the AIF must establish methods for ongoing assessment of the standard of performance of the third-party.

6.1.1.3 Delegation

The Portfolio manager(s) may either be individual(s) ora licensed manager which is authorized or registered to perform such function and accordingly it may not necessarily be authorized as an AIFM (e.g., an EU MiFID investment company) and acceptable to the MFSA.The AIF may confer the portfolio management function to managers licensed in third countriesprovided that a cooperation agreement is in placebetween the MFSA and the supervisory authorities of the manager’s third country. Portfolio managementactivities may not be delegated to the depositary.

6.1.2 Valuation

AIFs must have in place appropriate valuation procedures to ensure the proper valuation of its assets. The valuation function must be either performed by:

• The AIF itself subject to the task being independent from the portfolio management and safeguards are in place to mitigate any conflicts of interest or undue influence upon the employees performing such task, being independent from the remuneration policy.

EY supports asset managers and investmentfund houses in defining or reviewing the risk management process and the formation of internal policies and procedures.

• An external valuer subject to mandatory professional registration recognized by law or legal or regulatory provisions or rules of professional conduct, independent from the AIF and any other persons with close links to the AIF.

The depositary shall not be appointed as external valuer unless it has functionally and hierarchically separated the performance of its depositary functions from its tasks as external valuer and the potential conflicts of interest are properly identified, managed,monitored and disclosed to the investors of the AIF.

External valuers must provide professional guarantees.The professional guarantees are to contain evidence of the external valuer’s capabilities in performing the valuation task, including evidence of:

• Sufficient personal and technical resources in respect of the AIF’s investment strategy and specific asset • Adequate procedures safeguarding proper and independent valuation • Adequate knowledge and understanding in respect of the AIF’s investment strategy and specific asset

The Malta Alternative Investment Funds | 27

In case that an external valuer is appointed to valueonly parts of the AIF’s portfolio, the external valuer isrequired to provide resources, procedures, knowledge and understanding which are sufficient in respect of such asset.

An AIFM itself or a delegated third-party may carry out the calculation of the net asset value and such activity shall not constitute as valuation of underlying assets provided that the AIFM or third-party is not providing valuations for individual assets, including those requiring subjective judgement, but simply incorporates into the calculation process the valuation of assets obtainedfrom the valuer

6.2 Remuneration

6.2.1 Principles or remuneration

An AIF must adopt a remuneration policy which governs all of the payments made by it to certain members of its staff in exchange for the services rendered, which activities have a material impact onits risk profile. It should broadly promote sound and effective risk management and does not encouragerisk taking which is inconsistent with its risk profile. The policy is to be reviewed by the AIF’s board of directors on a periodic basis, at least annually.

The Annex II principles

• The remuneration policy must include measures to avoid conflicts of interest.• The management body of the AIF must periodically review the remuneration policy and is responsible for its implementation.• The implementation of the remuneration policy must be subject to an independent review at least annually.• Guaranteed bonuses should be “exceptional” and may only occur in the context of hiring new staff for the first year of service.• Payments related to the early termination of a contract must reflect performance over time and not reward failure.• The fixed and variable components of total remuneration should be appropriately balanced with the fixed component to represent a sufficiently high proportion of the total remuneration.• At least 50% of any variable remuneration must consist of non-cash variable payments such as units or shares in the AIF, which will be subject to an appropriate retention policy designed to align incentives with the interests of the AIF and its investors.• At least 40% of variable remuneration should be deferred over a period which is appropriate in view of the life cycle and redemption policy of the AIF. The period shall be at least 3 to 5 years unless the life cycle of the AIF is shorter.• The variable remuneration must be paid or vest only if it is sustainable according to the financial situation of the AIF as a whole. The total variable remuneration must generally be “considerably contracted” where subdued or negative financial performance of the AIF occurs, including through reducing payouts of amounts previously earned (including by malus or clawback arrangements).• AIFs that are significant in terms of their size, their internal organization and the nature, the scope and the complexity of their activities must establish a remuneration committee. The members of which are not to perform any executive functions in the AIF.

28 | The Malta Alternative Investment Funds

6.2.2 Applicability of remuneration provisions

In general, an AIF shall have remuneration policies and practices for those categories of staff — referred to as “identified staff” — whose professional activities have a material impact on its risk profile.14 These Identified Staff shall be subject to the remunerationprovisions unless the AIF is able to demonstrate thatsuch staff, while it may be classified as “Identified Staff”, have no material impact on the AIF’s risk profilein undertaking their duties.

For this purpose, remuneration shall consist of: • All forms of payments or benefits paid by the AIF, including carried interest• Any transfer of units or shares of the AIF, in exchange for professional services rendered by the AIF’s identified staff

AIFs may also set up a remuneration committee that would be responsible for the implementation andadaptation of the remuneration policy and, if established, must operate independently and at leastbe composed by a majority of members who do not perform any executive function within the AIF.

6.2.3 Application of the proportionality principle

AIFs may in certain cases have the remuneration provisions related to the establishment of the remuneration committee and the requirements on thePay-Out process disapplied entirely subject to the authorization of the competent authorities. 15

The MFSA had issued guidelines to the financial services industry on the application of theproportionality principle on March 2014. These guidelines note that, in taking measures to comply with the remuneration principles, AIFs should complyin a way and to the extent that is appropriate to theirsize, internal organization and the nature, scope and complexity of their activities.

The AIF is to consider all of the three factors cumulatively. By way of example, an AIF which is significant only with respect to one or two criteria may still be able to derogate from the requirement to eitherestablish the remuneration committee or from applying the requirements related to the Pay-Out process. The MFSA’s guidelines further provide thatan AIF may not apply lower thresholds based on proportionality and the specific numerical criteria mayonly be disapplied in their entirety that where it passes the proportionality test. For example, the specific numerical criteria set out in Annex II principles (e.g., the minimum portion of 40% to 60% of variable remuneration that should be deferred), if disapplied,may only be disapplied in their entirety otherwise it must be complied with in full without variation.

14 Referring to senior management, risk takers, control functions and other risk takers including members of the board of directors (executive and non-executive) and persons involved in the portfolio management function15 Refers to the requirements on: variable remuneration in instruments; retention; deferral; and ex-post incorporation of risk for variable remuneration (e.g., clawback/ malus arrangements).

The Malta Alternative Investment Funds | 29

The following tables illustrate the thresholds under or above which the MFSA’s guidelines and the correspondingprinciples may be applied or disapplied.

6.2.4 Delegation

Contrary to ESMA’s guidelines on remuneration, the MFSA in its guidelines noted that third-party entities to which either the portfolio management or risk management is being delegated will not be subject tothe remuneration requirements applicable to the AIF.16

6.3 Capital requirements

The AIF is to have sufficient financial resources at itsdisposal to enable it to conduct its business effectively,to meet its liabilities and to be prepared to cope withthe risks to which it is exposed. It is to maintain an“initial capital” of €300,000 and that the net asset value of the AIF is expected to exceed this amount on an ongoing basis.

In addition if the portfolio of the AIF exceeds a value of €250m, it is required to maintain “own funds” equal to the highest of:

• 0.02% of the AIF’s portfolio in excess of €250m capped at €10m

16 ESMA guidelines on sound remuneration policies under the AIFMD (ESMA/2013/232)17 Within the meaning of Article 21 of the capital requirements directive (Directive 2006/49/EC)

Value of portfolio ofthe AIF

Do the rules on the“pay-out process” apply?

Does the AIF need to establish a remuneration committee?

Leveraged

Unleveraged

Less than €100mBetween €100m and €1.25bOver €1.25b

Less than €500mBetween €500mand €6bOver €6b

NoMay be disapplied on the basis of proportionality Yes. Full application

NoMay be disapplied on the basis of proportionality Yes. Full application

NoMay be disapplied on the basis of proportionality Yes. Full application

NoMay be disapplied on the basis of proportionality Yes. Full application

Type of AIF

Or• One quarter of the preceding year’s fixed overheads that may therefore exceed the cap of €10m specified in the AIFM directive.17

Preparatory Pre-licensing Post-licensing

Initial submission of documents for authorization including: • Application Form • Draft documents and any

additional information

• Submission of final documents

• Listing on the official list of licensed entities

• Issue of licence

MFS

AM

ain

docu

men

ts

7.1 Initial consideration

In practice, a large amount of work will be performedby the promoters, consultants, auditors or legal advisors and proposed service providers before submission of the application for authorization of an AIF.

7.2 Authorization process and requirements

An AIF established in Malta, should obtain authorization and license from the MFSA to be able to operate. The approval process for setting up a new AIF can be divided into three phases:

Phase 1 — Preparatory phase

• AIF promoters or managers prepare a detailed proposal of their activities and discuss the terms at meetings with the MFSA in order for the MFSA to provide relevant guidance and clarifications as necessary.

Authorization process

• AIF promoters submit the draft application documents as outlined below, which documents will be reviewed by the MFSA and may request additional evidence, corrections, or proof of the fit and proper test, among other things. • The MFSA will consider the nature of the proposed AIF and a decision will be made regarding which SLCs should apply. These represent ongoing requirements which need to be satisfied.

EY supports asset managers and investment fund houses with the investment fund setupand application for authorization, as well as restructuring and liquidation.

The authorization process can be summarised as follows:

30 | The Malta Alternative Investment Funds

07 Authorization

• Personal questionnaire and competency form of the compliance officer and money laundering reporting officer

In the case of internally managed AIFs (see Secion 6), the following additional documents must also be submitted:

• Information including personal questionnaire and competency forms on the investment committee members• Investment committee terms of reference • Confirmations from the portfolio manager and investment committee• Portfolio and risk delegation agreements (as applicable)• Risk management policy document; • Business plan• Copy of the cover note to the insurance policy if the AIF intends to cover potential professional liability risks by way of professional indemnity insurance

The MFSA recommends applicants to file an application only once all constituents of the project are in final draft form.

Phase 2 — Pre-licensing phase

• When all review points noted in the draft application are resolved, the MFSA will issue an “in principle” approval for a license. Following this, AIF promoters must: • Finalize any outstanding matters • Submit signed final application documents.• A license will be issued once all pre-licensing issues are resolved.

Phase 3 — Post-licensing/pre-commencement of business phase

• The MFSA will determine whether the applicant needs to satisfy any post-licensing matters before formal commencement of business can take off.

The initial application documents submission shouldinclude:

• Application form• Application fee• A near final draft offering document/ marketing document• A near final draft of the memorandum and articles of association/partnership deed/ trust deed/ fund rules (as applicable)• Resolution from the board of directors/ General partners/management company;• Information including personal questionnaire forms on the directors/general partners of the AIF• Information on the qualifying founder shareholders (holding 10% or more of the voting rights) including Personal questionnaire forms • Personal questionnaire forms, competency forms and CVs of the individuals responsible for the investment management and risk management decisions of the AIF

The Malta Alternative Investment Funds | 31

8.1 Special purpose vehicles

An SPV is a legal entity which is set up for a specific limited purpose by another entity (i.e., the originator), in that the SPV has no purpose other than the transaction for which it has been created. An AIF (or the AIFM acting on behalf of the AIF) will establish anSPV in order to facilitate investments in certain assetssuch as benefiting from a regulatory and tax perspective by incorporating the SPV in a more attractive jurisdiction or to finance a new venture without increasing the debt burden of the AIF.

From a regulatory perspective, the MFSA defines an SPV as being setup by the AIF as part of its investment strategy for the purpose of achieving itsinvestment objectives, being (directly or indirectly)owned and controlled via majority of voting shares and having the majority of the SPV’s directors in common with the AIF. For a Malta-based AIF using an SPV for investment purposes, it must ensure that theSPV is established in a jurisdiction which is not a FATF blacklisted country, it maintains at all time the majority of directorship and it must ensure that theinvestments effected through any SPV are inaccordance with the investment objectives, policiesand restrictions of the AIF.

8.2 Re-domiciliation of AIFs

Maltese legislation allows for the re-domiciliation of corporate entities, which means that an investmentfund established as an investment company in another jurisdiction may continue to exist in Malta under certain conditions. The continuation allows forthe transfer of the corporate entity seat ofincorporation from one jurisdiction to Malta thus allowing the continuing corporate existence of the re-domiciled corporate entity.

EY supports asset managers and investmentfund houses in the regulatory assessment and implementation of bespoke features for investment funds.

32 | The Malta Alternative Investment Funds

For an investment fund to be re-domiciled to Malta, it must be, formed and registered in an Approved Jurisdiction, able to adopt a similar corporate structure proposed to the AIF (e.g., as an investment company), allowed to re-domicile by the laws of the approved jurisdiction and not be in the process of dissolution or winding up.

The process is seamless given that the AIF regime allows service providers to be based in other jurisdictions. Also, there is no transfer of assets and the status of investors does not change.

8.3 Side pocket

Where an AIF invests in illiquid assets, some or all of these assets may, under certain circumstances, be transferred to a side pocket. The purpose of side pockets is to mitigate risks arising from certain assetsbecoming illiquid, thus the AIF would not realise such asset to meet its redemption obligations, or turns outto be hard-to-value and as a result the price of shares for subscription and redemption will not accurately reflect the fair value of the assets as it cannot bevalued accurately.

08 Salient features of AIFs

• Any side letter issued must be retained at the registered office of the AIF and is to be available for inspection by the MFSA during compliance visits.

8.5 Draw downs

AIFs (established as SICAVs) targeting qualifying or extraordinary investors may enter into written agreements with investors to effect draw downs oncommitted funds thus allowing investor funds to be drawn down by the AIF or its asset manager as investment opportunities arises.

Any AIF to provide such arrangement is to comply with the following conditions:

• Request on committed funds shall be effected pro-rata amongst all relevant investors in the AIF.• Any fresh call for further commitments shall be made once all outstanding commitments from existing investors have been requested.• Any shares to be issued at a “discount” to existing investors on committed funds, the nature of which to be disclosed in the AIF’s constitutional documents, shall be applicable only to any outstanding commitment provided that shares are issued at a price not below the NAV at the time the investor first subscribed to the shares.18

• Copies of the written agreements are to be held at the AIF’s registered office and are to be available for inspection by MFSA officials during compliance visits.• Specific risk warnings to be included in the offering document noting that investors will be issued shares at a “discount” if the NAV of the share prevailing at the time of the draw down exceeds the pre-agreed price otherwise the investor would, in effect, be paying a premium for such shares.

The assets in the side pocket would be separated fromthe main pool of assets allowing the AIF to continue inthe issue and redemption of shares in the liquid pool of assets.

On the date of the creation of the side pocket, the assets are allocated to the new share class – the side pocket. The investors of the existing share class will receive shares in the side pocket on a pro-rata basis according to their holding in the existing share class.

The side pocket is closed to any new subscriptions andsuspended from redemptions.

The AIFM is required to manage the assets in the sidepocket with the objective of realising them in the bestinterest of, and if warranted, distributing the proceedsto, investors. Shares in the side pocket are to beredeemed upon the sale of the asset or when the asset is transferred to the main liquid portfolio ofassets.

The MFSA permits the use of side pockets provided that statutory information is disclosed in the AIF’s constitutional documents and that certain conditions are satisfied.

8.4 Side letters

The use of side letters allows for greater flexibility to the AIF or its asset manager to enter into tailored arrangements with specific investors without the requirement to amend the conditions disclosed in the AIF’s constitutional documents.

To create a side letter, the following conditions are to be met:

• The side letter must be approved by the AIF’s board of directors prior to being issued.

The Malta Alternative Investment Funds | 33

18 Companies Act (investment companies with variable share capital) regulations (Legal notice 241 of 2006, as amended)

9.1 Introduction

Marketing relates to any direct or indirect offering orplacement at the initiative, or on behalf, of the AIFM of units or shares of AIFs it manages to investors domiciled EU/EEA member states.

Specifically, the AIFM directive defines “marketing” as the “direct or indirect offering or placement at the initiative of the AIFM or on behalf of the AIFM of units or shares of an AIF it manages to or with investorsdomiciled or with a registered office in the EU”. Thismeans that the marketing provisions of the AIFMdirective do not apply to “reverse solicitation” or “passive marketing” (i.e., marketing which is not at thedirect or indirect initiative of the AIFM). An EU professional investor may thus invest, on its own initiative, in AIFs anywhere in the world. This may also be the only route for a non-EU AIFM to access investors in the EU should it not satisfy thepassporting provisions under the AIFM directive orthe National Private Placement Regulations.

9.2 Marketing of an AIF

The marketing of AIFs depends on whether or not they are managed in line with, and subject to, the full AIFM directive requirements (Full AIFM regime AIF).Full AIFM regime AIFs are AIFs which are managed by an authorised AIFM or authorized as an internally managed AIF. In summary, a Full AIFM regime AIF can be marketed to:

• Professional investors in the EU/EEA: An EU AIFM would benefit from the passporting regime to market the units of the AIF they manage to professional investors throughout the EU/EEA.

EY supports asset managers and investment fund houses in the regulatory assessment andnotification for the distribution of the investment fund.

Or• Retail investors in the EU/EEA under stricter national rules: Each EU/EEA member states may permit authorized AIFM to market the shares or units of the AIF they manage to retail investors in the member states.

9.2.1 EU AIFMs and non-EU AIFMs

EU AIFM

The marketing regime for EU/non-EU domiciled AIFsby, or on behalf of, EU AIFMs is summarized in the table on page 35.

Non-EU AIFM

The AIFM directive applies to non-EU AIFMs that manage EU AIFs or market AIFs (EU or non-EU) to EU investors. The marketing regime for EU/non-EU domiciled AIFs by, or on behalf of, non-EU AIFMs issummarized in the table on page 35. The risk profile of a UCITS may be defined as the measure of risk aversion relative to the investment strategy (i.e. risk-reward trade-off)

34 | The Malta Alternative Investment Funds

09 Marketing under the AIFM directive

The Malta Alternative Investment Funds | 35

DomicilesAIFM AIF

Marketedin the EU?

Is AIFMdirectiveapplicable?

AIFMmarketingregime

Requirementsapplicable to theAIFM and AIF

Requirementsapplicable to third-countrydomiciles

EUEUEU

EU

EU EUNon-EU

Non-EU

YesNoYes

No

YesYesYes

Yes

PassportNoneNPPRs (until 2018)

Passport(expected in late 2016)

None

Full directiveFull directiveFull directive except the provisions on depositary but an entity must be appointed to execute thedepositary functionsFull directive

Full directive except the provisions on depositary and annual reports

NoneNoneCooperation agreements (1)AML requirements (2)

Cooperation agreements (1)AML requirements (2)Tax agreements (3)Cooperation agreements (1)

(1) Cooperation agreement between the competent authorities of the AIFM home member state and the supervisory authorities of the AIF third country. See Annex 1 for the list of cooperation arrangements signed by the MFSA. (2) The AIF third-country is not listed as a NCCT by the financial action task force (FATF). (3) An OECD model article 26 compliant agreement must be signed between the non-EU AIF third-country, AIFM member state and any other EU member state in which the non-EU AIF will be marketed.

DomicilesAIFM AIF

Marketedin the EU?

Is AIFMdirectiveapplicable?

AIFMmarketingregime

Requirementsapplicable to theAIFM and AIF

Requirementsapplicable to third-countrydomiciles

(1) Annual report, disclosure to investors and reporting to competent authorities. (2) Cooperation agreement between the competent authorities of each member state where the AIF is marketed, the AIF’s home member state (or the AIF’s country of establishment supervisory authorities for non-EU AIFs) and the supervisory authorities of the AIFM third country of establishment. See Annex 1 for the list of cooperation arrangements signed by the MFSA. (3) The AIFM third country is not listed as a NCCT by the Financial Action Task Force (FATF).(4) An OECD Model Article 26 compliant agreement must be signed between the non-EU AIF third country, AIFM member state and any other EU member state in which the non-EU AIF will be marketed.

Yes

Yes

Yes

No

Yes

No

Yes

No

EU

EU

Non-EU

Non-EU

Non-EU

Non-EU

Non-EU

Non-EU

EU AIFM

Non-EU AIFM

Provisions on transparency(1), and major holdings andcontrol (if applicable) Full directive; “member state of reference” authorization (4) to manage EU AIFs or market AIFs in EU

(expected from 2017)Full directive; “member stateof reference” authorization tomanage EU AIFs Provisions on transparency (1),and major holdings and control(if applicable) (expected from 2017) Full directive; “member state of reference” authorization tomarket non-EU AIFs in EUNone

Cooperation agreements (2) AML requirements (3)

Cooperation agreements (2) AML requirements (3)Tax agreement (4)

Cooperation agreements (2) AML requirements (3)Tax agreement (4)

Cooperation agreements (2) AML requirements (3)

Cooperation agreements (2) AML requirements (3)Tax agreement (4)

NPPRs (until 2018)

Passport (expected after 2016)

None

NPPRs (until 2018)

Passport

None

9.3 Internally managed AIFs — a passporting alternative

As a practical matter, an EU AIFM which markets anEU AIF, or an internally managed EU AIF, will have an advantage over any EU or non-EU AIFM which markets a non-EU AIF, as the EU AIF has the benefit of the marketing regime. The AIFM directive provides that where the legal form of the AIF allows for internal management and that the AIF chooses not to appoint an external AIFM, the AIF may itself be authorised as an AIFM. The Maltese regulatory framework already allows for an AIF to be internallymanaged. Non-EU asset managers can therefore avail themselves of the marketing provisions by establishing an internally managed AIF to be marketed as an authorised AIFM, which in turn coulddelegate the investment management function to thenon-EU asset manager.

9.4 The notification procedure

Before EU AIFMs (or “internally managed” EU AIFs) or non-EU AIFMs benefit from the passporting provisions(once it is phased in for third-countries) to markettheir AIFs to “professional investors” in a EU member state, they must notify the competent authority in their respective home member state or member stateof reference for each AIF.

The notification must include: • A notification letter, identifying the AIF which the AIFM intends to market and information on where it is established• The AIF’s offering document or instruments of incorporation• The identity of the depositary of the AIF

36 | The Malta Alternative Investment Funds

• A description of, or any information on, the AIF available to investors, as well as information that must be provided to them before they invest• Information on where the master AIF is established, if the AIF is a feeder AIF• Any additional information concerning disclosure obligations of the AIF• The identification of the member state(s) in which it intends to market the AIF• Details of the measures to be undertaken to prevent the AIF from being marketed to Retail Investors

For “internally” managed AIFs, the notification letter shall also include a programme of its operations.19