the leading edgeanesthesianewsletter.ahsrcm.com/assets/sites/2/2016/07/... · 2016-07-07 ·...

TRANSCRIPT

SUMMER 2016 ISSUE

Welcome ....................................... 1

Documentation Updates for ICD-10 Specificity ..................................... 2

2016 ASA Quality Reporting Options ......................................... 6

Bundled Payments Arrive ........... 8

Perioperative Surgical Home and Professional Liability .................. 11

Prepare for more ICD-10 Codes and for Specificity Denials ......... 13

MIPS: an Introduction ................ 16

ACOs: Will Growth Continue? ...... 20

Price Transparency-Slow Progress ..................................... 26

How to Deal with Patient “Financial Hardship” .................................... 31

877 501 1611 | [email protected] | anesthesianewsletter.ahsrcm.com

THE LEADING EDGE

PERFORMANCE THAT MATTERS

THE LEADING EDGE

Welcome!

Welcome to the Summer edition of the Leading Edge.

In our first feature, we highlight the October updates to ICD-10: more codes and the “specificity” requirement. We have a companion piece with specific anesthesia documentation suggestions.

Next an update on bundled payments which are likely to affect many, if not most, anesthesiologists very soon. Then an update on 2016 ASA Quality Reporting options.

We also revisit Perioperative Surgical Homes and the impact they may have on professional liability.

In our other feature articles, we have an introduction to MIPS which we believe will be the Medicare measurements (plural, encompassing quality (replacing PQRS), cost (replacing VBM), clinical improvement (new) and advancing care information (replacing MU)) that most anesthesiologists and other physicians will need to report starting in 2017.

Related to that, in our “Did you Know” section, we summarize physician participation in PQRS during 2014. A surprising number of physicians did not participate. If that trend continues, they will face increasing Medicare payment penalties.

Next we look at recent ACO trends and some of the headwinds that the 1000 existing ACOs face.

Our Price Transparency article highlights the practical difficulties faced by consumers, insurers and providers. Despite many motivations, ready availability of good price information remains very limited.

In our Compliance Corner, we describe why it is important for practices and hospitals to have formal procedures to deal with patient financial hardship. Any other approach to waiving co-pays, deductibles, etc. is problematic from a legal and compliance perspective.

You can print any article in this newsletter as a PDF and there is a PDF “button” to download the entire newsletter for email or printing.

We appreciate your feedback and suggestions. Please call or email me with comments and topics: [email protected] and (908) 279-8120.

Bill Gilbert

877 501 1611 | [email protected] | anesthesianewsletter.ahsrcm.com 01

Documentation Updates for ICD-10 Specificity As noted in our ICD-10 feature, the CMS “flexibilities” published a year ago expire at the end of September. The key language from CMS is “While diagnosis coding to the correct level of specificity is the goal for all claims, for 12 months after ICD-10 implementation, Medicare … will not deny physician … claims … based solely on the specificity of the ICD-10 diagnosis code as long as the physician/practitioner used a valid code from the right family.” (emphasis added)

AdvantEdge has analyzed coding patterns for anesthesia clients to determine the types of situations that could lead to a denial after October 1. Fortunately, the proportion of claims affected appears to be relatively small, on the order of ten percent or less. But even that fraction would have significant financial impact.

As a result, we are issuing updated ICD-10 documentation guidance which highlights the most common situations where more specificity is required. The objective is to get all documentation up to the new standard before October in order to minimize denials.

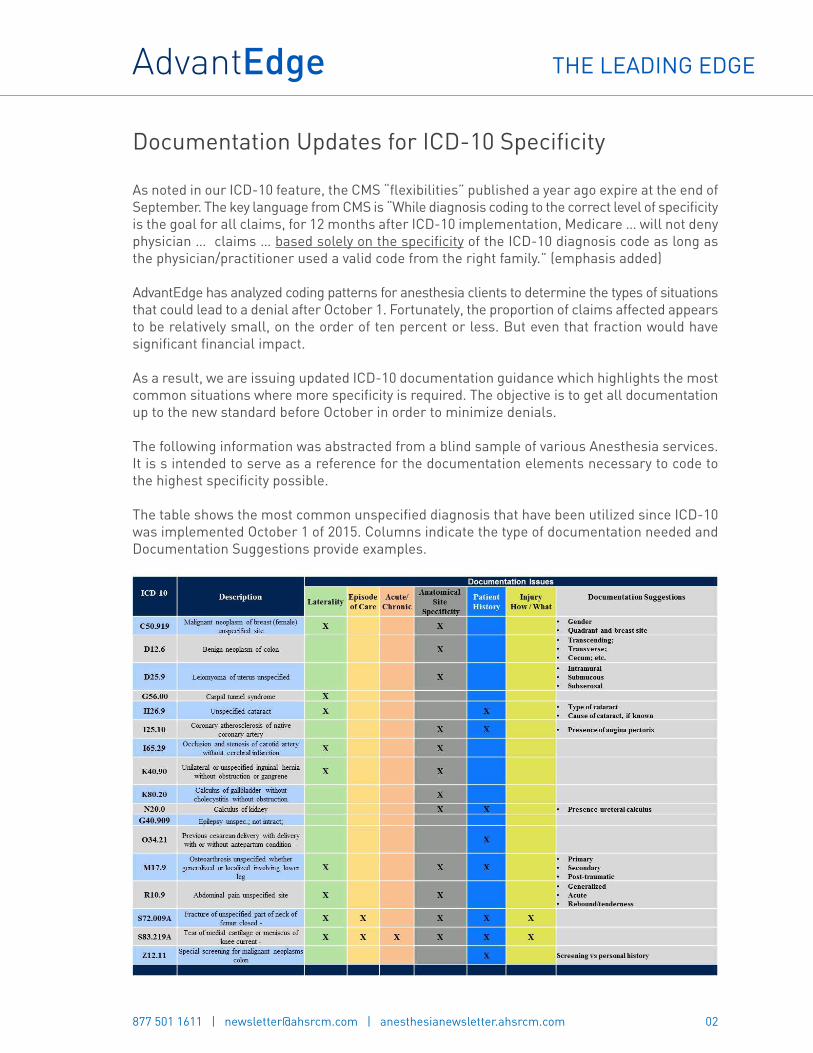

The following information was abstracted from a blind sample of various Anesthesia services. It is s intended to serve as a reference for the documentation elements necessary to code to the highest specificity possible.

The table shows the most common unspecified diagnosis that have been utilized since ICD-10 was implemented October 1 of 2015. Columns indicate the type of documentation needed and Documentation Suggestions provide examples.

02

THE LEADING EDGE

877 501 1611 | [email protected] | anesthesianewsletter.ahsrcm.com

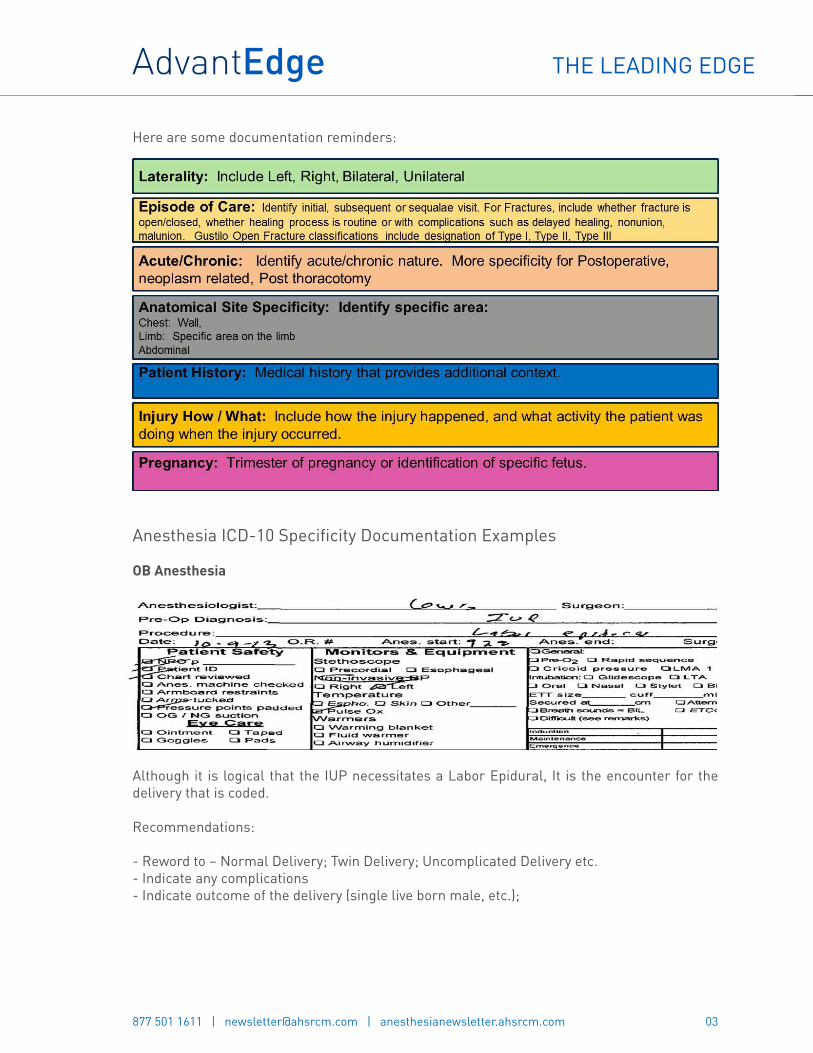

Here are some documentation reminders:

Anesthesia ICD-10 Specificity Documentation Examples

OB Anesthesia

Although it is logical that the IUP necessitates a Labor Epidural, It is the encounter for the delivery that is coded.

Recommendations:

- Reword to – Normal Delivery; Twin Delivery; Uncomplicated Delivery etc.- Indicate any complications- Indicate outcome of the delivery (single live born male, etc.);

03

THE LEADING EDGE

877 501 1611 | [email protected] | anesthesianewsletter.ahsrcm.com

Neoplasm

This patient is having a breast mass removed; however, in the pre-operative evaluation there is an indication of cancer and chemotherapy.

Neoplasms in ICD-10 require significant documentation details:

- Laterality; - R/L (as indicated here)- Anatomic location - Location on the breast, such as inner upper quadrant etc.;- Is the carcinoma the primary site, or secondary; - In this patient, is the breast primary? Or is it a metastases site?- The type of neoplasm - Is the breast mass benign or malignant?

Cardiac

For the pericardial tamponade, ICD-10 instructions note to code the underlying disease first;

Both diagnosis should be listed on the anesthesia record

04

THE LEADING EDGE

877 501 1611 | [email protected] | anesthesianewsletter.ahsrcm.com

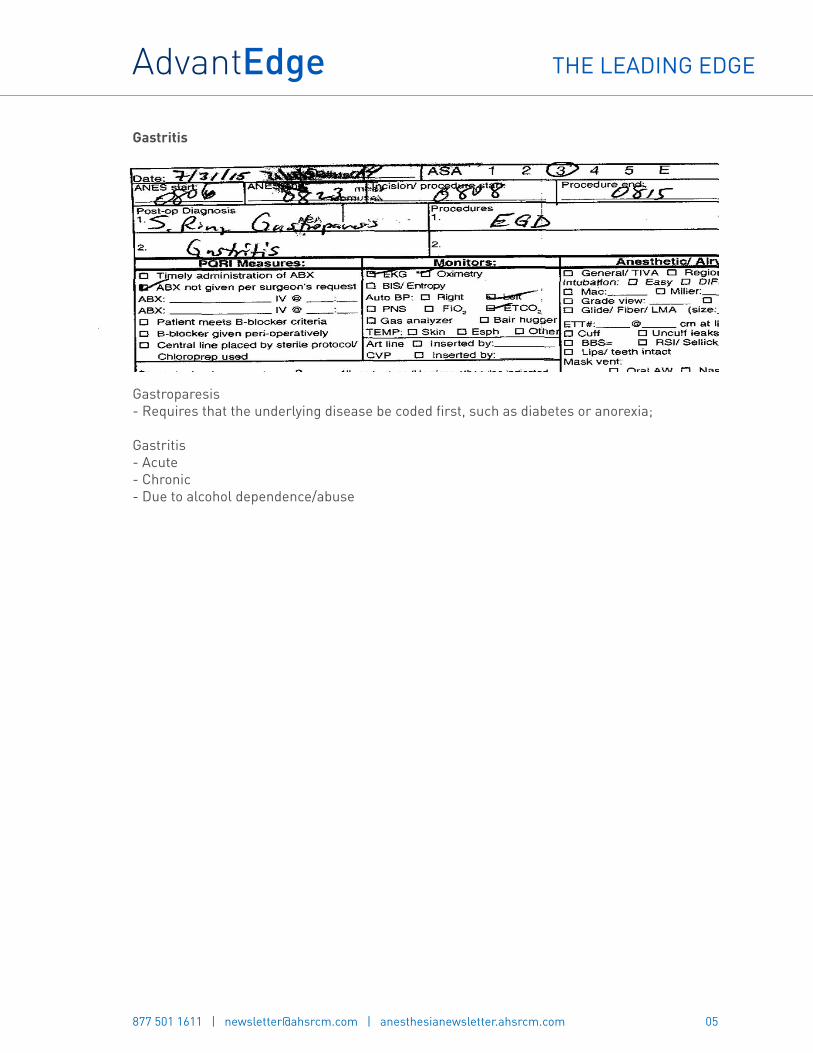

Gastritis

Gastroparesis- Requires that the underlying disease be coded first, such as diabetes or anorexia;

Gastritis- Acute- Chronic- Due to alcohol dependence/abuse

05

THE LEADING EDGE

877 501 1611 | [email protected] | anesthesianewsletter.ahsrcm.com

2016 ASA Quality Reporting Options

The Anesthesia Quality Institute (AQI) was established by the American Society of Anesthesiologist (ASA) to aid in facilitating quality management through education and quality data feedback.

ASA is offering two Quality reporting options for 2016, Qualified Registry (QR) and Qualified Clinical Data Registry (QCDR).

- The Qualified registry (QR) must report 9 individual PQRS measure covering at least3 National Quality Strategy domains (NQS). Reporting must include all Medicare PartB Fee for Service patients. A cross cutting measure is required for face-to-faceencounters. The types of measures are PQRS measures only.

- The Qualified Clinical Data Registry (QCDR) must report 9 PQRS measures and ASA/QCDR measures covering at least 3 NQS Domains plus 2 outcome Measures. Mustreport on all Medicare and Non-Medicare patients. No cross cutting measure is required.Types of measures to report are a combination of PQRS and ASA/QCDR measures.

For both reporting options an eligible profession must report on >50% of all eligible cases for 9 measures. If providers fail to report, it could result in up to a 6% reduction in payments.

Benefits to participate in National Anesthesia Clinical Outcomes Registry (NACOR QCDR):

- View performance vs. other participating groups- Identify Outliers- Access Educational Resources- Meet Regulatory Requirement

QCDR data must be submitted to AQI servers; this is the only way files will be accepted.

Up to this point in time, it has been technically complex to submit the AQI data. Effective in June 2016, AQI has outsourced its technical operation and data warehousing to ArborMetrix in Ann Arbor, MI. AQI will standardize file format requirements and move to XML as its standard format. It is hoped that this will reduce the technical complexity, though that remains to be seen.

Vendors must assess the current file format of all data files that are being submitted to NACOR. The AQI website publishes a list of NACOR minimum dataset vendors and QCDR vendors who meet the XML format for submission to AQI. AdvantEdge is considered Minimum Dataset Vendor.

ASA Quality Reporting service deadlines to report:

- October 31st, 2016: Registration for ASA Quality Reporting- One month of production data must be submitted to AQI within 60 days after contract signing.

06

THE LEADING EDGE

877 501 1611 | [email protected] | anesthesianewsletter.ahsrcm.com

- January 31st, 2017: Submission of January 2016 – November 2016 data- February 15th, 2017: Submission of December 2016 data

Facilities that are using EPIC may be able to create tables showing both PQRS and ASA/QCDR measure codes. When Providers document the flow sheet rows in EPIC they can be sent on the billing and compliance reports to AdvantEdge. AdvantEdge will then send the individual patient data to AQI. EPIC is currently working on being able to send data directly to AQI in XML format. This is projected to be ready mid to late summer 2016. Once EPIC is able to submit XML format, data can be configured to send files to AQI directly from the facility. The billing will then send the Minimum data requirement XML file to AQI. Both the billing and the facility would use a unique anesthesia identifier so that AQI can integrate the files with all of the information then captured.

For non- EPIC users, a paper form may also be used to capture the data.

07

THE LEADING EDGE

877 501 1611 | [email protected] | anesthesianewsletter.ahsrcm.com

—————————–Information submitted by Rebecca Carl, AdvantEdge – Dayton, OH

Bundled Payments Arrive

Bundled payment initiatives began as voluntary demonstration programs designed to coordinate care, lower costs, and improve outcomes. But they are becoming more common due to their potential to enhance care coordination and lower costs.

Anesthesia finds itself involved in the Medicare bundled payment for knee and hip replacements. In addition, some commercial payers continue to try to bundle anesthesia with common endoscopy center procedures, particularly colonoscopies. As an example, Aetna has tried to do so, or has done so, in some portions of New Jersey, Pennsylvania and Ohio. In the latter case, intensive push back from anesthesiologists and others has slowed, but not stopped the process.

Bundled Payments Expand

According to CMS More than 1,500 facilities nationwide are currently testing bundled payment innovation models.1 For Medicare, these numbers will continue to grow as the U.S. Department of Health & Human Services (HHS) forges ahead with its goal to tie 50 percent of all traditional or fee-for-service Medicare payments to quality or value through alternative payment models, such as accountable care organizations (ACOs) or bundled payment arrangements, by 2018.2

The first mandatory bundled payment program is the Comprehensive Care for Joint Replacement (CJR) Model.3 This model, which went into effect April 1, 2016, is designed to test bundled payment and quality measurement for hip and knee replacements in approximately 800 hospitals across 67 metropolitan service areas. Hospitals are required to participate in this bundle and are accountable for the quality and cost of the entire episode of care, including 90 days post-discharge.

Data from early bundled payment experience show that more than 80 percent of participating hospitals report improved patient engagement, reduced administrative costs, and increased alignment with physicians.4

08

THE LEADING EDGE

877 501 1611 | [email protected] | anesthesianewsletter.ahsrcm.com

—————————–[1] “Bundled Payments for Care Improvement (BPCI) Initiative: General Information,” CMS, Last updated April

29, 2016[2] U.S. Department of Health & Human Services, “Better, Smarter, Healthier: In Historic Announcement, HHS

Sets Clear Goals and Timeline for Shifting Medicare Reimbursements from Volume to Value,” Press Release,January 26, 2015

[3] “Comprehensive Care for Joint Replacement Model,” CMS, Last updated May 6, 2016[4] Ahlquist, Gary; Javanmardian, Minoo; Belokrinitsky, Igor; Porwal. Amika, “Infographic: Healthcare Bundles,”

Strategy&, PwC, March 7, 2014

Impact on Anesthesiologists

The impact of bundled payments on anesthesiologists can be significant. Some bundle models require physicians to negotiate payment arrangements directly with the hospital or hospitals included in the bundle. The hospitals—not the payers—then pay physicians accordingly.5

For the CJR, this is not the case. Physicians involved, including anesthesiologists, continue to be paid with traditional fee for service. However, when the time comes to distribute incentives and penalties, the hospitals involved will certainly want to include physicians, particularly if there are penalties!

If a practice is owned by or employed by a health system/hospital, the hospital can more easily negotiate a shared-savings arrangement and/or other mechanisms for participation in the bundle. Contracted groups need to create similar arrangements but the hospital may find it more complex. As a result, it is recommended that independent groups take a proactive approach with their hospitals involved in CJR.

Some hospitals have used a co-management approach in which any patient undergoing a surgery or admission automatically has a hospitalist consultation. A potential problem with this approach is that the hospitalist may duplicate testing that was performed prior to admission, driving up costs for the hospital while yielding minimal improvements in outcome.

A better option might be the perioperative surgical home (see our companion article) though that approach is far from commonplace.

With bundled payments top of mind for physicians and hospitals, it behooves practices to proactively establish an initial framework for CJR and position it as a foundation for other bundled payment arrangements and, ultimately, effective population health management.

A Bundled Payment Example

Missouri’s CoxHealth entered a voluntary bundled payment arrangement in 2014 with a primary goal of reducing readmissions.6 The five-hospital health system’s first bundled payment venture focused on two areas: pneumonia and respiratory infections. In 2015, CoxHealth voluntarily took on two additional bundles, congestive heart failure (CHF) and acute myocardial infarction (AMI). It implemented the joint replacement bundle including hip and knee replacements in April 2016.

Collaboration with physicians is essential when entering a bundled payment program, according to the health system. By effectively engaging physicians during voluntary bundled payment

09

THE LEADING EDGE

877 501 1611 | [email protected] | anesthesianewsletter.ahsrcm.com

—————————–[5] Curry, Angie; Fee, James, “Ramping Up for Bundled Payments: Fostering Alignment between Hospitals and

Physicians,” HFMA’s Healthcare Finance Strategies, May 1, 2016[6] Curry, Angie; Fee, James, “Ramping Up for Bundled Payments: Fostering Alignment between Hospitals and

Physicians,” HFMA’s Healthcare Finance Strategies, May 1, 2016

initiatives, a strong foundation for success was established as it expanded its bundled payment efforts.

CoxHealth believes the following three strategies for alignment and participation were key in their success:

1. Reiterate the Importance of Coded Data on Publicly Reported Outcomes – i.e. severity ofillness and risk of mortality, both of which can have a big impact on quality and outcomesmeasures.

2. Perform Peer-to-Peer Physician Education for Clinical Documentation – comprehensivetraining covering how to document thorough and complete history to accurately reflect riskadjustment.

3. Revamp Documentation Processes – Physician assistants and nurse practitioners shouldbe properly trained and prepared to assist orthopedic surgeons and other physicians withdocumentation when necessary.

10

THE LEADING EDGE

877 501 1611 | [email protected] | anesthesianewsletter.ahsrcm.com

Perioperative Surgical Home and Professional Liability

Given the increased responsibilities inherent in the perioperative surgical home (PSH) model, many have started to wonder if it will lead to an increase in legal vulnerabilities for anesthesiologists.

The PSH is an anesthesiologist-led practice model geared toward improving the quality, safety and cost of patient care. It was first proposed several years ago by the American Society of Anesthesiologists (ASA). Currently, a majority of patients move through distinct episodes of the perioperative process, including preoperative, intraoperative, postoperative and post-discharge care. On the other hand, the PSH treats the entire perioperative experience as a single continuum, with the anesthesiologist coordinating and managing all aspects of care.

While the PSH concept can be seen as a gain by anesthesiologists looking to expand their responsibilities, it does raise questions about whether existing professional liability policies are adequate.

The good news, according to experienced attorneys quoted by Anesthesiology News, is that safe migration into the PSH model is possible and a function of vigilance, preparation and communication.1

Professional Liability

Wade Willard, JD, vice president of claims at Preferred Physicians Medical, a Kansas-based company that provides professional liability insurance to anesthesiologist’s points out, “The PSH certainly represents an expanding role for anesthesiologists. And I think insurance companies will eventually need to adjust their underwriting to reflect this changing role and the potential losses that may follow.”

Although the specter of medical malpractice may be very real, it’s certainly no reason to be fearful of what may be a great opportunity, says Mark Weiss, principal of the Mark F. Weiss Law Firm in Los Angeles. “I think malpractice is a nonissue with respect to the PSH. It’s a nonissue because every single time a physician has an interaction with a patient, there’s a chance of being sued for malpractice.” Weiss continued “Assuming there is a way to make money and run a profitable practice being the point person of the PSH, then why wouldn’t an anesthesiologist want to do it?”

Weiss suggests there are three primary medical malpractice risks for anesthesiologists working within the PSH:

- First – possibility of lawsuit following an allegation regarding care delivery;- Second – Anesthesiologists belong to a profitable group face the indirect risk of one member

of the group being sued, affecting the entire group.

11

THE LEADING EDGE

877 501 1611 | [email protected] | anesthesianewsletter.ahsrcm.com

—————————–[1] Vlessides, Michael, “Does the Perioperative Surgical Home Model Affect Malpractice Coverage?” Anesthesiology

News, June 15, 2016

- Third – The notion of the “negligent referral—you were in charge, and as the point person inthe perioperative process, you brought in someone who wasn’t competent,” Weiss said. “Oryou should have brought in someone and you didn’t.”

Adjustments Necessary

Evolving responsibilities sometimes mean evolving insurance policies, Willard explains, “Anytime a specialty gets into an area that maybe they’re not normally exposed to, we’re always careful to remind them that this may represent a broader scope of practice and they need to adjust their approach to reflect this larger responsibility,” he continued. “You just can’t have the singular lens of anesthesiologists doing what they’ve always done.”

The answer, then, is communication between practitioners and the companies that insure them. “Anesthesiologists who are now in this role had better be sure that their malpractice policy describes these new activities as part of the practice of anesthesiology,” Weiss stated. “So you need to have a discussion with your insurance company to make them aware of what you’re doing. Because some policies will have exclusions, you want to make sure that what you’re doing doesn’t fall within an exclusion. In the end, you don’t want someone to say, ‘We thought you were an anesthesiologist but you weren’t being an anesthesiologist that day, so we’re not insuring you.’ You don’t want that to happen.”

PSH Evolution

Insurance companies also will need to determine their needs from an underwriting perspective. The good news, Willard said, is that changes such as these are evolutionary rather than revolutionary. “It’s not like tomorrow all anesthesiologists are going to be practicing in the PSH model,” he said. “It will likely start more in the academic institutions and work its way out. And during that time, insurance companies, anesthesiologists and the societies are all going to have a chance to look at how it’s working.”

“From a risk management perspective, it goes back to recognizing your changing role, making sure you feel comfortable in that role and determining if you need any additional training,” Willard offers. “The second part is from the insurance perspective. Companies want to be aware of, and have a discussion with, the practitioners that are going to be taking on the PSH role, especially these initial ones. It won’t necessarily change our relationship with them; we just want to be aware of it.”

Overall the experts agree that fear of the “what ifs,” should not deter anesthesiologists from performing responsibilities associated with the PSH. “That’s why you have malpractice insurance,” Weiss said and Willard agreed, adding. “I think the PSH is a way for anesthesiologists to make themselves more relevant and cement their place in the perioperative process.”

12

THE LEADING EDGE

877 501 1611 | [email protected] | anesthesianewsletter.ahsrcm.com

—————————–This article is for informational purposes only and not for the purpose of providing legal or insurance advice.

Prepare for more ICD-10 codes and for Specificity Denials

Most of us remember that a year ago, tremendous time, focus and resources were devoted to ICD-10. Fortunately those efforts were rewarded as the October 1 transition went smoothly.

One factor that helped was a set of “flexibilities” issued by CMS and the AMA in early July. The key language from CMS is “While diagnosis coding to the correct level of specificity is the goal for all claims, for 12 months after ICD-10 implementation, Medicare … will not deny physician … claims … based solely on the specificity of the ICD-10 diagnosis code as long as the physician/practitioner used a valid code from the right family.” (emphasis added)

With October of 2016 rapidly approaching, it is now time to prepare for a world where Medicare will deny a claim based on insufficient specificity of the ICD-10 diagnosis code. In fact, ICD10Watch reports that some coders are seeing “private healthcare payers increasing specificity requirements slowly.” Of course, private payers were never required to follow the CMS flexibilities though they generally have.

The same publication also points out that where specificity is required for medical necessity, it has always been required. According to Denise Williams, senior vice president of revenue integrity services at Revant Solutions, “If there is a specific code required to support medical necessity, then all characters of the code must be accurate to meet medical necessity.”

New and Revised ICD-10 Codes

In addition, a large number of new ICD-10 codes plus changes to codes and to instructions are coming October 1 when the “FY2017 code set” goes into effect. On June 22, CMS published the final addenda list, including an updated tabular, alphabetic index, neoplasm table, table of drugs and chemicals and index of external causes.

This major update is the end of a five-year code freeze. As a result, it picks up a long list of changes discussed at biannual ICD-10 Coordination and Maintenance Committee meetings over the past 5 years.

The Oct. 1 changes include 1,974 new codes, 311 deleted codes and 425 revised codes. The biggest impacts include Chapter 4 (Endocrine, nutritional and metabolic diseases), Chapter 13 (Diseases of the musculoskeletal system and connective tissue) and Chapter 19 (Injury, poisoning and certain other consequences of external causes).

Additionally, the final changes include a myraid of changes to Tabular instructions.

Specificity

AdvantEdge has analyzed coding patterns for our major specialties to determine the types of situations that could lead to a denial after October 1. Fortunately, the proportion of claims

13

THE LEADING EDGE

877 501 1611 | [email protected] | anesthesianewsletter.ahsrcm.com

affected appears to be relatively small, on the order of ten percent on average. But even that fraction would have significant financial impact.

As a result, we are issuing updated ICD-10 documentation guidance which highlights the most common situations where more specificity is required. The objective is to get all documentation up to the new standard before October in order to minimize denials.

Some common examples include:

- Chest Pain Unspecified (R07.9)- Fever Unspecified (R50.9)- Diarrhea Unspecified (R19.7)- Disorder of the bone Unspecified (M89.9)- Pain in Leg Unspecified (M79.606)- Asthma Unspecified (J45.901)

In our specialty sections you will find specific guidance for:

- Anesthesia- Emergency Medicine- Pathology- Radiology

For practices that do their own diagnosis coding, the following tips may help.

1. Comprehensive Training

Ensuring that providers and employees involved in coding are sufficiently trained in ICD-10, e.g.

- Know ICD-10 for common conditions for your specialty and access to necessary resourcematerial

- Appropriate and complete clinical documentation practices- Understand the guidelines that drive code selection.

2. Help referring and referral physicians

One of the primary challenges specialty practices face is the quality of the data that the referring physician / technologist passes on to the specialist. Referring physicians and technologists must provide enough specific information so the specialty physicians can include the details in their report.

Physicians must state the diagnosis as specifically as they can, while also being sure to link conditions when needed. If the reason for the condition is known including it can lead to a more specific diagnosis.

3. List All Treated Diagnoses

When assigning ICD-10 codes, you should first code the main or most serious diagnosis, which is typically determined as follows:

14

THE LEADING EDGE

877 501 1611 | [email protected] | anesthesianewsletter.ahsrcm.com

- The primary reason for the encounter-or-- The condition with the highest risk of morbidity/mortality that the physician is

addressing during this encounter

After the primary diagnosis, then list additional diagnoses describing other conditions that the patient has. “Code all documented conditions that coexist at the time of the encounter/visit, and require or affect patient care treatment or management,” the ICD-10 manual states. “Do not code conditions that were previously treated and no longer exist. However, history codes (Z80-Z87) may be used as secondary codes if the historical condition or family history has an impact on current care or influences treatment.”

15

THE LEADING EDGE

877 501 1611 | [email protected] | anesthesianewsletter.ahsrcm.com

MIPS – An Introduction

In late April, CMS released its proposed rule to implement the 2015 Medicare Access and CHIP Reauthorization Act (MACRA)–all 962 pages of it! The proposed rule links Medicare payments to quality patient care through a framework called the “Quality Payment Program.” It has two paths:

1. The first path, Advanced Alternative Payment Models (APMs), would include someACOs and other capitated programs. APMs are structures that can receive up to a5% annual Medicare incentive payment. But CMS anticipates that most Medicareclinicians will initially participate through MIPS, instead of APMs.1

2. The second option, The Merit-based Incentive Payment System (MIPS), consolidatesthe Physician Quality Reporting System (PQRS), the Value-based Payment Modifier(VBM), and the Medicare Electronic Health Record (EHR) Incentive Program.

The rest of this article focuses on MIPS since most physicians will be included.

Who is Eligible?

According to CMS, Eligible clinicians (as opposed to “eligible professionals,” or EPs) include physicians, physician assistants (PAs), nurse practitioners (NPs), clinical nurse specialists (CNS), certified registered nurse anesthetists (CRNAs), and groups that include such physicians.

Budget Neutrality

The law requires MIPS to be budget neutral, which means no new money is being freed up to pay bonuses. MIPS will allocate penalty money from providers who score low to pay incentive bonuses to providers who score high. Clinicians’ MIPS scores would be used to compute a positive, negative, or neutral adjustment to their Medicare payments.

One exception to budget neutrality is that for the first 5 years of the program, Congress has allocated $500 million to pay “exceptional performance bonuses” for those EPs whose MIPS scores are exceptionally high, thereby allowing those EPs to earn an additional 10%. This means that in the 4th and 5th years of the program, EPs could earn a 19% bonus (9% regular and 10% exceptional).4

16

THE LEADING EDGE

877 501 1611 | [email protected] | anesthesianewsletter.ahsrcm.com

—————————–[1] “Notice of Proposed Rule Making Medicare Access and CHIP Reauthorization Act of 2015 Quality Payment

Program,” CMS, April 28, 2016[2] “FYI Synopsis of MIPS Proposed Rule,” Vaughn & Associates, May 2, 2016[3] “FYI Synopsis of MIPS Proposed Rule,” Vaughn & Associates, May 2, 2016[4] “Notice of Proposed Rule Making Medicare Access and CHIP Reauthorization Act of 2015 Quality Payment

Program,” CMS, April 28, 2016

Percentage of Payments/Penalties

In the first MIPS performance year – 2017, the incentive/penalty (paid in 2019) will be capped at 4%, but it will grow 1-2% each year. As a result, in 5 years the incentive/penalty will be as large as 9%.5 CMS will begin measuring performance for doctors and other clinicians through MIPS in January 2017, with payments based on those measures beginning in 2019.

MIPS Scoring

An EP’s MIPS Composite Score (i.e., total score) is based on 4 performance categories, the combined percentage of which total 100%.6

Quality – 50% of total score in the first year; 30% by year 3

- Replaces PQRS and the quality component of the Value Modifier Program.- Clinicians choose six measures versus the nine currently required under PQRS.- Allows reporting options to accommodate differences in specialty and practices. - Reporting can be via claims (for some measures), qualified registries, QCDRs, EHRs,- and web reporting (for large groups).

Advancing Care Information – 25% of total score in the first year

- Replaces the Medicare EHR Incentive Program for physicians, also known asMeaningful Use.

- Clinicians choose to report customizable measures that reflect how they use EHRtechnology in their day-to-day practice, with a particular emphasis on interoperabilityand information exchange.

- Different than the existing MU program, this category would not require all-or-nothingEHR measurement or quarterly reporting.

Clinical Practice Improvement Activities – 15% of total score in the first year

- Clinicians would be rewarded for clinical practice improvement activities such asactivities focused on care coordination, beneficiary engagement, and patient safety.

- Clinicians may choose measures from more than 90 activities in 9 different categories.- In this category, clinicians would receive credit for participating in APMs and in

Patient-Centered Medical Homes.

Costs – 10% in the first year, but rises to 30% in year 3

- Replaces the cost component of the Value Modifier Program, also known as Resource Use.- The score would be based on Medicare claims. Clinicians do not need to report

17

THE LEADING EDGE

877 501 1611 | [email protected] | anesthesianewsletter.ahsrcm.com

—————————–[5] “CMS Releases Proposed Rule on MACRA Implementation,” HBMA Washington Report, April Issue[6] “FYI Synopsis of MIPS Proposed Rule,” Vaughn & Associates, May 2, 2016

—————————–[7] “Notice of Proposed Rule Making Medicare Access and CHIP Reauthorization Act of 2015 Quality Payment

Program,” CMS, April 28, 2016[8] “Notice of Proposed Rule Making Medicare Access and CHIP Reauthorization Act of 2015 Quality Payment

Program,” CMS, April 28, 2016

anything, CMS will do its own calculations on costs.- This category would use more than 40 episode-specific measures to account for

differences among specialties.

Points versus Percentages

While Quality counts for 50% of the MIPS Composite Score, there are 80-90 maximum points one can earn, depending on the group size, within that category. Likewise, the Advancing Care Information category is worth only 25% of the MIPS Composite Score, yet that category has 100 possible points. Clinical Practice Improvement Activities is worth 15% of the MIPS Composite Score, yet it has 60 possible points. The number of points scored in each category will determine how much of the maximum is achieved. In general, it appears that CMS is establishing a system to “grade on the curve” with many practices likely to be in the middle, meaning a small net incentive or penalty. Of course, those who score near the top of the curve will receive the maximum incentive.

Provisions Related to Public Reporting and Transparency7

Continuing efforts towards transparent information and patient-centered care, and to help patients make informed choices, the results of the Quality Payment Program/MIPS scores, including aggregate and individual scores for each performance category, will be publicly available on the Physician Compare website.

The law requires public reporting of the following information:

- Names of clinicians in Advanced APMs- As feasible, the names and performance of Advanced APMs- MIPS scores for clinicians, including aggregate and individual scores for each

performance category.

Consistent with current Physician Compare policies for the Physician Quality Reporting System and the Medicare EHR Incentive program, there has been a proposal for a 30-day preview period in advance of the publication of any data on Physician Compare. Clinicians would be able to review and submit corrections prior to any information being made public.8

18

THE LEADING EDGE

877 501 1611 | [email protected] | anesthesianewsletter.ahsrcm.com

—————————–[9] Belliveau, Jacqueline, “AMA Releases Value-Based Care, MACRA Resources for Providers,” RevCycleIntelligence,

May 2, 2016

Proposed -vs- Final Rule

The Final Rule will be published later this year, most likely in November, with MIPS and APMs going into effect January 1st, 2017. Reporting in 2017 will determine payments/penalties two years in 2019.

In response to the proposed rulemaking, AMA commended CMS for eliminating meaningful use and reducing quality reporting. It also gave the federal agency suggestions about the future of value-based payment models.9

“Our initial review suggests that CMS has been listening to physicians’ concerns,” said Steven J. Stack, MD, AMA President, in an official press release. “In particular, it appears that CMShas made significant improvements by recasting the EHR Meaningful Use program and byreducing quality reporting burdens.”

“The existing Medicare pay-for-performance programs are burdensome, meaningless and punitive. The new incentive system needs to be relevant to the real-world practice of medicine and establish meaningful links between payments and the quality of patient care, while reducing red tape.”

At the same time, many of those preparing to comment on the proposed rule don’t think CMS has gone far enough in reducing the burden on physicians from quality reporting. As a result, it is likely that the final rule will tweak some of the details. But no one expects it to be fundamentally different since the basic framework was set in the 2015 MACRA legislation.

19

THE LEADING EDGE

877 501 1611 | [email protected] | anesthesianewsletter.ahsrcm.com

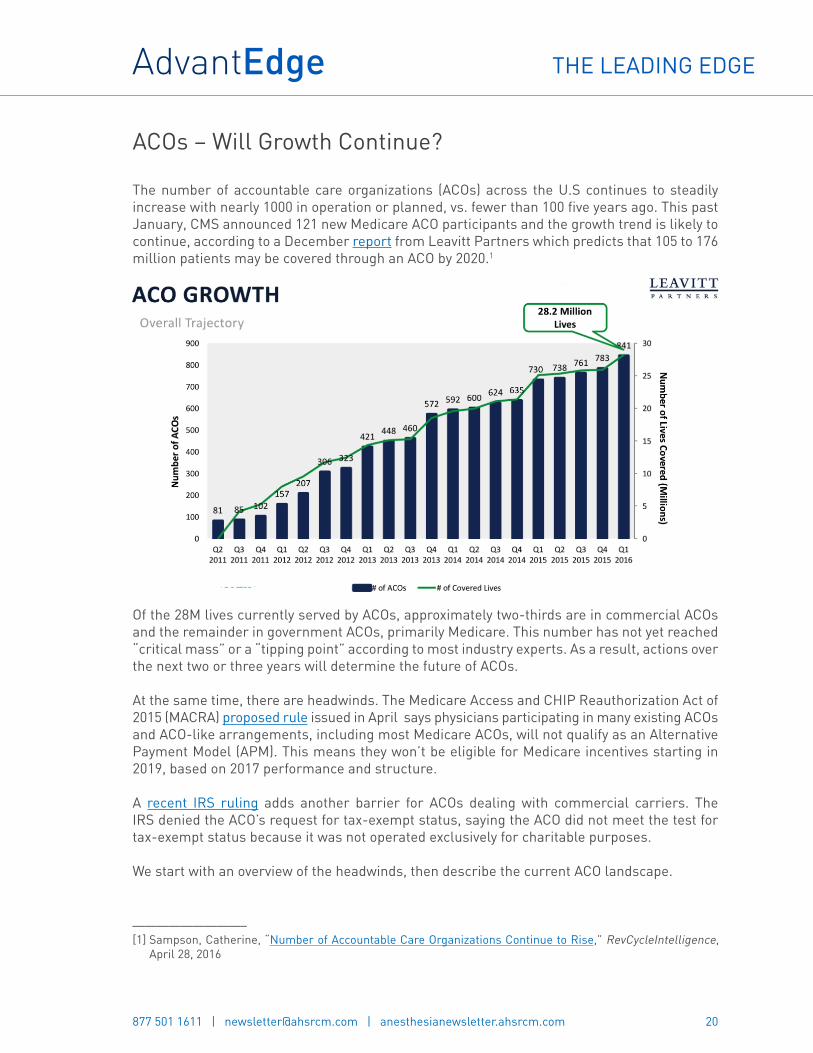

ACOs – Will Growth Continue?

The number of accountable care organizations (ACOs) across the U.S continues to steadily increase with nearly 1000 in operation or planned, vs. fewer than 100 five years ago. This past January, CMS announced 121 new Medicare ACO participants and the growth trend is likely to continue, according to a December report from Leavitt Partners which predicts that 105 to 176 million patients may be covered through an ACO by 2020.1

Of the 28M lives currently served by ACOs, approximately two-thirds are in commercial ACOs and the remainder in government ACOs, primarily Medicare. This number has not yet reached “critical mass” or a “tipping point” according to most industry experts. As a result, actions over the next two or three years will determine the future of ACOs.

At the same time, there are headwinds. The Medicare Access and CHIP Reauthorization Act of 2015 (MACRA) proposed rule issued in April says physicians participating in many existing ACOs and ACO-like arrangements, including most Medicare ACOs, will not qualify as an Alternative Payment Model (APM). This means they won’t be eligible for Medicare incentives starting in 2019, based on 2017 performance and structure.

A recent IRS ruling adds another barrier for ACOs dealing with commercial carriers. The IRS denied the ACO’s request for tax-exempt status, saying the ACO did not meet the test for tax-exempt status because it was not operated exclusively for charitable purposes.

We start with an overview of the headwinds, then describe the current ACO landscape.

20

THE LEADING EDGE

877 501 1611 | [email protected] | anesthesianewsletter.ahsrcm.com

—————————–[1] Sampson, Catherine, “Number of Accountable Care Organizations Continue to Rise,” RevCycleIntelligence,

April 28, 2016

MACRA: Qualifying as APMs

The Medicare Access and CHIP Reauthorization Act of 2015 (MACRA) proposed rule estimated that as few as 30,000 physicians could qualify initially for APM payments, which are seen as more lucrative with less-burdensome quality reporting, compared with the alternative Merit-based Incentive Payment System (MIPS) track.

The proposed rule says only the following APMs will qualify participating physicians for bonus payments and exemption from MIPS reporting:2

- Comprehensive Primary Care Plus (CPC+)- Next Generation ACO- Medicare Shared Savings Program (MSSP) Tracks 2 and 3- Oncology Care Model with two-sided risk- Comprehensive ESRD Care (for large dialysis organizations)

Although the proposed rule states that CMS will continue to add to the list of qualifying APMs, bundled payment programs and Track 1 MSSP ACOs were not initially included. 95% of the 434 MSSP ACOs are in Track 1, according to a CMS official, and participating physicians would not qualify for APM payments. In addition, physicians participating with approximately 800 hospitals in the Comprehensive Care for Joint Replacement (CJR) model also would not qualify for APM payments.

A release from U.S. Department of Health and Human Services (HHS) acknowledged a number of physicians who participate in existing APMs will not qualify for MACRA bonus payments. As an alternative, the proposed rule aimed to offer them financial rewards within MIPS “to make it easy for clinicians to switch between the components of the Quality Payment Program based on what works best for them and their patients,” the release stated. HHS officials noted that they expect most Medicare clinicians to initially participate in MIPS.

The preliminary appeal of the APM track for physicians was the accompanying 5% annual bonus which provides a more generous annual update through 2024 than that available through MIPS.

At the same time, its worth noting that the proposed rule also established three financial risk criteria that APM participants need to meet:

- Marginal risk of at least 30%- Minimal loss rate of no more than 4%- Total potential risk of at least 4% of expected expenditures

21

THE LEADING EDGE

877 501 1611 | [email protected] | anesthesianewsletter.ahsrcm.com

—————————–[2] Daly, Rich, “Many Existing APMs Excluded under Proposed Physician Pay Rules,” HFMA, April 28, 2016

—————————–[3] 3. RBMA Radiology Hot Topics February 3-10, 2016 (pdf)

Impact of Proposed APM Rules

According to a NAACOS survey, if the proposed APM requirements are finalized, 56% of Medicare ACOs are likely to leave the MSSP, which hosts the vast majority of Medicare ACOs. 11% of such ACOs were unsure whether they would remain in the program and 32% said it was very or somewhat likely that they would stay in the program (with 2% of respondents ineligible to remain in Track 1).

In a poll conducted in February by RBMA,3 77% of the 94 respondents reported they are not participating in an ACO. Nearly two-thirds of these respondents (63%) indicated they are not currently participating in an ACO and have no intention of ever participating, while an additional 14% reported they are not currently participating, but are considering doing so in the future. Of the remaining 23% currently participating in an ACO, almost 10% have achieved shared savings while 14% have not. The results are noticeably similar to those of an August 2013 poll, which found 74% were not participating in an ACO (with 23% considering doing so) and 26% actively participating, including only 5% that had achieved shared savings and 21% that had not.

IRS Ruling Impact

While the recent IRS ruling does not apply to Medicare-only ACOs, it is expected to slow ACO growth unless the ruling is overturned. Especially considering that two-thirds of ACOs to date are commercial. ACO advocates expect that some members of Congress may propose legislation to create a more favorable tax status for commercial ACOs. Certainly commercial insurers and others involved with these ACOs will be lobbying to change the ruling. Otherwise, many feel that the tax implications will prevent the formation of new ACOs and may even cause existing ones that are struggling to disband.

Types of ACOs

According to Leavitt Partners and Stephen M. Shortell PhD, MPH, MBA of the Berkeley School of Public Health, there are 6 major types of ACOs, three that are health system or hospital-centric and three that are physician-centric:

- Full Spectrum Integrated- Hospital Alliance- Independent Hospital- Independent Physician Group- Physician Group Alliance- Expanded Physician Group

According to a recent Leavitt Partners survey, the first 2 types have, on average, many more

22

THE LEADING EDGE

877 501 1611 | [email protected] | anesthesianewsletter.ahsrcm.com

affiliated physicians and a higher percentage of employed physicians vs. the other types.

As a general rule, the physician types are more nimble, allowing them to move faster. In early studies, they have also shown the most success in cost savings. Some think this may be because hospital-centric ACOs face a conflict between keeping people out of the hospital (a major source of cost savings) and their traditional revenue stream from in-patients.

ACO Performance

The New England Journal of Medicine’s recent study “Early Performance of Accountable Care Organizations in Medicare,” assessed the early performance of MSSP ACOs.4 The study used Medicare claims from 2009 through 2013 and a difference-in-differences design. Researchers compared changes in spending and performance on quality measures from before the start of ACO contracts to after the start of the contracts. The scope included the 220 ACOs entering the MSSP in mid-2012 (2012 ACO cohort) or January 2013 (2013 ACO cohort) and those served by non-ACO providers (control group), with adjustment for geographic area and beneficiary characteristics. Researchers analyzed the 2012 and 2013 ACO cohorts separately because entry time could reflect the capacity of an ACO to achieve savings, and then compared ACO savings according to organizational structure, baseline spending, and concurrent ACO contracting with commercial insurers.

The study’s findings showed greater savings in independent primary care groups than in hospital-integrated groups. The first full year of MSSP contracts directly associated with early reductions in Medicare spending among 2012 entrants, but not among the 2013 entrants. Adjusted Medicare spending and spending trends were similar in the ACO cohorts and the control group during the pre-contract period. In 2013, the differential change in total adjusted annual spending was −$144 per beneficiary in the 2012 ACO cohort as compared with the control group, consistent with a 1.4% savings, but only −$3 per beneficiary in the 2013 ACO cohort as compared with the control. Estimated savings were consistently greater in independent primary care groups than in hospital-integrated groups among 2012 and 2013 MSSP entrants. MSSP contracts were associated with improved performance on some quality measures and unchanged performance on others.

A recent Dartmouth Institute for Health Policy and Clinical Practice study found Medicare ACOs have modest savings in the use of high-cost care such as hospitals (including emergency departments) and skilled nursing facilities. On average, study ACOs saved $136 per beneficiary through better coordination of care. But, savings were $456 per beneficiary for “clinically vulnerable” patients (those treated for three or more conditions). Not surprisingly, this highlights the importance for ACOs of coordinating care for those who have the most medical needs. The study can be seen at this link.

23

THE LEADING EDGE

877 501 1611 | [email protected] | anesthesianewsletter.ahsrcm.com

—————————–[4] McWilliams, J. Michael; Hatfield, Laura A; Chernew, Michael E; Landon, Bruce E; Schwartz, Aaron L., “EarlyPerformance of Accountable Care Organizations in Medicare,“ New England Journal of Medicine, April 13, 2016DOI: 10.1056/NEJMsa1600142

Need for ACOs: Lack of Coordinated Care

A recent Nielsen Strategic Health Perspectives survey highlights some of the problems that ACOs are trying to solve:

- Eighty-nine percent of primary care physicians say they often remind patients about preventivescreenings, but only 14 percent of patients say they get these reminders.

- More than two-thirds of adult Americans are overweight or obese, yet only 5 percent of patientsreport that their physicians recommended a weight loss program.

- Only half of patients are experiencing physicians who better know their history, primarily dueto the ability to share information through electronic medical records.

- Patients with multiple chronic illnesses, who would most benefit from care coordination,receive only slightly more follow-ups and care management as everyone else.

- Only about one-third have 24/7 access to care through their physician’s office other than theemergency room.

ACO Examples

To be successful, ACOs must adhere to the principles of strong philosophical alignment with top management, shared long-term objectives, aligned incentives, transparency and resource commitment, says Blue Shield of California CEO Paul Markovich.5 He adds there must be a strong belief in these principles from top management and among the ACO’s partners. Trust between providers and a payer is also an important factor and begins with all stakeholders truly wanting to deliver the best quality healthcare for the lowest price. Once trust is established, Markovich says, shared data analytics and payer-provided resources can add to an ACO’s success.

In Arizona, Sonora Quest Laboratories, a joint venture owned by Banner Health and Quest Diagnostics Incorporated, has been working to fully integrate the laboratories of the University of Arizona Health Network with those of Sonora Quest and Laboratory Services of Arizona- the Banner inpatient lab organization. Banner Health participates in multiple ACOs and has been successful with Medicare’s Pioneer ACO program. In a recent keynote, President and CEO David A. Dexter discussed how Sonora Quest Laboratories is changing in the ways needed to support physicians delivering care to ACO patients.6

Dexter emphasized the importance for all lab organizations to understand the “Triple Aim of CMS” in order to succeed during the ongoing transformation of healthcare; i.e.

1. Improve population and community health;2. Seamless coordination of care; and,3. Reduce per capita costs through improvement.

24

THE LEADING EDGE

877 501 1611 | [email protected] | anesthesianewsletter.ahsrcm.com

—————————–[5] Moody, Katherine, “Blue Shield Of California CEO: ACO Success Happens When You ‘Stick To The Principles‘,”

FierceHealthPayer, May 10, 2016[6] Michel, Robert, “At Executive War College 2016, Two Big Lab Market Trends,” Dark Intelligence Group Vol.

XXIII, No. 6, May 2, 2016

“ACOs need data analytics in real time that is delivered to care coordinators to make it actionable. This data also needs to support providers’ key metrics for CMS. The ACO data load into the population health software is typically four to 12 weeks behind real time,” Dexter continued. “That creates an opportunity for Sonora Quest Laboratories to provide their data in real time to both the ACOs and the clinicians treating the ACO patients. We are investing significantly in information technology so as to provide such data in real time.”

Similarly, in the New York metro, Northwell’s lab division has formed a laboratory joint venture. Executive Director and Senior Vice President for Laboratory Services at Northwell Health, James M. Crawford, MD, PhD, says his lab’s strategies to add value contribute to improved patient outcomes while helping reduce the cost-per-encounter. “Through standardization and some consolidation, the JV is on track to deliver $40 million in savings to the partners in the next 30 months. It is also positioned to expand its market share of office-based physicians in the region.” Crawford continued. “Our decision was to partner with an organization that is already at the front edge of genetic testing and was willing to collaborate with us in ways that fully support our clinical mission to our parent health system. We then spent almost three full years visiting potential partners, developing a request for qualifications (ROQ); then doing site visits of the respondents to the ROQ. Late last year, we wrapped up negotiations with our choice of a business partner. In January, we launched a shared genetic testing partnership with Bio-Reference Laboratories, Inc., of Elmwood Park, New Jersey.”

ACO Alternatives

Bundled payment initiatives have some characteristics of ACOs but are generally not as complex. But they offer similar potential to enhance care coordination, just in a more narrow scope.

According to CMS, more than 1,500 facilities nationwide are currently testing bundled payment innovation models.7 These numbers will continue to grow as HHS moves forward with its goal to tie 50% of all traditional or fee-for-service Medicare payments to quality or value through APMs, ACOs or bundled payment arrangements, by 2018.

So far, the bundled payment model is working. More than 80% of participating hospitals report improved patient engagement, reduced administrative costs, and increased alignment with physicians.

Summary

The move toward ACOs and similar forms of payment based on cost and quality outcomes is expected to continue. At the same time, ACOs are still very immature and their future is by no means guaranteed. The industry has survived many early ACOs struggling and even leaving Medicare. At this point, if early data showing savings and improved outcomes are borne out, more ACOs will be formed and others will be expanded. But if the cost savings can’t be shown or if ACOs continue to face legal, tax or other impediments, the future will be much more limited. At this point in time, it is too early to tell which way the momentum will take the industry.

25

THE LEADING EDGE

877 501 1611 | [email protected] | anesthesianewsletter.ahsrcm.com

—————————–[7] Curry, Angie; Fee, James, “Ramping Up for Bundled Payments: Fostering Alignment Between Hospitals and

Physicians,” hfma, May 1, 2016

Price Transparency: Slow Progress

One family recently experienced after receiving a $629 medical bill for the application of a Band-Aid to their 1-year-old’s finger.1 Their daughter’s brief visit to the ER resulted for a small cut on her finger was concluded with a band-aid. They were later told the Band-Aid cost $7 and the rest of the price was the “emergency department facility fees.”

This family’s experience is far too common. Hospital Pricing Specialists LLC recently concluded a report where it found wide variance in the average price for a CT scan of the head or brain in Pennsylvania facilities. Prices included $185.05 for a doctor’s office visit, $569.16 for a testing facility, and $1,745.05 for a hospital visit.2

Situations such as these have been driving interest in more health care price transparency for some years. However, progress remains slow for reasons we explore in this article.

Background

Health Care Cost Institute’s study of commercial healthcare prices shows that employers and insurers providing private health coverage pay highly variable prices for routine services and procedures, depending on the state where people live.3 The study analyzed 3 billion medical claims from Aetna, Humana and UnitedHealthcare during 2012 and 2013, constituting about 25% of the commercially insured market. The data represent prices actually paid to hospitals and doctors—much more important than the prices charged—but often difficult and sometimes impossible to obtain due to non-disclosure clauses in contracts.

Researchers found the national average price for 242 common services varied extensively across states as well as within metropolitan areas. For example, the average price for a knee replacement in South Carolina paid by one of the three large for-profit insurers was almost $47,000, while the average price of the same bundled procedure in New Jersey totaled only $24,000. In Cleveland, the average price paid for a pregnancy ultrasound was $522 and in Canton, Ohio, the average price was $183.

States with the highest average prices, compared with a national benchmark, included Alaska, Minnesota, New Hampshire, North Dakota and Wisconsin while Arizona, Florida, Maryland and Tennessee had medical services that were priced much lower than the national average.

Researchers said geographic costs certainly play a role in different prices across though it is hard to tell what amount of difference is justifiable. “The remaining variation is most likely due to differences in underlying market dynamics, such as varying market power, a lack of transparency or the availability of alternative treatments,” the authors wrote in their study

26

THE LEADING EDGE

877 501 1611 | [email protected] | anesthesianewsletter.ahsrcm.com

—————————–[1] Rappleye, Emily, “Why Everyone Is Talking About A $629 Band-Aid,” Becker’s Orthopedic Review, May 13, 2016[2] Louie, Rick, “Head CT Scan Prices Vary Widely Among Pennsylvania Facilities – Hospitals, Doctor Offices, and

Testing Facilities,” Hospital Pricing Specialists, May 17, 2016[3] Herman, Bob, “The Striking Variation of Commercial Healthcare Prices,” Modern Healthcare A.M., April 28, 2016

for Health Affairs. Indeed, other researchers who used Health Care Cost Institute claims data theorized late last year that hospital consolidation often drove up prices unjustifiably.

The Blue Cross and Blue Shield Association has released similar findings on price with data from its member plans, and Cast Light Health found its employer clients also pay wildly different prices for the same procedures depending on where people live.

Provider Efforts

According to a recent Navicure survey of 300 providers, most providers (88%) have developed the capability to offer patients estimates at the time of service. The growing share of healthcare costs paid by individuals was evident in the 43% of survey respondents who said at least 20% of their revenue comes from patients.

Of course, much of that revenue shift comes from growth in high-deductible health plan (HDHP) enrollment. The share of policyholders who have employer-sponsored insurance and are enrolled in HDHPs has steadily increased in recent years, reaching 28% of employees in 2015, according to an annual Mercer survey released recently. HDHPs also cover 49% of all non-group enrollees in 2016, up from 36% in 2015 according to the latest national survey by the Kaiser Family Foundation.

For a case study, Change Healthcare studied the three-year results from one client using its price transparency tool and found that 90% of the 15,000 employees used HDHPs and 66% acted on information provided to make a related healthcare decision. The high utilization amongst employees was attributed to careful and ongoing education of health plan enrollees, as well as ongoing support from the employer. The case study found the price transparency tool provided one employer with $1.1 million in claims-verified savings. It was also credited with saving HDHP enrollees an average of $516 each year.

The Kaiser researchers urge active reach out to policyholders, writing in their report: “Proactively contacting patients and providing information about less expensive care may be more effective than passively waiting for them to seek this information on their own via a website.”

Similarly, for their April study: “Examining a Health Care Price Transparency Tool: Who Uses It, And How They Shop for Care,” Health Affairs evaluated the experiences in the period 2011–12 of an insured population of non-elderly adults with Aetna’s Member Payment Estimator, a web-based tool that provides real-time, personalized, episode-level price estimates.4 While they found that usage still remained low, overall use of the tool increased during the study period, and for some procedures, the number of people searching for prices was high relative to the number of people who received the service. Among Aetna patients who had an imaging service, childbirth, or one of several outpatient procedures, the study found searchers for price information were significantly more likely to be younger and healthier and to have incurred

27

THE LEADING EDGE

877 501 1611 | [email protected] | anesthesianewsletter.ahsrcm.com

—————————–[4] Sinaiko, Anna; Rosenthal, Meredith, “Examining A Health Care Price Transparency Tool: Who Uses It, And

How They Shop for Care,” Health Affairs, April 2016; doi: 10.1377/hlthaff.2015.0746 Health Aff April 2016 vol.35 no. 4 662-670

—————————–[5] Daly, Rich, “Price Transparency Tool Results Differ,” hfma, May 20, 2016

higher annual deductible spending than patients who did not search for price information.

The results suggest campaigns designed to deliver price information to consumers may be important to increase patients’ engagement with price transparency tools.

The Other Side of the Coin

A recent study published by JAMA found, somewhat surprisingly, that one price transparency tool appeared to increase spending.

Researchers examined healthcare spending among 148,655 employees of two large companies. Spending by those offered a price transparency tool increased when compared with 295,983 employees at companies not offered the tool during a recent one-year period.5 The mean outpatient spending increased by $212 among employees offered the tool and by $153 among a control group. Following an adjustment for demographic and health characteristics, the study’s authors concluded that the tool’s availability was associated with a mean $59 increase in outpatient spending vs $30 for those without an available tool. It is worth noting that the usage of the tool was very low at 10%.

These results contrast markedly with the results in the Change Healthcare study noted above. Some hypothesize that the large difference in usage of the price transparency tool is driving the results.

Price Transparency Tools

In addition to tools from insurance companies, firms such as Change Healthcare (see above), Castlight, Vitals, and Blink Health (drug prices) are focused exclusively on providing price information and tools. As the New York Times recently pointed out, “Even when people have access to the newly available information, they may not use it. And when they do, they may not rely on the insight. It is impossible to know, for example, whether a dermatologist who costs twice as much as another can more successfully diagnose skin cancer.”

Castlight’s experience shows how the early promise of price transparency has been slowed by the complexity of the healthcare world. In business for eight years, Castlight works with employers to give their employees better information in order to, in theory, help workers make better medical decisions. Despite early promise, Castlight has run into several barriers:

- Changing how people pick doctors and hospitals is much harder than expected,- Getting prices and related information is difficult,- It is much harder to engage employees when making a healthcare decision (e.g. which

provider(s), what care is needed, etc.), and- Many fewer people are shopping than employers or Castlight expected.

28

THE LEADING EDGE

877 501 1611 | [email protected] | anesthesianewsletter.ahsrcm.com

Per the Times, “Castlight executives insist is it still very early. “We overestimated the speed here,” said Dr. Giovanni Colella, the company’s chief executive and one of its founders. “Transparency hasn’t even started,” he said.”

Today’s reality is echoed by Mitch Rothschild, the executive chairman of Castlight competitor, Vitals. “It’s a heavy lift,” he said. “It really requires behavioral change for most of America.”

A major limitation to current tools is the limited quality data. “It’s hard to make heads or tails out of all the quality information out there,” said Suzanne Delbanco, the executive director for the Catalyst for Payment Reform.

Legislative Activity

Policymakers have acknowledged the importance of price transparency with more than two-thirds of states mandating or beginning to mandate All-Payer Claims Databases that collect payer claims data, according to the All-Payer Claims Database Council. In addition, over half of states have enacted laws or regulations establishing price transparency websites or requiring plans, hospitals, or physicians to provide price information to patients.

However, a recent Supreme Court ruling means that employer “self-funded” plans do not have to participate in All-Payer Claims Databases. As a result, one of the most promising avenues for price transparency has been emasculated, at least for the near term.

At the same time, Representatives Michael Burgess (R-TX), MD, and Gene Green (D-TX) just introduced the Healthcare Price Transparency Promotion Act of 2016.

The act would amend the Social Security Act by requiring states to develop and maintain laws requiring “disclosure of information on hospital charges, to make such information available to the public, and to provide individuals with information about estimated out-of-pocket costs for healthcare services.”

The AHA wrote a letter fully supporting the bill.

Summary: The Consumer’s Experience

A number of factors are currently slowing the trend toward more transparent healthcare prices. But consumer behavior is clearly the biggest factor driven by these forces and others:

- If the medical need is urgent, consumers may not have the time to use the tools andeven if they do, their focus is not likely to be on the cost.

- Many consumers are still on employer plans with small deductibles and co-pays,with little financial incentive to compare prices.

- Older consumers with traditional Medicare coverage also have little incentive tocompare prices.

- Consumers on high deductible plans who incur significant healthcare costs know

29

THE LEADING EDGE

877 501 1611 | [email protected] | anesthesianewsletter.ahsrcm.com

—————————–[6] Phillips; Kathryn, Schleifer, David; Hagelskamp, Carolin, “Most Americans Do Not Believe That There Is an

Association Between Health Care Prices And Quality Of Care,” Health Affairs, April 2016

that their annual spending will exceed the plan’s deductible, reducing the incentive to look at price.

- In many rural areas and in some other areas, there may only be one specialist, or theprices may not vary much.

- Many people rely on their doctor’s referrals for specialists, tests, etc. Others rely onrecommendations from friends.

- If a health plan wants its users to get coordinated care from a closed group of providers,shopping may be discouraged.

- Consumers may avoid low-price care if they perceive low price to be associated withlow quality or if quality information is not readily available.

On the latter point, Health Affairs conducted a nationally representative survey to examine whether consumers perceive that price and quality are associated and whether the way in which questions are framed affects consumers’ responses.6 It was found that a majority of those surveyed (58–71%) did not think that price and quality are associated. But a substantial minority did perceive an association (21–24%) or were unsure whether there was one (8–16%). Those who had compared prices were more likely to perceive that price and quality were associated.

Despite the many obstacles, it is clear that pressures for more transparency will increase. But it will take concerted efforts by providers, insurers and entrepreneurs to provide the information, tools and incentives needed for price transparency to have real impact on healthcare costs.

30

THE LEADING EDGE

877 501 1611 | [email protected] | anesthesianewsletter.ahsrcm.com

How to Deal with Patient “Financial Hardship”

As billing professionals we hear it all too often, a patient calls the physician or their office because they say they cannot afford to pay. Now the provider is calling us to request a discount or to write off the balance, in hopes of quieting the squeaky wheel or due to basic human compassion. At AdvantEdge, we are reimbursement specialists and often patients ourselves, and we get it. But, we are here for a reason: to get our clients the funds that they have worked so hard for, and to keep our clients out of any potential compliance hot water. This article highlights the need for each practice and hospital to have a meaningful financial policy in place and to use it in a consistent manner.

Medicare, along with every federal payor and most commercial payors, has specific regulations requiring providers to collect balances due from patients unless there is a meaningful and valid hardship waiver on file. As charitable as physicians want to be, the law does not allow routine write-offs of co-pays and deductibles. If the provider does routinely offer discounts or waivers of deductibles without properly investigating a patient’s financial situation, the practice runs the risk of violating its payor contracts, being accused of committing insurance fraud, and/or paying an illegal kickback to induce patients to seek treatment from the practice.

Some payor contracts also require the practice to bill the payor the lowest rate that the practice bills any of its patients, a so-called “most favored nation provision.” Typical Medicare participation agreements are subject to this type of provision. If a practice or hospital waives deductibles or co-pays, then insurers often take the position that the amount being billed to the insurer ought to be reduced by the amount waived.

Financial hardship determinations are typically based upon a review of household income, assets and liabilities in relation to current Federal Poverty Income Guidelines https://aspe.hhs.gov/poverty-guidelines.

Hardship waivers should not be granted based on a patient’s comments about their inability to pay or how a provider “feels” about the patients’ circumstance. Patient inability to pay must be documented with appropriate financial proof such as copies of tax returns, W-2s, 1099s, recent pay checks, copies of household bills, etc. Note that non-essential expenses such as credit card bills should not factor into hardship determinations.

A practice or hospital should create and apply its own guidelines, e.g. 20% above the federal poverty definition, as long as the same standards apply to all patients. The patient’s hardship should be periodically reviewed to ensure their status has not changed. It is also advisable to maintain all records and information gathered while determining hardship, along with the amounts waived.

What about the Uninsured? When it comes to uninsured patients who are willing to pay for services, offering a cash or “prompt pay” discount may be possible, as long as you are cognizant of the payor contracts where you are obligated to offer your “lowest rate.” Additionally, no practice or hospital should have multiple fee schedules or they may find that payors adjust “usual and customary fees” to the lowest fee schedule amount.

31

THE LEADING EDGE

877 501 1611 | [email protected] | anesthesianewsletter.ahsrcm.com

Unfortunately, the current healthcare system with its myriad regulations is not geared toward encouraging or allowing providers to offer free or highly discounted care to patients. Providing free care may seem like a compassionate idea, but it is likely to create costly liability issues unless done using a formal policy.

32

THE LEADING EDGE

877 501 1611 | [email protected] | anesthesianewsletter.ahsrcm.com