the ma community investment tax credit joe kriesberg march 2015

TRANSCRIPT

The MA Community Investment Tax Credit

Joe KriesbergMarch 2015

Innovation Forum:Lessons Learned1) CDCs must reflect authentic community-

base2) CDCs must develop a strategy tailored to

their local market context3) The CDC business model needs updating4) New real estate development must be

balanced with long-term stewardship of existing portfolios

5) We need to break down boundaries between CED and other sectors

Innovation Forum:Lessons Learned6) Evidence and data are increasingly important

for defining needs and impact7) We need to apply “state of the art”

communication strategies to secure broader support

8) Collaboration at all levels is critical9) 21st century community development needs to

be community-centric, not real estate centric10) Need to balance supply-side and demand-side

community development

Our Strategy Support changes needed to advance all 10

lessons Use training, technical assistance, and

peer learning to lift CDC practice Use partnerships and programs to advance

new innovations and best practices Seek policy and system change CITC is a way to drive multiple goals

simultaneously – and to do so at scale

Goal of CITC“To enable local residents and stakeholders to work with and through community development corporations to partner with nonprofit, public and private entities to improve economic opportunities for low- and moderate-income households and other residents in urban, rural and suburban communities across the Commonwealth."

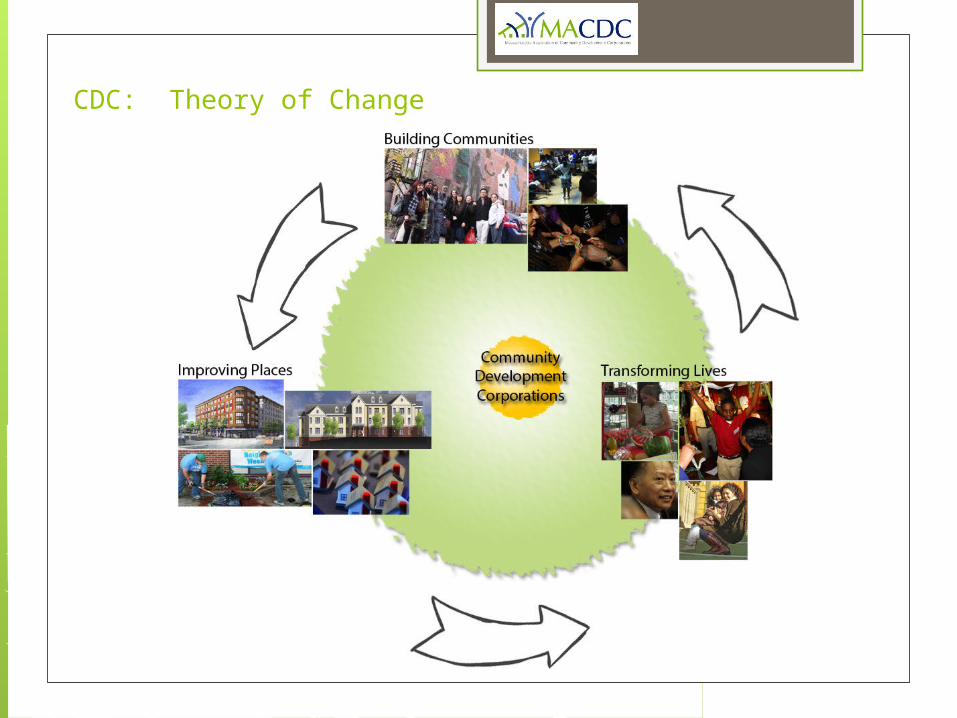

CDC: Theory of Change

CITC:Leverage Partnership & Collaboration

What does CITC provide? Authorizes DHCD to allocate the following to Certified

CDCs selected through a competition: • 2013: $750,000 in community investment grants• 2014: $3M in Community Investment Tax Credits• 2015-2019: $6M in Community Investment Tax

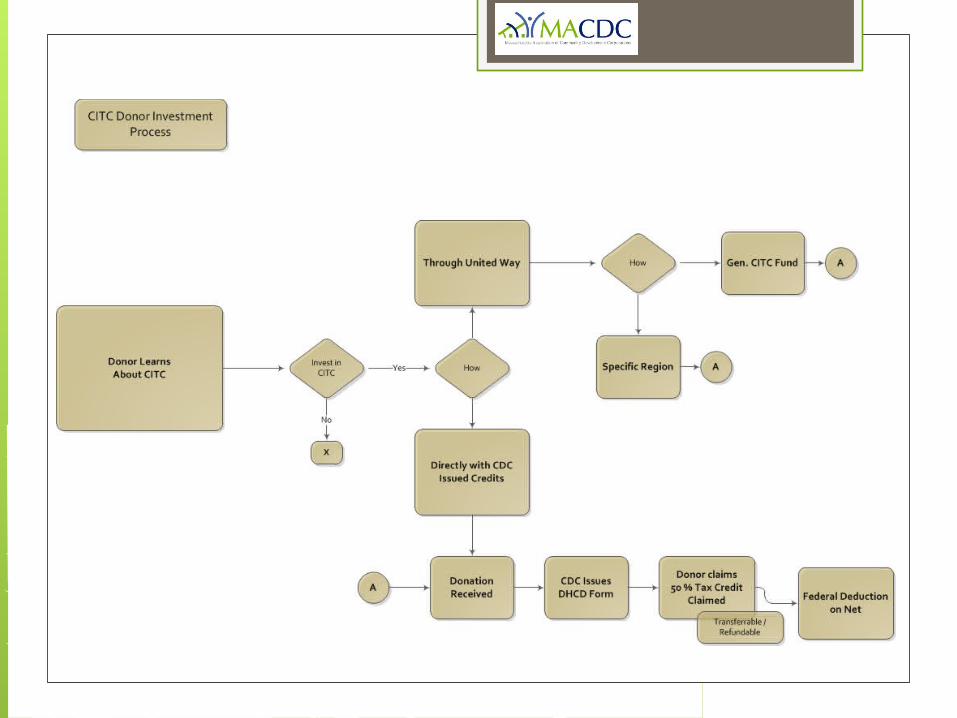

Credits annually Potential to generate $66 million over seven years Community Investment Tax credits provide a 50%

credit on donations to selected CDCs $50K to $150K in tax credits each year for 3 years 20% Rural, 30% Gateway Cities

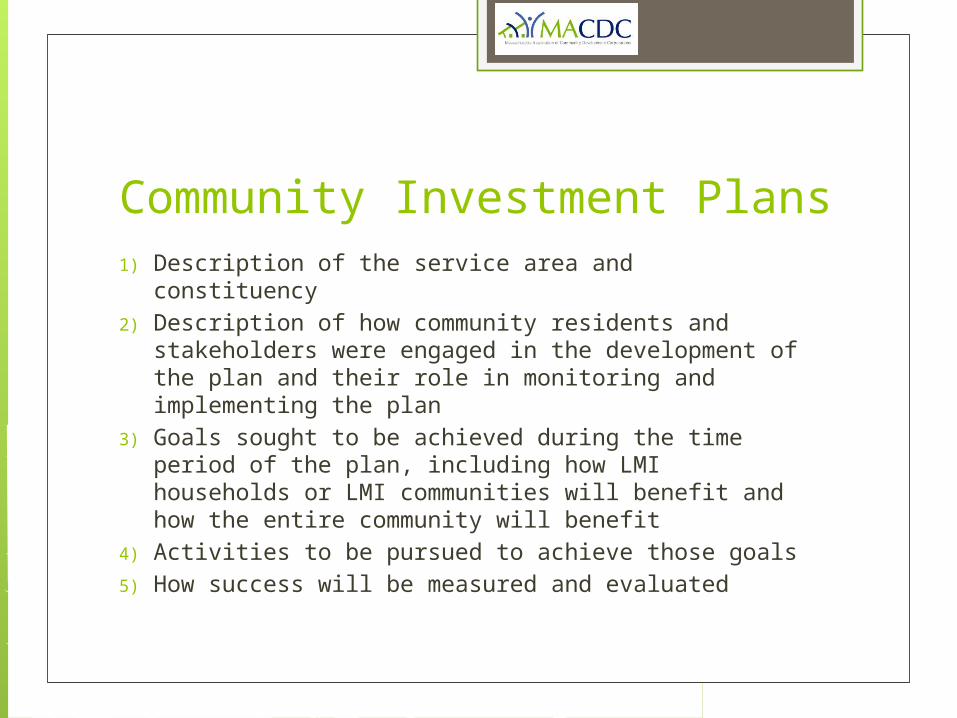

Community Investment Plans1) Description of the service area and constituency2) Description of how community residents and

stakeholders were engaged in the development of the plan and their role in monitoring and implementing the plan

3) Goals sought to be achieved during the time period of the plan, including how LMI households or LMI communities will benefit and how the entire community will benefit

4) Activities to be pursued to achieve those goals5) How success will be measured and evaluated

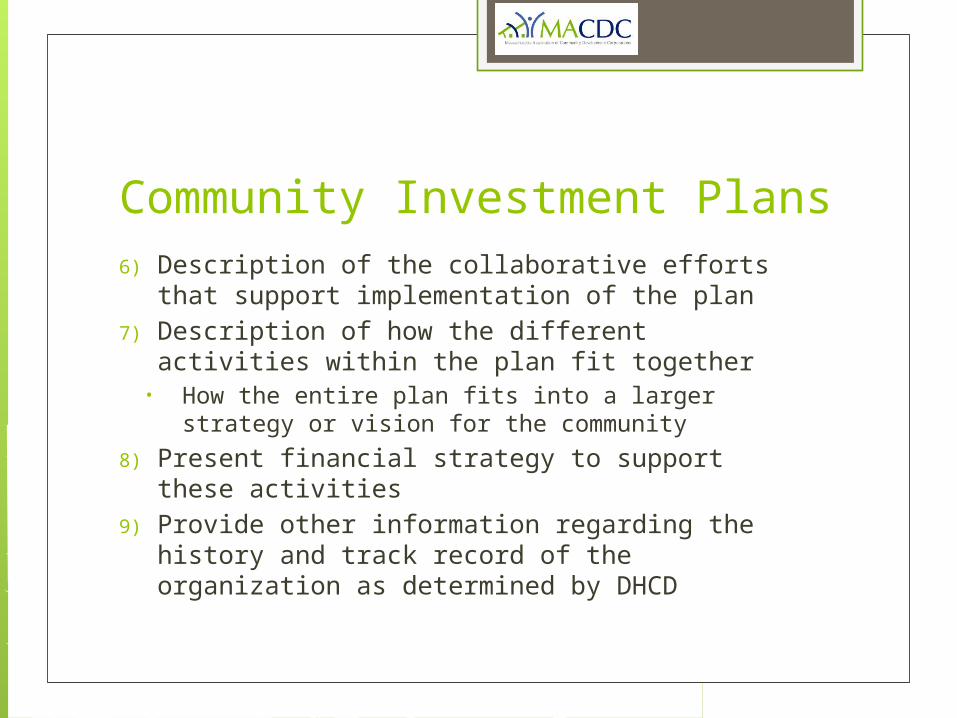

Community Investment Plans6) Description of the collaborative efforts that

support implementation of the plan 7) Description of how the different activities within

the plan fit together• How the entire plan fits into a larger strategy or

vision for the community

8) Present financial strategy to support these activities

9) Provide other information regarding the history and track record of the organization as determined by DHCD

CITC: Tax Savings Examples

(Illustration - 35% Tax Bracket)

Situations vary. Consult your tax advisor.

Minimum Donation Maximum Donation

$ 1,000 $ 2,000,000

Community Investment Tax Credit $ 500 $ 1,000,000

Federal Tax Deduction (35%) $ 175 $ 350,000

Total Tax Savings $ 675 $ 1,350,000

Final out-of-pocket donation $ 325 $ 650,000

Evaluation @ CDC level Community Mission Program Organizational Financial

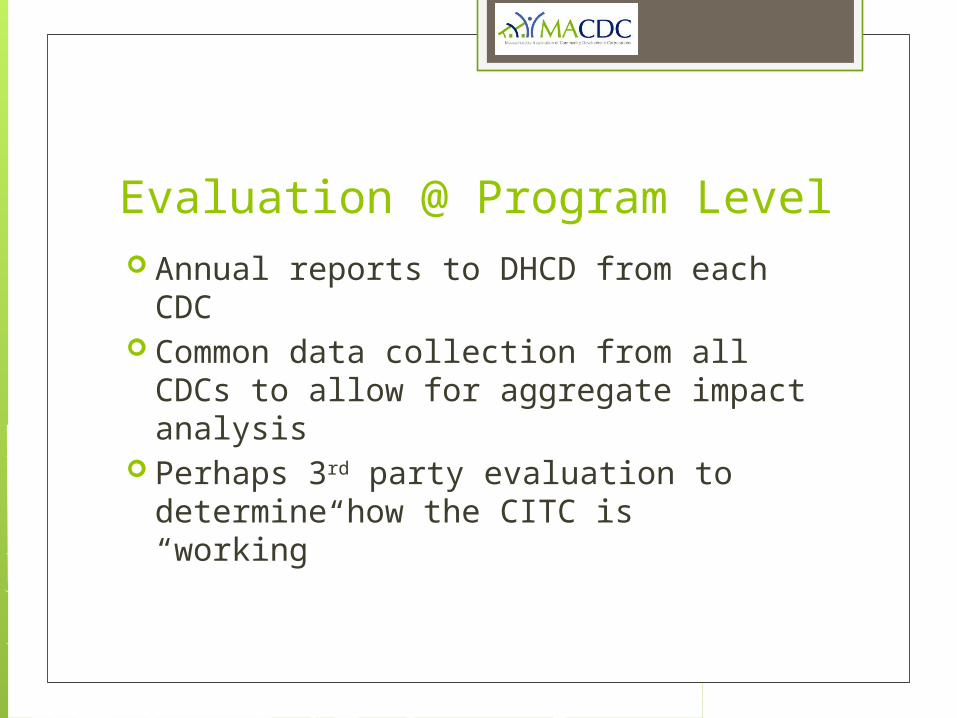

Evaluation @ Program Level Annual reports to DHCD from each CDC Common data collection from all CDCs

to allow for aggregate impact analysis Perhaps 3rd party evaluation to

determine how the CITC is “working”

What MACDC is doing Helping DHCD and DOR Educating potential donors Building the United Way Partnership Offering training through Mel King

Institute Providing 1-1 technical assistance to

CDCs

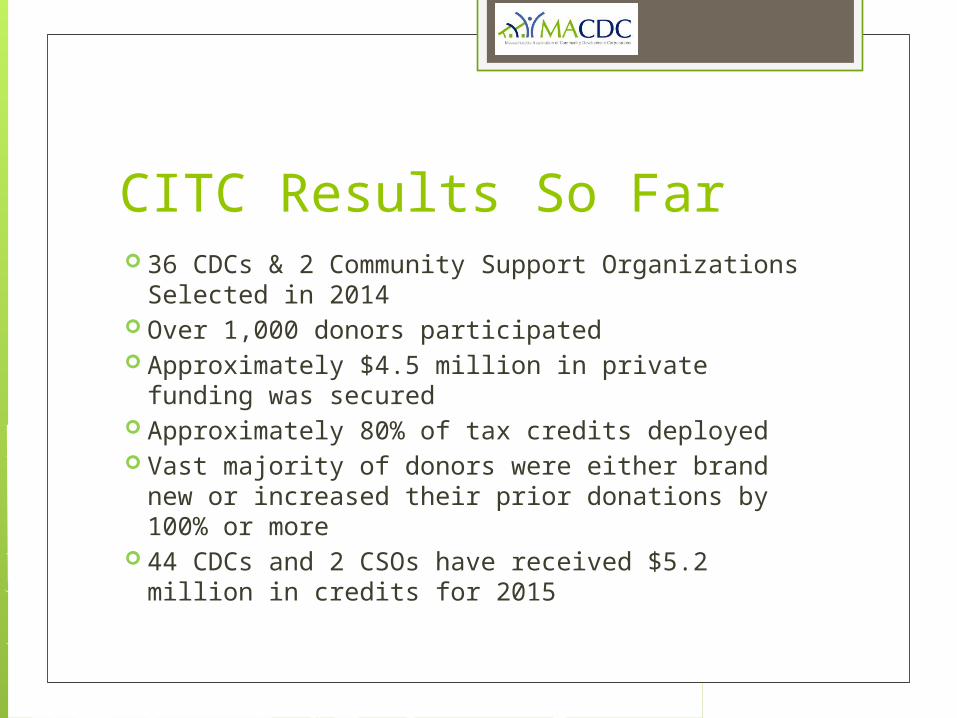

CITC Results So Far 36 CDCs & 2 Community Support Organizations

Selected in 2014 Over 1,000 donors participated Approximately $4.5 million in private funding was

secured Approximately 80% of tax credits deployed Vast majority of donors were either brand new or

increased their prior donations by 100% or more 44 CDCs and 2 CSOs have received $5.2 million

in credits for 2015

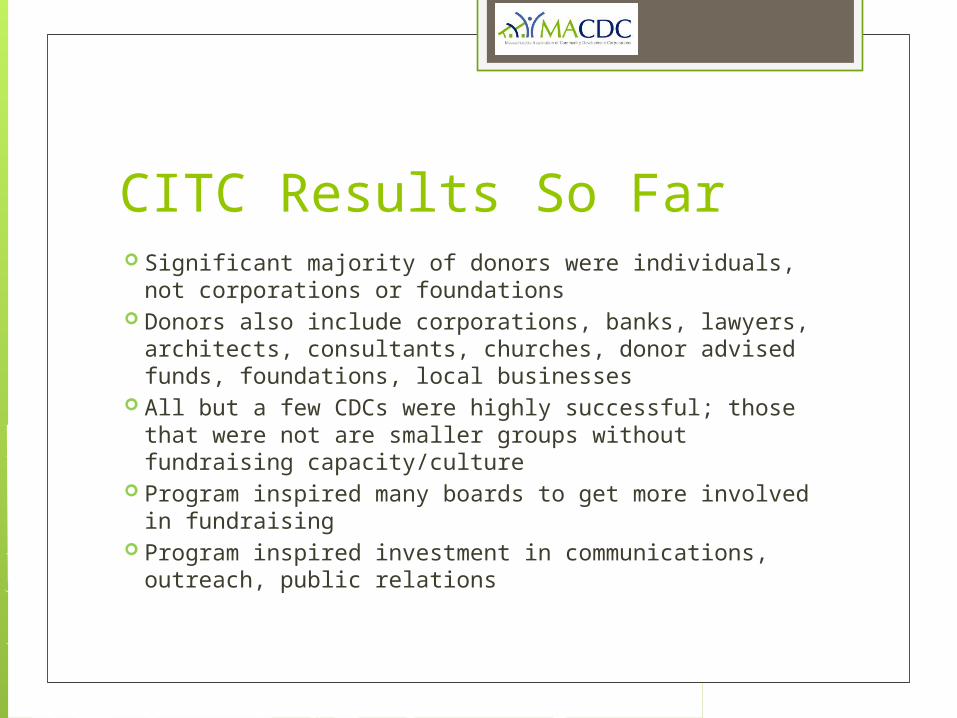

CITC Results So Far Significant majority of donors were individuals, not

corporations or foundations Donors also include corporations, banks, lawyers,

architects, consultants, churches, donor advised funds, foundations, local businesses

All but a few CDCs were highly successful; those that were not are smaller groups without fundraising capacity/culture

Program inspired many boards to get more involved in fundraising

Program inspired investment in communications, outreach, public relations

CITC Challenges Confusion regarding the fact that this is a donation

not an investment Slow roll out of rules & procedures Inadequate communication between/among state

agencies, United Way and program participants Slow & cumbersome processing of credits National Banks unwilling to respond to local

program Some donors think it is too good to be true Hard to break through gatekeepers Keeping the “CITC Promise”